Chapter 18. Integrated Audits of Public Companies. McGraw-Hill/Irwin. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

|

|

|

- Alan Ball

- 5 years ago

- Views:

Transcription

1 Chapter 18 Integrated Audits of Public Companies McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

2 Nature of an Integrated Audit Auditors of public companies should report on: Financial statements and Internal control over financial reporting Based on provisions of PCAOB Standard No. 5, the audits of internal control and financial reporting should be integrated 18-2

3 Sarbanes-Oxley Act of 2002 Section (a) requires annual report filed with SEC to include an internal control report Management acknowledges responsibility for establishing and maintaining adequate internal control Provides assessment of internal control effectiveness at end of fiscal year 404(b) requires CPA firm to audit internal control and express an opinion on effectiveness of internal control. (Required for companies with a capitalization in excess of $75,000,000) 18-3

4 Management s Responsibility Accept responsibility for effectiveness Evaluate the effectiveness using suitable criteria Support the evaluation with sufficient evidence Provide a report on internal control 18-4

5 Management s Report on I/C Report must: State that it is management s responsibility to establish and maintain adequate internal control. Identify management s framework for evaluating internal control. Include management s assessment of the effectiveness of the company s internal control over financial reporting as of the end of the most recent fiscal period, including a statement as to whether internal control over financial reporting is effective. Include a statement that the company s auditors have issued an attestation report on management s assessment. 18-5

6 Management Assessment Management can be assisted by consultants but not by the CPA firm that conducts the audit of financial statements Must understand definition of internal control adopted by the SEC Evaluation must use an accepted control framework such as Internal Control-Integrated Framework created by COSO. Must understand concepts of control deficiency, significant deficiency and material weakness 18-6

7 18-7

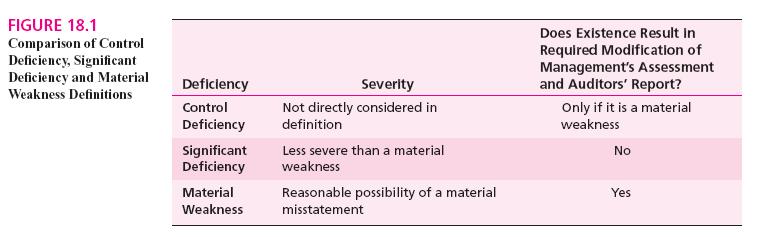

8 Relationships Among Deficiencies Deficiency in Internal Control Less than Significant Material Significant Deficiency Weakness 18-8

9 Control concepts Control deficiency exists when the design or operation of a control does not allow management or employees, in the normal course of performing their functions, to prevent or detect misstatements on a timely basis Levels of severity of control deficiencies Less than a significant deficiency Significant deficiency less severe than material weakness yet important enough to merit attention Material weakness reasonable possibility that a material misstatement will not be prevented or detected 18-9

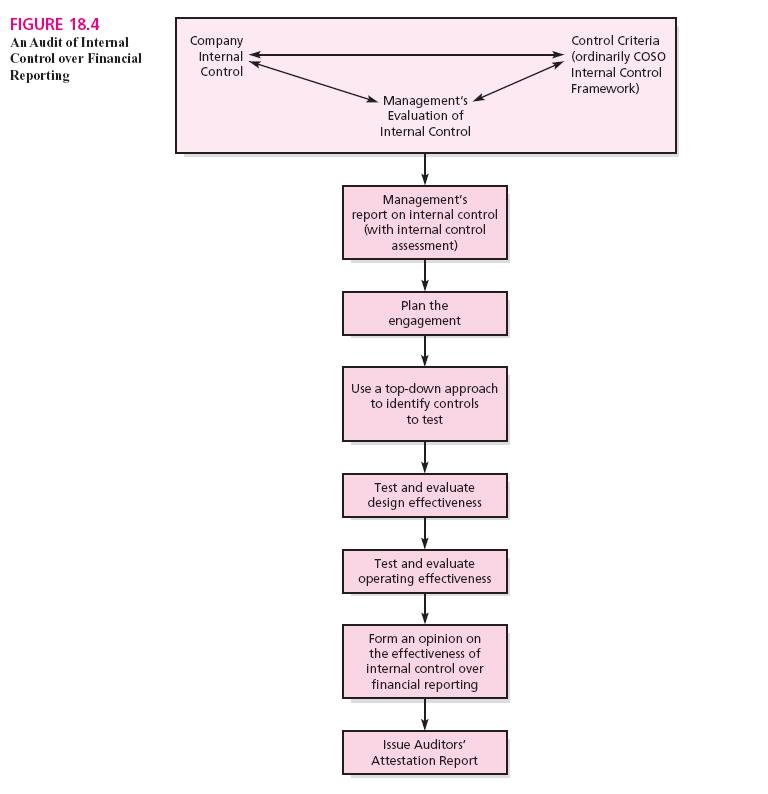

10 Objective of Management s Evaluation of I/C Provide a reasonable basis for its annual assessment Process Evaluate design effectiveness of controls Evaluate operating effectiveness of internal control Documentation of process Reporting 18-10

11 Auditor s Objective Plan and perform the audit to obtain reasonable assurance about whether material weaknesses exist to express an opinion on company s internal control over financial reporting Evidence gathered as of date specified in management s assessment normally the last day of the company s fiscal year 18-11

12 Audit Steps 1. Plan the engagement 2. Use a top-down approach to identify controls to test 3. Test and evaluate design effectiveness of internal control 4. Test and evaluate operating effectiveness of internal control 5. Form an opinion on the effectiveness of internal control 18-12

13 18-13

14 Plan the Engagement Efficient planning requires coordination with financial statement audit Consider matters such as: Client s industry Regulatory matters Client s business Recent changes in client s operations 18-14

15 Auditors Consideration of I/C Difference between audit of internal control and audit of financial statements Time period Audit of internal control as of date Audit of financial statements entire financial statement period Differences between small and large clients Degree of complexity of operations 18-15

16 Top-Down Approach 18-16

17 Top-Down Approach Goal is to focus on testing those controls that are most important to auditor s conclusion on internal control, avoiding those that are less important Starts at top Entity-level controls those in control environment or monitoring components of internal control Emphasize those relating to audit committee effectiveness, fraud, and period-end process Direct or indirect effect 18-17

18 18-18

19 Significant Accounts and Disclosures Account significant if reasonable possibility that it could contain a misstatement that individually or in aggregate has a material effect on financial statements Factors Size and composition. Susceptibility of loss due to errors or fraud. Volume of activity, complexity, and homogeneity of individual transactions. Nature of the account. Accounting and reporting complexity. Exposure to losses. Possibility of significant contingent liabilities. Existence of related party transactions. Changes from the prior period

20 Identifying Relevant Assertions Relevant Those that have meaningful bearing on whether account is presented fairly (1) existence or occurrence; (2) completeness; (3) valuation or allocation; (4) rights and obligations; and/or (5) presentation and disclosure

21 Design Effectiveness Routine transactions are for recurring activities, Examples: sales, purchases, cash receipts and disbursements, and payroll. Nonroutine transactions occur only periodically; they generally are not part of the routine flow of transactions Examples: transactions such as counting and pricing inventory, calculating depreciation expense, or determining prepaid expenses. Accounting estimates are activities involving management s judgments or assumptions, Examples: determining the allowance for doubtful accounts, estimating warranty reserves and assessing assets for impairment 18-21

22 Likely Source of Misstatements Understand the flow of transactions; Verify points within the company s processes at which a misstatement could arise that could be material; Identify the controls management has implemented to address these potential misstatements; and Identify the controls management has implemented to prevent or detect on a timely basis unauthorized acquisition, use, or disposition of the company s assets that could result in a material misstatement

23 Selecting Controls Not necessary to design tests of all controls Redundant controls Do not need to test if duplicate control is tested Design tests for preventive and/or detective controls Complementary controls Should both be tested 18-23

24 Performing Walk-Throughs Walk-through Tracing a transaction from its origination through the company s information system until it is reflected in the company s financial reports Provide evidence to: Verify that they have identified points at which a significant risk of misstatement to a relevant assertion exists. Verify their understanding of the design of controls, including those related to the prevention or detection of fraud. Evaluate the effectiveness of the design of controls. Confirm whether controls have been placed in operation (implemented)

25 Tests of Operating Effectiveness Nature Inquiries, inspections, observations and reperformance Vary exact tests when possible Timing Sufficient period of time Periodic controls wait to after report date Extent Depend on frequency of control 18-25

26 Frequency of Testing 18-26

27 Relationship Between Audits Tests of controls Same for internal control audit and financial statement audit Evidence from internal control audit can be used for financial statement audit Differences between audits Objectives are different Integrated audit Testing should be spread through the year to satisfy both objectives 18-27

28 Effects of Internal Control Testing on Audit Substantive Procedures Integrated audit requires tests of controls for all major account and relevant assertions Will lead to decreased scope of substantive procedures However, significant deficiencies or material weaknesses could lead to more substantive procedures Not acceptable to omit substantive procedures completely 18-28

29 Effect of Substantive Procedures on Audit of Internal Control Findings from substantive procedures may affect audit of internal control Could provide evidence of effectiveness or ineffectiveness of internal control over financial reporting Example: Identification of material misstatement in financial statements is indicative of at least a significant deficiency in internal control 18-29

30 Form an opinion Evaluate: 1. The results of their evaluation of the design, 2. The results of tests of the operating effectiveness of controls, 3. Negative results of substantive procedures performed during the financial statement audit, and 4. Any identified control deficiencies

31 18-31

32 Circumstances Affecting the Auditors Opinions 18-32

33 Other Communication Requirements Communicate in writing to management All control deficiencies regardless of severity To audit committee Material weaknesses, significant deficiencies and that all deficiencies have been communicated to management To board of directors If conclude oversight of financial reporting and internal control is ineffective 18-33

34 Other Report Reporting on Whether a Previously Reported Material Weakness Continues to Exist Management believes material weakness has been eliminated Auditor engaged to report on whether material weakness continues to exist Engagement focused on evidence regarding material weakness 18-34

35 Integrated Audis for Nonpublic Companies A nonpublic company may choose to have an integrated audit of its financial statements and its internal control. While the service is very similar to that for public companies, it differs as follows: 18-35

CLIENT ALERT: INTERNAL CONTROL OVER FINANCIAL REPORTING

CLIENT ALERT: INTERNAL CONTROL OVER FINANCIAL REPORTING All public companies either have begun or will soon begin a process, required under Section 404 of the Sarbanes-Oxley Act of 2002 ( SOX ), of reviewing

CLIENT ALERT: INTERNAL CONTROL OVER FINANCIAL REPORTING All public companies either have begun or will soon begin a process, required under Section 404 of the Sarbanes-Oxley Act of 2002 ( SOX ), of reviewing

Chapter 7. Auditing Internal Control over Financial Reporting. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 7 Auditing Internal Control over Financial Reporting McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Management Responsibilities under Section 404 Management

Chapter 7 Auditing Internal Control over Financial Reporting McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Management Responsibilities under Section 404 Management

Chapter 06. Audit Planning, Understanding the Client, Assessing Risks, and Responding. McGraw-Hill/Irwin

Chapter 06 Audit Planning, Understanding the Client, Assessing Risks, and Responding McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Obtaining Clients Submit a

Chapter 06 Audit Planning, Understanding the Client, Assessing Risks, and Responding McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Obtaining Clients Submit a

Comparison of the PCAOB s Auditing Standards No. 5 and No. 2 (Certain key differences are highlighted by underlining)

") Comparison of the PCAOB s Auditing Standards No. 5 and No. 2 (Certain key differences are highlighted by underlining) Topic AS No. 5 AS No. 2 Objective of ICFR Audit Planning the ICFR Audit Integration

Comparison of the PCAOB s Auditing Standards No. 5 and No. 2 (Certain key differences are highlighted by underlining) Topic AS No. 5 AS No. 2 Objective of ICFR Audit Planning the ICFR Audit Integration

An Examination of an Entity s Internal Control Over Financial Reporting That Is Integrated With an Audit of Its Financial Statements

ASB Meeting July 30 August 1, 2013 Agenda Item 3B AT Section 501 An Examination of an Entity s Internal Control Over Financial Reporting That Is Integrated With an Audit of Its Financial Statements Source:

ASB Meeting July 30 August 1, 2013 Agenda Item 3B AT Section 501 An Examination of an Entity s Internal Control Over Financial Reporting That Is Integrated With an Audit of Its Financial Statements Source:

covered member immediate family impaired not a covered member close relative not impaired

BUS 425 Auditing Tad Miller May 22, 2017 Audit Planning, Analytical Procedures, Materiality & Risk, Internal Control Evaluation and Audit Plan 1. INDEPENDENCE All independence problems refer to a client

BUS 425 Auditing Tad Miller May 22, 2017 Audit Planning, Analytical Procedures, Materiality & Risk, Internal Control Evaluation and Audit Plan 1. INDEPENDENCE All independence problems refer to a client

Community Bankers Conference

3rd Annual Regional and Community Bankers Conference The Federal Reserve Bank of Boston Disclaimer NEVER WRONG DON T COMPLETELY RELY UPON Recent Developments in Audit Practice SOX, FDICIA 112, Other Robert

3rd Annual Regional and Community Bankers Conference The Federal Reserve Bank of Boston Disclaimer NEVER WRONG DON T COMPLETELY RELY UPON Recent Developments in Audit Practice SOX, FDICIA 112, Other Robert

AUDIT RESPONSIBILITIES AND OBJECTIVES

AUDIT RESPONSIBILITIES AND OBJECTIVES CHAPTER 6 Copyright 2017 Pearson Education, Ltd. 6-1 CHAPTER 1 LEARNING OBJECTIVES 6-1 Explain the objective of conducting an audit of financial statements and an

AUDIT RESPONSIBILITIES AND OBJECTIVES CHAPTER 6 Copyright 2017 Pearson Education, Ltd. 6-1 CHAPTER 1 LEARNING OBJECTIVES 6-1 Explain the objective of conducting an audit of financial statements and an

An Audit of Internal Control Over Financial Reporting Performed in Conjunction with An Audit of Financial Statements

AUDITING STANDARD No. 2 An Audit of Internal Control Over Financial Reporting Performed in Conjunction with An Audit of Financial Statements March 9, 2004 AUDITING AND RELATED PROFESSIONAL PRACTICE STANDARDS

AUDITING STANDARD No. 2 An Audit of Internal Control Over Financial Reporting Performed in Conjunction with An Audit of Financial Statements March 9, 2004 AUDITING AND RELATED PROFESSIONAL PRACTICE STANDARDS

An Audit of Internal Control Over Financial Reporting Performed in Conjunction with An Audit of Financial Statements

Page A 1 Standard Appendix Auditing Standard No. 2 AUDITING AND RELATED PROFESSIONAL PRACTICE STANDARDS Auditing Standard No. 2 An Audit of Internal Control Over Financial Reporting Performed in Conjunction

Page A 1 Standard Appendix Auditing Standard No. 2 AUDITING AND RELATED PROFESSIONAL PRACTICE STANDARDS Auditing Standard No. 2 An Audit of Internal Control Over Financial Reporting Performed in Conjunction

B S R & Co. LLP. Reporting on Internal. Reporting An Overview. Sarbanes Oxley Act (SOX) 28 December 2013

28 December 2013") B S R & Co. LLP Reporting on Internal Controls over Financial Reporting An Overview Sarbanes Oxley Act (SOX) 28 December 2013 Agenda Sarbanes Oxley Key Sections COSO Framework Management Approach to ICOFR

B S R & Co. LLP Reporting on Internal Controls over Financial Reporting An Overview Sarbanes Oxley Act (SOX) 28 December 2013 Agenda Sarbanes Oxley Key Sections COSO Framework Management Approach to ICOFR

Report on Inspection of KPMG AG Wirtschaftspruefungsgesellschaft (Headquartered in Berlin, Federal Republic of Germany)

") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Berlin, Federal Republic of Germany) Issued by the Public Company

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Berlin, Federal Republic of Germany) Issued by the Public Company

Detailed competency map

Detailed competency map Additional competency requirements for entry to the Hong Kong Institute of CPAs qualification programme (Professional bridging examination) Fields of competency The items listed

Detailed competency map Additional competency requirements for entry to the Hong Kong Institute of CPAs qualification programme (Professional bridging examination) Fields of competency The items listed

Report on Inspection of Deloitte LLP (Headquartered in Toronto, Canada) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2014 (Headquartered in Toronto, Canada) Issued by the Public Company Accounting Oversight

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2014 (Headquartered in Toronto, Canada) Issued by the Public Company Accounting Oversight

CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a. AUDITING THEORY Risk Assessment and Response to Assessed Risks

Page 1 of 7 CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a Related PSAs: PSA 400, 315 and 330 AUDITING THEORY Risk Assessment and Response to Assessed Risks 1. Which of the following is correct statement?

Page 1 of 7 CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a Related PSAs: PSA 400, 315 and 330 AUDITING THEORY Risk Assessment and Response to Assessed Risks 1. Which of the following is correct statement?

Audrey A. Gramling Kennesaw State University. Larry E. Rittenberg. University of Wisconsin Madison. Karla M. Johnstone

Auditin Audrey A. Gramling Kennesaw State University Larry E. Rittenberg University of Wisconsin Madison Karla M. Johnstone University of Wisconsin Madison /% SOUTH-WESTERN *% CENGAGE Learning- Australia

Auditin Audrey A. Gramling Kennesaw State University Larry E. Rittenberg University of Wisconsin Madison Karla M. Johnstone University of Wisconsin Madison /% SOUTH-WESTERN *% CENGAGE Learning- Australia

Auditing and Attestation (AUD) - Content Outline Effective January 2014

- Content Outline Effective January 2014") Auditing and Attestation (AUD) - Content Outline Effective January 2014 The Auditing and Attestation section tests knowledge and understanding of the following professional standards: Auditing standards

Auditing and Attestation (AUD) - Content Outline Effective January 2014 The Auditing and Attestation section tests knowledge and understanding of the following professional standards: Auditing standards

Report on Inspection of KAP Purwantono, Sungkoro & Surja (Headquartered in Jakarta, Republic of Indonesia)

") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 Inspection of KAP Purwantono, (Headquartered in Jakarta, Republic of Indonesia)

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 Inspection of KAP Purwantono, (Headquartered in Jakarta, Republic of Indonesia)

Auditing Standards and Practices Council

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 330 THE AUDITOR S PROCEDURES IN RESPONSE TO ASSESSED RISKS PHILIPPINE STANDARD ON AUDITING 330 THE AUDITOR S PROCEDURES IN RESPONSE

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 330 THE AUDITOR S PROCEDURES IN RESPONSE TO ASSESSED RISKS PHILIPPINE STANDARD ON AUDITING 330 THE AUDITOR S PROCEDURES IN RESPONSE

Chapter 5. Evidence and Documentation. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Chapter 5 Evidence and Documentation McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Relationship of Audit LO# 1 Evidence to the Audit Report Financial statements

Chapter 5 Evidence and Documentation McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Relationship of Audit LO# 1 Evidence to the Audit Report Financial statements

FDICIA Reporting for Financial Institutions. Reporting Changes Under Part 363 and SAS 130

FDICIA Reporting for Financial Institutions Reporting Changes Under Part 363 and SAS 130 CONTENTS 02 INTRODUCTION REQUIREMENTS BY TIER 03 03 Management Assessment 04 05 03 Independent Auditors FILING DEADLINES

FDICIA Reporting for Financial Institutions Reporting Changes Under Part 363 and SAS 130 CONTENTS 02 INTRODUCTION REQUIREMENTS BY TIER 03 03 Management Assessment 04 05 03 Independent Auditors FILING DEADLINES

2016 INSPECTION OF BHARAT PARIKH & ASSOCIATES CHARTERED ACCOUNTANTS. Preface

2016 INSPECTION OF BHARAT PARIKH & ASSOCIATES CHARTERED ACCOUNTANTS Preface In 2016, the Public Company Accounting Oversight Board ("PCAOB" or "the Board") conducted an inspection of the registered public

2016 INSPECTION OF BHARAT PARIKH & ASSOCIATES CHARTERED ACCOUNTANTS Preface In 2016, the Public Company Accounting Oversight Board ("PCAOB" or "the Board") conducted an inspection of the registered public

Chapter 13. Auditing the Inventory Management Process

Chapter 13 Auditing the Inventory Management Process Copyright 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Chapter 13 Auditing the Inventory Management Process Copyright 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

After completing this Session, you should be able to answer the following questions:

About this Course Welcome to CMA Auditing Course, Part II. Below, you will find a short summary of the modules. Upon registration, further introductory resources will tell you: How the course is organized

About this Course Welcome to CMA Auditing Course, Part II. Below, you will find a short summary of the modules. Upon registration, further introductory resources will tell you: How the course is organized

Report on Inspection of KPMG Auditores Consultores Ltda. (Headquartered in Santiago, Republic of Chile)

") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Santiago, Republic of Chile) Issued by the Public Company Accounting

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Santiago, Republic of Chile) Issued by the Public Company Accounting

Evaluating Internal Controls

A SSURANCE AND A DVISORY BUSINESS S ERVICES Fourth in the Series!@# Evaluating Internal Controls Evaluating Overall Effectiveness, Identifying Matters for Improvement, and Ongoing Assessment of Controls

A SSURANCE AND A DVISORY BUSINESS S ERVICES Fourth in the Series!@# Evaluating Internal Controls Evaluating Overall Effectiveness, Identifying Matters for Improvement, and Ongoing Assessment of Controls

2013 INSPECTION OF GEORGE STEWART, CPA

2013 INSPECTION OF GEORGE STEWART, CPA In 2013, the Public Company Accounting Oversight Board ("PCAOB" or "the Board") conducted an inspection of the registered public accounting firm George Stewart, CPA

2013 INSPECTION OF GEORGE STEWART, CPA In 2013, the Public Company Accounting Oversight Board ("PCAOB" or "the Board") conducted an inspection of the registered public accounting firm George Stewart, CPA

Report on Inspection of PricewaterhouseCoopers Audit (Headquartered in Neuilly-Sur-Seine, French Republic)

") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Neuilly-Sur-Seine, French Republic) Issued by the Public Company

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Neuilly-Sur-Seine, French Republic) Issued by the Public Company

INTERNATIONAL STANDARD ON AUDITING 500 AUDIT EVIDENCE CONTENTS

INTERNATIONAL STANDARD ON 500 AUDIT EVIDENCE (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph Introduction... 1-2 Concept of Audit Evidence...

INTERNATIONAL STANDARD ON 500 AUDIT EVIDENCE (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph Introduction... 1-2 Concept of Audit Evidence...

2013 INSPECTION OF ENTERPRISE CPAS, LTD.

2013 INSPECTION OF ENTERPRISE CPAS, LTD. In 2013, the Public Company Accounting Oversight Board ("PCAOB" or "the Board") conducted an inspection of the registered public accounting firm Enterprise CPAs,

2013 INSPECTION OF ENTERPRISE CPAS, LTD. In 2013, the Public Company Accounting Oversight Board ("PCAOB" or "the Board") conducted an inspection of the registered public accounting firm Enterprise CPAs,

The Auditor s Consideration of the Internal Audit Function in an Audit of Financial Statements

Auditor s Consideration of Internal Audit Function 381 AU Section 322 The Auditor s Consideration of the Internal Audit Function in an Audit of Financial Statements (Supersedes SAS No. 9) Source: SAS No.

Auditor s Consideration of Internal Audit Function 381 AU Section 322 The Auditor s Consideration of the Internal Audit Function in an Audit of Financial Statements (Supersedes SAS No. 9) Source: SAS No.

AT Assertions, Audit Procedures and Audit Evidence Red Sirug Page 1

AUDITING THEORY Red Sirug ASSERTIONS A ND A UDIT OBJECTIVES ASSERTIONS, A UDIT PROCEDURES A ND A UDIT EVIDENCE Nature of Assertions: Financial statements are not statements of facts. They are a collection

AUDITING THEORY Red Sirug ASSERTIONS A ND A UDIT OBJECTIVES ASSERTIONS, A UDIT PROCEDURES A ND A UDIT EVIDENCE Nature of Assertions: Financial statements are not statements of facts. They are a collection

Chapter 8. Planning and Testing Operating Effectiveness of Internal Control over Financial Reporting. Prepared by Richard J.

Chapter 8 Planning and Testing Operating Effectiveness of Internal Control over Financial Reporting Prepared by Richard J. Campbell Copyright 2011, Wiley and Sons Learning Objectives 1. Learn the relationships

Chapter 8 Planning and Testing Operating Effectiveness of Internal Control over Financial Reporting Prepared by Richard J. Campbell Copyright 2011, Wiley and Sons Learning Objectives 1. Learn the relationships

CHAPTER 10: SUBSTANTIVE TESTS OF TRANSACTIONS AND BALANCES

CHAPTER 10: SUBSTANTIVE TESTS OF TRANSACTIONS AND BALANCES 1 RELATIONSHIP BETWEEN TESTS OF CONTROLS AND SUBSTANTIVE TESTS OF TRANSACTIONS Most controls built around transaction flows. Tests of controls:

CHAPTER 10: SUBSTANTIVE TESTS OF TRANSACTIONS AND BALANCES 1 RELATIONSHIP BETWEEN TESTS OF CONTROLS AND SUBSTANTIVE TESTS OF TRANSACTIONS Most controls built around transaction flows. Tests of controls:

McGraw-Hill/Irwin. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 03 Engagement Planning "Vision without action is a daydream. Action without vision is a nightmare. Japanese

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 03 Engagement Planning "Vision without action is a daydream. Action without vision is a nightmare. Japanese

Report on. Issued by the. Public Company Accounting Oversight Board. June 16, 2016 THIS IS A PUBLIC VERSION OF A PCAOB INSPECTION REPORT

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 Inspection of Paredes, Zaldívar, Burga & Asociados Sociedad Civil de (Headquartered

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 Inspection of Paredes, Zaldívar, Burga & Asociados Sociedad Civil de (Headquartered

29 th Regional Conference of WIRC

29 th Regional Conference of WIRC Internal Financial Control - Auditors responsibility The Lalit International, Mumbai 6 December 2014 Contents 1 Provisions of Companies Act, 2013 2 Auditors responsibility

29 th Regional Conference of WIRC Internal Financial Control - Auditors responsibility The Lalit International, Mumbai 6 December 2014 Contents 1 Provisions of Companies Act, 2013 2 Auditors responsibility

McGraw-Hill/Irwin. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 03 Engagement Planning "Vision without action is a daydream. Action without vision is a nightmare. Japanese

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 03 Engagement Planning "Vision without action is a daydream. Action without vision is a nightmare. Japanese

Mapping Document AU Section 322 to Clarified Statement on Auditing Standards Using the Work of Internal Auditors

1 MAPPING DOCUMENT CLARIFIED STATEMENT ON AUDITING STANDARDS USING THE WORK OF INTERNAL AUDITORS This mapping document demonstrates how the material in extant AU section 322, The Auditor s Consideration

1 MAPPING DOCUMENT CLARIFIED STATEMENT ON AUDITING STANDARDS USING THE WORK OF INTERNAL AUDITORS This mapping document demonstrates how the material in extant AU section 322, The Auditor s Consideration

Presenter: CPA CATHERINE MUEMA

Presenter: CPA CATHERINE MUEMA ISA 230 requires an auditor to prepare audit documentation that is sufficient and appropriate to support the basis for the Auditor s report and confirm that the audit process

Presenter: CPA CATHERINE MUEMA ISA 230 requires an auditor to prepare audit documentation that is sufficient and appropriate to support the basis for the Auditor s report and confirm that the audit process

Report on Inspection of KPMG Cardenas Dosal, S.C. (Headquartered in Mexico City, United Mexican States)

") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Mexico City, United Mexican States) Issued by the Public Company

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Mexico City, United Mexican States) Issued by the Public Company

Public Company Accounting Oversight Board

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2008 (Headquartered in New York, New York) Issued by the Public Company Accounting

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2008 (Headquartered in New York, New York) Issued by the Public Company Accounting

Chapter 02. Professional Standards. McGraw-Hill/Irwin. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 02 Professional Standards McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Authority of Organizations Public Company Accounting Oversight Board Auditing,

Chapter 02 Professional Standards McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Authority of Organizations Public Company Accounting Oversight Board Auditing,

Auditing Standards and Practices Council

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT PHILIPPINE STANDARD ON AUDITING

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT PHILIPPINE STANDARD ON AUDITING

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT CONTENTS

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT (Effective for audits of financial statements for periods beginning

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT (Effective for audits of financial statements for periods beginning

AN AUDIT OF INTERNAL CONTROL THAT IS INTEGRATED WITH AN AUDIT OF FINANCIAL STATEMENTS: GUIDANCE FOR AUDITORS OF SMALLER PUBLIC COMPANIES

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org PRELIMINARY STAFF VIEWS AN AUDIT OF INTERNAL CONTROL THAT IS INTEGRATED WITH AN AUDIT OF FINANCIAL

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org PRELIMINARY STAFF VIEWS AN AUDIT OF INTERNAL CONTROL THAT IS INTEGRATED WITH AN AUDIT OF FINANCIAL

Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement

Issued December 2007 International Standard on Auditing Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement The Malaysian Institute of Certified Public Accountants

Issued December 2007 International Standard on Auditing Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement The Malaysian Institute of Certified Public Accountants

Business development companies

Business development companies Considerations related to internal controls over financial reporting (ICFR) By Matt Forstenhausler and Seren Tahiroglu Financial Services B usiness development companies

Business development companies Considerations related to internal controls over financial reporting (ICFR) By Matt Forstenhausler and Seren Tahiroglu Financial Services B usiness development companies

STATEMENT OF AUDITING STANDARDS 500 AUDIT EVIDENCE

STATEMENT OF AUDITING STANDARDS 500 AUDIT EVIDENCE (Issued January 2004) Contents Paragraphs Introduction 1-2 Concept of Audit Evidence 3-6 Sufficient Appropriate Audit Evidence 7-14 The Use of Assertions

STATEMENT OF AUDITING STANDARDS 500 AUDIT EVIDENCE (Issued January 2004) Contents Paragraphs Introduction 1-2 Concept of Audit Evidence 3-6 Sufficient Appropriate Audit Evidence 7-14 The Use of Assertions

VERSION #1 PLEASE WRITE ON YOUR SCANTRON

VERSION #1 PLEASE WRITE ON YOUR SCANTRON ECON 132A MIDTERM #1 ANDERSON PLEASE answer multiple choice questions on green scantron and the rest in your blue book. When you are done put your scantron inside

VERSION #1 PLEASE WRITE ON YOUR SCANTRON ECON 132A MIDTERM #1 ANDERSON PLEASE answer multiple choice questions on green scantron and the rest in your blue book. When you are done put your scantron inside

Modern Auditing: Assurance Services and the Integrity of Financial Reporting, 8 th Edition

Modern Auditing: Assurance Services and the Integrity of Financial Reporting, 8 th Edition William C. Boynton California Polytechnic State University at San Luis Obispo Raymond N. Johnson Portland State

Modern Auditing: Assurance Services and the Integrity of Financial Reporting, 8 th Edition William C. Boynton California Polytechnic State University at San Luis Obispo Raymond N. Johnson Portland State

VERSION #1 WRITE ON YOUR SCANTRON!!!

ECON 132A WINTER 2009 MIDTERM #2 Name: Date: ANSWER ALL MULTIPLE CHOICE QUESTIONS ON GREEN SCANTRON ANSWER QUESTIONS 29 & 30 IN THE SPACE PROVIDED ANSWER THE SIMULATION ASSIGNMENT IN YOUR BLUE-BOOK, PUT

ECON 132A WINTER 2009 MIDTERM #2 Name: Date: ANSWER ALL MULTIPLE CHOICE QUESTIONS ON GREEN SCANTRON ANSWER QUESTIONS 29 & 30 IN THE SPACE PROVIDED ANSWER THE SIMULATION ASSIGNMENT IN YOUR BLUE-BOOK, PUT

In 1992, the Committee of Sponsoring Organizations of the Treadway Commission (COSO) issued a

issued a") Checkpoint Contents Accounting, Audit & Corporate Finance Library Editorial Materials Audit and Attest Internal Control Communications Chapter 1 INTRODUCTION AND OVERVIEW 100 Background 100 Background

Checkpoint Contents Accounting, Audit & Corporate Finance Library Editorial Materials Audit and Attest Internal Control Communications Chapter 1 INTRODUCTION AND OVERVIEW 100 Background 100 Background

Audit Evidence. ISA 500 Issued December International Standard on Auditing

Issued December 2007 International Standard on Auditing Audit Evidence The Malaysian Institute of Certified Public Accountants (Institut Akauntan Awam Bertauliah Malaysia) INTERNATIONAL STANDARD ON AUDITING

Issued December 2007 International Standard on Auditing Audit Evidence The Malaysian Institute of Certified Public Accountants (Institut Akauntan Awam Bertauliah Malaysia) INTERNATIONAL STANDARD ON AUDITING

Accounting 408 Exam 2, Chapters 3, 4, 5, 6, E, F

Accounting 408 Exam 2, Chapters 3, 4, 5, 6, E, F Summer 2017 Name Row Multiple Choice Questions. (2 points each, 100 points total) Read each question carefully and indicate the one best answer to each

Accounting 408 Exam 2, Chapters 3, 4, 5, 6, E, F Summer 2017 Name Row Multiple Choice Questions. (2 points each, 100 points total) Read each question carefully and indicate the one best answer to each

STAFF QUESTIONS AND ANSWERS

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org STAFF QUESTIONS AND ANSWERS AUDITING INTERNAL CONTROL OVER FINANCIAL REPORTING Summary: Staff

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org STAFF QUESTIONS AND ANSWERS AUDITING INTERNAL CONTROL OVER FINANCIAL REPORTING Summary: Staff

Audit Practice Introduced by HKSA (HKSA 300, 315 and 330) 10 July 2008

10 July 2008") Audit Practice Introduced by HKSA (HKSA 300, 315 and 330) 10 July 2008 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2006-08 Nelson 1 Overview HK auditing standards

Audit Practice Introduced by HKSA (HKSA 300, 315 and 330) 10 July 2008 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2006-08 Nelson 1 Overview HK auditing standards

Report on Inspection of K. R. Margetson Ltd. (Headquartered in Vancouver, Canada) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Vancouver, Canada) Issued by the Public Company Accounting

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Vancouver, Canada) Issued by the Public Company Accounting

Background. Required Communications of Other Internal Control Deficiencies

Checkpoint Contents Accounting, Audit & Corporate Finance Library Editorial Materials Audit and Attest Management Letter Comments: Operations and Controls Chapter 1 Communication of Management Comments

Checkpoint Contents Accounting, Audit & Corporate Finance Library Editorial Materials Audit and Attest Management Letter Comments: Operations and Controls Chapter 1 Communication of Management Comments

FREQUENTLY ASKED QUESTIONS ABOUT INTERNAL CONTROL OVER FINANCIAL REPORTING

FREQUENTLY ASKED QUESTIONS ABOUT INTERNAL CONTROL OVER FINANCIAL REPORTING Nature and Timing of the Reporting Requirement When must registrants begin to report on internal control over financial reporting?

FREQUENTLY ASKED QUESTIONS ABOUT INTERNAL CONTROL OVER FINANCIAL REPORTING Nature and Timing of the Reporting Requirement When must registrants begin to report on internal control over financial reporting?

Mapping of Original ISA 315 to New ISA 315 s Standards and Application Material (AM) Agenda Item 2-C

Agenda Item 2-C") Mapping of to 315 s and Application Material (AM) Agenda Item 2-C AM 1. The purpose of this International Standard on Auditing (ISA) is to establish standards and to provide guidance on obtaining an understanding

Mapping of to 315 s and Application Material (AM) Agenda Item 2-C AM 1. The purpose of this International Standard on Auditing (ISA) is to establish standards and to provide guidance on obtaining an understanding

Report on Inspection of Deloitte & Associes (Headquartered in Neuilly-sur-Seine, French Republic) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Neuilly-sur-Seine, French Republic) Issued by the Public Company

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Neuilly-sur-Seine, French Republic) Issued by the Public Company

Report on Inspection of Deloitte, S.L. (Headquartered in Madrid, Kingdom of Spain) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Madrid, Kingdom of Spain) Issued by the Public Company Accounting

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Madrid, Kingdom of Spain) Issued by the Public Company Accounting

Analytical Procedures

SINGAPORE STANDARD ON AUDITING SSA 520 Analytical Procedures Conforming Amendments SSA 315 (Redrafted), Identifying and Assessing the Risks of Material Misstatement Through Understanding the Entity and

SINGAPORE STANDARD ON AUDITING SSA 520 Analytical Procedures Conforming Amendments SSA 315 (Redrafted), Identifying and Assessing the Risks of Material Misstatement Through Understanding the Entity and

Audit Workshop Part 2 12 December 2009

Audit Workshop Part 2 12 December 2009 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2006-09 Nelson Consulting Limited 1 Agenda for Part 1 and Part 2 Planning Risk

Audit Workshop Part 2 12 December 2009 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2006-09 Nelson Consulting Limited 1 Agenda for Part 1 and Part 2 Planning Risk

Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity and Its Environment

ISA 315 (Revised) Issued September 2012; updated February 2018 International Standard on Auditing Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity and Its Environment

ISA 315 (Revised) Issued September 2012; updated February 2018 International Standard on Auditing Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity and Its Environment

1. Corporate management (including the CEO) must certify monthly and annually their organization s internal controls over financial reporting.

must certify monthly and annually their organization s internal controls over financial reporting.") Chapter 1 Auditing and Internal Control TRUE/FALSE 1. Corporate management (including the CEO) must certify monthly and annually their organization s internal controls over financial reporting. F 2. Both

Chapter 1 Auditing and Internal Control TRUE/FALSE 1. Corporate management (including the CEO) must certify monthly and annually their organization s internal controls over financial reporting. F 2. Both

(Effective for audits of financial statements for periods ending on or after December 15, 2013) CONTENTS

CONTENTS") INTERNATIONAL STANDARD ON AUDITING 315 (REVISED) IDENTIFYING AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT THROUGH UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT Introduction (Effective for audits of

INTERNATIONAL STANDARD ON AUDITING 315 (REVISED) IDENTIFYING AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT THROUGH UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT Introduction (Effective for audits of

Report on Inspection of Ernst & Young Accountants LLP (Headquartered in Rotterdam, Kingdom of The Netherlands)

") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2013 (Headquartered in Rotterdam, Kingdom of The Netherlands) Issued by the Public

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2013 (Headquartered in Rotterdam, Kingdom of The Netherlands) Issued by the Public

McGraw-Hill/Irwin. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 04 Management Fraud and Audit Risk Learning Objectives 1. Define business risk and understand how management

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 04 Management Fraud and Audit Risk Learning Objectives 1. Define business risk and understand how management

[RELEASE NOS ; ; FR-77; File No. S ]

![[RELEASE NOS ; ; FR-77; File No. S ]](/thumbs/75/72094692.jpg "[RELEASE NOS ; ; FR-77; File No. S ]") SECURITIES AND EXCHANGE COMMISSION 17 CFR PART 241 [RELEASE NOS. 33-8810; 34-55929; FR-77; File No. S7-24-06] Commission Guidance Regarding Management s Report on Internal Control Over Financial Reporting

SECURITIES AND EXCHANGE COMMISSION 17 CFR PART 241 [RELEASE NOS. 33-8810; 34-55929; FR-77; File No. S7-24-06] Commission Guidance Regarding Management s Report on Internal Control Over Financial Reporting

Due: Tuesday, May 1, 2007 by 5:45 p.m.

A439: Advance Auditing 2007 Final exam Directions: The final exam consists of 30 multiple choice questions. Ground Rules. As a take-home exam you may use notes, the internet, auditing textbooks or other

A439: Advance Auditing 2007 Final exam Directions: The final exam consists of 30 multiple choice questions. Ground Rules. As a take-home exam you may use notes, the internet, auditing textbooks or other

Report on Inspection of Ernst & Young Accountants LLP (Headquartered in Rotterdam, Kingdom of the Netherlands)

") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Rotterdam, Kingdom of the Netherlands) Issued by the Public

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Rotterdam, Kingdom of the Netherlands) Issued by the Public

Navigating the PCAOB s and SEC s internal control expectations A discussion. June 2015

Navigating the PCAOB s and SEC s internal control expectations A discussion June 2015 Setting the scene ICFR guidance: PCAOB Auditing Standard No. 5 (May 2007) PCAOB staff views: An Audit of Internal Control

Navigating the PCAOB s and SEC s internal control expectations A discussion June 2015 Setting the scene ICFR guidance: PCAOB Auditing Standard No. 5 (May 2007) PCAOB staff views: An Audit of Internal Control

PCAOB Auditing Standard 15 addresses audit evidence. What is audit evidence?

PCAOB Auditing Standard 15 addresses audit evidence. What is audit evidence? Audit evidence is all the information, whether obtained from audit procedures or other sources, that is used by the auditor

PCAOB Auditing Standard 15 addresses audit evidence. What is audit evidence? Audit evidence is all the information, whether obtained from audit procedures or other sources, that is used by the auditor

ACC 269 Auditing and Assurance Services

ACC 269 Auditing and Assurance Services COURSE DESCRIPTION: Prerequisites: ACC 220 Corequisites: None This course introduces selected topics pertaining to the objectives, theory, and practices in engagements

ACC 269 Auditing and Assurance Services COURSE DESCRIPTION: Prerequisites: ACC 220 Corequisites: None This course introduces selected topics pertaining to the objectives, theory, and practices in engagements

SRI LANKA AUDITING STANDARD 315 (REVISED)

") SRI LANKA AUDITING STANDARD 315 (REVISED) IDENTIFYING AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT THROUGH UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT (Effective for audits of financial statements

SRI LANKA AUDITING STANDARD 315 (REVISED) IDENTIFYING AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT THROUGH UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT (Effective for audits of financial statements

1. Auditors may be independent in fact but not independent in appearance. 3. Attestation standards provide guidance for a wide variety of engagements

Chapter 02 Professional Standards True / False Questions 1. Auditors may be independent in fact but not independent in appearance. True False 2. Auditing Standards issued by the PCAOB are the sole source

Chapter 02 Professional Standards True / False Questions 1. Auditors may be independent in fact but not independent in appearance. True False 2. Auditing Standards issued by the PCAOB are the sole source

The Blue Sage Group. Sarbanes-Oxley. 404 Compliance Program. The Blue Sage Group

The Blue Sage Group Sarbanes-Oxley 404 Compliance Program The Blue Sage Group Agenda The Blue Sage Group 404 Compliance Challenges Meeting the 404 Challenges TBSG 404 Compliance Program Assessment and

The Blue Sage Group Sarbanes-Oxley 404 Compliance Program The Blue Sage Group Agenda The Blue Sage Group 404 Compliance Challenges Meeting the 404 Challenges TBSG 404 Compliance Program Assessment and

Audit Practice Introduced by HKSA (HKSA 315 and 330) 1 February 2008

1 February 2008") Audit Practice Introduced by HKSA (HKSA 315 and 330) 1 February 2008 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2006-08 Nelson 1 Overview HK auditing standards

Audit Practice Introduced by HKSA (HKSA 315 and 330) 1 February 2008 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2006-08 Nelson 1 Overview HK auditing standards

International Standard on Auditing (Ireland) 315

315") International Standard on Auditing (Ireland) 315 Identifying and Assessing the Risks of Material Misstatement Through Understanding the Entity and its Environment MISSION To contribute to Ireland having

International Standard on Auditing (Ireland) 315 Identifying and Assessing the Risks of Material Misstatement Through Understanding the Entity and its Environment MISSION To contribute to Ireland having

Audit Quality Assurance workshop Audit Planning by: CPA Steve Obock Associate Director- KPMG Kenya March 2017

Audit Quality Assurance workshop Audit Planning by: CPA Steve Obock Associate Director- KPMG Kenya March 2017 Uphold public interest Agenda Introduction Developing an audit strategy Setting audit materiality

Audit Quality Assurance workshop Audit Planning by: CPA Steve Obock Associate Director- KPMG Kenya March 2017 Uphold public interest Agenda Introduction Developing an audit strategy Setting audit materiality

CHAPTER 9 TESTS OF CONTROLS

CHAPTER 9 TESTS OF CONTROLS 1 TESTS OF CONTROLS Provide auditor with evidence to support their assessment of control risk. When control risk assessed at less than high, necessary to gather evidence that

CHAPTER 9 TESTS OF CONTROLS 1 TESTS OF CONTROLS Provide auditor with evidence to support their assessment of control risk. When control risk assessed at less than high, necessary to gather evidence that

International Standard on Auditing (Ireland) 402 Audit Considerations Relating to an Entity using a Service Organisation

402 Audit Considerations Relating to an Entity using a Service Organisation") International Standard on Auditing (Ireland) 402 Audit Considerations Relating to an Entity using a Service Organisation MISSION To contribute to Ireland having a strong regulatory environment in which

International Standard on Auditing (Ireland) 402 Audit Considerations Relating to an Entity using a Service Organisation MISSION To contribute to Ireland having a strong regulatory environment in which

Audit & Assurance Update January 16, In This Issue. Background. Background. Key Provisions of the Estimates Standard

Audit & Assurance Update January 16, 2019 In This Issue Background Key Provisions of the Specialist Amendments Key Provisions of the Estimates Standard Applicability and Effective Date Comparison with

Audit & Assurance Update January 16, 2019 In This Issue Background Key Provisions of the Specialist Amendments Key Provisions of the Estimates Standard Applicability and Effective Date Comparison with

3/29/15. Module 3: Audit objectives, evidence, procedures, and documentation

Assignment reminder: Assignment #1 (see Module 5) is due at the end of Week 5 (see Course Schedule). You may wish to take a look at it now in order to familiarize yourself with the requirements and to

Assignment reminder: Assignment #1 (see Module 5) is due at the end of Week 5 (see Course Schedule). You may wish to take a look at it now in order to familiarize yourself with the requirements and to

Internal Financial Control (IFC)& Internal Financial Controls over Financial Reporting (IFCoFR)

& Internal Financial Controls over Financial Reporting (IFCoFR)") Internal Financial Control (IFC)& Internal Financial Controls over Financial Reporting (IFCoFR) Origin of IFC The first significant focus on internal control certification related to financial reporting

Internal Financial Control (IFC)& Internal Financial Controls over Financial Reporting (IFCoFR) Origin of IFC The first significant focus on internal control certification related to financial reporting

Audit evidence. chapter. Chapter learning objectives. When you have completed this chapter you will be able to:

chapter 9 Audit evidence Chapter learning objectives When you have completed this chapter you will be able to: explain the assertions contained in the financial statements explain the use of assertions

chapter 9 Audit evidence Chapter learning objectives When you have completed this chapter you will be able to: explain the assertions contained in the financial statements explain the use of assertions

Chapter 16. Auditing Operations and Completing the Audit. McGraw-Hill/Irwin. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 16 Auditing Operations and Completing the Audit McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Auditing Operations Corporate earnings are considered as

Chapter 16 Auditing Operations and Completing the Audit McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Auditing Operations Corporate earnings are considered as

Internal Controls and Sampling Tests

Question 1: What important concepts should management consider in the design and implementation of internal controls? The two concepts that are important for management to consider in the design and implementation

Question 1: What important concepts should management consider in the design and implementation of internal controls? The two concepts that are important for management to consider in the design and implementation

1. A series of business and related auditing failures led to the passage of the Sarbanes-Oxley Act (2002).

.") Chapter 02 The Financial Statement Auditing Environment True / False Questions 1. A series of business and related auditing failures led to the passage of the Sarbanes-Oxley Act (2002). True False 2. The

Chapter 02 The Financial Statement Auditing Environment True / False Questions 1. A series of business and related auditing failures led to the passage of the Sarbanes-Oxley Act (2002). True False 2. The

CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a AUDITING THEORY AUDIT PLANNING

CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a Related PSAs: PSA 300, 310, 320, 520 and 570 Appointment of the Independent Auditor AUDITING THEORY AUDIT PLANNING Page 1 of 9 Early appointment of the

CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a Related PSAs: PSA 300, 310, 320, 520 and 570 Appointment of the Independent Auditor AUDITING THEORY AUDIT PLANNING Page 1 of 9 Early appointment of the

PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD ) ) In the Matter of ) PCAOB Release No.104-2013-087

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD ) ) In the Matter of ) PCAOB Release No.104-2013-087

Implementation Tool for Auditors

Implementation Tool for Auditors CANADIAN AUDITING STANDARDS (CAS) DECEMBER 2017 STANDARD DISCUSSED CAS 315, Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity

Implementation Tool for Auditors CANADIAN AUDITING STANDARDS (CAS) DECEMBER 2017 STANDARD DISCUSSED CAS 315, Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity

Report on Inspection of KPMG Audit Limited (Headquartered in Hamilton, Bermuda) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Hamilton, Bermuda) Issued by the Public Company Accounting

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2015 (Headquartered in Hamilton, Bermuda) Issued by the Public Company Accounting

WATCH WORDS FROM THE PEER REVIEW PROCESS

WATCH WORDS FROM THE PEER REVIEW PROCESS Peer Review 3 NOT DOCUMENTED = NOT PERFORMED Vendor-obtained practice aids, checklists and forms are NOT audit evidence Sources of audit evidence Books, records,

WATCH WORDS FROM THE PEER REVIEW PROCESS Peer Review 3 NOT DOCUMENTED = NOT PERFORMED Vendor-obtained practice aids, checklists and forms are NOT audit evidence Sources of audit evidence Books, records,

Corporate Governance Update. SOX 404 and Internal Controls

Corporate Governance Update SOX 404 and Internal Controls Speakers Barbara Borden bborden@cooley.com 858.550.6243 Brad Peck bpeck@cooley.com 858.550.6012 Steven Spector (858) 453-7200 x229 sspector@arenapharm.com

Corporate Governance Update SOX 404 and Internal Controls Speakers Barbara Borden bborden@cooley.com 858.550.6243 Brad Peck bpeck@cooley.com 858.550.6012 Steven Spector (858) 453-7200 x229 sspector@arenapharm.com

How well you are prepared to deal with IFC

September 9, 2016 How well you are prepared to deal with IFC Price Waterhouse & Co Amit Agrawal & Madhavi D K Internal Financial Controls over Financial Reporting (IFCFR) Particulars Background Overview

September 9, 2016 How well you are prepared to deal with IFC Price Waterhouse & Co Amit Agrawal & Madhavi D K Internal Financial Controls over Financial Reporting (IFCFR) Particulars Background Overview

International Standard on Auditing (UK) 315 (Revised June 2016)

315 (Revised June 2016)") Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 315 (Revised June 2016) Identifying and Assessing the Risks of Material Misstatement Through Understanding

Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 315 (Revised June 2016) Identifying and Assessing the Risks of Material Misstatement Through Understanding

SA 402(REVISED) AUDIT CONSIDERATIONS RELATING TO AN ENTITY USING

AUDIT CONSIDERATIONS RELATING TO AN ENTITY USING") Part I : Engagement and Quality Control Standards I.271 SA 402(REVISED) AUDIT CONSIDERATIONS RELATING TO AN ENTITY USING A SERVICE ORGANISATION (EFFECTIVE FOR ALL AUDITS RELATING TO ACCOUNTING PERIODS

Part I : Engagement and Quality Control Standards I.271 SA 402(REVISED) AUDIT CONSIDERATIONS RELATING TO AN ENTITY USING A SERVICE ORGANISATION (EFFECTIVE FOR ALL AUDITS RELATING TO ACCOUNTING PERIODS