2016 INSPECTION OF BHARAT PARIKH & ASSOCIATES CHARTERED ACCOUNTANTS. Preface

|

|

|

- Charity Cummings

- 6 years ago

- Views:

Transcription

1

2 2016 INSPECTION OF BHARAT PARIKH & ASSOCIATES CHARTERED ACCOUNTANTS Preface In 2016, the Public Company Accounting Oversight Board ("PCAOB" or "the Board") conducted an inspection of the registered public accounting firm Bharat Parikh & Associates ("the Firm") pursuant to the Sarbanes-Oxley Act of 2002 ("the Act"). Inspections are designed and performed to provide a basis for assessing the degree of compliance by a firm with applicable requirements related to issuer audit work. For a description of the procedures the Board's inspectors may perform to fulfill this responsibility, see Part I.C of this report (which also contains additional information concerning PCAOB inspections generally). The inspection included reviews of portions of two issuer audits performed by the Firm. These reviews were intended to identify whether deficiencies existed in the reviewed audit work, and whether such deficiencies indicated defects or potential defects in the Firm's system of quality control over audit work. In addition, the inspection included a review of policies and procedures related to certain quality control processes of the Firm that could be expected to affect audit quality. The Board is issuing this report in accordance with the requirements of the Act. The Board is releasing to the public Part I of the report and portions of Part IV of the report. Part IV of the report consists of the Firm's comments, if any, on a draft of the report. If the nonpublic portions of the report discuss criticisms of or potential defects in the firm's system of quality control, those discussions also could eventually be made public, but only to the extent the firm fails to address the criticisms to the Board's satisfaction within 12 months of the issuance of the report. Appendix A presents the text of the paragraphs of the auditing standards that are referenced in Part I.A. in relation to the description of auditing deficiencies there. Note on this report's citations to auditing standards: On March 31, 2015, the PCAOB adopted a reorganization of its auditing standards using a topical structure and a single, integrated numbering system. See Reorganization of PCAOB Auditing Standards and Related Amendments to PCAOB Standards and Rules, PCAOB Release No (Mar. 31, 2015). The reorganization will be effective as of December 31, 2016, but the reorganized numbering system may be used before that date. In this report, citations to PCAOB auditing standards use the numbering system and titles of

3 Page 2 standards that were in effect at the time of the primary inspection procedures. A table cross-referencing the section numbers of those standards included in Part I of this report as reorganized is included at Appendix B.

4 Page 3 PROFILE OF THE FIRM 1 Offices Ownership structure 5 (Ahmedabad, Mumbai, New Delhi, and Vadodara, Republic of India; and Plano, Texas) Partnership Partners / professional staff 2 8 /16 Issuer audit clients 2 Lead partners on issuer audit work 3 1 Other names used in audit reports Bharat Parikh & Associates 1 The information presented here is as understood by the inspection team, generally as of the outset of the inspection, based on the Firm's self-reporting and the inspection team's review of certain information. Additional information, including additional detail on audit reports issued by the Firm, is available in the Firm's filings with the Board, available at 2 The number of partners and professional staff is provided here as an indication of the size of the Firm, and does not necessarily represent the number of the Firm's professionals who participate in audits of issuers. The number of partners cited above represents the number of individuals with an ownership interest in the Firm. 3 The number of lead partners on issuer audit work represents the total number of Firm personnel (not necessarily limited to personnel with an ownership interest) who had primary responsibility for an issuer audit (as defined in AS No. 10, Supervision of the Audit Engagement) during the twelve-month period preceding the outset of the inspection.

5 Page 4 PART I INSPECTION PROCEDURES AND CERTAIN OBSERVATIONS Members of the Board's staff ("the inspection team") conducted primary procedures for the inspection from March 14, 2016 to March 18, A. Review of Audit Engagements The inspection procedures included a review of portions of two issuer audits performed by the Firm. The inspection team identified matters that it considered to be deficiencies in the performance of the work it reviewed. The descriptions of the deficiencies in Part I.A of this report include, at the end of the description of each deficiency, references to specific paragraphs of the auditing standards that relate to those deficiencies. The text of those paragraphs is set forth in Appendix A to this report. The references in this sub-part include only standards that primarily relate to the deficiencies; they do not present a comprehensive list of every auditing standard that applies to the deficiencies. Further, certain broadly applicable aspects of the auditing standards that may be relevant to a deficiency, such as provisions requiring due professional care, including the exercise of professional skepticism; the accumulation of sufficient appropriate audit evidence; and the performance of procedures that address risks, are not included in any references to the auditing standards in this sub-part, unless the lack of compliance with these standards is the primary reason for the deficiency. These broadly applicable provisions are described in Part I.B of this report. Certain deficiencies identified were of such significance that it appeared to the inspection team that the Firm, at the time it issued its audit report, had not obtained sufficient appropriate audit evidence to support its opinion that the financial statements were presented fairly, in all material respects, in accordance with the applicable 4 For this purpose, "primary procedures" include field work, other review of audit work papers, and the evaluation of the Firm's quality control policies and procedures through review of documentation and interviews of Firm personnel. Primary procedures do not include (1) inspection planning, which is performed prior to primary procedures, and (2) inspection follow-up procedures, wrap-up, analysis of results, and the preparation of the inspection report, which extend beyond the primary procedures.

6 Page 5 financial reporting framework. In other words, in these audits, the auditor issued an opinion without satisfying its fundamental obligation to obtain reasonable assurance about whether the financial statements were free of material misstatement. The fact that one or more deficiencies in an audit reach this level of significance does not necessarily indicate that the financial statements are materially misstated. It is often not possible for the inspection team, based only on the information available from the auditor, to reach a conclusion on those points. Whether or not associated with a disclosed financial reporting misstatement, an auditor's failure to obtain the reasonable assurance that the auditor is required to obtain is a serious matter. It is a failure to accomplish the essential purpose of the audit, and it means that, based on the audit work performed, the audit opinion should not have been issued. 5 The audit deficiencies that reached this level of significance are described below. Issuer A (1) the failure to perform sufficient procedures to test the occurrence and valuation of revenue (AS No. 14, paragraph 30); (2) the failure to perform sufficient procedures to test equity (AS No. 13, paragraph 8); and 5 Inclusion in an inspection report does not mean that the deficiency remained unaddressed after the inspection team brought it to the Firm's attention. Depending upon the circumstances, compliance with PCAOB standards may require the Firm to perform additional audit procedures, or to inform a client of the need for changes to its financial statements or reporting on internal control, or to take steps to prevent reliance on its previously expressed audit opinions. The Board expects that firms will comply with these standards, and an inspection may include a review of the adequacy of a firm's compliance with these requirements, either with respect to previously identified deficiencies or deficiencies identified during that inspection. Failure by a firm to take appropriate actions, or a firm's misrepresentations in responding to an inspection report, about whether it has taken such actions, could be a basis for Board disciplinary sanctions.

7 Page 6 Issuer B (3) the failure to perform sufficient procedures to test the existence of cash (AS No. 13, paragraph 8). (1) the failure to perform sufficient procedures to test the occurrence and valuation of revenue (AS No. 13, paragraphs 8 and 11; AS No. 15, paragraph 27); (2) the failure to perform sufficient procedures to test the existence of accounts receivable (AS No. 13, paragraphs 8 and 11; AU 330, paragraphs.34 and.35); and (3) the failure to perform sufficient procedures to test the existence and valuation of inventory (AS No. 13, paragraph 8; AU 331, paragraph.09; AU 342, paragraph.04). B. Auditing Standards Each deficiency described above could relate to several applicable provisions of the standards that govern the conduct of audit work. The paragraphs of the standards that are cited for each deficiency are those that most directly relate to the deficiency. The deficiencies also relate, however, to other paragraphs of those standards and to other auditing standards, including those concerning due professional care, responses to risk assessments, and audit evidence. Many audit deficiencies involve a lack of due professional care. AU 230, Due Professional Care in the Performance of Work, paragraphs.02,.05, and.06, requires the independent auditor to plan and perform his or her work with due professional care and sets forth aspects of that requirement. AU 230, paragraphs.07 through.09, and AS No. 13, The Auditor's Responses to the Risks of Material Misstatement, paragraph 7, specify that due professional care requires the exercise of professional skepticism. These standards state that professional skepticism is an attitude that includes a questioning mind and a critical assessment of the appropriateness and sufficiency of audit evidence. AS No. 13, paragraphs 3, 5, and 8, requires the auditor to design and implement audit responses that address the risks of material misstatement, and AS No. 15, Audit Evidence, paragraph 4, requires the auditor to plan and perform audit procedures to

8 Page 7 obtain sufficient appropriate audit evidence to provide a reasonable basis for the audit opinion. Sufficiency is the measure of the quantity of audit evidence, and the quantity needed is affected by the risk of material misstatement in the audit of financial statements and the quality of the audit evidence obtained. The appropriateness of evidence is measured by its quality; to be appropriate, evidence must be both relevant and reliable in providing support for the related conclusions. The paragraphs of the standards that are described immediately above are not cited in Part I.A, unless those paragraphs are the most directly related to the relevant deficiency. B.1. List of Specific Auditing Standards Referenced in Part I.A. The table below lists the specific auditing standards that are referenced in Part I.A of this report, cross-referenced to the issuer audits for which each standard is cited. PCAOB Auditing Standards AS No. 13, The Auditor's Responses to the Risks of Material Misstatement AS No. 14, Evaluating Audit Results AS No. 15, Audit Evidence AU 330, The Confirmation Process AU 331, Inventories AU 342, Auditing Accounting Estimates A and B A B B B B Issuers C. Information Concerning PCAOB Inspections that is Generally Applicable to Triennially Inspected Firms A Board inspection includes a review of certain portions of selected audit work performed by the inspected firm and a review of certain aspects of the firm's quality control system. The inspections are designed to identify deficiencies in audit work and

9 Page 8 defects or potential defects in the firm's system of quality control related to the firm's audit work. The focus on deficiencies, defects, and potential defects necessarily carries through to reports on inspections and, accordingly, Board inspection reports are not intended to serve as balanced report cards or overall rating tools. Further, the inclusion in an inspection report of certain deficiencies, defects, and potential defects should not be construed as an indication that the Board has made any determination about other aspects of the inspected firm's systems, policies, procedures, practices, or conduct not included within the report. C.1. Reviews of Audit Work Inspections include reviews of portions of selected audits of financial statements and, where applicable, audits of internal control over financial reporting ("ICFR"). For these audits, the inspection team selects certain portions of the audits for inspection, and it reviews the engagement team's work papers and interviews engagement personnel regarding those portions. If the inspection team identifies a potential issue that it is unable to resolve through discussion with the firm and any review of additional work papers or other documentation, the inspection team ordinarily provides the firm with a written comment form on the matter and the firm is allowed the opportunity to provide a written response to the comment form. If the response does not resolve the inspection team's concerns, the matter is considered a deficiency and is evaluated for inclusion in the inspection report. The inspection team selects the audits, and the specific portions of those audits, that it will review, and the inspected firm is not allowed an opportunity to limit or influence the selections. Audit deficiencies that the inspection team may identify include a firm's failure to identify, or to address appropriately, financial statement misstatements, including failures to comply with disclosure requirements, 6 as well as a 6 When it comes to the Board's attention that an issuer's financial statements appear not to present fairly, in a material respect, the financial position, results of operations, or cash flows of the issuer in conformity with the applicable financial reporting framework, the Board's practice is to report that information to the Securities and Exchange Commission ("SEC" or "the Commission"), which has jurisdiction to determine proper accounting in issuers' financial statements. Any description in this report of financial statement misstatements or failures to comply with SEC disclosure requirements should not be understood as an indication that the SEC has considered or made any determination regarding these issues unless otherwise expressly stated.

10 Page 9 firm's failure to perform, or to perform sufficiently, certain necessary audit procedures. An inspection may not involve the review of all of the firm's audit work, nor is it designed to identify every deficiency in the reviewed audits. Accordingly, a Board inspection report should not be understood to provide any assurance that a firm's audit work, or the relevant issuers' financial statements or reporting on ICFR, are free of any deficiencies not specifically described in an inspection report. In some cases, the conclusion that a firm did not perform a procedure may be based on the absence of documentation and the absence of persuasive other evidence, even if the firm claimed to have performed the procedure. AS No. 3, Audit Documentation, provides that, in various circumstances including PCAOB inspections, a firm that has not adequately documented that it performed a procedure, obtained evidence, or reached an appropriate conclusion must demonstrate with persuasive other evidence that it did so, and that oral assertions and explanations alone do not constitute persuasive other evidence. In reaching its conclusions, an inspection team considers whether audit documentation or any other evidence that a firm might provide to the inspection team supports the firm's contention that it performed a procedure, obtained evidence, or reached an appropriate conclusion. In the case of every matter cited in the public portion of a final inspection report, the inspection team has carefully considered any contention by the firm that it did so but just did not document its work, and the inspection team has concluded that the available evidence does not support the contention that the firm sufficiently performed the necessary work. Identified deficiencies in the audit work that exceed a significance threshold (which is described in Part I.A of the inspection report) are summarized in the public portion of the inspection report. 7 The Board cautions against extrapolating from the results presented in the public portion of a report to broader conclusions about the frequency of deficiencies throughout the firm's practice. Individual audit engagements and areas of inspection focus are most often selected on a risk-weighted basis and not randomly. Areas of 7 The discussion in this report of any deficiency observed in a particular audit engagement reflects information reported to the Board by the inspection team and does not reflect any determination by the Board as to whether the Firm has engaged in any conduct for which it could be sanctioned through the Board's disciplinary process. In addition, any references in this report to violations or potential violations of law, rules, or professional standards are not a result of an adversarial adjudicative process and do not constitute conclusive findings for purposes of imposing legal liability.

11 Page 10 focus vary among selected audit engagements, but often involve audit work on the most difficult or inherently uncertain areas of financial statements. Thus, the audit work is generally selected for inspection based on factors that, in the inspection team's view, heighten the possibility that auditing deficiencies are present, rather than through a process intended to identify a representative sample. C.2. Review of a Firm's Quality Control System QC 20, System of Quality Control for a CPA Firm's Accounting and Auditing Practice, provides that an auditing firm has a responsibility to ensure that its personnel comply with the applicable professional standards. This standard specifies that a firm's system of quality control should encompass the following elements: (1) independence, integrity, and objectivity; (2) personnel management; (3) acceptance and continuance of issuer audit engagements; (4) engagement performance; and (5) monitoring. The inspection team's assessment of a firm's quality control system is derived both from the results of its procedures specifically focused on the firm's quality control policies and procedures, and also from inferences that can be drawn from deficiencies in the performance of individual audit engagements. Audit deficiencies, whether alone or when aggregated, may indicate areas where a firm's system has failed to provide reasonable assurance of quality in the performance of audit work. Even deficiencies that do not result in an insufficiently supported audit opinion may indicate a defect or potential defect in a firm's quality control system. 8 If identified deficiencies, when accumulated and evaluated, indicate defects or potential defects in the firm's system of quality control, the nonpublic portion of this report would include a discussion of those issues. When evaluating whether identified deficiencies in individual audit engagements indicate a defect or potential defect in a firm's system of quality control, the inspection team considers the nature, significance, and frequency of deficiencies; 9 related firm methodology, guidance, and practices; and possible root causes. 8 Not every audit deficiency suggests a defect or potential defect in a firm's quality control system, and this report may not discuss every audit deficiency the inspection team identified. 9 An evaluation of the frequency of a type of deficiency may include consideration of how often the inspection team reviewed audit work that presented the opportunity for similar deficiencies to occur. In some cases, even a type of deficiency that is observed infrequently in a particular inspection may, because of some combination of its nature, its significance, and the frequency with which it has been

12 Page 11 Inspections also include a review of certain of the firm's practices, policies, and processes related to audit quality, which constitute a part of the firm's quality control system. This review addresses practices, policies, and procedures concerning audit performance, training, compliance with independence standards, client acceptance and retention, and the establishment of policies and procedures. END OF PART I observed in previous inspections of the firm, be cause for concern about a quality control defect or potential defect.

13 Page 12 PARTS II AND III OF THIS REPORT ARE NONPUBLIC AND ARE OMITTED FROM THIS PUBLIC DOCUMENT

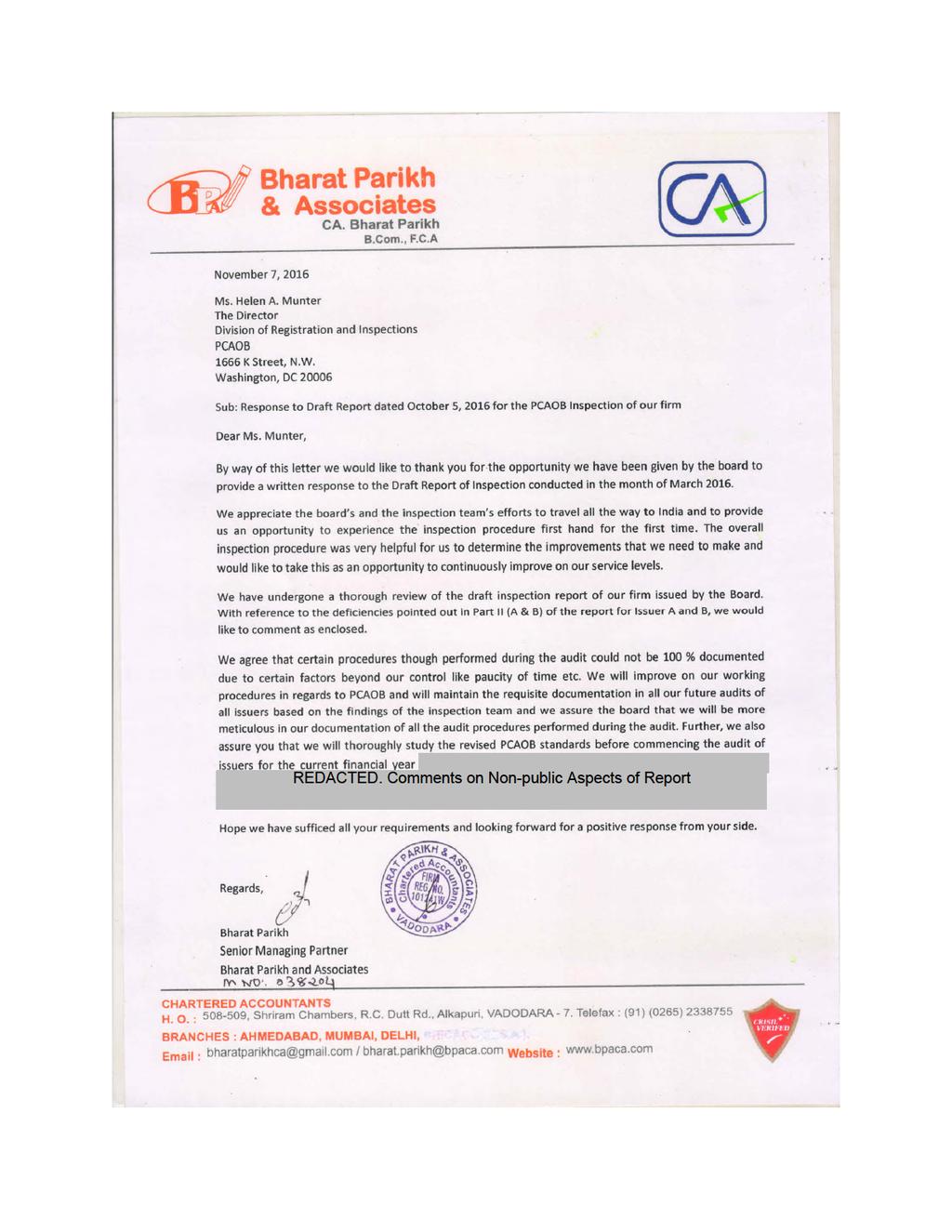

14 Page 13 PART IV RESPONSE OF THE FIRM TO DRAFT INSPECTION REPORT Pursuant to section 104(f) of the Act, 15 U.S.C. 7214(f), and PCAOB Rule 4007(a), the Firm provided a written response to a draft of this report. Pursuant to section 104(f) of the Act and PCAOB Rule 4007(b), the Firm's response, minus any portion granted confidential treatment, is attached hereto and made part of this final inspection report The Board does not make public any of a firm's comments that address a nonpublic portion of the report unless a firm specifically requests otherwise. In some cases, the result may be that none of a firm's response is made publicly available. In addition, pursuant to section 104(f) of the Act, 15 U.S.C. 7214(f), and PCAOB Rule 4007(b), if a firm requests, and the Board grants, confidential treatment for any of the firm's comments on a draft report, the Board does not include those comments in the final report at all. The Board routinely grants confidential treatment, if requested, for any portion of a firm's response that addresses any point in the draft that the Board omits from, or any inaccurate statement in the draft that the Board corrects in, the final report.

15

16 PCAOB Release No Page A-1 APPENDIX A AUDITING STANDARDS REFERENCED IN PART I.A This appendix provides the text of the auditing standard paragraphs that are referenced in Part I.A of this report. Footnotes that are included in this appendix, and any other Notes, are from the original auditing standards that are referenced. While this appendix contains the specific portions of the relevant standards cited with respect to the deficiencies in Part I.A of this report, other portions of the standards (including those described in Part I.B of this report) may provide additional context, descriptions, related requirements, or explanations; the complete standards are available on the PCAOB's website at AS No. 13, The Auditor's Responses to the Risks of Material Misstatement Responses Involving the Nature, Timing, and Extent of Audit Procedures AS No The auditor should design and perform audit procedures in a manner that addresses the assessed risks of material misstatement for each relevant assertion of each significant account and disclosure. Issuers A and B For significant risks, the auditor should perform substantive procedures, including tests of details, that are specifically responsive to the assessed risks. Issuer B RESPONSES TO SIGNIFICANT RISKS AS No Note: Auditing Standard No. 12 discusses identification of significant risks10/ and states that fraud risks are significant risks. Footnote to AS No / See paragraph 71 of Auditing Standard No. 12 for factors that the auditor should evaluate in determining which risks are significant risks.

17 PCAOB Release No Page A-2 AS No. 14, Evaluating Audit Results EVALUATING THE PRESENTATION OF THE FINANCIAL STATEMENTS, INCLUDING THE DISCLOSURES AS No The auditor must evaluate whether the financial statements are presented fairly, in all material respects, in conformity with the applicable financial reporting framework. Issuer A Note: AU sec. 411, The Meaning of Present Fairly in Conformity With Generally Accepted Accounting Principles, establishes requirements for evaluating the presentation of the financial statements. Auditing Standard No. 6, Evaluating Consistency of Financial Statements, establishes requirements regarding evaluating the consistency of the accounting principles used in financial statements. Note: The auditor should look to the requirements of the Securities and Exchange Commission for the company under audit with respect to the accounting principles applicable to that company. AS No. 15, Audit Evidence SELECTING SPECIFIC ITEMS AS No The application of audit procedures to items that are selected as described in paragraphs of this standard does not constitute audit sampling, and the results of those audit procedures cannot be projected to the entire population.12/ Issuer B Footnote to AS No / If misstatements are identified in the selected items, see paragraphs and paragraphs of Auditing Standard No. 14.

18 PCAOB Release No Page A-3 AU 330, The Confirmation Process Confirmation of Accounts Receivable AU For the purpose of this section, accounts receivable means a. The entity's claims against customers that have arisen from the sale of goods or services in the normal course of business, and b. Issuer B A financial institution's loans. Confirmation of accounts receivable is a generally accepted auditing procedure. As discussed in paragraph.06, it is generally presumed that evidence obtained from third parties will provide the auditor with higher-quality audit evidence than is typically available from within the entity. Thus, there is a presumption that the auditor will request the confirmation of accounts receivable during an audit unless one of the following is true: Accounts receivable are immaterial to the financial statements. The use of confirmations would be ineffective. fn 4 The auditor's combined assessed level of inherent and control risk is low, and the assessed level, in conjunction with the evidence expected to be provided by analytical procedures or other substantive tests of details, is sufficient to reduce audit risk to an acceptably low level for the applicable financial statement assertions. In many situations, both confirmation of accounts receivable and other substantive tests of details are necessary to reduce audit risk to an acceptably low level for the applicable financial statement assertions. Footnote to AU fn 4 For example, if, based on prior years' audit experience or on experience with similar engagements, the auditor concludes that response rates to properly designed confirmation requests will be inadequate, or if responses are known or expected to be unreliable, the auditor may determine that the use of confirmations would be ineffective. AU An auditor who has not requested confirmations in the examination of accounts receivable should document how he or she overcame this presumption. Issuer B

19 PCAOB Release No Page A-4 AU 331, Inventories Inventories AU When inventory quantities are determined solely by means of a physical count, and all counts are made as of the balance-sheet date or as of a single date within a reasonable time before or after the balance-sheet date, it is ordinarily necessary for the independent auditor to be present at the time of count and, by suitable observation, tests, and inquiries, satisfy himself respecting the effectiveness of the methods of inventory-taking and the measure of reliance which may be placed upon the client's representations about the quantities and physical condition of the inventories. Issuer B AU 342, Auditing Accounting Estimates AU The auditor is responsible for evaluating the reasonableness of accounting estimates made by management in the context of the financial statements taken as a whole. As estimates are based on subjective as well as objective factors, it may be difficult for management to establish controls over them. Even when management's estimation process involves competent personnel using relevant and reliable data, there is potential for bias in the subjective factors. Accordingly, when planning and performing procedures to evaluate accounting estimates, the auditor should consider, with an attitude of professional skepticism, both the subjective and objective factors. Issuer B

20 PCAOB Release No Page B-1 APPENDIX B REORGANIZED STANDARDS REFERENCED IN PART I.A On March 31, 2015, the PCAOB adopted the reorganization of its auditing standards using a topical structure and a single, integrated numbering system. See Reorganization of PCAOB Auditing Standards and Related Amendments to PCAOB Standards and Rules, PCAOB Release No (Mar. 31, 2015). On September 17, 2015, the SEC approved the PCAOB's adoption of the reorganization. The reorganized standards will be effective as of December 31, The citations to PCAOB auditing standards included in this report use the numbering system and titles of standards that were in effect at the time of the primary inspection procedures. This table provides the section numbers of those standards included in Part I of this report as reorganized, as well as the titles of the standards both before and after the reorganization. The complete standards are available on the PCAOB's website at Auditing Standards before the reorganization Audit Documentation AS No. 3 AS No. 13 The Auditor's Responses to the Risks of Material Misstatement AS No. 14 Evaluating Audit Results AS No. 15 Audit Evidence Due Professional Care in the AU 230 Performance of Work The Confirmation Process AU 330 Inventories AU 331 Auditing Accounting Estimates AU 342 Auditing Standards as reorganized AS 1215 AS 2301 AS 2810 AS 1105 AS 1015 AS 2310 AS 2510 AS 2501 Audit Documentation The Auditor's Responses to the Risks of Material Misstatement Evaluating Audit Results Audit Evidence Due Professional Care in the Performance of Work The Confirmation Process Auditing Inventories Auditing Accounting Estimates

Report on Inspection of KPMG Auditores Consultores Ltda. (Headquartered in Santiago, Republic of Chile)

") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Santiago, Republic of Chile) Issued by the Public Company Accounting

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Santiago, Republic of Chile) Issued by the Public Company Accounting

Report on Inspection of KPMG AG Wirtschaftspruefungsgesellschaft (Headquartered in Berlin, Federal Republic of Germany)

") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Berlin, Federal Republic of Germany) Issued by the Public Company

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Berlin, Federal Republic of Germany) Issued by the Public Company

Report on. Issued by the. Public Company Accounting Oversight Board. June 16, 2016 THIS IS A PUBLIC VERSION OF A PCAOB INSPECTION REPORT

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 Inspection of Paredes, Zaldívar, Burga & Asociados Sociedad Civil de (Headquartered

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 Inspection of Paredes, Zaldívar, Burga & Asociados Sociedad Civil de (Headquartered

Report on Inspection of Deloitte LLP (Headquartered in Toronto, Canada) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2014 (Headquartered in Toronto, Canada) Issued by the Public Company Accounting Oversight

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2014 (Headquartered in Toronto, Canada) Issued by the Public Company Accounting Oversight

Report on Inspection of K. R. Margetson Ltd. (Headquartered in Vancouver, Canada) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Vancouver, Canada) Issued by the Public Company Accounting

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Vancouver, Canada) Issued by the Public Company Accounting

Report on Inspection of KPMG SAS (Headquartered in Bogota, Republic of Colombia) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Bogota, Republic of Colombia) Issued by the Public Company

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Bogota, Republic of Colombia) Issued by the Public Company

Report on Inspection of Grant Thornton Auditores Independentes (Headquartered in Sao Paulo, Federative Republic of Brazil)

") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 Auditores Independentes (Headquartered in Sao Paulo, Federative Republic of Brazil)

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 Auditores Independentes (Headquartered in Sao Paulo, Federative Republic of Brazil)

Report on Inspection of Navarro Amper & Co. (Headquartered in Taguig City, Republic of the Philippines)

") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Taguig City, Republic of the Philippines) Issued by the Public

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Taguig City, Republic of the Philippines) Issued by the Public

Report on Inspection of KAP Purwantono, Sungkoro & Surja (Headquartered in Jakarta, Republic of Indonesia)

") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 Inspection of KAP Purwantono, (Headquartered in Jakarta, Republic of Indonesia)

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 Inspection of KAP Purwantono, (Headquartered in Jakarta, Republic of Indonesia)

Report on Inspection of KPMG Audit Limited (Headquartered in Hamilton, Bermuda) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Hamilton, Bermuda) Issued by the Public Company Accounting

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Hamilton, Bermuda) Issued by the Public Company Accounting

Report on Inspection of PricewaterhouseCoopers Audit (Headquartered in Neuilly-Sur-Seine, French Republic)

") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Neuilly-Sur-Seine, French Republic) Issued by the Public Company

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Neuilly-Sur-Seine, French Republic) Issued by the Public Company

Report on Inspection of KPMG (Headquartered in Sydney, Commonwealth of Australia) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2017 (Headquartered in Sydney, Commonwealth of Australia) Issued by the Public Company

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2017 (Headquartered in Sydney, Commonwealth of Australia) Issued by the Public Company

Report on Inspection of KPMG Cardenas Dosal, S.C. (Headquartered in Mexico City, United Mexican States)

") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Mexico City, United Mexican States) Issued by the Public Company

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Mexico City, United Mexican States) Issued by the Public Company

Report on Inspection of Deloitte & Associes (Headquartered in Neuilly-sur-Seine, French Republic) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Neuilly-sur-Seine, French Republic) Issued by the Public Company

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Neuilly-sur-Seine, French Republic) Issued by the Public Company

Report on Inspection of BDO LLP (Headquartered in Singapore, Republic of Singapore) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2018 (Headquartered in Singapore, Republic of Singapore) Issued by the Public Company

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2018 (Headquartered in Singapore, Republic of Singapore) Issued by the Public Company

Report on Inspection of Deloitte, S.L. (Headquartered in Madrid, Kingdom of Spain) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Madrid, Kingdom of Spain) Issued by the Public Company Accounting

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Madrid, Kingdom of Spain) Issued by the Public Company Accounting

2013 INSPECTION OF GEORGE STEWART, CPA

2013 INSPECTION OF GEORGE STEWART, CPA In 2013, the Public Company Accounting Oversight Board ("PCAOB" or "the Board") conducted an inspection of the registered public accounting firm George Stewart, CPA

2013 INSPECTION OF GEORGE STEWART, CPA In 2013, the Public Company Accounting Oversight Board ("PCAOB" or "the Board") conducted an inspection of the registered public accounting firm George Stewart, CPA

Report on Inspection of Ernst & Young Accountants LLP (Headquartered in Rotterdam, Kingdom of the Netherlands)

") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Rotterdam, Kingdom of the Netherlands) Issued by the Public

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Rotterdam, Kingdom of the Netherlands) Issued by the Public

Report on Inspection of Ernst & Young Accountants LLP (Headquartered in Rotterdam, Kingdom of The Netherlands)

") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2013 (Headquartered in Rotterdam, Kingdom of The Netherlands) Issued by the Public

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2013 (Headquartered in Rotterdam, Kingdom of The Netherlands) Issued by the Public

Report on Inspection of Crowe Horwath LLP (Headquartered in Chicago, Illinois) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Chicago, Illinois) Issued by the Public Company Accounting

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Chicago, Illinois) Issued by the Public Company Accounting

2013 INSPECTION OF ENTERPRISE CPAS, LTD.

2013 INSPECTION OF ENTERPRISE CPAS, LTD. In 2013, the Public Company Accounting Oversight Board ("PCAOB" or "the Board") conducted an inspection of the registered public accounting firm Enterprise CPAs,

2013 INSPECTION OF ENTERPRISE CPAS, LTD. In 2013, the Public Company Accounting Oversight Board ("PCAOB" or "the Board") conducted an inspection of the registered public accounting firm Enterprise CPAs,

Report on Inspection of KPMG AZSA LLC (Headquartered in Tokyo, Japan) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2013 (Headquartered in Tokyo, Japan) Issued by the Public Company Accounting Oversight

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2013 (Headquartered in Tokyo, Japan) Issued by the Public Company Accounting Oversight

Inspection of Petrie Raymond, Chartered Accountants L.L.P. (Headquartered in Montreal, Canada) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Inspection of Petrie Raymond, Chartered Accountants L.L.P. (Headquartered in Montreal, Canada)

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Inspection of Petrie Raymond, Chartered Accountants L.L.P. (Headquartered in Montreal, Canada)

Public Company Accounting Oversight Board

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2008 (Headquartered in New York, New York) Issued by the Public Company Accounting

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2008 (Headquartered in New York, New York) Issued by the Public Company Accounting

Special Inspection of Seale and Beers, CPAs, LLC (Headquartered in Las Vegas, Nevada) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org (Headquartered in Las Vegas, Nevada) Issued by the Public Company Accounting Oversight Board

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org (Headquartered in Las Vegas, Nevada) Issued by the Public Company Accounting Oversight Board

Inspection of HJ & Associates, LLC (Headquartered in Salt Lake City, Utah) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Inspection of HJ & Associates, LLC (Headquartered in Salt Lake City, Utah) Issued by the Public

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Inspection of HJ & Associates, LLC (Headquartered in Salt Lake City, Utah) Issued by the Public

PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD ) ) In the Matter of ) PCAOB Release No.104-2013-087

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD ) ) In the Matter of ) PCAOB Release No.104-2013-087

An Audit of Internal Control Over Financial Reporting Performed in Conjunction with An Audit of Financial Statements

AUDITING STANDARD No. 2 An Audit of Internal Control Over Financial Reporting Performed in Conjunction with An Audit of Financial Statements March 9, 2004 AUDITING AND RELATED PROFESSIONAL PRACTICE STANDARDS

AUDITING STANDARD No. 2 An Audit of Internal Control Over Financial Reporting Performed in Conjunction with An Audit of Financial Statements March 9, 2004 AUDITING AND RELATED PROFESSIONAL PRACTICE STANDARDS

An Audit of Internal Control Over Financial Reporting Performed in Conjunction with An Audit of Financial Statements

Page A 1 Standard Appendix Auditing Standard No. 2 AUDITING AND RELATED PROFESSIONAL PRACTICE STANDARDS Auditing Standard No. 2 An Audit of Internal Control Over Financial Reporting Performed in Conjunction

Page A 1 Standard Appendix Auditing Standard No. 2 AUDITING AND RELATED PROFESSIONAL PRACTICE STANDARDS Auditing Standard No. 2 An Audit of Internal Control Over Financial Reporting Performed in Conjunction

Special Considerations Audits of Group Financial Statements (Including the Work of Component Auditors)

") Special Considerations---Audits of Group Financial Statements 665 AU-C Section 600 Special Considerations Audits of Group Financial Statements (Including the Work of Component Auditors) Source: SAS No.

Special Considerations---Audits of Group Financial Statements 665 AU-C Section 600 Special Considerations Audits of Group Financial Statements (Including the Work of Component Auditors) Source: SAS No.

SRI LANKA AUDITING STANDARD 600 SPECIAL CONSIDERATIONS AUDITS OF GROUP FINANCIAL STATEMENTS (INCLUDING THE WORK OF COMPONENT AUDITORS) CONTENTS

CONTENTS") SRI LANKA AUDITING STANDARD 600 SPECIAL CONSIDERATIONS AUDITS OF GROUP FINANCIAL STATEMENTS (INCLUDING THE WORK OF COMPONENT AUDITORS) (Effective for audits of group financial statements for periods beginning

SRI LANKA AUDITING STANDARD 600 SPECIAL CONSIDERATIONS AUDITS OF GROUP FINANCIAL STATEMENTS (INCLUDING THE WORK OF COMPONENT AUDITORS) (Effective for audits of group financial statements for periods beginning

INTERNATIONAL STANDARD ON AUDITING 500 AUDIT EVIDENCE CONTENTS

INTERNATIONAL STANDARD ON 500 AUDIT EVIDENCE (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph Introduction... 1-2 Concept of Audit Evidence...

INTERNATIONAL STANDARD ON 500 AUDIT EVIDENCE (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph Introduction... 1-2 Concept of Audit Evidence...

STANDING ADVISORY GROUP MEETING

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org STANDING ADVISORY GROUP MEETING CONSIDERATION OF OUTREACH AND RESEARCH REGARDING THE AUDITOR'S

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org STANDING ADVISORY GROUP MEETING CONSIDERATION OF OUTREACH AND RESEARCH REGARDING THE AUDITOR'S

Auditing & Assurance Services, 7e (Louwers) Chapter 2 Professional Standards

Chapter 2 Professional Standards") Auditing & Assurance Services, 7e (Louwers) Chapter 2 Professional Standards 1) Control risk is A) the probability that a material misstatement could not be prevented or detected by the entity's internal

Auditing & Assurance Services, 7e (Louwers) Chapter 2 Professional Standards 1) Control risk is A) the probability that a material misstatement could not be prevented or detected by the entity's internal

Mapping Document AU Section 322 to Clarified Statement on Auditing Standards Using the Work of Internal Auditors

1 MAPPING DOCUMENT CLARIFIED STATEMENT ON AUDITING STANDARDS USING THE WORK OF INTERNAL AUDITORS This mapping document demonstrates how the material in extant AU section 322, The Auditor s Consideration

1 MAPPING DOCUMENT CLARIFIED STATEMENT ON AUDITING STANDARDS USING THE WORK OF INTERNAL AUDITORS This mapping document demonstrates how the material in extant AU section 322, The Auditor s Consideration

Audit & Assurance Update January 16, In This Issue. Background. Background. Key Provisions of the Estimates Standard

Audit & Assurance Update January 16, 2019 In This Issue Background Key Provisions of the Specialist Amendments Key Provisions of the Estimates Standard Applicability and Effective Date Comparison with

Audit & Assurance Update January 16, 2019 In This Issue Background Key Provisions of the Specialist Amendments Key Provisions of the Estimates Standard Applicability and Effective Date Comparison with

Audit Evidence. ISA 500 Issued December International Standard on Auditing

Issued December 2007 International Standard on Auditing Audit Evidence The Malaysian Institute of Certified Public Accountants (Institut Akauntan Awam Bertauliah Malaysia) INTERNATIONAL STANDARD ON AUDITING

Issued December 2007 International Standard on Auditing Audit Evidence The Malaysian Institute of Certified Public Accountants (Institut Akauntan Awam Bertauliah Malaysia) INTERNATIONAL STANDARD ON AUDITING

Auditing and Assurance Standards Council

Auditing and Assurance Standards Council Philippine Standard on Auditing 600 (Revised and Redrafted) SPECIAL CONSIDERATIONS AUDITS OF GROUP FINANCIAL STATEMENTS (INCLUDING THE WORK OF COMPONENT AUDITORS)

Auditing and Assurance Standards Council Philippine Standard on Auditing 600 (Revised and Redrafted) SPECIAL CONSIDERATIONS AUDITS OF GROUP FINANCIAL STATEMENTS (INCLUDING THE WORK OF COMPONENT AUDITORS)

Chapter 18. Integrated Audits of Public Companies. McGraw-Hill/Irwin. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 18 Integrated Audits of Public Companies McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Nature of an Integrated Audit Auditors of public companies should

Chapter 18 Integrated Audits of Public Companies McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Nature of an Integrated Audit Auditors of public companies should

The Auditor s Consideration of the Internal Audit Function in an Audit of Financial Statements

Auditor s Consideration of Internal Audit Function 381 AU Section 322 The Auditor s Consideration of the Internal Audit Function in an Audit of Financial Statements (Supersedes SAS No. 9) Source: SAS No.

Auditor s Consideration of Internal Audit Function 381 AU Section 322 The Auditor s Consideration of the Internal Audit Function in an Audit of Financial Statements (Supersedes SAS No. 9) Source: SAS No.

THE AUDITOR S RESPONSIBILITIES AND FUNCTIONS, INTRODUCTION TO GAAS, AND THE GENERAL STANDARDS (INCLUDING THE QUALITY CONTROL STANDARDS)

") 100-230 THE AUDITOR S RESPONSIBILITIES AND FUNCTIONS, INTRODUCTION TO GAAS, AND THE GENERAL STANDARDS (INCLUDING THE QUALITY CONTROL STANDARDS) EFFECTIVE DATE AND APPLICABILITY Original Pronouncements

100-230 THE AUDITOR S RESPONSIBILITIES AND FUNCTIONS, INTRODUCTION TO GAAS, AND THE GENERAL STANDARDS (INCLUDING THE QUALITY CONTROL STANDARDS) EFFECTIVE DATE AND APPLICABILITY Original Pronouncements

Auditing Standard 16

Certified Sarbanes-Oxley Expert Official Prep Course Part K Sarbanes Oxley Compliance Professionals Association (SOXCPA) The largest association of Sarbanes Oxley Professionals in the world Auditing Standard

Certified Sarbanes-Oxley Expert Official Prep Course Part K Sarbanes Oxley Compliance Professionals Association (SOXCPA) The largest association of Sarbanes Oxley Professionals in the world Auditing Standard

1. Auditors may be independent in fact but not independent in appearance. 3. Attestation standards provide guidance for a wide variety of engagements

Chapter 02 Professional Standards True / False Questions 1. Auditors may be independent in fact but not independent in appearance. True False 2. Auditing Standards issued by the PCAOB are the sole source

Chapter 02 Professional Standards True / False Questions 1. Auditors may be independent in fact but not independent in appearance. True False 2. Auditing Standards issued by the PCAOB are the sole source

Auditing Standards and Practices Council

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 330 THE AUDITOR S PROCEDURES IN RESPONSE TO ASSESSED RISKS PHILIPPINE STANDARD ON AUDITING 330 THE AUDITOR S PROCEDURES IN RESPONSE

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 330 THE AUDITOR S PROCEDURES IN RESPONSE TO ASSESSED RISKS PHILIPPINE STANDARD ON AUDITING 330 THE AUDITOR S PROCEDURES IN RESPONSE

Chapter 02. Professional Standards. Multiple Choice Questions. 1. Control risk is

Chapter 02 Professional Standards Multiple Choice Questions 1. Control risk is A. the probability that a material misstatement could not be prevented or detected by the entity's internal control policies

Chapter 02 Professional Standards Multiple Choice Questions 1. Control risk is A. the probability that a material misstatement could not be prevented or detected by the entity's internal control policies

STATEMENT OF AUDITING STANDARDS 500 AUDIT EVIDENCE

STATEMENT OF AUDITING STANDARDS 500 AUDIT EVIDENCE (Issued January 2004) Contents Paragraphs Introduction 1-2 Concept of Audit Evidence 3-6 Sufficient Appropriate Audit Evidence 7-14 The Use of Assertions

STATEMENT OF AUDITING STANDARDS 500 AUDIT EVIDENCE (Issued January 2004) Contents Paragraphs Introduction 1-2 Concept of Audit Evidence 3-6 Sufficient Appropriate Audit Evidence 7-14 The Use of Assertions

AGS 10. Joint Audits AUDIT GUIDANCE STATEMENT

AUDIT GUIDANCE STATEMENT AGS 10 Joint Audits AGS 10 Joint Audits was approved by the Council of the Institute of Singapore Chartered Accountants (formerly known as Institute of Certified Public Accountants

AUDIT GUIDANCE STATEMENT AGS 10 Joint Audits AGS 10 Joint Audits was approved by the Council of the Institute of Singapore Chartered Accountants (formerly known as Institute of Certified Public Accountants

CLIENT ALERT: INTERNAL CONTROL OVER FINANCIAL REPORTING

CLIENT ALERT: INTERNAL CONTROL OVER FINANCIAL REPORTING All public companies either have begun or will soon begin a process, required under Section 404 of the Sarbanes-Oxley Act of 2002 ( SOX ), of reviewing

CLIENT ALERT: INTERNAL CONTROL OVER FINANCIAL REPORTING All public companies either have begun or will soon begin a process, required under Section 404 of the Sarbanes-Oxley Act of 2002 ( SOX ), of reviewing

Mapping of Original ISA 315 to New ISA 315 s Standards and Application Material (AM) Agenda Item 2-C

Agenda Item 2-C") Mapping of to 315 s and Application Material (AM) Agenda Item 2-C AM 1. The purpose of this International Standard on Auditing (ISA) is to establish standards and to provide guidance on obtaining an understanding

Mapping of to 315 s and Application Material (AM) Agenda Item 2-C AM 1. The purpose of this International Standard on Auditing (ISA) is to establish standards and to provide guidance on obtaining an understanding

Audit programs that can be easily tailored to address the risks associated with your individual

Checkpoint Contents Accounting, Audit & Corporate Finance Library Editorial Materials Audit and Attest Audits of Nonpublic Companies Chapter 1 Introduction and Overview 100 Introduction 100 Introduction

Checkpoint Contents Accounting, Audit & Corporate Finance Library Editorial Materials Audit and Attest Audits of Nonpublic Companies Chapter 1 Introduction and Overview 100 Introduction 100 Introduction

AGS 10. Joint Audits AUDIT GUIDANCE STATEMENT

AUDIT GUIDANCE STATEMENT AGS 10 Joint Audits This Audit Guidance Statement was approved by the Council of the Institute of Singapore Chartered Accountants (formerly known as Institute of Certified Public

AUDIT GUIDANCE STATEMENT AGS 10 Joint Audits This Audit Guidance Statement was approved by the Council of the Institute of Singapore Chartered Accountants (formerly known as Institute of Certified Public

IAASB Main Agenda (December 2004) Page Agenda Item

Page Agenda Item") IAASB Main Agenda (December 2004) Page 2004 2159 Agenda Item 7-B PROPOSED INTERNATIONAL STANDARD ON AUDITING XXX THE AUDIT OF GROUP FINANCIAL STATEMENTS CONTENTS Paragraph Introduction... 1-3 Definitions...

IAASB Main Agenda (December 2004) Page 2004 2159 Agenda Item 7-B PROPOSED INTERNATIONAL STANDARD ON AUDITING XXX THE AUDIT OF GROUP FINANCIAL STATEMENTS CONTENTS Paragraph Introduction... 1-3 Definitions...

2. The auditors' report on a corporation's financial statements usually is addressed to the president of the company.

Chapter 02 Professional Standards True / False Questions 1. To express an opinion on financial statements, the auditor obtains reasonable assurance about whether the financial statements as a whole are

Chapter 02 Professional Standards True / False Questions 1. To express an opinion on financial statements, the auditor obtains reasonable assurance about whether the financial statements as a whole are

Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement

Issued December 2007 International Standard on Auditing Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement The Malaysian Institute of Certified Public Accountants

Issued December 2007 International Standard on Auditing Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement The Malaysian Institute of Certified Public Accountants

February 23, Office of the Secretary Public Company Accounting Oversight Board 1666 K Street, N.W. Washington, D.C.

McGladrey & Pullen LLP Third Floor 3600 American Blvd West Bloomington, MN 55431 O 952.835.9930 February 23, 2007 Office of the Secretary Public Company Accounting Oversight Board 1666 K Street, N.W. Washington,

McGladrey & Pullen LLP Third Floor 3600 American Blvd West Bloomington, MN 55431 O 952.835.9930 February 23, 2007 Office of the Secretary Public Company Accounting Oversight Board 1666 K Street, N.W. Washington,

Chapter 02. Professional Standards. McGraw-Hill/Irwin. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 02 Professional Standards McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Authority of Organizations Public Company Accounting Oversight Board Auditing,

Chapter 02 Professional Standards McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Authority of Organizations Public Company Accounting Oversight Board Auditing,

STAFF QUESTIONS AND ANSWERS

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org STAFF QUESTIONS AND ANSWERS AUDITING INTERNAL CONTROL OVER FINANCIAL REPORTING Summary: Staff

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org STAFF QUESTIONS AND ANSWERS AUDITING INTERNAL CONTROL OVER FINANCIAL REPORTING Summary: Staff

Statements. This Standard is effective for reviews of financial statements for periods ending on or after 31 December 2013.

SINGAPORE STANDARD ON REVIEW ENGAGEMENTS SSRE 2400 (Revised) Engagements to Review Historical Financial Statements This revised Singapore Standard on Review Engagements (SSRE) 2400 supersedes SSRE 2400

SINGAPORE STANDARD ON REVIEW ENGAGEMENTS SSRE 2400 (Revised) Engagements to Review Historical Financial Statements This revised Singapore Standard on Review Engagements (SSRE) 2400 supersedes SSRE 2400

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT CONTENTS

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT (Effective for audits of financial statements for periods beginning

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT (Effective for audits of financial statements for periods beginning

General Principles for Engagements Performed in Accordance With Statements on Standards for Accounting and Review Services

General Principles for Engagements 2115 AR-C Section 60 General Principles for Engagements Performed in Accordance With Statements on Standards for Accounting and Review Services Source: SSARS No. 21;

General Principles for Engagements 2115 AR-C Section 60 General Principles for Engagements Performed in Accordance With Statements on Standards for Accounting and Review Services Source: SSARS No. 21;

STANDING ADVISORY GROUP MEETING

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202)862-8430 www.pcaobus.org PROPOSAL TO RECONSIDER THE HIERARCHY OF AUDITING STANDARDS AND GUIDANCE NOVEMBER 17-18, 2004

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202)862-8430 www.pcaobus.org PROPOSAL TO RECONSIDER THE HIERARCHY OF AUDITING STANDARDS AND GUIDANCE NOVEMBER 17-18, 2004

INTERNATIONAL STANDARD ON AUDITING 402 AUDIT CONSIDERATIONS RELATING TO ENTITIES USING SERVICE ORGANIZATIONS CONTENTS

INTERNATIONAL STANDARD ON 402 AUDIT CONSIDERATIONS RELATING TO ENTITIES (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph Introduction...

INTERNATIONAL STANDARD ON 402 AUDIT CONSIDERATIONS RELATING TO ENTITIES (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph Introduction...

Auditing Standards and Practices Council

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT PHILIPPINE STANDARD ON AUDITING

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT PHILIPPINE STANDARD ON AUDITING

Government Auditing Standards

United States Government Accountability Office GAO By the Comptroller General of the United States August 2011 Government Auditing Standards 2011 Internet Version CONTENTS CHAPTER 1... 1 GOVERNMENT AUDITING:

United States Government Accountability Office GAO By the Comptroller General of the United States August 2011 Government Auditing Standards 2011 Internet Version CONTENTS CHAPTER 1... 1 GOVERNMENT AUDITING:

International Standard on Auditing (UK) 600 (Revised June 2016)

600 (Revised June 2016)") Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 600 (Revised June 2016) Special Considerations Audits of Group Financial Statements (Including

Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 600 (Revised June 2016) Special Considerations Audits of Group Financial Statements (Including

ASB Meeting January 12-15, 2015

ASB Meeting January 12-15, 2015 Agenda Item 3A Chapter 1, Concepts Common to All Attestation Engagements, of Attestation Standards: Clarification and Recodification Introduction 1.1 This chapter of Statements

ASB Meeting January 12-15, 2015 Agenda Item 3A Chapter 1, Concepts Common to All Attestation Engagements, of Attestation Standards: Clarification and Recodification Introduction 1.1 This chapter of Statements

IAASB Main Agenda (September 2004) Page Agenda Item PROPOSED REVISED INTERNATIONAL STANDARD ON AUDITING 540

Page Agenda Item PROPOSED REVISED INTERNATIONAL STANDARD ON AUDITING 540") IAASB Main Agenda (September 2004) Page 2004 1651 Agenda Item 4-A PROPOSED REVISED INTERNATIONAL STANDARD ON AUDITING 540 AUDITING ACCOUNTING ESTIMATES AND RELATED DISCLOSURES (EXCLUDING THOSE INVOLVING

IAASB Main Agenda (September 2004) Page 2004 1651 Agenda Item 4-A PROPOSED REVISED INTERNATIONAL STANDARD ON AUDITING 540 AUDITING ACCOUNTING ESTIMATES AND RELATED DISCLOSURES (EXCLUDING THOSE INVOLVING

covered member immediate family impaired not a covered member close relative not impaired

BUS 425 Auditing Tad Miller May 22, 2017 Audit Planning, Analytical Procedures, Materiality & Risk, Internal Control Evaluation and Audit Plan 1. INDEPENDENCE All independence problems refer to a client

BUS 425 Auditing Tad Miller May 22, 2017 Audit Planning, Analytical Procedures, Materiality & Risk, Internal Control Evaluation and Audit Plan 1. INDEPENDENCE All independence problems refer to a client

Via

Grant Thornton International Barry Barber Worldwide Director of Audit and Risk Management 399 Thornall Street Edison, New Jersey 08837 732-516-5500 732-516-5550 Direct 732-516-5502 Fax email barry.barber@gt.com

Grant Thornton International Barry Barber Worldwide Director of Audit and Risk Management 399 Thornall Street Edison, New Jersey 08837 732-516-5500 732-516-5550 Direct 732-516-5502 Fax email barry.barber@gt.com

Navigating the PCAOB s and SEC s internal control expectations A discussion. June 2015

Navigating the PCAOB s and SEC s internal control expectations A discussion June 2015 Setting the scene ICFR guidance: PCAOB Auditing Standard No. 5 (May 2007) PCAOB staff views: An Audit of Internal Control

Navigating the PCAOB s and SEC s internal control expectations A discussion June 2015 Setting the scene ICFR guidance: PCAOB Auditing Standard No. 5 (May 2007) PCAOB staff views: An Audit of Internal Control

IAASB Main Agenda (March 2016) Agenda Item. Initial Discussion on the IAASB s Future Project Related to ISA 315 (Revised) 1

Agenda Item. Initial Discussion on the IAASB s Future Project Related to ISA 315 (Revised) 1") Agenda Item 3-A Initial Discussion on the IAASB s Future Project Related to ISA 315 (Revised) 1 Objectives of the IAASB Discussion The objective of this agenda item are to: (a) Present initial background

Agenda Item 3-A Initial Discussion on the IAASB s Future Project Related to ISA 315 (Revised) 1 Objectives of the IAASB Discussion The objective of this agenda item are to: (a) Present initial background

AN AUDIT OF INTERNAL CONTROL THAT IS INTEGRATED WITH AN AUDIT OF FINANCIAL STATEMENTS: GUIDANCE FOR AUDITORS OF SMALLER PUBLIC COMPANIES

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org PRELIMINARY STAFF VIEWS AN AUDIT OF INTERNAL CONTROL THAT IS INTEGRATED WITH AN AUDIT OF FINANCIAL

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org PRELIMINARY STAFF VIEWS AN AUDIT OF INTERNAL CONTROL THAT IS INTEGRATED WITH AN AUDIT OF FINANCIAL

IAASB CAG Public Session (March 2018) CONFORMING AND CONSEQUENTIAL AMENDMENTS ARISING FROM DRAFT PROPOSED ISA 540 (REVISED) 1

CONFORMING AND CONSEQUENTIAL AMENDMENTS ARISING FROM DRAFT PROPOSED ISA 540 (REVISED) 1") Agenda Item B.4 CONFORMING AND CONSEQUENTIAL AMENDMENTS ARISING FROM DRAFT PROPOSED ISA 540 (REVISED) 1 ISA 200, Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance

Agenda Item B.4 CONFORMING AND CONSEQUENTIAL AMENDMENTS ARISING FROM DRAFT PROPOSED ISA 540 (REVISED) 1 ISA 200, Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance

Checkpoint Contents Accounting, Audit & Corporate Finance Library Editorial Materials Audit and Attest PCAOB Audits Chapter 1 Overview 100 Background

Checkpoint Contents Accounting, Audit & Corporate Finance Library Editorial Materials Audit and Attest PCAOB Audits Chapter 1 Overview 100 Background 100 Background 100.1 For many years, auditors had traditionally

Checkpoint Contents Accounting, Audit & Corporate Finance Library Editorial Materials Audit and Attest PCAOB Audits Chapter 1 Overview 100 Background 100 Background 100.1 For many years, auditors had traditionally

Evaluating Internal Controls

A SSURANCE AND A DVISORY BUSINESS S ERVICES Fourth in the Series!@# Evaluating Internal Controls Evaluating Overall Effectiveness, Identifying Matters for Improvement, and Ongoing Assessment of Controls

A SSURANCE AND A DVISORY BUSINESS S ERVICES Fourth in the Series!@# Evaluating Internal Controls Evaluating Overall Effectiveness, Identifying Matters for Improvement, and Ongoing Assessment of Controls

Re: Proposed Statement on Standards for Attestation Engagements, Attestation Standards: Clarification and Recodification

Deloitte & Touche LLP Ten Westport Road PO Box 820 Wilton, CT 06897-0820 Tel: +1 203 761 3000 Fax: +1 203 834 2200 www.deloitte.com Ms. Sherry Hazel American Institute of Certified Public Accountants 1211

Deloitte & Touche LLP Ten Westport Road PO Box 820 Wilton, CT 06897-0820 Tel: +1 203 761 3000 Fax: +1 203 834 2200 www.deloitte.com Ms. Sherry Hazel American Institute of Certified Public Accountants 1211

CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a. AUDITING THEORY Risk Assessment and Response to Assessed Risks

Page 1 of 7 CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a Related PSAs: PSA 400, 315 and 330 AUDITING THEORY Risk Assessment and Response to Assessed Risks 1. Which of the following is correct statement?

Page 1 of 7 CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a Related PSAs: PSA 400, 315 and 330 AUDITING THEORY Risk Assessment and Response to Assessed Risks 1. Which of the following is correct statement?

Compilation Engagements

SINGAPORE STANDARD ON RELATED SERVICES SSRS 4410 (REVISED) Compilation Engagements This revised Singapore Standard on Related Services (SSRS) 4410 supersedes SSRS 4410 Engagements to Compile Financial

SINGAPORE STANDARD ON RELATED SERVICES SSRS 4410 (REVISED) Compilation Engagements This revised Singapore Standard on Related Services (SSRS) 4410 supersedes SSRS 4410 Engagements to Compile Financial

Audit programs that can be easily tailored to address the risks associated with your individual audit engagements. 2

Checkpoint Contents Accounting, Audit & Corporate Finance Library Editorial Materials Audit and Attest Audits of Nonpublic Companies Chapter 1 Introduction and Overview 100 Introduction 100 Introduction

Checkpoint Contents Accounting, Audit & Corporate Finance Library Editorial Materials Audit and Attest Audits of Nonpublic Companies Chapter 1 Introduction and Overview 100 Introduction 100 Introduction

Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity and Its Environment

ISA 315 (Revised) Issued September 2012; updated February 2018 International Standard on Auditing Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity and Its Environment

ISA 315 (Revised) Issued September 2012; updated February 2018 International Standard on Auditing Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity and Its Environment

Comments to be received by 30 June 2005

4 April 2005 To: Members of the Hong Kong Institute of CPAs All other interested parties INVITATION TO COMMENT ON IAASB EXPOSURE DRAFTS OF PROPOSED ISA 600 (REVISED) THE AUDIT OF GROUP FINANCIAL STATEMENTS

4 April 2005 To: Members of the Hong Kong Institute of CPAs All other interested parties INVITATION TO COMMENT ON IAASB EXPOSURE DRAFTS OF PROPOSED ISA 600 (REVISED) THE AUDIT OF GROUP FINANCIAL STATEMENTS

Comparison of the PCAOB s Auditing Standards No. 5 and No. 2 (Certain key differences are highlighted by underlining)

") Comparison of the PCAOB s Auditing Standards No. 5 and No. 2 (Certain key differences are highlighted by underlining) Topic AS No. 5 AS No. 2 Objective of ICFR Audit Planning the ICFR Audit Integration

Comparison of the PCAOB s Auditing Standards No. 5 and No. 2 (Certain key differences are highlighted by underlining) Topic AS No. 5 AS No. 2 Objective of ICFR Audit Planning the ICFR Audit Integration

up Texas Society of ~ Certified Public Accountants

up Texas Society of ~ Certified Public Accountants Office of the Secretary 1666 K Street, N.W. Washington, D.C. 20006-2803 RE: Proposed Auditing Standard An Audit of Internal Control Over Financial Reporting

up Texas Society of ~ Certified Public Accountants Office of the Secretary 1666 K Street, N.W. Washington, D.C. 20006-2803 RE: Proposed Auditing Standard An Audit of Internal Control Over Financial Reporting

A Firm s System of Quality Control

A Firm s System of Quality Control 2759 QC Section 10 A Firm s System of Quality Control (Supersedes SQCS No. 7.) Source: SQCS No. 8; SAS No. 122; SAS No. 128. Effective date: Applicable to a CPA firm's

A Firm s System of Quality Control 2759 QC Section 10 A Firm s System of Quality Control (Supersedes SQCS No. 7.) Source: SQCS No. 8; SAS No. 122; SAS No. 128. Effective date: Applicable to a CPA firm's

International Auditing and Assurance Standards Board International Federation of Accountants 529 Fifth Avenue, 6 h Floor New York, NY 10017

August 1, 2017 International Auditing and Assurance Standards Board International Federation of Accountants 529 Fifth Avenue, 6 h Floor New York, NY 10017 Via IAASB website at www.iaasb.org Antony Nettleton

August 1, 2017 International Auditing and Assurance Standards Board International Federation of Accountants 529 Fifth Avenue, 6 h Floor New York, NY 10017 Via IAASB website at www.iaasb.org Antony Nettleton

) ) ) ) ) ) ) ) ) ) ) )

) ) ) ) ) ) ) ) ) ) )") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org PROPOSED AUDITING STANDARD RELATED TO COMMUNICATIONS WITH AUDIT COMMITTEES AND RELATED AMENDMENTS

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org PROPOSED AUDITING STANDARD RELATED TO COMMUNICATIONS WITH AUDIT COMMITTEES AND RELATED AMENDMENTS

STANDING ADVISORY GROUP MEETING DESIGNING AND IMPLEMENTING A SYSTEM OF QUALITY CONTROL OCTOBER 13-14, 2010

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org STANDING ADVISORY GROUP MEETING DESIGNING AND IMPLEMENTING A SYSTEM OF QUALITY CONTROL OCTOBER

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org STANDING ADVISORY GROUP MEETING DESIGNING AND IMPLEMENTING A SYSTEM OF QUALITY CONTROL OCTOBER

Agreeing the Terms of Audit Engagements

ISA 210 Issued March 2009; updated February 2018 International Standard on Auditing Agreeing the Terms of Audit Engagements INTERNATIONAL STANDARD ON AUDITING 210 AGREEING THE TERMS OF AUDIT ENGAGEMENTS

ISA 210 Issued March 2009; updated February 2018 International Standard on Auditing Agreeing the Terms of Audit Engagements INTERNATIONAL STANDARD ON AUDITING 210 AGREEING THE TERMS OF AUDIT ENGAGEMENTS

Audit Committee Oversight of Auditors

PCAOB Issues Guidance to Audit Committees on Audit Firm Inspection Process SUMMARY The Public Company Accounting Oversight Board has issued a release to assist audit committees in: understanding the PCAOB

PCAOB Issues Guidance to Audit Committees on Audit Firm Inspection Process SUMMARY The Public Company Accounting Oversight Board has issued a release to assist audit committees in: understanding the PCAOB

IAASB Main Agenda (March 2005) Page Agenda Item 12-C

Page Agenda Item 12-C") IAASB Main Agenda (March 2005) Page 2005 429 Agenda Item 12-C [ISA AND IAPS SPLIT] PROPOSED INTERNATIONAL AUDITING PRACTICE STATEMENT XXX THE APPLICATION OF INTERNATIONAL STANDARDS ON AUDITING IN AN AUDIT

IAASB Main Agenda (March 2005) Page 2005 429 Agenda Item 12-C [ISA AND IAPS SPLIT] PROPOSED INTERNATIONAL AUDITING PRACTICE STATEMENT XXX THE APPLICATION OF INTERNATIONAL STANDARDS ON AUDITING IN AN AUDIT

Auditing Standards and Practices Council

Auditing Standards and Practices Council AUDIT EVIDENCE PHILIPPINE STANDARDON AUDITING 500 (REVISED) AUDIT EVIDENCE (Effective for audits of financial statements for periods beginning on or after December

Auditing Standards and Practices Council AUDIT EVIDENCE PHILIPPINE STANDARDON AUDITING 500 (REVISED) AUDIT EVIDENCE (Effective for audits of financial statements for periods beginning on or after December

REGISTERED CANDIDATE AUDITOR (RCA) TECHNICAL COMPETENCE REQUIREMENTS

TECHNICAL COMPETENCE REQUIREMENTS") REGISTERED CANDIDATE AUDITOR (RCA) TECHNICAL COMPETENCE REQUIREMENTS 1. Context After completion of the recognised training contract, a period of specialisation is required, appropriate to the level required

REGISTERED CANDIDATE AUDITOR (RCA) TECHNICAL COMPETENCE REQUIREMENTS 1. Context After completion of the recognised training contract, a period of specialisation is required, appropriate to the level required

Memo. Date: October 2018 INTRODUCTION

Memo To: All Public Accounting Firms From: Kathy Zaplitny, CPA, CA Senior Director, Stakeholder Services & Engagement Re: FOCUS ON PRACTICE INSPECTION REPORTABLE DEFICIENCIES 2017-18 Date: October 2018

Memo To: All Public Accounting Firms From: Kathy Zaplitny, CPA, CA Senior Director, Stakeholder Services & Engagement Re: FOCUS ON PRACTICE INSPECTION REPORTABLE DEFICIENCIES 2017-18 Date: October 2018

1666 K Street, NW K Street, NW Washington, D.C Telephone: (202) Facsimile: (202)