Provided by Academy of Professional Accounting (APA)

|

|

|

- Hilary Austin

- 5 years ago

- Views:

Transcription

1 Professional Accounting Education Provided by Academy of Professional Accounting (APA) CMA Part I Section A External Financial Reporting Decisions CMA Lecturer: Eric HU ACCAspace 中国 ACCA 特许公认会计师教育平台 Copyright ACCAspace.com

2 Section A External Financial Reporting Decisions Unit 1:Definition and Objectives Unit 2:Users of Financial Statements External Users Internal Users Chapter 1:Concepts of Financial Reporting Unit 1:Balance Sheet Items Accounts Receivable Inventory Investments Property Plant Equipment Intangible Assets Liabilities Equity(Ref. Financial Statements) Unit 3:Accrual Basis of Accounting Section A:External Financial Reporting Decisions Unit 4:Financial Statements Balance Sheet Income Statement Statement of Cash Flows Statement of Changes in Equity Notes to Financial Statements Relationships among them Chapter 2:Recognition, Valuation and Disclosure Unit 2:Income Statement Items Revenue Recognition Income Measurement Unit 3:Specific Items 2

3 (1) Definition (2) Classification of Inventory (3) Cost basis of inventory (4) Inventory Accounting System (5) Inventory Errors (6) Inventory flow method (7) Inventory Measurement at the end of the year 3

4 (1)Definition:tangible assets 1 To be used up currently for sale 2 In the form of work-in-process to be completed and sold 3 Held for sale in the ordinary course of business (2)Classification of Inventory 1 Raw material 2 Work-in-process product 3 Finished goods / purchased goods(for retailer) 4

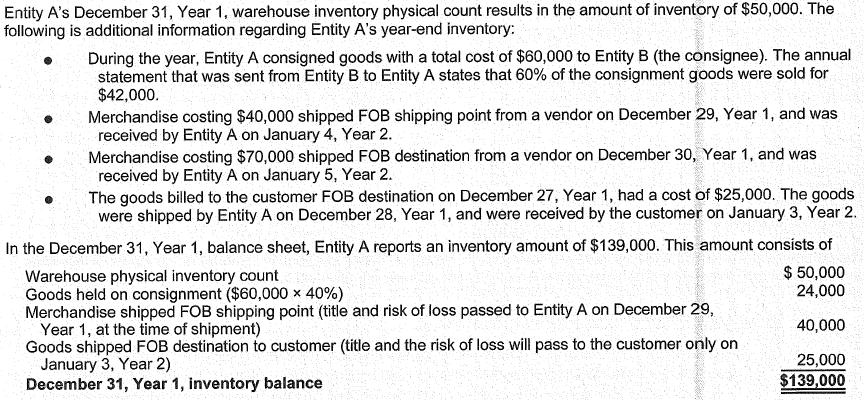

5 (3)Cost basis of Inventory:all costs incurred in bringing inventories to their existing location and ready-to-use condition Purchased inventories:price paid, import duties, other unrecoverable taxes, handling, insurance, freight-in, and other costs directly incurred. Manufactured inventories:direct materials, direct labor costs, manufacturing overhead costs Special inventories:goods out on consignment Goods in transit(fob Shipping point & destination) 5

6 6

7 (4)Inventory Accounting System Beginning Inventory + Purchased - Sold(COGS) =Ending Inventory 1 Perpetual inventory system:updates inventory constantly Beginning Inventory + Purchased - Sold(COGS) =Ending Inventory 1 Periodic inventory system:updates at specific intervals(based on physical count) Beginning Inventory + Purchased - Ending Inventory =Sold(COGS) 7

8 (4)Inventory Accounting System 8

9 (4)Inventory Accounting System 9

10 (5)Inventory Errors 1 Record>Actual,inventory overstated Record<Actual,inventory understated Record=Actual,inventory appropriated 2 Inventory COGS Net Income Retained Earnings on the Balance Sheet on the Income Statement on the Income Statement on the Balance Sheet 10

11 (5)Inventory Errors 11

12 (6)Inventory Flow Methods:accurate but not cost effective 1 Specific Identification Method Purchased:Inventory A1 100,@5 Inventory A2 50,@4 Sold: Inventory A1 30,@5 COGS=30*5+20*4=230 Inventory A2 20,@4 12

13 (6)Inventory Flow Methods: 2 Average Method:perpetual basis Moving-average method 13

14 (6)Inventory Flow Methods: 2 Average Method:perpetual basis Weighted-average method Cost per unit=(100*20+20*32+30*14)/( )=20.40 COGS = Beginning Inventory + Purchased - Ending Inventory =100*20 + (20*32+30*14) - 40*20.40=110*20.4=

15 (6)Inventory Flow Methods: 3 First in, First out Method(FIFO):Sales related April 1: Cost per unit=20,cogs=70*20=1400 October1:Cost per unit=20&32,cogs=30*20+10*32=920 Total COGS= =2320,EI=10*32+30*14=740 15

16 (6)Inventory Flow Methods: 4 Last in, First out Method(LIFO):Prohibited and out of date April 1: Cost per unit=32&20,cogs=20*32+50*20=1640 October1:Cost per unit=14&20,cogs=30*14+10*20=620 Total COGS= =2260,EI=( )*20=800 16

17 (7)Inventory Measurement at the end of the year 1 Lower of cost or market(lcm) Difference(write down) is a loss and prohibited to be reversed later. 2 Market value:identity the scope and compare Ceiling:NRV=estimated selling price-cost of completion-cost of disposal Floor:NRV-normal profit margin CRC:Current replacement cost 17

18 (7)Inventory Measurement at the end of the year 2 Market value:identity the scope and compare CRC2 Market Value is ceiling. Ceiling CRC1 Market Value is CRC1. Floor CRC3 Market Value is floor. 18

19 (7)Inventory Measurement at the end of the year 2 Market value:identity the scope and compare 19

20 (1) Definition (2) Classification of Inventory (3) Cost basis of inventory (4) Inventory Accounting System (5) Inventory Errors (6) Inventory flow method (7) Inventory Measurement at the end of the year 20

21 Professional Accounting Education Provided by Academy of Professional Accounting (APA)