Cost & Management Accounting Bachelors of Business (Specialized in Finance) Study Notes & Tutorial Questions Chapter 3: Labor Costing

|

|

|

- Myron Gregory

- 6 years ago

- Views:

Transcription

Study Notes & Tutorial Questions Chapter 3: Labor Costing")

1 Cost & Management Accounting Bachelors of Business (Specialized in Finance) Study Notes & Tutorial Questions Chapter 3: Labor Costing 1

2 INTRODUCTION Labour is the second element of cost after materials. Labour cost represents the remuneration for employees effort in the production process. Controlling labour cost involves complex procedures since it involves human beings and controlling human behaviour is complex. This chapter will explain the process for determining and controlling labour cost. Labour as a factor of production. Factors of production are resources or inputs that are used to facilitate the production of goods and services. Labour is the effort of employees required to transform raw material into finished goods and services. Labour takes the form of employee knowledge, expertise and experience. Without these skills, production cannot take place. Labour encompasses all categories of the workforce of an organisation spanning from top management down through the hierarchy of responsibility to the grass root workforce. From the perspective of cost accounting, labour cost determination and control is very important because it has huge cost implications for the organization. Labour cost consists of: recruitment cost, cost of training and staff development, wages and salaries, employee bonuses, overtime premium, group incentives etc. if these cost are not properly controlled, total cost may not be minimized. Labour recruitment process cost Labour recruitment refers to the process of engaging employees in the organization for their services. Depending on the policy of the organisation, the mode of recruitment is determined either internally or externally. The following steps are usually undertaken: A job analysis is done to determine the role, responsibilities, and person specification required. Internally- an advert is placed on company notice board and a search conducted. Externally, consideration is given to various search options like labour office, newspapers, outsourcing, job fairs, executive searches and so on. Applicants respond to companies invitation and the company proceeds to shortlist potential applicants. 2

3 Selection Process Interviews are conducted- whether structured or unstructured. A structured interview should have an agreed format with questions ordered to evaluate applicants. The right candidate is selected using pre-determined criteria. Labour Induction and Placement This is a programme carried out to ensure that new employees are as soon as possible integrated into the culture of the organisation by becoming familiar with the values and norms of the organisation. Employees are then placed according to their experiences and competencies. Training may then be provided to ensure enhanced performance. Training may involve a consideration of the following: Training needs analysis Assess training budget. Prioritize what is most critical. Define skills, knowledge abilities and objectives desired after the training. Consider the training method. Evaluate the training Labour recruitment cost as well as other labour cost therefore includes the following: Advertising cost Interviewing expenses Training expenses Cost of wastages of new employees Wages and salaries of employees Overtime premiums Employee bonuses Retirement payments etc. Labour Timing and Assessment. After employees have been engaged and they begin to work, there is the need to time them as they work so as to assess their performance and also to make it possible to cost work that they 3

4 do. Various organisations use different methods to time their employees. Examples of methods used include the following: The use of the Attendance Register The use of Clock Cards The use of Attendance Boards The use of Job Sheets and Job Books etc The above records will then be used as evidence of: The number of hours worked by employees The time spent by each employee on any Job The number of hours during which each employee was idle etc. These will then form the basis for computing the wages of employees. Labour Behaviour and Control Labour is about human beings and so it is relatively difficult to control human behaviour. However, it is important that steps are taken by the organisation to control human behaviour. Some of the mechanisms for labour control are: Time keeping- employees are required to record the time he /she reported for work and the time he/she departed from the work place. The employee is also required to record the time spent on each job or work that he/she does. Monitoring and supervision- employees are monitored and supervised by senior officers who observe the work attitude of the employee. Evaluation- the work of the employee is evaluated by his peers, clients and by management. This motivates staff to exhibit positive work attitude. Reward schemes- rewarding effective employees through bonuses and incentives drives employees to work hard. Job evaluation This is a technique which seeks to show the relative worth of each job so as to rank it against other jobs and ultimately establish the appropriate weight of remuneration to attach to the job. Job evaluation analyses the content of each job using yardsticks such as degree of responsibility, decisions involved, training and experience required, working conditions etc, awarding points for each yardstick. 4

5 Merit rating Whilst job evaluation assesses the worth of the job, merit rating measures the jobholder s performance so as to determine whether the employee should be promoted, demoted or given a special award. It also uses its own yardsticks on the performance and attributes of the employee like accuracy, initiative, level of responsiveness, willingness etc. Most industries employ rating techniques at the end of each year in order to determine the progress of each employee within the salary structure. Work study This is a system of increasing or maximizing the productivity of an operating unit by reorganizing the work of that unit. Work study is sub-divided into two major methods namely methods study and work measurement. Method study This is the recording and critical examination of existing methods of doing work and comparing same with proposed methods with a view to coming up with easier methods which would be more effective and cheaper on the long run. Work measurement As the name suggests, work measurement seeks to measure the time required for a qualified worker to complete a specific assignment at a specified level of performance. 5

6 Labour Cost Computation There are two basic methods of remunerating labour; time based remuneration and output based remuneration. Time Rate Methods of Remuneration The amount earned by the employee is based on the number of hours spent at his place of work and not on the quantity of work produced. The Gross wage is calculated as Hours Worked Rate per hour. However when overtime is worked, the payment to the employee will also include premium on the overtime hours. Advantages of Time rate methods of remuneration are: It is simple to operate and easy to understand The quality of work produced tends to be higher since the worker is not in a rush to complete a job in order to maximize his earnings. Disadvantages of Time rate methods of remuneration are: There is no financial incentive to produce more than a minimum amount. In fact, there is often an incentive to produce as little as possible so that the worker can increase his wage. To monitor and check idleness the employer will be obliged to incur supervision cost. The method is often unfair because lazy workers and hard workers are paid the same rates. Piece rate methods of remuneration Under this method, the amount earned by the employee is based on the number of units produced. Piece rates can be examined under three headings, namely: 1. Straight Piece Rate 2. Differential Piece Rate 3. Piece Rate with guaranteed time Rate 6

7 Straight Piece Rate Under straight piece rates the payment to the employee is computed thus: No. of units produced Rate per unit. The worker receives a fixed rate for each unit produced which does not depend on the time taken to produce it. Earnings therefore depend on the volume of the worker s output. Advantages 1. Effort is rewarded and in consequence, the employee is given the incentive to produce more 2. Because employees are self-motivated, less supervision is required. 3. The employer benefits from a reduction in the overhead cost per unit of production. Disadvantages 1. There is a danger that quality will be sacrificed and in order to avoid such a situation the employer would spend more on inspection and quality control 2. Piece workers, after earning certain remuneration during a week, might be satisfied and slacken their pace, arrive late or absent themselves. Plant is therefore left idle and capacity is under-utilised. 3. A considerable degree of time is involved in setting standard times and as these are subject to the agreement of trade union representatives, further time is often spent in detail negotiation before piece rates are established. 4. If an error is made and piece rates are set too high, it is difficult subsequently to reduce them. This could prove to be extremely costly. Piece Rate with Guaranteed Day Rate It is a system adopted to compensate employees on account of low production, leading to earnings under piece rate being below the normal day rate remuneration. If an employee s earnings according to the piece work are less than the normal Day Rate, he is paid the day rate instead of the Piece Rate. 7

8 Differential Piece Rate Under this scheme the piece work rate changes at different levels of efficiency or production. The object of this is to provide a strong incentive to reach the maximum rate of production. Premium Bonus Schemes Bonus schemes are intended to reward employees for their efficiency in saving cost for the organisation through the saving of time. These are therefore schemes for sharing extra profits with employees. Conceptually, bonus can only be awarded where there has been cost savings or improved performance that leads the organisation to exceed its profit target. To be able to compute bonuses, we must first appreciate the following concepts: Time allowed: This refers to the expected time to be spent in doing some piece of work e.g. if time set for one unit is 5 hours, then 100 units shall be 500 hours. Time allowed may therefore not be the same as the hours worked. Time taken: This the number of hours actually used in performing a piece of work. Time saved: It is the difference between time allowed and hours worked, when time allowed is greater than hours worked. Premium bonus: This is paid when time has been saved; the magnitude of the bonus therefore depends upon the time saved. Types of Premium Bonus Schemes These include the following: (i) Halsey Bonus Scheme (ii) Halsey Weir Bonus Scheme (iii) Rowan Bonus Scheme Halsey Scheme According to this scheme, the time saved should be apportioned equally between the employer and the employee. 8

9 Bonus = ½ Time Saved Day Rate Note: Time allowed Time Taken = Time Saved Halsey Weir Scheme Under this scheme the proportion is 2:1in favour of the employer. Thus the employee gets only a third of time saved at the rate per hour. Bonus = ⅓ Time Saved Day rate Rowan Scheme Under this system, the bonus award to the employee is the proportion between time taken and Time allowed of the It therefore follows that if the employee saves more time, he gets a greater bonus. Many business organisations determine their bonuses through negotiation with employee groups. The factors that influence the size of the bonus include the following: Time saved by employees Cost saved by employees Improved productivity The amount of super profits made by the business organisation The achievements of other budgetary targets etc. Over Time Remuneration Schemes Over time is the time spent beyond the normal working hours or days. Overtime wage rates are expressed as time plus a fraction or in multiples of time, e.g. a. Time and one half b. Time and one third c. Double time 9

10 d. Time and one fifth etc. Meaning of Time Time refers to the basic rate e.g. if the normal rate of pay is MVR 500 an hour, then the time is MVR 500. Meaning of Additional Rate The additional rate is called the overtime premium and whatever it is the amount involved is arrived at by multiplying the description by the basic rate e.g. The overtime rate is time and one half, the basic rate is MVR 500. The premium shall be MVR 250 = ½ MVR 500. Overtime Premium It is the portion of the overtime pay over and above the basic rate of pay. Basically, overtime premium is treated as indirect wages. The only time it is treated as direct wages is when the overtime is worked according to the customer s request to complete his order within a specified period. Group incentive schemes These are bonuses awarded to a team of employees rather than individual employees. The incentives are enjoyed by every member of the team based on an agreed formula of sharing. Advantages of Group Incentive Schemes It enhances team spirit among employees and organizational cohesiveness Quality of output is not unduly compromised Compared to individual incentive schemes, it is relatively easy and less expensive to administer It avoids unhealthy competitive rivalry among employees Disadvantages of Group Incentive Schemes Lazy team members are rewarded the as hard working group members. This does not provide motivation for individual hard work. Individual incentive Scheme These are bonus schemes that reward individual employees for their efficiencies. Advantages of Individual Incentive Schemes Individual employees are motivated to be more and more efficient and productive 10

11 It may generate competitive spirit among employees Employee morale is raised since individual effort is rewarded Ultimately, both the employee and the business organisation obtain enhanced benefits. Disadvantages of Individual incentive schemes o Employees may compromise on quality in an effort to increase their bonus earnings o Excessive competition can bring about unhealthy rivalry o The determination of standard performance levels for the purpose of determining efficiency levels can conflict in the organisation o It is relatively more difficult and expensive to operate an individual incentive scheme compared to a group incentive schemes. Direct and indirect cost of labour As already discussed, labour cost is either direct or indirect. The direct labour cost is the labour cost incurred on employees who are engaged in directly transforming the raw materials into finished goods. It must be noted that, is only the basic wages paid to direct workers that constitute direct labour cost. Policy related cost incurred on direct workers is not direct labour but rather indirect labour. Examples of these policy related costs include: workmen compensation premium paid to insurance companies employer s social security fund contribution bonuses paid to employees overtime premium paid to employees where the overtime is worked regularly as company policy etc. Wages cost incurred on indirect workers is indirect wages. Labour Cost Minimization Techniques Involved in minimizing labour cost. Some of the techniques include the following: Effective labour monitoring and control Reduce labour turnover Eliminate or reduce labour related fraud 11

12 Labour Turnover This is a term which signifies the extent to which employees leave an organisation. It can be measured by using the following formulae: Number of employees leaving To obtain the maximum benefit from the Calculation, the rate of labour turnover should be compared with rate for previous periods and if available, the rate for other businesses in the area and in the industry as a whole. If the number of leavers is high relative to the total number of employees, a high ratio will emerge. An increase in the number of employees leaving or a reduction in the total workforce will cause an increase in the rate compared with previous periods. The effect of a high rate is reflected in loss of output, lowering of morale and higher cost. Loss of output occurs because of: (a) The gap between the person leaving and his replacement; (b) The length of time taken to train a new employee to the level of efficiency of the previous employee; (c) The reduced effort given by an employee during the days or weeks immediately prior to the date of departure. 12

13 Cost of Labour Turn Over In addition to the increase in the cost per unit from reduced production and low morale, the following costs are likely to be higher when the rate of labour turnover is on the increase: (i) (ii) (iii) (iv) (v) (vi) Advertising for personnel and interviewing expenses Re-imbursement of removal and settling in expenses removal of furniture to new house and subsistence allowance between date of commencement and date of moving. Training, including the new employee s wages during the training period, the wages and salaries of instructors, materials used in the training process. Scrap and defective work during initial stages Machine break-down Pension scheme administration etc. Causes of Labour Turnover Although Labour turnover cannot be eliminated completely, the problem can be tackled by an understanding of the events and circumstances by which it is caused. Why do people leave? The following are some of the possible reasons: (i) (ii) (iii) (iv) (v) Dissatisfaction with the job, wages, hours of work or working conditions; Discontent due to the relationship with the employee s Supervisors and or Colleagues; Lack of promotion opportunities; Personal matters e.g. ill health, marriage, pregnancy, moving to a new area. Sometimes employees are discharged due to redundancy, incompetence, lateness, and absenteeism and for disciplinary reasons. Reduction in the Labour Turnover Rate In order to reduce the rate of labour turnover, the following should be considered: (i) Regular Statistics should be provided analyzing labour turnover by cause and indicating whether the cause was avoidable or unavoidable and whether the person left voluntarily or was dismissed; we should however note that there are some 13

14 dangers in such an analysis because employees who leave do not always give the true reasons for leaving. (ii) Seek ways in which the selection of applicants can be improved in order to prevent situations arising where employees are discontented or unsuitable. (iii) Ensure that the labour requirements are properly planned in order to avoid redundancy (iv) Consider the introduction of high wages plan or some other form of incentives. (v) See that the working environment is congenial. (vi) Consider whether the transfer of a dissatisfied employee to another department will remove the cause of the dissatisfaction. (vii) Hold annual medical check-ups in order to prevent ill-health at a later date. (viii) Consider whether the fringe benefits are competitive, e.g. pension scheme, subsidized meals, sports and social facilities. (ix) Develop better human relationship between management and workers As it is important for an organisation to keep its skilled and experienced employees, a target labour turnover rate could be set with the personnel manager being responsible if the rate is higher than target. Internal Check and Payroll Fraud There is ample scope for perpetration of fraud at some stage during the paration and payment of wages. For this reason, it is essential that some form of controls exist to prevent fraud or to detect it in its early stages. The dangers to be avoided are: The payment of wages to employees who do not exist, The payment to an employee of an amount which is more than he is entitled to receive. Precautions to reduce payroll fraud 1. Segregating the work so that the payroll procedures are not the responsibility of only one or two persons e.g. the clerk who prepared the wage sheet should not also make-up or distribute the wage packets. 2. Adopting adequate authorization procedures: Piece work tickets should be signed by an inspector and the employee s foreman; only overtime properly authorized should be paid; 14

15 changes in wage rates and salaries should only be processed if the personnel manager completes and signs the appropriate forms. 3. Proper Supervision: The distribution of the pay envelopes must be supervised by a senior official and preferably by one who can identify the recipient. 4. Instituting suitable procedures, e.g. a procedure should be laid down for dealing with unclaimed wages. 5. Creating a Programme for internal checks. As part of the Programme, the personnel officer might periodically check the payroll to ensure that payments are not being made to fictitious employees. If the organisation is sufficiently large, the internal audit department could be very much involved in the creating and working of the internal check Programme. Types of payrolls for labour The payroll is the process of determining the net wage earnings of each employee in the organisation. The payroll could either be computerized or could be done manually. With the manual payroll, the earnings of each employee are computed by human effort without the use of the computer. The computerized payroll uses computer software and inputs the basic variables for each employee such as: hours worked overtime hours units produced wage rate per unit or hour statutory deductions voluntary deductions etc Labour Payroll preparation In preparing the payroll, the following procedure is followed: Determine the basic wages of each employee. This done by multiplying the hours worked or units produced by the agreed wage rate Add all other allowances to the basic wages to obtain the gross wages Calculate the various deductions to be made. These are of two types: statutory and voluntary deductions. The statutory deductions are required to be deducted by law and so 15

16 the amount of deduction is determined by the law. These deductions include the following: o Social Security contributions o Employee Personal Income Tax (P.A.Y.E.) o National Health Insurance etc Examples of voluntary deductions include: Trade Union contributions Provident fund contribution Employee welfare contribution etc. When the total deductions are taken from the gross wages, then we obtain the wages of each employee. The Differences between Labour cost accounting and Payroll accounting Labour cost accounting relates to the determination of the cost of labour chargeable to various jobs, customers, clients and overhead accounts. Under labour cost accounting, the objective is to ascertain the labour cost that can be charged to products and services. In this regard the following are considered as labour cost: Wages and salaries of employees Insurance for workmen compensation Employee bonuses Employee share schemes etc. Payroll accounting relates to the process of computing the amount of earnings of employees as well as the various payments made for and on the behalf of employees. Examples of payment on behalf of employees include the following: Employer s Social Security Contribution for employee Employee Social Security Contributions Personal Income Tax of employees Welfare deductions for employees etc. 16

17 Under payroll accounting, labour cost such as workmen compensation, employee insurance etc. are not considered. It is only amounts payable to or on behalf of employees that are considered. 17

18 Practice Questions Question 1 Hours worked = 50hours Rate per Hour = MVR 2000 Calculate Gross wage? Question 2 No. of units produced = 1,000 units Rate per Unit = MVR 16,000 Calculate Gross wage? Question 3 Question 4 18

19 Question 5 Question 6 19

20 Question 7 20

21 Question 8 21

22 Question 9 22

23 Question 10 Question 11 Question 12 23

24 Question 13 Question 14 Question 15 Question 16 24

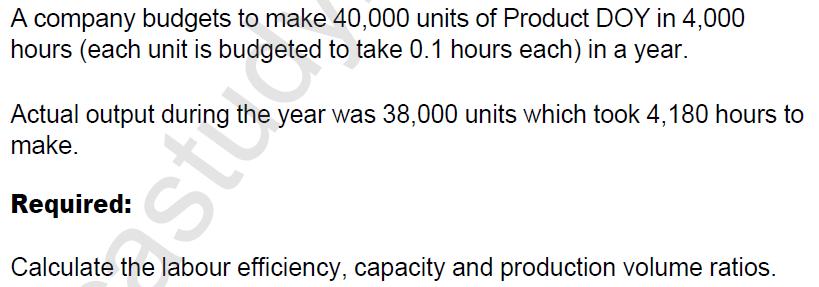

25 Question 17 Rush & Fluster Co budgets to make 25,000 standard units of output (in four hours each) during a budget period of 100,000 hours. Actual output during the period was 27,000 units which took 120,000 hours to make. Required Calculate the efficiency, capacity and production volume ratios. Question 18 Penny Pincher is paid 50c for each towel she weaves, but she is guaranteed a minimum wage of $60 for a 40 hour week. In a series of four weeks, she makes 100, 120, 140 and 160 towels. Required Calculate her pay each week, and the conversion cost per towel if production OH is added at the rate of $2.50 per direct labour hour. 25

26 Question 19 The following data relate to work at a certain factory. Normal working day 8 hours Basic rate of pay per hour $6 Standard time allowed to produce 1 unit 2 minutes Premium bonus 75% of time saved at basic rate What will be the labour cost in a day when 340 units are made? Question 20 Jaffa Co employs two types of labour: skilled workers, considered to be direct workers, and semi-skilled workers considered to be indirect workers. Skilled workers are paid $10 per hour and semi-skilled $5 per hour. The skilled workers have worked 20 hours overtime this week, 12 hours on specific orders and 8 hours on general overtime. Overtime is paid at a rate of time and a quarter. The semi-skilled workers have worked 30 hours overtime, 20 hours for a specific order at a customer s request and the rest for general purposes. Overtime again is paid at time and a quarter. What would be the total overtime pay considered to be a direct cost for this week? Question 21 The following data relate to work in the finishing department of certain factory. Normal working day 8 hours Basic rate of pay per hour $6 Standard time allowed to produce 1 unit 5 minutes Premium bonus payable at the basic rate 60% of time saved On a particular day one employee finishes 190 units. Calculate his gross pay for the day. 26

27 Question 22 Employee A is a carpenter and normally works 36 hours per week. The standard rate of pay is $3.70 per hour. A premium of 50% of basic hourly rate is paid for all overtime hours worked. During the last week of October, Employee A worked 42 hours. The overtime hours worked were for the following reasons: Machine breakdown 4 hours To complete a special job at the request of a customer 2 hours How much of Employee A s earning for the last week of October would have been treated as direct wages? Question 23 A company has 35 direct production employees at the beginning of last year and 25 direct production employees at the end of the year. During the year, a total of 15 direct production employees had left the company to work for local competitors. Calculate the labour turnover rate for the last year. Question 24 27

28 Question 25 28

29 Question 26 29

30 Question 27 30

31 Question 28 31

32 Question 29 32

33 Question 30 Question 31 33

34 Question 32 Question 33 34

35 Question 34 Question 35 35

36 Question 36 36

Chapter 4 Accounting For Labour Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing)

") Chapter 4 Accounting For Labour Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Measuring Labour Activity Production & Productivity Production is the quantity

Chapter 4 Accounting For Labour Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Measuring Labour Activity Production & Productivity Production is the quantity

Classifying and accounting for Labour costs

Intro to Labour Costs Remuneration methods Incentive schemes and productivity Labour turnover Classifying and accounting for Labour costs 1 Critical cost in all organisations Need to make employee investments

Intro to Labour Costs Remuneration methods Incentive schemes and productivity Labour turnover Classifying and accounting for Labour costs 1 Critical cost in all organisations Need to make employee investments

COST & MANAGEMENT ACCOUNTING

OM SAI RAM COST & MANAGEMENT ACCOUNTING [EXECUTIVE PROGRAMME] CA. Jitender Singh Specialized Trainer for [Material, Labour, Overheads, Marginal Costing & Standard Costing] Get ready to LEARN with FUN..

OM SAI RAM COST & MANAGEMENT ACCOUNTING [EXECUTIVE PROGRAMME] CA. Jitender Singh Specialized Trainer for [Material, Labour, Overheads, Marginal Costing & Standard Costing] Get ready to LEARN with FUN..

Professor Vipin Labour Cost

Labour Cost Labour cost is a second major element of cost. The control of labour cost and its accounting is very difficult as it deals with human element. Labour is the most perishable commodity and as

Labour Cost Labour cost is a second major element of cost. The control of labour cost and its accounting is very difficult as it deals with human element. Labour is the most perishable commodity and as

Unit 6 : Planning, Organisation and Control of Resources POCR07-1. Labour Management

Unit 6 : Planning, Organisation and ontrol of Resources POR07-1 Introduction Labour Management lthough the construction process has become more mechanised in recent years, it still requires labour resources.

Unit 6 : Planning, Organisation and ontrol of Resources POR07-1 Introduction Labour Management lthough the construction process has become more mechanised in recent years, it still requires labour resources.

IB Business Management Human Resource Management 2.4 Motivation Summary Notes

www.businessmanagementib.com PAYMENT OR FINANCIAL REWARD SYSTEMS HOURLY WAGE RATE An hourly wage rate or time rate is set for the job perhaps by comparing with other firms or similar jobs. The wage level

www.businessmanagementib.com PAYMENT OR FINANCIAL REWARD SYSTEMS HOURLY WAGE RATE An hourly wage rate or time rate is set for the job perhaps by comparing with other firms or similar jobs. The wage level

3 Labour. Basic Concepts

3 Labour Basic Concepts Labour Cost Direct Labour Indirect Labour Idle Time Normal Idle Time Abnormal Idle Time Time Keeping Time Booking Overtime Overtime Premium Labour Turnover The cost of wages and

3 Labour Basic Concepts Labour Cost Direct Labour Indirect Labour Idle Time Normal Idle Time Abnormal Idle Time Time Keeping Time Booking Overtime Overtime Premium Labour Turnover The cost of wages and

Years Exam Question. ` 5.40 Standard time per unit

CA R. K. Mehta Labour Costing CA Past Years Exam Question Question : 1 (May,1998) Calculate the earnings of workers A, B and C under straight piece rate system ad Merrick s multiple piece rate system from

CA R. K. Mehta Labour Costing CA Past Years Exam Question Question : 1 (May,1998) Calculate the earnings of workers A, B and C under straight piece rate system ad Merrick s multiple piece rate system from

Chapter 3. Accounting for Labor

Chapter 3 Accounting for Labor Learning Objectives LO1 Distinguish between features of hourly rate and piece-rate plans. LO2 Specify procedures for controlling labor costs. LO3 Account for labor costs

Chapter 3 Accounting for Labor Learning Objectives LO1 Distinguish between features of hourly rate and piece-rate plans. LO2 Specify procedures for controlling labor costs. LO3 Account for labor costs

Chapter 6. Motivating Workers

Chapter 6 Motivating Workers Motivation is the reason why employees want to work hard and work effectively for the business. It is a feeling or drive that stimulates employees to work hard for achieving

Chapter 6 Motivating Workers Motivation is the reason why employees want to work hard and work effectively for the business. It is a feeling or drive that stimulates employees to work hard for achieving

SECTION 4 PAYMENT OF WAGES

SECTION 4 PAYMENT OF WAGES Page no. Payment of Wages 92 Payment of Wages Act 1991 92 Deductions 93 Disputes 94 National Minimum Wage 95 Determining average hourly rate of pay 95 Reckonable and Non-Reckonable

SECTION 4 PAYMENT OF WAGES Page no. Payment of Wages 92 Payment of Wages Act 1991 92 Deductions 93 Disputes 94 National Minimum Wage 95 Determining average hourly rate of pay 95 Reckonable and Non-Reckonable

Why you should have an EMPLOYEE HANDBOOK and how to prepare one. Labour Department Hong Kong

Why you should have an EMPLOYEE HANDBOOK and how to prepare one Labour Department Hong Kong WHY YOU SHOULD HAVE AN EMPLOYEE HANDBOOK AND HOW TO PREPARE ONE LABOUR DEPARTMENT HONG KONG APRIL 1988 Printed

Why you should have an EMPLOYEE HANDBOOK and how to prepare one Labour Department Hong Kong WHY YOU SHOULD HAVE AN EMPLOYEE HANDBOOK AND HOW TO PREPARE ONE LABOUR DEPARTMENT HONG KONG APRIL 1988 Printed

Which of the following is correct? Select correct option: Units sold=opening finished goods units + Units produced Closing finished goods units Units

Which of the following is correct? Units sold=opening finished goods units + Units produced Closing finished goods units Units Sold = Units produced + Closing finished goods units - Opening finished goods

Which of the following is correct? Units sold=opening finished goods units + Units produced Closing finished goods units Units Sold = Units produced + Closing finished goods units - Opening finished goods

COST ACCOUNTING QUESTION ONE

QUESTION ONE COST ACCOUNTING a) Briefly explain the term limiting factor A limiting factor is a binding constraint upon the organization. It prevents indefinite expansion or unlimited profits. It may be

QUESTION ONE COST ACCOUNTING a) Briefly explain the term limiting factor A limiting factor is a binding constraint upon the organization. It prevents indefinite expansion or unlimited profits. It may be

POLICY: REMUNERATION

POLICY: REMUNERATION www.afrimat.co.za F2016 1. Purpose Afrimat Limited and its subsidiaries are committed to ensuring that its remuneration practices enable the company to: 1.1.1 Attract and retain critical

POLICY: REMUNERATION www.afrimat.co.za F2016 1. Purpose Afrimat Limited and its subsidiaries are committed to ensuring that its remuneration practices enable the company to: 1.1.1 Attract and retain critical

General Guide to Employment Law Introduction

General Guide to Employment Law Introduction In recent years, the relationship between employer and employee has been regulated more and more by legislation, much of which has originated at EU level. Human

General Guide to Employment Law Introduction In recent years, the relationship between employer and employee has been regulated more and more by legislation, much of which has originated at EU level. Human

COST ACCOUNTING (PART-5) LABOR COST CONTROL - 1

LABOR COST CONTROL - 1") COST ACCOUNTING (PART-5) LABOR COST CONTROL - 1 1. INTRODUCTION Dear students, welcome to the lecture series on cost accounting, today in this lecture we shall cover the topic labor cost control. We shall

COST ACCOUNTING (PART-5) LABOR COST CONTROL - 1 1. INTRODUCTION Dear students, welcome to the lecture series on cost accounting, today in this lecture we shall cover the topic labor cost control. We shall

51 Rewarding Special Groups

839 51 Rewarding Special Groups Learning outcomes On completing this chapter you should know about: Elements of directors and senior executives pay Types of payment for manual workers Payment and incentive

839 51 Rewarding Special Groups Learning outcomes On completing this chapter you should know about: Elements of directors and senior executives pay Types of payment for manual workers Payment and incentive

PAYROLL AND PERSONNEL CYCLE

TOPIC 7 PAYROLL AND PERSONNEL CYCLE TOPIC OVERVIEW With human resources and payroll departments under more pressure than ever before, a modern automated payroll solution is essential for any business.

TOPIC 7 PAYROLL AND PERSONNEL CYCLE TOPIC OVERVIEW With human resources and payroll departments under more pressure than ever before, a modern automated payroll solution is essential for any business.

COMPENSATION AND REWARDS. The complex process includes decisions regarding variable pay and benefits

COMPENSATION AND REWARDS Definition: The sum total of all forms of payments or rewards provided to employees for performing tasks to achieve organizational objectives. Compensation- Nature and scope The

COMPENSATION AND REWARDS Definition: The sum total of all forms of payments or rewards provided to employees for performing tasks to achieve organizational objectives. Compensation- Nature and scope The

Recruitment & Selection

Recruitment & Selection Revision Presentations 2004 The Recruitment Process Reasons to Recruit Staff Business is expanding due to: Increasing sales of existing products Developing new products Entering

Recruitment & Selection Revision Presentations 2004 The Recruitment Process Reasons to Recruit Staff Business is expanding due to: Increasing sales of existing products Developing new products Entering

Learning Objectives. Understand the different types of compensation. Understand what is strategic compensation planning

Ibrahim Sameer Learning Objectives Define compensation Understand the different types of compensation Understand what is strategic compensation planning Understand the factors affecting wage rate Understand

Ibrahim Sameer Learning Objectives Define compensation Understand the different types of compensation Understand what is strategic compensation planning Understand the factors affecting wage rate Understand

Cost Analysis and Estimating for Engineering and Management

Cost Analysis and Estimating for Engineering and Management Chapter 2 Labor Analysis Ch 2-1 Overview Labor and Labor Costs Determining Costs Labor Hour Time Study Work Sampling Wages and Fringe Benefits

Cost Analysis and Estimating for Engineering and Management Chapter 2 Labor Analysis Ch 2-1 Overview Labor and Labor Costs Determining Costs Labor Hour Time Study Work Sampling Wages and Fringe Benefits

Chapter 13: Motivation at work Motivation. Motivation theories

Chapter 13: Motivation at work Motivation People work for a number of reasons. Most people work because they need to earn money to survive, while others work voluntarily for other reasons. Motivation is

Chapter 13: Motivation at work Motivation People work for a number of reasons. Most people work because they need to earn money to survive, while others work voluntarily for other reasons. Motivation is

SYLLABUS. Class B.Com IV Sem. (All) Subject: Cost Accounting

Subject: Cost Accounting") CLASS:-B.Com. IV Semester SYLLABUS Class B.Com IV Sem. (All) Subject: Cost Accounting Unit-I Unit- II Unit III Unit IV Unit V Cost: Meaning, Concept and Classification. Elements of Cost, Nature & Importance,

CLASS:-B.Com. IV Semester SYLLABUS Class B.Com IV Sem. (All) Subject: Cost Accounting Unit-I Unit- II Unit III Unit IV Unit V Cost: Meaning, Concept and Classification. Elements of Cost, Nature & Importance,

1: NATURE CONCEPTS AND FUNCTIONS OF HRM

Subject Paper No and Title 9: HUMAN RESOURCE MANAGEMENT Module No and Title Module Tag 1: NATURE CONCEPTS AND FUNCTIONS OF HRM COM_P9_M1 TABLE OF CONTENTS 1. Learning Outcomes 2. Introduction Human Resource

Subject Paper No and Title 9: HUMAN RESOURCE MANAGEMENT Module No and Title Module Tag 1: NATURE CONCEPTS AND FUNCTIONS OF HRM COM_P9_M1 TABLE OF CONTENTS 1. Learning Outcomes 2. Introduction Human Resource

CAS -7 COST ACCOUNTING STANDARD ON EMPLOYEE COST

Cost Accounting Standards Board CAS -7 COST ACCOUNTING STANDARD ON EMPLOYEE COST The following is the COST ACCOUNTING STANDARD 7 (CAS - 7) issued by the Council of The Institute of Cost Accountants of

Cost Accounting Standards Board CAS -7 COST ACCOUNTING STANDARD ON EMPLOYEE COST The following is the COST ACCOUNTING STANDARD 7 (CAS - 7) issued by the Council of The Institute of Cost Accountants of

Maternity Entitlement Guidance Note

Maternity Entitlement Guidance Note The legislation is contained in the Employment Rights Act 1996, and the Maternity and Parental Leave etc Regulations 1999. Case law and the provisions of the Sex Discrimination

Maternity Entitlement Guidance Note The legislation is contained in the Employment Rights Act 1996, and the Maternity and Parental Leave etc Regulations 1999. Case law and the provisions of the Sex Discrimination

Responsive Industries Limited

Responsive Industries Limited Nomination & Remuneration Policy Policy Name Nomination & Remuneration Policy Background Reconstitution of Remuneration Committee as Nomination and Remuneration Committee

Responsive Industries Limited Nomination & Remuneration Policy Policy Name Nomination & Remuneration Policy Background Reconstitution of Remuneration Committee as Nomination and Remuneration Committee

MID SUSSEX DISTRICT COUNCIL Pay Policy Statement Financial year

MID SUSSEX DISTRICT COUNCIL Pay Policy Statement Financial year 2016-17 1. Purpose The Council has an obligation under Section 38 (1) of the Localism Act 2011 to prepare a Pay Policy Statement for each

MID SUSSEX DISTRICT COUNCIL Pay Policy Statement Financial year 2016-17 1. Purpose The Council has an obligation under Section 38 (1) of the Localism Act 2011 to prepare a Pay Policy Statement for each

PAY AND THE NATIONAL MINIMUM WAGE

PAY AND THE NATIONAL MINIMUM WAGE ELIGIBILITY FOR THE NATIONAL MINIMUM WAGE The national minimum wage is payable to most workers, not of compulsory school age, who ordinarily work under contract in the

PAY AND THE NATIONAL MINIMUM WAGE ELIGIBILITY FOR THE NATIONAL MINIMUM WAGE The national minimum wage is payable to most workers, not of compulsory school age, who ordinarily work under contract in the

Managing Human Resources Bohlander Snell

5 MANAGING PEOPLE Compensation & Incentive Plans Managing Human Resources Bohlander Snell 14 th edition PowerPoint Presentation by Charlie Cook The University of West Alabama Chapter Contents Summarized

5 MANAGING PEOPLE Compensation & Incentive Plans Managing Human Resources Bohlander Snell 14 th edition PowerPoint Presentation by Charlie Cook The University of West Alabama Chapter Contents Summarized

STATE OWNED ENTERPRISES REMUNERATION GUIDELINES

STATE OWNED ENTERPRISES REMUNERATION GUIDELINES PART A CHAIRPERSONS & NON-EXECUTIVE DIRECTORS AUGUST 2007 Restricted Contents 1. DEFINITIONS 3 2. PURPOSE 4 3. GENERAL 4 4. REMUNERATION GUIDELINES 5 5.

STATE OWNED ENTERPRISES REMUNERATION GUIDELINES PART A CHAIRPERSONS & NON-EXECUTIVE DIRECTORS AUGUST 2007 Restricted Contents 1. DEFINITIONS 3 2. PURPOSE 4 3. GENERAL 4 4. REMUNERATION GUIDELINES 5 5.

GENDER PAY GAP REPORT APRIL 2019

GENDER PAY GAP REPORT APRIL 2019 0 Building a diverse workforce and maintaining an inclusive workplace is vitally important to Portmeirion Group in achieving our strategic vision and is an integral element

GENDER PAY GAP REPORT APRIL 2019 0 Building a diverse workforce and maintaining an inclusive workplace is vitally important to Portmeirion Group in achieving our strategic vision and is an integral element

COST AND MANAGEMENT ACCOUNTING

EXECUTIVE PROGRAMME COST AND MANAGEMENT ACCOUNTING SAMPLE TEST PAPER (This test paper is for practice and self study only and not to be sent to the institute) Time allowed: 3 hours Maximum marks : 100

EXECUTIVE PROGRAMME COST AND MANAGEMENT ACCOUNTING SAMPLE TEST PAPER (This test paper is for practice and self study only and not to be sent to the institute) Time allowed: 3 hours Maximum marks : 100

Type of Pay Hours Rate Amount. Regular Pay 40 $8.00 per hour = $ $12.00 per hour. Gross Pay $368.00

Chapter 6 Understanding Pay and Benefits Gross Pay, Deductions, and Net Pay Gross pay is the amount you earn before any deductions are subtracted. Amounts subtracted from your gross pay are called. When

Chapter 6 Understanding Pay and Benefits Gross Pay, Deductions, and Net Pay Gross pay is the amount you earn before any deductions are subtracted. Amounts subtracted from your gross pay are called. When

Wage and Salary Administration

CHAPTER - 5 Wage and Salary Administration Wage and Salary Fixation. Constitutional Perspective and norms for wage and salary determination. Law relating to payment of wages, salary and bonus. Regulation

CHAPTER - 5 Wage and Salary Administration Wage and Salary Fixation. Constitutional Perspective and norms for wage and salary determination. Law relating to payment of wages, salary and bonus. Regulation

2. Recruitment and Selection

1. Human Resources Human resource management (HRM) is the area of administrative focus dealing with an organization's employees. There are Four Main Job Roles in a business: Directors: Appointed to run

1. Human Resources Human resource management (HRM) is the area of administrative focus dealing with an organization's employees. There are Four Main Job Roles in a business: Directors: Appointed to run

Pay, Benefits, and Working Conditions

Chapter 6 Pay, Benefits, and Working Conditions 6.1 Understanding Pay and Benefits 6.2 Work Schedules and Unions 2010 South-Western, Cengage Learning Lesson 6.1 Understanding Pay and Benefits GOALS Compute

Chapter 6 Pay, Benefits, and Working Conditions 6.1 Understanding Pay and Benefits 6.2 Work Schedules and Unions 2010 South-Western, Cengage Learning Lesson 6.1 Understanding Pay and Benefits GOALS Compute

IIII HILLGROVE RESOURCES LIMITED IIII ACN

REMUNERATION AND BENEFITS POLICY IIII HILLGROVE RESOURCES LIMITED IIII ACN 004 297 116 Level 17 Australia Square, 264 George Street, Sydney NSW 2000, Australia T +61 2 8247 9300 F +61 2 8247 9399 www.hillgroveresources.com

REMUNERATION AND BENEFITS POLICY IIII HILLGROVE RESOURCES LIMITED IIII ACN 004 297 116 Level 17 Australia Square, 264 George Street, Sydney NSW 2000, Australia T +61 2 8247 9300 F +61 2 8247 9399 www.hillgroveresources.com

POLICY: REMUNERATION

POLICY: REMUNERATION www.afrimat.co.za F2019 1. Purpose Afrimat Limited and its subsidiaries are committed to ensuring that its remuneration practices enable the company to: 2. Policy 1.1.1 Attract and

POLICY: REMUNERATION www.afrimat.co.za F2019 1. Purpose Afrimat Limited and its subsidiaries are committed to ensuring that its remuneration practices enable the company to: 2. Policy 1.1.1 Attract and

Paying Overtime Under the FLSA: Part 1. Presented on Wednesday, April 5, 2017

Paying Overtime Under the FLSA: Part 1 Presented on Wednesday, April 5, 2017 HOUSEKEEPING Credit Questions Topic Speaker HOUSEKEEPING Certificates delivered by email no later than 5/05/2017 Be watching

Paying Overtime Under the FLSA: Part 1 Presented on Wednesday, April 5, 2017 HOUSEKEEPING Credit Questions Topic Speaker HOUSEKEEPING Certificates delivered by email no later than 5/05/2017 Be watching

Paper F8. Audit and Assurance. March/June 2018 Sample Questions. Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Fundamentals Level Skills Module Audit and Assurance March/June 2018 Sample Questions F8 ACCA Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A ALL 15 questions

Fundamentals Level Skills Module Audit and Assurance March/June 2018 Sample Questions F8 ACCA Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A ALL 15 questions

Payroll Policy. Purpose of Policy. The policy is to cover the administration of the payroll service. Overview

Purpose of Policy Overview Scope: Mandatory Policy The policy is to cover the administration of the payroll service The policy covers the range of services provided by payroll, the legislative requirements

Purpose of Policy Overview Scope: Mandatory Policy The policy is to cover the administration of the payroll service The policy covers the range of services provided by payroll, the legislative requirements

> > > > > > > > Chapter 9 Human Resource Management, Motivation, and Labor-Management Relations. Kamrul Huda Talukdar Lecturer North South University

> > > > > > > > Chapter 9 Human Resource Management, Motivation, and Labor-Management Relations Kamrul Huda Talukdar Lecturer North South University Human resource management - function of attracting,

> > > > > > > > Chapter 9 Human Resource Management, Motivation, and Labor-Management Relations Kamrul Huda Talukdar Lecturer North South University Human resource management - function of attracting,

1.1. In these Terms of Business the following definitions apply:

Page 1 CONTRACT WITH THE CLIENT (SUPPLYING TEMPORARY STAFF SERVICES/CLIENT TERMS OF BUSINESS) 1. DEFINITIONS 1.1. In these Terms of Business the following definitions apply: Assignment Client means the

Page 1 CONTRACT WITH THE CLIENT (SUPPLYING TEMPORARY STAFF SERVICES/CLIENT TERMS OF BUSINESS) 1. DEFINITIONS 1.1. In these Terms of Business the following definitions apply: Assignment Client means the

The intellectual property rights of third parties will be respected by all concerned. Thus, unlawful copies are neither offered, nor produced.

CODE OF CONDUCT 0 Prerequisites The beeline GmbH Code of Conduct is based on standards set by the International Labour Organization (ILO) and combines other current international standards. 0.1 Legal Compliance

CODE OF CONDUCT 0 Prerequisites The beeline GmbH Code of Conduct is based on standards set by the International Labour Organization (ILO) and combines other current international standards. 0.1 Legal Compliance

EQUALITY AND DIVERSITY POLICY

POLICIES AND PROCEDURES PP6 EQUALITY AND DIVERSITY POLICY Approved by Version Issue Date Review Date Contact Person Trust Board Sept 2003 Three 01/03/2009 01/03/2011 Head of Personnel Equal Opportunities:

POLICIES AND PROCEDURES PP6 EQUALITY AND DIVERSITY POLICY Approved by Version Issue Date Review Date Contact Person Trust Board Sept 2003 Three 01/03/2009 01/03/2011 Head of Personnel Equal Opportunities:

Grievance Function in Industrial Relations Learning Objectives To understand the meaning & content of grievances the formal & informal presentation

Learning Objectives To understand the meaning & content of grievances the formal & informal presentation of grievances the role of personnel department in grievance handling. the advantages of grievance

Learning Objectives To understand the meaning & content of grievances the formal & informal presentation of grievances the role of personnel department in grievance handling. the advantages of grievance

Human resource department is responsible for coordinating all activities involving the company s employees.

Human resource department is responsible for coordinating all activities involving the company s employees. They study the labour market (where employers meet employees) to see what occupations and skills

Human resource department is responsible for coordinating all activities involving the company s employees. They study the labour market (where employers meet employees) to see what occupations and skills

Overtime Compensation

Published on MTAS (http://www.mtas.tennessee.edu) April 07, 2019 Overtime Compensation Dear Reader: The following document was created from the MTAS website (mtas.tennessee.edu). This website is maintained

Published on MTAS (http://www.mtas.tennessee.edu) April 07, 2019 Overtime Compensation Dear Reader: The following document was created from the MTAS website (mtas.tennessee.edu). This website is maintained

A CHAPTER FROM THE BUSINESS TOOLKIT

WAGES A CHAPTER FROM THE BUSINESS TOOLKIT This is only one chapter of the tlkit. You can download the full document or any of the other chapters from the Partner Africa website. www.partnerafrica.org/business-tlkit

WAGES A CHAPTER FROM THE BUSINESS TOOLKIT This is only one chapter of the tlkit. You can download the full document or any of the other chapters from the Partner Africa website. www.partnerafrica.org/business-tlkit

About the Tutorial. Audience. Prerequisites. Disclaimer & Copyright. Human Resource Management

[DOCUMENT TITLE] About the Tutorial Human Resource Management is an operation in companies, designed to maximize employee performance in order to meet the employer's strategic goals and objectives. It

[DOCUMENT TITLE] About the Tutorial Human Resource Management is an operation in companies, designed to maximize employee performance in order to meet the employer's strategic goals and objectives. It

FROM HIRING TO FIRING A BASIC GUIDE TO THE THAI EMPLOYMENT LAW LIFE CYCLE

FROM HIRING TO FIRING A BASIC GUIDE TO THE THAI EMPLOYMENT LAW LIFE CYCLE HIRING Recruitment Recruiting in Thailand is often done through database recruitment, licensed headhunting firms, or by placing

FROM HIRING TO FIRING A BASIC GUIDE TO THE THAI EMPLOYMENT LAW LIFE CYCLE HIRING Recruitment Recruiting in Thailand is often done through database recruitment, licensed headhunting firms, or by placing

Financial Accounting and Auditing Paper-III Financial Accounting

Revised Syllabus of the Courses of B.Com. Programme at T.Y.B.Com. with Effect from the Academic Year 2015-2016 for IDOL Students Financial Accounting and Auditing Paper-III Financial Accounting SECTION

Revised Syllabus of the Courses of B.Com. Programme at T.Y.B.Com. with Effect from the Academic Year 2015-2016 for IDOL Students Financial Accounting and Auditing Paper-III Financial Accounting SECTION

Johanna Shikongo Cell:

Johanna Shikongo Cell: 0812850115 Email: jn2082@gmail.com Discuss the different approaches to job design Explain the methods of job design Explain the concept of job analysis Describe the job description

Johanna Shikongo Cell: 0812850115 Email: jn2082@gmail.com Discuss the different approaches to job design Explain the methods of job design Explain the concept of job analysis Describe the job description

III B.Com [ ] Semester V Core: Cost Accounting 502C Multiple Choice Questions.

![III B.Com [ ] Semester V Core: Cost Accounting 502C Multiple Choice Questions.](/thumbs/81/83995654.jpg "III B.Com [ ] Semester V Core: Cost Accounting 502C Multiple Choice Questions.") 1 of 36 8/28/2013 10:47 PM Dr.G.R.Damodaran College of Science (Autonomous, affiliated to the Bharathiar University, recognized by the UGC)Reaccredited at the 'A' Grade Level by the NAAC and ISO 9001:2008

1 of 36 8/28/2013 10:47 PM Dr.G.R.Damodaran College of Science (Autonomous, affiliated to the Bharathiar University, recognized by the UGC)Reaccredited at the 'A' Grade Level by the NAAC and ISO 9001:2008

AMERICAN LIBRARY ASSOCIATION PERSONNEL POLICY MANUAL. Item Number: 202 Page 1 of 12. COMPENSATION POLICY Issued 09/01/02

Item Number: 202 Page 1 of 12 I. COMPENSATION POLICY It is the policy of the American Library Association ( ALA ) to provide a competitive total compensation package to all employees based on their level

Item Number: 202 Page 1 of 12 I. COMPENSATION POLICY It is the policy of the American Library Association ( ALA ) to provide a competitive total compensation package to all employees based on their level

PAY POLICY STATEMENT FOR THE FINANCIAL YEAR 2016/2017. Appendix 2

PAY POLICY STATEMENT FOR THE FINANCIAL YEAR 2016/2017 Appendix 2 Statement of Pay Policy for the year 1 April 2016 to 31 March 2017 1. Introduction Sections 38 43 of the Localism Act 2011 require the Authority

PAY POLICY STATEMENT FOR THE FINANCIAL YEAR 2016/2017 Appendix 2 Statement of Pay Policy for the year 1 April 2016 to 31 March 2017 1. Introduction Sections 38 43 of the Localism Act 2011 require the Authority

INTER CA MAY PAPER 3 : COST AND MANAGEMENT ACCOUTING Branch: Multiple Date: Page 1

INTER CA MAY 2018 PAPER 3 : COST AND MANAGEMENT ACCOUTING Branch: Multiple Date: Note: Question 1 is compulsory. Attempt any five from the rest. Note: All questions are compulsory. Question 1 (5 Marks

INTER CA MAY 2018 PAPER 3 : COST AND MANAGEMENT ACCOUTING Branch: Multiple Date: Note: Question 1 is compulsory. Attempt any five from the rest. Note: All questions are compulsory. Question 1 (5 Marks

CONTRACT WITH THE TEMPORARY WORKERS (TERMS OF ENGAGEMENT/CONTRACT FOR SERVICES) 1.1. In these Terms of Engagement the following definitions apply:

1.1. In these Terms of Engagement the following definitions apply:") Page 1 CONTRACT WITH THE TEMPORARY WORKERS (TERMS OF ENGAGEMENT/CONTRACT FOR SERVICES) 1. DEFINITIONS 1.1. In these Terms of Engagement the following definitions apply: Assignment Client means the period

Page 1 CONTRACT WITH THE TEMPORARY WORKERS (TERMS OF ENGAGEMENT/CONTRACT FOR SERVICES) 1. DEFINITIONS 1.1. In these Terms of Engagement the following definitions apply: Assignment Client means the period

Managing People and Finance. Outcome One. Pupil Notes. National 5

Managing People and Finance Outcome One Pupil Notes National 5 The Human Resources Department is the department that deals with all aspects of employee relations on behalf of the owners. The HR department

Managing People and Finance Outcome One Pupil Notes National 5 The Human Resources Department is the department that deals with all aspects of employee relations on behalf of the owners. The HR department

TAMAR BRIDGE and TORPOINT FERRY JOINT COMMITTEE

TAMAR BRIDGE and TORPOINT FERRY JOINT COMMITTEE PAY POLICY STATEMENT 2018/2019 version history Date Version Number Author Comments 23 May 2018 V1.0 C Humphries Post staff side consultation Pay Policy Statement

TAMAR BRIDGE and TORPOINT FERRY JOINT COMMITTEE PAY POLICY STATEMENT 2018/2019 version history Date Version Number Author Comments 23 May 2018 V1.0 C Humphries Post staff side consultation Pay Policy Statement

2. People in Business

Compiled by: Shubhanshi Gaudani 1 2. People in Business 2.1 Motivating Workers Business Studies, CIE IGCSE (0450) 2.1.1 Importance of well motivated workforce WHY PEOPLE WORK AND WHAT MOTIVATION MEANS

Compiled by: Shubhanshi Gaudani 1 2. People in Business 2.1 Motivating Workers Business Studies, CIE IGCSE (0450) 2.1.1 Importance of well motivated workforce WHY PEOPLE WORK AND WHAT MOTIVATION MEANS

March 22, Internal Audit Report Municipal Payroll Review Finance Department

Internal Audit Report 2005-3 Introduction. The Municipality of Anchorage has a complex payroll system that includes nine unions, a wide variety of work schedules and leave plans, and serves about 2,900

Internal Audit Report 2005-3 Introduction. The Municipality of Anchorage has a complex payroll system that includes nine unions, a wide variety of work schedules and leave plans, and serves about 2,900

CHAPTER 1 Strategic Compensation: A Component of Human Resource Systems

CHAPTER 1 Strategic Compensation: A Component of Human Resource Systems Multiple Choice Questions 1. Which type of compensation program is based, in part, on the human capital theory? a) merit pay b) seniority

CHAPTER 1 Strategic Compensation: A Component of Human Resource Systems Multiple Choice Questions 1. Which type of compensation program is based, in part, on the human capital theory? a) merit pay b) seniority

Nomination And Remuneration Policy

Nomination And Remuneration Policy TABLE OF CONTENTS 1 Background 2 2 Definitions 2 3 Purpose 3 4 Objectives 4 5 Applicability 5 6 Nomination And Remuneration Committee (NRC) Formulation And 5 Structure

Nomination And Remuneration Policy TABLE OF CONTENTS 1 Background 2 2 Definitions 2 3 Purpose 3 4 Objectives 4 5 Applicability 5 6 Nomination And Remuneration Committee (NRC) Formulation And 5 Structure

CTAS e-li. Published on e-li (http://eli.ctas.tennessee.edu) January 03, 2018 Calculating Overtime Pay

January 03, 2018 Calculating Overtime Pay") Published on e-li (http://eli.ctas.tennessee.edu) January 03, 2018 Calculating Overtime Pay Dear Reader: The following document was created from the CTAS electronic library known as e-li. This online library

Published on e-li (http://eli.ctas.tennessee.edu) January 03, 2018 Calculating Overtime Pay Dear Reader: The following document was created from the CTAS electronic library known as e-li. This online library

Example: Counting The Cost Of Employee Turnover

Employee turnover is an issue every organisation deals with on a regular basis. The size of your business, your industry and the wider employment market will have an effect on turnover. However, the greatest

Employee turnover is an issue every organisation deals with on a regular basis. The size of your business, your industry and the wider employment market will have an effect on turnover. However, the greatest

The Authority has a third group of employees, namely the Chief Executive and two Directors, of whom one is uniformed and one non-uniformed.

Kent and Medway Fire and Rescue Authority Pay Policy Statement 2016/17 Appendix 1 to Item No: B2 Introduction The Pay Policy Statement set out below has been compiled in accordance with Sections 38 to

Kent and Medway Fire and Rescue Authority Pay Policy Statement 2016/17 Appendix 1 to Item No: B2 Introduction The Pay Policy Statement set out below has been compiled in accordance with Sections 38 to

Paying Overtime under the FLSA Part 1: The Rules and Regulations of Overtime under the FLSA Part 1

Paying Overtime under the FLSA Part 1: The Rules and Regulations of Overtime under the FLSA Part 1 Presented on Wednesday, August 31, 2016 1 2 Housekeeping 3 Credit Questions Today s topic Speaker To earn

Paying Overtime under the FLSA Part 1: The Rules and Regulations of Overtime under the FLSA Part 1 Presented on Wednesday, August 31, 2016 1 2 Housekeeping 3 Credit Questions Today s topic Speaker To earn

Secondment Policy and Procedure

Policy Owner Owner: Author: Screening and Proofing Section 75 screened: Human Rights proofed: Consultation Human Resources Head of Human Resources 18 March 2014 No equality issues identified 11 June 2014

Policy Owner Owner: Author: Screening and Proofing Section 75 screened: Human Rights proofed: Consultation Human Resources Head of Human Resources 18 March 2014 No equality issues identified 11 June 2014

Concepts in Enterprise Resource Planning. Chapter 6 Human Resources Processes with ERP

Concepts in Enterprise Resource Planning Chapter 6 Human Resources Processes with ERP Chapter Objectives Explain why the Human Resources function is critical to the success of a company Describe the key

Concepts in Enterprise Resource Planning Chapter 6 Human Resources Processes with ERP Chapter Objectives Explain why the Human Resources function is critical to the success of a company Describe the key

REMUNERATION POLICY AND PROCEDURES FOR DIRECTORS AND SENIOR MANAGEMENT

REMUNERATION POLICY AND PROCEDURES FOR DIRECTORS AND SENIOR MANAGEMENT 1. INTRODUCTION 1.1 Purpose 1.1.1 This Remuneration Policy and Procedures is the guiding document ( Document ) for the Board of Directors

REMUNERATION POLICY AND PROCEDURES FOR DIRECTORS AND SENIOR MANAGEMENT 1. INTRODUCTION 1.1 Purpose 1.1.1 This Remuneration Policy and Procedures is the guiding document ( Document ) for the Board of Directors

Redundancy: Avoidance and Handling Policy and Procedure

2013 Redundancy: Avoidance and Handling Policy and Procedure 1. What is meant by Redundancy? 1.1 Redundancy arises when employees are dismissed because: The employer has ceased, or intends to cease, to

2013 Redundancy: Avoidance and Handling Policy and Procedure 1. What is meant by Redundancy? 1.1 Redundancy arises when employees are dismissed because: The employer has ceased, or intends to cease, to

The human resource management function the employment cycle. Business Management Unit 3 Area of Study 1

The human resource management function the employment cycle Business Management Unit 3 Area of Study 1 Phases of the human resource/staffing process and their related activities Phase Activities Stage

The human resource management function the employment cycle Business Management Unit 3 Area of Study 1 Phases of the human resource/staffing process and their related activities Phase Activities Stage

DHHS Internal Control Checklist Disclaimer

DHHS Internal Control Checklist Disclaimer Your handouts contain several checklists to use when reviewing internal controls. These checklists were all developed by independent sources, and some have been

DHHS Internal Control Checklist Disclaimer Your handouts contain several checklists to use when reviewing internal controls. These checklists were all developed by independent sources, and some have been

Collective Agreement For posted employees. Road Transport and Mechanics

1 Collective Agreement For posted employees. Road Transport and Mechanics Between Company: and Swedish Transport Workers Union Corp. ID no.: Address: Olof Palmes gata 29 SE-101 330 Stockholm Country: Sweden

1 Collective Agreement For posted employees. Road Transport and Mechanics Between Company: and Swedish Transport Workers Union Corp. ID no.: Address: Olof Palmes gata 29 SE-101 330 Stockholm Country: Sweden

COST ACCOUNTING b.com part II Regular & Private (SUPPLEMENTARY) Solved Paper. Compiled & Solved by: Sameer Hussain

Solved Paper. Compiled & Solved by: Sameer Hussain") COST ACCOUNTING b.com part II 2014 Regular & Private (SUPPLEMENTARY) Solved Paper Compiled & Solved by: Sameer Hussain Instructions: (1) Attempt any FIVE questions. (2) All questions carry equal marks.

COST ACCOUNTING b.com part II 2014 Regular & Private (SUPPLEMENTARY) Solved Paper Compiled & Solved by: Sameer Hussain Instructions: (1) Attempt any FIVE questions. (2) All questions carry equal marks.

Registered Redundancy Policy

Registered Redundancy Policy References Other CLC policies relating to this policy Promoting Equality and Fair Treatment at Work Disciplinary Policy Wellbeing at Work Policy Staff Handbook Management of

Registered Redundancy Policy References Other CLC policies relating to this policy Promoting Equality and Fair Treatment at Work Disciplinary Policy Wellbeing at Work Policy Staff Handbook Management of

POST GRADUATE DIPLOMA IN HUMAN RESOURCE MANAGEMENT (PGDHRM) Semester I PROGRAMME CURRICULUM

Semester I PROGRAMME CURRICULUM") POST GRADUATE DIPLOMA IN HUMAN RESOURCE MANAGEMENT (PGDHRM) PROGRAMME CURRICULUM Semester I 1. Human Resource Management 2. HR Development & Training 3. Performance and Potential Management 4. Industrial

POST GRADUATE DIPLOMA IN HUMAN RESOURCE MANAGEMENT (PGDHRM) PROGRAMME CURRICULUM Semester I 1. Human Resource Management 2. HR Development & Training 3. Performance and Potential Management 4. Industrial

financial incentives. piecework plans. perquisites. D) Taylor bonuses. E) group incentive plans.

Taylor bonuses. E) group incentive plans.") MULTIPLE HOIE. hoose the one alternative that best completes the statement or answers the question. 1 Popularized by Frederick Taylor in the late 1800s, financial rewards paid to workers whose production

MULTIPLE HOIE. hoose the one alternative that best completes the statement or answers the question. 1 Popularized by Frederick Taylor in the late 1800s, financial rewards paid to workers whose production

CERTIFICATIONS IN HUMAN RESOURCES» PHRi TM Professional in Human Resources - International TM. PHRi EXAM CONTENT OUTLINE

CERTIFICATIONS IN HUMAN RESOURCES» PHRi TM Professional in Human Resources - International TM PHRi EXAM CONTENT OUTLINE PHRi EXAM CONTENT OUTLINE AT-A-GLANCE PHRi EXAM WEIGHTING BY FUNCTIONAL AREA:» HR

CERTIFICATIONS IN HUMAN RESOURCES» PHRi TM Professional in Human Resources - International TM PHRi EXAM CONTENT OUTLINE PHRi EXAM CONTENT OUTLINE AT-A-GLANCE PHRi EXAM WEIGHTING BY FUNCTIONAL AREA:» HR

LEGAL ALERT? APRIL 2006? EMPLOYMENT LAWS IN NIGERIA IN THE 21ST CENTURY.

LEGAL ALERT? APRIL 2006? EMPLOYMENT LAWS IN NIGERIA IN THE 21ST CENTURY. In this Issue. 1. Subscribe & Unsubscribe to Legal Alert. 2. Legal Alerts & "Spam" Software. 3. Business Quote of the Month. 4.

LEGAL ALERT? APRIL 2006? EMPLOYMENT LAWS IN NIGERIA IN THE 21ST CENTURY. In this Issue. 1. Subscribe & Unsubscribe to Legal Alert. 2. Legal Alerts & "Spam" Software. 3. Business Quote of the Month. 4.

NHS Employers Briefing Note Gender Pay Gap Reporting

NHS Employers Briefing Note Gender Pay Gap Reporting Introduction The Equality Act 2010 (Specific Duties and Public Authorities) Regulations 2017 (the Regulations ) set out a public authority s gender

NHS Employers Briefing Note Gender Pay Gap Reporting Introduction The Equality Act 2010 (Specific Duties and Public Authorities) Regulations 2017 (the Regulations ) set out a public authority s gender

Effingham County Board of Commissioners

Effingham County Board of Commissioners THE OFFICE OF HUMAN RESOURCES EMPLOYMENT POLICIES SECTION 3: PAY FOR PERFORMANCE 3.01 POSITION CLASSIFICATION PLAN 3.02 PAY PLAN 3.03 COMPENSATION 3.04 HOURS OF

Effingham County Board of Commissioners THE OFFICE OF HUMAN RESOURCES EMPLOYMENT POLICIES SECTION 3: PAY FOR PERFORMANCE 3.01 POSITION CLASSIFICATION PLAN 3.02 PAY PLAN 3.03 COMPENSATION 3.04 HOURS OF

TULSA TECHNOLOGY CENTER PER 35

Employee Compensation Policy The Board of Education shall contract with, and fix the duties and compensation of employees of the District. The provision of employee compensation as remuneration for work

Employee Compensation Policy The Board of Education shall contract with, and fix the duties and compensation of employees of the District. The provision of employee compensation as remuneration for work

Unit 1 Cost Accounts, Unit Costing & Reconciliation. (a) Marginal Costing (b) Job Costing (c) Batch Costing (d) Contract Costing

Marginal Costing (b) Job Costing (c) Batch Costing (d) Contract Costing") Unit 1 Cost Accounts, Unit Costing & Reconciliation 1.Which one of the following is not a method of costing? (a) Marginal Costing (b) Job Costing (c) Batch Costing (d) Contract Costing 2. Which one of

Unit 1 Cost Accounts, Unit Costing & Reconciliation 1.Which one of the following is not a method of costing? (a) Marginal Costing (b) Job Costing (c) Batch Costing (d) Contract Costing 2. Which one of

Contract of Employment

Contract of Employment THIS Contract of Employment has been made between [name] [address] [city and postal code] [CVR number] (hereinafter "the Enterprise") and [name] [address] [city and postal code]

Contract of Employment THIS Contract of Employment has been made between [name] [address] [city and postal code] [CVR number] (hereinafter "the Enterprise") and [name] [address] [city and postal code]

Understanding Your Pay

Understanding Your Pay Providing you with an overview of your pay at the Deluxe family of companies This information provides an outline of our compensation programs and guidelines. It is not intended

Understanding Your Pay Providing you with an overview of your pay at the Deluxe family of companies This information provides an outline of our compensation programs and guidelines. It is not intended

Board and Committee Charters. The Gruden Group Limited

Board and Committee Charters The Gruden Group Limited The Gruden Group Limited (Gruden) ABN 56 125 943 240 Approved by the Board on 26 May 2016 Board Charter In carrying out the responsibilities and powers

Board and Committee Charters The Gruden Group Limited The Gruden Group Limited (Gruden) ABN 56 125 943 240 Approved by the Board on 26 May 2016 Board Charter In carrying out the responsibilities and powers

Before the South Dakota Public Utilities Commission of the State of South Dakota

Direct Testimony Laura A. Patterson Before the South Dakota Public Utilities Commission of the State of South Dakota In the Matter of the Application of Black Hills Power, Inc., a South Dakota Corporation

Direct Testimony Laura A. Patterson Before the South Dakota Public Utilities Commission of the State of South Dakota In the Matter of the Application of Black Hills Power, Inc., a South Dakota Corporation

Sickness Absence Policy

Sickness Absence Policy POLICY STATEMENT: This policy is intended to help provide appropriate support for Managers and employees to manage and monitor sickness. Absence has a direct and negative impact

Sickness Absence Policy POLICY STATEMENT: This policy is intended to help provide appropriate support for Managers and employees to manage and monitor sickness. Absence has a direct and negative impact

Fundamentals Level Skills Module, Paper F8. Section B

Answers Fundamentals Level Skills Module, Paper F8 Audit and Assurance September/December 2015 Answers Section B 1 Ethical threats and managing these risks (i) Ethical threat The finance director is the

Answers Fundamentals Level Skills Module, Paper F8 Audit and Assurance September/December 2015 Answers Section B 1 Ethical threats and managing these risks (i) Ethical threat The finance director is the

Classifications. Financial vs. Non-financial Direct vs Non-direct financial

Compensation The human resource management function that deals with every type of reward individuals receive in exchange for performing organisational tasks Major costs for organisations Classifications

Compensation The human resource management function that deals with every type of reward individuals receive in exchange for performing organisational tasks Major costs for organisations Classifications

APPENDIX 1. Ealing Council. Draft Work Related Injury/Illness Policy and Process 23/05/08

APPENDIX 1 Ealing Council Draft Work Related Injury/Illness Policy and Process 23/05/08 Work Related Injury/Illness Policy and Process Contents page 1 POLICY STATEMENT... 1 2 SCOPE... 1 3 DEFINITIONS...

APPENDIX 1 Ealing Council Draft Work Related Injury/Illness Policy and Process 23/05/08 Work Related Injury/Illness Policy and Process Contents page 1 POLICY STATEMENT... 1 2 SCOPE... 1 3 DEFINITIONS...

Remuneration and Nominations Committee Terms of Reference NOTE: THESE TERMS OF REFERENCE HAVE BEEN ALIGNED TO THE KING IV RECOMMENDATIONS.

Remuneration and Nominations Committee Terms of Reference NOTE: THESE TERMS OF REFERENCE HAVE BEEN ALIGNED TO THE KING IV RECOMMENDATIONS. August 2018 1. INTRODUCTION These Terms of Reference have been

Remuneration and Nominations Committee Terms of Reference NOTE: THESE TERMS OF REFERENCE HAVE BEEN ALIGNED TO THE KING IV RECOMMENDATIONS. August 2018 1. INTRODUCTION These Terms of Reference have been

EXEMPT VS. NON-EXEMPT Identifying Employee Classification

EXEMPT VS. NON-EXEMPT Identifying Employee Classification Employee Classification Keeping it all straight The comptroller of a small company notices that her accounting clerk works a lot of overtime. In

EXEMPT VS. NON-EXEMPT Identifying Employee Classification Employee Classification Keeping it all straight The comptroller of a small company notices that her accounting clerk works a lot of overtime. In

Report of the Director of Human Resources to the meeting of the Appointment Panel to be held on 10 November A

Report of the Director of Human Resources to the meeting of the Appointment Panel to be held on 10 November 2015. A Subject: Appointment process to the position of permanent City Solicitor. Summary Statement:

Report of the Director of Human Resources to the meeting of the Appointment Panel to be held on 10 November 2015. A Subject: Appointment process to the position of permanent City Solicitor. Summary Statement:

IDAHO STATE UNIVERSITY POLICIES AND PROCEDURES (ISUPP) Compensation of Employees ISUPP 3150

Compensation of Employees ISUPP 3150") IDAHO STATE UNIVERSITY POLICIES AND PROCEDURES (ISUPP) Compensation of Employees ISUPP 3150 POLICY INFORMATION Policy Section: Human Resources Policy Title: Compensation of Employees Responsible Executive

IDAHO STATE UNIVERSITY POLICIES AND PROCEDURES (ISUPP) Compensation of Employees ISUPP 3150 POLICY INFORMATION Policy Section: Human Resources Policy Title: Compensation of Employees Responsible Executive