Chapter 16. The auditors report

|

|

|

- Gwendolyn Sparks

- 5 years ago

- Views:

Transcription

1 Chapter 16 The auditors report

2 Learning objectives To explain the nature and importance of the audit report. To describe the various components of the audit report. To explain the nature of the auditor s responsibility for other information contained in the annual report. To discuss the nature of the assurance provided in the audit report in respect of information other than financial statements disclosed in the annual report. To describe the auditors responsibilities in respect of the directors report and the strategic report. To discuss the information provided in audit report about the auditor s work. To discuss when an emphasis of matter or other matter paragraph might be required in the audit report. To discuss the various forms of modified opinions and identify the circumstances under which each type would be issued by auditors. To outline the reason why auditors have started to include a disclaimer to third parties paragraph in the audit report. To outline auditors responsibilities for reporting on corporate governance issues. To outline the procedures the auditor will undertake to review the corporate governance statement. To describe the implications of electronic publication of the audit report. 2

3 Signing audit report completes audit process In signing audit report auditors communicate satisfaction or dissatisfaction with financial statements. If satisfied unmodified or clean opinion. If dissatisfied modified opinion (qualified opinions disclaimers of opinion opinions with emphasis of matter or other matter paragraph). FRC and APB earlier adopted auditing standards issued by IAASB, except ISA 700 and APB revised and issued in 2013 a clarified version of ISA 700 for use in the UK and Ireland. APB/FRC did adopt ISA 705 and ISA

4 The modified audit opinion main features Title To whom the report is addressed Identification of statements upon which the auditors are reporting Statement of auditors responsibilities Statement of directors responsibilities Scope of the audit of the financial statements The opinion on truth and fairness and compliance with CA 2006 and accounting standards Emphasis of matter or other matters paragraphs 4

Figure")

5 The unmodified opinion (1) Figure

Figure 16.")

6 The unmodified opinion (2) Figure 16.1 (continued) 6

Figure 16.")

7 The unmodified opinion (3) Figure 16.1 (continued) 7

8 The unmodified opinion (4) Figure 16.1 (continued) 8

9 Directors Report Companies Act 2006 requires a directors report to be prepared and for the auditor to report whether the information contained therein is consistent with the financial statements. Where the auditors consider that the directors report is inconsistent with the financial statements they should discuss the matter with the directors and try to get them to adjust either the directors report or the financial statements to remove the inconsistency. If the directors refuse and the auditors believe the inconsistency is material, the auditor is required to describe the inconsistency in a separate paragraph in their report. 9

10 Strategic Report Statutory instrument in 2013 states that all companies except small companies) should prepare a strategic report to inform users about the company and how successful the directors have been in promoting the success of the company. All strategic reports must contain the following information: A fair review of the company s business. A description of the principal risks and uncertainties facing the company. Quoted companies are required to disclose additional matters (see p 673-4) Auditors have, in their audit report, to provide a positive statement that the strategic report is consistent with the financial statements 10

11 Quoted companies additional audit requirements Explanations of audit work for companies complying with the UK Corporate Governance Code Directors remuneration Matters reported on by exception Corporate governance 11

12 Companies complying with the UK Corporate Governance Code: Explanations of audit work Since 2013 ISA 700 requires the following to be disclosed in the audit report: i. Description of the assessed risks of material misstatement highlighted by the auditor as having the greatest effect on: a) the overall audit strategy b) the allocation of resources in the audit c) directing the efforts of the audit team. ii. An explanation of how the auditor applied the concept of materiality in planning and performing the audit. iii. The audit report should provide an overview of the scope of the audit, identifying how they addressed the issues of risk and materiality. 12

13 Directors remuneration The Cos Act 2006 states quoted companies must prepare an annual directors remuneration report, and the auditors must ensure it is consistent with their knowledge of the company. They have specific responsibility for checking the accuracy and completeness of information in a table showing as a single figure total remuneration of each director and the amount of each component, such as salary, fees, benefits, deferred amounts, the value of shares received or share options, and pension input. If it has not been prepared in accordance with the Act, and is not in agreement with the accounting records and returns, they must give details in the audit report. Before doing this they should try to convince the directors/audit committee to include the correct information in the remuneration report. Since the remuneration report contains both an audited and an unaudited part they should ensure the two parts are adequately distinguished in the annual report. 13

14 Matters reported on by exception: FRC suggested wording We have nothing to report in respect of the following: Under the ISAs (UK and Ireland), we are required to report to you if, in our opinion, information in the annual report is: materially inconsistent with the information in the audited financial statements; or apparently materially incorrect based on, or materially inconsistent with our knowledge of the Group acquired in the course of performing our audit; or is otherwise misleading. In particular, we are required to consider whether we have identified any inconsistencies between our knowledge acquired during the audit and the directors statement that they consider the annual report is fair, balanced and understandable and whether the annual report appropriately discloses those matters that we communicated to the audit committee which we consider should have been disclosed. 14

15 Emphasis of matter paragraph Likely to be rare. A modification but not a qualification, but paragraph refers to financial statement note where matter is described: An uncertainty relating to the future outcome of exceptional litigation or regulatory action or ability to continue as a going concern Early application of a new accounting standard with pervasive effect in advance of its effective date. A major catastrophe with significant effect on the entity s financial position. 15

16 Emphasis of Matter uncertain outcome of potential litigation In forming our opinion on the financial statements, which is not modified, we have considered the adequacy of the disclosures made in note 22 to the financial statements concerning the uncertain outcome of the potential litigation following the receipt of two letters before claim from legal advisors to Craig Whyte and Aidan Earley. The Company commissioned an independent investigation to investigate the first letter before claim, which was concluded on 17 May On 30 May 2013, following the receipt of a second letter before claim, the Company announced that the investigation had been concluded. The Company is satisfied that a thorough investigation was conducted despite the inherent limitations of a private inquiry, and considers the claims have no legal merit. The Company has also engaged the services of Allen and Overy to defend against these possible claims, and the Company has had no communication with Messrs Whyte & Earley or their legal advisers since 30 May The ultimate outcome of this matter cannot presently be determined, and accordingly no adjustments have been made to these financial statements as a result of this matter. 16

17 Other matter paragraph examples MAY BE QUALIFICATION where limitation of scope imposed by management is pervasive but auditor has not withdrawn from audit engagement should disclaim an opinion and explain in other matter paragraph why not possible to withdraw OR NOT A QUALIFICATION where an entity prepares two sets of financial statements in compliance with two accounting frameworks, both appropriate, auditor may include an other matter paragraph stating they have issued an audit report on another set of financial statements prepared using a different Accounting Framework and that they issued an audit report on those statements. 17

18 Forms of modification Figure

19 Limitation of scope (1) Arises if auditors are not able to obtain all the evidence required to issue an unqualified opinion. May be material but not persuasive except for limitation see pages May be persuasive disclaimer see pages

")

20 Limitation of scope (2) 20

21 Limitation of scope (3) 21

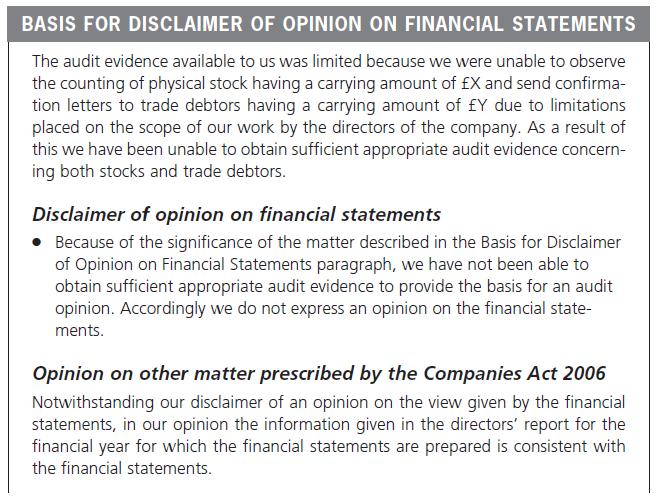

22 Disclaimer of responsibility(1) 22

23 Disclaimer of responsibility (2) 23

24 Disagreement Disagreement arises when auditors can form an opinion on a matter that differs from opinion of management. For instance: Inappropriate accounting policies Inappropriate application of accounting policies; or Inappropriate or inadequate disclosures. Material but not persuasive except for disagreement see page 691. Persuasive adverse opinion see page

25 Except for disagreement 25

26 Adverse opinion 26

27 Disclaimer of responsibility Suggested wording following the Bannerman case This report is made solely to the company s members, as a body, in accordance with Chapter 3 of Part 16 of the Companies Act Our audit work has been undertaken so that we might state to the company s members those matters we are required to state to them in an auditor s report and for no other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than the company and the company s members as a body, for our audit work, for this report, or for the opinions we have formed. 27

28 Reporting on corporate governance (1) Combined Code and Listing Rules set framework for responsibilities of directors/auditors. Rules require directors of listed companies to set out in the Annual Report how they have applied the Code principles in a way useful and understandable to shareholders. The directors include a statement on whether they have complied, and, where not, state which provisions have not been complied with and why. Listing Rules require auditors to review ten provisions in the companies statement of corporate governance. Of particular importance is the requirement for auditors to review whether the information in respect of going concern and internal control are appropriately disclosed. Code requires auditors to describe their reporting responsibilities usually in audit report. 28

29 Reporting on corporate governance (2) Where, a company does not comply with a Combined Code requirement, within scope of the auditors review, but has properly disclosed fact in its corporate governance statement, the auditors are not required to make reference to non-compliance. Auditor need not perform additional procedures to determine the appropriateness of reasons given for nondisclosure of a provision but merely that the directors description of the non-disclosure is adequate. Where auditors do not believe the disclosure of a departure from a provision of the code has been adequate, they need to report this fact in their audit report not a qualification but an other matter. 29

30 Example of non-qualification of corporate governance matters Rolls Royce 2013 Under the Listing Rules we are required to review: the directors statement set out on page 72, in relation to going concern; and the part of the corporate governance report on page 39 relating to the company s compliance with the nine provisions of the UK Corporate Governance Code (2010) specified for our review. We have nothing to report in respect of the above responsibilities Note: the 2012 Code increased to ten the number of provisions to be reviewed 30

Table")

31 Ten listing rules on which auditor is to report (1) Table

Table 16.")

32 Nine listing rules on which auditor is to report (2) Table 16.1 (continued) 32

Table 16.")

33 Nine listing rules on which auditor is to report (3) Table 16.1 (continued) 33

Table 16.")

34 Nine listing rules on which auditor is to report (3) Table 16.1 (continued) 34

35 Electronic publication of auditors reports Publication of audit reports on internet problematic: Information on the web is more easily changed. May not be apparent what information audited. Information can be accessed world-wide. Where a client intends to distribute its financial statements electronically auditors should: Review process by which electronic financial statements are derived from manually signed accounts. Check proposed electronic version is identical in content with manually signed accounts. Check conversion of manually signed accounts into an electronic form has not distorted overall presentation of the financial information. 35

36 Figure 16.1 Example of an unmodified audit opinion for a nonpublicly traded company

37 Figure 16.2 Forms of qualification matrix

Preparing an audit report for Limited Partnerships

AUDIT AND ASSURANCE FACULTY HELPSHEET This helpsheet was last updated in July 2017 and is based on the relevant laws and regulations that apply as at 1 June 2017. Preparing an audit report for Limited

AUDIT AND ASSURANCE FACULTY HELPSHEET This helpsheet was last updated in July 2017 and is based on the relevant laws and regulations that apply as at 1 June 2017. Preparing an audit report for Limited

Preparing an audit report for Limited Liability Partnerships (LLPs)

") AUDIT AND ASSURANCE FACULTY HELPSHEET This helpsheet was last updated in July 2017 and is based on the relevant laws and regulations that apply as at 1 June 2017. Preparing an audit report for Limited

AUDIT AND ASSURANCE FACULTY HELPSHEET This helpsheet was last updated in July 2017 and is based on the relevant laws and regulations that apply as at 1 June 2017. Preparing an audit report for Limited

Independent Auditor s report

Independent auditor s report to the members of Opinion on the financial statements of In our opinion the consolidated and Parent Company financial statements of : give a true and fair view of the state

Independent auditor s report to the members of Opinion on the financial statements of In our opinion the consolidated and Parent Company financial statements of : give a true and fair view of the state

FOR SELECTED ITEMS (Effective for all audits relating to accounting periods beginning on or after April 1, 2010)

") SA 501* AUDIT EVIDENCE SPECIFIC CONSIDERATIONS FOR SELECTED ITEMS (Effective for all audits relating to accounting periods beginning on or after April 1, 2010) Contents Paragraph(s) Introduction Scope

SA 501* AUDIT EVIDENCE SPECIFIC CONSIDERATIONS FOR SELECTED ITEMS (Effective for all audits relating to accounting periods beginning on or after April 1, 2010) Contents Paragraph(s) Introduction Scope

IAASB Main Agenda (December 2009) Agenda Item. Engagements to Compile Financial Information Issues and IAASB Task Force Proposals I.

Agenda Item. Engagements to Compile Financial Information Issues and IAASB Task Force Proposals I.") Agenda Item 3-A Engagements to Compile Financial Information Issues and IAASB Task Force Proposals I. Objective 1. The objective of this Paper is to consider significant issues to be addressed in the revision

Agenda Item 3-A Engagements to Compile Financial Information Issues and IAASB Task Force Proposals I. Objective 1. The objective of this Paper is to consider significant issues to be addressed in the revision

CLARIFIED INTERNATIONAL STANDARDS ON AUDITIING WHAT DOES IT MEAN FOR AUDITORS IN THE UK AND IRELAND?

CLARIFIED INTERNATIONAL STANDARDS ON AUDITIING WHAT DOES IT MEAN FOR AUDITORS IN THE UK AND IRELAND? By: Danielle McWall, BSc (Hons), ACA, MBA, MIIA. Examiner - P1 Auditing Background Following the many

CLARIFIED INTERNATIONAL STANDARDS ON AUDITIING WHAT DOES IT MEAN FOR AUDITORS IN THE UK AND IRELAND? By: Danielle McWall, BSc (Hons), ACA, MBA, MIIA. Examiner - P1 Auditing Background Following the many

SRI LANKA AUDITING STANDARD 501 AUDIT EVIDENCE SPECIFIC CONSIDERATIONS FOR SELECTED ITEMS CONTENTS

SRI LANKA AUDITING STANDARD 501 AUDIT EVIDENCE SPECIFIC CONSIDERATIONS FOR SELECTED ITEMS Introduction (Effective for audits of financial statements for periods beginning on or after 01 January 2012) CONTENTS

SRI LANKA AUDITING STANDARD 501 AUDIT EVIDENCE SPECIFIC CONSIDERATIONS FOR SELECTED ITEMS Introduction (Effective for audits of financial statements for periods beginning on or after 01 January 2012) CONTENTS

INTERNATIONAL STANDARD ON AUDITING 210 TERMS OF AUDIT ENGAGEMENTS CONTENTS

INTERNATIONAL STANDARD ON AUDITING 210 TERMS OF AUDIT ENGAGEMENTS (Effective for audits of financial statements for periods beginning on or after December 15, 2006. Appendix 2 contains conforming amendments

INTERNATIONAL STANDARD ON AUDITING 210 TERMS OF AUDIT ENGAGEMENTS (Effective for audits of financial statements for periods beginning on or after December 15, 2006. Appendix 2 contains conforming amendments

International Standard on Auditing (UK) 501

501") Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 501 Audit Evidence Specifi c Considerations for Selected Items The FRC s mission is to promote

Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 501 Audit Evidence Specifi c Considerations for Selected Items The FRC s mission is to promote

AUDIT EVIDENCE SPECIFIC CONSIDERATIONS FOR SELECTED ITEM SRI LANKA AUDITING STANDARD 501 AUDIT EVIDENCE SPECIFIC CONSIDERATIONS FOR SELECTED ITEMS

SRI LANKA AUDITING STANDARD 501 AUDIT EVIDENCE SPECIFIC CONSIDERATIONS FOR SELECTED ITEMS (Effective for audits of financial statements for periods beginning on or after 01 January 2014) CONTENTS Paragraph

SRI LANKA AUDITING STANDARD 501 AUDIT EVIDENCE SPECIFIC CONSIDERATIONS FOR SELECTED ITEMS (Effective for audits of financial statements for periods beginning on or after 01 January 2014) CONTENTS Paragraph

International Standard on Auditing (Ireland) 501 Audit Evidence Specific Considerations for Selected Items

501 Audit Evidence Specific Considerations for Selected Items") International Standard on Auditing (Ireland) 501 Audit Evidence Specific Considerations for Selected Items MISSION To contribute to Ireland having a strong regulatory environment in which to do business

International Standard on Auditing (Ireland) 501 Audit Evidence Specific Considerations for Selected Items MISSION To contribute to Ireland having a strong regulatory environment in which to do business

IAASB Agenda Item (September 2008) Page Agenda Item (MARKED FROM EXPOSURE DRAFT)

Page Agenda Item (MARKED FROM EXPOSURE DRAFT)") IAASB Agenda Item (September 2008) Page 2008 1777 Agenda Item 4-B (MARKED FROM EXPOSURE DRAFT) PROPOSED INTERNATIONAL STANDARD ON AUDITING 501 (REDRAFTED) AUDIT EVIDENCE SPECIFIC CONSIDERATIONS FOR SELECTED

IAASB Agenda Item (September 2008) Page 2008 1777 Agenda Item 4-B (MARKED FROM EXPOSURE DRAFT) PROPOSED INTERNATIONAL STANDARD ON AUDITING 501 (REDRAFTED) AUDIT EVIDENCE SPECIFIC CONSIDERATIONS FOR SELECTED

File No: PERMANENT AUDIT FILE INDEX Annual update confirmation. Business details 1. Background to client

Client: Year/Period End: PERMANENT AUDIT FILE INDEX Annual update confirmation Business details 1. Background to client 2. Financial History 3. Register of laws and regulations 4. Related parties 5. Group

Client: Year/Period End: PERMANENT AUDIT FILE INDEX Annual update confirmation Business details 1. Background to client 2. Financial History 3. Register of laws and regulations 4. Related parties 5. Group

INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 501. Audit Evidence Specific Considerations for Selected Items (ISA (NZ) 501)

501. Audit Evidence Specific Considerations for Selected Items (ISA (NZ) 501)") Issued 07/11 INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 501 Audit Evidence Specific Considerations for Selected Items (ISA (NZ) 501) Issued July 2011 Effective for audits of historical financial

Issued 07/11 INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 501 Audit Evidence Specific Considerations for Selected Items (ISA (NZ) 501) Issued July 2011 Effective for audits of historical financial

INTERNATIONAL STANDARD ON AUDITING (IRELAND) 210 AGREEING THE TERMS OF AUDIT ENGAGEMENTS

210 AGREEING THE TERMS OF AUDIT ENGAGEMENTS") INTERNATIONAL STANDARD ON AUDITING (IRELAND) 210 AGREEING THE TERMS OF AUDIT ENGAGEMENTS MISSION To contribute to Ireland having a strong regulatory environment in which to do business by supervising and

INTERNATIONAL STANDARD ON AUDITING (IRELAND) 210 AGREEING THE TERMS OF AUDIT ENGAGEMENTS MISSION To contribute to Ireland having a strong regulatory environment in which to do business by supervising and

INTERNATIONAL STANDARD ON AUDITING 260 COMMUNICATION WITH THOSE CHARGED WITH GOVERNANCE CONTENTS

Introduction INTERNATIONAL STANDARD ON AUDITING 260 COMMUNICATION WITH THOSE CHARGED WITH GOVERNANCE (Effective for audits of financial statements for periods beginning on or after December 15, 2009) +

Introduction INTERNATIONAL STANDARD ON AUDITING 260 COMMUNICATION WITH THOSE CHARGED WITH GOVERNANCE (Effective for audits of financial statements for periods beginning on or after December 15, 2009) +

INTERNATIONAL STANDARD ON AUDITING (UK AND IRELAND) 505 EXTERNAL CONFIRMATIONS

505 EXTERNAL CONFIRMATIONS") INTERNATIONAL STANDARD ON AUDITING (UK AND IRELAND) 505 Introduction EXTERNAL CONFIRMATIONS (Effective for audits of financial statements for periods ending on or after 15 December 2010) CONTENTS Paragraph

INTERNATIONAL STANDARD ON AUDITING (UK AND IRELAND) 505 Introduction EXTERNAL CONFIRMATIONS (Effective for audits of financial statements for periods ending on or after 15 December 2010) CONTENTS Paragraph

INTERNATIONAL STANDARD ON AUDITING 402 AUDIT CONSIDERATIONS RELATING TO ENTITIES USING SERVICE ORGANIZATIONS CONTENTS

INTERNATIONAL STANDARD ON 402 AUDIT CONSIDERATIONS RELATING TO ENTITIES (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph Introduction...

INTERNATIONAL STANDARD ON 402 AUDIT CONSIDERATIONS RELATING TO ENTITIES (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph Introduction...

SA 210 (REVISED) AGREEING THE TERMS OF AUDIT ENGAGEMENTS (EFFECTIVE FOR ALL AUDITS RELATING TO ACCOUNTING PERIODS BEGINNING ON OR AFTER APRIL 1, 2010)

AGREEING THE TERMS OF AUDIT ENGAGEMENTS (EFFECTIVE FOR ALL AUDITS RELATING TO ACCOUNTING PERIODS BEGINNING ON OR AFTER APRIL 1, 2010)") Part I : Engagement and Quality Control Standards I.53 SA 210 (REVISED) AGREEING THE TERMS OF AUDIT ENGAGEMENTS (EFFECTIVE FOR ALL AUDITS RELATING TO ACCOUNTING PERIODS BEGINNING ON OR AFTER APRIL 1, 2010)

Part I : Engagement and Quality Control Standards I.53 SA 210 (REVISED) AGREEING THE TERMS OF AUDIT ENGAGEMENTS (EFFECTIVE FOR ALL AUDITS RELATING TO ACCOUNTING PERIODS BEGINNING ON OR AFTER APRIL 1, 2010)

THE IFRS WORKSHOP. Hilton Hotel. Saturday, 11 February /02/2017 Uphold Public Interest

THE IFRS WORKSHOP Hilton Hotel Saturday, 11 February 2017 11/02/2017 Uphold Public Interest 2 1. 2. 3. 4. 5. 6. 7. OVERVIEW WHICH REPORTS ARE AFFECTED NEW AND REVISED STANDARDS KAM ISA 720 REVISED ETHICS

THE IFRS WORKSHOP Hilton Hotel Saturday, 11 February 2017 11/02/2017 Uphold Public Interest 2 1. 2. 3. 4. 5. 6. 7. OVERVIEW WHICH REPORTS ARE AFFECTED NEW AND REVISED STANDARDS KAM ISA 720 REVISED ETHICS

McGraw-Hill/Irwin. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 12 Reports on Audited Financial Statements The television industry doesn t like to see the complexity of

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 12 Reports on Audited Financial Statements The television industry doesn t like to see the complexity of

PGDBFS 103 International Financial Accounting and Policy (IFAP)

") June 2018 PGDBFS 103 International Financial Accounting and Policy (IFAP) Tutorial 09: Comparative International Auditing and Corporate Governance Malinda Boyagoda BSc. Business Admin (USJP), ACA, ACMA,

June 2018 PGDBFS 103 International Financial Accounting and Policy (IFAP) Tutorial 09: Comparative International Auditing and Corporate Governance Malinda Boyagoda BSc. Business Admin (USJP), ACA, ACMA,

CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a. AUDITING THEORY Risk Assessment and Response to Assessed Risks

Page 1 of 7 CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a Related PSAs: PSA 400, 315 and 330 AUDITING THEORY Risk Assessment and Response to Assessed Risks 1. Which of the following is correct statement?

Page 1 of 7 CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a Related PSAs: PSA 400, 315 and 330 AUDITING THEORY Risk Assessment and Response to Assessed Risks 1. Which of the following is correct statement?

APB ETHICAL STANDARD 4 (REVISED) FEES, REMUNERATION AND EVALUATION POLICIES, LITIGATION, GIFTS AND HOSPITALITY

FEES, REMUNERATION AND EVALUATION POLICIES, LITIGATION, GIFTS AND HOSPITALITY") APB ETHICAL STANDARD 4 (REVISED) FEES, REMUNERATION AND EVALUATION POLICIES, LITIGATION, GIFTS AND HOSPITALITY (Revised December 2010) Contents paragraph Introduction 1-4 Fees 5-43 Remuneration and evaluation

APB ETHICAL STANDARD 4 (REVISED) FEES, REMUNERATION AND EVALUATION POLICIES, LITIGATION, GIFTS AND HOSPITALITY (Revised December 2010) Contents paragraph Introduction 1-4 Fees 5-43 Remuneration and evaluation

Standards for Investment Reporting

January 2006 Standards for Investment Reporting 4000 INVESTMENT REPORTING STANDARDS APPLICABLE TO PUBLIC REPORTING ENGAGEMENTS ON PRO FORMA FINANCIAL INFORMATION LIMITED The Auditing Practices Board Limited,

January 2006 Standards for Investment Reporting 4000 INVESTMENT REPORTING STANDARDS APPLICABLE TO PUBLIC REPORTING ENGAGEMENTS ON PRO FORMA FINANCIAL INFORMATION LIMITED The Auditing Practices Board Limited,

Amounts posted to trade receivables were not related to valid sales.

SECTION A CASE QUESTIONS (Total: 50 marks) Answer 1(a) The balance of trade receivables as at 30 June 2014 significantly increased when compared to that of 31 December 2013, which did not match with the

SECTION A CASE QUESTIONS (Total: 50 marks) Answer 1(a) The balance of trade receivables as at 30 June 2014 significantly increased when compared to that of 31 December 2013, which did not match with the

3. STRUCTURING ASSURANCE ENGAGEMENTS

3. STRUCTURING ASSURANCE ENGAGEMENTS How do standards and guidance help professional accountants provide assurance? What are the practical considerations when structuring an assurance engagement? 3. STRUCTURING

3. STRUCTURING ASSURANCE ENGAGEMENTS How do standards and guidance help professional accountants provide assurance? What are the practical considerations when structuring an assurance engagement? 3. STRUCTURING

IAASB Main Agenda (December 2011) Agenda Item

Agenda Item") Engagement Level Audit Quality Exhibiting appropriate values, ethics and attitudes; Agenda Item 6-B 1. An audit of an entity s financial statements involves independent auditors gathering sufficient appropriate

Engagement Level Audit Quality Exhibiting appropriate values, ethics and attitudes; Agenda Item 6-B 1. An audit of an entity s financial statements involves independent auditors gathering sufficient appropriate

INTERNATIONAL STANDARD ON AUDITING 580 WRITTEN REPRESENTATIONS CONTENTS

INTERNATIONAL STANDARD ON AUDITING 580 WRITTEN REPRESENTATIONS (Effective for audits of financial statements for periods beginning on or after December 15, 2009) CONTENTS Paragraph Introduction Scope of

INTERNATIONAL STANDARD ON AUDITING 580 WRITTEN REPRESENTATIONS (Effective for audits of financial statements for periods beginning on or after December 15, 2009) CONTENTS Paragraph Introduction Scope of

evidence explained Chapter 6 The search for

Chapter 6 The search for evidence explained Learning objectives Explain why the audit evidence search is a central concept of auditing. Identify the stages of the audit process and show that evidence has

Chapter 6 The search for evidence explained Learning objectives Explain why the audit evidence search is a central concept of auditing. Identify the stages of the audit process and show that evidence has

AUDIT COMMITTEE. each member must be financially literate (as determined by the Board);

;") AUDIT COMMITTEE 1. Membership and Quorum a minimum of five directors appointed by the Board, one of whom must be the chair of the HR and Compensation Committee; only Independent directors, as determined

AUDIT COMMITTEE 1. Membership and Quorum a minimum of five directors appointed by the Board, one of whom must be the chair of the HR and Compensation Committee; only Independent directors, as determined

REGISTERED CANDIDATE AUDITOR (RCA) TECHNICAL COMPETENCE REQUIREMENTS

TECHNICAL COMPETENCE REQUIREMENTS") REGISTERED CANDIDATE AUDITOR (RCA) TECHNICAL COMPETENCE REQUIREMENTS 1. Context After completion of the recognised training contract, a period of specialisation is required, appropriate to the level required

REGISTERED CANDIDATE AUDITOR (RCA) TECHNICAL COMPETENCE REQUIREMENTS 1. Context After completion of the recognised training contract, a period of specialisation is required, appropriate to the level required

International Standard on Auditing (UK) 620 (Revised June 2016)

620 (Revised June 2016)") Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 620 (Revised June 2016) Using the Work of an Auditor s Expert The FRC s mission is to promote

Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 620 (Revised June 2016) Using the Work of an Auditor s Expert The FRC s mission is to promote

Performance Auditing

Auditing Standard AUS 806 (July 2002) Performance Auditing Prepared by the Auditing & Assurance Standards Board of the Australian Accounting Research Foundation Issued by the Australian Accounting Research

Auditing Standard AUS 806 (July 2002) Performance Auditing Prepared by the Auditing & Assurance Standards Board of the Australian Accounting Research Foundation Issued by the Australian Accounting Research

Standards on Review Engagements (SREs) E- 1220

E- 1220") Standards on Review Engagements (SREs) E- 1220 E- 1221 Engagement Standards Standards on Review Engagements SRE 2400, Engagements to Review Financial Statements (April 1, 2010) SRE 2410, Review of Interim

Standards on Review Engagements (SREs) E- 1220 E- 1221 Engagement Standards Standards on Review Engagements SRE 2400, Engagements to Review Financial Statements (April 1, 2010) SRE 2410, Review of Interim

Auditing & Assurance Services, 7e (Louwers) Chapter 2 Professional Standards

Chapter 2 Professional Standards") Auditing & Assurance Services, 7e (Louwers) Chapter 2 Professional Standards 1) Control risk is A) the probability that a material misstatement could not be prevented or detected by the entity's internal

Auditing & Assurance Services, 7e (Louwers) Chapter 2 Professional Standards 1) Control risk is A) the probability that a material misstatement could not be prevented or detected by the entity's internal

INTERNATIONAL STANDARD ON AUDITING 500 AUDIT EVIDENCE CONTENTS

INTERNATIONAL STANDARD ON 500 AUDIT EVIDENCE (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph Introduction... 1-2 Concept of Audit Evidence...

INTERNATIONAL STANDARD ON 500 AUDIT EVIDENCE (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph Introduction... 1-2 Concept of Audit Evidence...

IAASB Main Agenda (March 2005) Page Agenda Item 12-C

Page Agenda Item 12-C") IAASB Main Agenda (March 2005) Page 2005 429 Agenda Item 12-C [ISA AND IAPS SPLIT] PROPOSED INTERNATIONAL AUDITING PRACTICE STATEMENT XXX THE APPLICATION OF INTERNATIONAL STANDARDS ON AUDITING IN AN AUDIT

IAASB Main Agenda (March 2005) Page 2005 429 Agenda Item 12-C [ISA AND IAPS SPLIT] PROPOSED INTERNATIONAL AUDITING PRACTICE STATEMENT XXX THE APPLICATION OF INTERNATIONAL STANDARDS ON AUDITING IN AN AUDIT

) ) ) ) ) ) ) ) ) ) ) )

) ) ) ) ) ) ) ) ) ) )") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org PROPOSED AUDITING STANDARD RELATED TO COMMUNICATIONS WITH AUDIT COMMITTEES AND RELATED AMENDMENTS

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org PROPOSED AUDITING STANDARD RELATED TO COMMUNICATIONS WITH AUDIT COMMITTEES AND RELATED AMENDMENTS

May 3, To the Jail Board Members and Management Western Tidewater Regional Jail Authority 2402 Godwin Blvd Suffolk, Virginia 23434

A PROFESSIONAL LIMITED LIABILITY COMPANY CERTIFIED PUBLIC ACCOUNTANTS May 3, 2016 To the Jail Board Members and Management Western Tidewater Regional Jail Authority 2402 Godwin Blvd Suffolk, Virginia 23434

A PROFESSIONAL LIMITED LIABILITY COMPANY CERTIFIED PUBLIC ACCOUNTANTS May 3, 2016 To the Jail Board Members and Management Western Tidewater Regional Jail Authority 2402 Godwin Blvd Suffolk, Virginia 23434

Terms of Engagement 105. Source: SAS No Effective for audits of financial statements for periods ending on or after December 15, 2012.

Terms of Engagement 105 AU-C Section 210 Terms of Engagement Source: SAS No. 122. Effective for audits of financial statements for periods ending on or after December 15, 2012. Introduction Scope of This

Terms of Engagement 105 AU-C Section 210 Terms of Engagement Source: SAS No. 122. Effective for audits of financial statements for periods ending on or after December 15, 2012. Introduction Scope of This

Using the Work. of an Expert. HKSA 620 Issued June 2005

Issued June 2005 Effective for audits of financial statements for periods beginning on or after 15 December 2004 Hong Kong Standard on Auditing 620 Using the Work of an Expert HONG KONG STANDARD ON AUDITING

Issued June 2005 Effective for audits of financial statements for periods beginning on or after 15 December 2004 Hong Kong Standard on Auditing 620 Using the Work of an Expert HONG KONG STANDARD ON AUDITING

Audit Evidence. ISA 500 Issued December International Standard on Auditing

Issued December 2007 International Standard on Auditing Audit Evidence The Malaysian Institute of Certified Public Accountants (Institut Akauntan Awam Bertauliah Malaysia) INTERNATIONAL STANDARD ON AUDITING

Issued December 2007 International Standard on Auditing Audit Evidence The Malaysian Institute of Certified Public Accountants (Institut Akauntan Awam Bertauliah Malaysia) INTERNATIONAL STANDARD ON AUDITING

INTERNATIONAL STANDARD ON AUDITING 620 USING THE WORK OF AN AUDITOR S EXPERT CONTENTS

INTERNATIONAL STANDARD ON 620 USING THE WORK OF AN AUDITOR S EXPERT (Effective for audits of financial statements for periods beginning on or after December 15, 2009) CONTENTS Paragraph Introduction Scope

INTERNATIONAL STANDARD ON 620 USING THE WORK OF AN AUDITOR S EXPERT (Effective for audits of financial statements for periods beginning on or after December 15, 2009) CONTENTS Paragraph Introduction Scope

STATEMENT OF AUDITING STANDARDS 500 AUDIT EVIDENCE

STATEMENT OF AUDITING STANDARDS 500 AUDIT EVIDENCE (Issued January 2004) Contents Paragraphs Introduction 1-2 Concept of Audit Evidence 3-6 Sufficient Appropriate Audit Evidence 7-14 The Use of Assertions

STATEMENT OF AUDITING STANDARDS 500 AUDIT EVIDENCE (Issued January 2004) Contents Paragraphs Introduction 1-2 Concept of Audit Evidence 3-6 Sufficient Appropriate Audit Evidence 7-14 The Use of Assertions

International Standard on Auditing (Ireland) 402 Audit Considerations Relating to an Entity using a Service Organisation

402 Audit Considerations Relating to an Entity using a Service Organisation") International Standard on Auditing (Ireland) 402 Audit Considerations Relating to an Entity using a Service Organisation MISSION To contribute to Ireland having a strong regulatory environment in which

International Standard on Auditing (Ireland) 402 Audit Considerations Relating to an Entity using a Service Organisation MISSION To contribute to Ireland having a strong regulatory environment in which

IAASB Main Agenda (December 2004) Page Agenda Item

Page Agenda Item") IAASB Main Agenda (December 2004) Page 2004 2159 Agenda Item 7-B PROPOSED INTERNATIONAL STANDARD ON AUDITING XXX THE AUDIT OF GROUP FINANCIAL STATEMENTS CONTENTS Paragraph Introduction... 1-3 Definitions...

IAASB Main Agenda (December 2004) Page 2004 2159 Agenda Item 7-B PROPOSED INTERNATIONAL STANDARD ON AUDITING XXX THE AUDIT OF GROUP FINANCIAL STATEMENTS CONTENTS Paragraph Introduction... 1-3 Definitions...

Auditing Standard for Islamic Financial Institutions No. 6

Auditing Standard for Islamic Financial Institutions No. 6 External Shari ah Audit (Independent Assurance Engagement on an Islamic Financial Institution s Compliance with Shari ah Principles and Rules)

Auditing Standard for Islamic Financial Institutions No. 6 External Shari ah Audit (Independent Assurance Engagement on an Islamic Financial Institution s Compliance with Shari ah Principles and Rules)

International Standard on Auditing (UK) 220 (Revised June 2016)

220 (Revised June 2016)") Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 220 (Revised June 2016) Quality Control for an Audit of Financial Statements The FRC is responsible

Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 220 (Revised June 2016) Quality Control for an Audit of Financial Statements The FRC is responsible

Reporting on an Examination of Controls at a Service Organization Relevant to User Entities Internal Control Over Financial Reporting

Reporting on an Examination of Controls at a Service Organization 1621 AT-C Section 320 Reporting on an Examination of Controls at a Service Organization Relevant to User Entities Internal Control Over

Reporting on an Examination of Controls at a Service Organization 1621 AT-C Section 320 Reporting on an Examination of Controls at a Service Organization Relevant to User Entities Internal Control Over

Informa PLC TERMS OF REFERENCE AUDIT COMMITTEE. Adopted by the Board on

Informa PLC TERMS OF REFERENCE AUDIT COMMITTEE Adopted by the Board on 12 th December 2017 CONTENTS Constitution and Purpose... 1 1. Membership... 1 2. Secretary... 3 3. Quorum... 3 4. Frequency of Meetings...

Informa PLC TERMS OF REFERENCE AUDIT COMMITTEE Adopted by the Board on 12 th December 2017 CONTENTS Constitution and Purpose... 1 1. Membership... 1 2. Secretary... 3 3. Quorum... 3 4. Frequency of Meetings...

ISA 230, Audit Documentation

International Auditing and Assurance Standards Board Exposure Draft December 2006 Comments are requested by March 31, 2007 Proposed Redrafted International Standard on Auditing ISA 230, Audit Documentation

International Auditing and Assurance Standards Board Exposure Draft December 2006 Comments are requested by March 31, 2007 Proposed Redrafted International Standard on Auditing ISA 230, Audit Documentation

Financial Reporting Council BDO LLP AUDIT QUALITY INSPECTION

Financial Reporting Council BDO LLP AUDIT QUALITY INSPECTION JUNE 2017 The Financial Reporting Council (FRC) is the UK s independent regulator responsible for promoting high quality corporate governance

Financial Reporting Council BDO LLP AUDIT QUALITY INSPECTION JUNE 2017 The Financial Reporting Council (FRC) is the UK s independent regulator responsible for promoting high quality corporate governance

10-B Service organizations ISAE 3402 Significant issues

IAASB Main Agenda (September 2007) Page 2007 2877 Agenda Item 10-B Service organizations ISAE 3402 Significant issues A. The Framework and ISAE 3000 A.1 The Assurance Framework and ISAE 3000 lay the foundations

IAASB Main Agenda (September 2007) Page 2007 2877 Agenda Item 10-B Service organizations ISAE 3402 Significant issues A. The Framework and ISAE 3000 A.1 The Assurance Framework and ISAE 3000 lay the foundations

Companion Policy Acceptable Accounting Principles and Auditing Standards

Companion Policy 52-107 Acceptable Accounting Principles and Auditing Standards PART 1 INTRODUCTION AND DEFINITIONS 1.1 Introduction and Purpose 1.2 Multijurisdictional Disclosure System 1.3 Calculation

Companion Policy 52-107 Acceptable Accounting Principles and Auditing Standards PART 1 INTRODUCTION AND DEFINITIONS 1.1 Introduction and Purpose 1.2 Multijurisdictional Disclosure System 1.3 Calculation

ASB Meeting January 12-15, 2015

ASB Meeting January 12-15, 2015 Agenda Item 3A Chapter 1, Concepts Common to All Attestation Engagements, of Attestation Standards: Clarification and Recodification Introduction 1.1 This chapter of Statements

ASB Meeting January 12-15, 2015 Agenda Item 3A Chapter 1, Concepts Common to All Attestation Engagements, of Attestation Standards: Clarification and Recodification Introduction 1.1 This chapter of Statements

ICAEW Technical Release

Technical Release ICAEW Technical Release TECH13/14AAF ABOUT ICAEW ICAEW is a world leading professional membership organisation that promotes, develops and supports over 147,000 chartered accountants

Technical Release ICAEW Technical Release TECH13/14AAF ABOUT ICAEW ICAEW is a world leading professional membership organisation that promotes, develops and supports over 147,000 chartered accountants

AGS 10. Joint Audits AUDIT GUIDANCE STATEMENT

AUDIT GUIDANCE STATEMENT AGS 10 Joint Audits This Audit Guidance Statement was approved by the Council of the Institute of Singapore Chartered Accountants (formerly known as Institute of Certified Public

AUDIT GUIDANCE STATEMENT AGS 10 Joint Audits This Audit Guidance Statement was approved by the Council of the Institute of Singapore Chartered Accountants (formerly known as Institute of Certified Public

Audit Documentation. HKSA 230 Issued February Effective for audits of financial information for periods beginning on or after 15 June 2006

HKSA 230 Issued February 2006 Effective for audits of financial information for periods beginning on or after 15 June 2006 Hong Kong Standard on Auditing 230 Audit Documentation 1 HKSA 230 HONG KONG STANDARD

HKSA 230 Issued February 2006 Effective for audits of financial information for periods beginning on or after 15 June 2006 Hong Kong Standard on Auditing 230 Audit Documentation 1 HKSA 230 HONG KONG STANDARD

Audit committee charter

DIRECTOR TOOLS Audit committee charter Role of the board The audit committee oversees and monitors the company s audit processes, including the internal control activities. The ASX Corporate Governance

DIRECTOR TOOLS Audit committee charter Role of the board The audit committee oversees and monitors the company s audit processes, including the internal control activities. The ASX Corporate Governance

International Standard on Auditing (Ireland) 500 Audit Evidence

500 Audit Evidence") International Standard on Auditing (Ireland) 500 Audit Evidence MISSION To contribute to Ireland having a strong regulatory environment in which to do business by supervising and promoting high quality

International Standard on Auditing (Ireland) 500 Audit Evidence MISSION To contribute to Ireland having a strong regulatory environment in which to do business by supervising and promoting high quality

Audit Committee Charter for XL Group Ltd

Audit Committee Charter for XL Group Ltd Audit Committee Charter for XL Group Ltd Purpose The Audit Committee is appointed by the Board to assist the Board in overseeing (1) the quality and integrity of

Audit Committee Charter for XL Group Ltd Audit Committee Charter for XL Group Ltd Purpose The Audit Committee is appointed by the Board to assist the Board in overseeing (1) the quality and integrity of

OSHKOSH CORPORATION BOARD OF DIRECTORS AUDIT COMMITTEE CHARTER. As Amended as of May 9, 2016

OSHKOSH CORPORATION BOARD OF DIRECTORS AUDIT COMMITTEE CHARTER As Amended as of May 9, 2016 Purpose The purpose of the Audit Committee of the Board of Directors ( Audit Committee ) shall include assisting

OSHKOSH CORPORATION BOARD OF DIRECTORS AUDIT COMMITTEE CHARTER As Amended as of May 9, 2016 Purpose The purpose of the Audit Committee of the Board of Directors ( Audit Committee ) shall include assisting

AUDIT COMMITTEE CHARTER REINSURANCE GROUP OF AMERICA, INCORPORATED. the audits of the Company s financial statements;

AUDIT COMMITTEE CHARTER REINSURANCE GROUP OF AMERICA, INCORPORATED I. Role of the Committee The Audit Committee (the Committee ) of the Reinsurance Group of America, Incorporated (the Company ) Board of

AUDIT COMMITTEE CHARTER REINSURANCE GROUP OF AMERICA, INCORPORATED I. Role of the Committee The Audit Committee (the Committee ) of the Reinsurance Group of America, Incorporated (the Company ) Board of

The Auditor s Communication With Those Charged With Governance

Auditor s Communication With Those Charged With Governance 209 AU-C Section 260 The Auditor s Communication With Those Charged With Governance Source: SAS No. 122; SAS No. 123; SAS No. 125; SAS No. 128.

Auditor s Communication With Those Charged With Governance 209 AU-C Section 260 The Auditor s Communication With Those Charged With Governance Source: SAS No. 122; SAS No. 123; SAS No. 125; SAS No. 128.

FOUNDATIONS IN ACCOUNTANCY Paper FAU (UK) Foundations in Audit (United Kingdom)

Foundations in Audit (United Kingdom)") Answers FOUNDATIONS IN ACCOUNTANCY Paper FAU (UK) Foundations in Audit (United Kingdom) June 2012 Answers Section A QUESTIONS 1 10 MULTIPLE CHOICE Question Answer See Note Below 1 A 1 2 D 2 3 C 3 4 B 4

Answers FOUNDATIONS IN ACCOUNTANCY Paper FAU (UK) Foundations in Audit (United Kingdom) June 2012 Answers Section A QUESTIONS 1 10 MULTIPLE CHOICE Question Answer See Note Below 1 A 1 2 D 2 3 C 3 4 B 4

SRI LANKA AUDITING STANDARD 620 USING THE WORK OF AN EXPERT CONTENTS

SRI LANKA AUDITING STANDARD 620 USING THE WORK OF AN EXPERT (Effective for all the audits carried out on or after..) CONTENTS Paragraph Introduction 1-5 Determining the Need to Use the Work of an Expert

SRI LANKA AUDITING STANDARD 620 USING THE WORK OF AN EXPERT (Effective for all the audits carried out on or after..) CONTENTS Paragraph Introduction 1-5 Determining the Need to Use the Work of an Expert

Compilation Engagements

IFAC Board Final Pronouncement March 2012 International Standard on Related Services ISRS 4410 (Revised), Compilation Engagements The International Auditing and Assurance Standards Board (IAASB) develops

IFAC Board Final Pronouncement March 2012 International Standard on Related Services ISRS 4410 (Revised), Compilation Engagements The International Auditing and Assurance Standards Board (IAASB) develops

INSTRUCTION ON METHODOLOGY ON PERFORMING FINANCIAL AUDIT AND REGULARITY AUDIT ( Official Gazette of MN, no. 07/15 from 17 th February 2015)

") On the basis of Article 38 item 1 point 4 of the Law on the State Audit Institution ( Official Gazette of Republic of Montenegro, no. 28/04, 27/06, 78/06, Official Gazette of Montenegro, no. 17/07, 73/10,

On the basis of Article 38 item 1 point 4 of the Law on the State Audit Institution ( Official Gazette of Republic of Montenegro, no. 28/04, 27/06, 78/06, Official Gazette of Montenegro, no. 17/07, 73/10,

4.1. The quorum necessary for the transaction of business shall be two members.

AUDIT COMMITTEE - TERMS OF REFERENCE Approved 26 February 2018 1. Constitution 1.1. The board hereby resolves to establish a committee of the board to be known as the Audit Committee. 2. Membership 2.1.

AUDIT COMMITTEE - TERMS OF REFERENCE Approved 26 February 2018 1. Constitution 1.1. The board hereby resolves to establish a committee of the board to be known as the Audit Committee. 2. Membership 2.1.

INTERNATIONAL STANDARD ON AUDITING 530 AUDIT SAMPLING AND OTHER MEANS OF TESTING CONTENTS

INTERNATIONAL STANDARD ON AUDITING 530 AUDIT SAMPLING AND OTHER MEANS OF TESTING (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph Introduction...

INTERNATIONAL STANDARD ON AUDITING 530 AUDIT SAMPLING AND OTHER MEANS OF TESTING (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph Introduction...

IAASB Main Agenda (March 2016) Agenda Item. Initial Discussion on the IAASB s Future Project Related to ISA 315 (Revised) 1

Agenda Item. Initial Discussion on the IAASB s Future Project Related to ISA 315 (Revised) 1") Agenda Item 3-A Initial Discussion on the IAASB s Future Project Related to ISA 315 (Revised) 1 Objectives of the IAASB Discussion The objective of this agenda item are to: (a) Present initial background

Agenda Item 3-A Initial Discussion on the IAASB s Future Project Related to ISA 315 (Revised) 1 Objectives of the IAASB Discussion The objective of this agenda item are to: (a) Present initial background

SUNEDISON, INC. AUDIT COMMITTEE CHARTER (Adopted October 29, 2008)

") SUNEDISON, INC. AUDIT COMMITTEE CHARTER (Adopted October 29, 2008) I. Purpose The primary purpose of the Audit Committee of the Board of Directors (the Committee ) is to assist the Board of Directors in

SUNEDISON, INC. AUDIT COMMITTEE CHARTER (Adopted October 29, 2008) I. Purpose The primary purpose of the Audit Committee of the Board of Directors (the Committee ) is to assist the Board of Directors in

WATCH WORDS FROM THE PEER REVIEW PROCESS

WATCH WORDS FROM THE PEER REVIEW PROCESS Peer Review 3 NOT DOCUMENTED = NOT PERFORMED Vendor-obtained practice aids, checklists and forms are NOT audit evidence Sources of audit evidence Books, records,

WATCH WORDS FROM THE PEER REVIEW PROCESS Peer Review 3 NOT DOCUMENTED = NOT PERFORMED Vendor-obtained practice aids, checklists and forms are NOT audit evidence Sources of audit evidence Books, records,

NOVEMBER 2016 PROFESSIONAL EXAMINATIONS AUDIT & ASSURANCE (PAPER 2.3) CHIEF EXAMINER S REPORT, QUESTIONS & MARKING SCHEME

CHIEF EXAMINER S REPORT, QUESTIONS & MARKING SCHEME") NOVEMBER 2016 PROFESSIONAL EXAMINATIONS AUDIT & ASSURANCE (PAPER 2.3) CHIEF EXAMINER S REPORT, QUESTIONS & MARKING SCHEME EXAMINER S GENERAL COMMENTS The standard of the paper for November, 2016 was high

NOVEMBER 2016 PROFESSIONAL EXAMINATIONS AUDIT & ASSURANCE (PAPER 2.3) CHIEF EXAMINER S REPORT, QUESTIONS & MARKING SCHEME EXAMINER S GENERAL COMMENTS The standard of the paper for November, 2016 was high

AuditQuality Q a. Fundamentals Auditor reporting CONSULTATION DRAFT

AuditQuality Q a Fundamentals Auditor reporting CONSULTATION DRAFT Is current auditor reporting, in particular the audit report, helpful to shareholders? This paper considers the information that auditors

AuditQuality Q a Fundamentals Auditor reporting CONSULTATION DRAFT Is current auditor reporting, in particular the audit report, helpful to shareholders? This paper considers the information that auditors

Audit Risk. Exposure Draft. IFAC International Auditing and Assurance Standards Board. October Response Due Date March 31, 2003

IFAC International Auditing and Assurance Standards Board October 2002 Exposure Draft Response Due Date March 31, 2003 Audit Risk Proposed International Standards on Auditing and Proposed Amendment to

IFAC International Auditing and Assurance Standards Board October 2002 Exposure Draft Response Due Date March 31, 2003 Audit Risk Proposed International Standards on Auditing and Proposed Amendment to

Audit Committee Charter

Audit Committee Charter 1. Background The Audit Committee is a Committee of the Board of Directors ( Board ) of Syrah Resources Limited (ACN 125 242 284) ( Syrah or the Company ) that was established under

Audit Committee Charter 1. Background The Audit Committee is a Committee of the Board of Directors ( Board ) of Syrah Resources Limited (ACN 125 242 284) ( Syrah or the Company ) that was established under

Paper FAU (UK) Foundations in Audit (United Kingdom) FOUNDATIONS IN ACCOUNTANCY. Monday 18 June 2012

Foundations in Audit (United Kingdom) FOUNDATIONS IN ACCOUNTANCY. Monday 18 June 2012") FOUNDATIONS IN ACCOUNTANCY Foundations in Audit (United Kingdom) Monday 18 June 2012 Time allowed: 2 hours This paper is divided into two sections: Section A ALL TEN questions are compulsory and MUST be

FOUNDATIONS IN ACCOUNTANCY Foundations in Audit (United Kingdom) Monday 18 June 2012 Time allowed: 2 hours This paper is divided into two sections: Section A ALL TEN questions are compulsory and MUST be

LLOYDS BANKING GROUP AUDIT COMMITTEE TERMS OF REFERENCE (LLOYDS BANKING GROUP PLC, LLOYDS BANK PLC, BANK OF SCOTLAND PLC & HBOS PLC)

") LLOYDS BANKING GROUP AUDIT COMMITTEE TERMS OF REFERENCE (LLOYDS BANKING GROUP PLC, LLOYDS BANK PLC, BANK OF SCOTLAND PLC & HBOS PLC) These terms of reference are the terms of reference for the Audit Committee

LLOYDS BANKING GROUP AUDIT COMMITTEE TERMS OF REFERENCE (LLOYDS BANKING GROUP PLC, LLOYDS BANK PLC, BANK OF SCOTLAND PLC & HBOS PLC) These terms of reference are the terms of reference for the Audit Committee

Joint submission by Chartered Accountants Australia and New Zealand and The Association of Chartered Certified Accountants

Joint submission by Chartered Accountants Australia and New Zealand and The Association of Chartered Certified Accountants [28 July 2017] TO: Professor Arnold Schilder The Chairman International Auditing

Joint submission by Chartered Accountants Australia and New Zealand and The Association of Chartered Certified Accountants [28 July 2017] TO: Professor Arnold Schilder The Chairman International Auditing

SA 402(REVISED) AUDIT CONSIDERATIONS RELATING TO AN ENTITY USING

AUDIT CONSIDERATIONS RELATING TO AN ENTITY USING") Part I : Engagement and Quality Control Standards I.271 SA 402(REVISED) AUDIT CONSIDERATIONS RELATING TO AN ENTITY USING A SERVICE ORGANISATION (EFFECTIVE FOR ALL AUDITS RELATING TO ACCOUNTING PERIODS

Part I : Engagement and Quality Control Standards I.271 SA 402(REVISED) AUDIT CONSIDERATIONS RELATING TO AN ENTITY USING A SERVICE ORGANISATION (EFFECTIVE FOR ALL AUDITS RELATING TO ACCOUNTING PERIODS

Audit Committee Terms of Reference

CORPORATE GOVERNANCE 1. Constitution Audit Committee Terms of Reference The Board hereby resolves to establish a Committee of the Board to be known as the Audit Committee ( the Committee ). 2. Membership

CORPORATE GOVERNANCE 1. Constitution Audit Committee Terms of Reference The Board hereby resolves to establish a Committee of the Board to be known as the Audit Committee ( the Committee ). 2. Membership

Audit programs that can be easily tailored to address the risks associated with your individual audit engagements. 2

Checkpoint Contents Accounting, Audit & Corporate Finance Library Editorial Materials Audit and Attest Audits of Nonpublic Companies Chapter 1 Introduction and Overview 100 Introduction 100 Introduction

Checkpoint Contents Accounting, Audit & Corporate Finance Library Editorial Materials Audit and Attest Audits of Nonpublic Companies Chapter 1 Introduction and Overview 100 Introduction 100 Introduction

APES 305 TERMS OF ENGAGEMENT

APES 305 TERMS OF ENGAGEMENT (Issued December 2007; Revised 1 June 2009) CONTENTS Section Scope and application...1 Definitions... 2 Terms of Engagement for Professional Services...3 General contents of

APES 305 TERMS OF ENGAGEMENT (Issued December 2007; Revised 1 June 2009) CONTENTS Section Scope and application...1 Definitions... 2 Terms of Engagement for Professional Services...3 General contents of

ABCANN GLOBAL CORPORATION CORPORATE GOVERNANCE POLICIES AND PROCEDURES

ABCANN GLOBAL CORPORATION CORPORATE GOVERNANCE POLICIES AND PROCEDURES OCTOBER 12, 2017 LIST OF SCHEDULES A. Board Mandate B. Audit Committee Charter C. Compensation Committee Charter D. Nominating and

ABCANN GLOBAL CORPORATION CORPORATE GOVERNANCE POLICIES AND PROCEDURES OCTOBER 12, 2017 LIST OF SCHEDULES A. Board Mandate B. Audit Committee Charter C. Compensation Committee Charter D. Nominating and

Scope of this SA Effective Date Objective Definitions Sufficient Appropriate Audit Evidence... 6

SA 500* AUDIT EVIDENCE (Effective for audits of financial statements for periods beginning on or after April 1, 2009) Contents Introduction Paragraph(s) Scope of this SA...1-2 Effective Date... 3 Objective...

SA 500* AUDIT EVIDENCE (Effective for audits of financial statements for periods beginning on or after April 1, 2009) Contents Introduction Paragraph(s) Scope of this SA...1-2 Effective Date... 3 Objective...

Audit and Risk Committee Charter September 2017

1. Purpose of the Charter 1.1. The Audit and Risk Committee ( Committee ) is a committee of the ASX Limited Board ( Board ). 1.2. This Charter sets out the role, responsibilities, composition and operation

1. Purpose of the Charter 1.1. The Audit and Risk Committee ( Committee ) is a committee of the ASX Limited Board ( Board ). 1.2. This Charter sets out the role, responsibilities, composition and operation

New auditing regime: checklist [1]

![New auditing regime: checklist [1]](/thumbs/75/72255631.jpg "New auditing regime: checklist [1]") Page 1 of 5 Published on AccountingWEB (http://www.accountingweb.co.uk) Home > New auditing regime: checklist New auditing regime: checklist [1] [2] published by Steve Collings [2] on Tue, 08/11/2011-16:32

Page 1 of 5 Published on AccountingWEB (http://www.accountingweb.co.uk) Home > New auditing regime: checklist New auditing regime: checklist [1] [2] published by Steve Collings [2] on Tue, 08/11/2011-16:32

Compilation Engagements

SINGAPORE STANDARD ON RELATED SERVICES SSRS 4410 (REVISED) Compilation Engagements This revised Singapore Standard on Related Services (SSRS) 4410 supersedes SSRS 4410 Engagements to Compile Financial

SINGAPORE STANDARD ON RELATED SERVICES SSRS 4410 (REVISED) Compilation Engagements This revised Singapore Standard on Related Services (SSRS) 4410 supersedes SSRS 4410 Engagements to Compile Financial

CHAMBER OF TAX CONSULTANT S STUDENT COMMITTEE. Presentation on

CHAMBER OF TAX CONSULTANT S STUDENT COMMITTEE Presentation on AUDIT AROUND THE COMPUTER INCLUDING AUDIT DOCUMENTATION by CA MEHUL R. SHETH 08TH JUNE 2018 1 An audit is a systematic and independent examination

CHAMBER OF TAX CONSULTANT S STUDENT COMMITTEE Presentation on AUDIT AROUND THE COMPUTER INCLUDING AUDIT DOCUMENTATION by CA MEHUL R. SHETH 08TH JUNE 2018 1 An audit is a systematic and independent examination

Fundamentals Level Skills Module, Paper F8 (IRL)

") Answers Fundamentals Level Skills Module, Paper F8 (IRL) Audit and Assurance (Irish) June 2014 Answers 1 (a) Trombone Ltd s payroll system deficiencies, controls and test of controls Deficiencies Controls

Answers Fundamentals Level Skills Module, Paper F8 (IRL) Audit and Assurance (Irish) June 2014 Answers 1 (a) Trombone Ltd s payroll system deficiencies, controls and test of controls Deficiencies Controls

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT CONTENTS

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT (Effective for audits of financial statements for periods beginning

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT (Effective for audits of financial statements for periods beginning

Auditor Independence Policy

Auditor Independence Policy Why Auditor Independence Matters Audit Review ~ May 2012 Auditor Independence Policy Why Auditor Independence Matters Contents Introduction 2 The International Dimension 2 The

Auditor Independence Policy Why Auditor Independence Matters Audit Review ~ May 2012 Auditor Independence Policy Why Auditor Independence Matters Contents Introduction 2 The International Dimension 2 The

CPA REVIEW SCHOOL OF THE PHILIPPINES Manila. AUDITING THEORY OTHER PSAs and PAPSs

Page 1 of 11 CPA REVIEW SCHOOL OF THE PHILIPPINES Manila AUDITING THEORY OTHER PSAs and PAPSs Related PSAs/PAPSs: PSA 501, 505, 510, 520, 540, 545, 550, 620, 560 and 580 PAPS 1000, 1005 and 1000Ph PSA

Page 1 of 11 CPA REVIEW SCHOOL OF THE PHILIPPINES Manila AUDITING THEORY OTHER PSAs and PAPSs Related PSAs/PAPSs: PSA 501, 505, 510, 520, 540, 545, 550, 620, 560 and 580 PAPS 1000, 1005 and 1000Ph PSA

Reporting on Pro Forma Financial Information

Reporting on Pro Forma Financial Information 1509 AT Section 401 Reporting on Pro Forma Financial Information Source: SSAE No. 10. Effective when the presentation of pro forma financial information is

Reporting on Pro Forma Financial Information 1509 AT Section 401 Reporting on Pro Forma Financial Information Source: SSAE No. 10. Effective when the presentation of pro forma financial information is

ASB Meeting July 30-August 1, 2013

ASB Meeting Agenda Item 2B Disposition of s in Extant AT 401, Reporting on Pro Forma Financial, in the Proposed Clarified (Mapping) s in Extant AT 401, Reporting on Pro Forma Financial in Proposed s in

ASB Meeting Agenda Item 2B Disposition of s in Extant AT 401, Reporting on Pro Forma Financial, in the Proposed Clarified (Mapping) s in Extant AT 401, Reporting on Pro Forma Financial in Proposed s in

3410N Assurance engagements relating to sustainability reports

3410N Assurance engagements relating to sustainability reports Royal NIVRA 3410N ASSURANCE ENGAGEMENTS RELATING TO SUSTAINABILITY REPORTS Introduction Scope of this Standard ( T1 and T2) 1. This Standard

3410N Assurance engagements relating to sustainability reports Royal NIVRA 3410N ASSURANCE ENGAGEMENTS RELATING TO SUSTAINABILITY REPORTS Introduction Scope of this Standard ( T1 and T2) 1. This Standard

AUDIT COMMITTEE CHARTER

AUDIT COMMITTEE CHARTER A. Purpose The purpose of the Audit Committee is to assist the Board of Directors (the Board ) oversight of: the quality and integrity of the Company s financial statements, financial

AUDIT COMMITTEE CHARTER A. Purpose The purpose of the Audit Committee is to assist the Board of Directors (the Board ) oversight of: the quality and integrity of the Company s financial statements, financial

IAASB CAG Public Session (March 2016) Agenda Item. Initial Discussion on the IAASB s Future Project Related to ISA 315 (Revised) 1

Agenda Item. Initial Discussion on the IAASB s Future Project Related to ISA 315 (Revised) 1") Agenda Item C.1 Initial Discussion on the IAASB s Future Project Related to ISA 315 (Revised) 1 Objectives of the IAASB CAG Discussion The objective of this agenda item are to: (a) Present initial background

Agenda Item C.1 Initial Discussion on the IAASB s Future Project Related to ISA 315 (Revised) 1 Objectives of the IAASB CAG Discussion The objective of this agenda item are to: (a) Present initial background