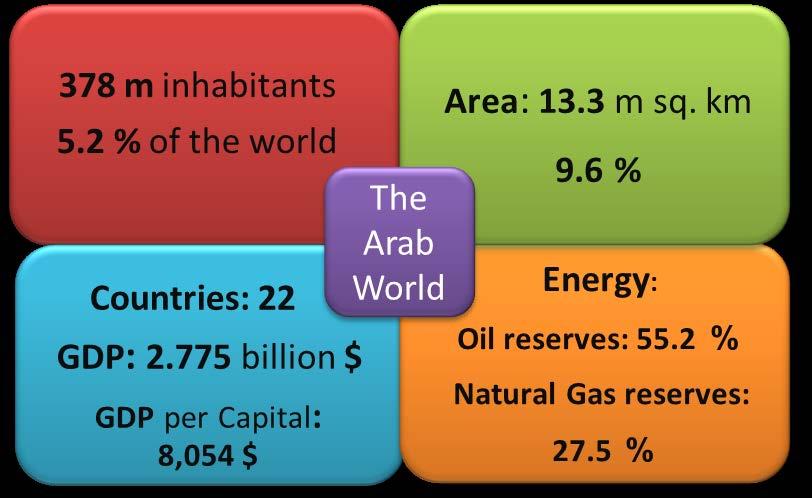

A Sustainable Development in the Mediterranean Area Basilica di San Giovanni Maggiore - Naples, By: Jamila Matar Director, Energy Department -LAS

|

|

|

- Winfred Harrell

- 5 years ago

- Views:

Transcription

1 AEIT annual International Conference 2015 A Sustainable Development in the Mediterranean Area Basilica di San Giovanni Maggiore - Naples, October 2015 By: Jamila Matar Director, Energy Department -LAS

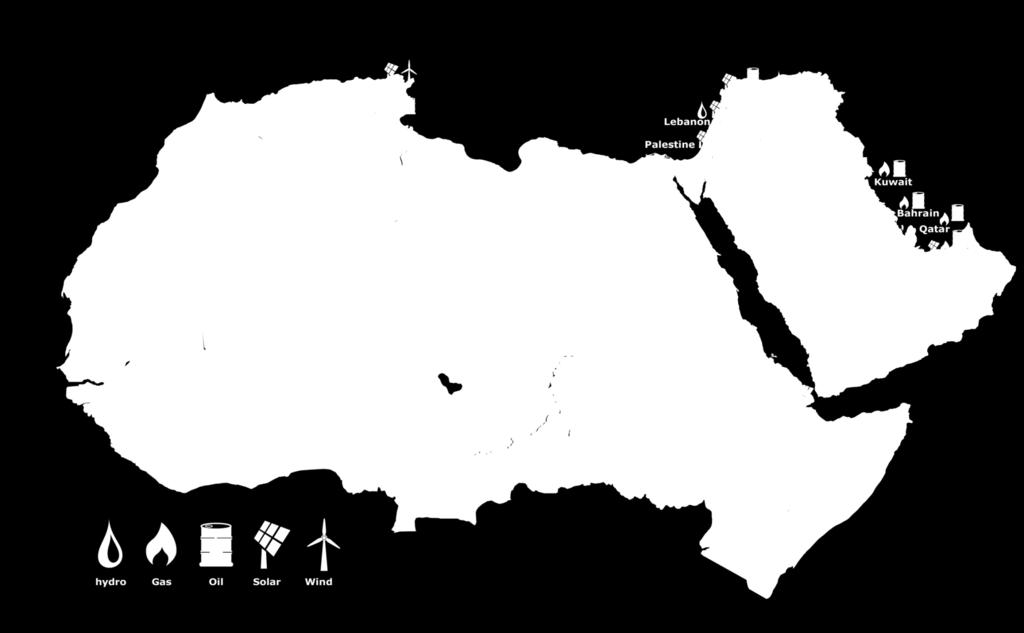

2 Oil, Gas and RE

3 Coal % 0.9 Diesel 2.8% Hydro % 4.6 Wind % 0.5 Installed Capacity (MW) By Fuel Type Solar % 0.1 others % 4.8 Steam % 24.9 The world Combined % 26.7 Gas %34.5 By Country Total installed Capacity: MW

4 / Electricity Demand Forecast Country Generated Power,GWh Peak Load MW Generated Power,GWh Peak Load MW Generated Power,GWh Peak Load MW Jordan 18,092 2,915 24,483 3,941 33,712 5,400 UAE 121,928 20, ,061 25, ,084 30,476 Bahrain 16,295 3,200 27,401 5,571 42,967 8,773 Tunisia 17,650 3,500 21,920 4,430 27,820 5,510 Algeria 63,371 12, ,103 19, ,520 28,382 KSA 337,154 59, ,705 79, ,398 99,700 Sudan 11,724 2,300 20,661 4,162 33,275 6,703 Syria 50,229 9,000 67,200 12,450 89,920 17,400 Iraq 115,000 16, ,000 23, ,000 28,100 Oman 25,000 5,053 34,710 7,100 47,000 9,600 Palestine 5,297 1,136 7,429 1,450 10,419 1,851 Qatar 36,016 6,752 52,369 9,634 60,000 10,942 Kuwait 65,861 13,025 96,771 19, ,188 28,120 Lebanon 13,000 2,880 16,592 3,676 20,186 4,472 Libya 40,373 6,931 54,124 9,222 65,721 11,285 Egypt 188,105 30, ,546 42, ,172 54,260 Morocco 33,621 5,617 46,053 7,696 61,920 10,284 Yemen 7,744 1,607 9,949 1,969 12,697 2,396

5 Additional Capacities During : 140 GW Renewable 7% Diesel 1% Haydro 5% Others 3% Steam Nuclear 0,4% Steam 32% Gas Tur. C C Nuclear Diesel C C 37% Gas Tur. 15% Renewable Haydro Others

6 Elect. Interconn. between Arab Countries Suited conditions Diversification of energy resources in the Arab world from oil and natural gas + RE Variation in daily, seasonal and annual demand for energy among the Arab States. Variation in peak loads times in the Arab States.

7 Elect. Interconn. between Arab Countries Economic and technical impacts Reduce the investment in electric power generation sector, due to the spinning reserve in electric power plants of each country. Benefit from the variation in peak times and time differences, which would allow increase of the potential capacity exchange between interconnected grids. Increase efficiency and reliability of electric power systems to provide support in emergencies. Use of electric interconnection grids to construct informationtransmitting networks between the interconnected countries.

8 Elect. Interconnection: current status EU Electricity Markets Italy EIJLLPST Interconnection Turkey Spain Under Consideration Lebanon Syria Palestine Jordan Iraq Iran Libya Egypt Morocco Algeria Tunisia Maghreb Interconnection Kuwait Bahrain Mauritania Under Consideration KSA Qatar 400 kv 220 kv 150 kv 90 kv 66 kv Existing Not operational/island operation Under-consideration,-study,-construction Sudan Yemen Djibouti Somalia Comoros GCC Interconnection UAE Oman

9 KSA Egypt Interconnection Biggest Electricity systems in the Arab world (90 GW) The interconnection will be performed at 500 KV level, DC, with a capacity of 3000 MW The MOU signed in 1 June 2013, the interconnection agreement in 1 December 2013 Total cost of the project is 1.6 billion USD Egyptian side will pay 610 million USD and the submarine cable will be jointly covered22 In Jan, 2014, the Trans Grid Solutions Inc. Canadian consultancy firm) got the contract. The contracts will be signed in 2015 and the commissioning date is 2018

10 Main Parts of the comprehensive Study III. Institutional & Regulatory frameworks II. Comparison of costs & benefits of exchange of electricity or NG I. Develop a strategy & master plan for upgrading of trade & energy between Arab Countries AMCE Comprehensive Study

11 Recommended Electrical Interconn. Projects Date projects expected to enter into service No. of Circuits Technology Voltage Countries involved 2017 Single Circuit (BtB) a.c. 500/400 kv. Libya Egypt Single Circuit a.c. 400 kv. Tunisia Libya Double Circuit (BtB) a.c. 400 kv. Saudi Jordan Double Circuit (BtB) a.c. 400 kv. Saudi Yemen Double Circuit a.c. 400 kv. Iraq Kuwait Reinforcement (Second Circuit) Reinforcement (Second Circuit) a.c. 400 kv. Egypt Jordan -6 a.c. 400 kv. Syria Jordan -7

12 Recommended Gas Projects Date projects expected to enter into service Capacity 20 BCM/Y 10 BCM/Y Project N/G pipeline between Libya and Egypt N/G pipeline between Iraq and Kuwait BCM/Y LNG Terminal in Bahrain

13 Main outcomes of the Study Review of generation plans in all Arab Countries up to 2030 Determining the preferred scenario of developing electrical and natural gas projects up to 2030 Identifying bottlenecks in internal networks that will result from increased flows over interconnections Calculation of total transfer capacity for all tie lines Preparation of pre-feasibility studies for electrical and gas projects indentified by consultant Development of implementation plans for the various projects Development of a cross border trade model

14 Generation cost expected savings Total cost of generation re-infored electrical Interconnection $127 Billion Peferred Scenario Present value (PV) of saving is $ 35 Billion Disbudded as follows 7 Billion Capital investment $ 120 Billion operational costs Plus an additional $ 11 Billion in Reduction of emissions of harmful gases

15 PA Electricity Market: Institutional Frameworks TSO: Transmission system operator

16 PA Electricity Market: Governance Docs MOU GA PAEM Arab Grid Code Commitment of Arab countries to Pan-Arab market integration Legal basis for Pan-Arab market and subsequent reforms Legal basis for Pan-Arab market institutions Objectives of Pan-Arab electricity market Guiding principles for development of Pan-Arab market Formation of, and roles and responsibilities of PA market institutions Commercial aspects of the Pan-Arab market, including operation, participation and administration Roles and responsibilities Metering, billing and settlement Minimum technical requirements for operation and planning national transmission networks & international interconnections Roles and responsibilities + Metering

17 Pan-Arab Electricity Market Integration Plan Fullyintegrated Pan-Arab Market Ultimate Pan-Arab Market Design Expand Regional Market Function Transition Market Existing Regional Markets Focus: Fullyinterconn. and synchroniz ed Pan- Arab electricity network Focus: Full wholesale competition supported by multiple markets Focus: Unbundle TSOs and introduce wholesale comp. Focus: Identify and expand trade opportunities Focus: GCC, EIJLLPST (8 countries) and Maghreb

18 Arab Electricity Market Evolution: Road Map Governing Institutions Governance Documents Time Table for Implementation Ratification and Coming into Force Membership (Signatories and Observers)

19 The Strategy.Implementation tools Implementation mechanism National Renewable Energy Plans Monitoring and Evaluation Annual Report Reporting System

20 The Strategy.Implementation tools The Way Toward the Implementation of the Road map Developing a Renewable Energy Road Map of Action for Arab Countries

21 Area of intervention and activities of E Policy and Regulatory Frameworks Integration Projects Arab-Regional and Internat. Coop Data Bases and Information Systems Events

22 Meetings and Events Internal Meetings AMCE Executive Office Meeting Experts Committee Meeting Group Meeting SHAMCI network meeting Events Arab Forum on Renewable Energy and EE Arab EE Day Arab China Energy Forum Arab RE&EE Forum Arab EE Day Workshops and Training AREF and NREAP workshop NEEAP regional annual workshop Industrial value chain of RE Electricity Sector Implications on Environment.

23 Regional and International Cooperation Thank you