Program Performance: Evaluations and Measurement

|

|

|

- Barrie Foster

- 5 years ago

- Views:

Transcription

1 Program Performance: Evaluations and Measurement [Session105] Tom Schumacher, University of Minnesota Ken Zeko, KPMG LLP Forensic John Stoxen, 3M Company Overview for Program Assessment Background The foundation and culture Commonly used metrics and tools Examples Questions and comments 1

2 Background: Why Do a Compliance Program Effectiveness Evaluation? Required under Federal Sentencing Compliance Program Guidelines Identifies gaps and weaknesses within and across your various programs Tells you the big picture How are your doing as an organization? Creates leadership support Results matter. Period. Guidelines Standard 8B2.1(b): (b) Due diligence and the promotion of an organizational culture that encourages a commitment to compliance with the law within the meaning of subsection (a) minimally require the following steps: (5) The organization shall take reasonable steps (B) to evaluate periodically the effectiveness of the organization s compliance and ethics program 2

3 Due Diligence Diligence: Vigilant activity; attentiveness Due Diligence: Such a measure of prudence, activity, or assiduity, as is properly to be expected from, and ordinarily exercised by, a reasonable and prudent man under the particular circumstances. What does due diligence mean for your organization? What is reasonable and prudent? Is there an industry standard? Is it the same degree of care used for other management priorities within a prudent organization? What are the hallmarks of due care for management priorities? Resources to do it right Metrics + Trending to measure progress Accountability for results (owned within operational management structure, not HR, Compliance, Counsel, Audits, etc.) Rewards/incentives Responsive action to improve points of weakness 3

4 Quick Quiz. How is your organization doing with compliance effectiveness evaluation? Completed Evaluation; In good shape 4

5 Completed Evaluation. Would rather not discuss results File 13ed the idea; in other words 5

6 Results of File 13 If you find that a person had a strong suspicion that things were not what they seemed or that someone had withheld some important facts, yet shut his eyes for fear of what he would learn, you may conclude that he acted knowingly, as I have used that word. Quiz #2 Write down the approximate number of employees in your organization Divide that number in half THAT IS THE NUMBER OF PEOPLE, ON AVERAGE, WHO HAVE WITNESSED SIGNIFICANT MISCONDUCT IN THE LAST YEAR AT YOUR ORGANIZATION Source: cross industry studies (two separate studies) 6

7 What to measure Your program itself Look to the Guidelines elements E.g. do you have training, is it working, do you have a Code, is it useful, is it followed, etc., do you have policies, are they accessible, do people follow them, etc. Just track the Guidelines. Outcomes: Is the dang thing working? How Compliance and Ethics Metrics Delivery Options Many options, may depend upon level of reliability sought Surveys (as part of a broader survey, as an independent survey, from a selected subset, etc.), interviews, consultants, peers, etc. Common Compliance and Ethics Metrics Observations of perceived misconduct Willingness to report misconduct/violations and violations in fact are reported when they are perceived to occur Perceptions about the organization s responsiveness to misconduct Fear of retaliation for reporting concerns Willingness to seek help within the organization for ethical issues Supervisors demonstrate/pay attention to ethics Leadership demonstrates/pays attention to ethics Open discussion of ethics in the workplace encouraged Ethical behavior rewarded at all levels Unethical behavior punished at all levels (management accountability) Perceptions of fair treatment in the workplace Employee willingness to deliver bad news to management Employee knowledge of workplace rules Employee commitment to the organization Confidence in preparedness to respond to ethical situations --May have many related/sub-questions organized in different compliance domains; may just ask a few questions in a broad employee survey. You have lots of options. 7

8 Resources (samples only) Academic Research E.g. Managing Ethics and Legal Compliance: What works and what hurts, Trevino et al, 41 California Management Review, No Consultants e.g. Executive Branch Employee Ethics Survey 2000, df E.g. United Nations Organizational Integrity Survey 2004, Reports E.g. National Business Ethics Survey, How Employees View Ethics in their Organizations, , available from KPMG Forensic, Integrity Survey , Benchmarking ERC Benchmarking Initiative (7 Questions for licensed use), more at Example: University of Minnesota Process Embedded within broader employee satisfaction survey 6 +1 question 6 culture 1 do they know about the hotline Observation/lesson Will look harder at external benchmarking metrics next time. 8

9 Survey Questions I have experienced or observed significant misconduct (violation of law, workplace rules, or significant University policy) in my unit/department within the last twelve months? Yes No If Yes, If the misconduct was not known by responsible University officials, did you or someone else report it to responsible University officials or the University s confidential reporting service? Yes, Yes, No, Don t I reported itothers reported it it was not reported know If Yes, Do you believe responsible University officials took appropriate corrective action? Strongly Disagree Disagree to Some Extent Uncertain Agree to Some Extent Strongly Agree I know where to report violations of law or policy (such as the University's confidential reporting line.) I believe I would be protected from retaliation if I report a suspected violation University leadership demonstrates integrity and ethical behavior

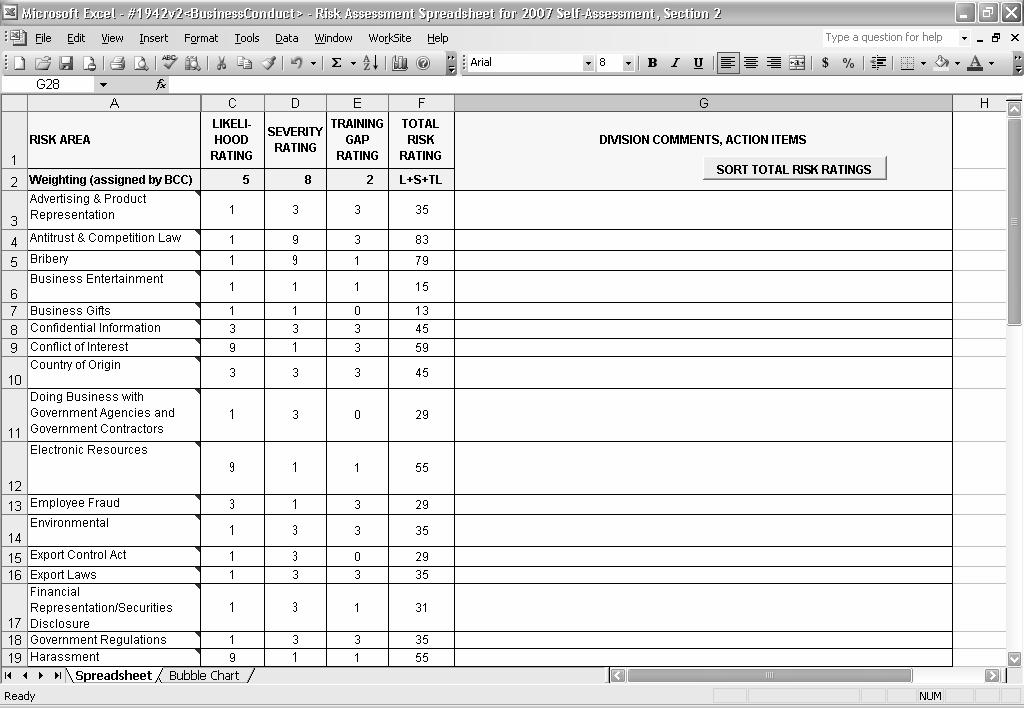

10 Example: Bi-Annual Business Conduct Self-Assessment Process 3 Business Conduct Program Structure Board Oversight Audit Committee CEO Executive Direction Business Conduct Committee Exec VP Div. VP/ Sub. MD Operational Initiatives Central Compliance Department Compliance Contact Compliance Contact 10

in the market channel(s) in which you participate. 2.")

11 3 3 REPORT 2007 BUSINESS CONDUCT SELF-ASSESSMENT DIVISION Revised June 2007 BACKGROUND BUSINESS CONDUCT SELF-ASSESSMENT PROCESS Revised March 2007 Section 1: Division Overview 3M Confidential 3M Confidential A. Division Structure 1. Name and job title of the 3M employee with ultimate accountability for legal and ethical compliance in your division. 2. Compliance Contact (name, regular position and effective date of Compliance Contact appointment). 3. Number of U.S.-based, current full-time equivalent 3M employee positions in your division. 4. List operating subsidiaries, joint ventures, etc. B. Business and Industry 3M 1. List your key customers (by industry segment, if appropriate) in the market channel(s) in which you participate. 2. If you have government customers outside the United States, briefly list which governments and types of products sold. INSTRUCTIONS FOR DIVISION COMPLIANCE CONTACTS 2007 BUSINESS CONDUCT SELF-ASSESSMENT Revised June M Confidential These Instructions are for use by division and Big B Compliance Contacts in completing the 2007 Business Conduct Self-Assessment ( Self-Assessment ). Introduction Compliance with law is only the beginning of 3M s business conduct program. We require compliance with the law, but we expect much more of ourselves. We have worked hard to build a culture where employees not only follow the letter of the law, but also the spirit of the law. The Self-Assessment process is intended to help 3M business leaders measure and improve upon the culture of legal compliance and ethical business conduct in their part of 3M s worldwide operations. At the direction of the 3M Business Conduct Committee, all 3M operating divisions complete this version of the Self-Assessment. The Self-Assessment is not intended to assess business or financial risk. It is not an audit or an investigation. Instead, the Self-Assessment is designed to help your division identify existing and emerging business conduct issues in its business activities and to think about how those issues can be dealt with most effectively, recognizing that risk can never be eliminated entirely. This type of periodic analysis is needed to ensure your organization has an effective compliance and ethics program. For more on the importance of an effective compliance program and why 3M uses the Self-Assessment, read the Background on the Self- Assessment Process document. A. Process for Completing the Self-Assessment To complete the Self-Assessment, you will need the following documents, all of which are available in the Compliance Contact TeamRoom in the Business Conduct Self-Assessment category, in the folder titled 2007 Self-Assessment Materials for Divisions : This document provides background information on 3M s Business Conduct Self-Assessment (Self-Assessment) process and on 3M s tradition of legal and ethical behavior. It can be shared with any 3M employee who will be involved in completing a Self-Assessment. 3M s Tradition of Legal and Ethical Compliance 3M has a long history of decentralized leadership in its worldwide operations. Senior management of business units, international subsidiaries and staff groups have been given the freedom and the responsibility to design and implement programs needed to succeed in their particular operations. This freedom has been a key driver of 3M s success. This responsibility has always included creation of an environment in which all employees act in accordance with 3M s values of uncompromising honesty and integrity. 3M Over the years, 3M has learned that some aspects of an effective compliance and ethics program can most efficiently handled on a global basis. 3M first published business conduct policies in 1988, to provide direction on the universal compliance and ethics principles that guide 3M s global operations. The Business Conduct Committee was created in 1991 and was given responsibility for putting together a program to carry out the global aspects of 3M s business conduct program, including: COMPLIANCE CONTACT TIPS Creating business conduct policies 2007 BUSINESS CONDUCT SELF-ASSESSMENT Communicating policies and expectations to 3M s global workforce Providing training to help employees apply business conduct policies Revised to June 2007 their jobs 3M Confidential Ensuring employees have a confidential and trusted means by which they can report suspected business conduct violations These suggestions should help Division and Big B Compliance Contacts efficiently complete the Business Fully and fairly investigating all reports of suspected violations Conduct Self Assessment ("Self-Assessment"). Each organization in the company is unique, so use your judgment as to whether these ideas will work in your business unit. Those of you who were Compliance Contacts in 2005 should notice a number of changes throughout the Self- Assessment that have been made to make the process more focused and streamlined. Divisions which have already completed the 2007 Self-Assessment have noticed a substantial reduction in the time required, compared with If questions come up while you complete your Self-Assessment, please call or the Central Compliance Department resources listed in the Background document. Tips for Division Compliance Contacts 1. Read the materials. Start by reading the Background, Instructions and Report documents in the Compliance Contact TeamRoom in the 2007 Division Self-Assessment Materials folder. You cannot map out an efficient strategy for completing the Self-Assessment until you visualize the whole process. 2. Seek assistance early. As you read the Instructions and Report, note who in your organization has the information you need to complete various sections. By asking for assistance on these sections early, you can give people weeks, rather than days, to respond. 3. Keep your Operating Committee informed. Only Division Vice Presidents/General Managers and Compliance Contacts received the kickoff notice from the Central Compliance Department about the upcoming Self-Assessment. It is your responsibility to inform the other Operating Committee members about the Self-Assessment process. You may forward the original kickoff to them if you Compliance Contact Tips for 2007 Business Conduct Self-Assessment 11

12 Section 1: Overview Follow Up on Action Items from Previous Self-Assessment Business Environment Operational Change Risk Areas Business Conduct Culture and Ethical Leadership Training and Evaluation Section 2: Risk Assessment Senior management discusses 26 business conduct risk areas on C&E matrix Consensus rankings assigned for Likelihood of violation Severity of violation Adequacy of training C&E matrix prioritizes risks 12

13 13

14 Section 3: Objective Metrics Online Training Completion 3M Standard Opinion Survey Ethics Questions Audit Findings Related to Ethics Business Conduct Violations 14

15 Section 4: Identification of Action Priorities Operating Committee & Compliance Contact: Review Self-Assessment Report Reach Consensus on Top 3+ Opportunities to Improve Compliance Culture Create Specific Action Plans For Each Priority Item with Person Responsible and Due Date Business Conduct Self-Assessment Report Widgets Business Business Conduct Committee Presentation March 1,

16 2006 Online Training Completion Percentage Division What You Need to Know about Employment Law for Leaders Understanding the FCPA Business Conduct Preventing Harassme nt (Employee Edition) Preventing Harassme nt (Supervisor Edition) Advertisin g Division 1 Division 2 Division Division 4 Division Division Division 7 Division Business-Wide Average All Division Average I can report unethical practices without fear of reprisal. 3M Avg Division 1 Division 2 Division 3 Division 4 Division 5 Division % 20% 40% 60% 80% % % Fav % Neutral % Unfav 16

17 Priority 1: Confidential Information Division 1: Employees have access to many types of confidential information and this was determined the highest risk area. Legal counsel will conduct a 30 minute group training on the importance of confidentiality with reference to the appropriate sections in the Business Conduct Policies before July 1. Division 2: Extensive external interactions in all functions and the division is exposed to risk if these are not handled properly. Ensure % compliance with corporate training and review key confidential risk areas by function. Owned by operating committee functional leaders and will be completed by end of April. Division 3: The organization s strategic direction and growth requires significant M&A and alliance activity with many types of confidential information being handled. Legal counsel to develop a specialized briefing for Steering Committee to be presented by April 30. HR to review and enhance module for new employee and refresher training by April 30. Division 4: Confidential information is shared with customers at multiple levels and by multiple functions. Develop Division Confidentiality Policy and Communications Plan by Compliance Contact and a designated team with efforts initiated by May 1. K P M G F O R E N S I C Integrity Survey A D V I S O R Y 17

18 Objectives Provide a behind-the-scenes look at corporate fraud and misconduct in the post-sarbanes-oxley era Offer organizations insights as they consider: Their exposures to fraud and misconduct risks The effectiveness of programs and controls relied on to mitigate fraud and misconduct risks Compare findings to previous KPMG Integrity Survey Methodology Blind national survey of pre-screened working adults that fell into demographics spanning: All levels of job responsibility 16 job functions 11 industry sectors 4 thresholds of organization size Paper based survey conducted between Nov. 04 and March 05 Benchmarked results where possible against findings in 2000 survey 4,056 respondents Confidence level 95%; Precision level (margin of error) +/- 2% 18

19 Key Findings Level of misconduct remains unchanged 74% reported that they have observed misconduct in the prior 12 month period compared to 76% in 2000 Half reported observing serious misconduct Conditions that facilitate Management s ability to prevent, detect, and respond to fraud and misconduct have improved since 2000 Pressure to engage in misconduct is down Confidence in reporting concerns to management is up Key Findings Employees in companies with comprehensive ethics and compliance programs reported more favorable results across the board than those employees at companies without such programs At companies with ethics and compliance programs: Fewer observations of misconduct Higher levels of confidence in management s commitment to integrity 19

20 Prevalence of Misconduct During the Prior 12 Months Prevalence of Misconduct That Could Cause a Significant Loss of Public Trust if Discovered

21 Root Causes of Misconduct Feel pressure to do whatever it takes to meet business targets Lack understanding of the standards that apply to their jobs Believe that their code of conduct is not taken seriously Lack resources to get the job done without cutting corners Believe they will be rewarded for results, not the means used to achieve them Believe policies or procedures are easy to bypass or override Fear losing their job if they do not meet targets otherwise Are seeking to bend the rules or steal for their own personal gain Propensity to Report Misconduct Notify supervisor or another manager 81 Try resolving the matter directly 53 Call the ethics or compliance hotline 38 Notify someone outside the organization 10 Look the other way or do nothing

22 Channels Employees Feel Comfortable Using to Report Misconduct Supervisor Local managers Peers or colleagues Human resources department Ethics or compliance hotline Legal department Senior executives Internal audit department Board of directors or audit committee Note: Chart does not foot to % due to rounding. Agree Unsure Disagree Channels Employee Feel Comfortable Using for Advice and Counsel Supervisor Peers or colleagues Local managers Legal department Human resources department Ethics or compliance hotline Senior executives Internal audit department Note: Chart does not foot to % due to rounding. Agree Unsure Disagree 22

23 Perceived Outcomes of Reporting Misconduct Appropriate action would be taken My report would be handled confidentially I would be protected from retaliation Those involved would be disciplined fairly regardless of their position I would be satisfied with the outcome I would be doing the right thing Note: Chart does not foot to % due to rounding. Agree Unsure Disagree Tone at the Top: Perceptions About the CEO and Other Senior Executives Are positive role models for the organization Know what type of behavior really goes on inside the organization Are approachable if employees have questions about ethics or need to deliver bad news Value ethics and integrity over short-term business goals Set achievable targets without violating my organization s code of conduct Would respond appropriately if they became aware of misconduct Set the right tone at the top on the importance of ethics and integrity Note: Chart does not foot to % due to rounding. Agree Unsure Disagree 23

24 Local Tone: Perceptions of Local Managers and Supervisors Are positive role models for the organization Know what type of behavior really goes on inside the organization Are approachable if employees have questions about ethics or need to deliver bad news Value ethics and integrity over short-term business goals Set achievable targets without violating my organization s code of conduct Would respond appropriately if they became aware of misconduct Set the right tone at the top on the importance of ethics and integrity Note: Chart does not foot to % due to rounding. Agree Unsure Disagree Team Culture and Environment: Perceptions of Individual Teams and Work Units People feel motivated and empowered to do the right thing People feel comfortable raising ethics concerns People apply the right values to their decisions and behaviors People share a high commitment to integrity The opportunity to engage in misconduct is minimal The ability to conceal misconduct is minimal The willingness to tolerate misconduct is minimal Adequate checks are carried out to detect misconduct Note: Chart does not foot to % due to rounding. Agree Unsure Disagree 24

25 Presenter s contact details Kenneth Zeko KPMG LLP (214) kzeko@kpmg.com The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation. 25

THE PENNSYLVANIA STATE UNIVERSITY 2013 VALUES & CULTURE SURVEY

THE PENNSYLVANIA STATE UNIVERSITY 2013 VALUES & CULTURE SURVEY EXECUTIVE SUMMARY In April of 2013, The Pennsylvania State University (the University) contracted with the Ethics Resource Center (ERC) to

THE PENNSYLVANIA STATE UNIVERSITY 2013 VALUES & CULTURE SURVEY EXECUTIVE SUMMARY In April of 2013, The Pennsylvania State University (the University) contracted with the Ethics Resource Center (ERC) to

CNB Ethics Frequently Asked Questions

CNB Ethics Frequently Asked Questions Why did CNB establish Ethics Policies for its entities? CNB established our Ethics policies to provide guidance for employees related to ethical conduct and to avoid

CNB Ethics Frequently Asked Questions Why did CNB establish Ethics Policies for its entities? CNB established our Ethics policies to provide guidance for employees related to ethical conduct and to avoid

CODE OF BUSINESS CONDUCT AND ETHICS. FRONTIER AIRLINES, INC. Adopted May 27, 2004

1. Introduction CODE OF BUSINESS CONDUCT AND ETHICS FRONTIER AIRLINES, INC. Adopted May 27, 2004 The Board of Directors adopted this Code of Business Conduct ( Code ) to establish basic legal and ethical

1. Introduction CODE OF BUSINESS CONDUCT AND ETHICS FRONTIER AIRLINES, INC. Adopted May 27, 2004 The Board of Directors adopted this Code of Business Conduct ( Code ) to establish basic legal and ethical

Blowing the Whistle on Workplace Misconduct

Blowing the Whistle on Workplace Misconduct December 2010 Founded in 1922, the Ethics Resource Center (ERC) is America s oldest nonprofit organization devoted to the advancement of high ethical standards

Blowing the Whistle on Workplace Misconduct December 2010 Founded in 1922, the Ethics Resource Center (ERC) is America s oldest nonprofit organization devoted to the advancement of high ethical standards

BUILDING COMPANIES WHERE VALUES AND ETHICAL CONDUCT MATTER ETHICS SURVEY TM GLOBAL BUSINESS USING COMMUNICATION AND TRUST TO STRENGTHEN YOUR WORKPLACE

BUILDING COMPANIES WHERE VALUES AND ETHICAL CONDUCT MATTER USING COMMUNICATION AND TRUST TO STRENGTHEN YOUR WORKPLACE OCTOBER 2018 GLOBAL BUSINESS ETHICS SURVEY TM This report is published by the Ethics

BUILDING COMPANIES WHERE VALUES AND ETHICAL CONDUCT MATTER USING COMMUNICATION AND TRUST TO STRENGTHEN YOUR WORKPLACE OCTOBER 2018 GLOBAL BUSINESS ETHICS SURVEY TM This report is published by the Ethics

The Company seeks to comply with both the letter and spirit of the laws and regulations in all jurisdictions in which it operates.

1. Policy Statement CRC HEALTH GROUP, INC. CRC HEALTH CORPORATION CODE OF BUSINESS CONDUCT AND ETHICS It is the policy of CRC Health Group to conduct its business affairs honestly and in an ethical manner.

1. Policy Statement CRC HEALTH GROUP, INC. CRC HEALTH CORPORATION CODE OF BUSINESS CONDUCT AND ETHICS It is the policy of CRC Health Group to conduct its business affairs honestly and in an ethical manner.

Ethics and Financial Reporting: Delivering on the Commitment

An address by Bill MacKinnon, FCA Chief Executive, KPMG LLP To the EthicsCentre, Toronto Ontario February 27, 2003 (check against delivery) 1 Thank you The world of auditing and financial reporting has

An address by Bill MacKinnon, FCA Chief Executive, KPMG LLP To the EthicsCentre, Toronto Ontario February 27, 2003 (check against delivery) 1 Thank you The world of auditing and financial reporting has

TEACHERS RETIREMENT BOARD. AUDITS AND RISK MANAGEMENT COMMITTEE Item Number: 9 SUBJECT: Scope and Structure of the Enterprise Compliance Program

TEACHERS RETIREMENT BOARD AUDITS AND RISK MANAGEMENT COMMITTEE Item Number: 9 SUBJECT: Scope and Structure of the Enterprise Compliance Program CONSENT: ATTACHMENT(S): 3 ACTION: DATE OF MEETING: / 30 mins

TEACHERS RETIREMENT BOARD AUDITS AND RISK MANAGEMENT COMMITTEE Item Number: 9 SUBJECT: Scope and Structure of the Enterprise Compliance Program CONSENT: ATTACHMENT(S): 3 ACTION: DATE OF MEETING: / 30 mins

11/2/2016. Board Member Liability and Responsibility for Compliance AGENDA

Board Member Liability and Responsibility for Compliance Erica Salmon Byrne Ethisphere Institute Scott Killingsworth Bryan Cave LLP SCCE Board Audit and Compliance Committee Conference November 7, 2016

Board Member Liability and Responsibility for Compliance Erica Salmon Byrne Ethisphere Institute Scott Killingsworth Bryan Cave LLP SCCE Board Audit and Compliance Committee Conference November 7, 2016

Successful HR Strategies for Building an Ethical Workplace Culture

1 Successful HR Strategies for Building an Ethical Workplace Culture Scott D. Ferrin, SHRM-SCP, CAE, PMP Prescott Area HRA May 18, 2017 Today s Agenda 2 1) Current State of Workplace Ethics 2) Why Good

1 Successful HR Strategies for Building an Ethical Workplace Culture Scott D. Ferrin, SHRM-SCP, CAE, PMP Prescott Area HRA May 18, 2017 Today s Agenda 2 1) Current State of Workplace Ethics 2) Why Good

Delta Dental of Michigan, Ohio, and Indiana. Compliance Plan

Delta Dental of Michigan, Ohio, and Indiana Compliance Plan Procedure #: 420-29 Issue Date: 5/15/2013 Last Revised Date: 5/23/2016 Last Review Date: 5/23/2016 Next Review Date: 5/23/2017 Title: Compliance

Delta Dental of Michigan, Ohio, and Indiana Compliance Plan Procedure #: 420-29 Issue Date: 5/15/2013 Last Revised Date: 5/23/2016 Last Review Date: 5/23/2016 Next Review Date: 5/23/2017 Title: Compliance

VC COMPLIANCE PROGRAM

Following the laws and regulations is not only great for you, but for everyone else. Dear Colleague, It is with great satisfaction that I am sharing this VC Compliance Program document with you. Based

Following the laws and regulations is not only great for you, but for everyone else. Dear Colleague, It is with great satisfaction that I am sharing this VC Compliance Program document with you. Based

2012 GUIDELINES MANUAL

2012 GUIDELINES MANUAL CHAPTER EIGHT - SENTENCING OF ORGANIZATIONS PART B - REMEDYING HARM FROM CRIMINAL CONDUCT, AND EFFECTIVE COMPLIANCE AND ETHICS PROGRAM 2. EFFECTIVE COMPLIANCE AND ETHICS PROGRAM

2012 GUIDELINES MANUAL CHAPTER EIGHT - SENTENCING OF ORGANIZATIONS PART B - REMEDYING HARM FROM CRIMINAL CONDUCT, AND EFFECTIVE COMPLIANCE AND ETHICS PROGRAM 2. EFFECTIVE COMPLIANCE AND ETHICS PROGRAM

Compliance & Ethics. a publication of the society of corporate compliance and ethics MAY 2018

Compliance & Ethics PROFESSIONAL corporatecompliance.org a publication of the society of corporate compliance and ethics MAY 2018 Meet Jamie Watts, CCEP-I Senior Compliance & Risk Advisor World Food Programme

Compliance & Ethics PROFESSIONAL corporatecompliance.org a publication of the society of corporate compliance and ethics MAY 2018 Meet Jamie Watts, CCEP-I Senior Compliance & Risk Advisor World Food Programme

Ethics SouthernStyle CODE OF ETHICS. E t h i c a l B e h a v i o r i s o u r S t a n d a r d

Ethics SouthernStyle CODE OF ETHICS E t h i c a l B e h a v i o r i s o u r S t a n d a r d Our Code of Ethics advises us on proper business conduct. It links our values Southern Style to the company s

Ethics SouthernStyle CODE OF ETHICS E t h i c a l B e h a v i o r i s o u r S t a n d a r d Our Code of Ethics advises us on proper business conduct. It links our values Southern Style to the company s

BIG LOTS, INC. CODE OF BUSINESS CONDUCT AND ETHICS

September 2003 BIG LOTS, INC. CODE OF BUSINESS CONDUCT AND ETHICS Introduction This Code of Business Conduct and Ethics covers a wide range of business principles to guide all directors, officers and associates

September 2003 BIG LOTS, INC. CODE OF BUSINESS CONDUCT AND ETHICS Introduction This Code of Business Conduct and Ethics covers a wide range of business principles to guide all directors, officers and associates

compliance reporting policy 13. COMPLIANCE REPORTING POLICY

compliance reporting policy 13. COMPLIANCE REPORTING POLICY compliance reporting policy What do we mean by reporting? Reporting means raising concerns about suspected misconduct, or about feeling uncomfortable

compliance reporting policy 13. COMPLIANCE REPORTING POLICY compliance reporting policy What do we mean by reporting? Reporting means raising concerns about suspected misconduct, or about feeling uncomfortable

CSL BEHRING COMPLIANCE PLAN

CSL BEHRING COMPLIANCE PLAN I. POLICY AND PURPOSE Statement of Values CSL Behring adheres to a policy of strict compliance with the laws and regulations governing its business, not only as a legal obligation,

CSL BEHRING COMPLIANCE PLAN I. POLICY AND PURPOSE Statement of Values CSL Behring adheres to a policy of strict compliance with the laws and regulations governing its business, not only as a legal obligation,

TDC WHISTLEBLOWER POLICY

TDC WHISTLEBLOWER POLICY May 1 2016 St. Kitts Nevis Anguilla T rading and Development Company Limited (T DC Ltd and Subsidiaries- hereinafter referred to as the Com pany ) Table of Contents A. Introduction..

TDC WHISTLEBLOWER POLICY May 1 2016 St. Kitts Nevis Anguilla T rading and Development Company Limited (T DC Ltd and Subsidiaries- hereinafter referred to as the Com pany ) Table of Contents A. Introduction..

Sarbanes-Oxley Act of 2002 Can private businesses benefit from it?

Sarbanes-Oxley Act of 2002 Can private businesses benefit from it? As used in this document, Deloitte means Deloitte Tax LLP, which provides tax services; Deloitte & Touche LLP, which provides assurance

Sarbanes-Oxley Act of 2002 Can private businesses benefit from it? As used in this document, Deloitte means Deloitte Tax LLP, which provides tax services; Deloitte & Touche LLP, which provides assurance

Whistleblowing policy

(School can insert logo) Whistleblowing policy Audience: Parents Trust employees, contractors and volunteers Local Governing Bodies Trustees Regional Boards Approved: Trustees July 2017 Other related policies:

(School can insert logo) Whistleblowing policy Audience: Parents Trust employees, contractors and volunteers Local Governing Bodies Trustees Regional Boards Approved: Trustees July 2017 Other related policies:

Measuring Corporate Culture: Enhancing the Board s Understanding

Corporate Governance Presents: Measuring Corporate Culture: Enhancing the Board s Understanding John C. Lenzi, Chief Compliance Officer, Altria Corporate Services, Altria Group, Inc. Timothy T. Lupfer,

Corporate Governance Presents: Measuring Corporate Culture: Enhancing the Board s Understanding John C. Lenzi, Chief Compliance Officer, Altria Corporate Services, Altria Group, Inc. Timothy T. Lupfer,

Audit Committee Performance Evaluation Form

Audit Committee Performance Evaluation Form This page has been intentionally left blank. The following questionnaire is based on emerging and leading practices to assist in the self-assessment of an audit

Audit Committee Performance Evaluation Form This page has been intentionally left blank. The following questionnaire is based on emerging and leading practices to assist in the self-assessment of an audit

Developing an Integrated Anti-Fraud, Compliance, and Ethics Program

Developing an Integrated Anti-Fraud, Compliance, and Ethics Program Establishing an Effective Anti-Fraud, Compliance, and Ethics Function 2018 Association of Certified Fraud Examiners, Inc. Discussion

Developing an Integrated Anti-Fraud, Compliance, and Ethics Program Establishing an Effective Anti-Fraud, Compliance, and Ethics Function 2018 Association of Certified Fraud Examiners, Inc. Discussion

Benchmarking 101: Shaping your E&C Program for Maximum Value

Benchmarking 101: Shaping your E&C Program for Maximum Value Presented on November 15, 2016 Copyright 2016NAVEXGlobal,Inc. AllRightsReserved. Page 0 Presented by Mary Bennett Vice President, Advisory Services,

Benchmarking 101: Shaping your E&C Program for Maximum Value Presented on November 15, 2016 Copyright 2016NAVEXGlobal,Inc. AllRightsReserved. Page 0 Presented by Mary Bennett Vice President, Advisory Services,

ASSOCIATED BANC-CORP CODE OF BUSINESS CONDUCT AND ETHICS

ASSOCIATED BANC-CORP CODE OF BUSINESS CONDUCT AND ETHICS Introduction This Code of Business Conduct and Ethics covers a wide range of business practices and procedures. It does not cover every issue that

ASSOCIATED BANC-CORP CODE OF BUSINESS CONDUCT AND ETHICS Introduction This Code of Business Conduct and Ethics covers a wide range of business practices and procedures. It does not cover every issue that

Verisk Analytics, Inc. Code of Business Conduct and Ethics As Amended June 5, 2018

Verisk Analytics, Inc. Code of Business Conduct and Ethics As Amended June 5, 2018 1. Introduction This Code of Business Conduct and Ethics ( Code ) has been adopted by our Board of Directors and summarizes

Verisk Analytics, Inc. Code of Business Conduct and Ethics As Amended June 5, 2018 1. Introduction This Code of Business Conduct and Ethics ( Code ) has been adopted by our Board of Directors and summarizes

THE STATE OF ETHICS & COMPLIANCE IN THE WORKPLACE MARCH 2018 GLOBAL BUSINESS ETHICS SURVEY TM

THE STATE OF ETHICS & COMPLIANCE IN THE WORKPLACE MARCH 2018 GLOBAL BUSINESS ETHICS SURVEY TM This report is published by the Ethics & Compliance Initiative (ECI). All content contained in this report

THE STATE OF ETHICS & COMPLIANCE IN THE WORKPLACE MARCH 2018 GLOBAL BUSINESS ETHICS SURVEY TM This report is published by the Ethics & Compliance Initiative (ECI). All content contained in this report

Whistleblowing Policy & Procedures

Whistleblowing Policy & Procedures Policy Date May 2016 (final version July 2016) Review Date May 2017 Page 1 of 14 Contents What is whistleblowing? The Trust s commitments to employees who whistle-blow

Whistleblowing Policy & Procedures Policy Date May 2016 (final version July 2016) Review Date May 2017 Page 1 of 14 Contents What is whistleblowing? The Trust s commitments to employees who whistle-blow

Self Assessment Workbook

Self Assessment Workbook Corporate Governance - Board of Directors March 2015 Ce document est aussi disponible en français. Deposit Insurance Corporation of Ontario Applicability The Self Assessment Workbook:

Self Assessment Workbook Corporate Governance - Board of Directors March 2015 Ce document est aussi disponible en français. Deposit Insurance Corporation of Ontario Applicability The Self Assessment Workbook:

Sheryl Vacca, CHC-F, CCEP-F, CHRC, CCEP-I, CHPC. SVP/Chief Compliance & Audit Officer University of California

Sheryl Vacca, CHC-F, CCEP-F, CHRC, CCEP-I, CHPC SVP/Chief & Audit Officer University of California Sheryl.vacca@ucop.edu Odell Guyton Director of Microsoft Corporation What is our framework? Strong Ethics

Sheryl Vacca, CHC-F, CCEP-F, CHRC, CCEP-I, CHPC SVP/Chief & Audit Officer University of California Sheryl.vacca@ucop.edu Odell Guyton Director of Microsoft Corporation What is our framework? Strong Ethics

CODE OF ETHICS FOR CHIEF EXECUTIVE OFFICER AND SENIOR FINANCIAL OFFICERS UGI CORPORATION

CODE OF ETHICS FOR CHIEF EXECUTIVE OFFICER AND SENIOR FINANCIAL OFFICERS OF UGI CORPORATION Introduction The reputation for integrity of UGI Corporation (the Company ) is a valuable asset that is vital

CODE OF ETHICS FOR CHIEF EXECUTIVE OFFICER AND SENIOR FINANCIAL OFFICERS OF UGI CORPORATION Introduction The reputation for integrity of UGI Corporation (the Company ) is a valuable asset that is vital

Society of Corporate Compliance & Ethics: West Coast Regional

Society of Corporate & Ethics: West Coast Regional Internal Audit and : The Importance of Collaboration & Skill Development: From Policy to Practice Odell Guyton, JD, CCEP CO-CHAIR SCCE Director of Microsoft

Society of Corporate & Ethics: West Coast Regional Internal Audit and : The Importance of Collaboration & Skill Development: From Policy to Practice Odell Guyton, JD, CCEP CO-CHAIR SCCE Director of Microsoft

#ITsHerFutureCA. Moving women forward into leadership roles. August, #ITsHerFutureCA

#ITsHerFutureCA #ITsHerFutureCA Moving women forward into leadership roles August, 2017 Report background Purpose The Governing Institute conducted a survey of female California state and local government

#ITsHerFutureCA #ITsHerFutureCA Moving women forward into leadership roles August, 2017 Report background Purpose The Governing Institute conducted a survey of female California state and local government

Doing the right thing the National Grid experience

Doing the right thing the National Grid experience Place your chosen image here. The four corners must just cover the arrow tips. For covers, the three pictures should be the same size and in a straight

Doing the right thing the National Grid experience Place your chosen image here. The four corners must just cover the arrow tips. For covers, the three pictures should be the same size and in a straight

August 4, 2010 Information Requests Round 1

August 4, 2010 Information Requests Round 1 CAC/MSOS (MPI) 1-50 Reference: 2009 Annual Report page 27. Preamble: In response to Goal 6, one of MPI s strategies is To continue to respond to the issues raised

August 4, 2010 Information Requests Round 1 CAC/MSOS (MPI) 1-50 Reference: 2009 Annual Report page 27. Preamble: In response to Goal 6, one of MPI s strategies is To continue to respond to the issues raised

2017 Internal Controls Survey

2017 Internal Controls Survey kpmg.com 2017 Internal Controls Survey Executive summary Although Sarbanes-Oxley (SOX) is not a new regulation, it has continued to evolve over the last 15 years since it

2017 Internal Controls Survey kpmg.com 2017 Internal Controls Survey Executive summary Although Sarbanes-Oxley (SOX) is not a new regulation, it has continued to evolve over the last 15 years since it

Bearing the Bad News Reporting to the Board on Internal Corruption. Peter Dent, National Leader Deloitte Forensics September 11, 2013

Bearing the Bad News Reporting to the Board on Internal Corruption Peter Dent, National Leader Deloitte Forensics September 11, 2013 Agenda Assessment of Risk in Canada Recent trends in enforcement activity

Bearing the Bad News Reporting to the Board on Internal Corruption Peter Dent, National Leader Deloitte Forensics September 11, 2013 Agenda Assessment of Risk in Canada Recent trends in enforcement activity

Internal Audit & Compliance Importance of Collaboration and Skill Development

Internal Audit & Compliance Importance of Collaboration and Skill Development Odell Guyton Director of Compliance Microsoft Corporation Co-Chair Society Corporate Compliance & Ethics Austin, Texas June

Internal Audit & Compliance Importance of Collaboration and Skill Development Odell Guyton Director of Compliance Microsoft Corporation Co-Chair Society Corporate Compliance & Ethics Austin, Texas June

2016 EMPLOYEE SURVEY RESULTS AND ANALYSIS

2016 EMPLOYEE SURVEY RESULTS AND ANALYSIS JULY 2016 Survey Administered by the Institutional Effectiveness Committee March-June 2016 Report Prepared by the Office of Institutional Advancement Data Support

2016 EMPLOYEE SURVEY RESULTS AND ANALYSIS JULY 2016 Survey Administered by the Institutional Effectiveness Committee March-June 2016 Report Prepared by the Office of Institutional Advancement Data Support

FCPA COMPLIANCE PROGRAMS

FCPA COMPLIANCE PROGRAMS JIMMY S. PAPPAS INTERNATIONAL INTERNAL INVESTIGATIONS CONFERENCE FRANKFURT, GERMANY DECEMBER 7, 2012 FCPA COMPLIANCE PROGRAMS - OVERVIEW! An effective compliance program is: A

FCPA COMPLIANCE PROGRAMS JIMMY S. PAPPAS INTERNATIONAL INTERNAL INVESTIGATIONS CONFERENCE FRANKFURT, GERMANY DECEMBER 7, 2012 FCPA COMPLIANCE PROGRAMS - OVERVIEW! An effective compliance program is: A

Creating a Global Ethics & Compliance Program that Will Truly Promote and Reinforce Ethical Behavior

Creating a Global Ethics & Compliance Program that Will Truly Promote and Reinforce Ethical Behavior Joel Rogers, VP Ethics, Compliance, and Content Strategy Kaplan EduNeering Monica Francois Marcel, Partner,

Creating a Global Ethics & Compliance Program that Will Truly Promote and Reinforce Ethical Behavior Joel Rogers, VP Ethics, Compliance, and Content Strategy Kaplan EduNeering Monica Francois Marcel, Partner,

CITY OF VANCOUVER ADMINISTRATIVE REPORT

CITY OF VANCOUVER ADMINISTRATIVE REPORT Report Date: April 30, 2008 Author: Mike Zora Phone No.: 604.873.7666 RTS No.: 06676 VanRIMS No.: 01-0500-21 Meeting Date: May 15, 2008 TO: FROM: SUBJECT: Standing

CITY OF VANCOUVER ADMINISTRATIVE REPORT Report Date: April 30, 2008 Author: Mike Zora Phone No.: 604.873.7666 RTS No.: 06676 VanRIMS No.: 01-0500-21 Meeting Date: May 15, 2008 TO: FROM: SUBJECT: Standing

Code of Business Conduct

Code of Business Conduct The Nyrstar Way Prevent harm Proactively manage risks related to our people, the environment, our strategy, our financials, and our assets Be open and honest Share one s point

Code of Business Conduct The Nyrstar Way Prevent harm Proactively manage risks related to our people, the environment, our strategy, our financials, and our assets Be open and honest Share one s point

Building an Effective Compliance and Ethics Program

CORPORATE INTEGRITY PRACTICE COMPLIANCE AND ETHICS LEADERSHIP COUNCIL Building an Effective Compliance and Ethics Program Data Insights for Driving Performance 1 March 2011 OBJECTIVES FOR OUR MEETING Key

CORPORATE INTEGRITY PRACTICE COMPLIANCE AND ETHICS LEADERSHIP COUNCIL Building an Effective Compliance and Ethics Program Data Insights for Driving Performance 1 March 2011 OBJECTIVES FOR OUR MEETING Key

Developmental Delay Rehabilitation Services Inc.

Developmental Delay Rehabilitation Services Inc. Corporate Compliance Plan Terence Blackwell, CEO Nathan Cohen, CCC/SLP, President Corporate Compliance Officer Table of Contents Section Name I. Corporate

Developmental Delay Rehabilitation Services Inc. Corporate Compliance Plan Terence Blackwell, CEO Nathan Cohen, CCC/SLP, President Corporate Compliance Officer Table of Contents Section Name I. Corporate

Code of Business Conduct and Ethics

Code of Business Conduct and Ethics Table of Contents Purpose... 1 Scope... 1 Policy... 2 Responsibilities... 8 Enforcement... 8 Review and Revision... 8 PURPOSE Pursuant to the Sarbanes-Oxley Act of 2002

Code of Business Conduct and Ethics Table of Contents Purpose... 1 Scope... 1 Policy... 2 Responsibilities... 8 Enforcement... 8 Review and Revision... 8 PURPOSE Pursuant to the Sarbanes-Oxley Act of 2002

KPMG N.V. Code of Conduct. kpmg.nl

KPMG N.V. Code of Conduct kpmg.nl Contents 01 02 06 08 10 12 12 Leadership message Introduction The KPMG Values Commitments Responsibilities Where to get help Compliance with the Code Leadership message

KPMG N.V. Code of Conduct kpmg.nl Contents 01 02 06 08 10 12 12 Leadership message Introduction The KPMG Values Commitments Responsibilities Where to get help Compliance with the Code Leadership message

Code of Conduct & Ethics

Code of Conduct & Ethics Interfor Code of Conduct & Ethics Contents Page 1 CEO Message A Message from our CEO 2 Our Code of 2 Conduct & Ethics Our Code of Conduct & Ethics 3 3 Guiding Principles Guiding

Code of Conduct & Ethics Interfor Code of Conduct & Ethics Contents Page 1 CEO Message A Message from our CEO 2 Our Code of 2 Conduct & Ethics Our Code of Conduct & Ethics 3 3 Guiding Principles Guiding

Developing an Integrated Anti-Fraud, Compliance, and Ethics Program

Developing an Integrated Anti-Fraud, Compliance, and Ethics Program Introduction Eric Feldman, CFE, CIG Affiliated Monitors, Inc. 2018 Association of Certified Fraud Examiners, Inc. CPE Information 2018

Developing an Integrated Anti-Fraud, Compliance, and Ethics Program Introduction Eric Feldman, CFE, CIG Affiliated Monitors, Inc. 2018 Association of Certified Fraud Examiners, Inc. CPE Information 2018

Developing an Integrated Anti-Fraud, Compliance, and Ethics Program

Developing an Integrated Anti-Fraud, Compliance, and Ethics Program Implementing a Whistleblower Helpline 2018 Association of Certified Fraud Examiners, Inc. Discussion Questions 1. Does your organization

Developing an Integrated Anti-Fraud, Compliance, and Ethics Program Implementing a Whistleblower Helpline 2018 Association of Certified Fraud Examiners, Inc. Discussion Questions 1. Does your organization

European CEI. Compliance 101

European CEI Compliance 101 Debbie Troklus, CHC-F, CCEP-F, CHRC, CHPC, CCEP-I Managing Director Aegis Compliance and Ethics Center dtroklus@aegis-compliance.com Sheryl Vacca, CHC- F, CCEP-F, CCEP-I, CHRC,

European CEI Compliance 101 Debbie Troklus, CHC-F, CCEP-F, CHRC, CHPC, CCEP-I Managing Director Aegis Compliance and Ethics Center dtroklus@aegis-compliance.com Sheryl Vacca, CHC- F, CCEP-F, CCEP-I, CHRC,

INTEGRITY MANAGEMENT CONTINUOUS IMPROVEMENT. Foundation for an Effective Safety Culture

INTEGRITY MANAGEMENT CONTINUOUS IMPROVEMENT Foundation for an Effective Safety Culture June 2011 Foundation for an Effective Safety Culture describes the key elements of organizational culture and business

INTEGRITY MANAGEMENT CONTINUOUS IMPROVEMENT Foundation for an Effective Safety Culture June 2011 Foundation for an Effective Safety Culture describes the key elements of organizational culture and business

Quality Management System Guidance. ISO 9001:2015 Clause-by-clause Interpretation

Quality Management System Guidance ISO 9001:2015 Clause-by-clause Interpretation Table of Contents 1 INTRODUCTION... 4 1.1 IMPLEMENTATION & DEVELOPMENT... 5 1.2 MANAGING THE CHANGE... 5 1.3 TOP MANAGEMENT

Quality Management System Guidance ISO 9001:2015 Clause-by-clause Interpretation Table of Contents 1 INTRODUCTION... 4 1.1 IMPLEMENTATION & DEVELOPMENT... 5 1.2 MANAGING THE CHANGE... 5 1.3 TOP MANAGEMENT

MEASURING ENGAGEMENT TO UNLOCK YOUR COMPANY S COMPETITIVE ADVANTAGE

MEASURING ENGAGEMENT TO UNLOCK YOUR COMPANY S COMPETITIVE ADVANTAGE Employee engagement is the extent to which employees are motivated to contribute to organizational success and are willing to apply discretionary

MEASURING ENGAGEMENT TO UNLOCK YOUR COMPANY S COMPETITIVE ADVANTAGE Employee engagement is the extent to which employees are motivated to contribute to organizational success and are willing to apply discretionary

Building a Fraud-Resistant Organization January 8, 2015

Building a Fraud-Resistant Organization January 8, 2015 The views expressed by the presenters do not necessarily represent the views, positions, or opinions of the Center for Audit Quality (CAQ), Financial

Building a Fraud-Resistant Organization January 8, 2015 The views expressed by the presenters do not necessarily represent the views, positions, or opinions of the Center for Audit Quality (CAQ), Financial

Developing an Integrated Anti-Fraud, Compliance, and Ethics Program

Developing an Integrated Anti-Fraud, Compliance, and Ethics Program Monitoring, Assessing, and Remediating the Program 2018 Association of Certified Fraud Examiners, Inc. Discussion Questions 1. How does

Developing an Integrated Anti-Fraud, Compliance, and Ethics Program Monitoring, Assessing, and Remediating the Program 2018 Association of Certified Fraud Examiners, Inc. Discussion Questions 1. How does

EY Center for Board Matters. Leading practices for audit committees

EY Center for Board Matters for audit committees As an audit committee member, your role is increasingly complex and demanding. Regulators, standard-setters and investors are pressing for more transparency

EY Center for Board Matters for audit committees As an audit committee member, your role is increasingly complex and demanding. Regulators, standard-setters and investors are pressing for more transparency

Compliance Program Effectiveness Guide

Compliance Program Effectiveness Guide June 2017 This Guide is a comparison of: Compliance Program Elements New York State, Social Services Law 363-D Office of Inspector General (OIG) Compliance Program

Compliance Program Effectiveness Guide June 2017 This Guide is a comparison of: Compliance Program Elements New York State, Social Services Law 363-D Office of Inspector General (OIG) Compliance Program

Southwest Airlines Co. Code of Ethics

Southwest Airlines Co. Code of Ethics Introduction Southwest Airlines Co. is committed to maintaining the highest standards of ethical business practices and legal and regulatory compliance. We place a

Southwest Airlines Co. Code of Ethics Introduction Southwest Airlines Co. is committed to maintaining the highest standards of ethical business practices and legal and regulatory compliance. We place a

Compliance Effectiveness Strategies HOW TO SUCCEED AS A COMPLIANCE PROFESSIONAL

Compliance Effectiveness Strategies HOW TO SUCCEED AS A COMPLIANCE PROFESSIONAL 2016 HCCA Compliance Institute Deann M. Baker, CHC, CCEP, CHRC Compliance Officer Sutter Health Sutter Care at Home Dwight

Compliance Effectiveness Strategies HOW TO SUCCEED AS A COMPLIANCE PROFESSIONAL 2016 HCCA Compliance Institute Deann M. Baker, CHC, CCEP, CHRC Compliance Officer Sutter Health Sutter Care at Home Dwight

Discussion Goals. Compliance Effectiveness Strategies HOW TO SUCCEED AS A COMPLIANCE PROFESSIONAL. Federal Sentencing Guidelines 3/16/2016

Compliance Effectiveness Strategies HOW TO SUCCEED AS A COMPLIANCE PROFESSIONAL 2016 HCCA Compliance Institute Deann M. Baker, CHC, CCEP, CHRC Compliance Officer Sutter Health Sutter Care at Home Dwight

Compliance Effectiveness Strategies HOW TO SUCCEED AS A COMPLIANCE PROFESSIONAL 2016 HCCA Compliance Institute Deann M. Baker, CHC, CCEP, CHRC Compliance Officer Sutter Health Sutter Care at Home Dwight

TERMS AND CONDITIONS OF EMPLOYMENT 5.03 CONFLICT OF INTEREST

. SECTION 5 TERMS AND CONDITIONS OF EMPLOYMENT 5.03 CONFLICT OF INTEREST AUTHORITY: TREASURY BOARD: TB#236/16 ADMINISTRATION: DEPUTY HEADS CEO OF PEI PUBLIC SERVICE COMMISSION CLERK OF THE EXECUTIVE COUNCIL

. SECTION 5 TERMS AND CONDITIONS OF EMPLOYMENT 5.03 CONFLICT OF INTEREST AUTHORITY: TREASURY BOARD: TB#236/16 ADMINISTRATION: DEPUTY HEADS CEO OF PEI PUBLIC SERVICE COMMISSION CLERK OF THE EXECUTIVE COUNCIL

2017 The Global ABB Integrity Program.

2017 The Global ABB Integrity Program www.abb.com/integrity Tone from the Top Don t Look the Other Way A culture of integrity is a prerequisite for a world-class business. Many valuable customers choose

2017 The Global ABB Integrity Program www.abb.com/integrity Tone from the Top Don t Look the Other Way A culture of integrity is a prerequisite for a world-class business. Many valuable customers choose

Corporate Compliance Plan

Corporate Compliance Plan Effective February 23, 2007 I. Compliance Policy Statement ABX Air, Inc. Corporate Compliance Plan This document is the Corporate Compliance Plan (this Plan ) of ABX Air, Inc.

Corporate Compliance Plan Effective February 23, 2007 I. Compliance Policy Statement ABX Air, Inc. Corporate Compliance Plan This document is the Corporate Compliance Plan (this Plan ) of ABX Air, Inc.

The IT Security Response to Misconduct Allegations

Security Executive Council Publication Series The IT Security Response to Misconduct Allegations Guidelines for Successful Investigations in Organizations by John D. Thompson, Esq. 2006 SECURITY EXECUTIVE

Security Executive Council Publication Series The IT Security Response to Misconduct Allegations Guidelines for Successful Investigations in Organizations by John D. Thompson, Esq. 2006 SECURITY EXECUTIVE

Computer Programs and Systems, Inc. Code of Business Conduct and Ethics

(as of January 28, 2013) Introduction This sets forth the guiding principles by which we operate Computer Programs and Systems, Inc. (the Company ) and conduct our daily business with our stockholders,

(as of January 28, 2013) Introduction This sets forth the guiding principles by which we operate Computer Programs and Systems, Inc. (the Company ) and conduct our daily business with our stockholders,

2011 Smithsonian Employee Perspective Survey Dashboard of Key Metrics

Dashboard of Key Metrics Satisfaction With Job Willing to Recommend Working at the Smithsonian 2010 Federal EVS Favorable Score, 72% 2010 SI Favorable Score, 84% 2011 SI Favorable Score, 82% 2010 Federal

Dashboard of Key Metrics Satisfaction With Job Willing to Recommend Working at the Smithsonian 2010 Federal EVS Favorable Score, 72% 2010 SI Favorable Score, 84% 2011 SI Favorable Score, 82% 2010 Federal

Swiss Code of Conduct. KPMG Switzerland

Swiss Code of Conduct KPMG Switzerland Content 3 A note from the CEO 4 Introduction 6 Our values 8 Our commitment 12 Our responsibilities 16 Where to get help 17 Compliance with the Code 18 Contact and

Swiss Code of Conduct KPMG Switzerland Content 3 A note from the CEO 4 Introduction 6 Our values 8 Our commitment 12 Our responsibilities 16 Where to get help 17 Compliance with the Code 18 Contact and

ISO & ISO TRAINING DAY 4 : Certifying ISO 37001

ISO 19600 & ISO 37001 TRAINING DAY 4 : Certifying ISO 37001 2017 SLIDE 1 DAY 4 Program Part 1 : Audit rules 1. Audit principles 2. Types of findings Part 2 : Audit process 3. The steps of an audit 4. Audit

ISO 19600 & ISO 37001 TRAINING DAY 4 : Certifying ISO 37001 2017 SLIDE 1 DAY 4 Program Part 1 : Audit rules 1. Audit principles 2. Types of findings Part 2 : Audit process 3. The steps of an audit 4. Audit

The Company seeks to comply with both the letter and spirit of the laws and regulations in all countries in which it operates.

1. Policy Statement ROOT9B HOLDINGS, INC. CODE OF BUSINESS CONDUCT AND ETHICS The Nasdaq listing standards require that the Company provide a code of conduct for all of its directors, officers and employees.

1. Policy Statement ROOT9B HOLDINGS, INC. CODE OF BUSINESS CONDUCT AND ETHICS The Nasdaq listing standards require that the Company provide a code of conduct for all of its directors, officers and employees.

MBS Code of Conduct. MBS places great importance on the values of ethical conduct, efficiency, fairness, impartiality and integrity.

MBS Code of Conduct 1. Purpose MBS values diversity and is committed to achieving a workforce which is inclusive and respectful of each other s differences. We are expected to treat all people we deal

MBS Code of Conduct 1. Purpose MBS values diversity and is committed to achieving a workforce which is inclusive and respectful of each other s differences. We are expected to treat all people we deal

Six Elements of Effective Compliance Training:

WHITE PAPER Six Elements of Effective Compliance Training: What Moves the Needle EXECUTIVE SUMMARY There are six elements to an effective compliance training program. This paper outlines these components

WHITE PAPER Six Elements of Effective Compliance Training: What Moves the Needle EXECUTIVE SUMMARY There are six elements to an effective compliance training program. This paper outlines these components

OUR CODE OF BUSINESS CONDUCT AND ETHICS

OUR CODE OF BUSINESS CONDUCT AND ETHICS Introduction This Code of Business Conduct and Ethics covers a wide range of business practices and procedures. It does not cover every issue that may arise, but

OUR CODE OF BUSINESS CONDUCT AND ETHICS Introduction This Code of Business Conduct and Ethics covers a wide range of business practices and procedures. It does not cover every issue that may arise, but

About the Presentations

About the Presentations The presentations cover the objectives found in the opening of each chapter. All chapter objectives are listed in the beginning of each presentation. You may customize the presentations

About the Presentations The presentations cover the objectives found in the opening of each chapter. All chapter objectives are listed in the beginning of each presentation. You may customize the presentations

University of Kentucky 2017 Engagement Survey. Human Resources Overall

2017 Engagement Survey Definition of Terms 3WEEKS of survey administration September 6 th 27 th 99% Response rate 86% in 2015 121 responded to the survey 1 Comment Question Sustainable Engagement: 85%

2017 Engagement Survey Definition of Terms 3WEEKS of survey administration September 6 th 27 th 99% Response rate 86% in 2015 121 responded to the survey 1 Comment Question Sustainable Engagement: 85%

Whistle Blowing Policy

Whistle Blowing Policy Introduction Whistle blowing occurs when an employee provides certain types of information, usually to their employer or a regulator, which has come to their attention through work.

Whistle Blowing Policy Introduction Whistle blowing occurs when an employee provides certain types of information, usually to their employer or a regulator, which has come to their attention through work.

CORPORATE GOVERNANCE POLICY

CORPORATE GOVERNANCE STATEMENT Atlantic is committed to building a diversified portfolio of resources assets that deliver superior returns to shareholders. Atlantic will seek to achieve this through strong

CORPORATE GOVERNANCE STATEMENT Atlantic is committed to building a diversified portfolio of resources assets that deliver superior returns to shareholders. Atlantic will seek to achieve this through strong

BOARD SKILL AND TRAINING BENCHMARKING ANALYSIS October 2012

BOARD SKILL AND TRAINING BENCHMARKING ANALYSIS October 2012 INTRODUCTION Benchmarking the performance of ICANN s board to principles and practices of other like-minded organizations can lead to overall

BOARD SKILL AND TRAINING BENCHMARKING ANALYSIS October 2012 INTRODUCTION Benchmarking the performance of ICANN s board to principles and practices of other like-minded organizations can lead to overall

Compliance Program Effectiveness

Compliance Program Effectiveness Presented by F. Lisa Murtha, Managing Director, Huron Consulting Group and Huron Consulting Services LLC. All rights reserved. The Presentation: Order of Topics Seven Core

Compliance Program Effectiveness Presented by F. Lisa Murtha, Managing Director, Huron Consulting Group and Huron Consulting Services LLC. All rights reserved. The Presentation: Order of Topics Seven Core

MiMedx Group, Inc. Code of Business Conduct and Ethics

MiMedx Group, Inc. Code of Business Conduct and Ethics 1. Introduction. 1.1 The Board of Directors of MiMedx Group, Inc. (together with its subsidiaries, the "Company") has adopted this Code of Business

MiMedx Group, Inc. Code of Business Conduct and Ethics 1. Introduction. 1.1 The Board of Directors of MiMedx Group, Inc. (together with its subsidiaries, the "Company") has adopted this Code of Business

MEASURING YOUR ORGANIZATION S CLIMATE FOR ETHICS: THE SURVEY APPROACH

MEASURING YOUR ORGANIZATION S CLIMATE FOR ETHICS: THE SURVEY APPROACH By Richard P. Kusserow, former DHHS Inspector General The U.S. Sentencing Commission explicitly recognized the significance of culture

MEASURING YOUR ORGANIZATION S CLIMATE FOR ETHICS: THE SURVEY APPROACH By Richard P. Kusserow, former DHHS Inspector General The U.S. Sentencing Commission explicitly recognized the significance of culture

Just cause terminations cannot be actioned unless due process is confirmed by the Deputy Minister, BC Public Service Agency.

Policy The objective of this administrative policy is to clarify the employer s roles, responsibilities and procedures with respect to just cause employment termination decisions under section 22(2) of

Policy The objective of this administrative policy is to clarify the employer s roles, responsibilities and procedures with respect to just cause employment termination decisions under section 22(2) of

RSM US CODE OF CONDUCT GROUNDED IN OUR VALUES - RESPECT, INTEGRITY, TEAMWORK, EXCELLENCE AND STEWARDSHIP

RSM US CODE OF CONDUCT GROUNDED IN OUR VALUES - RESPECT, INTEGRITY, TEAMWORK, EXCELLENCE AND STEWARDSHIP MESSAGE FROM JOE ADAMS RSM US MANAGING PARTNER & CEO At RSM US LLP (RSM), we ve spent nearly 90

RSM US CODE OF CONDUCT GROUNDED IN OUR VALUES - RESPECT, INTEGRITY, TEAMWORK, EXCELLENCE AND STEWARDSHIP MESSAGE FROM JOE ADAMS RSM US MANAGING PARTNER & CEO At RSM US LLP (RSM), we ve spent nearly 90

716 West Ave Austin, TX USA

FRAUD-RELATED INTERNAL CONTROLS GLOBAL Headquarters the gregor building 716 West Ave Austin, TX 78701-2727 USA Figure 2.1 COSO defines an internal control as a process, effected by an entity s board of

FRAUD-RELATED INTERNAL CONTROLS GLOBAL Headquarters the gregor building 716 West Ave Austin, TX 78701-2727 USA Figure 2.1 COSO defines an internal control as a process, effected by an entity s board of

Audit Committee Self Assessment

Audit Committee Institute United Kingdom Audit Committee Self Assessment The audit committee should regularly assess its own effectiveness and the adequacy of its terms of reference, work plans, forums

Audit Committee Institute United Kingdom Audit Committee Self Assessment The audit committee should regularly assess its own effectiveness and the adequacy of its terms of reference, work plans, forums

WHISTLE BLOWING POLICY

WHISTLE BLOWING POLICY Status Last reviewed: Review Date Recommended Spring 2017 Spring 2018 Resources and References Somerset County Council Policy adopted in full Updated August 2014 1. Introduction

WHISTLE BLOWING POLICY Status Last reviewed: Review Date Recommended Spring 2017 Spring 2018 Resources and References Somerset County Council Policy adopted in full Updated August 2014 1. Introduction

Internal Controls & Ethics

Internal Controls and Ethics Internal Controls & Ethics 1 Session Objectives Refresher on Internal Audit Be able to assess risks in your department Be able to apply internal control concepts to mitigate

Internal Controls and Ethics Internal Controls & Ethics 1 Session Objectives Refresher on Internal Audit Be able to assess risks in your department Be able to apply internal control concepts to mitigate

Supervision Policy. Safeguarding in Education

Supervision Policy Safeguarding in Education This policy has been written to ensure Worth Primary School fulfils its responsibilities under the 2012 Early Years Foundation Stage (EYFS 2012) in providing

Supervision Policy Safeguarding in Education This policy has been written to ensure Worth Primary School fulfils its responsibilities under the 2012 Early Years Foundation Stage (EYFS 2012) in providing

When making decisions affecting Long Island University s assets and/or resources, individuals must adhere to the following standards:

Conflict of Interest/Commitment Policy for Long Island University Introduction As part of its educational mission, Long Island University believes in the importance of interacting with the wider community

Conflict of Interest/Commitment Policy for Long Island University Introduction As part of its educational mission, Long Island University believes in the importance of interacting with the wider community

CODE OF CONDUCT. At HITT, our focus goes beyond simply getting the job done; it s about how we conduct ourselves while we do it.

At HITT, our focus goes beyond simply getting the job done; it s about how we conduct ourselves while we do it. Our team members actions are a direct representation of the company an organization that

At HITT, our focus goes beyond simply getting the job done; it s about how we conduct ourselves while we do it. Our team members actions are a direct representation of the company an organization that

Director Training and Qualifications

4711 Yonge Street Suite 700 Toronto ON M2N 6K8 Telephone: 416-325-9444 Toll Free 1-800-268-6653 Fax: 416-325-9722 4711, rue Yonge Bureau 700 Toronto (Ontario) M2N 6K8 Téléphone : 416 325-9444 Sans frais

4711 Yonge Street Suite 700 Toronto ON M2N 6K8 Telephone: 416-325-9444 Toll Free 1-800-268-6653 Fax: 416-325-9722 4711, rue Yonge Bureau 700 Toronto (Ontario) M2N 6K8 Téléphone : 416 325-9444 Sans frais

Acceleron Pharma Inc. Code of Business Conduct and Ethics

I. INTRODUCTION Acceleron Pharma Inc. Code of Business Conduct and Ethics (Amended & Restated as of March 1, 2018) This Code of Business Conduct and Ethics ( Code ) provides a general statement of the

I. INTRODUCTION Acceleron Pharma Inc. Code of Business Conduct and Ethics (Amended & Restated as of March 1, 2018) This Code of Business Conduct and Ethics ( Code ) provides a general statement of the

CODE OF BUSINESS CONDUCT AND ETHICS

CODE OF BUSINESS CONDUCT AND ETHICS INTRODUCTION This Code of Business Conduct and Ethics (the Code ) embodies the commitment of Sama Resources Inc. ( Sama ) to conduct its business in accordance with

CODE OF BUSINESS CONDUCT AND ETHICS INTRODUCTION This Code of Business Conduct and Ethics (the Code ) embodies the commitment of Sama Resources Inc. ( Sama ) to conduct its business in accordance with

McKesson at-a-glance America s oldest and largest healthcare services company

Leveraging Ethics and Compliance Program Assessments to Enhance Program Effectiveness and Manage Risk SCCE Compliance and Ethics Institute October 6, 2013 Amii Barnard-Bahn Chief Compliance & Ethics Officer

Leveraging Ethics and Compliance Program Assessments to Enhance Program Effectiveness and Manage Risk SCCE Compliance and Ethics Institute October 6, 2013 Amii Barnard-Bahn Chief Compliance & Ethics Officer

CODE OF BUSINESS CONDUCT AND ETHICS

CODE OF BUSINESS CONDUCT AND ETHICS PURPOSE && SCOPE As a Trimac team member it is important to know that everyone must act ethically, morally and legally at all times no exceptions. This document outlines:

CODE OF BUSINESS CONDUCT AND ETHICS PURPOSE && SCOPE As a Trimac team member it is important to know that everyone must act ethically, morally and legally at all times no exceptions. This document outlines:

7 Elements Roundtable

7 Elements Roundtable Listen. Learn. Share. Connect Rules Participants break into 7 groups Introductions Get acquainted; build your network Each groups should delegate secretary (notes) & a speaker to

7 Elements Roundtable Listen. Learn. Share. Connect Rules Participants break into 7 groups Introductions Get acquainted; build your network Each groups should delegate secretary (notes) & a speaker to

The most commonly applied model for designing and auditing internal

Fair Value Accounting Fraud: New Global Risks and Detection Techniques By Gerard M. Zack Copyright 2009 by Gerard M. Zack Appendix C Internal Controls over Fair Value Accounting Applications The most commonly

Fair Value Accounting Fraud: New Global Risks and Detection Techniques By Gerard M. Zack Copyright 2009 by Gerard M. Zack Appendix C Internal Controls over Fair Value Accounting Applications The most commonly

DeVry Education Group Ethics and Compliance Services Policy C-1. Speak Up: Asking Questions & Raising Concerns

DeVry Education Group Ethics and Compliance Services Policy C-1 Speak Up: Asking Questions & Raising Concerns Effective Date: April 30, 2010 Revision Date: December 01, 2013 Policy Owned by: Ethics and

DeVry Education Group Ethics and Compliance Services Policy C-1 Speak Up: Asking Questions & Raising Concerns Effective Date: April 30, 2010 Revision Date: December 01, 2013 Policy Owned by: Ethics and

Page: Page 1 of 5 Effective Date: January 27, 2004 Authorized By: President and CEO Function: Executive

Page 1 of 5 I. PURPOSE The Board of Directors has adopted the following Code of Business Conduct and Ethics (this Code ) for officers, directors and employees of RBC Bearings Incorporated (the Company

Page 1 of 5 I. PURPOSE The Board of Directors has adopted the following Code of Business Conduct and Ethics (this Code ) for officers, directors and employees of RBC Bearings Incorporated (the Company