ResearchFARM. EU Online Retailing 2011: Sizes and Forecasts.

|

|

|

- Curtis Horton

- 5 years ago

- Views:

Transcription

1 ResearchFARM EU Online Retailing 2011: Sizes and Forecasts

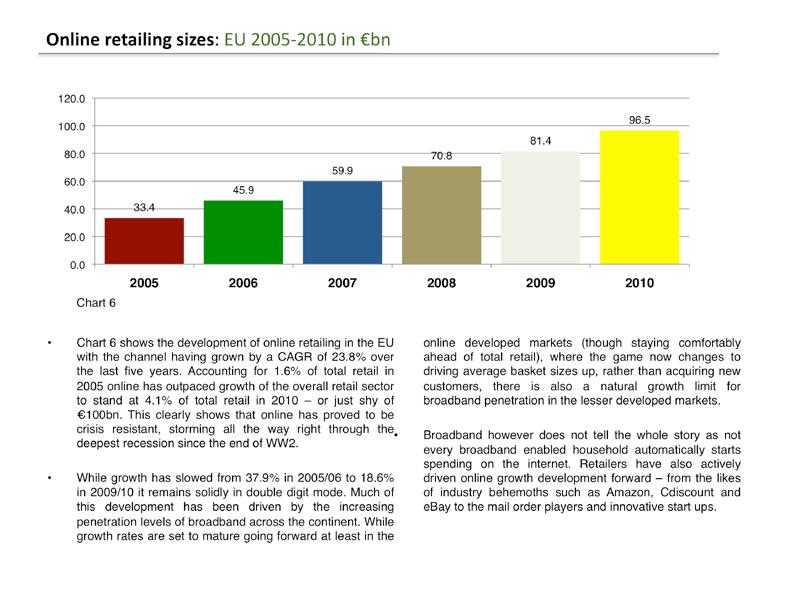

2 OVERVIEW The broad development in online retailing over the period can be characterised as moving from multichannel in 2005 to m-commerce in 2010 and towards internationalisation by As such a massive prize awaits the winning retail players, serving potential customers across the whole EU market or 126m connected households as of We forecast that this number will gently rise to 163m households over the next 5 years. While much of the historic growth of online retailing has been driven by increasing broadband penetration, the rapid growth spurt is now over. Broadband penetration rates will soon reach a natural ceiling in most of the more advanced online markets of north and western Europe. This means that retailers now have to focus on driving average basket sizes up. On top of this the competitive environment has become considerably tougher with the number of online retail businesses soaring across the EU over the last decade. Arguably, this is another reason why retailers need to think beyond the national online market and in a true paradigm change need to adopt a pan EU perspective. We expect the nature of online retailing to change significantly going forward, current cross border shopping trends are set to intensify, especially where linguistic similarities exist, so for example in France, (Walloon) Belgium and (non EU) Switzerland; Germany and Austria; Holland and (Flamish) Belgium and so on. For online retailing the future is rosy, and by 2015 we expect the retail universe to have considerably moved closer to a reality where EU shoppers order their wine, fine foods and clothes from Italy, France and Spain, their furniture from Scandinavia, DIY equipment and musical instruments from Germany and CEE, books and DVDs from the UK, etc whilst other sectors such as consumer electronics and media will become even more globalised than they currently are. Learn - which EU online markets are growth hotspots, laggards and how the sizes will have developed by 2015 Target - the most promising future markets and understand where you have to play in future to win Assess - the potential, as more EU household move online and see what sped can be tapped

3 DEFINITIONS All our data captures online retail spend on physical goods. This means that travel and tourism (airline tickets and hotel bookings which usually make up a huge share of e-commerce) as well as online financial services (insurance, banking), gambling and digital downloads of music and video content have been excluded. Also excluded have been traditional mail order sales and a share of C2C sales, stemming from the likes of ebay or priceminister, where consumers buy and sell second hand goods to other consumers. That said often these sites are now used to fulfill the online functions of dedicated retail businesses with ebay especially targeting fashion players for its boutique offering etc. As such we had to use a degree of estimation to build the data set. As a result, our sizes are significantly smaller than those reported by other market research institutes. However we feel that it is better to give a floor in terms of data and leave room for upward revisions in market size. Whilst the online market might be bigger in some instances (this also depends on definitional issues), we can say with confidence that our numbers reflect what is being spent by EU consumers in the online world today. This gives our clients the most elementary spend on physical goods online, where the buying process has involved the internet. Our forecasts are based on projected broadband connection growth correlated with a rise in average basket spend on online. Both measures are quite conservatively calculated, based on an assumption that inflation will level out around the 2% mark over the five year period, that current mail order spend will migrate to online further and that online shopping will become a lot more normal to EU consumers, especially the older generations, going forward. A key growth driver will be the value credentials the internet offers, again this not only impacts austerity hit countries, but is valid for the whole Union. Online prices are perceived to be cheaper and price comparison is much easier to carry out online than in physical stores. An allowance has also been made for m-commerce (though this is still relatively tiny in the EU) and cross border spend, which will intensify, especially as some markets are slowly maturing (UK).

4 TABLE OF CONTENTS Executive summary Market fundamentals: EU Broadband connections (000) 2009: sufficient precondition and enabler Broadband connections CAGR growth in EU27 (%): All about eastern Europe EU Retail spend per household 2010 ( ): Top 10 Retail spend per HH CAGR growth in EU27 (%): All about eastern Europe II Online sizes: Definition Online retailing sizes: EU in bn Online retailing sizes: The leading countries Online retailing sizes: EU 27, in bn p10 p15 p16 p17 p18 p19 p20 p22 p24 p25 Online retailing sizes: EU 27, growth rates, CAGR Online retailing sizes: EU 27 Top 10, 2010 in bn, CAGR (%) Online retailing sizes: EU 27, 2010 % of total retail Broadband connected household spend on online Online retailing household spend (Broadband connection): EU ( ) Broadband enabled HH spend online 2010 ( ) Top 10: Scandinavia leading the way Online spend per broadband enabled household: EU 27, in Online spend per broadband enabled HH: EU 27, growth rates, CAGR (%) Broadband enabled HH spend online 2010 ( ) 10-27: CEE and Southern Europe p26 p27 p28 p30 p31 p33 p34 p35 p36

5 TABLE OF CONTENTS Forecast Broadband penetration EU 27: 2010, % of total households Broadband penetration EU 27: 2015 forecast, % of total households, Periphery catch-up Households with a broadband connection (000): EU 27, f Households with a broadband connection: EU 27, f, growth Forecast: Broadband connected household spend on online Online retailing household spend (Broadband): EU f ( ), steady nominal gains Online spend per broadband enabled household: EU 27, f in Online spend per broadband enabled HH: EU 27, growth rates, CAGR p37 p38 p39 p40 p41 p42 p43 p45 p46 Forecasting online sizes: Definition & methodology Online retailing sizes: EU in bn Online retailing sizes: EU 27, f in bn Online retailing sizes: EU 27, f growth rates, CAGR (%) Nominal online retailing growth (%) EU 27: CEE and Southern EU on top Online retailing sizes 2015f: The leading countries, France to leapfrog the UK by 2015 The evolution of online retailing: a 15 year view Sources & further reading p47 p48 p50 p51 p52 p53 p55 p56

Chart 6: Online retailing sizes: EU 2005-2010 in bn Chart 7: Online retailing sizes: The leading countries Chart 8: Online retailing sizes: EU 27 Top 10")

6 TABLE OF CONTENTS Chart 1: Broadband connections (000) 2009 Chart 2: Broadband connections CAGR growth in EU27 (%) Chart 3: EU Retail spend per household 2010 ( ) Chart 4: Retail spend per HH Chart 5: CAGR growth in EU27 (%) Chart 6: Online retailing sizes: EU in bn Chart 7: Online retailing sizes: The leading countries Chart 8: Online retailing sizes: EU 27 Top in bn Chart 9: EU 27 Top CAGR (%) Chart 10: Online retailing household spend (Broadband connection): EU ( ) Chart 11: Broadband enabled HH spend online 2010 ( ) Top 10 Chart 12: Broadband enabled HH spend online 2010 ( ) (I) Chart 13: Broadband enabled HH spend online 2010 ( ) (II) Chart 14: Online retailing household spend (Broadband): EU f ( ) Chart 15: Online retailing sizes: EU in bn Chart 16: Nominal online retailing growth (%) EU 27 (I) Chart 17: Nominal online retailing growth (%) EU 27 (II) Chart 18: Online retailing sizes 2015f: The leading countries Chart 19: The evolution of online retailing: a 15 year view Table 1: Online retailing sizes: EU 27, in bn Table 2: Online retailing sizes: EU 27, growth rates, CAGR (%) Table 3: Online retailing sizes: EU 27, 2010 % of total retail Table 4: Online spend per broadband enabled household: EU 27, in Table 5: Online spend per broadband enabled HH: EU 27, growth rates, CAGR (%) Table 6: Broadband penetration EU 27: 2010, % of total households Table 7: Broadband penetration EU 27: 2015 forecast, % of total households Table 8: Households with a broadband connection (000): EU 27, f Table 9: Households with a broadband connection: EU 27, f, growth Table 10: Online spend per broadband enabled household: EU 27, f in Table 11: Online spend per broadband enabled HH: EU 27, growth rates, CAGR Table 12: Online retailing sizes: EU 27, f in bn Table 13: Online retailing sizes: EU 27, f growth rates, CAGR (%) p16 p17 p18 p19 p19 p22 p24 p27 p27 p31 p33 p36 p36 p43 p48 p52 p52 p53 p55 p25 p26 p28 p34 p35 p38 p39 p40 p41 p45 p46 p50 p51

![TESTIMONIALS AND CLIENTS About our last report «I found it very insightful. [...] Impressed with the amount of information that has been covered by your report.](/docs-images/83/88055119/images/7-0.jpg "» (Retail merchandising company) «I found the document easy to read, well laid out and the content thought-provoking.")

7 TESTIMONIALS AND CLIENTS About our last report «I found it very insightful. [...] Impressed with the amount of information that has been covered by your report.» (Retail merchandising company) «I found the document easy to read, well laid out and the content thought-provoking. It reminds me of the major considerations that affect our markets, and to address these key issues when approaching the global brands and retailers. Retail Predictions 2011 is a very good demonstration of the quality of how ResearchFarm operates and communicates.» (Technology supplier) «The content is very interesting to us, as we look after many of the largest shopping centres and we also represent many international retailers entering our market. There is plenty of food for thought.» (Property consultants) «It looks impressive.» (Property company) «It was helpful. It helped me to persuade my boss to take on a project about e-commerce research. I was really surprised by the importance of legal issues. I never read that elsewhere before.» (Government) «Thank you again for the study. These are very, very interesting, well explained (so, logical) predictions. Highly reliable and useful (I like the idea very much that loyalty schemes will move onto smartphones). It s quite impressive!» (Publishing group) «Great research, very useful.» (Retailer) «We have enjoyed reading your research information and have found it to be helpful in validating some of the other Grocery industry news information and predictions.» (Retailer) «On DLF s (Danish Association of Fast Moving Consumer Goods Manufacturers) New Years Conference on the 20th of January 2011 we had the great pleasure to hear ResearchFarm speak about future trends in online grocery retailing. The feed back from the conference participants was very positive as they gave Research- Farm s presentation the highest score of all speakers, finding the analysis about the key success factors of chosen EU and US online retailers both very interesting and inspiring. We can therefore give ResearchFarm our best recommendation.» Dagligvareleverandørerne Danish Association of Fast Moving Consumer Goods Manufacturers

8 OUR METHODOLOGY LAY THE GROUND FOR NEW GROWTH! Researchfarm strives to deliver a starting point for constructive discussions and provide clear solutions and direction. Our in depth observations of fundamental changes combined with our strategic insights into the sector and our entrepreneurial thinking provide unrivalled, actionable and meaningful solutions. Our recommendations will enable you to formulate new strategies, head for the right milestones, drive future growth and set the right incentives. DELIVERING ADDED VALUE THROUGH OUR REPORTS 1. ACTIONABLE RECOMMENDATIONS Our reports provide you with recommendations for each chapter to help your strategic decisions. 2. BEST PRACTICE Every chapter features a case example and in-depth insights and recommendations. 3. INTERVIEWS WITH KEY PEOPLE The report is based on in depth conversation with business leaders, CEOs and CRM specialists. ABOUT RESEARCHFARM ResearchFarm is a start up boutique focused on strategic insight and innovative topics and trends in the FMCG/retail space. A key word for us is innovation. We try to unearth what works and what doesn t and tell our audience about it. For us the client comes first, as such we are focused on the story to tell, sharing insight and analysis, not on getting our names in the media though we will engage in this as well occasionally.

9 SAMPLE PAGES SAMPLE PAGES

10 SAMPLE PAGES SAMPLE PAGES

11 HOW TO ORDER PRICE OF THIS REPORT This report is priced GBP990 (57 pages, delivered as a PDF file). VISIT OUR WEBSITE ORDER ONLINE Payment modes offered: By bank transfer When checking out, please check invoice as payment mode. We then send you an invoice. By credit/debit card Secure payment via Paypal. If you want to pay with your credit/debit card you don t need a Paypal account, just use the appropriate option when landing on the Paypal page after checking out. RECEIVE YOUR REPORT BY ResearchFarm Ltd Suite nd Floor St. John Street London EC1V 4PY (UK) CONTACT Phone +44 (0) sales@researchfarm.co.uk Web

HOW TO BUILD ON AND OFFLINE LOYALTY

ResearchFARM RETAIL ANALYSTS HOW TO BUILD ON AND OFFLINE LOYALTY Strategies series Inspiration from a number of best practice case examples from both Retail, FMCG and Foodservice in the EU/US, going beyond

ResearchFARM RETAIL ANALYSTS HOW TO BUILD ON AND OFFLINE LOYALTY Strategies series Inspiration from a number of best practice case examples from both Retail, FMCG and Foodservice in the EU/US, going beyond

ResearchFARM ONLINE RETAILING IN THE EU Strategies & Recommendations One Currency, One Market, One Channel RETAIL ANALYSTS

ResearchFARM RETAIL ANALYSTS ONLINE RETAILING IN THE EU 2011 Strategies & Recommendations One Currency, One Market, One Channel JULY 2011 WE HAVE QUESTIONS FOR YOU... Retailers What are the strategic imperatives

ResearchFARM RETAIL ANALYSTS ONLINE RETAILING IN THE EU 2011 Strategies & Recommendations One Currency, One Market, One Channel JULY 2011 WE HAVE QUESTIONS FOR YOU... Retailers What are the strategic imperatives

ResearchFARM UNITED KINGDOM ONLINE RETAILING SERIES FEBRUARY At the online retailing forefront Sizes, players, opportunities and threats

UNITED KINGDOM ONLINE RETAILING SERIES At the online retailing forefront Sizes, players, opportunities and threats FEBRUARY 2011 ResearchFARM RETAIL ANALYSTS Once again Tesco is at the cutting edge of

UNITED KINGDOM ONLINE RETAILING SERIES At the online retailing forefront Sizes, players, opportunities and threats FEBRUARY 2011 ResearchFARM RETAIL ANALYSTS Once again Tesco is at the cutting edge of

SPECIAL OFFER SUBSCRIPTION SERVICE (20+ REPORTS) 9,000. ResearchFARM. Retail Analysts. 1 YEAR SUBSCRIPTION 9,000.

9,000. ResearchFARM. Retail Analysts. 1 YEAR SUBSCRIPTION 9,000.") SPECIAL OFFER ResearchFARM www.researchfarm.co.uk SUBSCRIPTION SERVICE (20+ REPORTS) 9,000 Retail Analysts November 2015 1 YEAR SUBSCRIPTION 9,000 ENRICH YOUR STRATEGIC DECISIONS WITH CUTTING EDGE ANALYTICAL

SPECIAL OFFER ResearchFARM www.researchfarm.co.uk SUBSCRIPTION SERVICE (20+ REPORTS) 9,000 Retail Analysts November 2015 1 YEAR SUBSCRIPTION 9,000 ENRICH YOUR STRATEGIC DECISIONS WITH CUTTING EDGE ANALYTICAL

AMAZON BENCHMARK ResearchFARM

NEW REPORT AMAZON BENCHMARK ResearchFARM www.researchfarm.co.uk Retail Analysts AMAZON: CROSS COUNTRY ANALYSIS AND RANGE COMPARISON BENCHMARKING WHERE ARE CARREFOUR S STRENGTHS? WHICH PRICE AND PACKAGING

NEW REPORT AMAZON BENCHMARK ResearchFARM www.researchfarm.co.uk Retail Analysts AMAZON: CROSS COUNTRY ANALYSIS AND RANGE COMPARISON BENCHMARKING WHERE ARE CARREFOUR S STRENGTHS? WHICH PRICE AND PACKAGING

STORE OF THE FUTURE Store Design in 2010 MARCH ResearchFARM RETAIL ANALYSTS

STORE OF THE FUTURE Store Design in 2010 MARCH 2010 ResearchFARM RETAIL ANALYSTS WE HAVE 10 QUESTIONS FOR YOU... What will store designers, landlords and retailers have to look out for over the next five

STORE OF THE FUTURE Store Design in 2010 MARCH 2010 ResearchFARM RETAIL ANALYSTS WE HAVE 10 QUESTIONS FOR YOU... What will store designers, landlords and retailers have to look out for over the next five

How online retailing will transform IKEA INCLUDED:

How online retailing will transform IKEA 2013 a crucial year for strategic decision making ResearchFARM INCLUDED: Access to our online database with 500+ retail pictures February 2013 IKEA: INTRODUCTION

How online retailing will transform IKEA 2013 a crucial year for strategic decision making ResearchFARM INCLUDED: Access to our online database with 500+ retail pictures February 2013 IKEA: INTRODUCTION

Aldi - Hard discounters 2012: the winning format. ResearchFARM

Aldi - Hard discounters 2012: the winning format A completely underestimated and misunderstood business model the Anglo Saxon expansion the introduction of FMCG A brands ResearchFARM INCLUDED: Access to

Aldi - Hard discounters 2012: the winning format A completely underestimated and misunderstood business model the Anglo Saxon expansion the introduction of FMCG A brands ResearchFARM INCLUDED: Access to

The Indian Digital Traveler Research. November 2017

The Indian Digital Traveler Research November 2017 Introduction CEO foreword Travelport s Global Traveler survey is rich with insights and stories about the modern traveler. The findings demonstrate the

The Indian Digital Traveler Research November 2017 Introduction CEO foreword Travelport s Global Traveler survey is rich with insights and stories about the modern traveler. The findings demonstrate the

Changing trends in multichannel shopping and browsing preferences. October 2013

Changing trends in multichannel shopping and browsing preferences October 2013 Page 1 Overview Since June 2010, edigitalresearch and Portaltech Reply have been tracking the changes in multichannel shopping

Changing trends in multichannel shopping and browsing preferences October 2013 Page 1 Overview Since June 2010, edigitalresearch and Portaltech Reply have been tracking the changes in multichannel shopping

European Consumer Packaging Perceptions study

WWW.PROCARTON.COM PRO CARTON EUROPEAN PACKAGING PERCEPTIONS STUDY 2018 European Consumer Packaging Perceptions study An independent assessment of the importance of packaging sustainability on consumers

WWW.PROCARTON.COM PRO CARTON EUROPEAN PACKAGING PERCEPTIONS STUDY 2018 European Consumer Packaging Perceptions study An independent assessment of the importance of packaging sustainability on consumers

THE NDL GUIDE TO RUNNING SUCCESSFUL PROMOTIONS

THE NDL GUIDE TO RUNNING SUCCESSFUL PROMOTIONS At NDL, we love working with media owners, global brands and their agencies. With our expert technology, inspirational content and promotional support services,

THE NDL GUIDE TO RUNNING SUCCESSFUL PROMOTIONS At NDL, we love working with media owners, global brands and their agencies. With our expert technology, inspirational content and promotional support services,

Economic study of the consumer benefits of ebay

Economic study of the consumer benefits of ebay A REPORT PREPARED FOR EBAY September 2008 Frontier Economics Ltd, London. i Frontier Economics September 2008 Economic study of the consumer benefits of

Economic study of the consumer benefits of ebay A REPORT PREPARED FOR EBAY September 2008 Frontier Economics Ltd, London. i Frontier Economics September 2008 Economic study of the consumer benefits of

AIRPLUS. WHAT TRAVEL PAYMENT IS ALL ABOUT.

AirPlus International Travel Management Study 2014, Vol. 1 of 3. A comparison of and global travel management trends, costs and business practices. AIRPLUS. WHAT TRAVEL PAYMENT IS ALL ABOUT. About the

AirPlus International Travel Management Study 2014, Vol. 1 of 3. A comparison of and global travel management trends, costs and business practices. AIRPLUS. WHAT TRAVEL PAYMENT IS ALL ABOUT. About the

Europe Direct Selling Report 2013

9 1,42 1, Table of Contents (1 of 2) 1. MANAGEMENT SUMMARY 2. EUROPE: REGIONAL Breakdown of Global Direct Selling Revenues, by Region, incl. Europe, 2012 Breakdown of Global Direct Selling Revenues, by

9 1,42 1, Table of Contents (1 of 2) 1. MANAGEMENT SUMMARY 2. EUROPE: REGIONAL Breakdown of Global Direct Selling Revenues, by Region, incl. Europe, 2012 Breakdown of Global Direct Selling Revenues, by

Germany 2015 mobile retail trends

Germany 2015 mobile retail trends Foreword foreword With more than 51 million (94% of internet users aged 14+) digital consumers in 2014, Germany undoubtedly is in the premier league of worlds most sophisticated

Germany 2015 mobile retail trends Foreword foreword With more than 51 million (94% of internet users aged 14+) digital consumers in 2014, Germany undoubtedly is in the premier league of worlds most sophisticated

Country factsheet - February Spain

Country factsheet - February 2014 Spain The fifth largest country in Europe and the leader in southern European e-commerce without yet having reached full maturity, Spain has many characteristics which

Country factsheet - February 2014 Spain The fifth largest country in Europe and the leader in southern European e-commerce without yet having reached full maturity, Spain has many characteristics which

Use of Internet Use of Internet Services by Citizens in the EU

Use of Internet Use of Internet Services by Citizens in the EU Digital Agenda Scoreboard 2016 The Digital Economy and Society Index (DESI) is a composite index that summarises relevant indicators on Europe

Use of Internet Use of Internet Services by Citizens in the EU Digital Agenda Scoreboard 2016 The Digital Economy and Society Index (DESI) is a composite index that summarises relevant indicators on Europe

FINLAND RESULTS AND PAN-EUROPEAN COMPARISONS Alison Fennah, VP Research and Marketing, IAB Europe. Helsinki, 20 th September 2012

FINLAND RESULTS AND PAN-EUROPEAN COMPARISONS Alison Fennah, VP Research and Marketing, IAB Europe Helsinki, 20 th September 2012 Presentation Agenda 1. Introduction Background Coverage and Methodology

FINLAND RESULTS AND PAN-EUROPEAN COMPARISONS Alison Fennah, VP Research and Marketing, IAB Europe Helsinki, 20 th September 2012 Presentation Agenda 1. Introduction Background Coverage and Methodology

MOBILE FIRST MENTALITY TURNING BROWSERS INTO BUYERS

THE BEST EVENT TO MEET WITH THE RIGHT PEERS WITHIN MY INDUSTRY. MOBILE SHOPPING DELIVERS SOLUTIONS, INNOVATION AND IDEAS THAT SIMPLY CAN T BE MISSED PHILIP WARD, HEAD OF EXPERIENCE AND DEVELOPMENT, CARPHONE

THE BEST EVENT TO MEET WITH THE RIGHT PEERS WITHIN MY INDUSTRY. MOBILE SHOPPING DELIVERS SOLUTIONS, INNOVATION AND IDEAS THAT SIMPLY CAN T BE MISSED PHILIP WARD, HEAD OF EXPERIENCE AND DEVELOPMENT, CARPHONE

GO FURTHER WITH YOUR OFFICE APPS

WHITE PAPER GO FURTHER WITH YOUR OFFICE APPS A practical guide to choosing the right markets and languages 2015 Lionbridge INTRODUCTION With more than a billion users, Microsoft Office is amongst the most

WHITE PAPER GO FURTHER WITH YOUR OFFICE APPS A practical guide to choosing the right markets and languages 2015 Lionbridge INTRODUCTION With more than a billion users, Microsoft Office is amongst the most

Webrooming vs Showrooming. a report by PushON ecommerce. Delivered.

Webrooming vs Showrooming a report by PushON ecommerce. Delivered. Introduction Retail has undergone immense change in recent years, driven largely by online and mobile technology. The growth of online

Webrooming vs Showrooming a report by PushON ecommerce. Delivered. Introduction Retail has undergone immense change in recent years, driven largely by online and mobile technology. The growth of online

European Consumers Myths or Reality? Bulletin

European Consumers Myths or Reality? Bulletin June 2013 @IABEurope #Mediascope IAB Europe Research Introduction As part of its research remit, IAB Europe conducts Mediascope Europe, widely recognised as

European Consumers Myths or Reality? Bulletin June 2013 @IABEurope #Mediascope IAB Europe Research Introduction As part of its research remit, IAB Europe conducts Mediascope Europe, widely recognised as

Observatory of digital uses

Observatory of digital uses Afterbanking or new banking uses January 2019 Methodology The study was carried out using representative samples from populations in five European countries aged 15 and over.

Observatory of digital uses Afterbanking or new banking uses January 2019 Methodology The study was carried out using representative samples from populations in five European countries aged 15 and over.

North America Online Payment Methods First Half Table of Contents

4 67 900 North America Online Payment Methods 2013 - First Half 2013 Table of Contents 1. MANAGEMENT SUMMARY 2. USA (TOP COUNTRY) Mobile Payment Trends, 2012/2013 Mobile Wallet Benefits When Paying In-Store,

4 67 900 North America Online Payment Methods 2013 - First Half 2013 Table of Contents 1. MANAGEMENT SUMMARY 2. USA (TOP COUNTRY) Mobile Payment Trends, 2012/2013 Mobile Wallet Benefits When Paying In-Store,

Turkey Launch Presentation Summary #Mediascope IAB Europe Research

Turkey Launch Presentation Summary 2012 @IABEurope #Mediascope IAB Europe Research Introduction As part of its research remit, IAB Europe conducts Mediascope Europe, widely recognised as the industry standard

Turkey Launch Presentation Summary 2012 @IABEurope #Mediascope IAB Europe Research Introduction As part of its research remit, IAB Europe conducts Mediascope Europe, widely recognised as the industry standard

TARGETING LOW & HIGH INCOME CONSUMERS AT RETAIL

TARGETING LOW & HIGH INCOME CONSUMERS AT RETAIL THERE ARE MANY WAYS FOR MARKETERS TO SEGMENT THEIR AUDIENCE: Age, gender, interest and location being quite common. That said, consumer behavior weighs heavily

TARGETING LOW & HIGH INCOME CONSUMERS AT RETAIL THERE ARE MANY WAYS FOR MARKETERS TO SEGMENT THEIR AUDIENCE: Age, gender, interest and location being quite common. That said, consumer behavior weighs heavily

IMPAIRED VISION. Why some airlines, hotels, rail and car rental suppliers don t understand the true value of the indirect sales channel.

IMPAIRED VISION Why some airlines, hotels, rail and car rental suppliers don t understand the true value of the indirect sales channel. IMPARIED VISION Despite the growth in travel avoidance technology,

IMPAIRED VISION Why some airlines, hotels, rail and car rental suppliers don t understand the true value of the indirect sales channel. IMPARIED VISION Despite the growth in travel avoidance technology,

Headline Verdana Bold Holiday shopping trends survey 2018 November 2018

Headline Verdana Bold Holiday shopping trends survey 2018 November 2018 Content Key Trends 3 Consumer Perception 5 Holiday Shopping 8 Omnichannel User Experience 20 2 WHERE, WHEN, WHAT Key Trends ECONOMIC

Headline Verdana Bold Holiday shopping trends survey 2018 November 2018 Content Key Trends 3 Consumer Perception 5 Holiday Shopping 8 Omnichannel User Experience 20 2 WHERE, WHEN, WHAT Key Trends ECONOMIC

Presented By: Jack R. Salvetti, Principal S.R. Snodgrass, P.C.

Presented By: Jack R. Salvetti, Principal S.R. Snodgrass, P.C. 2018 S.R. Snodgrass, P.C. All Rights Reserved 2 3 Number of Commercial Banks (2000 2017) 9,000 8,500 8,315 8,082 8,000 7,500 7,887 7,767 7,628

Presented By: Jack R. Salvetti, Principal S.R. Snodgrass, P.C. 2018 S.R. Snodgrass, P.C. All Rights Reserved 2 3 Number of Commercial Banks (2000 2017) 9,000 8,500 8,315 8,082 8,000 7,500 7,887 7,767 7,628

The future of pharmacy is multichannel, with a fast growing digital focus.

PRESS RELEASE May 2014 SEMPORA market study: The UK retail pharmacy market 2014: consumer survey The future of pharmacy is multichannel, with a fast growing digital focus. London, 21 st May 2014 The latest

PRESS RELEASE May 2014 SEMPORA market study: The UK retail pharmacy market 2014: consumer survey The future of pharmacy is multichannel, with a fast growing digital focus. London, 21 st May 2014 The latest

OCT. 28, FBIC Global publication: 8 Buying trends to Watch This Holiday

8 Buying trends To Watch this Holiday Price Over Convenience Across the board, analysts agree that while the consumer s buying power and excitement is much stronger this holiday over last, economic concerns

8 Buying trends To Watch this Holiday Price Over Convenience Across the board, analysts agree that while the consumer s buying power and excitement is much stronger this holiday over last, economic concerns

SCALING LAND-BASED INNOVATION GROUP DECISION-MAKING TOOLKIT

SCALING LAND-BASED INNOVATION GROUP DECISION-MAKING TOOLKIT Why should I use this toolkit? Having an opportunity to expand what you do is always exciting, but as well as posing operational and financial

SCALING LAND-BASED INNOVATION GROUP DECISION-MAKING TOOLKIT Why should I use this toolkit? Having an opportunity to expand what you do is always exciting, but as well as posing operational and financial

EAS-IAAPA. «Entertainment and The Digital Industry» From here to

EAS-IAAPA «Entertainment and The Digital Industry» From here to 2020... 2 VISION MARKETING WILL NEVER BE THE SAME ANYMORE. 3 Source: Financial Times The ad model is changing dramatically 4 From a passive

EAS-IAAPA «Entertainment and The Digital Industry» From here to 2020... 2 VISION MARKETING WILL NEVER BE THE SAME ANYMORE. 3 Source: Financial Times The ad model is changing dramatically 4 From a passive

Retail Trend Monitor. THE KEY DRIVERS OF RETAIL CHANGE NOW AND NEXT Insights from GfK s Retail Trend Monitor 2017

THE KEY DRIVERS OF RETAIL CHANGE NOW AND NEXT Insights from GfK s Retail Trend Monitor 2017 TABLE OF CONTENTS 1. Introduction: The evolving retail landscape...3 2. The big retail trends: Which are driving

THE KEY DRIVERS OF RETAIL CHANGE NOW AND NEXT Insights from GfK s Retail Trend Monitor 2017 TABLE OF CONTENTS 1. Introduction: The evolving retail landscape...3 2. The big retail trends: Which are driving

Grow Revenue by Decreasing Cart Abandonment and Increasing Sale Frequency

Grow Revenue by Decreasing Cart Abandonment and Increasing Sale Frequency In 2016, ecommerce merchants lost an estimated $4.6 trillion worth of merchandise to abandoned carts, up from $4.2 trillion in

Grow Revenue by Decreasing Cart Abandonment and Increasing Sale Frequency In 2016, ecommerce merchants lost an estimated $4.6 trillion worth of merchandise to abandoned carts, up from $4.2 trillion in

Only 6 out of 10 retailers in Europe have a clear omnichannel strategy. The impact of e-commerce on the retail business

Only 6 out of 10 retailers in Europe have a clear omnichannel strategy. The impact of e-commerce on the retail business Online web store 62% 31% Online web store tablet / smartphone Physical store 82%

Only 6 out of 10 retailers in Europe have a clear omnichannel strategy. The impact of e-commerce on the retail business Online web store 62% 31% Online web store tablet / smartphone Physical store 82%

SITE INCENTIVE TRAVEL FACTBOOK 2007 Pan-European Report

SITE INCENTIVE TRAVEL FACTBOOK 2007 Pan-European Report The third Pan-European report by IMEX on incentive travel again considers the decision-making motives of programme planners, together with trends,

SITE INCENTIVE TRAVEL FACTBOOK 2007 Pan-European Report The third Pan-European report by IMEX on incentive travel again considers the decision-making motives of programme planners, together with trends,

White Paper. Clothing Playbook. Making a success of your clothing season

White Paper Clothing Playbook Making a success of your clothing season Table of Contents Table of Contents... 2 Run a Clothing Playbook... 3 Creating sales momentum in the season... 5 Stars and Dogs...

White Paper Clothing Playbook Making a success of your clothing season Table of Contents Table of Contents... 2 Run a Clothing Playbook... 3 Creating sales momentum in the season... 5 Stars and Dogs...

Four Trends Shaping the Future of Retail

Four Trends Shaping the Future of Retail Wireless Networks Are Enhancing the Shopper Experience WHITE PAPER Four Trends Shaping the Future of Retail WIRELESS NETWORKS ARE ENHANCING THE SHOPPER EXPERIENCE

Four Trends Shaping the Future of Retail Wireless Networks Are Enhancing the Shopper Experience WHITE PAPER Four Trends Shaping the Future of Retail WIRELESS NETWORKS ARE ENHANCING THE SHOPPER EXPERIENCE

Chapter 1 Introduction and main conclusions

SIDE 1 Chapter 1 Introduction and main conclusions 1.1 Introduction Consumers can help ensure more effective competition if they are active and continuously consider whether they can buy a better or cheaper

SIDE 1 Chapter 1 Introduction and main conclusions 1.1 Introduction Consumers can help ensure more effective competition if they are active and continuously consider whether they can buy a better or cheaper

Customer engagement: transforming the business in the age of the client

Customer engagement: transforming the business in the age of the client Silvia Carlassara CRM and Sales Planning, Intesa Sanpaolo Customer Experience Conference, Financial Services London, 25 October 2017

Customer engagement: transforming the business in the age of the client Silvia Carlassara CRM and Sales Planning, Intesa Sanpaolo Customer Experience Conference, Financial Services London, 25 October 2017

Five Surprises About (and Offline)

") Five Surprises About How Indians Shop Online (and Offline) By Nimisha Jain and Kanika Sanghi Digital is influencing more and more Indians shopping activities. But the important details behind that the

Five Surprises About How Indians Shop Online (and Offline) By Nimisha Jain and Kanika Sanghi Digital is influencing more and more Indians shopping activities. But the important details behind that the

A global retailer. Working with words I Sales and advertising. Starting point (%, I J H

s... (%, I J H JÊÊ Talking Learning objectives in this unit about sales and advertising Talking about obligation and permission using modal verbs Interrupting and avoiding interruption Controlling the

s... (%, I J H JÊÊ Talking Learning objectives in this unit about sales and advertising Talking about obligation and permission using modal verbs Interrupting and avoiding interruption Controlling the

accorprofile . employees countries hotels worldwide MARKET SEGMENTS AND LOCATION PRICE HOTEL CHAIN WHERE Budget Motel 6

* o Talking about competition Comparing products and companies Saying prices Comparing and choosing Case study Making a supermarket competitive Starting point 1 Do you work in a competitive industry /

* o Talking about competition Comparing products and companies Saying prices Comparing and choosing Case study Making a supermarket competitive Starting point 1 Do you work in a competitive industry /

GROCERY SHOPPING: WHAT S NEXT? CHALLENGES AND OPPORTUNITIES FOR RETAILERS AND INDUSTRY. Janaina Roque Integration Consulting

GROCERY SHOPPING: WHAT S NEXT? CHALLENGES AND OPPORTUNITIES FOR RETAILERS AND INDUSTRY Janaina Roque Integration Consulting The opportunity for growth FMCGs present very different opportunities for growth

GROCERY SHOPPING: WHAT S NEXT? CHALLENGES AND OPPORTUNITIES FOR RETAILERS AND INDUSTRY Janaina Roque Integration Consulting The opportunity for growth FMCGs present very different opportunities for growth

Americas retail report

Americas retail report Redefining loyalty for retail June 2015 Redefining loyalty for retail Today, American consumers have more shopping choices than ever before. They have access to more diverse retailers

Americas retail report Redefining loyalty for retail June 2015 Redefining loyalty for retail Today, American consumers have more shopping choices than ever before. They have access to more diverse retailers

Shifting Environment From a Focus on Products to Customer Centricity

Shifting Environment From a Focus on Products to Customer Centricity Contents Section 1: Affinity Marketing Section 2: Customer Centricity: A Differentiating Factor Section 3: Customer Centricity in Bancassurance

Shifting Environment From a Focus on Products to Customer Centricity Contents Section 1: Affinity Marketing Section 2: Customer Centricity: A Differentiating Factor Section 3: Customer Centricity in Bancassurance

Global Retail Trends & the 10 fastest growing markets, 2011 By Marc Hubbard, VP North America Planet Retail Ltd June

Global Retail Trends & the 10 fastest growing markets, 2011 By Marc Hubbard, VP North America Planet Retail Ltd June 14 2011 part of Contents 1. Introduction 2. Retail Trends in 2011 3. The 10 Fastest

Global Retail Trends & the 10 fastest growing markets, 2011 By Marc Hubbard, VP North America Planet Retail Ltd June 14 2011 part of Contents 1. Introduction 2. Retail Trends in 2011 3. The 10 Fastest

The Smart Way Suggested products to buy online Most of us have made a purchase online. Whether you have or not, this topic provides tips to guide you during your next online purchase. An item that might

The Smart Way Suggested products to buy online Most of us have made a purchase online. Whether you have or not, this topic provides tips to guide you during your next online purchase. An item that might

NO CASH SUMMER survey

NO CASH SUMMER survey Cash and usage of European consumers at home and on holiday Thierry Meerschaert (thierry.meerschaert@insites-consulting.com) Frederico Goncalves (frederico.goncalves@insites-consulting.com)

NO CASH SUMMER survey Cash and usage of European consumers at home and on holiday Thierry Meerschaert (thierry.meerschaert@insites-consulting.com) Frederico Goncalves (frederico.goncalves@insites-consulting.com)

NISA RETAIL Nick Read, CEO

NISA RETAIL Nick Read, CEO Collective Purchasing WHERE DID NISA COME FROM? WHERE DID NISA COME FROM? WHERE DID NISA COME FROM? Nisa was designed to provide benefits to independent retailers At the core

NISA RETAIL Nick Read, CEO Collective Purchasing WHERE DID NISA COME FROM? WHERE DID NISA COME FROM? WHERE DID NISA COME FROM? Nisa was designed to provide benefits to independent retailers At the core

The Importance of Sustainability in Packaging:

The Importance of Sustainability in Packaging: Major brand owners and retailers in 5 key European markets speak up PACKAGING FOR Pro Carton & Smithers Pira Sustainability Study An independent assessment

The Importance of Sustainability in Packaging: Major brand owners and retailers in 5 key European markets speak up PACKAGING FOR Pro Carton & Smithers Pira Sustainability Study An independent assessment

A closer look at Online Travel Agencies challenges

2010 Amadeus IT Group SA Brighter, Bolder, Better IT Solutions A closer look at Online Travel Agencies challenges Сергей Разарёнов «Амадеус информационные технологии» Москва, 09 декабря 2010 1 Business

2010 Amadeus IT Group SA Brighter, Bolder, Better IT Solutions A closer look at Online Travel Agencies challenges Сергей Разарёнов «Амадеус информационные технологии» Москва, 09 декабря 2010 1 Business

WORKING FOR OUR BRAND

WORKING FOR OUR BRAND WELCOME TO OUR WOW FACTORS I AM DELIGHTED TO INTRODUCE RIVER ISLAND S EMPLOYER BRAND WOW FACTORS. AS A COMPANY, WE CONTINUE TO DEVELOP IN ALL SORTS OF NEW AREAS, BENEFITING FROM

WORKING FOR OUR BRAND WELCOME TO OUR WOW FACTORS I AM DELIGHTED TO INTRODUCE RIVER ISLAND S EMPLOYER BRAND WOW FACTORS. AS A COMPANY, WE CONTINUE TO DEVELOP IN ALL SORTS OF NEW AREAS, BENEFITING FROM

Alfred Griffioen. Doing business in Europe

Alfred Griffioen Doing business in Europe 2 Alliance experts is a global network of business development specialists We help companies to enter new markets profitably Choose your export country Start selling

Alfred Griffioen Doing business in Europe 2 Alliance experts is a global network of business development specialists We help companies to enter new markets profitably Choose your export country Start selling

KROGER AND PERSONALIZATION: A GROCERY RETAILER BECOMING A MEDIA PLAYER?

KROGER AND PERSONALIZATION: A GROCERY RETAILER BECOMING A MEDIA PLAYER? 2018 KROGER ALWAYS STARTS WITH THE CUSTOMER 2,800 STORES IN 35 STATES 60MM+ Households 1 OUT OF 2 HOUSEHOLDS IN THE US Confidential

KROGER AND PERSONALIZATION: A GROCERY RETAILER BECOMING A MEDIA PLAYER? 2018 KROGER ALWAYS STARTS WITH THE CUSTOMER 2,800 STORES IN 35 STATES 60MM+ Households 1 OUT OF 2 HOUSEHOLDS IN THE US Confidential

Creating Compelling Retail Experiences

EBOOK Creating Compelling Retail Experiences with Movable Ink + Oracle Marketing Cloud The Amazon Effect It s no secret that retail is undergoing a massive transformation. Everything from the in-store

EBOOK Creating Compelling Retail Experiences with Movable Ink + Oracle Marketing Cloud The Amazon Effect It s no secret that retail is undergoing a massive transformation. Everything from the in-store

Meaning and Definition

Meaning and Definition For a common man e-commerce is known as buying and selling of products and services over internet. E commerce in its simplest form can be defined as the application of computer and

Meaning and Definition For a common man e-commerce is known as buying and selling of products and services over internet. E commerce in its simplest form can be defined as the application of computer and

Payment Methods: What International Consumers Want, Need and Expect

Payment Methods: What International Consumers Want, Need and Expect By First Data and Market Strategies International 2011 First Data Corporation. All trademarks, service marks and trade names referenced

Payment Methods: What International Consumers Want, Need and Expect By First Data and Market Strategies International 2011 First Data Corporation. All trademarks, service marks and trade names referenced

Christmas survey 2017 What will Christmas have in store for Belgians this year?

Christmas survey 2017 What will Christmas have in store for Belgians this year? Christmas survey 2017 What will Christmas have in store for Belgians this year? Belgians spend less online compared to Europeans

Christmas survey 2017 What will Christmas have in store for Belgians this year? Christmas survey 2017 What will Christmas have in store for Belgians this year? Belgians spend less online compared to Europeans

Global Content Strategy

Global Content Strategy Cerner Transforms Content into an International Sales Asset Client: Cerner Corporation / Industries: Health, Technology content-science.com contentwrx.com review.content-science.com

Global Content Strategy Cerner Transforms Content into an International Sales Asset Client: Cerner Corporation / Industries: Health, Technology content-science.com contentwrx.com review.content-science.com

Sensis e-business Report

September 2010 Sensis e-business Report The Online Experience of Small and Medium Enterprises Table of Contents INTRODUCTION... 1 ABOUT THE SURVEY... 2 EXECUTIVE SUMMARY... 4 LEVELS OF COMPUTER OWNERSHIP...

September 2010 Sensis e-business Report The Online Experience of Small and Medium Enterprises Table of Contents INTRODUCTION... 1 ABOUT THE SURVEY... 2 EXECUTIVE SUMMARY... 4 LEVELS OF COMPUTER OWNERSHIP...

Mobile Shopping. November Copyright 2012 Lightspeed Research. Proprietary Information. All Rights Reserved.

Mobile Shopping November 2012 1 About the survey The survey was conducted on Lightspeed Research's UK online panel in November 2012. There were 2744 respondents to the initial part of the survey, all of

Mobile Shopping November 2012 1 About the survey The survey was conducted on Lightspeed Research's UK online panel in November 2012. There were 2744 respondents to the initial part of the survey, all of

SAVVY CROSS BORDER SHOPPERS: HOW TO SELL TO CUSTOMERS IN CANADA

SAVVY CROSS BORDER SHOPPERS: HOW TO SELL TO CUSTOMERS IN CANADA INTRODUCTION At Flow, we want to make it as easy as possible for retailers and brands to engage in cross border e-commerce. Each installment

SAVVY CROSS BORDER SHOPPERS: HOW TO SELL TO CUSTOMERS IN CANADA INTRODUCTION At Flow, we want to make it as easy as possible for retailers and brands to engage in cross border e-commerce. Each installment

Topic 5 - Customer Care. Higher Administration & IT

Topic 5 - Customer Care Higher Administration & IT 1 Learning Intentions / Success Criteria Learning Intentions Customer Care Success Criteria By end of this topic you will be able to describe the following

Topic 5 - Customer Care Higher Administration & IT 1 Learning Intentions / Success Criteria Learning Intentions Customer Care Success Criteria By end of this topic you will be able to describe the following

GLOBAL B2B E-COMMERCE MARKET 2018

PUBLICATION DATE: SEPTEMBER 2018 PAGE 2 GENERAL INFORMATION I PAGE 3 KEY FINDINGS I PAGE 4-7 TABLE OF CONTENTS I PAGE 8 REPORT-SPECIFIC SAMPLE CHARTS I PAGE 9 METHODOLOGY I PAGE 10 RELATED REPORTS I PAGE

PUBLICATION DATE: SEPTEMBER 2018 PAGE 2 GENERAL INFORMATION I PAGE 3 KEY FINDINGS I PAGE 4-7 TABLE OF CONTENTS I PAGE 8 REPORT-SPECIFIC SAMPLE CHARTS I PAGE 9 METHODOLOGY I PAGE 10 RELATED REPORTS I PAGE

Our aim is not to be the biggest, but to be the best supplier of Java skilled professionals in

Our aim is not to be the biggest, but to be the best supplier of Java skilled professionals in Europe Why use J people? J People is a team of honest, positive, well-balanced and successful people who operate

Our aim is not to be the biggest, but to be the best supplier of Java skilled professionals in Europe Why use J people? J People is a team of honest, positive, well-balanced and successful people who operate

BA (Hons) Communication. Cohort: BAHC/15B/FT. Examinations for 2017/2018 Semester II. & 2018 Semester I

Communication. Cohort: BAHC/15B/FT. Examinations for 2017/2018 Semester II. & 2018 Semester I") BA (Hons) Communication Cohort: BAHC/15B/FT Examinations for 2017/2018 Semester II & 2018 Semester I MODULE: CUSTOMER RELATIONSHIP MANAGEMENT MODULE CODE: SMKG 3408B Duration: 2 Hours and 15 Minutes Instructions

BA (Hons) Communication Cohort: BAHC/15B/FT Examinations for 2017/2018 Semester II & 2018 Semester I MODULE: CUSTOMER RELATIONSHIP MANAGEMENT MODULE CODE: SMKG 3408B Duration: 2 Hours and 15 Minutes Instructions

Holiday Optimization Guide 2013

Holiday Optimization Guide 2013 Contents Yahoo! Bing Network Drives Value for the Retail Industry Audience Insights in Retail Category Optimization Strategies and Timelines Must-Haves for the Holiday Audience

Holiday Optimization Guide 2013 Contents Yahoo! Bing Network Drives Value for the Retail Industry Audience Insights in Retail Category Optimization Strategies and Timelines Must-Haves for the Holiday Audience

FOCUS ON SOCIAL MEDIA

FOCUS ON SOCIAL MEDIA THIS IS FOR FINANCIAL ADVISER USE ONLY AND SHOULDN T BE RELIED UPON BY ANY OTHER PERSON. INTRODUCTION The purpose of this guide is to help you develop your social media presence.

FOCUS ON SOCIAL MEDIA THIS IS FOR FINANCIAL ADVISER USE ONLY AND SHOULDN T BE RELIED UPON BY ANY OTHER PERSON. INTRODUCTION The purpose of this guide is to help you develop your social media presence.

LATAM. This is a format that will become of increasing significance to brands.

Once a channel purely for trade customers, Cash & Carry (C&C) stores are now selling directly to 46 million households across Latin America. End consumers are increasingly choosing to shop there, with

Once a channel purely for trade customers, Cash & Carry (C&C) stores are now selling directly to 46 million households across Latin America. End consumers are increasingly choosing to shop there, with

12 reasons to place your business travel in our hands

12 reasons to place your business travel in our hands #1 We re your complete travel solution Despite an incredibly vague, but desperately urgent travel requirement from my customer, you managed to do an

12 reasons to place your business travel in our hands #1 We re your complete travel solution Despite an incredibly vague, but desperately urgent travel requirement from my customer, you managed to do an

Juan Carlos. García. General Director Amazon Mexico. "Our obsession is metrics"

Juan Carlos García General Director Amazon Mexico "Our obsession is metrics" He started out as an e-commerce entrepreneur and is one of the pioneers of this platform when many did not believe in it. Today

Juan Carlos García General Director Amazon Mexico "Our obsession is metrics" He started out as an e-commerce entrepreneur and is one of the pioneers of this platform when many did not believe in it. Today

Digital Shopper Relevancy

Consumer Products and Retail the way we see it Digital Shopper Relevancy Profiting from Your Customers Desired All-Channel Experience Contents Introduction 3 Executive Summary 4 The Many Faces of the Digital

Consumer Products and Retail the way we see it Digital Shopper Relevancy Profiting from Your Customers Desired All-Channel Experience Contents Introduction 3 Executive Summary 4 The Many Faces of the Digital

The 10 Big Mistakes People Make When Running Customer Surveys

The 10 Big Mistakes People Make When Running Customer Surveys If you want to understand what drives customer loyalty for your business and how to align your business to improve customer loyalty, Genroe

The 10 Big Mistakes People Make When Running Customer Surveys If you want to understand what drives customer loyalty for your business and how to align your business to improve customer loyalty, Genroe

AN EXCERPT FROM: The Loyalty Connection: Secrets To Customer Retention And Increased Profits

AN EXCERPT FROM: The Loyalty Connection: Secrets To Customer Retention And Increased Profits By Bob Thompson CEO, CustomerThink Corporation Founder, CRMGuru.com March 2005 Compliments of Copyright 2005

AN EXCERPT FROM: The Loyalty Connection: Secrets To Customer Retention And Increased Profits By Bob Thompson CEO, CustomerThink Corporation Founder, CRMGuru.com March 2005 Compliments of Copyright 2005

YOUTH ODYSSEY. Page 1

2014 YOUTH ODYSSEY Page 1 2014 Youth Odyssey is a study that focuses on youths aged 15 21, a group that represents 6.1 million people in Great Britain (source: GB TGI). This is a time of change in the

2014 YOUTH ODYSSEY Page 1 2014 Youth Odyssey is a study that focuses on youths aged 15 21, a group that represents 6.1 million people in Great Britain (source: GB TGI). This is a time of change in the

Achieving i total t retail

www.pwc.com Achieving i total t retail Consumer expectations driving the next retail business model January, 2014 Jeff Holmes PwC Retail & Consumer Managing Director Contents Hypothetical case study discussion

www.pwc.com Achieving i total t retail Consumer expectations driving the next retail business model January, 2014 Jeff Holmes PwC Retail & Consumer Managing Director Contents Hypothetical case study discussion

Priorities for Digital Measurement. Report. WHITE PAPER September Five Practical Steps to help companies comply with the E-Privacy Directive

WHITE PAPER September 2017 Five Practical Steps to help companies comply with the E-Privacy Directive Priorities for Digital Measurement Report Date goes here CONTENT 3 Executive Summary 5 Introduction

WHITE PAPER September 2017 Five Practical Steps to help companies comply with the E-Privacy Directive Priorities for Digital Measurement Report Date goes here CONTENT 3 Executive Summary 5 Introduction

Always On: Out of Home Lives 2014

Always On: Out of Home Lives 2014 FEPE Conference, Vienna 5 June 2014 Aims and questions In a world of increasingly Mobile Living, how is Out of Home influencing people? Where does it now sit in the media

Always On: Out of Home Lives 2014 FEPE Conference, Vienna 5 June 2014 Aims and questions In a world of increasingly Mobile Living, how is Out of Home influencing people? Where does it now sit in the media

Sensis e-business Report

August 2005 Sensis e- Report The Online Experience of Small and Medium Enterprises Table of Contents Introduction... 1 About the surveys... 2 Executive summary... 4 Levels of computerisation... 6 Equipment

August 2005 Sensis e- Report The Online Experience of Small and Medium Enterprises Table of Contents Introduction... 1 About the surveys... 2 Executive summary... 4 Levels of computerisation... 6 Equipment

Maine Online Global IBT Online Website Localization and International Online Marketing for Exports

Maine Online Global IBT Online Website Localization and International Online Marketing for Exports 1 Introduction April 2017 Go Global with Website Localization and International Online Marketing! Presented

Maine Online Global IBT Online Website Localization and International Online Marketing for Exports 1 Introduction April 2017 Go Global with Website Localization and International Online Marketing! Presented

The Auto Dealer s Guide to Digital Retailing

The Auto Dealer s Guide to Digital Retailing TABLE OF CONTENTS The Digital Retailing Evolution pg. 4 Consumer Expectations pg. 6 Dealer Expectations pg. 8 Consumers Still Want to Visit Dealerships pg.

The Auto Dealer s Guide to Digital Retailing TABLE OF CONTENTS The Digital Retailing Evolution pg. 4 Consumer Expectations pg. 6 Dealer Expectations pg. 8 Consumers Still Want to Visit Dealerships pg.

CREATING YOUR 90-DAY PLAN PARTICIPANT WORKBOOK IT IS IN YOUR POWER TO BRING YOUR MOST SUCCESSFUL IDEAS TO LIFE

CREATING YOUR 90-DAY PLAN KEY STRATEGIES TO MEET YOUR GOALS AND EXCEED YOUR EXPECTATIONS PARTICIPANT WORKBOOK IT IS IN YOUR POWER TO BRING YOUR MOST SUCCESSFUL IDEAS TO LIFE CANADA AUSTRALIA THE WORLD

CREATING YOUR 90-DAY PLAN KEY STRATEGIES TO MEET YOUR GOALS AND EXCEED YOUR EXPECTATIONS PARTICIPANT WORKBOOK IT IS IN YOUR POWER TO BRING YOUR MOST SUCCESSFUL IDEAS TO LIFE CANADA AUSTRALIA THE WORLD

ResearchFARM. Convenience store 2020 Centre of the local ecosystem

Convenience store 2020 Centre of e local ecosystem The grow opportunity in establishing a hub protecting e investment into physical locations ResearchFARM INCLUDED: Access to our online database wi 500+

Convenience store 2020 Centre of e local ecosystem The grow opportunity in establishing a hub protecting e investment into physical locations ResearchFARM INCLUDED: Access to our online database wi 500+

ECC-Net statistics 1 regarding e-commerce

ECC-Net statistics 1 regarding e-commerce 2012-2013 The European Consumer Centre Network The European Consumer Centre Network (ECC-Net) consists of 30 centres based in each EU Member State, Norway and

ECC-Net statistics 1 regarding e-commerce 2012-2013 The European Consumer Centre Network The European Consumer Centre Network (ECC-Net) consists of 30 centres based in each EU Member State, Norway and

PLANNING FOR CHANGING CONSUMER CONFIDENCE

PLANNING FOR CHANGING CONSUMER CONFIDENCE TODAY S HIGH STREET A recent Guardian poll found that 91% of people thought more retailers would go bust as a result of falling consumer confidence Dixons saw

PLANNING FOR CHANGING CONSUMER CONFIDENCE TODAY S HIGH STREET A recent Guardian poll found that 91% of people thought more retailers would go bust as a result of falling consumer confidence Dixons saw

LOYALTY PROGRAMS THAT GO BEYOND REWARDS. How to understand your customers and keep them coming back

LOYALTY PROGRAMS THAT GO BEYOND REWARDS How to understand your customers and keep them coming back TABLE OF CONTENTS 1. WELCOME TO THE WORLD OF LOYALTY PROGRAMS... 2. A BIT OF HISTORY... 3. LOYALTY PROGRAM

LOYALTY PROGRAMS THAT GO BEYOND REWARDS How to understand your customers and keep them coming back TABLE OF CONTENTS 1. WELCOME TO THE WORLD OF LOYALTY PROGRAMS... 2. A BIT OF HISTORY... 3. LOYALTY PROGRAM

x A deep dive into buy-side attitudes and adoption

Attitudes towards Programmatic Advertising x A deep dive into buy-side attitudes and adoption September 2016 CONTENT Introduction Summary Programmatic is mainstream x Drivers, Barriers and Business Impacts

Attitudes towards Programmatic Advertising x A deep dive into buy-side attitudes and adoption September 2016 CONTENT Introduction Summary Programmatic is mainstream x Drivers, Barriers and Business Impacts

Consumer Insights into the U.S. Gift Card Market: 2011

Consumer Insights into the U.S. Gift Card Market: 2011 By First Data and Market Strategies International 2011 First Data Corporation. All trademarks, service marks and trade names referenced in this material

Consumer Insights into the U.S. Gift Card Market: 2011 By First Data and Market Strategies International 2011 First Data Corporation. All trademarks, service marks and trade names referenced in this material

octave A simple overview digital Digital Marketing Guide

Digital Marketing Guide A simple overview A brief introduction Contents 1.0 Introduction 2.0 Changing Media 2.1 Internet Usage 2.2 User activity online 2.3 Social Media 2.4 Mobile 2.5 Ecommerce - Impact

Digital Marketing Guide A simple overview A brief introduction Contents 1.0 Introduction 2.0 Changing Media 2.1 Internet Usage 2.2 User activity online 2.3 Social Media 2.4 Mobile 2.5 Ecommerce - Impact

Hi, I am Saša Djunisijević, Founder of The Whiteboarder. Years

Hi, I am Saša Djunisijević, Founder of The Whiteboarder. Years of dealing with the most demanding small, mid-sized and large companies helped me to form excellent understanding of different businesses.

Hi, I am Saša Djunisijević, Founder of The Whiteboarder. Years of dealing with the most demanding small, mid-sized and large companies helped me to form excellent understanding of different businesses.

Home Textiles. Trade Route & Competitive Forces in the European Market

Home Textiles Trade Route & Competitive Forces in the Market The nature of trade in home textiles is set to keep changing in the near future. The market is becoming increasingly globalised, resulting in

Home Textiles Trade Route & Competitive Forces in the Market The nature of trade in home textiles is set to keep changing in the near future. The market is becoming increasingly globalised, resulting in

FREQUENTLY ASKED QUESTIONS STUDENT UNIONS

FREQUENTLY STUDENT UNIONS PRODUCT OVERVIEW What is TOTUM? TOTUM is a brand new digital platform that replaces NUS extra and builds on the brand s success. We know. We re a little late to the digital party.

FREQUENTLY STUDENT UNIONS PRODUCT OVERVIEW What is TOTUM? TOTUM is a brand new digital platform that replaces NUS extra and builds on the brand s success. We know. We re a little late to the digital party.

Maksim Grishakov. Yandex.Market Beru Bringly

Maksim Grishakov Yandex.Market Beru Bringly Yandex Market (JV) Ecosystem and its elements Domestic e-commerce marketplace with 1P and 3P sales, along 15 product categories for basket shopping Yandex Market

Maksim Grishakov Yandex.Market Beru Bringly Yandex Market (JV) Ecosystem and its elements Domestic e-commerce marketplace with 1P and 3P sales, along 15 product categories for basket shopping Yandex Market

Includes proprietary Amazon Grocery shopper survey results about purchasing intent of Amazon branded private label products

Amazon 2013: Online Grocery New solutions on the horizon How to cooperate as a FMCG player & what to consider Includes proprietary Amazon Grocery shopper survey results about purchasing intent of Amazon

Amazon 2013: Online Grocery New solutions on the horizon How to cooperate as a FMCG player & what to consider Includes proprietary Amazon Grocery shopper survey results about purchasing intent of Amazon

Creating a > experience through mobility

Creating a > experience through mobility By really understanding who is shopping in their stores, how they shop and how mobile influences their shopping behaviors, retailers can respond with mobile shopping,

Creating a > experience through mobility By really understanding who is shopping in their stores, how they shop and how mobile influences their shopping behaviors, retailers can respond with mobile shopping,

Putra Business School. GSM 5170 Management Information System. Dr. Rusli Haji Abdullah

Putra Business School GSM 5170 Management Information System Dr. Rusli Haji Abdullah Lecture 4 Case Study 1: When you re Big, You can be your Own B2B E-Marketplace Case Study 2: The mobile commerce explosion

Putra Business School GSM 5170 Management Information System Dr. Rusli Haji Abdullah Lecture 4 Case Study 1: When you re Big, You can be your Own B2B E-Marketplace Case Study 2: The mobile commerce explosion

THE FUTURE OF SHOPPER MARKETING. janeperry

THE FUTURE OF SHOPPER MARKETING janeperry Intro Macro factors affecting shoppers Changing shopper behaviours and implications What does it all mean for brands and retailers? FORCES SHAPING SHOPPER 85%

THE FUTURE OF SHOPPER MARKETING janeperry Intro Macro factors affecting shoppers Changing shopper behaviours and implications What does it all mean for brands and retailers? FORCES SHAPING SHOPPER 85%