Domain 3 MICROECONOMICS

|

|

|

- Laurel Bailey

- 5 years ago

- Views:

Transcription

1 Domain 3 MICROECONOMICS

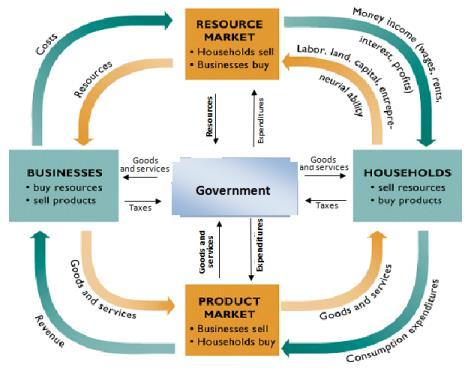

2 Georgia Standards of Excellence MICRO CONCEPT CLUSTER SSEMI1 Describe how households and businesses are interdependent and interact through flows of goods, services, resources, and money. Circular flow Money as a medium of exchange

3 Demonstration Activity The student will describe how consumers and businesses interact in the U.S. economy.

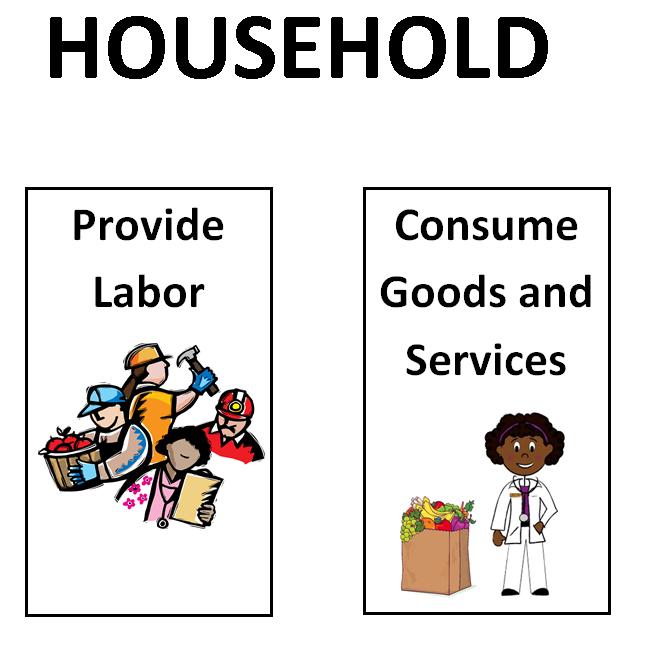

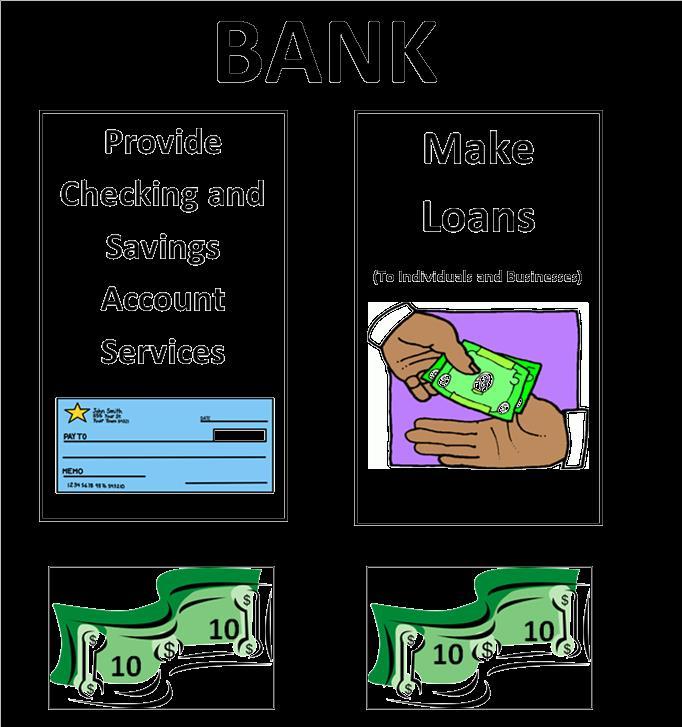

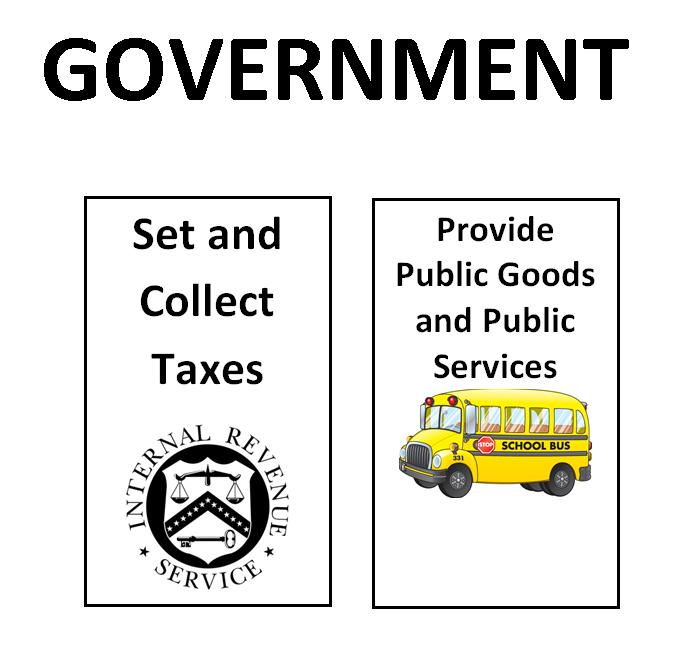

4 SS5E2 The student will describe the functions of four major sectors in the U.S. a. Describe the household function in providing resources and consuming goods and services. b. Describe the private business function in producing goods and services. c. Describe the bank function in providing checking accounts, savings accounts, and loans. d. Describe the government function in taxation and providing certain goods and services.

5

6

7

8 CIRCULAR FLOW

9

10

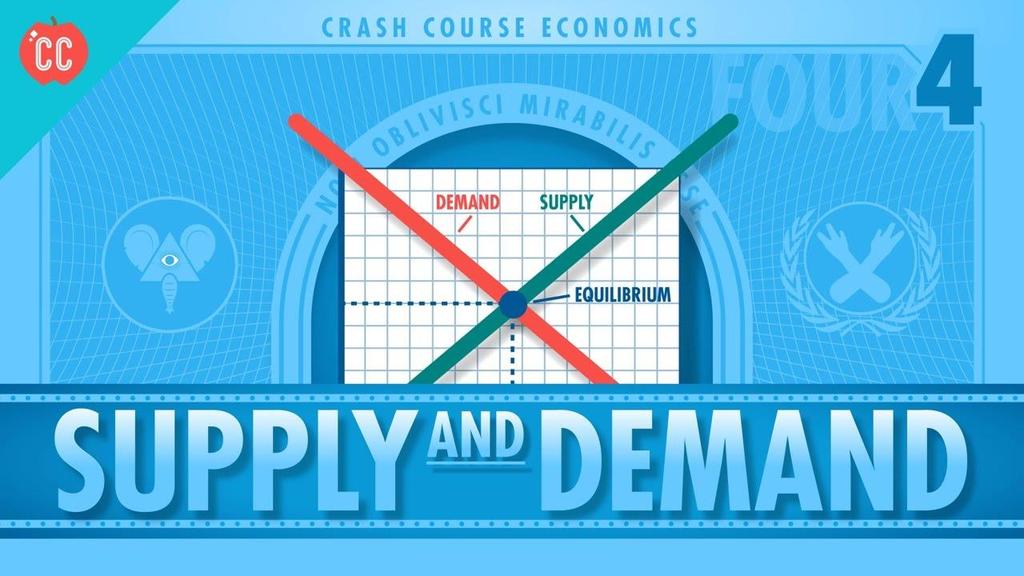

11 Georgia Standards of Excellence MICRO CONCEPT CLUSTER SSEMI2 Explain how the law of demand, the law of supply and prices work to determine production and distribution in a market economy. Law of demand Law of supply Prices Profit Production Distribution Equilibrium Incentives

12 Indiana Jones Demand and Supply

13 Understanding Demand What is the law of demand? How do the substitution effect and income effect influence decisions? What is a demand schedule? What is a demand curve?

14 What Is the Law of Demand? The law of demand states that consumers buy more of a good when its price decreases and less when its price increases. The law of demand is the result of two separate behavior patterns that overlap, the substitution effect and the income effect. These two effects describe different ways that a consumer can change his or her spending patterns for other goods.

15 The Substitution Effect and Income Effect The Substitution Effect The substitution effect occurs when consumers react to an increase in a good s price by consuming less of that good and more of other goods. The Income Effect The income effect happens when a person changes his or her consumption of goods and services as a result of a change in real income.

16 The Demand Schedule A demand schedule is a table that lists the quantity of a good a person will buy at each different price. A market demand schedule is a table that lists the quantity of a good all consumers in a market will buy at each different price. Demand Schedules Individual Demand Schedule Market Demand Schedule Price of a slice of pizza Quantity demanded per day Price of a slice of pizza Quantity demanded per day $.50 $ $.50 $ $1.50 $ $1.50 $ $ $ $ $

17 Price per slice (in dollars) The Demand Curve A demand curve is a graphical representation of a demand schedule. When reading a demand curve, assume all outside factors, such as income, are held constant. Market Demand Curve Demand Slices of pizza per day

18 Demand & Supply Curves Inverse Relationship Positive Relationship

19 Shifts of the Demand Curve What is the difference between a change in quantity demanded and a shift in the demand curve? What factors can cause shifts in the demand curve? How does the change in the price of one good affect the demand for a related good?

20 Shifts in Demand Ceteris paribus is a Latin phrase economists use meaning all other things held constant. A demand curve is accurate only as long as the ceteris paribus assumption is true. When the ceteris paribus assumption is dropped, movement no longer occurs along the demand curve. Rather, the entire demand curve shifts.

21 What Causes a Shift in Demand? Several factors can lead to a change in demand: 1. Income Changes in consumers incomes affect demand. A normal good is a good that consumers demand more of when their incomes increase. An inferior good is a good that consumers demand less of when their income increases. 2. Consumer Expectations Whether or not we expect a good to increase or decrease in price in the future greatly affects our demand for that good today. 3. Population Changes in the size of the population also affects the demand for most products. 4. Consumer Tastes and Advertising Advertising plays an important role in many trends and therefore influences demand.

22 Shift in Demand Change in Demand due to one of the Determinants of Demand (absent of a price change) Demand is the whole curve. Quantity Demanded is one point on the curve at a particular Price.

23 Prices of Related Goods The demand curve for one good can be affected by a change in the demand for another good. Complements are two goods that are bought and used together. Example: skis and ski boots Substitutes are goods used in place of one another. Example: skis and snowboards

24

25 The Law of Supply According to the law of supply, suppliers will offer more of a good at a higher price. Price As price increases Supply Quantity supplied increases Price As price falls Supply Quantity supplied falls

26 How Does the Law of Supply Work? Economists use the term quantity supplied to describe how much of a good is offered for sale at a specific price. The promise of increased revenues when prices are high encourages firms to produce more. Rising prices draw new firms into a market and add to the quantity supplied of a good.

27 Supply Schedules A market supply schedule is a chart that lists how much of a good all suppliers will offer at different prices. Market Supply Schedule Price per slice of pizza Slices supplied per day $.50 1,000 $1.00 1,500 $1.50 2,000 $2.00 2,500 $2.50 3,000

28 Price (in dollars) Supply Curves A market supply curve is a graph of the quantity supplied of a good by all suppliers at different prices. Market Supply Curve Supply Output (slices per day)

29 Changes in Supply How do input costs affect supply? How can the government affect the supply of a good? What other factors can influence supply?

30 Input Costs and Supply Any change in the cost of an input such as the raw materials, machinery, or labor used to produce a good, will affect supply. As input costs increase, the firm s marginal costs also increase, decreasing profitability and supply. Input costs can also decrease. New technology can greatly decrease costs and increase supply.

31 Government Influences on Supply By raising or lowering the cost of producing goods, the government can encourage or discourage an entrepreneur or industry. Subsidies A subsidy is a government payment that supports a business or market. Subsidies cause the supply of a good to increase. Taxes The government can reduce the supply of some goods by placing an excise tax on them. An excise tax is a tax on the production or sale of a good. Regulation Regulation occurs when the government steps into a market to affect the price, quantity, or quality of a good. Regulation usually raises costs.

32 Other Factors Influencing Supply The Global Economy The supply of imported goods and services has an impact on the supply of the same goods and services here. Government import restrictions will cause a decrease in the supply of restricted goods. Future Expectations of Prices Expectations of higher prices will reduce supply now and increase supply later. Expectations of lower prices will have the opposite effect. Number of Suppliers If more firms enter a market, the market supply of the good will rise. If firms leave the market, supply will decrease.

33 Combining Supply and Demand How do supply and demand create balance in the marketplace? What are differences between a market in equilibrium and a market in disequilibrium? What are the effects of price ceilings and price floors?

34 Equilibrium Quantity Price per slice Balancing the Market The point at which quantity demanded and quantity supplied come together is known as equilibrium. Finding Equilibrium $3.50 Equilibrium Point Combined Supply and Demand Schedule $3.00 $2.50 Price of a slice of pizza Quantity demanded Quantity supplied Result $2.00 $1.50 $1.00 Equilibrium Price a $ $ Shortage from excess demand $ Equilibrium $.50 0 Supply Demand Slices of pizza per day $2.00 $2.50 $ Surplus from excess supply

35 Market Disequilibrium If the market price or quantity supplied is anywhere but at the equilibrium price, the market is in a state called disequilibrium. There are two causes for disequilibrium: Excess Demand Excess demand occurs when quantity demanded is more than quantity supplied. Excess Supply Excess supply occurs when quantity supplied exceeds quantity demanded. Interactions between buyers and sellers will always push the market back towards equilibrium.

36 Price Ceilings In some cases the government steps in to control prices. These interventions appear as price ceilings and price floors. A price ceiling is a maximum price that can be legally charged for a good. An example of a price ceiling is rent control, a situation where a government sets a maximum amount that can be charged for rent in an area. Price Ceilings result in a SHORTAGE.

37 Price Floors A price floor is a minimum price, set by the government, that must be paid for a good or service. One well-known price floor is the minimum wage, which sets a minimum price that an employer can pay a worker for an hour of labor. Price Floors result in a SURPLUS

38 Minimum Wage Laws in the States

39 Changes in Market Equilibrium How do shifts in supply affect market equilibrium? How do shifts in demand affect market equilibrium? How can we use supply and demand curves to analyze changes in market equilibrium?

40 Shifts in Supply Understanding a Shift Since markets tend toward equilibrium, a change in supply will set market forces in motion that lead the market to a new equilibrium price and quantity sold. Excess Supply A surplus is a situation in which quantity supplied is greater than quantity demanded. If a surplus occurs, producers reduce prices to sell their products. This creates a new market equilibrium. A Fall in Supply The exact opposite will occur when supply is decreased. As supply decreases, producers will raise prices and demand will decrease.

41 Shifts in Demand Excess Demand A shortage is a situation in which quantity demanded is greater than quantity supplied. Search Costs Search costs are the financial and opportunity costs consumers pay when searching for a good or service. A Fall in Demand When demand falls, suppliers respond by cutting prices, and a new market equilibrium is found.

42 Price Price Analyzing Shifts in Supply and Demand Graph A: A Change in Supply $800 Graph B: A Change in Demand $60 $600 a b $50 Supply $400 Original supply c $40 $30 a c b $200 0 New supply Demand $20 $ New demand Original demand Output (in millions) Output (in thousands) Graph A shows how the market finds a new equilibrium when there is an increase in supply. Graph B shows how the market finds a new equilibrium when there is an increase in demand.

43 The Role of Prices What role do prices play in a free market system? What advantages do prices offer? How do prices allow for efficient resource allocation?

44 The Role of Prices in a Free Market Prices serve a vital role in a free market economy. Prices help move land, labor, and capital into the hands of producers, and finished goods in to the hands of buyers. Prices create efficient resource allocation for producers and a language that both consumers and producers can use.

45 Advantages of Prices Prices provide a language for buyers and sellers. 1. Prices as an Incentive Prices communicate to both buyers and sellers whether goods or services are scarce or easily available. Prices can encourage or discourage production. 2. Signals Think of prices as a traffic light. A relatively high price is a green light telling producers to make more. A relatively low price is a red light telling producers to make less. 3. Flexibility In many markets, prices are much more flexible than production levels. They can be easily increased or decreased to solve problems of excess supply or excess demand. 4. Price System is "Free" Unlike central planning, a distribution system based on prices costs nothing to administer.

46 Efficient Resource Allocation Resource Allocation A market system, with its fully changing prices, ensures that resources go to the uses that consumers value most highly. Market Problems Imperfect competition between firms in a market can affect prices and consumer decisions. Spillover costs, or externalities, are costs of production, such as air and water pollution, that spill over onto people who have no control over how much of a good is produced. If buyers and sellers have imperfect information on a product, they may not make the best purchasing or selling decision.

47 Costs of Production How do firms decide how much labor to hire? What are production costs? How do firms decide how much to produce?

48 A Firm s Labor Decisions Business owners have to consider how the number of workers they hire will affect their total production. The marginal product of labor is the change in output from hiring one additional unit of labor, or worker. Marginal Product of Labor Labor (number of workers) Output (beanbags per hour) Marginal product of labor

49 Marginal Product of labor (beanbags per hour) Marginal Returns Increasing marginal returns occur when marginal production levels increase with new investment. Diminishing marginal returns occur when marginal production levels decrease with new investment. Negative marginal returns occur when the marginal product of labor becomes negative. Increasing, Diminishing, and Negative Marginal Returns Increasing marginal returns Diminishing marginal returns Labor (number of workers) Negative marginal returns 8 9

50 Production Costs A fixed cost is a cost that does not change, regardless of how much of a good is produced. Examples: rent and salaries Variable costs are costs that rise or fall depending on how much is produced. Examples: costs of raw materials, some labor costs. The total cost equals fixed costs plus variable costs. The marginal cost is the cost of producing one more unit of a good.

51 Setting Output Marginal revenue is the additional income from selling one more unit of a good. It is usually equal to price. To determine the best level of output, firms determine the output level at which marginal revenue is equal to marginal cost. Production Costs Beanbags (per hour) Fixed cost Variable cost Total cost (fixed cost + variable cost) Marginal cost Marginal revenue (market price) Total revenue Profit (total revenue total cost) 0 $36 $0 $36 $24 $0 $ $

52

53 Georgia Standards of Excellence MICRO CONCEPT CLUSTER SSEMI3 Explain the organization and role of business and analyze the four types of market structure in the US economy. Organization of Business Sole proprietorship Partnership Corporation Market Structures Monopoly Oligopoly Monopolistic competition Pure competition

54 Sole Proprietorships What role do sole proprietorships play in our economy? What are the advantages of a sole proprietorship? What are the disadvantages of a sole proprietorship?

55 The Role of Sole Proprietorships A business organization is an establishment formed to carry on commercial enterprise. Sole proprietorships are the most common form of business organization. Most sole proprietorships are small. All together, sole proprietorships generate only about 6 percent of all United States sales. A sole proprietorship is a business owned and managed by a single individual.

56 Characteristics of Proprietorships Most sole proprietorships earn modest incomes. Many proprietors run their businesses part-time.

57 Advantages of Sole Proprietorships Sole proprietorships offer their owners many advantages: Ease of Start-Up With a small amount of paperwork and legal expenses, just about anyone can start a sole proprietorship. Relatively Few Regulations A proprietorship is the least-regulated form of business organization. Sole Receiver of Profit After paying taxes, the owner of sole proprietorship keeps all the profits. Full Control Owners of sole proprietorships can run their businesses as they wish. Easy to Discontinue Besides paying off legal obligations, such as taxes and debt, no other legal obligations need to be met to stop doing business.

58 Disadvantages of Sole Proprietorships Sole proprietorships have limited access to resources, such as physical capital. Human capital can also be limited, because no one knows everything. Sole proprietorships also lack permanence. Whenever an owner closes shop due to illness, retirement, or any other reason, the business ceases to exist. The biggest disadvantage of sole proprietorships is unlimited personal liability. Liability is the legally bound obligation to pay debts.

59 Partnerships What types of partnerships exist? What are the advantages of partnerships? What are the disadvantages of partnerships?

60 Types of Partnerships Partnerships fall into three categories: General Partnership In a general partnership, partners share equally in both responsibility and liability. Limited Partnership In a limited partnership, only one partner is required to be a general partner, or to have unlimited personal liability for the firm. Limited Liability Partnership A newer type of partnership is the limited liability partnership. In this form, all partners are limited partners.

61 Advantages of Partnerships Partnerships offer entrepreneurs many benefits. 1. Ease of Start-Up Partnerships are easy to establish. There is no required partnership agreement, but it is recommended that partners develop articles of partnership. 2. Shared Decision Making and Specialization In a successful partnership, each partner brings different strengths and skills to the business. 3. Larger Pool of Capital Each partner's assets, or money and other valuables, improve the firm's ability to borrow funds for operations or expansion. 4. Taxation Individual partners are subject to taxes, but the business itself does not have to pay taxes.

62 Disadvantages of Partnerships Unless the partnership is a limited liability partnership, at least one partner has unlimited liability. General partners are bound by each other s actions. Partnerships also have the potential for conflict. Partners need to ensure that they agree about work habits, goals, management styles, ethics, and general business philosophies.

63 Corporations, Mergers, and Multinationals What types of corporations exist? What are the advantages of incorporation? What are the disadvantages of incorporation? How can corporations combine? What role do multinational corporations play?

64 Types of Corporations A corporation is a legal entity, or being, owned by individual stockholders. Stocks, or shares, represent a stockholder s portion of ownership of a corporation. A corporation which issues stock to a limited a number of people is known as a closely held corporation. A publicly held corporation, buys and sells its stock on the open market.

65 Advantages of Incorporation Advantages for the Stockholders Individual investors do not carry responsibility for the corporation s actions. Shares of stock are transferable, which means that stockholders can sell their stock to others for money. Advantages for the Corporation Corporations have potential for more growth than other business forms. Corporations can borrow money by selling bonds. Corporations can hire the best available labor to create and market the best services or goods possible. Corporations have long lives.

66 Disadvantages of Incorporation Corporations are not without their disadvantages, including: Difficulty and Expense of Start-Up Corporate charters can be expensive and time consuming to establish. A state license, known as a certificate of incorporation, must be obtained. Double Taxation Corporations must pay taxes on their income. Owners also pay taxes on dividends, or the portion of the corporate profits paid to them. Loss of Control Managers and boards of directors, not owners, manage corporations. More Regulation Corporations face more regulations than other kinds of business organizations.

67 Multinationals Advantages of MNCs Multinationals benefit consumers by offering products worldwide. They also spread new technologies and production methods across the globe. Disadvantages of MNCs Some people feel that MNCs unduly influence culture and politics where they operate. Critics of multinationals are concerned about wages and working conditions provided by MNCs in foreign countries. Multinational corporations (MNCs) are large corporations headquartered in one country that have subsidiaries throughout the world.

68 Perfect Competition What conditions must exist for perfect competition? What are barriers to entry and how do they affect the marketplace? What are prices and output like in a perfectly competitive market?

69 The Four Conditions for Perfect Competition Perfect competition is a market structure in which a large number of firms all produce the same product. 1. Many Buyers and Sellers There are many participants on both the buying and selling sides. 2. Identical Products There are no differences between the products sold by different suppliers. 3. Informed Buyers and Sellers The market provides the buyer with full information about the product and its price. 4. Free Market Entry and Exit Firms can enter the market when they can make money and leave it when they can't.

70 Barriers to Entry Factors that make it difficult for new firms to enter a market are called barriers to entry. Start-up Costs The expenses that a new business must pay before the first product reaches the customer are called start-up costs. Technology Some markets require a high degree of technological know-how. As a result, new entrepreneurs cannot easily enter these markets.

71 Equilibrium Quantity Price Price and Output One of the primary characteristics of perfectly competitive markets is that they are efficient. In a perfectly competitive market, price and output reach their equilibrium levels. Market Equilibrium in Perfect Competition Supply Equilibrium Price Demand Quantity

72 Monopoly How do economists define the word monopoly? How are monopolies formed? What is price discrimination? How do firms with monopoly set output?

73 Defining Monopoly A monopoly is a market dominated by a single seller. Monopolies form when barriers prevent firms from entering a market that has a single supplier. Monopolies can take advantage of their monopoly power and charge high prices.

74 Forming a Monopoly Different market conditions can create different types of monopolies. 1. Economies of Scale If a firm's start-up costs are high, and its average costs fall for each additional unit it produces, then it enjoys what economists call economies of scale. An industry that enjoys economies of scale can easily become a natural monopoly. 2. Natural Monopolies A natural monopoly is a market that runs most efficiently when one large firm provides all of the output. 3. Technology and Change Sometimes the development of a new technology can destroy a natural monopoly.

75 Government Monopolies A government monopoly is a monopoly created by the government. Technological Monopolies The government grants patents, licenses that give the inventor of a new product the exclusive right to sell it for a certain period of time. Franchises and Licenses A franchise is a contract that gives a single firm the right to sell its goods within an exclusive market. A license is a government-issued right to operate a business. Industrial Organizations In rare cases, such as sports leagues, the government allows companies in an industry to restrict the number of firms in the market.

76 Price Discrimination Price discrimination is the division of customers into groups based on how much they will pay for a good. Although price discrimination is a feature of monopoly, it can be practiced by any company with market power. Market power is the ability to control prices and total market output. Targeted discounts, like student discounts and manufacturers rebate offers, are one form of price discrimination. Price discrimination requires some market power, distinct customer groups, and difficult resale.

77 Price Output Decisions Even a monopolist faces a limited choice it can choose to set either output or price, but not both. Monopolists will try to maximize profits; therefore, compared with a perfectly competitive market, the monopolist produces fewer goods at a higher price. A monopolist sets output at a point where marginal revenue is equal to marginal cost. Setting a Price in a Monopoly Market Price $11 $3 B A Marginal Cost C Demand 9,000 Output (in doses) Marginal Revenue

78 Monopolistic Competition and Oligopoly How does monopolistic competition compare to a monopoly and to perfect competition? How can firms compete without lowering prices? How do firms in a monopolistically competitive market set output? What is an oligopoly?

79 Four Conditions of Monopolistic Competition In monopolistic competition, many companies compete in an open market to sell products which are similar, but not identical. 1. Many Firms As a rule, monopolistically competitive markets are not marked by economies of scale or high start-up costs, allowing more firms. 2. Few Artificial Barriers to Entry Firms in a monopolistically competitive market do not face high barriers to entry. 3. Slight Control over Price Firms in a monopolistically competitive market have some freedom to raise prices because each firm's goods are a little different from everyone else's. 4. Differentiated Products Firms have some control over their selling price because they can differentiate, or distinguish, their goods from other products in the market.

80 Nonprice Competition Nonprice competition is a way to attract customers through style, service, or location, but not a lower price. 1. Characteristics of Goods The simplest way for a firm to distinguish its products is to offer a new size, color, shape, texture, or taste. 2. Location of Sale A convenience store in the middle of the desert differentiates its product simply by selling it hundreds of miles away from the nearest competitor. 3. Service Level Some sellers can charge higher prices because they offer customers a higher level of service. 4. Advertising Image Firms also use advertising to create apparent differences between their own offerings and other products in the marketplace.

81 Prices, Profits, and Output Prices Prices will be higher than they would be in perfect competition, because firms have a small amount of power to raise prices. Profits While monopolistically competitive firms can earn profits in the short run, they have to work hard to keep their product distinct enough to stay ahead of their rivals. Costs and Variety Monopolistically competitive firms cannot produce at the lowest average price due to the number of firms in the market. They do, however, offer a wide array of goods and services to consumers.

82 Oligopoly Oligopoly describes a market dominated by a few large, profitable firms. Collusion Collusion is an agreement among members of an oligopoly to set prices and production levels. Price- fixing is an agreement among firms to sell at the same or similar prices. Cartels A cartel is an association by producers established to coordinate prices and production.

83 Comparison of Market Structures Markets can be grouped into four basic structures: perfect competition, monopolistic competition, oligopoly, and monopoly Comparison of Market Structures Perfect Competition Monopolistic Competition Oligopoly Monopoly Number of firms Many Many Two to four dominate One Variety of goods None Some Some None Control over prices None Little Some Complete Barriers to entry and exit None Low High Complete Examples Wheat, shares of stock Jeans, books Cars, movie studios Public water

84 Regulation and Deregulation How do firms use market power? What market practices does the government regulate or ban to protect competition? What is deregulation?

85 Market Power Market power is the ability of a company to control prices and output. Markets dominated by a few large firms tend to have higher prices and lower output than markets with many sellers. To control prices and output like a monopoly, firms sometimes use predatory pricing. Predatory pricing sets the market price below cost levels for the short term to drive out competitors.

86 Government and Competition Government policies keep firms from controlling the prices and supply of important goods. Antitrust laws are laws that encourage competition in the marketplace. 1. Regulating Business Practices The government has the power to regulate business practices if these practices give too much power to a company that already has few competitors. 2. Breaking Up Monopolies The government has used antitrust legislation to break up existing monopolies, such as the Standard Oil Trust and AT&T. 3. Blocking Mergers A merger is a combination of two or more companies into a single firm. The government can block mergers that would decrease competition. 4. Preserving Incentives In 1997, new guidelines were introduced for proposed mergers, giving companies an opportunity to show that their merging benefits consumers.

87 Deregulation Deregulation is the removal of some government controls over a market. Deregulation is used to promote competition. Many new competitors enter a market that has been deregulated. This is followed by an economically healthy weeding out of some firms from that market, which can be hard on workers in the short term.

88 What are your questions?

Perfect Competition. Chapter 7 Section Main Menu

Perfect Competition What conditions must exist for perfect competition? What are barriers to entry and how do they affect the marketplace? What are prices and output like in a perfectly competitive market?

Perfect Competition What conditions must exist for perfect competition? What are barriers to entry and how do they affect the marketplace? What are prices and output like in a perfectly competitive market?

Perfect Competition Chapter 7 Section 1

Perfect Competition Chapter 7 Section 1 Four Conditions of Perfect Perfect competition is a market structure in which a large number of firms all produce the same product. Many buyers and sellers Identical

Perfect Competition Chapter 7 Section 1 Four Conditions of Perfect Perfect competition is a market structure in which a large number of firms all produce the same product. Many buyers and sellers Identical

Chapter 7 Notes 20. Chapter 7 Vocab Practice 32. Be An Entrepreneur 30. Chapter 8 Notes 20. Cooperative Business Notes 20

Name: Period: Week: 28 29 Dates: 3/2-3/16 Unit: Markets & Business Organizations Chapters: 7 8 Monday Tuesday Wednesday Thursday Friday 2 O *Chapter 7 9 E *Ch 8 *Cooperative Business Organization 3 E 4

Name: Period: Week: 28 29 Dates: 3/2-3/16 Unit: Markets & Business Organizations Chapters: 7 8 Monday Tuesday Wednesday Thursday Friday 2 O *Chapter 7 9 E *Ch 8 *Cooperative Business Organization 3 E 4

Objective: What conditions must exist for perfect competition? What are barriers to entry and how do they affect the marketplace?

Perfect Competition Objective: What conditions must exist for perfect competition? What are barriers to entry and how do they affect the marketplace? *Be sure to leave a couple blank lines under each question

Perfect Competition Objective: What conditions must exist for perfect competition? What are barriers to entry and how do they affect the marketplace? *Be sure to leave a couple blank lines under each question

Chapter 7: Market Structures

SCHS SOCIAL STUDIES What you need to know UNIT THREE 1. Describe 4 conditions that are in place for a perfectly competitive market 2. Describe and give characteristics of a monopoly 3. Describe and give

SCHS SOCIAL STUDIES What you need to know UNIT THREE 1. Describe 4 conditions that are in place for a perfectly competitive market 2. Describe and give characteristics of a monopoly 3. Describe and give

Chapter 7. Section 3: Monopolist Competition & Oligopoly

Chapter 7 Section 3: Monopolist Competition & Oligopoly Monopolist Competition Many companies compete in an open market to sell products that are similar but not identical Each firms hold a monopoly over

Chapter 7 Section 3: Monopolist Competition & Oligopoly Monopolist Competition Many companies compete in an open market to sell products that are similar but not identical Each firms hold a monopoly over

Multiple Choice Identify the letter of the choice that best completes the statement or answers the question.

Final day 2 Multiple Choice Identify the letter of the choice that best completes the statement or answers the question. 1. What determines how a change in prices will affect total revenue for a company?

Final day 2 Multiple Choice Identify the letter of the choice that best completes the statement or answers the question. 1. What determines how a change in prices will affect total revenue for a company?

Understanding Supply. Chapter 5 Section Main Menu

Understanding Supply What is the law of supply? What are supply schedules and supply curves? What is elasticity of supply? What factors affect elasticity of supply? The Law of Supply According to the law

Understanding Supply What is the law of supply? What are supply schedules and supply curves? What is elasticity of supply? What factors affect elasticity of supply? The Law of Supply According to the law

The following key should help you understand the different types of activities students engage in during the course:

AP Microeconomics Course Overview Name Description AP Microeconomics AP Microeconomics studies the behavior of individuals and businesses as they exchange goods and services in the marketplace. Students

AP Microeconomics Course Overview Name Description AP Microeconomics AP Microeconomics studies the behavior of individuals and businesses as they exchange goods and services in the marketplace. Students

Chapter 4: Demand. Section I: Understanding Demand. Section II: Shifts of the Demand Curve. Section III: Elasticity of Demand

Chapter 4: Demand Section I: Understanding Demand Section II: Shifts of the Demand Curve Section III: Elasticity of Demand Section 1: Understanding Demand LEQ: What is the law of demand? VOCAB: demand

Chapter 4: Demand Section I: Understanding Demand Section II: Shifts of the Demand Curve Section III: Elasticity of Demand Section 1: Understanding Demand LEQ: What is the law of demand? VOCAB: demand

GACE Economics Assessment Test I (038) Curriculum Crosswalk

Curriculum Crosswalk") Subarea I. Fundamental Economic Concepts (20%) Objective 1: Demonstrates an understanding of the fundamental concepts of economics A. Understands the concepts of scarcity, choice, and opportunity cost

Subarea I. Fundamental Economic Concepts (20%) Objective 1: Demonstrates an understanding of the fundamental concepts of economics A. Understands the concepts of scarcity, choice, and opportunity cost

Eco402 - Microeconomics Glossary By

Eco402 - Microeconomics Glossary By Break-even point : the point at which price equals the minimum of average total cost. Externalities : the spillover effects of production or consumption for which no

Eco402 - Microeconomics Glossary By Break-even point : the point at which price equals the minimum of average total cost. Externalities : the spillover effects of production or consumption for which no

Microeconomics. Use the graph below to answer question number 3

More Tutorial at Microeconomics 1. Opportunity costs are the values of the: a. minimal budgets of families on welfare b. hidden charges passed on to consumers c. monetary costs of goods and services *

More Tutorial at Microeconomics 1. Opportunity costs are the values of the: a. minimal budgets of families on welfare b. hidden charges passed on to consumers c. monetary costs of goods and services *

Microeconomics. Use the graph below to answer question number 3

More Tutorial at Microeconomics 1. Opportunity costs are the values of the: a. minimal budgets of families on welfare b. hidden charges passed on to consumers c. monetary costs of goods and services *

More Tutorial at Microeconomics 1. Opportunity costs are the values of the: a. minimal budgets of families on welfare b. hidden charges passed on to consumers c. monetary costs of goods and services *

Econ Basics. You should copy some information directly into your notebooks (Look for the Dollar Sign) LARGE = Grab as much (all) from the slide

LARGE = Grab as much (all) from the slide") Econ Basics You should copy some information directly into your notebooks (Look for the Dollar Sign) LARGE = Grab as much (all) from the slide small = bookend key phrases or ideas What is Economics? Economics

Econ Basics You should copy some information directly into your notebooks (Look for the Dollar Sign) LARGE = Grab as much (all) from the slide small = bookend key phrases or ideas What is Economics? Economics

Section I (20 questions; 1 mark each)

") Foundation Course in Managerial Economics- Solution Set- 1 Final Examination Marks- 100 Section I (20 questions; 1 mark each) 1. Which of the following statements is not true? a. Societies face an important

Foundation Course in Managerial Economics- Solution Set- 1 Final Examination Marks- 100 Section I (20 questions; 1 mark each) 1. Which of the following statements is not true? a. Societies face an important

1. Identify the 5 characteristics of perfect competition. 1. Numerous buyers and sellers 2. Standardized/identical product 3. Freedom to enter and

1. Identify the 5 characteristics of perfect competition. 1. Numerous buyers and sellers 2. Standardized/identical product 3. Freedom to enter and exit the market 4. Producers have no control over prices

1. Identify the 5 characteristics of perfect competition. 1. Numerous buyers and sellers 2. Standardized/identical product 3. Freedom to enter and exit the market 4. Producers have no control over prices

Market Structures. Perfect competition Monopolistic Competition Oligopoly Monopoly

Market Structures The classification of market structures can be arranged along a continuum, ranging from perfect competition, the most competitive market, to monopoly, the lease competitive: Perfect competition

Market Structures The classification of market structures can be arranged along a continuum, ranging from perfect competition, the most competitive market, to monopoly, the lease competitive: Perfect competition

Name Date Period -Econ Unit 2: Chapter 4-7- Demand, Supply, Prices and Markets

/ 88 Packet /20 Notes Unit 2 BIG PICTURE Questions /12 Name Date Period -Econ Unit 2: Chapter 4-7- Demand, Supply, Prices and Markets /108 Total Packet What is BIG PICTURE for Unit 2? To find the answer,

/ 88 Packet /20 Notes Unit 2 BIG PICTURE Questions /12 Name Date Period -Econ Unit 2: Chapter 4-7- Demand, Supply, Prices and Markets /108 Total Packet What is BIG PICTURE for Unit 2? To find the answer,

Economics. E.1.4 Describe how people respond predictably to positive and negative incentives.

Standard 1: Scarcity and Economic Reasoning Students will understand that productive resources are limited; therefore, people cannot have all the goods and services they want. As a result, they must choose

Standard 1: Scarcity and Economic Reasoning Students will understand that productive resources are limited; therefore, people cannot have all the goods and services they want. As a result, they must choose

Economics DESCRIPTION. EXAM INFORMATION Items

EXAM INFORMATION Items 58 Points 60 Prerequisites NONE Course Length ONE SEMESTER DESCRIPTION This course focuses on the study of economic problems and the methods by which societies solve them. Characteristics

EXAM INFORMATION Items 58 Points 60 Prerequisites NONE Course Length ONE SEMESTER DESCRIPTION This course focuses on the study of economic problems and the methods by which societies solve them. Characteristics

Name & Block: Word Definition Provide an Example (Must be a sentence) Demand (79)

Demand (79)") Name & Block: Economics: Unit Two Study Guide Standards: SSEMI2 Explain how the law of demand, the law of supply, and prices work to determine production and distribution in a market economy. a. Define

Name & Block: Economics: Unit Two Study Guide Standards: SSEMI2 Explain how the law of demand, the law of supply, and prices work to determine production and distribution in a market economy. a. Define

Economics DESCRIPTION. EXAM INFORMATION Items

EXAM INFORMATION Items 58 Points 60 Prerequisites NONE Grade Level 10-12 Course Length ONE SEMESTER DESCRIPTION This course focuses on the study of economic problems and the methods by which societies

EXAM INFORMATION Items 58 Points 60 Prerequisites NONE Grade Level 10-12 Course Length ONE SEMESTER DESCRIPTION This course focuses on the study of economic problems and the methods by which societies

Economics Unit 2. The United States Economic System

Economics Unit 2 The United States Economic System Demand Objective 2.01: Illustrate how supply and demand affects prices. What is Demand? Demand: The desire, willingness, and ability to buy a good or

Economics Unit 2 The United States Economic System Demand Objective 2.01: Illustrate how supply and demand affects prices. What is Demand? Demand: The desire, willingness, and ability to buy a good or

A Correlation of. To the Mississippi College- and Career- Readiness Standards Social Studies

A Correlation of To the 2018 Mississippi College- and Career- Readiness Standards Social Studies Table of Contents E.1... 3 E.2... 6 E.3... 7 E.4... 11 E.5... 15 E.6... 19 E.7... 24 E.8... 26 E.9... 28

A Correlation of To the 2018 Mississippi College- and Career- Readiness Standards Social Studies Table of Contents E.1... 3 E.2... 6 E.3... 7 E.4... 11 E.5... 15 E.6... 19 E.7... 24 E.8... 26 E.9... 28

Chapter 5: Supply Section 1

Chapter 5: Supply Section 1 Key Terms supply: the amount of goods available law of supply: producers offer more of a good as its price increases and less as its price falls quantity supplied: the amount

Chapter 5: Supply Section 1 Key Terms supply: the amount of goods available law of supply: producers offer more of a good as its price increases and less as its price falls quantity supplied: the amount

MARKET STRUCTURES. Economics Marshall High School Mr. Cline Unit Two FC

MARKET STRUCTURES Economics Marshall High School Mr. Cline Unit Two FC Price Discrimination Our previous example assumed that the monopolist must charge the same price to all consumers. But in some cases,

MARKET STRUCTURES Economics Marshall High School Mr. Cline Unit Two FC Price Discrimination Our previous example assumed that the monopolist must charge the same price to all consumers. But in some cases,

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. FIGURE 1-2

Questions of this SAMPLE exam were randomly chosen and may NOT be representative of the difficulty or focus of the actual examination. The professor did NOT review these questions. MULTIPLE CHOICE. Choose

Questions of this SAMPLE exam were randomly chosen and may NOT be representative of the difficulty or focus of the actual examination. The professor did NOT review these questions. MULTIPLE CHOICE. Choose

AP Microeconomics Review With Answers

AP Microeconomics Review With Answers 1. Firm in Perfect Competition (Long-Run Equilibrium) 2. Monopoly Industry with comparison of price & output of a Perfectly Competitive Industry (which means show

AP Microeconomics Review With Answers 1. Firm in Perfect Competition (Long-Run Equilibrium) 2. Monopoly Industry with comparison of price & output of a Perfectly Competitive Industry (which means show

Microeconomics: MIE1102

TEXT CHAPTERS TOPICS 1, 2 ECONOMICS, ECONOMIC SYSTEMS, MARKET ECONOMY 3 DEMAND AND SUPPLY. MARKET EQUILIBRIUM 4 ELASTICITY OF DEMAND AND SUPPLY 5 DEMAND & CONSUMER BEHAVIOR 6 PRODUCTION FUNCTION 7 COSTS

TEXT CHAPTERS TOPICS 1, 2 ECONOMICS, ECONOMIC SYSTEMS, MARKET ECONOMY 3 DEMAND AND SUPPLY. MARKET EQUILIBRIUM 4 ELASTICITY OF DEMAND AND SUPPLY 5 DEMAND & CONSUMER BEHAVIOR 6 PRODUCTION FUNCTION 7 COSTS

Micro Economics Review

Micro Economics Review 1. Intro to Economics a. What is Economics? i. Scarcity and the factors of production 1. Explain why scarcity and choice are basic problems of economics 2. Identify the factors of

Micro Economics Review 1. Intro to Economics a. What is Economics? i. Scarcity and the factors of production 1. Explain why scarcity and choice are basic problems of economics 2. Identify the factors of

12) What determines the distribution of goods and services in a market economy?

What determines the distribution of goods and services in a market economy?") The Principles of Economics: EOCT Review 1) What is scarcity? How is scarcity different from shortages? 2) What are the three factors of production: 3) Define "labor" and give an example: 4) Define "land"

The Principles of Economics: EOCT Review 1) What is scarcity? How is scarcity different from shortages? 2) What are the three factors of production: 3) Define "labor" and give an example: 4) Define "land"

Social Studies Curriculum Guide GRADE 12 ECONOMICS

Social Studies Curriculum Guide GRADE 12 ECONOMICS It is the policy of the Fulton County School System not to discriminate on the basis of race, color, sex, religion, national origin, age, or disability

Social Studies Curriculum Guide GRADE 12 ECONOMICS It is the policy of the Fulton County School System not to discriminate on the basis of race, color, sex, religion, national origin, age, or disability

One Stop Shop For Educators. Economics

Economics The economics course provides students with a basic foundation in the field of economics. The course has five sections: fundamental concepts, microeconomics, macroeconomics, international economics,

Economics The economics course provides students with a basic foundation in the field of economics. The course has five sections: fundamental concepts, microeconomics, macroeconomics, international economics,

Unit 2 Supply and Demand

Unit 2 Supply and Demand Microeconomics - analyzes the Small Unit economic behavior of Individuals, Households and Firms to understand their decision-making process. -America s Free Enterprise- An economy

Unit 2 Supply and Demand Microeconomics - analyzes the Small Unit economic behavior of Individuals, Households and Firms to understand their decision-making process. -America s Free Enterprise- An economy

A Correlation of. To the. Pennsylvania Academic Standards Economics Grades 9 & 12

A Correlation of To the Introduction This document demonstrates how Pearson, meets the Pennsylvania Academic s for,. Pearson is excited to announce its NEW program! Helping students build an essential,

A Correlation of To the Introduction This document demonstrates how Pearson, meets the Pennsylvania Academic s for,. Pearson is excited to announce its NEW program! Helping students build an essential,

Chapter 7: Market Structures Section 2

Chapter 7: Market Structures Section 2 Objectives 1. Describe characteristics and give examples of a monopoly. 2. Describe how monopolies, including government monopolies, are formed. 3. Explain how a

Chapter 7: Market Structures Section 2 Objectives 1. Describe characteristics and give examples of a monopoly. 2. Describe how monopolies, including government monopolies, are formed. 3. Explain how a

Chapter 7: Market Structures Section 2

Chapter 7: Market Structures Section 2 Objectives 1. Describe characteristics and give examples of a monopoly. 2. Describe how monopolies, including government monopolies, are formed. 3. Explain how a

Chapter 7: Market Structures Section 2 Objectives 1. Describe characteristics and give examples of a monopoly. 2. Describe how monopolies, including government monopolies, are formed. 3. Explain how a

CHAPTER 8: SECTION 1 A Perfectly Competitive Market

CHAPTER 8: SECTION 1 A Perfectly Competitive Market Four Types of Markets A market structure is the setting in which a seller finds itself. Market structures are defined by their characteristics. Those

CHAPTER 8: SECTION 1 A Perfectly Competitive Market Four Types of Markets A market structure is the setting in which a seller finds itself. Market structures are defined by their characteristics. Those

Econ Microeconomics Notes

Econ 120 - Microeconomics Notes Daniel Bramucci December 1, 2016 1 Section 1 - Thinking like an economist 1.1 Definitions Cost-Benefit Principle An action should be taken only when its benefit exceeds

Econ 120 - Microeconomics Notes Daniel Bramucci December 1, 2016 1 Section 1 - Thinking like an economist 1.1 Definitions Cost-Benefit Principle An action should be taken only when its benefit exceeds

Question # 1 of 15 ( Start time: 01:24:42 PM ) Total Marks: 1 A person with a diminishing marginal utility of income: Will be risk averse. Will be risk neutral. Will be risk loving. Cannot decide without

Question # 1 of 15 ( Start time: 01:24:42 PM ) Total Marks: 1 A person with a diminishing marginal utility of income: Will be risk averse. Will be risk neutral. Will be risk loving. Cannot decide without

Total Test Questions: 80 Levels: Grades Units of Credit:.50

DESCRIPTION This course focuses on the study of economic problems and the methods by which societies solve them. Characteristics of the market economy of the United States and its function in the world

DESCRIPTION This course focuses on the study of economic problems and the methods by which societies solve them. Characteristics of the market economy of the United States and its function in the world

Economic Profit. Accounting. Profit. Explicit. Costs. Implicit costs (including a normal profit) Accounting. costs (explicit costs only) T O T A L

Accounting. costs (explicit costs only) T O T A L") Profits Least expensive source of money for expanding business operations ost firms attempt to maximize profit Ultimately must break-even cover their costs of production Profits act as an incentive and

Profits Least expensive source of money for expanding business operations ost firms attempt to maximize profit Ultimately must break-even cover their costs of production Profits act as an incentive and

2000 AP Microeconomics Exam Answers

2000 AP Microeconomics Exam Answers 1. B Scarcity is the main economic problem!!! 2. D If the wages of farm workers and movie theater employee increase, the supply of popcorn and movies will decrease (shift

2000 AP Microeconomics Exam Answers 1. B Scarcity is the main economic problem!!! 2. D If the wages of farm workers and movie theater employee increase, the supply of popcorn and movies will decrease (shift

Chapter 4. Demand, Supply and Markets. These slides supplement the textbook, but should not replace reading the textbook

Chapter 4 Demand, Supply and Markets These slides supplement the textbook, but should not replace reading the textbook 1 What is a market? A group of buyers and sellers with the potential to trade 2 What

Chapter 4 Demand, Supply and Markets These slides supplement the textbook, but should not replace reading the textbook 1 What is a market? A group of buyers and sellers with the potential to trade 2 What

CONTENTS. Introduction to the Series. 1 Introduction to Economics 5 2 Competitive Markets, Demand and Supply Elasticities 37

CONTENTS Introduction to the Series iv 1 Introduction to Economics 5 2 Competitive Markets, Demand and Supply 17 3 Elasticities 37 4 Government Intervention in Markets 44 5 Market Failure 53 6 Costs of

CONTENTS Introduction to the Series iv 1 Introduction to Economics 5 2 Competitive Markets, Demand and Supply 17 3 Elasticities 37 4 Government Intervention in Markets 44 5 Market Failure 53 6 Costs of

Grades Prentice Hall. Economics Georgia Performance Standards, Economics. Grades 9-12

Prentice Hall Economics 2010 Grades 9-12 C O R R E L A T E D T O Georgia Performance Standards, Economics Grades 9-12 FORMAT FOR CORRELATION TO THE GEORGIA PERFORMANCE STANDARDS Subject Area: Economics

Prentice Hall Economics 2010 Grades 9-12 C O R R E L A T E D T O Georgia Performance Standards, Economics Grades 9-12 FORMAT FOR CORRELATION TO THE GEORGIA PERFORMANCE STANDARDS Subject Area: Economics

Chapter 6: Combining Supply and Demand

SCHS SOCIAL STUDIES What you need to know UNIT TWO 1. Explain how supply and demand create balance in the marketplace 2. Explain how a market reacts to a fall in supply by moving to a new equilibrium 3.

SCHS SOCIAL STUDIES What you need to know UNIT TWO 1. Explain how supply and demand create balance in the marketplace 2. Explain how a market reacts to a fall in supply by moving to a new equilibrium 3.

Economics Challenge Online State Qualification Practice Test. 1. An increase in aggregate demand would tend to result from

1. An increase in aggregate demand would tend to result from A. an increase in tax rates. B. a decrease in consumer spending. C. a decrease in net export spending. D. an increase in business investment.

1. An increase in aggregate demand would tend to result from A. an increase in tax rates. B. a decrease in consumer spending. C. a decrease in net export spending. D. an increase in business investment.

Unit 1: Introduction to Economics

Microeconomics Syllabus AP Economics Textbooks & Resources: McConnell, Campbell & Stanley Brue. Economics: Principles, Problems, and Policies. 16 th ed., New York, NY: McGraw Hill, 2005. Morton, John.

Microeconomics Syllabus AP Economics Textbooks & Resources: McConnell, Campbell & Stanley Brue. Economics: Principles, Problems, and Policies. 16 th ed., New York, NY: McGraw Hill, 2005. Morton, John.

EOCT Test Semester 2 final

EOCT Test Semester 2 final 1. The best definition of Economics is a. The study of how individuals spend their money b. The study of resources and government c. The study of the allocation of scarce resources

EOCT Test Semester 2 final 1. The best definition of Economics is a. The study of how individuals spend their money b. The study of resources and government c. The study of the allocation of scarce resources

Market structures Perfect competition

Market structures Perfect competition Market Structures Market structure refers to the number and size of buyers and sellers in the market for a good or service. A market can be defined as a group of firms

Market structures Perfect competition Market Structures Market structure refers to the number and size of buyers and sellers in the market for a good or service. A market can be defined as a group of firms

Section 1 Understanding Supply

Chapter 5 - Supply Section 1 Understanding Supply Supply the amount of goods available Law of Supply Tendency for suppliers to offer more of a good at a higher price. Law of Supply Price As price increases

Chapter 5 - Supply Section 1 Understanding Supply Supply the amount of goods available Law of Supply Tendency for suppliers to offer more of a good at a higher price. Law of Supply Price As price increases

Microeconomics. More Tutorial at

Microeconomics 1. Suppose a firm in a perfectly competitive market produces and sells 8 units of output and has a marginal revenue of $8.00. What would be the firm s total revenue if it instead produced

Microeconomics 1. Suppose a firm in a perfectly competitive market produces and sells 8 units of output and has a marginal revenue of $8.00. What would be the firm s total revenue if it instead produced

AP Microeconomics. Content Skills Learning Targets Assessment Resources & Technology

St. Michael Albertville High School Teacher: Matthew Rooker AP Microeconomics October 2014 Content Skills Learning Targets Assessment Resources & Technology November 2014 Content Skills Learning Targets

St. Michael Albertville High School Teacher: Matthew Rooker AP Microeconomics October 2014 Content Skills Learning Targets Assessment Resources & Technology November 2014 Content Skills Learning Targets

SHORT QUESTIONS AND ANSWERS FOR ECO402

SHORT QUESTIONS AND ANSWERS FOR ECO402 Question: How does opportunity cost relate to problem of scarcity? Answer: The problem of scarcity exists because of limited production. Thus, each society must make

SHORT QUESTIONS AND ANSWERS FOR ECO402 Question: How does opportunity cost relate to problem of scarcity? Answer: The problem of scarcity exists because of limited production. Thus, each society must make

Microeconomics

Microeconomics 978-1-63545-005-7 To learn more about all our offerings Visit Knewtonalta.com Source Author(s) (Text or Video) Title(s) Link (where applicable) OpenStax Steve Greenlaw - University of Mary

Microeconomics 978-1-63545-005-7 To learn more about all our offerings Visit Knewtonalta.com Source Author(s) (Text or Video) Title(s) Link (where applicable) OpenStax Steve Greenlaw - University of Mary

Week One What is economics? Chapter 1

Week One What is economics? Chapter 1 Economics: is the social science that studies the choices that individuals, businesses, governments, and entire societies make as they cope with scarcity and the incentives

Week One What is economics? Chapter 1 Economics: is the social science that studies the choices that individuals, businesses, governments, and entire societies make as they cope with scarcity and the incentives

COST OF PRODUCTION & THEORY OF THE FIRM

MICROECONOMICS: UNIT III COST OF PRODUCTION & THEORY OF THE FIRM One of the concepts mentioned in both Units I and II was and its components, total cost and total revenue. In this unit, costs and revenue

MICROECONOMICS: UNIT III COST OF PRODUCTION & THEORY OF THE FIRM One of the concepts mentioned in both Units I and II was and its components, total cost and total revenue. In this unit, costs and revenue

Four Conditions for Perfect Competition

Name: Date: Block # Economics Guided Reading Unit 3, Day 3 Homework Directions Chapter Seven Market Structures Section 1 Perfect Competition Following the page and heading prompts to read your Economics

Name: Date: Block # Economics Guided Reading Unit 3, Day 3 Homework Directions Chapter Seven Market Structures Section 1 Perfect Competition Following the page and heading prompts to read your Economics

1.3. Levels and Rates of Change Levels: example, wages and income versus Rates: example, inflation and growth Example: Box 1.3

1 Chapter 1 1.1. Scarcity, Choice, Opportunity Cost Definition of Economics: Resources versus Wants Wants: more and better unlimited Versus Needs: essential limited Versus Demand: ability to pay + want

1 Chapter 1 1.1. Scarcity, Choice, Opportunity Cost Definition of Economics: Resources versus Wants Wants: more and better unlimited Versus Needs: essential limited Versus Demand: ability to pay + want

CORRELATION OF EMC ECONOMICS: NEW WAYS OF THINKING 2011 TO THE GEORGIA PERFORMANCE STANDARDS. Subject Area: Economics State-Funded Course: Economics

CORRELATION OF EMC ECONOMICS: NEW WAYS OF THINKING 2011 TO THE GEORGIA PERFORMANCE STANDARDS Subject Area: Economics State-Funded Course: Economics Textbook Title: Economics: New Ways of Thinking Publisher:

CORRELATION OF EMC ECONOMICS: NEW WAYS OF THINKING 2011 TO THE GEORGIA PERFORMANCE STANDARDS Subject Area: Economics State-Funded Course: Economics Textbook Title: Economics: New Ways of Thinking Publisher:

Reading Essentials and Study Guide

Lesson 1 Market Structures ESSENTIAL QUESTION How do varying market structures impact prices in a market economy? Reading HELPDESK Academic Vocabulary theoretical existing only in theory; not practical

Lesson 1 Market Structures ESSENTIAL QUESTION How do varying market structures impact prices in a market economy? Reading HELPDESK Academic Vocabulary theoretical existing only in theory; not practical

GACE Economics Assessment Test at a Glance

GACE Economics Assessment Test at a Glance Updated June 2017 See the GACE Economics Assessment Study Companion for practice questions and preparation resources. Assessment Name Economics Grade Level 6

GACE Economics Assessment Test at a Glance Updated June 2017 See the GACE Economics Assessment Study Companion for practice questions and preparation resources. Assessment Name Economics Grade Level 6

Eco 202 Exam 2 Spring 2014

Eco 202 Exam 2 Spring 2014 PLEASE ANSWER 50 OF THE FOLLOWING QUESTIONS. 1. Jon Brooks quit his job in a bicycle shop, where he earned $15,000 per year, to become a graduate student in economics. At the

Eco 202 Exam 2 Spring 2014 PLEASE ANSWER 50 OF THE FOLLOWING QUESTIONS. 1. Jon Brooks quit his job in a bicycle shop, where he earned $15,000 per year, to become a graduate student in economics. At the

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

AUBG, Fall 2015, Principles Micro with P. Stankov, Sample MT2 NOTE: The actual no. of questions on the actual MT will be 30, each for 0.67 grade points. MULTIPLE CHOICE. Choose the one alternative that

AUBG, Fall 2015, Principles Micro with P. Stankov, Sample MT2 NOTE: The actual no. of questions on the actual MT will be 30, each for 0.67 grade points. MULTIPLE CHOICE. Choose the one alternative that

Essential Questions Content Skills Assessments Standards/PIs Resources/Notes. Discriminates between scarcity and shortage.

Map: AP Economics Type: Consensus Grade Level: 12 School Year: 2010-2011 Author: Jessica Cartusciello District/Building: Island Trees/Island Trees High School Created: 06/28/2010 Last Updated: 07/22/2010

Map: AP Economics Type: Consensus Grade Level: 12 School Year: 2010-2011 Author: Jessica Cartusciello District/Building: Island Trees/Island Trees High School Created: 06/28/2010 Last Updated: 07/22/2010

FINALTERM EXAMINATION FALL 2006

FINALTERM EXAMINATION FALL 2006 QUESTION NO: 1 (MARKS: 1) - PLEASE CHOOSE ONE Compared to the equilibrium price and quantity sold in a competitive market, a monopolist Will charge a price and sell a quantity.

FINALTERM EXAMINATION FALL 2006 QUESTION NO: 1 (MARKS: 1) - PLEASE CHOOSE ONE Compared to the equilibrium price and quantity sold in a competitive market, a monopolist Will charge a price and sell a quantity.

ECO201: PRINCIPLES OF MICROECONOMICS FIRST MIDTERM EXAMINATION

YOUR NAME Row Number ECO201: PRINCIPLES OF MICROECONOMICS FIRST MIDTERM EXAMINATION Prof. Bill Even November 14, 2011 FORM 2 Directions 1. Fill in your scantron with your unique-id and the form number

YOUR NAME Row Number ECO201: PRINCIPLES OF MICROECONOMICS FIRST MIDTERM EXAMINATION Prof. Bill Even November 14, 2011 FORM 2 Directions 1. Fill in your scantron with your unique-id and the form number

ECO201: PRINCIPLES OF MICROECONOMICS FIRST MIDTERM EXAMINATION

YOUR NAME Row Number ECO201: PRINCIPLES OF MICROECONOMICS FIRST MIDTERM EXAMINATION Prof. Bill Even November 14, 2011 FORM 4 Directions 1. Fill in your scantron with your unique-id and the form number

YOUR NAME Row Number ECO201: PRINCIPLES OF MICROECONOMICS FIRST MIDTERM EXAMINATION Prof. Bill Even November 14, 2011 FORM 4 Directions 1. Fill in your scantron with your unique-id and the form number

ECO 2023 Principles of Microeconomics Fall 2013 Practice Test #2. 1. Which of the following are factors of production?

ECO 2023 Principles of Microeconomics Fall 2013 Practice Test #2 1. Which of the following are factors of production? A. Output in a production function. B. Productivity. C. Land, labor, capital, and entrepreneurship.

ECO 2023 Principles of Microeconomics Fall 2013 Practice Test #2 1. Which of the following are factors of production? A. Output in a production function. B. Productivity. C. Land, labor, capital, and entrepreneurship.

MICROECONOMICS SECTION I. Time - 70 minutes 60 Questions

MICROECONOMICS SECTION I Time - 70 minutes 60 Questions Directions: Each of the questions or incomplete statements below is followed by five suggested answers or completions. Select the one that is best

MICROECONOMICS SECTION I Time - 70 minutes 60 Questions Directions: Each of the questions or incomplete statements below is followed by five suggested answers or completions. Select the one that is best

Introduction to Business and Marketing Semester 1 Exam Review

Name: Class: Date: Introduction to Business and Marketing Semester 1 Exam Review Completion Complete each statement. 1. wants are wants that are widely shared by many people. 2. Most companies that sell

Name: Class: Date: Introduction to Business and Marketing Semester 1 Exam Review Completion Complete each statement. 1. wants are wants that are widely shared by many people. 2. Most companies that sell

1. Explain 2. Describe 3. Create 4. Interpret

Law of Demand Section:- B Objectives 1. Explain the law of demand. 2. Describe how the substitution effect and the income effect influence decisions. 3. Create a demand schedule for an individual and a

Law of Demand Section:- B Objectives 1. Explain the law of demand. 2. Describe how the substitution effect and the income effect influence decisions. 3. Create a demand schedule for an individual and a

Postgraduate Diploma in Marketing December 2017 Examination Economic and Legal Impact (Econ)

") Postgraduate Diploma in Marketing December 2017 Examination Economic and Legal Impact (Econ) Date: 20 December 2017 Time: 0830 Hrs 1130 Hrs Duration: Three (03) Hrs ) Total marks for this paper is 100

Postgraduate Diploma in Marketing December 2017 Examination Economic and Legal Impact (Econ) Date: 20 December 2017 Time: 0830 Hrs 1130 Hrs Duration: Three (03) Hrs ) Total marks for this paper is 100

13 C H A P T E R O U T L I N E

PEARSON PRINCIPLES OF MICROECONOMICS E L E V E N T H E D I T I O N CASE FAIR OSTER Prepared by: Fernando Quijano w/shelly Tefft 2of 37 PART III MARKET IMPERFECTIONS AND THE ROLE OF GOVERNMENT Monopoly

PEARSON PRINCIPLES OF MICROECONOMICS E L E V E N T H E D I T I O N CASE FAIR OSTER Prepared by: Fernando Quijano w/shelly Tefft 2of 37 PART III MARKET IMPERFECTIONS AND THE ROLE OF GOVERNMENT Monopoly

Chapter 4 DEMAND. Essential Question: How do we decide what to buy?

Chapter 4: Demand Section 1 Chapter 4 DEMAND Essential Question: How do we decide what to buy? Key Terms demand: the desire to own something and the ability to pay for it law of demand: consumers will

Chapter 4: Demand Section 1 Chapter 4 DEMAND Essential Question: How do we decide what to buy? Key Terms demand: the desire to own something and the ability to pay for it law of demand: consumers will

Monopoly CHAPTER. Goals. Outcomes

CHAPTER 15 Monopoly Goals in this chapter you will Learn why some markets have only one seller Analyze how a monopoly determines the quantity to produce and the price to charge See how the monopoly s decisions

CHAPTER 15 Monopoly Goals in this chapter you will Learn why some markets have only one seller Analyze how a monopoly determines the quantity to produce and the price to charge See how the monopoly s decisions

Microeconomics Exam Notes

Microeconomics Exam Notes Opportunity Cost What you give up to get it Production Possibility Frontier Maximum attainable combination of two products (Concept of Opportunity Cost). Main Decision Makers:

Microeconomics Exam Notes Opportunity Cost What you give up to get it Production Possibility Frontier Maximum attainable combination of two products (Concept of Opportunity Cost). Main Decision Makers:

DEMAND AND SUPPLY. Chapter 3. Principles of Macroeconomics by OpenStax College is licensed under a Creative Commons Attribution 3.

DEMAND AND SUPPLY Chapter 3 Principles of Macroeconomics by OpenStax College is licensed under a Creative Commons Attribution 3.0 Unported License Demand for Goods and Services Demand refers to the amount

DEMAND AND SUPPLY Chapter 3 Principles of Macroeconomics by OpenStax College is licensed under a Creative Commons Attribution 3.0 Unported License Demand for Goods and Services Demand refers to the amount

Curriculum Standard One: The students will understand common economic terms and concepts and economic reasoning.

Curriculum Standard One: The students will understand common economic terms and concepts and economic reasoning. *1. The students will examine the causal relationship between scarcity and the need for

Curriculum Standard One: The students will understand common economic terms and concepts and economic reasoning. *1. The students will examine the causal relationship between scarcity and the need for

4. A mixed economy combines two different economic types. Which two economic types are combined?

1. Identify the type of economy featured in the United States. A. Command Economy B. Market Economy C. Mixed Economy D. Traditional Economy 2. Which is the strongest motivating force within a market economy

1. Identify the type of economy featured in the United States. A. Command Economy B. Market Economy C. Mixed Economy D. Traditional Economy 2. Which is the strongest motivating force within a market economy

Objective: What is the law of supply? What are supply schedules and supply curves? What is elasticity of supply?

Understanding Supply Objective: What is the law of supply? What are supply schedules and supply curves? What is elasticity of supply? *Be sure to leave a couple blank lines under each question and answer

Understanding Supply Objective: What is the law of supply? What are supply schedules and supply curves? What is elasticity of supply? *Be sure to leave a couple blank lines under each question and answer

ECO201: PRINCIPLES OF MICROECONOMICS SECOND MIDTERM EXAMINATION

Name Seat Assignment ECO201: PRINCIPLES OF MICROECONOMICS SECOND MIDTERM EXAMINATION November 17, 2009 FORM 3. Directions 1. FILL IN YOUR SCANTRON WITH YOUR UNIQUE ID AND THE FORM NUMBER LISTED ON THIS

Name Seat Assignment ECO201: PRINCIPLES OF MICROECONOMICS SECOND MIDTERM EXAMINATION November 17, 2009 FORM 3. Directions 1. FILL IN YOUR SCANTRON WITH YOUR UNIQUE ID AND THE FORM NUMBER LISTED ON THIS

Directions: This problem set is graded. Feel free to ask me questions. Turn your answers in on the provided scantron form.

Micro Problem Set III WCC Fall 2015 Directions: This problem set is graded. Feel free to ask me questions. Turn your answers in on the provided scantron form. A=True / B=False 25 Points 1) All combinations

Micro Problem Set III WCC Fall 2015 Directions: This problem set is graded. Feel free to ask me questions. Turn your answers in on the provided scantron form. A=True / B=False 25 Points 1) All combinations

NB: STUDENTS ARE REQUESTED IN THEIR OWN INTEREST TO WRITE LEGIBLY AND IN INK.

1 INFORMATION & INSTRUCTIONS: DURATION: THREE (3) HOURS TOTAL MARKS: 300 INTERNAL EXAMINER : PROFESSOR D. MAHADEA EXTERNAL EXAMINER: MR R. SIMSON NB: STUDENTS ARE REQUESTED IN THEIR OWN INTEREST TO WRITE

1 INFORMATION & INSTRUCTIONS: DURATION: THREE (3) HOURS TOTAL MARKS: 300 INTERNAL EXAMINER : PROFESSOR D. MAHADEA EXTERNAL EXAMINER: MR R. SIMSON NB: STUDENTS ARE REQUESTED IN THEIR OWN INTEREST TO WRITE

District Test Review answers are at the end of the test

District Test Review answers are at the end of the test Multiple Choice Identify the choice that best completes the statement or answers the question. 1. Cars and automobile insurance are examples of:

District Test Review answers are at the end of the test Multiple Choice Identify the choice that best completes the statement or answers the question. 1. Cars and automobile insurance are examples of:

INTRODUCTION ECONOMIC PROFITS

INTRODUCTION This chapter addresses the following key questions: What are profits? What are the unique characteristics of competitive firms? How much output will a competitive firm produce? Chapter 7 THE

INTRODUCTION This chapter addresses the following key questions: What are profits? What are the unique characteristics of competitive firms? How much output will a competitive firm produce? Chapter 7 THE

JANUARY EXAMINATIONS 2008

No. of Pages: (A) 9 No. of Questions: 38 EC1000A micro 2008 JANUARY EXAMINATIONS 2008 Subject Title of Paper ECONOMICS EC1000 MICROECONOMICS Time Allowed Two Hours (2 Hours) Instructions to candidates

No. of Pages: (A) 9 No. of Questions: 38 EC1000A micro 2008 JANUARY EXAMINATIONS 2008 Subject Title of Paper ECONOMICS EC1000 MICROECONOMICS Time Allowed Two Hours (2 Hours) Instructions to candidates

Economics. East Poinsett County School District

Economics East Poinsett County School District Economics: Third Quarter Strand: Economic Fundamentals Content Standard 1: Students shall examine scarcity and choice. EF.1.E.1 Explain the role scarcity

Economics East Poinsett County School District Economics: Third Quarter Strand: Economic Fundamentals Content Standard 1: Students shall examine scarcity and choice. EF.1.E.1 Explain the role scarcity

ECO201: PRINCIPLES OF MICROECONOMICS SECOND MIDTERM EXAMINATION

Name Seat Assignment ECO201: PRINCIPLES OF MICROECONOMICS SECOND MIDTERM EXAMINATION November 17, 2009 FORM 4. Directions 1. FILL IN YOUR SCANTRON WITH YOUR UNIQUE ID AND THE FORM NUMBER LISTED ON THIS

Name Seat Assignment ECO201: PRINCIPLES OF MICROECONOMICS SECOND MIDTERM EXAMINATION November 17, 2009 FORM 4. Directions 1. FILL IN YOUR SCANTRON WITH YOUR UNIQUE ID AND THE FORM NUMBER LISTED ON THIS

ECO201: PRINCIPLES OF MICROECONOMICS SECOND MIDTERM EXAMINATION

Name Seat Assignment ECO201: PRINCIPLES OF MICROECONOMICS SECOND MIDTERM EXAMINATION November 17, 2009 FORM 1. Directions 1. FILL IN YOUR SCANTRON WITH YOUR UNIQUE ID AND THE FORM NUMBER LISTED ON THIS

Name Seat Assignment ECO201: PRINCIPLES OF MICROECONOMICS SECOND MIDTERM EXAMINATION November 17, 2009 FORM 1. Directions 1. FILL IN YOUR SCANTRON WITH YOUR UNIQUE ID AND THE FORM NUMBER LISTED ON THIS

ECO201: PRINCIPLES OF MICROECONOMICS FIRST MIDTERM EXAMINATION

YOUR NAME Row Number ECO201: PRINCIPLES OF MICROECONOMICS FIRST MIDTERM EXAMINATION Prof. Bill Even Novermber 12, 2014 FORM 1 Directions 1. Fill in your scantron with your unique-id and the form number

YOUR NAME Row Number ECO201: PRINCIPLES OF MICROECONOMICS FIRST MIDTERM EXAMINATION Prof. Bill Even Novermber 12, 2014 FORM 1 Directions 1. Fill in your scantron with your unique-id and the form number

ECO201: PRINCIPLES OF MICROECONOMICS FIRST MIDTERM EXAMINATION

YOUR NAME Row Number ECO201: PRINCIPLES OF MICROECONOMICS FIRST MIDTERM EXAMINATION Prof. Bill Even Novermber 12, 2014 FORM 3 Directions 1. Fill in your scantron with your unique-id and the form number

YOUR NAME Row Number ECO201: PRINCIPLES OF MICROECONOMICS FIRST MIDTERM EXAMINATION Prof. Bill Even Novermber 12, 2014 FORM 3 Directions 1. Fill in your scantron with your unique-id and the form number

Individual & Market Demand and Supply

Mr Sydney Armstrong ECN 1100 Introduction to Microeconomic Lecture Note (3) Individual & Market Demand and Supply The tools of demand and supply can take us a far way in understanding both specific economic

Mr Sydney Armstrong ECN 1100 Introduction to Microeconomic Lecture Note (3) Individual & Market Demand and Supply The tools of demand and supply can take us a far way in understanding both specific economic

COURSE: Introduction to Business GRADE(S): 9-12

: 9-12") COURSE: Introduction to Business GRADE(S): 9-12 UNIT: Allocation of Resources TIMEFRAME: 90 Days 1 COURSE: Introduction to Business GRADE(S): 9-12 UNIT: Economic Systems TIMEFRAME: 90 Days NBEA STANDARDS:

COURSE: Introduction to Business GRADE(S): 9-12 UNIT: Allocation of Resources TIMEFRAME: 90 Days 1 COURSE: Introduction to Business GRADE(S): 9-12 UNIT: Economic Systems TIMEFRAME: 90 Days NBEA STANDARDS:

INTI COLLEGE MALAYSIA FOUNDATION IN BUSINESS INFORMATION TECHNOLOGY (CFP) ECO105: ECONOMICS 1 FINAL EXAMINATION: JANUARY 2006 SESSION

ECO105: ECONOMICS 1 FINAL EXAMINATION: JANUARY 2006 SESSION") ECO105 (F) / Page 1 of 12 Section A INTI COLLEGE MALAYSIA FOUNDATION IN BUSINESS INFORMATION TECHNOLOGY (CFP) ECO105: ECONOMICS 1 FINAL EXAMINATION: JANUARY 2006 SESSION Instructions: This section consists

ECO105 (F) / Page 1 of 12 Section A INTI COLLEGE MALAYSIA FOUNDATION IN BUSINESS INFORMATION TECHNOLOGY (CFP) ECO105: ECONOMICS 1 FINAL EXAMINATION: JANUARY 2006 SESSION Instructions: This section consists

ECON 102 Brown Final Exam (New Material) Practice Exam Solutions

Practice Exam Solutions") www.liontutors.com ECON 102 Brown Final Exam (New Material) Practice Exam Solutions 1. B A very large percent of their earnings comes from economic rent 2. B Any funds left, after everyone who has a claim

www.liontutors.com ECON 102 Brown Final Exam (New Material) Practice Exam Solutions 1. B A very large percent of their earnings comes from economic rent 2. B Any funds left, after everyone who has a claim

PRINCIPLES OF MICROECONOMICS E L E V E N T H E D I T I O N CASE FAIR OSTER. PEARSON Prepared by: Fernando Quijano w/shelly Tefft

PRINCIPLES OF MICROECONOMICS E L E V E N T H E D I T I O N CASE FAIR OSTER PEARSON Prepared by: Fernando Quijano w/shelly Tefft 2 of 25 PART III MARKET IMPERFECTIONS AND THE ROLE OF GOVERNMENT Monopoly

PRINCIPLES OF MICROECONOMICS E L E V E N T H E D I T I O N CASE FAIR OSTER PEARSON Prepared by: Fernando Quijano w/shelly Tefft 2 of 25 PART III MARKET IMPERFECTIONS AND THE ROLE OF GOVERNMENT Monopoly