Fraud and the Small Business Owner

|

|

|

- Britton Taylor

- 6 years ago

- Views:

Transcription

1 Fraud and the Small Business Owner Can you recognize it when you see it? National Society of Accountants Annual Meeting August 15, 2009 Erik H. Lindquist, CFE Presenter

2 Definition The use of one s occupation for personal enrichment through the deliberate misuse of the employing organizations resources or assets

3 Trends and Concerns Estimated Losses from Fraud Billion Dollars Billion Dollars Estimates are based on 6% of GDP for period

4

5 How we classify fraud Asset Misappropriation - 89% of all cases Corruption - 27% Fraudulent Financial Statements - 10% percentages will be greater than 100% due to cross-over in categories

6 In Asset Misappropriation CASH IS KING 84 % of reported frauds in 2006 survey were cash related Median loss is $93,000 per CASE Types of Asset Misappropriation Fraudulent Disbursements 74.1% Skimming 16.6% Larceny 10.3%

7 Fraudulent Disbursements The greatest opportunity to the employees of a small business Billing Schemes (1) Payroll Schemes Check Tampering (2) Expense Reimbursement (3) Register Disbursement Median Loss - $125,000

8 Summary from ACFE Report to the Nation--2006

9 How do you discover fraud? Tip 46.6% Internal Audit 19.4% Accident 20.0% Internal Controls 23.3% External Audit 9.1% Notified By Police 3.2%

10 How do you discover fraud? Tip from employee - 59% Tip from customer % Anonymous tip % Tip from vendor %

11 How to Prevent Fraud Internal Controls Background Checks on Employees (preemployment) Regular Fraud Audits (six month cycle) Established Fraud Policy Be Willing to Prosecute Ethics Training Anonymous Reporting Mechanism Workplace Surveillance

12 Fraud Vulnerability - another 12 step program Preliminary meeting Gather Information Customize Assessment Management interviews Preliminary Interviews with supervisors Field interviews and Controls testing Use findings to ID Vulnerabilities Determine Prob. of Occurrence Determine Severity of impact Develop Recommendations Post Assessment Report

13 Fraud Prevention Fraud prevention is the most cost-effective way to reduce fraud Involves two fundamental activities: Sustain a culture of honesty and high ethics Assess the risks for fraud, develop concrete responses to mitigate the risks, and eliminate the opportunities for fraud 14

14 Fraud Prevention Sustain a Culture of Honesty & High Ethics Five critical elements: 1. Have management model appropriate behavior 2. Hire the right kind of employees 3. Communicate expectations and require periodic written acceptance to the expectations 4. Create a positive work environment 5. Enforce policies for handling fraud 15

15 Fraud Prevention Research on Why People Lie Have fear of punishment or adverse consequences Have a habit of lying Seen others lie or have had negative modeling Feel if they tell the truth they won t get what they want 16

16 Fraud Prevention Eliminate Fraud Opportunities Organizations should: Identify and measure fraud risks Implement preventative and detective controls Create widespread monitoring by employees Have internal and external auditors 17

17 Organizational Culture Way to Create a Culture of Honesty, Openness, and Assistance 1. Hire honest people and provide fraud awareness training. 2. Create a positive work environment. 3. Provide an employee assistance program 18 (EAP). How This Step Is Accomplished 1. Verify all information on the applicant s résumé and application. 2. Require all applicants to affirm the truth of the matters set forth in their application and résumé. 3. Train management to conduct thorough and skillful interviews. 1. Create expectations about honesty by having a good corporate code of conduct and conveying those expectations throughout the organization. 2. Have open door or easy access policies. 3. Have positive personnel and operating procedures. 1. Implement an EAP that helps employees deal with personal and nonsharable pressures in their lives.

18 Eliminate Opportunities for Fraud Five ways to eliminate fraud opportunities: 1. Have good internal controls 2. Discourage collusion 3. Monitor employees and provide a whistleblowing system 4. Create an expectation of punishment and 5. Conduct proactive auditing 19

19 Early Fraud Detection Three Primary Ways to Detect Fraud 1.By chance 2.By providing whistle-blowing systems 3.By data mining 20

20 Early Fraud Detection Whistle-blowing Systems A reporting hotlines or online system that allows others to call in or submit an anonymous tip of a fraud suspicion Examples: Internal systems/hotlines The Association of Certified Fraud Examiners Allegiance 21

21 Early Fraud Detection Mining Company Databases Mining databases for suspicious trends, numbers, and other anomalies. Data-mining programs: ACL Picalo 22

22 How to delicately ask the owner about this issue Are you concerned about sales and cash trends not tracking consistently? How many employees have access to the checkbook - who signs checks - who reconciles? No less then 3 people should handle the cash disbursements! One to draft check-one to sign and one to reconcile the bank statement

23 How to delicately ask the owner about this issue How often do you count inventory? Are your employees paid a competitive wage? Do you do background checks on financial staff? Have you ever had a fraud vulnerability check-up

24 How to delicately ask the owner about this issue Do you believe an annual audit or review covers your risk to fraud? It doesn t this is called the expectation gap Can your employees anonymously report concerns to you? Do you review your monthly financials for unusual trends? A/P, Inventory, Cash, A/R, Trial Balance Ensure that all Journal Entries have descriptions

25 Preventing Fraud A Summary Create a culture of Honesty, Openness, and Assistance Have a Code of Ethics Implement Employee Assistance Programs Eliminate Opportunities Have good internal controls Provide tip hotlines Discourage Collusion Create a Positive Work Environment Hire honest people and provide fraud awareness training Create an expectation of punishment Monitor employees Publicize company policies Proactively audit for fraud 26

26 Preventing Fraud Suggested Model Tone at the Top Investigation and Follow-up Education and Training Proactive Detection Integrity Risk and Controls 27 Reporting and Monitoring

27 Reforms Bypass Non-Profits Sarbanes-Oxley Does Not apply Public Trust Is Being Eroded IRS Is Raising Alarms in Congress For Regulations To Be Implemented

28 Loss Of Public Confidence Leads To Drop in Donations/Contributions Increase of Negative Press May Actually Attract the Wrong Type of Employee Death Spiral of Drops in Membership and Donations

29

30 For more information Erik H. Lindquist, CFE Lindquist & Associates, LLC Resources: Fraud ExaminationW. Steve Albrecht et al Third Edition, Cengage Learning; 2009 Association of Certified Fraud Examiners Fraud Casebook Lessons from the Bad Side of Business edited by Joseph T. Wells, CFE, CPA; Wiley, 2007

FRAUD SCHEMES. South Carolina HFMA Finance & Reimbursement Forum. November 13, 2012 WITH RELATED INTERNAL CONTROLS

FRAUD SCHEMES WITH RELATED INTERNAL CONTROLS South Carolina HFMA Finance & Reimbursement Forum November 13, 2012 2 Fraud Facts: Estimated loss of 5% of annual revenues to occupational fraud Financial statement

FRAUD SCHEMES WITH RELATED INTERNAL CONTROLS South Carolina HFMA Finance & Reimbursement Forum November 13, 2012 2 Fraud Facts: Estimated loss of 5% of annual revenues to occupational fraud Financial statement

Fraud Prevention Training

Fraud Prevention Training The Massachusetts Collectors and Treasurers Association Sixty-Sixth Annual Education Conference June 15, 2015 Presented By: Eric Demas, CFE Melanson Heath edemas@melansonheath.com

Fraud Prevention Training The Massachusetts Collectors and Treasurers Association Sixty-Sixth Annual Education Conference June 15, 2015 Presented By: Eric Demas, CFE Melanson Heath edemas@melansonheath.com

Presented by Ed Williamson and Erica Bailey

Presented by Ed Williamson and Erica Bailey Internal Controls & Fraud Detection Objectives Background on internal controls Review of organizational and functional level controls Fraud prevention and risk

Presented by Ed Williamson and Erica Bailey Internal Controls & Fraud Detection Objectives Background on internal controls Review of organizational and functional level controls Fraud prevention and risk

Eric Kinsherf, CPA MMAAA Conference June 12, 2018

Eric Kinsherf, CPA MMAAA Conference June 12, 2018 Agenda Overview What is Fraud? How does Fraud happen? How to Detect and Prevent Fraud Summarize Objectives Gain better Understanding of Fraud Risk Illustrate

Eric Kinsherf, CPA MMAAA Conference June 12, 2018 Agenda Overview What is Fraud? How does Fraud happen? How to Detect and Prevent Fraud Summarize Objectives Gain better Understanding of Fraud Risk Illustrate

Fraud Awareness Jennifer Murtha Clara Ewing

Fraud Awareness Jennifer Murtha Clara Ewing The Monkey Business Illusion 2 Fraud Defined The term fraud is defined in Black's Law Dictionary (Sixth Edition, 1990) as: An intentional perversion of truth

Fraud Awareness Jennifer Murtha Clara Ewing The Monkey Business Illusion 2 Fraud Defined The term fraud is defined in Black's Law Dictionary (Sixth Edition, 1990) as: An intentional perversion of truth

FRD510. Principles of Fraud Examination - 20 hours. Objectives

FRD510 Principles of Fraud Examination - 20 hours Objectives Call them the CSI experts of the financial world. Accountants play a central role in the detection and deterrence of fraud in all its notorious

FRD510 Principles of Fraud Examination - 20 hours Objectives Call them the CSI experts of the financial world. Accountants play a central role in the detection and deterrence of fraud in all its notorious

Virginia Association of School Business Officers Getting Reacquainted with Internal Controls Presented by John S. Aldridge, CPA

Virginia Association of School Business Officers Getting Reacquainted with Internal Controls Presented by John S. Aldridge, CPA Introduction What are internal controls? Simple Definition Internal control

Virginia Association of School Business Officers Getting Reacquainted with Internal Controls Presented by John S. Aldridge, CPA Introduction What are internal controls? Simple Definition Internal control

Fraud Prevention, Detection, and Internal Controls

Fraud Prevention, Detection, and Internal Controls Budget, Accounting and Reporting Council May 28, 2015 Sherrie Ard, CPA, CFE Financial Management Specialist Local Government Performance Center Local

Fraud Prevention, Detection, and Internal Controls Budget, Accounting and Reporting Council May 28, 2015 Sherrie Ard, CPA, CFE Financial Management Specialist Local Government Performance Center Local

38 Years of Excellent Client Service New COSO Model and How Internal Controls Help to Reduce Opportunity for Fraud

38 Years of Excellent Client Service New COSO Model and How Internal Controls Help to Reduce Opportunity for Fraud Presented By William Blend, CPA, CFE Session Overview Review the new COSO model on internal

38 Years of Excellent Client Service New COSO Model and How Internal Controls Help to Reduce Opportunity for Fraud Presented By William Blend, CPA, CFE Session Overview Review the new COSO model on internal

Fraud in the Insurance Industry How it Can Impact Your Agency

A MarshBerry Publication Volume XXIX, Issue 4 APRIL 2013 Authored by Molly McCarthy, Senior Consultant 440.392.6584 email: Molly.McCarthy@MarshBerry.com Fraud in the Insurance Industry How it Can Impact

A MarshBerry Publication Volume XXIX, Issue 4 APRIL 2013 Authored by Molly McCarthy, Senior Consultant 440.392.6584 email: Molly.McCarthy@MarshBerry.com Fraud in the Insurance Industry How it Can Impact

Information and and training provid v ed by Smith Elliott Elliott Kearns & Compan

Nuts and Bolts of Avoiding Fraud in Your Organization Information and training provided by Smith Elliott Kearns & Company, LLC as part of this Fraud Avoidance presentation is intended for reference only.

Nuts and Bolts of Avoiding Fraud in Your Organization Information and training provided by Smith Elliott Kearns & Company, LLC as part of this Fraud Avoidance presentation is intended for reference only.

MANAGING FRAUD RISK. Teresa D. Thamer, CPA, CFE Brenau University

MANAGING FRAUD RISK Teresa D. Thamer, CPA, CFE Brenau University Overview I. Understanding what Fraud is and is not II. Identifying and assessing key fraud risk areas III. Developing a Comprehensive Fraud

MANAGING FRAUD RISK Teresa D. Thamer, CPA, CFE Brenau University Overview I. Understanding what Fraud is and is not II. Identifying and assessing key fraud risk areas III. Developing a Comprehensive Fraud

Who Owns Fraud Uniting Corporate Executives to Manage Your Anti-Fraud Program

Who Owns Fraud Uniting Corporate Executives to Manage Your Anti-Fraud Program Monday June 13, 2011 10:20 11:40 San Diego, California Who owns fraud why is it important? Many companies struggle to determine

Who Owns Fraud Uniting Corporate Executives to Manage Your Anti-Fraud Program Monday June 13, 2011 10:20 11:40 San Diego, California Who owns fraud why is it important? Many companies struggle to determine

Can You Spot Fraudsters?

Can You Spot Fraudsters? CACUBO Workshop March 22, 2018 Eric Conforti, CPA, CFE 1 Who Are We? A One-Firm Firm: Over 2,200 industry experts to partner with when specific industry knowledge is needed during

Can You Spot Fraudsters? CACUBO Workshop March 22, 2018 Eric Conforti, CPA, CFE 1 Who Are We? A One-Firm Firm: Over 2,200 industry experts to partner with when specific industry knowledge is needed during

Laurie Beets. PDG 27 th National College & University Bursars & SFS Conference

Foiling Fraudsters Laurie Beets Oklahoma State University Acknowledgements 2006 Fraud Examiners Manual, Association of Certified Fraud Examiners (ACFE) 2012 Report to the Nation on Occupational Fraud &

Foiling Fraudsters Laurie Beets Oklahoma State University Acknowledgements 2006 Fraud Examiners Manual, Association of Certified Fraud Examiners (ACFE) 2012 Report to the Nation on Occupational Fraud &

OUTSMART FRAUD. Strategic Internal Controls to Prevent Business Fraud

OUTSMART FRAUD Strategic Internal Controls to Prevent Business Fraud GrowthForce LLC 800 Rockmead Drive Suite 200 Phone 281.358.2007 Fax 281.358.4120 OUTSMART BUSINESS FRAUD Using statistical data from

OUTSMART FRAUD Strategic Internal Controls to Prevent Business Fraud GrowthForce LLC 800 Rockmead Drive Suite 200 Phone 281.358.2007 Fax 281.358.4120 OUTSMART BUSINESS FRAUD Using statistical data from

SMALL BUSINESS FRAUD ASSESSMENT INTERNAL CONTROL QUESTIONNAIRE Download your risk assessment form at

SMALL BUSINESS FRAUD ASSESSMENT INTERNAL CONTROL QUESTIONNAIRE Download your risk assessment form at www.businessfraudprevention.org/forms.html Owner: Date: Discussed with: Question Yes No N/A Comments

SMALL BUSINESS FRAUD ASSESSMENT INTERNAL CONTROL QUESTIONNAIRE Download your risk assessment form at www.businessfraudprevention.org/forms.html Owner: Date: Discussed with: Question Yes No N/A Comments

Anti-Fraud Programs and Control Policy

Anti-Fraud Programs and Control Policy OVERVIEW This document provides an overview of the programs and controls Tahoe Resources Inc. ( Tahoe ) follows in order to evaluate fraud risk as it pertains to

Anti-Fraud Programs and Control Policy OVERVIEW This document provides an overview of the programs and controls Tahoe Resources Inc. ( Tahoe ) follows in order to evaluate fraud risk as it pertains to

FRAUD AWARENESS UPDATE

Tammy Michaud, CPA, Principal Sarah Belliveau, CPA, Senior Manager FRAUD AWARENESS UPDATE berrydunn.com CATEGORIES OF FRAUD Asset misappropriations (stealing) Theft or misuse of assets Corruption Inappropriate

Tammy Michaud, CPA, Principal Sarah Belliveau, CPA, Senior Manager FRAUD AWARENESS UPDATE berrydunn.com CATEGORIES OF FRAUD Asset misappropriations (stealing) Theft or misuse of assets Corruption Inappropriate

Auditors Fraud Primer

Auditors Fraud Primer CAST Presentation Dallas Chapter IIA/Dallas Chapter ACFE Joint Meeting November 1, 2011 Cityplace Conference Center Dallas, Texas Ray Lindsay, CPA/CFF CFE Overview Fraud and Occupational

Auditors Fraud Primer CAST Presentation Dallas Chapter IIA/Dallas Chapter ACFE Joint Meeting November 1, 2011 Cityplace Conference Center Dallas, Texas Ray Lindsay, CPA/CFF CFE Overview Fraud and Occupational

Fraud Risk Management

Fraud Risk Management Specific Anti-Fraud Controls (Process or Transaction Level) 2017 Association of Certified Fraud Examiners, Inc. Discussion Questions 1. Does your organization have adequate staffing

Fraud Risk Management Specific Anti-Fraud Controls (Process or Transaction Level) 2017 Association of Certified Fraud Examiners, Inc. Discussion Questions 1. Does your organization have adequate staffing

Journal of Business & Economics Research January 2006 Volume 4, Number 1

Family Owned Business Fraud: The Silent Thief M. Tony Bledsoe, (E-mail: bledsoem@meredith.edu), Meredith College Susan B. Wessels, (E-mail: wesselss@meredith.edu), Meredith College Abstract The ACFE 2002

Family Owned Business Fraud: The Silent Thief M. Tony Bledsoe, (E-mail: bledsoem@meredith.edu), Meredith College Susan B. Wessels, (E-mail: wesselss@meredith.edu), Meredith College Abstract The ACFE 2002

OCCUPATIONAL FRAUD IN GOVERNMENT AND STEPS TO PREVENT AND DETECT IT

OCCUPATIONAL FRAUD IN GOVERNMENT AND STEPS TO PREVENT AND DETECT IT This session will explore government fraud risks as well as common areas of abuse and corresponding red flags. It will also provide ideas

OCCUPATIONAL FRAUD IN GOVERNMENT AND STEPS TO PREVENT AND DETECT IT This session will explore government fraud risks as well as common areas of abuse and corresponding red flags. It will also provide ideas

FRAUD DETECTION. Early Detection = $ Saved. Red Flag = Danger. But a symptom = FRAUD. Accounting Anomalies. Accounting Anomalies

Proactive Fraud Auditing End of Chapter 4 in Albrecht FRAUD DETECTION Recognizing the Symptoms of Fraud Actg 537 Identify Risk Exposures 1 2 Identify Fraud Symptoms for Each Exposure Proactively Look for

Proactive Fraud Auditing End of Chapter 4 in Albrecht FRAUD DETECTION Recognizing the Symptoms of Fraud Actg 537 Identify Risk Exposures 1 2 Identify Fraud Symptoms for Each Exposure Proactively Look for

Fraud Prevention: How to Identify and Protect Your Higher Ed Institution

Fraud Prevention: How to Identify and Protect Your Higher Ed Institution November 16, 2017 Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC-registered investment

Fraud Prevention: How to Identify and Protect Your Higher Ed Institution November 16, 2017 Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC-registered investment

ACCTG 533: Module 14: Asset Misappropriation Fraud. [Slide Content]: Asset Misappropriation Fraud. [Jeanne H. Yamamura]: Asset Misappropriation Fraud

![ACCTG 533: Module 14: Asset Misappropriation Fraud. [Slide Content]: Asset Misappropriation Fraud. [Jeanne H. Yamamura]: Asset Misappropriation Fraud](/thumbs/81/83190759.jpg "ACCTG 533: Module 14: Asset Misappropriation Fraud. [Slide Content]: Asset Misappropriation Fraud. [Jeanne H. Yamamura]: Asset Misappropriation Fraud") ACCTG 533: Module 14: Asset Misappropriation Fraud Asset Misappropriation Fraud Asset Misappropriation Fraud Asset Misappropriation Fraud Theft or misuse of company assets Most common type of fraud Every

ACCTG 533: Module 14: Asset Misappropriation Fraud Asset Misappropriation Fraud Asset Misappropriation Fraud Asset Misappropriation Fraud Theft or misuse of company assets Most common type of fraud Every

Karen L. Mosteller, CPA, CHBC

Karen L. Mosteller, CPA, CHBC Recognize the Red Flags of Fraud and areas of vulnerability Examine checks and balances that should be implemented Establish processes and procedures needed for fraud protection

Karen L. Mosteller, CPA, CHBC Recognize the Red Flags of Fraud and areas of vulnerability Examine checks and balances that should be implemented Establish processes and procedures needed for fraud protection

10/6/2018. Frank Gorrell, MSA, CPA, CGMA. Payroll fraud happens! No organization is immune! We ll checks the stats We ll review controls

Frank Gorrell, MSA, CPA, CGMA Payroll fraud happens! No organization is immune! We ll checks the stats We ll review controls 1 Association of Certified Fraud Examiners (ACFE) Report to the Nations 2018

Frank Gorrell, MSA, CPA, CGMA Payroll fraud happens! No organization is immune! We ll checks the stats We ll review controls 1 Association of Certified Fraud Examiners (ACFE) Report to the Nations 2018

Fraud prevention, detection and investigation

BUSINESS RISK MANAGEMENT LTD Fraud prevention, detection and investigation Who should attend? Internal auditors in organisations without a dedicated fraud team Auditors who need to learn about the most

BUSINESS RISK MANAGEMENT LTD Fraud prevention, detection and investigation Who should attend? Internal auditors in organisations without a dedicated fraud team Auditors who need to learn about the most

STUDY UNIT TEN INTERNAL AUDIT RESPONSIBILITIES FOR FRAUD

STUDY UNIT TEN INTERNAL AUDIT RESPONSIBILITIES FOR FRAUD 1 10.1 Fraud -- Nature, Prevention, and Detection..................................... 1 10.2 Fraud -- Indicators........................................................

STUDY UNIT TEN INTERNAL AUDIT RESPONSIBILITIES FOR FRAUD 1 10.1 Fraud -- Nature, Prevention, and Detection..................................... 1 10.2 Fraud -- Indicators........................................................

Fraud Risk Management

Fraud Risk Management Introduction Bethmara Kessler, CFE, CISA Campbell Soup Company 2017 Association of Certified Fraud Examiners, Inc. CPE Information 2017 Association of Certified Fraud Examiners, Inc.

Fraud Risk Management Introduction Bethmara Kessler, CFE, CISA Campbell Soup Company 2017 Association of Certified Fraud Examiners, Inc. CPE Information 2017 Association of Certified Fraud Examiners, Inc.

MIS 5208 Week 2 Fraud Detection & Prevention

MIS 5208 Week 2 Fraud Detection & Prevention Introductions, Course Outline, and Other Administration Issues Ed Ferrara, MSIA, CISSP eferrara@temple.edu Fraud Awareness & Internal Controls Awareness Internal

MIS 5208 Week 2 Fraud Detection & Prevention Introductions, Course Outline, and Other Administration Issues Ed Ferrara, MSIA, CISSP eferrara@temple.edu Fraud Awareness & Internal Controls Awareness Internal

Answering the Call. Increased Ethics, Governance & Compliance through the implementation of a Whistleblower Hotline.

Answering the Call Increased Ethics, Governance & Compliance through the implementation of a Whistleblower Hotline. Tina Marshall & Mark Nance American Fidelity Corporation Agenda Why? Definitions, Regulations,

Answering the Call Increased Ethics, Governance & Compliance through the implementation of a Whistleblower Hotline. Tina Marshall & Mark Nance American Fidelity Corporation Agenda Why? Definitions, Regulations,

Internal Control Awareness: Tips for Improving Business Practices

Internal Control Awareness: Tips for Improving Business Practices S U S A N H A C K E R I N T E R N A L A U D I T O R Agenda Understand the value of internal controls. Learn some basic principles and best

Internal Control Awareness: Tips for Improving Business Practices S U S A N H A C K E R I N T E R N A L A U D I T O R Agenda Understand the value of internal controls. Learn some basic principles and best

Moving the Needle: Fighting Fraud from the Inside Through Audit. Mary Breslin, CFE, CIA President Empower Audit Training and Consulting

Moving the Needle: Fighting Fraud from the Inside Through Audit Mary Breslin, CFE, CIA President Empower Audit Training and Consulting Moving the Needle Fighting Fraud from the Inside Through Audit Mary

Moving the Needle: Fighting Fraud from the Inside Through Audit Mary Breslin, CFE, CIA President Empower Audit Training and Consulting Moving the Needle Fighting Fraud from the Inside Through Audit Mary

FRAUD DETERRENCE AND DETECTION

FRAUD DETERRENCE AND DETECTION Segregation of Duties Corruption Scheme Red Flags Unchecked authority to approve No formal documented procedures Circumventing normal policies and procedures Employees receiving

FRAUD DETERRENCE AND DETECTION Segregation of Duties Corruption Scheme Red Flags Unchecked authority to approve No formal documented procedures Circumventing normal policies and procedures Employees receiving

With Jodi Kippe, CPA & Partner Retail Dealer Practice at Crowe Horwath LLP. Moderated by Mike Bowers, Executive Editor at DealersEdge

How to Identify and Stop Internal Theft in the Dealership! Failing to be alert for employee schemes to embezzle or otherwise steal from the dealership can be not only costly - It's embarrassing! With Jodi

How to Identify and Stop Internal Theft in the Dealership! Failing to be alert for employee schemes to embezzle or otherwise steal from the dealership can be not only costly - It's embarrassing! With Jodi

With Jodi Kippe, CPA & Partner Retail Dealer Practice at Crowe Horwath LLP. Moderated by Mike Bowers, Executive Editor at DealersEdge

How to Identify and Stop Internal Theft in the Dealership! Failing to be alert for employee schemes to embezzle or otherwise steal from the dealership can be not only costly - It's embarrassing! With Jodi

How to Identify and Stop Internal Theft in the Dealership! Failing to be alert for employee schemes to embezzle or otherwise steal from the dealership can be not only costly - It's embarrassing! With Jodi

Internal Controls for Deans, Directors and Chairs

Internal Controls for Deans, Directors and Chairs Presented by: Laura Howat, CPA Controller/Director Financial Management Financial and Business Services Phone: 801-581-5077 Email: laura.howat@admin.utah.edu

Internal Controls for Deans, Directors and Chairs Presented by: Laura Howat, CPA Controller/Director Financial Management Financial and Business Services Phone: 801-581-5077 Email: laura.howat@admin.utah.edu

Creating a Fraud Risk Assessment and Implementing a Continuous Monitoring Program. Christopher DiLorenzo, CFE, CPA, CIA, CRMA

Creating a Fraud Risk Assessment and Implementing a Continuous Monitoring Program Christopher DiLorenzo, CFE, CPA, CIA, CRMA 2015 Association of Certified Fraud Examiners, Inc. Creating a Robust Fraud

Creating a Fraud Risk Assessment and Implementing a Continuous Monitoring Program Christopher DiLorenzo, CFE, CPA, CIA, CRMA 2015 Association of Certified Fraud Examiners, Inc. Creating a Robust Fraud

Auditing for Fraud. Planning & Approaches

Auditing for Fraud Planning & Approaches Today s Agenda Introductions What is Fraud? Internal audit and fraud Managing Fraud as an organization 2 Today s Agenda Introductions 3 Clark Schaefer Consulting?

Auditing for Fraud Planning & Approaches Today s Agenda Introductions What is Fraud? Internal audit and fraud Managing Fraud as an organization 2 Today s Agenda Introductions 3 Clark Schaefer Consulting?

Employee Dishonesty: Prevention and Detection

Employee Dishonesty: Prevention and Detection Frontline Risk Management Series Welcome to this session on Employee Dishonesty, a risk management module presented by CUMIS General Insurance s Risk Solutions

Employee Dishonesty: Prevention and Detection Frontline Risk Management Series Welcome to this session on Employee Dishonesty, a risk management module presented by CUMIS General Insurance s Risk Solutions

CHAPTER 6 GOVERNMENT ACCOUNTABILITY

Kern County Administrative Policy and Procedures Manual CHAPTER 6 GOVERNMENT ACCOUNTABILITY Section Page 601. General Statement... 1 602. Definitions... 1 603. Fraud, Waste, and Abuse... 1 604. Fraud Protocol...

Kern County Administrative Policy and Procedures Manual CHAPTER 6 GOVERNMENT ACCOUNTABILITY Section Page 601. General Statement... 1 602. Definitions... 1 603. Fraud, Waste, and Abuse... 1 604. Fraud Protocol...

2009 ACBO Annual Conference

Developing an Effective Anti Fraud Program 2009 ACBO Annual Conference October 26, 2009 1 Presenters Linda Saddlemire Carroll King Ernie Cooper VLS Fraud Solutions Team Members 2 Carroll King Tapestry

Developing an Effective Anti Fraud Program 2009 ACBO Annual Conference October 26, 2009 1 Presenters Linda Saddlemire Carroll King Ernie Cooper VLS Fraud Solutions Team Members 2 Carroll King Tapestry

ACFE FRAUD PREVENTION CHECK-UP ASSOCIATION OF CERTIFIED FRAUD EXAMINERS

ACFE FRAUD PREVENTION ASSOCIATION OF CERTIFIED FRAUD EXAMINERS ACFE FRAUD PREVENTION One of the ACFE s most valuable fraud prevention resources, the ACFE Fraud Prevention Check-Up is a simple yet powerful

ACFE FRAUD PREVENTION ASSOCIATION OF CERTIFIED FRAUD EXAMINERS ACFE FRAUD PREVENTION One of the ACFE s most valuable fraud prevention resources, the ACFE Fraud Prevention Check-Up is a simple yet powerful

Fraud Awareness February 27, 2015

Fraud Awareness February 27, 2015 Clara Ewing Megan Dix Fraud Defined The term fraud is defined in Black's Law Dictionary (Sixth Edition, 1990) as: An intentional perversion of truth for the purpose of

Fraud Awareness February 27, 2015 Clara Ewing Megan Dix Fraud Defined The term fraud is defined in Black's Law Dictionary (Sixth Edition, 1990) as: An intentional perversion of truth for the purpose of

Common Frauds Found in Not-for- Profit Organizations

Common Frauds Found in Not-for- Profit Organizations NCACPA Not-for-Profit Conference May 19, 2015 Presented by Lynda M. Dennis CPA, CGFO, PhD Today s Session Overview 2014 Occupational Fraud Report Findings

Common Frauds Found in Not-for- Profit Organizations NCACPA Not-for-Profit Conference May 19, 2015 Presented by Lynda M. Dennis CPA, CGFO, PhD Today s Session Overview 2014 Occupational Fraud Report Findings

Chapter 7 Internal Controls

Chapter 7 Internal Controls Establishment of and adherence to internal controls is a major part of managing an organization. Internal controls serve as the first line of defense in safeguarding assets

Chapter 7 Internal Controls Establishment of and adherence to internal controls is a major part of managing an organization. Internal controls serve as the first line of defense in safeguarding assets

Speaker: Steve Dawson 7/13/2017

Speaker: Steve Dawson 7/13/2017 THE CONSTRUCTION PROCESS OF FRAUD PREVENTION: The Absolutes of the Organization s Anti-Fraud Program Presented for the 2017 TACA On the Road Area Training Presented by STEVE

Speaker: Steve Dawson 7/13/2017 THE CONSTRUCTION PROCESS OF FRAUD PREVENTION: The Absolutes of the Organization s Anti-Fraud Program Presented for the 2017 TACA On the Road Area Training Presented by STEVE

2/20/15. Trevor Stewart, CPA Director of Business Services Source documentation includes CCIA and FCMAT

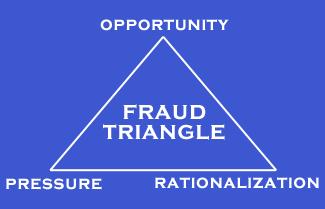

2/20/15 Trevor Stewart, CPA Director of Business Services Source documentation includes CCIA and FCMAT The Fraud Triangle factors that influence the commission of fraud The Fraud Tree occupational fraud

2/20/15 Trevor Stewart, CPA Director of Business Services Source documentation includes CCIA and FCMAT The Fraud Triangle factors that influence the commission of fraud The Fraud Tree occupational fraud

Investigation into Cash Irregularities Within a City Facility

Investigation into Cash Irregularities Within a City Facility May 13, 2004 Office of the City Auditor This page is intentionally blank. Office of the City Auditor Investigation into Cash Irregularities

Investigation into Cash Irregularities Within a City Facility May 13, 2004 Office of the City Auditor This page is intentionally blank. Office of the City Auditor Investigation into Cash Irregularities

Embezzlement & Fraud How You Can Protect Yourself. Pam Newman, CMA,CFM, MBA

Embezzlement & Fraud How You Can Protect Yourself Pam Newman, CMA,CFM, MBA Pam Newman BS and MBA from University of Nebraska CMA Certified Management Accountant CFM Certified Financial Manager President

Embezzlement & Fraud How You Can Protect Yourself Pam Newman, CMA,CFM, MBA Pam Newman BS and MBA from University of Nebraska CMA Certified Management Accountant CFM Certified Financial Manager President

Fraud Prevention, Detection and Control. Elizabeth Coles, CPA Aldrich CPAs + Advisors LLP

Fraud Prevention, Detection and Control Elizabeth Coles, CPA Aldrich CPAs + Advisors LLP 1 Agenda Who and Why? Fraud Schemes and Risks Fraud Prevention what can you do? 3 Who Commits Fraud? Long time,

Fraud Prevention, Detection and Control Elizabeth Coles, CPA Aldrich CPAs + Advisors LLP 1 Agenda Who and Why? Fraud Schemes and Risks Fraud Prevention what can you do? 3 Who Commits Fraud? Long time,

Data Analytics: Where Do I Start?

Data Analytics: Where Do I Start? Ryan Merryman, CPA, CFF, CITP, CFE David Heneke, CPA, CISA Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC-registered

Data Analytics: Where Do I Start? Ryan Merryman, CPA, CFF, CITP, CFE David Heneke, CPA, CISA Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC-registered

FRAUD AND PROFESSIONAL ETHICS IN HIGHER EDUCATION

FRAUD AND PROFESSIONAL ETHICS IN HIGHER EDUCATION Brent Stevens, CPA, CGMA Partner in Charge Higher Education Services Group RubinBrown WHY YOU ARE HERE TODAY? *Image courtesy of Association of Certified

FRAUD AND PROFESSIONAL ETHICS IN HIGHER EDUCATION Brent Stevens, CPA, CGMA Partner in Charge Higher Education Services Group RubinBrown WHY YOU ARE HERE TODAY? *Image courtesy of Association of Certified

Changing Your Paradigm on Risks and Controls

Changing Your Paradigm on Risks and Controls Stacey Walker, CPA, CFE Director, Internal Auditing Office of Audit, Compliance & Privacy October 31, 2018 OBJECTIVE: PARADIGM CHANGE Paradigm A set of assumptions,

Changing Your Paradigm on Risks and Controls Stacey Walker, CPA, CFE Director, Internal Auditing Office of Audit, Compliance & Privacy October 31, 2018 OBJECTIVE: PARADIGM CHANGE Paradigm A set of assumptions,

MMA Trade Show. Conduc1ng an Inves1ga1ve Audit January 21, Presented by: John Sullivan, CFE Melanson Heath

MMA Trade Show Conduc1ng an Inves1ga1ve Audit January 21, 2017 Presented by: John Sullivan, CFE Melanson Heath Associa1on of Cer1fied Fraud Examiners 2016 Global Fraud Study Figure 1. Sta1s1cs (ACFE, 2016).

MMA Trade Show Conduc1ng an Inves1ga1ve Audit January 21, 2017 Presented by: John Sullivan, CFE Melanson Heath Associa1on of Cer1fied Fraud Examiners 2016 Global Fraud Study Figure 1. Sta1s1cs (ACFE, 2016).

Not-For-Profit Finance Forum 2018 Xero and Internal Controls

Not-For-Profit Finance Forum 2018 Xero and Internal Controls Clyde Young and Courtney West Who we are? Australia and New Zealand network of Accounting Firms The sixth largest grouping of Accounting Firms

Not-For-Profit Finance Forum 2018 Xero and Internal Controls Clyde Young and Courtney West Who we are? Australia and New Zealand network of Accounting Firms The sixth largest grouping of Accounting Firms

Alyssa G. Martin, CPA Brandon Tanous, CIA, Using the COSO CFE, CGAP, CRMA Framework to Develop a Strong and Preventive Control Environment

Speakers Using the COSO Framework to Develop a Strong and Preventive Control Environment Weaver Public Sector CPE Event Alyssa G. Martin, CPA Dallas Executive Partner, Advisory Services 25+ years of public

Speakers Using the COSO Framework to Develop a Strong and Preventive Control Environment Weaver Public Sector CPE Event Alyssa G. Martin, CPA Dallas Executive Partner, Advisory Services 25+ years of public

The most commonly applied model for designing and auditing internal

Fair Value Accounting Fraud: New Global Risks and Detection Techniques By Gerard M. Zack Copyright 2009 by Gerard M. Zack Appendix C Internal Controls over Fair Value Accounting Applications The most commonly

Fair Value Accounting Fraud: New Global Risks and Detection Techniques By Gerard M. Zack Copyright 2009 by Gerard M. Zack Appendix C Internal Controls over Fair Value Accounting Applications The most commonly

INTERNAL AUDIT Fraud Investigation Process Campus Administrative Training Series April 24, 2017

INTERNAL AUDIT Fraud Investigation Process Campus Administrative Training Series April 24, 2017 Stewart Cobine, CPA AVP & Chief Audit Officer Maggie Harrell, CFE Senior Investigative Auditor FOCUS OF SESSION

INTERNAL AUDIT Fraud Investigation Process Campus Administrative Training Series April 24, 2017 Stewart Cobine, CPA AVP & Chief Audit Officer Maggie Harrell, CFE Senior Investigative Auditor FOCUS OF SESSION

Fraud Detection and Prevention

Fraud Detection and Prevention Presented by: Louise Hanson, Moss Adams LLP Emily Ogden, Moss Adams LLP April 24, 2014 1 DISCLOSURE STATEMENT The material appearing in this presentation is for informational

Fraud Detection and Prevention Presented by: Louise Hanson, Moss Adams LLP Emily Ogden, Moss Adams LLP April 24, 2014 1 DISCLOSURE STATEMENT The material appearing in this presentation is for informational

What Are Your Auditors Doing? Presented by Carrie Kennedy, Partner Travis Smith, Partner Moss Adams LLP

What Are Your Auditors Doing? Presented by Carrie Kennedy, Partner Travis Smith, Partner Moss Adams LLP 1 MOSS ADAMS AT A GLANCE Full service national CPA firm providing assurance, tax, and consulting

What Are Your Auditors Doing? Presented by Carrie Kennedy, Partner Travis Smith, Partner Moss Adams LLP 1 MOSS ADAMS AT A GLANCE Full service national CPA firm providing assurance, tax, and consulting

How to Prevent Financial Fraud at Your Church VONNA LAUE

How to Prevent Financial Fraud at Your Church VONNA LAUE Agenda Why churches fall victim to fraud Financial control best practices Recognize and respond to financial fraud Why Churches Fall Victim to Fraud

How to Prevent Financial Fraud at Your Church VONNA LAUE Agenda Why churches fall victim to fraud Financial control best practices Recognize and respond to financial fraud Why Churches Fall Victim to Fraud

Fraud and Ethics Compliance

1 Fraud and Ethics Compliance United ISD Internal Audit Department Marta G. Stahl, CPA School Year 2014-2015 School Year 2013-2014 2 Purpose This presentation is intended to familiarize you with State

1 Fraud and Ethics Compliance United ISD Internal Audit Department Marta G. Stahl, CPA School Year 2014-2015 School Year 2013-2014 2 Purpose This presentation is intended to familiarize you with State

Diving into the 2013 COSO Framework. Presented by: Ronald A. Conrad

Diving into the 2013 COSO Framework Presented by: Ronald A. Conrad 2 Objectives Obtain an understanding of why the COSO Framework has been updated Understand how the framework has changed Identify the

Diving into the 2013 COSO Framework Presented by: Ronald A. Conrad 2 Objectives Obtain an understanding of why the COSO Framework has been updated Understand how the framework has changed Identify the

Whistleblower Policy

Whistleblower Policy Table of Contents POLICY OVERVIEW... 1 STATEMENT OF PURPOSE... 1 SCOPE OF POLICY... 1 COMPLAINT HANDLING PROCESS... 2 DISCLOSURE OF MISCONDUCT... 2 CONFIDENTIALITY... 2 SAFEGUARDS

Whistleblower Policy Table of Contents POLICY OVERVIEW... 1 STATEMENT OF PURPOSE... 1 SCOPE OF POLICY... 1 COMPLAINT HANDLING PROCESS... 2 DISCLOSURE OF MISCONDUCT... 2 CONFIDENTIALITY... 2 SAFEGUARDS

Internal Control Fundamentals and Introduction to Fraud - Spring Brenda M. Shannon, CPA, CIA Chief Audit Executive New Mexico State University

Internal Control Fundamentals and Introduction to Fraud - Spring 2010 - Brenda M. Shannon, CPA, CIA Chief Audit Executive New Mexico State University Objectives To give participants a high-level overview

Internal Control Fundamentals and Introduction to Fraud - Spring 2010 - Brenda M. Shannon, CPA, CIA Chief Audit Executive New Mexico State University Objectives To give participants a high-level overview

Fraud Detection and Prevention

Fraud Detection and Prevention Washington Association of School Business Officials May 7, 2015 Sherrie Ard, CPA, CFE Local Government Performance Center Financial Management Specialist FRAUD 2 Overview

Fraud Detection and Prevention Washington Association of School Business Officials May 7, 2015 Sherrie Ard, CPA, CFE Local Government Performance Center Financial Management Specialist FRAUD 2 Overview

Accounting 408 Exam 2, Chapters 3, 4, 5, 6, E, F

Accounting 408 Exam 2, Chapters 3, 4, 5, 6, E, F Summer 2017 Name Row Multiple Choice Questions. (2 points each, 100 points total) Read each question carefully and indicate the one best answer to each

Accounting 408 Exam 2, Chapters 3, 4, 5, 6, E, F Summer 2017 Name Row Multiple Choice Questions. (2 points each, 100 points total) Read each question carefully and indicate the one best answer to each

Community College Audit and Compliance Workshop. VAVRINEK, TRINE, DAY & CO., LLP April 15, 2014

Community College Audit and Compliance Workshop VAVRINEK, TRINE, DAY & CO., LLP April 15, 2014 Audit Responsibilities Overview An annual financial statement and compliance audit of California Community

Community College Audit and Compliance Workshop VAVRINEK, TRINE, DAY & CO., LLP April 15, 2014 Audit Responsibilities Overview An annual financial statement and compliance audit of California Community

Developing an Integrated Anti-Fraud, Compliance, and Ethics Program

Developing an Integrated Anti-Fraud, Compliance, and Ethics Program Introduction Eric Feldman, CFE, CIG Affiliated Monitors, Inc. 2018 Association of Certified Fraud Examiners, Inc. CPE Information 2018

Developing an Integrated Anti-Fraud, Compliance, and Ethics Program Introduction Eric Feldman, CFE, CIG Affiliated Monitors, Inc. 2018 Association of Certified Fraud Examiners, Inc. CPE Information 2018

Internal Controls. They Are Everyone s Business. Valdosta State University Office of Internal Audits June 2016

Internal Controls They Are Everyone s Business Valdosta State University Office of Internal Audits June 2016 1 Presentation Overview Understand Internal Controls Identify Control Weaknesses Fraud Best

Internal Controls They Are Everyone s Business Valdosta State University Office of Internal Audits June 2016 1 Presentation Overview Understand Internal Controls Identify Control Weaknesses Fraud Best

12/6/2016. Who Is Booth Management Consulting? Key Team Members. What is an Agreed-Upon Procedures Engagement?

Overview of Financial & Administrative Review Agenda U.S. Department of Housing and Urban Development Office of Housing Counseling Overview of Financial & Administrative Reviews December 6, 2016 2:00 PM

Overview of Financial & Administrative Review Agenda U.S. Department of Housing and Urban Development Office of Housing Counseling Overview of Financial & Administrative Reviews December 6, 2016 2:00 PM

TACKLING HEALTH CARE FRAUD, WASTE, AND ABUSE WHERE DO YOU START?

TACKLING HEALTH CARE FRAUD, WASTE, AND ABUSE WHERE DO YOU START? William Gedman CPA, CIA Vice President Quality Audit, Fraud & Abuse UPMC Insurance Services Division Pittsburgh, PA Session Outline Elements

TACKLING HEALTH CARE FRAUD, WASTE, AND ABUSE WHERE DO YOU START? William Gedman CPA, CIA Vice President Quality Audit, Fraud & Abuse UPMC Insurance Services Division Pittsburgh, PA Session Outline Elements

INTERNAL CONTROLS AND FRAUD DETECTION. Jill Reyes, Director Laura Manlove, Manager

INTERNAL CONTROLS AND FRAUD DETECTION Jill Reyes, Director Laura Manlove, Manager Today s presenters Jill Reyes Director, Risk Advisory Services RSM US LLP Melbourne, Florida jill.reyes@rsmus.com +1 321

INTERNAL CONTROLS AND FRAUD DETECTION Jill Reyes, Director Laura Manlove, Manager Today s presenters Jill Reyes Director, Risk Advisory Services RSM US LLP Melbourne, Florida jill.reyes@rsmus.com +1 321

PREVENTING FRAUD BEFORE IT IS TOO LATE Presented to LeadingAge Michigan Annual Conference and Trade Show May 19, 2015

Arlen S. Lasinsky Frost, Ruttenberg & Rothblatt, P.C. alasinsky@frrcpas.com 847/282-6352 Phone and Fax www.frrcpas.com PREVENTING FRAUD BEFORE IT IS TOO LATE Presented to LeadingAge Michigan Annual Conference

Arlen S. Lasinsky Frost, Ruttenberg & Rothblatt, P.C. alasinsky@frrcpas.com 847/282-6352 Phone and Fax www.frrcpas.com PREVENTING FRAUD BEFORE IT IS TOO LATE Presented to LeadingAge Michigan Annual Conference

Fraud in Today s Economic Environment

Fraud in Today s Economic Environment Presented by: Victor Hieken, CPA, CFE Jeffrey Streif, CPA, CFE, CISA, QSA Bill Slaughter, CPA Economic Uncertainty Unemployment What is Fraud? A misrepresentation

Fraud in Today s Economic Environment Presented by: Victor Hieken, CPA, CFE Jeffrey Streif, CPA, CFE, CISA, QSA Bill Slaughter, CPA Economic Uncertainty Unemployment What is Fraud? A misrepresentation

Fraud and the Internal Audit role Course Outline

Fraud and the Internal Audit role Course Outline Day 1 Fraud risks Background Fraud explained: definitions Fraud statistics Why is fraud such a serious issue? The cost of fraud Who commits fraud? Trends

Fraud and the Internal Audit role Course Outline Day 1 Fraud risks Background Fraud explained: definitions Fraud statistics Why is fraud such a serious issue? The cost of fraud Who commits fraud? Trends

Company owners and managers may hesitate to admit it, but fraud could be taking

CREDIT & FINANCE Do You Trust Your Employees? Occupational fraud can cost companies big money, but is preventable BY DAN ALAIMO Key Elements Occupational fraud is a common and costly part of the workplace,

CREDIT & FINANCE Do You Trust Your Employees? Occupational fraud can cost companies big money, but is preventable BY DAN ALAIMO Key Elements Occupational fraud is a common and costly part of the workplace,

Internal Control Program

DFA Conversations Office of the University Controller Internal Control Program November 20, 2017 Introduction Bill Sibert, University Controller Erica Jessup, Senior Financial Analyst Phil Turke, Payroll

DFA Conversations Office of the University Controller Internal Control Program November 20, 2017 Introduction Bill Sibert, University Controller Erica Jessup, Senior Financial Analyst Phil Turke, Payroll

This Questionnaire/Guide is intended to assist you in decision making, as well as in day-to-day operations. Best Regards,

In an effort to disseminate information and assure that we are in compliance with guidelines caused by the Sarbanes Oxley Act that proper internal controls are being adhered to, we have developed some

In an effort to disseminate information and assure that we are in compliance with guidelines caused by the Sarbanes Oxley Act that proper internal controls are being adhered to, we have developed some

Forensic Accounting. The What, Why and How Fraud Detection and Prevention Ulrike Hugl Nov 16 17_2017

Forensic Accounting. The What, Why and How Fraud Detection and Prevention Ulrike Hugl Nov 16 17_2017 2017 ulrike.hugl@uibk.ac.at 1 Background of forensic accounting FA or Forensic Auditing, Forensic Investigation

Forensic Accounting. The What, Why and How Fraud Detection and Prevention Ulrike Hugl Nov 16 17_2017 2017 ulrike.hugl@uibk.ac.at 1 Background of forensic accounting FA or Forensic Auditing, Forensic Investigation

Office of the Utah Legislative Auditor General. Fraud Prevention. Utah Government Finance Officers Association. Spring 2017 Conference

Office of the Utah Legislative Auditor General Fraud Prevention Utah Government Finance Officers Association Spring 2017 Conference Utah Legislative Auditor General Constitutional Charge and Authority

Office of the Utah Legislative Auditor General Fraud Prevention Utah Government Finance Officers Association Spring 2017 Conference Utah Legislative Auditor General Constitutional Charge and Authority

AUDIT RISK ASSESSMENT AND RESPONSES TO ASSESSED RISK BY Geoffrey Byamugisha Partner, Ernst & Young. Lessons on Audit Risk. Responding to fraud risk

AUDIT RISK ASSESSMENT AND RESPONSES TO ASSESSED RISK BY Geoffrey Byamugisha Partner, Ernst & Young ICPAU Page 1 COURSE CONTENT Lessons on Audit Risk Identification of audit risk and audit risk assessment

AUDIT RISK ASSESSMENT AND RESPONSES TO ASSESSED RISK BY Geoffrey Byamugisha Partner, Ernst & Young ICPAU Page 1 COURSE CONTENT Lessons on Audit Risk Identification of audit risk and audit risk assessment

Internal Audit Policy and Procedures Internal Audit Charter

Mission Statement Internal Audit Policy and Procedures Internal Audit Charter The mission of the Internal Audit Department is to provide independent and objective reviews and assessments of the business

Mission Statement Internal Audit Policy and Procedures Internal Audit Charter The mission of the Internal Audit Department is to provide independent and objective reviews and assessments of the business

Nonprofit Association of the Midlands. August 26, 2014

Nonprofit Association of the Midlands August 26, 2014 Nonprofit Financial Management General Practices Capable bookkeeper Accrual accounting GAAP Monthly financial statements Sarbanes Oxley: Financial

Nonprofit Association of the Midlands August 26, 2014 Nonprofit Financial Management General Practices Capable bookkeeper Accrual accounting GAAP Monthly financial statements Sarbanes Oxley: Financial

OVERVIEW. Common Personality Traits of Fraudsters. Common Sources of Pressure. Changes in Behavior

Red Flags of Fraud OVERVIEW Red Flags of Fraud are warning signs that may indicate a higher fraud risk. They are NOT evidence that fraud is actually occurring. Many employees demonstrate one or more of

Red Flags of Fraud OVERVIEW Red Flags of Fraud are warning signs that may indicate a higher fraud risk. They are NOT evidence that fraud is actually occurring. Many employees demonstrate one or more of

Why Reporting Hotlines Are Considered a Best Practice

WhitePaper Why Reporting Hotlines Are Considered a Best Practice 11/22/17 Table of Contents Abstract.. 2 The Call for Higher Ethical Standards.....4 Specific Ethical Concerns...5 Best Practices and Reporting

WhitePaper Why Reporting Hotlines Are Considered a Best Practice 11/22/17 Table of Contents Abstract.. 2 The Call for Higher Ethical Standards.....4 Specific Ethical Concerns...5 Best Practices and Reporting

Internal Controls and the Internal Auditor. Presented By: Richard Kudlik, CPA

Internal Controls and the Internal Auditor Presented By: Richard Kudlik, CPA Interrelated Components Control Environment Risk Assessment Control Activities Information and Communication Monitoring What

Internal Controls and the Internal Auditor Presented By: Richard Kudlik, CPA Interrelated Components Control Environment Risk Assessment Control Activities Information and Communication Monitoring What

Ten Payment Fraud Protections

Ten Payment Fraud Protections 1. Payee Positive Pay a. Provided by banks b. Banks match check serial numbers and dollar amounts against a company provided list of checks issued and only pays those checks

Ten Payment Fraud Protections 1. Payee Positive Pay a. Provided by banks b. Banks match check serial numbers and dollar amounts against a company provided list of checks issued and only pays those checks

Standards for Internal Control in New York State Government 2016 Update

Standards for Internal Control in New York State Government 2016 Update Presented to the New York State Internal Control Association John F. Buyce Audit Director April 28, 2016 1 Last Revised in 2007 A

Standards for Internal Control in New York State Government 2016 Update Presented to the New York State Internal Control Association John F. Buyce Audit Director April 28, 2016 1 Last Revised in 2007 A

Fraud in Construction Companies: Lessons From the Trenches

Fraud in Construction Companies: Lessons From the Trenches Presented by Angela Morelock, CPA, CFE, CFF, ABV, Certified Forensic Accountant www.bkdforensics.com Twitter: @AngelaMorelock Cost of Fraud &

Fraud in Construction Companies: Lessons From the Trenches Presented by Angela Morelock, CPA, CFE, CFF, ABV, Certified Forensic Accountant www.bkdforensics.com Twitter: @AngelaMorelock Cost of Fraud &

Fraud Risk Management

Fraud Risk Management Using Automated Continuous Monitoring Tools 2017 Association of Certified Fraud Examiners, Inc. Discussion Questions 1. Does your organization use continuous and/or automated monitoring

Fraud Risk Management Using Automated Continuous Monitoring Tools 2017 Association of Certified Fraud Examiners, Inc. Discussion Questions 1. Does your organization use continuous and/or automated monitoring

INTEGRATING FORENSIC INVESTIGATION TECHNIQUES INTO INTERNAL AUDITING

INTEGRATING FORENSIC INVESTIGATION TECHNIQUES INTO INTERNAL AUDITING The internal auditors roles in combating fraud are becoming more profound within an organization. Internal auditors may assume a variety

INTEGRATING FORENSIC INVESTIGATION TECHNIQUES INTO INTERNAL AUDITING The internal auditors roles in combating fraud are becoming more profound within an organization. Internal auditors may assume a variety

WHISTLE BLOWER (EMPLOYEE PROTECTION) POLICY

POLICY") W A S H I N G T O N C O L L E G E P O L I C I E S WHISTLE BLOWER (EMPLOYEE PROTECTION) POLICY Washington College strives to operate in an ethical, honest and lawful manner and expects its employees, students,

W A S H I N G T O N C O L L E G E P O L I C I E S WHISTLE BLOWER (EMPLOYEE PROTECTION) POLICY Washington College strives to operate in an ethical, honest and lawful manner and expects its employees, students,

Internal Control: The Human Risk Factor

Internal Control: The Human Risk Factor 1 E U D O R I E N T A T I O N F O R N E W U N I O N A N D C O N F E R E N C E O F F I C E R S A U G U S T 2 8 S E P T E M B E R 1, 2 0 1 7 Ann Gibson, PhD, CPA Andrews

Internal Control: The Human Risk Factor 1 E U D O R I E N T A T I O N F O R N E W U N I O N A N D C O N F E R E N C E O F F I C E R S A U G U S T 2 8 S E P T E M B E R 1, 2 0 1 7 Ann Gibson, PhD, CPA Andrews

SUSTAINING AN ETHICAL CULTURE: IT S NOT ALWAYS BLACK AND WHITE

SUSTAINING AN ETHICAL CULTURE: IT S NOT ALWAYS BLACK AND WHITE Most companies want to do the right thing when it comes to ethics. It seems that it should be as easy as telling everyone in the organization

SUSTAINING AN ETHICAL CULTURE: IT S NOT ALWAYS BLACK AND WHITE Most companies want to do the right thing when it comes to ethics. It seems that it should be as easy as telling everyone in the organization

Internal Control: The Human Risk Factor

Internal Control: The Human Risk Factor 1 P R E S E N T A T I O N F O R T H E S P D N E W C F O O R I E N T A T I O N P R O G R A M M A Y 1 5, 2 0 1 7 Ann Gibson, PhD, CPA Andrews University Purposes of

Internal Control: The Human Risk Factor 1 P R E S E N T A T I O N F O R T H E S P D N E W C F O O R I E N T A T I O N P R O G R A M M A Y 1 5, 2 0 1 7 Ann Gibson, PhD, CPA Andrews University Purposes of

Detecting & Preventing Procurement Fraud Using Data Analysis to Detect Improper Disbursements

Detecting & Preventing Procurement Fraud Using Data Analysis to Detect Improper Disbursements April 29, 2014 2:00 3:00pm ET Andrew Simpson, MBA Chief Operating Officer, CaseWare Analytics Paul Soos, CFE,

Detecting & Preventing Procurement Fraud Using Data Analysis to Detect Improper Disbursements April 29, 2014 2:00 3:00pm ET Andrew Simpson, MBA Chief Operating Officer, CaseWare Analytics Paul Soos, CFE,