High Performance Non Interest Income. a High Performance Briefing by Resurgent Performance

|

|

|

- Joanna Short

- 5 years ago

- Views:

Transcription

1 High Performance Non Interest Income a High Performance Briefing by

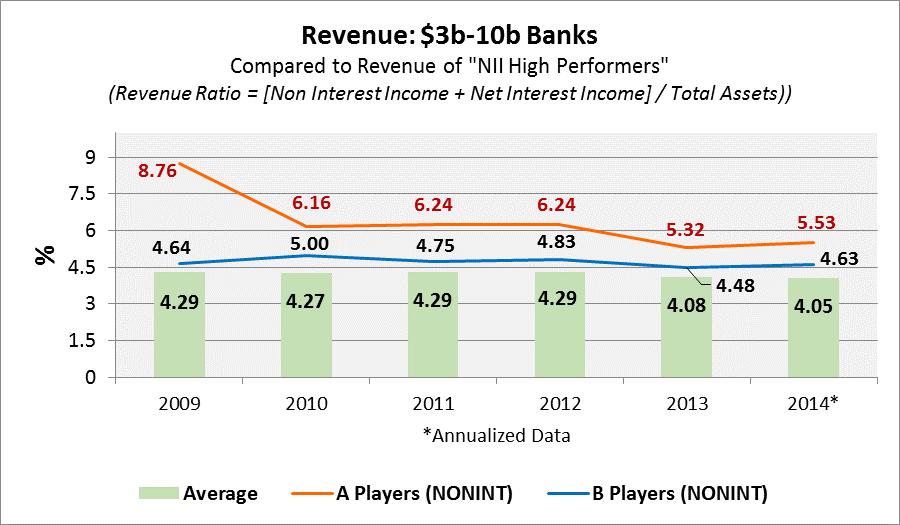

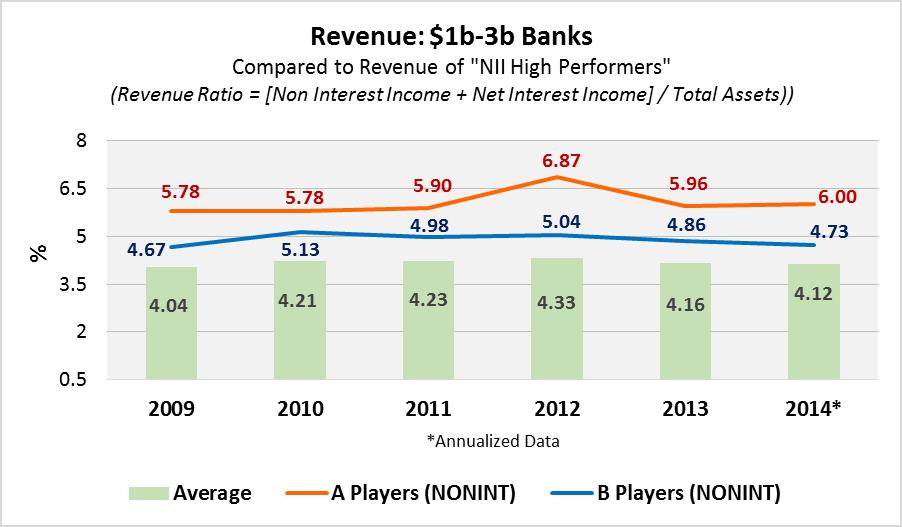

2 High Performance Non Interest Income Non Interest Income (NII) has been an elusive metric for many years. Finding the secret formula that balances increased NII with customer acquisition has proven beyond taxing to bankers. Now, given the current challenges with loan growth, the need for enhanced NII is more pronounced than ever before. The community banking industry continues to seek an answer to the (literal) million dollar question, What combination of services and fees will land banks with the highest shareholder return and the happiest customers? Banking is a service business, and true quality is worth a price. The marketing shift to FREE only temporarily answered this question. Banks notoriously marketed many of their services, such as checking, as fee-free for the exchange of increased overdraft charges. New regulations have greatly hindered this strategy, however, and counting on overdrafts to largely boost NII has proven unsustainable in the new, and ever-changing, industry. Because of decreased fee income driven by regulatory changes and higher expenses, the typical free checking account currently loses over $150 every year. At the same time, constantly evolving, customer-driven technology has put expenses on the rise. Unfortunately, these costly new apps and electronic tools are not being adequately subsidized by increased fee income. As an example, many banks are still not sufficiently charging for remote deposit scanners. The imbalance between technology output and fee income certainly makes revenue growth difficult. In 2015 evaluating service offerings and related fees should be a top initiative for most community banks, as the average and underperforming banks undoubtedly need increased NII in order to survive and grow. A change in thinking, strategy, and marketing, is imperative for these banks to reach High Performance. In order to help banks plan and strategize, we have analyzed current and historical Non Interest Income data, mapped it against other metrics, and defined and studied the Resurgent Performance Non Interest Income High Performers. The Modified Universe of Banks As with all of our other High Performance briefings, we used the RPI modified universe to determine our data set. First, we divided banks with assets between $50 million and $10 billion into four asset bands. To eliminate extremes that could skew data, we removed all banks that were in the top or bottom 3% on any of the six metrics included in our study: Non Interest Income Non Interest Expense Net Interest Margin Return on Assets Return on Equity Efficiency Ratio For comparative purposes, we standardized our NII data by calculating a ratio for all banks included in the data set: [Non Interest Income / Total Assets]. We then defined our NII High Performers as banks that rank in the top 20 percentile for their respective asset band. 2

3 It is our philosophy that metric analyses and competitor comparisons are an essential aid in continuous improvement and should always be a high priority on executives task lists. High Performance is further broken down into two groups: A Players, or those who score in the th percentile, and B players, or those who score in the 80-89th percentile. Those banks that are below the line of High Performance should aim for the respectable, and achievable, B Player status in order to increase revenue and attain organic growth. High Performance Illustrated Comparing the NII High Performers to the average performers, not only on NII but on all key metrics, allows us to identify important correlations and determine trends in asset size performance. In previous papers we have found that true High Performance on one critical metric frequently lends itself to High Performance across the board to 2014 Non Interest Income Each asset band graph shows that the relative High Performers consistently, and significantly, outperformed their average counterparts, and the disparity only increases with asset size. This size-dependent disparity is not surprising, as larger community banks typically have more sophisticated, automated systems that allow them to better realize and control broader fee income. In addition, larger organizations have more profitable wealth management and insurance offerings, which drive greater fees. Overall, however, the $1 billion to $3 billion dollar banks historically prove to be doing the best job at balancing their product offerings with expenses. The High Performance trend lines show NII to be on the decline following a spike in 2012, which was primarily related to exceptional mortgage fee income. As discussed earlier, more stringent regulations, which are not being balanced with new sources of fee income, is likely the culprit for the decline. 3

4 4

5 2009 to 2014 Overall Revenue The $3 billion to $10 billion dollar banks reported the highest asset proportional revenue numbers over the last five years. However, these banks, along with the $1 billion to $3 billion dollar banks, have also experienced the most pronounced drop in revenue since The smaller banks, on the other hand, have better maintained their total revenue. This trend indicates that the True Local Community banks are producing more relative interest income, given that the larger banks have consistently outperformed them on NII. 5

6 6

7 2014 Non Interest Income In line with the five year history, the $1 billion to $3 billion dollar banks show the best NII performance for the first three quarters of 2014, with the $3 billion to $10 billion banks not far behind. The larger banks continue to have a more significant gap between their high and average performers compared to the smaller banks. This illustrates the fact that asset size does matter due to the operating leverage it affords the bank Non Interest Expense The highest performers on NII are also spending more money, as the Non Interest Expense graph illustrates. The reality is that various lines of business can be people-intensive and simultaneously less capital intensive. However, the net payoff from strategically chosen services can, of course, be significantly greater than revenue from net interest margin alone. 7

8 2014 Return on Assets The obvious correlation between higher fee income generation and Return on Assets is true across all segments. Furthermore, we believe this correlation will become even more pronounced as the industry becomes increasingly more dependent on NII Return on Equity Return on Equity (ROE) is unsurprisingly comparable to the Return on Assets trends. While the difference is slight, the NII High Performers are consistently reporting higher ROE compared to the average performers. Given the array of services that are not capital dependent, we expect top NII banks to produce above historical average ROE results to a greater extent in 2015 than in prior years. 8

9 2014 Efficiency Ratio Interestingly enough, NII High Performers are outperformed by the average banks on Efficiency. This is partially due to the fact that in 2014 mortgage banking was especially challenging relative to net profitability. Among other factors impacting 2014 performance, many banks made investments/expenditures into increased lending capabilities. Some of these investments will produce benefits in The 2014 Efficiency of NII High Performers will not be sustained; increased application of technology will absolutely drive higher levels of productivity and more opportunities for fee income. Furthermore, as the industry hastens its pace of consolidation, we will see even greater efficiency levels in the magnitude of 10% to 20% improvement. 9

10 Determining where your bank currently stands is an essential part of the improvement process. In order to define a path to High Performance, you must take a critical look at your bank s products, pricing, markets, policies, and procedures. Your bank is in the position to provide the answers and cross-sell in the process. The Play Book First Things First: Optimize Your Current Fees Are your bank s current fee structures and service levels in line with your High Performing competition? Is your bank realizing all potential service fee income? Does your bank have clearly defined NII targets and goals? Is acceptable branch performance partly based on Non Interest Income goals? Do employees understand the importance of fee income? Are your service features and product offerings specifically aligned to your customers needs? If you can t solidly answer these questions with yes, it s time to engage in a Non Interest Income study. Realizing current fee potential could produce huge gains, and potentially even High Performance status. From our experience, the incremental lift will be in the range of 7 to 18 basis points on assets on average. For some banks, the lift will be much higher. The study can be bank-led, or outside advisory can be hired to assist with research, evaluation, and implementation. Either way, the study will work to do the following: Evaluate real improvement opportunity for revenue and service levels Set fee realization targets by product, lines of business, and / or position Create reporting tools for effective short-term growth and long-term continuous improvement Determine whether NII product-related technology is being used to its fullest capacity Evaluate product systems set ups for revenue leakage Create and distribute a clear and concise fee exception policy Link fee income to compensation and performance reviews Make Non Interest Income an integral part of all scorecards Align the depth and breadth of offerings with customer profiles Be The Trusted Advisor Wealth management is no longer solely for older adults and the affluent. There are ways to profitably extend money managing services to all clientele. The industry is shifting to a model where Wealth Consultants and Trusted Advisors are replacing transactional bankers, and customers can now largely take care of their transactions on their phone, computer, or ATM. In fact, younger customers prefer to do so. Consequently, when they do take the time to enter the bank, they are looking for something more. Clearly convenience and expert advice are part of the new solution needed. Simply put, customers and business owners want applicable money advice. They want to know how to save, how to invest, what to invest in, how to pay off debt, when to take out a loan, how to save for college, and even the basics of setting up a budget. Of course, your niche markets will determine what kind of advisory services you offer. If you serve the under-banked, perhaps your bank should offer one-on-one budget creation help. Or, if you serve a college town, consider offering classes regarding paying off student debt. Retirement savings workshops would of course be useful to a middle-aged client base. Small to mid size business owners also have specialized needs. Figure out what your customers want to know and give them the answers; become their Trusted Advisor. 10

11 While the margin may be small, workshops, classes, and consulting-like services can be a pathway to gaining customers and selling related services. If they trust you, they will bank with you, and there s no better way of gaining trust than providing helpful, specialized advice. What s Trending in 2015? Innovative Fees As technology continues to evolve, and customer profiles and demands continue to change, banks have an opportunity to be truly innovative, and differentiate themselves, with their service offerings. Peer to Peer Transactional Payment Service Customers want the ability to instantly transfer money to their college kids, best friends, church, Girl Scout Troop, and more. Small businesses also seek out payment solutions. Phone Application, Website, and ATM Advertisements There s money in selling electronic advertising space, and it s a great way to offset free services and marginally profitable business lines provided to the customer Debit and Credit Card Personalization Personalization, especially with younger adults, is very popular. Your bank can certainly capitalize on this trend by letting customers adorn their banking card with their initials, favorite sports team, or pictures of their kids. There is no magic bullet. The key is tailoring your services to your bank customers specific needs and executing them with superior service. Partnering with Local Businesses Similar to the ever-popular Groupon and Scoutmob, offering customers exclusive local dining and shopping deals via your bank s phone application is a novel idea. Customers win with deals, businesses win with increased traffic, and the bank wins with advertisement fees. Creative, uncommon, and non-conventional service offerings will work to increase income, satisfy customers, and serve as fantastic marketing tools. Put Someone in Charge Banks should consider implementing an in-bank committee in charge of service and fee income innovation. Outside of brainstorming creative and market-relevant offerings, the team can dually serve to define and track NII goals. That committee head should be a new officer primarily tasked with building non interest income. When it s someone s job, the job gets done. The Prescription Simply stated, a deep and thorough analysis of your bank s current NII practices and related service levels are critically important to your bank s long term survival and share value growth. Peak performance requires understanding, and persistently tracking, your competitors services and fees. It requires listening to your customers to determine what they want from their bank s Trusted Advisors. It requires truly exceptional, and regularly measured, customer service. It requires thoughtful innovation and a fresh mindset. While it may not be quick, or pain free, the pay off and long term gains will be significant. The industry is changing, and to keep up, your bank must change too. Forget your old practices, forget your old philosophies, and steer clear of operating under the, This is the way it s always be done attitude. Start 2015 with renewed perspective and the motivation to be, and deliver, more than the average bank. Your customers, and shareholders, will thank you. 11

U.S. COMMUNITY BANK RESULTS. Creating a New Level of Bank Service for Community Bank Customers U.S. COMMUNITY BANKS 1

U.S. COMMUNITY BANK RESULTS Creating a New Level of Bank Service for Community Bank Customers U.S. COMMUNITY BANKS 1 CREATING A NEW LEVEL OF SERVICE FOR U.S. COMMUNITY BANK CUSTOMERS Welcome to the third

U.S. COMMUNITY BANK RESULTS Creating a New Level of Bank Service for Community Bank Customers U.S. COMMUNITY BANKS 1 CREATING A NEW LEVEL OF SERVICE FOR U.S. COMMUNITY BANK CUSTOMERS Welcome to the third

Financial Services: Maximize Revenue with Better Marketing Data. Marketing Data Solutions for the Financial Services Industry

Financial Services: Maximize Revenue with Better Marketing Data Marketing Data Solutions for the Financial Services Industry DataMentors, LLC April 2014 1 Financial Services: Maximize Revenue with Better

Financial Services: Maximize Revenue with Better Marketing Data Marketing Data Solutions for the Financial Services Industry DataMentors, LLC April 2014 1 Financial Services: Maximize Revenue with Better

Marketing Data Solutions for the Financial Services Industry

Marketing Data Solutions for the Financial Services Industry Maximize your revenue with better data. Publication Date: July, 2015 www.datamentors.com info@datamentors.com 01. Maximize Revenue with Better

Marketing Data Solutions for the Financial Services Industry Maximize your revenue with better data. Publication Date: July, 2015 www.datamentors.com info@datamentors.com 01. Maximize Revenue with Better

How Banks Can Generate More Revenue and Profit by Enabling Customer Centricity

executive brief How Banks Can Generate More Revenue and Profit by Enabling Customer Centricity Customer centricity is not a new concept. For the past 15 years, banks have been talking about overcoming

executive brief How Banks Can Generate More Revenue and Profit by Enabling Customer Centricity Customer centricity is not a new concept. For the past 15 years, banks have been talking about overcoming

Measuring for Success: Redirect Your KPI s

Measuring for Success: Redirect Your KPI s CUNA Technology Council David Potterton, Research Director September, 2014 Changing Banking Models Hitting the Mainstream My own mother even pays bills on her

Measuring for Success: Redirect Your KPI s CUNA Technology Council David Potterton, Research Director September, 2014 Changing Banking Models Hitting the Mainstream My own mother even pays bills on her

Benefits of Investing in Digital Onboarding for Small-Business Banking

Benefits of Investing in Digital Onboarding for Small-Business Banking OCTOBER 2017 Prepared for: 2017 Avoka. All rights reserved. Reproduction of this white paper by any means is strictly prohibited.

Benefits of Investing in Digital Onboarding for Small-Business Banking OCTOBER 2017 Prepared for: 2017 Avoka. All rights reserved. Reproduction of this white paper by any means is strictly prohibited.

WINNING THE BATTLE FOR TALENT IN BANKING. Current and Future Recruiting Strategies for Community Banks

WINNING THE BATTLE FOR TALENT IN BANKING Current and Future Recruiting Strategies for Community Banks BANKING ON THE RIGHT TALENT CORE Recruiting Practices for Community Banks A Note from JR Llewellyn,

WINNING THE BATTLE FOR TALENT IN BANKING Current and Future Recruiting Strategies for Community Banks BANKING ON THE RIGHT TALENT CORE Recruiting Practices for Community Banks A Note from JR Llewellyn,

DIGITALIZATION IS NOT GOING DIGITAL THE CHALLENGE FOR RETAIL BANKS

DIGITALIZATION IS NOT GOING DIGITAL THE CHALLENGE FOR RETAIL BANKS FINANCIAL FORUM INNOVATIONS Sofia June 2016 1 TWO TRENDS ARE CONVERGING WHICH PRESENT BANKS WITH BOTH CHALLENGE AND OPPORTUNITY 1? Banks

DIGITALIZATION IS NOT GOING DIGITAL THE CHALLENGE FOR RETAIL BANKS FINANCIAL FORUM INNOVATIONS Sofia June 2016 1 TWO TRENDS ARE CONVERGING WHICH PRESENT BANKS WITH BOTH CHALLENGE AND OPPORTUNITY 1? Banks

Retail Banking Insights

Retail Banking Insights Number 6 March 2015 Driving Revenue Growth In Retail Banking Annual revenue growth for U.S. retail banks has hovered near 2 percent since 2010, hindered by historically low interest

Retail Banking Insights Number 6 March 2015 Driving Revenue Growth In Retail Banking Annual revenue growth for U.S. retail banks has hovered near 2 percent since 2010, hindered by historically low interest

Banking on gender differences? Similarities and differences in financial services preferences of women and men in a digital world

Banking on gender differences? Similarities and differences in financial services preferences of women and men in a digital world are embracing mobile financial services at higher rates. Banking on gender

Banking on gender differences? Similarities and differences in financial services preferences of women and men in a digital world are embracing mobile financial services at higher rates. Banking on gender

Lecture Materials BANK MARKETING. Lance Kessler President Lance Kessler & Associates Mechanicsburg, Pennsylvania

Lecture Materials BANK MARKETING Lance Kessler President Lance Kessler & Associates Mechanicsburg, Pennsylvania lekessler@aol.com 717-766-1005 August 2, 2016 Graduate School of Banking at the University

Lecture Materials BANK MARKETING Lance Kessler President Lance Kessler & Associates Mechanicsburg, Pennsylvania lekessler@aol.com 717-766-1005 August 2, 2016 Graduate School of Banking at the University

Sydbank s Business Model 2017

2017 1 Summary As a nationwide advisory bank, Sydbank has a significant presence in all parts of Denmark as well as in Northern Germany. Sydbank is a bank for most people but not the same bank for everyone.

2017 1 Summary As a nationwide advisory bank, Sydbank has a significant presence in all parts of Denmark as well as in Northern Germany. Sydbank is a bank for most people but not the same bank for everyone.

PREVIEW OF Mobile Banking, Mobile Payments

Accurate Financial Data Since 1989 PREVIEW OF Mobile Banking, Mobile Payments What Consumers Value 2015 RateWatch Sales and Service: 1.800.348.1831 www.rate-watch.com Contents Introduction...4 1. Which

Accurate Financial Data Since 1989 PREVIEW OF Mobile Banking, Mobile Payments What Consumers Value 2015 RateWatch Sales and Service: 1.800.348.1831 www.rate-watch.com Contents Introduction...4 1. Which

The Future of Banking Transformation to a new norm CCG Catalyst Consulting Group

The Future of Banking Transformation to a new norm CONFIDENTIALITY STATEMENT This document and its contents are confidential and the exclusive property of CCG Catalyst, LLC d.b.a. CCG Catalyst Consulting

The Future of Banking Transformation to a new norm CONFIDENTIALITY STATEMENT This document and its contents are confidential and the exclusive property of CCG Catalyst, LLC d.b.a. CCG Catalyst Consulting

BECOMING A VIRTUAL FD

PAGE 1 BECOMING A VIRTUAL FD The idea of helping your clients remotely or virtually has been around for some time. Advances in mobile technology have made the concept of a Virtual Finance Director (FD)

PAGE 1 BECOMING A VIRTUAL FD The idea of helping your clients remotely or virtually has been around for some time. Advances in mobile technology have made the concept of a Virtual Finance Director (FD)

BUSINESS INTELLIGENCE: IT S TIME TO TAKE PRIVATE EQUITY TO THE NEXT LEVEL

BUSINESS INTELLIGENCE: IT S TIME TO TAKE PRIVATE EQUITY TO THE NEXT LEVEL BUSINESS CONSULTANTS DEEP TECHNOLOGISTS In a challenging economic environment, portfolio management has taken on greater importance.

BUSINESS INTELLIGENCE: IT S TIME TO TAKE PRIVATE EQUITY TO THE NEXT LEVEL BUSINESS CONSULTANTS DEEP TECHNOLOGISTS In a challenging economic environment, portfolio management has taken on greater importance.

Panther Digital Marketing Reasons Why Businesses are Hiring Digital Marketing Consultants in 2018

15 Reasons why businesses are hiring Digital Marketing 1. Poor Sales Sales numbers for your business are stagnant or below expectations and you re receiving very few or no leads coming through your website.

15 Reasons why businesses are hiring Digital Marketing 1. Poor Sales Sales numbers for your business are stagnant or below expectations and you re receiving very few or no leads coming through your website.

About LPL Financial. Serving financial professionals and their clients for four decades

About LPL Financial Serving financial professionals and their clients for four decades About LPL Financial LPL Financial is the nation s largest independent broker-dealer*, a top RIA custodian, and a leading

About LPL Financial Serving financial professionals and their clients for four decades About LPL Financial LPL Financial is the nation s largest independent broker-dealer*, a top RIA custodian, and a leading

Rethink and Reset. Grow Revenue and Customer Loyalty Revenue Expansion Program

Rethink and Reset Grow Revenue and Customer Loyalty Revenue Expansion Program Fiserv can help you generate incremental annual revenue of up to $4 million for every $1 billion dollars asset size more than

Rethink and Reset Grow Revenue and Customer Loyalty Revenue Expansion Program Fiserv can help you generate incremental annual revenue of up to $4 million for every $1 billion dollars asset size more than

Create Opportunities to Meet the Financial Needs of Your Bank Customers

Create Opportunities to Meet the Financial Needs of Your Bank Customers E. LOYD POHL, CEO POHL CONSULTING AND TRAINING WWW.POHLCONSULTING.COM INFO@POHLCONSULTING.COM 1 If a customer has a need but "If

Create Opportunities to Meet the Financial Needs of Your Bank Customers E. LOYD POHL, CEO POHL CONSULTING AND TRAINING WWW.POHLCONSULTING.COM INFO@POHLCONSULTING.COM 1 If a customer has a need but "If

Product and Pricing Engines (PPE): Strategic Uses for Compliance, Competitiveness and Profit

: Strategic Uses for Compliance, Competitiveness and Profit") Strategic pricing tools improve success with prospects and create financial benefit for the firm. Once Considered a More Efficient Substitute for a Rate Sheet Pricing Engines are Evolving to be the Compliance

Strategic pricing tools improve success with prospects and create financial benefit for the firm. Once Considered a More Efficient Substitute for a Rate Sheet Pricing Engines are Evolving to be the Compliance

Questions and Answers with Key Executives from Akcelerant and Temenos

Questions and Answers with Key Executives from Akcelerant and Hear what the CEOs are saying... G.A. (Jay) Mossman III Founder & CEO David Arnott Chief Executive Officer Why is this event significant and

Questions and Answers with Key Executives from Akcelerant and Hear what the CEOs are saying... G.A. (Jay) Mossman III Founder & CEO David Arnott Chief Executive Officer Why is this event significant and

EXPECT MORE WESTFIELD BANK 2017 ANNUAL REPORT

EXPECT MORE WESTFIELD BANK 2017 ANNUAL REPORT 2 EXPECT MORE FROM WESTFIELD BANK NEW AND EXCITING POSSIBILITIES FOR THE FUTURE ARE EMERGING FROM THE FOUNDATION OF WHAT CAME BEFORE. At Westfield Bank, we

EXPECT MORE WESTFIELD BANK 2017 ANNUAL REPORT 2 EXPECT MORE FROM WESTFIELD BANK NEW AND EXCITING POSSIBILITIES FOR THE FUTURE ARE EMERGING FROM THE FOUNDATION OF WHAT CAME BEFORE. At Westfield Bank, we

How Will Your Bank Thrive?

How Will Your Bank Thrive? Pennsylvania Association of Community Bankers Annual Convention September 24, 2016 Timothy Reimink Managing Director Crowe Horwath LLP Session Description Some people wonder

How Will Your Bank Thrive? Pennsylvania Association of Community Bankers Annual Convention September 24, 2016 Timothy Reimink Managing Director Crowe Horwath LLP Session Description Some people wonder

Management Science Introduction

Management Science Introduction Strategy is the intersection of a desired future state and the action(s) designed to achieve that desired state. The success of any Strategy is dependent upon relevant experience,

Management Science Introduction Strategy is the intersection of a desired future state and the action(s) designed to achieve that desired state. The success of any Strategy is dependent upon relevant experience,

How to become a CLTV aligned organization?

Abstract The significance of Customer Lifetime Value (CLTV) is now being increasingly acknowledged among the decision makers around the world. However, only a few actually take the plunge and implement

Abstract The significance of Customer Lifetime Value (CLTV) is now being increasingly acknowledged among the decision makers around the world. However, only a few actually take the plunge and implement

BANK SATISFACTION BAROMETER (BSB)

") REPORT 2017 BANK SATISFACTION BAROMETER (BSB) 1 CONTENTS BANK SATISFACTION BAROMETER 2017 INTRODUCTION 3 BANK SATISFACTION BAROMETER 4 1 THE TRADITIONAL BANK VALUE PROPOSITION IS CHANGING 8 2 PRODUCT AND

REPORT 2017 BANK SATISFACTION BAROMETER (BSB) 1 CONTENTS BANK SATISFACTION BAROMETER 2017 INTRODUCTION 3 BANK SATISFACTION BAROMETER 4 1 THE TRADITIONAL BANK VALUE PROPOSITION IS CHANGING 8 2 PRODUCT AND

Business Pulse. Exploring dual perspectives on the top 10 risks and opportunities in 2013 and beyond. The COO perspective

Business Pulse Exploring dual perspectives on the top 10 risks and opportunities in 2013 and beyond The COO perspective The COO perspective at a glance Your time is precious. In order to get you the insights

Business Pulse Exploring dual perspectives on the top 10 risks and opportunities in 2013 and beyond The COO perspective The COO perspective at a glance Your time is precious. In order to get you the insights

ADVANTAGES OF REVENUE MANAGEMENT TECHNOLOGY

12 ADVANTAGES OF REVENUE MANAGEMENT TECHNOLOGY By IDeaS Revenue Solutions www.ideas.com Hotels invest big in their revenue management software. These significant investments mean it s extremely important

12 ADVANTAGES OF REVENUE MANAGEMENT TECHNOLOGY By IDeaS Revenue Solutions www.ideas.com Hotels invest big in their revenue management software. These significant investments mean it s extremely important

FROM OWNING TO EXITING IN A FAMILY OWNED BUSINESS

FROM OWNING TO EXITING MANAGING THE RISKS OF TRANSITION IN A FAMILY OWNED BUSINESS 1 TABLE OF CONTENTS INTRODUCTION... 2 CREATING A SUCCESSION-DRIVEN STRATEGIC PLAN... 3 CREATING AN ALIGNED SUCCESSION

FROM OWNING TO EXITING MANAGING THE RISKS OF TRANSITION IN A FAMILY OWNED BUSINESS 1 TABLE OF CONTENTS INTRODUCTION... 2 CREATING A SUCCESSION-DRIVEN STRATEGIC PLAN... 3 CREATING AN ALIGNED SUCCESSION

16 SECRETS TO INCREASE BUSINESS CASH FLOW

16 SECRETS TO INCREASE BUSINESS CASH FLOW SUMMARY Eight out of 10 businesses fail within the first 18 months, and 96 percent of businesses fail within ten years. A company may have all the revenue in the

16 SECRETS TO INCREASE BUSINESS CASH FLOW SUMMARY Eight out of 10 businesses fail within the first 18 months, and 96 percent of businesses fail within ten years. A company may have all the revenue in the

Cisco Remote Expert Smart Solution for Retail Banking Enabling Personalized and Pervasive Sales and Service Across Delivery Channels

Solution Overview Cisco Remote Expert Smart Solution for Retail Banking Enabling Personalized and Pervasive Sales and Service Across Delivery Channels For too long, the financial services industry has

Solution Overview Cisco Remote Expert Smart Solution for Retail Banking Enabling Personalized and Pervasive Sales and Service Across Delivery Channels For too long, the financial services industry has

Healthcare Expertise for Your Business

Healthcare Expertise for Your Business The Premier Bank Serving Healthcare Businesses in Texas Texas Capital Bank specializes in serving the diverse and complex needs of the rapidly changing healthcare

Healthcare Expertise for Your Business The Premier Bank Serving Healthcare Businesses in Texas Texas Capital Bank specializes in serving the diverse and complex needs of the rapidly changing healthcare

It starts today. Chief Executive Officer s Message

It starts today Darryl White Chief Executive Officer BMO is on the move. Adapting. Innovating. Working hard to anticipate customers expectations and deliver value to shareholders. Always. Now it s year

It starts today Darryl White Chief Executive Officer BMO is on the move. Adapting. Innovating. Working hard to anticipate customers expectations and deliver value to shareholders. Always. Now it s year

TRANSITIONING YOUR BUSINESS WHAT YOU NEED TO KNOW

TRANSITIONING YOUR BUSINESS WHAT YOU NEED TO KNOW Thinking about transitioning your business undoubtedly raises questions and concerns. You ve likely considered factors such as payouts, technology solutions,

TRANSITIONING YOUR BUSINESS WHAT YOU NEED TO KNOW Thinking about transitioning your business undoubtedly raises questions and concerns. You ve likely considered factors such as payouts, technology solutions,

CLAconnect.com/creditunions. Impact the Future of Credit Unions

CLAconnect.com/creditunions Impact the Future of Credit Unions We Believe Enabling your success means a better world for all of us, but now, more than ever, a greater number of operational, regulatory,

CLAconnect.com/creditunions Impact the Future of Credit Unions We Believe Enabling your success means a better world for all of us, but now, more than ever, a greater number of operational, regulatory,

T H E FUTURE O F MONEY R E P O R T

T H E FUTURE O F MONEY R E P O R T K O S K I R E S E A R C H LILAH KOSKI WWW.KOSKIRESEARCH.COM KOSKI RESEARCH 2018. ALL RIGHTS RESERVED. T H E F U T U R E O F M O N E Y I N S I G H T S T O I M P R O V

T H E FUTURE O F MONEY R E P O R T K O S K I R E S E A R C H LILAH KOSKI WWW.KOSKIRESEARCH.COM KOSKI RESEARCH 2018. ALL RIGHTS RESERVED. T H E F U T U R E O F M O N E Y I N S I G H T S T O I M P R O V

THE LPL INDEPENDENT ADVISOR INSTITUTE TAKE THE NEXT STEP FOR YOUR FUTURE

1 THE LPL INDEPENDENT ADVISOR INSTITUTE TAKE THE NEXT STEP FOR YOUR FUTURE Make Your Mark on the World As you prepare for the next chapter of your professional journey, do you find yourself seeking more

1 THE LPL INDEPENDENT ADVISOR INSTITUTE TAKE THE NEXT STEP FOR YOUR FUTURE Make Your Mark on the World As you prepare for the next chapter of your professional journey, do you find yourself seeking more

THREE WAYS TO OPTIMIZE YOUR RESOURCES FOR GROWTH

THREE WAYS TO OPTIMIZE YOUR RESOURCES FOR GROWTH GROWTH. FROM THE INSIDE OUT. As much as businesses are known to require capital to grow, it is not uncommon to find cost-cutting and product innovation

THREE WAYS TO OPTIMIZE YOUR RESOURCES FOR GROWTH GROWTH. FROM THE INSIDE OUT. As much as businesses are known to require capital to grow, it is not uncommon to find cost-cutting and product innovation

Starting Your Own Business

Brief 01.00 Last Revised: 08/2015 Prepared by: Greater Cincinnati and Dayton Chapters Starting Your Own Business Want to start your own business? Our best advice to you is "Be careful!" Why? Because more

Brief 01.00 Last Revised: 08/2015 Prepared by: Greater Cincinnati and Dayton Chapters Starting Your Own Business Want to start your own business? Our best advice to you is "Be careful!" Why? Because more

Customer Segmentation and Market Analytics FHLB Regional Member Meetings

Customer Segmentation and Market Analytics 2018 FHLB Regional Member Meetings 158 Route 206 Gladstone, NJ 07934 P: (908) 604-9336 F: (908) 604-5951 finpro@finpro.us www.finpro.us 0 The evolution of customer

Customer Segmentation and Market Analytics 2018 FHLB Regional Member Meetings 158 Route 206 Gladstone, NJ 07934 P: (908) 604-9336 F: (908) 604-5951 finpro@finpro.us www.finpro.us 0 The evolution of customer

Innovations in Small Dollar Payments 1

Innovations in Small Dollar Payments 1 Peter Burns Anne Stanley October 2001 Summary: On September 25, 2001, the Payment Cards Center of the Federal Reserve Bank of Philadelphia sponsored a workshop on

Innovations in Small Dollar Payments 1 Peter Burns Anne Stanley October 2001 Summary: On September 25, 2001, the Payment Cards Center of the Federal Reserve Bank of Philadelphia sponsored a workshop on

Bricks To Clicks. Agenda

1 Agenda 2 Agenda The evolution in branch banking Where are we heading? Taking advantage of these changes 3 Four Reasons For Changes In Banking Channels 1. Growing population and geographic shifts in population

1 Agenda 2 Agenda The evolution in branch banking Where are we heading? Taking advantage of these changes 3 Four Reasons For Changes In Banking Channels 1. Growing population and geographic shifts in population

What Lies Ahead. Mike Jacoutot, Founder & Managing Partner Butler Street February 3, 2015

What Lies Ahead Mike Jacoutot, Founder & Managing Partner Butler Street February 3, 2015 The Whirlwind Digital Darwinism When Charles Darwin presented his theory of evolution in 1859, he described a world

What Lies Ahead Mike Jacoutot, Founder & Managing Partner Butler Street February 3, 2015 The Whirlwind Digital Darwinism When Charles Darwin presented his theory of evolution in 1859, he described a world

INCREASING REVENUE GENERATION

INCREASING REVENUE GENERATION Drive maximum returns from your ATM investment. An NCR White Paper It s not a question of if, it s a question of when. As customer needs change and evolve, keeping pace with

INCREASING REVENUE GENERATION Drive maximum returns from your ATM investment. An NCR White Paper It s not a question of if, it s a question of when. As customer needs change and evolve, keeping pace with

Finding the Key to Sales Excellence: What Do High Performers Look Like?

Finding the Key to Sales Excellence: What Do High Performers Look Like? Nicholas T. Miller, President, Clarity Advantage Corporation Charles Wendel, President, Financial Institutions Consulting he value

Finding the Key to Sales Excellence: What Do High Performers Look Like? Nicholas T. Miller, President, Clarity Advantage Corporation Charles Wendel, President, Financial Institutions Consulting he value

Succession Planning for Solo and Small Firms and Rewards for Retiring Lawyers

Succession Planning for Solo and Small Firms and Rewards for Retiring Lawyers Presenters Arthur G. Greene Arthur G. Greene Consulting, Bedford, NH Chapter 2 - MSBA Page #2-1 Chapter 2 - MSBA Page #2-2

Succession Planning for Solo and Small Firms and Rewards for Retiring Lawyers Presenters Arthur G. Greene Arthur G. Greene Consulting, Bedford, NH Chapter 2 - MSBA Page #2-1 Chapter 2 - MSBA Page #2-2

WHY EMPLOYEE ENGAGEMENT MATTERS. Kathy Bowersox

WHY EMPLOYEE ENGAGEMENT MATTERS By Kathy Bowersox Are your employees engaged? Do you know if they are? Do you care? How relevant is employee engagement in terms of business success? In a word, VERY! If

WHY EMPLOYEE ENGAGEMENT MATTERS By Kathy Bowersox Are your employees engaged? Do you know if they are? Do you care? How relevant is employee engagement in terms of business success? In a word, VERY! If

Welcome to Today s Web Seminar SPONSOR BY CONTENT FROM

Welcome to Today s Web Seminar SPONSOR BY CONTENT FROM HOSTED BY Moderator: Michael Sisk Contributing Editor, American Banker Michael Sisk is a New York-based journalist who has covered business and the

Welcome to Today s Web Seminar SPONSOR BY CONTENT FROM HOSTED BY Moderator: Michael Sisk Contributing Editor, American Banker Michael Sisk is a New York-based journalist who has covered business and the

The Future Of Social Selling

A Forrester Consulting Thought Leadership Paper Commissioned By Hearsay Social Customer Life-Cycle Selling Requires A New Approach May 2013 Table Of Contents Executive Summary... 2 Current State/Concept

A Forrester Consulting Thought Leadership Paper Commissioned By Hearsay Social Customer Life-Cycle Selling Requires A New Approach May 2013 Table Of Contents Executive Summary... 2 Current State/Concept

Performance Management in Higher Education

Performance Management in Higher Education Advisory Services and Software Solutions That Enable Colleges and Universities to Succeed in a Changing Environment Given the number and magnitude of pressures

Performance Management in Higher Education Advisory Services and Software Solutions That Enable Colleges and Universities to Succeed in a Changing Environment Given the number and magnitude of pressures

Using Financial Services. Banking on the Go. Financial Literacy Theme. Using Financial Services. 21st Century Skill(s)

") UNIT 2 Using Financial Services Topic Using Mobile Banking LEARNING OBJECTIVE(S) Students will: explain common mobile banking features and uses. research and evaluate mobile banking services offered by

UNIT 2 Using Financial Services Topic Using Mobile Banking LEARNING OBJECTIVE(S) Students will: explain common mobile banking features and uses. research and evaluate mobile banking services offered by

Assessing the state of Web site functionality in the financial services industry fifth update

IBM Institute for Business Value Assessing the state of Web site functionality in the financial services industry fifth update It has been three years since the IBM Institute for Business Value began tracking

IBM Institute for Business Value Assessing the state of Web site functionality in the financial services industry fifth update It has been three years since the IBM Institute for Business Value began tracking

The Finance Digital Executive s Playbook for Adopting a Conversational Approach to Mobile Banking

The Finance Digital Executive s Playbook for Adopting a Conversational Approach to Mobile Banking Content DETERMINING YOUR MOBILE STRATEGY... 4 THE STATE OF ONLINE FINANCE... 4 THE BENEFITS OF A CONVERSATIONAL

The Finance Digital Executive s Playbook for Adopting a Conversational Approach to Mobile Banking Content DETERMINING YOUR MOBILE STRATEGY... 4 THE STATE OF ONLINE FINANCE... 4 THE BENEFITS OF A CONVERSATIONAL

Business Assessment. Advisor Tool Galliard, Inc. All Rights Reserved

+ Family Business Assessment Advisor Tool 2015 Galliard, Inc. All Rights Reserved + Purpose: To discuss and assess six major focus areas for familyowned and closely-held businesses. 2015 Galliard, Inc.

+ Family Business Assessment Advisor Tool 2015 Galliard, Inc. All Rights Reserved + Purpose: To discuss and assess six major focus areas for familyowned and closely-held businesses. 2015 Galliard, Inc.

Banking on Small-Business Needs Sponsored by:

Banking on Small-Business Needs Sponsored by: 2014 Yodlee. All rights reserved. Reproduction of this white paper by any means is strictly prohibited. EXECUTIVE SUMMARY Banking on Small-Business Needs,

Banking on Small-Business Needs Sponsored by: 2014 Yodlee. All rights reserved. Reproduction of this white paper by any means is strictly prohibited. EXECUTIVE SUMMARY Banking on Small-Business Needs,

EMERGING STRATEGIC INVESTMENT OPPORTUNITIES FOR SACCOS

EMERGING STRATEGIC INVESTMENT OPPORTUNITIES FOR SACCOS PRESENTATION BY DR. GAMALIEL HASSAN STIMA SACCO UGANDA COOPERATIVE SAVINGS AND CREDIT UNION LIMITED 2 ND NATIONAL ANNUAL SACCO CONFERENCE 28 TH AUGUST

EMERGING STRATEGIC INVESTMENT OPPORTUNITIES FOR SACCOS PRESENTATION BY DR. GAMALIEL HASSAN STIMA SACCO UGANDA COOPERATIVE SAVINGS AND CREDIT UNION LIMITED 2 ND NATIONAL ANNUAL SACCO CONFERENCE 28 TH AUGUST

Bringing patients into focus

Health Care Of special interest to Health care executives Insights for 5executives Bringing patients into focus Using analytics to create a 360-degree view The patient is again becoming the focus of the

Health Care Of special interest to Health care executives Insights for 5executives Bringing patients into focus Using analytics to create a 360-degree view The patient is again becoming the focus of the

Market leadership through Product Innovation

Market leadership through Product Innovation Temenos Investor Day 1. We have the best track record for innovation 2. We are extending our product leadership 3. Our evolving architecture opens new markets

Market leadership through Product Innovation Temenos Investor Day 1. We have the best track record for innovation 2. We are extending our product leadership 3. Our evolving architecture opens new markets

COGENT REPORTS. Agile Experienced. Powerful. Accurate. In 2018 we are changing the rules!

cogent-reports.com COGENT Agile Experienced Reliable Powerful Revolutionary Accurate Trusted Consultative REPORTS In 2018 we are changing the rules! Introducing new capabilities and offerings designed

cogent-reports.com COGENT Agile Experienced Reliable Powerful Revolutionary Accurate Trusted Consultative REPORTS In 2018 we are changing the rules! Introducing new capabilities and offerings designed

FOUR STEPS TO BECOMING FLUENT IN THE LANGUAGE OF PRICING

FOUR STEPS TO BECOMING FLUENT IN THE LANGUAGE OF PRICING By Sudipto Banerjee, Amadeus Petzke, Just Schürmann, Matt Beckett, and David Langkamp Pricing is a powerful language. Higher prices can signal different

FOUR STEPS TO BECOMING FLUENT IN THE LANGUAGE OF PRICING By Sudipto Banerjee, Amadeus Petzke, Just Schürmann, Matt Beckett, and David Langkamp Pricing is a powerful language. Higher prices can signal different

Achieving the Cross-Sell - Advanced Relationship Strategy. James T. Rager Vice-Chairman Personal & Commercial Banking Royal Bank of Canada

Achieving the Cross-Sell - Advanced Relationship Strategy James T. Rager Vice-Chairman Personal & Commercial Banking Royal Bank of Canada Nesbitt Burns Financial Services Conference (Please check against

Achieving the Cross-Sell - Advanced Relationship Strategy James T. Rager Vice-Chairman Personal & Commercial Banking Royal Bank of Canada Nesbitt Burns Financial Services Conference (Please check against

Zurich Financial Services & AMS. An evolving partnership. April Samulewicz. Mark Smith. Global Head of Talent Attraction & Recruitment CoE

Zurich Financial Services & AMS An evolving partnership April Samulewicz Global Head of Talent Attraction & Recruitment CoE Zurich Mark Smith Client Relationship Director Alexander Mann Solutions Alexander

Zurich Financial Services & AMS An evolving partnership April Samulewicz Global Head of Talent Attraction & Recruitment CoE Zurich Mark Smith Client Relationship Director Alexander Mann Solutions Alexander

GETTING QUALITY CASES WITH ONLINE MARKETING

2017 GUIDE TO GETTING QUALITY CASES WITH ONLINE MARKETING for Solo & Small Law Firms BY: WILL PALMER KANSAS & MISSOURI MARKETS TABLE OF CONTENTS Page 1. Why an Effective Online Strategy Can Grow Law Firm

2017 GUIDE TO GETTING QUALITY CASES WITH ONLINE MARKETING for Solo & Small Law Firms BY: WILL PALMER KANSAS & MISSOURI MARKETS TABLE OF CONTENTS Page 1. Why an Effective Online Strategy Can Grow Law Firm

How Financial Chatbots Are Transforming Digital Banking Produced by Abe

How Financial Chatbots Are Transforming Digital Banking Produced by Abe Abe builds conversational banking solutions for progressive community banks. CONTENTS Keeping Pace with Evolving Financial Technologies....3

How Financial Chatbots Are Transforming Digital Banking Produced by Abe Abe builds conversational banking solutions for progressive community banks. CONTENTS Keeping Pace with Evolving Financial Technologies....3

Commerzbank 4.0: simple digital efficient Winning in the German Retail Banking Market

: Winning in the German Retail Banking Market 10 May 2017 Commerzbank AG Michael Mandel Member of the Board of Managing Directors London Achieving profitable growth and gaining market share Customers (GER*;

: Winning in the German Retail Banking Market 10 May 2017 Commerzbank AG Michael Mandel Member of the Board of Managing Directors London Achieving profitable growth and gaining market share Customers (GER*;

Presented By: Jack R. Salvetti, Principal S.R. Snodgrass, P.C.

Presented By: Jack R. Salvetti, Principal S.R. Snodgrass, P.C. 2018 S.R. Snodgrass, P.C. All Rights Reserved 2 3 Number of Commercial Banks (2000 2017) 9,000 8,500 8,315 8,082 8,000 7,500 7,887 7,767 7,628

Presented By: Jack R. Salvetti, Principal S.R. Snodgrass, P.C. 2018 S.R. Snodgrass, P.C. All Rights Reserved 2 3 Number of Commercial Banks (2000 2017) 9,000 8,500 8,315 8,082 8,000 7,500 7,887 7,767 7,628

WHITE PAPER Funding Speech Analytics 101: A Guide to Funding Speech Analytics and Leveraging Insights Gained to Improve ROI

s WHITE PAPER Funding Speech Analytics 101: A Guide to Funding Speech Analytics and Leveraging Insights Gained to Improve ROI 1-800-639-1700 mycallfinder.com A Guide to Funding Speech Analytics and Leveraging

s WHITE PAPER Funding Speech Analytics 101: A Guide to Funding Speech Analytics and Leveraging Insights Gained to Improve ROI 1-800-639-1700 mycallfinder.com A Guide to Funding Speech Analytics and Leveraging

Predictive Customer Interaction Management

Predictive Customer Interaction Management An architecture that enables organizations to leverage real-time events to accurately target products and services. Don t call us. We ll call you. That s what

Predictive Customer Interaction Management An architecture that enables organizations to leverage real-time events to accurately target products and services. Don t call us. We ll call you. That s what

WHITEPAPER. Unlocking Your ATM Big Data : Understanding the power of real-time transaction monitoring and analytics.

Unlocking Your ATM Big Data : Understanding the power of real-time transaction monitoring and analytics www.inetco.com Summary Financial organizations are heavily investing in self-service and omnichannel

Unlocking Your ATM Big Data : Understanding the power of real-time transaction monitoring and analytics www.inetco.com Summary Financial organizations are heavily investing in self-service and omnichannel

ELEVATE YOU. your career. TOMORROW. See where. takes

ELEVATE your career. TOMORROW See where takes YOU. SMALL FIRM ATTENTION. WITH THE COMPLETE FINANCIAL WORLD AT YOUR FINGERTIPS. Life as a financial professional holds incredible opportunities for career

ELEVATE your career. TOMORROW See where takes YOU. SMALL FIRM ATTENTION. WITH THE COMPLETE FINANCIAL WORLD AT YOUR FINGERTIPS. Life as a financial professional holds incredible opportunities for career

How cashless payments will reshape commerce in Asia

Nuttawut Atiratana, Tanai Khiaonarong, Sayan Pariwat Bank of {NuttawuA, TanaiK, SayanP}@bot.or.th Abstract How cashless payments will reshape commerce in Asia is an important issue, not just for Asian

Nuttawut Atiratana, Tanai Khiaonarong, Sayan Pariwat Bank of {NuttawuA, TanaiK, SayanP}@bot.or.th Abstract How cashless payments will reshape commerce in Asia is an important issue, not just for Asian

Webtrends for Banking. Give your customers cross-channel experiences that are relevant, personal and valuable. Solution Overview

Webtrends for Banking Give your customers cross-channel experiences that are relevant, personal and valuable. Solution Overview Webtrends 2014 Webtrends, Inc. All Rights Reserved Solution Overview Webtrends

Webtrends for Banking Give your customers cross-channel experiences that are relevant, personal and valuable. Solution Overview Webtrends 2014 Webtrends, Inc. All Rights Reserved Solution Overview Webtrends

Social Media Profit Guide

The Ultimate Guide to Converting Likes to Profits Social Media Profit Guide...because you can t take likes to the bank SECTION 1 Make Money on Social Media You can t take likes to the bank. They might

The Ultimate Guide to Converting Likes to Profits Social Media Profit Guide...because you can t take likes to the bank SECTION 1 Make Money on Social Media You can t take likes to the bank. They might

AUSTRALIA SUMMER INTERN PROGRAM STREAMS

AUSTRALIA SUMMER INTERN PROGRAM STREAMS Explore your options in Australia Before you apply for the ANZ Australia Summer Intern Program, you ll need to work out what part of our business best suits your

AUSTRALIA SUMMER INTERN PROGRAM STREAMS Explore your options in Australia Before you apply for the ANZ Australia Summer Intern Program, you ll need to work out what part of our business best suits your

Achieving high performance in the chemical industry. Strategies for a new era

Achieving high performance in the chemical industry Strategies for a new era Strategies for a new era Myriad challenges shape the chemical industry agenda: Chemical company executives navigate through

Achieving high performance in the chemical industry Strategies for a new era Strategies for a new era Myriad challenges shape the chemical industry agenda: Chemical company executives navigate through

To tweet or not to tweet. Investing in social media for wealth managers

To tweet or not to tweet Investing in social media for wealth managers Other papers in this series: Advice goes virtual April 2015 It got so late so soon: Wealth and asset managers awake to the new digital

To tweet or not to tweet Investing in social media for wealth managers Other papers in this series: Advice goes virtual April 2015 It got so late so soon: Wealth and asset managers awake to the new digital

Let s embrace tomorrow, Today. Empowering solutions for your business

Let s embrace tomorrow, Today. Empowering solutions for your business The future belongs to those who look ahead. MOVE FORWARD WITH CONFIDENCE With an eye toward the future, we re here to help client firms

Let s embrace tomorrow, Today. Empowering solutions for your business The future belongs to those who look ahead. MOVE FORWARD WITH CONFIDENCE With an eye toward the future, we re here to help client firms

OPEN BOOK INSIGHT. marketing efforts on prospects that match those characteristics, helping you get more impact from your prospecting dollars.

Assessing Customer Profitability It s a standard business adage that it is easier (and less expensive) to sell to a current customer than to acquire a new one. Determining which of your customers is most

Assessing Customer Profitability It s a standard business adage that it is easier (and less expensive) to sell to a current customer than to acquire a new one. Determining which of your customers is most

When cost cutting alone isn t enough

Consumer products Of special interest to Consumer products executives Insights for 5executives When cost cutting alone isn t enough Sustainable cost reduction means knowing your culture EY s Global Consumer

Consumer products Of special interest to Consumer products executives Insights for 5executives When cost cutting alone isn t enough Sustainable cost reduction means knowing your culture EY s Global Consumer

COGENT REPORTS. Agile Experienced. Powerful. Accurate. Offering unique, dynamic solutions designed to meet the evolving needs of our clients

cogent-reports.com COGENT Agile Experienced Reliable Powerful Revolutionary Accurate Trusted Consultative REPORTS Offering unique, dynamic solutions designed to meet the evolving needs of our clients Our

cogent-reports.com COGENT Agile Experienced Reliable Powerful Revolutionary Accurate Trusted Consultative REPORTS Offering unique, dynamic solutions designed to meet the evolving needs of our clients Our

Enhancing deposit profitability Beat the marketplace squeeze by applying advanced analytics to your deposit business

Enhancing deposit profitability Beat the marketplace squeeze by applying advanced analytics to your deposit business Deposits form the foundation of most financial institutions operations. Not only are

Enhancing deposit profitability Beat the marketplace squeeze by applying advanced analytics to your deposit business Deposits form the foundation of most financial institutions operations. Not only are

Trends Shaping the Bank of the Future

Trends Shaping the Bank of the Future MBA Bank Management and Directors Conference November 30, 2017 Timothy Reimink Managing Director 2017 Crowe Horwath 2017 Crowe Horwath LLP 1LLP This presentation was

Trends Shaping the Bank of the Future MBA Bank Management and Directors Conference November 30, 2017 Timothy Reimink Managing Director 2017 Crowe Horwath 2017 Crowe Horwath LLP 1LLP This presentation was

New Standards. Eivind Kolding CEO, Danske Bank

New Standards Eivind Kolding CEO, Danske Bank 1 Why a new strategy for Danske Bank? Profit before tax (DKK bn) Losses (DKK bn) Global Industry Trust (%) 19.3 18.5 17.6 28 24 Technology 79 Automotive 66

New Standards Eivind Kolding CEO, Danske Bank 1 Why a new strategy for Danske Bank? Profit before tax (DKK bn) Losses (DKK bn) Global Industry Trust (%) 19.3 18.5 17.6 28 24 Technology 79 Automotive 66

Building Sustainability in Highly Competitive Markets

Building Sustainability in Highly Competitive Markets Building a Brand in Business Banking Buck Bierly, INC. October 2013 1 Building Sustainability, Building Your Brand We are assuming... Your bank is

Building Sustainability in Highly Competitive Markets Building a Brand in Business Banking Buck Bierly, INC. October 2013 1 Building Sustainability, Building Your Brand We are assuming... Your bank is

ELITE ADVISOR. Lead Generation. 12 months of marketing activities

2016 ELITE ADVISOR Lead Generation R O A D M A P 12 months of marketing activities 2016 ELITE ADVISOR Lead Generation Roadmap This lead generation roadmap provides a year-long schedule of activities that

2016 ELITE ADVISOR Lead Generation R O A D M A P 12 months of marketing activities 2016 ELITE ADVISOR Lead Generation Roadmap This lead generation roadmap provides a year-long schedule of activities that

The Magnificent 7 Cs of Change in U.S. Financial Services. Mark Sievewright President, Fiserv Credit Union Solutions October 25, 2013

The Magnificent 7 Cs of Change in U.S. Financial Services Mark Sievewright President, Fiserv Credit Union Solutions October 25, 2013 3 Game Changers The 7Cs: Consolidation Convergence Customer (Member)

The Magnificent 7 Cs of Change in U.S. Financial Services Mark Sievewright President, Fiserv Credit Union Solutions October 25, 2013 3 Game Changers The 7Cs: Consolidation Convergence Customer (Member)

EXPANDING BRAND PRESENCE IN A TIME OF BRANCH REDUCTIONS

EXPANDING BRAND PRESENCE IN A TIME OF BRANCH REDUCTIONS EXECUTIVE SUMMARY Each year, CEB TowerGroup conducts a detailed adoption and investment analysis of 29 key technologies in the retail banking space.

EXPANDING BRAND PRESENCE IN A TIME OF BRANCH REDUCTIONS EXECUTIVE SUMMARY Each year, CEB TowerGroup conducts a detailed adoption and investment analysis of 29 key technologies in the retail banking space.

ULTIMATE GUIDE TO IMPROVING CASH FLOW

ULTIMATE GUIDE TO IMPROVING CASH FLOW Cash flow is the lifeblood of your business. There are plenty of complicated strategies and complex business philosophies out there. But, what you really need is a

ULTIMATE GUIDE TO IMPROVING CASH FLOW Cash flow is the lifeblood of your business. There are plenty of complicated strategies and complex business philosophies out there. But, what you really need is a

A GUIDE TO BEST PRACTICES SMALL BUSINESS BASICS:

SMALL BUSINESS BASICS: A GUIDE TO BEST PRACTICES Starting Your Business Controlling Cash Flow Increasing Profitability Growing Your Business Protecting Your Assets Planning for Business Transition Similar

SMALL BUSINESS BASICS: A GUIDE TO BEST PRACTICES Starting Your Business Controlling Cash Flow Increasing Profitability Growing Your Business Protecting Your Assets Planning for Business Transition Similar

Accenture Interactive Point of View Series. Banking on Digital. Building trust and innovation in Financial Services

Accenture Interactive Point of View Series Banking on Building trust and innovation in Financial Services Banking on Building trust and innovation in Financial Services The digital era could not have come

Accenture Interactive Point of View Series Banking on Building trust and innovation in Financial Services Banking on Building trust and innovation in Financial Services The digital era could not have come

6 Steps to Revamp Your Small Business Marketing Strategy

6 Steps to Revamp Your Small Business Marketing Strategy Looking for better results? Craft a new plan. 1 INTRODUCTION If you re running digital marketing tactics, you have a strategy behind it, right?

6 Steps to Revamp Your Small Business Marketing Strategy Looking for better results? Craft a new plan. 1 INTRODUCTION If you re running digital marketing tactics, you have a strategy behind it, right?

SunTrust Retail Line of Business

SunTrust Retail Line of Business Gene Kirby Corporate Executive Vice President Retail Line of Business Manager Ryan Beck & Co. Financial Institutions Investor Conference November 2005 LEGAL DISCLOSURE

SunTrust Retail Line of Business Gene Kirby Corporate Executive Vice President Retail Line of Business Manager Ryan Beck & Co. Financial Institutions Investor Conference November 2005 LEGAL DISCLOSURE

RE-ENVISIONING WEALTH. Ascent Private Capital Management of U.S. Bank

RE-ENVISIONING WEALTH Ascent Private Capital Management of U.S. Bank Transcending convention with a forward focus, through the widest lens. Re-envisioning WEALTH. More than money. ASSETS. More than financial.

RE-ENVISIONING WEALTH Ascent Private Capital Management of U.S. Bank Transcending convention with a forward focus, through the widest lens. Re-envisioning WEALTH. More than money. ASSETS. More than financial.

HIGH-PERFORMING ADVISOR TEAMS

FOCUS RESEARCH SERIES ISSUE 4 HIGH-PERFORMING ADVISOR TEAMS By Kenton Shirk, Director, Intermediary, Cerulli Associates This study of high-performing was conducted by Cerulli Associates in partnership

FOCUS RESEARCH SERIES ISSUE 4 HIGH-PERFORMING ADVISOR TEAMS By Kenton Shirk, Director, Intermediary, Cerulli Associates This study of high-performing was conducted by Cerulli Associates in partnership

Farm Succession Planning

Agriculture Farm Succession Planning Ten steps toward the future you want. 1 Agriculture Farm Succession Planning Succession planning Succession planning is often on the minds of farmers. That s really

Agriculture Farm Succession Planning Ten steps toward the future you want. 1 Agriculture Farm Succession Planning Succession planning Succession planning is often on the minds of farmers. That s really

FARM MANAGEMENT CONSULTING Advisory Solutions to Enhance Farm Profitability and Operations

FARM MANAGEMENT CONSULTING Advisory Solutions to Enhance Farm Profitability and Operations OUR CORE SERVICES Introduction Management and strategic planning Farm business reviews Production economics and

FARM MANAGEMENT CONSULTING Advisory Solutions to Enhance Farm Profitability and Operations OUR CORE SERVICES Introduction Management and strategic planning Farm business reviews Production economics and

Outsourcing and the Role of Strategic Alliances

Outsourcing and the Role of Strategic Alliances Introduction The Times They Are A-changin Bob Dylan As publishers, we recognize that our own operations need to evolve if we are going to survive in the

Outsourcing and the Role of Strategic Alliances Introduction The Times They Are A-changin Bob Dylan As publishers, we recognize that our own operations need to evolve if we are going to survive in the

Winning Advantage. Seeking Profitability through Technology Integration

Raef Lee Managing Director SEI Advisor Network rlee@seic.com 610-676-1044 @SEIRaefL Winning Advantage Seeking Profitability through Technology Integration Agenda Who is SEI? The Problem What is Technology

Raef Lee Managing Director SEI Advisor Network rlee@seic.com 610-676-1044 @SEIRaefL Winning Advantage Seeking Profitability through Technology Integration Agenda Who is SEI? The Problem What is Technology

MODELED FOR GROWTH MODELED FOR GROWTH. Practice Management. Practice Management

Practice Management Practice Management MODELED FOR GROWTH MODELED FOR GROWTH Adding financial services to an already successful CPA or tax practice enables you to serve a broader range of clients and

Practice Management Practice Management MODELED FOR GROWTH MODELED FOR GROWTH Adding financial services to an already successful CPA or tax practice enables you to serve a broader range of clients and