Cheniere Energy and the LNG Market. NARUC LNG Working Group November 8, 2015 Patricia Outtrim, Vice President, Government and Regulatory Affairs

|

|

|

- Gillian Lambert

- 6 years ago

- Views:

Transcription

1 Cheniere Energy and the LNG Market NARUC LNG Working Group November 8, 2015 Patricia Outtrim, Vice President, Government and Regulatory Affairs

2 Forward Looking Statements 2 This presentation contains certain statements that are, or may be deemed to be, forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. All statements, other than statements of historical facts, included or incorporated by reference herein are forward-looking statements. Included among forward-looking statements are, among other things: statements regarding the ability of Cheniere Energy Partners, L.P. to pay distributions to its unitholders or Cheniere Energy Partners LP Holdings, LLC to pay dividends to its shareholders; statements regarding Cheniere Energy Inc. s, Cheniere Energy Partners LP Holdings, LLC s or Cheniere Energy Partners, L.P. s expected receipt of cash distributions from their respective subsidiaries; statements that Cheniere Energy Partners, L.P. expects to commence or complete construction of its proposed liquefied natural gas ( LNG ) terminals, liquefaction facilities, pipeline facilities or other projects, or any expansions thereof, by certain dates or at all; statements that Cheniere Energy, Inc. expects to commence or complete construction of its proposed LNG terminals, liquefaction facilities, pipeline facilities or other projects by certain dates or at all; statements regarding future levels of domestic and international natural gas production, supply or consumption or future levels of LNG imports into or exports from North America and other countries worldwide, or purchases of natural gas, regardless of the source of such information, or the transportation or other infrastructure, or demand for and prices related to natural gas, LNG or other hydrocarbon products; statements regarding any financing transactions or arrangements, or ability to enter into such transactions; statements relating to the construction of our proposed liquefaction facilities and natural gas liquefaction trains ( Trains ), or modifications to the Creole Trail Pipeline, including statements concerning the engagement of any engineering, procurement and construction ("EPC") contractor or other contractor and the anticipated terms and provisions of any agreement with any EPC or other contractor, and anticipated costs related thereto; statements regarding any agreement to be entered into or performed substantially in the future, including any revenues anticipated to be received and the anticipated timing thereof, and statements regarding the amounts of total LNG regasification, liquefaction or storage capacities that are, or may become, subject to contracts; statements regarding counterparties to our commercial contracts, construction contracts and other contracts; statements regarding our planned development and construction of additional Trains, including the financing of such Trains; statements that our Trains, when completed, will have certain characteristics, including amounts of liquefaction capacities; statements regarding our business strategy, our strengths, our business and operation plans or any other plans, forecasts, projections or objectives, including anticipated revenues and capital expenditures and EBITDA, any or all of which are subject to change; statements regarding projections of revenues, expenses, earnings or losses, working capital or other financial items; statements regarding legislative, governmental, regulatory, administrative or other public body actions, approvals, requirements, permits, applications, filings, investigations, proceedings or decisions; statements regarding our anticipated LNG and natural gas marketing activities; and any other statements that relate to non-historical or future information. These forward-looking statements are often identified by the use of terms and phrases such as achieve, anticipate, believe, contemplate, develop, estimate, example, expect, forecast, goals, opportunities, plan, potential, project, propose, subject to, strategy, target, and similar terms and phrases, or by use of future tense. Although we believe that the expectations reflected in these forward-looking statements are reasonable, they do involve assumptions, risks and uncertainties, and these expectations may prove to be incorrect. You should not place undue reliance on these forward-looking statements, which speak only as of the date of this presentation. Our actual results could differ materially from those anticipated in these forward-looking statements as a result of a variety of factors, including those discussed in Risk Factors in the Cheniere Energy, Inc., Cheniere Energy Partners, L.P. and Cheniere Energy Partners LP Holdings, LLC Annual Reports on Form 10-K filed with the SEC on February 20, 2015, which are incorporated by reference into this presentation. All forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by these Risk Factors. These forward-looking statements are made as of the date of this presentation, and other than as required under the securities laws, we undertake no obligation to publicly update or revise any forward-looking statements.

3 U.S. LNG Export Projects 5 projects under construction (Sabine Pass T1-5, Corpus T1-2, CameronT1-3, Freeport T1-3, Cove Point) - Total capacity: ~64 mtpa 2 projects (Corpus Christi T3, Sabine T6) have received FERC permit: + 9 mtpa 7 more LNG projects have filed complete FERC applications*: + 66 mtpa Oregon LNG Jordan Cove Dominion Cove Point Golden Pass Magnolia Southern LNG Freeport LNG Gulf LNG Lake Charles Corpus Christi Cameron LNG Sabine Pass Under Construction Filed FERC Application 3 Source: Office of Oil and Gas Global Security and Supply, Office of Fossil Energy, U.S. Department of Energy; U.S. Federal Energy Regulatory Commission; Company releases; Cheniere Research.

4 U.S. Ascent to One of the Largest LNG Producers

5 Producer Ranking Under performance: declining reserves; domestic needs Capacity Production

6 Sluggish Supply Growth Led to Stagnant Trade in Past 3 Years PNG LNG start up in 2014 was the first sustained liquefaction capacity to come online since Pluto LNG in 2012 mtpa Historical LNG Trade No. of LNG Production Trains LNG Production Trains In Service Total LNG Trade 6 Source: Cheniere Research, GIIGNL

7 Though Sense of Scarcity Died Down, Long Term LNG Growth Remains Solid Competition intensifying, potentially driving adjustments to LNG contract terms and re-distribution of risk Benefits the industry in the longer run Demand pull from new markets not to be underestimated 7 Source: Wood Mackenzie Q3 2015, Cheniere Research

8 Lower LNG Prices Bring New Demand Opportunities Lower-priced LNG and gas become competitive against dirtier burning options, especially in the power sector 8 Source: NYMEX, ICE, PIRA, METI

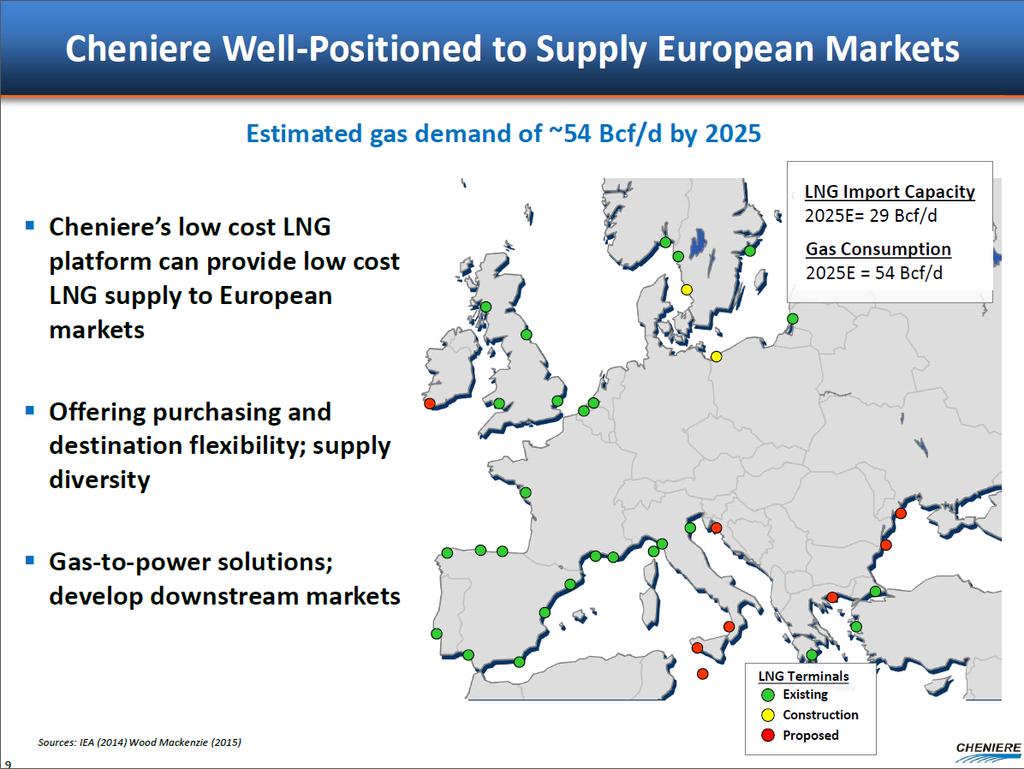

9

Existing India KJV")

10 Asia Emerging Markets Turkmenistan- China Pipeline +3 Bcf/d China West-East #2 Pipeline +2.9 Bcf/d 170 Central Asia LNG Terminals (Bcf/d) Existing India KJV Pipeline +2.8 Bcf/d Krishna Godavari Basin Under Construction Planned Unconventional Gas Potential Proved Reserves (Tcf) Major Pipelines Source: BP Statistical Review 2012, PFC Energy (2013), Cheniere Research

11 FSRUs Bring New Markets Online Quickly There is 132 mtpa of potential new demand from FSRU terminal markets by the end of 2021 mtpa 200 FSRU Capacity Buildup Speculative Possible Planned Construction Operational 0 11 Source: Cheniere Research

12 FSRU Markets Emerge in Months, Not Years All three markets started importing by May 2015 and are already importing almost 1 million tonnes per month 12 mt Egypt, Pakistan & Jordan LNG Imports Jan Feb Mar Apr May Jun Jul Aug Sep Source: IHS Waterborne Note: September figures are preliminary Egypt Pakistan Jordan Egypt s Second FSRU Timeline May 2015 Egas Releases FSRU Tender August 2015 Egas Awards FSRU To BW September 2015 FSRU Arrives in Egypt October 2015 FSRU Starts Commercial Operations

13 New Liquefaction Projects Face Major Hurdles Pace of international investment projects inherently slow Despite highly optimistic targets, we estimate no FIDs outside of the US in 2015 Risk of delays, cancellations of large scale projects Projects become marginal as IRRs are slashed and payback periods delayed CCL T1-2, SPL T5 and Freeport T3 have taken FID Risk of creating a supply shortfall post 2020 Aging facilities and depleting reserves to exacerbate issue Demand for long-term supplies will respond to avert supply shortages 13 Source: Cheniere Research, Company disclosures

14 Low Oil Prices Place Post 2020 Supplies at Risk Nameplate Liquefaction Capacity ~ 311 mtpa; 2020 expected at ~ 445 mtpa Current prices bring above ground risks into focus, threatens commerciality of some proposed projects mtpa SPL T1, Gorgon T1, Gladstone T1 APLNG T2, PFLNG 1, MLNG Tiga T9 SPL T2, Gorgon T2 Gladstone T2 Gorgon T3, Wheatstone T1 Wheatstone T2 Cove Point Ichthys T2, Prelude FLNG, PFLNG 2 SPL T5, CCL T1, Cameron T2 Cameron T1 CCL T2, Cameron T3 Freeport T2, Yamal T1 Freeport T3, Yamal T2 Asia Pacific Atlantic Basin APLNG T1 SPL T3 SPL T4 Ichthys T1 Freeport T1 Risk of Supply Shortfall? Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q Source: Cheniere Research

15 15 Conclusions New project sanctioning slowing further Large-scale projects are more prone to delays; funding challenges New markets and new players to make up an increasing share of the LNG demand pie Including in Asia, Middle East and Europe More independents enter the market These markets exhibit different profiles than the typical big markets we are used to Smaller loads, intermittent demand, additional uncertainty to manage and more risk averse Contracting terms need to be more aligned with buyers needs US LNG better positioned to service these markets Abundant, reliable, affordable supplies with flexible contracting options Enables buyers to be more responsive and better adapt to market conditions Enhances liquidity and drives market towards optimization, efficiency

16 16 Executing on Strategy 2025 Forecast for Cheniere Energy, Inc. ~60 mtpa LNG by 2025 ~14% of the total LNG market One of the largest exporters of LNG on a global basis ~9 Bcf/d One of the largest natural gas buyers in the U.S. $50B+ in U.S. infrastructure Significant investment in U.S. infrastructure ~1,000 permanent jobs created Supporting over 200,000 indirect jobs Flexible, Scalable, industryleading platform

17 17 Cheniere s Key Businesses LNG PLATFORM GAS PROCUREMENT CHENIERE MARKETING FUTURE DEVELOPMENTS Four planned LNG terminals to be located along Gulf of Mexico ~60 mtpa planned Scalable platform SPL T1-5 and CCL 1-2 underpinned by long-term contracts, competitive capital costs Providing feedstock for LNG production Redundant pipeline capacity ensures reliable gas deliverability Upstream pipeline capacity provides access to diverse supply sources LNG sales, FOB or DES, provided to customers on a short, mid, and long-term basis ~9 mtpa LNG volumes expected from SPL T1-6 and CCL T1-3 3 chartered LNG vessels to date Developing/ investing in infrastructure to facilitate hydrocarbon revolution in Texas and beyond Optimize value of LNG platform Identify opportunities in related markets

Trains 1-5 are under construction; First")

Trains 1-2 are under construction; First LNG")

First LNG targeted in late 2021 Under Construction Proposed 18 (1)")

18 Cheniere LNG Platform Sabine Pass Liquefaction 6 train development 27 mtpa (~3.8 Bcf/d in export capacity) Trains 1-5 are under construction; First LNG expected in late 2015 Train 6 under development, FID expected 2015/16 Live Oak LNG 1 ~5 mtpa development (~0.8Bcf/d) First LNG targeted in late 2021 Live Oak LNG TX Corpus Christi Liquefaction Sabine Pass Liquefaction Corpus Christi Liquefaction 5 train development 22.5 mtpa (~3.2 Bcf/d in export capacity) Trains 1-2 are under construction; First LNG expected in late 2018 Train 3 under development; FID expected 2015/16 Trains 4-5 under development; Permitting process initiated June 2015 Creole Trail PL LA Louisiana LNG Louisiana LNG 1 ~5 mtpa development (~0.7Bcf/d) First LNG targeted in late 2021 Under Construction Proposed 18 (1) Cheniere Energy, Inc. has agreed in principle to partner with Parallax Enterprises, LLC on these projects

19 Cheniere Energy Global Customers U.K. BG Centrica Spain Gas Natural Fenosa Endesa Iberdrola France Total EDF Portugal EDP 8.6 South Korea Kogas India GAIL Indonesia Pertamina Australia Woodside Supply Purchase Agreements

20 20 The U.S. Is A Low Cost Source of LNG Estimated breakeven LNG pricing range, Delivered Ex-Ship to Asia $20 $18.5 $16.0 $17.0 LNG prices ($/MMBtu) $15 $10 $8.4 $11.5 $9.5 $13.0 $12.0 $14.0 $14.5 $13.0 $7.7 $5 Cheniere Gulf Coast West Africa Western Canada Northwest Australia East Africa Southeast Asia Source: Note: Cheniere Research, Wood Mackenzie, company filings and investor materials. Breakeven prices derived assuming unlevered after-tax returns of 10% on Canadian projects and 12% on all other projects over construction plus 20 years of operation. Henry Hub at $3.00/MMBtu The U.S. is one of the lowest cost natural gas providers in the world U.S. liquefaction project costs are also significantly lower due to less project development needed The breakeven LNG price for Cheniere LNG export facilities is one of the lowest compared to other proposed LNG projects

5.3 Bcf/d of pipeline interconnection Artist s rendition Design production capacity is expected to be ~4.")

21 21 Sabine Pass Liquefaction Brownfield LNG Export Project Utilizes Existing Assets, Trains 1-5 Under Construction Current Facility ~1,000 acres in Cameron Parish, LA 40 ft. ship channel 3.7 miles from coast 2 berths; 4 dedicated tugs 5 LNG storage tanks (~17 Bcfe of storage) 5.3 Bcf/d of pipeline interconnection Artist s rendition Design production capacity is expected to be ~4.5 mtpa per train, using ConocoPhillips Optimized Cascade Process Liquefaction Trains 1 5: Fully Contracted Lump Sum Turnkey EPC contracts w/ Bechtel T1 & T2 EPC contract price ~$4.1B Overall project ~95% complete (as of 9/2015) Operations estimated late 2015/2016 T3 & T4 EPC contract price ~$3.8B Overall project ~74% complete (as of 9/2015) Operations estimated 2016/2017 T5 EPC contract price ~$3.0B Construction commenced June 2015 Liquefaction Train 6 FID upon obtaining commercial contracts and financing Significant infrastructure in place including storage, marine and pipeline interconnection facilities; pipeline quality natural gas to be sourced from U.S. pipeline network

22 Sabine Pass Liquefaction Construction July

23 Aerial View of SPL Construction August 2015 Train 6 Under Development T5 Soil Stabilization Train 5 Train 3 T3 Ethylene Cold Box T3 Methane Cold Box Train 4 T1 Methane Cold Box T1 Ethylene Cold Box Air Coolers Propane Condenser Area Train 1 T2 Methane Cold Box T2 Ethylene Cold Box Train 2

overall project progress as of September 2015 is 95.2% complete vs. Target Plan of 97.")

24 SPL Construction Completion Schedules Trains 1 5 BG DFCD March 2016 First LNG GN DFCD June 2016 Early Engineering KOGAS DFCD Jun 2017 April 2017 GAIL DFCD Mar 2018 Sept 2017 TOTAL & CENTRICA DFCD Dec 2019 Oct Stage 1 (Trains 1&2) overall project progress as of September 2015 is 95.2% complete vs. Target Plan of 97.5%: Engineering, Procurement, Subcontracts and Construction are 100%, 100%, 82.2% and 91.5% complete against Target Plan of 99.8%, 100%, 87.0% and 96.4% respectively Bechtel Delivered the Train 1 Commissioning and Start-up Plan in Feb, projecting Fuel Gas introduction in Sep, Feed Gas introduction in Oct, and Ready for Start-up in Dec; all in support of the current First LNG Target by year-end 2015, and Target Substantial Completion in Mar 2016 Stage 2 (Trains 3&4) overall project progress as of September 2015 is 73.6% complete vs. Target Plan of 79.6%: Engineering, Procurement, Subcontracts and Construction are 100%, 98.9%, 50.0% and 40.4% complete against Target Plan of 98.8%, 98.2%, 62.3% and 55.1% respectively Stage 3 (Trains 5&6) overall project progress: NTP on Train 5 issued to Bechtel on June 30 th Soil stabilization civil works are in progress and the current plan estimates Train 5 operational in 52 months from NTP

286,500,000 (1) 182,500,000 182,500,000 182,500,000 104,750,000 (1) 91,250,000 Annual Fixed Fees (2) ~$723 MM (3) ~$454 MM ~$548 MM ~$548 MM ~$314 MM")

25 LNG Sale and Purchase Agreements (SPAs) Sabine Pass Liquefaction ~20 mtpa take-or-pay style commercial agreements ~$2.9B annual fixed fee revenue for 20 years BG Gulf Coast LNG Gas Natural Fenosa Korea Gas Corporation GAIL (India) Limited Total Gas & Power N.A. Centrica plc Annual Contract Quantity (MMBtu) 286,500,000 (1) 182,500, ,500, ,500, ,750,000 (1) 91,250,000 Annual Fixed Fees (2) ~$723 MM (3) ~$454 MM ~$548 MM ~$548 MM ~$314 MM ~$274 MM Fixed Fees $/MMBtu (2) $ $3.00 $2.49 $3.00 $3.00 $3.00 $3.00 LNG Cost 115% of HH 115% of HH 115% of HH 115% of HH 115% of HH 115% of HH Term of Contract (4) Guarantor 20 years BG Energy Holdings Ltd. 20 years Gas Natural SDG S.A. Corporate / Guarantor Credit Rating (5) A-/A2/A- BBB/Baa2/BBB+ Fee During Force Majeure Up to 24 months Up to 24 months Contract Start 20 years 20 years N/A NR/Baa2/BBB- Train 1 + additional volumes with Trains 2,3,4 Train 2 Train 3 Train 4 N/A A+/Aa3/AA- N/A N/A 20 years Total S.A. AA-/Aa1/AA- N/A Train 5 20 years N/A A-/Baa1/A- N/A Train 5 25 (1) BG has agreed to purchase 182,500,000 MMBtu, 36,500,000 MMBtu, 34,000,000 MMBtu and 33,500,000 MMBtu of LNG volumes annually upon the commencement of operations of Trains 1, 2, 3 and 4, respectively. Total has agreed to purchase 91,250,000 MMBtu of LNG volumes annually plus 13,400,000 MMBtu of seasonal LNG volumes upon the commencement of Train 5 operations. (2) A portion of the fee is subject to inflation, approximately 15% for BG Group, 13.6% for Gas Natural Fenosa, 15% for KOGAS and GAIL (India) Ltd and 11.5% for Total and Centrica. (3) Following commercial in service date of Train 4. BG will provide annual fixed fees of approximately $520 million during Trains 1-2 operations and an additional $203 million once Trains 3-4 are operational. (4) SPAs have a 20 year term with the right to extend up to an additional 10 years. Gas Natural Fenosa has an extension right up to an additional 12 years in certain circumstances. (5) Ratings are provided by S&P/Moody s/fitch and subject to change, suspension or withdrawal at anytime and are not a recommendation to buy, hold or sell any security.

26 Corpus Christi Liquefaction Project 26 Houston New Orleans Corpus Christi Gulf of Mexico Under Construction Trains 1-2 Artist s rendition Design production capacity is expected to be ~4.5 mtpa per train, using ConocoPhillips Optimized Cascade Process Initiated Development Trains 4-5 Train 3 Proposed 5 Train Facility >1,000 acres owned and/or controlled 2 berths, 4 LNG storage tanks (~13.5 Bcfe of storage) Key Project Attributes 45 ft. ship channel 14 miles from coast Protected berth Premier Site Conditions 23-mile 48 and 42 parallel pipelines will connect to several interstate and intrastate pipelines Liquefaction Trains 1-2: Under Construction Lump Sum Turnkey EPC contracts w/ Bechtel T1 & T2 EPC contract price ~$7.1B Construction commenced May 2015 Operations estimated 2018 Liquefaction Train 3: Partially Contracted 0.8 mtpa contracted to date Targeting additional 2.1 mtpa Reach FID upon contracting Liquefaction Trains 4-5: Initiated Development Permit process started June 2015 Commenced Construction on Trains 1-2 in May 2015

27 27 Corpus Christi LNG Site in the Middle of an Industrial Zone Aerial Map of Surrounding Area Cheniere Cheniere CCL Cheniere

28 28 August Construction

29 29 August Construction

30 Corpus Christi Liquefaction Economic Benefits Announced infrastructure investment of ~$14.5 billion (Stages 1 & 2) Direct Jobs Peak 4,000 construction jobs 430 permanent jobs at terminal Indirect & Induced Jobs* Construction activities will create on average 31,000 Texas jobs per year over nine years Up to 92,000 jobs in Texas in a typical year that will be supported from the E&P activity needed to meet natural gas demand for exports from CCL ~5,000 jobs per year in the Coastal Bend region supported from ongoing CCL operations Economic Impacts* $6.9 Billion to South Texas GDP and $4.8 Billion in wages to regional workers during construction $49.6 Billion in economic activity in the State of Texas during construction $21.8 Billion to U.S. GDP over first 25 years of ongoing operations $9.8 - $15.8 Billion/yr improvement to US Balance of Trade 30 * Data derived from The Perryman Group, "The Anticipated Impact of Cheniere's Proposed Corpus Christi Liquefaction Facility on Business Activity in Corpus Christi, Texas, and the US: 2015 Update," June 2015.

31 Gas Procurement Corpus Christi Terminal CCL contracting long-term direct and upstream pipeline transport capacity Tennessee P/L: KM Tejas P/L: 0.3 Bcf/d 0.25 Bcf/d NGPL P/L: Bcf/d CCL purchasing natural gas from producers and marketers Woodford Marcellus / Utica NGPL Tennessee Gas HPL KM Tejas Oasis Enterprise Granite Wash Permian Basin Barnett Haynesville Eagle Ford Shale Plays Basins Corpus Christi 31 Source: Lippman Consulting, Baker Hughes and Bentek, as of January 2014

32 Corpus Christi Liquefaction Project Schedule Train 1 DFCD Train 1 Guaranteed Current Level 3 Schedule Feb-19 Oct-19 Train 2 DFCD Train 2 Guaranteed Jul-20 Current Level 3 Schedule Jun-19 Stage 1 (Trains 1&2) overall project progress as of September 2015 is ahead of target: Engineering, Procurement, and Construction has progressed to 82.0%, 32.0%, and 0.4% compared to a plan of 77.1%, 21.5%, and 0.9% respectively. NTP issued, construction commenced for Trains 1-2 in May Note: Based on Guaranteed Substantial and Target Completion Dates per EPC contract.

79.36 117.32 39.68 78.20 44.12 40.00 40.")

$3.50 $3.")

")

33 33 Corpus Christi Liquefaction SPAs SPA progress: ~8.42 mtpa take-or-pay style commercial agreements ~$1.5B annual fixed fee revenue for 20 years PT Pertamina (Persero) Endesa S.A. Iberdrola S.A. Gas Natural Fenosa Woodside Energy Trading Électricité de France EDP Energias de Portugal S.A. Annual Contract Quantity (TBtu) Annual Fixed Fees (1) ~$278 MM ~$411 MM ~$139 MM ~$274 MM ~$154 MM ~$140 MM ~$140 MM Fixed Fees $/MMBtu (1) $3.50 $3.50 $3.50 $3.50 $3.50 $3.50 $3.50 LNG Cost 115% of HH 115% of HH 115% of HH 115% of HH 115% of HH 115% of HH 115% of HH Term of Contract (2) 20 years 20 years 20 years 20 years 20 years 20 years 20 years Guarantor N/A N/A N/A Gas Natural SDG, S.A. Woodside Petroleum, LTD Guarantor/Corporate Credit Rating (3) BB+/Baa3/BBB- BBB/Baa2/BBB+ BBB/Baa1/BBB+ BBB/Baa2/BBB+ BBB+/Baa1/BBB+ A+/A1/A+ BB+/Baa3/BBB- Contract Start Train 1 / Train2 Train 1 Train 1 / Train 2 Train 2 Train 2 Train 2 Train 3 N/A N/A (1) 11.5% of the fee is subject to inflation for Pertamina and Woodside; 14% for all others (2) SPA has a 20 year term with the right to extend up to an additional 10 years. (3) Ratings are provided by S&P/Moody s/fitch and subject to change, suspension or withdrawal at anytime and are not a recommendation to buy, hold or sell any security.

34 34 Proposed Development Other Hydrocarbon Exports Estimated investment opportunity up to $2B Facilities to export up to 1 MMbpd liquid hydrocarbons Initial development expected to be supported with 3rd party contracts Initial investment expected up to $1B, initial commercialization ~200kbpd In discussions with potential customers for contracting capacity Regulatory process fairly straightforward Estimated start of operations: 2017

35 Q&A SPL Construction July

CHENIERE ENERGY, INC. Louisiana Energy Conference. June 2016

CHENIERE ENERGY, INC. Louisiana Energy Conference June 2016 Forward Looking Statements This presentation contains certain statements that are, or may be deemed to be, forward-looking statements within

CHENIERE ENERGY, INC. Louisiana Energy Conference June 2016 Forward Looking Statements This presentation contains certain statements that are, or may be deemed to be, forward-looking statements within

CHENIERE ENERGY, INC.

CHENIERE ENERGY, INC. U.S. LNG in the new energy price environment January 2016 Forward Looking Statements This presentation contains certain statements that are, or may be deemed to be, forward-looking

CHENIERE ENERGY, INC. U.S. LNG in the new energy price environment January 2016 Forward Looking Statements This presentation contains certain statements that are, or may be deemed to be, forward-looking

Cheniere Energy, Inc. July 2015

Cheniere Energy, Inc. July 2015 Forward Looking Statements 2 This presentation contains certain statements that are, or may be deemed to be, forward-looking statements within the meaning of Section 27A

Cheniere Energy, Inc. July 2015 Forward Looking Statements 2 This presentation contains certain statements that are, or may be deemed to be, forward-looking statements within the meaning of Section 27A

US LNG Supply into Europe. Baltic Energy Summit, Vilnius November 25 th, 2015 Helena Wisden, Cheniere Marketing International

US LNG Supply into Europe Baltic Energy Summit, Vilnius November 25 th, 2015 Helena Wisden, Cheniere Marketing International Forward Looking Statements This presentation contains certain statements that

US LNG Supply into Europe Baltic Energy Summit, Vilnius November 25 th, 2015 Helena Wisden, Cheniere Marketing International Forward Looking Statements This presentation contains certain statements that

CHENIERE ENERGY, INC. CLARKSONS PLATOU ENERGY & SHIPPING CONFERENCE. January 2016

CHENIERE ENERGY, INC. CLARKSONS PLATOU ENERGY & SHIPPING CONFERENCE January 2016 Forward Looking Statements This presentation contains certain statements that are, or may be deemed to be, forward-looking

CHENIERE ENERGY, INC. CLARKSONS PLATOU ENERGY & SHIPPING CONFERENCE January 2016 Forward Looking Statements This presentation contains certain statements that are, or may be deemed to be, forward-looking

Shale Gas and U.S. LNG Exports. Vienna, January 29, 2013 Jean Abiteboul President, Cheniere Supply & Marketing

Shale Gas and U.S. LNG Exports Vienna, January 29, 2013 Jean Abiteboul President, Cheniere Supply & Marketing Forward Looking Statements This presentation contains certain statements that are, or may be

Shale Gas and U.S. LNG Exports Vienna, January 29, 2013 Jean Abiteboul President, Cheniere Supply & Marketing Forward Looking Statements This presentation contains certain statements that are, or may be

CHENIERE ENERGY, INC J.P. MORGAN GLOBAL HIGH YIELD & LEVERAGED FINANCE CONFERENCE. March 2016

CHENIERE ENERGY, INC. 2016 J.P. MORGAN GLOBAL HIGH YIELD & LEVERAGED FINANCE CONFERENCE March 2016 Forward Looking Statements This presentation contains certain statements that are, or may be deemed to

CHENIERE ENERGY, INC. 2016 J.P. MORGAN GLOBAL HIGH YIELD & LEVERAGED FINANCE CONFERENCE March 2016 Forward Looking Statements This presentation contains certain statements that are, or may be deemed to

CHENIERE ENERGY, INC.

CHENIERE ENERGY, INC. J.P. MORGAN WEST COAST ENERGY INFRASTRUCTURE/MLP 1x1 FORUM March 2016 Forward Looking Statements This presentation contains certain statements that are, or may be deemed to be, forward-looking

CHENIERE ENERGY, INC. J.P. MORGAN WEST COAST ENERGY INFRASTRUCTURE/MLP 1x1 FORUM March 2016 Forward Looking Statements This presentation contains certain statements that are, or may be deemed to be, forward-looking

CHENIERE ENERGY, INC.

CHENIERE ENERGY, INC. Factors Affecting Global Coal-Gas Competition NGI Workshop - Global Competition Between Coal and Natural Gas October 15th 218 Najla Jamoussi Director, Market Fundamentals & Corporate

CHENIERE ENERGY, INC. Factors Affecting Global Coal-Gas Competition NGI Workshop - Global Competition Between Coal and Natural Gas October 15th 218 Najla Jamoussi Director, Market Fundamentals & Corporate

Cheniere Energy Partners, L.P. / Cheniere Energy, Inc. Proposed Sabine Pass LNG Facility Expansion Adding Liquefaction Capabilities.

Cheniere Energy Partners, L.P. / Cheniere Energy, Inc. Proposed Sabine Pass LNG Facility Expansion Adding Liquefaction Capabilities June 4, 2010 Forward Looking Statements This presentation contains certain

Cheniere Energy Partners, L.P. / Cheniere Energy, Inc. Proposed Sabine Pass LNG Facility Expansion Adding Liquefaction Capabilities June 4, 2010 Forward Looking Statements This presentation contains certain

CHENIERE ENERGY, INC.

CHENIERE ENERGY, INC. THE GAS PACKAGE - THE ROLE OF US LNG European Parliament Public Hearing Andrew Walker Vice-President, Strategy, Cheniere Marketing May 23, 2016 Forward Looking Statements This presentation

CHENIERE ENERGY, INC. THE GAS PACKAGE - THE ROLE OF US LNG European Parliament Public Hearing Andrew Walker Vice-President, Strategy, Cheniere Marketing May 23, 2016 Forward Looking Statements This presentation

Cheniere Energy & the Global LNG Market. March 2015

Cheniere Energy & the Global LNG Market March 2015 Forward Looking Statements 2 This presentation contains certain statements that are, or may be deemed to be, forward-looking statements within the meaning

Cheniere Energy & the Global LNG Market March 2015 Forward Looking Statements 2 This presentation contains certain statements that are, or may be deemed to be, forward-looking statements within the meaning

Cheniere Energy and The Coastal Bend

Cheniere Energy and The Coastal Bend Jason French Director of Government and Public Affairs Aransas Pass Chamber of Commerce Luncheon January 13, 2015 Forward Looking Statements This presenta-on contains

Cheniere Energy and The Coastal Bend Jason French Director of Government and Public Affairs Aransas Pass Chamber of Commerce Luncheon January 13, 2015 Forward Looking Statements This presenta-on contains

CHENIERE ENERGY, INC. How is the Rest of the World s LNG Interfacing With Europe?

CHENIERE ENERGY, INC. How is the Rest of the World s LNG Interfacing With Europe? European Gas Conference - Vienna Andrew Walker VP LNG Strategy January 23, 18 2 Safe Harbor Statements Forward-Looking

CHENIERE ENERGY, INC. How is the Rest of the World s LNG Interfacing With Europe? European Gas Conference - Vienna Andrew Walker VP LNG Strategy January 23, 18 2 Safe Harbor Statements Forward-Looking

The Case for Investing in LNG Export Terminals in the US. Marine Money 2017 Meg Gentle, CEO

The Case for Investing in LNG Export Terminals in the US Marine Money 2017 Meg Gentle, CEO June 19, 2017 Cautionary statement Forward looking statement Non-GAAP Financial Measures The information in this

The Case for Investing in LNG Export Terminals in the US Marine Money 2017 Meg Gentle, CEO June 19, 2017 Cautionary statement Forward looking statement Non-GAAP Financial Measures The information in this

Forward Looking Statements This presentation contains certain statements that are, or may be deemed to be, forward looking statements within the meani

Outlook for U.S. LNG Exports METI, Japan LNG Producer Consumer Conference Charif Souki CEO, Cheniere Energy Inc. Forward Looking Statements This presentation contains certain statements that are, or may

Outlook for U.S. LNG Exports METI, Japan LNG Producer Consumer Conference Charif Souki CEO, Cheniere Energy Inc. Forward Looking Statements This presentation contains certain statements that are, or may

ROYAL DUTCH SHELL PLC LEADER IN GLOBAL GAS

ROYAL DUTCH SHELL PLC LEADER IN GLOBAL GAS DEFINITIONS AND CAUTIONARY NOTE Resources: Our use of the term resources in this announcement includes quantities of oil and gas not yet classified as Securities

ROYAL DUTCH SHELL PLC LEADER IN GLOBAL GAS DEFINITIONS AND CAUTIONARY NOTE Resources: Our use of the term resources in this announcement includes quantities of oil and gas not yet classified as Securities

CHENIERE ENERGY, INC.

CHENIERE ENERGY, INC. * Sabine Pass LNG, L.P. Cheniere Energy Partners, L.P. Cheniere Energy, Inc. 91% *Corpus Christi LNG, LLC Cheniere Energy, Inc. 100% *Creole Trail LNG, L.P. Cheniere Energy, Inc.

CHENIERE ENERGY, INC. * Sabine Pass LNG, L.P. Cheniere Energy Partners, L.P. Cheniere Energy, Inc. 91% *Corpus Christi LNG, LLC Cheniere Energy, Inc. 100% *Creole Trail LNG, L.P. Cheniere Energy, Inc.

Corporate Presentation

Corporate Presentation Enercom Conference Denver, Colorado August 2018 John Howie, President Tellurian Production Company Cautionary statements Forward-looking statements The information in this presentation

Corporate Presentation Enercom Conference Denver, Colorado August 2018 John Howie, President Tellurian Production Company Cautionary statements Forward-looking statements The information in this presentation

Safe Harbor Statements. CHENIERE ENERGY, INC. NYSE American: LNG CHENIERE ENERGY, INC. The LNG market: new opportunities and challenges

IEEJ:December 18 IEEJ18 CHENIERE ENERGY, INC. The LNG market: new opportunities and challenges 23 rd International Gas and Power Summit, Paris. November 22, 18 Eric Bensaude Managing Director Commercial

IEEJ:December 18 IEEJ18 CHENIERE ENERGY, INC. The LNG market: new opportunities and challenges 23 rd International Gas and Power Summit, Paris. November 22, 18 Eric Bensaude Managing Director Commercial

Trends in International LNG

Trends in International LNG Anthony Patten, Partner, Allens Presentation to AMPLA State Conference Fremantle, Western Australia 18 May 2012 Allens is an independent partnership operating in alliance with

Trends in International LNG Anthony Patten, Partner, Allens Presentation to AMPLA State Conference Fremantle, Western Australia 18 May 2012 Allens is an independent partnership operating in alliance with

Cheniere Energy. March 2014

Cheniere Energy March 2014 Forward Looking Statements 2 This presentation contains certain statements that are, or may be deemed to be, forward-looking statements within the meaning of Section 27A of the

Cheniere Energy March 2014 Forward Looking Statements 2 This presentation contains certain statements that are, or may be deemed to be, forward-looking statements within the meaning of Section 27A of the

Morgan Stanley Midstream MLP & Diversified Natural Gas Corporate Access Day. March 4, 2014

Morgan Stanley Midstream MLP & Diversified Natural Gas Corporate Access Day March 4, 2014 Forward Looking Statements 2 This presentation contains certain statements that are, or may be deemed to be, forward-looking

Morgan Stanley Midstream MLP & Diversified Natural Gas Corporate Access Day March 4, 2014 Forward Looking Statements 2 This presentation contains certain statements that are, or may be deemed to be, forward-looking

Natural Gas Market Outlook FGU Conference, June 2017 Shelley Corman

Natural Gas Market Outlook FGU Conference, June 217 Shelley Corman Important Information Forward-looking statements disclosure Statements made at this conference or in the materials distributed in conjunction

Natural Gas Market Outlook FGU Conference, June 217 Shelley Corman Important Information Forward-looking statements disclosure Statements made at this conference or in the materials distributed in conjunction

Global LNG Market dynamics, key trends and market outlook

REUTERS / Anne Kat Brevik Global LNG Market dynamics, key trends and market outlook December 14, 217 What to address Market dynamics, key trends and market outlook The role and outlook for U.S. LNG China

REUTERS / Anne Kat Brevik Global LNG Market dynamics, key trends and market outlook December 14, 217 What to address Market dynamics, key trends and market outlook The role and outlook for U.S. LNG China

LNG Exports: A Brief Introduction

LNG Exports: A Brief Introduction Natural gas one of the world s most useful substances is burned to heat homes and run highly-efficient electrical powerplants. It is used as a feedstock in the manufacture

LNG Exports: A Brief Introduction Natural gas one of the world s most useful substances is burned to heat homes and run highly-efficient electrical powerplants. It is used as a feedstock in the manufacture

Cheniere Energy January 2014

Cheniere Energy January 2014 Forward Looking Statements 2 This presentation contains certain statements that are, or may be deemed to be, forward-looking statements within the meaning of Section 27A of

Cheniere Energy January 2014 Forward Looking Statements 2 This presentation contains certain statements that are, or may be deemed to be, forward-looking statements within the meaning of Section 27A of

Corporate Presentation. March 2008

Corporate Presentation March 2008 Safe Harbor Act This presentation contains certain statements that are, or may be deemed to be, forward-looking statements within the meaning of Section 27A of the Securities

Corporate Presentation March 2008 Safe Harbor Act This presentation contains certain statements that are, or may be deemed to be, forward-looking statements within the meaning of Section 27A of the Securities

Natural Gas Supply, Demand, and the Prospects for North American LNG Exports

Natural Gas Supply, Demand, and the Prospects for North American LNG Exports December 3 rd, 2014 Robert D. Stibolt Senior Managing Director Observations on natural gas prices and project returns Price

Natural Gas Supply, Demand, and the Prospects for North American LNG Exports December 3 rd, 2014 Robert D. Stibolt Senior Managing Director Observations on natural gas prices and project returns Price

Cheniere Energy October 2013

Cheniere Energy October 2013 Forward Looking Statements 2 This presentation contains certain statements that are, or may be deemed to be, forward-looking statements within the meaning of Section 27A of

Cheniere Energy October 2013 Forward Looking Statements 2 This presentation contains certain statements that are, or may be deemed to be, forward-looking statements within the meaning of Section 27A of

TEEKAY LNG PARTNERS Q EARNINGS AND BUSINESS OUTLOOK PRESENTATION February 18, 2016

TEEKAY LNG PARTNERS Q4-2015 EARNINGS AND BUSINESS OUTLOOK PRESENTATION February 18, 2016 Forward Looking Statement This presentation contains forward-looking statements (as defined in Section 21E of the

TEEKAY LNG PARTNERS Q4-2015 EARNINGS AND BUSINESS OUTLOOK PRESENTATION February 18, 2016 Forward Looking Statement This presentation contains forward-looking statements (as defined in Section 21E of the

An Overview of U.S. Liquefied Natural Gas Exports

Executive Brief An Overview of U.S. Liquefied Natural Gas Exports Executive Summary The world is competing for the tremendous advantage offered by affordable U.S. natural gas. Relative to globally expensive

Executive Brief An Overview of U.S. Liquefied Natural Gas Exports Executive Summary The world is competing for the tremendous advantage offered by affordable U.S. natural gas. Relative to globally expensive

Natural Gas: Challenges for the Industry, the LNG Chain, and Implications for Market Structure

27 September 216 Algiers Natural Gas: Challenges for the Industry, the LNG Chain, and Implications for Market Structure Plenary Session 2 Introduction Market context Session objectives Low gas prices across

27 September 216 Algiers Natural Gas: Challenges for the Industry, the LNG Chain, and Implications for Market Structure Plenary Session 2 Introduction Market context Session objectives Low gas prices across

Today s Presentation Update on US LNG projects U.S. Gas Market Overview Impact of U.S. LNG on Global LNG Dynamics Sabine Pass First Cargo: 24 th Feb 2

CHENIERE ENERGY, INC. LNG Market Outlook and US LNG s Function - The Perspective from Cheniere IEEJ 2 October 217 Andrew Walker VP Strategy and Communication Today s Presentation Update on US LNG projects

CHENIERE ENERGY, INC. LNG Market Outlook and US LNG s Function - The Perspective from Cheniere IEEJ 2 October 217 Andrew Walker VP Strategy and Communication Today s Presentation Update on US LNG projects

The Evolving Global LNG Industry South Africa Gas Options, Cape Town, 3 rd 5 th October 2016

The Evolving Global LNG Industry South Africa Gas Options, Cape Town, 3 rd 5 th October 2016 John Mauel Head of Energy Transactions, United States Norton Rose Fulbright US LLP An industry in transformation

The Evolving Global LNG Industry South Africa Gas Options, Cape Town, 3 rd 5 th October 2016 John Mauel Head of Energy Transactions, United States Norton Rose Fulbright US LLP An industry in transformation

IHS LATIN AMERICA LPG SEMINAR

ENTERPRISE PRODUCTS PARTNERS L.P. IHS LATIN AMERICA LPG SEMINAR November 8, 2016 Joseph Fasullo Manager, International NGLs ALL RIGHTS RESERVED. ENTERPRISE PRODUCTS PARTNERS L.P. enterpriseproducts.com

ENTERPRISE PRODUCTS PARTNERS L.P. IHS LATIN AMERICA LPG SEMINAR November 8, 2016 Joseph Fasullo Manager, International NGLs ALL RIGHTS RESERVED. ENTERPRISE PRODUCTS PARTNERS L.P. enterpriseproducts.com

The Shale Invasion: Will U.S. LNG Cross the Pond? New terminals ramp up exports.

? The Shale Invasion: Will U.S. LNG Cross the Pond? New terminals ramp up exports. Morningstar Commodities Research 6 December 2016 Sandy Fielden Director, Oil and Products Research +1 512 431-8044 sandy.fielden@morningstar.com

? The Shale Invasion: Will U.S. LNG Cross the Pond? New terminals ramp up exports. Morningstar Commodities Research 6 December 2016 Sandy Fielden Director, Oil and Products Research +1 512 431-8044 sandy.fielden@morningstar.com

US LNG Export Growth and the Benefits to Midstream

US LNG Export Growth and the Benefits to Midstream July 2018 The US is on the brink of adding significant LNG export capacity in 2019 and becoming a sizable player in the global LNG market. In 2017, the

US LNG Export Growth and the Benefits to Midstream July 2018 The US is on the brink of adding significant LNG export capacity in 2019 and becoming a sizable player in the global LNG market. In 2017, the

Investor Presentation

Investor Presentation First nine months 2017 activity update October 18, 2017 Disclaimer This document is strictly confidential. Any unauthorised access to, appropriation of, copying, modification, use

Investor Presentation First nine months 2017 activity update October 18, 2017 Disclaimer This document is strictly confidential. Any unauthorised access to, appropriation of, copying, modification, use

Summary LNG, an increasingly important energy option in Asia and the rest of the world But challenges remain for LNG to play an expected bigger role S

Prospect and Challenges in the World and Asian LNG Market LNG Producer Consumer Conference September 19, 2012 The Institute of Energy Economics Japan Ken Koyama 0 Summary LNG, an increasingly important

Prospect and Challenges in the World and Asian LNG Market LNG Producer Consumer Conference September 19, 2012 The Institute of Energy Economics Japan Ken Koyama 0 Summary LNG, an increasingly important

HGAP. Haynesville Global Access Pipeline. Tellurian Midstream Group April 2018

HGAP Haynesville Global Access Pipeline Tellurian Midstream Group April 2018 Cautionary statements Forward looking statements The information in this presentation includes forward-looking statements within

HGAP Haynesville Global Access Pipeline Tellurian Midstream Group April 2018 Cautionary statements Forward looking statements The information in this presentation includes forward-looking statements within

Corporate presentation. October 2017

Corporate presentation October 2017 Cautionary statements Forward looking statements The information in this presentation includes forward-looking statements within the meaning of Section 27A of the Securities

Corporate presentation October 2017 Cautionary statements Forward looking statements The information in this presentation includes forward-looking statements within the meaning of Section 27A of the Securities

17 th INTERNATIONAL CONFERENCE & EXHIBITION ON LIQUEFIED NATURAL GAS (LNG 17)

") 17 th INTERNATIONAL CONFERENCE & EXHIBITION ON LIQUEFIED NATURAL GAS (LNG 17) 17 th INTERNATIONAL CONFERENCE & EXHIBITION ON LIQUEFIED NATURAL GAS (LNG 17)

17 th INTERNATIONAL CONFERENCE & EXHIBITION ON LIQUEFIED NATURAL GAS (LNG 17) 17 th INTERNATIONAL CONFERENCE & EXHIBITION ON LIQUEFIED NATURAL GAS (LNG 17)

LNG Impact on U.S. Domestic Natural Gas Markets

LNG Impact on U.S. Domestic Natural Gas Markets Disclaimer This presentation contains statements about future events and expectations that can be characterized as forward-looking statements, including,

LNG Impact on U.S. Domestic Natural Gas Markets Disclaimer This presentation contains statements about future events and expectations that can be characterized as forward-looking statements, including,

LNG strategy and the outlook for global gas markets

LNG strategy and the outlook for global gas markets October 16 th, 2012 Jean-Marie Dauger Executive Vice-president GDF SUEZ The LNG market Strong growth particularly in Asia An LNG market of ~550 Mt in

LNG strategy and the outlook for global gas markets October 16 th, 2012 Jean-Marie Dauger Executive Vice-president GDF SUEZ The LNG market Strong growth particularly in Asia An LNG market of ~550 Mt in

Background, Issues, and Trends in Underground Hydrocarbon Storage

Background, Issues, and Trends in Underground Hydrocarbon Storage David E. Dismukes Center for Energy Studies Louisiana State University Environmental Permitting Class January 29, 2009 Description of the

Background, Issues, and Trends in Underground Hydrocarbon Storage David E. Dismukes Center for Energy Studies Louisiana State University Environmental Permitting Class January 29, 2009 Description of the

LNG Shipping: How Long Will The Good Times Last?

LNG Shipping: How Long Will The Good Times Last? Poten & Partners November 1 HOUSTON NEW YORK LONDON ATHENS SINGAPORE GUANGZHOU PERTH A GLOBAL BROKER AND COMMERCIAL ADVISOR FOR THE ENERGY AND OCEAN TRANSPORTATION

LNG Shipping: How Long Will The Good Times Last? Poten & Partners November 1 HOUSTON NEW YORK LONDON ATHENS SINGAPORE GUANGZHOU PERTH A GLOBAL BROKER AND COMMERCIAL ADVISOR FOR THE ENERGY AND OCEAN TRANSPORTATION

LNG Exports in the Pacific Northwest Jordan Cove Update

LNG Exports in the Pacific Northwest Jordan Cove Update Pacific Northwest Economic Region 27 th Annual Summit July 25, 2017 Portland, Oregon Betsy Spomer Executive Vice-President, Veresen President & CEO,

LNG Exports in the Pacific Northwest Jordan Cove Update Pacific Northwest Economic Region 27 th Annual Summit July 25, 2017 Portland, Oregon Betsy Spomer Executive Vice-President, Veresen President & CEO,

Markets and Opportunities. Paul Burgener March 2015

Markets and Opportunities Paul Burgener March 2015 Disclaimer Copyright BP Energy Company. All rights reserved. Contents of this presentation do not necessarily reflect the Company s views. This presentation

Markets and Opportunities Paul Burgener March 2015 Disclaimer Copyright BP Energy Company. All rights reserved. Contents of this presentation do not necessarily reflect the Company s views. This presentation

North America OECD Europe Asia Pacific

Australian LNG: Asia s natural supplier of LNG Peter Cleary, Vice President LNG Markets and Eastern Australia Commercial AJBCC: 52nd Australia-Japan Joint Business Conference Plenary Session Four: Energy

Australian LNG: Asia s natural supplier of LNG Peter Cleary, Vice President LNG Markets and Eastern Australia Commercial AJBCC: 52nd Australia-Japan Joint Business Conference Plenary Session Four: Energy

Cheniere Energy October 2011

Cheniere Energy October 2011 Forward Looking Statements This presentation contains certain statements that are, or may be deemed to be, forward-looking statements within the meaning of Section 27A of the

Cheniere Energy October 2011 Forward Looking Statements This presentation contains certain statements that are, or may be deemed to be, forward-looking statements within the meaning of Section 27A of the

U.S. Natural Gas and the Potential for LNG Export Growth

U.S. Natural Gas and the Potential for LNG Export Growth Presentation to: 2018 Wyoming Oil & Gas Fair By: John Harpole September 12, 2018 It is not a scarce resource anymore 2 US RIG COUNTS: Aug 2018

U.S. Natural Gas and the Potential for LNG Export Growth Presentation to: 2018 Wyoming Oil & Gas Fair By: John Harpole September 12, 2018 It is not a scarce resource anymore 2 US RIG COUNTS: Aug 2018

North American Gas: A dynamic environment. Josh McCall BP North American Gas and Power November 16, 2011

North American Gas: A dynamic environment Josh McCall BP North American Gas and Power November 16, 2011 Disclaimer Copyright BP Energy Company. All rights reserved. Contents of this presentation do not

North American Gas: A dynamic environment Josh McCall BP North American Gas and Power November 16, 2011 Disclaimer Copyright BP Energy Company. All rights reserved. Contents of this presentation do not

Changes are Coming: The Emergence of U.S. LNG Exports

OCTOBER 25 TH 2016 Changes are Coming: The Emergence of U.S. LNG Exports 34 th USAEE/IAEE North American Conference Tulsa, Oklahoma Where Are We Today? 1. The Global LNG Market & Emergence of US Volumes

OCTOBER 25 TH 2016 Changes are Coming: The Emergence of U.S. LNG Exports 34 th USAEE/IAEE North American Conference Tulsa, Oklahoma Where Are We Today? 1. The Global LNG Market & Emergence of US Volumes

Höegh LNG The floating LNG services provider. Company and Market Update May 2012

Höegh LNG The floating LNG services provider Company and Market Update May 2012 Forward looking statements This presentation contains forward-looking statements which reflects management s current expectations,

Höegh LNG The floating LNG services provider Company and Market Update May 2012 Forward looking statements This presentation contains forward-looking statements which reflects management s current expectations,

U.S. Natural Gas and the Poten3al for LNG Export Growth

U.S. Natural Gas and the Poten3al for LNG Export Growth Presentation to: 2018 Wyoming Oil & Gas Fair By: John Harpole September 12, 2018 It is not a scarce resource anymore 2 US RIG COUNTS: Aug 2018 vs

U.S. Natural Gas and the Poten3al for LNG Export Growth Presentation to: 2018 Wyoming Oil & Gas Fair By: John Harpole September 12, 2018 It is not a scarce resource anymore 2 US RIG COUNTS: Aug 2018 vs

LNG Market Trends & Price Transparency

LNG Market Trends & Price Transparency Tokyo Fiona Poynter April 2015 London Houston Washington New York Portland Calgary Santiago Bogota Rio de Janeiro Singapore Beijing Tokyo Sydney Dubai Moscow Astana

LNG Market Trends & Price Transparency Tokyo Fiona Poynter April 2015 London Houston Washington New York Portland Calgary Santiago Bogota Rio de Janeiro Singapore Beijing Tokyo Sydney Dubai Moscow Astana

Natural Gas & LNG Fundamentals. Greg Kist Vice President, Marketing, Corporate & Government Relations

Natural Gas & LNG Fundamentals Greg Kist Vice President, Marketing, Corporate & Government Relations Marketing & Risk Management Strategy Hedge up to 50% of production currently focused on protecting AECO

Natural Gas & LNG Fundamentals Greg Kist Vice President, Marketing, Corporate & Government Relations Marketing & Risk Management Strategy Hedge up to 50% of production currently focused on protecting AECO

DEFINITIONS AND CAUTIONARY NOTE Resources: Our use of the term resources in this presentation includes quantities of oil and gas not yet classified as

NEW TECHNOLOGY FOR GAS PRODUCTION The Critical Role of Innovation in Meeting the Supply Challenge De la Rey Venter Global Head of LNG 1 DEFINITIONS AND CAUTIONARY NOTE Resources: Our use of the term resources

NEW TECHNOLOGY FOR GAS PRODUCTION The Critical Role of Innovation in Meeting the Supply Challenge De la Rey Venter Global Head of LNG 1 DEFINITIONS AND CAUTIONARY NOTE Resources: Our use of the term resources

AIChE: Natural Gas Utilization Workshop Overcoming Hurdles of Technology Implementation

AIChE: Natural Gas Utilization Workshop Overcoming Hurdles of Technology Implementation Natural Gas in the United States: An Overview of Resources and Factors Affecting the Market November 2, 216 Justin

AIChE: Natural Gas Utilization Workshop Overcoming Hurdles of Technology Implementation Natural Gas in the United States: An Overview of Resources and Factors Affecting the Market November 2, 216 Justin

LNG: DEVELOPMENTS GLOBALLY AND IN EUROPE. Roger Bounds Vice President Global Gas at Shell 17 th March 2016

LNG: DEVELOPMENTS GLOBALLY AND IN EUROPE Roger Bounds Vice President Global Gas at Shell 17 th March 2016 Copyright of Copyright Royal Dutch of COMPANY Shell plc NAME 1 DEFINITIONS AND CAUTIONARY NOTE

LNG: DEVELOPMENTS GLOBALLY AND IN EUROPE Roger Bounds Vice President Global Gas at Shell 17 th March 2016 Copyright of Copyright Royal Dutch of COMPANY Shell plc NAME 1 DEFINITIONS AND CAUTIONARY NOTE

LNG as a global market ESCP London School London, September 22nd, 2015 GUY BROGGI SENIOR ADVISOR, LNG DIVISON

LNG as a global market ESCP London School London, September 22nd, 2015 GUY BROGGI SENIOR ADVISOR, LNG DIVISON Today s Menu (and take-aways ) Latest changes in the LNG landscape 2014 was a continuation

LNG as a global market ESCP London School London, September 22nd, 2015 GUY BROGGI SENIOR ADVISOR, LNG DIVISON Today s Menu (and take-aways ) Latest changes in the LNG landscape 2014 was a continuation

Corporate presentation. June 2017

Corporate presentation June 2017 Cautionary statement Forward looking statement Non-GAAP financial measures The information in this presentation includes forward-looking statements within the meaning of

Corporate presentation June 2017 Cautionary statement Forward looking statement Non-GAAP financial measures The information in this presentation includes forward-looking statements within the meaning of

The Shifting Sands of Natural Gas Abundance

August 17, 2016 The Shifting Sands of Natural Gas Abundance Richard Meyer Manager, Energy Analysis & Standards Here s how global energy changed between 2014 and 2015. Winners were oil, natural gas, renewables.

August 17, 2016 The Shifting Sands of Natural Gas Abundance Richard Meyer Manager, Energy Analysis & Standards Here s how global energy changed between 2014 and 2015. Winners were oil, natural gas, renewables.

Disclaimer & Important Notice

GLNG Project FID 13 January 2011 1 Disclaimer & Important Notice This presentation contains forward looking statements that are subject to risk factors associated with the oil and gas industry. It is believed

GLNG Project FID 13 January 2011 1 Disclaimer & Important Notice This presentation contains forward looking statements that are subject to risk factors associated with the oil and gas industry. It is believed

Corporate presentation. January 2019

Corporate presentation January 2019 Cautionary statements Forward-looking statements The information in this presentation includes forward-looking statements within the meaning of Section 27A of the Securities

Corporate presentation January 2019 Cautionary statements Forward-looking statements The information in this presentation includes forward-looking statements within the meaning of Section 27A of the Securities

The Uncertain Future For ANS LNG Exports

The Uncertain Future For ANS LNG Exports Presented to: LSI Energy in Alaska Conference Anchorage, AK Presented by: Paul R. Carpenter Steven H. Levine Anul Thapa The Brattle Group 44 Brattle Street Cambridge,

The Uncertain Future For ANS LNG Exports Presented to: LSI Energy in Alaska Conference Anchorage, AK Presented by: Paul R. Carpenter Steven H. Levine Anul Thapa The Brattle Group 44 Brattle Street Cambridge,

CenterPoint Energy Services. Current Market Fundamentals June 27, 2013

CenterPoint Energy Services Current Market Fundamentals June 27, 2013 CenterPoint Energy is one of the largest combined electric and natural gas delivery companies in the U.S. Asset portfolio CNP Footprint

CenterPoint Energy Services Current Market Fundamentals June 27, 2013 CenterPoint Energy is one of the largest combined electric and natural gas delivery companies in the U.S. Asset portfolio CNP Footprint

LNG Exports A Story of American Innovation and Opportunity. Tyler Energy Summit Jason French March 31, 2014

LNG Exports A Story of American Innovation and Opportunity Tyler Energy Summit Jason French March 31, 2014 Forward Looking Statements This presentation contains certain statements that are, or may be deemed

LNG Exports A Story of American Innovation and Opportunity Tyler Energy Summit Jason French March 31, 2014 Forward Looking Statements This presentation contains certain statements that are, or may be deemed

International gas markets: recent developments and prospects

International gas markets: recent developments and prospects Christopher Allsopp New College Oxford Director, Oxford Institute for Energy Studies December 2012 International gas markets are changing rapidly

International gas markets: recent developments and prospects Christopher Allsopp New College Oxford Director, Oxford Institute for Energy Studies December 2012 International gas markets are changing rapidly

Brian A. Habacivch Constellation, Commodities Management Group October 20, 2018

North American Energy Outlook The Transformative Role of Shale in the Global Hydrocarbons Market Why It Matters to Commercial, Institutional, and Industrial End Users Brian A. Habacivch Constellation,

North American Energy Outlook The Transformative Role of Shale in the Global Hydrocarbons Market Why It Matters to Commercial, Institutional, and Industrial End Users Brian A. Habacivch Constellation,

Copyright 2018 RBN Energy. Permian Global Access Pipeline (PGAP) Natural Gas Market Analysis

Natural Gas Market Analysis") Permian Global Access Pipeline (PGAP) Natural Gas Market Analysis Permian Global Access Pipeline (PGAP)» Natural gas production growth in the Permian will continue to accelerate, resulting in outbound

Permian Global Access Pipeline (PGAP) Natural Gas Market Analysis Permian Global Access Pipeline (PGAP)» Natural gas production growth in the Permian will continue to accelerate, resulting in outbound

Natural Gas Market Update

Natural Gas Market Update John Jicha - MGE Director - Energy Supply and Trading Madison Gas and Electric Company Agenda What a difference ten years can make Low prices Fundamental factors impacting the

Natural Gas Market Update John Jicha - MGE Director - Energy Supply and Trading Madison Gas and Electric Company Agenda What a difference ten years can make Low prices Fundamental factors impacting the

The impact of US LNG on European gas prices

January 2018 The impact of US LNG on European gas prices Increasing US exports of LNG will change how gas prices are determined in Europe Import dependency for the European Union, pushed higher as a result

January 2018 The impact of US LNG on European gas prices Increasing US exports of LNG will change how gas prices are determined in Europe Import dependency for the European Union, pushed higher as a result

Edgardo Curcio President AIEE

Edgardo Curcio President AIEE The First National Conference on Liquefied Natural Gas for Transports - Italy and the Mediterranean Sea April 11, 2013 What is LNG? The LNG (Liquefied Natural Gas) is a fluid

Edgardo Curcio President AIEE The First National Conference on Liquefied Natural Gas for Transports - Italy and the Mediterranean Sea April 11, 2013 What is LNG? The LNG (Liquefied Natural Gas) is a fluid

Covington, LA ~ May 2018

LOUISIANA ~ UNO Economic Outlook & Real Estate Forecast Seminar Covington, LA ~ May 2018 Louisiana is in the midst of an industrial boom unlike any other in our history, with over $110 billion in industrial

LOUISIANA ~ UNO Economic Outlook & Real Estate Forecast Seminar Covington, LA ~ May 2018 Louisiana is in the midst of an industrial boom unlike any other in our history, with over $110 billion in industrial

Third Quarter 2011 Presentation of financial results 30 November 2011

Höegh LNG The floating LNG services provider Third Quarter 2011 Presentation of financial results 30 November 2011 Forward looking statements This presentation contains forward-looking statements which

Höegh LNG The floating LNG services provider Third Quarter 2011 Presentation of financial results 30 November 2011 Forward looking statements This presentation contains forward-looking statements which

North American Gas Outlook. Jen Snyder Head of North American Gas Research Wood Mackenzie

North American Gas Outlook Jen Snyder Head of North American Gas Research Wood Mackenzie 2011 Summer Seminar August 1, 2011 End of study area 31 N 32 N $/mmbtu 33 N Resource Doesn t Always Meet Expectations

North American Gas Outlook Jen Snyder Head of North American Gas Research Wood Mackenzie 2011 Summer Seminar August 1, 2011 End of study area 31 N 32 N $/mmbtu 33 N Resource Doesn t Always Meet Expectations

Kitimat LNG Pacific Trail Pipeline

Kitimat LNG Pacific Trail Pipeline Premier s B.C. Natural Resource Forum Rod Maier, Chevron Canada Limited January 23, 2014 Cautionary Statement CAUTIONARY STATEMENT RELEVANT TO FORWARD-LOOKING INFORMATION

Kitimat LNG Pacific Trail Pipeline Premier s B.C. Natural Resource Forum Rod Maier, Chevron Canada Limited January 23, 2014 Cautionary Statement CAUTIONARY STATEMENT RELEVANT TO FORWARD-LOOKING INFORMATION

ROYAL DUTCH SHELL PLC LNG CANADA FINAL INVESTMENT DECISION

OCTOBER 2 ND 2018 ROYAL DUTCH SHELL PLC WEBCAST TO MEDIA AND ANALYSTS BY JESSICA UHL, CHIEF FINANCIAL OFFICER OF ROYAL DUTCH SHELL PLC, MAARTEN WETSELAAR, INTEGRATED GAS AND NEW ENERGIES DIRECTOR OF ROYAL

OCTOBER 2 ND 2018 ROYAL DUTCH SHELL PLC WEBCAST TO MEDIA AND ANALYSTS BY JESSICA UHL, CHIEF FINANCIAL OFFICER OF ROYAL DUTCH SHELL PLC, MAARTEN WETSELAAR, INTEGRATED GAS AND NEW ENERGIES DIRECTOR OF ROYAL

Trends, Issues and Market Changes for Crude Oil and Natural Gas

Trends, Issues and Market Changes for Crude Oil and Natural Gas East Iberville Community Advisory Panel Meeting Syngenta September 26, 2012 Center for Energy Studies David E. Dismukes, Ph.D. Center for

Trends, Issues and Market Changes for Crude Oil and Natural Gas East Iberville Community Advisory Panel Meeting Syngenta September 26, 2012 Center for Energy Studies David E. Dismukes, Ph.D. Center for

Liquefied Natural Gas Limited

Liquefied Natural Gas Limited Greg Vesey Managing Director and Chief Executive Officer Who s Going To Jump In First? North American Gas Forum October 2, 2017 ASX: LNG and OTC ADR: LNGLY Forward looking

Liquefied Natural Gas Limited Greg Vesey Managing Director and Chief Executive Officer Who s Going To Jump In First? North American Gas Forum October 2, 2017 ASX: LNG and OTC ADR: LNGLY Forward looking

Atlantic LNG: Has the boat sailed? Is the US out of the LNG trade and what are the implications for Europe?

Atlantic LNG: Has the boat sailed? Is the US out of the LNG trade and what are the implications for Europe? James Osten Principal North American Energy Markets LNG Trade Different for U.S. Than Europe

Atlantic LNG: Has the boat sailed? Is the US out of the LNG trade and what are the implications for Europe? James Osten Principal North American Energy Markets LNG Trade Different for U.S. Than Europe

Will the growth of LNG create a global gas market?

Will the growth of LNG create a global gas market? Chris Evans Vice President Global LNG Supply Shell Gas & Power FLAME, Amsterdam 25 th February 25 Increasing choice for consumers and producers Environmental

Will the growth of LNG create a global gas market? Chris Evans Vice President Global LNG Supply Shell Gas & Power FLAME, Amsterdam 25 th February 25 Increasing choice for consumers and producers Environmental

Platts 8 th Annual Pipeline Development & Expansion Conference. Gas-Electric Coordination Update

Platts 8 th Annual Pipeline Development & Expansion Conference Gas-Electric Coordination Update Anders Johnson, Director System Design KinderMorgan Pipelines September 17, 2013 Hilton Houston Post Oak,

Platts 8 th Annual Pipeline Development & Expansion Conference Gas-Electric Coordination Update Anders Johnson, Director System Design KinderMorgan Pipelines September 17, 2013 Hilton Houston Post Oak,

Western Oklahoma Residue Takeaway Impact of Growing SCOOP/STACK Supply

Western Oklahoma Residue Takeaway Impact of Growing SCOOP/STACK Supply Craig Harris Executive Vice President & Chief Commercial Officer October 28, 2016 Forward-looking Statements This presentation and

Western Oklahoma Residue Takeaway Impact of Growing SCOOP/STACK Supply Craig Harris Executive Vice President & Chief Commercial Officer October 28, 2016 Forward-looking Statements This presentation and

[LNG MARKET ANALYSIS ] 1. LNG Market Analysis

![[LNG MARKET ANALYSIS ] 1. LNG Market Analysis](/thumbs/83/87599942.jpg "[LNG MARKET ANALYSIS ] 1. LNG Market Analysis") [LNG MARKET ANALYSIS ] 1 LNG Market Analysis LNG Market Analysis Volume: 20 th April 2018 LNG and Natural Gas Price Assessment 14 th 20 th April 2018 [LNG MARKET ANALYSIS ] 2 LNG Analysis Global LNG prices

[LNG MARKET ANALYSIS ] 1 LNG Market Analysis LNG Market Analysis Volume: 20 th April 2018 LNG and Natural Gas Price Assessment 14 th 20 th April 2018 [LNG MARKET ANALYSIS ] 2 LNG Analysis Global LNG prices

38th Annual Alaska Resources Conference

38th Annual Alaska Resources Conference November 16, 2017 Keith Meyer 1 AGDC JOINT AGREEMENT Pence 2 PRESENTATION OVERVIEW Alaska LNG system economic overview. China agreement; implications for Alaska

38th Annual Alaska Resources Conference November 16, 2017 Keith Meyer 1 AGDC JOINT AGREEMENT Pence 2 PRESENTATION OVERVIEW Alaska LNG system economic overview. China agreement; implications for Alaska

Corporate presentation. March 2018

Corporate presentation March 2018 Cautionary statements Forward looking statements The information in this presentation includes forward-looking statements within the meaning of Section 27A of the Securities

Corporate presentation March 2018 Cautionary statements Forward looking statements The information in this presentation includes forward-looking statements within the meaning of Section 27A of the Securities

ENERGY OUTLOOK 2017 FALL/WINTER

ENERGY OUTLOOK 2017 FALL/WINTER With more than 105 years in the energy industry, BOK Financial is committed to helping you succeed. In this issue of the Energy Outlook, you ll learn more about the current

ENERGY OUTLOOK 2017 FALL/WINTER With more than 105 years in the energy industry, BOK Financial is committed to helping you succeed. In this issue of the Energy Outlook, you ll learn more about the current

Corporate presentation. January 2018

Corporate presentation January 2018 Cautionary statements Forward looking statements The information in this presentation includes forward-looking statements within the meaning of Section 27A of the Securities

Corporate presentation January 2018 Cautionary statements Forward looking statements The information in this presentation includes forward-looking statements within the meaning of Section 27A of the Securities

Liquefied Natural Gas Limited

Liquefied Natural Gas Limited Greg Vesey Managing Director and Chief Executive Officer LNG Exports - Perspectives North American Gas Forum - 3 October 2016 ASX: LNG and OTC ADR: LNGLY Forward looking statement

Liquefied Natural Gas Limited Greg Vesey Managing Director and Chief Executive Officer LNG Exports - Perspectives North American Gas Forum - 3 October 2016 ASX: LNG and OTC ADR: LNGLY Forward looking statement

Liquefied Natural Gas Limited

Liquefied Natural Gas Limited Greg Vesey Managing Director and Chief Executive Officer LNG Exports - Perspectives North American Gas Forum - 3 October 2016 ASX: LNG and OTC ADR: LNGLY Forward looking statement

Liquefied Natural Gas Limited Greg Vesey Managing Director and Chief Executive Officer LNG Exports - Perspectives North American Gas Forum - 3 October 2016 ASX: LNG and OTC ADR: LNGLY Forward looking statement

PBF Energy. State College, PA. North East Association of Rail Shippers Fall Conference. October 1, 2014

PBF Energy North East Association of Rail Shippers Fall Conference State College, PA October 1, 2014 Safe Harbor Statements This presentation contains forward-looking statements made by PBF Energy Inc.

PBF Energy North East Association of Rail Shippers Fall Conference State College, PA October 1, 2014 Safe Harbor Statements This presentation contains forward-looking statements made by PBF Energy Inc.

Rice Global E&C Forum

Rice Global E&C Forum "Will Shale revolution trigger game changes in Asian Energy Market and LNG?" Tevin Vongvanich President and Chief Executive Officer PTT Exploration and Production Public Company Limited

Rice Global E&C Forum "Will Shale revolution trigger game changes in Asian Energy Market and LNG?" Tevin Vongvanich President and Chief Executive Officer PTT Exploration and Production Public Company Limited

Shale Gas & Oil: Global Implications for our Energy Future

Shale Gas & Oil: Global Implications for our Energy Future Dr Basim Faraj Faraj Consultants Pty Ltd Brisbane, Australia Petroleum Exploration Society of Australia (PESA) (Queensland Branch) Hilton Hotel

Shale Gas & Oil: Global Implications for our Energy Future Dr Basim Faraj Faraj Consultants Pty Ltd Brisbane, Australia Petroleum Exploration Society of Australia (PESA) (Queensland Branch) Hilton Hotel

216 IEEJ216 Key points of this report Oversupply in the international LNG market will expand further in the coming years. Upstream industry is cutting

216 IEEJ216 423 rd Forum on Research Works on July 26, 216 Outlook for Gas Market The Institute of Energy Economics, Japan Yoshikazu Kobayashi Senior Economist, Manager, Gas Group, Fossil Fuels & Electric

216 IEEJ216 423 rd Forum on Research Works on July 26, 216 Outlook for Gas Market The Institute of Energy Economics, Japan Yoshikazu Kobayashi Senior Economist, Manager, Gas Group, Fossil Fuels & Electric

Anadarko LNG and China

Anadarko LNG and China Scott Moore Vice President Worldwide Marketing US-China Oil and Gas Industry Forum September 26, 2014 Regarding Forward-Looking Statements and Other Matters This presentation contains

Anadarko LNG and China Scott Moore Vice President Worldwide Marketing US-China Oil and Gas Industry Forum September 26, 2014 Regarding Forward-Looking Statements and Other Matters This presentation contains

The Really Big Game Changer: Crude Oil Production from Shale Resources and the Tuscaloosa Marine Shale

The Really Big Game Changer: Crude Oil Production from Shale Resources and the Tuscaloosa Marine Shale Baton Rouge Chamber of Commerce Regional Stakeholders Breakfast June 27, 2012 Center for Energy Studies

The Really Big Game Changer: Crude Oil Production from Shale Resources and the Tuscaloosa Marine Shale Baton Rouge Chamber of Commerce Regional Stakeholders Breakfast June 27, 2012 Center for Energy Studies

Evaluating the Impacts of Market Shifts on Local Markets and Assets. Ron Norman May 20, 2009

Evaluating the Impacts of Market Shifts on Local Markets and Assets Ron Norman May 20, 2009 Gas market outlooks are only one component of an effective marketing or procurement strategy Agenda Gas Market

Evaluating the Impacts of Market Shifts on Local Markets and Assets Ron Norman May 20, 2009 Gas market outlooks are only one component of an effective marketing or procurement strategy Agenda Gas Market