OCEAN CARRIERS: MARKET CONDITIONS, CARRIER LOGISTICS AND CHANGING INDUSTRY DYNAMICS. Bill Sheridan. APL Network Operations & Logistics

|

|

|

- Russell Stevenson

- 5 years ago

- Views:

Transcription

1 OCEAN CARRIERS: MARKET CONDITIONS, CARRIER LOGISTICS AND CHANGING INDUSTRY DYNAMICS Bill Sheridan APL Network Operations & Logistics

2 William F. Sheridan Director Network Operations, Western Region Seattle, WA June 27, 2012

3 Contents Economic Trends Market Dynamics Chassis Paradigm Sustainability Navigating our Future 1

4 2 Economic Trends

5 Global Demand for Key Markets & Trades TRANSATLANTIC 2011 Size: 6.1 m TEU 2012 Growth Rate: 4.1% HH 4.1% BH ASIA - EUROPE 2011 Size: 23.2 m TEU 2012 Growth Rate: 5.8% HH 6.3% BH TRANSPACIFIC 2011 Size: 20.8 m TEU 2012 Growth Rate: 4.5% HH 7.0% BH AFRICA IMPORTS 2011 Size: 5.6 m TEU 2012 Growth Rate: 10.8% INTRA-ASIA 2011 Size: 45.5 m TEU 2012 Growth Rate: LH 10.8% HH 9.7% BH SS 6.9% LTAM 2011 Size: 13.4 m TEU 2012 Growth Rate: NS/EW 8.5% HH 9.3% BH Intra LTAM 9.2% Notes World trade is forecasted to be MTEU by Remaining volume unaccounted in the map primarily include Africa exports and Central Asia total trade Source: Seabury, GPS

6 Containerized trade continues to grow in 2012 but at a more moderate pace Global GDP and Container Demand Growth 20.0% 15.0% 10.0% 5.0% 0.0% -5.0% -10.0% 11.2% 4.8% 3.8% 2.3% 11.1% 2.9% 13.4% 3.6% 13.9% 4.9% 10.9% 4.6% 10.2% 5.3% 11.0% 5.4% 2.8% 4.0% -0.7% -9.9% 14.0% 5.2% 7.3% 3.8% 7.7% 3.2% 7.8% 3.9% -15.0% F 2013F Global GDP Container Demand Growth Note: EIU data forecasts used for 2012 and 2013 Source: Drewry, Seabury, Clarksons, IMF WEO Sep2011/Jan 2012, EIU Global Forecasting 4

7 This is largely driven by slower global growth in 2012 due to uncertainties arising out of the European government debt issues GDP Growth 15.0% CAGR ( ) 10.0% 5.0% 0.0% 8.2% 6.9% 3.2% 1.9% -0.8% India 8.0% China 11.2% Global 4.4% US 2.6% EU27 2.6% -5.0% F 2013F 2014F 2015F 2016F EU27 US Global China India Source: IMF WEO Sep2011/Jan2012, EIU Global Forecasting 5

8 Oversupply is likely to extend into 2013 due to orders of >8,000 TEU vessels during 2010 and 2011 Demand and Supply Growth Rate Forecast F 2013F Demand Growth Supply Growth Source: Alphaliner, Drewry, Clarksons, Seabury, MDS 6

9 In 2011, challenging freight rate environment and rising fuel costs have negatively impacted liner earnings Liner Companies FY11 Results : Ranked by EBIT Margin (%) EBIT (US$ millions) EBIT Margin (%) EBIT Margin (%) EBIT (US$M) 4.0% % 0.0% -2.0% -4.0% -6.0% -8.0% -10.0% -12.0% 2.2% 1.7% % -1.9% % % % % % % % % % % % ,000 OOCL HPL CMA- CGM MAERSK MOL HMM APL HANJIN NYK K-LINE CSAV 7 Notes APL results for Liner division and is proxied by Core EBIT. Maersk results are inclusive of Damco Logistics but exclude terminals and gains on sale Operating profit used as proxy for EBIT: HMM and Hanjin Ordinary income as proxy for EBIT: MOL and Kline Recurring income as proxy for EBIT: NYK Source: Company financial reports

10 Main Carriers Operating Margins 1Q 2012 vs 4Q

11 Strong delivery flow in next 12 months but lack of recent newbuild orders will result in diminishing deliveries from 2H 2013 Thousand TEU Delivery is expected to peak in 2Q 12, with ~.5M TEUs coming on stream this quarter 2.5% % % % % Q 12 2Q 12 3Q 12 4Q 12 1Q 13 2Q 13 3Q 13 4Q 13 1Q 14 2Q 14 3Q 14 4Q 14 1Q 15 2Q 15 3Q 15 4Q % Scheduled Newbuild % of Global Fleet Source: MDS March2012 9

12 Containerships >10,000 teu : Monthly deliveries in 2012 breakdown by Carrier 2012 Vessel Delivery by Carrier Source: Alphaliner 10

13 Challenging container shipping environment is forcing liners to manage capacity Source: Alphaliner 11

14 12 Market Dynamics

15 Market Dynamics In order to remain competitive many carriers have ordered ultra large ships. Thirteen different carriers have ordered ships over 12,500 TEU. Demand growth is not keeping pace, resulting in pressure on rates which have already reached non-compensatory levels in key trades. Carriers are operating in the red, resulting in idle capacity and more slowsteaming. Carriers are looking for ways to control costs while still providing quality service and innovative solutions to their customers. 13

16 Trade flows to/from Asia have shifted significantly. Shifting pattern in Asia is producing a significant increase in equipment repositioning as inbound flows are growing in countries other than China where the outbound demand is highest. Top EB countries are not growing their WB volumes as fast as other Asian countries, creating increasing mismatch of in/ out volumes in Asia North China South China Japan Vietnam UAE Malaysia US Exports growing to SEA, M East which need longer transit Repositioning Boxes need to be repositioned to major exporting regions e.g. North China This relatively recent shift in flow creates longer equipment turn, drives up repositioning cost to get the boxes to China where they are needed to support outbound demand, and increases the size of the equipment fleet carriers must have to service the market.increasing costs. 14

17 15 Domestic Intermodal

18 World Containerized Trade Outlook World containerized trade estimated to have moderate growth this year. TP growth is expected to pick up in 2013 Containerized Trade Growth Intra Asia Global 4.2% 7.1% 17.2% 16.0% 15.3% 15.0% 9.3% 8.3% 8.4% 6.9% 6.8% 6.7% 6.4% 5.9% 5.5% 4.9% 0.4% 2.4% Global Trade Growth Alphaliner (Mar 20, 2012) 7.7% 6.5% 7.5% Clarksons (Feb 21, 2012) 7.9% 7.7% 8.3% Drewry (Dec 22, 2011) 6.5% 5.4% - JP Morgan (Nov 29, 2011) 6.4% 4.5% 6.3% Global Insights (Sep 30, 2011) 6.9% 6.8% 6.7% Transpacific HH Trade Growth Clarksons (Feb 21, 2012) -0.4% 4.2% 6.1% Alphaliner* (Jan 10, 2012) -0.8% 4.6% 5.1% Drewry (Dec 22, 2011) 0.4% 3.1% PIERS (Dec 2, 2011) 0.2% 2.7% 4.9% Transpacific (HH) Asia Europe (HH) 13.9% 15.1% E 2013E Asia-Europe HH Trade Growth Clarksons** (Feb 21, 2012) 3.3% 2.8% 6.1% Alphaliner* (Jan 10, 2012) 2.8% 1.5% 6.3% Drewry (Dec 22, 2011) 3.9% 2.0% 16 Source: Equity analysts, shipping consultants and SLM estimates Note: *Alphaliner TP is FE-US, ASEU is FE-Europe **Clarksons growth is Far East to Europe

19 17 Chassis Paradigm

is forum under FMC authority where carriers can discuss operational issues OCEMA established chassis pools as a first step of rationalizing Chassis")

20 Chassis Background USA is only location where carriers provide chassis Carriers are pursuing paradigm shift away from Liner chassis provisioning OCEMA (Ocean Carrier Equipment Maintenance Agreement) is forum under FMC authority where carriers can discuss operational issues OCEMA established chassis pools as a first step of rationalizing Chassis provisioning 18

21 Paradigm Shift Overview Carriers are considering the following approaches -Continue with current program Carrier provided - Pool Participation Continue to supply chassis, but join a pool -Trucker model Divest chassis, new owner charges trucker 19

22 What is APL doing APL will phase out its container chassis fleet beginning 2012 and will conclude by By relying on providers who specialize in chassis management, this will ensure that equipment is deployed more efficiently. In Spring 2012, APL will begin a pilot program at terminals in Denver and Salt Lake City. 20

23 21 Sustainability

Low Sulphur Fuel Cold")

24 Continued Environmental Initiatives Eco-responsible operations for a sustainable future Optimize speed, schedule, weather routing and best practices to reduce CO 2 emissions (Slow Steaming) Low Sulphur Fuel Cold Ironing Seawater Scrubber Ballast Water Treatment Slide Valves Environmentally friendly paint on ship hulls Voluntary Speed Reduction in Southern California waters to reduce emissions Eliminating drayage thru on-dock rail 22 22

25 Service Options: Investing in our Network New CGG Facility 43 Acres Container Capacity: 1,600 Stalls, 400 Decked Gates: 4 Inbound/3 Outbound M&R: 19,000 Sq. Ft. Shop 10 Bay Chassis/ Container Repair Fleet Expansion 34 Vessels ordered Delivery between Q and 2014 Best fuel efficiency in the industry 10x14,000 TEU Vessels Productivity Improvements at GGS Crane Backreach Opens up more traffic lanes under the hook Better traffic flow, increased efficiency Future growth Increased safety 23

26 Future developments such as the widening of the Panama Canal in 2014 will help exporters Larger vessels with increased deadweight Provide the capability to serve USEC from Asia Post Panamax trade patterns expected to shift, benefiting Atlantic Coast Ports Upgraded infrastructure is required to increase capacity and efficiently move products for global import and export customers Source: Drewry Supply Chain Advisors 24

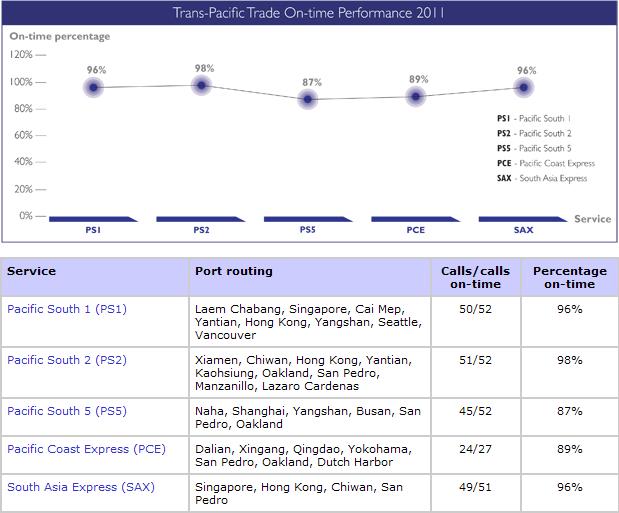

27 Service Reliability 94% on-time performance within the Trans-Pacific Trade 25

28 26 Navigating Our Future

29 While uncertainty remains in 2012, we continue to focus on managing costs and operational efficiencies Ordered 34 new vessels which can potentially replace existing charters Capacity management Cost Structure Example Slow steaming Exploring technological advancements New vessel specifications Fixed cost Bunker G&A Variable cost Enhancing operational efficiencies Densification of volume (e.g. costs efficiencies through volume increase in own terminals) Centralization of processes (e.g. Global Service Centre, Chongqing, China) Relocation of US headquarters to Phoenix 27

30 Navigating Our Future Building Integrated Partnerships Collaboration TSA discussions with the Shipper Advisory Council Establish multi-year contracts to reduce rate volatility Planning Accurate forecasting tied to equipment and space commitments Use IT solutions to exchange business information and optimize visibility Integrated Partnerships Sharing TSA revenue index Adjusted TSA bunker formula Share pain points and KPIs thru regular business reviews Innovation Identify opportunities and create new solutions up and down the supply chain Find creative ways to contract, seeking stability and clarity 28

31 Thank You

32 Value Chain Origin services Our value chain Destination services Warehouse Land Consol Terminals Container shipping Terminals Deconsol Land Warehouse Visibility NOL s container shipping and logistics businesses form a value chain which offers customers reliable, time-definite and costeffective services from origin to destination. As supply chains become more complex, our total value chain proposition offers strong advantages for customers

33 End-to-end solutions 31

Gene Seroka APL President, Americas. January 9, 2013 New York, NY

Gene Seroka APL President, Americas January 9, 2013 New York, NY Contents Economic Trends Market Dynamics Building a Sustainable Organization Integrated Partnerships 1 2 Economic Trends Global Demand for

Gene Seroka APL President, Americas January 9, 2013 New York, NY Contents Economic Trends Market Dynamics Building a Sustainable Organization Integrated Partnerships 1 2 Economic Trends Global Demand for

Gene Seroka APL President, Americas. January 24, 2013 Tampa, Florida

Gene Seroka APL President, Americas January 24, 2013 Tampa, Florida Contents Economic Trends Market Dynamics Building a Sustainable Organization Integrated Partnerships 1 2 Economic Trends Global Demand

Gene Seroka APL President, Americas January 24, 2013 Tampa, Florida Contents Economic Trends Market Dynamics Building a Sustainable Organization Integrated Partnerships 1 2 Economic Trends Global Demand

Gene Seroka APL President, Americas

Gene Seroka APL President, Americas March 7, 2013 Los Angeles, CA Contents Economic Trends Market Dynamics Building a Sustainable Organization Integrated Partnerships 1 2 Economic Trends Market Size &

Gene Seroka APL President, Americas March 7, 2013 Los Angeles, CA Contents Economic Trends Market Dynamics Building a Sustainable Organization Integrated Partnerships 1 2 Economic Trends Market Size &

Gene Seroka APL President, Americas

Gene Seroka APL President, Americas April 27, 2012 Specialty Crop Trade Council - San Diego, CA Global Demand for Key Markets & Trades TRANS-ATLANTIC 2010 Size: 4.8 m TEU 2011 HH Growth: ~ 3-5% ASIA-EUROPE

Gene Seroka APL President, Americas April 27, 2012 Specialty Crop Trade Council - San Diego, CA Global Demand for Key Markets & Trades TRANS-ATLANTIC 2010 Size: 4.8 m TEU 2011 HH Growth: ~ 3-5% ASIA-EUROPE

Contents. Economic Trends. Market Dynamics. Building a Sustainable Organization. Integrated Partnerships. Open Dialogue

Contents Economic Trends Market Dynamics Building a Sustainable Organization Integrated Partnerships Open Dialogue 1 2 Economic Trends Market Size & Growth Rate Overall Growth outlook is expected to be

Contents Economic Trends Market Dynamics Building a Sustainable Organization Integrated Partnerships Open Dialogue 1 2 Economic Trends Market Size & Growth Rate Overall Growth outlook is expected to be

ALVAREZ & MARSAL CONTAINER SHIPPING INDUSTRY OVERVIEW VIRGINIA MARITIME ASSOCIATION INTERNATIONAL TRADE SYMPOSIUM

ALVAREZ & MARSAL CONTAINER SHIPPING INDUSTRY OVERVIEW VIRGINIA MARITIME ASSOCIATION INTERNATIONAL TRADE SYMPOSIUM May 3, 2012 Robert F. Sappio CONTENTS I. Background II. Macro-economic Outlook III. Industry

ALVAREZ & MARSAL CONTAINER SHIPPING INDUSTRY OVERVIEW VIRGINIA MARITIME ASSOCIATION INTERNATIONAL TRADE SYMPOSIUM May 3, 2012 Robert F. Sappio CONTENTS I. Background II. Macro-economic Outlook III. Industry

2016 Annual Results. Orient Overseas (International) Limited. March 2017

Limited. March 2017") 2016 Annual Results Orient Overseas (International) Limited March 2017 Disclaimer The information provided is for reference only and includes data obtained from sources provided by the relevant information

2016 Annual Results Orient Overseas (International) Limited March 2017 Disclaimer The information provided is for reference only and includes data obtained from sources provided by the relevant information

What next for container shipping? Ng Yat Chung Group President & CEO 18 October 2012

What next for container shipping? Ng Yat Chung Group President & CEO 18 October 2012 Today s presentation Current reality Turning point in industry history Positioning for the future 1 Today s presentation

What next for container shipping? Ng Yat Chung Group President & CEO 18 October 2012 Today s presentation Current reality Turning point in industry history Positioning for the future 1 Today s presentation

Cool Logistics Asia. Lars Kastrup, Senior Vice President - Asia, CMA CGM September 2, 2015

Cool Logistics Asia Lars Kastrup, Senior Vice President - Asia, CMA CGM September 2, 2015 CMA CGM, a Leader in Container Shipping Led by its founder, Mr Jacques R. Saadé, CMA CGM is a leading worldwide

Cool Logistics Asia Lars Kastrup, Senior Vice President - Asia, CMA CGM September 2, 2015 CMA CGM, a Leader in Container Shipping Led by its founder, Mr Jacques R. Saadé, CMA CGM is a leading worldwide

Expectations for Port Customers and Clients. Dan Sheehy -NYK Line AAPA Meeting October 23, 2008

Expectations for Port Customers and Clients Dan Sheehy -NYK Line AAPA Meeting October 23, 2008 Areas for Review 1. Overview of NYK Line 2. Liner Trade Business 3. Demand versus Supply Outlook 4. Bunker

Expectations for Port Customers and Clients Dan Sheehy -NYK Line AAPA Meeting October 23, 2008 Areas for Review 1. Overview of NYK Line 2. Liner Trade Business 3. Demand versus Supply Outlook 4. Bunker

CONTAINER TRADE FLOWS AND TRADE LANE CHANGES

CONTAINER TRADE FLOWS AND TRADE LANE CHANGES International Trade Symposium Norfolk VA May 9, 2013 Today s Speaker Hayes H. Howard CEO, BlueWater Reporting 2 Agenda Introduction About BlueWater Reporting

CONTAINER TRADE FLOWS AND TRADE LANE CHANGES International Trade Symposium Norfolk VA May 9, 2013 Today s Speaker Hayes H. Howard CEO, BlueWater Reporting 2 Agenda Introduction About BlueWater Reporting

Urner Barry Conference, May 4, 2014 William C. Duggan, Jr, Maersk Line North American Refrigerated Services. By Land and By Sea: Today s.

Urner Barry Conference, May 4, 2014 William C. Duggan, Jr, Maersk Line North American Refrigerated Services By Land and By Sea: Today s Transportation Capacities, costs and coverage Agenda Key Messages

Urner Barry Conference, May 4, 2014 William C. Duggan, Jr, Maersk Line North American Refrigerated Services By Land and By Sea: Today s Transportation Capacities, costs and coverage Agenda Key Messages

Ocean Carrier Issues and Perspectives. Shifting International Trade Routes, January 23 rd

Ocean Carrier Issues and Perspectives Shifting International Trade Routes, January 23 rd page 2 Introduction Dean Rodin Managing Director Maersk Line Caribbean Sea Cluster Maersk Line at a glance 596 vessels

Ocean Carrier Issues and Perspectives Shifting International Trade Routes, January 23 rd page 2 Introduction Dean Rodin Managing Director Maersk Line Caribbean Sea Cluster Maersk Line at a glance 596 vessels

(America) LLC. The Impact of Super Container Ships & VSAs. Todd Rives SVP & CCO

LLC. The Impact of Super Container Ships & VSAs. Todd Rives SVP & CCO") (America) LLC The Impact of Super Container Ships & VSAs Todd Rives SVP & CCO CMA CGM GROUP Statistics CMA CGM 11.4m 18 000 Employees 650 430 400 TEUs carried in 2013 Offices Worldwide Operated vessel

(America) LLC The Impact of Super Container Ships & VSAs Todd Rives SVP & CCO CMA CGM GROUP Statistics CMA CGM 11.4m 18 000 Employees 650 430 400 TEUs carried in 2013 Offices Worldwide Operated vessel

Wan Hai Lines Q1 Update. Laura Su HSBC Taiwan Executive Forum May. 24, 2017

Wan Hai Lines 2017 Q1 Update Laura Su HSBC Taiwan Executive Forum May. 24, 2017 General Overview Global Service Network 86 Operated Vessels Total Capacity of 224,177 TEUs 3 Intra-Asia Services 28 Dedicated

Wan Hai Lines 2017 Q1 Update Laura Su HSBC Taiwan Executive Forum May. 24, 2017 General Overview Global Service Network 86 Operated Vessels Total Capacity of 224,177 TEUs 3 Intra-Asia Services 28 Dedicated

What Lies Ahead? David Arsenault Founder & President Logistics Transformation Solutions, LLC

What Lies Ahead? David Arsenault Founder & President Logistics Transformation Solutions, LLC June 7, 2017 1 Logistics Transformation Solutions, LLC Founded: October, 2016 Global Supply Chain & Maritime

What Lies Ahead? David Arsenault Founder & President Logistics Transformation Solutions, LLC June 7, 2017 1 Logistics Transformation Solutions, LLC Founded: October, 2016 Global Supply Chain & Maritime

Business Performance in FY2009 and Outlook for FY2010. Mitsui O.S.K. Lines, Ltd. April 2010

Business Performance in FY2009 and Outlook for FY2010 Mitsui O.S.K. Lines, Ltd. April 2010 HP Contents FY2009 Results [Consolidated] 2 Key Points of FY2009 Full-year Results [Consolidated] 4 Results Comparison

Business Performance in FY2009 and Outlook for FY2010 Mitsui O.S.K. Lines, Ltd. April 2010 HP Contents FY2009 Results [Consolidated] 2 Key Points of FY2009 Full-year Results [Consolidated] 4 Results Comparison

Transload Insights: Better Flexibility and Cost Savings

Transload Insights: Better Flexibility and Cost Savings John Paul Jimenez, The Home Depot Don Esterbrook, NorthWest Seaport Alliance Rob Brown, Union Pacific Don Esterbrook, The Northwest Seaport Alliance

Transload Insights: Better Flexibility and Cost Savings John Paul Jimenez, The Home Depot Don Esterbrook, NorthWest Seaport Alliance Rob Brown, Union Pacific Don Esterbrook, The Northwest Seaport Alliance

The Port of New York & New Jersey. A partnership between two states A premier gateway to the world

The Port of New York & New Jersey A partnership between two states A premier gateway to the world Presentation Overview A Gateway for Global Trade The Port s integral role in the world s trade network

The Port of New York & New Jersey A partnership between two states A premier gateway to the world Presentation Overview A Gateway for Global Trade The Port s integral role in the world s trade network

April 30, State of the Trade Carrier Perspective

April 30, 2013 State of the Trade Carrier Perspective World Trade Outlook From 1980 to 2013, world container traffic is expected to grow by 9.2% a year in average. But real GDP and Trade volume is expected

April 30, 2013 State of the Trade Carrier Perspective World Trade Outlook From 1980 to 2013, world container traffic is expected to grow by 9.2% a year in average. But real GDP and Trade volume is expected

Optimisation of Transport Costs: What is first, the market or infrastructure? XIX AAPA Latin American Congress of Ports Manta Ecuador

Optimisation of Transport Costs: What is first, the market or infrastructure? XIX AAPA Latin American Congress of Ports Manta Ecuador Summary Ports sector performance Evolving supply chain Regionalisation

Optimisation of Transport Costs: What is first, the market or infrastructure? XIX AAPA Latin American Congress of Ports Manta Ecuador Summary Ports sector performance Evolving supply chain Regionalisation

Meeting #2 August 3, :00-6:00 pm

Meeting #2 August 3, 2017 3:00-6:00 pm Welcome Michael Kosmala, Coraggio Group Committee Charge & Study Focus Charge: Provide industry knowledge and guidance to the Port of Portland leadership on the Port

Meeting #2 August 3, 2017 3:00-6:00 pm Welcome Michael Kosmala, Coraggio Group Committee Charge & Study Focus Charge: Provide industry knowledge and guidance to the Port of Portland leadership on the Port

Consolidation and the alliance shuffle: what could it mean for shippers

Consolidation and the alliance shuffle: what could it mean for shippers STEVE SAXON TPM ASIA, OCTOBER 2016 The voice of the shipper Service does not meet the defined transit standards This is a mess to

Consolidation and the alliance shuffle: what could it mean for shippers STEVE SAXON TPM ASIA, OCTOBER 2016 The voice of the shipper Service does not meet the defined transit standards This is a mess to

The Emergence of. Florida s Seaports and Inland Ports. Florida League of Cities - International Relations Committee November 17, 2011

The Emergence of Florida s Seaports and Inland Ports Florida League of Cities - International Relations Committee November 17, 2011 History of the Global Supply Chain 2 Supply Chain, Circa 1950 Regional

The Emergence of Florida s Seaports and Inland Ports Florida League of Cities - International Relations Committee November 17, 2011 History of the Global Supply Chain 2 Supply Chain, Circa 1950 Regional

84 th International Propeller Club Convention Fundamental Changes to a Traditional Transportation Paradigm. October 7, 2009

84 th International Propeller Club Convention Fundamental Changes to a Traditional Transportation Paradigm October 7, 2009 Today s Objectives Endeavor to provide a broad context for today s session by

84 th International Propeller Club Convention Fundamental Changes to a Traditional Transportation Paradigm October 7, 2009 Today s Objectives Endeavor to provide a broad context for today s session by

Container Shipping. Outlook and Issues for US East Coast Shippers and Ports. Tina Liu Country Manager, China. October 15, 2015 TPM Shenzhen

Container Shipping Outlook and Issues for US East Coast Shippers and Ports October 15, 2015 TPM Shenzhen Tina Liu Country Manager, China Agenda Container volume growth Mega-alliances Mega-ships Port diversification

Container Shipping Outlook and Issues for US East Coast Shippers and Ports October 15, 2015 TPM Shenzhen Tina Liu Country Manager, China Agenda Container volume growth Mega-alliances Mega-ships Port diversification

Ocean Market Update. February 9, 2012

Ocean Market Update February 9, 2012 Agenda 2012/2012 Market Trends Status of EB TP Capacity Changes In Alliances Conclusions Photo placeholder 2 Global box container trade growth 2011 (Oct YTD): 7.1%

Ocean Market Update February 9, 2012 Agenda 2012/2012 Market Trends Status of EB TP Capacity Changes In Alliances Conclusions Photo placeholder 2 Global box container trade growth 2011 (Oct YTD): 7.1%

Stock code:2615 WAN HAI LINES 2018 Q1. Tommy Hsieh/Laura Su May. 16, 2018

Stock code:2615 WAN HAI LINES 2018 Q1 Tommy Hsieh/Laura Su May. 16, 2018 Disclaimer Intra-Asia Services The information contained in this presentation and its accompanying announcements, including content

Stock code:2615 WAN HAI LINES 2018 Q1 Tommy Hsieh/Laura Su May. 16, 2018 Disclaimer Intra-Asia Services The information contained in this presentation and its accompanying announcements, including content

Volatility in Container Shipping

Volatility in Container Shipping TPM Asia 2013, Shenzhen Simon Heaney Research Manager Drewry Supply Chain Advisors 16-17 October 2013 2 Agenda 1. Volatility in container shipping s DNA 2. Recent container

Volatility in Container Shipping TPM Asia 2013, Shenzhen Simon Heaney Research Manager Drewry Supply Chain Advisors 16-17 October 2013 2 Agenda 1. Volatility in container shipping s DNA 2. Recent container

Providing Cost Effective, Reliable Services

Northwest Container Services NWCS 1 Northwest Container Services NWCS Providing Cost Effective, Reliable Services Northwest Container Services (NWCS) has been the Pacific Northwest s premier provider of

Northwest Container Services NWCS 1 Northwest Container Services NWCS Providing Cost Effective, Reliable Services Northwest Container Services (NWCS) has been the Pacific Northwest s premier provider of

APL UPDATE LONG BEACH MARCH 2019 APL UPDATE

LONG BEACH MARCH 2019 % YoY growth Trans-Pacific market expected to remain robust in 2019 Trans-Pacific Supply & Demand YoY% Growth 2018-2019 16% 14% 12% 10% 8% 6% 4% 2% 0% -2% -4% -6% Demand +6.0% Supply

LONG BEACH MARCH 2019 % YoY growth Trans-Pacific market expected to remain robust in 2019 Trans-Pacific Supply & Demand YoY% Growth 2018-2019 16% 14% 12% 10% 8% 6% 4% 2% 0% -2% -4% -6% Demand +6.0% Supply

Business Performance in FY2012-2nd Quarter. Mitsui O.S.K. Lines, Ltd. October 2012

Business Performance in -2nd Quarter Mitsui O.S.K. Lines, Ltd. October 2012 HP Contents 2nd Quarter s [Consolidated] 2 Outlines of 2nd Quarter s [Consolidated] 4 Forecast [Consolidated] 6 Key Points of

Business Performance in -2nd Quarter Mitsui O.S.K. Lines, Ltd. October 2012 HP Contents 2nd Quarter s [Consolidated] 2 Outlines of 2nd Quarter s [Consolidated] 4 Forecast [Consolidated] 6 Key Points of

Growth, Liner Consolidation and Impacts on Ports & Inland Connectivity. Jolke Helbing

Growth, Liner Consolidation and Impacts on Ports & Inland Connectivity Jolke Helbing Global Container Market - Historical Global containerised trade has been increasingly steadily, since the slowdown:

Growth, Liner Consolidation and Impacts on Ports & Inland Connectivity Jolke Helbing Global Container Market - Historical Global containerised trade has been increasingly steadily, since the slowdown:

International Union of Marine Insurance (IUMI) Conference Singapore

Conference Singapore") International Union of Marine Insurance (IUMI) Conference Singapore September 13, 2004 Address by NOL Group President and CEO, David Lim Growth, Interdependency and Convergence Challenges in the Container

International Union of Marine Insurance (IUMI) Conference Singapore September 13, 2004 Address by NOL Group President and CEO, David Lim Growth, Interdependency and Convergence Challenges in the Container

The global supply outlook

The global supply outlook Global Liner Shipping Conference 16 th May 217 - Hamburg Neil Dekker, Director - Container Research Drewry dekker@drewry.co.uk Agenda Global supply 217-2 Drewry forecast Scrapping

The global supply outlook Global Liner Shipping Conference 16 th May 217 - Hamburg Neil Dekker, Director - Container Research Drewry dekker@drewry.co.uk Agenda Global supply 217-2 Drewry forecast Scrapping

CARGO E-CHARTBOOK Q OVERVIEW

CARGO E-CHARTBOOK Q4 OVERVIEW Airline cargo businesses continue to face difficult conditions with demand for air freight falling in Q4, yields continuing to trend downward, and oil prices remaining high.

CARGO E-CHARTBOOK Q4 OVERVIEW Airline cargo businesses continue to face difficult conditions with demand for air freight falling in Q4, yields continuing to trend downward, and oil prices remaining high.

Shipping Market Outlook

Shipping Market Outlook Hamburg, 19 November 15 Slide 1 Market Environment Structural Trends of Global Dry Market North America Lower energy prices and higher consumer confidence will bode well for container

Shipping Market Outlook Hamburg, 19 November 15 Slide 1 Market Environment Structural Trends of Global Dry Market North America Lower energy prices and higher consumer confidence will bode well for container

THE POTENTIAL IMPACT OF A LEVY ON BUNKER FUELS ON DRY BULK SPOT FREIGHT RATES N.T. Chowdhury and J. Dinwoodie

THE POTENTIAL IMPACT OF A LEVY ON BUNKER FUELS ON DRY BULK SPOT FREIGHT RATES N.T. Chowdhury and J. Dinwoodie School of Management, University of Plymouth Business School, Plymouth, UK PL4 8AA ABSTRACT

THE POTENTIAL IMPACT OF A LEVY ON BUNKER FUELS ON DRY BULK SPOT FREIGHT RATES N.T. Chowdhury and J. Dinwoodie School of Management, University of Plymouth Business School, Plymouth, UK PL4 8AA ABSTRACT

Transportation: New challenges and rising costs

Transportation: New challenges and rising costs Han Ning, Director, Drewry China ning@drewry.co.uk RISI Asia Conference - Shenzhen 23 rd May 2017 Agenda New challenges Economy and trade New challenges

Transportation: New challenges and rising costs Han Ning, Director, Drewry China ning@drewry.co.uk RISI Asia Conference - Shenzhen 23 rd May 2017 Agenda New challenges Economy and trade New challenges

Robert MORRIS Georgia Ports Authority

The Harbor Boom: Meeting future Challenges Through Investment & Development Robert MORRIS Georgia Ports Authority Georgia Ports Authority Staying Ahead of the Curve Meeting Demands of Annual Double-Digit

The Harbor Boom: Meeting future Challenges Through Investment & Development Robert MORRIS Georgia Ports Authority Georgia Ports Authority Staying Ahead of the Curve Meeting Demands of Annual Double-Digit

LATC: Executive Series Old Country Ranch Club. January 9, 2018 BUSINESS UPDATE. Dr. Noel Hacegaba. Managing Director and. Chief Commercial Officer

LATC: Executive Series Old Country Ranch Club January 9, 2018 BUSINESS UPDATE Managing Director and Dr. Noel Hacegaba Chief Commercial Officer Agenda Business performance by line of business Industry updates

LATC: Executive Series Old Country Ranch Club January 9, 2018 BUSINESS UPDATE Managing Director and Dr. Noel Hacegaba Chief Commercial Officer Agenda Business performance by line of business Industry updates

Liner alliances: rationale ESPO Tim Power Director, Head of Maritime Advisors. 15 th May 2014

Liner alliances: rationale ESPO 2014 Tim Power Director, Head of Maritime Advisors 15 th May 2014 2 Contents 1. Liner fundamentals Liner economics and the cycle Historical market growth Historical supply

Liner alliances: rationale ESPO 2014 Tim Power Director, Head of Maritime Advisors 15 th May 2014 2 Contents 1. Liner fundamentals Liner economics and the cycle Historical market growth Historical supply

SHIPPING WATCH 2017 TOC AMSTERDAM JUNE Andrew Penfold. Director - Global Maritime

SHIPPING WATCH 2017 TOC AMSTERDAM JUNE 2017 Andrew Penfold Director - Global Maritime CONTENT 2 Overview shipping market developments Supply/demand balances Ship sizes and cascading Alliances terminal

SHIPPING WATCH 2017 TOC AMSTERDAM JUNE 2017 Andrew Penfold Director - Global Maritime CONTENT 2 Overview shipping market developments Supply/demand balances Ship sizes and cascading Alliances terminal

CARRIER STRATEGIES, COST vs VALUE & THE SUPPLY CHAIN IMPACT

CARRIER STRATEGIES, COST vs VALUE & THE SUPPLY CHAIN IMPACT June 9 th 2015 TOC Rotterdam Andrew Penfold Director Ocean Shipping Consultants Far-reaching changes are underway. What will be the supply/demand

CARRIER STRATEGIES, COST vs VALUE & THE SUPPLY CHAIN IMPACT June 9 th 2015 TOC Rotterdam Andrew Penfold Director Ocean Shipping Consultants Far-reaching changes are underway. What will be the supply/demand

PIANC. World Association for Waterborne Transport Infrastructure LOGISTICS AND TRANSPORT FLOWS IN THE MEDITERRANEAN SEA: CONSEQUENCES FOR PORTS

PIANC World Association for Waterborne Transport Infrastructure LOGISTICS AND TRANSPORT FLOWS IN THE MEDITERRANEAN SEA: CONSEQUENCES FOR PORTS Gerardo Landaluce Development & Commercial Director, Port

PIANC World Association for Waterborne Transport Infrastructure LOGISTICS AND TRANSPORT FLOWS IN THE MEDITERRANEAN SEA: CONSEQUENCES FOR PORTS Gerardo Landaluce Development & Commercial Director, Port

Competitive and Sustainable Port Management as the key to Competitiveness

Soc. Port. de Buenaventura Competitive and Sustainable Port Management as the key to Competitiveness 19 November 2018 Guatemala City, Guatemala Robert West Bob.West@Duaga.com +1 617 309 0521 27 Years of

Soc. Port. de Buenaventura Competitive and Sustainable Port Management as the key to Competitiveness 19 November 2018 Guatemala City, Guatemala Robert West Bob.West@Duaga.com +1 617 309 0521 27 Years of

CARGO E-CHARTBOOK Q OVERVIEW

CARGO E-CHARTBOOK Q OVERVIEW Airline cargo businesses are starting to see an improvement in forward looking demand indicators, but continued increases in capacity have placed downward pressure on yields

CARGO E-CHARTBOOK Q OVERVIEW Airline cargo businesses are starting to see an improvement in forward looking demand indicators, but continued increases in capacity have placed downward pressure on yields

Driving Our Ports Toward Greater Efficiency Gene Seroka, Executive Director Port of Los Angeles

Driving Our Ports Toward Greater Efficiency Gene Seroka, Executive Director Port of Los Angeles 27 th Annual Apparel Importers Trade and Transportation Conference November 4, 2015 Carrier Business is Stabilizing

Driving Our Ports Toward Greater Efficiency Gene Seroka, Executive Director Port of Los Angeles 27 th Annual Apparel Importers Trade and Transportation Conference November 4, 2015 Carrier Business is Stabilizing

Freight Transportation Megatrends

Freight Transportation Megatrends Copyright 2006 Global Insight, Inc. Freight Demand Modeling: Tools for Public-Sector Decision Making Conference Paul Bingham Global Insight, Inc. Washington, DC September

Freight Transportation Megatrends Copyright 2006 Global Insight, Inc. Freight Demand Modeling: Tools for Public-Sector Decision Making Conference Paul Bingham Global Insight, Inc. Washington, DC September

Outlook for Shipping and Freight Costs

Outlook for Shipping and Freight Costs Martin Dixon, Director - Head of Research Products dixon@drewry.co.uk RISI PPI Transport Symposium 22, Savannah September 25-27, 2017 Agenda Developments in world

Outlook for Shipping and Freight Costs Martin Dixon, Director - Head of Research Products dixon@drewry.co.uk RISI PPI Transport Symposium 22, Savannah September 25-27, 2017 Agenda Developments in world

Evergreen Marine Corp Investor Conference

TSE: 2603 Evergreen Marine Corp. 2018 Investor Conference Challenge Innovation Teamwork Legal Disclaimer The information contained in this presentation, including all forward-looking information, is subject

TSE: 2603 Evergreen Marine Corp. 2018 Investor Conference Challenge Innovation Teamwork Legal Disclaimer The information contained in this presentation, including all forward-looking information, is subject

The outlook for port development in the Mediterranean Meda Ports & Shipping Summit

The outlook for port development in the Mediterranean Meda Ports & Shipping Summit The role of Mediterranean ports in a sustainable and more efficient logistics MTEU 30 25 20 15 10 5 Evolution of major

The outlook for port development in the Mediterranean Meda Ports & Shipping Summit The role of Mediterranean ports in a sustainable and more efficient logistics MTEU 30 25 20 15 10 5 Evolution of major

Greening Supply Chains TPM Nate Springer, BSR Blair Chikasuye, HP Sarah Flagg, DAMCO Lee Kindberg, Maersk

Greening Supply Chains TPM 2015 Nate Springer, BSR Blair Chikasuye, HP Sarah Flagg, DAMCO Lee Kindberg, Maersk BSR (Business for Social Responsibility) A global nonprofit organization that works with its

Greening Supply Chains TPM 2015 Nate Springer, BSR Blair Chikasuye, HP Sarah Flagg, DAMCO Lee Kindberg, Maersk BSR (Business for Social Responsibility) A global nonprofit organization that works with its

Container Market Outlook

Container Market Outlook Alan Murphy CEO and Co-Founder SeaIntel Maritime Analysis October 12 th, 2016 TPM Asia 1 SeaIntel Container Shipping Analysts - Founded January 1 st, 2011 - Fully independent,

Container Market Outlook Alan Murphy CEO and Co-Founder SeaIntel Maritime Analysis October 12 th, 2016 TPM Asia 1 SeaIntel Container Shipping Analysts - Founded January 1 st, 2011 - Fully independent,

PORT OF SAVANNAH Garden City Terminal: The Southeast Gateway for the U.S. Presented to

PORT OF SAVANNAH Garden City Terminal: The Southeast Gateway for the U.S. Presented to June 6, 2017 Chatham ICTF served by CSX Transportation Mason ICTF served by Norfolk Southern Railroad GARDEN CITY

PORT OF SAVANNAH Garden City Terminal: The Southeast Gateway for the U.S. Presented to June 6, 2017 Chatham ICTF served by CSX Transportation Mason ICTF served by Norfolk Southern Railroad GARDEN CITY

Investor Presentation February 2018 Slide 1. Investor Presentation February 2018

Investor Presentation February 2018 Slide 1 Investor Presentation February 2018 Forward Looking Statements Statements made during this presentation that set forth expectations, predictions, projections

Investor Presentation February 2018 Slide 1 Investor Presentation February 2018 Forward Looking Statements Statements made during this presentation that set forth expectations, predictions, projections

CARGO E-CHARTBOOK Q OVERVIEW

CARGO E-CHARTBOOK Q OVERVIEW Airline cargo businesses are starting to see a slightly better demand environment and further improvement in forward looking indicators, but continued increases in capacity

CARGO E-CHARTBOOK Q OVERVIEW Airline cargo businesses are starting to see a slightly better demand environment and further improvement in forward looking indicators, but continued increases in capacity

PANAMA CANAL EXPANSION

noun 1. a purposeful or industrious undertaking (especially one that requires effort or boldness) 2. earnest and conscientious activity intended to do or accomplish something. PANAMA CANAL EXPANSION 1

noun 1. a purposeful or industrious undertaking (especially one that requires effort or boldness) 2. earnest and conscientious activity intended to do or accomplish something. PANAMA CANAL EXPANSION 1

North American Trade & Transportation Future Trends

2012 Port Finance Seminar Miami, Florida Session 8: Infrastructure Investment for the Future North American Trade & Transportation Future Trends Presented By M. John Vickerman Principal Williamsburg, Virginia

2012 Port Finance Seminar Miami, Florida Session 8: Infrastructure Investment for the Future North American Trade & Transportation Future Trends Presented By M. John Vickerman Principal Williamsburg, Virginia

DCT Gdansk Presentation January 2017

DCT Gdansk Presentation January 2017 2 Company Profile DCT Gdansk: Resources and Technical Specifications Terminal description: The largest and the fastest-growing container terminal in the Baltic Sea

DCT Gdansk Presentation January 2017 2 Company Profile DCT Gdansk: Resources and Technical Specifications Terminal description: The largest and the fastest-growing container terminal in the Baltic Sea

CANADA S GATEWAYS: SUPPLY CHAIN PERFORMANCE MONITORING INITIATIVES. Leipzig, May 2, 2012

CANADA S GATEWAYS: SUPPLY CHAIN PERFORMANCE MONITORING INITIATIVES Leipzig, May 2, 2012 1 Canada s Gateways and Trade Corridors: System-wide Approach Need objective fact-based metrics to: Asia-Pacific

CANADA S GATEWAYS: SUPPLY CHAIN PERFORMANCE MONITORING INITIATIVES Leipzig, May 2, 2012 1 Canada s Gateways and Trade Corridors: System-wide Approach Need objective fact-based metrics to: Asia-Pacific

ASPECTS REGARDING WORLD ECONOMIC CRISIS IMPACT ON MARITIME TRANSPORT AND CONTAINER TERMINALS

ASPECTS REGARDING WORLD ECONOMIC CRISIS IMPACT ON MARITIME TRANSPORT AND CONTAINER TERMINALS Violeta POPESCU 1 Hazel MENADIL 2 1 Ph. D. Assoc. Prof., Ovidius University of Constantza, Romania 2 Lecturer,

ASPECTS REGARDING WORLD ECONOMIC CRISIS IMPACT ON MARITIME TRANSPORT AND CONTAINER TERMINALS Violeta POPESCU 1 Hazel MENADIL 2 1 Ph. D. Assoc. Prof., Ovidius University of Constantza, Romania 2 Lecturer,

Shipping. Neutral. Sector Note. Reorganization around Maersk and allies

Sector Note June 27, 2013 Shipping Neutral Reorganization around Maersk and allies Nutcracker situation intensifying Booz Allen and Hamilton Consulting used the term nutcracker to describe Korea in 1997

Sector Note June 27, 2013 Shipping Neutral Reorganization around Maersk and allies Nutcracker situation intensifying Booz Allen and Hamilton Consulting used the term nutcracker to describe Korea in 1997

Trade Update & Opportunity Outlook. Gene Seroka Executive Director, Port of Los Angeles May 19, 2017

Trade Update & Opportunity Outlook Gene Seroka Executive Director, Port of Los Angeles May 19, 2017 2016 Re-Cap By Lines of Business -.5% +21% +8.5% Liquid Bulk (Petroleum) 93,223,412 barrels Autos (WWL)

Trade Update & Opportunity Outlook Gene Seroka Executive Director, Port of Los Angeles May 19, 2017 2016 Re-Cap By Lines of Business -.5% +21% +8.5% Liquid Bulk (Petroleum) 93,223,412 barrels Autos (WWL)

Seaport Group. West Coast Container Traffic Trends. February West Coast Container Volumes 2010

West Coast Container Traffic Trends Seaport Group February 2011 For further information and comments, please contact Terence Smyth on +1 604 732 8255 or tsmyth@seaport.com. This bulletin deals primarily

West Coast Container Traffic Trends Seaport Group February 2011 For further information and comments, please contact Terence Smyth on +1 604 732 8255 or tsmyth@seaport.com. This bulletin deals primarily

Perfect Storm to Calmer Seas, The Timeline for Global Shipping Recovery

Perfect Storm to Calmer Seas, The Timeline for Global Shipping Recovery A Joint Webcast from IHS Global Insight and Lloyd s Register-Fairplay Research Introducing the IHS Global Insight and Lloyd s Register-Fairplay

Perfect Storm to Calmer Seas, The Timeline for Global Shipping Recovery A Joint Webcast from IHS Global Insight and Lloyd s Register-Fairplay Research Introducing the IHS Global Insight and Lloyd s Register-Fairplay

Economic Outlook & Traffic Performance

CARGO CHARTBOOK Key points After a very volatile first quarter, so far in Q2 air cargo markets appear to be back down to end-2014 levels 2015 Q2 2014 was a comeback year for air cargo, freight tonnes carried

CARGO CHARTBOOK Key points After a very volatile first quarter, so far in Q2 air cargo markets appear to be back down to end-2014 levels 2015 Q2 2014 was a comeback year for air cargo, freight tonnes carried

NUTC BAC PANEL. May

NUTC BAC PANEL May 4 2017 Containership Industry Environment Where we are today Years of overbuilding and reduced trade growth have resulted in chronic global overcapacity Rates are not renumerative with

NUTC BAC PANEL May 4 2017 Containership Industry Environment Where we are today Years of overbuilding and reduced trade growth have resulted in chronic global overcapacity Rates are not renumerative with

Global Supply Chain Management: Seattle-Tacoma

Boston Strategies International, Inc. February 2008 Global Infrastructure Series Global Supply Chain Management: Seattle-Tacoma www.bostonstrategies.com b t t t i (1) (781) 250 8150 Page 1 This report

Boston Strategies International, Inc. February 2008 Global Infrastructure Series Global Supply Chain Management: Seattle-Tacoma www.bostonstrategies.com b t t t i (1) (781) 250 8150 Page 1 This report

GRINDROD LIMITED ADDITIONAL INFORMATION FOR ANALYSTS for the year ended 31 December 2016

www.grindrod.com GRINDROD LIMITED ADDITIONAL INFORMATION FOR ANALYSTS for the year ended 31 December 2016 MANAGEMENT SEGMENTAL BALANCE SHEETS AS AT 31 DECEMBER 2016 R000 FREIGHT SERVICES SHIPPING FINANCIAL

www.grindrod.com GRINDROD LIMITED ADDITIONAL INFORMATION FOR ANALYSTS for the year ended 31 December 2016 MANAGEMENT SEGMENTAL BALANCE SHEETS AS AT 31 DECEMBER 2016 R000 FREIGHT SERVICES SHIPPING FINANCIAL

Turbulent Waters for Ocean Carriers and Ports. Doug Hansen NYKP, LLC/Ceres Terminals Inc. 2 February 2017 Tampa, Florida

Turbulent Waters for Ocean Carriers and Ports Doug Hansen NYKP, LLC/Ceres Terminals Inc. 2 February 2017 Tampa, Florida 1 NYK Ports, LLC Who we are. Vancouver Duluth Montreal Halifax Stockton Oakland Port

Turbulent Waters for Ocean Carriers and Ports Doug Hansen NYKP, LLC/Ceres Terminals Inc. 2 February 2017 Tampa, Florida 1 NYK Ports, LLC Who we are. Vancouver Duluth Montreal Halifax Stockton Oakland Port

USWC Port Congestion & ILWU/PMA Contract Update. Last update: November 12, 2014

USWC Port Congestion & ILWU/PMA Contract Update Last update: November 12, 2014 ILWU / PMA CONTRACT UPDATE July 1 st : ILWU / PMA the 6 year contract expired without new contract in place Both parties agree

USWC Port Congestion & ILWU/PMA Contract Update Last update: November 12, 2014 ILWU / PMA CONTRACT UPDATE July 1 st : ILWU / PMA the 6 year contract expired without new contract in place Both parties agree

TRB - Annual Meeting

TRB - Annual Meeting NATIONAL DREDGING NEEDS STUDY PHILLIP J. THORPE Institute for Water Resources 16 January 2002 AGENDA Background Information Historical Perspective Global and US Trade World and US

TRB - Annual Meeting NATIONAL DREDGING NEEDS STUDY PHILLIP J. THORPE Institute for Water Resources 16 January 2002 AGENDA Background Information Historical Perspective Global and US Trade World and US

Drewry Dry Bulk shipping market. Drewry 2013

1 1 Dry bulk shipping: are we at the end of the tunnel? Mare Forum, Istanbul Lisarain Yu Jiang Senior Consultant Drewry Maritime Advisors 21 March 213, Istanbul Barometer of dry bulk shipping market All

1 1 Dry bulk shipping: are we at the end of the tunnel? Mare Forum, Istanbul Lisarain Yu Jiang Senior Consultant Drewry Maritime Advisors 21 March 213, Istanbul Barometer of dry bulk shipping market All

CARGO E-CHARTBOOK Q3 2011

CARGO E-CHARTBOOK Q3 211 OVERVIEW The past quarter has seen cargo markets deteriorate significantly. Having been flat for more than a year cargo volumes began to decline from July. Cargo rates are also

CARGO E-CHARTBOOK Q3 211 OVERVIEW The past quarter has seen cargo markets deteriorate significantly. Having been flat for more than a year cargo volumes began to decline from July. Cargo rates are also

Discussion of Report: Container Use in Western Canada: Inland Terminals,, Container Utilization, Service and Regulatory Issues

Discussion of Report: Container Use in Western Canada: Inland Terminals,, Container Utilization, Service and Regulatory Issues WESTAC, Victoria April 30, 2008 Study Parameters Study initiated in April

Discussion of Report: Container Use in Western Canada: Inland Terminals,, Container Utilization, Service and Regulatory Issues WESTAC, Victoria April 30, 2008 Study Parameters Study initiated in April

Challenges with Evaluating Container Port Projects and the Corps of Engineers

Challenges with Evaluating Container Port Projects and the Corps of Engineers Smart Rivers Conference 14 September 2011 Kevin Knight Economist Institute for Water Resources U.S. Corps of Engineers 1 Trends

Challenges with Evaluating Container Port Projects and the Corps of Engineers Smart Rivers Conference 14 September 2011 Kevin Knight Economist Institute for Water Resources U.S. Corps of Engineers 1 Trends

MMC s PORT CONSOLIDATION INITIATIVE Migration of Johor Port s Containers to PTP

MMC s PORT CONSOLIDATION INITIATIVE Migration of Johor Port s Containers to PTP Ports in Johor Are Losing Their Competitiveness to Singapore Ports in Singapore Unethical And Anti Competition Actions Johor

MMC s PORT CONSOLIDATION INITIATIVE Migration of Johor Port s Containers to PTP Ports in Johor Are Losing Their Competitiveness to Singapore Ports in Singapore Unethical And Anti Competition Actions Johor

Grindrod Limited Additional information for analysts

www.grindrod.com Grindrod Limited Additional information for analysts for the year ended 31 December 2017 MANAGEMENT SEGMENTAL BALANCE SHEETS AS AT 31 DECEMBER 2017 R000 PORTS TERMINALS MARINE FUELS AGRICULTURAL

www.grindrod.com Grindrod Limited Additional information for analysts for the year ended 31 December 2017 MANAGEMENT SEGMENTAL BALANCE SHEETS AS AT 31 DECEMBER 2017 R000 PORTS TERMINALS MARINE FUELS AGRICULTURAL

Cool Logistics Asia. September 2017 RAUL SACA

1 Cool Logistics Asia September 2017 RAUL SACA 2 Agenda Fruit trades, Volumes and trends. Reefer Container Perishable Shipping. Trends and Developments affecting Fruit trades. Digitization of the industry.

1 Cool Logistics Asia September 2017 RAUL SACA 2 Agenda Fruit trades, Volumes and trends. Reefer Container Perishable Shipping. Trends and Developments affecting Fruit trades. Digitization of the industry.

Enhancing and Expanding Containerized Commodity Movements. Libby Ogard Prime Focus LLC June 13, 2013

Enhancing and Expanding Containerized Commodity Movements Libby Ogard Prime Focus LLC June 13, 2013 An Empty Box is a Terrible Thing to Waste! 20% of all ocean containers are repositioned empty Stakeholders

Enhancing and Expanding Containerized Commodity Movements Libby Ogard Prime Focus LLC June 13, 2013 An Empty Box is a Terrible Thing to Waste! 20% of all ocean containers are repositioned empty Stakeholders

LNG Shipping: How Long Will The Good Times Last?

LNG Shipping: How Long Will The Good Times Last? Poten & Partners November 1 HOUSTON NEW YORK LONDON ATHENS SINGAPORE GUANGZHOU PERTH A GLOBAL BROKER AND COMMERCIAL ADVISOR FOR THE ENERGY AND OCEAN TRANSPORTATION

LNG Shipping: How Long Will The Good Times Last? Poten & Partners November 1 HOUSTON NEW YORK LONDON ATHENS SINGAPORE GUANGZHOU PERTH A GLOBAL BROKER AND COMMERCIAL ADVISOR FOR THE ENERGY AND OCEAN TRANSPORTATION

HAMBURGER HAFEN UND LOGISTIK AG COMPANY PRESENTATION

HAMBURGER HAFEN UND LOGISTIK AG COMPANY PRESENTATION CHEUVREUX GERMAN CORPORATE CONFERENCE FRANKFURT, JANUARY 2011 Hamburger Hafen und Logistik AG DISCLAIMER The facts and information contained herein

HAMBURGER HAFEN UND LOGISTIK AG COMPANY PRESENTATION CHEUVREUX GERMAN CORPORATE CONFERENCE FRANKFURT, JANUARY 2011 Hamburger Hafen und Logistik AG DISCLAIMER The facts and information contained herein

GLOBAL AND DOMESTIC OUTLOOKS

A A PA A n n u a l C o n f e r e n c e O c t o b e r 2 5, 2 016 GLOBAL AND DOMESTIC OUTLOOKS The supply chains are changing sometimes radically How are industr y and governments adapting? P i e r c e H

A A PA A n n u a l C o n f e r e n c e O c t o b e r 2 5, 2 016 GLOBAL AND DOMESTIC OUTLOOKS The supply chains are changing sometimes radically How are industr y and governments adapting? P i e r c e H

What Investors Want to Know: Container Shipping Chartbook

What Investors Want to Know: Container Shipping Chartbook Angelina Valavina, Senior Director EMEA Utilities & Transport June 2017 Contents 1 Recovery Depends on Market Discipline 2 2 Cost Cutting Still

What Investors Want to Know: Container Shipping Chartbook Angelina Valavina, Senior Director EMEA Utilities & Transport June 2017 Contents 1 Recovery Depends on Market Discipline 2 2 Cost Cutting Still

TANKER MARKET INSIGHT

TANKER MARKET INSIGHT October 18 Research Department, Teekay Tankers Sep-17 Oct-17 Nov-17 Jan-18 Feb-18 Apr-18 May-18 Jul-18 Aug-18 Sep-17 Oct-17 Nov-17 Jan-18 Feb-18 Apr-18 May-18 Jul-18 Aug-18 $ 000s

TANKER MARKET INSIGHT October 18 Research Department, Teekay Tankers Sep-17 Oct-17 Nov-17 Jan-18 Feb-18 Apr-18 May-18 Jul-18 Aug-18 Sep-17 Oct-17 Nov-17 Jan-18 Feb-18 Apr-18 May-18 Jul-18 Aug-18 $ 000s

Measuring Supply Chain Performance A Government Perspective. APCGI Workshop Toronto June 18, 2010

Measuring Supply Chain Performance A Government Perspective APCGI Workshop Toronto June 18, 2010 1 Agenda Why should governments measure supply chain performance? 1. Policy Context 2. Supply Chain Metrics

Measuring Supply Chain Performance A Government Perspective APCGI Workshop Toronto June 18, 2010 1 Agenda Why should governments measure supply chain performance? 1. Policy Context 2. Supply Chain Metrics

The profit maximizing liner shipping problem with flexible frequencies: logistical and environmental considerations

The profit maximizing liner shipping problem with flexible frequencies: logistical and environmental considerations Harilaos N. Psaraftis Technical University of Denmark Main reference 2 DTU Management

The profit maximizing liner shipping problem with flexible frequencies: logistical and environmental considerations Harilaos N. Psaraftis Technical University of Denmark Main reference 2 DTU Management

THE NEW PANAMA CANAL IN A GLOBAL CONTEXT

San Jose State University SJSU ScholarWorks Faculty Publications School of Management 6-11-2015 THE NEW PANAMA CANAL IN A GLOBAL CONTEXT Herman L. Boschken San Jose State University, herman.boschken@sjsu.edu

San Jose State University SJSU ScholarWorks Faculty Publications School of Management 6-11-2015 THE NEW PANAMA CANAL IN A GLOBAL CONTEXT Herman L. Boschken San Jose State University, herman.boschken@sjsu.edu

Shanghai (Export) Container Shipping Capacity Trading Contract

Container Shipping Capacity Trading Contract") Shanghai (Export) Container Shipping Capacity Trading Contract (Prepared in February 2014, Amended in October 2014) Trading Symbol UW Subject Matter of Contract Export container capacity for the Shanghai

Shanghai (Export) Container Shipping Capacity Trading Contract (Prepared in February 2014, Amended in October 2014) Trading Symbol UW Subject Matter of Contract Export container capacity for the Shanghai

Panama Canal Impact on the Liner Container Shipping Industry and the Transshipment Activity in the Republic of Panama

Transportation Research Forum Panama Canal Impact on the Liner Container Shipping Industry and the Transshipment Activity in the Republic of Panama Dr. Anatoly Hochstein National Ports & Waterways Institute

Transportation Research Forum Panama Canal Impact on the Liner Container Shipping Industry and the Transshipment Activity in the Republic of Panama Dr. Anatoly Hochstein National Ports & Waterways Institute

Quadra Commodities. Anthony Diamante Director and Chartering Manager

Quadra Commodities Anthony Diamante Director and Chartering Manager Trends in the Dry Bulk Ocean freight market and freight market outlook IAOM Capetown December 2014 1 2014 in review weaker than expected

Quadra Commodities Anthony Diamante Director and Chartering Manager Trends in the Dry Bulk Ocean freight market and freight market outlook IAOM Capetown December 2014 1 2014 in review weaker than expected

Oppenheimer Industrial Growth Conference. May 8, 2018

Oppenheimer Industrial Growth Conference May 8, 2018 1 Oppenheimer Industrial Growth Conference May 8, 2018 Forward-Looking Statements Statements made during this presentation that set forth expectations,

Oppenheimer Industrial Growth Conference May 8, 2018 1 Oppenheimer Industrial Growth Conference May 8, 2018 Forward-Looking Statements Statements made during this presentation that set forth expectations,

BNSF Railway. Moving you Forward

BNSF Railway Moving you Forward Northwestern University Transportation Center April 15, 2010 All slides are copyright 2010, BNSF Railway Company, All Rights Reserved. No part of this publication may be

BNSF Railway Moving you Forward Northwestern University Transportation Center April 15, 2010 All slides are copyright 2010, BNSF Railway Company, All Rights Reserved. No part of this publication may be

A Vision to the Future of Collaboration: Introducing XVELA

INSERT PARTNER LOGO Robert Inchausti, CTO & Christopher Mazza, CCO CONNECT. COLLABORATE. INNOVATE. A Vision to the Future of Collaboration: Introducing XVELA 2014 F1 Champion Louis Hamilton It isn t simply

INSERT PARTNER LOGO Robert Inchausti, CTO & Christopher Mazza, CCO CONNECT. COLLABORATE. INNOVATE. A Vision to the Future of Collaboration: Introducing XVELA 2014 F1 Champion Louis Hamilton It isn t simply

TPM Asia Shenzhen Oct 2012

Intermodal Rail : Finally an Opportunity for South China Shippers? TPM Asia Shenzhen 17-18 Oct 2012 Speaker : Sunny Ho Executive Director The Hong Kong Shippers Council Shippers are getting more and more

Intermodal Rail : Finally an Opportunity for South China Shippers? TPM Asia Shenzhen 17-18 Oct 2012 Speaker : Sunny Ho Executive Director The Hong Kong Shippers Council Shippers are getting more and more

THE DYNAMICS OF THE US CONTAINER MARKET AND IMPLICATIONS FOR THE US PORT INDUSTRY

THE DYNAMICS OF THE US CONTAINER MARKET AND IMPLICATIONS FOR THE US PORT INDUSTRY A PRESENTATION TO: CHANGING TRADE PATTERNS JANUARY 24, 2013 MARTIN ASSOCIATES 941 Wheatland Avenue, Suite 203 Lancaster,

THE DYNAMICS OF THE US CONTAINER MARKET AND IMPLICATIONS FOR THE US PORT INDUSTRY A PRESENTATION TO: CHANGING TRADE PATTERNS JANUARY 24, 2013 MARTIN ASSOCIATES 941 Wheatland Avenue, Suite 203 Lancaster,

Investor Presentation November 2017 Slide 1. Investor Presentation November 2017

Investor Presentation November 2017 Slide 1 Investor Presentation November 2017 Forward Looking Statements Statements made during this presentation that set forth expectations, predictions, projections

Investor Presentation November 2017 Slide 1 Investor Presentation November 2017 Forward Looking Statements Statements made during this presentation that set forth expectations, predictions, projections

AAPA Training Session An Intermodal Perspective

AAPA Training Session An Intermodal Perspective Theodore Prince 23 October 2008 Baltimore, MD 1 Introduction Overview of the shipping industry Dates back to the Phoenicians (or before) Uniform processes

AAPA Training Session An Intermodal Perspective Theodore Prince 23 October 2008 Baltimore, MD 1 Introduction Overview of the shipping industry Dates back to the Phoenicians (or before) Uniform processes

The Suez Canal and the Changing Face of Middle East Logistics. 3 rd Trans Middle East Conference Cairo, Egypt November 2007

The Suez Canal and the Changing Face of Middle East Logistics 3 rd Trans Middle East Conference Cairo, Egypt November 2007 Who We Are PRELIMINARY Supply Chain Research Supply Market Forecasts Supply Chain

The Suez Canal and the Changing Face of Middle East Logistics 3 rd Trans Middle East Conference Cairo, Egypt November 2007 Who We Are PRELIMINARY Supply Chain Research Supply Market Forecasts Supply Chain