Chapter 6 Prices and Decision Making

|

|

|

- Elfreda Reynolds

- 5 years ago

- Views:

Transcription

1 Chapter 6 Prices and Decision Making CHAPTER INTRODUCTION SECTION 1 SECTION 2 SECTION 3 Prices as Signals The Price System at Work Social Goals vs. Market Efficiency CHAPTER SUMMARY CHAPTER ASSESSMENT 3 Click a hyperlink to go to the corresponding section. Press the ESC key at any time to exit the presentation.

2 Economics and You What factors do you consider when you need to make a decision to buy something? Price may be one of the most important factors of all. In this chapter, you will learn how price serves as a signal to both buyers and sellers. Click the Speaker button to listen to Economics and You. 4 Chapter Objectives Section 1: Prices as Signals Explain how prices act as signals. Describe the advantages of using prices as a way to allocate economic products. Understand the difficulty of allocating scarce goods and services without using prices. 5

3 Chapter Objectives Section 2: The Price System at Work Understand how prices are determined in competitive markets. Explain how economic models can be used to predict and explain price changes. Apply the concepts of elasticity to changes in prices. 6 Chapter Objectives Section 3: Social Goals vs. Market Efficiency Describe the consequence of having a fixed price in a market. Explain how loan supports and deficiency payments work. Understand what is meant when markets talk. 7

4 Click the mouse button to return to the Contents slide. Study Guide Main Idea Competitive markets and prices are important to capitalism. Reading Strategy Graphic Organizer As you read the section, complete a graphic organizer similar to the one on page 137 of your textbook by providing examples from your own experience that show how the price system provides for freedom of choice. 9 to display the information. Section 1 begins on page 137 of your textbook.

5 Study Guide (cont.) Key Terms price rationing ration coupon rebate Objectives After studying this section, you will be able to: Explain how prices act as signals. Describe the advantages of using prices as a way to allocate economic products. Understand the difficulty of allocating scarce goods and services without using prices. 10 to display the information. Section 1 begins on page 137 of your textbook. Study Guide (cont.) Applying Economic Concepts Rationing Have you and your friends ever tried to share something a candy bar, cake, or pizza when there really wasn t enough to go around? What are different ways to make allocations? Click the Speaker button to listen to the Cover Story. 11 Section 1 begins on page 137 of your textbook.

6 Introduction Life is full of signals that help us make decisions. For example, when we pull up to an intersection, we look to see if the traffic light is green, yellow, or red. We look at the other cars to see if any have their blinkers on, and in this way we receive signals from other drivers regarding their intentions to turn. 12 Introduction (cont.) Doctors even tell us that pain is a signal that something is wrong with our body and may need attention. But have you ever thought about the signals that help us make our everyday economic decisions? It turns out something as simple as a price the monetary value of a product as established by supply and demand is a signal that helps us make our economic decisions. 13

7 Introduction (cont.) Prices communicate information and provide incentives to buyers and sellers. High prices are signals for producers to produce more and for buyers to buy less. Low prices are signals for producers to produce less and for buyers to buy more. 14 Did You Know? During the oil crisis in the early 1970s, the proposed gas rationing program raised serious differences of opinion among Americans. Some people argued that every adult American should get the same number of gas rationing coupons. Others argued that owners of newer, more fuelefficient cars would not need as many coupons as owners of older, gas-guzzling models. 15

8 16 Did You Know? Those who lived in western states believed they should receive more coupons than Easterners because they traveled longer distances. Some people called for every car owner to receive a certain number of coupons; others said this plan discriminated against families with several drivers who shared one car. 17

9 Advantages of Prices Prices are neutral because they do not favor the buyer or the consumer. They are the result of competition. Prices are flexible, allowing for the shocks of unforeseen events and changes in the market. Prices have no administration costs. Prices are familiar and easily understood. 18 Discussion Question In your opinion, why does the neutrality of prices stimulate competition? Students answers will vary but should indicate an understanding that buyers pay the price because they choose to accept it; otherwise, they would go to another producer with a lower price and buy there. 19

10 Allocations Without Prices Rationing, or the system where the government decides everyone s fair share, leads to the question of fairness. Rationing leads to high administrative costs. Rationing leads to fewer incentives to work and produce. 20 Discussion Question Imagine that no matter how much you studied, you already knew you were going to get a B in Economics. How would this affect your incentive to study? Students should indicate that in school, the grade is often the incentive; therefore, knowing the grade beforehand could be detrimental to the student. 21

11 Prices as a System Together, prices comprise a system that helps buyers and sellers allocate resources between markets, linking all markets in the economy. 22 Discussion Question Why do you think rebates were not enough to reenergize the big-car market during the 1970s energy crisis? Students should indicate that the rebates did not solve the problems of getting and paying for the additional gasoline the larger cars required. In addition, the additional costs of gasoline could well add up to the rebate amount over the life of the car. 23

12 Section Assessment Main Idea Using your notes from the graphic organizer activity on page 137 of your textbook, describe how price affects decisions that consumers make. Consumers will purchase less at a high price and more at a low price. Consumers also weigh the price against their need. 24 Section Assessment (cont.) Describe how producers and consumers react to prices. When prices are high, producers produce more and consumers buy less. When prices are low, producers produce less and consumers demand more. 25

13 Section Assessment (cont.) List the advantages of using prices to distribute economic products. Advantages include neutrality, flexibility, lack of administrative costs, and familiarity. 26 Section Assessment (cont.) Explain the difficulties of allocating goods and services without a price system. Difficulties include an unfair system of allocation, the high cost of administering the system, and the negative impact of the system on incentive to work and produce. 27

14 Section Assessment (cont.) Understanding Cause and Effect List five items you would like to buy. How does the price of each item affect your decision to allocate your scarce resources your money and your time? Explain. Answers will vary. 28 Section Close Debate the following statement: In every respect, price is the best system of allocating goods and services. 29

15 Click the mouse button to return to the Contents slide. Study Guide Main Idea Changes in demand and supply cause prices to change. Reading Strategy Graphic Organizer As you read the section, complete a graphic organizer similar to the one on page 142 of your textbook, showing how a surplus and shortage affect prices, demand, and supply. 31 to display the information. Section 2 begins on page 142 of your textbook.

16 Study Guide (cont.) Key Terms economic model market equilibrium surplus shortage equilibrium price Objectives After studying this section, you will be able to: Understand how prices are determined in competitive markets. Explain how economic models can be used to predict and explain price changes. Apply the concepts of elasticity to changes in prices. 32 to display the information. Section 2 begins on page 142 of your textbook. Study Guide (cont.) Applying Economic Concepts Equilibrium Price When something is at equilibrium, it tends to remain at rest. What causes prices to reach, and then stay at, equilibrium? Click the Speaker button to listen to the Cover Story. 33 Section 2 begins on page 142 of your textbook.

17 Introduction One of the most appealing features of a competitive market economy is that everyone who participates has a hand in determining prices. This is why economists consider prices to be neutral and impartial. The process of establishing prices is remarkable because buyers and sellers have exactly the opposite hopes and desires. 34 Introduction (cont.) Buyers want to find good buys at low prices. Sellers hope for high prices and large profits. Neither can get exactly what they want, so some adjustment is necessary to reach a compromise. 35

18 Did You Know? In spring and summer 1988, drought hit the United States, drying out a broad band of the country form the eastern Appalachian Mountains all the way to the Pacific coast. Parts of Iowa, Illinois, and other North Central farm states went for months with little or no rain. By the end of June, more than 1,300 counties in 30 states had been declared droughtdisaster areas. Continued on next slide 36 Did You Know? The drought resulted in a grain shortage (typical harvest dropped by almost onethird, but stored eased the blow), as well as a meat shortage (farmers had to slaughter live-stock early because they had no grain for the animals). By year s end, food prices were up 5.2 percent. 37

19 The Price Adjustment Process Together, demand and supply make a complete picture of the market. Price adjustments help a competitive market reach market equilibrium, with fairly equal supply and demand. 38 The Price Adjustment Process (cont.) 39

Surpluses occur when supply exceeds")

Shortages occur when demand exceeds")

20 The Price Adjustment Process (cont.) Surpluses occur when supply exceeds demand. 40 The Price Adjustment Process (cont.) Shortages occur when demand exceeds supply. 41

The equilibrium price is the")

43")

21 The Price Adjustment Process (cont.) The equilibrium price is the price at which supply meets demand. 42 The Price Adjustment Process (cont.) 43

22 Discussion Question Imagine that you want to go to a concert but you find it is sold out at ticket outlets. What effect will this shortage of tickets have on the price of any remaining concert tickets? Their price will increase. 44 Explaining and Predicting Prices A change in price is normally the result of a change in supply, a change in demand, or both. 45

Even small changes in an inelastic supply can create big")

Elastic supply and demand help keep prices from")

23 Explaining and Predicting Prices (cont.) Even small changes in an inelastic supply can create big changes in price. 46 Explaining and Predicting Prices (cont.) Elastic supply and demand help keep prices from changing dramatically. 47

24 Discussion Question U.S. soybean farmers had a recordhigh harvest in What likely effect did the increase in the supply of soybeans have on their price? Students should indicate that the price of soybeans dropped dramatically. 48 The Competitive Price Theory The theory of competitive pricing represents a set of ideal conditions and outcomes; it serves as a model to measure market performance. In theory, a competitive market allocates resources efficiently. To be competitive, sellers are forced to lower prices, which makes them find ways to keep their costs down. Competition among buyers keeps prices from falling too far. 49

25 Discussion Question Why do experts say that a market economy is one that runs itself? A market economy offers a climate where buyers and sellers set prices; there is no need for a bureaucracy or planning commission. 50 Section Assessment Main Idea Explain how a change in demand can affect prices. Changes in income, tastes, and so on affect demand and, therefore, price. 51

26 Section Assessment (cont.) Describe how prices are determined in a competitive market. Prices are adjusted through competition between buyers and sellers. 52 Section Assessment (cont.) Explain why economic models are useful. They show how markets work by helping analyze behavior and predict outcomes. 53

27 Section Assessment (cont.) Explain how different cases of demand and supply elasticity are related to price changes. The more elastic, the smaller the price change; the less elastic, the larger the price change. 54 Section Assessment (cont.) Understanding Cause and Effect What signal does a high price send to buyers and sellers? A high prices tells buyers that they should buy less and tells sellers they should offer more. 55

28 Section Assessment (cont.) Making Inferences What do merchants usually do to sell items that are overstocked? What does this tell you about the equilibrium price for the product? They lower the price of the items. The equilibrium price is lower than the present price. 56 Section Close Discuss the following: Price represents the balancing of the forces of demand and supply. 57

29 Click the mouse button to return to the Contents slide. Study Guide Main Idea To achieve one or more of its social goals, government sometimes sets prices. Reading Strategy Graphic Organizer As you read the section, complete a cause-and-effect chart similar to the one on page 150 of your textbook by explaining how price ceilings affect quantity supplied. 59 to display the information. Section 3 begins on page 150 of your textbook.

30 Study Guide (cont.) Key Terms price ceiling minimum wage price floor target price nonrecourse loan deficiency payment Objectives After studying this section, you will be able to: Describe the consequence of having a fixed price in a market. Explain how loan supports and deficiency payments work. Understand what is meant when markets talk. 60 to display the information. Section 3 begins on page 150 of your textbook. Study Guide (cont.) Applying Economic Concepts Price Floor Chances are that you have worked for the minimum wage at some time in your life. Why is this an example of a price floor? Click the Speaker button to listen to the Cover Story. 61 Section 3 begins on page 150 of your textbook.

31 Introduction Chapter 2 examined seven broad economic and social goals that most people seem to share. We also observed that these goals, while commendable, were sometimes in conflict with one another. These goals were also partially responsible for the increased role that government plays in our economy. The goals most compatible with a market economy are freedom, efficiency, full employment, price stability, and economic growth. 62 Introduction (cont.) Attempts to achieve the other two goals equity and security usually require policies that distort market outcomes. In other words, we may have to give up a little efficiency and freedom in order to achieve equity and security. Whether this is good or bad often depends on a person s perspective. 63

32 Introduction (cont.) After all, the person who receives a subsidy is more likely to support it however, it is usually wise to evaluate each situation on its own merits, as the benefits of a program may well exceed the costs. What is common to all of these situations, however, is that the outcomes can be achieved only at the cost of interfering with the market. 64 Introduction (cont.) After all, the person who receives a subsidy is more likely to support it than is the taxpayer who pays for it. In general, it is usually wise to evaluate each situation on its own merits, as the benefits of a program may well exceed the costs. What is common to all of these situations, however, is that the outcomes can be achieved only at the cost of interfering with the market. 65

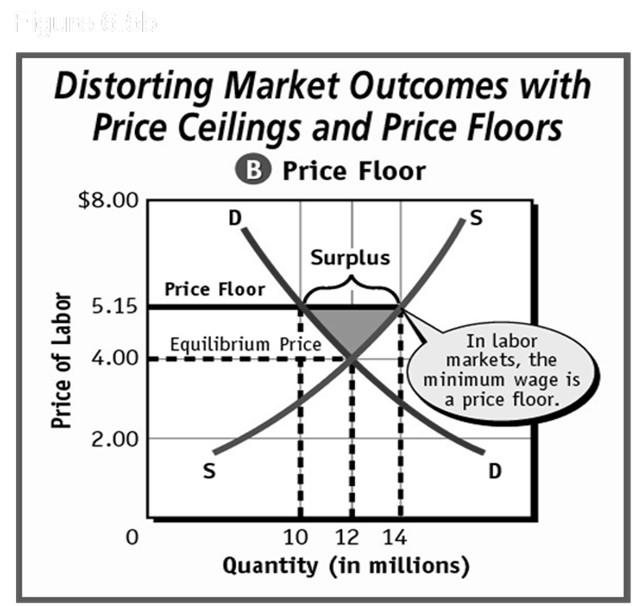

33 Did You Know? During the nation s Great Depression, prices for farm products tumbled. Farmers lost much money, and many even lost their farms. At the same time, the farms produced surplus crops. To combat this, in 1933, the government passed the Agricultural Adjustment Act. In part, this act authorized payments to farmers who agreed to reduce the acreage they farmed. This effectively reduced the crop surplus and boosted farmer income. 66 Distorting Market Outcomes Achieving equity and security (two of the seven broad economic and social goals) usually requires policies that distort market outcomes. One way to achieve these goals is to set socially desirable prices, which interferes with the pricing system. Setting price ceilings affects the allocation of resources. The minimum wage is an example of a price floor. 67

34 Distorting Market Outcomes (cont.) 68 Distorting Market Outcomes (cont.) 69

35 Discussion Question Do you agree with economists who argue that the minimum wage actually contributes to unemployment rates? Why or why not? Answers will vary but should reflect an understanding of the purpose of price floors. 70 Agricultural Price Supports Government loan support was offered in the 1930s through Commodity Credit Corporation to help stabilize agricultural prices. The CCC loan program led to food surpluses. The CCC switched to deficiency payments, which prevented the government from holding surplus food and had farmers sell their crops on the open market. 71

36 Agricultural Price Supports (cont.) In 1996, Congress passed FAIR Federal Agricultural Improvement and Reform Act. Cash payments replaced price supports and deficiency payments. The payments ended up costing as much. In 2002, farmers will no longer receive any kind of payments. 72 Discussion Question In your opinion, which kind of price support provides farmers with the most incentive to sell their crops at the highest possible price? Answers will vary but students may point out that government makes up the price difference, offering little incentive to farmers. 73

37 When Markets Talk Markets talk when prices move up or down dramatically. Buyers and sellers respond to changes in the market through their decisions. 74