Challenges & Best Practices in Managing the Account Reconciliation Process

|

|

|

- Lee Hubbard

- 6 years ago

- Views:

Transcription

Rate (before you leave) Attachments (you can download today s materials)")

1 Challenges & Best Practices in Managing the Account Reconciliation Process Presenters: Donna Dean, CPA Experis Finance Director, Finance & Accounting Susan Parcells, CPA BlackLine Systems Director Finance Transformation and Product Expert General Information Share the webinar Ask a question Votes (polling questions) Rate (before you leave) Attachments (you can download today s materials) Experis Thursday, September 27,

Answer polling questions asked throughout the Webinar")

2 Earning CPE Credit To receive 1.0 CPE credit for this Webinar, participants must: Attend the Webinar for at least 50 minutes on individual computers (one person per computer) Answer polling questions asked throughout the Webinar Experis Thursday, September 27, Meet Our Presenters Donna Dean, CPA - Director Finance & Accounting Experis Finance Susan Parcells, CPA - Director Finance Transformation and Product Expert BlackLine Systems Experis Thursday, September 27,

3 Agenda Why perform reconciliations? Attributes of an effective reconciliation process Warning signs of reconciliation process issues Common root causes of reconciliation issues Account reconciliation process improvement framework Getting to leading practices Technology and process automation options Automation using BlackLine Recap Experis Thursday, September 27, Polling Question #1 Which of the following are features of your company s reconciliation process? A. Timely reconciliation on a scheduled basis B. Clearance of all reconciling items within agreed timeframes C. Segregation of duties and responsibilities (including authorization) D. Centralized control, tracking and reporting with strong management oversight E. Formalized reconciliation policy and procedures Experis Thursday, September 27,

4 Why Perform Account Reconciliations? Assures reliable and accurate financial statements Avoids significant ifi write-offs/management t surprises Provides accurate management reporting for decision-making Investors - Vendors Customers - Regulators Critical tool for understanding balance sheet and business conditions Helps to detect fraudulent activity Regulatory compliance SOX - FDICIA MAR Reconciliations are a critical internal control. Experis Thursday, September 27, Balance Sheet Account Reconciliation Attributes of an Effective Reconciliation Process Formalized Reconciliation Policy and Procedures Centralized Control, Tracking and Reporting Segregation of Duties and Responsibilities Prioritization based on the risk profile of account activity Timely Clearing of Reconciling and Aged Items Management oversight / commitment / authorization Effective Reconciliation Process Benefits of an Effective Reconciliation Process Improved accuracy/completeness of financial systems Investor/customer/vendor confidence Reduced external audit scrutiny/fees Improved accuracy of information for decision making Avoids financial information embarrassment/penalties Improves fraud detection measures Experis Thursday, September 27,

account prioritization Manually intensive process, low automation Account knowledge retained by specific individuals")

account prioritization Manually intensive process, low automation Account knowledge retained by specific individuals")

5 Balance Sheet Account Reconciliation Warning Signs of Process Issues Typical warning signs: Approval Copies of supporting documentation Prepared at a specific point in time Review & Challenge Prepare An assessment of the validity, correctness and appropriateness of an account balance Documented by relevant calculations, clear and complete explanations Reconcile Balances & Resolve Aged Items In compliance with company policy and relevant accounting standards Document Significant old unreconciled values Inconsistent/no supporting documentation for reconciliations No detailed follow-up action plans No (risk-based) account prioritization Manually intensive process, low automation Account knowledge retained by specific individuals Experis Thursday, September 27, Balance Sheet Account Reconciliation Common Root Causes of Process Issues Analysis of the issues identifies the underlying root causes: Issues Root Causes Prioritization not based on the risk profile of account activity Inadequate management oversight/commitment Lack of formalized reconciliation policy Inadequate reconciliation procedures Poor segregation of duties and unclear responsibilities Lack of centralized control Insufficient tracking and reporting Significant old unreconciled values Lack of adequately trained personnel No detailed follow-up action plans No (risk-based) account prioritization Manually intensive process, low automation Account knowledge retained by specific individuals Experis Thursday, September 27,

6 Polling Question #2 Benefits of an effective account reconciliation process include all of the following EXCEPT: A. More efficient external audit process B. Avoidance of financial misstatements C. Prevention of fraud D. Improved accuracy of data for decision making Experis Thursday, September 27, Balance Sheet Account Reconciliation Process Improvement Framework Experis Thursday, September 27,

7 Balance Sheet Account Reconciliation Remediation Methodology Understand Transaction Flow Detail Outstanding Transactions Research Outstanding Items Prepare Correcting Entries Document Control Weaknesses Timely preparation Clear comments, explanations and documents Record required adjustments Improve processes that create recurring problems Experis Thursday, September 27, Balance Sheet Account Reconciliation Risk-Based Account Prioritization Focus on accounts that could contain a significant or material misstatement Quantitative characteristics: Volume of transactions Dollar balance of account Normal account balance Use a rating system, e.g.: 1 = High Risk 2 = Medium Risk 3 = Low Risk or Key / Non-Key Accounts Qualitative characteristics: Complexity of transactions Complexity and subjectivity of accounting rules Degree of regulatory oversight Internal controls over transaction processing Level of automation/manual intervention Key target areas: Payroll Inventory Bank accounts Receivables Payables Taxes Experis Thursday, September 27,

8 Balance Sheet Account Reconciliation Process Improvement Initiatives ACCOUNT RATIONALIZATION Rationalize the number of accounts by identifying and eliminating accounts no longer required PROCESS OWNERSHIP Ensure the process is centrally coordinated. Ensure clear ownership of each account and implement quality control reviews by a central team STANDARDIZATION Establish and apply standard definition of reconciled and the methodology to be used to attain it and where feasible deploy a standard reconciliation template Prepare PROCESS MONITORING Improve information management and workflow (standard forms, formal approvals, supporting documentation, action plan documentation, regular MI reporting) SEGREGATION Ensure reconciliations are prepared for each relevant account, avoiding the grouping of accounts, particularly where this would involve netting PRIORITIZATION Prioritized timing of reconciliations on risk criteria and reconcile high-risk, priority accounts early (before period close, if possible) Approval Review and Challenge An assessment of the validity, correctness and appropriateness of an account balance Reconcile Balances and Resolve Aged Items Document TRAINING Train staff in policy and procedure. Rotate reconciliations between staff to ensure knowledge base is process driven rather than staff driven. Introduce peer reviews AUTOMATION Automate processes wherever possible. Technology introduces system controls leading to efficiencies in the close process and improved audit transparency Experis Thursday, September 27, Polling Question #3 Which of the following is NOT an indicator of a high risk account? A. Complexity and subjectivity of accounting rules applicable to the account B. Inexperienced preparer responsible for reconciling the account C. High degree of regulatory oversight affecting the account D. High volume of transactions posted to the account each month Experis Thursday, September 27,

9 Balance Sheet Account Reconciliation Technology and Process Automation Considerations Technology can shorten the reconciliation cycle and improve controls MS Excel Use Excel worksheets for smaller reconciliations Frequently used software in accounting and finance groups Requires consistent formatting of data fields to be analyzed (i.e., numeric to numeric, or text to text) File size is limited Number of fields used for efficient analyzing or matching of transaction data are limited MS Access Use Access database queries for large / complex reconciliations Functions with consistently formatted data fields (i.e., numeric to numeric, text to text) File size is almost unlimited Number of fields used for efficient analyzing or matching of transaction data are unlimited Results can be displayed as a MS Access report or exported back to MS Excel for reporting or inclusion in other files In-house Processes Develop in-house processes supported by IT programming and operations Address manual reconciliations that are too large or complex to be performed efficiently Provide a high degree of autonomy and flexibility for the user Specialized Reconciliation Software Deploy specialized reconciliation software Database design using predefined templates Easily accessible supporting documents and company policies and procedures Readily available reports to see the status of all reconciliations Experis Thursday, September 27, Balance Sheet Account Reconciliation Technology Options and Features Data Security and Integrity Locking input cells, data validation MS Excel MS Access In-house Processes Specialist Reconciliation Software Input/Output Controls Cross checks, balancing, conditional formatting Segregation of Duties Defines duties, roles and responsibilities Backup and Archival Regular backup on secured server Development Controls Control, development, testing and approval Documentation Controls Documentation of use and application Access Controls Define and restrict user access, rights and privileges Change Controls Defined process for system changes Version Controls Use of naming conventions Experis Thursday, September 27,

10 Automation Using BlackLine Experis Thursday, September 27,

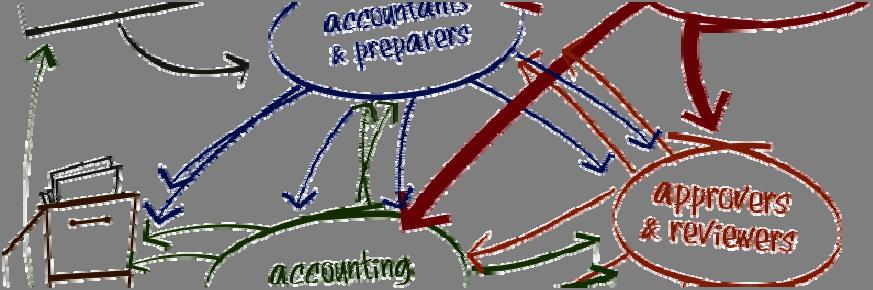

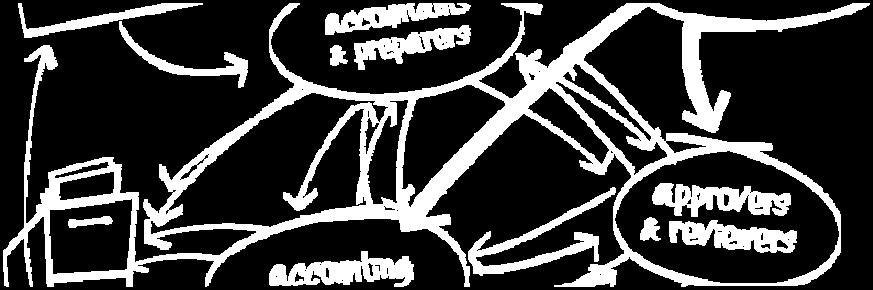

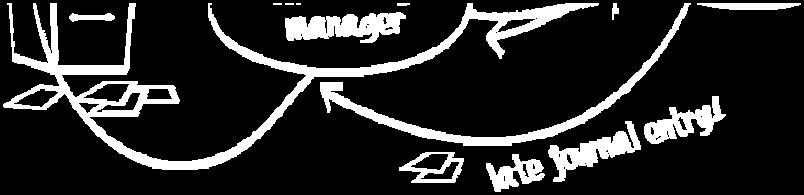

11 Experis Thursday, September 27, BlackLine Process Experis Thursday, September 27,

12 Account Task Transaction Reconciliations Management Matching Variance Analysis Journal Entry Consolidation Integrity Manager Ideal Automated Platform Real-time monitoring and reporting Controlled process Data integrity and integration Experis Thursday, September 27, SSAE 16 + ISAE 3402 Internationally recognized auditing standards developed by the AICPA and IAASB Third-party opinions on control effectiveness Experis Thursday, September 27,

13 ROI & Cutting Costs Auto-certification Increased staff productivity Reduced paper, printing, storage, overhead, auditor fees Improved process management Faster close Return on investment is one of the most important indicators of value MeadWestVaco Corporation ROI: 495% Payback: 2 Months Cox Communications ROI: 227% Payback: 6 Months Education Management Corporation ROI: 138% Payback: 10 Months Experis Thursday, September 27, Experis Thursday, September 27,

14 Experis Thursday, September 27, Experis Thursday, September 27,

15 Experis Thursday, September 27, Balance Sheet Integrity Account Reconciliation Recap Today we have: Reviewed the basics of account reconciliation and why differences arise Considered your individual account reconciliation processes and compared them to effective processes Considered the warning signs of a poor reconciliation process and the areas of weakness they may indicate Started to consider steps toward leading practices Taken a high-speed tour through the process improvement steps that will lead to account reconciliation process optimization appropriate for any business Learned about the BlackLine automation technology Experis Thursday, September 27,

16 Questions? For more information: Donna Dean, CPA Director Finance & Accounting Experis Finance Susan Parcells, CPA Director Finance Transformation and Product Expert BlackLine Systems Experis Thursday, September 27, Experis Finance is a leader in innovative professional services that help companies create competitive advantage, custom tailoring our project solutions and professional resourcing services to fit our clients needs in risk advisory, tax and finance & accounting. Experis Thursday, September 27,

17 More information For more information, please visit Experis Thursday, September 27,

Unit 10: Financial Accounting 2 In a series of 2 for this unit Learning outcome 3-4. Sample

Unit 10: Financial Accounting 2 In a series of 2 for this unit Learning outcome 3-4 Types of Account Reconciliation Account reconciliation within the account Account reconciliation with an external account

Unit 10: Financial Accounting 2 In a series of 2 for this unit Learning outcome 3-4 Types of Account Reconciliation Account reconciliation within the account Account reconciliation with an external account

IMPROVING THE CLOSE PROCESS UTILIZING FINANCE GOVERNANCE TECHNOLOGIES

IMPROVING THE CLOSE PROCESS UTILIZING FINANCE GOVERNANCE TECHNOLOGIES TODAY S AGENDA 8:00am 8:30am 8:30am 8:45am 8:45am 9:15am 9:15am 9:45am 9:45am 10:15am 10:15am 10:30am Breakfast and Networking Opening

IMPROVING THE CLOSE PROCESS UTILIZING FINANCE GOVERNANCE TECHNOLOGIES TODAY S AGENDA 8:00am 8:30am 8:30am 8:45am 8:45am 9:15am 9:15am 9:45am 9:45am 10:15am 10:15am 10:30am Breakfast and Networking Opening

Continuous Monitoring: Getting Results Today!

Continuous Monitoring: Getting Results Today! Gerard (Rod) Brennan, PhD, CFE Risk & Internal Control Officer NA, Siemens Corporation Jason A. Gross, CPA, CIA, CFE, CISA, ACDA Vice President, Controls Management,

Continuous Monitoring: Getting Results Today! Gerard (Rod) Brennan, PhD, CFE Risk & Internal Control Officer NA, Siemens Corporation Jason A. Gross, CPA, CIA, CFE, CISA, ACDA Vice President, Controls Management,

OPERATIONAL RISK EXAMINATION TECHNIQUES

OPERATIONAL RISK EXAMINATION TECHNIQUES 1 OVERVIEW Examination Planning Oversight Policies, Procedures, and Limits Measurement, Monitoring, and MIS Internal Controls and Audit 2 Risk Assessment: Develop

OPERATIONAL RISK EXAMINATION TECHNIQUES 1 OVERVIEW Examination Planning Oversight Policies, Procedures, and Limits Measurement, Monitoring, and MIS Internal Controls and Audit 2 Risk Assessment: Develop

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT CONTENTS

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT (Effective for audits of financial statements for periods beginning

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT (Effective for audits of financial statements for periods beginning

September 19, 2007 San Francisco Chapter

Optimizing Spreadsheet Controls A Proactive Approach to Sustaining Compliance September 19, 2007 Welcome! Today s Facilitators Dannette Roberts Industry Partner Manager Microsoft Corporation Terry Nystrom

Optimizing Spreadsheet Controls A Proactive Approach to Sustaining Compliance September 19, 2007 Welcome! Today s Facilitators Dannette Roberts Industry Partner Manager Microsoft Corporation Terry Nystrom

Optimizing the close cycle using nextgeneration account reconciliation best practices and tools

Point of View February 4, 2016 Complimentary Research Optimizing the close cycle using nextgeneration account reconciliation best practices and tools By Kars Stal, Jason Sacco, and Elvie Lucero Executive

Point of View February 4, 2016 Complimentary Research Optimizing the close cycle using nextgeneration account reconciliation best practices and tools By Kars Stal, Jason Sacco, and Elvie Lucero Executive

IAASB Main Agenda (December 2008) Page Agenda Item

Page Agenda Item") IAASB Main Agenda (December 2008) Page 2008 2669 Agenda Item 2-C PROPOSED INTERNATIONAL STANDARD ON AUDITING 265 COMMUNICATING DEFICIENCIES IN INTERNAL CONTROL (Effective for audits of financial statements

IAASB Main Agenda (December 2008) Page 2008 2669 Agenda Item 2-C PROPOSED INTERNATIONAL STANDARD ON AUDITING 265 COMMUNICATING DEFICIENCIES IN INTERNAL CONTROL (Effective for audits of financial statements

The Road to Continuous Assurance. Jason A. Gross, CPA, CIA, CFE, CISA, ACDA Vice President, Controls Management Siemens Financial Services, Inc.

The Road to Continuous Assurance Jason A. Gross, CPA, CIA, CFE, CISA, ACDA Vice President, Controls Management Siemens Financial Services, Inc. Challenge Statement: Implement a CCM program for the Organization

The Road to Continuous Assurance Jason A. Gross, CPA, CIA, CFE, CISA, ACDA Vice President, Controls Management Siemens Financial Services, Inc. Challenge Statement: Implement a CCM program for the Organization

The Road to Continuous Assurance. Jason A. Gross, CPA, CIA, CFE, CISA, ACDA Vice President, Controls Management Siemens Financial Services, Inc.

The Road to Continuous Assurance Jason A. Gross, CPA, CIA, CFE, CISA, ACDA Vice President, Controls Management Siemens Financial Services, Inc. Agenda Key Drivers for Successful Implementation Technology

The Road to Continuous Assurance Jason A. Gross, CPA, CIA, CFE, CISA, ACDA Vice President, Controls Management Siemens Financial Services, Inc. Agenda Key Drivers for Successful Implementation Technology

Bottom-line Savings through Contract Compliance and Cost Recovery

Bottom-line Savings through Contract Compliance and Cost Recovery Presenters: George Albarelli, John Fiore, Chris Fejko and Tarek Ibrahim November 13, 2012 General Information Share the webinar Ask a question

Bottom-line Savings through Contract Compliance and Cost Recovery Presenters: George Albarelli, John Fiore, Chris Fejko and Tarek Ibrahim November 13, 2012 General Information Share the webinar Ask a question

Minneapolis Public Schools Special School District No. 1 Minneapolis, Minnesota. Communications Letter of the Student Activity Accounts.

Minneapolis, Minnesota Communications Letter of the Student Activity Accounts June 30, 2018 Table of Contents Report on Matters Identified as a Result of the Audit of the Financial Statements 1 Material

Minneapolis, Minnesota Communications Letter of the Student Activity Accounts June 30, 2018 Table of Contents Report on Matters Identified as a Result of the Audit of the Financial Statements 1 Material

Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement

Issued December 2007 International Standard on Auditing Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement The Malaysian Institute of Certified Public Accountants

Issued December 2007 International Standard on Auditing Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement The Malaysian Institute of Certified Public Accountants

2-2 The major characteristics of CPA firms that permit them to fulfill their social function competently and independently are:

Link full download Solution Manual : http://testbankair.com/download/solution-manual-forauditing-and-assurance-services-16th-edition-by-arens-elder-beasley-and-hogan Link full download test bank: http://testbankair.com/download/test-bank-for-auditing-andassurance-services-16th-edition-by-arens-elder-beasley-and-hogan/

Link full download Solution Manual : http://testbankair.com/download/solution-manual-forauditing-and-assurance-services-16th-edition-by-arens-elder-beasley-and-hogan Link full download test bank: http://testbankair.com/download/test-bank-for-auditing-andassurance-services-16th-edition-by-arens-elder-beasley-and-hogan/

Chapter 2. The CPA Profession

Chapter 2 The CPA Profession Review Questions 2-1 The four major services that CPAs provide are: 1. Audit and assurance services Assurance services are independent professional services that improve the

Chapter 2 The CPA Profession Review Questions 2-1 The four major services that CPAs provide are: 1. Audit and assurance services Assurance services are independent professional services that improve the

The definition of a deficiency is also set forth in the attached Appendix I.

Deloitte & Touche LLP 361 South Marine Corps Drive Tamuning, GU 96913-3973 USA Tel: (671)646-3884 Fax: (671)649-4932 www.deloitte.com May 26, 2014 Mr. David Paul General Manager Marshalls Energy Company,

Deloitte & Touche LLP 361 South Marine Corps Drive Tamuning, GU 96913-3973 USA Tel: (671)646-3884 Fax: (671)649-4932 www.deloitte.com May 26, 2014 Mr. David Paul General Manager Marshalls Energy Company,

REGISTERED CANDIDATE AUDITOR (RCA) TECHNICAL COMPETENCE REQUIREMENTS

TECHNICAL COMPETENCE REQUIREMENTS") REGISTERED CANDIDATE AUDITOR (RCA) TECHNICAL COMPETENCE REQUIREMENTS 1. Context After completion of the recognised training contract, a period of specialisation is required, appropriate to the level required

REGISTERED CANDIDATE AUDITOR (RCA) TECHNICAL COMPETENCE REQUIREMENTS 1. Context After completion of the recognised training contract, a period of specialisation is required, appropriate to the level required

computer-assisted Chapter 10 Substantive testing, audit techniques and audit programmes

Chapter 10 Substantive testing, computer-assisted audit techniques and audit programmes Learning objectives To describe the substantive procedures an auditor would perform to prove that recorded transactions

Chapter 10 Substantive testing, computer-assisted audit techniques and audit programmes Learning objectives To describe the substantive procedures an auditor would perform to prove that recorded transactions

See your auditor clearly. Transparency report: How we perform quality audit engagements

See your auditor clearly. Transparency report: How we perform quality audit engagements February 2014 Table of contents 1) A message from the CEO and Managing Partner Assurance 2 2) Quality control policies

See your auditor clearly. Transparency report: How we perform quality audit engagements February 2014 Table of contents 1) A message from the CEO and Managing Partner Assurance 2 2) Quality control policies

A Financial Executive s Guide to Internal Controls & Fraud Prevention in the Cloud

A Financial Executive s Guide to Internal Controls & Fraud Prevention in the Cloud July 2018 Greenlight Technologies. All rights reserved. 1 Speakers James Rice Vice President of Customer Solutions Greenlight

A Financial Executive s Guide to Internal Controls & Fraud Prevention in the Cloud July 2018 Greenlight Technologies. All rights reserved. 1 Speakers James Rice Vice President of Customer Solutions Greenlight

Auditing Standards and Practices Council

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT PHILIPPINE STANDARD ON AUDITING

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT PHILIPPINE STANDARD ON AUDITING

Optimizing Your Finance Function

Optimizing Your Finance Function Presenter s Tuesday, Name September 20, 2011 Presented By: Sharon Hubiak Director, Finance & Accounting Jeffrey Creech Director, Finance & Accounting Audio and Tech Support

Optimizing Your Finance Function Presenter s Tuesday, Name September 20, 2011 Presented By: Sharon Hubiak Director, Finance & Accounting Jeffrey Creech Director, Finance & Accounting Audio and Tech Support

Sheena Tran, CPA May 19, 2014

Internal Controls Review 2012/13 Sheena Tran, CPA May 19, 2014 TO: ACCCA BOARD OF DIRECTORS This is considered to be a financial review and recommendations for the Association of California Community College

Internal Controls Review 2012/13 Sheena Tran, CPA May 19, 2014 TO: ACCCA BOARD OF DIRECTORS This is considered to be a financial review and recommendations for the Association of California Community College

Seminar Internal Control Identification and Filtering

Seminar Internal Control Identification and Filtering 4 March 2011 by Stephen Ho Definition The process designed, implemented and maintained by those charged with governance, management and other personnel

Seminar Internal Control Identification and Filtering 4 March 2011 by Stephen Ho Definition The process designed, implemented and maintained by those charged with governance, management and other personnel

Cash Management Services

Cash Management Services Bank on your time with Cash Management Services 1 2 3 4 5 6 7 8 9 10 Information Reporting Effective cash management at your fingertips. Direct Deposit A better way to pay your

Cash Management Services Bank on your time with Cash Management Services 1 2 3 4 5 6 7 8 9 10 Information Reporting Effective cash management at your fingertips. Direct Deposit A better way to pay your

2/27/2017. Segregation of Duties/ Internal Controls. Objectives. Agenda

Segregation of Duties/ Internal Controls 2017 WASBO Accounting Conference David Maccoux, Shareholder Objectives Discuss failures of internal controls to detect or prevent fraud and learn how to implement

Segregation of Duties/ Internal Controls 2017 WASBO Accounting Conference David Maccoux, Shareholder Objectives Discuss failures of internal controls to detect or prevent fraud and learn how to implement

SAP Business One designed for all your small and midsize company s needs

SAP Business One designed for all your small and midsize company s needs Whatever your business we ve got you covered Affordable low total cost of ownership Industry solutions tailored to your needs Comprehensive

SAP Business One designed for all your small and midsize company s needs Whatever your business we ve got you covered Affordable low total cost of ownership Industry solutions tailored to your needs Comprehensive

Chapter 06. Audit Planning, Understanding the Client, Assessing Risks, and Responding. McGraw-Hill/Irwin

Chapter 06 Audit Planning, Understanding the Client, Assessing Risks, and Responding McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Obtaining Clients Submit a

Chapter 06 Audit Planning, Understanding the Client, Assessing Risks, and Responding McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Obtaining Clients Submit a

IAASB Main Agenda (March 2005) Page Agenda Item 12-C

Page Agenda Item 12-C") IAASB Main Agenda (March 2005) Page 2005 429 Agenda Item 12-C [ISA AND IAPS SPLIT] PROPOSED INTERNATIONAL AUDITING PRACTICE STATEMENT XXX THE APPLICATION OF INTERNATIONAL STANDARDS ON AUDITING IN AN AUDIT

IAASB Main Agenda (March 2005) Page 2005 429 Agenda Item 12-C [ISA AND IAPS SPLIT] PROPOSED INTERNATIONAL AUDITING PRACTICE STATEMENT XXX THE APPLICATION OF INTERNATIONAL STANDARDS ON AUDITING IN AN AUDIT

Audit Quality Assurance workshop Audit Planning by: CPA Steve Obock Associate Director- KPMG Kenya March 2017

Audit Quality Assurance workshop Audit Planning by: CPA Steve Obock Associate Director- KPMG Kenya March 2017 Uphold public interest Agenda Introduction Developing an audit strategy Setting audit materiality

Audit Quality Assurance workshop Audit Planning by: CPA Steve Obock Associate Director- KPMG Kenya March 2017 Uphold public interest Agenda Introduction Developing an audit strategy Setting audit materiality

Background. Required Communications of Other Internal Control Deficiencies

Checkpoint Contents Accounting, Audit & Corporate Finance Library Editorial Materials Audit and Attest Management Letter Comments: Operations and Controls Chapter 1 Communication of Management Comments

Checkpoint Contents Accounting, Audit & Corporate Finance Library Editorial Materials Audit and Attest Management Letter Comments: Operations and Controls Chapter 1 Communication of Management Comments

Corporate Governance Update. SOX 404 and Internal Controls

Corporate Governance Update SOX 404 and Internal Controls Speakers Barbara Borden bborden@cooley.com 858.550.6243 Brad Peck bpeck@cooley.com 858.550.6012 Steven Spector (858) 453-7200 x229 sspector@arenapharm.com

Corporate Governance Update SOX 404 and Internal Controls Speakers Barbara Borden bborden@cooley.com 858.550.6243 Brad Peck bpeck@cooley.com 858.550.6012 Steven Spector (858) 453-7200 x229 sspector@arenapharm.com

Fraud Detection and Prevention

Fraud Detection and Prevention Presented by: Louise Hanson, Moss Adams LLP Emily Ogden, Moss Adams LLP April 24, 2014 1 DISCLOSURE STATEMENT The material appearing in this presentation is for informational

Fraud Detection and Prevention Presented by: Louise Hanson, Moss Adams LLP Emily Ogden, Moss Adams LLP April 24, 2014 1 DISCLOSURE STATEMENT The material appearing in this presentation is for informational

Report on Inspection of PricewaterhouseCoopers Audit (Headquartered in Neuilly-Sur-Seine, French Republic)

") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Neuilly-Sur-Seine, French Republic) Issued by the Public Company

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Neuilly-Sur-Seine, French Republic) Issued by the Public Company

County of Sutter. Management Letter. June 30, 2012

County of Sutter Management Letter June 30, 2012 County of Sutter Index Page Management Letter 3 Management Report Schedule of Current Year s 4 Schedule of Prior Auditor Comments 9 Prior Year Information

County of Sutter Management Letter June 30, 2012 County of Sutter Index Page Management Letter 3 Management Report Schedule of Current Year s 4 Schedule of Prior Auditor Comments 9 Prior Year Information

AN AUDIT OF INTERNAL CONTROL THAT IS INTEGRATED WITH AN AUDIT OF FINANCIAL STATEMENTS: GUIDANCE FOR AUDITORS OF SMALLER PUBLIC COMPANIES

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org PRELIMINARY STAFF VIEWS AN AUDIT OF INTERNAL CONTROL THAT IS INTEGRATED WITH AN AUDIT OF FINANCIAL

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org PRELIMINARY STAFF VIEWS AN AUDIT OF INTERNAL CONTROL THAT IS INTEGRATED WITH AN AUDIT OF FINANCIAL

Lawrence Berkeley National Lab. Observations from Audit Procedures October 17, 2005

Lawrence Berkeley National Lab Observations from Audit Procedures October 17, 2005 Table of Contents Page Your Needs and Expectations 3 Background 4 Risk Assessment 5 Audit Strategy 6 Details of Work Performed

Lawrence Berkeley National Lab Observations from Audit Procedures October 17, 2005 Table of Contents Page Your Needs and Expectations 3 Background 4 Risk Assessment 5 Audit Strategy 6 Details of Work Performed

Hong Kong Deposit Protection Board

Hong Kong Deposit Protection Board Independent Assessment Program and Self-Declaration for Compliance with the Guideline on Information Required for Determining and Paying Compensation ( Program Guide

Hong Kong Deposit Protection Board Independent Assessment Program and Self-Declaration for Compliance with the Guideline on Information Required for Determining and Paying Compensation ( Program Guide

SAN FRANCISCO COURT APPOINTED SPECIAL ADVOCATE PROGRAM

SAN FRANCISCO COURT APPOINTED SPECIAL ADVOCATE PROGRAM FINANCIAL PROCEDURES MANUAL Table of Contents GENERAL ACCOUNTING POLICY AND PROCEDURES... 3 OVERALL ACCOUNTING SYSTEM DESIGN... 3 CONTROL OBJECTIVE...

SAN FRANCISCO COURT APPOINTED SPECIAL ADVOCATE PROGRAM FINANCIAL PROCEDURES MANUAL Table of Contents GENERAL ACCOUNTING POLICY AND PROCEDURES... 3 OVERALL ACCOUNTING SYSTEM DESIGN... 3 CONTROL OBJECTIVE...

FRAUD AWARENESS UPDATE

Tammy Michaud, CPA, Principal Sarah Belliveau, CPA, Senior Manager FRAUD AWARENESS UPDATE berrydunn.com CATEGORIES OF FRAUD Asset misappropriations (stealing) Theft or misuse of assets Corruption Inappropriate

Tammy Michaud, CPA, Principal Sarah Belliveau, CPA, Senior Manager FRAUD AWARENESS UPDATE berrydunn.com CATEGORIES OF FRAUD Asset misappropriations (stealing) Theft or misuse of assets Corruption Inappropriate

Internal Audit. Lecture # 09 By: Kanchan Damithendra

Internal Audit Lecture # 09 By: Kanchan Damithendra What is Internal Audit? Scope and Objectives of Internal Auditing Monitoring of internal control. The establishment of adequate internal control is a

Internal Audit Lecture # 09 By: Kanchan Damithendra What is Internal Audit? Scope and Objectives of Internal Auditing Monitoring of internal control. The establishment of adequate internal control is a

Release 11 Feature Highlights

Release 11 Feature This document summarizes a handful of top-level features of each module and component. Module / Component Common / Overall Feature Multi-user and multi-company Robust & Reliable - Microsoft

Release 11 Feature This document summarizes a handful of top-level features of each module and component. Module / Component Common / Overall Feature Multi-user and multi-company Robust & Reliable - Microsoft

CPAB Audit Quality Insights Report: 2018 Fall Inspections Results

10 18 CPAB Audit Quality Insights Report: 2018 Fall Inspections Results WORLD-CLASS AUDIT REGULATION CPAB-CCRC.ca What we do The Canadian Public Accountability Board (CPAB) oversees public accounting firms

10 18 CPAB Audit Quality Insights Report: 2018 Fall Inspections Results WORLD-CLASS AUDIT REGULATION CPAB-CCRC.ca What we do The Canadian Public Accountability Board (CPAB) oversees public accounting firms

Internal Financial Control (IFC)& Internal Financial Controls over Financial Reporting (IFCoFR)

& Internal Financial Controls over Financial Reporting (IFCoFR)") Internal Financial Control (IFC)& Internal Financial Controls over Financial Reporting (IFCoFR) Origin of IFC The first significant focus on internal control certification related to financial reporting

Internal Financial Control (IFC)& Internal Financial Controls over Financial Reporting (IFCoFR) Origin of IFC The first significant focus on internal control certification related to financial reporting

How well you are prepared to deal with IFC

September 9, 2016 How well you are prepared to deal with IFC Price Waterhouse & Co Amit Agrawal & Madhavi D K Internal Financial Controls over Financial Reporting (IFCFR) Particulars Background Overview

September 9, 2016 How well you are prepared to deal with IFC Price Waterhouse & Co Amit Agrawal & Madhavi D K Internal Financial Controls over Financial Reporting (IFCFR) Particulars Background Overview

Mapping of Original ISA 315 to New ISA 315 s Standards and Application Material (AM) Agenda Item 2-C

Agenda Item 2-C") Mapping of to 315 s and Application Material (AM) Agenda Item 2-C AM 1. The purpose of this International Standard on Auditing (ISA) is to establish standards and to provide guidance on obtaining an understanding

Mapping of to 315 s and Application Material (AM) Agenda Item 2-C AM 1. The purpose of this International Standard on Auditing (ISA) is to establish standards and to provide guidance on obtaining an understanding

Internal Auditing 101

Internal Auditing 101 Presented By: Sam Capuano - Manager of Internal Audit, Wolf & Co. John Gallagher - Director of Internal Audit, SEFCU (NY) Barry Lucas - Internal Auditor, Desco FCU (Ohio) 1 Introductions

Internal Auditing 101 Presented By: Sam Capuano - Manager of Internal Audit, Wolf & Co. John Gallagher - Director of Internal Audit, SEFCU (NY) Barry Lucas - Internal Auditor, Desco FCU (Ohio) 1 Introductions

Public Accounting System

Public Accounting System We understand that an accounting system is really all about: Better Decision Making As a trusted advisor, you must be able to provide your clients with the information that may

Public Accounting System We understand that an accounting system is really all about: Better Decision Making As a trusted advisor, you must be able to provide your clients with the information that may

Minimizing fraud exposure with effective ERP segregation of duties controls

Minimizing fraud exposure with effective ERP segregation of duties controls Prepared by: Luke Leaon, Manager, RSM US LLP luke.leaon@rsmus.com, +1 612 629 9072 Adam Harpool, Manager, RSM US LLP adam.harpool@rsmus.com,

Minimizing fraud exposure with effective ERP segregation of duties controls Prepared by: Luke Leaon, Manager, RSM US LLP luke.leaon@rsmus.com, +1 612 629 9072 Adam Harpool, Manager, RSM US LLP adam.harpool@rsmus.com,

Cash Reconciliations and Cash Handling

Cash Reconciliations and Cash Handling WASBO Accounting Conference March, 2016 Handling Cash Cash may be the most vulnerable asset in your LEA. How do you safeguard your cash? Timely reconciliation of

Cash Reconciliations and Cash Handling WASBO Accounting Conference March, 2016 Handling Cash Cash may be the most vulnerable asset in your LEA. How do you safeguard your cash? Timely reconciliation of

Sarbanes-Oxley: Company Case Study - Viacom Inc. IT General Controls - Sustaining Compliance Efforts. Anthony Noble VP, IT Internal Audit

Sarbanes-Oxley: A Focus on IT Controls Company Case Study - Viacom Inc. IT General Controls - Sustaining Compliance Efforts Anthony Noble VP, IT Internal Audit Today s Agenda Introduction Viacom Methodology

Sarbanes-Oxley: A Focus on IT Controls Company Case Study - Viacom Inc. IT General Controls - Sustaining Compliance Efforts Anthony Noble VP, IT Internal Audit Today s Agenda Introduction Viacom Methodology

Ten Payment Fraud Protections

Ten Payment Fraud Protections 1. Payee Positive Pay a. Provided by banks b. Banks match check serial numbers and dollar amounts against a company provided list of checks issued and only pays those checks

Ten Payment Fraud Protections 1. Payee Positive Pay a. Provided by banks b. Banks match check serial numbers and dollar amounts against a company provided list of checks issued and only pays those checks

The definition of a deficiency is also set forth in the attached Appendix I.

Deloitte & Touche LLP 361 South Marine Corps Drive Tamuning, GU 96913-3911 USA September 22, 2015 Tel: (671)646-3884 Fax: (671)649-4932 www.deloitte.com Mr. David Paul General Manager Marshalls Energy

Deloitte & Touche LLP 361 South Marine Corps Drive Tamuning, GU 96913-3911 USA September 22, 2015 Tel: (671)646-3884 Fax: (671)649-4932 www.deloitte.com Mr. David Paul General Manager Marshalls Energy

Chapter 7: Fraud, Internal Control, and Cash. Vocabulary Quiz. Solutions to Vocabulary Quiz

Vocabulary Quiz Solutions to Vocabulary Quiz 1. Internal control 2. Cash 3. Petty cash fund 4. Deposits in transit 5. Cash equivalents 6. Cash budget 7. Internal auditors 8. NSF check 9. Outstanding checks

Vocabulary Quiz Solutions to Vocabulary Quiz 1. Internal control 2. Cash 3. Petty cash fund 4. Deposits in transit 5. Cash equivalents 6. Cash budget 7. Internal auditors 8. NSF check 9. Outstanding checks

General Business Accounting System

General Business Accounting System We understand that an accounting system is really all about: Better Decision Making As a business grows it becomes more difficult for management to keep up with all the

General Business Accounting System We understand that an accounting system is really all about: Better Decision Making As a business grows it becomes more difficult for management to keep up with all the

Jodi Copeland Region Manager, Fiserv Risk & Compliance

Reconciliation & Compliance: Frontier Overview Jodi Copeland Region Manager, Fiserv Risk & Compliance 2 Agenda Current Reconciliation Challenges Frontier Benefits Typical Uses for Frontier Solution Overview

Reconciliation & Compliance: Frontier Overview Jodi Copeland Region Manager, Fiserv Risk & Compliance 2 Agenda Current Reconciliation Challenges Frontier Benefits Typical Uses for Frontier Solution Overview

Importing & Exporting Data with Dynamics GP

Importing & Exporting Data with Dynamics GP September 27, 2018 To Receive CPE Credit Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader is the person who

Importing & Exporting Data with Dynamics GP September 27, 2018 To Receive CPE Credit Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader is the person who

Seminar on Audit of SME: Practitioners Challenges

Seminar on Audit of SME: Practitioners Challenges Western India Regional Council of The Institute of Chartered Accountants Of India Audit Manual & Documentation - Understanding the appropriate documents

Seminar on Audit of SME: Practitioners Challenges Western India Regional Council of The Institute of Chartered Accountants Of India Audit Manual & Documentation - Understanding the appropriate documents

Audit Preparation Best Practices

Audit Preparation Best Practices November 4, 2014 Jeffrey P. Allen, CPA, CGFM Senior Manager Maner Costerisan 5 Audience Poll How many have been through an audit? Multiple times? Why do you have an audit?

Audit Preparation Best Practices November 4, 2014 Jeffrey P. Allen, CPA, CGFM Senior Manager Maner Costerisan 5 Audience Poll How many have been through an audit? Multiple times? Why do you have an audit?

IT Service Delivery And Support Week Seven: SLA. IT Auditing and Cyber Security Fall 2016 Instructor: Liang Yao

IT Service Delivery And Support Week Seven: SLA IT Auditing and Cyber Security Fall 2016 Instructor: Liang Yao 1 Outsourcing Drivers Outsourced IT Works Outsourced IT Activity Samples Top Three Outsourcing

IT Service Delivery And Support Week Seven: SLA IT Auditing and Cyber Security Fall 2016 Instructor: Liang Yao 1 Outsourcing Drivers Outsourced IT Works Outsourced IT Activity Samples Top Three Outsourcing

Audit Recommendations Status Report as of December 31, 2018

SO U THWEST F LORIDA Internal Audit Report Audit Recommendations Report as of December 31, 2018 Date: March 15, 2019 To: The Honorable Linda Doggett, Lee County Clerk of the Circuit Court & Comptroller

SO U THWEST F LORIDA Internal Audit Report Audit Recommendations Report as of December 31, 2018 Date: March 15, 2019 To: The Honorable Linda Doggett, Lee County Clerk of the Circuit Court & Comptroller

Internal Control Program

DFA Conversations Office of the University Controller Internal Control Program November 20, 2017 Introduction Bill Sibert, University Controller Erica Jessup, Senior Financial Analyst Phil Turke, Payroll

DFA Conversations Office of the University Controller Internal Control Program November 20, 2017 Introduction Bill Sibert, University Controller Erica Jessup, Senior Financial Analyst Phil Turke, Payroll

You can easily view comparative data and drill through for transaction details.

analyzing financial and operational information (such as number of sales reps, occupancy rates or cycle time), giving you a very powerful business management tool that leverages your financial data. You

analyzing financial and operational information (such as number of sales reps, occupancy rates or cycle time), giving you a very powerful business management tool that leverages your financial data. You

Reliable Financial Reporting. Evaluating Deficiencies in Internal Control Over Financial Reporting

Reliable Financial Reporting Evaluating Deficiencies in Internal Control Over Financial Reporting Steve Glover May 2017 The right to use this material without explicit written permission is hereby granted

Reliable Financial Reporting Evaluating Deficiencies in Internal Control Over Financial Reporting Steve Glover May 2017 The right to use this material without explicit written permission is hereby granted

ReconArt for NetSuite

ReconArt for NetSuite Automating Your Reconciliations Do you wish there was a single tool that could automate all your data matching and reconciliation activities? There is - ReconArt for NetSuite Now

ReconArt for NetSuite Automating Your Reconciliations Do you wish there was a single tool that could automate all your data matching and reconciliation activities? There is - ReconArt for NetSuite Now

Presentation by: CPA Zachary Muthui

Audit Planning and Risk Assessment Presentation by: CPA Zachary Muthui Uphold public interest Audit planning Objectives of audit planning To ensure that the audit is performed in a smooth and effective

Audit Planning and Risk Assessment Presentation by: CPA Zachary Muthui Uphold public interest Audit planning Objectives of audit planning To ensure that the audit is performed in a smooth and effective

Implementation Tool for Auditors

Implementation Tool for Auditors CANADIAN AUDITING STANDARDS (CAS) DECEMBER 2017 STANDARD DISCUSSED CAS 315, Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity

Implementation Tool for Auditors CANADIAN AUDITING STANDARDS (CAS) DECEMBER 2017 STANDARD DISCUSSED CAS 315, Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity

Step inside your new look business with SAP Business One. SAP Solution Brief SAP Solutions for Small Midsize Businesses

Step inside your new look business with SAP Business One SAP Solution Brief SAP Solutions for Small Midsize Businesses SAP Business One designed for all your small and midsize company s needs Whatever

Step inside your new look business with SAP Business One SAP Solution Brief SAP Solutions for Small Midsize Businesses SAP Business One designed for all your small and midsize company s needs Whatever

Sample Audit Committee. of Auditors and Management

Sample Audit Committee Questions to Ask of Auditors and Management 2 Sample Audit Committee Questions to Ask of Auditors and Management u Sample Audit Committee Questions to Ask of Auditors and Management

Sample Audit Committee Questions to Ask of Auditors and Management 2 Sample Audit Committee Questions to Ask of Auditors and Management u Sample Audit Committee Questions to Ask of Auditors and Management

What Are Your Auditors Doing? Presented by Carrie Kennedy, Partner Travis Smith, Partner Moss Adams LLP

What Are Your Auditors Doing? Presented by Carrie Kennedy, Partner Travis Smith, Partner Moss Adams LLP 1 MOSS ADAMS AT A GLANCE Full service national CPA firm providing assurance, tax, and consulting

What Are Your Auditors Doing? Presented by Carrie Kennedy, Partner Travis Smith, Partner Moss Adams LLP 1 MOSS ADAMS AT A GLANCE Full service national CPA firm providing assurance, tax, and consulting

IAASB CAG Public Session (March 2018) CONFORMING AND CONSEQUENTIAL AMENDMENTS ARISING FROM DRAFT PROPOSED ISA 540 (REVISED) 1

CONFORMING AND CONSEQUENTIAL AMENDMENTS ARISING FROM DRAFT PROPOSED ISA 540 (REVISED) 1") Agenda Item B.4 CONFORMING AND CONSEQUENTIAL AMENDMENTS ARISING FROM DRAFT PROPOSED ISA 540 (REVISED) 1 ISA 200, Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance

Agenda Item B.4 CONFORMING AND CONSEQUENTIAL AMENDMENTS ARISING FROM DRAFT PROPOSED ISA 540 (REVISED) 1 ISA 200, Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance

COSO Updates and Expectations. IIA San Diego Chapter January 8, 2014

COSO Updates and Expectations IIA San Diego Chapter January 8, 2014 Agenda Overview of 2013 Internal Control-Integrated Framework and Companion Guidance 2013 Framework General Enhancements by Component

COSO Updates and Expectations IIA San Diego Chapter January 8, 2014 Agenda Overview of 2013 Internal Control-Integrated Framework and Companion Guidance 2013 Framework General Enhancements by Component

Abila MIP Fund Accounting

Page 1 Fund Accounting Feature Compare Make an informed decision when you choose your fund accounting system. Use this checklist during your evaluation of Fund Accounting. Write in the names of up to two

Page 1 Fund Accounting Feature Compare Make an informed decision when you choose your fund accounting system. Use this checklist during your evaluation of Fund Accounting. Write in the names of up to two

Innovation and Internal Controls

Innovation and Internal Controls AGA Dallas Chapter January 25, 2018 Renee L. Hayden, CPA, CFE Interim Managing Director Center for Performance Excellence City of Dallas Training Objective: Learn About

Innovation and Internal Controls AGA Dallas Chapter January 25, 2018 Renee L. Hayden, CPA, CFE Interim Managing Director Center for Performance Excellence City of Dallas Training Objective: Learn About

Copyright 2011 Resource Information Associates, Inc., Makers of Pontem Software.

A Quick Overview Counties, Cities, Villages, Townships Charter Schools Non-Profit Organizations Large or Small Organizations Pontem s scalable pricing provides affordability regardless of your organization

A Quick Overview Counties, Cities, Villages, Townships Charter Schools Non-Profit Organizations Large or Small Organizations Pontem s scalable pricing provides affordability regardless of your organization

Segregation of Duties: Best Practices for Cybersecurity and More

WHITE PAPER Segregation of Duties: Best Practices for Cybersecurity and More The news is filled with stories of alarming cybersecurity breaches, networks being hacked, and malware running amok. However,

WHITE PAPER Segregation of Duties: Best Practices for Cybersecurity and More The news is filled with stories of alarming cybersecurity breaches, networks being hacked, and malware running amok. However,

NCR Passport for Commercial. Part of NCR s enterprise hub for remote deposit capture

NCR Passport for Commercial Part of NCR s enterprise hub for remote deposit capture For more information on RDC, speak to your sales contact or go to ncr.com. Easy and secure deposits from where their

NCR Passport for Commercial Part of NCR s enterprise hub for remote deposit capture For more information on RDC, speak to your sales contact or go to ncr.com. Easy and secure deposits from where their

Eric Anderson, City Manager. Scottie Nix, Internal Auditor

City of Tacoma Internal Audit Office Memorandum TO: FROM: SUBJECT: Eric Anderson, City Manager Scottie Nix, Internal Auditor Improving SAP Roles Assignment and Monitoring at the City of Tacoma Follow Up

City of Tacoma Internal Audit Office Memorandum TO: FROM: SUBJECT: Eric Anderson, City Manager Scottie Nix, Internal Auditor Improving SAP Roles Assignment and Monitoring at the City of Tacoma Follow Up

AICPA Peer Review Program Compliance: Responding to Latest Developments

FOR LIVE PROGRAM ONLY AICPA Peer Review Program Compliance: Responding to Latest Developments WEDNESDAY, MAY 31, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved

FOR LIVE PROGRAM ONLY AICPA Peer Review Program Compliance: Responding to Latest Developments WEDNESDAY, MAY 31, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved

Sarbanes-Oxley Act of 2002 Can private businesses benefit from it?

Sarbanes-Oxley Act of 2002 Can private businesses benefit from it? As used in this document, Deloitte means Deloitte Tax LLP, which provides tax services; Deloitte & Touche LLP, which provides assurance

Sarbanes-Oxley Act of 2002 Can private businesses benefit from it? As used in this document, Deloitte means Deloitte Tax LLP, which provides tax services; Deloitte & Touche LLP, which provides assurance

Audit committee performance evaluation

Audit committee performance evaluation 1 Next The following questionnaire is based on emerging and leading practices to assist in the self-assessment of an audit committee s performance. It is not intended

Audit committee performance evaluation 1 Next The following questionnaire is based on emerging and leading practices to assist in the self-assessment of an audit committee s performance. It is not intended

The Blue Sage Group. Sarbanes-Oxley. 404 Compliance Program. The Blue Sage Group

The Blue Sage Group Sarbanes-Oxley 404 Compliance Program The Blue Sage Group Agenda The Blue Sage Group 404 Compliance Challenges Meeting the 404 Challenges TBSG 404 Compliance Program Assessment and

The Blue Sage Group Sarbanes-Oxley 404 Compliance Program The Blue Sage Group Agenda The Blue Sage Group 404 Compliance Challenges Meeting the 404 Challenges TBSG 404 Compliance Program Assessment and

The 5 Levels of Corporate Performance Management (CPM) Maturity: Climbing to the Top Floor

Maturity: Climbing to the Top Floor") Sponsor Ask, Share, Learn Within the Largest Community of Corporate Finance Professionals The 5 Levels of Corporate Performance Management (CPM) Maturity: Climbing to the Top Floor Learning Objectives

Sponsor Ask, Share, Learn Within the Largest Community of Corporate Finance Professionals The 5 Levels of Corporate Performance Management (CPM) Maturity: Climbing to the Top Floor Learning Objectives

ERP Is it for me? American Public Power Association Business & Financial Conference September 17, 2018

ERP Is it for me? American Public Power Association Business & Financial Conference September 17, 2018 About your instructor Amanda Lasinski, Consulting Manager > Energy and Utilities Team > 12 years of

ERP Is it for me? American Public Power Association Business & Financial Conference September 17, 2018 About your instructor Amanda Lasinski, Consulting Manager > Energy and Utilities Team > 12 years of

MAS90 & MAS200 Order of Closing

Business & Accounting Solutions, LLC 3900 Orchard Lake Rd, Suite 60 Farmington Hills, MI 8336 8-893-1060 phone, 8-893-1063 fax www.orionbas.com MAS90 & MAS00 Order of Closing Year-end and Period End processing

Business & Accounting Solutions, LLC 3900 Orchard Lake Rd, Suite 60 Farmington Hills, MI 8336 8-893-1060 phone, 8-893-1063 fax www.orionbas.com MAS90 & MAS00 Order of Closing Year-end and Period End processing

Copyright 2009 Club Resources International. Disclaimer

Copyright 2009 Club Resources International For internal use only at the purchasing club or organization. Materials purchased from the Club Resources International website are for the exclusive use of

Copyright 2009 Club Resources International For internal use only at the purchasing club or organization. Materials purchased from the Club Resources International website are for the exclusive use of

CAAS 104 Cost Audit and Assurance Standard on Knowledge of Business, its Processes and the Business Environment

CAAS 104 Cost Audit and Assurance Standard on Knowledge of Business, its Processes and the Business Environment The following is the Cost Audit and Assurance Standard (CAAS 104) on Knowledge of Business,

CAAS 104 Cost Audit and Assurance Standard on Knowledge of Business, its Processes and the Business Environment The following is the Cost Audit and Assurance Standard (CAAS 104) on Knowledge of Business,

Institute of Chartered Accountants of India. Standards on Auditing

Institute of Chartered Accountants of India Standards on Auditing Presented by: CA Sunil Nagrani February 16, 2013 Contents SA 315 - Identifying and Assessing the Risk of Material Misstatement Through

Institute of Chartered Accountants of India Standards on Auditing Presented by: CA Sunil Nagrani February 16, 2013 Contents SA 315 - Identifying and Assessing the Risk of Material Misstatement Through

Presentation 5. Landscaper Transactions & Reconciliations Educating Bookkeepers for Business, Inc.

Presentation 5 Landscaper Transactions & Reconciliations Chapter 1: Templates Edit: Preferences: Accounting Lists: Templates Templates: Select Template Type Lists: Templates: Basic Customization Lists:

Presentation 5 Landscaper Transactions & Reconciliations Chapter 1: Templates Edit: Preferences: Accounting Lists: Templates Templates: Select Template Type Lists: Templates: Basic Customization Lists:

Advanced Finance for Governing Board Members. Charter Schools: Advancing the Promise!! 2015 Annual Conference

Advanced Finance for Governing Board Members Charter Schools: Advancing the Promise!! 2015 Annual Conference Governing Body Responsibilities with regard to finance Fiduciary responsibilities outlined in

Advanced Finance for Governing Board Members Charter Schools: Advancing the Promise!! 2015 Annual Conference Governing Body Responsibilities with regard to finance Fiduciary responsibilities outlined in

Success in Joint Ventures: Sustained Compliance and Audit Oversight

Success in Joint Ventures: Sustained Compliance and Audit Oversight Gene DeLaddy, CIA Senior Vice President, Chief Compliance & Privacy Officer, Chief Audit Executive Dave Pyland, CPA Director, Internal

Success in Joint Ventures: Sustained Compliance and Audit Oversight Gene DeLaddy, CIA Senior Vice President, Chief Compliance & Privacy Officer, Chief Audit Executive Dave Pyland, CPA Director, Internal

Financial Controls Checklist

Financial Controls Checklist Board of Health: Board of Health for the Leeds, Grenville & Lanark District Health Unit Period ended: Dec. 31/17 Objective: The objective of the Financial Controls Checklist

Financial Controls Checklist Board of Health: Board of Health for the Leeds, Grenville & Lanark District Health Unit Period ended: Dec. 31/17 Objective: The objective of the Financial Controls Checklist

Executive Directors Series: Overview of an assurance engagement

Executive Directors Series: Overview of an assurance engagement Presented by Richard Games CPA, CA, MPAcc, BCom Bradley Jacoby Games Chartered Professional Accountants The presentation is of a general

Executive Directors Series: Overview of an assurance engagement Presented by Richard Games CPA, CA, MPAcc, BCom Bradley Jacoby Games Chartered Professional Accountants The presentation is of a general

Wokingham Borough Council

Wokingham Borough Council Audit Committee Summary For the year ended 31 March 2015 Audit Results Report ISA (UK & Ireland) 260 September 2015 Contents Page Section 1 Executive summary 3 Section 2 Extent

Wokingham Borough Council Audit Committee Summary For the year ended 31 March 2015 Audit Results Report ISA (UK & Ireland) 260 September 2015 Contents Page Section 1 Executive summary 3 Section 2 Extent

Internal Financial Controls (IFC) - An Overview

- An Overview") Internal Financial Controls (IFC) - An Overview Increased responsibilities of the Board: Companies Act 2013 Board s responsibility extended to ensure Legal compliances to all applicable statutes. The increasingly

Internal Financial Controls (IFC) - An Overview Increased responsibilities of the Board: Companies Act 2013 Board s responsibility extended to ensure Legal compliances to all applicable statutes. The increasingly

STREAMLINE ACCOUNT RECONCILIATION FOR A SAFE & EFFICIENT FINANCIAL CLOSE

September 2014 STREAMLINE ACCOUNT RECONCILIATION FOR A SAFE & EFFICIENT FINANCIAL CLOSE SAP AND BLACKLINE: AN END- TO- END SOLUTION A financial close is not an optional business process. Public companies

September 2014 STREAMLINE ACCOUNT RECONCILIATION FOR A SAFE & EFFICIENT FINANCIAL CLOSE SAP AND BLACKLINE: AN END- TO- END SOLUTION A financial close is not an optional business process. Public companies

Internal Controls. They Are Everyone s Business. Valdosta State University Office of Internal Audits June 2016

Internal Controls They Are Everyone s Business Valdosta State University Office of Internal Audits June 2016 1 Presentation Overview Understand Internal Controls Identify Control Weaknesses Fraud Best

Internal Controls They Are Everyone s Business Valdosta State University Office of Internal Audits June 2016 1 Presentation Overview Understand Internal Controls Identify Control Weaknesses Fraud Best

CHAPTER 2 THEORETICAL FOUNDATIONS

CHAPTER 2 THEORETICAL FOUNDATIONS This chapter covered the theoretical foundation used in the analysis and implementation process of this thesis. The main terms and concepts that are covered in this section

CHAPTER 2 THEORETICAL FOUNDATIONS This chapter covered the theoretical foundation used in the analysis and implementation process of this thesis. The main terms and concepts that are covered in this section

Track 1: Sage 300 CRE Financials

**Note on session numbering: Sessions are numbered with the track number timeslot. Track Numbers follow the top of the session grid, while the Timeslot numbers follow the left side of the grid. Please

**Note on session numbering: Sessions are numbered with the track number timeslot. Track Numbers follow the top of the session grid, while the Timeslot numbers follow the left side of the grid. Please