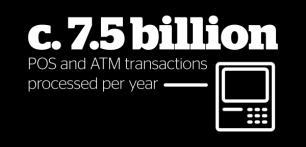

PSD2 is on top of our agenda

|

|

|

- Bennett Rice

- 5 years ago

- Views:

Transcription

1

2 PSD2 is on top of our agenda Stating the obvious There is no do nothing option for payment service providers Even basic PSD2 compliance requires strategic choices There is a highway of opportunities The timeline is tight and call for action is NOW! 2

3 Our journey the next 30 min PSD2 The Nordic Way Worldline and background for the discussion Kim: has been working with challenges of Nordic payment business the last 9 years How to jump into the fast lane Challenges and strategic decisions Harald: has 20 years of knowledge within finance and European payments 3

4 Our international footprint and leveraging Atos presence in 72 countries and our colleagues 4

a core member and active contributor in the EACHA Innovation")

5 Actively contributing to the payments landscape Shaping the industry via participation in various industry bodies equensworldline is: co-writing the EPC SCT Inst Implementation Guidelines in the SEMSTF and co-chairing the EPC Scheme Technical Forum (ESTF) part of the ISO Instant Payments Taskforce review group, drafting the new ISO standards for Instant Payments messaging a member of IPFA actively contributing to improve cross-border payments a core member of the ECB led Taskforce on achieving interoperability in Instant Payments a member of the ECB Advisory Group on Market Infrastructures for Payments (AMI-pay) a core member and active contributor in the EACHA Innovation Group, which drafted the Instant Payments Interoperability Framework, published at eacha.org currently already operating 10 interoperability connections with other ACHs (some exclusively such as DIAS in Greece), the most of any ACH in Europe and is the initiator and technical operator of the European Clearing Cooperative, aimed at facilitating interoperability in Europe a member of CAPS and Berlin Group actively involved and influencing to the development of different PSD2 standards 5

6 At the heart of information and influence Worldline is an active participant in two key PSD2 foras The Berlin Group focuses on developing interoperability standards for payments across Europe. Worldline has been part of the group since its start in 2004 and is a central participant in the group s PSD2 taskforce. CAPS is PSD2 services beyond basic compliance. The group develop standards for e.g. directory services, dispute management services, development tools, authentication solutions, mobile integration to name but a few. By gaining insight and influence through its involvements, Worldline can ensure that our service offerings remain relevant to our clients. 6

7 PSD2 Timeline - 18 months to get ready Putting a challenge to all participants PSD2 enters into force in the EU Deadline for responses to EBA s discussion paper on RTSs for SCA Deadline for responses to EBA s consultation paper on RTSs for SCA Final draft on RTSs for SCA from EBA Q (expected) Publication of the EBA Guideline for SCA and XS2A Deadline for all EU member states to adopt PSD2 on a national level Appliance of PSD The new GDPR enters into force Q (expected) Application of the RTSs for SCA and XS2A 7

8 The two most important new roles an Business opportunity for both new and existing players Article 66: Rules on access to payment account in the case of payment initiation services. 1. Member States shall ensure that a payer has the right to make use of a payment initiation service provider to obtain payment services Article 67: Rules on access to and use of payment account information in the case of account information services. 1. Member States shall ensure that a payment service user has the right to make use of services enabling access to account information 8

9 Nordic candidates for the new roles Illustrative - non-exhaustive Established players Fintechs Big Tech 9

10 New revenue stream Three step approach Moving up the value chain will expand the revenue pool Compliance Control Expand Banking utilities / low or no customer relationship: Comply with legislation by responding to info demands at low costs Provide minimum services Secure customer relationship by controlling account info Provide data Services (Retail bank) TPP services (Commercial bank) Value added services with partners to provide a full e2e user experience Every day life banks / strong customer relationship Defensive Retain Offensive 10

for AISPs and PISP as well as the security solutions to support the new requirements for strong")

11 Three levels of services and needs Serving three different PSD2 strategies for Nordic banks Compliance Ensure basic compliance by fulfilling the requirements of access (e.g. via APIs) for AISPs and PISP as well as the security solutions to support the new requirements for strong customer authentication (SCA) Success factors: Compliance, cost-efficiency and time to market Control Embrace the new opportunities Offer premium PSD2 services to AISPs and PISPs Differentiate by delivering best in class UI/UX for SCA Success factors: standardised interfaces, international connectivity Expand Expand the role in the value chain. Become an AISP to aggregate or analyse data from other banks (ASPSPs) Become a PISP to deliver alternative payment solutions to commercial clients Success factors: Scale and flexibility Defensive Retain Offensive 11

12 The challenges banks will face with PSD2 Most banks will need to allocate significant resources to PSD2 activities Preparation for XS2A Getting the APIs and interfaces ready Setting up documentation and test data for TPPs Preparing for Strong Customer Authentication (SCA) Is the bank s current SCA solution adequate and user friendly? Keeping up on information and ensuring ongoing compliance Adapting the solutions as the specifications (RTSs) are finalised Identify strategic opportunities as they arise Managing the day to day interaction with the TPPs Load balancing Identification and authentication of the TPPs (checking the EBA register) Fraud and dispute management 12

13

For retailers, PSP banks as TPP")

For a Bank, or")

Hubs can")

14 Several use cases but one industrial approach From standardization to adaptation to local specifications Offensive strategy Compliancy Interoperability For TPPs (AISP & PISP) For retailers, PSP banks as TPP themselves Connectivity with banks Management of partners and merchants Management of users & credentials For Banks (role AS PSP) For a Bank, or group of banks Compliancy with PSD2 & RTS : Security, SCA Scalability Audit & dispute management For Hubs (following local initiatives) Hubs can be created in Europe Interoperability with hubs Common APIs for members (Banks & TPPS) Central dispute management(ex) 14

Authentication hub")

15 Developer portal Developer portal How our XS2A offer is delivered Efficient reuse of proven existing ewl assets Trusted Transaction Platform covers the digital transaction routing & validation services Digital Banking platform covers all digital channels of a bank including open banking Instant Payments Testing for market Q1 17 Already provides PIS (222M trxs in 2016) e-mandates live since 2016 Delivers e-identity services (Tax Authority) Authentication hub Empower Tier1 banking channels (4m actives users) Fraud management Various available enablers to develop your business API oriented by design 15

16 XS2A offerings Benefits for the bank Cost effective compliance In a way a bank can benefit from change opportunities Safe & secure Trusted connections and able to monitor transactions, screen TPP etc. Grow revenues Provide new services/apis, become TPP and cooperate with Fintechs Retain customer facing Make bank account centre of digital experience Modular offerings with easy integration in a short time frame allows you to select the component required and combine its own assets 16

17

18 Nordic questions Worldline s new PSD2 white paper explores Are the Nordic banks particularly well suited to move beyond compliance and fully exploit the strategic opportunities of PSD2? What are the main challenges for the Nordic banks in terms of realising the potential within PSD2? What should they do to fully benefit from the new reality defined by EU? 18

19 Nordic advantages and the challenges The Nordics are generally well positioned for PSD2 Advantages Collaborative spirit and experience The idea of open/shared infrastructure is not new High degree of digitisation Customers are open for innovative digital services Common e-id solutions Fast time to market for XS2A Strong focus and investment will on mobile payments payment innovation leading Europe Challenges Legacy platforms Bank and payments infrastructure must prepare for open-banking Same e-id solutions used across private and public sector Difficult to separate bank access from government access Resources to be used for both: Defend market position with payment innovation Handle compliance 19

20 Conclusion: - Worldline can help you offload the PSD2 challenge and bring you on the fast lane for PSD2 compliant end user offerings 20

21 PSD2 The Nordic Way - a PSD2 whitepaper from Worldline Nordic* 21

22 Appendixes For more information please contact:

23 Timeline and roadmap 8 Dec 2015 EBA released first draft of the discussion paper June September 2016 Consultation period on draft RTS 13 April 2017 (est.) EBA RTS for SCA and XS2A adopted by the commission October 2018 Mandatory application of RTS for SCA and XS2A by ASPS, PSPs and Authorities Jan 2016 PSD2 is published in the official journal of the EU PSD2 enter into force 13 Jan 2017 delayed Deadline for EBA to finalize draft on authentication and submit it to EU Commission 13 Jan 2018 Deadline for member states of the EU to transpose PSD2 in the member state law Compliancy H1 2017: - PIS processing - Self registration portal - Basic APIs in developer portal - Dashboard (basic) Compliancy + optional H AIS processing - Standard procedures (dispute) - API man. advanced - Front end integration tools Optional - H Granted access (mandates) - Fraud man. 23