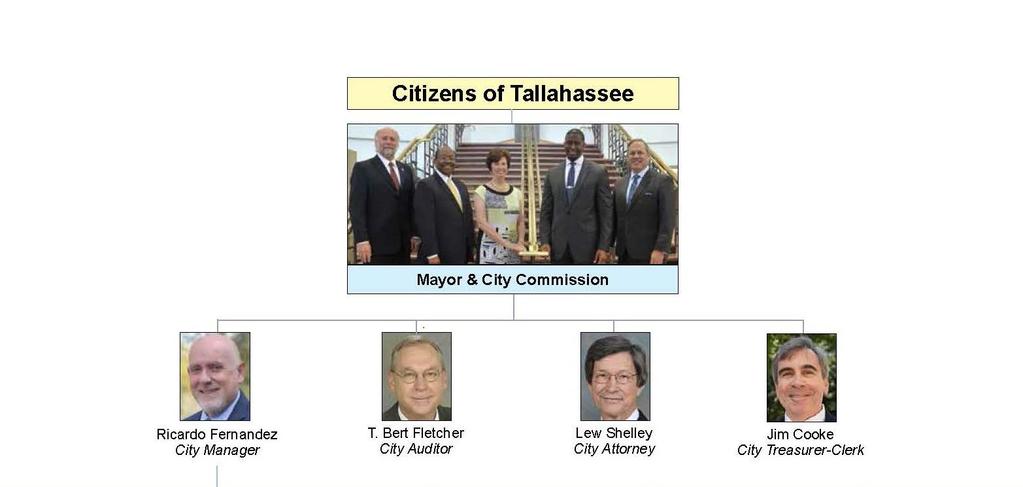

Internal Audit How the Internal Audit Function Facilitates Internal Controls. Office of the City Auditor City of Tallahassee

|

|

|

- Victor Brooks

- 6 years ago

- Views:

Transcription

1 Internal Audit How the Internal Audit Function Facilitates Internal Controls Office of the City Auditor City of Tallahassee 1

2 Internal Audits and Internal Controls Session Purpose: How does an internal audit function assist management in ensuring an entity has established an adequate internal control framework as provided for by COSO and the GAO Green Book (Standards for Internal Control in the Federal Government ) 2

3 COSO Committee of Sponsoring Organizations of the Treadway Commission (COSO): Comprised of five agencies: American Accounting association AICPA Institute of Internal Auditors Institute of Management Accountants Financial Executives International 3

4 GAO GREEN BOOK Standards for Internal Control in the Federal Government Issued by the Government Accountability Office (GAO) Last updated in September 2014 Green Book adapts COSO principles for a government environment 4

5 COSO Definition of Internal Controls A process effected by an entity that provides reasonable assurance that the entity s objectives will be achieved. Objectives include: Effective and Efficient Operations Reliability of reporting Compliance with applicable laws, regulations, and policies 5

6 Green Book Definition of Internal Controls A process effected by an entity s oversight body, management, and other personnel that provides reasonable assurance that the objectives of an entity will be achieved. These objectives and related risks can be broadly classified into one or more of the following three categories: Operations (effectiveness and efficiency) Reporting (reliability) Compliance (with applicable laws and regulations) 6

7 COSO and Green Book Internal Control Components Control Environment Risk Assessment Control Activities Information and Communication Monitoring Activities 7

8 COSO and Green Book Internal Control Components 8

9 COSO: Internal Audit Internal auditors play an important role in evaluating the effectiveness of control systems. As an independent function reporting to top management, internal audit is able to assess the internal controls systems implemented by the organization and contribute to ongoing effectiveness. As such, internal audit often plays a significant monitoring role. 9

10 Green Book: Internal Audit Section of the Green Book provides that internal audits play an important role in Monitoring Activities by performing independent, objective evaluations of control design and testing of internal controls. Internal audits provide greater objectivity as they are performed by reviewers that do not have responsibility for the activities being evaluated. 10

11 11

12 City Auditor s Office Follow both GAGAS and IIA Standards All Audits are Performance Audits Complete average 20 audits annually Undergo an external peer review every three years 12

13 OFFICE OF THE CITY AUDITOR Organization Chart July 14, 2015 CITY AUDITOR T. Bert Fletcher ADMINISTRATIVE SPECIALIST II Michelle Davis SENIOR AUDIT MANAGER Don Hancock SENIOR IT AUDITOR Patrick Cowen AUDIT MANAGER Dennis Sutton SENIOR AUDITOR Cameisha Smith SENIOR AUDITOR Vanessa Spaulding 13

14 14

15 What we Audit Any City department, activity, or function (except the Mayor and City Commission Offices) Any entity that receives City funds as a grant, loan, or contract recipient Joint City/County entities Blueprint (Capital Infrastructure) CRA (Redevelopment) Consolidated Dispatch Agency (City/County/Sheriff) 15

16 Annual Audit Plan Required by City charter Over 250 auditable topics and areas List updated each year Conduct an annual risk analysis All topics/areas are ranked 16

17 Risk Factors 1. Size of Operation/Fiscal Impact 2. Experience of Management 3. Complexity of Operations/Activity 4. Public Sensitivity 5. Threats to Public Health, Safety and Welfare 6. Susceptibility to Fraud, Waste, & Abuse 17

18 Other Sources for Planned Audit 1. Audit Shop awareness 2. Solicited Input from: Mayor and Commissioners City Leadership City Advisory Boards Independent Ethics Board Neighborhood Associations 18

19 Citywide Cash Controls One main revenue office but 26 other City locations where revenues and receipts are collected Based Audit Program on City Internal Control Policy, which in turn was based on COSO Access to and Accountability for Resources Direct Activity management Segregation of Duties Physical Controls Execution of Transactions and Events Recording of Transactions and Events Information Processing Documentation 19

20 Citywide Cash Controls (Continued) 1. Collections stored in unlocked cabinets and drawers (or purses and books!) 2. Permits and receipts not controlled or accounted for 3. Management not reviewing collection reports 4. Duties not adequately segregated 5. Checks not endorsed for days 6. Collections not timely deposited 7. Lack of electronic transfers 8. No documented transfers of custody 20

New comprehensive audit conducted based on citizen concerns Audit identified scheme - estimated $80,000 adoption fees diverted Former employee convicted Enhanced controls")

21 Audit of the Animal Services Center Inadequate segregation of duties in regard to adoption fees First identified in Citywide Cash Controls Audit (no changes made other than allegedly increased managerial reviews) New comprehensive audit conducted based on citizen concerns Audit identified scheme - estimated $80,000 adoption fees diverted Former employee convicted Enhanced controls subsequently implemented 21

22 Audit of Electric and Gas Revenues GAS ELECTRIC Complex Meters with Billing System multipliers Over $1 million in unbilled consumption identified Some significant over billed consumption also Very technical lot of reliance on electric staff Focused on accuracy of meters through meter testing Audit procedures identified 2 commercial customers getting free electricity Audit found $1.6 million billing error 22

23 Annual Citywide Disbursements Audit 350,000 transactions totaling over $1 billion Stratification and Categorization Applied Payroll Retirement Energy Acquisitions All Other Multiple criteria applied to each sample item Comprehensive testing 23

24 Annual Citywide Disbursements Audit (Continued) Relied Upon by external auditors Findings: Lack of control over time and attendance records Overpaid an insurance provider $53,000 Competitive procurement practices not followed Duplicate payments identified Extra pay period included in retirement benefit determinations Ineligible former employees and dependents inappropriately allowed to participate in the City s health insurance program Unique improvements: Revision to retirement ordinances Efficiencies for frequently paid vendors Implementation of an automated payroll time and attendance system 24

25 Investments Size: Pension ($1 billion) and Non-Pension ($600 million) Audits addressed: Investment Performance Investment policy in accordance with best practices Investments properly diversified Investments allowable types (e.g., not too risky or overly conservative) Whether internal controls were adequate 25

26 Investments (continued) Findings Earnings allocation errors resulted in over $2 million of City earnings being incorrectly allocated Inadequate and untimely reconciliations of investment and custodian statements Capability for incompatible duties regarding transfer of funds 26

27 Audit of Commercial Insurance Acquisition Excess coverages purchased for property, liability and workers compensation Fees and premiums averaged $3.6 million annually Same broker and companies selected every year even though competitive processes used 27

28 Audit of Commercial Insurance Acquisition Audit recommended alternative competitive procurement process Selected broker not allowed to receive commission from selected providers and carriers to ensure no conflict of interest Actual savings of $434,000 realized in first full year new process used. 28

29 29

Committee for Senior Business Administrators. Segregation of Duties

Committee for Senior Business Administrators Segregation of Duties Presented by: Tammy R. Hoskens and Margaret (Peggy) B. Zapalac University Risk and Compliance May 21, 2009 Segregation of Duties Segregation

Committee for Senior Business Administrators Segregation of Duties Presented by: Tammy R. Hoskens and Margaret (Peggy) B. Zapalac University Risk and Compliance May 21, 2009 Segregation of Duties Segregation

TRA Internal Audit Fiscal Year 2019 Audit Plan

TRA Internal Audit Fiscal Year 2019 Audit Plan Leslie Nagel, CPA, CEBS, CIA Chief Audit Executive Approved by TRA Audit Comittee April 10, 2018 Approved by TRA Board of Trustees April 11, 2018 TRA Internal

TRA Internal Audit Fiscal Year 2019 Audit Plan Leslie Nagel, CPA, CEBS, CIA Chief Audit Executive Approved by TRA Audit Comittee April 10, 2018 Approved by TRA Board of Trustees April 11, 2018 TRA Internal

Final Audit Follow-Up As of May 31, 2015

Final Audit Follow-Up As of May 31, 2015 T. Bert Fletcher, CPA, CGMA City Auditor Audit of Selected Departments Performing Accounts Receivable Functions (Report #1204 issued February 15, 2012) Report #1512

Final Audit Follow-Up As of May 31, 2015 T. Bert Fletcher, CPA, CGMA City Auditor Audit of Selected Departments Performing Accounts Receivable Functions (Report #1204 issued February 15, 2012) Report #1512

Advanced Finance for Governing Board Members. Charter Schools: Advancing the Promise!! 2015 Annual Conference

Advanced Finance for Governing Board Members Charter Schools: Advancing the Promise!! 2015 Annual Conference Governing Body Responsibilities with regard to finance Fiduciary responsibilities outlined in

Advanced Finance for Governing Board Members Charter Schools: Advancing the Promise!! 2015 Annual Conference Governing Body Responsibilities with regard to finance Fiduciary responsibilities outlined in

Audit Follow-Up. Audit of Selected Departments Performing Accounts Receivable Functions (Report #1204 issued February 15, 2012)

") Audit Follow-Up As of December 31, 2013 T. Bert Fletcher, CPA, CGMA City Auditor Audit of Selected Departments Performing Accounts Receivable Functions (Report #1204 issued February 15, 2012) Report #1414

Audit Follow-Up As of December 31, 2013 T. Bert Fletcher, CPA, CGMA City Auditor Audit of Selected Departments Performing Accounts Receivable Functions (Report #1204 issued February 15, 2012) Report #1414

Seminar Internal Control Identification and Filtering

Seminar Internal Control Identification and Filtering 4 March 2011 by Stephen Ho Definition The process designed, implemented and maintained by those charged with governance, management and other personnel

Seminar Internal Control Identification and Filtering 4 March 2011 by Stephen Ho Definition The process designed, implemented and maintained by those charged with governance, management and other personnel

The most commonly applied model for designing and auditing internal

Fair Value Accounting Fraud: New Global Risks and Detection Techniques By Gerard M. Zack Copyright 2009 by Gerard M. Zack Appendix C Internal Controls over Fair Value Accounting Applications The most commonly

Fair Value Accounting Fraud: New Global Risks and Detection Techniques By Gerard M. Zack Copyright 2009 by Gerard M. Zack Appendix C Internal Controls over Fair Value Accounting Applications The most commonly

The Basics of Internal Controls & Segregation of Duties

The Basics of Internal Controls & Segregation of Duties Presented by: Kevin L. Pegish, CPA Senior Audit Manager Northwest Region klpegish@ohioauditor.gov Internal Controls, we will discuss the following:

The Basics of Internal Controls & Segregation of Duties Presented by: Kevin L. Pegish, CPA Senior Audit Manager Northwest Region klpegish@ohioauditor.gov Internal Controls, we will discuss the following:

Audit Follow-Up. As of September 30, Summary

Audit Follow-Up As of September 30, 2016 T. Bert Fletcher, CPA, CGMA City Auditor Audit of Parks, Recreation and Neighborhood Affairs Trousdell Aquatics Center and Gymnastics Center Revenues (Report #1606,

Audit Follow-Up As of September 30, 2016 T. Bert Fletcher, CPA, CGMA City Auditor Audit of Parks, Recreation and Neighborhood Affairs Trousdell Aquatics Center and Gymnastics Center Revenues (Report #1606,

Ten Payment Fraud Protections

Ten Payment Fraud Protections 1. Payee Positive Pay a. Provided by banks b. Banks match check serial numbers and dollar amounts against a company provided list of checks issued and only pays those checks

Ten Payment Fraud Protections 1. Payee Positive Pay a. Provided by banks b. Banks match check serial numbers and dollar amounts against a company provided list of checks issued and only pays those checks

Single Audit Update: Internal Control over Compliance and the GAO s Green Book. MSBO s 80 th Annual Conference April 19, 2018

Single Audit Update: Internal Control over Compliance and the GAO s Green Book MSBO s 80 th Annual Conference April 19, 2018 Presented by: Stephen W. Blann, CPA, CGFM, CGMA Director of Governmental Audit

Single Audit Update: Internal Control over Compliance and the GAO s Green Book MSBO s 80 th Annual Conference April 19, 2018 Presented by: Stephen W. Blann, CPA, CGFM, CGMA Director of Governmental Audit

Internal Control in Higher Education

Internal Control in Higher Education Daniel Adams Office of Audit Services Audit Services Mission To provide assurance and advisory services that are independent, objective and risk-based in order to protect

Internal Control in Higher Education Daniel Adams Office of Audit Services Audit Services Mission To provide assurance and advisory services that are independent, objective and risk-based in order to protect

INTERNAL CONTROLS 101

INTERNAL CONTROLS 101 Presented by: Christopher White, CPA Kristina Hoyng, CPA Northwest Region Overview of Topic Internal Controls - The Basics Components of Internal Controls Benefits of Internal Controls

INTERNAL CONTROLS 101 Presented by: Christopher White, CPA Kristina Hoyng, CPA Northwest Region Overview of Topic Internal Controls - The Basics Components of Internal Controls Benefits of Internal Controls

City Property Damage Claims Processing and Collection

City Property Damage Claims Processing and Collection March 30, 2016 Report 201602 City Auditor: Jed Johnson, CIA, CGAP Major Contributor: Marla Hamilton Staff Auditor Jonna Murphy Staff Auditor Contents

City Property Damage Claims Processing and Collection March 30, 2016 Report 201602 City Auditor: Jed Johnson, CIA, CGAP Major Contributor: Marla Hamilton Staff Auditor Jonna Murphy Staff Auditor Contents

SAN FRANCISCO COURT APPOINTED SPECIAL ADVOCATE PROGRAM

SAN FRANCISCO COURT APPOINTED SPECIAL ADVOCATE PROGRAM FINANCIAL PROCEDURES MANUAL Table of Contents GENERAL ACCOUNTING POLICY AND PROCEDURES... 3 OVERALL ACCOUNTING SYSTEM DESIGN... 3 CONTROL OBJECTIVE...

SAN FRANCISCO COURT APPOINTED SPECIAL ADVOCATE PROGRAM FINANCIAL PROCEDURES MANUAL Table of Contents GENERAL ACCOUNTING POLICY AND PROCEDURES... 3 OVERALL ACCOUNTING SYSTEM DESIGN... 3 CONTROL OBJECTIVE...

2/27/2017. Segregation of Duties/ Internal Controls. Objectives. Agenda

Segregation of Duties/ Internal Controls 2017 WASBO Accounting Conference David Maccoux, Shareholder Objectives Discuss failures of internal controls to detect or prevent fraud and learn how to implement

Segregation of Duties/ Internal Controls 2017 WASBO Accounting Conference David Maccoux, Shareholder Objectives Discuss failures of internal controls to detect or prevent fraud and learn how to implement

Office of the City Manager

Office of the City Manager TO: FROM: Finance/Audit Committee Ruthe Holden, Internal Audit Manager SUBJECT: Final Fraud Risk Assessment Report-Phase 1 Recommendation This report is for information only.

Office of the City Manager TO: FROM: Finance/Audit Committee Ruthe Holden, Internal Audit Manager SUBJECT: Final Fraud Risk Assessment Report-Phase 1 Recommendation This report is for information only.

Scope, Objectives, and Methodology. Report #1208

Audit Follow-Up As of September 30, 2012 Sam M. McCall, Ph.D., CPA, CGFM, CIA, CGAP City Auditor Treasurer-Clerk s Revenue Office (Report #1208 issued March 20, 2012) Report #1305 January 24, 2013 Summary

Audit Follow-Up As of September 30, 2012 Sam M. McCall, Ph.D., CPA, CGFM, CIA, CGAP City Auditor Treasurer-Clerk s Revenue Office (Report #1208 issued March 20, 2012) Report #1305 January 24, 2013 Summary

General Government and Gainesville Regional Utilities Vendor Master File Audit

FINAL AUDIT REPORT A Report to the City Commission General Government and Gainesville Regional Utilities Vendor Master File Audit Mayor Lauren Poe Mayor Pro-Tem Adrian Hayes-Santos Commission Members David

FINAL AUDIT REPORT A Report to the City Commission General Government and Gainesville Regional Utilities Vendor Master File Audit Mayor Lauren Poe Mayor Pro-Tem Adrian Hayes-Santos Commission Members David

Audit Follow-Up. Audit of Growth Management Revenues (Report #1710, Issued May 11, 2017) Report #1802 November 28, As of September 30, 2017

Report #1802 November 28, As of September 30, 2017") Audit Follow-Up As of September 30, 2017 T. Bert Fletcher, CPA, CGMA City Auditor Audit of Growth Management Revenues (Report #1710, Issued May 11, 2017) Report #1802 November 28, 2017 Summary Twelve of

Audit Follow-Up As of September 30, 2017 T. Bert Fletcher, CPA, CGMA City Auditor Audit of Growth Management Revenues (Report #1710, Issued May 11, 2017) Report #1802 November 28, 2017 Summary Twelve of

Assistance. and Guidance Report. Administration and Processing of Leave and Attendance Report #1219 September 5, 2012

Assistance and Guidance Report Sam M. McCall, Ph.D., CPA, CGFM, CIA, CGAP City Auditor Administration and Processing of Leave and Attendance Report #1219 September 5, 2012 Introduction This guidance is

Assistance and Guidance Report Sam M. McCall, Ph.D., CPA, CGFM, CIA, CGAP City Auditor Administration and Processing of Leave and Attendance Report #1219 September 5, 2012 Introduction This guidance is

Internal Controls Integrating COSO

Community Action Partnership 2016 Annual Convention August 30 September 2, 2016 Austin, TX J.W. Marriott Austin Internal Controls Integrating COSO Thursday, September 1, 2016 9:15 am 10:45 am Presented

Community Action Partnership 2016 Annual Convention August 30 September 2, 2016 Austin, TX J.W. Marriott Austin Internal Controls Integrating COSO Thursday, September 1, 2016 9:15 am 10:45 am Presented

Internal Financial Control (IFC)& Internal Financial Controls over Financial Reporting (IFCoFR)

& Internal Financial Controls over Financial Reporting (IFCoFR)") Internal Financial Control (IFC)& Internal Financial Controls over Financial Reporting (IFCoFR) Origin of IFC The first significant focus on internal control certification related to financial reporting

Internal Financial Control (IFC)& Internal Financial Controls over Financial Reporting (IFCoFR) Origin of IFC The first significant focus on internal control certification related to financial reporting

3.6.2 Internal Audit Charter Adopted by the Board: November 12, 2013

3.6.2 Internal Audit Charter Adopted by the Board: November 12, 2013 I. PURPOSE The purpose of this Charter is to formally define LACERS internal audit function s purpose, authority, and responsibility.

3.6.2 Internal Audit Charter Adopted by the Board: November 12, 2013 I. PURPOSE The purpose of this Charter is to formally define LACERS internal audit function s purpose, authority, and responsibility.

EFFICIENT USE OF AUDIT COMMITTEES

AGENDA EFFICIENT USE OF AUDIT COMMITTEES BRENT YOUNG, CPA JERRY GAITHER, CPA Best practices related to: Audit Committee Process Internal Audit Risk Management 2 AUDIT COMMITTEE PROCESS AND PROCEDURES Audit

AGENDA EFFICIENT USE OF AUDIT COMMITTEES BRENT YOUNG, CPA JERRY GAITHER, CPA Best practices related to: Audit Committee Process Internal Audit Risk Management 2 AUDIT COMMITTEE PROCESS AND PROCEDURES Audit

This Questionnaire/Guide is intended to assist you in decision making, as well as in day-to-day operations. Best Regards,

In an effort to disseminate information and assure that we are in compliance with guidelines caused by the Sarbanes Oxley Act that proper internal controls are being adhered to, we have developed some

In an effort to disseminate information and assure that we are in compliance with guidelines caused by the Sarbanes Oxley Act that proper internal controls are being adhered to, we have developed some

A Discussion About Internal Controls February 2016

A Discussion About Internal Controls February 2016 What we will cover today 001 Introductions 002 Defining Internal Controls 003 COSO Internal Controls Integrated Framework 004 Approach to Designing Internal

A Discussion About Internal Controls February 2016 What we will cover today 001 Introductions 002 Defining Internal Controls 003 COSO Internal Controls Integrated Framework 004 Approach to Designing Internal

Financial Controls Checklist

Financial Controls Checklist Board of Health: Board of Health for the Leeds, Grenville & Lanark District Health Unit Period ended: Dec. 31/17 Objective: The objective of the Financial Controls Checklist

Financial Controls Checklist Board of Health: Board of Health for the Leeds, Grenville & Lanark District Health Unit Period ended: Dec. 31/17 Objective: The objective of the Financial Controls Checklist

Guide for the Preservation of Records For Public Water Utilities

Guide for the Preservation of Records For Public Water Utilities No. Types of Records Record Retention Corporate and General 1. Capital Stock Records:.. 2. Proxies and Voting Lists:... 3. Annual Report

Guide for the Preservation of Records For Public Water Utilities No. Types of Records Record Retention Corporate and General 1. Capital Stock Records:.. 2. Proxies and Voting Lists:... 3. Annual Report

Common Questions on Segregation of Duties

Common Questions on Segregation of Duties Why should duties be segregated? What duties should be segregated? How can management determine if duties are properly segregated? What if management has inadequate

Common Questions on Segregation of Duties Why should duties be segregated? What duties should be segregated? How can management determine if duties are properly segregated? What if management has inadequate

Guide to Internal Controls

Guide to Internal Controls Table of Contents Introduction to Internal Controls...3 Roles...4 Components....5 Control Environment...5 Risk assessment...6 Control Activities...7 Information & Communication...9

Guide to Internal Controls Table of Contents Introduction to Internal Controls...3 Roles...4 Components....5 Control Environment...5 Risk assessment...6 Control Activities...7 Information & Communication...9

ACADEMIC DEPARTMENT FISCAL REVIEW

CSU The California State University Office of Audit and Advisory Services ACADEMIC DEPARTMENT FISCAL REVIEW California State University, Dominguez Hills College of Health, Human Services, and Nursing Audit

CSU The California State University Office of Audit and Advisory Services ACADEMIC DEPARTMENT FISCAL REVIEW California State University, Dominguez Hills College of Health, Human Services, and Nursing Audit

503: Adopting an Internal Control -Integrated Framework, Benefits for Nonprofit Organizations

503: Adopting an Internal -Integrated Framework, Benefits for Nonprofit Organizations Richella Abell-Hawes VP-Compliance & Quality, Arc Herkimer Jessica French 1 Quality Systems Director, Arc Herkimer

503: Adopting an Internal -Integrated Framework, Benefits for Nonprofit Organizations Richella Abell-Hawes VP-Compliance & Quality, Arc Herkimer Jessica French 1 Quality Systems Director, Arc Herkimer

503: Adopting an Internal Control -Integrated Framework, Benefits for Nonprofit Organizations

503: Adopting an Internal -Integrated Framework, Benefits for Nonprofit Organizations Richella Abell-Hawes VP-Compliance & Quality, Arc Herkimer Jessica French 1 Quality Systems Director, Arc Herkimer

503: Adopting an Internal -Integrated Framework, Benefits for Nonprofit Organizations Richella Abell-Hawes VP-Compliance & Quality, Arc Herkimer Jessica French 1 Quality Systems Director, Arc Herkimer

Final Audit Follow-Up As of May 31, 2015

Final Audit Follow-Up As of May 31, 2015 T. Bert Fletcher, CPA, CGMA City Auditor Audit of the Tallahassee Community Redevelopment Agency (Report #1425 issued August 22, 2014) Report #1510 June 17, 2015

Final Audit Follow-Up As of May 31, 2015 T. Bert Fletcher, CPA, CGMA City Auditor Audit of the Tallahassee Community Redevelopment Agency (Report #1425 issued August 22, 2014) Report #1510 June 17, 2015

Office of the City Auditor. Committed to increasing government efficiency, effectiveness, accountability and transparency

Office of the City Auditor Committed to increasing government efficiency, effectiveness, accountability and transparency Issue Date: TABLE OF CONTENTS Executive Summary... ii Recommendation... iv Background...1

Office of the City Auditor Committed to increasing government efficiency, effectiveness, accountability and transparency Issue Date: TABLE OF CONTENTS Executive Summary... ii Recommendation... iv Background...1

9. Internal control Internal control, as defined in accounting and auditing, is a process for assuring achievement of an organization's objectives in

9. Internal control Internal control, as defined in accounting and auditing, is a process for assuring achievement of an organization's objectives in operational effectiveness and efficiency, reliable

9. Internal control Internal control, as defined in accounting and auditing, is a process for assuring achievement of an organization's objectives in operational effectiveness and efficiency, reliable

ESSEX POLICE, FIRE AND CRIME COMMISSIONER, FIRE AND RESCUE AUTHORITY

ESSEX POLICE, FIRE AND CRIME COMMISSIONER, FIRE AND RESCUE AUTHORITY DRAFT Internal Audit Strategy 2018/19 Presented at the audit committee meeting of: 15 December 2017 This report is solely for the use

ESSEX POLICE, FIRE AND CRIME COMMISSIONER, FIRE AND RESCUE AUTHORITY DRAFT Internal Audit Strategy 2018/19 Presented at the audit committee meeting of: 15 December 2017 This report is solely for the use

Internal Control Systems

Internal Control Systems What are Internal Controls? Internal Controls are a set of rules, policies, and procedures a municipality can implement to provide reasonable assurances that: its financial reports

Internal Control Systems What are Internal Controls? Internal Controls are a set of rules, policies, and procedures a municipality can implement to provide reasonable assurances that: its financial reports

Common Questions on Segregation of Duties

Common Questions on Segregation of Duties Why should duties be segregated? What duties should be segregated? How can management determine if duties are properly segregated? What if management has inadequate

Common Questions on Segregation of Duties Why should duties be segregated? What duties should be segregated? How can management determine if duties are properly segregated? What if management has inadequate

APPENDIX 2 COMMUNITY DEVELOPMENT COMMISSION FINANCIAL CHECKLIST REQUIRED FOR ALL APPLICANTS (A SITE VISIT MAY BE CONDUCTED LATER)

") REQUIRED FOR ALL APPLICANTS (A SITE VISIT MAY BE CONDUCTED LATER) AGENCY NAME: AGENCY ADDRESS AGENCY PHONE: DATE PREPARED: PREPARED BY: TITLE: EMAIL: AGENCY GENERAL INFORMATION EXECUTIVE DIRECTOR /CITY

REQUIRED FOR ALL APPLICANTS (A SITE VISIT MAY BE CONDUCTED LATER) AGENCY NAME: AGENCY ADDRESS AGENCY PHONE: DATE PREPARED: PREPARED BY: TITLE: EMAIL: AGENCY GENERAL INFORMATION EXECUTIVE DIRECTOR /CITY

Minnesota State Community and Technical College

Office of Internal Auditing Minnesota State Community and Technical College Internal Control and Compliance Audit Reference Number 2017-01 Report Classification: Public Dear Members of the Minnesota State

Office of Internal Auditing Minnesota State Community and Technical College Internal Control and Compliance Audit Reference Number 2017-01 Report Classification: Public Dear Members of the Minnesota State

Audit Follow Up. Electric Revenues (Report #0602, Issued November 15, 2005) As of March 31, Summary. Report #0714 May 17, 2007

As of March 31, Summary. Report #0714 May 17, 2007") Audit Follow Up As of March 31, 2007 Electric Revenues (Report #0602, Issued November 15, 2005) Report #0714 May 17, 2007 Summary The Electric Utility and Utility Business and Customer Services have completed

Audit Follow Up As of March 31, 2007 Electric Revenues (Report #0602, Issued November 15, 2005) Report #0714 May 17, 2007 Summary The Electric Utility and Utility Business and Customer Services have completed

Internal Audit Report. Contract Administration: 601CT Contracts TxDOT Internal Audit Division

Internal Audit Report Contract Administration: 601CT Contracts TxDOT Internal Audit Division Objective Review contract administration and governance of 601CT contracts for structural compliance with laws

Internal Audit Report Contract Administration: 601CT Contracts TxDOT Internal Audit Division Objective Review contract administration and governance of 601CT contracts for structural compliance with laws

EXAMINATION OF CERTAIN FINANCIAL PROCESSES AND INTERNAL CONTROLS OF THE KENTUCKY CORRECTIONAL INDUSTRIES

EXAMINATION OF CERTAIN FINANCIAL PROCESSES AND INTERNAL CONTROLS OF THE KENTUCKY CORRECTIONAL INDUSTRIES CRIT LUALLEN AUDITOR OF PUBLIC ACCOUNTS www.auditor.ky.gov 105 SEA HERO ROAD, SUITE 2 FRANKFORT,

EXAMINATION OF CERTAIN FINANCIAL PROCESSES AND INTERNAL CONTROLS OF THE KENTUCKY CORRECTIONAL INDUSTRIES CRIT LUALLEN AUDITOR OF PUBLIC ACCOUNTS www.auditor.ky.gov 105 SEA HERO ROAD, SUITE 2 FRANKFORT,

Integrating COSO s Fraud Risk Management Guide on an Enterprise Scale

Integrating COSO s Fraud Risk Management Guide on an Enterprise Scale September 15, 2017 Vincent Walden Partner EY Atlanta Delores White Director, Internal Audit Southern Company Scott Hulsey Chief Compliance

Integrating COSO s Fraud Risk Management Guide on an Enterprise Scale September 15, 2017 Vincent Walden Partner EY Atlanta Delores White Director, Internal Audit Southern Company Scott Hulsey Chief Compliance

INTERNAL CONTROLS AUDITOR JOHN BYRD, SENIOR AUDITOR TONYA CARRIGAN, SENIOR AUDITOR

1 INTERNAL CONTROLS FOR THE BEGINNING AUDITOR JOHN BYRD, SENIOR AUDITOR TONYA CARRIGAN, SENIOR AUDITOR UF HEALTH SHANDS HOSPITAL AHIA 32 nd Annual Conference August 25-28, 2013 Chicago, Illinois www.ahia.org

1 INTERNAL CONTROLS FOR THE BEGINNING AUDITOR JOHN BYRD, SENIOR AUDITOR TONYA CARRIGAN, SENIOR AUDITOR UF HEALTH SHANDS HOSPITAL AHIA 32 nd Annual Conference August 25-28, 2013 Chicago, Illinois www.ahia.org

SEGREGATION OF DUTIES for SAP

SEGREGATION OF DUTIES for SAP SEGREGATION-OF-DUTIES In todays modern, technology driven world, segregation-of-duties (SoD) is enforced through business applications and ERP s, but highlighting breakdowns

SEGREGATION OF DUTIES for SAP SEGREGATION-OF-DUTIES In todays modern, technology driven world, segregation-of-duties (SoD) is enforced through business applications and ERP s, but highlighting breakdowns

REPORT ON AN AUDIT OF THE CITY'S PURCHASE CARD PROGRAM AUDIT PROJECT #9914

REPORT ON AN AUDIT OF THE CITY'S PURCHASE CARD PROGRAM AUDIT PROJECT #9914 Jim Carpenter Acting Audit Manager Auditor-In-Charge Beth Breier, CPA, CISA Senior Auditor Roberta McManus, CPA, CIA, CGFO Interim

REPORT ON AN AUDIT OF THE CITY'S PURCHASE CARD PROGRAM AUDIT PROJECT #9914 Jim Carpenter Acting Audit Manager Auditor-In-Charge Beth Breier, CPA, CISA Senior Auditor Roberta McManus, CPA, CIA, CGFO Interim

Protecting Fixed Assets: Internal Controls for Non Profits

Protecting Fixed Assets: Internal Controls for Non Profits 25 September 2012 Community Sector Council Newfoundland and Labrador (CSC) Darlene Scott, Senior Program Associate darlenescott@cscnl.ca www.communitysector.nl.ca

Protecting Fixed Assets: Internal Controls for Non Profits 25 September 2012 Community Sector Council Newfoundland and Labrador (CSC) Darlene Scott, Senior Program Associate darlenescott@cscnl.ca www.communitysector.nl.ca

AUDIT OF SELECTED DEPARTMENTS PERFORMING ACCOUNTS RECEIVABLE FUNCTIONS

February 15, 2012 Sam M. McCall, Ph.D., CPA, CGFM, CIA, CGAP City Auditor HIGHLIGHTS Highlights of City Auditor Report #1204, a report to the City Commission and City management WHY THIS AUDIT WAS CONDUCTED

February 15, 2012 Sam M. McCall, Ph.D., CPA, CGFM, CIA, CGAP City Auditor HIGHLIGHTS Highlights of City Auditor Report #1204, a report to the City Commission and City management WHY THIS AUDIT WAS CONDUCTED

University System of Maryland University of Maryland, College Park

Audit Report University System of Maryland University of Maryland, College Park May 2015 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY For further information

Audit Report University System of Maryland University of Maryland, College Park May 2015 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY For further information

Audit Committee Charter

0 Audit Committee Charter Approved January 21, 2015 Statement of Purpose: The primary function of the Audit Committee is to assist the Board of Directors in fulfilling its oversight responsibilities related

0 Audit Committee Charter Approved January 21, 2015 Statement of Purpose: The primary function of the Audit Committee is to assist the Board of Directors in fulfilling its oversight responsibilities related

Financial Internal Controls Initiative. Martha Kerner Assistant Vice Chancellor for Business Services

Financial Internal Controls Initiative Martha Kerner Assistant Vice Chancellor for Business Services April 27, 2015 Presentation Objectives: I. Understand the framework on which the Financial Internal

Financial Internal Controls Initiative Martha Kerner Assistant Vice Chancellor for Business Services April 27, 2015 Presentation Objectives: I. Understand the framework on which the Financial Internal

2010 Joint Chairmen s Report. UMB Progress to Address Audit Findings. (R30B/R75T), pages 133/ Release of Restricted Funds

, pages 133/ Release of Restricted Funds") 2010 Joint Chairmen s Report UMB Progress to Address Audit Findings (R30B/R75T), pages 133/145-146 Release of Restricted Funds 1 Subject: 2010 Joint Chairmen s Report - UMB Progress to Address Audit Findings

2010 Joint Chairmen s Report UMB Progress to Address Audit Findings (R30B/R75T), pages 133/145-146 Release of Restricted Funds 1 Subject: 2010 Joint Chairmen s Report - UMB Progress to Address Audit Findings

Fraud Prevention, Detection, and Internal Controls

Fraud Prevention, Detection, and Internal Controls Budget, Accounting and Reporting Council May 28, 2015 Sherrie Ard, CPA, CFE Financial Management Specialist Local Government Performance Center Local

Fraud Prevention, Detection, and Internal Controls Budget, Accounting and Reporting Council May 28, 2015 Sherrie Ard, CPA, CFE Financial Management Specialist Local Government Performance Center Local

A. General Information

Management Systems Questionnaire for Standard Cost Reimbursement Grants (Jan 2016) 1. Legal name of applicant organization: 2. Name and title of individual completing this questionnaire: 3. Signature of

Management Systems Questionnaire for Standard Cost Reimbursement Grants (Jan 2016) 1. Legal name of applicant organization: 2. Name and title of individual completing this questionnaire: 3. Signature of

CONVENT OF THE SACRED HEART SCHOOL FOUNDATION FINANCIAL REGULATIONS

CONVENT OF THE SACRED HEART SCHOOL FOUNDATION FINANCIAL REGULATIONS Approved by Convent of the Sacred Heart School Foundation, Board of Governors on 9 th October 2008 Policy Statement So that all officers

CONVENT OF THE SACRED HEART SCHOOL FOUNDATION FINANCIAL REGULATIONS Approved by Convent of the Sacred Heart School Foundation, Board of Governors on 9 th October 2008 Policy Statement So that all officers

Dutchess County Department of Planning and Community Development Division of Mass Transit January 2007 December 2008

Dutchess County Department of Planning and Community Development Division of Mass Transit January 2007 December 2008 COMPTROLLER S SUMMARY... 2 Organization and Background... 2 Audit Scope, Objective and

Dutchess County Department of Planning and Community Development Division of Mass Transit January 2007 December 2008 COMPTROLLER S SUMMARY... 2 Organization and Background... 2 Audit Scope, Objective and

Implementation Tool for Auditors

Implementation Tool for Auditors CANADIAN AUDITING STANDARDS (CAS) DECEMBER 2017 STANDARD DISCUSSED CAS 315, Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity

Implementation Tool for Auditors CANADIAN AUDITING STANDARDS (CAS) DECEMBER 2017 STANDARD DISCUSSED CAS 315, Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity

Internal Control Questionnaire and Assessment

Bureau of Financial Monitoring and Accountability Florida Department of Economic Opportunity September 15, 2016 107 East Madison Street Caldwell Building Tallahassee, Florida 32399 www.floridajobs.org

Bureau of Financial Monitoring and Accountability Florida Department of Economic Opportunity September 15, 2016 107 East Madison Street Caldwell Building Tallahassee, Florida 32399 www.floridajobs.org

AUDIT UNDP COUNTRY OFFICE AZERBAIJAN. Report No Issue Date: 22 January 2014

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN AZERBAIJAN Report No. 1234 Issue Date: 22 January 2014 Table of Contents Executive Summary i I. Introduction 1 II. About the Office

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN AZERBAIJAN Report No. 1234 Issue Date: 22 January 2014 Table of Contents Executive Summary i I. Introduction 1 II. About the Office

Internal financial controls

Internal financial controls Synopsis Refresh on IFC Snapshot from revised ICAI guidance note Approach for ICFR implementation 2 IFC, as per Companies Act, 2013 As per Section 134 of the Companies Act 2013,

Internal financial controls Synopsis Refresh on IFC Snapshot from revised ICAI guidance note Approach for ICFR implementation 2 IFC, as per Companies Act, 2013 As per Section 134 of the Companies Act 2013,

Fraud Risk Management

Fraud Risk Management Specific Anti-Fraud Controls (Process or Transaction Level) 2017 Association of Certified Fraud Examiners, Inc. Discussion Questions 1. Does your organization have adequate staffing

Fraud Risk Management Specific Anti-Fraud Controls (Process or Transaction Level) 2017 Association of Certified Fraud Examiners, Inc. Discussion Questions 1. Does your organization have adequate staffing

Employee Relations Approved General Government Operating Budget ER - 1. Municipal Manager. Employee Relations

Municipal Manager Administration Benefits Central Payroll Employment, Classification & Records Labor Relations ER - 1 Description The Municipality of Anchorage Department provides employment services,

Municipal Manager Administration Benefits Central Payroll Employment, Classification & Records Labor Relations ER - 1 Description The Municipality of Anchorage Department provides employment services,

OFFICE OF THE AUDITOR

OFFICE OF THE AUDITOR DEPARTMENT OF PUBLIC WORKS PROGRAM AUDIT FEBRUARY 2007 Dennis J. Gallagher Auditor Dennis J. Gallagher Auditor City and County of Denver 201 West Colfax Ave., Dept. 705 Denver, Colorado

OFFICE OF THE AUDITOR DEPARTMENT OF PUBLIC WORKS PROGRAM AUDIT FEBRUARY 2007 Dennis J. Gallagher Auditor Dennis J. Gallagher Auditor City and County of Denver 201 West Colfax Ave., Dept. 705 Denver, Colorado

What Happens When Internal Controls Fail

What Happens When Internal Controls Fail 1 Your Presenters Brian Sanvidge Principal Baker Tilly Ellen Labita Partner Baker Tilly Danielle Callaci Manager Baker Tilly 2 Today s Agenda > What are Internal

What Happens When Internal Controls Fail 1 Your Presenters Brian Sanvidge Principal Baker Tilly Ellen Labita Partner Baker Tilly Danielle Callaci Manager Baker Tilly 2 Today s Agenda > What are Internal

INFRAREIT, INC. Corporate Governance Guidelines

INFRAREIT, INC. Corporate Governance Guidelines The Board of Directors (the Board ) of InfraREIT, Inc. (the Company ) has adopted these Corporate Governance Guidelines (these Guidelines ), in order to

INFRAREIT, INC. Corporate Governance Guidelines The Board of Directors (the Board ) of InfraREIT, Inc. (the Company ) has adopted these Corporate Governance Guidelines (these Guidelines ), in order to

Diving into the 2013 COSO Framework. Presented by: Ronald A. Conrad

Diving into the 2013 COSO Framework Presented by: Ronald A. Conrad 2 Objectives Obtain an understanding of why the COSO Framework has been updated Understand how the framework has changed Identify the

Diving into the 2013 COSO Framework Presented by: Ronald A. Conrad 2 Objectives Obtain an understanding of why the COSO Framework has been updated Understand how the framework has changed Identify the

The Episcopal Diocese of Kentucky

The Episcopal Diocese of Kentucky Internal Control Questionnaire Manual of Business Methods in Church Affairs (Spring 2012) Chapter II: Internal Controls, Section C The following Internal Control Questionnaire

The Episcopal Diocese of Kentucky Internal Control Questionnaire Manual of Business Methods in Church Affairs (Spring 2012) Chapter II: Internal Controls, Section C The following Internal Control Questionnaire

Diocese of Covington Policies & Procedures Manual Section: Compliance Accounting Policy: Internal Control & Segregation of Duties

Internal Control refers to the policies and procedures established to provide reasonable assurance that parish assets are safeguarded, that accountability is achieved, and that errors in financial records

Internal Control refers to the policies and procedures established to provide reasonable assurance that parish assets are safeguarded, that accountability is achieved, and that errors in financial records

Anticipated Completion: January 31, 2018.

1 The Cash Room was staffed with only one person several times during the day. 1. Cash Room staff swipe their badges each time they enter the Cash Room, even when entering with another staff member. The

1 The Cash Room was staffed with only one person several times during the day. 1. Cash Room staff swipe their badges each time they enter the Cash Room, even when entering with another staff member. The

e. inadequacy or ineffectiveness of the internal audit program and other monitoring activities;

TABLE OF CONTENTS Page I. BACKGROUND 1 II. SCOPE OF THE BANK INTERNAL CONTROL SYSTEM 2 1. Definition and Objectives 2 2. Stakeholders in the Bank Internal Control System 3 3. Factors to Consider in the

TABLE OF CONTENTS Page I. BACKGROUND 1 II. SCOPE OF THE BANK INTERNAL CONTROL SYSTEM 2 1. Definition and Objectives 2 2. Stakeholders in the Bank Internal Control System 3 3. Factors to Consider in the

Financial Resources: Control of finances The institution exercises appropriate control over all its financial resources.

3.10.3 Financial Resources: Control of finances The institution exercises appropriate control over all its financial resources. Judgment Compliant Non-Compliant Not Applicable Compliance Report Narrative

3.10.3 Financial Resources: Control of finances The institution exercises appropriate control over all its financial resources. Judgment Compliant Non-Compliant Not Applicable Compliance Report Narrative

Fire Department Inventory Management Audit

Fire Department Inventory Management Audit With over $3 million spent annually on inventory, the Fire Department needs stronger inventory management practices and controls Independence you can rely on

Fire Department Inventory Management Audit With over $3 million spent annually on inventory, the Fire Department needs stronger inventory management practices and controls Independence you can rely on

EXAMINATION REPORT Wastewater Management Division Contractor Hiring & Payment Practices

EXAMINATION REPORT Wastewater Management Division Contractor Hiring & Payment Practices July 2017 Office of the Auditor Audit Services Division City and County of Denver Page 1 The Auditor of the City

EXAMINATION REPORT Wastewater Management Division Contractor Hiring & Payment Practices July 2017 Office of the Auditor Audit Services Division City and County of Denver Page 1 The Auditor of the City

Record Retention. Professional Insurance Agents of Florida 1390 Timberlane Rd. Tallahassee, FL

Record Retention Professional Insurance Agents of Florida 1390 Timberlane Rd. Tallahassee, FL 32312 850-893-8245 www.piafl.org Record Retention Guidelines Below are few comments about the record retention

Record Retention Professional Insurance Agents of Florida 1390 Timberlane Rd. Tallahassee, FL 32312 850-893-8245 www.piafl.org Record Retention Guidelines Below are few comments about the record retention

Internal Controls: Providing an Effective Control Environment. Why This Session Is Needed. Lesson Overview & Module Objectives

Internal Controls: Providing an Effective Control Environment Internal Controls 1 Why This Session Is Needed Uniform Guidance has expanded the requirements and increased the focus on internal controls

Internal Controls: Providing an Effective Control Environment Internal Controls 1 Why This Session Is Needed Uniform Guidance has expanded the requirements and increased the focus on internal controls

Internal Control Questionnaire and Assessment

Bureau of Financial Monitoring and Accountability Florida Department of Economic Opportunity September 30, 2017 107 East Madison Street Caldwell Building Tallahassee, Florida 32399 www.floridajobs.org

Bureau of Financial Monitoring and Accountability Florida Department of Economic Opportunity September 30, 2017 107 East Madison Street Caldwell Building Tallahassee, Florida 32399 www.floridajobs.org

Alyssa G. Martin, CPA Brandon Tanous, CIA, Using the COSO CFE, CGAP, CRMA Framework to Develop a Strong and Preventive Control Environment

Speakers Using the COSO Framework to Develop a Strong and Preventive Control Environment Weaver Public Sector CPE Event Alyssa G. Martin, CPA Dallas Executive Partner, Advisory Services 25+ years of public

Speakers Using the COSO Framework to Develop a Strong and Preventive Control Environment Weaver Public Sector CPE Event Alyssa G. Martin, CPA Dallas Executive Partner, Advisory Services 25+ years of public

AUDIT OF THE TREASURER-CLERK S REVENUE OFFICE

March 20, 2012 Sam M. McCall, Ph.D., CPA, CGFM, CIA, CGAP City Auditor HIGHLIGHTS Highlights of City Auditor Report #1208, a report to the City Commission and City management WHY THIS AUDIT WAS CONDUCTED

March 20, 2012 Sam M. McCall, Ph.D., CPA, CGFM, CIA, CGAP City Auditor HIGHLIGHTS Highlights of City Auditor Report #1208, a report to the City Commission and City management WHY THIS AUDIT WAS CONDUCTED

FRAUD AWARENESS UPDATE

Tammy Michaud, CPA, Principal Sarah Belliveau, CPA, Senior Manager FRAUD AWARENESS UPDATE berrydunn.com CATEGORIES OF FRAUD Asset misappropriations (stealing) Theft or misuse of assets Corruption Inappropriate

Tammy Michaud, CPA, Principal Sarah Belliveau, CPA, Senior Manager FRAUD AWARENESS UPDATE berrydunn.com CATEGORIES OF FRAUD Asset misappropriations (stealing) Theft or misuse of assets Corruption Inappropriate

Fiscal Oversight Fundamentals

Fiscal Oversight Fundamentals Module 1: School District Finances: Roles and Responsibilities 2012 New York State School Boards Association, Latham NY The Five-Point Plan 1. Requires training for school

Fiscal Oversight Fundamentals Module 1: School District Finances: Roles and Responsibilities 2012 New York State School Boards Association, Latham NY The Five-Point Plan 1. Requires training for school

UNIVERSITY OF NEVADA, LAS VEGAS REBEL CARD SERVICES CENTER Internal Audit Report July 1, 2008 through June 30, 2009

UNIVERSITY OF NEVADA, LAS VEGAS REBEL CARD SERVICES CENTER Internal Audit Report July 1, 2008 through June 30, 2009 GENERAL OVERVIEW The RebelCard Services Center (RCSC) operates under the Student Life

UNIVERSITY OF NEVADA, LAS VEGAS REBEL CARD SERVICES CENTER Internal Audit Report July 1, 2008 through June 30, 2009 GENERAL OVERVIEW The RebelCard Services Center (RCSC) operates under the Student Life

EGYPTIAN AREA AGENCY ON AGING Fiscal Monitoring Program

EGYPTIAN AREA AGENCY ON AGING Fiscal Monitoring Program Fiscal Year: Name of Project/Site: (TIN #) Address: (city) (state) (zip code) Project Director/Site Manager: Geographic Area Served: (county) Project/Site

EGYPTIAN AREA AGENCY ON AGING Fiscal Monitoring Program Fiscal Year: Name of Project/Site: (TIN #) Address: (city) (state) (zip code) Project Director/Site Manager: Geographic Area Served: (county) Project/Site

EXTERNAL AUDITOR INDEPENDENCE CHARTER

EXTERNAL AUDITOR INDEPENDENCE CHARTER 1.0 ESTABLISHMENT OF COMMITTEE This Charter sets out the circumstances in which the Company s Auditor may perform Services and the procedures to be followed to obtain

EXTERNAL AUDITOR INDEPENDENCE CHARTER 1.0 ESTABLISHMENT OF COMMITTEE This Charter sets out the circumstances in which the Company s Auditor may perform Services and the procedures to be followed to obtain

Final Audit Follow-Up

Final Audit Follow-Up As of March 31, 2011 Sam M. McCall, Ph.D., CPA, CGFM, CIA, CGAP City Auditor Selected Solid Waste Activities (Report #1104 issued January 19, 2011) Report #1113 June 16, 2011 Summary

Final Audit Follow-Up As of March 31, 2011 Sam M. McCall, Ph.D., CPA, CGFM, CIA, CGAP City Auditor Selected Solid Waste Activities (Report #1104 issued January 19, 2011) Report #1113 June 16, 2011 Summary

Preparing for a Headache-free Audit

Preparing for a Headache-free Audit PRESENTED TO SWMSBO Conference 2017 PRESENTED BY Molly R. Fish, CPA PREPARED BY Molly Fish, CPA Date Objectives Understand audit terminology Gain awareness of audit

Preparing for a Headache-free Audit PRESENTED TO SWMSBO Conference 2017 PRESENTED BY Molly R. Fish, CPA PREPARED BY Molly Fish, CPA Date Objectives Understand audit terminology Gain awareness of audit

Audit Follow-Up. As of March 31, Summary

Audit Follow-Up As of March 31, 2016 T. Bert Fletcher, CPA, CGMA City Auditor Audit of Parks, Recreation and Neighborhood Affairs Trousdell Aquatics Center and Gymnastics Center Revenues (Report #1606,

Audit Follow-Up As of March 31, 2016 T. Bert Fletcher, CPA, CGMA City Auditor Audit of Parks, Recreation and Neighborhood Affairs Trousdell Aquatics Center and Gymnastics Center Revenues (Report #1606,

SIGAR JULY. Special Inspector General for Afghanistan Reconstruction

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR Financial Audit 13-11 Department of State s Afghanistan Media Project: Audit of Incurred Costs by HUDA Development Organization Afghanistan

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR Financial Audit 13-11 Department of State s Afghanistan Media Project: Audit of Incurred Costs by HUDA Development Organization Afghanistan

Assurance Research Advisory Group Firm Data

Assurance Research Advisory Group Firm Data Program Summary The AICPA Assurance Research Advisory Group (ARAG) seeks to drive research relative to private company assurance issues that are most pressing

Assurance Research Advisory Group Firm Data Program Summary The AICPA Assurance Research Advisory Group (ARAG) seeks to drive research relative to private company assurance issues that are most pressing

INTERNAL CONTROL HANDBOOK

INTERNAL CONTROL HANDBOOK INTERNAL CONTROL HANDBOOK ILLINOIS STATE BOARD OF EDUCATION SCHOOL BUSINESS SERVICES DIVISION Revised July, 2017 Most Content remains the same as published in 1993 Prepared by

INTERNAL CONTROL HANDBOOK INTERNAL CONTROL HANDBOOK ILLINOIS STATE BOARD OF EDUCATION SCHOOL BUSINESS SERVICES DIVISION Revised July, 2017 Most Content remains the same as published in 1993 Prepared by

Audit Training-of-Trainers Workshop, November 2014, Vienna Components of internal control within organization

Audit Training-of-Trainers Workshop, 18-19 November 2014, Vienna Components of internal control within organization Andrei Busuioc, Senior Financial Management Specialist, CFRR Session objectives The session

Audit Training-of-Trainers Workshop, 18-19 November 2014, Vienna Components of internal control within organization Andrei Busuioc, Senior Financial Management Specialist, CFRR Session objectives The session

Module 1: Safeguarding District Resources: Roles & Responsibilities

Module 1: Safeguarding District Resources: Roles & Responsibilities Presenter: Jamie P. McPherson Leadership Development Manager New School Board Member Mandated Training Day Two: Fiscal Oversight Training

Module 1: Safeguarding District Resources: Roles & Responsibilities Presenter: Jamie P. McPherson Leadership Development Manager New School Board Member Mandated Training Day Two: Fiscal Oversight Training

Financial Statement Close Process

Financial Statement Close Process Process Control Objective Risk Control Considerations Segregation of Duties Accounting functions are properly segregated. Unauthorized and inaccurate transactions may

Financial Statement Close Process Process Control Objective Risk Control Considerations Segregation of Duties Accounting functions are properly segregated. Unauthorized and inaccurate transactions may

Seattle Public Schools The Office of Internal Audit

Seattle Public Schools The Office of Internal Audit Internal Audit Report September 1, 2014 through Current Issue Date: June 21, 2016 Executive Summary Background Information The function is centralized

Seattle Public Schools The Office of Internal Audit Internal Audit Report September 1, 2014 through Current Issue Date: June 21, 2016 Executive Summary Background Information The function is centralized

Final Audit Follow Up

Final Audit Follow Up As of September 30, 2005 Sam M. McCall, CPA, CGFM, CIA, CGAP City Auditor Citywide Disbursements - 2003 (Report #0410, Issued April 15, 2004) Report #0611 March 8, 2006 Summary This

Final Audit Follow Up As of September 30, 2005 Sam M. McCall, CPA, CGFM, CIA, CGAP City Auditor Citywide Disbursements - 2003 (Report #0410, Issued April 15, 2004) Report #0611 March 8, 2006 Summary This

Internal Controls. June-20-17

Internal Controls June-20-17 Background The Audit Committee is responsible for ensuring the adequacy and effectiveness of HRM s systems of internal control in relation to financial controls and risk management

Internal Controls June-20-17 Background The Audit Committee is responsible for ensuring the adequacy and effectiveness of HRM s systems of internal control in relation to financial controls and risk management

Notice of Intended Action-Chapter 81 Standards for School Business Official Preparation Programs Presented at Public Hearing: May 22, 2012

81.7(1) Standard 1. Each school business official candidate shall demonstrate an understanding of Uniform Financial Accounting, Governmental GAAP accounting, and statutory concepts. a. Is responsible for

81.7(1) Standard 1. Each school business official candidate shall demonstrate an understanding of Uniform Financial Accounting, Governmental GAAP accounting, and statutory concepts. a. Is responsible for

FRAUD DETERRENCE AND DETECTION

FRAUD DETERRENCE AND DETECTION Segregation of Duties Corruption Scheme Red Flags Unchecked authority to approve No formal documented procedures Circumventing normal policies and procedures Employees receiving

FRAUD DETERRENCE AND DETECTION Segregation of Duties Corruption Scheme Red Flags Unchecked authority to approve No formal documented procedures Circumventing normal policies and procedures Employees receiving