REPORT WRITING & INDEPENDENT REVIEW

|

|

|

- Marlene Barker

- 6 years ago

- Views:

Transcription

1 REPORT WRITING & INDEPENDENT REVIEW 1 PRESENTED BY FAITH NGWENYA TECHNICAL & STANDARDS SERVICES EXECUTIVE

2 Professional Accountant 2

3 3 QUALITY CONTROL ISQC 1 Monitoring ISQC 1 Engagement performance Human Resources. Acceptance and continuance Ethical requirements Leadership responsibilities

4 4 ISQC 1 RISK AND COMPLIANCE Leadership responsibility Policies and procedures not documented No on -going review of policies and procedures No cold file reviews (audit) -Lack of supervision and control -Methodology (audit) not effective Monitoring Engagement performance - References not obtained for new staff -Fit and proper declarations not obtained - Insufficient training on ISA/IFRS and record keeping Non-compliance with ISQC1 Human Resources Independence & ethical requirements Client acceptance & continuance - Independence declaration from staff not obtained - Register of identified threats & safeguards not maintained - No integrity checks plus client identification - Procedures not documented - - Engagement letters not issued

5 5 Leadership responsibility Organisation structure Enforcement of policies Setting tone from the top Communicate with staff Leadership responsibility Document policies & procedures Establish policies & procedures

6 6 SETTING TONE AT THE TOP Commitment to continuous improvement Performance of effective & efficient reviews Associate with right clients Tone at the top Commitment to technical excellence & quality Clear standards & robust processes Recruitment of skilled & competent staff

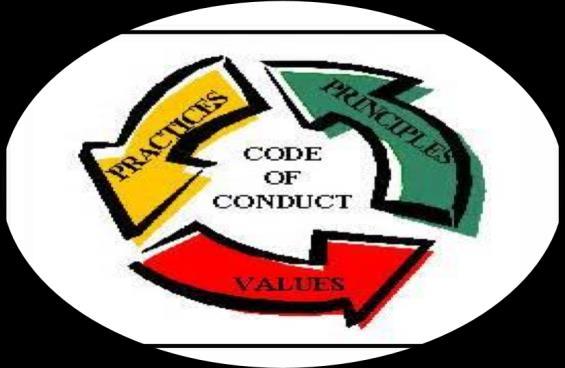

7 7 ETHICAL REQUIREMENTS Code of Conduct Ethical dilemma procedures Independence

8 8 INDEPENDENCE Independence of record keeping and compilation Compilation Independence of Decision making Independent review Audit Independent of business entity

9 9 INDEPENDENCE Appointment Services agreed upon Execution of performance Regulations & standards Independence Acceptance & continuance Engagement letter & planning Engagement performance Compliance of performance

10 10 INDEPENDENCE AND ETHICS Obtain information Obtain information on potential threat to independence & ethics Evaluate Evaluate any threats to independence & ethics Document Document & report on conclusions Action Take appropriate action to mitigate the risks to ethics & independence.

11 11 ACCEPTANCE AND CONTINUANCE Integrity of the client Acceptance and continuance Can comply with ethical requirements Practice is competent and & has sufficient time, resources & competence

12 12 HUMAN RESOURCES Recruitment and Appointment Professional development Performance evaluation, compensation & promotions Ability/Aptitude Values Competence Motivation Quality of work

13 13 ASSIGNMENT AND ENGAGEMENT TEAM Identity and role of engagement partner communicated Engagement partner has appropriate capabailities, competence, authority & time Responsibilities of engagement partner clearly defined & communicated

14 14 ENGAGEMENT PERFORMANCE Professional Standards Regulatory requirements Performance obligations

15 15 ENGAGEMENT PERFORMANCE Performance Activity Engagement letter Resource allocation Planning engagement Monitoring Performance Criteria Service/agreed upon deliverables Competence-engagement fit Responsibility & accountability duties Quality assurance supervision & review strategies & reports Work flow planning Reporting Performance obligations Integrated work plan documented and sign off File & report review processes Document discussions & communications

16 16 CONSULTATION OR SECONDMENTS Appropriate consultation has taken place on difficult issues Sufficient resources available to enable appropriate consultation Nature and scope of consultations documented Conclusions reached from consultations are documented & implemented

17 17 CONSULTATION OR SECONDMENTS Strategy Objective Supervision Monitoring Risk identification & provide guidance Continuous quality assurance review to prevent risks Review Ensure compliance & correction of risks Documentation Proof of evidence

18 18 MONITORING Establish a monitoring process designed to provide it with reasonable assurance that policies & procedures relating to the system of quality control/assurance are relevant, adequate & operating efficiently. Internal assessment Functionality & compliance External assessment Relevance & benchmarking Professional assessment Inspection & compliance

19 Compilation Engagement [ISRS 4410] 19 Prepared by: Rashied Small, Hashim Salie, Shafiek Dollie & Yaeesh Yasseen

accounting framework that must be adopted, and (iii)corporate governance issues that should be complied with")

20 20 Public Interest Score Public Interest Score: The public interest score is a mechanism introduced by the Companies Act that determines: (i) the type of engagement that must be performed, (ii)accounting framework that must be adopted, and (iii)corporate governance issues that should be complied with

21 21 PUBLIC INTEREST SCORE COMPONENTS

22 22 PUBLIC INTEREST SCORE - CRITERIA A number of points that equal the average number of employees during the financial year. One point for every R 1 million (or portion thereof) in third-party liabilities at the financial year end. One point for every R 1 million (or portion thereof) in turnover during the financial year One point for every individual who, at the end of the financial year, is known to directly or indirectly have a beneficial interest.

23 1. Is the company a public company or a state-owned company? 2. Is company a private company and controls fiduciary assets OM >R5m? < 100 No Aud/IR Duties of Acc Off No Application of PIS to Private Companies and CCs Owner Managed Greater/= than 350 PIS Yes Yes No Non- Owner Managed Acc Officer Yes Greater/= than 350 PIS EXT Is entity CC Less than 350 PIS and greater/equal to than 100 PIS No Audit/N o IR INT Audit Audit Less than 350 PIS and greater/equal to than 100 PIS Int Less than 100 PIS Non CA/CA Ext CA Independe nt Review

24 24 PUBLIC INTEREST SCORE - APPLICATION Public Interest Score Financial Reporting Standard Audit PIS 350 IFRS / IFRS for SMEs YES PIS 100 and < 350 and AFS were internally compiled PIS 100 and < 350 and AFS independently compiled PIS < 100 and AFS independently compiled IFRS / IFRS for SMEs IFRS / IFRS for SMEs IFRS / IFRS for SMEs YES NO NO PIS < 100 and AFS internally compiled The Financial Reporting Standard as determined by the company for as long as no Financial Reporting Standard is prescribed NO

25 25 PUBLIC INTEREST SCORE - PRACTITIONERS

and the procedures prescribed in terms of")

26 26 COMPILATION ISRS 4410 Assurance: A compilation does not involve and audit or review, no assurance about the financial statements is provided Compilation provide implied assurance about the fair presentation and relevance of the financial statements (requirement of accounting standards) and the procedures prescribed in terms of ISRS 4410

27 27 LEGISLATION S 29 and s30 requires the compilation Companies Act Accounting Standards Qualitative characteristics and presentation of financial information ISQC 1 ISRS 4410 Competence required to perform the compilation Responsibilities of the compiler and the procedures to follow

28 28 Compilation Engagement Compilation is defined as an engagement in which the professional applies his accounting and financial competence to assist management to prepare financial statements in accordance with the appropriate accounting framework based on information provided by management.

29 Compilation 29 When should a compilation be performed Assist management in making judgement in compiling financial statements Management requires reports for decision making For planning purpose support financial and tax planning Supporting documentation valuation or sale of a business or interest in a business Purposes of other engagements base for review or audit engagement

30 30 Compiler s Responsibilities Financial statement risks Independence Verification of information Compiler

31 Uses of compilation 31 When are the uses of a compilation? Assist management in making judgement in compiling financial statements management requires reports for decision making purposes For planning purpose support financial and tax planning Supporting documentation valuation or sale of a business or interest in a business Purposes of other engagements based of review and audit engagement

32 Benefits of compilation 32 What are the benefits of compilations? Cost effective save time and money because of the work required Use of an expert technical financial reporting competence and ethics Flexible and targeted engagements compilation can be used as an agreed upon engagement Independence improve the quality and integrity of the financial statements

33 33 What are the procedures for a compilation? Accept Apply risk assessment of the client risk profile fit (ISCQ 1) Engagement letter competent to accept the engagement Plan Understand the nature of the business and its operations Understand and evaluate the accounting system Execute Reconcile the financial information with the accounting records Discuss significant matters and judgements with management Report Discuss the financial statements with management Prepare the compilation report

34 34 What preparation is required for a compilation? ISRS 4410 Compilation Engagement [objective, purposes and procedures] Professional judgement [fair representation of financial statements] Code of Ethical Conduct [objectivity,integrity, professional conduct & competence, due care, confidentiality] Accepting the engagement Quality control [competence to perform task, quality control procedures]

35 Acceptance Checklist 35 Checklist before accepting a compilation Risk assessment of client fits practice risk profile Management s integrity reliance placed on information provided for compilation Previous accountant reasons for change or reason for appointment Purpose of assignment needs of the external and/or internal users Internal controls reliability of accounting systems to produce accurate information Competence of professional ability to perform the engagement

36 36 Mini Case Study Client 1: Technology business that is known for its integrity and innovation. The owners are involved in community activities and established a strong relationship. The client has been referred by the previous accountant (a trusted friend who is retiring) and stated that there is no professional reason not to accept the client. Client 2: Entertainment business that opened a casino in the heart of the community. The community including law enforcement agencies has petitioned the establishment and requested the relocation of the business because of their concerns about the possible negative social impact it may have on the community. To date the financial statements of the business was prepared internally.

37 Factors to consider 37 What factors to consider for a compilation? Public Interest Score legislative requirements Purpose of compilation will external users place reliance on the financial statements Benefits of professional s competence benefits management can gain from the assistance Limitation of financial statements historical costs principle and the judgement

38 Engagement content 38 What are the key contents for a compilation? Customised specific to satisfy the requirements and circumstance of engagement Objectives and scope explicit statement that it is a non-assurance engagement (no audit) Responsibilities details of management s and professional responsibilities Purpose of financial statements users, purposes and distribution Reporting nature and type of reporting as well as means/channels of communication

39 39 What must be done for recurring engagement? NO CHANGES Circumstance and conditions of the engagement does not change no need to issue a new engagement letter Changes - Misunderstanding of compilation - Changes in terms of engagement - Changes in management - Changes in ownership of business - Changes in nature of business - Changes in accounting framework

40 40 What other factors should be considered? Use and distribution of reports Publication of financial statements (website) Supporting schedules prepared by management Reliance placed on information received from third parties Billing arrangements Other Services

41 41 What are the critical processes in planning? Business - Nature of business - Governance Materiality - Context of IFRS - Misstatements - Reliability Communication - Management - Compilation team - Team & client staff Planning of compilation Procedures - ISRS System & controls - Reconcile records

42 Procedures 42 What procedures are followed for a compilation? Understanding the business assess the level of risks and materiality Understanding the accounting system type of transactions and accounting records Estimates and judgement assess the accuracy and reliability of judgements Incomplete information obtain explanations from management (evidence) Unusual transactions investigate significant transactions and variances in balances

43 43 Compilation - Procedures

44 44 What procedures are followed for compilation? Discussions Nature of business Accounting system Principles & practice Judgements Reconcile to records Incomplete data Consideration Judgements reasonability Unusual transactions recognition Completeness cutoff procedures Fair representation - truthfulness Customisation Compliance accounting framework Adjustments to statements Recommendations to management Concerns - resolved

45 45 What contents is part of compilation report? Preparation of financial statements based on information provided by management Responsibilities of management relation to governance, compilation engagement and financial statements Accounting Framework used for the preparation of the financial statements Compliance with format of financial statements components of the statements Responsibilities of compiler complied with ISRS 4410 (procedures) and ethical behaviour Not an assurance function: no need to verify the transactions and information provided by management No opinion is expressed Special purpose description of the engagement and use of the statements

46 Review Engagement [ISRE 2400] 46 Prepared by: Rashied Small, Hashim Salie, Shafiek Dollie & Yaeesh Yasseen

47 47 Review Engagement A review provides limited assurance that the financial statements conform to generally accepted accounting principles. This type of assurance is known as negative assurance. This means that as the professional accountant is only providing assurance that nothing has come to their attention that would indicate the financial information is not presented in accordance with accounting standards.

48 48 What is the objective of a review? The professional accountant inquires and performs procedures to determine whether the financial statements prepared by management is free from material misstatements due to fraud and errors. In a review the professional accountant provides limited or moderate assurance about the fair presentation and reliability of the financial statements nothing has come to the attention of the reviewer that the financial statements do not fairly presents, in all material respect in accordance with the accounting framework.

49 Use of review 49 When is the independent review used? Provide users of financial statements with some assurance level of reliability To support proposals and applications for financing or change in ownership through sale of interest Provide assurance of compliance to reporting regulations Supporting management with internal review of the business Support the risk management strategy and governance of the business

50 Benefits of review 50 What are the benefits of a review? Cost effective gain limited assurance on the reliability of the financial statements Limited assurance financial statements are free of material misstatement Flexible and targeted engagements review focuses on the areas of potential risks of misstatement Use of expert reviewer s experience can be used as a risk management strategy

51 51 What are the pre-condition for a review? The accounting framework used to prepare the financial statements must be acceptable and appropriate for the business. The scope to conduct a review should not be restricted as a result of management not be willing grant the professional accountant access to the accounting records and documents supporting the financial statements. Proceed with review

52 52 What are steps involved in a review? Determine whether a review is necessary and appropriate Identify potential risks that may result in material misstatement of the financial statements Perform the review by applying appropriate procedures analytical procedures as per ISRE 2400 Conduct additional procedure for areas of possible risks of misstatement Prepare the review report arrive at a conclusion (limited assurance)

53 53 Parties Responsibilities

54 54 What are the procedures for a review? Accept Apply risk assessment of the client risk profile fit (ISCQ 1) Engagement letter competent to accept the engagement Plan Understand the nature of the business and its operations Identify areas of material misstatement in financial statements Execute Perform analytical procedures obtain sufficient evidence Perform additional procedures on areas of risk Report Evaluate evidence obtained communication with management Prepare the review report

55 55 What preparation is required for a review? ISRE 2400 Review Engagement [objective, purposes and procedures] Professional judgement [fair representation of financial statements] Code of Ethical Conduct [objectivity,integrity, professional conduct & competence, due care, confidentiality] Accepting the engagement Quality control [competence to perform task, quality control procedures]

56 56 What is professional skepticism? Professional skepticism is an attitude that includes a questioning mind, being alert to conditions which may indicate possible misstatement due to error or fraud, and a critical assessment of evidence. Attitude to be able to: Identify and respond to conditions that indicate possible misstatement Critically assess evidence obtained Question managements explanations and representations Draw conclusions based and the facts and evidence obtained

57 57 What is professional judgement? Professional judgment involves the application of competence and experience in making informed decisions about the courses of action that are appropriate for the circumstances. Circumstances where professional judgement may be used: Determining materiality for the engagement Determining areas of possible material misstatement of statements Allocating of staff members that fits their competence levels Designing analytical and additional procedures for the engagement Evaluating evidence to support the conclusion - sufficiency

Quality of information risk that the information required may not be reliable or available Purpose of assignment management may use the review to avoid negative audit reports Outstanding")

58 Acceptance Checklist 58 Checklist before accepting a review Risk assessment of client fits practice risk profile Owner s and management s integrity misuse of the review report (claiming it is an audit) Quality of information risk that the information required may not be reliable or available Purpose of assignment management may use the review to avoid negative audit reports Outstanding matters significant matters impacting performing the review effectively Complexity of business financial statements are complex and requires specialized knowledge and experience

59 59 ENGAGEMENT LETTER Reporting Purpose & objective Engagement letter Financial statement risk Procedures Mgnt s responsibility Restriction on scope

60 Factors to consider 60 What factors to consider for a review? Public Interest Score legislative requirements Integrity of management indication of unethical behaviour, infringement of regulations or unwillingness to provide information Limitation on scope restriction on access to information or staff, unrealistic deadlines or quality of information Internal controls process and procedures to mitigate risks of material misstatement of financial statements

61 Engagement content 61 What are the key contents for a review? Customised specific to satisfy the requirements and circumstance of engagement Objectives and scope explicit statement that it is not an audit but limited assurance is provided Responsibilities details of management s and professional responsibilities Purpose of financial statements users, purposes and distribution Reporting nature and type of reporting as well as means/channels of communication

62 62 What must be done for recurring engagement? NO CHANGES Circumstance and conditions of the engagement does not change no need to issue a new engagement letter Changes - Misunderstanding of compilation - Changes in terms of engagement - Changes in management - Changes in ownership of business - Changes in nature of business - Changes in accounting framework

63 63 What are the critical processes in planning? Business - Nature of business - Governance Materiality - Context of IFRS - Misstatements - Reliability Communication - Management - Compilation team - Team & client staff Planning of review Procedures - ISRE Analytical procedures - Additional procedures

64 64 MATERIALITY Prior results Transactions Material risks Industry practice Mgnt s judgement

65 65 What are causes of material misstatements? Material misstatement is when it would significantly change or influence the decisions of informed users of the financial statements. Possible causes of misstatement of financial statements: Fraud and errors (recognition and measurement) Departure from the accounting framework Inappropriate estimates Lack of full disclosure of significant matters

66 66 Review - Procedures Understand business Information risk Accounting framework Review procedures Analytical procedures Accounting systems Financial statement assertions

67 Procedures 67 What procedures are followed for a review? Understanding the business assess the level of risks and materiality Identifying misstatements identify possible risks of misstatement of financial statements Evaluate internal controls assess controls to mitigate material misstatements Analytical procedures obtain evidence for possible misstatement identified Additional procedures investigate and obtain evidence relating to material misstatements

68 68 What contents is part of review report? Responsibilities of management relation to governance, review engagement and preparation of financial statements Accounting Framework used for the preparation of the financial statements Compliance with format of financial statements components of the statements Responsibilities of reviewer complied with ISRE 2400 (procedures) and ethical behaviour Limited assurance function: Evaluate the misstatement of financial statements Draw a conclusion on whether financial statements are free of material misstatement Purpose of engagement description of the engagement and use of the statements

69 69 FORMING AN APPROPRIATE CONCLUSION Negative Assurance: Reviewer is satisfied based on the evidence obtained that the financial statements are free of misstatements Qualification of Assurance: The nature of matters may render the financial statements misleading, a qualified or adverse opinion may be expressed.

70 COMPARATIVE ANALYSIS 70 COMPARISONS Compilation Independent review Audit Level of assurance obtained by Accountants or Auditors that the financial statements are not materially misstated Accountant does not obtain or provide any assurance that there are no material modification that should be made to the financial statements Accountant obtains limited assurance that there are no material modification that should be made to the financial statements The auditor obtains a high, but not absolute, level of assurance about whether the financial statements are free of material misstatement Objective To assist management in presenting financial information in the form of financial statements without undertaking to provide any assurance that there are no material modifications that should be made to the financial statements To obtain limited assurance that there are no material modification that should be made to the financial statements To obtain a high level of assurance about whether the financial statements as a whole are free of material misstatement thereby enabling the auditor to express an opinion on whether the financial statements are presented fairly, in all material respects

71 71 COMPARISONS Compilation Independent review Audit Assurance provided to the user of the financial statements None the report states that no assurance is provided None the report provides a statement that the accountant is not aware of any material modifications that should be made to the financial statements None the auditor provides an opinion as to whether the financial statements present fairly, in all material respects, the company s financial position, results of operations and cash flows Situations requiring different levels of service Generally appropriate or privately held companies and are often prepared for simple situations (e.g., a lender needs IFRS financial statements instead of the statements the internal accounting system produces or the lender needs the comfort provided by knowing that an accountant read the financial statements) Often prepared for privately held companies because of requirements of outside third parties (such as banks, creditors and potential purchasers) that are looking for comfort that the financial statements are not materially misstated Often prepared for companies because outside third parties (such as banks, creditors, potential purchasers and outside investors) require an auditor s opinion on the financial statements

72 Agreed upon Engagement [ISRS 4400] 72

73 73 Agreed upon Engagement An agreed-upon procedures engagement is an engagement in which an auditor/professional accountant is engaged to carry out those procedures of an audit nature to which the auditor and the entity and any appropriate third parties have agreed and to report on factual findings.

74 74 What is objective of agreed upon engagement? The objective of an agreed-upon procedures engagement is for the professional accountant to: carry out procedures of an investigative nature to which the parties have agreed report on factual findings No assurance is expressed provide a factual findings reports without expressing an opinion or making recommendations Users of the report assess the findings reported and draw their own conclusions from the work performed Use of the report is restricted to those parties that have agreed to the procedures to be performed - others, unaware of the reasons for the procedures, may misinterpret the results

75 75 What is the contents of the agreement? Nature of the engagement - no audit or review (no assurance or opinion expressed) Purpose for the engagement Identification of the financial information or activities to which the agreed-upon procedures will be applied Nature, timing and extent of the specific procedures to be applied Anticipated form of the report of factual findings Limitations on distribution of the report of factual findings

76 76 What are steps involved in an engagement? Determine the nature and complexity of the engagement Design the procedures to be performed to conduct the engagement Investigate and obtain sufficient evidence relating to the engagement documents all evidence Evaluate the evidence obtained to support the conclusion Prepare the engagement report prepare a factual findings report

77 77 What preparation is required for a engagement? ISRS 4400 Agreed upon Engagement [objective, purposes and procedures] Procedures [investigation of financial and nonfinancial information] Code of Ethical Conduct [objectivity,integrity, professional conduct & competence, due care, confidentiality] Accepting the engagement Quality control [competence to perform task, quality control procedures]

78 78 What contents is part of engagement report? Purpose of engagement description of the engagement and use of the report Not audit or review no assurance or opinion expressed Responsibilities of management facilitate the engagement process Responsibilities of professional accountant complied with ISRS 4400 (procedures) and ethical behaviour Procedures that will be applied Limitation of engagement: Financial information that engagement relates to Distribution and use of the report Format of the report Fee structure and timeframe

79 Engagement Letter 79 Prepared by: Rashied Small, Hashim Salie, Shafiek Dollie & Yaeesh Yasseen

80 80 What is an Engagement Letter (E.L.)? Engagement letters are a key document in the relationship between you and your client, providing a written confirmation of the work that will be carried out Agreement of service binding the Profession Accountant with the client. Service Level Agreement which stipulates the nature, type and conditions of services to be performed Engagement letter is a legal contract which is binding on the parties to the agreement

81 81 What is the purpose of E.L.? Ensures both parties are on the same page Serves as a risk management tool Forms the foundation of client communication and trust Mandatory in your practice quality control.

82 82 What are the primary contents? Purpose and objectives of the assignment Responsibilities of management A statement stating the professional is an independent contractor. Standards that will be followed for the terms of the assignment Reporting format and communication channels Deliverables of the assignment Type and timing of the assignment - timeframe Basis of determining cost for the assignment Procedures for amendments to the assignment State REPORT WRITING any - CPD limitations 2017

Compilation Engagements

IFAC Board Final Pronouncement March 2012 International Standard on Related Services ISRS 4410 (Revised), Compilation Engagements The International Auditing and Assurance Standards Board (IAASB) develops

IFAC Board Final Pronouncement March 2012 International Standard on Related Services ISRS 4410 (Revised), Compilation Engagements The International Auditing and Assurance Standards Board (IAASB) develops

Professional Competence for Engagement Partners Responsible for Audits of Financial Statements (Revised)

") IFAC Board Final Pronouncement December 2014 International Education Standard (IES ) 8 Professional Competence for Engagement Partners Responsible for Audits of Financial Statements (Revised) This document

IFAC Board Final Pronouncement December 2014 International Education Standard (IES ) 8 Professional Competence for Engagement Partners Responsible for Audits of Financial Statements (Revised) This document

INTERNATIONAL STANDARD ON AUDITING 260 COMMUNICATION WITH THOSE CHARGED WITH GOVERNANCE CONTENTS

Introduction INTERNATIONAL STANDARD ON AUDITING 260 COMMUNICATION WITH THOSE CHARGED WITH GOVERNANCE (Effective for audits of financial statements for periods beginning on or after December 15, 2009) +

Introduction INTERNATIONAL STANDARD ON AUDITING 260 COMMUNICATION WITH THOSE CHARGED WITH GOVERNANCE (Effective for audits of financial statements for periods beginning on or after December 15, 2009) +

INTERNATIONAL STANDARD ON AUDITING 210 TERMS OF AUDIT ENGAGEMENTS CONTENTS

INTERNATIONAL STANDARD ON AUDITING 210 TERMS OF AUDIT ENGAGEMENTS (Effective for audits of financial statements for periods beginning on or after December 15, 2006. Appendix 2 contains conforming amendments

INTERNATIONAL STANDARD ON AUDITING 210 TERMS OF AUDIT ENGAGEMENTS (Effective for audits of financial statements for periods beginning on or after December 15, 2006. Appendix 2 contains conforming amendments

Compilation Engagements

SINGAPORE STANDARD ON RELATED SERVICES SSRS 4410 (REVISED) Compilation Engagements This revised Singapore Standard on Related Services (SSRS) 4410 supersedes SSRS 4410 Engagements to Compile Financial

SINGAPORE STANDARD ON RELATED SERVICES SSRS 4410 (REVISED) Compilation Engagements This revised Singapore Standard on Related Services (SSRS) 4410 supersedes SSRS 4410 Engagements to Compile Financial

Auditing Standards and Practices Council

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT PHILIPPINE STANDARD ON AUDITING

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT PHILIPPINE STANDARD ON AUDITING

Review of agreed-upon procedures engagements questionnaire

Review of agreed-upon procedures engagements questionnaire Review code Reviewer Review date Introduction Standards on Related Services (ASRSs) detail the responsibilities of an assurance practitioner,

Review of agreed-upon procedures engagements questionnaire Review code Reviewer Review date Introduction Standards on Related Services (ASRSs) detail the responsibilities of an assurance practitioner,

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT CONTENTS

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT (Effective for audits of financial statements for periods beginning

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT (Effective for audits of financial statements for periods beginning

STATEMENT OF AUDITING STANDARDS 500 AUDIT EVIDENCE

STATEMENT OF AUDITING STANDARDS 500 AUDIT EVIDENCE (Issued January 2004) Contents Paragraphs Introduction 1-2 Concept of Audit Evidence 3-6 Sufficient Appropriate Audit Evidence 7-14 The Use of Assertions

STATEMENT OF AUDITING STANDARDS 500 AUDIT EVIDENCE (Issued January 2004) Contents Paragraphs Introduction 1-2 Concept of Audit Evidence 3-6 Sufficient Appropriate Audit Evidence 7-14 The Use of Assertions

INTERNATIONAL STANDARD ON AUDITING (IRELAND) 210 AGREEING THE TERMS OF AUDIT ENGAGEMENTS

210 AGREEING THE TERMS OF AUDIT ENGAGEMENTS") INTERNATIONAL STANDARD ON AUDITING (IRELAND) 210 AGREEING THE TERMS OF AUDIT ENGAGEMENTS MISSION To contribute to Ireland having a strong regulatory environment in which to do business by supervising and

INTERNATIONAL STANDARD ON AUDITING (IRELAND) 210 AGREEING THE TERMS OF AUDIT ENGAGEMENTS MISSION To contribute to Ireland having a strong regulatory environment in which to do business by supervising and

International Standard on Auditing (Ireland) 500 Audit Evidence

500 Audit Evidence") International Standard on Auditing (Ireland) 500 Audit Evidence MISSION To contribute to Ireland having a strong regulatory environment in which to do business by supervising and promoting high quality

International Standard on Auditing (Ireland) 500 Audit Evidence MISSION To contribute to Ireland having a strong regulatory environment in which to do business by supervising and promoting high quality

IAASB Main Agenda (December 2011) Agenda Item

Agenda Item") Engagement Level Audit Quality Exhibiting appropriate values, ethics and attitudes; Agenda Item 6-B 1. An audit of an entity s financial statements involves independent auditors gathering sufficient appropriate

Engagement Level Audit Quality Exhibiting appropriate values, ethics and attitudes; Agenda Item 6-B 1. An audit of an entity s financial statements involves independent auditors gathering sufficient appropriate

AUSTRALIAN GAAS 2007 AUDITING STANDARDS CHECKLISTS

AUSTRALIAN GAAS 2007 AUDITING STANDARDS CHECKLISTS COLIN PARKER B.Bus FCA MAICD Principal, GAAP Consulting www.gaap.com.au AUSTRALIAN GAAS* 2007 AUDITING STANDARDS CHECKLISTS AS AT 1 JANUARY 2007 COLIN

AUSTRALIAN GAAS 2007 AUDITING STANDARDS CHECKLISTS COLIN PARKER B.Bus FCA MAICD Principal, GAAP Consulting www.gaap.com.au AUSTRALIAN GAAS* 2007 AUDITING STANDARDS CHECKLISTS AS AT 1 JANUARY 2007 COLIN

ASB Meeting January 12-15, 2015

ASB Meeting January 12-15, 2015 Agenda Item 3A Chapter 1, Concepts Common to All Attestation Engagements, of Attestation Standards: Clarification and Recodification Introduction 1.1 This chapter of Statements

ASB Meeting January 12-15, 2015 Agenda Item 3A Chapter 1, Concepts Common to All Attestation Engagements, of Attestation Standards: Clarification and Recodification Introduction 1.1 This chapter of Statements

Scope of this SA Effective Date Objective Definitions Sufficient Appropriate Audit Evidence... 6

SA 500* AUDIT EVIDENCE (Effective for audits of financial statements for periods beginning on or after April 1, 2009) Contents Introduction Paragraph(s) Scope of this SA...1-2 Effective Date... 3 Objective...

SA 500* AUDIT EVIDENCE (Effective for audits of financial statements for periods beginning on or after April 1, 2009) Contents Introduction Paragraph(s) Scope of this SA...1-2 Effective Date... 3 Objective...

A Firm s System of Quality Control

A Firm s System of Quality Control 2759 QC Section 10 A Firm s System of Quality Control (Supersedes SQCS No. 7.) Source: SQCS No. 8; SAS No. 122; SAS No. 128. Effective date: Applicable to a CPA firm's

A Firm s System of Quality Control 2759 QC Section 10 A Firm s System of Quality Control (Supersedes SQCS No. 7.) Source: SQCS No. 8; SAS No. 122; SAS No. 128. Effective date: Applicable to a CPA firm's

Assurance Hand Note Professional Stage-Knowledge Level By: Shafique Ahmed-Sr. Officer (Internal Audit-BSRM) Assurance

Assurance") Assurance 1 CONTENTS OF ASSURANCE 01. Preliminary of Assurance: 1.01 Assurance Engagement: 1.02 Key elements of an assurance engagement: 1.03 Levels of assurance 1.04 Objective of an Audit: 1.05 True &

Assurance 1 CONTENTS OF ASSURANCE 01. Preliminary of Assurance: 1.01 Assurance Engagement: 1.02 Key elements of an assurance engagement: 1.03 Levels of assurance 1.04 Objective of an Audit: 1.05 True &

INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 500

500") Issued 07/11 Compiled 10/15 INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 500 Audit Evidence (ISA (NZ) 500) This compilation was prepared in October 2015 and incorporates amendments up to and including

Issued 07/11 Compiled 10/15 INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 500 Audit Evidence (ISA (NZ) 500) This compilation was prepared in October 2015 and incorporates amendments up to and including

Pre-Engagement Activities and Audit Planning By: Tariq Mahmood FCA, ACMA

Model Audit Practice Manual Pre-Engagement Activities and Audit Planning By: Tariq Mahmood FCA, ACMA Today s Learnings Pre-Engagement Activities Audit Planning Procedures Completion of Sample Forms (Annexures)

Model Audit Practice Manual Pre-Engagement Activities and Audit Planning By: Tariq Mahmood FCA, ACMA Today s Learnings Pre-Engagement Activities Audit Planning Procedures Completion of Sample Forms (Annexures)

THE IFRS WORKSHOP. Hilton Hotel. Saturday, 11 February /02/2017 Uphold Public Interest

THE IFRS WORKSHOP Hilton Hotel Saturday, 11 February 2017 11/02/2017 Uphold Public Interest 2 1. 2. 3. 4. 5. 6. 7. OVERVIEW WHICH REPORTS ARE AFFECTED NEW AND REVISED STANDARDS KAM ISA 720 REVISED ETHICS

THE IFRS WORKSHOP Hilton Hotel Saturday, 11 February 2017 11/02/2017 Uphold Public Interest 2 1. 2. 3. 4. 5. 6. 7. OVERVIEW WHICH REPORTS ARE AFFECTED NEW AND REVISED STANDARDS KAM ISA 720 REVISED ETHICS

Report on Inspection of KPMG AG Wirtschaftspruefungsgesellschaft (Headquartered in Berlin, Federal Republic of Germany)

") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Berlin, Federal Republic of Germany) Issued by the Public Company

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Berlin, Federal Republic of Germany) Issued by the Public Company

A FRAMEWORK FOR AUDIT QUALITY. KEY ELEMENTS THAT CREATE AN ENVIRONMENT FOR AUDIT QUALITY February 2014

A FRAMEWORK FOR AUDIT QUALITY KEY ELEMENTS THAT CREATE AN ENVIRONMENT FOR AUDIT QUALITY February 2014 This document was developed and approved by the International Auditing and Assurance Standards Board

A FRAMEWORK FOR AUDIT QUALITY KEY ELEMENTS THAT CREATE AN ENVIRONMENT FOR AUDIT QUALITY February 2014 This document was developed and approved by the International Auditing and Assurance Standards Board

Standard on Assurance Engagements ASAE 3500 Performance Engagements

ASAE 3500 (July 2008) (Amended October 2008) Standard on Assurance Engagements ASAE 3500 Issued by the Auditing and Assurance Standards Board Obtaining a Copy of this Standard on Assurance Engagements

ASAE 3500 (July 2008) (Amended October 2008) Standard on Assurance Engagements ASAE 3500 Issued by the Auditing and Assurance Standards Board Obtaining a Copy of this Standard on Assurance Engagements

IoD Code of Practice for Directors

The Four Pillars of Governance Best Practice Institute of Directors in New Zealand (Inc). IoD Code of Practice for Directors This Code provides guidance to directors to assist them in carrying out their

The Four Pillars of Governance Best Practice Institute of Directors in New Zealand (Inc). IoD Code of Practice for Directors This Code provides guidance to directors to assist them in carrying out their

Continuing Professional Development (CPD) Requirements for New Zealand Licensed Auditors

Requirements for New Zealand Licensed Auditors") Policy and guidance Continuing Professional Development (CPD) Requirements for New Zealand Licensed Auditors (Effective 1 July 2016) CONTENTS 1 CPD Policy for New Zealand licensed auditors... 3 1.1 Introduction...

Policy and guidance Continuing Professional Development (CPD) Requirements for New Zealand Licensed Auditors (Effective 1 July 2016) CONTENTS 1 CPD Policy for New Zealand licensed auditors... 3 1.1 Introduction...

McGraw-Hill/Irwin. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 03 Engagement Planning "Vision without action is a daydream. Action without vision is a nightmare. Japanese

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 03 Engagement Planning "Vision without action is a daydream. Action without vision is a nightmare. Japanese

AGS 10. Joint Audits AUDIT GUIDANCE STATEMENT

AUDIT GUIDANCE STATEMENT AGS 10 Joint Audits This Audit Guidance Statement was approved by the Council of the Institute of Singapore Chartered Accountants (formerly known as Institute of Certified Public

AUDIT GUIDANCE STATEMENT AGS 10 Joint Audits This Audit Guidance Statement was approved by the Council of the Institute of Singapore Chartered Accountants (formerly known as Institute of Certified Public

Guidance Note: Corporate Governance - Audit Committee. March Ce document est aussi disponible en français.

Guidance Note: Corporate Governance - Audit Committee March 2015 Ce document est aussi disponible en français. Applicability The Guidance Note: Corporate Governance Audit Committee (the Guidance Note )

Guidance Note: Corporate Governance - Audit Committee March 2015 Ce document est aussi disponible en français. Applicability The Guidance Note: Corporate Governance Audit Committee (the Guidance Note )

SRI LANKA AUDITING STANDARD 300 PLANNING AN AUDIT OF FINANCIAL STATEMENTS CONTENTS

SRI LANKA AUDITING STANDARD 300 PLANNING AN AUDIT OF FINANCIAL STATEMENTS (Effective for all the audits carried out on or after ) CONTENTS Paragraph Introduction 1-5 Preliminary Engagement Activities 6-7

SRI LANKA AUDITING STANDARD 300 PLANNING AN AUDIT OF FINANCIAL STATEMENTS (Effective for all the audits carried out on or after ) CONTENTS Paragraph Introduction 1-5 Preliminary Engagement Activities 6-7

Achieve. Performance objectives

Achieve Performance objectives Performance objectives are benchmarks of effective performance that describe the types of work activities students and affiliates will be involved in as trainee accountants.

Achieve Performance objectives Performance objectives are benchmarks of effective performance that describe the types of work activities students and affiliates will be involved in as trainee accountants.

File No: PERMANENT AUDIT FILE INDEX Annual update confirmation. Business details 1. Background to client

Client: Year/Period End: PERMANENT AUDIT FILE INDEX Annual update confirmation Business details 1. Background to client 2. Financial History 3. Register of laws and regulations 4. Related parties 5. Group

Client: Year/Period End: PERMANENT AUDIT FILE INDEX Annual update confirmation Business details 1. Background to client 2. Financial History 3. Register of laws and regulations 4. Related parties 5. Group

Standard on Quality Control (SQC)-1 Need for Documentaton. Abhay Vasant Arolkar

-1 Need for Documentaton. Abhay Vasant Arolkar") Standard on Quality Control (SQC)-1 Need for Documentaton By Abhay Vasant Arolkar Audit Scenario World over auditors are hauled up before courts and faced with huge punitive damages where they could not

Standard on Quality Control (SQC)-1 Need for Documentaton By Abhay Vasant Arolkar Audit Scenario World over auditors are hauled up before courts and faced with huge punitive damages where they could not

Client: Model File Limited Prepared by: MK Date: 30/03/17

5.02 A. Audit Strategy: Refer to Section 6.2.3 of the Manual for further guidance on completion of the Audit Strategy. See Appendix I - Section 6 on the matters that may be considered in developing an

5.02 A. Audit Strategy: Refer to Section 6.2.3 of the Manual for further guidance on completion of the Audit Strategy. See Appendix I - Section 6 on the matters that may be considered in developing an

CLARIFIED INTERNATIONAL STANDARDS ON AUDITIING WHAT DOES IT MEAN FOR AUDITORS IN THE UK AND IRELAND?

CLARIFIED INTERNATIONAL STANDARDS ON AUDITIING WHAT DOES IT MEAN FOR AUDITORS IN THE UK AND IRELAND? By: Danielle McWall, BSc (Hons), ACA, MBA, MIIA. Examiner - P1 Auditing Background Following the many

CLARIFIED INTERNATIONAL STANDARDS ON AUDITIING WHAT DOES IT MEAN FOR AUDITORS IN THE UK AND IRELAND? By: Danielle McWall, BSc (Hons), ACA, MBA, MIIA. Examiner - P1 Auditing Background Following the many

Audit Evidence This section is effective for audits of financial statements for periods ending on or after December 15, 2012.

Audit Evidence 395 AU-C Section 500 Audit Evidence Source: SAS No. 122; SAS No. 128. See section 9500 for interpretations of this section. Effective for audits of financial statements for periods ending

Audit Evidence 395 AU-C Section 500 Audit Evidence Source: SAS No. 122; SAS No. 128. See section 9500 for interpretations of this section. Effective for audits of financial statements for periods ending

RELEVANT TO ACCA QUALIFICATION PAPER P7. Studying Paper P7? Performance objectives 17 and 18 are relevant to this exam

RELEVANT TO ACCA QUALIFICATION PAPER P7 Studying Paper P7? Performance objectives 17 and 18 are relevant to this exam Acceptance decisions for audit and assurance engagements The syllabus for Paper P7,

RELEVANT TO ACCA QUALIFICATION PAPER P7 Studying Paper P7? Performance objectives 17 and 18 are relevant to this exam Acceptance decisions for audit and assurance engagements The syllabus for Paper P7,

Case Report from Audit Firm Inspection Results

Case Report from Audit Firm Inspection Results July 2014 Certified Public Accountants and Auditing Oversight Board Table of Contents Expectations for Audit Firms... 1 Important Points for Users of this

Case Report from Audit Firm Inspection Results July 2014 Certified Public Accountants and Auditing Oversight Board Table of Contents Expectations for Audit Firms... 1 Important Points for Users of this

Independent Auditor s report

Independent auditor s report to the members of Opinion on the financial statements of In our opinion the consolidated and Parent Company financial statements of : give a true and fair view of the state

Independent auditor s report to the members of Opinion on the financial statements of In our opinion the consolidated and Parent Company financial statements of : give a true and fair view of the state

THE NEW AND REVISED INTERPRETATIONS CONTAINED IN THIS DOCUMENT ARE EFFECTIVE ON AUGUST 31, 2017 UNLESS OTHERWISE NOTED.

THE NEW AND REVISED INTERPRETATIONS CONTAINED IN THIS DOCUMENT ARE EFFECTIVE ON AUGUST 31, 2017 UNLESS OTHERWISE NOTED. Ethics interpretations are promulgated by the executive committee of the Professional

THE NEW AND REVISED INTERPRETATIONS CONTAINED IN THIS DOCUMENT ARE EFFECTIVE ON AUGUST 31, 2017 UNLESS OTHERWISE NOTED. Ethics interpretations are promulgated by the executive committee of the Professional

SRI LANKA AUDITING STANDARD 300 PLANNING AN AUDIT OF FINANCIAL STATEMENTS CONTENTS

SRI LANKA AUDITING STANDARD 300 PLANNING AN AUDIT OF FINANCIAL STATEMENTS (Effective for audits of financial statements for periods beginning on or after 01 January 2014) * CONTENTS Paragraph Introduction

SRI LANKA AUDITING STANDARD 300 PLANNING AN AUDIT OF FINANCIAL STATEMENTS (Effective for audits of financial statements for periods beginning on or after 01 January 2014) * CONTENTS Paragraph Introduction

Auditing Standards and Practices Council

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 330 THE AUDITOR S PROCEDURES IN RESPONSE TO ASSESSED RISKS PHILIPPINE STANDARD ON AUDITING 330 THE AUDITOR S PROCEDURES IN RESPONSE

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 330 THE AUDITOR S PROCEDURES IN RESPONSE TO ASSESSED RISKS PHILIPPINE STANDARD ON AUDITING 330 THE AUDITOR S PROCEDURES IN RESPONSE

McGraw-Hill/Irwin. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 03 Engagement Planning "Vision without action is a daydream. Action without vision is a nightmare. Japanese

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 03 Engagement Planning "Vision without action is a daydream. Action without vision is a nightmare. Japanese

Standards on Review Engagements (SREs) E- 1220

E- 1220") Standards on Review Engagements (SREs) E- 1220 E- 1221 Engagement Standards Standards on Review Engagements SRE 2400, Engagements to Review Financial Statements (April 1, 2010) SRE 2410, Review of Interim

Standards on Review Engagements (SREs) E- 1220 E- 1221 Engagement Standards Standards on Review Engagements SRE 2400, Engagements to Review Financial Statements (April 1, 2010) SRE 2410, Review of Interim

The Auditor s Communication With Those Charged With Governance

Auditor s Communication With Those Charged With Governance 209 AU-C Section 260 The Auditor s Communication With Those Charged With Governance Source: SAS No. 122; SAS No. 123; SAS No. 125; SAS No. 128.

Auditor s Communication With Those Charged With Governance 209 AU-C Section 260 The Auditor s Communication With Those Charged With Governance Source: SAS No. 122; SAS No. 123; SAS No. 125; SAS No. 128.

Dexia Group Audit Charter

January 2013 Dexia Group Audit Charter The present Charter states the fundamental principles governing the internal audit function in the Dexia Group, describing its objectives, its role, responsibilities

January 2013 Dexia Group Audit Charter The present Charter states the fundamental principles governing the internal audit function in the Dexia Group, describing its objectives, its role, responsibilities

Planning an Audit 259

Planning an Audit 259 AU-C Section 300 Planning an Audit Source: SAS No. 122; SAS No. 128. Effective for audits of financial statements for periods ending on or after December 15, 2012. Introduction Scope

Planning an Audit 259 AU-C Section 300 Planning an Audit Source: SAS No. 122; SAS No. 128. Effective for audits of financial statements for periods ending on or after December 15, 2012. Introduction Scope

Performance Auditing

Auditing Standard AUS 806 (July 2002) Performance Auditing Prepared by the Auditing & Assurance Standards Board of the Australian Accounting Research Foundation Issued by the Australian Accounting Research

Auditing Standard AUS 806 (July 2002) Performance Auditing Prepared by the Auditing & Assurance Standards Board of the Australian Accounting Research Foundation Issued by the Australian Accounting Research

Companion Policy Acceptable Accounting Principles and Auditing Standards

Companion Policy 52-107 Acceptable Accounting Principles and Auditing Standards PART 1 INTRODUCTION AND DEFINITIONS 1.1 Introduction and Purpose 1.2 Multijurisdictional Disclosure System 1.3 Calculation

Companion Policy 52-107 Acceptable Accounting Principles and Auditing Standards PART 1 INTRODUCTION AND DEFINITIONS 1.1 Introduction and Purpose 1.2 Multijurisdictional Disclosure System 1.3 Calculation

Understanding a financial statement audit

www.pwc.com Understanding a financial statement audit May 2017 Understanding a financial statement audit 1 Preface Role of audit The need for companies financial statements 1 to be audited by an independent

www.pwc.com Understanding a financial statement audit May 2017 Understanding a financial statement audit 1 Preface Role of audit The need for companies financial statements 1 to be audited by an independent

International Forum of Independent Audit Regulators Report on 2013 Survey of Inspection Findings April 10, 2014

Executive Summary International Forum of Independent Audit Regulators Report on 2013 Survey of Inspection Findings April 10, 2014 This report summarizes the results of the second survey conducted by the

Executive Summary International Forum of Independent Audit Regulators Report on 2013 Survey of Inspection Findings April 10, 2014 This report summarizes the results of the second survey conducted by the

AICPA STANDARDS FOR PERFORMING AND REPORTING ON PEER REVIEWS. Effective for Peer Reviews Commencing on or After January 1, 2009

AICPA STANDARDS FOR PERFORMING AND REPORTING ON PEER REVIEWS Effective for Peer Reviews Commencing on or After January 1, 2009 Guidance for Performing and Reporting on Peer Reviews Copyright 2008 by American

AICPA STANDARDS FOR PERFORMING AND REPORTING ON PEER REVIEWS Effective for Peer Reviews Commencing on or After January 1, 2009 Guidance for Performing and Reporting on Peer Reviews Copyright 2008 by American

FRAUD RISK FACTORS CHECKLIST (Source: New AU Section 240, Appendix A)

") Page 136 of 174 FRAUD RISK FACTORS CHECKLIST (Source: New AU Section 240, Appendix A) RECOGNIZING RISK FACTORS THAT SHOULD GET YOUR ATTENTION How to use the checklist: 1. Review this checklist towards

Page 136 of 174 FRAUD RISK FACTORS CHECKLIST (Source: New AU Section 240, Appendix A) RECOGNIZING RISK FACTORS THAT SHOULD GET YOUR ATTENTION How to use the checklist: 1. Review this checklist towards

Report on Inspection of Deloitte LLP (Headquartered in Toronto, Canada) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2014 (Headquartered in Toronto, Canada) Issued by the Public Company Accounting Oversight

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2014 (Headquartered in Toronto, Canada) Issued by the Public Company Accounting Oversight

Working with the external auditor

Working with the external auditor 0 Audit committees have an essential role to play in ensuring the integrity and transparency of corporate reporting. The PwC Audit Committee Guide is designed to help

Working with the external auditor 0 Audit committees have an essential role to play in ensuring the integrity and transparency of corporate reporting. The PwC Audit Committee Guide is designed to help

INTERNATIONAL STANDARD ON AUDITING 505 EXTERNAL CONFIRMATIONS CONTENTS

INTERNATIONAL STANDARD ON AUDITING 505 EXTERNAL CONFIRMATIONS (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph Introduction... 1-6 Relationship

INTERNATIONAL STANDARD ON AUDITING 505 EXTERNAL CONFIRMATIONS (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph Introduction... 1-6 Relationship

Report on Inspection of KPMG Auditores Consultores Ltda. (Headquartered in Santiago, Republic of Chile)

") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Santiago, Republic of Chile) Issued by the Public Company Accounting

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Santiago, Republic of Chile) Issued by the Public Company Accounting

Summary findings inspection quality of statutory audits Big 4 firms

Page 1 of 6 Summary findings inspection quality of statutory audits Big 4 firms Between April 2013 and the end of July 2014, the Netherlands Authority for the Financial Markets (AFM) carried out regular

Page 1 of 6 Summary findings inspection quality of statutory audits Big 4 firms Between April 2013 and the end of July 2014, the Netherlands Authority for the Financial Markets (AFM) carried out regular

Report on. Issued by the. Public Company Accounting Oversight Board. June 16, 2016 THIS IS A PUBLIC VERSION OF A PCAOB INSPECTION REPORT

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 Inspection of Paredes, Zaldívar, Burga & Asociados Sociedad Civil de (Headquartered

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 Inspection of Paredes, Zaldívar, Burga & Asociados Sociedad Civil de (Headquartered

Initial Professional Development Technical Competence (Revised)

") IFAC Board Final Pronouncement January Exposure 2014 Draft October 2011 Comments due: February 29, 2012 International Education Standard (IES) 2 Initial Professional Development Technical Competence (Revised)

IFAC Board Final Pronouncement January Exposure 2014 Draft October 2011 Comments due: February 29, 2012 International Education Standard (IES) 2 Initial Professional Development Technical Competence (Revised)

PHILIPPINE STANDARD ON AUDITING 300 PLANNING AN AUDIT OF FINANCIAL STATEMENTS CONTENTS

PHILIPPINE STANDARD ON AUDITING 300 PLANNING AN AUDIT OF FINANCIAL STATEMENTS (Effective for audits of financial statements for periods beginning on or after December 15, 2009) CONTENTS Paragraph Introduction

PHILIPPINE STANDARD ON AUDITING 300 PLANNING AN AUDIT OF FINANCIAL STATEMENTS (Effective for audits of financial statements for periods beginning on or after December 15, 2009) CONTENTS Paragraph Introduction

STANDARD ON QUALITY CONTROL (SQC) 1

1") STANDARD ON QUALITY CONTROL (SQC) 1 Quality control for firms that perform audits and reviews of historical financial information, and other assurance and related services engagements Presented by: KHUSHROO

STANDARD ON QUALITY CONTROL (SQC) 1 Quality control for firms that perform audits and reviews of historical financial information, and other assurance and related services engagements Presented by: KHUSHROO

Section 22. Scope of section. Accreditation. Eligibility Criteria

Section 22 Accreditation of Audit Firms, Reporting Accountants, Reporting Accountant Specialists and IFRS Advisers to provide accounting and/or advisory services to applicant issuers Scope of section The

Section 22 Accreditation of Audit Firms, Reporting Accountants, Reporting Accountant Specialists and IFRS Advisers to provide accounting and/or advisory services to applicant issuers Scope of section The

AICPA Peer Review Program Compliance: Responding to Latest Developments

AICPA Peer Review Program Compliance: Responding to Latest Developments TUESDAY, JUNE 24, 2014 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for 2 CPE credit hours. To earn credit

AICPA Peer Review Program Compliance: Responding to Latest Developments TUESDAY, JUNE 24, 2014 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for 2 CPE credit hours. To earn credit

Annexure B Section 22

Annexure B Section 22 Accreditation of Audit Firms, Reporting Accountants, Reporting Accountant Specialists and IFRS Advisers to provide accounting and/or advisory services to applicant issuers Scope of

Annexure B Section 22 Accreditation of Audit Firms, Reporting Accountants, Reporting Accountant Specialists and IFRS Advisers to provide accounting and/or advisory services to applicant issuers Scope of

Guidance: Transition for Logbooks for RCA Applications under RG 180 Auditor registration (2016)

") Guidance: Transition for Logbooks for RCA Applications under RG 180 Auditor registration (2016) In order to register as a Registered Company Auditor (RCA), an applicant must meet the requirements of s.1280

Guidance: Transition for Logbooks for RCA Applications under RG 180 Auditor registration (2016) In order to register as a Registered Company Auditor (RCA), an applicant must meet the requirements of s.1280

Report on Inspection of KAP Purwantono, Sungkoro & Surja (Headquartered in Jakarta, Republic of Indonesia)

") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 Inspection of KAP Purwantono, (Headquartered in Jakarta, Republic of Indonesia)

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 Inspection of KAP Purwantono, (Headquartered in Jakarta, Republic of Indonesia)

Basel Committee on Banking Supervision. Consultative Document. External audits of banks. Issued for comment by 21 June 2013

Basel Committee on Banking Supervision Consultative Document External audits of banks Issued for comment by 21 June 2013 March 2013 This publication is available on the BIS website (www.bis.org). Bank

Basel Committee on Banking Supervision Consultative Document External audits of banks Issued for comment by 21 June 2013 March 2013 This publication is available on the BIS website (www.bis.org). Bank

AUDIT RISK ASSESSMENT AND RESPONSES TO ASSESSED RISK BY Geoffrey Byamugisha Partner, Ernst & Young. Lessons on Audit Risk. Responding to fraud risk

AUDIT RISK ASSESSMENT AND RESPONSES TO ASSESSED RISK BY Geoffrey Byamugisha Partner, Ernst & Young ICPAU Page 1 COURSE CONTENT Lessons on Audit Risk Identification of audit risk and audit risk assessment

AUDIT RISK ASSESSMENT AND RESPONSES TO ASSESSED RISK BY Geoffrey Byamugisha Partner, Ernst & Young ICPAU Page 1 COURSE CONTENT Lessons on Audit Risk Identification of audit risk and audit risk assessment

SA 230 Audit Documentation SA 300 Planning an Audit of FS

ICAI YMEC & AASB Hosted by WIRC of ICAI Workshop on Auditing Standards SA 230 Audit Documentation SA 300 Planning an Audit of FS 22 nd November 2014 Disclaimer These are my personal views and can not be

ICAI YMEC & AASB Hosted by WIRC of ICAI Workshop on Auditing Standards SA 230 Audit Documentation SA 300 Planning an Audit of FS 22 nd November 2014 Disclaimer These are my personal views and can not be

FOUNDATIONS IN ACCOUNTANCY Paper FAU (UK) Foundations in Audit (United Kingdom)

Foundations in Audit (United Kingdom)") Answers FOUNDATIONS IN ACCOUNTANCY Paper FAU (UK) Foundations in Audit (United Kingdom) June 2012 Answers Section A QUESTIONS 1 10 MULTIPLE CHOICE Question Answer See Note Below 1 A 1 2 D 2 3 C 3 4 B 4

Answers FOUNDATIONS IN ACCOUNTANCY Paper FAU (UK) Foundations in Audit (United Kingdom) June 2012 Answers Section A QUESTIONS 1 10 MULTIPLE CHOICE Question Answer See Note Below 1 A 1 2 D 2 3 C 3 4 B 4

Evaluating Internal Controls

A SSURANCE AND A DVISORY BUSINESS S ERVICES Fourth in the Series!@# Evaluating Internal Controls Evaluating Overall Effectiveness, Identifying Matters for Improvement, and Ongoing Assessment of Controls

A SSURANCE AND A DVISORY BUSINESS S ERVICES Fourth in the Series!@# Evaluating Internal Controls Evaluating Overall Effectiveness, Identifying Matters for Improvement, and Ongoing Assessment of Controls

Quality Control Review Checklist

Institute of Cost and Management Accountants of Pakistan Quality Control Review Checklist For Cost Audit Engagements Issued By Quality Assurance Board Table of Contents 1. PRE ENGAGEMENT ACTIVITIES...

Institute of Cost and Management Accountants of Pakistan Quality Control Review Checklist For Cost Audit Engagements Issued By Quality Assurance Board Table of Contents 1. PRE ENGAGEMENT ACTIVITIES...

Planning an Audit of Financial Statements

ISA 300 February 2008 International Standard on Auditing Planning an Audit of Financial Statements INTERNATIONAL STANDARD ON AUDITING 300 Planning an Audit of Financial Statements Explanatory Foreword

ISA 300 February 2008 International Standard on Auditing Planning an Audit of Financial Statements INTERNATIONAL STANDARD ON AUDITING 300 Planning an Audit of Financial Statements Explanatory Foreword

Using the Work of an Auditor s Specialist

Using the Work of an Auditor s Specialist 749 AU-C Section 620 Using the Work of an Auditor s Specialist Source: SAS No. 122. See section 9620 for interpretations of this section. Effective for audits

Using the Work of an Auditor s Specialist 749 AU-C Section 620 Using the Work of an Auditor s Specialist Source: SAS No. 122. See section 9620 for interpretations of this section. Effective for audits

CORPORATE GOVERNANCE KING III COMPLIANCE REGISTER 2017

CORPORATE GOVERNANCE KING III COMPLIANCE REGISTER 2017 This document has been prepared in terms of the JSE Listing Requirements and sets out the application of the 75 corporate governance principles by

CORPORATE GOVERNANCE KING III COMPLIANCE REGISTER 2017 This document has been prepared in terms of the JSE Listing Requirements and sets out the application of the 75 corporate governance principles by

Internal controls over Financial Reporting Key concepts. Presentation by Jayesh Gandhi at WIRC

Internal controls over Financial Reporting Key concepts Presentation by Jayesh Gandhi at WIRC Page 1 ICFR Key Concepts WIRC 28 May 2016 Agenda Scope and requirements Overview of internal controls as per

Internal controls over Financial Reporting Key concepts Presentation by Jayesh Gandhi at WIRC Page 1 ICFR Key Concepts WIRC 28 May 2016 Agenda Scope and requirements Overview of internal controls as per

General Policies & Procedures. SV 5.0 Clean Harbors Vendor Code of Business Conduct and Ethics

1. Purpose This Code is intended to govern the conduct of Clean Harbors, Inc. and all of its subsidiaries Vendors when doing business with or on behalf of Clean Harbors, Inc. For the purpose of this Code,

1. Purpose This Code is intended to govern the conduct of Clean Harbors, Inc. and all of its subsidiaries Vendors when doing business with or on behalf of Clean Harbors, Inc. For the purpose of this Code,

) ) ) ) ) ) ) ) ) ) ) )

) ) ) ) ) ) ) ) ) ) )") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org PROPOSED AUDITING STANDARD RELATED TO COMMUNICATIONS WITH AUDIT COMMITTEES AND RELATED AMENDMENTS

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org PROPOSED AUDITING STANDARD RELATED TO COMMUNICATIONS WITH AUDIT COMMITTEES AND RELATED AMENDMENTS

(Adopted by the Board of Directors on 13 May 2009 and amended on 24 September 2009, 13 September 2012 and 27 November 2013)

") Thomas Cook Group plc THE AUDIT COMMITTEE TERMS OF REFERENCE (Adopted by the Board of Directors on 13 May 2009 and amended on 24 September 2009, 13 September 2012 and 27 November 2013) Chairman and members

Thomas Cook Group plc THE AUDIT COMMITTEE TERMS OF REFERENCE (Adopted by the Board of Directors on 13 May 2009 and amended on 24 September 2009, 13 September 2012 and 27 November 2013) Chairman and members

AICPA Peer Review Program Compliance: Responding to Latest Developments

FOR LIVE PROGRAM ONLY AICPA Peer Review Program Compliance: Responding to Latest Developments WEDNESDAY, MAY 31, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved

FOR LIVE PROGRAM ONLY AICPA Peer Review Program Compliance: Responding to Latest Developments WEDNESDAY, MAY 31, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved

PROFESSIONAL LEVEL PART-A: OVERVIEW OF AUDITING AND ASSURANCE

SYLLABS 2016 Part-D Weightage Part-E Part-C Part-A PROFESSIONAL LEVEL P2 - Audit & Assurance Part-B Part-A Overview of Auditing and Assurance 15% Part-B Audit Planning 20% Part-C Internal Controls 20%

SYLLABS 2016 Part-D Weightage Part-E Part-C Part-A PROFESSIONAL LEVEL P2 - Audit & Assurance Part-B Part-A Overview of Auditing and Assurance 15% Part-B Audit Planning 20% Part-C Internal Controls 20%

Format and organization of GAGAS Auditor preparation of financials is a significant threat to independence 3 party arrangements in government State

The Yellow Book = GAGAS GAGAS = Generally Accepted Government Auditing Standards Overlay of Generally Accepted Auditing Standards (GAAS) issued by the Auditing Standards Board GAGAS contains the framework

The Yellow Book = GAGAS GAGAS = Generally Accepted Government Auditing Standards Overlay of Generally Accepted Auditing Standards (GAAS) issued by the Auditing Standards Board GAGAS contains the framework

AICPA STANDARDS FOR PERFORMING AND REPORTING ON PEER REVIEWS

December 2017 PRP Section 1000 AICPA STANDARDS FOR PERFORMING AND REPORTING ON PEER REVIEWS Notice to Readers In order to be admitted to or retain their membership in the AICPA, members of the AICPA who

December 2017 PRP Section 1000 AICPA STANDARDS FOR PERFORMING AND REPORTING ON PEER REVIEWS Notice to Readers In order to be admitted to or retain their membership in the AICPA, members of the AICPA who

The World Bank Audit Firm Assessment Questionnaire

The World Bank Audit Firm Assessment Questionnaire Assessment of audit firms in the Africa Region Background The Bank s financial management Bank Procedures (BP) and Operations Policy (OP) (BP/OP 10.00)

The World Bank Audit Firm Assessment Questionnaire Assessment of audit firms in the Africa Region Background The Bank s financial management Bank Procedures (BP) and Operations Policy (OP) (BP/OP 10.00)

Statements of Membership Obligations 1 7

IFAC Board Statements of Membership Obligations Issued April 2004 Statements of Membership Obligations 1 7 The mission of the International Federation of Accountants (IFAC) is to serve the public interest,

IFAC Board Statements of Membership Obligations Issued April 2004 Statements of Membership Obligations 1 7 The mission of the International Federation of Accountants (IFAC) is to serve the public interest,

Engagements to Perform. Agreed-Upon Procedures. Regarding Financial Information

Issued November 2004 Effective upon issue Hong Kong Standard on Related Services 4400 Engagements to Perform Agreed-Upon Procedures Regarding Financial Information ENGAGEMENTS TO PERFORM AGREED-UPON PROCEDURES

Issued November 2004 Effective upon issue Hong Kong Standard on Related Services 4400 Engagements to Perform Agreed-Upon Procedures Regarding Financial Information ENGAGEMENTS TO PERFORM AGREED-UPON PROCEDURES

Report on Inspection of PricewaterhouseCoopers Audit (Headquartered in Neuilly-Sur-Seine, French Republic)

") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Neuilly-Sur-Seine, French Republic) Issued by the Public Company

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Neuilly-Sur-Seine, French Republic) Issued by the Public Company

Auditing Standard 16

Certified Sarbanes-Oxley Expert Official Prep Course Part K Sarbanes Oxley Compliance Professionals Association (SOXCPA) The largest association of Sarbanes Oxley Professionals in the world Auditing Standard

Certified Sarbanes-Oxley Expert Official Prep Course Part K Sarbanes Oxley Compliance Professionals Association (SOXCPA) The largest association of Sarbanes Oxley Professionals in the world Auditing Standard

FREQUENTLY ASKED QUESTIONS ABOUT INTERNAL CONTROL OVER FINANCIAL REPORTING

FREQUENTLY ASKED QUESTIONS ABOUT INTERNAL CONTROL OVER FINANCIAL REPORTING Nature and Timing of the Reporting Requirement When must registrants begin to report on internal control over financial reporting?

FREQUENTLY ASKED QUESTIONS ABOUT INTERNAL CONTROL OVER FINANCIAL REPORTING Nature and Timing of the Reporting Requirement When must registrants begin to report on internal control over financial reporting?

Public Company Accounting Oversight Board

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2008 (Headquartered in New York, New York) Issued by the Public Company Accounting

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2008 (Headquartered in New York, New York) Issued by the Public Company Accounting

Special Considerations Audits of Group Financial Statements (Including the Work of Component Auditors)

") Special Considerations---Audits of Group Financial Statements 665 AU-C Section 600 Special Considerations Audits of Group Financial Statements (Including the Work of Component Auditors) Source: SAS No.

Special Considerations---Audits of Group Financial Statements 665 AU-C Section 600 Special Considerations Audits of Group Financial Statements (Including the Work of Component Auditors) Source: SAS No.

STANDING ADVISORY GROUP MEETING

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202)862-8430 www.pcaobus.org PROPOSAL TO RECONSIDER THE HIERARCHY OF AUDITING STANDARDS AND GUIDANCE NOVEMBER 17-18, 2004

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202)862-8430 www.pcaobus.org PROPOSAL TO RECONSIDER THE HIERARCHY OF AUDITING STANDARDS AND GUIDANCE NOVEMBER 17-18, 2004

Implementation Tool for Auditors

Implementation Tool for Auditors CANADIAN AUDITING STANDARDS (CAS) APRIL 2017 Using the Work of a Management s Expert STANDARD DISCUSSED CAS 500, Audit Evidence This Implementation Tool for Auditors (Tool)

Implementation Tool for Auditors CANADIAN AUDITING STANDARDS (CAS) APRIL 2017 Using the Work of a Management s Expert STANDARD DISCUSSED CAS 500, Audit Evidence This Implementation Tool for Auditors (Tool)

Practice Note 8 Engineers and Ethical Obligations

www.ipenz.nz Practice Note 8 Engineers and Ethical Obligations Engineering Practice ISSN 1176-0907 Version 2, October 2016 Preface The purpose of the Practice Note Engineers and Ethical Obligations is

www.ipenz.nz Practice Note 8 Engineers and Ethical Obligations Engineering Practice ISSN 1176-0907 Version 2, October 2016 Preface The purpose of the Practice Note Engineers and Ethical Obligations is

New auditing regime: checklist [1]

![New auditing regime: checklist [1]](/thumbs/75/72255631.jpg "New auditing regime: checklist [1]") Page 1 of 5 Published on AccountingWEB (http://www.accountingweb.co.uk) Home > New auditing regime: checklist New auditing regime: checklist [1] [2] published by Steve Collings [2] on Tue, 08/11/2011-16:32

Page 1 of 5 Published on AccountingWEB (http://www.accountingweb.co.uk) Home > New auditing regime: checklist New auditing regime: checklist [1] [2] published by Steve Collings [2] on Tue, 08/11/2011-16:32

3410N Assurance engagements relating to sustainability reports

3410N Assurance engagements relating to sustainability reports Royal NIVRA 3410N ASSURANCE ENGAGEMENTS RELATING TO SUSTAINABILITY REPORTS Introduction Scope of this Standard ( T1 and T2) 1. This Standard

3410N Assurance engagements relating to sustainability reports Royal NIVRA 3410N ASSURANCE ENGAGEMENTS RELATING TO SUSTAINABILITY REPORTS Introduction Scope of this Standard ( T1 and T2) 1. This Standard

Concepts Common to All Attestation Engagements

Concepts Common to All Attestation Engagements 1391 AT-C Section 105 Concepts Common to All Attestation Engagements Source: SSAE No. 18. Effective for practitioners' reports dated on or after May 1, 2017.

Concepts Common to All Attestation Engagements 1391 AT-C Section 105 Concepts Common to All Attestation Engagements Source: SSAE No. 18. Effective for practitioners' reports dated on or after May 1, 2017.

Internal Audit Quality Analysis Evaluation against the Standards International Standards for the Professional Practice of Internal Auditing (2017)

") Internal Audit Quality Analysis Evaluation against the Standards International Standards for the Professional Practice of Internal Auditing (2017) Assessor 1: Assessor 2: Date: Date: Legend: Generally

Internal Audit Quality Analysis Evaluation against the Standards International Standards for the Professional Practice of Internal Auditing (2017) Assessor 1: Assessor 2: Date: Date: Legend: Generally

The Auditor s Responses to Assessed Risks