ECONOMIC IMPACTS AND MARKET CHALLENGES FOR THE METHANE TO DERIVATIVES PETROCHEMICAL SUB-SECTOR

|

|

|

- Kerry Kennedy

- 5 years ago

- Views:

Transcription

1 ECONOMIC IMPACTS AND MARKET CHALLENGES FOR THE METHANE TO DERIVATIVES PETROCHEMICAL SUB-SECTOR

2 Overview Canadian Energy Research Institute Founded in 1975, the Canadian Energy Research Institute (CERI) is an independent, registered charitable organization specializing in the analysis of energy economics and related environmental policy issues in the energy production, transportation, and consumption sectors. Our mission is to provide relevant, independent, and objective economic research of energy and environmental issues to benefit business, government, academia and the public. CERI publications include: Market specific studies Geopolitical analyses Commodity reports (crude oil, electricity and natural gas) In addition, CERI hosts an annual Petrochemical Conference.

3 Canadian Energy Research Institute CERI receives financial support from its core funders which include Natural Resources Canada, Alberta Energy and the Canadian Association of Petroleum Producers. In addition, the institute benefits from funds provided by donors which include: Alberta s Industrial Heartland Association Chemistry Industry Association of Canada Government of Saskatchewan Ivey Foundation University of Calgary CERI also receives in-kind support from the following contributors: Alberta Energy Regulator Advisian Worley Parsons Group Petroleum Services Assoc of Canada Lithuanian Energy Institute Deloitte Canada Ltd. Atlantic Institute for Market Studies

4 Presentation Outline 1. Natural Gas Market 2. Petrochemical Industry 3. Methane-based Products 4. Economic and Environmental Analysis 5. Concluding Remarks

5 Natural Gas Supply and Demand Forecasts Canadian natural gas production forecast Export market under threat. Industrial use, oil sands, power generation, LNG, chemicals and petrochemicals production mmcfd Pipeline Exports LNG Exports Supply Demand

6 The Export Market Challenge

7 Where do we find new markets for Western Canadian Natural Gas? Petrochemicals

8 Global Petrochemical Outlook Source: IHS Chemical 2016

9 North America Petrochemical Outlook Low cost feedstock advantage leading to investments in chemicals and derivatives

Source: Argus")

10 Methanol Outlook Methanol demand is forecast to grow at 4% globally compound annual growth rate (CAGR) Source: Argus 2017

11 Petrochemicals in Canada 9,000 92%/8% 60%/40% 0%/100% 75%/25% kt/yr 8,000 7,000 6,000 5,000 4,000 7,399 1,722 4, ,000 2,000 1,000-5,677 4,538 1, , Alberta Ontario Quebec Canada Olefins Aromatics Total

12 Methane as a Feedstock

13 Methane Derivatives Acetic Acid Credit potential if sequestered? Methane (CH 4 ) CO 2 Synthesis Gas (Syngas) Hydrogen (H 2 ) Methanol (MeOH) Formaldehyde Methyl tert-butyl ether (MTBE) Dimethyl ether (DME) Methylamine Methanol to Olefins (MTO) Methanol to Propylene (MTP) Methanol to Gasoline (MTG) METHYL METHACRYLATE (MMA) Natural Gas (N.G) Ammonia Urea Natural gas Liquified liquids Petroleum Gas (NGLs) (LPG) Fischer-Tropsch Process

14 Economic Assessment 1. Assessment of 9 technologies: Methanol, Hydrogen, MTP, MTO, MTG, Ammonia, Urea, Formaldehyde and Fischer Tropsch Gasoline 2. Key Assumptions 3. Life Cycle Costs (LCC): NPV of CAPEX (ISBL- inside battery limits and OSBL Outside Battery Limits), Natural Gas costs, taxes, etc. 4. Jurisdictional competitiveness comparison: AB, ON, USGC 5. Discounted NPV and Internal Rate of Return (IRR) 6. Direct and indirect economic impacts: GDP, Employment

15 CO 2 Tax Assumptions ($/T CO2) Canada: 20 (2019), 30 (2020), 40 (2021), 50 (2022->) Alberta: 30 (2019), 30 (2020), 40 (2021), 50 (2022->) Ontario: Mid-range CO 2 Price Forecast (ICF Study for OEB)

16 Price Assumptions Derivative prices are kept constant Where available 2016 are used Natural Gas Price Assumption USGC AB ON Average 2016 Prices Natural Gas (US$/ MMBTU) Henry, AECO and Dawn Hubs Prices

17 Growth Assumptions

18 Results: IRR for 9 Methane Derivatives Applying the new US Corporate Tax Code improves the IRR of Hydrogen and Methanol by 1.7% and 1.5%, respectively.

19 Methanol NPV Jurisdictional Comparison Gone

20 Hydrogen NPV Jurisdictional Comparison Gone Higher Exemption limit

21 Now 12%-14% Methanol: Life Cycle Costs Make-up

22 Methanol Tax Rebates Scenarios 1: Provincial Tax Rebate Could Increase IRR by: 1.1% in AB 0.9% in ON 2: Corporate Tax Rebate Could Increase IRR by: 2.3% in AB 2% in ON

23 GDP Economic Impacts Product Alberta (GDP C$ Million) Ontario (GDP C$ Million) Provincial National Provincial National FTS H Methanol Employment: Person years Jurisdiction H2 MeOH FTS Provincial Canada Provincial Canada Provincial Canada Alberta 1,059 1,509 7,499 10,686 9,230 13,153 Ontario 1,908 2,287 13,520 16,200 16,623 19,918

24 Concluding Remarks New capacity for ethylene, propylene and methanol followed energy and demand growth dynamics Results show that some opportunities exists for methane derivatives sub-sector in Alberta. This is driven principally by 10-15% low feedstock prices, OPEX and corporate taxes. CO 2 taxes based on custom approaches for trade exposed industries seems to sustain economic competitiveness against the USGC. New natural gas feedstock demand 0.5 bcfd However, the new US Tax Code will likely make USGC the most competitive jurisdiction. For example, it improves the IRR of Hydrogen and Methanol by 1.7% and 1.5%, respectively.

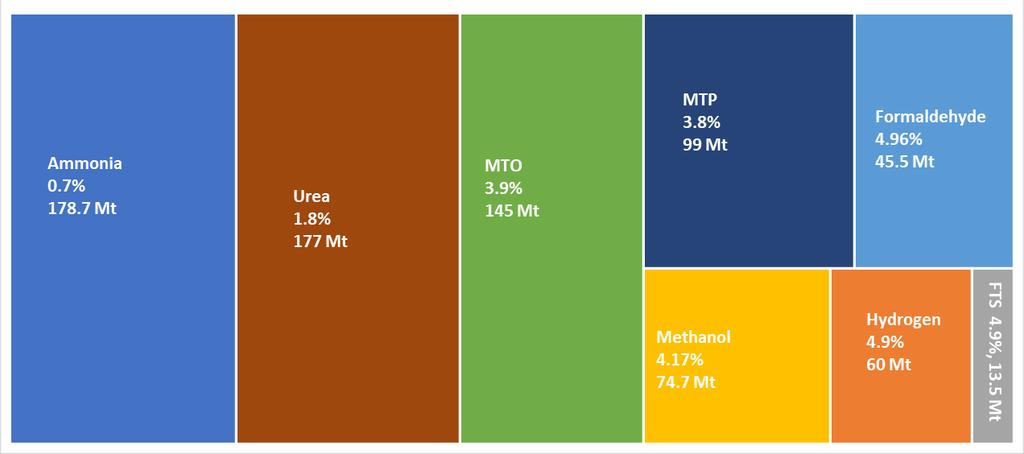

25 US Tax Code Change is Significant NPV Advantage to USGC Compared to Canadian Product Jurisdictions Due to Tax Code Change (US$ million) Ammonia 24.0 Formaldehyde 0.6 FTS Hydrogen 1.7 Methanol MTO 28.9 MTP 33.7 MTG 14.3 Urea 17.6

26 Thank You for Your Time CANADIAN ENERGY RESEARCH UPCOMING STUDIES: Economic and Emission Impacts of Oil Sands Production Carbon Management Impacts on Electricity Markets Economic and Emissions Impacts of Conventional Oil and Gas Production UPCOMING CONFERENCE: Petrochemical: June , Kananaskis, AB Allan Fogwill President & CEO