MGCR 293 DEMAND THEORY. Professors: Dr. K. Salmasi Dr. T. Nizami Dr. T. Sidthidet T.A.: Brianna Mooney

|

|

|

- Brianne Blankenship

- 6 years ago

- Views:

Transcription

1 MGCR 293 DEMAND THEORY Professors: Dr. K. Salmasi Dr. T. Nizami Dr. T. Sidthidet T.A.: Brianna Mooney

2 1. CHAPTER REVIEW

3 THE MARKET DEMAND CURVE A curve that illustrates the quantity of goods that consumers are willing and able to purchase at each price

4 Changes with the Demand Curve 1. Movement along the curve Occurs when there is a change in price 2. Shift of the entire curve Occurs due to non-price determinants of demand: Changes in income Changes in tastes and preferences Prices of related goods (substitutes and complements) Advertising Change in population

5

6 PRICE ELASTICITY OF DEMAND Own Price Elasticity: percentage change in quantity demanded as a result of a 1% change in price η = P ΔQ Q ΔP Elastic (η<-1): greater than 1% change in Q Inelastic (η>-1):less than 1% change in Q Unitary elastic (η=-1): equal to 1% change in Q Perfect inelastic (η =0 0% change in Q Perfect elastic (η =- ) infinite change in Q

7 FACTORS AFFECTING PRICE ELASTICITY 1. Number of similarity of substitute products (many substitutes=elastic) 2. Products price relative to consumer s budget. (small items=inelastic) 3. Length of time good pertains (nondurable goods=elastic)

8 Price Elasticity & Marginal Revenue: MR= P 1+ 1 η Income Elasticity of Demand: η I = positive for normal goods, negative for inferior goods η I = I ΔQ Q ΔI Cross-Price Elasticity: η xy =substitute if positive, compliment if negative η xy = Advertising Elasticity: η A >1! elastic, <1! inelastic P y Q x ΔQ x ΔP y η A = A ΔQ Q ΔA

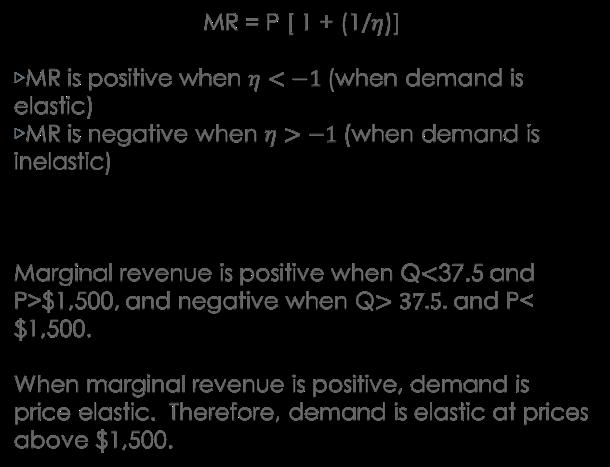

9 MARGINAL REVENUE AND ELASTICITY

10

11 ELASTICITY AND TOTAL REVENUE When demand is inelastic, total revenue will increase if price increases Consumers are less sensitive to changes in price, therefore the potential gain of increasing price would offset the potential loss When demand is elastic, total revenue will increase by decreasing the price Consumers are more responsive to changes in price, therefore the potential gain would not outweigh the potential loss

12 2. CHAPTER QUESTIONS

13 QUESTION 1 The Dolan Corporation, a maker of small engines, determines that in 2008 the demand curve for its products is P= Q a) To sell 20 engines per month, what price would Dolan have to charge?

14 SOLUTION a) P= Q P=200-50(20) P=1000 b) If managers set a price of $500, how many engines will Dolan sell per month?

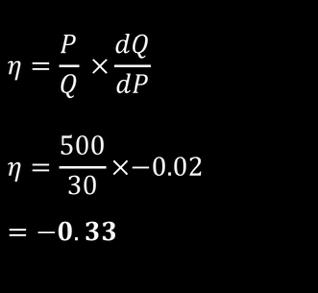

15 SOLUTION b) 500= Q Q=1500/50= per month c)what is the price elasticity of demand if price equals $500.

16 SOLUTION

17 QUESTION 1

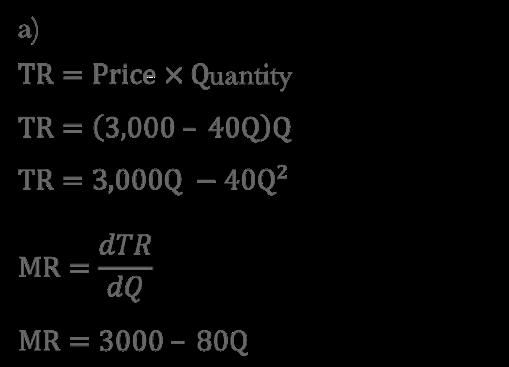

18 QUESTION 2 The Johnson Robot Company s marketing managers estimate that the demand curve for the company s robots in 2008 is P= Q a) Derive the marginal revenue curve for the firm

19 SOLUTION

20 QUESTION 2 b) At what price is the demand for the firm s product price elastic? c) If the firm wants to maximize its dollar sales volume, what price should it charge?

21 b) MR=0 3,000 80Q=0 Q=37.5 P=3,000-40(37.5) =$1,500 **Note: Demand is Unitary Elasticity when MR=0, price elastic when MR is positive, and price inelastic when MR is negative. We want to see where marginal revenue is positive, negative, and equal to zero MR: P=$1,400, Q=40 P= $1,500, Q=37.5 P=$1,800, Q=30

22

23 SOLUTION c) Maximize Total Revenue TR is maximized when MR=0 According to b), MR=0 when P=$1,500 (the price of unit elasticity) TR= $1,500 x 37.5 TR= $56,250

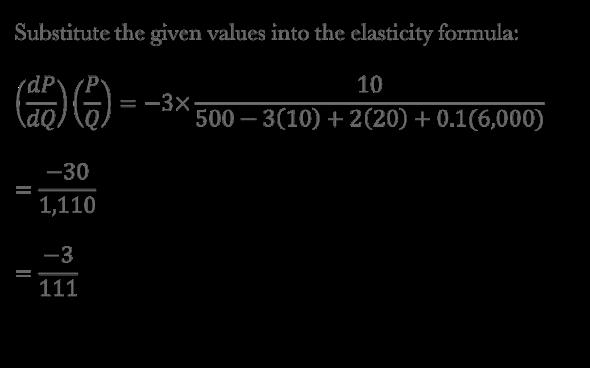

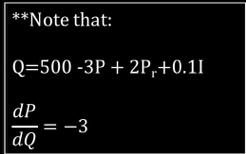

24 QUESTION 3 Q=500 3P +2P r +0.1I P r = price of rival products = 20 I = per capita disposable income = 6,000 P = price = 10 a) What is the price elasticity of demand for the firm s product?

25 SOLUTION

26 QUESTION 3 b) What is the income elasticity of demand for the firm s product? c)what is the cross-price elasticity of demand between its product and its rival s product? d) What is the implicit assumption regarding the population in the market?

27 SOLUTION Substitute the given values into the formulas for Income Elasticity and Cross Elasticity, respectively: b) Q I I = 0.1(6000) Q 1,110 = 600 1,110 c) Q P r P r Q = 2(20) 1,110 = 40 1,110 d) The assumption is that population is CONSTANT

28 QUESTION 4 The Haas Corporation s executive vice president argues for a reduction in the price of the firm s product. He says such a price cut will increase the firm s sales and profits. a) The firm s marketing manager responds that the price elasticity of demand for the firm s product is about Why is this fact relevant? a) The firm s president concurs with the option of the executive vice president. Is she correct?

29 SOLUTION 4

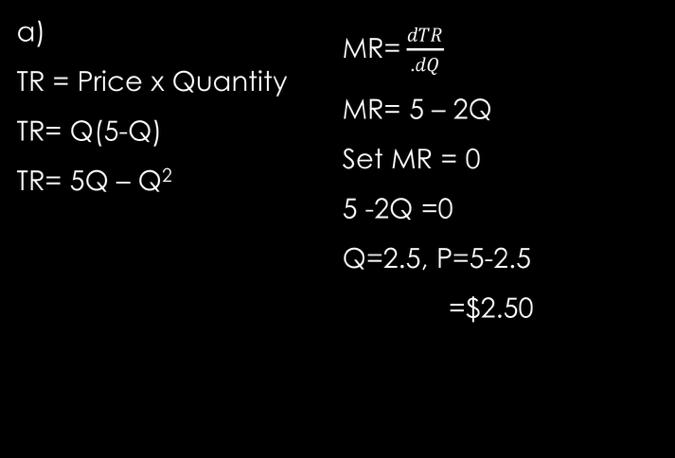

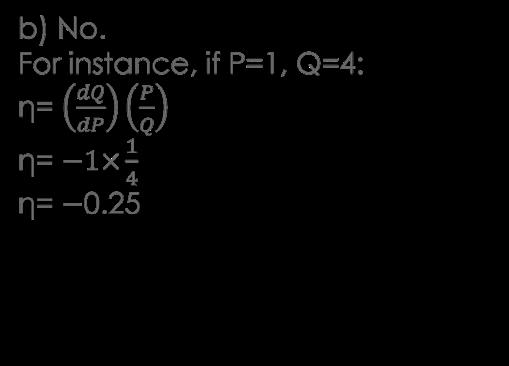

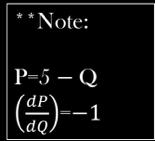

30 QUESTION 5 Demand curve: P = 5 Q Current price is $1 a) Evaluate the wisdom of the firm s pricing policy. Profit-maximizing price occurs when MR = 0 b) A marketing specialists says that the price elasticity of demand for the firm s product is Is this correct?

31 SOLUTION

32 SOLUTION

33 QUESTION 6 Richard Tennant has concluded, The consumption of cigarettes is relatively insensitive to change in price. But, the demand for individual brands is highly elastic in its response to price. In 1918, for example, Lucky Strike was sold for a short time at a higher retail price than Camel and Chesterfield and rapidly lost half its business. a) Explain why the demand for a particular brand is more elastic than the demand for all cigarettes. If Lucky Strike raised its prices by 1 percent in 1918, was the price elasticity of demand for its product greater than -2?

34 SOLUTION a) As there are many brands available for consumption, the price elasticity is elastic, as it is easy for consumer to switch to a close substitute. But since there is no substitute for cigarettes in general, the price elasticity is inelastic. The elasticity for Lucky Strike was less than -2.

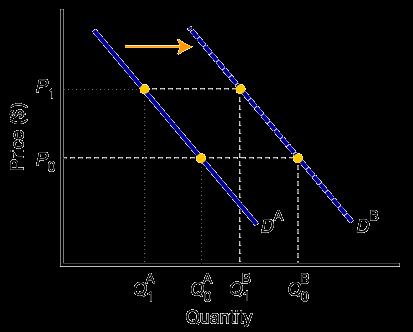

35 QUESTION 6 b) Do you think that the demand curve for cigarettes is the same now as it was in 1918? If not, describe in detail the factors that have shifted the demand curve and whether each has shifted it to the left or right?

36 SOLUTION b) No, the demand curve for cigarettes has likely shifted to the left due to changes in consumer tastes and preferences (becoming more health conscious).

37 QUESTION 7 Price elasticity of demand for cigarettes is between -0.3 and -0.4, and the income elasticity of demand is about 0.5. a) Suppose the federal government, influenced by findings that link cigarettes and cancer, were to impose a tax on cigarettes that increased their price by 15%. What effect would this have on cigarette consumption?

38 SOLUTION Therefore, cigarette consumption would fall between 4.5-6% due to the increase in price of 15%

39 QUESTION 7 b) Suppose a brokerage house advised you to buy cigarette stocks because if income were to rise by 50 % in the next decade, cigarette sales would bound to spurt enormously. What would be your reaction to this advice?

40 SOLUTION b) Expected demand would increase by half of that, i.e 25%, since income elasticity equals 0.5. Other stocks are better

41 QUESTION 8 A survey of major U.S. firms estimates on average, the advertising elasticity of demand is only about Doesn t this indicate that managers spend too much on advertising?

42 SOLUTION An advertising elasticity of demand of means that a 1% increase in advertising expenditure results in a minimal increase for quantity demand. This could indicate that advertising is not the most effective factor in increasing quantity demanded. However, this is an average number across many industries, and advertising is more effective in some industries than others, thus this statement is not necessarily true for all firms.

43 QUESTION 9 Q=100P -3.1 (I 2.3 )(A 0.1 ) a) What is the price elasticity of demand? b) Will price increase result in increase or decrease in the amount spent on the product? c) What is the income elasticity of demand?

44 SOLUTION a) The price elasticity of demand is equal to the exponent of the P variable in the demand function, or b) Since -3.1 is an elastic price elasticity, increasing price will reduce a firm s total revenue. c) The income elasticity of demand is equal to the exponent of the I variable in the demand function, or 2.3.

45 QUESTION 9 d) What is the advertising elasticity of demand? e) If the population in the market increased by 10%, what is the effect on the quantity demanded if P, I, and A are held constant?

46 SOLUTION d) The advertising elasticity of demand is equal to the exponent of the A variable in the demand function, or 0.1. e) The quantity demanded will increase by 10% (Q is defined as quantity demanded per capita. Quantity demanded per capita remains the same, however total quantity demanded increases by 10%).

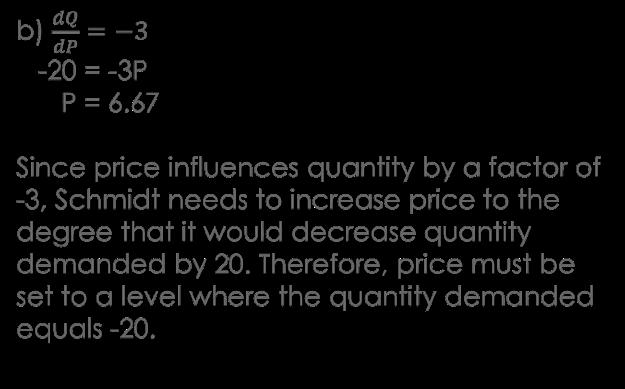

47 QUESTION 10 Q=400 3P +4I +0.6A Q quantity demanded P products price (in $) I per capita disposable income (thousands of $) A advertising expenditure (thousands of $ per month) Population is assumed to be constant

48 QUESTION 10 a) During the next decade, per capita disposable income is expected to increase by $5000. What effect will this have on the firm s sales? b) If Schmidt wants to raise its price enough to offset the effect of the increase in per capita disposable income, by how much must it raise its price?

49 SOLUTION a) Q=400-3P +(4 x 5) + 0.6A Q= 400-3P A Therefore, Quantity demanded would increase by 20, and thus sales would increase by 20.

50 SOLUTION

51 QUESTION 10 c) If Schmidt raises its price by this amount, will it increase or decrease elasticity of demand? Explain.

52 SOLUTION d) As price increases, demand becomes more elastic

53 Any questions?

Ch. 7 outline. 5 principles that underlie consumer behavior

Ch. 7 outline The Fundamentals of Consumer Choice The focus of this chapter is on how consumers allocate (distribute) their income. Prices of goods, relative to one another, have an important role in how

Ch. 7 outline The Fundamentals of Consumer Choice The focus of this chapter is on how consumers allocate (distribute) their income. Prices of goods, relative to one another, have an important role in how

1.2.3 Price, Income and Cross Elasticities of Demand

1.2.3 Price, Income and Cross Elasticities of Demand Price elasticity of demand The price elasticity of demand is the responsiveness of a change in demand to a change in price. The formula for this is:

1.2.3 Price, Income and Cross Elasticities of Demand Price elasticity of demand The price elasticity of demand is the responsiveness of a change in demand to a change in price. The formula for this is:

Microeconomics, Module 4: Consumers in the Marketplace. Practice Problems. (The attached PDF file has better formatting.) Updated: July 10, 2006

Updated: July 10, 2006") Microeconomics, Module 4: Consumers in the Marketplace Practice Problems (The attached PDF file has better formatting.) Updated: July 10, 2006 Exercise 4.1: Price Elasticity of Demand The price of a good

Microeconomics, Module 4: Consumers in the Marketplace Practice Problems (The attached PDF file has better formatting.) Updated: July 10, 2006 Exercise 4.1: Price Elasticity of Demand The price of a good

Formula: Price of elasticity of demand= Percentage change in quantity demanded Percentage change in price

1 MICRO ECONOMICS~ CHAPTER FOUR CHAPTER FOUR PRICE ELASTICITY OF DEMAND You know that when supply increases, the equilibrium price falls and the equilibrium quantity increases THE PRICE ELASTICITY OF DEMAND~

1 MICRO ECONOMICS~ CHAPTER FOUR CHAPTER FOUR PRICE ELASTICITY OF DEMAND You know that when supply increases, the equilibrium price falls and the equilibrium quantity increases THE PRICE ELASTICITY OF DEMAND~

ECO 610: Lecture 2. Theory of Demand; Elasticity; and Marketing and Consumer Behavior

ECO 610: Lecture 2 Theory of Demand; Elasticity; and Marketing and Consumer Behavior Theory of Demand; Elasticity; and Marketing and Consumer Behavior: Outline Demand Theory and Marketing Research Households

ECO 610: Lecture 2 Theory of Demand; Elasticity; and Marketing and Consumer Behavior Theory of Demand; Elasticity; and Marketing and Consumer Behavior: Outline Demand Theory and Marketing Research Households

Chapter 3 Quantitative Demand Analysis

Chapter 3 Quantitative Demand Analysis EX1: Suppose a 10 percent price decrease causes consumers to increase their purchases by 30%. What s the price elasticity? EX2: Suppose the 10 percent decrease in

Chapter 3 Quantitative Demand Analysis EX1: Suppose a 10 percent price decrease causes consumers to increase their purchases by 30%. What s the price elasticity? EX2: Suppose the 10 percent decrease in

UNIT 4 PRACTICE EXAM

UNIT 4 PRACTICE EXAM 1. The prices paid for resources affect A. the money incomes of households in the economy B. the allocation of resources among different firms and industries in the economy C. the

UNIT 4 PRACTICE EXAM 1. The prices paid for resources affect A. the money incomes of households in the economy B. the allocation of resources among different firms and industries in the economy C. the

Copyright 2010 Pearson Education Canada

What are the effects of a high gas price on buying plans? You can see some of the biggest effects at car dealers lots, where SUVs remain unsold while sub-compacts sell in greater quantities. But how big

What are the effects of a high gas price on buying plans? You can see some of the biggest effects at car dealers lots, where SUVs remain unsold while sub-compacts sell in greater quantities. But how big

1 of 14 5/1/2014 4:56 PM

1 of 14 5/1/2014 4:56 PM Any point on the budget constraint Gives the consumer the highest level of utility. Represent a combination of two goods that are affordable. Represents combinations of two goods

1 of 14 5/1/2014 4:56 PM Any point on the budget constraint Gives the consumer the highest level of utility. Represent a combination of two goods that are affordable. Represents combinations of two goods

MONOPOLY. Characteristics

OBJECTIVES Explain how managers should set price and output when they have market power With monopoly power, the firm s demand curve is the market demand curve. A monopolist is the only seller of a product

OBJECTIVES Explain how managers should set price and output when they have market power With monopoly power, the firm s demand curve is the market demand curve. A monopolist is the only seller of a product

Demand - the desire, ability, and willingness to buy a product.

Demand - the desire, ability, and willingness to buy a product. 1. You must have the desire for the product 2. You must be able to make a purchase 3. You must be willing to make a purchase 4. Purchases

Demand - the desire, ability, and willingness to buy a product. 1. You must have the desire for the product 2. You must be able to make a purchase 3. You must be willing to make a purchase 4. Purchases

DEMAND ESTIMATION (PART I)

") BEC 30325: MANAGERIAL ECONOMICS Session 02 DEMAND ESTIMATION (PART I) Dr. Sumudu Perera Session Outline Definition of Demand Law of Demand Price Elasticity of Demand Elasticity and Total Revenue Income

BEC 30325: MANAGERIAL ECONOMICS Session 02 DEMAND ESTIMATION (PART I) Dr. Sumudu Perera Session Outline Definition of Demand Law of Demand Price Elasticity of Demand Elasticity and Total Revenue Income

Figure 4 1 Price Quantity Quantity Per Pair Demanded Supplied $ $ $ $ $10 2 8

Econ 101 Summer 2005 In class Assignment 2 Please select the correct answer from the ones given Figure 4 1 Price Quantity Quantity Per Pair Demanded Supplied $ 2 18 3 $ 4 14 4 $ 6 10 5 $ 8 6 6 $10 2 8

Econ 101 Summer 2005 In class Assignment 2 Please select the correct answer from the ones given Figure 4 1 Price Quantity Quantity Per Pair Demanded Supplied $ 2 18 3 $ 4 14 4 $ 6 10 5 $ 8 6 6 $10 2 8

Chapter Summary and Learning Objectives

CHAPTER 11 Firms in Perfectly Competitive Markets Chapter Summary and Learning Objectives 11.1 Perfectly Competitive Markets (pages 369 371) Explain what a perfectly competitive market is and why a perfect

CHAPTER 11 Firms in Perfectly Competitive Markets Chapter Summary and Learning Objectives 11.1 Perfectly Competitive Markets (pages 369 371) Explain what a perfectly competitive market is and why a perfect

Review Questions. The Own-Wage Elasticity of Labor Demand. Choose the letter that represents the BEST response.

Chapter 4 Labor Demand Elasticities 49 Review Questions Choose the letter that represents the BEST response. The Own-Wage Elasticity of Labor Demand 1. If the wage paid to automobile workers goes up by

Chapter 4 Labor Demand Elasticities 49 Review Questions Choose the letter that represents the BEST response. The Own-Wage Elasticity of Labor Demand 1. If the wage paid to automobile workers goes up by

At P = $120, Q = 1,000, and marginal revenue is ,000 = $100

Microeconomics, monopoly, final exam practice problems (The attached PDF file has better formatting.) *Question 1.1: Marginal Revenue Assume the demand curve is linear.! At P = $100, total revenue is $200,000.!

Microeconomics, monopoly, final exam practice problems (The attached PDF file has better formatting.) *Question 1.1: Marginal Revenue Assume the demand curve is linear.! At P = $100, total revenue is $200,000.!

Competitive Markets. Chapter 5 CHAPTER SUMMARY

Chapter 5 Competitive Markets CHAPTER SUMMARY This chapter discusses the conditions for perfect competition. It also investigates the significance of competitive equilibrium in a perfectly competitive

Chapter 5 Competitive Markets CHAPTER SUMMARY This chapter discusses the conditions for perfect competition. It also investigates the significance of competitive equilibrium in a perfectly competitive

Chapter 4: Understanding Demand

SCHS SOCIAL STUDIES What you need to know UNIT TWO 1. What a competitive market is and how it is described by the supply and demand model 2. What a supply curve shows 3. The difference between a movement

SCHS SOCIAL STUDIES What you need to know UNIT TWO 1. What a competitive market is and how it is described by the supply and demand model 2. What a supply curve shows 3. The difference between a movement

MICROECONOMICS SECTION I. Time - 70 minutes 60 Questions

MICROECONOMICS SECTION I Time - 70 minutes 60 Questions Directions: Each of the questions or incomplete statements below is followed by five suggested answers or completions. Select the one that is best

MICROECONOMICS SECTION I Time - 70 minutes 60 Questions Directions: Each of the questions or incomplete statements below is followed by five suggested answers or completions. Select the one that is best

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. FIGURE 1-2

Questions of this SAMPLE exam were randomly chosen and may NOT be representative of the difficulty or focus of the actual examination. The professor did NOT review these questions. MULTIPLE CHOICE. Choose

Questions of this SAMPLE exam were randomly chosen and may NOT be representative of the difficulty or focus of the actual examination. The professor did NOT review these questions. MULTIPLE CHOICE. Choose

Chapter 2 Market analysis

Chapter 2 Market analysis Market analysis is concerned with collecting and interpreting data about customers and the market so that businesses adopt a relevant marketing strategy. Businesses carry out

Chapter 2 Market analysis Market analysis is concerned with collecting and interpreting data about customers and the market so that businesses adopt a relevant marketing strategy. Businesses carry out

AS/ECON AF Answers to Assignment 1 October 2007

AS/ECON 4070 3.0AF Answers to Assignment 1 October 2007 Q1. Find all the efficient allocations in the following 2 person, 2 good, 2 input economy. The 2 goods, food and clothing, are produced using labour

AS/ECON 4070 3.0AF Answers to Assignment 1 October 2007 Q1. Find all the efficient allocations in the following 2 person, 2 good, 2 input economy. The 2 goods, food and clothing, are produced using labour

sample test 3 - spring 2013

sample test 3 - spring 2013 Multiple Choice Identify the letter of the choice that best completes the statement or answers the question. 1. A natural monopoly occurs when a. the product is sold in its

sample test 3 - spring 2013 Multiple Choice Identify the letter of the choice that best completes the statement or answers the question. 1. A natural monopoly occurs when a. the product is sold in its

Practice Exam 3: S201 Walker Fall with answers to MC

Practice Exam 3: S201 Walker Fall 2007 - with answers to MC Print Your Name: I. Multiple Choice (3 points each) 1. If marginal utility is falling then A. total utility must be falling. B. marginal utility

Practice Exam 3: S201 Walker Fall 2007 - with answers to MC Print Your Name: I. Multiple Choice (3 points each) 1. If marginal utility is falling then A. total utility must be falling. B. marginal utility

Student Manual Principles of Economics

Student Manual Principles of Economics Beat The Market On Line: An Interactive Microeconomics Game. GoldSimulations www.goldsimulations.com Beat The Market : Student Manual Published by GoldSimulations

Student Manual Principles of Economics Beat The Market On Line: An Interactive Microeconomics Game. GoldSimulations www.goldsimulations.com Beat The Market : Student Manual Published by GoldSimulations

Monopoly. 3 Microeconomics LESSON 5. Introduction and Description. Time Required. Materials

LESSON 5 Monopoly Introduction and Description Lesson 5 extends the theory of the firm to the model of a Students will see that the profit-maximization rules for the monopoly are the same as they were

LESSON 5 Monopoly Introduction and Description Lesson 5 extends the theory of the firm to the model of a Students will see that the profit-maximization rules for the monopoly are the same as they were

Chapter 3. Table of Contents. Introduction. Empirical Methods for Demand Analysis

Chapter 3 Empirical Methods for Demand Analysis Table of Contents 3.1 Elasticity 3.2 Regression Analysis 3.3 Properties & Significance of Coefficients 3.4 Regression Specification 3.5 Forecasting 3-2 Introduction

Chapter 3 Empirical Methods for Demand Analysis Table of Contents 3.1 Elasticity 3.2 Regression Analysis 3.3 Properties & Significance of Coefficients 3.4 Regression Specification 3.5 Forecasting 3-2 Introduction

Elasticity of Demand

Elasticity of Demand Elasticity of Demand The law of demand states that an increase in price causes a decrease in quantity demanded (and vice-versa) Question: How much quantity demanded changes in response

Elasticity of Demand Elasticity of Demand The law of demand states that an increase in price causes a decrease in quantity demanded (and vice-versa) Question: How much quantity demanded changes in response

Topic 4c. Elasticity. What is the difference between this. and this? 1 of 23

Topic 4c Elasticity What is the difference between this and this? 1 of 23 Defining and Measuring Elasticity (I) Price elasticity of demand Ø The price elasticity of demand is the ratio of the percent change

Topic 4c Elasticity What is the difference between this and this? 1 of 23 Defining and Measuring Elasticity (I) Price elasticity of demand Ø The price elasticity of demand is the ratio of the percent change

Chapter 4. Elasticity. In this chapter you will learn to. Price Elasticity of Demand

Chapter 4 Elasticity In this chapter you will learn to 1. Explain the meaning of price elasticity of demand and how it is measured. 2. Describe the relationship between demand elasticity and total expenditure.

Chapter 4 Elasticity In this chapter you will learn to 1. Explain the meaning of price elasticity of demand and how it is measured. 2. Describe the relationship between demand elasticity and total expenditure.

6. In the early part of 1998, crude oil prices fell to a nine-year low at $13.28 a barrel.

Questions 1. Delta Software earned $10 million this year. Suppose the growth rate of Delta's profits and the interest rate are both constant and Delta will be in business forever. Determine the value of

Questions 1. Delta Software earned $10 million this year. Suppose the growth rate of Delta's profits and the interest rate are both constant and Delta will be in business forever. Determine the value of

Economics E201 (Professor Self) Sample Questions for Exam Two, Fall 2013

Sample Questions for Exam Two, Fall 2013") , Fall 2013 Your exam will have two parts covering the topics in chapters 4 (page 91 through end of chapter), 5 and 6 from the Parkin chapters and chapter 10 (up to page 317, up to but not including the

, Fall 2013 Your exam will have two parts covering the topics in chapters 4 (page 91 through end of chapter), 5 and 6 from the Parkin chapters and chapter 10 (up to page 317, up to but not including the

Bremen School District 228 Social Studies Common Assessment 2: Midterm

Bremen School District 228 Social Studies Common Assessment 2: Midterm AP Microeconomics 55 Minutes 60 Questions Directions: Each of the questions or incomplete statements in this exam is followed by five

Bremen School District 228 Social Studies Common Assessment 2: Midterm AP Microeconomics 55 Minutes 60 Questions Directions: Each of the questions or incomplete statements in this exam is followed by five

Chapter 6. Elasticity

Chapter 6 Elasticity Both the elasticity coefficient and the total revenue test for measuring price elasticity of demand are presented in this chapter. The text discusses the major determinants of price

Chapter 6 Elasticity Both the elasticity coefficient and the total revenue test for measuring price elasticity of demand are presented in this chapter. The text discusses the major determinants of price

PRICING. Quantity demanded is the number of the firm s product customers wish to purchase. What affects the quantity demanded?

PRICING So far we have supposed perfect competition: the firm cannot affect the price. Whatever the firm produces is sold at the world market price. Most commodity businesses are highly competitive: regardless

PRICING So far we have supposed perfect competition: the firm cannot affect the price. Whatever the firm produces is sold at the world market price. Most commodity businesses are highly competitive: regardless

Section I (20 questions; 1 mark each)

") Foundation Course in Managerial Economics- Solution Set- 1 Final Examination Marks- 100 Section I (20 questions; 1 mark each) 1. Which of the following statements is not true? a. Societies face an important

Foundation Course in Managerial Economics- Solution Set- 1 Final Examination Marks- 100 Section I (20 questions; 1 mark each) 1. Which of the following statements is not true? a. Societies face an important

Chapter Eleven. Topics. Marginal Revenue and Price. A firm s revenue is:

Chapter Eleven Monopoly Topics Monopoly Profit Maximization. Effects of a Shift of the Demand Curve. Market Power. Welfare Effects of Monopoly. Cost Advantages That Create Monopolies. Government Actions

Chapter Eleven Monopoly Topics Monopoly Profit Maximization. Effects of a Shift of the Demand Curve. Market Power. Welfare Effects of Monopoly. Cost Advantages That Create Monopolies. Government Actions

2007 NATIONAL ECONOMICS CHALLENGE NCEE/Goldman Sachs Foundation

2007 NATIONAL ECONOMICS CHALLENGE NCEE/Goldman Sachs Foundation National Round I: Microeconomics David Ricardo Division 1. If your income tax liability is $15,000 and your income is $60,000, your A. average

2007 NATIONAL ECONOMICS CHALLENGE NCEE/Goldman Sachs Foundation National Round I: Microeconomics David Ricardo Division 1. If your income tax liability is $15,000 and your income is $60,000, your A. average

Introduction to Agricultural Economics Agricultural Economics 105 Spring 2013 First Hour Exam Version 1

Introduction to Agricultural Economics Agricultural Economics 105 Spring 2013 First Hour Exam Version 1 Name Section There is only ONE best correct answer per question. Place your answer on the attached

Introduction to Agricultural Economics Agricultural Economics 105 Spring 2013 First Hour Exam Version 1 Name Section There is only ONE best correct answer per question. Place your answer on the attached

6. The law of diminishing marginal returns begins to take effect at labor input level: a. 0 b. X c. Y d. Z

Chapter 5 MULTIPLE-CHOICE QUESTIONS 1. The short run is defined as a period in which: a. the firm cannot change its output level b. all inputs are variable but technology is fixed c. input prices are fixed

Chapter 5 MULTIPLE-CHOICE QUESTIONS 1. The short run is defined as a period in which: a. the firm cannot change its output level b. all inputs are variable but technology is fixed c. input prices are fixed

Chapter 33: Terms of Trade

Chapter 33: Terms of Trade 1 The Terms of Trade The division of the gains from trade depends on the terms of trade. The terms of trade are measured by the ratio of the price of exports to the price of

Chapter 33: Terms of Trade 1 The Terms of Trade The division of the gains from trade depends on the terms of trade. The terms of trade are measured by the ratio of the price of exports to the price of

SUBJ SCORE # Version D: Page 1 of 9. (signature) 2. Please write your name and GU ID carefully and legibly at the top of this page.

2. Please write your name and GU ID carefully and legibly at the top of this page.") SUBJ SCORE # Version D: Page 1 of 9 Economics 001 NAME Professor Levinson GU ID # Midterm #2 November 12, 2012 DO NOT BEGIN WORKING UNTIL THE INSTRUCTOR TELLS YOU TO DO SO. READ THESE INSTRUCTIONS FIRST.

SUBJ SCORE # Version D: Page 1 of 9 Economics 001 NAME Professor Levinson GU ID # Midterm #2 November 12, 2012 DO NOT BEGIN WORKING UNTIL THE INSTRUCTOR TELLS YOU TO DO SO. READ THESE INSTRUCTIONS FIRST.

The Basics of Supply and Demand

C H A P T E R 2 The Basics of Supply and Demand Prepared by: Fernando & Yvonn Quijano CHAPTER 2 OUTLINE 2.1 Supply and Demand 2.2 The Market Mechanism 2.3 Changes in Market Equilibrium 2.4 Elasticities

C H A P T E R 2 The Basics of Supply and Demand Prepared by: Fernando & Yvonn Quijano CHAPTER 2 OUTLINE 2.1 Supply and Demand 2.2 The Market Mechanism 2.3 Changes in Market Equilibrium 2.4 Elasticities

MONOPOLISTIC COMPETITION

14 MONOPOLISTIC COMPETITION The online shoe store shoebuy.com lists athletic shooes made by 56 different producers in 40 different categories and price between$25 and $850. It offers 1,404 different types

14 MONOPOLISTIC COMPETITION The online shoe store shoebuy.com lists athletic shooes made by 56 different producers in 40 different categories and price between$25 and $850. It offers 1,404 different types

EC1010 Introduction to Micro Economics (Econ 6003)

") Cork Institute of Technology (Institiuid Teicneolaiochta Chorcai) Alternative Semester 1 Examination 2007/2008 (Winter 2007) EC1010 Introduction to Micro Economics (Econ 6003) (Time: 2 Hours) External

Cork Institute of Technology (Institiuid Teicneolaiochta Chorcai) Alternative Semester 1 Examination 2007/2008 (Winter 2007) EC1010 Introduction to Micro Economics (Econ 6003) (Time: 2 Hours) External

a. Sells a product differentiated from that of its competitors d. produces at the minimum of average total cost in the long run

I. From Seminar Slides: 3, 4, 5, 6. 3. For each of the following characteristics, say whether it describes a perfectly competitive firm (PC), a monopolistically competitive firm (MC), both, or neither.

I. From Seminar Slides: 3, 4, 5, 6. 3. For each of the following characteristics, say whether it describes a perfectly competitive firm (PC), a monopolistically competitive firm (MC), both, or neither.

Chapter 13. Microeconomics. Monopolistic Competition: The Competitive Model in a More Realistic Setting

Microeconomics Modified by: Yun Wang Florida International University Spring, 2018 1 Chapter 13 Monopolistic Competition: The Competitive Model in a More Realistic Setting Chapter Outline 13.1 Demand and

Microeconomics Modified by: Yun Wang Florida International University Spring, 2018 1 Chapter 13 Monopolistic Competition: The Competitive Model in a More Realistic Setting Chapter Outline 13.1 Demand and

Exam 3 Practice Questions

Exam 3 Practice Questions 1. The price elasticity of demand is a measure of: a) how quickly a particular market reaches equilibrium. b) the change in supply associated with lower prices. c) the percent

Exam 3 Practice Questions 1. The price elasticity of demand is a measure of: a) how quickly a particular market reaches equilibrium. b) the change in supply associated with lower prices. c) the percent

Economic Analysis for Business Decisions Multiple Choice Questions Unit-2: Demand Analysis

Economic Analysis for Business Decisions Multiple Choice Questions Unit-2: Demand Analysis 1. The law of demand states that an increase in the price of a good: a. Increases the supply of that good. b.

Economic Analysis for Business Decisions Multiple Choice Questions Unit-2: Demand Analysis 1. The law of demand states that an increase in the price of a good: a. Increases the supply of that good. b.

Question Paper Business Economics I (MB1B3): January 2009

: January 2009") Question Paper Business Economics I (MB1B3): January 2009 Answer all 78 questions. Marks are indicated against each question. 1. Which of the following is not responsible for an increase in demand for

Question Paper Business Economics I (MB1B3): January 2009 Answer all 78 questions. Marks are indicated against each question. 1. Which of the following is not responsible for an increase in demand for

ECON 251. Exam 1 Pink. Fall 2013

ECON 251 1. By definition, opportunity cost is a. The value of the best alternative b. The sum of the value of all available alternatives c. The amount of money it takes to buy an item d. Always greater

ECON 251 1. By definition, opportunity cost is a. The value of the best alternative b. The sum of the value of all available alternatives c. The amount of money it takes to buy an item d. Always greater

Chapter 4: Demand Section 2

Chapter 4: Demand Section 2 Objectives 1. Explain the difference between a change in quantity demanded and a shift in the demand curve. 2. Identify the factors that create changes in demand and that can

Chapter 4: Demand Section 2 Objectives 1. Explain the difference between a change in quantity demanded and a shift in the demand curve. 2. Identify the factors that create changes in demand and that can

1. Demand: willingness to buy a good or service and the ability to pay for it; how much of an item an individual is willing to purchase at each price

1. Demand: willingness to buy a good or service and the ability to pay for it; how much of an item an individual is willing to purchase at each price 2. The two things needed for demand to exist are: willingness

1. Demand: willingness to buy a good or service and the ability to pay for it; how much of an item an individual is willing to purchase at each price 2. The two things needed for demand to exist are: willingness

Monopolistic Competition. Chapter 17

Monopolistic Competition Chapter 17 The Four Types of Market Structure Number of Firms? Many firms One firm Few firms Differentiated products Type of Products? Identical products Monopoly Oligopoly Monopolistic

Monopolistic Competition Chapter 17 The Four Types of Market Structure Number of Firms? Many firms One firm Few firms Differentiated products Type of Products? Identical products Monopoly Oligopoly Monopolistic

Midterm 1 60 minutes Econ 1101: Principles of Microeconomics October 8, Exam Form A

Midterm 1 60 minutes Econ 1101: Principles of Microeconomics October 8, 2012 Exam Form A Name Student ID number Signature Teaching Assistant Section The answer form (the bubble sheet) and this question

Midterm 1 60 minutes Econ 1101: Principles of Microeconomics October 8, 2012 Exam Form A Name Student ID number Signature Teaching Assistant Section The answer form (the bubble sheet) and this question

ECON 101 Introduction to Economics1

ECON 101 Introduction to Economics1 Session 6 The Concept of Elasticity I Lecturer: Mrs. Helen A. Seshie-Nasser, Department of Economics Contact Information: @ug.edu.gh College of Education School of Continuing

ECON 101 Introduction to Economics1 Session 6 The Concept of Elasticity I Lecturer: Mrs. Helen A. Seshie-Nasser, Department of Economics Contact Information: @ug.edu.gh College of Education School of Continuing

Econ 001: Midterm 2 (Dr. Stein) Answer Key March 31, 2008

Answer Key March 31, 2008") Instructions: Econ 001: Midterm 2 (Dr. Stein) Answer Key March 31, 2008 This is a 60-minute examination. Write all answers in the blue books provided. Show all work. Use diagrams where appropriate and

Instructions: Econ 001: Midterm 2 (Dr. Stein) Answer Key March 31, 2008 This is a 60-minute examination. Write all answers in the blue books provided. Show all work. Use diagrams where appropriate and

1 of 38 4/29/14 10:16 PM

1. award: Refer to Figure 1.8. If the university decides to lower grading standards, then This curve will shift rightward. This curve will pivot up and to the left. The curve will begin to bend downward

1. award: Refer to Figure 1.8. If the university decides to lower grading standards, then This curve will shift rightward. This curve will pivot up and to the left. The curve will begin to bend downward

CHAPTER NINE MONOPOLY

CHAPTER NINE MONOPOLY This chapter examines how a market controlled by a single producer behaves. What price will a monopolist charge for his output? How much will he produce? The basic characteristics

CHAPTER NINE MONOPOLY This chapter examines how a market controlled by a single producer behaves. What price will a monopolist charge for his output? How much will he produce? The basic characteristics

Mechanism through which buyers (demanders) and sellers (suppliers) communicate to trade goods and services.

and sellers (suppliers) communicate to trade goods and services.") By the end of this learning plan, you will be able to: Use marginal (Cost-Benefit) analysis in decision-making Apply supply and demand analysis to price determination Assess the role price plays in a market

By the end of this learning plan, you will be able to: Use marginal (Cost-Benefit) analysis in decision-making Apply supply and demand analysis to price determination Assess the role price plays in a market

Chapter 11. Monopoly

Chapter 11 Monopoly Topics Monopoly Profit Maximization. Market Power. Welfare Effects of Monopoly. Cost Advantages That Create Monopolies. Government Actions That Create Monopolies. Government Actions

Chapter 11 Monopoly Topics Monopoly Profit Maximization. Market Power. Welfare Effects of Monopoly. Cost Advantages That Create Monopolies. Government Actions That Create Monopolies. Government Actions

I DEMAND THAT YOU LEARN ABOUT DEMAND! Economics Marshall High School Mr. Cline Unit Two BA

I DEMAND THAT YOU LEARN ABOUT DEMAND! Economics Marshall High School Mr. Cline Unit Two BA Pencils for Sale: How many pencils would you be willing to buy if I sold them for $1.00 each? How many pencils

I DEMAND THAT YOU LEARN ABOUT DEMAND! Economics Marshall High School Mr. Cline Unit Two BA Pencils for Sale: How many pencils would you be willing to buy if I sold them for $1.00 each? How many pencils

Chapter 6 Elasticity: The Responsiveness of Demand and Supply

hapter 6 Elasticity: The Responsiveness of emand and Supply 1 Price elasticity of demand measures: how responsive to price changes suppliers are. how responsive sales are to changes in the price of a related

hapter 6 Elasticity: The Responsiveness of emand and Supply 1 Price elasticity of demand measures: how responsive to price changes suppliers are. how responsive sales are to changes in the price of a related

Unit II: Supply, Demand, and Consumer Choice Problem Set #2

1. /20 4. /30 2. /20 5. /10 3. /10 6. /10 Total: /100 Name: Team: Unit II: Supply, Demand, and Consumer Choice Problem Set #2 1. EXPLAIN an experience or example that shows the real world application of

1. /20 4. /30 2. /20 5. /10 3. /10 6. /10 Total: /100 Name: Team: Unit II: Supply, Demand, and Consumer Choice Problem Set #2 1. EXPLAIN an experience or example that shows the real world application of

Econ 101, section 3, F06 Schroeter Exam #2, Red. Choose the single best answer for each question.

Econ 101, section 3, F06 Schroeter Exam #2, Red Choose the single best answer for each question. 1. Which of the following is consistent with elastic demand? a. A 10% increase in price results in a 5%

Econ 101, section 3, F06 Schroeter Exam #2, Red Choose the single best answer for each question. 1. Which of the following is consistent with elastic demand? a. A 10% increase in price results in a 5%

The Competitive Model in a More Realistic Setting

CHAPTER 13 Monopolistic Competition: The Competitive Model in a More Realistic Setting Chapter Summary and Learning Objectives 13.1 Demand and Marginal Revenue for a Firm in a Monopolistically Competitive

CHAPTER 13 Monopolistic Competition: The Competitive Model in a More Realistic Setting Chapter Summary and Learning Objectives 13.1 Demand and Marginal Revenue for a Firm in a Monopolistically Competitive

Problem Set 4 Eco 112, Fall 2011 Chapters covered: Ch. 8 and Ch. 9 (up to slide 15 Price Discrimination) Due date: October 20, 2011

Due date: October 20, 2011") Problem Set 4 Eco 112, Fall 2011 Chapters covered: Ch. 8 and Ch. 9 (up to slide 15 Price Discrimination) Due date: October 20, 2011 There are 30 multiple choice questions in this problem set. Answer these

Problem Set 4 Eco 112, Fall 2011 Chapters covered: Ch. 8 and Ch. 9 (up to slide 15 Price Discrimination) Due date: October 20, 2011 There are 30 multiple choice questions in this problem set. Answer these

Lesson-9. Elasticity of Supply and Demand

Lesson-9 Elasticity of Supply and Demand Price Elasticity Businesses know that they face demand curves, but rarely do they know what these curves look like. Yet sometimes a business needs to have a good

Lesson-9 Elasticity of Supply and Demand Price Elasticity Businesses know that they face demand curves, but rarely do they know what these curves look like. Yet sometimes a business needs to have a good

2007 Thomson South-Western

Elasticity... allows us to analyze supply and demand with greater precision. is a measure of how much buyers and sellers respond to changes in market conditions THE ELASTICITY OF DEMAND The price elasticity

Elasticity... allows us to analyze supply and demand with greater precision. is a measure of how much buyers and sellers respond to changes in market conditions THE ELASTICITY OF DEMAND The price elasticity

Monopoly and How It Arises

Monopoly and How It Arises A monopoly is a market: That produces a good or service for which no close substitute exists In which there is one supplier that is protected from competition by a barrier preventing

Monopoly and How It Arises A monopoly is a market: That produces a good or service for which no close substitute exists In which there is one supplier that is protected from competition by a barrier preventing

TheRevisionGuide (www.therevisionguide.com) is a free online resource for Economics and Business Studies.

is a free online resource for Economics and Business Studies.") TheRevisionGuide.com Accelerating your potential Economics Revision AS Economics Demand Notes by: Apsara Sumanasiri Student Name : Date:. TheRevisionGuide (www.therevisionguide.com) is a free online resource

TheRevisionGuide.com Accelerating your potential Economics Revision AS Economics Demand Notes by: Apsara Sumanasiri Student Name : Date:. TheRevisionGuide (www.therevisionguide.com) is a free online resource

Imperfect Competition

Imperfect Competition 6.1 There are only two firms producing a particular product. The demand for the product is given by the relation p = 24 Q, where p denotes the price (in dollars per unit) and Q denotes

Imperfect Competition 6.1 There are only two firms producing a particular product. The demand for the product is given by the relation p = 24 Q, where p denotes the price (in dollars per unit) and Q denotes

Econ 2113 Test #2 Dr. Rupp Fall 2008

D Econ 2113 Test #2 Dr. Rupp Fall 2008 Name Pledge: I have neither given nor received aid on this exam Version A Signature: Directions: Bubble in name: Last, First Bubble in 00 in Special Codes Sign the

D Econ 2113 Test #2 Dr. Rupp Fall 2008 Name Pledge: I have neither given nor received aid on this exam Version A Signature: Directions: Bubble in name: Last, First Bubble in 00 in Special Codes Sign the

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

MBA 640, Survey of Macroeconomics Fall 2006, Quiz #2 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The price elasticity of demand is defined

MBA 640, Survey of Macroeconomics Fall 2006, Quiz #2 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The price elasticity of demand is defined

CLEP Microeconomics Practice Test

Practice Test Time 90 Minutes 80 Questions For each of the questions below, choose the best answer from the choices given. 1. In economics, the opportunity cost of an item or entity is (A) the out-of-pocket

Practice Test Time 90 Minutes 80 Questions For each of the questions below, choose the best answer from the choices given. 1. In economics, the opportunity cost of an item or entity is (A) the out-of-pocket

Supply and Demand. Objective 8.04

Supply and Demand Objective 8.04 Supply and Demand Pages 258-259 259 copy bold terms and give a definition or description of each. Page 261 Copy the questions Worksheet A-2A 1. Surplus When the amount

Supply and Demand Objective 8.04 Supply and Demand Pages 258-259 259 copy bold terms and give a definition or description of each. Page 261 Copy the questions Worksheet A-2A 1. Surplus When the amount

Midterm 1 60 minutes Econ 1101: Principles of Microeconomics October 12, Exam Form A

Midterm 1 60 minutes Econ 1101: Principles of Microeconomics October 12, 2015 Exam Form A Name Student ID number Signature Teaching Assistant Section The answer form (the bubble sheet) and this question

Midterm 1 60 minutes Econ 1101: Principles of Microeconomics October 12, 2015 Exam Form A Name Student ID number Signature Teaching Assistant Section The answer form (the bubble sheet) and this question

Professor Christina Romer SUGGESTED ANSWERS TO PROBLEM SET 2

Economics 2 Spring 2016 rofessor Christina Romer rofessor David Romer SUGGESTED ANSWERS TO ROBLEM SET 2 1.a. Recall that the price elasticity of supply is the percentage change in quantity supplied divided

Economics 2 Spring 2016 rofessor Christina Romer rofessor David Romer SUGGESTED ANSWERS TO ROBLEM SET 2 1.a. Recall that the price elasticity of supply is the percentage change in quantity supplied divided

Chapter Eleven. Monopoly

Chapter Eleven Monopoly Topics Monopoly Profit Maximization. Effects of a Shift of the Demand Curve. Market Power. Welfare Effects of Monopoly. Cost Advantages That Create Monopolies. Government Actions

Chapter Eleven Monopoly Topics Monopoly Profit Maximization. Effects of a Shift of the Demand Curve. Market Power. Welfare Effects of Monopoly. Cost Advantages That Create Monopolies. Government Actions

Homework 4 Economics

Homework 4 Economics 501.01 Manisha Goel Due: Tuesday, March 1, 011 (beginning of class). Draw and label all graphs clearly. Show all work. Explain. Question 1. Governments often regulate the price of

Homework 4 Economics 501.01 Manisha Goel Due: Tuesday, March 1, 011 (beginning of class). Draw and label all graphs clearly. Show all work. Explain. Question 1. Governments often regulate the price of

Gregory Clark Econ 1A, Winter 2012 SAMPLE FINAL

Gregory Clark Econ 1A, Winter 2012 SAMPLE FINAL 1. Medical doctors in the USA earn very high incomes compared to some other countries such as Canada. Label each of the following with N for NORMATIVE, or

Gregory Clark Econ 1A, Winter 2012 SAMPLE FINAL 1. Medical doctors in the USA earn very high incomes compared to some other countries such as Canada. Label each of the following with N for NORMATIVE, or

Demand- how much of a product consumers are willing and able to buy at a given price during a given period.

Ch. 4 Demand Ch. 4.1 The Demand Curve (Learning Objective- explain the Law of Demand) In your world- What are the goods and services that you demand? What happens to your buying when the price goes up

Ch. 4 Demand Ch. 4.1 The Demand Curve (Learning Objective- explain the Law of Demand) In your world- What are the goods and services that you demand? What happens to your buying when the price goes up

Introduction. Learning Objectives. Learning Objectives. Economics Today Twelfth Edition. Chapter 20 Demand and Supply Elasticity

Roger LeRoy Miller Economics Today Twelfth Edition Chapter 20 Demand and Supply Elasticity Introduction Cigarette consumption is relatively unresponsive to price changes, so higher cigarette taxes do not

Roger LeRoy Miller Economics Today Twelfth Edition Chapter 20 Demand and Supply Elasticity Introduction Cigarette consumption is relatively unresponsive to price changes, so higher cigarette taxes do not

AP Microeconomics Review With Answers

AP Microeconomics Review With Answers 1. Firm in Perfect Competition (Long-Run Equilibrium) 2. Monopoly Industry with comparison of price & output of a Perfectly Competitive Industry (which means show

AP Microeconomics Review With Answers 1. Firm in Perfect Competition (Long-Run Equilibrium) 2. Monopoly Industry with comparison of price & output of a Perfectly Competitive Industry (which means show

Eco 300 Intermediate Micro

Eco 300 Intermediate Micro Instructor: Amalia Jerison Office Hours: T 12:00-1:00, Th 12:00-1:00, and by appointment BA 127A, aj4575@albany.edu A. Jerison (BA 127A) Eco 300 Spring 2010 1 / 66 Page 261,

Eco 300 Intermediate Micro Instructor: Amalia Jerison Office Hours: T 12:00-1:00, Th 12:00-1:00, and by appointment BA 127A, aj4575@albany.edu A. Jerison (BA 127A) Eco 300 Spring 2010 1 / 66 Page 261,

Introduction to Agricultural Economics Agricultural Economics 105 Spring 2017 First Hour Exam Version 1

1 Name Introduction to Agricultural Economics Agricultural Economics 105 Spring 2017 First Hour Exam Version 1 There is only ONE best, correct answer per question. Place your answer on the attached sheet.

1 Name Introduction to Agricultural Economics Agricultural Economics 105 Spring 2017 First Hour Exam Version 1 There is only ONE best, correct answer per question. Place your answer on the attached sheet.

Supply and Demand. The Basis of Microeconomics

Supply and Demand The Basis of Microeconomics Learning Targets I can explain how the forces of supply and demand impact a market economy and what variables affect these forces. (Including a discussion

Supply and Demand The Basis of Microeconomics Learning Targets I can explain how the forces of supply and demand impact a market economy and what variables affect these forces. (Including a discussion

ECO 162: MICROECONOMICS

ECO 162: MICROECONOMICS PREPARED BY Dr. V.G.R. CHANDRAN Email: vgrchan@gmail.com Website: www.vgrchandran.com/default.html UNIVERSITI TEKNOLOGI MARA 0 P a g e TUTORIAL QUESTIONS ALL RIGHTS RESERVED 2010

ECO 162: MICROECONOMICS PREPARED BY Dr. V.G.R. CHANDRAN Email: vgrchan@gmail.com Website: www.vgrchandran.com/default.html UNIVERSITI TEKNOLOGI MARA 0 P a g e TUTORIAL QUESTIONS ALL RIGHTS RESERVED 2010

Monopolistic Competition

Monopolistic Competition CHAPTER16 C H A P T E R C H E C K L I S T When you have completed your study of this chapter, you will be able to 1 Describe and identify monopolistic competition. 2 Explain how

Monopolistic Competition CHAPTER16 C H A P T E R C H E C K L I S T When you have completed your study of this chapter, you will be able to 1 Describe and identify monopolistic competition. 2 Explain how

Chapter 6 Elasticity: The Responsiveness of Demand and Supply

Economics 6 th edition 1 Chapter 6 Elasticity: The Responsiveness of Demand and Supply Modified by Yulin Hou For Principles of Microeconomics Florida International University Fall 2017 The Price Elasticity

Economics 6 th edition 1 Chapter 6 Elasticity: The Responsiveness of Demand and Supply Modified by Yulin Hou For Principles of Microeconomics Florida International University Fall 2017 The Price Elasticity

ECON 251 Exam 2 Pink. Fall 2012

ECON 251 Exam 2 Pink Use the table below to answer the following four questions The table below shows Harry s total utility from consuming beer and wine. The price of beer is $2 per bottle. The price of

ECON 251 Exam 2 Pink Use the table below to answer the following four questions The table below shows Harry s total utility from consuming beer and wine. The price of beer is $2 per bottle. The price of

23 Perfect Competition

23 Perfect Competition Learning Objectives After you have studied this chapter, you should be able to 1. define price taker, total revenues, marginal revenue, short-run shutdown price, short-run breakeven

23 Perfect Competition Learning Objectives After you have studied this chapter, you should be able to 1. define price taker, total revenues, marginal revenue, short-run shutdown price, short-run breakeven

Market Structure & Imperfect Competition

In the Name of God Sharif University of Technology Graduate School of Management and Economics Microeconomics (for MBA students) 44111 (1393-94 1 st term) - Group 2 Dr. S. Farshad Fatemi Market Structure

In the Name of God Sharif University of Technology Graduate School of Management and Economics Microeconomics (for MBA students) 44111 (1393-94 1 st term) - Group 2 Dr. S. Farshad Fatemi Market Structure

ECONOMICS ASSIGNMENT CLASS XII MICRO ECONOMICS UNIT I INTRODUCTION. 4. Is free medicine given to patients in Govt. Hospital a scarce commodity?

ECONOMICS ASSIGNMENT CLASS XII MICRO ECONOMICS UNIT I INTRODUCTION 1. What is the Slope of PPC? What does it show? 2. When can PPC be a straight line? 3. Do all attainable combination of two goods that

ECONOMICS ASSIGNMENT CLASS XII MICRO ECONOMICS UNIT I INTRODUCTION 1. What is the Slope of PPC? What does it show? 2. When can PPC be a straight line? 3. Do all attainable combination of two goods that

University of Toronto February 6, ECO 100Y INTRODUCTION TO ECONOMICS Midterm Test # 3

Department of Economics Prof. Gustavo Indart University of Toronto February 6, 2009 SOLUTIONS ECO 100Y INTRODUCTION TO ECONOMICS Midterm Test # 3 LAST NAME FIRST NAME STUDENT NUMBER INSTRUCTIONS: 1. The

Department of Economics Prof. Gustavo Indart University of Toronto February 6, 2009 SOLUTIONS ECO 100Y INTRODUCTION TO ECONOMICS Midterm Test # 3 LAST NAME FIRST NAME STUDENT NUMBER INSTRUCTIONS: 1. The

Elasticity. Krzysztof Kołodziejczyk, PhD

Elasticity Krzysztof Kołodziejczyk, PhD https://flic.kr/p/j4fg3d Agenda 1. Price elasticity of demand 2. Extreme cases of elasticity 3. Elasticity and pricing 4. Elasticity in the long-term and short-term

Elasticity Krzysztof Kołodziejczyk, PhD https://flic.kr/p/j4fg3d Agenda 1. Price elasticity of demand 2. Extreme cases of elasticity 3. Elasticity and pricing 4. Elasticity in the long-term and short-term

ECO 100Y L0201 INTRODUCTION TO ECONOMICS. Midterm Test #1

epartment of Economics Prof. Gustavo Indart University of Toronto October 26, 2007 ECO 100Y L0201 INTROUCTION TO ECONOMICS SOLUTIONS Midterm Test #1 LAST NAME FIRST NAME INSTRUCTIONS: STUENT NUMBER 1.

epartment of Economics Prof. Gustavo Indart University of Toronto October 26, 2007 ECO 100Y L0201 INTROUCTION TO ECONOMICS SOLUTIONS Midterm Test #1 LAST NAME FIRST NAME INSTRUCTIONS: STUENT NUMBER 1.

CH 5 sample questions - 80

Class: Date: CH 5 sample questions - 80 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The price elasticity of demand measures the that results from a.

Class: Date: CH 5 sample questions - 80 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The price elasticity of demand measures the that results from a.

1. Welfare economics is the study of a. the well-being of less fortunate people. b. welfare programs in the United States.

1. Welfare economics is the study of a. the well-being of less fortunate people. b. welfare programs in the United States. c. the effect of income redistribution on work effort. d. how the allocation of

1. Welfare economics is the study of a. the well-being of less fortunate people. b. welfare programs in the United States. c. the effect of income redistribution on work effort. d. how the allocation of

3. At the price of $60 each, sellers offer and buyers wish to purchase pairs of jeans a day. A. 60; 20 B. 8; 24 C. 16; 16 D. 24; 8

EC201 Exam II Review 1. Ingrid has been waiting for the show "Mamma Mia!" to come to town. When it finally does come, ticket prices are $60. Ingrid's reservation price is $75. But when Ingrid tries to

EC201 Exam II Review 1. Ingrid has been waiting for the show "Mamma Mia!" to come to town. When it finally does come, ticket prices are $60. Ingrid's reservation price is $75. But when Ingrid tries to