6/14/ :41 PM 1

|

|

|

- Willis Shepherd

- 5 years ago

- Views:

Transcription

1 6/14/ :41 PM 1

2 My name is Neil MacDonald; I am a Solutions Consultant at Binary Stream Software, a Dynamics GP and AX ISV. I am a CPA, CMA having received my accounting designation over 20 years ago. In my career, I ve been a Credit Manager responsible for AR and collections for a multi-national trucking company; I ve led IT teams who built and ran multi-million dollar call centers the largest being over 99,000 square feet- as a PMP I ve run many large IT based projects, I ve been in sales, and most recently I am in a position where I provide and demo solutions to our clients in a presales role. 2

3 But how many sales in this economy are standard? As companies have to get more creative in how they sell, as sales guys create new and wonderful ways to bundle products or incent the customer to buy, things get more complex. What about sales where the product or service is delivered over time? Do you sell warranties? Do you have service or maintenance contracts included in your product prices? Do you sell systems that include both hardware and software? 4

4 If you answered yes to any of these questions, you are no doubt familiar with SOP 97-2 and EIFT 08-1, plus the standards that they evolved into. Terms like VSOE, TPE, BESP or Fair Value are familiar to you. For those of you unfamiliar with them, let s just take a minute to review them quickly. If you are selling items in a bundle, or at a discount, or as a BOGO type transaction, each item must be assigned a proportionate amount of revenue. But how do you determine what that amount should be? 5

5 These terms simply define the methods used to determine Fair Value: VSOE Vendor Specific Objective Evidence. Basically, this means, what evidence do you, as a vendor, have to determine the fair value to sell this item on its own? What is its standalone fair value? Using your specific evidence, you need to assign a Fair Value to each item in the bundle or in the contract. What if you have difficulty determining the fair value? Use TPE Third Party Evidence. In other words, what do other parties, other vendors, sell this item for? Unable to get that info? Then determine the BESP Best Estimated Selling Price, and use that value 6

6 The key to this is the term evidence. Since GAAP is very much rules based, you need to follow the rules and document every decision, then be consistent in applying it. Software has its own set of rules over and above this.sop 97-2 deals with that. This presentation is too short to go into the specifics of SOP 97-2, but basically, if you can determine a contract exists, you must either follow the VSOE rules, or in the absence of VSOE, the residual method can be used. Talk to your auditors for more details. Let s look at an example of a VSOE calculation: 7

7 Say you sell a computer system, with the following components: CPU, Monitor, KB/Mouse and a 1 year service contract. You sell it for $1,000. How do you allocate the revenue to those items? The really important one her is the service contact since it is a 12 month contract, it is deferred, and you need to be sure you claim the correct revenue for it. First, determine the Fair Value. Let s keep it simple and say you also sell these items as standalone components, like this: CPU $700 Monitor $300 KB/Mouse $100 Ser. Contract $100 Based on your Vendor Specific Objective Evidence, these values become the Fair Value used to reallocate the revenue. Total cost is $1200. To reallocate the revenue, we need to determine each components relative value, then express it as a factor of the $1,000 sale. CPU: $700/$1200 * $1000 = $ Monitor: $300/$1200 * $1000 = $ KB/Mouse: $100/$1200 * $1000 = $83.33 Ser Contract: $100/$1200 * $1000 = $83.33 Now this is a VERY simple example, but you can see how it works. 8

8 But now, businesses are having to prepare for a new standard FASB Topic 606 have been released as ASU and IFRS 15. While the release date has been pushed by one year, it is rapidly going to be upon us, especially considering that reporting requires 2 retrospective years, meaning you need to be learning how to apply this standard now.. The effective date for public companies and certain NFPs is for all fiscal periods beginning after 12/15/17. This includes both annual and interim (i.e. quarterly) reporting. For all other companies, the new standard is effective for fiscal periods beginning after 12/15/18 for annual reporting and 12/15/19 for interim (quarterly) reporting. 9

9 10

10 So first off, what are the key differences between the existing standards and the new standards? Today s accounting standards are rule based there is a strict set of rules that you must follow. You must do this, you cannot do that The new standards are PRINCIPLE based. This means that there is much more interpretation allowed on the part of businesses in complying with the new standards. Of course, that also means that you need to justify and clearly document the decisions you have made and disclose them on your financials. Let s do a quick comparison. 11

11 Current US GAAP defines when revenue is realized and recognized as follows: There must be persuasive evidence of an arrangement. A contract, for example. There must be a fixed and determinable price for that arrangement. Delivery has occurred. Collectability is reasonably assured. If these elements are satisfied, you can recognize the revenue. Of course, if delivery has occurred, but over a period of time, then the revenue must be deferred over that time period. The new revenue standard, ASU and IFRS 15 define revenue recognition to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which an entity expects to be entitled in exchange for those goods or services. It then defines 5 steps needed to determine revenue recognition, both amount and timing: You need to: Identify the contract Identify the performance obligations Determine the transaction price Allocate the transaction price Recognize revenue when (or as) performance obligations are satisfied. Notice that the term delivery is no longer used. And it calls for a well-documented judgement what are you entitled to? Let s look at the 5 steps a bit deeper: 12

12 5 Steps 13

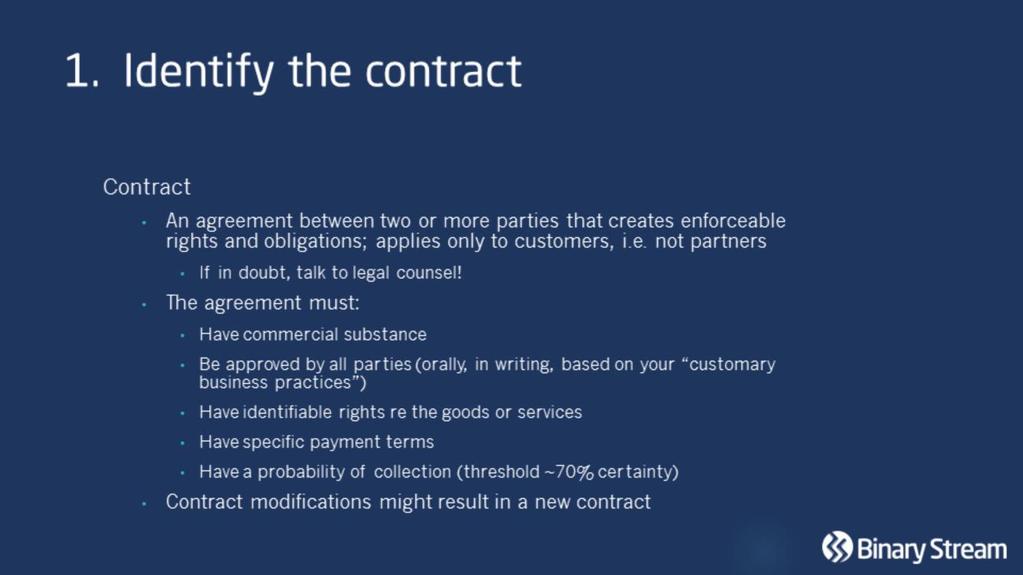

13 Identify the contract An agreement between two or more parties that creates enforceable rights and obligations: If in doubt, talk to your legal counsel! The agreement must Have commercial substance Be approved by the parties orally, in writing or based on you normal business practice Have identifiable rights re the goods and services Have specific payment terms Have a probability of collection (US GAAP recommends 70-80% surety, IFRS 50%) If multiple related contracts are entered into at or around the same time with the same customer, an argument might be made that these are in fact a single contract or agreement. An example might be a hardware sale and a software sale, to be used on that hardware, on separate contracts. Are they negotiated as a package with a single commercial objective? Does consideration for one contract depend on successful performance, or on the price, of a related contract? Are the goods and / or services a single performance obligation? Quick example you enter into an agreement with a customer, but no contract has yet been signed. Work begins and you incur costs. Can you recognize the revenue? What if a deposit has been paid? Requires JUDGEMENT. Is this normal business practice? Is it a documented policy to begin work prior to signature? Even though there is no signature, are you confident you can collect the money owed? This also requires an on-going assessment to ensure your contracts continue to meet the definition of a contract despite any changes, add-ons etc. For example, it is possible for a contract amendment to actually create a new contract based on the definitions of the standard. In this case, the original contract is concluded, and a new one created; thus these steps start over for the new contract. If you are large enough to have a revenue group, keep them busy! If not, consult your legal counsel. 14

14 15

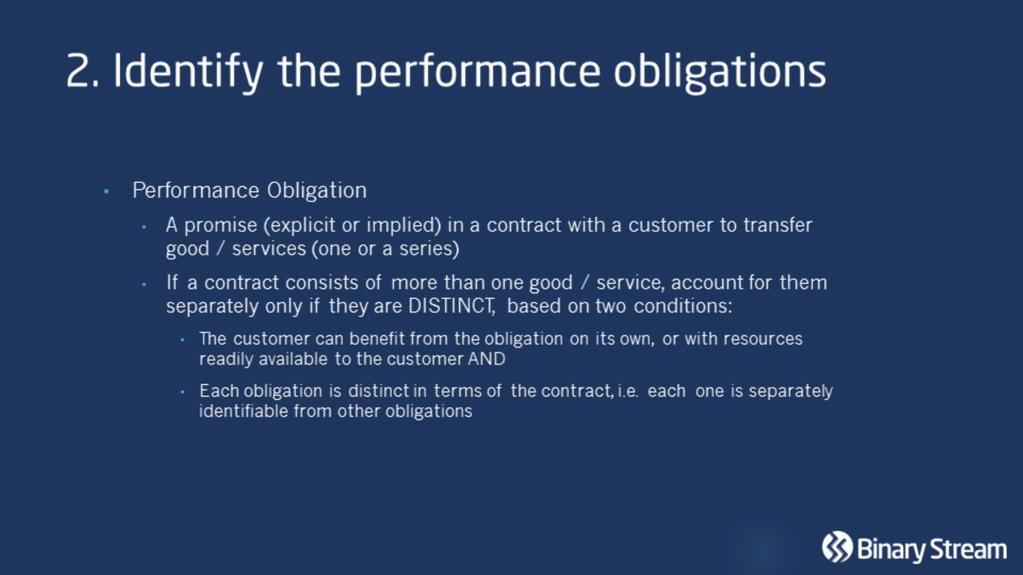

15 Identify the Performance Obligation A promise (explicit or implied in a contract with a customer to transfer goods or services If a contract consists of more than one goods or service item, account for them separately only if they are DISTINCT, based on two conditions The customer can benefit from the obligation on its own, or with resources readily available to the customer. AND Each obligation is distinct in terms of the contract; in other words each one is separately identifiable form other obligations. Quick example you make and sell proprietary, highly customized software, specific to your client s needs. No other vendor makes or can modify the software. You work on and deliver a beta version for customer testing. Can you recognize any revenue up to this point? Is it distinct? Can the customer benefit from the software as it is, or with other readily available resources? Maybe it s beta, so if it doesn t work sufficiently for business use and no one else can make it work, then I would argue no. If it works such that the customer benefits, but just needs a few tweaks, then possibly yes. Was the software sold as a separately identifiable obligation? For example, according to the contract, did you sell software and support (two separate obligations) or did you sell a solution, which includes software and support? 16

16 17

17 18

18 Determine the transaction price of each obligation This is the amount of consideration to which an entity is entitled for transferring the good or services to the customer The standard requires that these values be reassessed at each reporting period. Variable consideration Expected value, which is a probability weighted amount Most likely amount This is new to the rev rec literature Example: your contract contains a clause that promises a $10,000 bonus if you deliver the goods early; no bonus if not early. Probability weighted value is $5,000 (equal probability you will be early or you won t) but this is not an option you either get $10,000 or $0, so choose the scenario that is most likely. The one you EXPECT to happen; to the extent that it is probable that a significant reversal will not occur. Document it. Time value of money this is NEW to the literature as well Only if significant If the period of performance and payment is greater than 1 year Example: A three year pre-paid contract Treated as a loan, with income / expense There are exceptions see Non-cash consideration, treated at fair value Consideration payable rebates (treat as a reduction of the transaction price or revenue unless for a distinct good or service that the customer transfers to the entity; in which case treat as a purchase of that good or service ) Examples and considerations: Maintenance contracts: 1 year, 3 year, 5 year. What is included in revenue? What is considered significant to your business? Average contract is <1 year > $50,000 vs an oddball 2 year contract for $2,000. It depends on your business! What rate is used? The standard ( ) says The prevailing interest rate in the relevant market. Again, talk to your revenue team or your legal counsel! 19

19 20

20 21

21 Allocate the transaction price Standalone selling price the observable price of a good or service where the entity sells that good or service separately; if it is not directly observable, estimate using all reasonably observable data Sound familiar? Who said VSOE, TPE, BESP was going away??? The terms may be gone from the literature, but you still need to decide on a standalone selling price, i.e. a fair value these methods might still apply. Estimates include: Market assessment (kind of like VSOE and TPE) Cost plus calculations Residual method (only for highly variable prices, or new products for which a price has not yet been established) 22

22 23

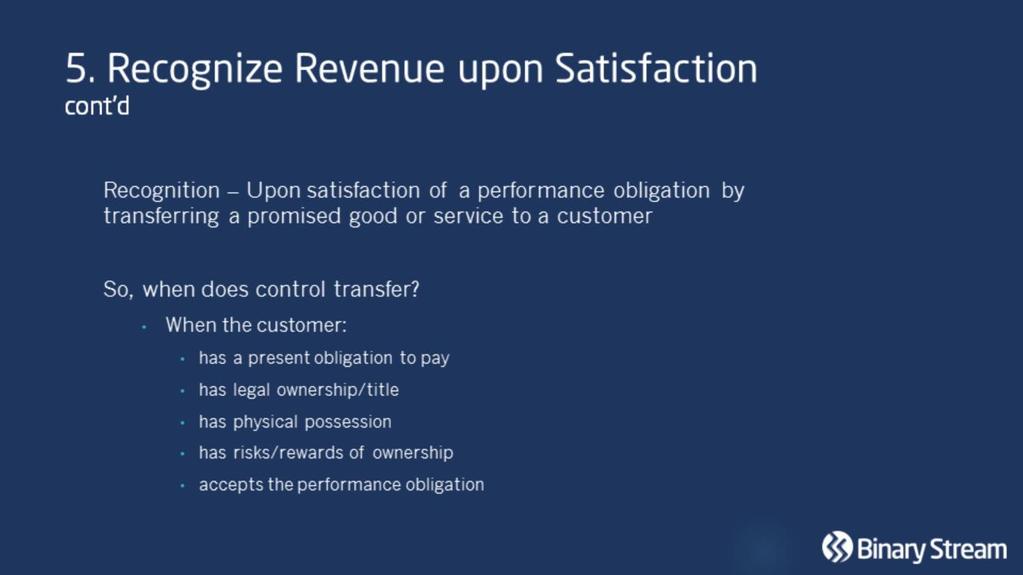

23 Recognize revenue upon satisfaction of the obligations Recognition satisfaction of a performance obligation by transferring a promised good or service to a customer, specifically, when the customer gains control Satisfied at a point in time if delivery is complete, and your obligation to the customer is complete Satisfied over time if: Performance creates or enhances an asset that the customer controls as it is created or enhanced; Performance does not create an asset with an alternative use, IF you expect to get paid; Benefits are received and consumed as the performance takes place, i.e. services, warranties Can be straight-line, milestone or event based, or percentage of completion When does the customer gain control? When the customer: Has a present obligation to pay Has legal ownership or title Has physical possession Has risks and rewards of ownership Accepts the performance obligation 25

24 26

25 27

26 These are the 5 steps outlined in the new standard 28

27 CONSIDERATIONS With the introduction of the new standard, there are no more specific standards for Construction Contracts, Software sales, or Real Estate. Basically most industry specific guidance goes away. The elimination of software-specific guidance means a possible acceleration in the timing of rev rec in situations where revenue was deferred due to a lack of VSOE of fair value. 29

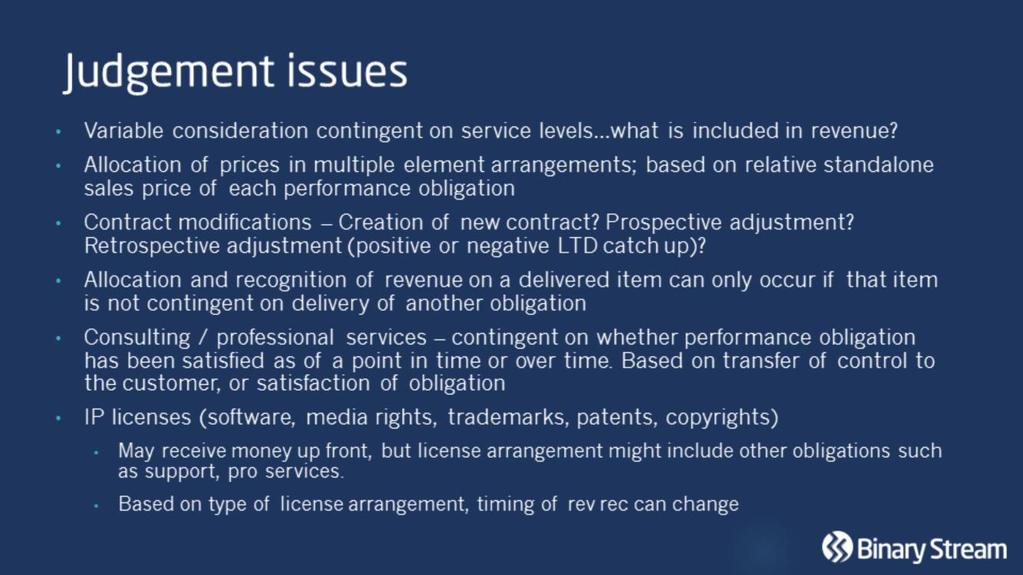

28 Lots of JUDGEMENT needed; more principles, less rules. Variable consideration, contingent on service level guarantees should these be included in the transaction price? Can there be a significant reversal? Judgement on allocation of prices to each service obligation in a multiple element transaction; based on relative standalone price of each performance obligation. Allocation and recognition of revenue on a delivered item can only occur if that item is not contingent on another obligation (undelivered item or future performance obligations). Consulting services revenue recognition is contingent on whether the performance obligation has been satisfied as of a point in time. Measuring progress toward satisfaction is based on the transfer of control to the customer. Intellectual Property licenses ( to 10-65) The licensor may receive money up front for licenses (software, media rights, franchises, patents, trademarks, copyrights). But license arrangements might include other obligations such as support, professional services etc. Based on the type of licensing, the timing of rev rec can change. 30

29 31

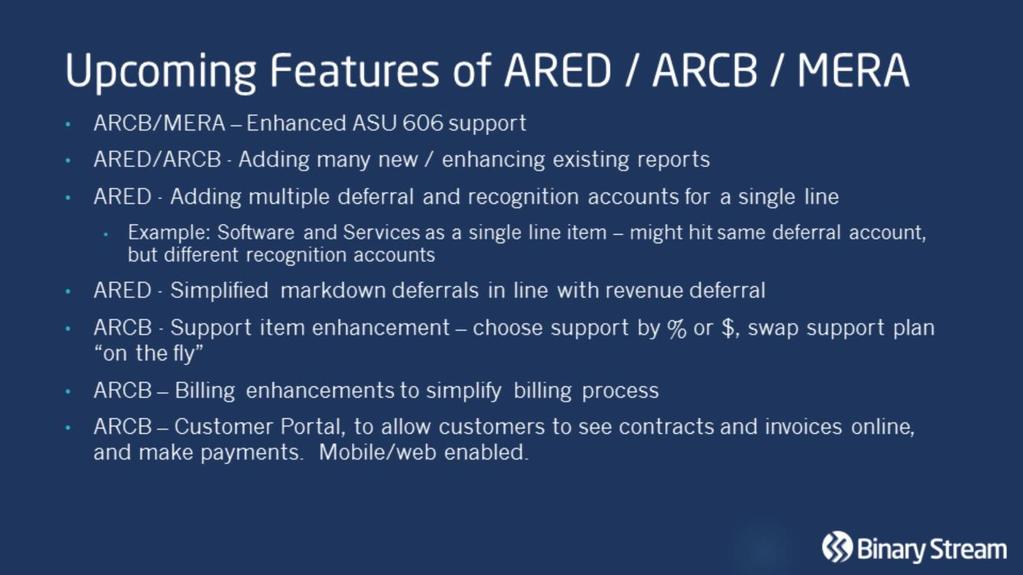

30 32

31 Now, we re here to talk about Dynamics GP How do you handle deferrals today? How do you handle VSOE Fair Value calculations? Where do you store the Fair Value, or Standalone Selling Price, amounts? How do you calculate and track milestone recognition? How do you calculate and track percentage of completion recognition? Are you ready for the future revenue standards, which are more judgement based? How are you going to store and record the transaction price for each performance obligation? 33

32 Number 1 answer EXCEL 34

33 Most of this can t be done in Dynamics GP today, so I posed these questions on the GPUG forum and got literally zero responses. I was looking for solutions from the ISV community in general, and found nothing! An I got from Microsoft says that based on what they know of the accounting standard, they have no plans to change the way Dynamics GP works. So what s the solution? Some of these things, such as basic straight line revenue recognition can be handled in the Dynamics GP Revenue and Expense Deferrals module. But most of these require a lot of manual effort moving dollars to Excel, then manually building the VSOE Fair Value calculations, and the recognition waterfall reports, or tracking the milestones and percentage of completion, followed by a complex reconciliation at month end, leading to a manual journal entry. And when the auditors come.that s when the real fun starts. 35

34 There are other options GP Project Accounting; GP Contract Admin. Complex, overkill for many situations. Options outside GP such as Softrax, Tennsoft etc. Expensive, outside GP. Another system to manage, upgrade, maintain. At Binary Stream, we have built a few products to make your life easier. 36

35 Our Advanced Revenue and Expense Deferrals (ARED) can create straight line deferrals, not by distribution, but by the line item. So if you have a 1 year and a 2 year item on the same invoice, you don t need to manually calculate how many dollars to attach to each deferral profile, ARED does it for you. And, ARED does not post all those journal entries in advance! (What accountant in his/her right mind wants journal entries posted into the next year, or two or more?) Using ARED, one of our customers, who had over 35,000 deferrals in Excel, is now able to close their monthly financials 11 days early every month! 37

36 Our Advanced Revenue and Expense Deferrals (ARED) can create straight line deferrals, not by distribution, but by the line item. So if you have a 1 year and a 2 year item on the same invoice, you don t need to manually calculate how many dollars to attach to each deferral profile, ARED does it for you. And, ARED does not post all those journal entries in advance! (What accountant in his/her right mind wants journal entries posted into the next year, or two or more?) Using ARED, one of our customers, who had over 35,000 deferrals in Excel, is now able to close their monthly financials 11 days early every month! 38

37 How about handling VSOE Fair Value calculations? Maybe this has not been an issue for you in the past, but the new accounting standard will touch many more businesses than the old standards did. Think about it business that fall under US GAAP are affected; companies that fall under IFRS are affected. No matter what business you are in, do you ever create a contract with a customer? If you sell them something, then you absolutely do! And unless you are selling strictly over the counter type goods, your business is affected! So how will you manage the calculations required to allocate the revenue properly? I see a big run on Excel licenses and Excel lessons coming up! Or. Binary Stream just released a new product called Multiple Element Revenue Allocation, or MERA, that stores or calculates both VSOE Fair Value amounts or Standalone selling prices, by Amount, based on List Price, based on the Invoice Amount, or as a Percentage of one or more other items. Again, this is a fully integrated Dynamics GP module that can be used on its own inside GP, or with our Advanced Revenue and Expense Deferrals. It simplifies the complex calculations required to remain compliant with the accounting standards both today and into the future. 39

38 40

39 Summary Existing standards New standards How we handle deferrals and price allocations today mainly in Excel Discussed solutions to manage these transaction inside Dynamics GP. Come see me later to discuss Binary Stream solutions in detail and see how they can benefit your business 41

40 Questions 42

Welcome to Today s Event. Questions / Slides. Viewing Tips & CPE Credit. Who is Tensoft? Tensoft Vital Statistics

Welcome to Today s Event FASB FASB IASB IASB Exposure Exposure Draft: Draft: Revenue from Contracts with Customers An Executive Webcast With Jeffrey Werner Viewing tips & CPE credit information About the

Welcome to Today s Event FASB FASB IASB IASB Exposure Exposure Draft: Draft: Revenue from Contracts with Customers An Executive Webcast With Jeffrey Werner Viewing tips & CPE credit information About the

ARE YOU READY FOR THE NEW REVENUE RECOGNITION STANDARD? TEN ILLUSTRATIONS 1

ARE YOU READY FOR THE NEW REVENUE RECOGNITION STANDARD? TEN ILLUSTRATIONS 1 Paul Arne Senior Partner & Chair, Technology Transactions Group MORRIS, MANNING & MARTIN, LLP 404.504.7784 pha@mmmlaw.com Sean

ARE YOU READY FOR THE NEW REVENUE RECOGNITION STANDARD? TEN ILLUSTRATIONS 1 Paul Arne Senior Partner & Chair, Technology Transactions Group MORRIS, MANNING & MARTIN, LLP 404.504.7784 pha@mmmlaw.com Sean

New revenue guidance Implementation in the technology sector

No. US2017-08 April 25, 2017 What s inside: Overview..1 Identify the contract.2 Identify performance obligations..6 Determine transaction price 9 Allocate transaction price 12 Recognize revenue. 14 Principal

No. US2017-08 April 25, 2017 What s inside: Overview..1 Identify the contract.2 Identify performance obligations..6 Determine transaction price 9 Allocate transaction price 12 Recognize revenue. 14 Principal

BECKER GEARTY CONTINUING PROFESSIONAL EDUCATION

Revenue Recognition: Now Next 973.822.2220 Learning Objectives Learning Objectives: With illustrative examples and an examination of important rules and principles, participants will acquire the background

Revenue Recognition: Now Next 973.822.2220 Learning Objectives Learning Objectives: With illustrative examples and an examination of important rules and principles, participants will acquire the background

The software revenue recognition picture begins to crystallize

Software Industry Revenue Recognition and the Revised Revenue Recognition Exposure Draft The software revenue recognition picture begins to crystallize As proposed in the November 2011 revised joint revenue

Software Industry Revenue Recognition and the Revised Revenue Recognition Exposure Draft The software revenue recognition picture begins to crystallize As proposed in the November 2011 revised joint revenue

NEED TO KNOW. IFRS 15 Revenue from Contracts with Customers

NEED TO KNOW IFRS 15 Revenue from Contracts with Customers 2 IFRS 15 REVENUE FROM CONTRACTS WITH CUSTOMERS IFRS 15 REVENUE FROM CONTRACTS WITH CUSTOMERS 3 TABLE OF CONTENTS Table of contents 3 1. Introduction

NEED TO KNOW IFRS 15 Revenue from Contracts with Customers 2 IFRS 15 REVENUE FROM CONTRACTS WITH CUSTOMERS IFRS 15 REVENUE FROM CONTRACTS WITH CUSTOMERS 3 TABLE OF CONTENTS Table of contents 3 1. Introduction

Revenue for chemical manufacturers

Revenue for chemical manufacturers The new standard s effective date is coming. US GAAP August 2017 kpmg.com/us/frv b Revenue for chemical manufacturers Revenue viewed through a new lens Again and again,

Revenue for chemical manufacturers The new standard s effective date is coming. US GAAP August 2017 kpmg.com/us/frv b Revenue for chemical manufacturers Revenue viewed through a new lens Again and again,

New revenue guidance Implementation in the software industry

No. US2017-13 July 25, 2017 What s inside: Overview 1 Step 1: Identify the contract. 2 Step 2: Identify performance obligations.6 Step 3: Determine transaction price 18 Step 4: Allocate transaction price.....21

No. US2017-13 July 25, 2017 What s inside: Overview 1 Step 1: Identify the contract. 2 Step 2: Identify performance obligations.6 Step 3: Determine transaction price 18 Step 4: Allocate transaction price.....21

TOPIC 606, REVENUE FROM CONTRACTS WITH CUSTOMERS

SEPTEMBER 2014 www.bdo.com THE NEWSLETTER FROM BDO S NATIONAL ASSURANCE PRACTICE TOPIC 606, REVENUE FROM CONTRACTS WITH CUSTOMERS u INTRODUCTION On May 28, 2014, the FASB issued its long-awaited standard,

SEPTEMBER 2014 www.bdo.com THE NEWSLETTER FROM BDO S NATIONAL ASSURANCE PRACTICE TOPIC 606, REVENUE FROM CONTRACTS WITH CUSTOMERS u INTRODUCTION On May 28, 2014, the FASB issued its long-awaited standard,

Global Communications GAAP Summit Madrid, Spain June 2014 Workshop 2: Organic growth

Global Communications GAAP Summit 2014 Madrid, Spain 23-24 Workshop 2: Organic growth After more than 10 years of deliberations the Boards have finally released the new revenue recognition standard! 2

Global Communications GAAP Summit 2014 Madrid, Spain 23-24 Workshop 2: Organic growth After more than 10 years of deliberations the Boards have finally released the new revenue recognition standard! 2

Preparing Your Company: Best Practices for the New Revenue Recognition Standards

Preparing Your Company: Best Practices for the New Revenue Recognition Standards Why are we here today? The changes to Revenue Recognition Standards will cause: Companies to put a structure in place to

Preparing Your Company: Best Practices for the New Revenue Recognition Standards Why are we here today? The changes to Revenue Recognition Standards will cause: Companies to put a structure in place to

As per Draft Notification of Ministry of Corporate Affairs dated 16 th February, 2016

IFRS 15 will be effective for IFRS reporters of the first interim period within annual reporting periods beginning on or after 1 st January 2017 and allow early adoption. The new standard will be effective

IFRS 15 will be effective for IFRS reporters of the first interim period within annual reporting periods beginning on or after 1 st January 2017 and allow early adoption. The new standard will be effective

New Revenue Recognition Standard Making it happen.

New Revenue Recognition Standard Making it happen. Terry Warfield Richard J. Johnson Chair in Accounting University of Wisconsin w/ Charlie Steward, Deloitte & Touche LLP Deloitte/FSA Faculty Consortium

New Revenue Recognition Standard Making it happen. Terry Warfield Richard J. Johnson Chair in Accounting University of Wisconsin w/ Charlie Steward, Deloitte & Touche LLP Deloitte/FSA Faculty Consortium

A shifting software revenue recognition landscape

Technology Industry A shifting software revenue recognition landscape Insights on potential impacts of the proposed revenue model on current US GAAP Volume 2 A shifting software revenue recognition landscape

Technology Industry A shifting software revenue recognition landscape Insights on potential impacts of the proposed revenue model on current US GAAP Volume 2 A shifting software revenue recognition landscape

Revenue Recognition: An Analysis of Topic 606

Revenue Recognition: An Analysis of Topic 606 For Technology and Life Sciences Companies February 13, 2018 www.aronsonllc.com www.aronsonllc.com/blogs Learning Objectives By the end of this webinar you

Revenue Recognition: An Analysis of Topic 606 For Technology and Life Sciences Companies February 13, 2018 www.aronsonllc.com www.aronsonllc.com/blogs Learning Objectives By the end of this webinar you

IFRS 15: Revenue from Contract with Customers. Credibility. Professionalism. AccountAbility 1

IFRS 15: Revenue from Contract with Customers Credibility. Professionalism. AccountAbility 1 Agenda Overview Illustrations 2 Definition of revenue Revenue is the fair value of consideration received or

IFRS 15: Revenue from Contract with Customers Credibility. Professionalism. AccountAbility 1 Agenda Overview Illustrations 2 Definition of revenue Revenue is the fair value of consideration received or

MARKS PANETH ACCOUNTING AND AUDITING ALERT: LONG-AWAITED FASB, IASB GUIDANCE SIGNIFICANTLY CHANGES REVENUE RECOGNITION IN FINANCIAL STATEMENTS

MARKS PANETH ACCOUNTING AND AUDITING ALERT: LONG-AWAITED FASB, IASB GUIDANCE SIGNIFICANTLY CHANGES REVENUE RECOGNITION IN FINANCIAL STATEMENTS The Financial Accounting Standards Board (FASB) and the International

MARKS PANETH ACCOUNTING AND AUDITING ALERT: LONG-AWAITED FASB, IASB GUIDANCE SIGNIFICANTLY CHANGES REVENUE RECOGNITION IN FINANCIAL STATEMENTS The Financial Accounting Standards Board (FASB) and the International

The new revenue standard

The new revenue standard Why is it so important? June 8, 2016 Agenda Overview Why should you care? The five step model Implementation challenges What should Companies be doing? Page 2 Overview Page 3 The

The new revenue standard Why is it so important? June 8, 2016 Agenda Overview Why should you care? The five step model Implementation challenges What should Companies be doing? Page 2 Overview Page 3 The

Presenter. Preparing to Adopt the New Revenue Recognition Standard. August 17, Preparing to Adopt the New Revenue Recognition Standard

Preparing to Adopt the New Revenue Paul Lundy, CPA 1 Presenter Paul Lundy Partner, Assurance Services Atlanta, Georgia paul.lundy@dhgllp.com 2 DHG Birmingham CPE Seminar 1 Objectives Describe the reasons

Preparing to Adopt the New Revenue Paul Lundy, CPA 1 Presenter Paul Lundy Partner, Assurance Services Atlanta, Georgia paul.lundy@dhgllp.com 2 DHG Birmingham CPE Seminar 1 Objectives Describe the reasons

Technical Line FASB final guidance

No. 2017-11 9 May 2017 Technical Line FASB final guidance How the new revenue standard affects retail and consumer products entities In this issue: Overview... 1 Customer options for additional goods and

No. 2017-11 9 May 2017 Technical Line FASB final guidance How the new revenue standard affects retail and consumer products entities In this issue: Overview... 1 Customer options for additional goods and

Implementation Tips for Revenue Recognition Standards. June 20, 2017

Implementation Tips for Revenue Recognition Standards June 20, 2017 Agenda Overview Journey to implement the new standard The challenge ahead Page 1 Overview Where are we now? Since the new standard was

Implementation Tips for Revenue Recognition Standards June 20, 2017 Agenda Overview Journey to implement the new standard The challenge ahead Page 1 Overview Where are we now? Since the new standard was

The New Global FASB/IASB Revenue Recognition Accounting Standard JD Edwards EnterpriseOne and World

JD Edwards Summit The New Global FASB/IASB Revenue Recognition Accounting Standard JD Edwards EnterpriseOne and World Seamus Moran - Senior Director Oracle Financials Product Management David Scott Senior

JD Edwards Summit The New Global FASB/IASB Revenue Recognition Accounting Standard JD Edwards EnterpriseOne and World Seamus Moran - Senior Director Oracle Financials Product Management David Scott Senior

Ramp Up to the New Revenue Standards in the Subscription World: Zuora

Ramp Up to the New Revenue Standards in the Subscription World: Zuora Preparing You for ASC 606 / IFRS 15 P 1 All businesses face challenges today in how to compute revenue. For subscription businesses,

Ramp Up to the New Revenue Standards in the Subscription World: Zuora Preparing You for ASC 606 / IFRS 15 P 1 All businesses face challenges today in how to compute revenue. For subscription businesses,

ready for change? revenue recognition. WHAT YOU DO KNOW COULD HURT YOU

ready for change? revenue recognition. WHAT YOU DO KNOW COULD HURT YOU 2 REVENUE RECOGNITION: WHAT YOU DO KNOW COULD HURT YOU Revenue recognition What You Do Know Could Hurt You Revenue recognition has

ready for change? revenue recognition. WHAT YOU DO KNOW COULD HURT YOU 2 REVENUE RECOGNITION: WHAT YOU DO KNOW COULD HURT YOU Revenue recognition What You Do Know Could Hurt You Revenue recognition has

ASC 606 For Software Companies: Step 5 - Recognizing Revenue. August 16, 2018 MEMBER OF ALLINIAL GLOBAL, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS

ASC 606 For Software Companies: Step 5 - Recognizing Revenue August 16, 2018 MEMBER OF ALLINIAL GLOBAL, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS 2018 Wolf & Company, P.C. Before we get started Today

ASC 606 For Software Companies: Step 5 - Recognizing Revenue August 16, 2018 MEMBER OF ALLINIAL GLOBAL, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS 2018 Wolf & Company, P.C. Before we get started Today

A PRACTICAL GUIDE TO REVENUE RECOGNITION. How will the new requirements under ASC 606 Revenue from Contracts with Customers affect your business?

A PRACTICAL GUIDE TO REVENUE RECOGNITION How will the new requirements under ASC 606 Revenue from Contracts with Customers affect your business? FEBRUARY 2017 BACKGROUND In May of 2014, the Financial Accounting

A PRACTICAL GUIDE TO REVENUE RECOGNITION How will the new requirements under ASC 606 Revenue from Contracts with Customers affect your business? FEBRUARY 2017 BACKGROUND In May of 2014, the Financial Accounting

The views in this summary are not Generally Accepted Accounting Principles until a consensus is reached and it is ratified by the Board.

EITF Issue 17-A, Issue Summary No. 1, Supplement No. 3 Appendix A 1. The purpose of this appendix is to provide Task Force members with a description and analysis of Alternative B, Original Alternative

EITF Issue 17-A, Issue Summary No. 1, Supplement No. 3 Appendix A 1. The purpose of this appendix is to provide Task Force members with a description and analysis of Alternative B, Original Alternative

Technical Line FASB final guidance

No. 2017-21 30 June 2017 Technical Line FASB final guidance How the new revenue standard affects airlines In this issue: Overview... 1 Loyalty programs mileage credits... 2 Estimating standalone selling

No. 2017-21 30 June 2017 Technical Line FASB final guidance How the new revenue standard affects airlines In this issue: Overview... 1 Loyalty programs mileage credits... 2 Estimating standalone selling

TOPIC 606, REVENUE FROM CONTRACTS WITH CUSTOMERS

MARCH 2017 www.bdo.com THE NEWSLETTER FROM BDO S NATIONAL ASSURANCE PRACTICE TOPIC 606, REVENUE FROM CONTRACTS WITH CUSTOMERS Introduction In 2014, the FASB issued its landmark standard, Revenue from Contracts

MARCH 2017 www.bdo.com THE NEWSLETTER FROM BDO S NATIONAL ASSURANCE PRACTICE TOPIC 606, REVENUE FROM CONTRACTS WITH CUSTOMERS Introduction In 2014, the FASB issued its landmark standard, Revenue from Contracts

Issues In-Depth. Boards Revise Joint Revenue Recognition Exposure Draft. January 2012, No Issues & Trends

Issues & Trends Issues In-Depth January 2012, No. 12-1 Contents The Model 3 Step 1 Identify the Contract with a Customer 4 Step 2 Identify the Separate Performance Obligations in the Contract 8 Step 3

Issues & Trends Issues In-Depth January 2012, No. 12-1 Contents The Model 3 Step 1 Identify the Contract with a Customer 4 Step 2 Identify the Separate Performance Obligations in the Contract 8 Step 3

New revenue guidance. Implementation in the consumer markets industry. At a glance

New revenue guidance Implementation in the consumer markets industry No. US2017-27 September 29, 2017 What s inside: Overview... 1 Identify the contract with the customer... 2 Identify performance obligations...

New revenue guidance Implementation in the consumer markets industry No. US2017-27 September 29, 2017 What s inside: Overview... 1 Identify the contract with the customer... 2 Identify performance obligations...

New revenue guidance Implementation in entertainment and media

No. US2017-19 August 25, 2017 What s inside Overview..1 Scope..2 Licenses....2 Multiple performance obligations..9 Variable consideration...11 Barter transactions.....13 Principal versus agent...14 Deferral

No. US2017-19 August 25, 2017 What s inside Overview..1 Scope..2 Licenses....2 Multiple performance obligations..9 Variable consideration...11 Barter transactions.....13 Principal versus agent...14 Deferral

Revenue Cycle Management for Software Companies

Revenue Cycle Management for Software Companies Understanding Your Company's Processes and Needs by Bob Scarborough, Tensoft CEO For software companies, the sales, billing and revenue management processes

Revenue Cycle Management for Software Companies Understanding Your Company's Processes and Needs by Bob Scarborough, Tensoft CEO For software companies, the sales, billing and revenue management processes

SIMPLIFYING SAAS AN ACCOUNTING PRIMER

SIMPLIFYING SAAS AN ACCOUNTING PRIMER www.ryansharkey.com TABLE OF CONTENTS Overview...3 Software Licensing Versus SaaS...3 Finer Points...4 The SaaS Lifecycle...5 Professional Services and Standalone

SIMPLIFYING SAAS AN ACCOUNTING PRIMER www.ryansharkey.com TABLE OF CONTENTS Overview...3 Software Licensing Versus SaaS...3 Finer Points...4 The SaaS Lifecycle...5 Professional Services and Standalone

IFRS Viewpoint. Inventory discounts and rebates

Accounting Tax Global IFRS Viewpoint Inventory discounts and rebates What s the issue? Discounts and rebates can be offered to purchasers in a number of ways, for example trade discounts, settlement discounts,

Accounting Tax Global IFRS Viewpoint Inventory discounts and rebates What s the issue? Discounts and rebates can be offered to purchasers in a number of ways, for example trade discounts, settlement discounts,

Applying IFRS in Retail and Consumer Products. IASB proposed standard. The revised revenue recognition proposal retail and consumer products

Applying IFRS in Retail and Consumer Products IASB proposed standard The revised revenue recognition proposal retail and consumer products March 2012 Contents Overview 1 Normal product sales 2 Rights of

Applying IFRS in Retail and Consumer Products IASB proposed standard The revised revenue recognition proposal retail and consumer products March 2012 Contents Overview 1 Normal product sales 2 Rights of

The Future of Revenue Recognition Understanding the Complexity

The Future of Revenue Recognition Understanding the Complexity September 13, 2012 Presenters and Content for Today s Tensoft Executive Webcast Courtesy of: Welcome to Today s Event Viewing tips & CPE credit

The Future of Revenue Recognition Understanding the Complexity September 13, 2012 Presenters and Content for Today s Tensoft Executive Webcast Courtesy of: Welcome to Today s Event Viewing tips & CPE credit

KPMG s CFO. Webcast. FASB/IASB Revenue Recognition Project. Joint FASB/IASB Revenue Recognition Project Update and Discussion with FASB Staff

KPMG s CFO Financial i Forum Webcast Joint FASB/IASB Revenue Recognition Project Update and Discussion with FASB Staff February 5, 2013 FASB/IASB Revenue Recognition Project 2002 2003 2008 2009 2010 2011

KPMG s CFO Financial i Forum Webcast Joint FASB/IASB Revenue Recognition Project Update and Discussion with FASB Staff February 5, 2013 FASB/IASB Revenue Recognition Project 2002 2003 2008 2009 2010 2011

Revenue from contracts with customers

Revenue from contracts with customers The standard is final A comprehensive look at the new revenue model No. INT2014-02 (supplement) June 18, 2014 What s inside: Overview... 1 Right of return... 2 Sell-through

Revenue from contracts with customers The standard is final A comprehensive look at the new revenue model No. INT2014-02 (supplement) June 18, 2014 What s inside: Overview... 1 Right of return... 2 Sell-through

Retail. IFRS 15 Revenue Are you good to go? May kpmg.com/ifrs KPMG IFRG Limited, a UK company limited by guarantee. All rights reserved.

Retail IFRS 15 Revenue Are you good to go? May 2017 kpmg.com/ifrs Are you good to go? IFRS 15 will change the way many retailers and wholesalers account for their contracts. To help you drive your implementation

Retail IFRS 15 Revenue Are you good to go? May 2017 kpmg.com/ifrs Are you good to go? IFRS 15 will change the way many retailers and wholesalers account for their contracts. To help you drive your implementation

Revenue from Contracts with Customers

Revenue from Contracts with Customers The standard is final A comprehensive look at the new revenue model No. US2014-01 (supplement) June 18, 2014 What s inside: Overview... 1 Right of return... 2 Sell-through

Revenue from Contracts with Customers The standard is final A comprehensive look at the new revenue model No. US2014-01 (supplement) June 18, 2014 What s inside: Overview... 1 Right of return... 2 Sell-through

CPA MOCK Evaluation Financial Reporting Module (Core 1) Page 1

Page 1") CPA MOCK Evaluation Financial Reporting Module (Core 1) Page 1 Overview The Core 1 and 2 examinations are a mix of objective format and case questions. The maximum length for an individual case will be

CPA MOCK Evaluation Financial Reporting Module (Core 1) Page 1 Overview The Core 1 and 2 examinations are a mix of objective format and case questions. The maximum length for an individual case will be

KEY LESSONS FROM SUCCESSFUL ASC 606 IMPLEMENTATIONS

KEY LESSONS FROM SUCCESSFUL ASC 606 IMPLEMENTATIONS 1 Revenue management is a complex exercise for most businesses. The incoming guidance change in the form of ASC 606 has made it even more complicated.

KEY LESSONS FROM SUCCESSFUL ASC 606 IMPLEMENTATIONS 1 Revenue management is a complex exercise for most businesses. The incoming guidance change in the form of ASC 606 has made it even more complicated.

Getting Your SaaS Business Prepared for the New Revenue Recognition Rules (ASC 606)

") Getting Your SaaS Business Prepared for the New Revenue Recognition Rules (ASC 606) Presented by: Steve Sehy, CaaS for SaaS Moderator: Chris Weber, SaaSOptics June 20, 2017 Welcome 30 seconds about us

Getting Your SaaS Business Prepared for the New Revenue Recognition Rules (ASC 606) Presented by: Steve Sehy, CaaS for SaaS Moderator: Chris Weber, SaaSOptics June 20, 2017 Welcome 30 seconds about us

Revenue from contracts with customers

Revenue from contracts with customers The standard is final A comprehensive look at the new revenue model No. INT2014-02 (supplement) 18 June 2014 (Revised 8 September 2014*) What s inside: Overview...

Revenue from contracts with customers The standard is final A comprehensive look at the new revenue model No. INT2014-02 (supplement) 18 June 2014 (Revised 8 September 2014*) What s inside: Overview...

Advanced Revenue Management

Business Solutions for Maximum Performance Advanced Revenue Management For Acumatica A Complete Solution For Managing Recurring Revenue and Payment Collections Advanced Revenue Management for Acumatica

Business Solutions for Maximum Performance Advanced Revenue Management For Acumatica A Complete Solution For Managing Recurring Revenue and Payment Collections Advanced Revenue Management for Acumatica

Revenue for retailers

Revenue for retailers The new standard s effective date is coming. US GAAP September 2017 kpmg.com/us/frv b Revenue for retailers Revenue viewed through a new lens Again and again, we are asked what s

Revenue for retailers The new standard s effective date is coming. US GAAP September 2017 kpmg.com/us/frv b Revenue for retailers Revenue viewed through a new lens Again and again, we are asked what s

SOP 97-2: CURRENT ISSUES IN VSOE ACCOUNTING. A Technical Brief

SOP 97-2: CURRENT ISSUES IN VSOE ACCOUNTING A Technical Brief Presented by: Ashwinpaul (Tony) C. Sondhi, PhD. Sponsored by: www.revenuerecognition.com - 1-2006 A. C. Sondhi and Associates About Ashwinpaul

SOP 97-2: CURRENT ISSUES IN VSOE ACCOUNTING A Technical Brief Presented by: Ashwinpaul (Tony) C. Sondhi, PhD. Sponsored by: www.revenuerecognition.com - 1-2006 A. C. Sondhi and Associates About Ashwinpaul

You can easily view comparative data and drill through for transaction details.

analyzing financial and operational information (such as number of sales reps, occupancy rates or cycle time), giving you a very powerful business management tool that leverages your financial data. You

analyzing financial and operational information (such as number of sales reps, occupancy rates or cycle time), giving you a very powerful business management tool that leverages your financial data. You

AASB 15 Revenue from contracts with customers. Consumer and industrial markets 15 November 2016

AASB 15 Revenue from contracts with customers Consumer and industrial markets 15 November 2016 Your facilitators for today are Kim Heng Kristen Haines Etienne Gouws Brandon Dalton 2 Agenda Introduction

AASB 15 Revenue from contracts with customers Consumer and industrial markets 15 November 2016 Your facilitators for today are Kim Heng Kristen Haines Etienne Gouws Brandon Dalton 2 Agenda Introduction

financial system can take several it s a more considered decision manage your business from anywhere for upgrading to an industrial strength

Solution Brief Intacct for QuickBooks Users For millions of small business owners, QuickBooks is the perfect accounting system. Cost-effective and easy-to-use, QuickBooks lets you organize your business

Solution Brief Intacct for QuickBooks Users For millions of small business owners, QuickBooks is the perfect accounting system. Cost-effective and easy-to-use, QuickBooks lets you organize your business

INVITATION TO COMMENT ON IASB EXPOSURE DRAFT OF REVENUE FROM CONTRACTS WITH CUSTOMERS Comments to be received by 20 February 2012

16 November 2011 To: Members of the Hong Kong Institute of CPAs All other interested parties INVITATION TO COMMENT ON IASB EXPOSURE DRAFT OF REVENUE FROM CONTRACTS WITH CUSTOMERS Comments to be received

16 November 2011 To: Members of the Hong Kong Institute of CPAs All other interested parties INVITATION TO COMMENT ON IASB EXPOSURE DRAFT OF REVENUE FROM CONTRACTS WITH CUSTOMERS Comments to be received

Guest Concepts, Inc. (702)

") Guest Concepts, Inc. (702) 998-4800 Welcome to our tutorial on the Lease End Renewal Process The process you will see here is extremely effective and has been used successfully with thousands of renewal

Guest Concepts, Inc. (702) 998-4800 Welcome to our tutorial on the Lease End Renewal Process The process you will see here is extremely effective and has been used successfully with thousands of renewal

WHITEPAPER. SimCrest, Inc. Cash Basis Accounting

for SimCrest, Inc. Cash Basis Accounting (Made for Microsoft Dynamics NAV) Last update 8/17/10 for Cash Basis 2010 R2 SimCrest, Inc 700 Central Expressway S, Ste 310 Allen, TX 75013 Phone 214-644-4000

for SimCrest, Inc. Cash Basis Accounting (Made for Microsoft Dynamics NAV) Last update 8/17/10 for Cash Basis 2010 R2 SimCrest, Inc 700 Central Expressway S, Ste 310 Allen, TX 75013 Phone 214-644-4000

Implementing the New Revenue Recognition Standard Helping others prepare and manage the upcoming revenue recognition standard

A ProNexus, LLC white paper Implementing the New Revenue Recognition Standard Helping others prepare and manage the upcoming revenue recognition standard December 2017 www.pronexusllc.com In May 2014,

A ProNexus, LLC white paper Implementing the New Revenue Recognition Standard Helping others prepare and manage the upcoming revenue recognition standard December 2017 www.pronexusllc.com In May 2014,

Advanced Revenue Management For Acumatica. A Complete Solution For Managing Recurring Revenue and Payments

Advanced Revenue Management For Acumatica A Complete Solution For Managing Recurring Revenue and Payments Advanced Revenue Management Advanced Revenue Management for Acumatica streamlines the operations

Advanced Revenue Management For Acumatica A Complete Solution For Managing Recurring Revenue and Payments Advanced Revenue Management Advanced Revenue Management for Acumatica streamlines the operations

Understanding Cash Management and Profit Improvement Washington Small Business Fair September 30, 2017

Understanding Cash Management and Profit Improvement Washington Small Business Fair September 30, 2017 Introduction A common scenario: - Insufficient cash reserves Cannot pay due bills Business fails No

Understanding Cash Management and Profit Improvement Washington Small Business Fair September 30, 2017 Introduction A common scenario: - Insufficient cash reserves Cannot pay due bills Business fails No

Understanding Cash Management and Profit Improvement

Understanding Cash Management and Profit Improvement Washington Small Business Fair September 30, 2017 Introduction A common scenario: - Insufficient cash reserves Cannot pay due bills Business fails No

Understanding Cash Management and Profit Improvement Washington Small Business Fair September 30, 2017 Introduction A common scenario: - Insufficient cash reserves Cannot pay due bills Business fails No

Revenue Recognition Changes Technological Impacts. Na ama Drukman Jan-2016

Revenue Recognition Changes Technological Impacts Na ama Drukman Jan-2016 Agenda New change represents a high risk Trends and Solution options Challenges and automation risks 2 Scope of the Change Potential

Revenue Recognition Changes Technological Impacts Na ama Drukman Jan-2016 Agenda New change represents a high risk Trends and Solution options Challenges and automation risks 2 Scope of the Change Potential

Up2Date Bookkeeping Plus Payroll Package. Please Click Below for a Video Demo of the Bookkeeping Spreadsheet

Up2Date Bookkeeping Plus Payroll Package Please Click Below for a Video Demo of the Bookkeeping Spreadsheet Please Click Below for a Video Demo of the Payroll Spreadsheet Description The Plus payroll package

Up2Date Bookkeeping Plus Payroll Package Please Click Below for a Video Demo of the Bookkeeping Spreadsheet Please Click Below for a Video Demo of the Payroll Spreadsheet Description The Plus payroll package

Adopt, Implement & Comply with US GAAP(ASC 606) & IFRS 15

& IFRS 15") Adopt, Implement & Comply with US GAAP(ASC 606) & IFRS 15 Agenda What is ASC 606 & IFRS 15? Business Challenges Transition Phase ASC 606 (Vs) IFRS 15 Revenue Recognition Process Case Studies Why OneGlobe?

Adopt, Implement & Comply with US GAAP(ASC 606) & IFRS 15 Agenda What is ASC 606 & IFRS 15? Business Challenges Transition Phase ASC 606 (Vs) IFRS 15 Revenue Recognition Process Case Studies Why OneGlobe?

The Purchasing Function:

ACCT 100 - Intro to Acct. Chapter 8 - Accounting for Purchases, A/P, and Cash Payments Prof. Johnson Where we have been: Last time we started our discussion for merchandising entities and focused on the

ACCT 100 - Intro to Acct. Chapter 8 - Accounting for Purchases, A/P, and Cash Payments Prof. Johnson Where we have been: Last time we started our discussion for merchandising entities and focused on the

Preparing Your Exit Strategy: 10 Ways To Increase The Value of Your Business

Preparing Your Exit Strategy: 10 Ways To Increase The Value of Your Business By TJ Van Voorhees, Co-founder and General Partner, Pacific Crest Group and Danny Krebs, Partner, The Alliance Counsel All entrepreneurs

Preparing Your Exit Strategy: 10 Ways To Increase The Value of Your Business By TJ Van Voorhees, Co-founder and General Partner, Pacific Crest Group and Danny Krebs, Partner, The Alliance Counsel All entrepreneurs

Headline. Description Specifications. BusinessManager. Customizable Marketing Materials

Headline Description Specifications Customizable Marketing Materials I Index BusinessManager Tools for ProfitStars Direct BusinessManager Brochures Business Facing Sheet...2 Trifold Brochure...3 BusinessManager

Headline Description Specifications Customizable Marketing Materials I Index BusinessManager Tools for ProfitStars Direct BusinessManager Brochures Business Facing Sheet...2 Trifold Brochure...3 BusinessManager

2016 Engineering & Construction Conference. June 15 17, 2016 The Westin Austin Downtown Austin, Texas

2016 Engineering & Construction Conference June 15 17, 2016 The Westin Austin Downtown Austin, Texas Breakout: Are You Prepared for FASB s New Revenue Recognition Standard? Jim Brant Managing Director,

2016 Engineering & Construction Conference June 15 17, 2016 The Westin Austin Downtown Austin, Texas Breakout: Are You Prepared for FASB s New Revenue Recognition Standard? Jim Brant Managing Director,

Intelligence Report. Getting real on revenue recognition implementations. By Diana Gilbert. Putting the new rules into action

Getting real on revenue recognition implementations Putting the new rules into action By Diana Gilbert June 2018 It s your turn to grab the baton and take your first lap with the new revenue recognition

Getting real on revenue recognition implementations Putting the new rules into action By Diana Gilbert June 2018 It s your turn to grab the baton and take your first lap with the new revenue recognition

Automating Vendor-Specific Objective Evidence (VSOE) & Fair Market Value (FMV) to Optimize Revenue Recognition

& Fair Market Value (FMV) to Optimize Revenue Recognition") Automating Vendor-Specific Objective Evidence (VSOE) & Fair Market Value (FMV) to Optimize Revenue Recognition Challenges & Opportunities with Multi-Element Scenarios Over the past few years, the financial

Automating Vendor-Specific Objective Evidence (VSOE) & Fair Market Value (FMV) to Optimize Revenue Recognition Challenges & Opportunities with Multi-Element Scenarios Over the past few years, the financial

Maximizing the Audit Experience for Nonprofits. Wednesday, November 4, 2015

Maximizing the Audit Experience for Nonprofits Wednesday, November 4, 2015 Welcome to the Webcast! Produced by www.501ctrust.org Providing nonprofit unemployment risk management services since 1982. Education

Maximizing the Audit Experience for Nonprofits Wednesday, November 4, 2015 Welcome to the Webcast! Produced by www.501ctrust.org Providing nonprofit unemployment risk management services since 1982. Education

Presented by: Steve Sehy, CPA, MBA Sponsors: SaaS Capital, SaaSOptics September 20, 2017

Getting Your Non-Public SaaS Business Prepared for the New Revenue Recognition Standards (ASC 606) Presented by: Steve Sehy, CPA, MBA Sponsors: SaaS Capital, SaaSOptics September 20, 2017 Welcome About

Getting Your Non-Public SaaS Business Prepared for the New Revenue Recognition Standards (ASC 606) Presented by: Steve Sehy, CPA, MBA Sponsors: SaaS Capital, SaaSOptics September 20, 2017 Welcome About

Integrating suppliers with your online store

Integrating suppliers with your online store You've figured out your market, planned on how you'll build and run your store and what your business model is. You've registered your business and you are

Integrating suppliers with your online store You've figured out your market, planned on how you'll build and run your store and what your business model is. You've registered your business and you are

A strategic playbook for taking on the new revenue recognition rules

A strategic playbook for taking on the new revenue recognition rules Set up for a smooth, thoughtful transition with this essential guide August 2016 By Diana Gilbert and Pat Voll Each company s path toward

A strategic playbook for taking on the new revenue recognition rules Set up for a smooth, thoughtful transition with this essential guide August 2016 By Diana Gilbert and Pat Voll Each company s path toward

PREPARING FOR THE NEW REV REC STANDARD WITH NETSUITE.

PREPARING FOR THE NEW REV REC STANDARD WITH NETSUITE www.netsuite.com Grab a seat and enjoy. Read Time: 10 minutes PREPARING FOR THE NEW REV REC STANDARD WITH NETSUITE The new revenue recognition standard,

PREPARING FOR THE NEW REV REC STANDARD WITH NETSUITE www.netsuite.com Grab a seat and enjoy. Read Time: 10 minutes PREPARING FOR THE NEW REV REC STANDARD WITH NETSUITE The new revenue recognition standard,

Convergence of IFRS & US GAAP

Institute of Internal Auditors Dallas Chapter IFRS Convergence of IFRS & US GAAP September 3, 2009 Presented by: Rob Bright, Principal Agenda Overview Developing and Managing an Adoption Plan Key differences

Institute of Internal Auditors Dallas Chapter IFRS Convergence of IFRS & US GAAP September 3, 2009 Presented by: Rob Bright, Principal Agenda Overview Developing and Managing an Adoption Plan Key differences

Questions to Ask Before Buying a Business

Questions to Ask Before Buying a Business Advantages of Buying a Business Last Verified: January 2016 A clear advantage to buying a business rather than beginning from scratch is that you skip the risk-filled

Questions to Ask Before Buying a Business Advantages of Buying a Business Last Verified: January 2016 A clear advantage to buying a business rather than beginning from scratch is that you skip the risk-filled

Accounting & Auditing News IFRS 15 Revenue from Contracts with Customers: Part 3B Impact on Retail, Wholesale and Distribution Sector

Philippines Technical Research 27 August 2014 (Issue 7) Accounting & Auditing News IFRS 15 Revenue from Contracts with Customers: Part 3B Impact on Retail, Wholesale and Distribution Sector How should

Philippines Technical Research 27 August 2014 (Issue 7) Accounting & Auditing News IFRS 15 Revenue from Contracts with Customers: Part 3B Impact on Retail, Wholesale and Distribution Sector How should

Issue Summary No. 1, Supplement No 1 * MEMO Issue Date September 28, Memo No. Thomas Faineteau EITF Coordinator (203)

") Memo No. Issue Summary No. 1, Supplement No 1 * MEMO Issue Date September 28, 2017 Meeting Date(s) EITF October 12, 2017 Contact(s) Project Project Stage Date previously discussed by EITF Previously distributed

Memo No. Issue Summary No. 1, Supplement No 1 * MEMO Issue Date September 28, 2017 Meeting Date(s) EITF October 12, 2017 Contact(s) Project Project Stage Date previously discussed by EITF Previously distributed

Transactions for Optimal Revenue Recognition

Welcome to Today s Event FASB Structuring IASB Software Exposure Sales Draft: Transactions Revenue from for Optimal Contracts Revenue with Recognition Customers An Executive Webcast With Jeffrey Werner

Welcome to Today s Event FASB Structuring IASB Software Exposure Sales Draft: Transactions Revenue from for Optimal Contracts Revenue with Recognition Customers An Executive Webcast With Jeffrey Werner

INTEGRATION GUIDE. Learn about the benefits of integrating your Denali modules

INTEGRATION GUIDE Learn about the benefits of integrating your Denali modules Integration Guide Copyright Notification At Cougar Mountain Software, Inc., we strive to produce high-quality software at reasonable

INTEGRATION GUIDE Learn about the benefits of integrating your Denali modules Integration Guide Copyright Notification At Cougar Mountain Software, Inc., we strive to produce high-quality software at reasonable

Recognising revenue in mobile phone services (Relevant to AAT Examination Paper 7 Financial Accounting and PBE Paper I Financial Accounting)

") Recognising revenue in mobile phone services (Relevant to AAT Examination Paper 7 Financial Accounting and PBE Paper I Financial Accounting) Patrick P. H. Ng, BA (Hons.), M. Phil., FCPA, FCCA, Department

Recognising revenue in mobile phone services (Relevant to AAT Examination Paper 7 Financial Accounting and PBE Paper I Financial Accounting) Patrick P. H. Ng, BA (Hons.), M. Phil., FCPA, FCCA, Department

Transition to IFRS 15 are you ready?

Transition to IFRS 15 are you ready? 01 May 2018 DOWNLOAD THE SLIDES TO ACCOMPANY THE WEBINAR FROM THE RESOURCES PANEL ON THE LEFT OF YOUR SCREEN THE WEBINAR WILL BEGIN SHORTLY Transition to IFRS 15 are

Transition to IFRS 15 are you ready? 01 May 2018 DOWNLOAD THE SLIDES TO ACCOMPANY THE WEBINAR FROM THE RESOURCES PANEL ON THE LEFT OF YOUR SCREEN THE WEBINAR WILL BEGIN SHORTLY Transition to IFRS 15 are

Oracle CRM: It s Really Better Than Salesforce.Com When You Do It Right

Oracle CRM: It s Really Better Than Salesforce.Com When You Do It Right By Patrick Krause, IT Convergence Prologue Like most medium-sized business-to-business service providers space, my organization brought

Oracle CRM: It s Really Better Than Salesforce.Com When You Do It Right By Patrick Krause, IT Convergence Prologue Like most medium-sized business-to-business service providers space, my organization brought

Switching from Basic to Advanced Accounting Software

The Complete Guide to Switching from Basic to Advanced Accounting Software An ebook published by: Red Wing Software, Inc. Table of Contents a Chapter 1 Signs You Are Outgrowing Your Basic Accounting System...1

The Complete Guide to Switching from Basic to Advanced Accounting Software An ebook published by: Red Wing Software, Inc. Table of Contents a Chapter 1 Signs You Are Outgrowing Your Basic Accounting System...1

Learning Best Practices For A/R Management To Release Tied Up Cash.

How Did Our Trucking Business Become A Bank? Learning Best Practices For A/R Management To Release Tied Up Cash. TM A Tailwind Management Systems White Paper INTRODUCTION NW Shippers, Inc. is a regional

How Did Our Trucking Business Become A Bank? Learning Best Practices For A/R Management To Release Tied Up Cash. TM A Tailwind Management Systems White Paper INTRODUCTION NW Shippers, Inc. is a regional

Cash Flow if you re out of money, you re out of business.

Cash Flow if you re out of money, you re out of business. Thanks for downloading this Cash Flow Cheat Sheet from SmartBusinessPlans.com.au Cash Flow is probably the most important aspect of keeping a business

Cash Flow if you re out of money, you re out of business. Thanks for downloading this Cash Flow Cheat Sheet from SmartBusinessPlans.com.au Cash Flow is probably the most important aspect of keeping a business

Straight Away Special Edition

Straight away Special edition In transition The latest on revenue recognition implementation 19 January 2015 The new revenue standard changes on the horizon A summary of the proposed amendments At a glance

Straight away Special edition In transition The latest on revenue recognition implementation 19 January 2015 The new revenue standard changes on the horizon A summary of the proposed amendments At a glance

Weighing the Benefits of a Paperless Office

Weighing the Benefits of a Paperless Office The complete decision-making guide for real-estate business owners ramu@paperlesspipeline.com www.paperlesspipeline.com page 1 of 11 Weighing the Benefits of

Weighing the Benefits of a Paperless Office The complete decision-making guide for real-estate business owners ramu@paperlesspipeline.com www.paperlesspipeline.com page 1 of 11 Weighing the Benefits of

Preparing for Your Audit. David F. Graling, CPA Ian Shuman, CPA

Preparing for Your Audit David F. Graling, CPA Ian Shuman, CPA Professional Bio David F. Graling, CPA President, Gelman, Rosenberg & Freedman CPAs More than 35 years of experience in public accounting,

Preparing for Your Audit David F. Graling, CPA Ian Shuman, CPA Professional Bio David F. Graling, CPA President, Gelman, Rosenberg & Freedman CPAs More than 35 years of experience in public accounting,

THE 7 KEYS TO HELP YOU FIND THE Right MARKETING TEAM

DISCOVER THE 7 KEYS TO HELP YOU FIND THE Right MARKETING TEAM by Jimmy Nicholas Founder & CEO of Jimmy Marketing 860.442.9999 www.jimmymarketing.com TABLE OF CONTENTS Welcome Letter from Jimmy Nicholas....................................

DISCOVER THE 7 KEYS TO HELP YOU FIND THE Right MARKETING TEAM by Jimmy Nicholas Founder & CEO of Jimmy Marketing 860.442.9999 www.jimmymarketing.com TABLE OF CONTENTS Welcome Letter from Jimmy Nicholas....................................

Completion and review

chapter 11 Completion and review Chapter learning objectives Upon completion of this chapter you will be able to: Subsequent events explain the purpose of a subsequent events review discuss the procedures

chapter 11 Completion and review Chapter learning objectives Upon completion of this chapter you will be able to: Subsequent events explain the purpose of a subsequent events review discuss the procedures

ASC 606 Transition: The role of ICFR and Auditor Expectations. Presented by Dave Christensen, Managing Consultant, Finance & Accounting February 2017

ASC 606 Transition: The role of ICFR and Auditor Expectations Presented by Dave Christensen, Managing Consultant, Finance & Accounting February 2017 Presenter Dave Christensen, CPA National Managing Consultant

ASC 606 Transition: The role of ICFR and Auditor Expectations Presented by Dave Christensen, Managing Consultant, Finance & Accounting February 2017 Presenter Dave Christensen, CPA National Managing Consultant

Legacy Revenue Recognition

September 27, 2017 2017.2 Copyright 2005, 2017, Oracle and/or its affiliates. All rights reserved. This software and related documentation are provided under a license agreement containing restrictions

September 27, 2017 2017.2 Copyright 2005, 2017, Oracle and/or its affiliates. All rights reserved. This software and related documentation are provided under a license agreement containing restrictions

Oracle Revenue Management Cloud

Oracle Revenue Management Cloud Oracle Revenue Management Cloud is a centralized, automated revenue management product that enables you to address revenue as defined in the ASC 606 and IFRS 15 accounting

Oracle Revenue Management Cloud Oracle Revenue Management Cloud is a centralized, automated revenue management product that enables you to address revenue as defined in the ASC 606 and IFRS 15 accounting

FASB Emerging Issues Task Force. Issue No Title: Applicability of SOP 97-2 to Certain Arrangements That Include Software Elements

FASB Emerging Issues Task Force Issue No. 09-3 Title: Applicability of SOP 97-2 to Certain Arrangements That Include Software Elements Document: Issue Summary No. 1 Date prepared: March 10, 2009 FASB Staff:

FASB Emerging Issues Task Force Issue No. 09-3 Title: Applicability of SOP 97-2 to Certain Arrangements That Include Software Elements Document: Issue Summary No. 1 Date prepared: March 10, 2009 FASB Staff:

Quarterly accounting roundup: An update on important developments The Dbriefs Financial Reporting series Robert Uhl, Partner, Deloitte & Touche LLP

Quarterly accounting roundup: An update on important developments The Dbriefs Financial Reporting series Robert Uhl, Partner, Deloitte & Touche LLP Chris Chiriatti, Managing Director, Deloitte & Touche

Quarterly accounting roundup: An update on important developments The Dbriefs Financial Reporting series Robert Uhl, Partner, Deloitte & Touche LLP Chris Chiriatti, Managing Director, Deloitte & Touche

New for 2009! Detecting and Correcting with the Client Data Review Feature

Chapter 17 New for 2009! Detecting and Correcting with the Client Data Review Feature Introduction: Features and Benefits Starting a Client Data Review Customizing the Client Data Review Center Account

Chapter 17 New for 2009! Detecting and Correcting with the Client Data Review Feature Introduction: Features and Benefits Starting a Client Data Review Customizing the Client Data Review Center Account

Working Draft: Time-share Revenue Recognition Implementation Issue. Financial Reporting Center Revenue Recognition

September 1, 2017 Financial Reporting Center Revenue Recognition Working Draft: Time-share Revenue Recognition Implementation Issue Issue #16-5: Principal versus Agent Considerations for Time-share Interval

September 1, 2017 Financial Reporting Center Revenue Recognition Working Draft: Time-share Revenue Recognition Implementation Issue Issue #16-5: Principal versus Agent Considerations for Time-share Interval

Revenue Recognition Changes Coming Sooner Than You Think: Five Key Considerations for Adopting ASU

Revenue Recognition Changes Coming Sooner Than You Think: Five Key Considerations for Adopting ASU 2014-09 Table of Contents Executive Overview: Business Impacts of the New Revenue 2 Recognition Standard

Revenue Recognition Changes Coming Sooner Than You Think: Five Key Considerations for Adopting ASU 2014-09 Table of Contents Executive Overview: Business Impacts of the New Revenue 2 Recognition Standard

Grow Your Business By Increasing The Average Sale Value

2007 ISSUE 2 CONTENTS. Issue 5. 2007 Grow Your Business By Increasing The Average Sale Value Sales Reps Need A Plan Avoid A Retirement Crisis Taking Control Of Profit Grow Your Business By Increasing The

2007 ISSUE 2 CONTENTS. Issue 5. 2007 Grow Your Business By Increasing The Average Sale Value Sales Reps Need A Plan Avoid A Retirement Crisis Taking Control Of Profit Grow Your Business By Increasing The

2016 Global Communications GAAP Summit. Transition: getting it right in a changing environment

2016 Transition: getting it right in a changing environment Workshop 2: Implementation of IFRS 15 2 Implementing IFRS 15 (illustrative table exercise) Stakeholders: CFO Audit Committee Board CIO RemCo

2016 Transition: getting it right in a changing environment Workshop 2: Implementation of IFRS 15 2 Implementing IFRS 15 (illustrative table exercise) Stakeholders: CFO Audit Committee Board CIO RemCo

Copyright holder is licensing this under the Creative Commons License, Attribution 3.0.

2010 by Scott Richards of Beyond the Numbers Copyright holder is licensing this under the Creative Commons License, Attribution 3.0. http://creativecommons.org/licenses/by/3.0/us/ This is a free e-book

2010 by Scott Richards of Beyond the Numbers Copyright holder is licensing this under the Creative Commons License, Attribution 3.0. http://creativecommons.org/licenses/by/3.0/us/ This is a free e-book