Good Governance and Anti-Corruption: The Role of Supreme Audit Institutions (SAIs)

|

|

|

- Preston Russell

- 5 years ago

- Views:

Transcription

1 Good Governance and Anti-Corruption: The Role of Supreme Audit Institutions (SAIs) Phillip Herr, Ph.D. Managing Director, Physical Infrastructure Issues U.S. Government Accountability Office

2 The Vision for Supreme Audit Institutions (SAIs) The International Organization of Supreme Audit Institutions (INTOSAI) has led efforts to enhance SAI performance. Supporting strong public financial management Strengthening good governance and accountability Supporting more efficient and effective programs Tackling corruption SAIs must lead by example Promoting transparency Enhancing accountability Providing checks and balances in government operations Page 2

3 External Factors that Affect SAI Performance Public financial management Budget formulation and execution Accounting and reporting Relationships between the executive, legislative, and judiciary Nature and role of political parties Media and civil society groups International partners Formal and informal state accountability Page 3

4 Core SAI Functions Independence and legal framework critical success factors Core Work Strategic/tactical planning and ongoing dialog re: priorities Audit types Financial Compliance Performance Judgment process (where applicable) Example: GAO has a bid protest resolution function and issues legal opinions. Page 4

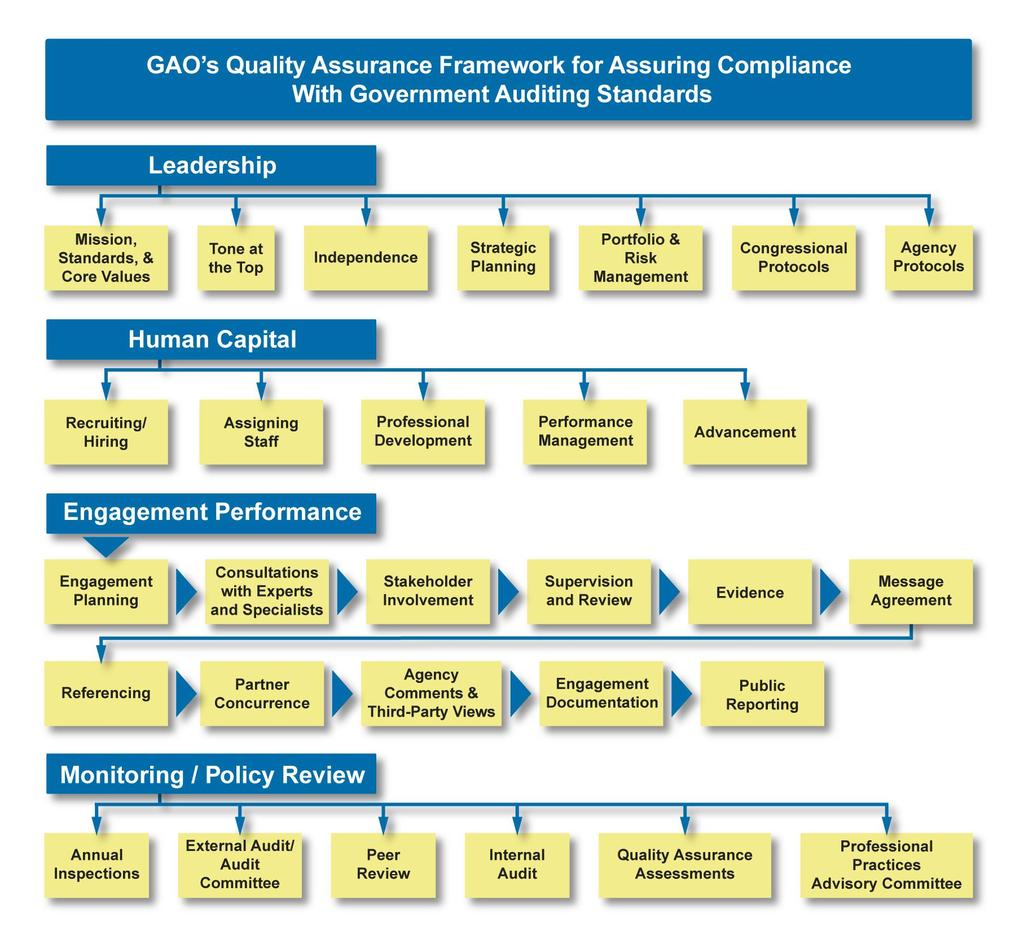

5 Background/History of GAO The early years Founded in 1921, based on the principles of financial auditing After WWII, shift from voucher audits to oversight of financial systems Government accounting principles created 1970s-1980s Interest in program outcomes, increased transparency Performance audits introduced Significant change in the audit workforce 2004: Name changed to Government Accountability Office New focus: oversight, insight, and foresight activities GAO s quality assurance framework Page 5

6 Page 6

7 Keys to SAI Success Human resource management Leadership Professional development/training Example: GAO requires 80 hours of professional development training every 2 years. Stakeholder engagement Example: GAO has protocols for executive agencies, Congress, and international organizations. Communication with civil society, citizens, and media FraudNet reporting capability Management structure and internal controls Page 7

8 SAI Oversight Functions Oversight activities determine whether government entities are: Carrying out their assigned tasks Spending funds for intended purposes Complying with laws and regulations Oversight is a key component of identifying Waste Fraud Abuse Multiple levels of government provide this oversight in addition to GAO Federal Inspector General offices, state/local auditors Page 8

9 SAI Insight Activities Insight activities involve: Determining which programs and policies work and which don t Sharing best practices and benchmarking information Horizontally across government Vertically through different levels of government Insight work requires: Different staff technical backgrounds Research design and methodological expertise High quality data Page 9

10 SAI Foresight Activities Foresight activities: identifying key trends and emerging challenges before they reach crisis proportions Serving an aging population Health and income support payments Long-range fiscal challenges Infrastructure funding Changing security threats like cyber attacks Information age demands Auditing in the Twitter era Complexities of globalization Trade, climate change Evolving governance structures Public/private partnerships Page 10

11 GAO Identifies High Risk Areas GAO s High Risk report has: Directed congressional attention to key problems 32 areas identified in the 2015 report Surface transportation funding Federal property/security Reforming the U.S. Postal Service Resulted in over $17 billion annually in financial benefits Resulted in many additional non-financial improvement actions Provided impetus for government-wide management reforms Increased the priority placed on these areas President s Management Agenda Office of Management and Budget s corrective action initiative Page 11

12 Reporting Results SAI reporting GAO issues about 1,000 reports and testimonies annually Social media is used to disseminate information GAO s annual performance measured against objectives Dollar cost savings Recommendations implemented Resources expended Employee-related indicators Value and benefits Improved accountability, transparency, and integrity Demonstrate ongoing relevance Page 12

13 GAO s 2015 Performance Indicators 2015 Annual Performance and Accountability Report $74.7 billion in financial benefits 79 percent of recommendations made were implemented within 4 years 109 Congressional testimonies Two-thirds of GAO products contained recommendations 90+ percent of GAO s workload comes from Congressional requests and mandates in law 90 percent of the workload is performance audits Page 13

14 GAO s Standard Setting Role The Yellow Book Framework for conducting high quality audits with competence, integrity, objectivity, and independence (2011 update) The Green Book Internal control helps an entity run its operations efficiently and effectively, report reliable information about its operations, and comply with applicable laws and regulations (2014 update) Cost Estimating and Assessment Guide Best practices to develop, manage, and evaluate capital program cost estimates during an acquisition program (2009) GAO Schedule Assessment Guide Best practices for project schedules (2015) Page 14

15 GAO s Center for Audit Excellence Legislation passed in December 2014 gave GAO authority to establish the Center Mission is to promote good governance and build the institutional capacity of domestic and international accountability organizations by providing affordable, high quality training, technical assistance, and related products and services. Center will provide customized fee-based training and technical assistance to meet the needs of domestic and foreign accountability organizations in four core areas: Performance audits Financial audits Institutional capacity building Leadership/supervision Center can also provide training and technical assistance on specialized topics such as internal controls, procurement, and audit methodologies. Center opened in October 2015 Page 15

16 GAO s Fraud Risk Management Framework Developed by GAO s Forensic Audit and Investigative Services team Encompasses control activities to prevent, detect, and respond to fraud, with an emphasis on prevention Recognizes environmental factors that influence or help managers achieve their objective to mitigate fraud risks Highlights the importance of monitoring and incorporating feedback Page 16

17 GAO s Fraud Framework Components Commit: Commit to combating fraud by creating an organizational culture and structure conducive to fraud risk management Demonstrate a senior-level commitment to combating fraud Involve all levels of the program in setting an antifraud tone Designate an entity to design and oversee fraud risk management activities Page 17

Assess: Plan regular fraud risk assessments and assess risks to determine a fraud risk profile Tailor the assessment to the program and involve relevant stakeholders Assess the likelihood and")

18 GAO s Fraud Framework Components (cont.) Assess: Plan regular fraud risk assessments and assess risks to determine a fraud risk profile Tailor the assessment to the program and involve relevant stakeholders Assess the likelihood and impact of fraud risks, determine risk tolerance, and examine existing controls Document the program s fraud risk profile, including risk tolerance, prioritization of risks, and other key findings and conclusions Page 18

Design and Implement: Design and implement a strategy with specific control activities to mitigate assessed fraud risks and collaborate to help ensure effective implementation Develop, document,")

19 GAO s Fraud Framework Components (cont.) Design and Implement: Design and implement a strategy with specific control activities to mitigate assessed fraud risks and collaborate to help ensure effective implementation Develop, document, and communicate an antifraud strategy Consider the benefits and costs of controls to prevent and detect potential fraud, and develop a fraud response plan Establish collaborative relationships (such as working groups) and create incentives Page 19

Evaluate and Adapt: Evaluate outcomes using a riskbased approach and adapt activities to improve fraud risk management Conduct risk-based monitoring on an ongoing basis and conduct evaluations")

20 GAO s Fraud Framework Components (cont.) Evaluate and Adapt: Evaluate outcomes using a riskbased approach and adapt activities to improve fraud risk management Conduct risk-based monitoring on an ongoing basis and conduct evaluations periodically Collect and analyze data on instances of detected fraud to monitor fraud trends Use results of monitoring, evaluation, and investigations to improve prevention, detection, and response Page 20

21 Who can use GAO s Fraud Framework? Auditors can use the Framework to help assess managers fraud risk efforts Managers of state, local, nonprofit and foreign government agencies may find the concepts and practices useful Supreme audit institutions can use it to develop country-specific fraud risk management guidance incorporate the practices and concepts into efforts to assess fraud risk management Page 21

22 Further Information To access GAO reports and guidance documents My contact information Phillip Herr, Ph.D. Managing Director, Physical Infrastructure Issues (202) Page 22