Renewable Energy Perspec1ves in La1n America in the Interna1onal Context. IASS Interna1onal Workshop. Session # 4 WIND - URUGUAY

|

|

|

- Cameron Woods

- 5 years ago

- Views:

Transcription

1 Renewable Energy Perspec1ves in La1n America in the Interna1onal Context IASS Interna1onal Workshop Session # 4 WIND - URUGUAY Potsdam, Germany October, 2012

2 OVERVIEW OF URUGUAY

3 Country name: República Oriental del Uruguay Land area: 176,215 km 2 Population: 3.3 million inhabitants Annual growth rate: 0.3 % Density: 18.8 inhabitants/km 2 Life expectancy: 76 years Infant mortality rate: 7.7/1000 (22.8 in Latin Am)

4

5 THE ENERGY SECTOR IN A STRONGLY GROWING COUNTRY

6 ENERGY FIGURES Total Energy Consumption Energy Consumption / inhabitant 3,107 ktoe 0,93 toe/inhab Electrification 99,2% Average annual power demand Peak power demand (july ) 1050 MW 1747 MW Genera1on: Open to market Grid Opera1on: Monopoly UTE (Public U8lity)

7 FRAMEWORK Uruguay has: - NO oil - NO natural gas - NO coal Almost no space for new large hydropower plants (75% of present electric mix)

8 PRIMARY GLOBAL ENERGY MIX ( ) Hydropower 20% Natural Gas 2% Wood 17% Electricity imports 5% Oil 56%

9 ENERGY SOURCE (GWh) Huge variations of hydropower!

10 SHARE OF OIL IMPORTS IN TOTAL IMPORTS/EXPORTS

11 ENERGY POLICY URUGUAY 2030

12 ENERGY POLICY : First defini1ons 2008: Council of Ministers 2010: Special Commiaee including all Poli1cal Par1es Four strategic guidelines Short, medium and long term goals Mul1dimensional and integrated vision, including technological, economic, geopoli1cal, environmental, ethical and social factors

as the main tools Enhanced par8cipa8on of private companies Transparent and stable regulatory Supply")

Keeping low")

13 STRATEGIC GUIDELINES Ins1tu1onal Government defines and coordinates energy policy Public u8lity (UTE) and NOC (ANCAP) as the main tools Enhanced par8cipa8on of private companies Transparent and stable regulatory Supply framework Energy mix diversifica8on (sources and suppliers) Reduce share of imported oil Increase share of domes8c sources Strong support to renewables, with no subsidies Building local capaci8es (technology transfer) Keeping low carbon footprint

14 STRATEGIC GUIDELINES (con1nue) Demand Strong support to energy efficiency in all energy sectors and all ac8vi8es (transport, building, industry) The State as a paradigma8c example Promo8ng a cultural change Social Adequate energy access to all ci8zens as a human right Energy policy embedded in na8onal social policies to face vulnerability

15 SHORT TERM GOALS (2015) (par1al) * 50% of renewable energy in the global primary energy mix Including: - 25% of electricity genera8on from unconven8onal renewable sources - 30% of agroindustrial and urban waste used to produce energy - 15% decrease of oil use in transport * LNG regasifica1on capacity * 100% electrifica1on

16 ENERGY SUPPLY AND RENEWABLE ENERGIES

17 WHY RENEWABLES? To keep low carbon emissions To avoid fossil fuel imports To drop and stabilize energy prices To build local capaci8es To improve energy independence WHICH RENEWABLES? Those which allow a social use, and are environmental and economically sustainable. Today: Bio energy (power, heat, biofuels) Solar Thermal (water heaters) Small Hydro Power Wind Power

18 WIND POWER LARGE SCALE

Technicians integrated in DNE")

Objec1ve: Iden8fica8on of")

19 CAPACITY GENERATION GEF Wind Power Energy Project in Uruguay ( ) Technicians integrated in DNE structure It created the first wind energy Technical Team at Public U8lity (UTE) Objec1ve: Iden8fica8on of the restric8ons for the development of wind energy in Uruguay and the development of measures for it suppression

Results: Lible par8cipa8on of world class companies Installa8on of the first private wind")

20 LEARNING PERIOD: CALL FOR PRIVATE COMPANIES First call for wind power purchase agreements with electric power company UTE state- owned In total 110 MW of wind power were offered, and were awarded 66 MW (built to date 25 MW) Results: Lible par8cipa8on of world class companies Installa8on of the first private wind farm

21 LEARNED LESSONS & DEVELOPED ACTIONS I Need for quality base informa1on Update of the wind power map Deepening of measures campaigns Interna8onal cer8fica8on resource assessment

22 LEARNED LESSONS & DEVELOPED ACTIONS II Need for adjustments in the regulatory framework Adequacy of electricity regulatory framework. Genera8ng authoriza8on (in order to avoid specula8ve market). Wind easement. Environmental & land use issues.

23 LEARNED LESSONS & DEVELOPED ACTIONS III Technological Defini1ons Not accep8ng offers based on prototypes. New Equipment (unused). Requirement of Cer8fica8on of generated energy Local Par1cipa1on Defini1ons 20% minimum Opera8on and Maintenance Local Control Center Need of adjustment in the bidding selec1on procedure

24 LEARNING PERIOD: UTE Experience Caracoles I 2008: Inaugura8on of a wind power farm with 10 MW of power. (Vestas V80 of 2MW each aerogenerator). Experience as a local model in large- scale genera8on, and prepara8on to meet the opera8on and maintenance as a basic requirements for future calls Uruguay- Spain Project Results: Posi8ve valoriza8on of the experience by UTE.

25 PRESENT SITUATION LEARNING PERIOD: MW 6:1 2010: Caracoles II 150 MW 7:1 2009:Call for wind power purchase agreements (20 years) 2012: Leasing/ Joint Venture 686 MW 2010: Call for wind power purchase agreements in same condi8on Promo8onal tariff to energy provided before Dec : Target: offers not awarded in 2010 tender.

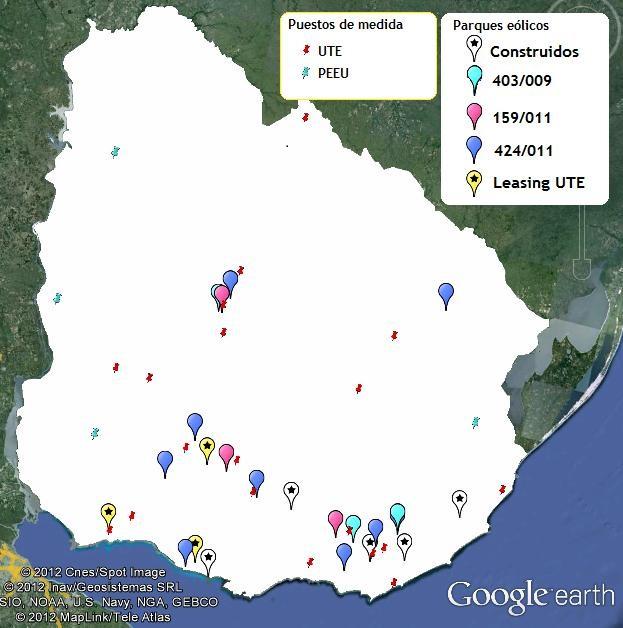

26 DISTRIBUTION

27 EVOLUTION I

28 EVOLUTION II 700 Planned Installed capacity (MW)

Logis8c")

29 CHALLENGES IN WIND POWER (I) Logis8c aspects for the installa8on of wind farms (services may act as boblenecks)

30 EVOLUTION III Power (MW) Energy (%)

Transmission")

31 CHALLENGES IN WIND POWER (II) Transmission infrastructure

32 CHALLENGES IN WIND POWER (III) Variability of the resource and dispatch in a system with strong Wind energy participation: Wind + Hydro + Biomass + NG R&D Short term predictions of wind (studies in progress)

33 WIND POWER MICROGENERATION

34 GRID- CONNECTED MICROGENERATION Uruguay: first country in La8n America to enable grid- connected renewable microgenera1on. Net metering contract Goal: To promote domes8c manufacturing To improve good energy prac8ces

35 MEASURES FOR THE INDUSTRIAL SECTOR Decree 158/2012 Possibility of installa8on of wind energy genera8on capaci8es and commercializa8on of surpluses by the industries. Capaci8es: 150 kw up to 60 MW.

36 FOR THIS PURPOSE Monthly public reports of measures from the DNE sta8ons

37 WIND POWER AND SOCIAL ISSUES Uruguay: 99,2 % of electrifica8on. Short term Goal: 100 % coverage by 2015 Alterna8ves in rural electrifica8on Laying of power lines Genera8on from hybrid systems of Renewable Energies

38 EXPECTED IMPACT OF THESE POLICIES

39 SHARES OF ELECTRICITY GENERATION BY 2015 Wind 24% Biomass 18% Hydro 51 % GNL 6% Oil 1 % 93% RENEWABLE

10% Biomass (genera1on) 5% 55%")

40 GLOBAL PRIMARY MIX 2015 Solar 1% Biofuels 3% Wind 7% Oils & deriva1ves 40% GNL 5% Hydro 14% Biomass (heat) 15% Biomass (others) 10% Biomass (genera1on) 5% 55% RENEWABLE

41 ANNUAL MEDIUM COST Parameter: Rain probabili8es 73 US$/MWh 46 US$/MWh

42 ANNUAL MEDIUM COST Parameter: Rain probabili8es 70 US$/MWh 25 US$/MWh

43

44 Thank you for your aeengon

45 Renewable Energy Perspec1ves in La1n America in the Interna1onal Context IASS Interna1onal Workshop Session # 4 WIND - URUGUAY Potsdam, Germany October, 2012