Econ Microeconomic Analysis and Policy

|

|

|

- Rebecca Pierce

- 6 years ago

- Views:

Transcription

1 ECON 500 Microeconomic Theory Econ Microeconomic Analysis and Policy Monopoly

2 Monopoly A monopoly is a single firm that serves an entire market and faces the market demand curve for its output. Unlike the perfectly competitive firm s output decision (which has no effect on market price), the monopoly s output decision will, in fact, determine the good s price. Furthermore, due to barriers to entry, other firms find it impossible or unprofitable to enter the market a monopoly operates in. Therefore, monopoly markets and markets characterized by perfect competition are polar opposite cases.

3 Barriers to Entry The reason a monopoly exists is that other firms find it unprofitable or impossible to enter the market. Barriers to entry are therefore the source of all monopoly power. If other firms could enter a market then the firm would, by definition, no longer be a monopoly. There are two general types of barriers to entry: Technical Barriers to Entry Legal Barriers to Entry

4 Barriers to Entry There are two general types of barriers to entry: Technical Barriers to Entry: Economies of Scale Proprietary Technology Ownership of unique resources Legal Barriers to Entry: Intellectual Property Rights Government Designation Firms may also expand productive resources to create barriers to entry.

5 Monopoly Output Choice ECON 500

6 Monopoly Output Choice Monopoly Markup

7 Monopoly Output Choice Two General Conclusions: A monopoly will choose to operate only in regions where the market demand curve is elastic, e Q,P < -1 The firm s markup over marginal cost depends inversely on the elasticity of market demand

8 Monopoly and Supply There is no unique relationship between price and quantity supplied in the case of a monopoly. Monopoly has no supply curve.

9 Monopoly and Profit ECON 500

10 Monopoly and Welfare ECON 500

11 Measuring Monopoly Power Lerner Index of Monopoly Power: Measure of monopoly power calculated as excess of price over marginal cost as a fraction of price. L = (P MC) P = 1 E d

12 Measuring Monopoly Power ECON 500

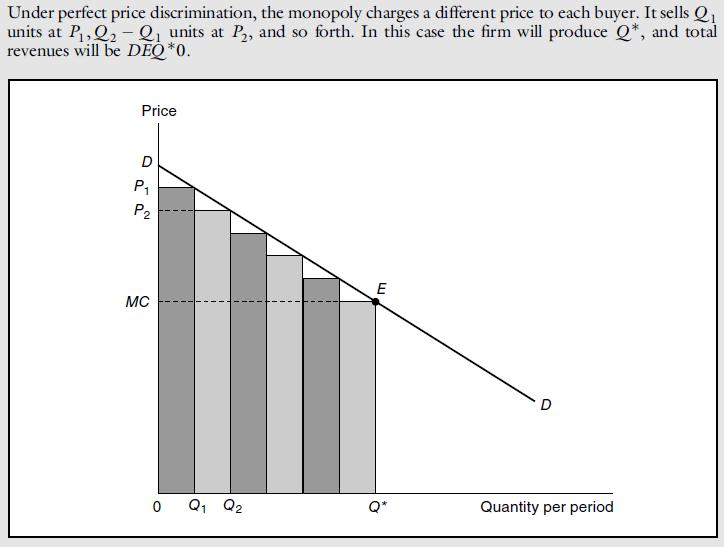

13 Capturing Consumer Surplus CAPTURING CONSUMER SURPLUS If a firm can charge only one price for all its customers, that price will be P* and the quantity produced will be Q*. Ideally, the firm would like to charge a higher price to consumers willing to pay more than P*, thereby capturing some of the consumer surplus under region A of the demand curve. The firm would also like to sell to consumers willing to pay prices lower than P*, but only if doing so does not entail lowering the price to other consumers. In that way, the firm could also capture some of the surplus under region B of the demand curve. price discrimination Practice of charging different prices to different consumers for similar goods.

14 Price Discrimination First-Degree Price Discrimination reservation price for a good. Maximum price that a customer is willing to pay first degree price discrimination reservation price. Practice of charging each customer her

15 ADDITIONAL PROFIT FROM PERFECT FIRST-DEGREE PRICE DISCRIMINATION Because the firm charges each consumer her reservation price, it is profitable to expand output to Q**. When only a single price, P*, is charged, the firm s variable profit is the area between the marginal revenue and marginal cost curves. With perfect price discrimination, this profit expands to the area between the demand curve and the marginal cost curve.

16

17 Second-Degree Price Discrimination second-degree price discrimination Practice of charging different prices per unit for different quantities of the same good or service. block pricing Practice of charging different prices for different quantities or blocks of a good. SECOND-DEGREE PRICE DISCRIMINATION Different prices are charged for different quantities, or blocks, of the same good. Here, there are three blocks, with corresponding prices P 1, P 2, and P 3. There are also economies of scale, and average and marginal costs are declining. Second-degree price discrimination can then make consumers better off by expanding output and lowering cost.

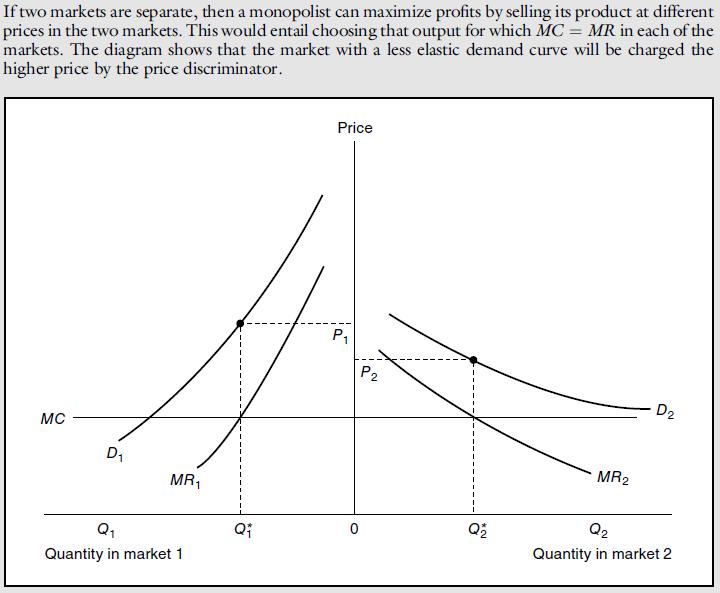

18 Third-Degree Price Discrimination third-degree price discrimination Practice of dividing consumers into two or more groups with separate demand curves and charging different prices to each group. CREATING CONSUMER GROUPS If third-degree price discrimination is feasible, how should the firm decide what price to charge each group of consumers? 1. We know that however much is produced, total output should be divided between the groups of customers so that marginal revenues for each group are equal. 2. We know that total output must be such that the marginal revenue for each group of consumers is equal to the marginal cost of production.

19 Let P 1 be the price charged to the first group of consumers, P2 the price charged to the second group, and C(QT) the total cost of producing output Q T = Q 1 + Q 2. Total profit is then π = P 1 Q 1 + P 2 Q 2 C Q T π Q 1 = P 1Q 1 Q 1 C Q 1 = 0 MR 1 = MC MR 2 = MC MR 1 = MR 2 = MC (11.1) DETERMINING RELATIVE PRICES MR = P E d P 1 = E 2 P E 1 (11.2)

20

21 THIRD-DEGREE PRICE DISCRIMINATION Consumers are divided into two groups, with separate demand curves for each group. The optimal prices and quantities are such that the marginal revenue from each group is the same and equal to marginal cost. Here group 1, with demand curve D 1, is charged P 1, and group 2, with the more elastic demand curve D 2, is charged the lower price P 2. Marginal cost depends on the total quantity produced Q T. Note that Q 1 and Q 2 are chosen so that MR 1 = MR 2 = MC.

22 NO SALES TO SMALLER MARKETS Even if third-degree price discrimination is feasible, it may not pay to sell to both groups of consumers if marginal cost is rising. Here the first group of consumers, with demand D 1, are not willing to pay much for the product. It is unprofitable to sell to them because the price would have to be too low to compensate for the resulting increase in marginal cost.

23 Intertemporal Price Discrimination and Peak-Load Pricing intertemporal price discrimination Spending money in socially unproductive efforts to acquire, maintain, or exercise monopoly. peak-load pricing acquire, maintain, or exercise monopoly. Intertemporal Price Discrimination Spending money in socially unproductive efforts to INTERTEMPORAL PRICE DISCRIMINATION Consumers are divided into groups by changing the price over time. Initially, the price is high. The firm captures surplus from consumers who have a high demand for the good and who are unwilling to wait to buy it. Later the price is reduced to appeal to the mass market.

24 Peak-Load Pricing PEAK-LOAD PRICING Demands for some goods and services increase sharply during particular times of the day or year. Charging a higher price P 1 during the peak periods is more profitable for the firm than charging a single price at all times. It is also more efficient because marginal cost is higher during peak periods.

25 The Two-Part Tariff two-part tariff Form of pricing in which consumers are charged both an entry and a usage fee. SINGLE CONSUMER TWO-PART TARIFF WITH A SINGLE CONSUMER The consumer has demand curve D. The firm maximizes profit by setting usage fee P equal to marginal cost and entry fee T* equal to the entire surplus of the consumer.

26 TWO CONSUMERS TWO-PART TARIFF WITH TWO CONSUMERS The profit-maximizing usage fee P* will exceed marginal cost. The entry fee T* is equal to the surplus of the consumer with the smaller demand. The resulting profit is 2T* + (P* MC)(Q 1 + Q 2 ). Note that this profit is larger than twice the area of triangle ABC.

27 Regulation of Monopoly Price Regulation

28 Regulation of Monopoly Price Regulation

29 Regulation of Monopoly Price Regulation Natural Monopoly Dilemma

30

31 ECON 500 Microeconomic Theory Econ Microeconomic Analysis and Policy Imperfect Competition

32

33 Bertrand Competition Two identical firms, producing identical products at a constant marginal cost (and constant average cost) c. The firms choose prices p 1 and p 2 simultaneously in a single period of competition. Since firms products are perfect substitutes, all sales go to the firm with the lowest price. Sales are split evenly if p 1 = p 2. The only pure-strategy (Nash) equilibrium of the Bertrand game is p 1 = p 2 = c

34 Cournot Competition Two identical firms, producing identical products at a constant marginal cost (and constant average cost) c. The firms choose prices q 1 and q 2 simultaneously in a single period of competition. The pure strategy (Nash) equilibrium of the Cournot game is a set of quantities where each firm correctly assumes how much its competitor will produce and sets its own production level accordingly. After this simple change in strategic variable, equilibrium price will be above marginal cost and firms will earn positive profit in the Nash equilibrium of the Cournot game.

35 The Cournot Model Cournot model Oligopoly model in which firms produce a homogeneous good, each firm treats the output of its competitors as fixed, and all firms decide simultaneously how much to produce. FIRM 1 S OUTPUT DECISION Firm 1 s profit-maximizing output depends on how much it thinks that Firm 2 will produce. If it thinks Firm 2 will produce nothing, its demand curve, labeled D 1 (0), is the market demand curve. The corresponding marginal revenue curve, labeled MR 1 (0), intersects Firm 1 s marginal cost curve MC 1 at an output of 50 units. If Firm 1 thinks that Firm 2 will produce 50 units, its demand curve, D 1 (50), is shifted to the left by this amount. Profit maximization now implies an output of 25 units. Finally, if Firm 1 thinks that Firm 2 will produce 75 units, Firm 1 will produce only 12.5 units. 5 75

36 REACTION CURVES reaction curve Relationship between a firm s profit-maximizing output and the amount it thinks its competitor will produce. REACTION CURVES AND COURNOT EQUILIBRIUM Firm 1 s reaction curve shows how much it will produce as a function of how much it thinks Firm 2 will produce. (The xs at Q2 = 0, 50, and 75 correspond to the examples shown in Figure 12.3.) Firm 2 s reaction curve shows its output as a function of how much it thinks Firm 1 will produce. In Cournot equilibrium, each firm correctly assumes the amount that its competitor will produce and thereby maximizes its own profits. Therefore, neither firm will move from this equilibrium.

37 COURNOT EQUILIBRIUM Cournot equilibrium Equilibrium in the Cournot model in which each firm correctly assumes how much its competitor will produce and sets its own production level accordingly. Cournot equilibrium is an example of a Nash equilibrium (and thus it is sometimes called a Cournot-Nash equilibrium). In a Nash equilibrium, each firm is doing the best it can given what its competitors are doing. As a result, no firm would individually want to change its behavior. In the Cournot equilibrium, each firm is producing an amount that maximizes its profit given what its competitor is producing, so neither would want to change its output.

38 The Linear Demand Curve An Example Two identical firms face the following market demand curve Also, MC 1 = MC 2 = 0 P = 30 Q Total revenue for firm 1: R 1 = PQ 1 = a Q Q 1 = aq 1 Q 1 2 Q 2 Q 1 then MR 1 = R 1 Q 1 = 30 2Q 1 Q 2 Setting MR 1 = 0 (the firm s marginal cost) and solving for Q 1, we find Firm 1 s reaction curve: Q 1 = Q 2 (12.1) By the same calculation, Firm 2 s reaction curve: Cournot equilibrium: Total quantity produced: Q 1 = Q 2 = 10 Q = Q 1 + Q 2 = 20 Q 2 = Q 2 (12.2) If the two firms collude, then the total profit-maximizing quantity is: Total revenue for the two firms: R = PQ = (30 Q)Q = 30Q Q 2, then MR 1 = R/ Q = 30 2Q Setting MR = 0 (the firm s marginal cost) we find that total profit is maximized at Q = 15. Then, Q 1 + Q 2 = 15 is the collusion curve. If the firms agree to share profits equally, each will produce half of the total output: Q 1 = Q 2 = 7.5

39 DUOPOLY EXAMPLE The demand curve is P = 30 Q, and both firms have zero marginal cost. In Cournot equilibrium, each firm produces 10. The collusion curve shows combinations of Q 1 and Q 2 that maximize total profits. If the firms collude and share profits equally, each will produce 7.5. Also shown is the competitive equilibrium, in which price equals marginal cost and profit is zero.

40 Cournot Competition General Model n firms, indexed by i = 1,,n each of which is producing q i with the cost function C i (q i ) where the total industry output is Q = q 1 + q q n and where the inverse demand revealing the market price is P(Q) with P (Q) < 0 A representative firm i maximizes it s profit π i = P(Q) q i - C i (q i ) where the first order condition with respect to it s own quantity is P(Q) q i + P (Q) q i C i (q i ) = 0 This first order condition must hold for all firms i = 1,,n and this system of equations can be solved for the Cournot-Nash equilibrium quantity q i * by imposing symmetry.

41 Natural Spring Duopoly Inverse demand: P(Q) = a Q where Q = Cost functions C i (q i ) = cq i Bertrand Equilibrium: P* = c; total output = Q* = a c * i = 0; total profit for all firms = * = 0

42 Natural Spring Duopoly Inverse demand: P(Q) = a Q where Q = Cost functions C i (q i ) = cq i Cournot Equilibrium: 1 = P(Q)q 1 cq 1 = (a q 1 q 2 c)q 1 2 = P(Q)q 2 cq 2 = (a q 1 q 2 c)q 2 a 2q 1 q 2 c = 0 q 1 = a q 1 2q 2 c = 0 q 2 = q 1 * = q 2 * = (a c)/3 total output = Q* = (2/3)(a c) P* = (a + 2c)/3; 1 * = 2 * = (1/9)(a c) 2 * = (2/9)(a c) 2

43 Natural Spring Duopoly Inverse demand: P(Q) = a Q where Q = Cost functions C i (q i ) = cq i Cartel Equilibrium: = (a q 1 q 2 c)q 1 + (a q 1 q 2 c)q 2 a 2q 1 2q 2 c = 0 q 1 * = q 2 * = (a c)/4 total output = Q* = (a c)/2 P* = (a + c)/2; 1 * = 2 * = (a c) 2 /8 * = (a c) 2 /4

44 Natural Spring Duopoly ECON 500

45 Number of Firms and Range of Outcomes: n = perfect competition n = 1 perfect cartel / monopoly π i = P(Q)q i cq i = (a q i Q -i - c)q i where Q -i = Q - q i π i / q i = a 2q i Q -i c = 0 q i = imposing symmetry Q -i * = Q* - q i * = n q i * - q i * = (n-1) q i * q i * = (a-c) / (n+1) Q* = (a-c) P* = a + c * = n ( )

46 Prices or Quantities Cournot model admits more realistic market structure outcomes as n varies. However, firms tend to set prices rather than quantities Allowing for capacity constraints in price competition establishes an isomorphism between price and quantity competition. First stage: choose capacities q 1, q 2 Second stage: price competition p 1, p 2 p 1 = p 2 < p or p 1 = p 2 > p can not be a Nash Eq. p 1 = p 2 = p is the only Nash Eq. in the pricing stage. Having observed the outcome of the second stage, capacity choices are made in a Cournot fashion in the fisrt stage.

47 Price Competition with Product Differentiation Suppose n firms simultaneously choose prices p 1, p 2,, p n of their differentiated goods. Firm i s demand is where, a i is the product specific attributes that enable differentiation. Firm i s profit function is with the first order condition These FOCs can be solved simultaneously to yield the Nash Equilibrium prices.

48 Price Competition with Product Differentiation ECON 500

49 Other Sources of Price Dispersion Even if the physical characteristics of the goods they sell are identical, competitors may have some ability to charge prices above marginal cost and earn positive profits if their location choices (quality, variety, transportation, etc. dimension) lead to spatial differentiation. Any positive search cost s incurred by the consumer that demand a single unit with identical gross surplus v to learn the prices of a number n of firms avoids the Bertrand Paradox and allows firms to arrive at a Nash Eq. where all firms charge the monopoly price v. Firms choices of where to locate in an attribute space in which consumers are distributed according to some density function with an increasing cost of buying at a location different than theirs also avoids Bertrand Paradox and allows for price (>MC) dispersion.

50 Hotelling s Beach Two firms locate at points a and b on the line of length L. Consumers are uniformly distributed along the same line and have quadratic costs of traveling to their firm of choice t(x-a) 2 A consumer at x will be indifferent between the two firms if p A + t(x a) 2 = p B + t(b x) 2 x b a pb pa 2 2 t( b a)

51 Hotelling s Beach The two firms demands are: Nash Equilibrium prices then become:

52 Tacit Collusion Do firms have to endure the Bertrand paradox (marginal cost pricing and zero profits) in each period of a repeated game or can they instead achieve more profitable outcomes through tacit collusion? In order for collusion to be sustainable collusive profit should exceed one time deviation profit

53 Tacit Collusion Do firms have to endure the Bertrand paradox (marginal cost pricing and zero profits) in each period of a repeated game or can they instead achieve more profitable outcomes through tacit collusion? Suppose Q = P MC=AC=10 P B = 10 Π i = 0 P C = 30 Π C = P M = 30-ε Π M = Collusion can be sustained if δ >1/2 r <1

54 Tacit Collusion Do firms have to endure the Bertrand paradox (marginal cost pricing and zero profits) in each period of a repeated game or can they instead achieve more profitable outcomes through tacit collusion? Suppose Q = P MC=AC=10 P B = 10 Π i = 0 P C = 30 Π C = P M = 30-ε Π M = With n firms collusion can be sustained if δ >1-(1/n) n <12

Recall from last time. Econ 410: Micro Theory. Cournot Equilibrium. The plan for today. Comparing Cournot, Stackelberg, and Bertrand Equilibria

Slide Slide 3 Recall from last time A Nash Equilibrium occurs when: Econ 40: Micro Theory Comparing Cournot, Stackelberg, and Bertrand Equilibria Monday, December 3 rd, 007 Each firm s action is a best

Slide Slide 3 Recall from last time A Nash Equilibrium occurs when: Econ 40: Micro Theory Comparing Cournot, Stackelberg, and Bertrand Equilibria Monday, December 3 rd, 007 Each firm s action is a best

Imperfect Competition

Imperfect Competition Lecture 5, ECON 4240 Spring 2018 Snyder et al. (2015), chapter 15 University of Oslo 2.14.2018 iacquadio & Traeger: Equilibrium, Welfare, & Information. UiO Spring 2018. 1/23 Outline

Imperfect Competition Lecture 5, ECON 4240 Spring 2018 Snyder et al. (2015), chapter 15 University of Oslo 2.14.2018 iacquadio & Traeger: Equilibrium, Welfare, & Information. UiO Spring 2018. 1/23 Outline

Microeconomics (Oligopoly & Game, Ch 12)

") Microeconomics (Oligopoly & Game, Ch 12) Lecture 17-18, (Minor 2 coverage until Lecture 18) Mar 16 & 20, 2017 CHAPTER 12 OUTLINE 12.1 Monopolistic Competition 12.2 Oligopoly 12.3 Price Competition 12.4

Microeconomics (Oligopoly & Game, Ch 12) Lecture 17-18, (Minor 2 coverage until Lecture 18) Mar 16 & 20, 2017 CHAPTER 12 OUTLINE 12.1 Monopolistic Competition 12.2 Oligopoly 12.3 Price Competition 12.4

Econ 121b: Intermediate Microeconomics

Econ 11b: Intermediate Microeconomics Dirk Bergemann, Spring 01 Week of 3/6-4/3 1 Lecture 16: Imperfectly Competitive Market 1.1 Price Discrimination In the previous section we saw that the monopolist

Econ 11b: Intermediate Microeconomics Dirk Bergemann, Spring 01 Week of 3/6-4/3 1 Lecture 16: Imperfectly Competitive Market 1.1 Price Discrimination In the previous section we saw that the monopolist

Chapter 14 TRADITIONAL MODELS OF IMPERFECT COMPETITION. Copyright 2005 by South-Western, a division of Thomson Learning. All rights reserved.

Chapter 14 TRADITIONAL MODELS OF IMPERFECT COMPETITION Copyright 2005 by South-Western, a division of Thomson Learning. All rights reserved. 1 Pricing Under Homogeneous Oligopoly We will assume that the

Chapter 14 TRADITIONAL MODELS OF IMPERFECT COMPETITION Copyright 2005 by South-Western, a division of Thomson Learning. All rights reserved. 1 Pricing Under Homogeneous Oligopoly We will assume that the

11. Oligopoly. Literature: Pindyck and Rubinfeld, Chapter 12 Varian, Chapter 27

11. Oligopoly Literature: Pindyck and Rubinfeld, Chapter 12 Varian, Chapter 27 04.07.2017 Prof. Dr. Kerstin Schneider Chair of Public Economics and Business Taxation Microeconomics Chapter 11 Slide 1 Chapter

11. Oligopoly Literature: Pindyck and Rubinfeld, Chapter 12 Varian, Chapter 27 04.07.2017 Prof. Dr. Kerstin Schneider Chair of Public Economics and Business Taxation Microeconomics Chapter 11 Slide 1 Chapter

Oligopoly: How do firms behave when there are only a few competitors? These firms produce all or most of their industry s output.

Topic 8 Chapter 13 Oligopoly and Monopolistic Competition Econ 203 Topic 8 page 1 Oligopoly: How do firms behave when there are only a few competitors? These firms produce all or most of their industry

Topic 8 Chapter 13 Oligopoly and Monopolistic Competition Econ 203 Topic 8 page 1 Oligopoly: How do firms behave when there are only a few competitors? These firms produce all or most of their industry

9 The optimum of Oligopoly

Microeconomics I - Lecture #9, December 1, 2008 9 The optimum of Oligopoly During previous lectures we have investigated two important forms of market structure: pure competition, where there are typically

Microeconomics I - Lecture #9, December 1, 2008 9 The optimum of Oligopoly During previous lectures we have investigated two important forms of market structure: pure competition, where there are typically

Oligopoly and Monopolistic Competition

Oligopoly and Monopolistic Competition Introduction Managerial Problem Airbus and Boeing are the only two manufacturers of large commercial aircrafts. If only one receives a government subsidy, how can

Oligopoly and Monopolistic Competition Introduction Managerial Problem Airbus and Boeing are the only two manufacturers of large commercial aircrafts. If only one receives a government subsidy, how can

Prof. Wolfram Elsner Faculty of Business Studies and Economics iino Institute of Institutional and Innovation Economics. Real-World Markets

Prof. Wolfram Elsner Faculty of Business Studies and Economics iino Institute of Institutional and Innovation Economics Real-World Markets Readings for this lecture Required reading this time: Real-World

Prof. Wolfram Elsner Faculty of Business Studies and Economics iino Institute of Institutional and Innovation Economics Real-World Markets Readings for this lecture Required reading this time: Real-World

Oligopoly Pricing. EC 202 Lecture IV. Francesco Nava. January London School of Economics. Nava (LSE) EC 202 Lecture IV Jan / 13

EC 202 Lecture IV Jan / 13") Oligopoly Pricing EC 202 Lecture IV Francesco Nava London School of Economics January 2011 Nava (LSE) EC 202 Lecture IV Jan 2011 1 / 13 Summary The models of competition presented in MT explored the consequences

Oligopoly Pricing EC 202 Lecture IV Francesco Nava London School of Economics January 2011 Nava (LSE) EC 202 Lecture IV Jan 2011 1 / 13 Summary The models of competition presented in MT explored the consequences

Part II. Market power

Part II. Market power Chapter 3. Static imperfect competition Slides Industrial Organization: Markets and Strategies Paul Belleflamme and Martin Peitz Cambridge University Press 2009 Introduction to Part

Part II. Market power Chapter 3. Static imperfect competition Slides Industrial Organization: Markets and Strategies Paul Belleflamme and Martin Peitz Cambridge University Press 2009 Introduction to Part

INTERMEDIATE MICROECONOMICS LECTURE 13 - MONOPOLISTIC COMPETITION AND OLIGOPOLY. Monopolistic Competition

13-1 INTERMEDIATE MICROECONOMICS LECTURE 13 - MONOPOLISTIC COMPETITION AND OLIGOPOLY Monopolistic Competition Pure monopoly and perfect competition are rare in the real world. Most real-world industries

13-1 INTERMEDIATE MICROECONOMICS LECTURE 13 - MONOPOLISTIC COMPETITION AND OLIGOPOLY Monopolistic Competition Pure monopoly and perfect competition are rare in the real world. Most real-world industries

The Analysis of Competitive Markets

C H A P T E R 12 The Analysis of Competitive Markets Prepared by: Fernando & Yvonn Quijano CHAPTER 12 OUTLINE 12.1 Monopolistic Competition 12.2 Oligopoly 12.3 Price Competition 12.4 Competition versus

C H A P T E R 12 The Analysis of Competitive Markets Prepared by: Fernando & Yvonn Quijano CHAPTER 12 OUTLINE 12.1 Monopolistic Competition 12.2 Oligopoly 12.3 Price Competition 12.4 Competition versus

Managerial Economics Chapter 9 Practice Question

ECO 3320 Lanlan Chu Managerial Economics Chapter 9 Practice Question 1. The market for widgets consists of two firms that produce identical products. Competition in the market is such that each of the

ECO 3320 Lanlan Chu Managerial Economics Chapter 9 Practice Question 1. The market for widgets consists of two firms that produce identical products. Competition in the market is such that each of the

UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A)

") UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Monopoly and oligopoly (PR 11.1-11.4 and 12.2-12.5) Advanced pricing with market power and equilibrium oligopolistic

UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Monopoly and oligopoly (PR 11.1-11.4 and 12.2-12.5) Advanced pricing with market power and equilibrium oligopolistic

UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Fall 2013

Fall 2013") UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Fall 2013 Pricing with market power and oligopolistic markets (PR 11.1-11.4 and 12.2-12.5) Module 4 Sep. 28, 2013

UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Fall 2013 Pricing with market power and oligopolistic markets (PR 11.1-11.4 and 12.2-12.5) Module 4 Sep. 28, 2013

Unit 13 AP Economics - Practice

DO NOT WRITE ON THIS TEST! Unit 13 AP Economics - Practice Multiple Choice Identify the choice that best completes the statement or answers the question. 1. A natural monopoly exists whenever a single

DO NOT WRITE ON THIS TEST! Unit 13 AP Economics - Practice Multiple Choice Identify the choice that best completes the statement or answers the question. 1. A natural monopoly exists whenever a single

Managerial Economics & Business Strategy Chapter 9. Basic Oligopoly Models

Managerial Economics & Business Strategy Chapter 9 Basic Oligopoly Models Overview I. Conditions for Oligopoly? II. Role of Strategic Interdependence III. Profit Maximization in Four Oligopoly Settings

Managerial Economics & Business Strategy Chapter 9 Basic Oligopoly Models Overview I. Conditions for Oligopoly? II. Role of Strategic Interdependence III. Profit Maximization in Four Oligopoly Settings

14.01 Principles of Microeconomics, Fall 2007 Chia-Hui Chen November 7, Lecture 22

Monopoly. Principles of Microeconomics, Fall Chia-Hui Chen November, Lecture Monopoly Outline. Chap : Monopoly. Chap : Shift in Demand and Effect of Tax Monopoly The monopolist is the single supply-side

Monopoly. Principles of Microeconomics, Fall Chia-Hui Chen November, Lecture Monopoly Outline. Chap : Monopoly. Chap : Shift in Demand and Effect of Tax Monopoly The monopolist is the single supply-side

Monopolistic Markets. Causes of Monopolies

Monopolistic Markets Causes of Monopolies The causes of monopolization Monoplositic resources Only one firm owns a resource which is crucial for production (e.g. diamond monopol of DeBeers). Monopols created

Monopolistic Markets Causes of Monopolies The causes of monopolization Monoplositic resources Only one firm owns a resource which is crucial for production (e.g. diamond monopol of DeBeers). Monopols created

Chapter 12. Oligopoly. Oligopoly Characteristics. ) of firms Product differentiation may or may not exist ) to entry. Chapter 12 2

of firms Product differentiation may or may not exist ) to entry. Chapter 12 2") Chapter Oligopoly Oligopoly Characteristics ( ) of firms Product differentiation may or may not exist ( ) to entry Chapter Oligopoly Equilibrium ( ) Equilibrium Firms are doing the best they can and have

Chapter Oligopoly Oligopoly Characteristics ( ) of firms Product differentiation may or may not exist ( ) to entry Chapter Oligopoly Equilibrium ( ) Equilibrium Firms are doing the best they can and have

Oligopoly and Monopolistic Competition

Oligopoly and Monopolistic Competition Introduction Managerial Problem Airbus and Boeing are the only two manufacturers of large commercial aircrafts. If only one receives a government subsidy, how can

Oligopoly and Monopolistic Competition Introduction Managerial Problem Airbus and Boeing are the only two manufacturers of large commercial aircrafts. If only one receives a government subsidy, how can

UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Monopoly Behavior Advanced Pricing with Market Power

Monopoly Behavior Advanced Pricing with Market Power") UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Monopoly Behavior Advanced Pricing with Market Power Session VI Sep 25, 2010 In a competitive market there are

UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Monopoly Behavior Advanced Pricing with Market Power Session VI Sep 25, 2010 In a competitive market there are

Chapter 13 MODELS OF MONOPOLY. Copyright 2005 by South-Western, a division of Thomson Learning. All rights reserved.

Chapter 13 MODELS OF MONOPOLY Copyright 2005 by South-Western, a division of Thomson Learning. All rights reserved. 1 Monopoly A monopoly is a single supplier to a market This firm may choose to produce

Chapter 13 MODELS OF MONOPOLY Copyright 2005 by South-Western, a division of Thomson Learning. All rights reserved. 1 Monopoly A monopoly is a single supplier to a market This firm may choose to produce

The Basic Spatial Model with a Single Monopolist

Economics 335 March 3, 999 Notes 8: Models of Spatial Competition I. Product differentiation A. Definition Products are said to be differentiated if consumers consider them to be imperfect substitutes.

Economics 335 March 3, 999 Notes 8: Models of Spatial Competition I. Product differentiation A. Definition Products are said to be differentiated if consumers consider them to be imperfect substitutes.

Finance 510 Midterm #2 Practice Questions

Finance 50 Midterm # Practice Questions ) ) Consider the following pricing game between Dell and Gateway. There are two types of demanders in the market, High and Low. High demanders value a computer at

Finance 50 Midterm # Practice Questions ) ) Consider the following pricing game between Dell and Gateway. There are two types of demanders in the market, High and Low. High demanders value a computer at

29/02/2016. Market structure II- Other types of imperfect competition. What Is Monopolistic Competition? OTHER TYPES OF IMPERFECT COMPETITION

Market structure II- Other types of imperfect competition OTHER TYPES OF IMPERFECT COMPETITION Characteristics of Monopolistic Competition Monopolistic competition is a market structure in which many firms

Market structure II- Other types of imperfect competition OTHER TYPES OF IMPERFECT COMPETITION Characteristics of Monopolistic Competition Monopolistic competition is a market structure in which many firms

ECONOMICS. Paper 3 : Fundamentals of Microeconomic Theory Module 28 : Non collusive and Collusive model

Subject Paper No and Title Module No and Title Module Tag 3 : Fundamentals of Microeconomic Theory 28 : Non collusive and Collusive model ECO_P3_M28 TABLE OF CONTENTS 1. Learning Outcomes 2. Introduction

Subject Paper No and Title Module No and Title Module Tag 3 : Fundamentals of Microeconomic Theory 28 : Non collusive and Collusive model ECO_P3_M28 TABLE OF CONTENTS 1. Learning Outcomes 2. Introduction

Networks, Telecommunications Economics and Strategic Issues in Digital Convergence. Prof. Nicholas Economides. Spring 2006

Networks, Telecommunications Economics and Strategic Issues in Digital Convergence Prof. Nicholas Economides Spring 2006 Basic Market Structure Slides The Structure-Conduct-Performance Model Basic conditions:

Networks, Telecommunications Economics and Strategic Issues in Digital Convergence Prof. Nicholas Economides Spring 2006 Basic Market Structure Slides The Structure-Conduct-Performance Model Basic conditions:

Final Exam - Solutions

Ecn 100 - Intermediate Microeconomic Theory University of California - Davis December 10, 009 Instructor: John Parman Final Exam - Solutions You have until 1:30pm to complete this exam. Be certain to put

Ecn 100 - Intermediate Microeconomic Theory University of California - Davis December 10, 009 Instructor: John Parman Final Exam - Solutions You have until 1:30pm to complete this exam. Be certain to put

OLIGOPOLY: Characteristics

OBJECTIVES Explain how managers of firms that operate in an oligopoly market can use strategic decision making to maintain relatively high profits Understand how the reactions of market rivals influence

OBJECTIVES Explain how managers of firms that operate in an oligopoly market can use strategic decision making to maintain relatively high profits Understand how the reactions of market rivals influence

Lecture 22. Oligopoly & Monopolistic Competition

Lecture 22. Oligopoly & Monopolistic Competition Course Evaluations on Thursday: Be sure to bring laptop, smartphone, or tablet with browser, so that you can complete your evaluation in class. Oligopoly

Lecture 22. Oligopoly & Monopolistic Competition Course Evaluations on Thursday: Be sure to bring laptop, smartphone, or tablet with browser, so that you can complete your evaluation in class. Oligopoly

EconS Oligopoly - Part 1

EconS 305 - Oligopoly - Part 1 Eric Dunaway Washington State University eric.dunaway@wsu.edu November 19, 2015 Eric Dunaway (WSU) EconS 305 - Lecture 31 November 19, 2015 1 / 32 Introduction We are now

EconS 305 - Oligopoly - Part 1 Eric Dunaway Washington State University eric.dunaway@wsu.edu November 19, 2015 Eric Dunaway (WSU) EconS 305 - Lecture 31 November 19, 2015 1 / 32 Introduction We are now

Eco 300 Intermediate Micro

Eco 300 Intermediate Micro Instructor: Amalia Jerison Office Hours: T 12:00-1:00, Th 12:00-1:00, and by appointment BA 127A, aj4575@albany.edu A. Jerison (BA 127A) Eco 300 Spring 2010 1 / 61 Monopoly Market

Eco 300 Intermediate Micro Instructor: Amalia Jerison Office Hours: T 12:00-1:00, Th 12:00-1:00, and by appointment BA 127A, aj4575@albany.edu A. Jerison (BA 127A) Eco 300 Spring 2010 1 / 61 Monopoly Market

ECN 3103 INDUSTRIAL ORGANISATION

ECN 3103 INDUSTRIAL ORGANISATION 5. Game Theory Mr. Sydney Armstrong Lecturer 1 The University of Guyana 1 Semester 1, 2016 OUR PLAN Analyze Strategic price and Quantity Competition (Noncooperative Oligopolies)

ECN 3103 INDUSTRIAL ORGANISATION 5. Game Theory Mr. Sydney Armstrong Lecturer 1 The University of Guyana 1 Semester 1, 2016 OUR PLAN Analyze Strategic price and Quantity Competition (Noncooperative Oligopolies)

Economics 101 Midterm Exam #2. April 9, Instructions

Economics 101 Spring 2009 Professor Wallace Economics 101 Midterm Exam #2 April 9, 2009 Instructions Do not open the exam until you are instructed to begin. You will need a #2 lead pencil. If you do not

Economics 101 Spring 2009 Professor Wallace Economics 101 Midterm Exam #2 April 9, 2009 Instructions Do not open the exam until you are instructed to begin. You will need a #2 lead pencil. If you do not

Solutions to Final Exam

Solutions to Final Exam AEC 504 - Summer 2007 Fundamentals of Economics c 2007 Alexander Barinov 1 Veni, vidi, vici (30 points) Two firms with constant marginal costs serve two markets for two different

Solutions to Final Exam AEC 504 - Summer 2007 Fundamentals of Economics c 2007 Alexander Barinov 1 Veni, vidi, vici (30 points) Two firms with constant marginal costs serve two markets for two different

Firm Supply. Market demand. Demand curve facing firm

Firm Supply 84 Firm Supply A. Firms face two sorts of constraints 1. technological constraints summarize in cost function 2. market constraints how will consumers and other firms react to a given firm

Firm Supply 84 Firm Supply A. Firms face two sorts of constraints 1. technological constraints summarize in cost function 2. market constraints how will consumers and other firms react to a given firm

14.27 Economics and E-Commerce Fall 14. Lecture 2 - Review

14.27 Economics and E-Commerce Fall 14 Lecture 2 - Review Prof. Sara Ellison MIT OpenCourseWare 4 basic things I want to get across in this review: Monopoly pricing function of demand, elasticity, & marginal

14.27 Economics and E-Commerce Fall 14 Lecture 2 - Review Prof. Sara Ellison MIT OpenCourseWare 4 basic things I want to get across in this review: Monopoly pricing function of demand, elasticity, & marginal

Quiz #5 Week 04/12/2009 to 04/18/2009

Quiz #5 Week 04/12/2009 to 04/18/2009 You have 30 minutes to answer the following 17 multiple choice questions. Record your answers in the bubble sheet. Your grade in this quiz will count for 1% of your

Quiz #5 Week 04/12/2009 to 04/18/2009 You have 30 minutes to answer the following 17 multiple choice questions. Record your answers in the bubble sheet. Your grade in this quiz will count for 1% of your

ECON 115. Industrial Organization

ECON 115 Industrial Organization 1. Review of the First Midterm 2. Review of Price Discrimination, Product Differentiation & Bundling 3. Introduction to Oligopolies 4. Introduction to Game Theory and Cournot

ECON 115 Industrial Organization 1. Review of the First Midterm 2. Review of Price Discrimination, Product Differentiation & Bundling 3. Introduction to Oligopolies 4. Introduction to Game Theory and Cournot

Chapter 12. Oligopoly. Oligopoly Characteristics. Oligopoly Equilibrium

Chapter Oligopoly Oligopoly Characteristics Small number of firms Product differentiation may or may not eist Barriers to entry Chapter Oligopoly Equilibrium Defining Equilibrium Firms are doing the best

Chapter Oligopoly Oligopoly Characteristics Small number of firms Product differentiation may or may not eist Barriers to entry Chapter Oligopoly Equilibrium Defining Equilibrium Firms are doing the best

Monopolistic Markets. Regulation

Monopolistic Markets Regulation Comparison of monopolistic and competitive equilibrium output The profits of a monopolist are maximized when MC(Q M ) = P(Q M ) + Q P (Q M ) negative In a competitive market:

Monopolistic Markets Regulation Comparison of monopolistic and competitive equilibrium output The profits of a monopolist are maximized when MC(Q M ) = P(Q M ) + Q P (Q M ) negative In a competitive market:

UNIVERSITY OF CAPE COAST CAPE COAST - GHANA BASIC OLIGOPOLY MODELS

UNIVERSITY OF CAPE COAST CAPE COAST - GHANA BASIC OLIGOPOLY MODELS Overview I. Conditions for Oligopoly? II. Role of Strategic Interdependence III. Profit Maximization in Four Oligopoly Settings Sweezy

UNIVERSITY OF CAPE COAST CAPE COAST - GHANA BASIC OLIGOPOLY MODELS Overview I. Conditions for Oligopoly? II. Role of Strategic Interdependence III. Profit Maximization in Four Oligopoly Settings Sweezy

ECON 230D2-002 Mid-term 1. Student Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

ECON 230D2-002 Mid-term 1 Name Student Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. Scenario 12.3: Suppose a stream is discovered whose

ECON 230D2-002 Mid-term 1 Name Student Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. Scenario 12.3: Suppose a stream is discovered whose

Economics 384 B1. Intermediate Microeconomics II. Assignment 2. S Landon Winter 2007

Economics 384 B1 Intermediate Microeconomics II Assignment 2 S Landon Winter 2007 Due: By 4:00pm, 2 April 2007 This assignment will be marked out of 100. The maximum number of marks that can be earned

Economics 384 B1 Intermediate Microeconomics II Assignment 2 S Landon Winter 2007 Due: By 4:00pm, 2 April 2007 This assignment will be marked out of 100. The maximum number of marks that can be earned

Do not open this exam until told to do so. Solution

Do not open this exam until told to do so. Department of Economics College of Social and Applied Human Sciences K. Annen, Fall 003 Final (Version): Intermediate Microeconomics (ECON30) Solution Final (Version

Do not open this exam until told to do so. Department of Economics College of Social and Applied Human Sciences K. Annen, Fall 003 Final (Version): Intermediate Microeconomics (ECON30) Solution Final (Version

Economics 203: Intermediate Microeconomics I. Sample Final Exam 1. Instructor: Dr. Donna Feir

Last Name: First Name: Student Number: Economics 203: Intermediate Microeconomics I Sample Final Exam 1 Instructor: Dr. Donna Feir Instructions: Make sure you write your name and student number at the

Last Name: First Name: Student Number: Economics 203: Intermediate Microeconomics I Sample Final Exam 1 Instructor: Dr. Donna Feir Instructions: Make sure you write your name and student number at the

Microeconomics. Claudia Vogel EUV. Winter Term 2009/2010. Market Power: Monopoly and Monopsony

Microeconomics Claudia Vogel EUV Winter Term 2009/2010 Claudia Vogel (EUV) Microeconomics Winter Term 2009/2010 1 / 34 Lecture Outline Part III Market Structure and Competitive Strategy 10 The Social Costs

Microeconomics Claudia Vogel EUV Winter Term 2009/2010 Claudia Vogel (EUV) Microeconomics Winter Term 2009/2010 1 / 34 Lecture Outline Part III Market Structure and Competitive Strategy 10 The Social Costs

Business Economics BUSINESS ECONOMICS. PAPER No. 1: MICROECONOMIC ANALYSIS MODULE No. 24: NON-COLLUSIVE OLIGOPOLY I

Subject Business Economics Paper No and Title Module No and Title Module Tag 1, Microeconomic Analysis 4, Non-Collusive Oligopoly I BSE_P1_M4 TABLE OF CONTENTS 1. Learning Outcomes. Introduction 3. Cournot

Subject Business Economics Paper No and Title Module No and Title Module Tag 1, Microeconomic Analysis 4, Non-Collusive Oligopoly I BSE_P1_M4 TABLE OF CONTENTS 1. Learning Outcomes. Introduction 3. Cournot

Seminar 3 Monopoly. Simona Montagnana. Week 25 March 20, 2017

Seminar 3 Monopoly Simona Montagnana Week 25 March 20, 2017 2/41 Question 2 2. Explain carefully why a natural monopoly might occur. a Discuss the problem of using marginal cost pricing to regulate a natural

Seminar 3 Monopoly Simona Montagnana Week 25 March 20, 2017 2/41 Question 2 2. Explain carefully why a natural monopoly might occur. a Discuss the problem of using marginal cost pricing to regulate a natural

14.1 Comparison of Market Structures

14.1 Comparison of Structures Chapter 14 Oligopoly 14-2 14.2 Cartels Cartel in Korea Oligopolistic firms have an incentive to collude, coordinate setting their prices or quantities, so as to increase their

14.1 Comparison of Structures Chapter 14 Oligopoly 14-2 14.2 Cartels Cartel in Korea Oligopolistic firms have an incentive to collude, coordinate setting their prices or quantities, so as to increase their

Part IV. Pricing strategies and market segmentation

Part IV. Pricing strategies and market segmentation Chapter 8. Group pricing and personalized pricing Slides Industrial Organization: Markets and Strategies Paul Belleflamme and Martin Peitz Cambridge

Part IV. Pricing strategies and market segmentation Chapter 8. Group pricing and personalized pricing Slides Industrial Organization: Markets and Strategies Paul Belleflamme and Martin Peitz Cambridge

1.. Consider the following multi-stage game. In the first stage an incumbent monopolist

University of California, Davis Department of Economics Time: 3 hours Reading time: 20 minutes PRELIMINARY EXAMINATION FOR THE Ph.D. DEGREE Industrial Organization June 27, 2006 Answer four of the six

University of California, Davis Department of Economics Time: 3 hours Reading time: 20 minutes PRELIMINARY EXAMINATION FOR THE Ph.D. DEGREE Industrial Organization June 27, 2006 Answer four of the six

UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Leftovers, review and takeaways Lectures Oct.

Leftovers, review and takeaways Lectures Oct.") UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Leftovers, review and takeaways Lectures 13-14 Oct. 1, 2011 Pricing While there is some involved analysis required,

UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Leftovers, review and takeaways Lectures 13-14 Oct. 1, 2011 Pricing While there is some involved analysis required,

ECON 2100 Principles of Microeconomics (Summer 2016) Monopoly

Monopoly") ECON 21 Principles of Microeconomics (Summer 216) Monopoly Relevant readings from the textbook: Mankiw, Ch. 15 Monopoly Suggested problems from the textbook: Chapter 15 Questions for Review (Page 323):

ECON 21 Principles of Microeconomics (Summer 216) Monopoly Relevant readings from the textbook: Mankiw, Ch. 15 Monopoly Suggested problems from the textbook: Chapter 15 Questions for Review (Page 323):

University of Victoria Winter Econ 203 Problem Set 3

University of Victoria Winter 2017 Econ 203 Problem Set 3 Coverage: Some extra questions on Chapter 11 Perfect Competition ; Chapter 12 Monopoly ; Chapter 13A: Game Theory. There are also some Chapter

University of Victoria Winter 2017 Econ 203 Problem Set 3 Coverage: Some extra questions on Chapter 11 Perfect Competition ; Chapter 12 Monopoly ; Chapter 13A: Game Theory. There are also some Chapter

Principles of Economics. January 2018

Principles of Economics January 2018 Monopoly Contents Market structures 14 Monopoly 15 Monopolistic competition 16 Oligopoly Principles of Economics January 2018 2 / 39 Monopoly Market power In a competitive

Principles of Economics January 2018 Monopoly Contents Market structures 14 Monopoly 15 Monopolistic competition 16 Oligopoly Principles of Economics January 2018 2 / 39 Monopoly Market power In a competitive

Game Theory & Firms. Jacob LaRiviere & Justin Rao April 20, 2016 Econ 404, Spring 2016

Game Theory & Firms Jacob LaRiviere & Justin Rao April 20, 2016 Econ 404, Spring 2016 What is Game Theory? Game Theory Intuitive Definition: Theory of strategic interaction Technical Definition: Account

Game Theory & Firms Jacob LaRiviere & Justin Rao April 20, 2016 Econ 404, Spring 2016 What is Game Theory? Game Theory Intuitive Definition: Theory of strategic interaction Technical Definition: Account

Unit 7. Firm behaviour and market structure: monopoly

Unit 7. Firm behaviour and market structure: monopoly Quiz 1. What of the following can be considered as the measure of a market power? A. ; B. ; C.. Answers A and B are both correct; E. All of the above

Unit 7. Firm behaviour and market structure: monopoly Quiz 1. What of the following can be considered as the measure of a market power? A. ; B. ; C.. Answers A and B are both correct; E. All of the above

Economics 101 Spring 2001 Section 4 - Hallam Quiz 10. For questions 1-9, consider firms using a technology with cost and marginal cost functions:

Economics 101 Spring 2001 Section 4 - Hallam Quiz 10 For questions 1-9, consider firms using a technology with cost and marginal cost functions: Cost (q) = 256 + 16 q + q 2 MC(q) = 16 + 2q 1. What is the

Economics 101 Spring 2001 Section 4 - Hallam Quiz 10 For questions 1-9, consider firms using a technology with cost and marginal cost functions: Cost (q) = 256 + 16 q + q 2 MC(q) = 16 + 2q 1. What is the

Chapter 9: Static Games and Cournot Competition

Chapter 9: Static Games and Cournot Competition Learning Objectives: Students should learn to:. The student will understand the ideas of strategic interdependence and reasoning strategically and be able

Chapter 9: Static Games and Cournot Competition Learning Objectives: Students should learn to:. The student will understand the ideas of strategic interdependence and reasoning strategically and be able

Microeconomics. Use the Following Graph to Answer Question 3

More Tutorial at www.dumblittledoctor.com Microeconomics 1. To an economist, a good is scarce when: *a. the amount of the good available is less than the amount that people want when the good's price equals

More Tutorial at www.dumblittledoctor.com Microeconomics 1. To an economist, a good is scarce when: *a. the amount of the good available is less than the amount that people want when the good's price equals

Ecn Intermediate Microeconomic Theory University of California - Davis December 10, 2009 Instructor: John Parman. Final Exam

Ecn 100 - Intermediate Microeconomic Theory University of California - Davis December 10, 2009 Instructor: John Parman Final Exam You have until 12:30pm to complete this exam. Be certain to put your name,

Ecn 100 - Intermediate Microeconomic Theory University of California - Davis December 10, 2009 Instructor: John Parman Final Exam You have until 12:30pm to complete this exam. Be certain to put your name,

The homework is due on Wednesday, December 7 at 4pm. Each question is worth 0.8 points.

Homework 9: Econ500 Fall, 2016 The homework is due on Wednesday, December 7 at 4pm. Each question is worth 0.8 points. Question 1 Suppose that all firms in a competitive industry have cost function c(q)=

Homework 9: Econ500 Fall, 2016 The homework is due on Wednesday, December 7 at 4pm. Each question is worth 0.8 points. Question 1 Suppose that all firms in a competitive industry have cost function c(q)=

Chapter 15: Industrial Organization

Chapter 15: Industrial Organization Imperfect Competition Product Differentiation Advertising Monopolistic Competition Oligopoly Collusion Cournot Model Stackelberg Model Bertrand Model Cartel Legal Provisions

Chapter 15: Industrial Organization Imperfect Competition Product Differentiation Advertising Monopolistic Competition Oligopoly Collusion Cournot Model Stackelberg Model Bertrand Model Cartel Legal Provisions

Economics of Industrial Organization. Lecture 12: Mergers

Economics of Industrial Organization Lecture 12: Mergers Mergers Thus far we have talked about industry dynamics in terms of firms entering and exiting the industry, and have assumed that all these firms

Economics of Industrial Organization Lecture 12: Mergers Mergers Thus far we have talked about industry dynamics in terms of firms entering and exiting the industry, and have assumed that all these firms

Lecture 2 OLIGOPOLY Copyright 2012 Pearson Education. All rights reserved.

Lecture 2 OLIGOPOLY 13-1 Copyright 2012 Pearson Education. All rights reserved. Chapter 13 Topics Market Structures ( A Recap). Noncooperative Oligopoly. Cournot Model. Stackelberg Model. Bertrand Model.

Lecture 2 OLIGOPOLY 13-1 Copyright 2012 Pearson Education. All rights reserved. Chapter 13 Topics Market Structures ( A Recap). Noncooperative Oligopoly. Cournot Model. Stackelberg Model. Bertrand Model.

Final Examination Suggested Solution ECON 201

Final Examination Suggested Solution ECON 201 Beomsoo Kim Spring 2014 1. (16 points, 4 points each)write down the definition of the following terms a) Positive Externality Action by either a producer or

Final Examination Suggested Solution ECON 201 Beomsoo Kim Spring 2014 1. (16 points, 4 points each)write down the definition of the following terms a) Positive Externality Action by either a producer or

Chapter 15 Oligopoly

Goldwasser AP Microeconomics Chapter 15 Oligopoly BEFORE YOU READ THE CHAPTER Summary This chapter explores oligopoly, a market structure characterized by a few firms producing a product that mayor may

Goldwasser AP Microeconomics Chapter 15 Oligopoly BEFORE YOU READ THE CHAPTER Summary This chapter explores oligopoly, a market structure characterized by a few firms producing a product that mayor may

Textbook questions: Competitors and Competition

Competitors and Competition This chapter focuses on how market structure affects competition. It begins with a discussion of how to identify competitors, define markets, and describe the market structure.

Competitors and Competition This chapter focuses on how market structure affects competition. It begins with a discussion of how to identify competitors, define markets, and describe the market structure.

ECON 311 MICROECONOMICS THEORY I

ECON 311 MICROECONOMICS THEORY I Profit Maximisation & Perfect Competition (Short-Run) Dr. F. Kwame Agyire-Tettey Department of Economics Contact Information: fagyire-tettey@ug.edu.gh Session Overview

ECON 311 MICROECONOMICS THEORY I Profit Maximisation & Perfect Competition (Short-Run) Dr. F. Kwame Agyire-Tettey Department of Economics Contact Information: fagyire-tettey@ug.edu.gh Session Overview

Economics II - October 27, 2009 Based on H.R.Varian - Intermediate Microeconomics. A Modern Approach

Economics II - October 7, 009 Based on H.R.Varian - Intermediate Microeconomics. A Modern Approach GAME THEORY Economic agents can interact strategically in a variety of ways, and many of these have been

Economics II - October 7, 009 Based on H.R.Varian - Intermediate Microeconomics. A Modern Approach GAME THEORY Economic agents can interact strategically in a variety of ways, and many of these have been

Economics 335, Spring 1999 Problem Set #9

Economics 335, Spring 1999 Problem Set #9 Name: 1. Two firms share a market with demand curve Q ã 120 " 1 2 p Each has cost function CŸy ã 1300 ò y 2 a. What is the outcome in this market if these firms

Economics 335, Spring 1999 Problem Set #9 Name: 1. Two firms share a market with demand curve Q ã 120 " 1 2 p Each has cost function CŸy ã 1300 ò y 2 a. What is the outcome in this market if these firms

Introduction. Managerial Problem. Solution Approach

Monopoly Introduction Managerial Problem Drug firms have patents that expire after 20 years and one expects drug prices to fall once generic drugs enter the market. However, as evidence shows, often prices

Monopoly Introduction Managerial Problem Drug firms have patents that expire after 20 years and one expects drug prices to fall once generic drugs enter the market. However, as evidence shows, often prices

Market Structure & Imperfect Competition

In the Name of God Sharif University of Technology Graduate School of Management and Economics Microeconomics (for MBA students) 44111 (1393-94 1 st term) - Group 2 Dr. S. Farshad Fatemi Market Structure

In the Name of God Sharif University of Technology Graduate School of Management and Economics Microeconomics (for MBA students) 44111 (1393-94 1 st term) - Group 2 Dr. S. Farshad Fatemi Market Structure

INTRODUCTORY ECONOMICS

4265 FIRST PUBLIC EXAMINATION Preliminary Examination for Philosophy, Politics and Economics Preliminary Examination for Economics and Management Preliminary Examination for History and Economics INTRODUCTORY

4265 FIRST PUBLIC EXAMINATION Preliminary Examination for Philosophy, Politics and Economics Preliminary Examination for Economics and Management Preliminary Examination for History and Economics INTRODUCTORY

AP Microeconomics: Test 5 Study Guide

AP Microeconomics: Test 5 Study Guide Mr. Warkentin nwarkentin@wyomingseminary.org 203 Sprague Hall 2017-2018 Academic Year Directions: The purpose of this sheet is to quickly capture the topics and skills

AP Microeconomics: Test 5 Study Guide Mr. Warkentin nwarkentin@wyomingseminary.org 203 Sprague Hall 2017-2018 Academic Year Directions: The purpose of this sheet is to quickly capture the topics and skills

Agenda. Profit Maximization by a Monopolist. 1. Profit Maximization by a Monopolist. 2. Marginal Revenue. 3. Profit Maximization Exercise

Agenda 1. Profit Maximization by a Monopolist 2. Marginal Revenue 3. Profit Maximization Exercise 4. Effect of Elasticities on Monopoly Price 5. Comparative Statics of Monopoly 6. Monopolist with Multiple

Agenda 1. Profit Maximization by a Monopolist 2. Marginal Revenue 3. Profit Maximization Exercise 4. Effect of Elasticities on Monopoly Price 5. Comparative Statics of Monopoly 6. Monopolist with Multiple

A few firms Imperfect Competition Oligopoly. Figure 8.1: Market structures

8.1 Setup Monopoly is a single firm producing a particular commodity. It can affect the market by changing the quantity; via the (inverse) demand function p (q). The tradeoff: either sell a lot cheaply,

8.1 Setup Monopoly is a single firm producing a particular commodity. It can affect the market by changing the quantity; via the (inverse) demand function p (q). The tradeoff: either sell a lot cheaply,

Contents. Concepts of Revenue I-13. About the authors I-5 Preface I-7 Syllabus I-9 Chapter-heads I-11

Contents About the authors I-5 Preface I-7 Syllabus I-9 Chapter-heads I-11 1 Concepts of Revenue 1.1 Introduction 1 1.2 Concepts of Revenue 2 1.3 Revenue curves under perfect competition 3 1.4 Revenue

Contents About the authors I-5 Preface I-7 Syllabus I-9 Chapter-heads I-11 1 Concepts of Revenue 1.1 Introduction 1 1.2 Concepts of Revenue 2 1.3 Revenue curves under perfect competition 3 1.4 Revenue

EXAMINATION #4 VERSION C General Equilibrium and Market Power November 24, 2015

Signature: William M. Boal Printed name: EXAMINATION #4 VERSION C General Equilibrium and Market Power November 24, 2015 INSTRUCTIONS: This exam is closed-book, closed-notes. Calculators, mobile phones,

Signature: William M. Boal Printed name: EXAMINATION #4 VERSION C General Equilibrium and Market Power November 24, 2015 INSTRUCTIONS: This exam is closed-book, closed-notes. Calculators, mobile phones,

Principles of Microeconomics Assignment 8 (Chapter 10) Answer Sheet. Class Day/Time

Answer Sheet. Class Day/Time") 1 Principles of Microeconomics Assignment 8 (Chapter 10) Answer Sheet Name Class Day/Time Questions of this homework are in the next few pages. Please find the answer of the questions and fill in the blanks

1 Principles of Microeconomics Assignment 8 (Chapter 10) Answer Sheet Name Class Day/Time Questions of this homework are in the next few pages. Please find the answer of the questions and fill in the blanks

INTERPRETATION. SOURCES OF MONOPOLY (Related to P-R pp )

") ECO 300 Fall 2005 November 10 MONOPOLY PART 1 INTERPRETATION Literally, just one firm in an industry But interpretation depends on how you define industry General idea a group of commodities that are close

ECO 300 Fall 2005 November 10 MONOPOLY PART 1 INTERPRETATION Literally, just one firm in an industry But interpretation depends on how you define industry General idea a group of commodities that are close

ECON6021. Market Structure. Profit Maximization. Monopoly a single firm A patented drug to cure SARS A single power supplier on HK Island

Market Structure ECON6021 Oligopoly Monopoly a single firm A patented drug to cure SARS A single power supplier on HK Island Oligopoly a few major players The top 4 cereal manufacturers sell 90% of all

Market Structure ECON6021 Oligopoly Monopoly a single firm A patented drug to cure SARS A single power supplier on HK Island Oligopoly a few major players The top 4 cereal manufacturers sell 90% of all

All but which of the following are true in the long-run for a competitive firm that maximizes profits?

Microeconomics, Module 11: Monopoly (Chapter 10) Illustrative Test Questions (The attached PDF file has better formatting.) Question 11.1: Profit Maximization: Monopoly Which of the following is true in

Microeconomics, Module 11: Monopoly (Chapter 10) Illustrative Test Questions (The attached PDF file has better formatting.) Question 11.1: Profit Maximization: Monopoly Which of the following is true in

Oligopoly. Fun and games. An oligopolist is one of a small number of producers in an industry. The industry is an oligopoly.

Oligopoly Fun and games Oligopoly An oligopolist is one of a small number of producers in an industry. The industry is an oligopoly. All oligopolists produce a standardized product. (If producers in an

Oligopoly Fun and games Oligopoly An oligopolist is one of a small number of producers in an industry. The industry is an oligopoly. All oligopolists produce a standardized product. (If producers in an

AP Microeconomics Review Session #3 Key Terms & Concepts

The Firm, Profit, and the Costs of Production 1. Explicit vs. implicit costs 2. Short-run vs. long-run decisions 3. Fixed inputs vs. variable inputs 4. Short-run production measures: be able to calculate/graph

The Firm, Profit, and the Costs of Production 1. Explicit vs. implicit costs 2. Short-run vs. long-run decisions 3. Fixed inputs vs. variable inputs 4. Short-run production measures: be able to calculate/graph

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Micro - HW 4 MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) In central Florida during the spring, strawberry growers are price takers. The reason

Micro - HW 4 MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) In central Florida during the spring, strawberry growers are price takers. The reason

Chapter 8 Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets

Managerial Economics & Business Strategy Chapter 8 Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All

Managerial Economics & Business Strategy Chapter 8 Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All

C H A P T E R 12. Monopolistic Competition and Oligopoly CHAPTER OUTLINE

C H A P T E R 12 Monopolistic Competition and Oligopoly CHAPTER OUTLINE 12.1 Monopolistic Competition 12.2 Oligopoly 12.3 Price Competition 12.4 Competition versus Collusion: The Prisoners Dilemma 12.5

C H A P T E R 12 Monopolistic Competition and Oligopoly CHAPTER OUTLINE 12.1 Monopolistic Competition 12.2 Oligopoly 12.3 Price Competition 12.4 Competition versus Collusion: The Prisoners Dilemma 12.5

Economics 361 Assessment

Economics 361 Assessment (1) Learning Objectives: Students who complete Economics 361 are expected to be able to use microeconomics as a means for evaluating alternative choices (e.g., policy choices;

Economics 361 Assessment (1) Learning Objectives: Students who complete Economics 361 are expected to be able to use microeconomics as a means for evaluating alternative choices (e.g., policy choices;

Overview 11/6/2014. Herfindahl Hirshman index of market concentration ...

Overview Market Structure and Competition Chapter 3 explores different types of market structures. Markets differ on two important dimensions: the number of firms, and the nature of product differentiation.

Overview Market Structure and Competition Chapter 3 explores different types of market structures. Markets differ on two important dimensions: the number of firms, and the nature of product differentiation.

Chapter 13. Oligopoly and Monopolistic Competition

Chapter 13 Oligopoly and Monopolistic Competition Chapter Outline Some Specific Oligopoly Models : Cournot, Bertrand and Stackelberg Competition When There are Increasing Returns to Scale Monopolistic

Chapter 13 Oligopoly and Monopolistic Competition Chapter Outline Some Specific Oligopoly Models : Cournot, Bertrand and Stackelberg Competition When There are Increasing Returns to Scale Monopolistic

Chapter 13. Chapter Outline. Some Specific Oligopoly Models : Cournot, Bertrand and Stackelberg Competition When There are Increasing Returns to Scale

Chapter 13 Oligopoly and Monopolistic Competition Chapter Outline Some Specific Oligopoly Models : Cournot, Bertrand and Stackelberg Competition When There are Increasing Returns to Scale Monopolistic

Chapter 13 Oligopoly and Monopolistic Competition Chapter Outline Some Specific Oligopoly Models : Cournot, Bertrand and Stackelberg Competition When There are Increasing Returns to Scale Monopolistic

Many sellers: There are many firms competing for the same group of customers.

Microeconomics 2 Chapter 16 Monopolistic Competition 16-1 Between monopoly and perfect Competition One type of imperfectly competitive market is an oligopoly, a market with only a few sellers, each offering

Microeconomics 2 Chapter 16 Monopolistic Competition 16-1 Between monopoly and perfect Competition One type of imperfectly competitive market is an oligopoly, a market with only a few sellers, each offering

Monopoly and How It Arises

Monopoly and How It Arises A monopoly is a market: That produces a good or service for which no close substitute exists In which there is one supplier that is protected from competition by a barrier preventing

Monopoly and How It Arises A monopoly is a market: That produces a good or service for which no close substitute exists In which there is one supplier that is protected from competition by a barrier preventing

Intermediate Microeconomics IMPERFECT COMPETITION BEN VAN KAMMEN, PHD PURDUE UNIVERSITY

Intermediate Microeconomics IMPERFECT COMPETITION BEN VAN KAMMEN, PHD PURDUE UNIVERSITY No, not the BCS Oligopoly: A market with few firms but more than one. Duopoly: A market with two firms. Cartel: Several

Intermediate Microeconomics IMPERFECT COMPETITION BEN VAN KAMMEN, PHD PURDUE UNIVERSITY No, not the BCS Oligopoly: A market with few firms but more than one. Duopoly: A market with two firms. Cartel: Several

14.54 International Trade Lecture 17: Increasing Returns to Scale

14.54 International Trade Lecture 17: Increasing Returns to Scale 14.54 Week 11 Fall 2016 14.54 (Week 11) Increasing Returns Fall 2016 1 / 25 Today s Plan 1 2 Increasing Returns to Scale: General Discussion

14.54 International Trade Lecture 17: Increasing Returns to Scale 14.54 Week 11 Fall 2016 14.54 (Week 11) Increasing Returns Fall 2016 1 / 25 Today s Plan 1 2 Increasing Returns to Scale: General Discussion