A New Representative Standard for Online Research

|

|

|

- Caitlin Walters

- 5 years ago

- Views:

Transcription

1

2 A New Representative Standard for Online Research Conquering the Challenge of the Dirty Little R Word Steve Gittelman President Mktg, Inc. Jeff Welch President Opinionology

3 Online Respondents: A Congestible Resource Demand for online respondents outstrips easily available online resources COMBAT FISHING

4 Mixing as an Operational Fix Mixing solves the operational constraints, but each cookie can have a unique taste

5 Mixing samples is more difficult than mixing cookies

6 Blending Creates Online Consistency How does blending differ from mixing? To blend is to mix so that the parts are no longer distinct

7 A blend is Consistent Demographics are not enough Blending variables must explain variance in data Grounded With standards we move closer to creating representative samples Multi mode based standards grounded in science may make a more cogent argument

8 Evaluating A Blend Is the model efficacious? Is the model adequately operationalized technically to be economical and scalable?

9 The Test: A Brave New World A three way comparison hosted by Phoenix Marketing International using the base wave of their Consumer Payments Study (CPS). Three companies completed independent samples: 1. Panel A using traditional sampling methods 2500 interviews. 2. GMI using Pinnacle 1000 interviews. 3. Mktg, Inc. using RealID behaviorally balanced sample provided by Opinionology 2000 interviews.

10 Phoenix Marketing International (PMI) Consumer Payments Study: Quota Completion

11 PMI Consumer Payments Study: Survey Metrics of Interest (Metrics provided by PMI)

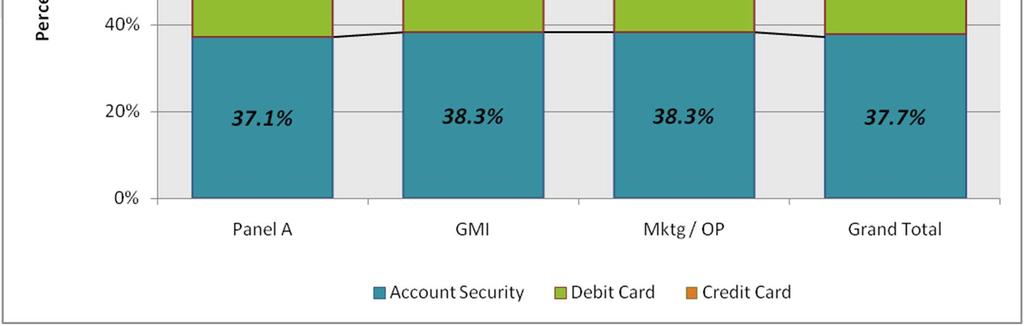

12 The following questions were used in a segmentation analysis: Over the next three years, I will use my debit card more and my credit card less often If a merchant offered me a discount or reward for using a certain payment type, I would be more likely to use that type of payment I understand the differences between a PIN-based and a signature-based debit card transaction I would be more inclined to deposit checks at ATMs if I could get a printed image of my checks as a receipt I would rather use an ATM at the bank branch office than wait in line to see a bank teller I feel that it is safe to transact online (shopping or banking online) I would pay more bills electronically if I could pay with my debit card I would pay more bills electronically if I could pay with my credit card I am willing to pay a $5 fee to make an instant payment by telephone to avoid being late for some bill payments I would use a prepaid card to pay some bills if it were easy to use and my providers accepted it I would use a prepaid card (not connected to my bank or card accounts) for Internet purchases if most merchants accepted it I would like to have an anonymous payment method for buying digital items online (paying for music, video, news, etc. from a preloaded account, and not revealing my identity) I am willing to pay a one-time fee of about $6 to purchase a re-loadable pre-paid gift card that can be used at any merchant If my bank offered it, I would use a person-to-person payment service that lets me easily send money to others from my bank account If I used a person-to-person payment service, I would prefer using a cell phone to using a computer to send the money from my account I have strong concerns about using my cell phone to make purchases if the payment is connected to my credit card account I have strong concerns about using my cell phone to make purchases if the payment is connected to my checking or savings account I am willing to use a secure store fingerprint system that lets me pay without having to show my card or check I am willing to use a card or device, connected to my credit card account, where the payment is activated by waving it near or tapping it on a payment terminal rather than swiping it through a terminal I am willing to use a card or device, connected to my bank (debit card/checking/savings) account, where the payment is activated by waving it near or tapping it on a payment terminal rather than swiping it through a terminal If a merchant gave me a 2% discount for using cash, I would use cash for that purchase instead of a debit card or credit card.

13 PMI Consumer Payments Study: Segmentations Overall

14 PMI Consumer Payments Study: Segmentations Within A Demographic Cell

15 PMI Consumer Payments Study: Segmentations Within A Demographic Cell

16 PMI Consumer Payments Study: Segmentations Within A Demographic Cell

17 PMI Consumer Payments Study: Segmentations Within A Demographic Cell

18 PMI Consumer Payments Study: Segmentations Within A Demographic Cell

19 PMI Consumer Payments Study: Segmentations Within A Demographic Cell

20 PMI Consumer Payments Study: Segmentations Within A Demographic Cell

21 PMI Consumer Payments Study: Aggregate Data Against Non Quota Controlled Benchmarks (CPS Dec. 2010)

22 PMI Consumer Payment Study: Average of Within Cell Deviations Against Non Quota Controlled Benchmarks

23 PMI Consumer Payments Study: Average Deviation Against Non Quota Controlled Benchmarks

24 PMI Consumer Payments Study: Average Deviation Against Non Quota Controlled Benchmarks

25 PMI Consumer Payment Study: Average Deviation Against Non Quota Controlled Benchmarks

26 PMI Consumer Payments Study: Average Deviation Against Non Quota Controlled Benchmarks

27 PMI Consumer Payments Study: Average Deviation Against Non Quota Controlled Benchmarks

28 PMI Consumer Payments Study: Average Deviation Against Non Quota Controlled Benchmarks

29 PMI Consumer Payments Study: Average Deviation Against Non Quota Controlled Benchmarks

30 PMI Consumer Payments Study: Average Deviation Against Non Quota Controlled Benchmarks

31 PMI Consumer Payments Study: Average Deviation Against Non Quota Controlled Benchmarks

32 PMI Consumer Payments Study: Respondent Quality

33 How does RealID work? Standard Questionnaire thirteen minutes in length. All respondents are pre profiled. Generates ten segmentations Buying Behavior (37 variables), Sociographics (31 variables), Media (31 variables) plus seven market segmentations: package goods, small electronic devices, banking, etc. Creates a behavioral fingerprint.

34 The Grand Mean: Creating the standard with different modes using the same profiling questionnaire

35 The Grand Mean: Mode Optimization (Three sources: CPS, Nielsen, Pew)

36 The Grand Mean: Mode Blending Optimization Outcome

37 Real ID Method: Mid Survey Tracking & Correction Buying Behavior

Profile Exchange Mid Study Correction (Patent Pending) Engagement by Qmetrics Hyperactivity Score Additional Data basing points")

38 RealID Respondent Stage 1 Digital Fingerprinting Sample Metrics Verification Score Consistency Longitudinal Consistency of Respondents (Patent Pending) Stage 2 The Grand Mean Project Profiling Questionnaire Segmentations Micro Behavioral Profiling (Patent pending) Profile Exchange Mid Study Correction (Patent Pending) Engagement by Qmetrics Hyperactivity Score Additional Data basing points Accutrac Respondent Accuracy Metric Grand Mean Segmentations

39

40 Questions? Steve Gittelman, Ph. D Office #: Cell #: Steve@mktginc.com Jeff Welch Office #: Cell #: jwelch@opinionology.com Thank you!