9. Japan 10. Republic of Korea 11. Malaysia 12. Mexico 13. New Zealand 14. Papua New Guinea 15. Peru 16. Republic of the Philippines

|

|

|

- Randolf Lynch

- 5 years ago

- Views:

Transcription

1 Background information on Asia-Pacific Economic Cooperation (APEC) Who are the members of APEC? APEC has 21 members referred to as member economies. The term member economies is used because the APEC cooperative process is predominantly concerned with trade and economic issues, with members engaging with one another as economic entities. APEC's member economies are: 1. Australia 2. Brunei Darussalam 3. Canada 4. Chile 5. People's Republic of China 6. Hong Kong 7. China 8. Indonesia 9. Japan 10. Republic of Korea 11. Malaysia 12. Mexico 13. New Zealand 14. Papua New Guinea 15. Peru 16. Republic of the Philippines 17. Russian Federation 18. Singapore 19. Chinese Taipei 20. Thailand 21. USA 22. Viet Nam. Importance to the Australian grain industry Over 70% of Australian grain exports go to APEC countries. What are APEC's main goals? Key to achieving APEC's vision are what are referred to as the 'Bogor Goals' of free and open trade and investment in the Asia-Pacific by 2010 for industrialised economies and 2020 for developing economies. These goals were agreed by APEC Economic Leaders in Bogor, Indonesia in To achieve these goals APEC member economies developed a framework in Osaka, Japan in 1995, which set out three key areas of cooperation. Sometimes known as the 'Three Pillars' of APEC, these are the areas of 1. Trade and investment liberalisation; 2. Business facilitation; and 3. Economic and technical cooperation. What is the APEC High Level Policy Dialogue on Agricultural Biotechnology Agricultural biotechnology is a revolutionary tool that is transforming the agricultural sector. It has the potential to spur economic growth, increase productivity in the agricultural sector, reduce hunger and malnutrition, and lessen the environmental impact of agricultural production. APEC's High Level Policy Dialogue on Agricultural Biotechnology (HLPDAB) is a recognition of the importance APEC Ministers and Leaders place on member economies' work on the safe introduction of biotechnology products, and on obtaining public acceptance of these products. Policy makers use the HLPDAB to develop regulatory frameworks, facilitate technology transfer, encourage investment and strengthen public confidence regarding biotechnology in order to increase agricultural productivity and protect the environment, with the ultimate objective of promoting food security.

")

2 Policy considerations and current practices on coexistence of agricultural production systems (conventional, organic and GM crops) Geoff Honey CEO

3 Policy considerations and current practices on co-existence of agricultural production systems (conventional, organic & GM crops) Opening Remarks Good afternoon and many thanks to the member countries of APEC to allow the grain industry to present this afternoon on policy issues that affect international trade and in particular the ability of the Australian and indeed the global grain industry to be able to co-exist with organic and conventionally bred crops. Ladies and gentlemen, during the time this session lasts the world population, on a net basis, will increase by 25,000 to a total of billion people. The areas of arable land is pretty much a given, in fact the existing natural resource base, our productive capacity, relies on is under threat from degradation for a variety of reasons and in extreme cases desertification. Add to this, a changing climate and a finite input resource base, in particular with mineral fertilisers such as phosphate. One thing is a given and that s the prominence of grain in the food security equation. Grain production on a global basis is in the region of 1900 to 2000 million tonnes per year. However, only 15% of global production is traded. Another consideration is that at any point in time, the world grain inventory represents around 90 days of consumption. The challenges are clear: 1. the importance of food security for an increasing population; and 2. protection and enhancement of our, i.e. the world s natural resource base. To meet these challenges we need to access to every tool available. This includes genetic engineering or genetic modification. Let s back our scientists and regulatory approval authorities. Australian is in a fortunate position to be able to be able to export 60% of our grain production. Australia will not go short of grain. However, Australia is also a world leader in developing drought tolerant characteristics in wheat using genetic modification. I would put it to this assembly that although we are a country of surplus, we have a moral obligation to share technology that would assist food security in developing countries. The question is do we as an industry, indeed as a country have the will to actively bring these technologies to commercial fruition backed by world s best practice regulatory approval processes? Individuals and organisations who are opposed to GM production, have just as much right to bring to market organic or conventionally bred crop products. As we will explore in this presentation, this has been accomplished in Australia with a cross industry market choice program designed to give grain growers choice in what they grow and deliver to end users, crop products that suit their needs. Ladies and gentlemen, co-existence can and does occur on a commercial basis in Australia and indeed in all the major grain exporting countries. Also, with increasing use of GM grain coming onto the global market, we need to get the trade policy protocols right. These include protocols or processes such as: the UN Cartagena Protocol on Biodiversity; and the the Global Low Level Presence initiative lead by Canada with 17 other countries, including Australia. Let s look at some of the issues..

4 Food security a global effort Challenges for the global grain trade Co-existence the Australian experience Concluding remarks

5 North America Europe Russia Ukraine East Asia Caribbean Central America North Africa Middle East South Asia Southeast Asia Imported South America Sub- Saharan Africa Oceania Exported

6 Roughly 300 million metric tons about 12 percent of total demand enter into world cereal & oilseed trade World food trade helps assure adequacy of diet for nearly a billion people today by complementing local & regional supplies Source: Bruinsma, Jell. The Resource Outlook to 2050 FAO Expert Meeting on How to Feed the World in 2050

7 Trade s complementary role grows more crucial & will outplace market growth 1.5 BMT more from the world s bread baskets & other areas is needed An estimated 600 MMT of grains & oilseeds about 15 percent of total production will be transformed & delivered for consumer needs. Source: Bruinsma, Jell. The Resource Outlook to 2050 FAO Expert Meeting on How to Feed the World in 2050

8 Source:

9 GM adoption: increasing worldwide 7

")

10 Australian grain export pathway Transport (road) Transport (road\rail) Export terminal Container packing Number of players Bulk of grain delivered at harvest Number of tonnes Fully integrated, multi commodity businesses with significant investment in storage and logistical capacity

11

12 GM crops will be increasingly regulated Klaus Amman

13 At very low % GM, costs are prohibitive and markets collapse Cost At lower % GM, avoidance costs rise exponentially At higher % GM, avoidance costs have minimal cost impact on food % GMO

14

15 Adherence to the Product Launch Stewardship by technology providers is critical for the global grain trade. A major component of the PLS program is for technology providers to obtain approval in all major markets with a functioning regulatory system before commercial release.

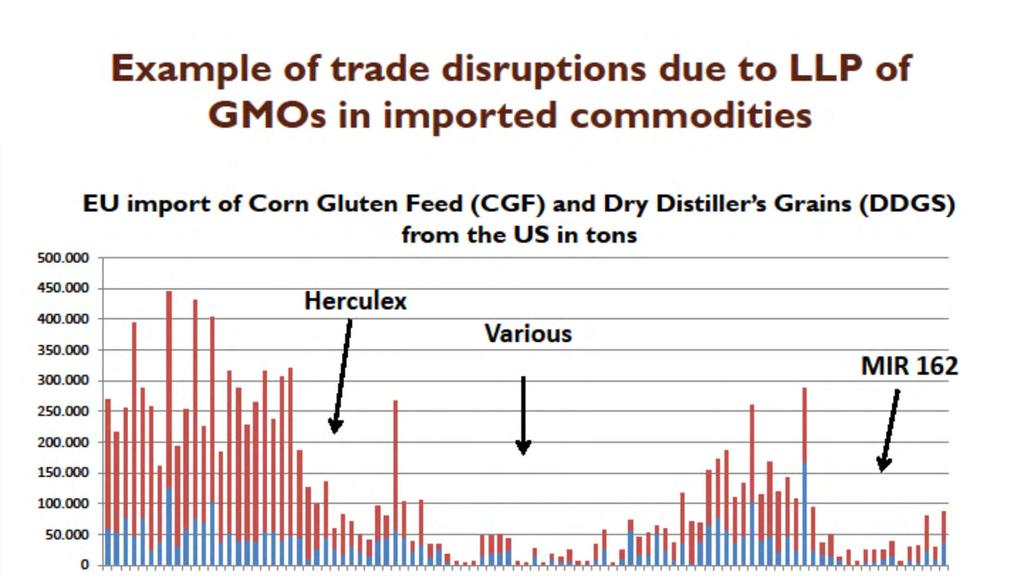

16 Rapid growth in the adoption of GM crops globally Global area of biotech crops has increased from 1.7 million ha in 1996 to million ha in 2014 Increasing volume and movement of GM crops in global grain trade Lack of alignment in obtaining global regulatory approvals for GM crops Lack in development of legislation by countries to address Low Level Presence (LLP) Increase in jurisdictions seeking to implement consumer labelling and/or certification of GM products Product Launch Stewardship Exporting countries: increasing use of GM at odds to Importing countries: zero tolerance policy on GM Increasing risk of unintended presence trade becomes problematic

17

18 Coexistence the Australian experience

19 Agriculture happens in nature commodity standards developed to deal with variation (pests, foreign materials, weed seed) Coexistence is about concurrent production of conventional, organic, IP (identity preserved) and GM crops consistent with supply chain preferences Based around thresholds Broad range of stakeholders biotech industry, regulatory agencies, producers, grain handlers, food manufacturers, consumers The Australian industry has adopted a Market Choice approach Canola Market Choice Framework 2007

NSW (ha s) 13.9 23.3 28.5 40.3 31.6 52.0 VIC (ha s) 31.2 39.4 22.3 19.0 21.2 37.0 WA (ha s) 86.0 94.8 121.7 167.6 260.0 AUST (ha s) 47.1 150.7 147.")

20 The level of adoption of GM canola has been below stakeholder expectations compared to adoption after 10 years release of : GM canola in Canada - 95% market share GM cotton in Australia - 98% market share 000 ha (est) NSW (ha s) VIC (ha s) WA (ha s) AUST (ha s) % Total Area

Market risk")

21 Australia s market choice approach Market choice approach developed to enable the Australian industry to continue to have access to all markets Non GM Australian industry has the systems and protocols to meet a variety of customer needs Market choice policy built on a set of market choice criteria: Australian approval Market assessment (customer requirements for choice) Market risk assessment & approvals Market risk mitigation (LLP/AP Thresholds) Market risk management (stewardship) Unintended Presence contingency plan

22 The project comprised a 3 year quantitative & qualitative benchmarking study Quantitative: On-farm impacts and differences between GM canola and non-gm canola weed control programs. Western Australia Study period Non GM 1051 GM 280 Total 1331 Qualitative: Explored attitudes perceptions and behaviour of both GM and non GM canola growers Tracked attitudes towards adoption and co-existence of GM and non-gm production systems New South Wales/Victoria Study period Non GM 968 GM 378 Total 1346

23 Coexistence concerns were not evident for GM canola growers: Also growing non GM canola With their neighbours With the surrounding farming community 70-95% of GM canola growers also grew non-gm canola 88% of GM canola growers did not receive any complaints Majority of complaints received were from people outside the farming community 19% of non GM growers had a neighbouring GM crop & 28% had GM crops in the district 94% of non GM canola growers said that GM canola had no impact on their farming operation Coexistence - farmer experience M/V APL Panama, Ensenada Beach, Jan 2006

24 Coexistence Australian supply chain experience GM technology has impacted the supply chain generally in the form of demands for increased traceability and quality assurance This applies to GM but also other opportunities such as high oleic oils and customer/regulatory requirements e.g. EU sustainability Industry s Market Choice approach has delivered supply of non GM oil and meal where demanded Supply chain responsible for managing and assuring non GM (declarations, testing, segregation) Consumers influenced by range of issues e.g. GM/non GM sourced products/ ingredients, sustainability, ethical production/fair trade, natural, animal welfare, allergens/intolerances, free from ; etc

25 Concluding comments GM technology has delivered a range of benefits for canola growers While adoption of GM canola in Australia has been slower than expected, coexistence concerns have not been a factor in slowing adoption The Market Choice approach developed has enabled the Australian industry to continue to have access to all markets Globally biotech crops have been the fastest adopted crop technology in recent times Continued growth in production and trade of grains and oilseeds is needed to meet demand for food The rapid growth in biotech crops combined with regulatory approaches of importing countries present challenges for the global grain trade Zero thresholds are impossible to achieve - no bulk handling system, no IP system can attain zero thresholds Compliance risk and supply chain disruptions are key considerations for the grain trade

26 If everyone is moving forward together, then success takes care of itself Henry Ford

27 Cargill sues Syngenta over unapproved corn trait - Sept. 12, 2014 Cargill filed a lawsuit today against Syngenta Seeds, Inc. in Louisiana state court, seeking damages from Syngenta for commercializing its Agrisure Viptera (MIR 162) corn seed before the product obtained import approval from China. Cargill s grain export facilities in Reserve and Westwego, Louisiana loaded the vessels that were destined for and rejected by China. Fall out: Cargill USD 90 million damages Farmers as a collective USD 1 Billion damages National Grain & Feed Association estimate cost to US corn industry of USD 2.9 Billion