Syllabus item: 42 Weight: 3

|

|

|

- Janis Richard

- 5 years ago

- Views:

Transcription

: The output that is produced, on average, by each unit of the variable factor.")

1 1.5 Theory of the firm and its market structures - Production and costs Syllabus item: 42 Weight: 3 Definition: Total product (TP): The total output that a firm produces, using its fixed and variable factors in a given time period Average product (AP): The output that is produced, on average, by each unit of the variable factor. (Total output number of units of the variable factor employed) Marginal product (MP): The extra output that is produced by using an extra unit of the variable factor Distinguish between the short run and long run in the context of production. Define total product, average product and marginal product, and construct diagrams to show their relationship. Explain the law of diminishing returns. Calculate total, average and marginal product from a set of data and/or diagrams. Short run: the period of time in which at least 1 f.o.p is fixed so that production can be altered by changing variable inputs. Long run: the period of time in which all f.o.p is variable, but the state of technology is fixed. Can expand scale or size of firm. All the planning takes place. Production in the short run: The law of diminishing returns Variable factors of production: Inputs which can be adjusted to alter production in the short run àlabor or materials Fixed factors of production: Inputs which cannot be adjusted to alter production in the short run à Capital or land

2 Capital Labour (L) Total product (TP) Average product (AP) Marginal product (MP) Table: Total, average, and marginal product per week - The total product keeps rising even though the marginal, and the average product is falling. - It is only when the marginal product is negative, with the addition of the ninth worker that total product starts to fall. - Marginal product curve cuts the average product curve at its highest point, where it is momentarily flat.

3 The law of diminishing returns: Definition: As more and more of a variable factor (e.g. Labour) are added to a fixed factor, output will rise initially but will eventually fall. 1) Short-run concept 2) Influences shape of SRAC curve 3) At least one of the f.o.p is fixed 4) Leads to inefficiency and waste of scarce resources 5) Where MP ( TP) starts to fall or, where MC ( TC/ TP) starts to rise (If AVC is rising, it implies diminishing marginal returns but for an accurate analysis it is necessary to do a marginal analysis, looking at changes in MC or even better at MP) 6) Output (TP) initially rises at an increasing rate (up to A), but marginal output then starts to diminish. This means that total output still increases, but at a decreasing rate (the slope of the curve tails off) AFC (SR) DMR (SR) Economies of scale (LR) Diseconomies of scale (LR)

.")

4 Syllabus item: 43 Weight: 3 Definition: Economic cost: the opportunity cost of the firm s production (including entrepreneur ship) Explain the meaning of economic costs as the opportunity cost of all resources employed by the firm (including 1. Explicit costs à Any costs to a firm that involve the direct payment of money i.e. Wage expense, rent or lease costs 2. Implicit costs entrepreneurship). Distinguish between explicit costs and implicit costs as the two components of economic costs. à Represented by lost opportunity in the use of a company's own resources, excluding cash i.e. the loss of interest income on funds, or depreciation of machinery used for a capital project. Costs of production: economic costs

Total variable cost (TVC): Total cost of the variable assets that a firm uses in a given time period.")

Long-run: all factors variable and therefore the firm can plan the ideal scale of the operation.")

5 Syllabus item: 44 Weight: 3 Definition: Total costs: the complete costs of producing output a) Total fixed cost (TFC): Total cost of the fixed assets that a firm uses in a given time period. They do not change as production is increased or decreased. They exist even if output is zero. b) Total variable cost (TVC): Total cost of the variable assets that a firm uses in a given time period. They vary with output. c) Total cost (TC): TFC +TVC Explain the distinction between the short run and the long run, with reference to fixed factors and variable factors. Distinguish between total costs, marginal costs and average costs. Draw diagrams illustrating the relationship between marginal costs and average costs, and explain the connection with production in the short run. Short-run: at least 1 f.o.p is fixed. In other words, the firm cannot change at least 1 factor Costs of production in the short run (e.g. factory building) Long-run: all factors variable and therefore the firm can plan the ideal scale of the operation. Short-run AFC, AVC, ATC, and MC curves The MC curve cuts the AVC and ATC curves at their lowest points. AFC falls as output increases, and, since it is the difference between ATC and AVC, the vertical gap between ATC and AVC gets smaller as output grows Definition: Average costs: Costs per unit of output. Total costs level of output a) Average fixed cost (AFC): Total fixed costs level of output b) Average variable cost (AVC): Total variable costs level of output c) Average (total) cost (ATC): Total costs level of output Marginal costs: The increase in total cost of producing an extra unit of output. Change in TC Change in level of output

Average variable cost (AVC) curve The average variable cost is U-shaped. AVC first decreases, reaches a minimum, and the increases.! Why?")

6 Short-run AFC, AVC< ATC< and MC curves Notes: a) Average fixed cost (AFC) curve: AFC decreases throughout the output (Q) range. AFC moves closer and closer to the horizontal axis à Why? AFC=TC/Q AFC as Q b) Average variable cost (AVC) curve The average variable cost is U-shaped. AVC first decreases, reaches a minimum, and the increases.! Why? Law of diminishing returns and the law of increasing costs c) Average total cost (ATC) curve ATC has similar shape of AVC. I It falls faster than AVC in the beginning and rises slower after reaching its minimum point.! Why? ATC = AFC + AVC. When the increase in AVC outweighs the decrease in AFC, the ATC will begin to increase forming the familiar U - shaped curve. d) Marginal cost (MC) curve: a. This curve also decreases at first, reaches a minimum, then increases. b. When MC < AVC, AVC are decreasing When MC > AVC, AVC are increasing. c. The only way for AVC to decrease (fall) is for the extra cost of the next unit produced (MC) to be less than the AVC of all the preceding units. d. MC intersects AVC and ATC at their minimum.

Economies of scale Long-run concept Measure the change in average unit cost Causes the LRAC to rise")

7 Syllabus item: 45 Weight: 3 Distinguish between increasing returns to scale, decreasing returns to scale and Definition: Returns to scale: à Long run concept that examines the change in total output as a result of increasing the total inputs constant returns to scale. (Dis) Economies of scale Long-run concept Measure the change in average unit cost Causes the LRAC to rise or fall Returns to scale Long-run concept Measures the change in total output Growth of firm can result in increasing, constant or decreasing returns to scale Production in the long run: returns to scale Efficient (=economies of scale) Inefficient (=diseconomies of scale)

Outline the relationship between")

8 Syllabus item: 46 Weight: 3 Main idea 1 Long run average cost curve (LRAC): 1. Since we know all costs are variable in the long run, we just call it the LRAC. 2. It is constructed from a series of SRAC curves + points which are tangent to the minimums of the SRAC curves associated with a series of different output levels (Q) Outline the relationship between short-run average costs and long-run average costs. Explain, using a diagram, the reason for the shape of the long-run average total cost curve. 3. U-shaped because of the existence of economies and diseconomies of scale Short run average cost curve (SRAC): 1. U-shaped because of the hypothesis of diminishing returns. Costs of production in the long run Main idea 2 In theory, LRAC curve is an envelope curve, as it envelops an infinite number of short-run average cost curves. SRAC curves represent all of the possible combinations of fixed and variable factors that could be used to produce different levels of output for this firm Ø The LRAC curve and SRAC curves At output level q3, LRAC is at its lowest point. This would be the economically efficient output level to achieve.

9 Definition: Economies of scale: Any decreases in long-run average costs that come about when a firm alters all of its f.o.p in order to increase its scale (size) of output à Leads to firms experiencing increasing returns to scale. Diseconomies of scale: Any increases in long-run average costs that come about when a firm alters all of its f.o.p in order to increase its scale (size) of output à Leads to firms experiencing decreasing returns to scale. Describe factors giving rise to economies of scale, including specialization, efficiency, marketing and indivisibilities. Describe factors giving rise to diseconomies of scale, including problems of coordination and communication Costs of production in the long run Main idea 1 Factors giving rise to economies of scale: a) Specialization b) Division of labour Main idea 2 Factors giving rise to diseconomies of scale: a) Control and communication problems b) Alienation and loss of identity c) Bulk buying d) Financial economies e) Transport economies f) Large machines g) Promotional economies

: All the revenue earned by the business. TR = p x q 2. Average revenue (AR): AR = TR q 3.")

10 1.5 Theory of the firm and its market structures - Revenues Syllabus item: 47 Weight: 3 Definition: Revenue: Income that a firm receives from selling its products, goods, and services, over a certain time period 1. Total revenue (TR): All the revenue earned by the business. TR = p x q 2. Average revenue (AR): AR = TR q 3. Marginal revenue (MR): Change in TR Change in q Distinguish between total revenue, average revenue and marginal revenue. Draw diagrams illustrating the relationship between total revenue, average revenue and marginal revenue. Calculate total revenue, average revenue and marginal revenue from a set of data and/or diagrams. 1. Perfect competition (When elasticity of demand is infinity) Theory Perfectly elastic demand curve Does not have to lower price as output increases and it wishes to sell more of its product AR =Price = MR Total revenue, average revenue and marginal revenue Cannot rise because consumer have perfect knowledge +products are homogenous

(When the demand curve is downward sloping, i.e. when elasticity of demand falls")

11 2. Imperfect competition (Monopoly, monopolistic competition, oligopoly etc.) (When the demand curve is downward sloping, i.e. when elasticity of demand falls as output increases) Price ($) Quantity Total revenue Average Marginal PED demanded (TR) ($) revenue (AR) revenue (QD) ($) (MR)($) AR = Price. Price has to be lowered to sell more products à D = AR curve MR falls as output increases twice as steeply as the AR curve and also goes below the x axis TR rises at first but will eventually start to fall as output increases. This is because negative MR + means that TR will fall ( Helpful for firms to know the impact that a change in the price of their product will have upon the total revenue that they receive)

12 Notes: The basic rules are: 1. When PED elastic à lower price to increase revenue 2. When PED inelastic à raise price to increase revenue 3. When PED unity à leave the price unchanged since revenue is already maximized

13 1.5 Theory of the firm and its market structures - Profit Syllabus item: 48 Weight: 3 Definition: Total profit: à In economics, it is Total revenue economic cost (the sum of explicit costs +implicit costs) à i.e. Abnormal, normal and loss Describe economic profit (abnormal profit) as the case where total revenue exceeds economic cost. Describe normal profit (zero economic profit) as the case where total revenue is equal to total economic costs or the situation in which the amount of revenue Economic cost: à Explicit costs + implicit costs earned is just sufficient to keep the firm in its current line of business. Explain that economic profit (abnormal profit) is profit over and above normal profit (zero economic profit), and that the firm earns normal profit when economic profit (abnormal profit) is zero. Economic profit and normal profit Main idea 1 Ø Profit = TR- TC à Profit = TR EC (EC includes explicit and implicit costs) If TR = TC à Normal profit (or zero economic profit) If TR > TC à Abnormal profit (or economic profit) If TR < TC à Loss (or negative economic profit)

14 Main idea 1 Ø Why a firm continues to operate even when earning zero economic profit Explain why a firm will continue to operate even when it earns zero economic profit (abnormal profit). Zero economic profit means that TR = EC. When we say a firm is earning zero economic profit, the firm is earning just the necessary revenues to cover payment for entrepreneurship (a cost) and all other implicit costs and explicit costs. Thus, it means that the firm has covered all Explain the meaning of loss as negative economic profit arising when total revenue is less than total cost. Calculate different profit levels from a set of data and/or diagrams. its opportunity costs, and will continue to operate. Economic profit and normal profit

use of the total")

Main idea 2 Maximum profit MC = MR (always.")

15 1.5 Theory of the firm and its market structures - Goals of firms Syllabus item: 49 Weight: 2 Main idea 1 There are two approaches to analyzing profit maximization: one involves the 1) use of the total revenue and total cost concepts, and the other involves the 2) use of marginal revenues and costs. (Though 2 nd approach is more relevant to analyzing Explain the goal of profit maximization where the difference between total revenue and total cost is maximized or where marginal revenue equals marginal cost. market structures) Main idea 2 Maximum profit MC = MR (always. No matter the market structure) Profit maximization

16 Syllabus item: 50 Weight: 4 Main idea 1 Revenue maximization: à Entrepreneurs may attempt to maximize their sales revenue by producing where the marginal revenue is zero. They will actually produce above the profit Describe alternative goals of firms, including revenue maximization, growth maximization, satisficing and corporate social responsibility. maximizing level of output. Growth maximization: à Companies may set their target to achieve growth in the short run, rather than profits, in order to gain a large market share and then dominate the market in the long run. Alternative goals for firms Main idea 2 Satisficing: à It is where an economic agent aims to perform satisfactorily rather than to a maximum level, in order to be able to pursue other goals. Corporate social responsibility (CSR): à This is where a business includes the public interest in its decision making. à i.e. Encouragng developing in the workforce and the local community through educational projects and fair trade projects à Advantages such as attracting and keeping a better workforce, building up reputation and developing brand loyalty for being an ethcal business à Disadvantages that companies may be adopting a CSR approach to gain a good reputation in order to take people s attention away from their main product

17 Syllabus item: 51 Weight: 4 Definition: Perfect competition: à A model used as the starting point to explain how firms operate. à Some industries in the world that get quite close to being perfectly competitive markets ex) wheat industry in European Union (Only differences are that there are costs in order to entry or exit the industry and also it is unlikely that producers and consumers will Describe, using examples, the assumed characteristics of perfect competition: a large number of firms; a homogeneous product; freedom of entry and exit; perfect information; perfect resource mobility. have perfect knowledge ) Assumptions of the model (Perfect competition) Main idea 1 The assumptions of perfect competition: Made up of large number of firms Individual firms are price takers (cannot affect the price of the industry; must sell at whatever the price is) Sell homogenous products (identical; no brand names) Freedom of entry and exiting the industry (=No barriers to entry or barrier to exit) Perfect knowledge Perfect information Perfect resource mobility

The firm can sell as much as it wants at P as it does not affect the industry supply curve an so it does not alter the industry price à The shape of the perfectly competitive firm s")

18 Syllabus item: 52 Weight: 3 Explain, using a diagram, the shape of the perfectly competitive firm s average revenue and marginal revenue curves, indicating that the assumptions of perfect competition imply that each firm is a price taker. Explain, using a diagram, that the perfectly competitive firm s average revenue and marginal revenue curves are derived from market equilibrium for the industry. Revenue curves (Perfect competition) Main idea 1 The industry is in perfect competition will face normal demand and supply curves à Firm derives its price of P from equilibrium price in the industry (= price taker ) The firm can sell as much as it wants at P as it does not affect the industry supply curve an so it does not alter the industry price à The shape of the perfectly competitive firm s AR and MR curves are perfectly elastic because each firm is a price-taker

, normal profit (zero")

19 Syllabus item: 53 Weight: 3 Normal profits in short-run: Explain, using diagrams, that it is possible for a perfectly competitive firm to make economic profit (abnormal profit), normal profit (zero economic profit) or negative economic profit in the short run based on the marginal cost and marginal revenue profit maximization rule. Abnormal profits in short-run: Profit maximization in the short run (Perfect comp.) Losses in short-run:

+ Allocatively efficiency (MC = AR) will make normal profit")

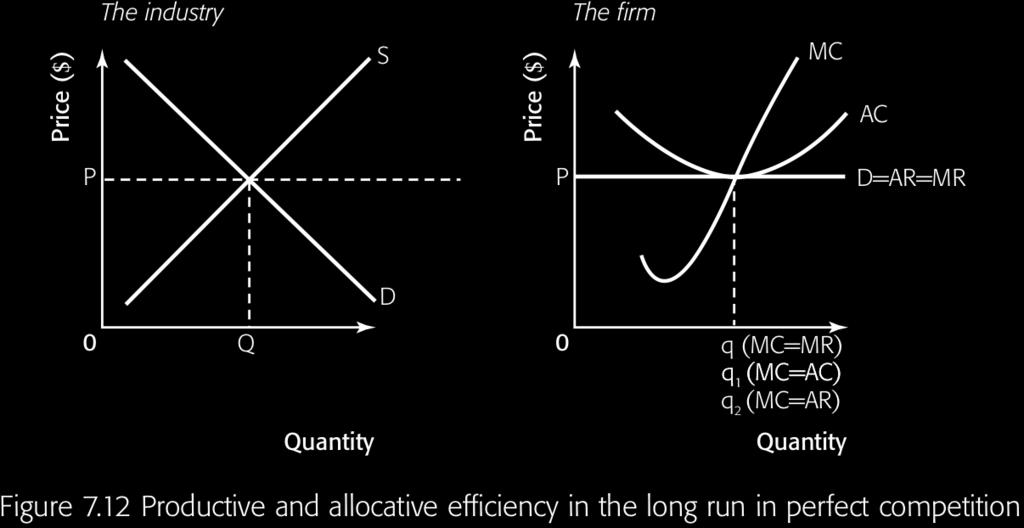

20 Main idea 1 In long-run, firms in perfect competition will make normal profits (zero economic profits) There is no abnormal profits. Explain, using a diagram, why, in the long run, a perfectly competitive firm Product efficiency (minimum AC) + Allocatively efficiency (MC = AR) will make normal profit (zero economic profit). Explain, using a diagram, how a perfectly competitive market will move from short-run equilibrium to long-run equilibrium. Firms are selling at price P, which they are taking from the industry. MC = MR so they are maximizing profits by producing q, and that output P = AC so they are making normal profits. Profit maximization in the long run (Perfect competition)

21 Main idea 2 Short-run abnormal profits to long-run normal profits As more and more firms enter the industry, attracted by the abnormal profits, the industry supply curve will start to shift to the right, driving down the price à abnormal profits that they had been making will start to be eroded As a result, we are left with the long run equilibrium position à We now find that the firms are making normal profits with P1 = C1. (exactly covering opportunity cost) à HOWEVER, there is no abnormal profit to attract more firms!! Ø Outcome: Bigger industries producing Q1 units, with smaller firms each producing q1 units. Short-run loss to long-run normal profits As more and more firms leave the industry, unable to achieve normal profit, the industry supply curve will start to shift to the left As a result, the demand curve is D1 = AR1 = MR1 à We now find that the firms are making normal profits with P1 = C1. (exactly covering opportunity cost) à HOWEVER, there is no abnormal profit to attract more firms!! Ø Outcome: A smaller industry producing only Q1 units, with bigger firms each producing q1 units.

Distinguish between the short run shut-down price and the break-even price.")

Break-even price down in the short run.")

22 Syllabus item: 55 Weight: 3 Definition: Shut-down price: à The level of price that enables a firm to cover its variable costs in the short-run, i.e. it is the price where P = AVC. If price does not cover AVC, then the firm will shut down in the short run. (P in figure 6.12) Distinguish between the short run shut-down price and the break-even price. Explain, using a diagram, when a loss-making firm would shut Break-even price: àthe level of price that enables a firm to cover all of its costs (FC + VC) in the long-run, i.e. it is the price where P = ATC. If price does not cover ATC, then the firm will shut down for good. (P1 in figure 6.12) Break-even price down in the short run. Explain, using a diagram, when a loss-making firm would shut down and exit the market in the long run. Calculate the short run shutdown price and the breakeven price from a set of data Shut-down price Shut-down price and break-even price

.")

.")

23 Syllabus item: 56 Weight: 3 Definition: Allocative efficiency: à It is where MC = AR. à The condition for allocative efficiency is P = MC (or, with externalities, MSB = MSC). Explain the meaning of the term allocative efficiency. Explain that the condition for allocative efficiency is P = MC (or, with externalities, MSB = MSC). Explain, using a diagram, why a perfectly competitive market leads to allocative efficiency in both the short run and the long run. Explain the meaning of the term productive/technical efficiency. Explain that the condition for productive efficiency is that production takes place at minimum average total cost. Explain, using a diagram, why a perfectly competitive firm will be productively efficient in the long run, though not necessarily in the short run. Definition: Productive/technical efficiency: Efficiency (Perfect competition) à Producing its product at the minimum ATC à q = productively efficient level of output (MC = AC)

24 Productive and allocative efficiency with short-run profits in perfect competition: Productive and allocative efficiency with short-run losses in perfect competition: Productive and allocative efficiency in the long run in perfect competition:

Practice Exam 3: S201 Walker Fall with answers to MC

Practice Exam 3: S201 Walker Fall 2007 - with answers to MC Print Your Name: I. Multiple Choice (3 points each) 1. If marginal utility is falling then A. total utility must be falling. B. marginal utility

Practice Exam 3: S201 Walker Fall 2007 - with answers to MC Print Your Name: I. Multiple Choice (3 points each) 1. If marginal utility is falling then A. total utility must be falling. B. marginal utility

23 Perfect Competition

23 Perfect Competition Learning Objectives After you have studied this chapter, you should be able to 1. define price taker, total revenues, marginal revenue, short-run shutdown price, short-run breakeven

23 Perfect Competition Learning Objectives After you have studied this chapter, you should be able to 1. define price taker, total revenues, marginal revenue, short-run shutdown price, short-run breakeven

Notes on Chapter 10 OUTPUT AND COSTS

Notes on Chapter 10 OUTPUT AND COSTS PRODUCTION TIMEFRAME There are many decisions made by the firm. Some decisions are major decisions that are hard to reverse without a big loss while other decisions

Notes on Chapter 10 OUTPUT AND COSTS PRODUCTION TIMEFRAME There are many decisions made by the firm. Some decisions are major decisions that are hard to reverse without a big loss while other decisions

AP Microeconomics Review Session #3 Key Terms & Concepts

The Firm, Profit, and the Costs of Production 1. Explicit vs. implicit costs 2. Short-run vs. long-run decisions 3. Fixed inputs vs. variable inputs 4. Short-run production measures: be able to calculate/graph

The Firm, Profit, and the Costs of Production 1. Explicit vs. implicit costs 2. Short-run vs. long-run decisions 3. Fixed inputs vs. variable inputs 4. Short-run production measures: be able to calculate/graph

ECON 102 Kagundu Final Exam (New Material) Practice Exam Solutions

Practice Exam Solutions") www.liontutors.com ECON 102 Kagundu Final Exam (New Material) Practice Exam Solutions 1. A A large number of firms will be able to operate in the industry because you only need to produce a small amount

www.liontutors.com ECON 102 Kagundu Final Exam (New Material) Practice Exam Solutions 1. A A large number of firms will be able to operate in the industry because you only need to produce a small amount

Total Costs. TC = TFC + TVC TFC = Fixed Costs. TVC = Variable Costs. Constant costs paid regardless of production

AP Microeconomics Total Costs TC = TFC + TVC TFC = Fixed Costs Constant costs paid regardless of production TVC = Variable Costs Costs that vary as production is changed Cost TFC TVC TFC Output Profit

AP Microeconomics Total Costs TC = TFC + TVC TFC = Fixed Costs Constant costs paid regardless of production TVC = Variable Costs Costs that vary as production is changed Cost TFC TVC TFC Output Profit

MICRO EXAM REVIEW SHEET

MICRO EXAM REVIEW SHEET 1. Firm in Perfect Competition (Long-Run Equilibrium) 2. Monopoly Industry with comparison of price & output of a Perfectly Competitive Industry 3. Natural Monopoly with Fair-Return

MICRO EXAM REVIEW SHEET 1. Firm in Perfect Competition (Long-Run Equilibrium) 2. Monopoly Industry with comparison of price & output of a Perfectly Competitive Industry 3. Natural Monopoly with Fair-Return

1.3. Levels and Rates of Change Levels: example, wages and income versus Rates: example, inflation and growth Example: Box 1.3

1 Chapter 1 1.1. Scarcity, Choice, Opportunity Cost Definition of Economics: Resources versus Wants Wants: more and better unlimited Versus Needs: essential limited Versus Demand: ability to pay + want

1 Chapter 1 1.1. Scarcity, Choice, Opportunity Cost Definition of Economics: Resources versus Wants Wants: more and better unlimited Versus Needs: essential limited Versus Demand: ability to pay + want

Practice Exam 3: S201 Walker Fall 2004

Practice Exam 3: S201 Walker Fall 2004 I. Multiple Choice (3 points each) 1. Which of the following statements about the short-run is false? A. The marginal product of labor may increase or decrease. B.

Practice Exam 3: S201 Walker Fall 2004 I. Multiple Choice (3 points each) 1. Which of the following statements about the short-run is false? A. The marginal product of labor may increase or decrease. B.

2010 Pearson Education Canada

What Is Perfect Competition? Perfect competition is an industry in which Many firms sell identical products to many buyers. There are no restrictions to entry into the industry. Established firms have

What Is Perfect Competition? Perfect competition is an industry in which Many firms sell identical products to many buyers. There are no restrictions to entry into the industry. Established firms have

AP Microeconomics Review With Answers

AP Microeconomics Review With Answers 1. Firm in Perfect Competition (Long-Run Equilibrium) 2. Monopoly Industry with comparison of price & output of a Perfectly Competitive Industry (which means show

AP Microeconomics Review With Answers 1. Firm in Perfect Competition (Long-Run Equilibrium) 2. Monopoly Industry with comparison of price & output of a Perfectly Competitive Industry (which means show

Perfect competition: occurs when none of the individual market participants (ie buyers or sellers) can influence the price of the product.

can influence the price of the product.") Perfect Competition In this section of work and the next one we derive the equilibrium positions of firms in order to determine whether or not it is profitable for a firm to produce and, if so, what quantities

Perfect Competition In this section of work and the next one we derive the equilibrium positions of firms in order to determine whether or not it is profitable for a firm to produce and, if so, what quantities

Which store has the lower costs: Wal-Mart or 7-Eleven? 2013 Pearson

Which store has the lower costs: Wal-Mart or 7-Eleven? Production and Cost 14 When you have completed your study of this chapter, you will be able to 1 Explain and distinguish between the economic and

Which store has the lower costs: Wal-Mart or 7-Eleven? Production and Cost 14 When you have completed your study of this chapter, you will be able to 1 Explain and distinguish between the economic and

Teaching about Market Structures

Teaching about Market Structures Felix B. Kwan, Ph.D. Professor of Econ/Finance, Maryville University AP Econ Conference - FRB St. Louis June 17-19, 2015 Profits Foundational Concepts Some basic terms/concepts

Teaching about Market Structures Felix B. Kwan, Ph.D. Professor of Econ/Finance, Maryville University AP Econ Conference - FRB St. Louis June 17-19, 2015 Profits Foundational Concepts Some basic terms/concepts

Chapter 33: Terms of Trade

Chapter 33: Terms of Trade 1 The Terms of Trade The division of the gains from trade depends on the terms of trade. The terms of trade are measured by the ratio of the price of exports to the price of

Chapter 33: Terms of Trade 1 The Terms of Trade The division of the gains from trade depends on the terms of trade. The terms of trade are measured by the ratio of the price of exports to the price of

The Behavior of Firms

Chapter 5 The Behavior of Firms This chapter focuses on how producers make decisions regarding supply. Individuals demand goods and services. Firms supply goods and services. An important assumption is

Chapter 5 The Behavior of Firms This chapter focuses on how producers make decisions regarding supply. Individuals demand goods and services. Firms supply goods and services. An important assumption is

The Production and Cost

The Production and Cost The Role of the Firm l The firm is an economic institution that transforms factors of production into consumer goods. It l Organizes factors of production. l Produces goods and

The Production and Cost The Role of the Firm l The firm is an economic institution that transforms factors of production into consumer goods. It l Organizes factors of production. l Produces goods and

Graded exercise questions. Level (I, ii, iii)

") Graded exercise questions Level (I, ii, iii) 248 MICRO ECONOMICS LEVEL 1 GRADED EXERCISE QUESTIONS (LEVEL I, II, III) INTRODUCTION 1. Why does an economic problem arise? 2. What is economics about? 3.

Graded exercise questions Level (I, ii, iii) 248 MICRO ECONOMICS LEVEL 1 GRADED EXERCISE QUESTIONS (LEVEL I, II, III) INTRODUCTION 1. Why does an economic problem arise? 2. What is economics about? 3.

CONTENTS. Introduction to the Series. 1 Introduction to Economics 5 2 Competitive Markets, Demand and Supply Elasticities 37

CONTENTS Introduction to the Series iv 1 Introduction to Economics 5 2 Competitive Markets, Demand and Supply 17 3 Elasticities 37 4 Government Intervention in Markets 44 5 Market Failure 53 6 Costs of

CONTENTS Introduction to the Series iv 1 Introduction to Economics 5 2 Competitive Markets, Demand and Supply 17 3 Elasticities 37 4 Government Intervention in Markets 44 5 Market Failure 53 6 Costs of

Theories of Returns. Total Product. Unit of workers

Theories of Returns Production Function: It shows a mathematical relationship between input factors and the output. Production function may be of the short run or the long run. A rational producer always

Theories of Returns Production Function: It shows a mathematical relationship between input factors and the output. Production function may be of the short run or the long run. A rational producer always

Edexcel (A) Economics A-level

Economics A-level") Edexcel (A) Economics A-level Theme 3: Business Behaviour & the Labour Market 3.3 Revenue Costs and Profits 3.3.2 Costs Notes Formulae to calculate types of costs Total cost: This is how much it costs

Edexcel (A) Economics A-level Theme 3: Business Behaviour & the Labour Market 3.3 Revenue Costs and Profits 3.3.2 Costs Notes Formulae to calculate types of costs Total cost: This is how much it costs

Introduction. Learning Objectives. Chapter 24. Perfect Competition

Chapter 24 Perfect Competition Introduction Estimates indicate that since 2003, the total amount of stored digital data on planet Earth has increased from 5 exabytes to more than 200 exabytes. Accompanying

Chapter 24 Perfect Competition Introduction Estimates indicate that since 2003, the total amount of stored digital data on planet Earth has increased from 5 exabytes to more than 200 exabytes. Accompanying

AGENDA Mon 10/12. Economics in Action Review QOD #21: Competitive Farming HW Review Pure Competition MR = MC HW: Read pp Q #7

AGENDA Mon 10/12 Economics in Action Review QOD #21: Competitive Farming HW Review Pure Competition MR = MC HW: Read pp 173-176 Q #7 QOD #21: Competitive Farming A purely competitive wheat farmer can sell

AGENDA Mon 10/12 Economics in Action Review QOD #21: Competitive Farming HW Review Pure Competition MR = MC HW: Read pp 173-176 Q #7 QOD #21: Competitive Farming A purely competitive wheat farmer can sell

Short-Run Costs and Output Decisions

Semester-I Course: 01 (Introductory Microeconomics) Unit IV - The Firm and Perfect Market Structure Lesson: Short-Run Costs and Output Decisions Lesson Developer: Jasmin Jawaharlal Nehru University Institute

Semester-I Course: 01 (Introductory Microeconomics) Unit IV - The Firm and Perfect Market Structure Lesson: Short-Run Costs and Output Decisions Lesson Developer: Jasmin Jawaharlal Nehru University Institute

2000 AP Microeconomics Exam Answers

2000 AP Microeconomics Exam Answers 1. B Scarcity is the main economic problem!!! 2. D If the wages of farm workers and movie theater employee increase, the supply of popcorn and movies will decrease (shift

2000 AP Microeconomics Exam Answers 1. B Scarcity is the main economic problem!!! 2. D If the wages of farm workers and movie theater employee increase, the supply of popcorn and movies will decrease (shift

Production and Cost Analysis I

CHAPTER 12 Production and Cost Analysis I Production is not the application of tools to materials, but logic to work. Peter Drucker McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All

CHAPTER 12 Production and Cost Analysis I Production is not the application of tools to materials, but logic to work. Peter Drucker McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All

Production and Cost Analysis I

CHAPTER 12 Production and Cost Analysis I Production is not the application of tools to materials, but logic to work. Peter Drucker McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All

CHAPTER 12 Production and Cost Analysis I Production is not the application of tools to materials, but logic to work. Peter Drucker McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All

ECO 162: MICROECONOMICS

ECO 162: MICROECONOMICS PREPARED BY Dr. V.G.R. CHANDRAN Email: vgrchan@gmail.com Website: www.vgrchandran.com/default.html UNIVERSITI TEKNOLOGI MARA 0 P a g e TUTORIAL QUESTIONS ALL RIGHTS RESERVED 2010

ECO 162: MICROECONOMICS PREPARED BY Dr. V.G.R. CHANDRAN Email: vgrchan@gmail.com Website: www.vgrchandran.com/default.html UNIVERSITI TEKNOLOGI MARA 0 P a g e TUTORIAL QUESTIONS ALL RIGHTS RESERVED 2010

Question Paper Business Economics I (MB1B3): January 2009

: January 2009") Question Paper Business Economics I (MB1B3): January 2009 Answer all 78 questions. Marks are indicated against each question. 1. Which of the following is not responsible for an increase in demand for

Question Paper Business Economics I (MB1B3): January 2009 Answer all 78 questions. Marks are indicated against each question. 1. Which of the following is not responsible for an increase in demand for

Pure Competition in the Short Run

08 Pure Competition in the Short Run McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. LO1 8-2 Four Market Models Pure competition Pure monopoly Monopolistic competition

08 Pure Competition in the Short Run McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. LO1 8-2 Four Market Models Pure competition Pure monopoly Monopolistic competition

ECONOMICS ASSIGNMENT CLASS XII MICRO ECONOMICS UNIT I INTRODUCTION. 4. Is free medicine given to patients in Govt. Hospital a scarce commodity?

ECONOMICS ASSIGNMENT CLASS XII MICRO ECONOMICS UNIT I INTRODUCTION 1. What is the Slope of PPC? What does it show? 2. When can PPC be a straight line? 3. Do all attainable combination of two goods that

ECONOMICS ASSIGNMENT CLASS XII MICRO ECONOMICS UNIT I INTRODUCTION 1. What is the Slope of PPC? What does it show? 2. When can PPC be a straight line? 3. Do all attainable combination of two goods that

MICROECONOMICS CHAPTER 10A/23 PERFECT COMPETITION. Professor Charles Fusi

MICROECONOMICS CHAPTER 10A/23 PERFECT COMPETITION Professor Charles Fusi Learning Objectives Identify the characteristics of a perfectly competitive market structure Discuss the process by which a perfectly

MICROECONOMICS CHAPTER 10A/23 PERFECT COMPETITION Professor Charles Fusi Learning Objectives Identify the characteristics of a perfectly competitive market structure Discuss the process by which a perfectly

Contents. Concepts of Revenue I-13. About the authors I-5 Preface I-7 Syllabus I-9 Chapter-heads I-11

Contents About the authors I-5 Preface I-7 Syllabus I-9 Chapter-heads I-11 1 Concepts of Revenue 1.1 Introduction 1 1.2 Concepts of Revenue 2 1.3 Revenue curves under perfect competition 3 1.4 Revenue

Contents About the authors I-5 Preface I-7 Syllabus I-9 Chapter-heads I-11 1 Concepts of Revenue 1.1 Introduction 1 1.2 Concepts of Revenue 2 1.3 Revenue curves under perfect competition 3 1.4 Revenue

Principles of Microeconomics Module 5.1. Understanding Profit

Principles of Microeconomics Module 5.1 Understanding Profit 180 Production Choices of Firms All firms have one goal in mind: MAX PROFITS PROFITS = TOTAL REVENUE TOTAL COST Two ways to reach this goal:

Principles of Microeconomics Module 5.1 Understanding Profit 180 Production Choices of Firms All firms have one goal in mind: MAX PROFITS PROFITS = TOTAL REVENUE TOTAL COST Two ways to reach this goal:

Syllabus item: 57 Weight: 3

1.5 Theory of the firm and its market structures - Monopoly Syllabus item: 57 Weight: 3 Main idea 1 Monopoly: - Only one firm producing the product (Firm = industry) - Barriers to entry or exit exists,

1.5 Theory of the firm and its market structures - Monopoly Syllabus item: 57 Weight: 3 Main idea 1 Monopoly: - Only one firm producing the product (Firm = industry) - Barriers to entry or exit exists,

Perfect Competition and The Supply Curve

chapter: 13 >> Perfect Competition and The Supply Curve The following materials are taken from Chap. 13, Economics, 2 nd ed., Krugman and Wells(2009), Worth Palgrave MaCmillan. 2009 Worth Publishers 1

chapter: 13 >> Perfect Competition and The Supply Curve The following materials are taken from Chap. 13, Economics, 2 nd ed., Krugman and Wells(2009), Worth Palgrave MaCmillan. 2009 Worth Publishers 1

ECON 311 MICROECONOMICS THEORY I

ECON 311 MICROECONOMICS THEORY I Profit Maximisation & Perfect Competition (Short-Run) Dr. F. Kwame Agyire-Tettey Department of Economics Contact Information: fagyire-tettey@ug.edu.gh Session Overview

ECON 311 MICROECONOMICS THEORY I Profit Maximisation & Perfect Competition (Short-Run) Dr. F. Kwame Agyire-Tettey Department of Economics Contact Information: fagyire-tettey@ug.edu.gh Session Overview

Unit 5. Producer theory: revenues and costs

Unit 5. Producer theory: revenues and costs Learning objectives to understand the concept of the short-run production function, describing the relationship between the quantity of inputs and the quantity

Unit 5. Producer theory: revenues and costs Learning objectives to understand the concept of the short-run production function, describing the relationship between the quantity of inputs and the quantity

Micro Semester Review Name:

Micro Semester Review Name: The following review is set up to emphasize certain concepts, graphs and terms. It is the responsibility of the individual teachers to emphasize and review the analysis aspects

Micro Semester Review Name: The following review is set up to emphasize certain concepts, graphs and terms. It is the responsibility of the individual teachers to emphasize and review the analysis aspects

ECON 101 Introduction to Economics1

ECON 101 Introduction to Economics1 Session 10 Cost Concept Lecturer: Mrs. Hellen A. Seshie-Nasser, Department of Economics Contact Information: haseshie@ug.edu.gh College of Education School of Continuing

ECON 101 Introduction to Economics1 Session 10 Cost Concept Lecturer: Mrs. Hellen A. Seshie-Nasser, Department of Economics Contact Information: haseshie@ug.edu.gh College of Education School of Continuing

Profit. Total Revenue The amount a firm receives for the sale of its output. Total Cost The market value of the inputs a firm uses in production.

Profit Total Revenue The amount a firm receives for the sale of its output. Total Cost The market value of the inputs a firm uses in production. Profit is the firm s total revenue minus its total cost.

Profit Total Revenue The amount a firm receives for the sale of its output. Total Cost The market value of the inputs a firm uses in production. Profit is the firm s total revenue minus its total cost.

Perfect Competition CHAPTER 14. Alfred P. Sloan. There s no resting place for an enterprise in a competitive economy. Perfect Competition 14

CHATER 14 erfect Competition There s no resting place for an enterprise in a competitive economy. Alfred. Sloan McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved.

CHATER 14 erfect Competition There s no resting place for an enterprise in a competitive economy. Alfred. Sloan McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved.

Slides and Images, Worth Publishers Inc. 8-1

Perfect Competition Michael J. Murray Slides and Images, Worth Publishers Inc. 8-1 Market Structure Analysis By observing a few industry characteristics, we can predict pricing and output behavior of the

Perfect Competition Michael J. Murray Slides and Images, Worth Publishers Inc. 8-1 Market Structure Analysis By observing a few industry characteristics, we can predict pricing and output behavior of the

Practice Test for Midterm 2 Econ Fall 2009 Instructor: Soojae Moon

Practice Test for Midterm 2 Econ 2010-200 Fall 2009 Instructor: Soojae Moon Please read carefully and choose the choice that best completes the statement or answers the question. Table 7-2 This table refers

Practice Test for Midterm 2 Econ 2010-200 Fall 2009 Instructor: Soojae Moon Please read carefully and choose the choice that best completes the statement or answers the question. Table 7-2 This table refers

Monopoly. 3 Microeconomics LESSON 5. Introduction and Description. Time Required. Materials

LESSON 5 Monopoly Introduction and Description Lesson 5 extends the theory of the firm to the model of a Students will see that the profit-maximization rules for the monopoly are the same as they were

LESSON 5 Monopoly Introduction and Description Lesson 5 extends the theory of the firm to the model of a Students will see that the profit-maximization rules for the monopoly are the same as they were

2007 Thomson South-Western

WHAT IS A COMPETITIVE MARKET? A competitive market has many buyers and sellers trading identical products so that each buyer and seller is a price taker. Buyers and sellers must accept the price determined

WHAT IS A COMPETITIVE MARKET? A competitive market has many buyers and sellers trading identical products so that each buyer and seller is a price taker. Buyers and sellers must accept the price determined

8 Perfect Competition

8 Perfect Competition CHAPTER 8 PERFECT COMPETITION 167 Figure 8.1 Depending upon the competition and prices offered, a wheat farmer may choose to grow a different crop. (Credit: modification of work by

8 Perfect Competition CHAPTER 8 PERFECT COMPETITION 167 Figure 8.1 Depending upon the competition and prices offered, a wheat farmer may choose to grow a different crop. (Credit: modification of work by

Eco 202 Exam 2 Spring 2014

Eco 202 Exam 2 Spring 2014 PLEASE ANSWER 50 OF THE FOLLOWING QUESTIONS. 1. Jon Brooks quit his job in a bicycle shop, where he earned $15,000 per year, to become a graduate student in economics. At the

Eco 202 Exam 2 Spring 2014 PLEASE ANSWER 50 OF THE FOLLOWING QUESTIONS. 1. Jon Brooks quit his job in a bicycle shop, where he earned $15,000 per year, to become a graduate student in economics. At the

Lecture on Competition 22 January 2003

Lecture on Competition 22 January 2003 Q: How common is Perfect Competition? A: It s not. It s RARE. I. Characteristics of PERFECT COMPETITION: Price Taker, Homogeneous Good, Perfect Info., No Transactions

Lecture on Competition 22 January 2003 Q: How common is Perfect Competition? A: It s not. It s RARE. I. Characteristics of PERFECT COMPETITION: Price Taker, Homogeneous Good, Perfect Info., No Transactions

Economic Analysis for Business Decisions Multiple Choice Questions Unit-2: Demand Analysis

Economic Analysis for Business Decisions Multiple Choice Questions Unit-2: Demand Analysis 1. The law of demand states that an increase in the price of a good: a. Increases the supply of that good. b.

Economic Analysis for Business Decisions Multiple Choice Questions Unit-2: Demand Analysis 1. The law of demand states that an increase in the price of a good: a. Increases the supply of that good. b.

In the last session we introduced the firm behaviour and the concept of profit maximisation. In this session we will build on the concepts discussed

In the last session we introduced the firm behaviour and the concept of profit maximisation. In this session we will build on the concepts discussed previously by examining cost structure, which is a key

In the last session we introduced the firm behaviour and the concept of profit maximisation. In this session we will build on the concepts discussed previously by examining cost structure, which is a key

The Theory and Estimation of Cost. Tools for Today s Decision Makers, 4/e By Paul Keat and Philip Young

The Theory and Estimation of Cost Chapter 8 Managerial Economics: Economic Managerial Economics: Economic Tools for Today s Decision Makers, 4/e By Paul Keat and Philip Young The Theory and Eti Estimation

The Theory and Estimation of Cost Chapter 8 Managerial Economics: Economic Managerial Economics: Economic Tools for Today s Decision Makers, 4/e By Paul Keat and Philip Young The Theory and Eti Estimation

Chapter Summary and Learning Objectives

CHAPTER 11 Firms in Perfectly Competitive Markets Chapter Summary and Learning Objectives 11.1 Perfectly Competitive Markets (pages 369 371) Explain what a perfectly competitive market is and why a perfect

CHAPTER 11 Firms in Perfectly Competitive Markets Chapter Summary and Learning Objectives 11.1 Perfectly Competitive Markets (pages 369 371) Explain what a perfectly competitive market is and why a perfect

WJEC (Wales) Economics A-level

Economics A-level") WJEC (Wales) Economics A-level Microeconomics Topic 1: Costs, Revenue and Profits 1.1 Costs, revenues and profits Notes The difference between the short run and the long run In the short run, the scale

WJEC (Wales) Economics A-level Microeconomics Topic 1: Costs, Revenue and Profits 1.1 Costs, revenues and profits Notes The difference between the short run and the long run In the short run, the scale

not to be republished NCERT Chapter 6 Non-competitive Markets 6.1 SIMPLE MONOPOLY IN THE COMMODITY MARKET

Chapter 6 We recall that perfect competition was theorised as a market structure where both consumers and firms were price takers. The behaviour of the firm in such circumstances was described in the Chapter

Chapter 6 We recall that perfect competition was theorised as a market structure where both consumers and firms were price takers. The behaviour of the firm in such circumstances was described in the Chapter

Decision Time Frames Pearson Education

11 OUTPUT AND COSTS Decision Time Frames The firm makes many decisions to achieve its main objective: profit maximization. Some decisions are critical to the survival of the firm. Some decisions are irreversible

11 OUTPUT AND COSTS Decision Time Frames The firm makes many decisions to achieve its main objective: profit maximization. Some decisions are critical to the survival of the firm. Some decisions are irreversible

Refer to the information provided in Figure 12.1 below to answer the questions that follow. Figure 12.1

1) A monopoly is an industry with A) a single firm in which the entry of new firms is blocked. B) a small number of firms each large enough to impact the market price of its output. C) many firms each

1) A monopoly is an industry with A) a single firm in which the entry of new firms is blocked. B) a small number of firms each large enough to impact the market price of its output. C) many firms each

2) All combinations of capital and labor along a given isoquant cost the same amount.

All combinations of capital and labor along a given isoquant cost the same amount.") Micro Problem Set III WCC Fall 2014 A=True / B=False 15 Points 1) If MC is greater than AVC, AVC must be rising. 2) All combinations of capital and labor along a given isoquant cost the same amount. 3)

Micro Problem Set III WCC Fall 2014 A=True / B=False 15 Points 1) If MC is greater than AVC, AVC must be rising. 2) All combinations of capital and labor along a given isoquant cost the same amount. 3)

Chapter 13. Microeconomics. Monopolistic Competition: The Competitive Model in a More Realistic Setting

Microeconomics Modified by: Yun Wang Florida International University Spring, 2018 1 Chapter 13 Monopolistic Competition: The Competitive Model in a More Realistic Setting Chapter Outline 13.1 Demand and

Microeconomics Modified by: Yun Wang Florida International University Spring, 2018 1 Chapter 13 Monopolistic Competition: The Competitive Model in a More Realistic Setting Chapter Outline 13.1 Demand and

Econ 2113: Principles of Microeconomics. Spring 2009 ECU

Econ 2113: Principles of Microeconomics Spring 2009 ECU Chapter 12 Monopoly Market Power Market power is the ability to influence the market, and in particular the market price, by influencing the total

Econ 2113: Principles of Microeconomics Spring 2009 ECU Chapter 12 Monopoly Market Power Market power is the ability to influence the market, and in particular the market price, by influencing the total

INTERMEDIATE MICROECONOMICS LECTURE 13 - MONOPOLISTIC COMPETITION AND OLIGOPOLY. Monopolistic Competition

13-1 INTERMEDIATE MICROECONOMICS LECTURE 13 - MONOPOLISTIC COMPETITION AND OLIGOPOLY Monopolistic Competition Pure monopoly and perfect competition are rare in the real world. Most real-world industries

13-1 INTERMEDIATE MICROECONOMICS LECTURE 13 - MONOPOLISTIC COMPETITION AND OLIGOPOLY Monopolistic Competition Pure monopoly and perfect competition are rare in the real world. Most real-world industries

micro economics - ii

micro economics - ii II SEMESTER Core course For B A ECONOMICS (CUCBCSS) (2014 Admission onwards) UNIVERSITY OF CALICUT SCHOOL OF DISTANCE EDUCATION Calicut university P.O, Malappuram Kerala, India 673

micro economics - ii II SEMESTER Core course For B A ECONOMICS (CUCBCSS) (2014 Admission onwards) UNIVERSITY OF CALICUT SCHOOL OF DISTANCE EDUCATION Calicut university P.O, Malappuram Kerala, India 673

Costs: Introduction. Costs 26/09/2017. Managerial Problem. Solution Approach. Take-away

Costs Costs: Introduction Managerial Problem Technology choice at home versus abroad: In western countries, firms use relatively capital-intensive technology. Will that same technology be cost minimizing

Costs Costs: Introduction Managerial Problem Technology choice at home versus abroad: In western countries, firms use relatively capital-intensive technology. Will that same technology be cost minimizing

7 Costs. Lesson. of Production. Introduction

Lesson 7 Costs of Production Introduction Our study now combines what we have learned about price from Lesson 5 with utility theory from Lesson 6 to allocate resources among cost factors. Consider that

Lesson 7 Costs of Production Introduction Our study now combines what we have learned about price from Lesson 5 with utility theory from Lesson 6 to allocate resources among cost factors. Consider that

CIE Economics A-level

CIE Economics A-level Topic 2: Price System and the Microeconomy c) Types of cost, revenue and profit, shortrun and long-run production Notes Short-run production function Fixed and variable factors of

CIE Economics A-level Topic 2: Price System and the Microeconomy c) Types of cost, revenue and profit, shortrun and long-run production Notes Short-run production function Fixed and variable factors of

Chapter 14 Perfectly competitive Market

Chapter 14 Perfectly competitive Market But first lets look at this Profit Maximization Profit Maximization This occurs where marginal revenue (MR) = marginal cost (MC). MR = MC Marginal revenue is the

Chapter 14 Perfectly competitive Market But first lets look at this Profit Maximization Profit Maximization This occurs where marginal revenue (MR) = marginal cost (MC). MR = MC Marginal revenue is the

Whoever claims that economic competition represents 'survival of the fittest' in the sense of the law of the jungle, provides the clearest possible

Whoever claims that economic competition represents 'survival of the fittest' in the sense of the law of the jungle, provides the clearest possible evidence of his lack of knowledge of economics. -George

Whoever claims that economic competition represents 'survival of the fittest' in the sense of the law of the jungle, provides the clearest possible evidence of his lack of knowledge of economics. -George

THE COSTS OF PRODUCTION PART II

THE COSTS OF PRODUCTION PART II It is one of the greatest economic errors to put any limitation on production... We have not the power to produce more than there is the potential to consume. - Louis D.

THE COSTS OF PRODUCTION PART II It is one of the greatest economic errors to put any limitation on production... We have not the power to produce more than there is the potential to consume. - Louis D.

7. True/False: Perfectly competitive firms can earn economic profits in the long run. a. True b. False

Economics 4020 Dr. Rupp Test #1 Sept 27 th, 2012 20 Multiple Choice questions (2.5 points each) Pledge (sign) I did not copy another student s answers 1. STC = 40 + 10Q + 0.1Q 2. SMC = 10 + 0.2Q. The market

Economics 4020 Dr. Rupp Test #1 Sept 27 th, 2012 20 Multiple Choice questions (2.5 points each) Pledge (sign) I did not copy another student s answers 1. STC = 40 + 10Q + 0.1Q 2. SMC = 10 + 0.2Q. The market

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Sample Test 3 Ch 10-13 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A cost incurred in the production of a good or service and for which

Sample Test 3 Ch 10-13 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A cost incurred in the production of a good or service and for which

Micro Economics M.A. Economics (Previous) External University of Karachi Micro-Economics

External University of Karachi Micro-Economics") Micro Economics M.A. Economics (Previous) External University of Karachi Micro-Economics Annual Examination 1997 Time allowed: 3 hours Marks: 100 Maximum 1) Attempt any five questions. 2) All questions

Micro Economics M.A. Economics (Previous) External University of Karachi Micro-Economics Annual Examination 1997 Time allowed: 3 hours Marks: 100 Maximum 1) Attempt any five questions. 2) All questions

ECON 2100 (Summer 2014 Sections 08 & 09) Exam #3D

Exam #3D") ECON 21 (Summer 214 Sections 8 & 9) Exam #3D Multiple Choice Questions: (3 points each) 1. I am taking of the exam. D. Version D 2. If a firm is currently operating at a point where costs of production

ECON 21 (Summer 214 Sections 8 & 9) Exam #3D Multiple Choice Questions: (3 points each) 1. I am taking of the exam. D. Version D 2. If a firm is currently operating at a point where costs of production

Supply and demand are the two words that economists use most often.

Chapter 13. The Costs of Production The Market Forces of Supply and Demand Supply and demand are the two words that economists use most often. Supply and demand are the forces that make market economies

Chapter 13. The Costs of Production The Market Forces of Supply and Demand Supply and demand are the two words that economists use most often. Supply and demand are the forces that make market economies

Perfectly Competitive Supply. Chapter 6. Learning Objectives

Perfectly Competitive Supply Chapter 6 McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Learning Objectives 1.Explain how opportunity cost is related to the supply

Perfectly Competitive Supply Chapter 6 McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Learning Objectives 1.Explain how opportunity cost is related to the supply

COST OF PRODUCTION & THEORY OF THE FIRM

MICROECONOMICS: UNIT III COST OF PRODUCTION & THEORY OF THE FIRM One of the concepts mentioned in both Units I and II was and its components, total cost and total revenue. In this unit, costs and revenue

MICROECONOMICS: UNIT III COST OF PRODUCTION & THEORY OF THE FIRM One of the concepts mentioned in both Units I and II was and its components, total cost and total revenue. In this unit, costs and revenue

I enjoy teaching this class. Good luck and have a nice Holiday!!

ECON 202-501 Fall 2008 Xiaoyong Cao Final Exam Form A Instructions: The exam consists of 2 parts. Part I has 35 multiple choice problems. You need to fill the answers in the table given in Part II of the

ECON 202-501 Fall 2008 Xiaoyong Cao Final Exam Form A Instructions: The exam consists of 2 parts. Part I has 35 multiple choice problems. You need to fill the answers in the table given in Part II of the

FINALTERM EXAMINATION FALL 2006

FINALTERM EXAMINATION FALL 2006 QUESTION NO: 1 (MARKS: 1) - PLEASE CHOOSE ONE Compared to the equilibrium price and quantity sold in a competitive market, a monopolist Will charge a price and sell a quantity.

FINALTERM EXAMINATION FALL 2006 QUESTION NO: 1 (MARKS: 1) - PLEASE CHOOSE ONE Compared to the equilibrium price and quantity sold in a competitive market, a monopolist Will charge a price and sell a quantity.

Perfect Competition Chapter 8

Perfect Competition Chapter 8 A Perfectly Competitive Market A perfectly competitive market is one in which economic forces operate unimpeded. A Perfectly Competitive Market For a market to be perfectly

Perfect Competition Chapter 8 A Perfectly Competitive Market A perfectly competitive market is one in which economic forces operate unimpeded. A Perfectly Competitive Market For a market to be perfectly

Production and Costs. Bibliography: Mankiw and Taylor, Ch. 6.

Production and Costs Bibliography: Mankiw and Taylor, Ch. 6. The Importance of Cost in Managerial Decisions Containing costs is a key issue in managerial decisionmaking Firms seek to reduce the number

Production and Costs Bibliography: Mankiw and Taylor, Ch. 6. The Importance of Cost in Managerial Decisions Containing costs is a key issue in managerial decisionmaking Firms seek to reduce the number

Firm Behavior and the Costs of Production

Firm Behavior and the Costs of Production WHAT ARE COSTS? The Firm s Objective The economic goal of the firm is to maximize profits. Total Revenue, Total Cost, and Profit Total Revenue, Total Cost, and

Firm Behavior and the Costs of Production WHAT ARE COSTS? The Firm s Objective The economic goal of the firm is to maximize profits. Total Revenue, Total Cost, and Profit Total Revenue, Total Cost, and

PART 1: MULTIPLE CHOICE

ECN 201, Spring 2001 NAME: Prof. Bruce Blonigen SS#: MIDTERM 2 - Version B Tuesday, May 22 **************************************************************************** Directions: This test is comprised

ECN 201, Spring 2001 NAME: Prof. Bruce Blonigen SS#: MIDTERM 2 - Version B Tuesday, May 22 **************************************************************************** Directions: This test is comprised

PART: A Introductory Micro Economics Capsules UNIT: I TOPIC: INTRODUCTION

CLASS- XII ECONOMICS PART: A Introductory Micro Economics Capsules UNIT: I TOPIC: INTRODUCTION A: Basic concepts 1. Definition of Economics 2. Central problems of an economy 3. Production possibility curve

CLASS- XII ECONOMICS PART: A Introductory Micro Economics Capsules UNIT: I TOPIC: INTRODUCTION A: Basic concepts 1. Definition of Economics 2. Central problems of an economy 3. Production possibility curve

COST THEORY. I What costs matter? A Opportunity Costs

COST THEORY Cost theory is related to production theory, they are often used together. However, here the question is how much to produce, as opposed to which inputs to use. That is, assume that we use

COST THEORY Cost theory is related to production theory, they are often used together. However, here the question is how much to produce, as opposed to which inputs to use. That is, assume that we use

The Firm s Objective. A Firm s Total Revenue and Total Cost. The economic goal of the firm is to maximize profits. A Firm s Profit

The s of Production Chapter 13 Copyright 2001 by Harcourt, Inc. The s of Production The Law of Supply: Firms are willing to produce and sell a greater quantity of a good when the price of the good is high.

The s of Production Chapter 13 Copyright 2001 by Harcourt, Inc. The s of Production The Law of Supply: Firms are willing to produce and sell a greater quantity of a good when the price of the good is high.

8 CHAPTER OUTLINE Costs in the Short Run Fixed Costs

e PART II I The Market System: Choices Made by Households and Firms e CASE FAIR OSTER PEARSON 2012 Pearson Education, Inc. Publishing as Prentice Hall PRINCIPLES OF MICROECONOMICS E L E V E N T H E D I

e PART II I The Market System: Choices Made by Households and Firms e CASE FAIR OSTER PEARSON 2012 Pearson Education, Inc. Publishing as Prentice Hall PRINCIPLES OF MICROECONOMICS E L E V E N T H E D I

ECO 162: MICROECONOMICS INTRODUCTION TO ECONOMICS Quiz 1. ECO 162: MICROECONOMICS DEMAND Quiz 2

INTRODUCTION TO ECONOMICS Quiz 1 Answer the entire question You are required to give brief explanation for each of the questions. 1. Explain the basic economic concepts with the help of Production Possibility

INTRODUCTION TO ECONOMICS Quiz 1 Answer the entire question You are required to give brief explanation for each of the questions. 1. Explain the basic economic concepts with the help of Production Possibility

1. Why is utility subjective? 2. What are inferior options? 3. Suppose the price of A is 1, the price of B is 2 and the price of C is 1.

Study Questions for Chapters 7-11 Chapter 7 1. Why is utility subjective? 2. What are inferior options? 3. Suppose the price of A is 1, the price of B is 2 and the price of C is 1.50 a. Complete the following

Study Questions for Chapters 7-11 Chapter 7 1. Why is utility subjective? 2. What are inferior options? 3. Suppose the price of A is 1, the price of B is 2 and the price of C is 1.50 a. Complete the following

Supply in a Competitive Market

Supply in a Competitive Market 8 Introduction 8 Chapter Outline 8.1 Market Structures and Perfect Competition in the Short Run 8.2 Profit Maximization in a Perfectly Competitive Market 8.3 Perfect Competition

Supply in a Competitive Market 8 Introduction 8 Chapter Outline 8.1 Market Structures and Perfect Competition in the Short Run 8.2 Profit Maximization in a Perfectly Competitive Market 8.3 Perfect Competition

CHAPTER 8: THE COSTS OF PRODUCTION

CHAPTER 8: THE COSTS OF PRODUCTION Introduction Now that we have examined consumer behavior in more detail, it is time to look at the decision making of the firm. Costs of production are important to determine

CHAPTER 8: THE COSTS OF PRODUCTION Introduction Now that we have examined consumer behavior in more detail, it is time to look at the decision making of the firm. Costs of production are important to determine

Chapter 7 Consumer/Producers and Market Efficiency

Midterm #2 Exam Study uestions: (A subset of these questions/concepts will be on the exam) Chapter 5 - Elasticity Define rice elasticity of demand. What does it mean to say demand is highly elastic? What

Midterm #2 Exam Study uestions: (A subset of these questions/concepts will be on the exam) Chapter 5 - Elasticity Define rice elasticity of demand. What does it mean to say demand is highly elastic? What

Econ 001: Midterm 2 (Dr. Stein) Answer Key March 23, 2011

Answer Key March 23, 2011") Instructions: Econ 001: Midterm 2 (Dr. Stein) Answer Key March 23, 2011 This is a 60-minute examination. Write all answers in the blue books provided. Show all work. Use diagrams where appropriate and

Instructions: Econ 001: Midterm 2 (Dr. Stein) Answer Key March 23, 2011 This is a 60-minute examination. Write all answers in the blue books provided. Show all work. Use diagrams where appropriate and

MONOPOLY. Characteristics

OBJECTIVES Explain how managers should set price and output when they have market power With monopoly power, the firm s demand curve is the market demand curve. A monopolist is the only seller of a product

OBJECTIVES Explain how managers should set price and output when they have market power With monopoly power, the firm s demand curve is the market demand curve. A monopolist is the only seller of a product

Chapter 11. Microeconomics. Technology, Production, and Costs. Modified by: Yun Wang Florida International University Spring 2018

Microeconomics Modified by: Yun Wang Florida International University Spring 2018 1 Chapter 11 Technology, Production, and Costs Chapter Outline 11.1 Technology: An Economic Definition 11.2 The Short Run

Microeconomics Modified by: Yun Wang Florida International University Spring 2018 1 Chapter 11 Technology, Production, and Costs Chapter Outline 11.1 Technology: An Economic Definition 11.2 The Short Run

ECO 610: Lecture 7. Perfectly Competitive Markets

ECO 610: Lecture 7 Perfectly Competitive Markets Perfectly Competitive Markets: Outline Goal: understanding firm and market supply in competitive markets Characteristics of perfectly competitive industries

ECO 610: Lecture 7 Perfectly Competitive Markets Perfectly Competitive Markets: Outline Goal: understanding firm and market supply in competitive markets Characteristics of perfectly competitive industries

L08. Chapter 11 Firms in Perfectly Competitive Markets

L08 Chapter 11 Firms in Perfectly Competitive Markets Def: Produced without using most conventional pesticides; fertilizers made with synthetic ingredients or sewage sludge; bioengineering; or ionizing

L08 Chapter 11 Firms in Perfectly Competitive Markets Def: Produced without using most conventional pesticides; fertilizers made with synthetic ingredients or sewage sludge; bioengineering; or ionizing

Microeonomics. Firms in Competitive Markets. In this chapter, look for the answers to these questions: Introduction: A Scenario. N.

C H A T E R 14 Firms in Competitive Markets R I N C I L E S O F Microeonomics N. Gregory Mankiw remium oweroint Slides by Ron Cronovich 2009 South-Western, a part of Cengage Learning, all rights reserved

C H A T E R 14 Firms in Competitive Markets R I N C I L E S O F Microeonomics N. Gregory Mankiw remium oweroint Slides by Ron Cronovich 2009 South-Western, a part of Cengage Learning, all rights reserved

Understanding Markets

Understanding Markets EC8005 Lecture 7 2014 Michael King 1 Revision: Consumer Theory 1. Qd = f(p,ps, Pc, Y, T, O) 2. Sd = f(p, T, I, G, Tx, Sy, O) 3. Types of goods 4. Shift along v s shift in demand/supply

Understanding Markets EC8005 Lecture 7 2014 Michael King 1 Revision: Consumer Theory 1. Qd = f(p,ps, Pc, Y, T, O) 2. Sd = f(p, T, I, G, Tx, Sy, O) 3. Types of goods 4. Shift along v s shift in demand/supply

Faculty of Economics, Thammasat University EE 211 Principles of Microeconomics (3 credits)

") Faculty of Economics, Thammasat University EE 211 Principles of Microeconomics (3 credits) Semester 1/2014 ----------------------------------------------------------------------------------------------

Faculty of Economics, Thammasat University EE 211 Principles of Microeconomics (3 credits) Semester 1/2014 ----------------------------------------------------------------------------------------------

Micro Perfect Competition Essentials 1 WCC

Micro erfect Competition Essentials 1 WCC Industry structure/characteristics affects how demand curves and revenue behave for a firm. erfectly Competitive Industry Characteristics 1) There are a large

Micro erfect Competition Essentials 1 WCC Industry structure/characteristics affects how demand curves and revenue behave for a firm. erfectly Competitive Industry Characteristics 1) There are a large

ECON 260 (2,3) Practice Exam #4 Spring 2007 Dan Mallela

Practice Exam #4 Spring 2007 Dan Mallela") ECON 260 (2,3) Practice Exam #4 Spring 2007 Dan Mallela Multiple Choice Identify the letter of the choice that best completes the statement or answers the question. 1. Profit is defined as a. net revenue

ECON 260 (2,3) Practice Exam #4 Spring 2007 Dan Mallela Multiple Choice Identify the letter of the choice that best completes the statement or answers the question. 1. Profit is defined as a. net revenue