Financial Regulation and Financial Inclusion

|

|

|

- Garry Warner

- 5 years ago

- Views:

Transcription

1 Financial Regulation and Financial Inclusion Nestor A. Espenilla, Jr. Deputy Governor, Supervision and Examination Sector Bangko Sentral ng Pilipinas 1 04 June 2010 Towards a Brave New World Re-shaping Financial Regulation Washington, D.C.

2 Presentation Outline The Global and Philippine Context Our Guiding Principles Proportionate Regulation Key Interventions for Financial Inclusion Regulatory and Supervisory Approach to Mobile Banking Our Next Steps 2

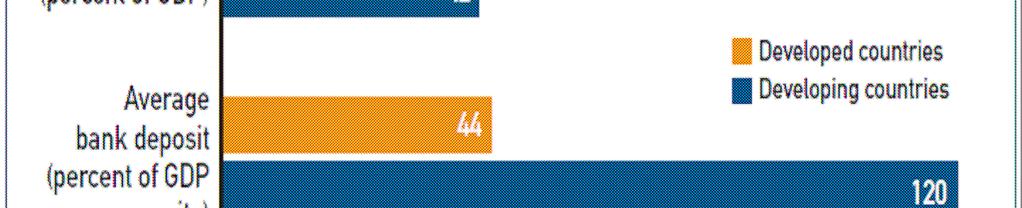

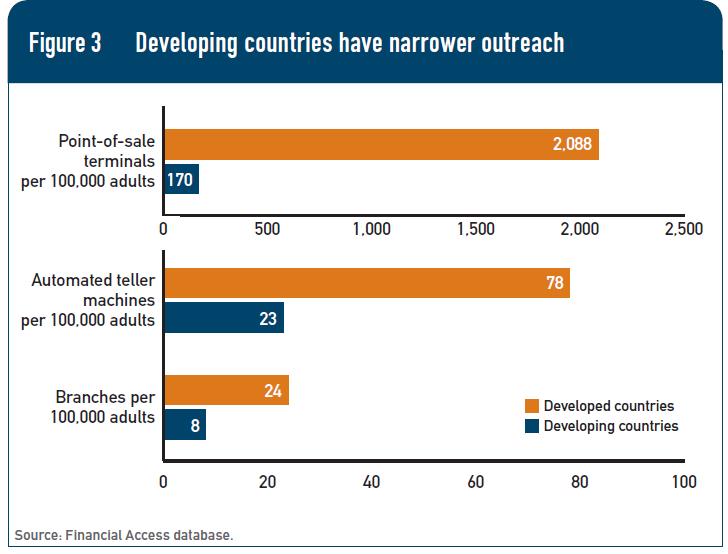

3 Global Context 3 Source: Financial Access 2009, CGAP

4 Global Context 2.5 billion adults, just over half of world s adult population, do not use formal financial services to save or borrow. 2.2 billion of these unserved adults live in Africa, Asia, Latin America, and the Middle East. Of the 1.2 billion adults who use formal financial services in Africa, Asia, and the Middle East, at least two-thirds, a little more than 800 million, live on less than $5 per day. Source: Half the World is Unbanked, 2009, Financial Access Initiative 4

5 Philippine Context Access to finance is a major challenge 609 out of 1,635 municipalities do not have banking offices, a 37% non-coverage (as of end December 2009) Concentration of services in higher income urban areas, leaving low income areas significantly underserved Archipelagic structure provides spatial obstacles/ barriers to access 5

6 Philippine Context Overseas Filipino Workers total over 8 million sending over USD 16 Billion (approx 10% of GDP) 60% of the population are younger than 30 years old Mobile phone penetration in the Philippines is at approximately 75% Computer and internet penetration is less than 5% 6

7 Our Guiding Principles Financial inclusion is a worthy policy objective, alongside the promotion of stability and efficiency in shaping the development of the financial system. It directly contributes to social cohesion and shared economic development. Market-based solutions to address financial access issues are feasible and can be addressed through an appropriately supportive regulatory environment. 7

8 Our Guiding Principles Financial inclusion involves delivery of a wide range of financial services such as savings, credit, insurance, payments, remittances. These products must be appropriately designed and priced for the particular market. Bank and non-bank based delivery channels can combine to reach the financially excluded more effectively. All financial service providers should be properly regulated to uphold consumer protection and financial system integrity. 8

9 Proportionate regulation is key. The following need to be balanced and addressed: Issue Point of Balance Possible Policy Initiatives Safety and Soundness Deposits should be wellprotected Innovative financial services to the low-income potentially expose deposit taking institutions to new risks Prudential regulation can impose undue regulatory burden Limit safety and soundness supervision to entities with deposit taking activities Distinguish deposit taking activities from fund transfer activities Risk-based supervision Ensure adequate supervisor capacity through training Close coordination with other financial regulators 9

10 Proportionate regulation is key. The following need to be balanced and addressed: Issue Point of Balance Possible Policy Initiatives Consumer Protection Financial Inclusion brings in new consumers who are potentially vulnerable. They need appropriate information and increased capacity to use financial access to their best interest. Financial education Price transparency and fair treatment regulation Contestable markets to drive competition in a multi-player environment (bank and nonbank) Consumer redress mechanisms 0

11 Proportionate regulation is key. The following need to be balanced and addressed: Issue Point of Balance Possible Policy Initiatives AML/CFT Need to manage the risks to financial system integrity of easy access to the financial system. Allow simplified KYC requirements for small value transactions only Leverage on KYC of other authorized institutions Recognize the use of technology in e-money systems in identifying and suppressing illegal activities 1

12 Key Interventions for Financial Inclusion MICROFINANCE Provision of a range of financial services to low income clients/ entrepreneurial poor credit, savings, insurance, fund transfers National Strategy for Microfinance and General Banking Law recognized the role and institutionalized microfinance in the financial system BSP established an enabling policy and regulatory environment for the delivery of commercially sustainable microfinance in the banking sector Promote conducive environment for continuous product innovation: micro-agri, micro-housing, microinsurance and mobile banking. MOBILE BANKING AND E-MONEY Develop e-money as acceptable and convenient surrogate for cash in low value payment transactions Collaborate with Telcos to develop regulated e-money ecosystem with wide and ubiquitous coverage reaching out to frontier areas BSP defined e-money, e-money issuers and developed a clear and proportionate regulatory framework for the business to move forward Leverage the reach of bank brick and mortar offices through operational partnership with e-money ecosystems 2 Bank- based Microfinance Regulated E-money Ecosystems Inclusive and Transformational Banking

13 Regulatory Approach to Mobile Banking 3 BSP recognized the potential of the convergence of mobile and banking services for financial inclusion. We adopted an open, flexible yet cautious approach to allow different pioneer models to flourish. Bank-based Model (Smart Money) 2004 Partnership between Smart Telco and BDO (biggest domestic universal bank) BDO issues/ owns Smart Money (accessed via Mastercard powered card) BDO uses Smart Telco s mobile technology platform and distribution outlets as delivery channel, in addition to their branches and ATM network A bank is the e-money issuer in this model, telco is the e-money technology provider Non-Bank Based Model (G-Cash) 2005 GXI, a subsidiary of Globe Telco, issues G-Cash (accessed via mobile device s virtual wallet) GXI uses Globe Telco s mobile technology platform for distribution outlets as delivery channel, in addition to individually authorized agents GXI is a non-bank entity licensed as e-money issuer (EMI), a BSP regulated entity Banks may partner with GXI and use G-cash for their mobile banking application

14 The Bank-Telco Partnership As a regulated non-bank E-money Issuer, GXI can develop its own network of cash in/cash out agents while remaining responsible that such agents comply with AML and consumer protection regulations. At present GXI has 18,000 agents. Smart Telco, as an E-money Technology Provider to banks, provide partner banks with the ability to use Smart Money as surrogate for cash. Partner banks have the responsibility tp ensure that Smart is compliant with AML and consumer protection regulations. Utilizing a vast and readily scalable agent network extends the ecosystem of e-money service channels and facilitates ready access to banking services through partnerships Deposit taking remains firmly with banks. The model provides scope for proportionate regulation on the part of the supervisor, without stretching limited supervisory resources. 4

15 Mobile Banking: Key Adjustments to Bank Supervision Targeted Regulations Circular 511 (2006) Guidelines on technology risk management Circular 542 (2006) Guidelines on consumer protection for electronic banking Circular 471 (2005) Regulations on registration of remittance/ money transfer agents Various Circulars on AML More flexible KYC rules mitigated by compensating controls Circular 649 (2009) Formally sets out general regulatory framework for e-money business Forthcoming Circular Enhancements to e-money outsourcing Supervisory Capacity Building Close interaction with industry players Specialist technology risk examiners (2005) Consumer protection and financial literacy advocacy 5

16 6 Circular 649 : Setting the Regulatory Framework for E-money Clearly defines e-money: Monetary value is always prepaid Does not bear interest nor earn added value/rewards Not deposit insured Fully re-convertible to cash Clearly defines E-money Issuers (EMIs): EMI license may be issued to either bank or non-bank. A licensed EMI can establish its own network of cash in/out agents for which it is fully responsible. A non-bank EMI s primary business should be e-money, and must comply with BSP requirements/safeguards. A Telco subsidiary dedicated to e-money business may be licensed as non-bank EMI (not Telco itself). This Subsidiary is subject to BSP supervision and may not extend credit without prior BSP authority. BSP requirements/safeguards: Minimum capital requirement of PhP 100 M (~USD 2 M) 100% liquidity cover on outstanding e-money liability E-money liability balances specifically booked as Accounts Payable E-money Transaction cap of PhP 100,000/month (~USD 2,000) Adequate operational risk management standards AML compliant Customer care responsibilities

17 Our Next Steps 7 Success breeds new challenges and risks. We need to prepare now. Steady advocacy for responsible finance Price transparency Fair treatment standards Close monitoring of market practices and developments Quick response to emergent risks Financial crime Abuse of financial services Over-indebtedness Financial literacy promotion

18 End of Presentation. 8