ACCOUNTING FOR MERCHANDISING OPERATIONS

|

|

|

- Barnard Sharp

- 5 years ago

- Views:

Transcription

1 Chapter 05 ACCOUNTING FOR MERCHANDISING OPERATIONS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved.

2 5-2 C 1 SERVICE COMPANIES Service organizations sell time to earn revenue. Examples: Accounting firms, law firms and plumbing services

3 5-3 C 1 MERCHANDISER Merchandising Companies Manufacturer Wholesaler Retailer Consumers

4 C 1 REPORTING INCOME FOR A MERCHANDISER 5-4 Merchandising companies sell products to earn revenue. Examples: sporting goods, clothing, and auto parts stores

5 C 2 OPERATING CYCLE FOR A MERCHANDISER Begins with the purchase of merchandise and ends with the collection of cash from the sale of merchandise. 5-5

6 5-6 C 2 INVENTORY SYSTEMS

7 5-7 C 2 INVENTORY SYSTEMS Perpetual systems continually update accounting records for merchandising transactions Periodic systems accounting records relating to merchandise transactions are updated only at the end of the accounting period

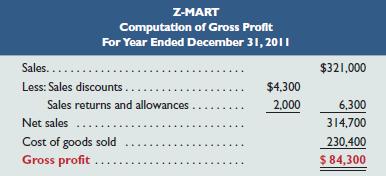

8 5-8 P1 MERCHANDISE PURCHASES On November 2, Z-Mart purchased $1,200 of merchandise inventory for cash.

9 5-9 P1 TRADE DISCOUNTS Used by manufacturers and wholesalers to offer better prices for greater quantities purchased. Example Z-Mart offers a 30% trade discount for orders of 1,000 units or more on its popular product Racer. Each Racer has a list price of $5.25. Quantity sold 1,000 Price per unit $ 5.25 Total 5,250 Less 30% discount (1,575) Invoice price $ 3,675

10 5-10 P1 ACCOUNTING FOR MERCHANDISE PURCHASES

11 5-11 P1 PURCHASE DISCOUNTS A deduction from the invoice price granted to induce early payment of the amount due.

12 5-12 P1 PURCHASE DISCOUNTS 2/10,n/30 Discount Percent Number of Days Discount Is Available Otherwise, Net (or All) Is Due in 30 Days Credit Period

13 5-13 P1 PURCHASE DISCOUNTS On November 2, Z-Mart purchased $1,200 of merchandise inventory on account, credit terms are 2/10, n/30.

14 5-14 P1 PURCHASE DISCOUNTS On November 12, Z-Mart paid the amount due on the purchase of November 2.

15 5-15 P1 PURCHASE DISCOUNTS After we post these entries, the accounts involved look like these:

16 5-16 P1 PURCHASE RETURNS AND ALLOWANCES Purchase Return... Merchandise returned by the purchaser to the supplier. Purchase Allowance... A reduction in the cost of defective or unacceptable merchandise received by a purchaser from a supplier.

17 5-17 P1 PURCHASE RETURNS AND ALLOWANCES On November 15, Z-Mart (buyer) issues a $300 debit memorandum for an allowance from Trex for defective merchandise.

18 5-18 P1 PURCHASE RETURNS AND ALLOWANCES Z-Mart purchases $1,000 of merchandise on June 1 with terms 2/10, n/60. Two days later, Z-Mart returns $100 of goods before paying the invoice. When Z-Mart later pays on June 11, it takes the 2% discount only on the $900 remaining balance.

19 P1 TRANSPORTATION COSTS AND OWNERSHIP TRANSFER 5-19

20 5-20 P1 TRANSPORTATION COSTS Z-Mart purchased merchandise on terms of FOB shipping point. The transportation charge is $75.

21 5-21 P1 ACCOUNTING FOR MERCHANDISE

22 P2 ACCOUNTING FOR MERCHANDISE SALES 5-22

23 5-23 P2 SALES OF MERCHANDISE Each sales transaction for a seller of merchandise involves two parts: Revenue received in the form of an asset from a customer. Recognition of the cost of merchandise sold to a customer.

24 5-24 P2 SALES OF MERCHANDISE On November 3, Z-Mart sold $2,400 of merchandise on credit. The merchandise has a cost basis to Z-Mart of $1,600.

25 5-25 P2 SALES DISCOUNTS Sales discounts on credit sales can benefit a seller by decreasing the delay in receiving cash and reducing future collection efforts.

26 5-26 P2 SALES DISCOUNTS Z-Mart completes a $1,000 credit sale with terms of 2/10, n/60. The account was paid in full within the 60-day period. The account was paid in full within the 10-day discount period.

27 5-27 P2 SALES RETURNS AND ALLOWANCES Sales returns and allowances usually involve dissatisfied customers and the possibility of lost future sales. Sales returns refer to merchandise that customers return to the seller after a sale. Sales allowances refer to reductions in the selling price of merchandise sold to customers.

28 5-28 P2 SALES RETURNS AND ALLOWANCES Recall Z-Mart s sale for $2,400 that had a cost of $1,600. Assume the customer returns part of the merchandise. The returned items sell for $800 and cost $600. Sales Returns and Allowances is a Contra Account subtracted from sales Defective inventory valued at estimated value not its cost

29 5-29 P2 SALES ALLOWANCES Assume that $800 of the merchandise Z-Mart sold on November 3 is defective but the buyer decides to keep it because Z-Mart offers a $100 price reduction. Sales Allowance

30 5-30 P2 MERCHANDISING COST FLOW IN THE ACCOUNTING CYCLE Beginning inventory Net purchases Period 1 Merchandise available for sale Ending inventory Beginning inventory Cost of goods sold Net purchases To Income Statement To Balance Sheet Period 2 Merchandise available for sale Ending inventory Cost of goods sold To Income Statement To Balance Sheet

31 P3 ADJUSTING ENTRIES FOR MERCHANDISERS 5-31 A merchandiser using a perpetual inventory system is usually required to make an adjustment to update the Merchandise Inventory account to reflect any loss of merchandise, including theft and deterioration. Z-Mart s Merchandise Inventory account at the end of year 2011 has a balance of $21,250, but a physical count reveals that only $21,000 of inventory exists. Inventory Shrinkage difference of physical count and recorded inventory

32 P3 CLOSING ENTRIES FOR MERCHANDISERS 5-32

33 5-33 P4 A multiple-step income statement format shows detailed computations of net sales and other costs and expenses, and reports subtotals for various classes of items.

34 5-34 P4 SINGLE-STEP INCOME STATEMENT

35 5-35 CLASSIFIED BALANCE SHEET Highly Liquid Less Liquid

36 5-36 GLOBAL VIEW Accounting for Merchandise Purchases and Sales Both U.S. GAAP and IFRS include broad and similar guidance for the accounting of merchandise purchases and sales. Financial Statement Differences 1. Order of expenses 2. Separate disclosures 3. Presentation of expenses 4. Classification of operating and nonoperating expenses 5. Alternative measures of income 6. Order of current and noncurrent items on the balance sheet

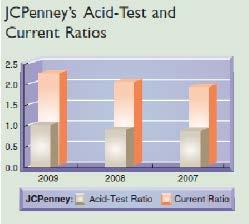

37 5-37 A1 ACID-TEST RATIO Acid-Test Ratio = Quick Assets Current Liabilities Acid-Test Ratio = Cash + S-T Investments + Receivables Current Liabilities A common rule of thumb is the acid-test ratio should have a value of at least 1.0 to conclude a company is unlikely to face liquidity problems in the near future.

38 5-38 A2 GROSS MARGIN RATIO Gross Margin Ratio = Net Sales - Cost of Goods Sold Net Sales Percentage of dollar sales available to cover expenses and provide a profit.

39 5-39 A1/A2 JCPENNEY

40 5-40 P5 APPENDIX 5A: PERIODIC INVENTORY SYSTEM (a) (b) (c) (d) (e) (f) (g) A periodic inventory system requires updating the inventory account only at the end of a period to reflect the quantity and cost of both the goods available and the goods sold.

41 5-41 P5 APPENDIX 5A: PERIODIC INVENTORY SYSTEM

42 5-42 P5 APPENDIX 5B: WORKSHEET PERPETUAL SYSTEM

43 END OF CHAPTER

Financial Accounting. John J. Wild. Sixth Edition. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 04 Reporting and Analyzing Merchandising Operations Conceptual

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 04 Reporting and Analyzing Merchandising Operations Conceptual

INVENTORIES AND COST OF SALES

Chapter 06 INVENTORIES AND COST OF SALES PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA McGraw-Hill/Irwin

Chapter 06 INVENTORIES AND COST OF SALES PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA McGraw-Hill/Irwin

CHAPTER 4 ACCOUNTING FOR MERCHANDISING OPERATIONS

CHAPTER 4 ACCOUNTING FOR MERCHANDISING OPERATIONS Key Terms and Concepts to Know Income Statements: Single-step income statement Multiple-step income statement Gross Margin = Gross Profit = Net Sales Cost

CHAPTER 4 ACCOUNTING FOR MERCHANDISING OPERATIONS Key Terms and Concepts to Know Income Statements: Single-step income statement Multiple-step income statement Gross Margin = Gross Profit = Net Sales Cost

Accounting for Merchandising Operations

5-1 Chapter 5 Accounting for Merchandising Operations Learning Objectives After studying this chapter, you should be able to: 1. Identify the differences between service and merchandising companies. 2.

5-1 Chapter 5 Accounting for Merchandising Operations Learning Objectives After studying this chapter, you should be able to: 1. Identify the differences between service and merchandising companies. 2.

Accounting for Merchandising Operations

5-1 Chapter 5 Accounting for Merchandising Operations Learning Objectives After studying this chapter, you should be able to: 1. Identify the differences between service and merchandising companies. 2.

5-1 Chapter 5 Accounting for Merchandising Operations Learning Objectives After studying this chapter, you should be able to: 1. Identify the differences between service and merchandising companies. 2.

ACCOUNTING FOR MERCHANDISING ACTIVITIES

Chapter 6 ACCOUNTING FOR MERCHANDISING ACTIVITIES Presented by: Endra M. Sagoro Economic Faculty YSU endra_ms@uny.ac.id Operating Cycle of a Merchandising Company Cash Accounts Receivable 2. Sale of merchandise

Chapter 6 ACCOUNTING FOR MERCHANDISING ACTIVITIES Presented by: Endra M. Sagoro Economic Faculty YSU endra_ms@uny.ac.id Operating Cycle of a Merchandising Company Cash Accounts Receivable 2. Sale of merchandise

ACCOUNTING FOR PERPETUAL AND PERIODIC INVENTORY METHODS

ACCOUNTING FOR PERPETUAL AND PERIODIC INVENTORY METHODS Key Terms and Concepts to Know Merchandise Inventory: Merchandise Inventory (Inventory or MI) refers to the goods the company has purchased and intends

ACCOUNTING FOR PERPETUAL AND PERIODIC INVENTORY METHODS Key Terms and Concepts to Know Merchandise Inventory: Merchandise Inventory (Inventory or MI) refers to the goods the company has purchased and intends

CHAPTER 5: MERCHANDISING OPERATIONS

CHAPTER 5: MERCHANDISING OPERATIONS CHAPTER SYNOPSIS Chapter 5 first compares a service business with a merchandising business and then discusses the purchase and sale of merchandise inventory. The chapter

CHAPTER 5: MERCHANDISING OPERATIONS CHAPTER SYNOPSIS Chapter 5 first compares a service business with a merchandising business and then discusses the purchase and sale of merchandise inventory. The chapter

Financial Accounting. John J. Wild. Sixth Edition. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 05 Reporting and Analyzing Inventories Conceptual Chapter

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 05 Reporting and Analyzing Inventories Conceptual Chapter

CHAPTER 5. Accounting for Merchandising Operations 2, 3, , 12, 13, 14

CHAPTER 5 Accounting for Merchandising Operations ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems *1. Identify the differences between

CHAPTER 5 Accounting for Merchandising Operations ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems *1. Identify the differences between

Chapter 5: Merchandising Operations and the Multiple-Step Income Statement

Vocabulary Quiz 1. A detailed inventory system in which the cost of each inventory item is maintained and the records continuously show the inventory that should be on hand. 2. A reduction given by a seller

Vocabulary Quiz 1. A detailed inventory system in which the cost of each inventory item is maintained and the records continuously show the inventory that should be on hand. 2. A reduction given by a seller

6) Items purchased for resale with a right of return must be presented separately from other inventories.

Items purchased for resale with a right of return must be presented separately from other inventories.") Chapter 8 Cost-based Inventories and Cost of Sales 1) Inventories are assets consisting of goods owned by the business and held for future sale or for use in the manufacture of goods for sale. Answer:

Chapter 8 Cost-based Inventories and Cost of Sales 1) Inventories are assets consisting of goods owned by the business and held for future sale or for use in the manufacture of goods for sale. Answer:

Managerial Accounting and Cost Concepts

Managerial Accounting and Cost Concepts Chapter 2 PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Copyright

Managerial Accounting and Cost Concepts Chapter 2 PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Copyright

Financial Accounting Chapter 6 Notes Inventories

Financial Accounting Notes Inventories I. Management Issues Associated with Accounting with Inventory. Defining Inventory: 1. Assets held for resale purpose in a normal course of business. (Current Asset)

Financial Accounting Notes Inventories I. Management Issues Associated with Accounting with Inventory. Defining Inventory: 1. Assets held for resale purpose in a normal course of business. (Current Asset)

MGACO1 INTERMEDIATE ACCOUNTING I

MGACO1 INTERMEDIATE ACCOUNTING I S. Daga Topic: INVENTORY TEXT: Chapter 8 (excl. appendix) TEXT QUESTIONS: E8-11, E8-22, P8-3, Case IC8-1 LEARNING GOALS: 1. RECOGNITION - Understand key inventory concerns.

MGACO1 INTERMEDIATE ACCOUNTING I S. Daga Topic: INVENTORY TEXT: Chapter 8 (excl. appendix) TEXT QUESTIONS: E8-11, E8-22, P8-3, Case IC8-1 LEARNING GOALS: 1. RECOGNITION - Understand key inventory concerns.

Chapter 8 Inventories: Measurement

Chapter 8 Inventories: Measurement QUESTIONS FOR REVIEW OF KEY TOPICS Question 8 1 Inventory for a manufacturing company consists of (1) raw materials, (2) work in process, and (3) finished goods. Raw

Chapter 8 Inventories: Measurement QUESTIONS FOR REVIEW OF KEY TOPICS Question 8 1 Inventory for a manufacturing company consists of (1) raw materials, (2) work in process, and (3) finished goods. Raw

Chapter 7: Merchandise Inventory

1 Chapter 7: Merchandise Inventory 2 3 Merchandise Inventory What is inventory? Items held for resale to customers Who has inventory? Wholesaler or Retailer - Merchandise Inventory Manufacturer - Raw Materials

1 Chapter 7: Merchandise Inventory 2 3 Merchandise Inventory What is inventory? Items held for resale to customers Who has inventory? Wholesaler or Retailer - Merchandise Inventory Manufacturer - Raw Materials

CHAPTER 8. Valuation of Inventories: A Cost-Basis Approach 1, 2, 3, 4, 5, 6, 7, 8, 11, 12, 14, 15, 16

CHAPTER 8 Valuation of Inventories: A Cost-Basis Approach ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Inventory accounts; determining

CHAPTER 8 Valuation of Inventories: A Cost-Basis Approach ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Inventory accounts; determining

Heintz & Parry. 20 th Edition. College Accounting

Heintz & Parry 20 th Edition College Accounting Chapter 13 Accounting for Merchandise Inventory 1 Explain the impact of merchandise inventory on the financial statements. Errors in inventory will cause

Heintz & Parry 20 th Edition College Accounting Chapter 13 Accounting for Merchandise Inventory 1 Explain the impact of merchandise inventory on the financial statements. Errors in inventory will cause

PREVIEW OF CHAPTER. Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 8-2

8-1 PREVIEW OF CHAPTER 8 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 8-2 8 Valuation of Inventories: A Cost-Basis Approach LEARNING OBJECTIVES After studying this chapter, you

8-1 PREVIEW OF CHAPTER 8 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 8-2 8 Valuation of Inventories: A Cost-Basis Approach LEARNING OBJECTIVES After studying this chapter, you

Chapter 9 Inventories: Additional Issues

Chapter 9 Inventories: Additional Issues QUESTIONS FOR REVIEW OF KEY TOPICS Question 9 1 GAAP generally requires the use of historical cost to value assets, but a departure from cost is necessary when

Chapter 9 Inventories: Additional Issues QUESTIONS FOR REVIEW OF KEY TOPICS Question 9 1 GAAP generally requires the use of historical cost to value assets, but a departure from cost is necessary when

Managerial Accounting: An Overview

Managerial Accounting: An Overview Chapter 1 PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Copyright

Managerial Accounting: An Overview Chapter 1 PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Copyright

Ch6 Practice Test Part 1: Multiple Choice Choose the most correct answer from the choices provided.

Part 1: Multiple Choice Choose the most correct answer from the choices provided. 1. The factor which determines whether or not goods should be included in a physical count of inventory is a. physical

Part 1: Multiple Choice Choose the most correct answer from the choices provided. 1. The factor which determines whether or not goods should be included in a physical count of inventory is a. physical

CHAPTER 6. Inventory Costing. Brief Questions Exercises Exercises 4, 5, 6, 7 3, 4, *14 3, 4, 5, 6, *12, *13 7, 8, 9, 10, 11, 12, 13

CHAPTER 6 Inventory Costing ASSIGNMENT CLASSIFICATION TABLE Study Objectives Brief Questions Exercises Exercises Problems Set A Problems Set B 1. Describe the steps in determining inventory quantities.

CHAPTER 6 Inventory Costing ASSIGNMENT CLASSIFICATION TABLE Study Objectives Brief Questions Exercises Exercises Problems Set A Problems Set B 1. Describe the steps in determining inventory quantities.

Inventories. 2. Explain the accounting for inventories and apply the inventory cost flow methods.

6-1 Chapter 6 Inventories Learning Objectives After studying this chapter, you should be able to: 1. Describe the steps in determining inventory quantities. 2. Explain the accounting for inventories and

6-1 Chapter 6 Inventories Learning Objectives After studying this chapter, you should be able to: 1. Describe the steps in determining inventory quantities. 2. Explain the accounting for inventories and

Accounting Principles: A Business Perspective, 8e Chapter 7: Measuring and Reporting Inventories

Accounting Principles: A Business Perspective, 8e Chapter 7: Measuring and Reporting Inventories Inventories and of Goods Sold For merchandising companies, inventory is often the largest asset on the balance

Accounting Principles: A Business Perspective, 8e Chapter 7: Measuring and Reporting Inventories Inventories and of Goods Sold For merchandising companies, inventory is often the largest asset on the balance

CHAPTER5. Accounting for Merchandising Operations. Apago PDF Enhancer. Study Objectives. Feature Story

CHAPTER5 Study Objectives After studying this chapter, you should be able to: [1] Identify the differences between service and merchandising companies. [2] Explain the recording of purchases under a perpetual

CHAPTER5 Study Objectives After studying this chapter, you should be able to: [1] Identify the differences between service and merchandising companies. [2] Explain the recording of purchases under a perpetual

Pengantar Akuntansi I Akuntansi Untuk Perusahaan Dagang

Modul ke: 08 Fakultas FEB Pengantar Akuntansi I Akuntansi Untuk Perusahaan Dagang Hari Setiyawati / Diah Iskandar/ Nurlis / Fitri Indriawati Program Studi Akuntansi Operasi Perusahaan Dagang Perusahaan

Modul ke: 08 Fakultas FEB Pengantar Akuntansi I Akuntansi Untuk Perusahaan Dagang Hari Setiyawati / Diah Iskandar/ Nurlis / Fitri Indriawati Program Studi Akuntansi Operasi Perusahaan Dagang Perusahaan

Chapter Outline. Study Objective 1 - Describe the Steps in Determining Inventory Quantities

Chapter 6 Financial Notes and BE Chapter Outline Study Objective 1 - Describe the Steps in Determining Inventory Quantities In a merchandising company, inventory consists of many different items. These

Chapter 6 Financial Notes and BE Chapter Outline Study Objective 1 - Describe the Steps in Determining Inventory Quantities In a merchandising company, inventory consists of many different items. These

Algorithmic Granite Bay Jet Ski, Incorporated

Algorithmic Granite Bay Jet Ski, Incorporated Level II 1 st Edition Transactions For June 10-16 and the Mid-Project Evaluation Did you backup your data files at the end of Module One? It is recommended

Algorithmic Granite Bay Jet Ski, Incorporated Level II 1 st Edition Transactions For June 10-16 and the Mid-Project Evaluation Did you backup your data files at the end of Module One? It is recommended

7-1. Prepared by Coby Harmon University of California, Santa Barbara Westmont College

7-1 Prepared by Coby Harmon University of California, Santa Barbara Westmont College 7 Accounting Information Systems Learning Objectives After studying this chapter, you should be able to: [1] Identify

7-1 Prepared by Coby Harmon University of California, Santa Barbara Westmont College 7 Accounting Information Systems Learning Objectives After studying this chapter, you should be able to: [1] Identify

COURSE DESCRIPTION. Rev 2.0 March 2017

COURSE DESCRIPTION This CE course provides information on inventory management. Information discussed includes inventory methods and accounting systems, cost of goods sold, and inventory turnovers and

COURSE DESCRIPTION This CE course provides information on inventory management. Information discussed includes inventory methods and accounting systems, cost of goods sold, and inventory turnovers and

Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 9-2

9-1 C H A P T E R 9 INVENTORIES: ADDITIONAL VALUATION ISSUES Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 9-2 Learning Objectives 1. Describe and apply the lower-of-cost-or-net realizable

9-1 C H A P T E R 9 INVENTORIES: ADDITIONAL VALUATION ISSUES Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 9-2 Learning Objectives 1. Describe and apply the lower-of-cost-or-net realizable

ACCOUNTING Canadian Eighth Edition Volume 1

ADAPTING YOUR LECTURE NOTES (FOR USERS OF WEYGANDT ET AL., ACCOUNTING PRINCIPLES, 4/C/E) Elizabeth A. Zaleschuk ACCOUNTING Canadian Eighth Edition Volume 1 Charles T. Horngren / Walter T. Harrison / M.

ADAPTING YOUR LECTURE NOTES (FOR USERS OF WEYGANDT ET AL., ACCOUNTING PRINCIPLES, 4/C/E) Elizabeth A. Zaleschuk ACCOUNTING Canadian Eighth Edition Volume 1 Charles T. Horngren / Walter T. Harrison / M.

FFQA 1. Complied by: Mohammad Faizan Farooq Qadri Attari ACCA (Finalist) Contact:

Contact:") FFQA 1 Objective of IAS 2 The objective of IAS 2 is to prescribe the accounting treatment for inventories. It provides guidance for determining the cost of inventories and for subsequently recognising

FFQA 1 Objective of IAS 2 The objective of IAS 2 is to prescribe the accounting treatment for inventories. It provides guidance for determining the cost of inventories and for subsequently recognising

CHAPTER 6. Inventories ASSIGNMENT CLASSIFICATION TABLE For Instructor Use Only 6-1. Brief. B Problems. A Problems 1, 2, 3, 4, 5

CHAPTER 6 Inventories ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Exercises A Problems B Problems 1. Describe the steps in determining inventory quantities. 1, 2, 3, 4, 5

CHAPTER 6 Inventories ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Exercises A Problems B Problems 1. Describe the steps in determining inventory quantities. 1, 2, 3, 4, 5

CEBU CPAR CENTER. M a n d a u e C I t y

Page 1 of 9 CEBU CPAR CENTER M a n d a u e C I t y AUDITING PROBLEMS AUDIT OF INVENTORIES PROBLEM NO. 1 The Pasay Company is a wholesale distributor of automobile replacement parts. Initial amounts taken

Page 1 of 9 CEBU CPAR CENTER M a n d a u e C I t y AUDITING PROBLEMS AUDIT OF INVENTORIES PROBLEM NO. 1 The Pasay Company is a wholesale distributor of automobile replacement parts. Initial amounts taken

Chapter 8: Cost-Based Inventories and Cost of Sales

Chapter 8: Cost-Based Inventories and Cost of Sales Case 8-1 Love Your Pet, Inc. 8-2 Alliance Appliance Ltd. 8-3 Terrific Titles Inc. Suggested Time Technical Review TR-1 Right to Recovery Asset... 5 TR-2

Chapter 8: Cost-Based Inventories and Cost of Sales Case 8-1 Love Your Pet, Inc. 8-2 Alliance Appliance Ltd. 8-3 Terrific Titles Inc. Suggested Time Technical Review TR-1 Right to Recovery Asset... 5 TR-2

C H A P T E R 8 VALUATION OF INVENTORIES: A COST-BASIS APPROACH

C H A P T E R 8 VALUATION OF INVENTORIES: A COST-BASIS APPROACH Inventories are: items held for sale, or goods to be used in the production of goods to be sold. Businesses with : Intermediate Accounting

C H A P T E R 8 VALUATION OF INVENTORIES: A COST-BASIS APPROACH Inventories are: items held for sale, or goods to be used in the production of goods to be sold. Businesses with : Intermediate Accounting

INVENTORIES, DISCUSSION QUESTIONS

INVENTORIES, DISCUSSION QUESTIONS Cristina Maslach Zampetakis Laschinger 1. The receiving report should be reconciled to the initial purchase order and the vendor s invoice before recording or paying for

INVENTORIES, DISCUSSION QUESTIONS Cristina Maslach Zampetakis Laschinger 1. The receiving report should be reconciled to the initial purchase order and the vendor s invoice before recording or paying for

CHAPTER 8. Valuation of Inventories: A Cost-Basis Approach 1, 2, 3, 4, 5, 6, 8, Perpetual vs. periodic. 2 9, 13, 14, 17, 20

CHAPTER 8 Valuation of Inventories: A Cost-Basis Approach ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Inventory accounts; determining

CHAPTER 8 Valuation of Inventories: A Cost-Basis Approach ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Inventory accounts; determining

CHAPTER 7 INVENTORIES

INVENTORIES DISCUSSION QUESTIONS 1. The receiving report should be reconciled to the initial purchase order and the vendor s invoice before inventory purchases are recorded and paid. This procedure will

INVENTORIES DISCUSSION QUESTIONS 1. The receiving report should be reconciled to the initial purchase order and the vendor s invoice before inventory purchases are recorded and paid. This procedure will

CHAPTER 6 INVENTORIES

1. The receiving report should be reconciled to the initial purchase order and the vendor s invoice before recording or paying for inventory purchases. This procedure will verify that the inventory received

1. The receiving report should be reconciled to the initial purchase order and the vendor s invoice before recording or paying for inventory purchases. This procedure will verify that the inventory received

Accounting Services. Study Guide

Accounting Services Study Guide Assessments: 0001 Accounts Payable Clerk 0002 Accounts Receivable Clerk 0003 Full-Charge Bookkeeper 0004 Payroll Clerk Endorsed by the American Institute of Professional

Accounting Services Study Guide Assessments: 0001 Accounts Payable Clerk 0002 Accounts Receivable Clerk 0003 Full-Charge Bookkeeper 0004 Payroll Clerk Endorsed by the American Institute of Professional

Chapter 2 An Introduction to Cost Terms and Purposes

Chapter 2 An Introduction to Cost Terms and Purposes Copyright 2003 Pearson Education Canada Inc. Slide 2-15 Costs and Cost Objects Cost a resource sacrificed or foregone to achieve a specific objective

Chapter 2 An Introduction to Cost Terms and Purposes Copyright 2003 Pearson Education Canada Inc. Slide 2-15 Costs and Cost Objects Cost a resource sacrificed or foregone to achieve a specific objective

Chapter 11 Vendors & Purchases. Copyright 2009 by The McGraw-Hill Companies, Inc. All Rights Reserved.

Chapter 11 Vendors & Purchases McGraw-Hill/Irwin Copyright 2009 by The McGraw-Hill Companies, Inc. All Rights Reserved. Vendors & Purchases Chapter 11 begins Part 3 of the book: Peachtree Complete Accounting

Chapter 11 Vendors & Purchases McGraw-Hill/Irwin Copyright 2009 by The McGraw-Hill Companies, Inc. All Rights Reserved. Vendors & Purchases Chapter 11 begins Part 3 of the book: Peachtree Complete Accounting

IFRS 15: Revenue from Contract with Customers. Credibility. Professionalism. AccountAbility 1

IFRS 15: Revenue from Contract with Customers Credibility. Professionalism. AccountAbility 1 Agenda Overview Illustrations 2 Definition of revenue Revenue is the fair value of consideration received or

IFRS 15: Revenue from Contract with Customers Credibility. Professionalism. AccountAbility 1 Agenda Overview Illustrations 2 Definition of revenue Revenue is the fair value of consideration received or

TEACHING AID EXPLORING ACCOUNTING AND REPORTING ALTERNATIVES FOR THE INVENTORY LCM PROCEDURE. Kennard S. Brackney, Ph.D. Professor

TEACHING AID EXPLORING ACCOUNTING AND REPORTING ALTERNATIVES FOR THE INVENTORY LCM PROCEDURE Kennard S. Brackney, Ph.D. Professor Philip R. Witmer, Ph.D. Professor witmerpr@appstate.edu (828) 262-6232

TEACHING AID EXPLORING ACCOUNTING AND REPORTING ALTERNATIVES FOR THE INVENTORY LCM PROCEDURE Kennard S. Brackney, Ph.D. Professor Philip R. Witmer, Ph.D. Professor witmerpr@appstate.edu (828) 262-6232

CHAPTER 6 INVENTORIES SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY. Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT

CHAPTER 6 INVENTORIES SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 C 8. 2 C 15. 3 K a 22. 7 C sg 29. 3

CHAPTER 6 INVENTORIES SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 C 8. 2 C 15. 3 K a 22. 7 C sg 29. 3

COURSE TITLE. Honors Accounting LENGTH. Full Year Grades DEPARTMENT. Business Education Barbara O Donnell, Supervisor SCHOOL

COURSE TITLE Honors Accounting LENGTH Full Year Grades 11-12 DEPARTMENT Business Education Barbara O Donnell, Supervisor SCHOOL Rutherford High School DATE Fall 2016 Honors Accounting Page 1 I. Introduction/Overview/Philosophy

COURSE TITLE Honors Accounting LENGTH Full Year Grades 11-12 DEPARTMENT Business Education Barbara O Donnell, Supervisor SCHOOL Rutherford High School DATE Fall 2016 Honors Accounting Page 1 I. Introduction/Overview/Philosophy

These Review Notes for the CHAE Examination. Stephen M. LeBruto, Ed.D, CPA, CHAE. i Management and Technology. Rosen College of Hospitality Management

CHAE Review Basics, Inventory and Internal Controls These Review Notes for the CHAE Examination Were Prepared By: Stephen M. LeBruto, Ed.D, CPA, CHAE HFTP Professor of Hospitality Financial i Management

CHAE Review Basics, Inventory and Internal Controls These Review Notes for the CHAE Examination Were Prepared By: Stephen M. LeBruto, Ed.D, CPA, CHAE HFTP Professor of Hospitality Financial i Management

PREVIEW OF CHAPTER 9-2

9-1 PREVIEW OF CHAPTER 9 9-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 9 Inventories: Additional Valuation Issues LEARNING OBJECTIVES After studying this chapter, you should

9-1 PREVIEW OF CHAPTER 9 9-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 9 Inventories: Additional Valuation Issues LEARNING OBJECTIVES After studying this chapter, you should

Advanced Accounting (Level 1) Vocabulary/Content

Vocabulary/Content") Unit 1: Introduction to Accounting (Module 1 Chapters 1 & 2) Suggested Duration: about 30 days Advanced Accounting (Level 1) Standards, Big Ideas, and Essential Questions Competencies and Accounting Core

Unit 1: Introduction to Accounting (Module 1 Chapters 1 & 2) Suggested Duration: about 30 days Advanced Accounting (Level 1) Standards, Big Ideas, and Essential Questions Competencies and Accounting Core

Adjusted Trial Balance Debit Credit Debit Credit Debit Credit Merchandise Inv. 16 Store Supplies 10 Store Equipment 20 Accum. Depr. Store Equip.

GRADED PROJECT Directions: Be sure to make an electronic copy of your answer before submitting it to Ashworth College for grading. Unless otherwise stated, answer in complete sentences, and be sure to

GRADED PROJECT Directions: Be sure to make an electronic copy of your answer before submitting it to Ashworth College for grading. Unless otherwise stated, answer in complete sentences, and be sure to

CHAPTER 6. Inventories 12, 13, , , 11 16, , 13

CHAPTER 6 Inventories ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems 1. Describe the steps in determining inventory quantities. 1, 2,

CHAPTER 6 Inventories ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems 1. Describe the steps in determining inventory quantities. 1, 2,

Revenue from Contracts with Customers

Revenue from Contracts with Customers The standard is final A comprehensive look at the new revenue model No. US2014-01 (supplement) June 18, 2014 What s inside: Overview... 1 Right of return... 2 Sell-through

Revenue from Contracts with Customers The standard is final A comprehensive look at the new revenue model No. US2014-01 (supplement) June 18, 2014 What s inside: Overview... 1 Right of return... 2 Sell-through

Revenue from contracts with customers

Revenue from contracts with customers The standard is final A comprehensive look at the new revenue model No. INT2014-02 (supplement) 18 June 2014 (Revised 8 September 2014*) What s inside: Overview...

Revenue from contracts with customers The standard is final A comprehensive look at the new revenue model No. INT2014-02 (supplement) 18 June 2014 (Revised 8 September 2014*) What s inside: Overview...

ACCOUNTING. Year Prerequisite: None (Personal Financial Management Recommended)

") ACCOUNTING BS000001 (1 st Semester) BS000002 (2 nd Semester) ACCOUNTING Grades 10, 11, 12 Year Prerequisite: None (Personal Financial Management Recommended) 1 Unit All This is a one-year course that will

ACCOUNTING BS000001 (1 st Semester) BS000002 (2 nd Semester) ACCOUNTING Grades 10, 11, 12 Year Prerequisite: None (Personal Financial Management Recommended) 1 Unit All This is a one-year course that will

7 Estimate the value of inventory using the. 8 Measure a company's management of. 9 Determine the value of inventory using the

1 Determine the value of inventory using the specific identification method under the perpetual inventory system 2 Determine the value of inventory using the first-in, first-out (FIFO) method under the

1 Determine the value of inventory using the specific identification method under the perpetual inventory system 2 Determine the value of inventory using the first-in, first-out (FIFO) method under the

Revenue from contracts with customers

Revenue from contracts with customers The standard is final A comprehensive look at the new revenue model No. INT2014-02 (supplement) June 18, 2014 What s inside: Overview... 1 Right of return... 2 Sell-through

Revenue from contracts with customers The standard is final A comprehensive look at the new revenue model No. INT2014-02 (supplement) June 18, 2014 What s inside: Overview... 1 Right of return... 2 Sell-through

C H A P T E R. Inventories. Corporate Financial Accounting 13e. human/istock/360/getty Images. Warren Reeve Duchac

C H A P T E R 6 Inventories Corporate Financial Accounting 13e Warren Reeve Duchac human/istock/360/getty Images Safeguarding Inventory (slide 1 of 2) Controls for safeguarding inventory begin as soon

C H A P T E R 6 Inventories Corporate Financial Accounting 13e Warren Reeve Duchac human/istock/360/getty Images Safeguarding Inventory (slide 1 of 2) Controls for safeguarding inventory begin as soon

Chapter 7 Condensed (Day 1)

") Chapter 7 Condensed (Day 1) I. Valuing and Cost of Goods Sold (COGS) II. Costing Methods: Specific Identification, FIFO, LIFO, and Average Cost III. When managers use FIFO, LIFO, and Average Cost IV. Lower-of-Cost-or-Market

Chapter 7 Condensed (Day 1) I. Valuing and Cost of Goods Sold (COGS) II. Costing Methods: Specific Identification, FIFO, LIFO, and Average Cost III. When managers use FIFO, LIFO, and Average Cost IV. Lower-of-Cost-or-Market

Revenue for chemical manufacturers

Revenue for chemical manufacturers The new standard s effective date is coming. US GAAP August 2017 kpmg.com/us/frv b Revenue for chemical manufacturers Revenue viewed through a new lens Again and again,

Revenue for chemical manufacturers The new standard s effective date is coming. US GAAP August 2017 kpmg.com/us/frv b Revenue for chemical manufacturers Revenue viewed through a new lens Again and again,

Q Financial Results

Q1 2017 Financial Results Safe Harbor The information presented herein may contain forward-looking statements. Such forward-looking statements include all statements other than statements of historical

Q1 2017 Financial Results Safe Harbor The information presented herein may contain forward-looking statements. Such forward-looking statements include all statements other than statements of historical

New revenue guidance. Implementation in the consumer markets industry. At a glance

New revenue guidance Implementation in the consumer markets industry No. US2017-27 September 29, 2017 What s inside: Overview... 1 Identify the contract with the customer... 2 Identify performance obligations...

New revenue guidance Implementation in the consumer markets industry No. US2017-27 September 29, 2017 What s inside: Overview... 1 Identify the contract with the customer... 2 Identify performance obligations...

Intuit QuickBooks Enterprise Solutions 11.0 Complete List of Reports

Intuit QuickBooks Enterprise Solutions 11.0 Complete List of Reports Intuit QuickBooks Enterprise Solutions is the most advanced QuickBooks product for businesses with more complex needs. It offers advanced

Intuit QuickBooks Enterprise Solutions 11.0 Complete List of Reports Intuit QuickBooks Enterprise Solutions is the most advanced QuickBooks product for businesses with more complex needs. It offers advanced

Itawamba Community College ACC 2213 Principles of Accounting I

Itawamba Community College ACC 2213 Principles of Accounting I The Business Division provides student learning opportunities in Accounting, Business Communications, Legal Environment of Business, Economics,

Itawamba Community College ACC 2213 Principles of Accounting I The Business Division provides student learning opportunities in Accounting, Business Communications, Legal Environment of Business, Economics,

ACC106 Office Accounting I Administration Outline

ACC106 Office Accounting I Administration Outline Course Information Organization Mercer County Community College Credits 3 Contact Hours 3 Description Basic accounting course designed for non-transfer

ACC106 Office Accounting I Administration Outline Course Information Organization Mercer County Community College Credits 3 Contact Hours 3 Description Basic accounting course designed for non-transfer

ACCOUNTING FOR RETAILER-ISSUED GIFT CARDS: REVENUE RECOGNITION AND FINANCIAL STATEMENT DISCLOSURES

Page 1 ACCOUNTING FOR RETAILER-ISSUED GIFT CARDS: REVENUE RECOGNITION AND FINANCIAL STATEMENT DISCLOSURES Janice L. Ammons, Quinnipiac University Gary P. Schneider, Quinnipiac University Aamer Sheikh,

Page 1 ACCOUNTING FOR RETAILER-ISSUED GIFT CARDS: REVENUE RECOGNITION AND FINANCIAL STATEMENT DISCLOSURES Janice L. Ammons, Quinnipiac University Gary P. Schneider, Quinnipiac University Aamer Sheikh,

CHAPTER 2: ACCOUNTING FOR MATERIALS

1. An effective cost control system should include: a. An established plan of objectives and goals to be achieved. b. Regular reports showing the difference between goals and actual performance. c. Specific

1. An effective cost control system should include: a. An established plan of objectives and goals to be achieved. b. Regular reports showing the difference between goals and actual performance. c. Specific

Accounting for Manufacturing

Accounting for Manufacturing 1 Accounting for Manufacturing and Inventory Impairments TABLE OF CONTENTS Accounting for manufacturing 2 Production activities 2 Production cost flows 3 Accounting for production

Accounting for Manufacturing 1 Accounting for Manufacturing and Inventory Impairments TABLE OF CONTENTS Accounting for manufacturing 2 Production activities 2 Production cost flows 3 Accounting for production

Sri Lanka Accounting Standard LKAS 2. Inventories

Sri Lanka Accounting Standard LKAS 2 Inventories CONTENTS paragraphs SRI LANKA ACCOUNTING STANDARD LKAS 2 INVENTORIES OBJECTIVE 1 SCOPE 2 5 DEFINITIONS 6 8 MEASUREMENT OF INVENTORIES 9 33 Cost of inventories

Sri Lanka Accounting Standard LKAS 2 Inventories CONTENTS paragraphs SRI LANKA ACCOUNTING STANDARD LKAS 2 INVENTORIES OBJECTIVE 1 SCOPE 2 5 DEFINITIONS 6 8 MEASUREMENT OF INVENTORIES 9 33 Cost of inventories

Type of Inventory. OVERVIEW In case of manufacturing concerns. Stores and Spares. Formulae for Determining Cost of Inventory

CHAPTER 4 INVENTORIES LEARNING OUTCOMES After studying this chapter, you will be able to: Understand the meaning of term 'Inventory'. Learn the technique of Specific identification method, FIFO, Average

CHAPTER 4 INVENTORIES LEARNING OUTCOMES After studying this chapter, you will be able to: Understand the meaning of term 'Inventory'. Learn the technique of Specific identification method, FIFO, Average

Management s Accountability to Stakeholders Stakeholders Provide Management is accountable for: Owners Operating activities Government Creditors

Chapter 15 Distinguish management accounting from financial accounting Management Management s Accountability to Stakeholders Stakeholders Owners Government Provide Management is accountable for: Operating

Chapter 15 Distinguish management accounting from financial accounting Management Management s Accountability to Stakeholders Stakeholders Owners Government Provide Management is accountable for: Operating

Kianoff & Associates Crystal Clear Reports for Sage 100

Kianoff & Associates Crystal Clear Reports for Sage 100 We have developed Crystal Reports for all current versions of Sage 100 and are available for most all modules. Accounts Payable BP801- Vendor File

Kianoff & Associates Crystal Clear Reports for Sage 100 We have developed Crystal Reports for all current versions of Sage 100 and are available for most all modules. Accounts Payable BP801- Vendor File

Agenda. Scan Based Trading a Case Study. Wholesale Distribution Industry. Industry Thought Leader 8/28/2012

Scan Based Trading a Case Study Wholesale Distribution Industry Anir Bhattacharyya Industry Thought Leader Agenda Wholesale Distribution Market Challenges & Trends Scan Based Trading Challenges What is

Scan Based Trading a Case Study Wholesale Distribution Industry Anir Bhattacharyya Industry Thought Leader Agenda Wholesale Distribution Market Challenges & Trends Scan Based Trading Challenges What is

CHAPTER 2 OVERVIEW OF BUSINESS PROCESSES

CHAPTER 2 OVERVIEW OF BUSINESS PROCESSES SUGGESTED ANSWERS TO DISCUSSION QUESTIONS 2.1 Three different types of information exist in Table 2.1: 1. Internally-generated financial data 2. Internally-generated

CHAPTER 2 OVERVIEW OF BUSINESS PROCESSES SUGGESTED ANSWERS TO DISCUSSION QUESTIONS 2.1 Three different types of information exist in Table 2.1: 1. Internally-generated financial data 2. Internally-generated

RETAILING. April 23, 2018

RETAILING April 23, 2018 TODAY S AGENDA Continue on with Unit 6: Pricing New Lesson: Pricing Policies Unit 6 Quiz - Friday PRICING POLICIES Retail pricing is influenced by both controllable and uncontrollable

RETAILING April 23, 2018 TODAY S AGENDA Continue on with Unit 6: Pricing New Lesson: Pricing Policies Unit 6 Quiz - Friday PRICING POLICIES Retail pricing is influenced by both controllable and uncontrollable

GLOSSARY OF TERMS ENTREPRENEURSHIP AND BUSINESS INNOVATION

Accounts Payable - short term debts incurred as the result of day-to-day operations. Accounts Receivable - monies due to your enterprise as the result of day-to-day operations. Accrual Based Accounting

Accounts Payable - short term debts incurred as the result of day-to-day operations. Accounts Receivable - monies due to your enterprise as the result of day-to-day operations. Accrual Based Accounting

Including International Financial Reporting Standards (IFRS)

") COMPILED BY AL KHADASH Financial Accounting Including International Financial Reporting Standards (IFRS) McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Accounting:

COMPILED BY AL KHADASH Financial Accounting Including International Financial Reporting Standards (IFRS) McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Accounting:

Pure Monopoly. McGraw-Hill/Irwin. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

10 Pure Monopoly McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Four Market Models Characteristics of the Four Basic Market Models Characteristic Number of firms

10 Pure Monopoly McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Four Market Models Characteristics of the Four Basic Market Models Characteristic Number of firms

LPA Retail System s 2012 User Fair

LPA Retail System s 2012 User Fair LPA BUSINESS MEASUREMENTS LPA Measuring what Matters to Reach your Business Goals Increase Revenue Decrease Costs Improve Accountability Improve ability to make informed

LPA Retail System s 2012 User Fair LPA BUSINESS MEASUREMENTS LPA Measuring what Matters to Reach your Business Goals Increase Revenue Decrease Costs Improve Accountability Improve ability to make informed

HONORS FINANCIAL ACCOUNTING

FREEHOLD REGIONAL HIGH SCHOOL DISTRICT OFFICE OF CURRICULUM AND INSTRUCTION BUSINESS ADMINISTRATION SPECIALIZED LEARNING CENTER HONORS FINANCIAL ACCOUNTING COURSE PHILOSOPHY The Financial Accounting course

FREEHOLD REGIONAL HIGH SCHOOL DISTRICT OFFICE OF CURRICULUM AND INSTRUCTION BUSINESS ADMINISTRATION SPECIALIZED LEARNING CENTER HONORS FINANCIAL ACCOUNTING COURSE PHILOSOPHY The Financial Accounting course

ACCOUNTING. Contest Basics SAC 2016

ACCOUNTING Contest Basics SAC 2016 P a g e 2 UIL Accounting Basics Agenda 1. Constitution & Contest Rules and NEW Handbook 2. 2017 Condensed Contest Schedule & Solution 3. State-adopted textbooks (high

ACCOUNTING Contest Basics SAC 2016 P a g e 2 UIL Accounting Basics Agenda 1. Constitution & Contest Rules and NEW Handbook 2. 2017 Condensed Contest Schedule & Solution 3. State-adopted textbooks (high

Vendor Partnership Manual. Section 16 - Allowances

Vendor Partnership Manual Section 16 - Allowances No changes have occurred in this chapter since our last update in January 2017. TABLE OF CONTENTS 1. Introduction... 1 1.1 What is Vendor Allowance?...

Vendor Partnership Manual Section 16 - Allowances No changes have occurred in this chapter since our last update in January 2017. TABLE OF CONTENTS 1. Introduction... 1 1.1 What is Vendor Allowance?...

Chapter 2. Job Order Costing and Analysis QUESTIONS

Chapter 2 Job Order Costing and Analysis QUESTIONS 1. Factory overhead is not identified with specific units (jobs) or batches (job lots). Therefore, to assign costs, estimates of the relation between

Chapter 2 Job Order Costing and Analysis QUESTIONS 1. Factory overhead is not identified with specific units (jobs) or batches (job lots). Therefore, to assign costs, estimates of the relation between

1. The cost of an item is the sacrifice of resources made to acquire it. 2. An expense is a cost charged against revenue in an accounting period.

Chapter 02 Cost Concepts and Behavior True / False Questions 1. The cost of an item is the sacrifice of resources made to acquire it. True False 2. An expense is a cost charged against revenue in an accounting

Chapter 02 Cost Concepts and Behavior True / False Questions 1. The cost of an item is the sacrifice of resources made to acquire it. True False 2. An expense is a cost charged against revenue in an accounting

Chapter 12: Vendors & Purchases

Chapter 12: Vendors & Purchases McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Vendors & Purchases Chapter 12 begins Part 3 of the book: Peachtree Complete Accounting

Chapter 12: Vendors & Purchases McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Vendors & Purchases Chapter 12 begins Part 3 of the book: Peachtree Complete Accounting

Chapter 2 Vendors. Copyright 2009 by The McGraw-Hill Companies, Inc. All Rights Reserved.

Chapter 2 Vendors McGraw-Hill/Irwin Copyright 2009 by The McGraw-Hill Companies, Inc. All Rights Reserved. Vendor Transactions In Chapter 2, you learn how Peachtree handles Accounts Payable transactions

Chapter 2 Vendors McGraw-Hill/Irwin Copyright 2009 by The McGraw-Hill Companies, Inc. All Rights Reserved. Vendor Transactions In Chapter 2, you learn how Peachtree handles Accounts Payable transactions

SOLUTIONS. Learning Goal 18

S1 Learning Goal 18 Multiple Choice 1. c FIFO puts the oldest costs into cost of goods sold and in a period of rising prices the oldest costs will be lowest costs. This leaves the latest and highest costs

S1 Learning Goal 18 Multiple Choice 1. c FIFO puts the oldest costs into cost of goods sold and in a period of rising prices the oldest costs will be lowest costs. This leaves the latest and highest costs

In this module, you will learn to place tickets on hold and sell tickets to a customer.

POS MERCURY PROGRAM GUIDE In this module, you will learn to place tickets on hold and sell tickets to a customer.» Benefits of Joining the Mercury Program Get more money back when buying or selling via

POS MERCURY PROGRAM GUIDE In this module, you will learn to place tickets on hold and sell tickets to a customer.» Benefits of Joining the Mercury Program Get more money back when buying or selling via

Inventories Corporate Accounting Summer Professor SP Kothari. June 24, 2004

Inventories 15.511 Corporate Accounting Summer 2004 Professor SP Kothari Sloan School of Management Massachusetts Institute of Technology June 24, 2004 1 Inventory Definition: Inventory is defined as goods

Inventories 15.511 Corporate Accounting Summer 2004 Professor SP Kothari Sloan School of Management Massachusetts Institute of Technology June 24, 2004 1 Inventory Definition: Inventory is defined as goods

SAP Lease Accounting Solution

LEASEACCELERATOR SAP Lease Accounting Solution LeaseAccelerator offers a complete lease accounting solution for companies with SAP-centric financial systems. Our application supports both the new standards

LEASEACCELERATOR SAP Lease Accounting Solution LeaseAccelerator offers a complete lease accounting solution for companies with SAP-centric financial systems. Our application supports both the new standards

New revenue guidance Implementation in the technology sector

No. US2017-08 April 25, 2017 What s inside: Overview..1 Identify the contract.2 Identify performance obligations..6 Determine transaction price 9 Allocate transaction price 12 Recognize revenue. 14 Principal

No. US2017-08 April 25, 2017 What s inside: Overview..1 Identify the contract.2 Identify performance obligations..6 Determine transaction price 9 Allocate transaction price 12 Recognize revenue. 14 Principal

Financial Controls Checklist

Financial Controls Checklist Board of Health: Board of Health for the Leeds, Grenville & Lanark District Health Unit Period ended: Dec. 31/17 Objective: The objective of the Financial Controls Checklist

Financial Controls Checklist Board of Health: Board of Health for the Leeds, Grenville & Lanark District Health Unit Period ended: Dec. 31/17 Objective: The objective of the Financial Controls Checklist

Due: Tuesday, May 1, 2007 by 5:45 p.m.

A439: Advance Auditing 2007 Final exam Directions: The final exam consists of 30 multiple choice questions. Ground Rules. As a take-home exam you may use notes, the internet, auditing textbooks or other

A439: Advance Auditing 2007 Final exam Directions: The final exam consists of 30 multiple choice questions. Ground Rules. As a take-home exam you may use notes, the internet, auditing textbooks or other

Chapter 2--Product Costing: Manufacturing Processes, Cost Terminology, and Cost Flows

Chapter 2--Product Costing: Manufacturing Processes, Cost Terminology, and Cost Flows Student: 1. Which of the following types of organizations is most likely to have a raw materials inventory account?

Chapter 2--Product Costing: Manufacturing Processes, Cost Terminology, and Cost Flows Student: 1. Which of the following types of organizations is most likely to have a raw materials inventory account?

Algorithmic Granite Bay Jet Ski, Incorporated

Algorithmic Granite Bay Jet Ski, Incorporated Level II 1 st Edition Transactions For June 3-9 Page 1 BEGIN THE PROGRAM AND ENTER THE DATA When you have: (1) Carefully read the introduction pages of this

Algorithmic Granite Bay Jet Ski, Incorporated Level II 1 st Edition Transactions For June 3-9 Page 1 BEGIN THE PROGRAM AND ENTER THE DATA When you have: (1) Carefully read the introduction pages of this

IAB LEVEL 2 AWARD IN COMPUTERISED BOOKKEEPING (QCF)

") IAB LEVEL 2 AWARD IN COMPUTERISED BOOKKEEPING (QCF) CONTENTS Qualification Accreditation Number 500/9261/3 (Accreditation review date 31 st December 2016) QUALIFICATION SPECIFICATION 1. Introduction 2.

IAB LEVEL 2 AWARD IN COMPUTERISED BOOKKEEPING (QCF) CONTENTS Qualification Accreditation Number 500/9261/3 (Accreditation review date 31 st December 2016) QUALIFICATION SPECIFICATION 1. Introduction 2.

Order Entry User Manual

Order Entry User Manual Confidential Information This document contains proprietary and valuable, confidential trade secret information of APPX Software, Inc., Richmond, Virginia Notice of Authorship This

Order Entry User Manual Confidential Information This document contains proprietary and valuable, confidential trade secret information of APPX Software, Inc., Richmond, Virginia Notice of Authorship This