Putting the trust back in &TRUST. BANK. Financial Communications Society Luncheon September 24, 2009

|

|

|

- Arthur Wheeler

- 5 years ago

- Views:

Transcription

1 Putting the trust back in BANK &TRUST. Financial Communications Society Luncheon September 24, 2009

2 CASUAL OBSERVATION: Marketers - from many industries - are spending money talking about trust. Airlines. Insurance. Investments. And of course... banks.

3 Such as... New Zealand Airlines Charles Schwab Sovereign Bank Ally Bank Geico Sun Trust

4 Is it working? We asked: Are consumers as concerned with trust as corporate America (banks in particular) seems to believe? What does trust actually mean in this context - and is it important? How do users interpret online content from banks? Does it affect their feelings about their financial institutions? How can financial institutions use the online channel to establish credibility with their customers - and potential customers?

5 TWO P A R T STUDY Quantitative high level assessment of WHAT people think about banks and trust issues Qualitative deeper insight into WHY specific bank websites are effective, or not, in building trust

6 Quantitative: What we learned Results were surprising - and more nuanced than anticipated. 80% 66% 56% rarely think about which bank they use do not think their banks care about their interests don't think their banks care about them at all 44% don't believe anything they see in banking ads or websites "sometimes" believe 49% what they see in banking ads or websites

7 When asked "Can you name a bank you can trust?" 40% answered with some variation of no.

8 But it gets surprising: 71% reported that they do not trust banks any less than they did 18 months ago. Only 36% said that when considering a bank, "security" and "safety" are the main decision drivers. (The leader was "customer service," at 52% by the way.)

9 That s the what. Let s talk about why? 14 lucky consumers came in to chat. We looked at 3 categories of banks.

10 Who we studied: The Establishment Wells Fargo Bank of America The Brand Extension E-Trade Bank The Challengers Ally Bank Redneck Bank

11 What was on the menu? The users did not know the intent of the study "Assume that you have re-located to a new part of the country and have to find a new bank." We gave users the URLs of the banks mentioned previously and asked to explore them. We eye-tracked their experiences, and then asked them to walk us through what they were thinking and what they were doing with each click. In the process, we focused our questions around issues of "trust."

Other words were mentioned as alternatives to trust : Credibility Dependability Honesty")

12 What we learned: Trust did not resonate as much as expected Most thought FDIC Insured = money is safe (all banks were viewed as safe) Other words were mentioned as alternatives to trust : Credibility Dependability Honesty Reliability

13 People s thoughts on: trust Will I be treated fairly? WIll I be valued? Identity theft - am I safe? What does a bank do in the community? How are its business practices? Is it scandal free? How complex are terms & conditions? How much fine print? Will they suggest services appropriate to me, or just try to sell me things? Is there a Chinese wall from investment banking arm? Does it have a track record of responsible lending practices? Are bonuses for bank executives coming out of my money?

14 People s thoughts on: banking Still Standing People felt that if a bank is still standing, it s safe. Not a lot of perceived differentiation Common sentiment: Most banks are pretty much the same. Not much has changed Current climate has not changed my view of banking.

New is good... to a point People value product innovation but don t trust too good to be true offers. Reference check: Have they been around? Do I know people who use them?")

15 People s thoughts on: communications More show less tell Users agreed that they want to be shown, not told, how a bank stands by its customers (customer service) and community (e.g. post-katrina, what did a bank do to help customers affected?) New is good... to a point People value product innovation but don t trust too good to be true offers. Reference check: Have they been around? Do I know people who use them? Could I ask THEM if they have good service? (social media might enable the entire customer base to be a potential reference.) Change the relationship, not the conversation Traditional media tactics won t work online When the user is one click away from learning more, claims have to be valid.

16 Credibilityvs Innovation It appears that the longer a bank has been in business, the less time that bank needs to spend establishing its credibility. Wells Fargo / Bank of America On the other side of the spectrum, the newer a banking institution is, the more users are dubious of "new" or "innovative" products, services, or offers. Perceived Track Record Redneck Bank / Ally Bank E-Trade Bank About the institution What customers want to hear: New Products

17 The Details:

18 Bank of America

19 Wells Fargo

20 Very positive response to "Keep the change" offer online Liked the idea that it was an offer that seemed to add value Didn't seem "too good to be true"

21 Very positive response to online chat offering Multiple users responded that it appeared precisely when they were confused about something

22 Users felt that B of A and Wells Fargo were both very forthcoming with information, beyond the point of what they expected Users applauded how informative the sites were, but also thought it was overkill, as their history & track record in and of themselves made them "credible"

23 Ironically, while people were consistently impressed by their "stability," they were not moved or impressed enough to view these banks as any different than any other bank - the sites served to reinforce notions of stability but didn't differentiate them in any way.

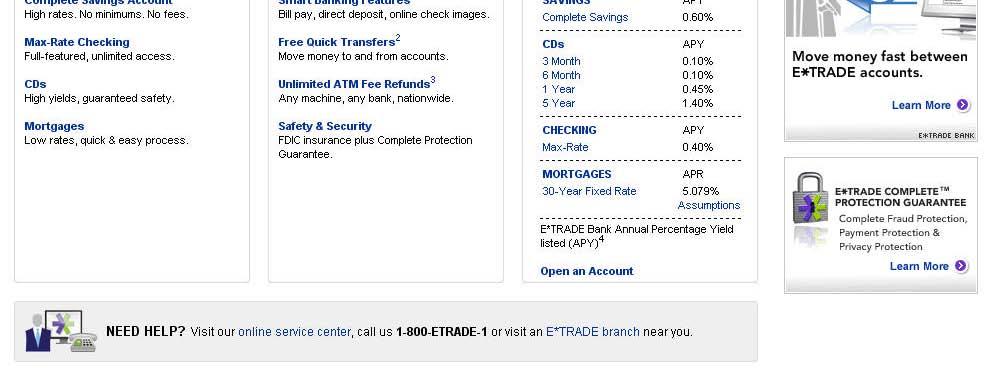

24 E-Trade Bank

but were unaware that E-Trade offered personal")

25 Users were very intrigued by the "newness" They all knew of E-Trade (and thus believed E-Trade to be a credible company) but were unaware that E-Trade offered personal banking.

and new (because it was a new")

26 The general impression was that E-Trade Bank did a good job of straddling the line of "credible" (because of E-Trade's name recognition) and new (because it was a new offering).

27 However, upon further examination - specifically, E-Trade's claim that there would never be any ATM fees of any kind struck people as "too good to be true."

28 The disclaimer that "We will not charge you a fee for withdrawing funds from any ATM nationwide, but the owner/operator of the ATM may" left a very negative impression among users. The additional point that Max Rate Checking Customers would also be excluded seemed to add salt to the wounds of those who didn t have $50,000 to put into checking.

29 Ally Bank

30 No one had any real knowledge of Ally Bank.

31 People were very impressed by the "customer service" link that stated what the wait time would be to speak with someone live.

32 Unlike Bank of America, people were annoyed by Ally's chat window pop up - they found it intrusive, haphazard, and "ad-like."

33 The graphs comparing their rates to other banks was initially viewed in a very positive light, as the first chart compared Ally to 6 other institutions.

34 However, the next graph compared Ally to only ONE other institution, which raised eyebrows with some who felt that showing fewer competitors meant that Ally was trying to hide something.

35 People thought the site was too "light on content" which would have been fine if they knew who Ally was, but because they had no brand awareness they found it to be "flimsy."

36 While the design of the site was viewed as "attractive", it was also found to be "not bank-like" - one user compared it to a pharmaceutical website.

37 Doing things differently actually raised several suspicions: I m suspicious of someone who says it s a CD but you can take your money out. It s re-defining what a CD IS. They re doing things differently, which makes you think about what are you getting and what are you giving up?

38 Redneck Bank

39 Redneck was an interesting case study - because of the tone, language, and positioning, literally everyone spent significant time on the site, and called it "memorable," "interesting," etc.

40 However, not one person thought it was a real website for a real bank - they all assumed it was a joke.

41 As a marketing tactic the site served to create recall; however, it was not favorable. Some people said that the constant references to being "trust worthy" made them seem less trust worthy; several people said that they didn't think this sort of humor was appropriate for a bank. As far as the site experience itself went, people thought it looked flimsy, and "unsafe." Additionally, they found it confusing and distracting.

42 Finally, those users who clicked the link to "bankin skool" were surprised to see a secondary site that was completely devoid of the identity on the initial site. That, in conjunction with their "traditional" language on identity theft and terms & conditions, left people feeling unsure as to how sincere this positioning actually is.

43 Wrapping Up Banks viewed as "credible" have more room to offer "new" and "innovative" services; when the credibility as an institution has been established, users are more interested in how that institution is different from its competition. But talk is not enough. Bank websites need to back up claims with real information about how customers are treated. Change the relationship, not just the conversation. Unknown banks offering new services are perceived somehow trying to "pull one over" on the consumers, or worse: simply not a credible bank.

44 Thank you.