CA Final, Paper 5, Advanced management Accounting, Chapter 1 Developments in Business Environment :Part 3. CA. Anurag Singal B.Com(H), ACA.

|

|

|

- Alfred Tate

- 5 years ago

- Views:

Transcription

1 CA Final, Paper 5, Advanced management Accounting, Chapter 1 Developments in Business Environment :Part 3 CA. Anurag Singal B.Com(H), ACA.

2 Understand the concept of Target Costing Understand the concept of Kaizen Costing 2

3 In target costing, a business starts by determining how much it wants to charge for a product. It then subtracts its desired profit from that price to arrive at the maximum cost it can afford to pay to produce that product. Target Costing is a tool, and comprehensive process, that dramatically improves an organization's capability to reduce costs and improve the bottom line. 3

4 Determine price point for approximate feature/benefit combination Price Target profit = Target Cost Iterate design trade off until target cost is hit Revalidate price point given revised design 4

5 Ensures proper planning well ahead of actual production and marketing Minimize non-value added activities Enhances employee awareness and empowerment Reduced time to market 5

6 Value Engineering Searching opportunities to modify the design of each component or part of a product to reduce cost without reducing functionality/quality of product. Value Analysis Studying the production activities to detect the non-value adding activities that may be eliminated to save costs without reducing functionality/quality of product. 6

7 Can we eliminate functions from the production process? Can we eliminate some durability or reliability? Can we minimize the design? Can we design the product better? Can we substitute parts? Can we combine steps? Can we Take supplier s assistance? 7

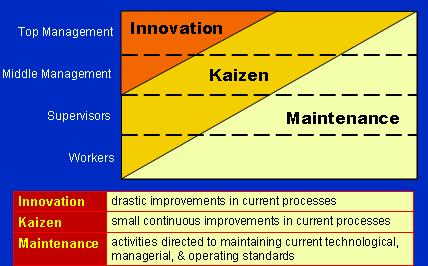

8 Similar to Target costing system Kaizen is a Japanese term for making improvements to a process through small, incremental amounts rather than large innovations Cost minimization steps include strategies in effective waste management, continuous product improvement or better deals in raw materials purchase. 8

9 9

10 Development process may get lengthened to a considerable extent Cost data required for analysis is costly and sometimes not even profitable Quality of products may get reduced due to use of cheap inputs 10

11 Results in cost control - All runaway costs avoided Results in better price control Through precise targeting and setting of its own price 11

12 Target Costing 1. Product specification 2. Target price & volume 3. Target profit 4.Target Cost 5. Product design Traditional Costing 1. Product specification 2.Product design 3.Estimated cost 4.Target cost 5.Target price 12

13 Data obtained from central accounting data base, namely accounts payable, bills of materials and inventory records Data mostly assumption based in the initial phase Competitor s information collected by marketing staff Data may be obtained through joint efforts of engineering and marketing staff reverse engineering 13

14 Assembly oriented industries Industries with diversified product lines Application of technology including factory automation Products with shorter life cycle 14

15 Create a project charter Obtain a management sponsor Obtain a budget Use project management tools Enroll full time participants Assign a strong team manager 15

16 A major textile manufacturer in USA introduced a target costing system. Beginning the project they have come to realize that cost management is different from other accounting efforts. Thus they have undertaken a target costing program to help them increase profits and decrease costs at the design stage. This approach was addresses using a series of 3 strategies: Strategy 1: Separate the functions of managerial and functional accounting so that each could serve its customers to the best advantage.. 16

17 Strategy 2 : Achieve a level of accurate product costing. Although this goal sometimes sounds simplistic, it is not always that easy to get product costs as close to actual as possible. Strategy 3: This strategy includes the discovery that an overwhelming majority of costs are created and built into the products before the manufacturing process ever begins. 17

18 You are a manager of ABC Paper Mills and have recently come across a particular type of paper which is being sold at a substantially lower rate by another company PQR Ltd than the price charged by your own mill. The Value chain for use of a tonne of such paper for PQR Ltd is: PQR Ltd. Merchant Printer Customer PQR Ltd sells this particular paper to Rs1466 per tonne. PQR pays for freight which amounts to Rs.30 per tonne. Average returns and allowances amount to 4% of sales and approximately equals Rs.60 per tonne. The Value chain of your company through which the paper reaches the ultimate customer is similar to that of PQR. However, your mill does not sell directly to merchant, the latter receiving paper from huge distribution center maintained by your Company at Punjab. Contd 18

19 Shipment cost from the mill to the distribution center is Rs.11 per tonne while operating costs in the distribution center are estimated at Rs.25 per tonne. The return on investment required by the distribution center for the investments made, amount to Rs.58 per tonne. Calculate the Mill Manufacturing Target Cost for this particular paper of ABC Paper Mills. Assume that the ROI expected by ABC is Rs.120 per tonne of paper. 19

20 Particulars Sale price of PQR Ltd to Merchant Less: Reduction towards Freight paid by PQR - Rs.30 Returns & Allowances Rs.60 Target Sale price for ABC Paper Mills Less: target profit margin = Overall ROI expected (given) Target cost for ABC Paper Mills Less: Value Addition at Distribution Center level (a) Shipping cost + Operating cost = Rs.11 + Rs.25=Rs.36 (b) ROI for distribution center = Rs.58 Amount (Rs.) 1, , , Target cost at Mill level 1,162 20

21 X Ltd. is engaged in the production of four products: A, B, C and D. The price charged for the four products are Rs.180, Rs.175, Rs.130 and Rs.180 respectively, Market research has indicated that if X Ltd can reduce the selling prices of its products by Rs.5, it will be successful in getting bulk orders and gain a significant share of market of those products. The company s profit markup is 25 per cent on cost of the product. The relevant information of products are as follows: Products A B C D Output in units Cost per unit Direct material (in Rs.) Direct labour (in Rs.) Machine hours Contd 21

22 The four products are usually produced in production runs of 20 units and sold in batches of 10 units. The production overhead is currently absorbed by using a machine hour rate, and the total of the production overheads for the period has been analysed as follows: Rs. Machine department costs 52,130 Setup costs 26,250 Stores receiving 18,000 Inspection/Quality Control 10,500 Material handling and dispatch 23,100 Contd 22

23 The cost drivers to be used for the overhead costs are as follows: Cost Cost drivers Setup costs Number of production runs Store receiving Requisitions raised Inspection/Quality control Number of production runs Materials handling and dispatch Order executed The number of requisitions raised in the stores was 100 for each product and the number of orders executed was 210, each order being for a batch of 10 units of a product. You are required: i) To compute the target cost for each product. ii) To compute total cost of each product using activity based costing. iii) Compare target cost and activity based cost of each product and comment whether the price reduction is profitable or not. 23

24 i) The target cost of each product after reduction is computed as follows: Product Present Price (Rs.) Proposed Price (Rs.) Target Cost (Rs. ) (with 25% Margin) A B C D Contd 24

25 ii) Statement showing cost/unit of Driver as per ABC Cost Amount Driver No. Cost/unit of Driver Set-ups 26,250 Production runs 105* Rs Stores receiving 18,000 Requisition 400** Rs Inspection/Quality 10,500 Production runs 105 Rs Handling/Dispatch 23,100 Orders 210 Rs Machine Department 52,130 Machine Hrs. 6,500 Rs * Production runs = (600/20) + (500/20) + (400/20) + (600/20) = 105 **Requisitions = 100 for each product or 400 total Machine hours = 2, , ,800 = 6,500 hours Contd 25

26 Statement showing Total Cost and Cost Per Unit as per ABC Rs. Item A B C D Direct Material 24,000 25,000 12,000 36,000 Direct Labour 16,800 10,500 5,600 12,600 Set-up 7,500 6,250 5,000 7,500 Stores receiving 4,500 4,500 4,500 4,500 Inspection/Quality 3,000 2,500 2,000 3,000 Handling/Dispatch 6,600 5,500 4,400 6,600 Machine Dept. Cost 19,248 12,030 6,416 14,436 Total Cost 81,648 66,280 39,916 84,636 Output (Units) Cost per unit Contd 26

27 iii) Comparison of Actual Cost and Target Cost Cost A B C D Actual Target Difference (-) 3.92 (-) 3.44 (-) 0.21 (+) 1.06 Comment: The total actual cost of A, B and C product is less than the target cost so there is no problem in reducing the cost of these product by Rs.5 from the present price. It will increase the profitability of the company but the cost of D is slightly more than the target cost, it is therefore, suggested that the company should either control it or redesign it. 27

28 AML Ltd. is engaged in production of three types of ice-cream products: Coco, Strawberry and Vanilla. The company presently sells 50,000 units of Rs. 25 per unit, Strawberry Rs. 20 per unit and Vanilla 60,000 Rs.15 per unit. The demand is sensitive to selling price and it has been observed that every reduction of Re. 1 per unit in selling price, increases the demand for each product by 10% to the previous level. The company has the production capacity of 60,500 units of Coco, 24,200 units of Strawberry and 72,600 units of Vanilla. The company marks up 25% on cost of the product The Company management decides to apply ABC analysis. For this purpose it identifies four activities and the rates as follows: Contd 28

29 Activity Cost Rate Ordering Rs.800 per purchase order Delivery Rs.700 per delivery Shelf stocking Rs.199 per hour Customer support and assistance Rs.1.10 p.u. sold. The other relevant information for the products are as follows: Coco Strawberry Vanilla Direct Material p.u. (Rs. ) Direct Labour p.u. (Rs. ) No. of purchase orders No. of deliveries Shelf stocking hours Contd 29

30 Under the traditional costing system, store support costs are 30% of prime cost. In ABC these costs are coming under customer support and assistance. Required: i. Calculate target cost for each product after a reduction of selling price required to achieve the sales equal to the production capacity. ii. Calculate the total cost and unit cost of each product at the maximum level using traditional costing. iii. Calculate the total cost and unit cost of each product at the maximum level using activity based costing. iv. Compare the cost of each product calculated in (i) and (ii) with (iii) and comment on it. 30

after reduction 23.00 18.00 13.00 Profit marks up 25% on cost i.")

31 i) Cost of products under target costing Demanded unit and selling price Coco Strawberry Vanilla Selling Price Demand Selling Price Demand Selling Price Demand Target cost of each product after reduction in selling price Coco Strawberry Vanilla Selling price (SP) after reduction Profit marks up 25% on cost i.e 20 % on SP Target cost of production (per unit) Contd 31

32 ii) Cost of product under traditional costing Coco Strawberry Vanilla Units Material cost (8,6,5 per unit) Labour cost (5,4,3 per unit) Prime cost Store support costs (30% of prime) Cost per unit Contd 32

33 iii) Cost of product under activity based costing Rs. Coco Strawberry Vanilla Units 60,500 24,200 72,600 Material cost (8,6,5 per unit) 484, , ,000 Labour cost (5,4,3 per unit) 302,500 96, ,800 Prime cost 786, , ,800 Ordering Rs. 800 (35, 30, 15) 28,000 24,000 12,000 Delivery Rs.700 (112, 66, 48) 78,400 46,200 33,600 Shelf Rs.199, (130,150,160) 25,870 29,850 31,840 Customer Rs ,550 26,620 79,860 Total Cost 985, ,, ,100 Cost Per unit Contd 33

(c) 2.11-0.83 0.23 (b) (c) 0.61-2.23 0.23 Note : The cost of product of strawberry is higher in ABC method in comparison to target costing and traditional methods.")

34 iv) Comparative Analysis of cost of production (Rs.) Coco Strawberry Vanilla (a) As per Target Costing (b) As per traditional Costing (c ) As per Activity Based Costing (a) (c) (b) (c) Note : The cost of product of strawberry is higher in ABC method in comparison to target costing and traditional methods. It indicated that actual profit under target costing is less than targeted. For remaining two products, ABC is most suitable. 34

35 Activity Based Costing Target Costing & Kaizen Costing 35

36 36