8/4/2016. Sponsored by: The Chief Inspector General and the Florida Chapter of the Association of Inspectors General. Florida Inspectors General

|

|

|

- Camron Caldwell

- 5 years ago

- Views:

Transcription

1 Sponsored by: The and the Florida Chapter of the Association of Inspectors General General Topics Covered in this Block of Instruction: What is a conflict of interest? What is an impairment to objectivity or independence? What disclosures are pertinent to IG Offices? What controls are pertinent to IG offices? What can be done to avoid the perception of a conflict of interest? What may happen if you disregard a conflict of interest? 1

2 Do not take this job. 2

3 3

4 4

5 Feared, Desired, and Respected 5

6 Conflicts of Interest and Impairments 6

7 We encounter opportunities for COIs to exist frequently Sometimes the COI pertains to our relationship or involvement with: The subject (party) of the audit or investigation The entity making the complaint Other parties involved in the complaint, condition, or subject s sphere of influence Past decisions affecting the complainant, subject, or subject matter Other COIs may exist for the audit or investigated parties as well, which may affect findings. How Will I recognize a Conflict of Interest? A situation in which an auditor or investigator, who is in a position of trust, has a: competing professional interest or, competing personal interest. Information or evidence of prejudice of an individual s ability to perform his or her duties and responsibilities objectively. Relationships and activities that suggest: revolving door insider dealing moral hazard perverse incentive self-evaluation Personal Impairments include, but are not limited to: Official, professional, personal, or financial relationships that might appear to lead the OIG to limit the extent of the work, to limit disclosure, or to alter the outcome of the work. Preconceived ideas toward activities, individuals, groups, organizations, objectives, or particular programs that could bias the outcome of the work. Previous involvement, especially recent involvement, in a decisionmaking or management capacity that could affect the work. Biases that may affect the objectivity of the OIG staff member in the performance of their work. Any audit or review by an individual who had previously performed work subject to review. 7

8 Interference or undue influence in the selection, appointment, and employment of OIG staff. Restrictions on funds or other resources dedicated to the OIG, such as timely, independent legal counsel, that could prevent the OIG from performing essential work. Interference or undue influence in the OIGs selection of what is to be examined, determination of scope and timing of work or approach to be used, the appropriate content of any resulting report, or resolution of audit findings. Influences that jeopardize continued employment of the inspector general or individual OIG staff for reasons other than competency or the need for OIG services. Interference with OIG access to documents or individuals necessary to perform OIG work. Improper political pressures that affect the selection of areas for review, the performance of those reviews, and the objective reporting of conclusions without fear of censure. Personal Impairments Conflicts of Interest And Impairments Official, professional, personal or financial relationships that might cause someone to limit the extent of the work, to limit disclosure or to alter the outcome of the work; Preconceived ideas toward activities, individuals, groups, organizations, investigative objectives or particular programs that could bias the outcome of the work; Previous involvement, especially recent involvement, in a decisionmaking or management capacity that could affect the work; Previous performance of work activities subject to audit or investigation. 8

9 External Impairments Interference or undue influence in the selection, appointment, and employment of Investigations Section members; Restrictions on funds or other resources dedicated to the investigative function; Influences that jeopardize continued employment of the Inspector General for reasons other than competency or the need for the office s services Interference with access to documents or individuals necessary to perform investigative work; Improper political pressures that affect the investigative plan, the performance of investigative activities, and the objective reporting of conclusions without fear of censure. Organizational Impairments An organization's independence can be affected by its place within the structure of the government entity of which it is a part. For example, for Governor s agencies, agency Inspectors General report to the Chief Inspector General, to achieve maximum independence. An organization s independence can also be affected by : Self-review Social Pressure Economic Interest Personal Relationship Familiarity Cognitive Biases Prevention of Conflicts of Interest and Impairments to Objectivity Professional Standards Penalties and Fines Reputational Harm Adverse Employment Action 9

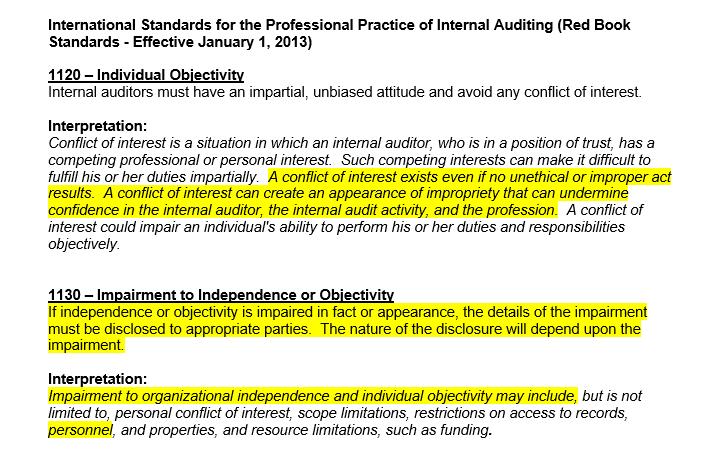

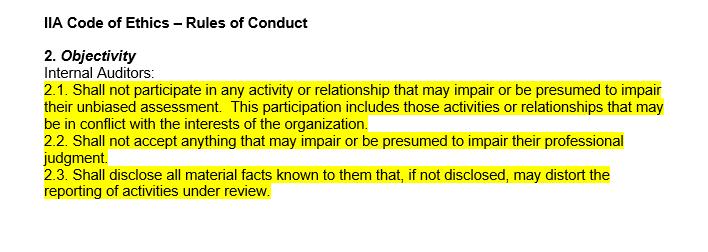

10 Professional Standards 10

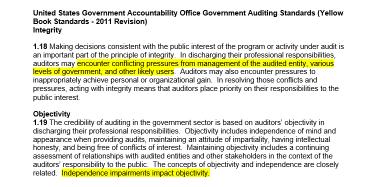

11 United States Government Accountability Office Government Auditing Standards (Yellow Book Standards Revision) Continued: 11

112.")

12 Penalties and Fines Dual public employment Employment of relatives Voting conflicts (conflict of interest in voting) Full and public disclosure of financial interests , , and Gifts law , Honoraria law Lobbying activities Reputational Harm Adverse Employment Action 12

13 Safeguards Safeguards are controls designed to eliminate, or reduce to an acceptable, level conflicts of interest, threats to independence, and threats to objectivity. What Controls or Policies Can be Implemented to Avoid Actual or Perceived Conflicts of Interest of Impairments to Objectivity? Controls or Policies Developed that require: The audit or investigative activity be independent, and members be objective in performing their work. The audit or investigative internal activity be free from interference in determining the scope of internal auditing, performing work, and communicating results Audit or investigative personnel are expected to have an impartial, unbiased attitude and avoid conflicts of interest What Other Controls or Policies can be implemented to Avoid Actual or Perceived Organizational Conflicts of Interest of or Organizational Impairments to Independence? Controls or Policies Developed that require or allow: Oversight of hiring practices Segregation of Duties ( Firewall between participants) Changes in reporting relationships Training Close supervision Rotation/Reassignment Outsourcing Disclosure Recusal Removal Discipline 13

14 Disclosures 14

15 In Case You Missed It: 15

16 What Other Controls or Policies Can be Implemented to Avoid Actual or Perceived Conflicts of Interest of Impairments to Objectivity? Use of Teams (dilutes singular influence) Peer Review Allowing Elapsed Time/Changed Circumstances Internal Consultations 16

; Terminating contracts;")

17 Additional Concerns Does Your IG Shop Do Any of These things? Evaluate contract proposals; Award Government contracts (for audit tracking tools, surveillance equipment, transcription services, ); Administering contracts (including ordering changes or giving technical direction in contract performance or contract quantities, evaluating contractor performance, and accepting or rejecting contractor products or services); Terminating contracts; Determining whether contract costs are reasonable, allocable, and allowable. 17

18 Penalties Dismissal Invalidation of Work Contested Findings Contested Conclusions Fines and Sanctions Forfeiture of Retirement Benefits (Felony Conviction) Contact Information: Eric W. Miller Agency for Health Care Administration Office of Inspector General 2727 Mahan Drive Tallahassee, FL