T ( P ( ) * FA F D A S

|

|

|

- Simon Paul

- 6 years ago

- Views:

Transcription

1 Supply and Demand Basics Law of Supply Law of Demand Equilibrium Key Topics Demand Supply Equilibrium (shortage/surplus) Floor/Ceiling Elasticity Indifference Curves Utility Physical Product (Supply Side) Cost Curves (Supply Side) Demand 1

2 Determinants of Demand Factors other than Price Income Tastes (Preferences) *FADS Prices of Related Goods Substitutes or Complements Expectations Number of Buyer International Effects 2

3 Supply Determinants of Supply Factors other than Price Price of Resources (inputs) Land, Labor, Capital, Entrepreneurship Technology Productivity Expectations Number of Producers Prices of Related Goods/Services International Effects Supply Change/Shift 3

4 Increase in Supply General Equilibrium Changes in Eq 4

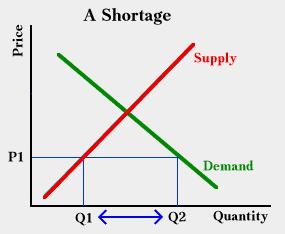

5 Surplus Shortage Price Floor 5

6 Price Ceiling Supply and Demand A Theory of Price The theory of supply and demand is a theory of price and output in "highly competitive" markets. Adam Smith had argued that each good or service has a "natural price." If the price (of beer, for example), were above the natural price, then more resources would be attracted into the trade (brewing, in the example), and the price would return to its "natural" level. Conversely if the price began below its "natural" level. Supply and Demand Two Sides Like a good controversy, every market has two sides. In this case, the two sides are (obviously?) buyers and sellers. The buyers are the "demand side" of the market. Sellers are the "supply side" of the market. Alfred Marshall compared the supply and demand sides to the two blades of scissors -- one won't cut. You have to have both. 6

7 Equilibrium of Supply and Demand In economic theory, the interaction of supply and demand is understood as equilibrium. Market "equilibrium" exists when the price is high enough so that the quantity supplied just equals the quantity demanded. In a diagram, the "equilibrium" price is the price at which the demand and supply curves cross. The corresponding quantity is the quantity that would be traded in a market equilibrium. Elasticity Cross-Price Elasticity The Cross-Price Elasticity of Demand measures the rate of response of quantity demanded of one good, due to a price change of another good. If two goods are substitutes, we should expect to see consumers purchase more of one good when the price of its substitute increases. 7

8 Complements if the two goods are complements, we should see a price rise in one good cause the demand for both goods to fall. Your course may use the more complicated Arc Cross-Price Elasticity of Demand formula. Calculating the Cross-Price Elasticity of Demand CPEoD = (% Change in Quantity Demand for Good X)/ (% Change in Price for Good Y) Income Elasticity The Income Elasticity of Demand measures the rate of response of quantity demand due to a raise (or lowering) in a consumers income. 8

9 IEoD = Formula (% Change in Quantity Demanded)/ (% Change in Income) Indifference Curves Indifferent curves The aim of indifference curve analysis is to analyze how a rational consumer chooses between two goods. In other words, how the change in the wage rate will affect the choice between leisure time and work time. Indifference analysis combines two concepts; indifference curves and budget lines (constraints) The indifference curve An indifference curve is a line that shows all the possible combinations of two goods between which a person is indifferent. In other words, it is a line that shows the consumption of different combinations of two goods that will give the same utility (satisfaction) to the person. For instance, in Figure 1 the indifference curve is I1. A person would receive the same utility (satisfaction) from consuming 4 hours of work and 6 hours of leisure, as they would if they consumed 7 hours of work and 3 hours of leisure. Figure 1: An indifference curve for work and leisure 9

10 Work vs. Leisure Shapes The shape of the indifference curve Figure 1 highlights that the shape of the indifference curve is not a straight line. It is conventional to draw the curve as bowed. This is due to the concept of the diminishing marginal rate of substitution between the two goods. The marginal rate of substitution is the amount of one good (i.e. work) that has to be given up if the consumer is to obtain one extra unit of the other good (leisure). More Indifference Curves The marginal rate of substitution (MRS) = change in good X / change in good Y The relationship between marginal utility and the marginal rate of substitution is often summarised with the following equation; MRS = Mux / Muy It is possible to draw more than one indifference curve on the same diagram. If this occurs then it is termed an indifference curve map (Figure 2). 10

11 Effects of Change The substitution effect The substitution effect is when the consumer switches consumption patterns due to the price change alone but remains on the same indifference curve. To identify the substitution effect a new budget line needs to be constructed. The budget line B1* is added, this budget line needs to be parallel with the budget line B2 and tangential to I1. The income effect The income effect highlights how consumption will change due to the consumer having a change in purchasing power as a result of the price change. The higher price means the budget line is B2, hence the optimum consumption point is Q2. This point is on a lower indifference curve (I2). Multiple Curves Costs Chapter 22 11

12 Costs and Physical Product Production is simply the conversion of inputs into outputs Inefficient Efficient Cost/Ratio In economics, the cost-of-production theory of value is the theory that the price of an object is determined by the sum of the cost of the resources that went into making it. The cost can be composed of the cost of any of the factors of production including labor, capital, land, management, or even technology. Physical Product to Costs Physical Product = Output TPP = Total Output TC (Total Cost) = Total Cost for each Output ATC = Average Total Cost ATC = AFC (fixed) + AVC (variable) MC = Marginal Cost 12

13 Marginal Cost MARGINAL COST CURVE: A curve that graphically represents the relation between the marginal cost incurred by a firm in the short-run run product of a good or service and the quantity of output produced. This curve is constructed to capture the relation between marginal cost and the level of output, holding other variables like technology and resource prices constant. Three related curves are average total cost curve, average variable cost curve, and average fixed cost curve. Average Total Cost AVERAGE TOTAL COST: Total cost per unit of output, found by dividing total cost by the quantity of output. When compared with price (per unit revenue), average total cost (ATC) indicates the per unit profitability of a profit-maximizing firm. Average total cost is one of three average cost concepts important to short-run run production analysis. The other two are average fixed cost and average variable cost. A related concept is marginal cost. Average Variable Cost AVERAGE VARIABLE COST: Total variable cost per unit of output, found by dividing total variable cost by the quantity of output. When compared with price (per unit revenue), average variable cost (AVC) indicates whether or not a profit-maximizing firm should shut down production in the short run. Average variable cost is one of three average cost concepts important to short-run run production analysis. The other two are average total cost and average fixed cost. A related concept is marginal cost. 13

14 Average Fixed Costs AVERAGE FIXED COST: Total fixed cost per unit of output, found by dividing total fixed cost by the quantity of output. When compared with price (per unit revenue), average fixed cost (AFC) indicates whether or not a profit-maximizing firm should shutdown production in the short run. Average fixed cost is one of three average cost concepts important to short-run run production analysis. The other two are average total cost and average variable cost. A related concept is marginal cost. More Costs Costs, putting $ figures on resources used in production ATC (cost per unit of output) Total cost / # units output produced MC is change in costs / change in output Short run = Diminishing Marginal Returns All Cost curves have a U shape Even More Costs Variable Costs Costs that rise and fall as production Fixed Costs Costs that must be paid whether a firm produces or not 14

15 Short Run When there are fixed resources and fixed costs, the firm is operating in the short run. ATC is often referred to as SRATC Short Run (not shorter) In Economics, short-runrun refers to the decision-making time frame of a firm in which at least one factor of production is fixed. Costs which are fixed in the short-run run have no impact on a firms decisions. A generic firm can make three changes in the short-run: run: Increase production Decrease production Shut down In the short-run, run, a profit maximizing firm will: Increase production if marginal cost is less than price; Decrease production if marginal cost is greater than price; Continue producing if average variable cost is less than price, even if average total cost is greater than price; Shut down if average variable cost is greater than price. Thus, the fixed cost is the largest loss a firm can incur in the short-run. run. Long Run A firm can choose to relocate, build a new plant, or purchase additional capital only in the long run, or planning stage. LR decisions involve all SR situations All resources are variable DMR does not apply LRATC= lowest cost combination when all combination of resources are variable 15

of land, labor, raw materials, and capital goods can be assumed to vary.")

16 Long Run (even longer) In economic models, the long run time frame assumes no fixed factors of production. Firms can enter or leave the marketplace, and the cost (and availability) of land, labor, raw materials, and capital goods can be assumed to vary. In contrast, in the short run time frame, certain factors are assumed to be fixed, because there is not sufficient time for them to change. This is related to the long run average cost (LRAC) curve, an important factor in microeconomic models. Producer Consumer Surplus Consumer Surplus 16

17 Consumer Surplus Cont Consumer surplus or Consumer's surplus (or in the plural Consumers' surplus) ) is the economic gain accruing to a consumer (or consumers) when they engage in trade. The gain is the difference between the price they are willing to pay (or reservation price) and the actual price. Producer Surplus The producer surplus is the amount that producers benefit by selling at a market price that is higher than they would be willing to sell for. Note that producer surplus flows through to the owners of the factors of production, unlike economic profit which is zero under perfect competition. 17

AP Microeconomics Review With Answers

AP Microeconomics Review With Answers 1. Firm in Perfect Competition (Long-Run Equilibrium) 2. Monopoly Industry with comparison of price & output of a Perfectly Competitive Industry (which means show

AP Microeconomics Review With Answers 1. Firm in Perfect Competition (Long-Run Equilibrium) 2. Monopoly Industry with comparison of price & output of a Perfectly Competitive Industry (which means show

Microeconomics: MIE1102

TEXT CHAPTERS TOPICS 1, 2 ECONOMICS, ECONOMIC SYSTEMS, MARKET ECONOMY 3 DEMAND AND SUPPLY. MARKET EQUILIBRIUM 4 ELASTICITY OF DEMAND AND SUPPLY 5 DEMAND & CONSUMER BEHAVIOR 6 PRODUCTION FUNCTION 7 COSTS

TEXT CHAPTERS TOPICS 1, 2 ECONOMICS, ECONOMIC SYSTEMS, MARKET ECONOMY 3 DEMAND AND SUPPLY. MARKET EQUILIBRIUM 4 ELASTICITY OF DEMAND AND SUPPLY 5 DEMAND & CONSUMER BEHAVIOR 6 PRODUCTION FUNCTION 7 COSTS

= AFC + AVC = (FC + VC)

") Chapter 13-14: Marginal Product, Costs, Revenue, and Profit Production Function The relationship between the quantity of inputs (workers) and quantity of outputs Total product (TP) is the total amount

Chapter 13-14: Marginal Product, Costs, Revenue, and Profit Production Function The relationship between the quantity of inputs (workers) and quantity of outputs Total product (TP) is the total amount

Micro Semester Review Name:

Micro Semester Review Name: The following review is set up to emphasize certain concepts, graphs and terms. It is the responsibility of the individual teachers to emphasize and review the analysis aspects

Micro Semester Review Name: The following review is set up to emphasize certain concepts, graphs and terms. It is the responsibility of the individual teachers to emphasize and review the analysis aspects

Practice Exam 3: S201 Walker Fall with answers to MC

Practice Exam 3: S201 Walker Fall 2007 - with answers to MC Print Your Name: I. Multiple Choice (3 points each) 1. If marginal utility is falling then A. total utility must be falling. B. marginal utility

Practice Exam 3: S201 Walker Fall 2007 - with answers to MC Print Your Name: I. Multiple Choice (3 points each) 1. If marginal utility is falling then A. total utility must be falling. B. marginal utility

Microeconomics Exam Notes

Microeconomics Exam Notes Opportunity Cost What you give up to get it Production Possibility Frontier Maximum attainable combination of two products (Concept of Opportunity Cost). Main Decision Makers:

Microeconomics Exam Notes Opportunity Cost What you give up to get it Production Possibility Frontier Maximum attainable combination of two products (Concept of Opportunity Cost). Main Decision Makers:

2010 Pearson Education Canada

What Is Perfect Competition? Perfect competition is an industry in which Many firms sell identical products to many buyers. There are no restrictions to entry into the industry. Established firms have

What Is Perfect Competition? Perfect competition is an industry in which Many firms sell identical products to many buyers. There are no restrictions to entry into the industry. Established firms have

MICRO EXAM REVIEW SHEET

MICRO EXAM REVIEW SHEET 1. Firm in Perfect Competition (Long-Run Equilibrium) 2. Monopoly Industry with comparison of price & output of a Perfectly Competitive Industry 3. Natural Monopoly with Fair-Return

MICRO EXAM REVIEW SHEET 1. Firm in Perfect Competition (Long-Run Equilibrium) 2. Monopoly Industry with comparison of price & output of a Perfectly Competitive Industry 3. Natural Monopoly with Fair-Return

ECON 101 KONG Midterm 2 CMP Review Session. Presented by Benji Huang

ECON 101 KONG Midterm 2 CMP Review Session Presented by Benji Huang Chapter 5 Efficiency and Equity Benefit, Cost, Surplus Consumers (1) A consumer benefits from the consumption of a product this benefit

ECON 101 KONG Midterm 2 CMP Review Session Presented by Benji Huang Chapter 5 Efficiency and Equity Benefit, Cost, Surplus Consumers (1) A consumer benefits from the consumption of a product this benefit

Slides and Images, Worth Publishers Inc. 8-1

Perfect Competition Michael J. Murray Slides and Images, Worth Publishers Inc. 8-1 Market Structure Analysis By observing a few industry characteristics, we can predict pricing and output behavior of the

Perfect Competition Michael J. Murray Slides and Images, Worth Publishers Inc. 8-1 Market Structure Analysis By observing a few industry characteristics, we can predict pricing and output behavior of the

IB Economics Microeconomics Review Mr. Dachpian

IB Economics Microeconomics Review Microeconomics Review AP Microeconomics Chapter 1: Limits, Alternatives, & Choices IB Economics Chapter 2: The Market System and the Circular Flow Market Economies and

IB Economics Microeconomics Review Microeconomics Review AP Microeconomics Chapter 1: Limits, Alternatives, & Choices IB Economics Chapter 2: The Market System and the Circular Flow Market Economies and

SCHOOL OF ACCOUNTING AND BUSINESS BSc. (APPLIED ACCOUNTING) GENERAL / SPECIAL DEGREE PROGRAMME

GENERAL / SPECIAL DEGREE PROGRAMME") All Rights Reserved No. of Pages - 07 No of Questions - 08 SCHOOL OF ACCOUNTING AND BUSINESS BSc. (APPLIED ACCOUNTING) GENERAL / SPECIAL DEGREE PROGRAMME YEAR I SEMESTER I INTAKE VIII (GROUP B) END SEMESTER

All Rights Reserved No. of Pages - 07 No of Questions - 08 SCHOOL OF ACCOUNTING AND BUSINESS BSc. (APPLIED ACCOUNTING) GENERAL / SPECIAL DEGREE PROGRAMME YEAR I SEMESTER I INTAKE VIII (GROUP B) END SEMESTER

Chapter 1- Introduction

Chapter 1- Introduction A SIMPLE ECONOMY Central PROBLEMS OF AN ECONOMY: scarcity of resources problem of choice Every society has to decide on how to use its scarce resources. Production, exchange and

Chapter 1- Introduction A SIMPLE ECONOMY Central PROBLEMS OF AN ECONOMY: scarcity of resources problem of choice Every society has to decide on how to use its scarce resources. Production, exchange and

Total Costs. TC = TFC + TVC TFC = Fixed Costs. TVC = Variable Costs. Constant costs paid regardless of production

AP Microeconomics Total Costs TC = TFC + TVC TFC = Fixed Costs Constant costs paid regardless of production TVC = Variable Costs Costs that vary as production is changed Cost TFC TVC TFC Output Profit

AP Microeconomics Total Costs TC = TFC + TVC TFC = Fixed Costs Constant costs paid regardless of production TVC = Variable Costs Costs that vary as production is changed Cost TFC TVC TFC Output Profit

Preview from Notesale.co.uk Page 6 of 89

Guns Butter 200 0 175 75 130 125 70 150 0 160 What it shows: the maximum combinations of two goods an economy can produce with its existing resources and technology; an economy can produce at points on

Guns Butter 200 0 175 75 130 125 70 150 0 160 What it shows: the maximum combinations of two goods an economy can produce with its existing resources and technology; an economy can produce at points on

Where are we? Second midterm on November 19. Review questions on th course web site. Today: chapter on perfect competition

Where are we? Second midterm on November 19 Review questions on th course web site. Today: chapter on perfect competition Topic for the second paper: Pick a chapter in Ariely after Chapter 4 and compare

Where are we? Second midterm on November 19 Review questions on th course web site. Today: chapter on perfect competition Topic for the second paper: Pick a chapter in Ariely after Chapter 4 and compare

1.3. Levels and Rates of Change Levels: example, wages and income versus Rates: example, inflation and growth Example: Box 1.3

1 Chapter 1 1.1. Scarcity, Choice, Opportunity Cost Definition of Economics: Resources versus Wants Wants: more and better unlimited Versus Needs: essential limited Versus Demand: ability to pay + want

1 Chapter 1 1.1. Scarcity, Choice, Opportunity Cost Definition of Economics: Resources versus Wants Wants: more and better unlimited Versus Needs: essential limited Versus Demand: ability to pay + want

Market Equilibrium, the Price Mechanism and Market Efficiency. Chapter 3

Market Equilibrium, the Price Mechanism and Market Efficiency Chapter 3 Equilibrium Equilibrium is defined as a state of rest, self-perpetuating in the absence of any outside disturbance. Example: a book

Market Equilibrium, the Price Mechanism and Market Efficiency Chapter 3 Equilibrium Equilibrium is defined as a state of rest, self-perpetuating in the absence of any outside disturbance. Example: a book

Chapter 13. What will you learn in this chapter? A competitive market. Perfect Competition

Chapter 13 Perfect Competition 214 by McGraw-Hill Education 1 What will you learn in this chapter? What the characteristics of a perfectly competitive market are. How to calculate average, marginal, and

Chapter 13 Perfect Competition 214 by McGraw-Hill Education 1 What will you learn in this chapter? What the characteristics of a perfectly competitive market are. How to calculate average, marginal, and

Edexcel (A) Economics A-level

Economics A-level") Edexcel (A) Economics A-level Theme 3: Business Behaviour & the Labour Market 3.3 Revenue Costs and Profits 3.3.2 Costs Notes Formulae to calculate types of costs Total cost: This is how much it costs

Edexcel (A) Economics A-level Theme 3: Business Behaviour & the Labour Market 3.3 Revenue Costs and Profits 3.3.2 Costs Notes Formulae to calculate types of costs Total cost: This is how much it costs

Perfect Competition CHAPTER 14. Alfred P. Sloan. There s no resting place for an enterprise in a competitive economy. Perfect Competition 14

CHATER 14 erfect Competition There s no resting place for an enterprise in a competitive economy. Alfred. Sloan McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved.

CHATER 14 erfect Competition There s no resting place for an enterprise in a competitive economy. Alfred. Sloan McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved.

Practice EXAM 3 Spring Professor Walker - E201

Practice EXAM 3 Spring 2009 - Professor Walker - E201 1. The theory behind short run production costs can be narrowed to an assumption that MC is expected to initially fall, but rise at larger levels of

Practice EXAM 3 Spring 2009 - Professor Walker - E201 1. The theory behind short run production costs can be narrowed to an assumption that MC is expected to initially fall, but rise at larger levels of

ECO 162: MICROECONOMICS INTRODUCTION TO ECONOMICS Quiz 1. ECO 162: MICROECONOMICS DEMAND Quiz 2

INTRODUCTION TO ECONOMICS Quiz 1 Answer the entire question You are required to give brief explanation for each of the questions. 1. Explain the basic economic concepts with the help of Production Possibility

INTRODUCTION TO ECONOMICS Quiz 1 Answer the entire question You are required to give brief explanation for each of the questions. 1. Explain the basic economic concepts with the help of Production Possibility

Notes on Chapter 10 OUTPUT AND COSTS

Notes on Chapter 10 OUTPUT AND COSTS PRODUCTION TIMEFRAME There are many decisions made by the firm. Some decisions are major decisions that are hard to reverse without a big loss while other decisions

Notes on Chapter 10 OUTPUT AND COSTS PRODUCTION TIMEFRAME There are many decisions made by the firm. Some decisions are major decisions that are hard to reverse without a big loss while other decisions

Name Block Date. Three parts: 1) Additional Concept practice; 2) Concept Review Qs; 3) Graphing Review

Additional Concept practice; 2) Concept Review Qs; 3) Graphing Review") Name Block Date Choose-Your-Own S1 Study Adventure AP Microeconomics Three parts: 1) Additional Concept practice; 2) Concept Review Qs; 3) Graphing Review Part 1: Additional concept practice Perfect competition

Name Block Date Choose-Your-Own S1 Study Adventure AP Microeconomics Three parts: 1) Additional Concept practice; 2) Concept Review Qs; 3) Graphing Review Part 1: Additional concept practice Perfect competition

Week One What is economics? Chapter 1

Week One What is economics? Chapter 1 Economics: is the social science that studies the choices that individuals, businesses, governments, and entire societies make as they cope with scarcity and the incentives

Week One What is economics? Chapter 1 Economics: is the social science that studies the choices that individuals, businesses, governments, and entire societies make as they cope with scarcity and the incentives

Practice Exam 3: S201 Walker Fall 2009

Practice Exam 3: S201 Walker Fall 2009 I. Multiple Choice (3 points each) 1. Which of the following statements about the short-run is false? A. The marginal product of labor may increase or decrease. B.

Practice Exam 3: S201 Walker Fall 2009 I. Multiple Choice (3 points each) 1. Which of the following statements about the short-run is false? A. The marginal product of labor may increase or decrease. B.

Midterm Exam Managerial Economics Dr. John B. Horowitz Fall 2004

Midterm Exam Managerial Economics Dr. John B. Horowitz Fall 2004 Choose the best answer: (right answers are shown by *) 1. If the price of gasoline is $2.00 and the price elasticity of demand is 0.5, how

Midterm Exam Managerial Economics Dr. John B. Horowitz Fall 2004 Choose the best answer: (right answers are shown by *) 1. If the price of gasoline is $2.00 and the price elasticity of demand is 0.5, how

Monopoly and How It Arises

Monopoly and How It Arises A monopoly is a market: That produces a good or service for which no close substitute exists In which there is one supplier that is protected from competition by a barrier preventing

Monopoly and How It Arises A monopoly is a market: That produces a good or service for which no close substitute exists In which there is one supplier that is protected from competition by a barrier preventing

Microeconomics. More Tutorial at

Microeconomics 1. Economists assume that the goal of the firm is to maximize A. total revenue B. total profit C. total costs D. total satisfaction 2. If a perfectly competitive firm produces 100 units

Microeconomics 1. Economists assume that the goal of the firm is to maximize A. total revenue B. total profit C. total costs D. total satisfaction 2. If a perfectly competitive firm produces 100 units

Econ 300: Intermediate Microeconomics, Spring 2014 Final Exam Study Guide 1

Econ 300: Intermediate Microeconomics, Spring 2014 Final Exam Study Guide 1 Chronological order of topics covered in class (to the best of my memory). Introduction to Microeconomics (Chapter 1) What is

Econ 300: Intermediate Microeconomics, Spring 2014 Final Exam Study Guide 1 Chronological order of topics covered in class (to the best of my memory). Introduction to Microeconomics (Chapter 1) What is

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

PRACTICE FOR PERFECT COMPETITION Fatma Nur Karaman MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) What is the difference between perfect competition

PRACTICE FOR PERFECT COMPETITION Fatma Nur Karaman MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) What is the difference between perfect competition

Understanding Production Costs. Principles of Microeconomics Module 4

Understanding Production Costs Principles of Microeconomics Module 4 Firm Decisions: Short Run and Long Run A firm s decisions are grouped as: Short-run decisions time horizon over which at least one of

Understanding Production Costs Principles of Microeconomics Module 4 Firm Decisions: Short Run and Long Run A firm s decisions are grouped as: Short-run decisions time horizon over which at least one of

23 Perfect Competition

23 Perfect Competition Learning Objectives After you have studied this chapter, you should be able to 1. define price taker, total revenues, marginal revenue, short-run shutdown price, short-run breakeven

23 Perfect Competition Learning Objectives After you have studied this chapter, you should be able to 1. define price taker, total revenues, marginal revenue, short-run shutdown price, short-run breakeven

INTRODUCTION ECONOMIC PROFITS

INTRODUCTION This chapter addresses the following key questions: What are profits? What are the unique characteristics of competitive firms? How much output will a competitive firm produce? Chapter 7 THE

INTRODUCTION This chapter addresses the following key questions: What are profits? What are the unique characteristics of competitive firms? How much output will a competitive firm produce? Chapter 7 THE

CH 14: Perfect Competition

CH 14: Perfect Competition Characteristics of Perfect Competition 1. Both buyers and sellers are price takers A price taker is a firm (or individual) who takes the price determined by market supply and

CH 14: Perfect Competition Characteristics of Perfect Competition 1. Both buyers and sellers are price takers A price taker is a firm (or individual) who takes the price determined by market supply and

Quiz #5 Week 04/12/2009 to 04/18/2009

Quiz #5 Week 04/12/2009 to 04/18/2009 You have 30 minutes to answer the following 17 multiple choice questions. Record your answers in the bubble sheet. Your grade in this quiz will count for 1% of your

Quiz #5 Week 04/12/2009 to 04/18/2009 You have 30 minutes to answer the following 17 multiple choice questions. Record your answers in the bubble sheet. Your grade in this quiz will count for 1% of your

Chapter 5: Price Controls: Multiple Choice Questions Chapter 6: Elasticity Multiple Choice Questions

Chapter 5: Price Controls: Multiple Choice Questions 1. ANSWER: d. ceiling. 2. ANSWER: a. a shortage, which cannot be eliminated through market adjustment. 3. ANSWER: b. the equilibrium price is below

Chapter 5: Price Controls: Multiple Choice Questions 1. ANSWER: d. ceiling. 2. ANSWER: a. a shortage, which cannot be eliminated through market adjustment. 3. ANSWER: b. the equilibrium price is below

FINALTERM EXAMINATION FALL 2006

FINALTERM EXAMINATION FALL 2006 QUESTION NO: 1 (MARKS: 1) - PLEASE CHOOSE ONE Compared to the equilibrium price and quantity sold in a competitive market, a monopolist Will charge a price and sell a quantity.

FINALTERM EXAMINATION FALL 2006 QUESTION NO: 1 (MARKS: 1) - PLEASE CHOOSE ONE Compared to the equilibrium price and quantity sold in a competitive market, a monopolist Will charge a price and sell a quantity.

Whoever claims that economic competition represents 'survival of the fittest' in the sense of the law of the jungle, provides the clearest possible

Whoever claims that economic competition represents 'survival of the fittest' in the sense of the law of the jungle, provides the clearest possible evidence of his lack of knowledge of economics. -George

Whoever claims that economic competition represents 'survival of the fittest' in the sense of the law of the jungle, provides the clearest possible evidence of his lack of knowledge of economics. -George

AP Microeconomics. Content Skills Learning Targets Assessment Resources & Technology

St. Michael Albertville High School Teacher: Matthew Rooker AP Microeconomics October 2014 Content Skills Learning Targets Assessment Resources & Technology November 2014 Content Skills Learning Targets

St. Michael Albertville High School Teacher: Matthew Rooker AP Microeconomics October 2014 Content Skills Learning Targets Assessment Resources & Technology November 2014 Content Skills Learning Targets

CHAPTER NINE MONOPOLY

CHAPTER NINE MONOPOLY This chapter examines how a market controlled by a single producer behaves. What price will a monopolist charge for his output? How much will he produce? The basic characteristics

CHAPTER NINE MONOPOLY This chapter examines how a market controlled by a single producer behaves. What price will a monopolist charge for his output? How much will he produce? The basic characteristics

1. Demand: willingness to buy a good or service and the ability to pay for it; how much of an item an individual is willing to purchase at each price

1. Demand: willingness to buy a good or service and the ability to pay for it; how much of an item an individual is willing to purchase at each price 2. Quantity demanded vs demand: quantity demanded is

1. Demand: willingness to buy a good or service and the ability to pay for it; how much of an item an individual is willing to purchase at each price 2. Quantity demanded vs demand: quantity demanded is

To produce more beach balls, you must give up ever increasing quantities of ice cream cones.

Unit 01: Basic Concepts (Macro/Micro) Scarcity The Economic Problem: Unlimited wants, limited economic resources Factors of Production: -Land -Labor -Capital -Entrepreneurship Big 3 Questions: -What to

Unit 01: Basic Concepts (Macro/Micro) Scarcity The Economic Problem: Unlimited wants, limited economic resources Factors of Production: -Land -Labor -Capital -Entrepreneurship Big 3 Questions: -What to

Syllabus item: 42 Weight: 3

1.5 Theory of the firm and its market structures - Production and costs Syllabus item: 42 Weight: 3 Definition: Total product (TP): The total output that a firm produces, using its fixed and variable factors

1.5 Theory of the firm and its market structures - Production and costs Syllabus item: 42 Weight: 3 Definition: Total product (TP): The total output that a firm produces, using its fixed and variable factors

a) I, II and III. b) I c) II and III only. d) I and III only. 2. Refer to the PPF diagram below. PPF

I, II and III. b) I c) II and III only. d) I and III only. 2. Refer to the PPF diagram below. PPF") 1. Suppose that - at a given level of an economic activity - marginal social cost is greater than marginal social benefit. Which of the following statements is TRUE? I. Social surplus would be higher at

1. Suppose that - at a given level of an economic activity - marginal social cost is greater than marginal social benefit. Which of the following statements is TRUE? I. Social surplus would be higher at

ADVANCED PLACEMENT MICROECONOMICS Maple Grove Senior High School Jeff Rush Social Studies Department

ADVANCED PLACEMENT MICROECONOMICS Maple Grove Senior High School Jeff Rush rushj@district279.org Social Studies Department Required textbook Economics, McConnell and Brue, 17 th edition, 2008. Course description

ADVANCED PLACEMENT MICROECONOMICS Maple Grove Senior High School Jeff Rush rushj@district279.org Social Studies Department Required textbook Economics, McConnell and Brue, 17 th edition, 2008. Course description

WHAT IS A COMPETITIVE MARKET?

Chapter 14. Firms in Competitive Markets WHAT IS A COMPETITIVE MARKET? A perfectly competitive market has the following characteristics: There are many buyers and sellers in the market. small relative

Chapter 14. Firms in Competitive Markets WHAT IS A COMPETITIVE MARKET? A perfectly competitive market has the following characteristics: There are many buyers and sellers in the market. small relative

Chapter 33: Terms of Trade

Chapter 33: Terms of Trade 1 The Terms of Trade The division of the gains from trade depends on the terms of trade. The terms of trade are measured by the ratio of the price of exports to the price of

Chapter 33: Terms of Trade 1 The Terms of Trade The division of the gains from trade depends on the terms of trade. The terms of trade are measured by the ratio of the price of exports to the price of

Question # 1 of 15 ( Start time: 01:24:42 PM ) Total Marks: 1 A person with a diminishing marginal utility of income: Will be risk averse. Will be risk neutral. Will be risk loving. Cannot decide without

Question # 1 of 15 ( Start time: 01:24:42 PM ) Total Marks: 1 A person with a diminishing marginal utility of income: Will be risk averse. Will be risk neutral. Will be risk loving. Cannot decide without

ECON 2100 Principles of Microeconomics (Summer 2016) Behavior of Firms in Perfectly Competitive Markets

Behavior of Firms in Perfectly Competitive Markets") ECON 21 Principles of Microeconomics (Summer 216) Behavior of Firms in Perfectly Competitive Markets Relevant readings from the textbook: Mankiw, Ch. 14 Firms in Competitive Markets Suggested problems

ECON 21 Principles of Microeconomics (Summer 216) Behavior of Firms in Perfectly Competitive Markets Relevant readings from the textbook: Mankiw, Ch. 14 Firms in Competitive Markets Suggested problems

Pledge (sign) I did not copy another student s answers

I did not copy another student s answers") Economics 4020 Dr. Rupp Test #1 Fri. Sept 23 rd, 2011 20 Multiple Choice questions (2.5 points each) Pledge (sign) I did not copy another student s answers 1. The profit maximization rule for a firm is

Economics 4020 Dr. Rupp Test #1 Fri. Sept 23 rd, 2011 20 Multiple Choice questions (2.5 points each) Pledge (sign) I did not copy another student s answers 1. The profit maximization rule for a firm is

Chapter 6: Sellers and Incentives

Chapter 6: Sellers and Incentives Modified by Chapter Outline 6. 6. 6. 6. 6. 6. 1. Sellers in a Perfectly Competitive Market 2. The Seller's Problem 3. From Seller's Problem to Supply Curve 4. Producer

Chapter 6: Sellers and Incentives Modified by Chapter Outline 6. 6. 6. 6. 6. 6. 1. Sellers in a Perfectly Competitive Market 2. The Seller's Problem 3. From Seller's Problem to Supply Curve 4. Producer

The Costs of Production Chapter 8!

The Costs of Production Chapter 8! Implicit Costs vs. Explicit Costs Implicit costs - the opportunity cost that is equal to what that has to be given up by a firm for using factors that it neither hires

The Costs of Production Chapter 8! Implicit Costs vs. Explicit Costs Implicit costs - the opportunity cost that is equal to what that has to be given up by a firm for using factors that it neither hires

Perfect Competition CHAPTER14

Perfect Competition CHAPTER14 MARKET TYPES The four market types are Perfect competition Monopoly Monopolistic competition Oligopoly MARKET TYPES Perfect Competition Perfect competition exists when Many

Perfect Competition CHAPTER14 MARKET TYPES The four market types are Perfect competition Monopoly Monopolistic competition Oligopoly MARKET TYPES Perfect Competition Perfect competition exists when Many

Microeonomics. Firms in Competitive Markets. In this chapter, look for the answers to these questions: Introduction: A Scenario. N.

C H A T E R 14 Firms in Competitive Markets R I N C I L E S O F Microeonomics N. Gregory Mankiw remium oweroint Slides by Ron Cronovich 2009 South-Western, a part of Cengage Learning, all rights reserved

C H A T E R 14 Firms in Competitive Markets R I N C I L E S O F Microeonomics N. Gregory Mankiw remium oweroint Slides by Ron Cronovich 2009 South-Western, a part of Cengage Learning, all rights reserved

ECO402_Final_Term_Solved_Quizzes By

ECO402_Final_Term_Solved_Quizzes By http://www.vustudents.net 1. The "perfect information" assumption of perfect competition includes all of the following except one. Which one? Consumers know their preferences.

ECO402_Final_Term_Solved_Quizzes By http://www.vustudents.net 1. The "perfect information" assumption of perfect competition includes all of the following except one. Which one? Consumers know their preferences.

MICRO FINAL EXAM Study Guide

AP MICROECONOMICS-217 Name: MICRO FINAL EXAM Study Guide Instructions: Please fight senioritis! Study & be efficient with your time. DUE: Friday April 28 th (Multiple choice block 4/26 th or 27 th Free

AP MICROECONOMICS-217 Name: MICRO FINAL EXAM Study Guide Instructions: Please fight senioritis! Study & be efficient with your time. DUE: Friday April 28 th (Multiple choice block 4/26 th or 27 th Free

SHORT QUESTIONS AND ANSWERS FOR ECO402

SHORT QUESTIONS AND ANSWERS FOR ECO402 Question: How does opportunity cost relate to problem of scarcity? Answer: The problem of scarcity exists because of limited production. Thus, each society must make

SHORT QUESTIONS AND ANSWERS FOR ECO402 Question: How does opportunity cost relate to problem of scarcity? Answer: The problem of scarcity exists because of limited production. Thus, each society must make

Supply in a Competitive Market

Supply in a Competitive Market 8 Introduction 8 Chapter Outline 8.1 Market Structures and Perfect Competition in the Short Run 8.2 Profit Maximization in a Perfectly Competitive Market 8.3 Perfect Competition

Supply in a Competitive Market 8 Introduction 8 Chapter Outline 8.1 Market Structures and Perfect Competition in the Short Run 8.2 Profit Maximization in a Perfectly Competitive Market 8.3 Perfect Competition

Lecture 11. Firms in competitive markets

Lecture 11 Firms in competitive markets By the end of this lecture, you should understand: what characteristics make a market competitive how competitive firms decide how much output to produce how competitive

Lecture 11 Firms in competitive markets By the end of this lecture, you should understand: what characteristics make a market competitive how competitive firms decide how much output to produce how competitive

Introduction: A Scenario. Firms in Competitive Markets. In this chapter, look for the answers to these questions:

14 Firms in Competitive Markets R I N C I L E S O F ECONOMICS FOURTH EDITION N. GREGORY MANKIW remium oweroint Slides by Ron Cronovich 2008 update 2008 South-Western, a part of Cengage Learning, all rights

14 Firms in Competitive Markets R I N C I L E S O F ECONOMICS FOURTH EDITION N. GREGORY MANKIW remium oweroint Slides by Ron Cronovich 2008 update 2008 South-Western, a part of Cengage Learning, all rights

Economics 323 Microeconomic Theory Fall 2015

pink=a FIRST EXAM Chapter Two Economics 323 Microeconomic Theory Fall 2015 1. The equilibrium price in a market is the price where a. supply equals demand b. no surpluses or shortages result c. no pressures

pink=a FIRST EXAM Chapter Two Economics 323 Microeconomic Theory Fall 2015 1. The equilibrium price in a market is the price where a. supply equals demand b. no surpluses or shortages result c. no pressures

Econ 2113: Principles of Microeconomics. Spring 2009 ECU

Econ 2113: Principles of Microeconomics Spring 2009 ECU Chapter 12 Monopoly Market Power Market power is the ability to influence the market, and in particular the market price, by influencing the total

Econ 2113: Principles of Microeconomics Spring 2009 ECU Chapter 12 Monopoly Market Power Market power is the ability to influence the market, and in particular the market price, by influencing the total

Short-Run Costs and Output Decisions

Semester-I Course: 01 (Introductory Microeconomics) Unit IV - The Firm and Perfect Market Structure Lesson: Short-Run Costs and Output Decisions Lesson Developer: Jasmin Jawaharlal Nehru University Institute

Semester-I Course: 01 (Introductory Microeconomics) Unit IV - The Firm and Perfect Market Structure Lesson: Short-Run Costs and Output Decisions Lesson Developer: Jasmin Jawaharlal Nehru University Institute

Lesson 3-2 Profit Maximization

Lesson 3-2 Profit Maximization Standard 3b: Students will explain the 5 dimensions of market structure and identify how perfect competition, monopoly, monopolistic competition, and oligopoly are characterized

Lesson 3-2 Profit Maximization Standard 3b: Students will explain the 5 dimensions of market structure and identify how perfect competition, monopoly, monopolistic competition, and oligopoly are characterized

Introduction to Agricultural Economics Agricultural Economics 105 Spring 2015 First Hour Exam Version 1

1 Introduction to Agricultural Economics Agricultural Economics 105 Spring 2015 First Hour Exam Version 1 Name Section There is only ONE best, correct answer per question. Place your answer on the attached

1 Introduction to Agricultural Economics Agricultural Economics 105 Spring 2015 First Hour Exam Version 1 Name Section There is only ONE best, correct answer per question. Place your answer on the attached

short run long run short run consumer surplus producer surplus marginal revenue

Test 3 Econ 3144 Name Fall 2005 Dr. Rupp 20 Multiple Choice Questions (50 points) & 4 Discussion (50 points) Signature I have neither given nor received aid on this exam Use this table to answer questions

Test 3 Econ 3144 Name Fall 2005 Dr. Rupp 20 Multiple Choice Questions (50 points) & 4 Discussion (50 points) Signature I have neither given nor received aid on this exam Use this table to answer questions

Principles of Microeconomics Module 5.1. Understanding Profit

Principles of Microeconomics Module 5.1 Understanding Profit 180 Production Choices of Firms All firms have one goal in mind: MAX PROFITS PROFITS = TOTAL REVENUE TOTAL COST Two ways to reach this goal:

Principles of Microeconomics Module 5.1 Understanding Profit 180 Production Choices of Firms All firms have one goal in mind: MAX PROFITS PROFITS = TOTAL REVENUE TOTAL COST Two ways to reach this goal:

University of Toronto July 27, ECO 100Y L0201 INTRODUCTION TO ECONOMICS Midterm Test # 2

Department of Economics Prof. Gustavo Indart University of Toronto July 27, 2006 SOLUTION ECO 100Y L0201 INTRODUCTION TO ECONOMICS Midterm Test # 2 LAST NAME FIRST NAME STUDENT NUMBER INSTRUCTIONS: 1.

Department of Economics Prof. Gustavo Indart University of Toronto July 27, 2006 SOLUTION ECO 100Y L0201 INTRODUCTION TO ECONOMICS Midterm Test # 2 LAST NAME FIRST NAME STUDENT NUMBER INSTRUCTIONS: 1.

Introduction to Business (Managerial) Economics

Economics") Contents Unit 1 Introduction to Business (Managerial) Economics Meaning of Managerial Economics... 2 Definitions of Managerial Economics... 2 Features (Characteristics) of Managerial Economics... 5 Nature

Contents Unit 1 Introduction to Business (Managerial) Economics Meaning of Managerial Economics... 2 Definitions of Managerial Economics... 2 Features (Characteristics) of Managerial Economics... 5 Nature

The Behavior of Firms

Chapter 5 The Behavior of Firms This chapter focuses on how producers make decisions regarding supply. Individuals demand goods and services. Firms supply goods and services. An important assumption is

Chapter 5 The Behavior of Firms This chapter focuses on how producers make decisions regarding supply. Individuals demand goods and services. Firms supply goods and services. An important assumption is

GRAPHS WHAAAA???!!!???

Mumford and Sons Supply and Demand GRAPHS WHAAAA???!!!??? Demand Combination of desire, ability, and willingness to buy a product Question: Demand Schedule Price Quantity How many movie DVDs Demanded would

Mumford and Sons Supply and Demand GRAPHS WHAAAA???!!!??? Demand Combination of desire, ability, and willingness to buy a product Question: Demand Schedule Price Quantity How many movie DVDs Demanded would

Some of the assumptions of perfect competition include:

This session focuses on how managers determine the optimal price, quantity and advertising decisions under perfect competition. In earlier sessions we have looked at the nature of competitive markets.

This session focuses on how managers determine the optimal price, quantity and advertising decisions under perfect competition. In earlier sessions we have looked at the nature of competitive markets.

Short-Run Costs and Output Decisions

Chapter 8 Short-Run Costs and Prepared by: Fernando & Yvonn Quijano 2007 Prentice Hall Business Publishing Principles of Economics 8e by Case and Fair Short-Run Costs and 8 Chapter Outline Costs in the

Chapter 8 Short-Run Costs and Prepared by: Fernando & Yvonn Quijano 2007 Prentice Hall Business Publishing Principles of Economics 8e by Case and Fair Short-Run Costs and 8 Chapter Outline Costs in the

Firm Behavior. Business Economics Managerial Decisions in Competitive Markets (Deriving the Supply Curve)) Perfect Competition.

) Perfect Competition.") Business Economics Managerial Decisions in Competitive Markets (Deriving the Supply Curve)) Thomas & Maurice, Chapter Herbert Stocker herbert.stocker@uibk.ac.at Institute of International Studies University

Business Economics Managerial Decisions in Competitive Markets (Deriving the Supply Curve)) Thomas & Maurice, Chapter Herbert Stocker herbert.stocker@uibk.ac.at Institute of International Studies University

Review Chapters 1 & 2

Review Chapters 1 & 2 ECON 1 Midterm 1 Review Session Scarcity or No Free Lunch Principle. Cost-Benefit Principle. Reservation Price. Economic Surplus = Benefit Cost. Opportunity Cost (DO NOT FORGET!!).

Review Chapters 1 & 2 ECON 1 Midterm 1 Review Session Scarcity or No Free Lunch Principle. Cost-Benefit Principle. Reservation Price. Economic Surplus = Benefit Cost. Opportunity Cost (DO NOT FORGET!!).

Eco402 - Microeconomics Glossary By

Eco402 - Microeconomics Glossary By Break-even point : the point at which price equals the minimum of average total cost. Externalities : the spillover effects of production or consumption for which no

Eco402 - Microeconomics Glossary By Break-even point : the point at which price equals the minimum of average total cost. Externalities : the spillover effects of production or consumption for which no

Chapter 13. Microeconomics. Monopolistic Competition: The Competitive Model in a More Realistic Setting

Microeconomics Modified by: Yun Wang Florida International University Spring, 2018 1 Chapter 13 Monopolistic Competition: The Competitive Model in a More Realistic Setting Chapter Outline 13.1 Demand and

Microeconomics Modified by: Yun Wang Florida International University Spring, 2018 1 Chapter 13 Monopolistic Competition: The Competitive Model in a More Realistic Setting Chapter Outline 13.1 Demand and

Econ 98 (CHIU) Midterm 1 Review: Part A Fall 2004

Midterm 1 Review: Part A Fall 2004") Disclaimer: The review may help you prepare for the exam. The review is not comprehensive and the selected topics may not be representative of the exam. In fact, we do not know what will be on the exam.

Disclaimer: The review may help you prepare for the exam. The review is not comprehensive and the selected topics may not be representative of the exam. In fact, we do not know what will be on the exam.

Firms in competitive markets: Perfect Competition and Monopoly

Lesson 6 Firms in competitive markets: Perfect Competition and Monopoly Henan University of Technology Sino-British College Transfer Abroad Undergraduate Programme 0 In this lesson, look for the answers

Lesson 6 Firms in competitive markets: Perfect Competition and Monopoly Henan University of Technology Sino-British College Transfer Abroad Undergraduate Programme 0 In this lesson, look for the answers

Thanksgiving Handout Economics 101 Fall 2000

Thanksgiving Handout Economics 101 Fall 2000 The purpose of this handout is to provide a variety of problems illustrating many of the ideas that we have discussed in class this semester. The questions

Thanksgiving Handout Economics 101 Fall 2000 The purpose of this handout is to provide a variety of problems illustrating many of the ideas that we have discussed in class this semester. The questions

Contents EXPLORING ECONOMICS

Contents About the authors I-5 Preface to second edition I-7 Chapter-heads I-9 Syllabus : Choice Based Credit System (CBCS) I-19 1 EXPLORING ECONOMICS 1.1 Why study economics? 1 1.2 Meaning of economics

Contents About the authors I-5 Preface to second edition I-7 Chapter-heads I-9 Syllabus : Choice Based Credit System (CBCS) I-19 1 EXPLORING ECONOMICS 1.1 Why study economics? 1 1.2 Meaning of economics

Chapter 8 Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets

Managerial Economics & Business Strategy Chapter 8 Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All

Managerial Economics & Business Strategy Chapter 8 Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All

Four Market Models. 1. Perfect Competition 2. Pure Monopoly 3. Monopolistic Competition 4. Oligopoly

Four Market Models 1. Perfect Competition 2. Pure Monopoly 3. Monopolistic Competition 4. Oligopoly Perfect Competition Chapter 14 Perfect Competition Characteristics 1. Very Large Numbers Many buyers/sellers

Four Market Models 1. Perfect Competition 2. Pure Monopoly 3. Monopolistic Competition 4. Oligopoly Perfect Competition Chapter 14 Perfect Competition Characteristics 1. Very Large Numbers Many buyers/sellers

The Four Main Market Structures

Competitive Firms and Markets The Four Main Market Structures Market structure: the number of firms in the market, the ease with which firms can enter and leave the market, and the ability of firms to

Competitive Firms and Markets The Four Main Market Structures Market structure: the number of firms in the market, the ease with which firms can enter and leave the market, and the ability of firms to

Market structures Perfect competition

Market structures Perfect competition Market Structures Market structure refers to the number and size of buyers and sellers in the market for a good or service. A market can be defined as a group of firms

Market structures Perfect competition Market Structures Market structure refers to the number and size of buyers and sellers in the market for a good or service. A market can be defined as a group of firms

FOUNDATION COURSE MOCK TEST PAPER PAPER 4: PART I : BUSINESS ECONOMICS

FOUNDATION COURSE MOCK TEST PAPER PAPER 4: PART I : BUSINESS ECONOMICS QUESTIONS 1. Economics is a Science which deals with wealth was referred by Alfred Marshal J.B. Say Adam Smith A.C. Pigou. 2. Exploitation

FOUNDATION COURSE MOCK TEST PAPER PAPER 4: PART I : BUSINESS ECONOMICS QUESTIONS 1. Economics is a Science which deals with wealth was referred by Alfred Marshal J.B. Say Adam Smith A.C. Pigou. 2. Exploitation

Managerial Economics, 01/12/2003. A Glossary of Terms

A Glossary of Terms The Digital Economist -A- Abundance--A physical or economic condition where the quantity available of a resource exceeds the quantity desired in the absence of a rationing system. Arbitrage

A Glossary of Terms The Digital Economist -A- Abundance--A physical or economic condition where the quantity available of a resource exceeds the quantity desired in the absence of a rationing system. Arbitrage

Production and Cost Analysis I

CHAPTER 12 Production and Cost Analysis I Production is not the application of tools to materials, but logic to work. Peter Drucker McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All

CHAPTER 12 Production and Cost Analysis I Production is not the application of tools to materials, but logic to work. Peter Drucker McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All

CONTENTS. Introduction to the Series. 1 Introduction to Economics 5 2 Competitive Markets, Demand and Supply Elasticities 37

CONTENTS Introduction to the Series iv 1 Introduction to Economics 5 2 Competitive Markets, Demand and Supply 17 3 Elasticities 37 4 Government Intervention in Markets 44 5 Market Failure 53 6 Costs of

CONTENTS Introduction to the Series iv 1 Introduction to Economics 5 2 Competitive Markets, Demand and Supply 17 3 Elasticities 37 4 Government Intervention in Markets 44 5 Market Failure 53 6 Costs of

ECO402 Final Term Solved Quizzes Dear all Friends, I am not responsible for any incorrect answer so you have to check it by your own.

ECO402 Final Term Solved Quizzes Dear all Friends, I am not responsible for any incorrect answer so you have to check it by your own. 1. The "perfect information" assumption of perfect competition includes

ECO402 Final Term Solved Quizzes Dear all Friends, I am not responsible for any incorrect answer so you have to check it by your own. 1. The "perfect information" assumption of perfect competition includes

Essential Graphs for Microeconomics

Essential Graphs for Microeconomics Basic Economic Concepts! roduction ossibilities Curve Good X A F B C W Concepts: oints on the curve-efficient oints inside the curve-inefficient oints outside the curve-unattainable

Essential Graphs for Microeconomics Basic Economic Concepts! roduction ossibilities Curve Good X A F B C W Concepts: oints on the curve-efficient oints inside the curve-inefficient oints outside the curve-unattainable

4. A situation in which the number of competing firms is relatively small is known as A. Monopoly B. Oligopoly C. Monopsony D. Perfect competition

1. Demand is a function of A. Firm B. Cost C. Price D. Product 2. The kinked demand curve explains A. Demand flexibility B. Demand rigidity C. Price flexibility D. Price rigidity 3. Imperfect competition

1. Demand is a function of A. Firm B. Cost C. Price D. Product 2. The kinked demand curve explains A. Demand flexibility B. Demand rigidity C. Price flexibility D. Price rigidity 3. Imperfect competition

Microeconomics, marginal costs, value, and revenue, final exam practice problems

Microeconomics, marginal costs, value, and revenue, final exam practice problems (The attached PDF file has better formatting.) *Question 1.1: Effects on Marginal Cost Which of the following is most likely

Microeconomics, marginal costs, value, and revenue, final exam practice problems (The attached PDF file has better formatting.) *Question 1.1: Effects on Marginal Cost Which of the following is most likely

Chapter 4. Demand, Supply and Markets. These slides supplement the textbook, but should not replace reading the textbook

Chapter 4 Demand, Supply and Markets These slides supplement the textbook, but should not replace reading the textbook 1 What is a market? A group of buyers and sellers with the potential to trade 2 What

Chapter 4 Demand, Supply and Markets These slides supplement the textbook, but should not replace reading the textbook 1 What is a market? A group of buyers and sellers with the potential to trade 2 What

Firms in Competitive Markets

1 Basic Economics Chapter 14 Firms in Competitive Markets Competitive markets (1) Market with many buyers and sellers (e.g., ) (2) Trading identical products (e.g., ) (3) Each buyer and seller is a price

1 Basic Economics Chapter 14 Firms in Competitive Markets Competitive markets (1) Market with many buyers and sellers (e.g., ) (2) Trading identical products (e.g., ) (3) Each buyer and seller is a price

1 of 14 5/1/2014 4:56 PM

1 of 14 5/1/2014 4:56 PM Any point on the budget constraint Gives the consumer the highest level of utility. Represent a combination of two goods that are affordable. Represents combinations of two goods

1 of 14 5/1/2014 4:56 PM Any point on the budget constraint Gives the consumer the highest level of utility. Represent a combination of two goods that are affordable. Represents combinations of two goods

ECO 2023 Principles of Microeconomics Fall 2013 Practice Test #2. 1. Which of the following are factors of production?

ECO 2023 Principles of Microeconomics Fall 2013 Practice Test #2 1. Which of the following are factors of production? A. Output in a production function. B. Productivity. C. Land, labor, capital, and entrepreneurship.

ECO 2023 Principles of Microeconomics Fall 2013 Practice Test #2 1. Which of the following are factors of production? A. Output in a production function. B. Productivity. C. Land, labor, capital, and entrepreneurship.

Perfect competition: occurs when none of the individual market participants (ie buyers or sellers) can influence the price of the product.

can influence the price of the product.") Perfect Competition In this section of work and the next one we derive the equilibrium positions of firms in order to determine whether or not it is profitable for a firm to produce and, if so, what quantities

Perfect Competition In this section of work and the next one we derive the equilibrium positions of firms in order to determine whether or not it is profitable for a firm to produce and, if so, what quantities