Which store has the lower costs: Wal-Mart or 7-Eleven? 2013 Pearson

|

|

|

- Frank Russell

- 6 years ago

- Views:

Transcription

1

2 Which store has the lower costs: Wal-Mart or 7-Eleven?

3 Production and Cost 14 When you have completed your study of this chapter, you will be able to 1 Explain and distinguish between the economic and accounting measures of a firm s cost of production and profit. 2 Explain the relationship between a firm s output and labor employed in the short run. 3 Explain the relationship between a firm s output and costs in the short run. 4 Derive and explain a firm s long-run average cost curve. CHAPTER CHECKLIST

4 14.1 ECONOMIC COST AND PROFIT The Firm s Goal To maximize profit Accounting Cost and Profit An accountant measures cost and profit to ensure that the firm pays the correct amount of income tax and to show the bank how the firm has used its bank loan. Economists predict the decisions that a firm makes to maximize its profit. These decisions respond to opportunity cost and economic profit.

5 14.1 ECONOMIC COST AND PROFIT Opportunity Cost The highest-valued alternative forgone is the opportunity cost of a firm s production. This opportunity cost is the amount that the firm must pay the owners of the factors of production it employs to attract them from their best alternative use. So a firm s opportunity cost of production is the cost of the factors of production it employs.

6 14.1 ECONOMIC COST AND PROFIT Explicit Costs and Implicit Costs An explicit cost is a cost paid in money. An implicit cost is an opportunity cost incurred by a firm when it uses a factor of production for which it does not make a direct money payment. The two main implicit costs are economic depreciation and the cost of using the firm owner s resources.

7 14.1 ECONOMIC COST AND PROFIT Economic depreciation is an opportunity cost of a firm using capital that it owns measured as the change in the market value of capital over a given period. Normal profit is the return to entrepreneurship. Normal profit is part of a firm s opportunity cost because it is the cost of the entrepreneur not running another firm.

8 14.1 ECONOMIC COST AND PROFIT Economic Profit A firm s economic profit equals total revenue minus total cost. Total cost is the sum of the explicit costs and implicit costs and is the opportunity cost of production. Because the firm s implicit costs is normal profit, the return to the entrepreneur equals normal profit plus economic profit. If a firm incurs an economic loss, the entrepreneur receives less than normal profit.

9 14.1 ECONOMIC COST AND PROFIT

10

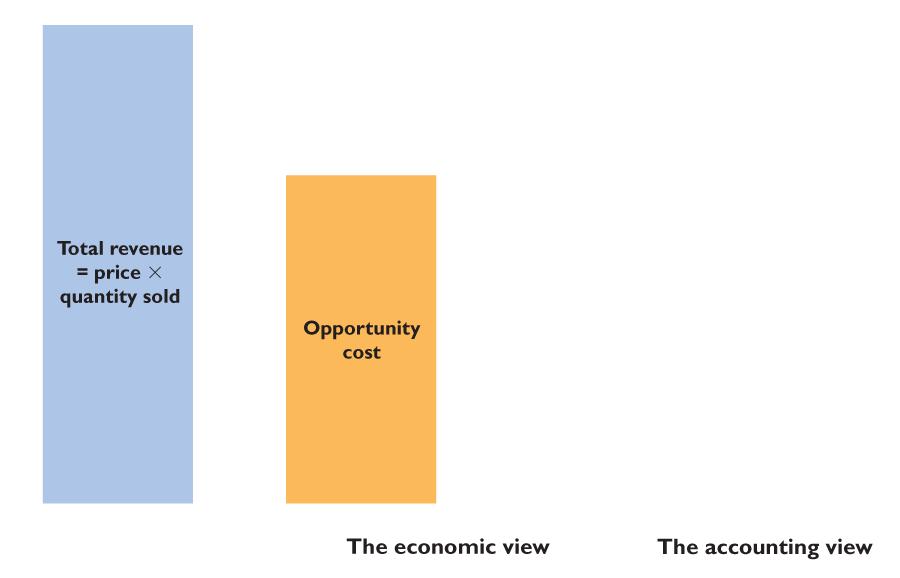

11 14.1 ECONOMIC COST AND PROFIT Figure 14.1 shows two views of cost and profit. Total revenue equals price multiplied by quantity sold. Economists measure economic profit as total revenue minus opportunity cost.

12

13 14.1 ECONOMIC COST AND PROFIT Opportunity cost is the sum of Explicit costs and Implicit cost (including normal profit).

14 14.1 ECONOMIC COST AND PROFIT Accountants measure cost as the sum of explicit costs and accounting depreciation. Accounting profit is total revenue minus accounting costs.

15 SHORT RUN AND LONG RUN The Short Run: Fixed Plant The short run is a time frame in which the quantities of some resources are fixed. In the short run, a firm can usually change the quantity of labor it uses but not the quantity of capital. The Long Run: Variable Plant The long run is a time frame in which the quantities of all resources can be changed. A sunk cost is irrelevant to the firm s decisions.

16 14.2 SHORT-RUN PRODUCTION To increase output with a fixed plant, a firm must increase the quantity of labor it uses. We describe the relationship between output and the quantity of labor by using three related concepts: Total product Marginal product Average product

17 14.2 SHORT-RUN PRODUCTION Total Product Total product (TP) is the total quantity of a good produced in a given period. Total product is an output rate the number of units produced per unit of time. Total product increases as the quantity of labor employed increases.

18 14.2 SHORT-RUN PRODUCTION Figure 14.2 shows the total product and the total product curve. Points A through H on the curve correspond to the columns of the table. The TP curve is like the PPF: It separates attainable points and unattainable points.

19

20 14.2 SHORT-RUN PRODUCTION Marginal Product Marginal product is the change in total product that results from a one-unit increase in the quantity of labor employed. Marginal product tells us the contribution to total product of adding one more worker. When the quantity of labor increases by more (or less) than one worker, calculate marginal product as: Marginal product Change in = total product Change in quantity of labor

21 14.2 SHORT-RUN PRODUCTION Figure 14.3 shows total product and marginal product. We can illustrate marginal product as the orange bars that form steps along the total product curve. The height of each step represents marginal product.

22

23 14.2 SHORT-RUN PRODUCTION The table calculates marginal product and the orange bars in part (b) illustrate it. Notice that the steeper the slope of the TP curve, the greater is marginal product.

24 14.2 SHORT-RUN PRODUCTION The total product and marginal product curves in this figure incorporate a feature of all production processes: Increasing marginal returns initially Decreasing marginal returns eventually Negative marginal returns

25 14.2 SHORT-RUN PRODUCTION Increasing Marginal Returns Increasing marginal returns occur when the marginal product of an additional worker exceeds the marginal product of the previous worker. Increasing marginal returns occur when a small number of workers are employed and arise from increased specialization and division of labor in the production process.

26 14.2 SHORT-RUN PRODUCTION Decreasing Marginal Returns Decreasing marginal returns occur when the marginal product of an additional worker is less than the marginal product of the previous worker. Decreasing marginal returns arise from the fact that more and more workers use the same equipment and work space. As more workers are employed, there is less and less that is productive for the additional worker to do.

27 14.2 SHORT-RUN PRODUCTION Decreasing marginal returns are so pervasive that they qualify for the status of a law: The law of decreasing returns states that: As a firm uses more of a variable input, with a given quantity of fixed inputs, the marginal product of the variable input eventually decreases.

28 14.2 SHORT-RUN PRODUCTION Average Product Average product is the total product per worker employed. It is calculated as: Average product = Total product Quantity of labor Another name for average product is productivity.

29 14.2 SHORT-RUN PRODUCTION Figure 14.4 shows average product and its relationship to marginal product. The table calculates average product. For example, 3 workers produce a total product of 6 gallons per hour, so average product is 6 3 = 2 gallons per worker.

30

31 14.2 SHORT-RUN PRODUCTION The figure graphs the average product against the quantity of labor employed. The average product curve is AP. When marginal product exceeds average product, average product is increasing.

32 14.2 SHORT-RUN PRODUCTION When marginal product is less than average product, average product is decreasing. When marginal product equals average product, average product is at its maximum.

33 14.3 SHORT-RUN COST To produce more output in the short run, a firm employs more labor, which means the firm must increase its costs. We describe the relationship between output and cost using three cost concepts: Total cost Marginal cost Average cost

34 14.3 SHORT-RUN COST Total Cost A firm s total cost (TC) is the cost of all the factors of production the firm uses. Total cost divides into two parts: Total fixed cost (TFC) is the cost of a firm s fixed factors of production used by a firm the cost of land, capital, and entrepreneurship. Total fixed cost doesn t change as output changes.

35 14.3 SHORT-RUN COST Total variable cost (TVC) is the cost of the variable factor of production used by a firm the cost of labor. To change its output in the short run, a firm must change the quantity of labor it employs, so total variable cost changes as output changes. Total cost is the sum of total fixed cost and total variable cost. That is, TC = TFC + TVC Table 14.2 on the next slide shows Sam s Smoothies costs.

36 14.3 SHORT-RUN COST

37 14.3 SHORT-RUN COST Figure 14.5 shows Sam s Smoothies total cost curves. Total fixed cost (TFC) is constant it graphs as a horizontal line. Total variable cost (TVC) increases as output increases. Total cost (TC) also increases as output increases.

38

39 14.3 SHORT-RUN COST The vertical distance between the total cost curve and the total variable cost curve is total fixed cost, as illustrated by the two arrows.

40 14.3 SHORT-RUN COST Marginal Cost A firm s marginal cost is the change in total cost that results from a one-unit increase in total product. Marginal cost tells us how total cost changes as total product changes. Table 14.3 on the next slide calculates marginal cost for Sam s Smoothies.

41

42 14.3 SHORT-RUN COST Average Cost There are three average cost concepts: Average fixed cost (AFC) is total fixed cost per unit of output. Average variable cost (AVC) is total variable cost per unit of output. Average total cost (ATC) is total cost per unit of output.

43 14.3 SHORT-RUN COST The average cost concepts are calculated from the total cost concepts as follows: TC = TFC + TVC Divide each total cost term by the quantity produced, Q, to give TC = TFC + TVC Q Q Q or, ATC = AFC + AVC

44

45 14.3 SHORT-RUN COST Figure 14.6 shows the average cost curves and marginal cost curve at Sam s Smoothies. Average fixed cost (AFC) decreases as output increases. The average variable cost curve (AVC) is U-shaped. The average total cost curve (ATC) is also U-shaped.

46

47 14.3 SHORT-RUN COST The vertical distance between ATC and AVC curves is equal to AFC, as illustrated by the two arrows. The marginal cost curve (MC) is U-shaped and intersects the average variable cost curve and the average total cost curve at their minimum points.

48 14.3 SHORT-RUN COST Why the Average Total Cost Curve Is U-Shaped Average total cost, ATC, is the sum of average fixed cost, AFC, and average variable cost, AVC. The shape of the ATC curve combines the shapes of the AFC and AVC curves. The U shape of the average total cost curve arises from the influence of two opposing forces: Spreading total fixed cost over a larger output Decreasing marginal returns

49 14.3 SHORT-RUN COST

50 14.3 SHORT-RUN COST Cost Curves and Product Curves The technology that a firm uses determines its costs. At low levels of employment and output, as the firm hires more labor, marginal product and average product rise, and marginal cost and average variable cost fall. Then, at the point of maximum marginal product, marginal cost is a minimum. As the firm hires more labor, marginal product decreases and marginal cost increases.

51 14.3 SHORT-RUN COST But average product continues to rise, and average variable cost continues to fall. Then, at the point of maximum average product, average variable cost is a minimum. As the firm hires even more labor, average product decreases and average variable cost increases.

52 14.3 SHORT-RUN COST Figure 14.7 illustrates the relationship between the product curves and cost curves. A firm s marginal cost curve is linked to its marginal product curve. If marginal product rises, marginal cost falls. If marginal product is a maximum, marginal cost is a minimum.

53

54 14.3 SHORT-RUN COST A firm s average variable cost curve is linked to its average product curve. If average product rises, average variable cost falls. If average product is a maximum, average variable cost is a minimum.

55 14.3 SHORT-RUN COST At small outputs, MP and AP rise and MC and AVC fall. At intermediate outputs, MP falls and MC rises and AP rises and AVC falls. At large outputs, MP and AP fall and MC and AVC rise.

56 14.3 SHORT-RUN COST Shifts in Cost Curves Technology A technological change that increases productivity shifts the TP curve upward. It also shifts the MP curve and the AP curve upward. With a better technology, the same inputs can produce more output, so an advance in technology lowers the average and marginal costs and shifts the short-run cost curves downward.

57 14.3 SHORT-RUN COST Prices of Factors of Production An increase in the price of a factor of production increases costs and shifts the cost curves. But how the curves shift depends on which resource price changes. An increase in rent or another component of fixed cost Shifts the fixed cost curves (TFC and AFC) upward. Shifts the total cost curve (TC) upward. Leaves the variable cost curves (AVC and TVC) and the marginal cost curve (MC) unchanged.

58 14.3 SHORT-RUN COST An increase in the wage rate or another component of variable cost Shifts the variable curves (TVC and AVC) upward. Shifts the marginal cost curve (MC) upward. Leaves the fixed cost curves (AFC and TFC) unchanged.

59 14.4 LONG-RUN COST Plant Size and Cost When a firm changes its plant size, its cost of producing a given output changes. Will the average total cost of producing a gallon of smoothie fall, rise, or remain the same? Each of these three outcomes arise because when a firm changes the size of its plant, it might experience: Economies of scale Diseconomies of scale Constant returns to scale

60 14.4 LONG-RUN COST Economies of Scale Economies of scale exist if when a firm increases its plant size and labor employed by the same percentage, its output increases by a larger percentage and average total cost decreases. The main source of economies of scale is greater specialization of both labor and capital.

61 14.4 LONG-RUN COST Diseconomies of Scale Diseconomies of scale exist if when a firm increases its plant size and labor employed by the same percentage, its output increases by a smaller percentage and average total cost increases. Diseconomies of scale arise from the difficulty of coordinating and controlling a large enterprise. Eventually, management complexity brings rising average total cost.

62 14.4 LONG-RUN COST Constant Returns to Scale Constant returns to scale exist if when a firm increases its plant size and labor employed by the same percentage, its output increases by the same percentage and average total cost remains constant. Constant returns to scale occur when a firm is able to replicate its existing production facility including its management system.

63 14.4 LONG-RUN COST The Long-Run Average Cost Curve The long-run average cost curve shows the lowest average cost at which it is possible to produce each output when the firm has had sufficient time to change both its plant size and labor employed.

64 14.4 LONG-RUN COST Figure 14.8 shows a long-run average cost curve. In the long run, Sam s Smoothies can vary both capital and labor inputs. With its current plant, Sam s ATC curve is ATC 1. With successively larger plants, Sam s ATC curves would be ATC 2, ATC 3, and ATC 4.

65

66 14.4 LONG-RUN COST The long-run average cost curve, LRAC, traces the lowest attainable average total cost of producing each output.

67 14.4 LONG-RUN COST Sam s experiences economies of scale as output increases to 14 gallons an hour, constant returns to scale for outputs between 14 gallons and 19 gallons an hour, and diseconomies of scale for outputs that exceed 19 gallons an hour.

68 Which Store Has the Lower Costs: Wal-Mart or 7 Eleven? Wal-Mart s small supercenters measure 99,000 square feet and serve an average of 30,000 customers a week. The average 7 Eleven store, mostly attached to gas stations, measures 2,000 square feet and serves 5,000 customers a week. Which retailing technology has the lower operating cost? The answer depends on the scale of operation. At a small number of customers per week, it costs less per customer to operate a store of 2,000 square feet than a store of 99,000 square feet.

69 Which Store Has the Lower Costs: Wal-Mart or 7 Eleven? The ATC curve of a store of 2,000 square feet is ATC 7 Eleven. The ATC curve of a store of 99,000 square feet is ATC Wal-Mart.

70 Which Store Has the Lower Costs: Wal-Mart or 7 Eleven? The dark blue curve is a retailer s LRAC curve. With Q customers a week, the average total cost of a transaction is the same in both stores.

71 Which Store Has the Lower Costs: Wal-Mart or 7 Eleven? For a store that serves more than Q customers a week, the least-cost method is the big store. For a store that serves fewer than Q customers a week, the least-cost method is the small store.

2012 Pearson Addison-Wesley

11 OUTPUT AND COSTS What do General Motors, PennPower, and Campus Sweaters, have in common? Like every firm, They must decide how much to produce. How many people to employ. How much and what type of

11 OUTPUT AND COSTS What do General Motors, PennPower, and Campus Sweaters, have in common? Like every firm, They must decide how much to produce. How many people to employ. How much and what type of

Course informa-on. Review ques-ons for second midterm (April 4 th ) on the course web site: h>p:// courses.umass.edu/econ103h

on the course web site: h>p:// courses.umass.edu/econ103h") Course informa-on Review ques-ons for second midterm (April 4 th ) on the course web site: h>p:// courses.umass.edu/econ103h Second midterm will have only 20 mul-ple choice and again a choice of 1 out

Course informa-on Review ques-ons for second midterm (April 4 th ) on the course web site: h>p:// courses.umass.edu/econ103h Second midterm will have only 20 mul-ple choice and again a choice of 1 out

Decision Time Frames Pearson Education

11 OUTPUT AND COSTS Decision Time Frames The firm makes many decisions to achieve its main objective: profit maximization. Some decisions are critical to the survival of the firm. Some decisions are irreversible

11 OUTPUT AND COSTS Decision Time Frames The firm makes many decisions to achieve its main objective: profit maximization. Some decisions are critical to the survival of the firm. Some decisions are irreversible

To do today: short-run production (only labor variable) To increase output with a fixed plant, a firm must increase the quantity of labor it uses.

To increase output with a fixed plant, a firm must increase the quantity of labor it uses.") To do today: short-run production (only labor variable) To increase output with a fixed plant, a firm must increase the quantity of labor it uses. Short-run production: only labor variable To increase

To do today: short-run production (only labor variable) To increase output with a fixed plant, a firm must increase the quantity of labor it uses. Short-run production: only labor variable To increase

Notes on Chapter 10 OUTPUT AND COSTS

Notes on Chapter 10 OUTPUT AND COSTS PRODUCTION TIMEFRAME There are many decisions made by the firm. Some decisions are major decisions that are hard to reverse without a big loss while other decisions

Notes on Chapter 10 OUTPUT AND COSTS PRODUCTION TIMEFRAME There are many decisions made by the firm. Some decisions are major decisions that are hard to reverse without a big loss while other decisions

OUTPUT AND COSTS. Chapter. Key Concepts. Decision Time Frames

Chapter 10 OUTPUT AND COSTS Key Concepts Decision Time Frames Firms have two decision time frames: Short run is the time frame in which the quantity of at least one factor of production is fixed. Long

Chapter 10 OUTPUT AND COSTS Key Concepts Decision Time Frames Firms have two decision time frames: Short run is the time frame in which the quantity of at least one factor of production is fixed. Long

The Production and Cost

The Production and Cost The Role of the Firm l The firm is an economic institution that transforms factors of production into consumer goods. It l Organizes factors of production. l Produces goods and

The Production and Cost The Role of the Firm l The firm is an economic institution that transforms factors of production into consumer goods. It l Organizes factors of production. l Produces goods and

Production and Cost Analysis I

CHAPTER 12 Production and Cost Analysis I Production is not the application of tools to materials, but logic to work. Peter Drucker McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All

CHAPTER 12 Production and Cost Analysis I Production is not the application of tools to materials, but logic to work. Peter Drucker McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All

Production and Cost Analysis I

CHAPTER 12 Production and Cost Analysis I Production is not the application of tools to materials, but logic to work. Peter Drucker McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All

CHAPTER 12 Production and Cost Analysis I Production is not the application of tools to materials, but logic to work. Peter Drucker McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All

Profit. Total Revenue The amount a firm receives for the sale of its output. Total Cost The market value of the inputs a firm uses in production.

Profit Total Revenue The amount a firm receives for the sale of its output. Total Cost The market value of the inputs a firm uses in production. Profit is the firm s total revenue minus its total cost.

Profit Total Revenue The amount a firm receives for the sale of its output. Total Cost The market value of the inputs a firm uses in production. Profit is the firm s total revenue minus its total cost.

Going Back To School. Meet Sam

Going Back To School Meet Sam Graduating Class of 12 Not a single callback for an interview Decision to go back to school Joined millions of students Why? The Costs of Production Chapter 9 Explicit Costs

Going Back To School Meet Sam Graduating Class of 12 Not a single callback for an interview Decision to go back to school Joined millions of students Why? The Costs of Production Chapter 9 Explicit Costs

The Firm s Objective. A Firm s Total Revenue and Total Cost. The economic goal of the firm is to maximize profits. A Firm s Profit

The s of Production Chapter 13 Copyright 2001 by Harcourt, Inc. The s of Production The Law of Supply: Firms are willing to produce and sell a greater quantity of a good when the price of the good is high.

The s of Production Chapter 13 Copyright 2001 by Harcourt, Inc. The s of Production The Law of Supply: Firms are willing to produce and sell a greater quantity of a good when the price of the good is high.

Theory of Produc-on. Lecture #4 Microeconomics

Theory of Produc-on Lecture #4 Microeconomics Topics 1. How firms produce goods and services. 2. Produc7on in the short run. 3. Costs or factors of produc7on. 4. Economies of scale and produc7on in the

Theory of Produc-on Lecture #4 Microeconomics Topics 1. How firms produce goods and services. 2. Produc7on in the short run. 3. Costs or factors of produc7on. 4. Economies of scale and produc7on in the

Week 5: The Costs of Production. 31 st March 2014

Week 5: The Costs of Production 31 st March 2014 WHAT ARE COSTS?! According to the Law of Supply:! Firms are willing to produce and sell a greater quantity of a good when the price of the good is high.!

Week 5: The Costs of Production 31 st March 2014 WHAT ARE COSTS?! According to the Law of Supply:! Firms are willing to produce and sell a greater quantity of a good when the price of the good is high.!

Total Costs. TC = TFC + TVC TFC = Fixed Costs. TVC = Variable Costs. Constant costs paid regardless of production

AP Microeconomics Total Costs TC = TFC + TVC TFC = Fixed Costs Constant costs paid regardless of production TVC = Variable Costs Costs that vary as production is changed Cost TFC TVC TFC Output Profit

AP Microeconomics Total Costs TC = TFC + TVC TFC = Fixed Costs Constant costs paid regardless of production TVC = Variable Costs Costs that vary as production is changed Cost TFC TVC TFC Output Profit

Firm Behavior and the Costs of Production

Firm Behavior and the Costs of Production WHAT ARE COSTS? The Firm s Objective The economic goal of the firm is to maximize profits. Total Revenue, Total Cost, and Profit Total Revenue, Total Cost, and

Firm Behavior and the Costs of Production WHAT ARE COSTS? The Firm s Objective The economic goal of the firm is to maximize profits. Total Revenue, Total Cost, and Profit Total Revenue, Total Cost, and

ECON 101 Introduction to Economics1

ECON 101 Introduction to Economics1 Session 10 Cost Concept Lecturer: Mrs. Hellen A. Seshie-Nasser, Department of Economics Contact Information: haseshie@ug.edu.gh College of Education School of Continuing

ECON 101 Introduction to Economics1 Session 10 Cost Concept Lecturer: Mrs. Hellen A. Seshie-Nasser, Department of Economics Contact Information: haseshie@ug.edu.gh College of Education School of Continuing

Cost schedules include the market value of all resources used in the production process.

By the end of this learning plan, you will be able to: Relate factor markets to production Assess the role price plays in a market economy Use marginal (Cost-Benefit) analysis in decision-making Cost schedules

By the end of this learning plan, you will be able to: Relate factor markets to production Assess the role price plays in a market economy Use marginal (Cost-Benefit) analysis in decision-making Cost schedules

The Market Forces of Supply and Demand

Theory of the Firm The Market Forces of Supply and Demand Supply and demand are the two words that economists use most often Supply and demand are the forces that make market economies work. Modern microeconomics

Theory of the Firm The Market Forces of Supply and Demand Supply and demand are the two words that economists use most often Supply and demand are the forces that make market economies work. Modern microeconomics

= AFC + AVC = (FC + VC)

") Chapter 13-14: Marginal Product, Costs, Revenue, and Profit Production Function The relationship between the quantity of inputs (workers) and quantity of outputs Total product (TP) is the total amount

Chapter 13-14: Marginal Product, Costs, Revenue, and Profit Production Function The relationship between the quantity of inputs (workers) and quantity of outputs Total product (TP) is the total amount

Lecture 10. The costs of production

Lecture 10 The costs of production By the end of this lecture, you should understand: what items are included in a firm s costs of production the link between a firm s production process and its total

Lecture 10 The costs of production By the end of this lecture, you should understand: what items are included in a firm s costs of production the link between a firm s production process and its total

5 FIRM BEHAVIOR AND THE ORGANIZATION OF INDUSTRY

5 FIRM BEHAVIOR AND THE ORGANIZATION OF INDUSTRY The s of Production 1 Copyright 2004 South-Western The Market Forces of Supply and Demand Supply and demand are the two words that economists use most often.

5 FIRM BEHAVIOR AND THE ORGANIZATION OF INDUSTRY The s of Production 1 Copyright 2004 South-Western The Market Forces of Supply and Demand Supply and demand are the two words that economists use most often.

Chapter 4 Production, Costs, and Profit.notebook. February 03, Chapter 4: Production, Costs, and Profits Pages

Chapter 4: Production, Costs, and Profits Pages 91 112 business an enterprise that brings individual, financial resources, and economic resources together to produce a good or service for economic gain

Chapter 4: Production, Costs, and Profits Pages 91 112 business an enterprise that brings individual, financial resources, and economic resources together to produce a good or service for economic gain

Practice Questions- Chapter 6

Practice Questions- Chapter 6 Harvey quit his job where he earned $45,000 a year. He figures his entrepreneurial talent or foregone entrepreneurial income to be $5,000 a year. To start the business, he

Practice Questions- Chapter 6 Harvey quit his job where he earned $45,000 a year. He figures his entrepreneurial talent or foregone entrepreneurial income to be $5,000 a year. To start the business, he

The Costs of Production Chapter 8!

The Costs of Production Chapter 8! Implicit Costs vs. Explicit Costs Implicit costs - the opportunity cost that is equal to what that has to be given up by a firm for using factors that it neither hires

The Costs of Production Chapter 8! Implicit Costs vs. Explicit Costs Implicit costs - the opportunity cost that is equal to what that has to be given up by a firm for using factors that it neither hires

The Theory and Estimation of Cost. Tools for Today s Decision Makers, 4/e By Paul Keat and Philip Young

The Theory and Estimation of Cost Chapter 8 Managerial Economics: Economic Managerial Economics: Economic Tools for Today s Decision Makers, 4/e By Paul Keat and Philip Young The Theory and Eti Estimation

The Theory and Estimation of Cost Chapter 8 Managerial Economics: Economic Managerial Economics: Economic Tools for Today s Decision Makers, 4/e By Paul Keat and Philip Young The Theory and Eti Estimation

Short-Run Costs and Output Decisions

Chapter 8 Short-Run Costs and Prepared by: Fernando & Yvonn Quijano 2007 Prentice Hall Business Publishing Principles of Economics 8e by Case and Fair Short-Run Costs and 8 Chapter Outline Costs in the

Chapter 8 Short-Run Costs and Prepared by: Fernando & Yvonn Quijano 2007 Prentice Hall Business Publishing Principles of Economics 8e by Case and Fair Short-Run Costs and 8 Chapter Outline Costs in the

HOMEWORK ECON SFU

HOMEWORK 1998-2 ECON 103 - SFU the law of diminishing returns have on short-run costs? Be specific. (e) âwhen... And when marginal product is diminishing, marginal cost is rising.â Illustrate and... ECON

HOMEWORK 1998-2 ECON 103 - SFU the law of diminishing returns have on short-run costs? Be specific. (e) âwhen... And when marginal product is diminishing, marginal cost is rising.â Illustrate and... ECON

Whoever claims that economic competition represents 'survival of the fittest' in the sense of the law of the jungle, provides the clearest possible

Whoever claims that economic competition represents 'survival of the fittest' in the sense of the law of the jungle, provides the clearest possible evidence of his lack of knowledge of economics. -George

Whoever claims that economic competition represents 'survival of the fittest' in the sense of the law of the jungle, provides the clearest possible evidence of his lack of knowledge of economics. -George

Chapter 7 Producers in the Short Run

Chapter 7 Producers in the Short Run 7.1 What are Firms? Organisation of Firms 1) Single proprietorship Has one owner who is personally responsible for the firm s actions and debts 2) Ordinary partnership

Chapter 7 Producers in the Short Run 7.1 What are Firms? Organisation of Firms 1) Single proprietorship Has one owner who is personally responsible for the firm s actions and debts 2) Ordinary partnership

CHAPTER 8: THE COSTS OF PRODUCTION

CHAPTER 8: THE COSTS OF PRODUCTION Introduction Now that we have examined consumer behavior in more detail, it is time to look at the decision making of the firm. Costs of production are important to determine

CHAPTER 8: THE COSTS OF PRODUCTION Introduction Now that we have examined consumer behavior in more detail, it is time to look at the decision making of the firm. Costs of production are important to determine

7 Costs. Lesson. of Production. Introduction

Lesson 7 Costs of Production Introduction Our study now combines what we have learned about price from Lesson 5 with utility theory from Lesson 6 to allocate resources among cost factors. Consider that

Lesson 7 Costs of Production Introduction Our study now combines what we have learned about price from Lesson 5 with utility theory from Lesson 6 to allocate resources among cost factors. Consider that

Chapter 11. Microeconomics. Technology, Production, and Costs. Modified by: Yun Wang Florida International University Spring 2018

Microeconomics Modified by: Yun Wang Florida International University Spring 2018 1 Chapter 11 Technology, Production, and Costs Chapter Outline 11.1 Technology: An Economic Definition 11.2 The Short Run

Microeconomics Modified by: Yun Wang Florida International University Spring 2018 1 Chapter 11 Technology, Production, and Costs Chapter Outline 11.1 Technology: An Economic Definition 11.2 The Short Run

Production and Cost. This Is What You Need to Know. Explain the difference between accounting and economic costs and how they affect the determination

Chiang_3E_CT_Micro_CH07_Layout 1 3/20/14 2:29 PM Page 175 7 Production and Cost Production and Cost Are Behind Decisions About Supply Having looked in the last chapter at what lies behind demand curves

Chiang_3E_CT_Micro_CH07_Layout 1 3/20/14 2:29 PM Page 175 7 Production and Cost Production and Cost Are Behind Decisions About Supply Having looked in the last chapter at what lies behind demand curves

Syllabus item: 42 Weight: 3

1.5 Theory of the firm and its market structures - Production and costs Syllabus item: 42 Weight: 3 Definition: Total product (TP): The total output that a firm produces, using its fixed and variable factors

1.5 Theory of the firm and its market structures - Production and costs Syllabus item: 42 Weight: 3 Definition: Total product (TP): The total output that a firm produces, using its fixed and variable factors

Costs: Introduction. Costs 26/09/2017. Managerial Problem. Solution Approach. Take-away

Costs Costs: Introduction Managerial Problem Technology choice at home versus abroad: In western countries, firms use relatively capital-intensive technology. Will that same technology be cost minimizing

Costs Costs: Introduction Managerial Problem Technology choice at home versus abroad: In western countries, firms use relatively capital-intensive technology. Will that same technology be cost minimizing

23 Perfect Competition

23 Perfect Competition Learning Objectives After you have studied this chapter, you should be able to 1. define price taker, total revenues, marginal revenue, short-run shutdown price, short-run breakeven

23 Perfect Competition Learning Objectives After you have studied this chapter, you should be able to 1. define price taker, total revenues, marginal revenue, short-run shutdown price, short-run breakeven

Costs in the Short Run: NOTE: Costs depend upon output!! Fixed Costs (FC) costs which do not change when a business changes its quantity of output.

costs which do not change when a business changes its quantity of output.") Costs in the Short Run: NOTE: Costs depend upon output!! Fixed Costs (FC) costs which do not change when a business changes its quantity of output. Variable Costs (VC) costs which do change when a business

Costs in the Short Run: NOTE: Costs depend upon output!! Fixed Costs (FC) costs which do not change when a business changes its quantity of output. Variable Costs (VC) costs which do change when a business

ECON 101 KONG Midterm 2 CMP Review Session. Presented by Benji Huang

ECON 101 KONG Midterm 2 CMP Review Session Presented by Benji Huang Chapter 5 Efficiency and Equity Benefit, Cost, Surplus Consumers (1) A consumer benefits from the consumption of a product this benefit

ECON 101 KONG Midterm 2 CMP Review Session Presented by Benji Huang Chapter 5 Efficiency and Equity Benefit, Cost, Surplus Consumers (1) A consumer benefits from the consumption of a product this benefit

AP Microeconomics Chapter 8 Outline

I. Learning Objectives In this chapter students should learn: A. Why economic costs include both explicit (revealed and expressed) costs and implicit (present but not obvious) costs. B. How the law of

I. Learning Objectives In this chapter students should learn: A. Why economic costs include both explicit (revealed and expressed) costs and implicit (present but not obvious) costs. B. How the law of

2010 Pearson Education Canada

What Is Perfect Competition? Perfect competition is an industry in which Many firms sell identical products to many buyers. There are no restrictions to entry into the industry. Established firms have

What Is Perfect Competition? Perfect competition is an industry in which Many firms sell identical products to many buyers. There are no restrictions to entry into the industry. Established firms have

ECONOMICS CHAPTER 8: COST AND REVENUE ANALYSIS Class: XII(ISC) Q1) Define the following:

Q1) Define the following:") Q1) Define the following: ECONOMICS CHAPTER 8: COST AND REVENUE ANALYSIS Class: XII(ISC) 2017-2018 i. Money cost Money cost refers to money expenses which the firm has to incur in purchasing or hiring

Q1) Define the following: ECONOMICS CHAPTER 8: COST AND REVENUE ANALYSIS Class: XII(ISC) 2017-2018 i. Money cost Money cost refers to money expenses which the firm has to incur in purchasing or hiring

ECONOMICS STANDARD XII (ISC) Chapter 8: Cost and Revenue Analysis

Chapter 8: Cost and Revenue Analysis") ECONOMICS STANDARD XII (ISC) Chapter 8: Cost and Revenue Analysis Q1) Define the following: i. Money cost Money cost refers to money expenses which the firm has to incur in purchasing or hiring factor

ECONOMICS STANDARD XII (ISC) Chapter 8: Cost and Revenue Analysis Q1) Define the following: i. Money cost Money cost refers to money expenses which the firm has to incur in purchasing or hiring factor

Mr Sydney Armstrong ECN 1100 Introduction to Microeconomics Lecture Note (6) The costs of Production Economic Costs

The costs of Production Economic Costs") Mr Sydney Armstrong ECN 1100 Introduction to Microeconomics Lecture Note (6) The costs of Production Economic Costs Costs exist because resources are scarce, productive and have alternative uses. When

Mr Sydney Armstrong ECN 1100 Introduction to Microeconomics Lecture Note (6) The costs of Production Economic Costs Costs exist because resources are scarce, productive and have alternative uses. When

Classnotes for chapter 13

Classnotes for chapter 13 Chapter 13: Very important Focuses on firms production and costs Examines firm behavior in more detail (previously we simply looked at the supply curve to understand firm behavior)

Classnotes for chapter 13 Chapter 13: Very important Focuses on firms production and costs Examines firm behavior in more detail (previously we simply looked at the supply curve to understand firm behavior)

#20: & # 8, 9, 10) 7 P # 2&3 HW:

7 P # 2&3 HW:") AGENDA Tues 10/6 QOD #20: Caution! Curves Ahead Law of Diminishing Marginal Returns Costs of Production (Review HW Q#1,2,5,6) Short & Long Run (Q # 8, 9, 10) Partner Practice Ch 7 P # 2&3 HW: Prep for

AGENDA Tues 10/6 QOD #20: Caution! Curves Ahead Law of Diminishing Marginal Returns Costs of Production (Review HW Q#1,2,5,6) Short & Long Run (Q # 8, 9, 10) Partner Practice Ch 7 P # 2&3 HW: Prep for

Supply and demand are the two words that economists use most often.

Chapter 13. The Costs of Production The Market Forces of Supply and Demand Supply and demand are the two words that economists use most often. Supply and demand are the forces that make market economies

Chapter 13. The Costs of Production The Market Forces of Supply and Demand Supply and demand are the two words that economists use most often. Supply and demand are the forces that make market economies

Short-Run Costs and Output Decisions

Semester-I Course: 01 (Introductory Microeconomics) Unit IV - The Firm and Perfect Market Structure Lesson: Short-Run Costs and Output Decisions Lesson Developer: Jasmin Jawaharlal Nehru University Institute

Semester-I Course: 01 (Introductory Microeconomics) Unit IV - The Firm and Perfect Market Structure Lesson: Short-Run Costs and Output Decisions Lesson Developer: Jasmin Jawaharlal Nehru University Institute

ECON 2100 Principles of Microeconomics (Summer 2016) The Production Process and Costs of Production

The Production Process and Costs of Production") ECON 21 Principles of Microeconomics (Summer 216) The Production Process and of Production Relevant readings from the textbook: Mankiw, Ch. 13 The of Production Suggested problems from the textbook: Chapter

ECON 21 Principles of Microeconomics (Summer 216) The Production Process and of Production Relevant readings from the textbook: Mankiw, Ch. 13 The of Production Suggested problems from the textbook: Chapter

3. Definition of constant returns to scale: the property whereby long-run average total cost stays the same as the quantity of output changes.

250 Chapter 13/The s of Production 3. Definition of constant returns to scale: the property whereby long-run average total cost stays the same as the quantity of output changes. 4. FYI: Lessons from a

250 Chapter 13/The s of Production 3. Definition of constant returns to scale: the property whereby long-run average total cost stays the same as the quantity of output changes. 4. FYI: Lessons from a

ECON 102 Brown Final Exam (New Material) Practice Exam Solutions

Practice Exam Solutions") www.liontutors.com ECON 102 Brown Final Exam (New Material) Practice Exam Solutions 1. B A very large percent of their earnings comes from economic rent 2. B Any funds left, after everyone who has a claim

www.liontutors.com ECON 102 Brown Final Exam (New Material) Practice Exam Solutions 1. B A very large percent of their earnings comes from economic rent 2. B Any funds left, after everyone who has a claim

The Costs of Production

The Costs of Production PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University 1 What are Costs? Total revenue = amount a firm receives for the sale of its output Total cost = market

The Costs of Production PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University 1 What are Costs? Total revenue = amount a firm receives for the sale of its output Total cost = market

CHAPTER-3 COST. (c) Average variable cost. (d) Opportunity costs. 1. Marginal cost is the cost:

Average variable cost. (d) Opportunity costs. 1. Marginal cost is the cost:") CHAPTER-3 COST (c) Average variable cost (d) Opportunity costs 1. Marginal cost is the cost: (a) Of the last unit production (b) Of the Marginal unit (c) Of the marginal efficient unit (d) Of the average

CHAPTER-3 COST (c) Average variable cost (d) Opportunity costs 1. Marginal cost is the cost: (a) Of the last unit production (b) Of the Marginal unit (c) Of the marginal efficient unit (d) Of the average

The Theory and Estimation of Cost. Chapter 7. Managerial Economics: Economic Tools for Today s Decision Makers, 5/e By Paul Keat and Philip Young

The Theory and Estimation of Cost Chapter 7 Managerial Economics: Economic Tools for Today s Decision Makers, 5/e By Paul Keat and Philip Young The Theory and Estimation of Cost The Importance of Cost

The Theory and Estimation of Cost Chapter 7 Managerial Economics: Economic Tools for Today s Decision Makers, 5/e By Paul Keat and Philip Young The Theory and Estimation of Cost The Importance of Cost

Week One What is economics? Chapter 1

Week One What is economics? Chapter 1 Economics: is the social science that studies the choices that individuals, businesses, governments, and entire societies make as they cope with scarcity and the incentives

Week One What is economics? Chapter 1 Economics: is the social science that studies the choices that individuals, businesses, governments, and entire societies make as they cope with scarcity and the incentives

Chapter 9. Businesses and the Costs of Produc2on

Chapter 9 Businesses and the Costs of Produc2on Copyright 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Economic

Chapter 9 Businesses and the Costs of Produc2on Copyright 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Economic

2000 AP Microeconomics Exam Answers

2000 AP Microeconomics Exam Answers 1. B Scarcity is the main economic problem!!! 2. D If the wages of farm workers and movie theater employee increase, the supply of popcorn and movies will decrease (shift

2000 AP Microeconomics Exam Answers 1. B Scarcity is the main economic problem!!! 2. D If the wages of farm workers and movie theater employee increase, the supply of popcorn and movies will decrease (shift

1. If the per unit cost of production falls, then... A.) the supply curve shifts right (or down)

the supply curve shifts right (or down)") 1. If the per unit cost of production falls, then... A.) the supply curve shifts right (or down) B.) there is a downward movement along the existing supply curve which does not shift C.) the supply curve

1. If the per unit cost of production falls, then... A.) the supply curve shifts right (or down) B.) there is a downward movement along the existing supply curve which does not shift C.) the supply curve

Costs of Production. Total Revenue - the amount a firm receives for the sale of its output.

Costs of Production Total Revenue - the amount a firm receives for the sale of its output. TR = P x Q Total Cost - the value of the inputs a firm uses in production. TC = FC + VC Profit is the firm s total

Costs of Production Total Revenue - the amount a firm receives for the sale of its output. TR = P x Q Total Cost - the value of the inputs a firm uses in production. TC = FC + VC Profit is the firm s total

Where are we? Second midterm on November 19. Review questions on th course web site. Today: chapter on perfect competition

Where are we? Second midterm on November 19 Review questions on th course web site. Today: chapter on perfect competition Topic for the second paper: Pick a chapter in Ariely after Chapter 4 and compare

Where are we? Second midterm on November 19 Review questions on th course web site. Today: chapter on perfect competition Topic for the second paper: Pick a chapter in Ariely after Chapter 4 and compare

In the last session we introduced the firm behaviour and the concept of profit maximisation. In this session we will build on the concepts discussed

In the last session we introduced the firm behaviour and the concept of profit maximisation. In this session we will build on the concepts discussed previously by examining cost structure, which is a key

In the last session we introduced the firm behaviour and the concept of profit maximisation. In this session we will build on the concepts discussed previously by examining cost structure, which is a key

Perfectly Competitive Supply. Chapter 6. Learning Objectives

Perfectly Competitive Supply Chapter 6 McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Learning Objectives 1.Explain how opportunity cost is related to the supply

Perfectly Competitive Supply Chapter 6 McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Learning Objectives 1.Explain how opportunity cost is related to the supply

THE COSTS OF PRODUCTION PART II

THE COSTS OF PRODUCTION PART II It is one of the greatest economic errors to put any limitation on production... We have not the power to produce more than there is the potential to consume. - Louis D.

THE COSTS OF PRODUCTION PART II It is one of the greatest economic errors to put any limitation on production... We have not the power to produce more than there is the potential to consume. - Louis D.

ECON 102 Kagundu Final Exam (New Material) Practice Exam Solutions

Practice Exam Solutions") www.liontutors.com ECON 102 Kagundu Final Exam (New Material) Practice Exam Solutions 1. A A large number of firms will be able to operate in the industry because you only need to produce a small amount

www.liontutors.com ECON 102 Kagundu Final Exam (New Material) Practice Exam Solutions 1. A A large number of firms will be able to operate in the industry because you only need to produce a small amount

Contemporary Economics: An Applications Approach. Production. Production Function. Chapter 4: Production and the Costs of Production

Contemporary Economics: An Applications Approach By Robert J. Carbaugh 4th Edition Chapter 4: Production and the Costs of Production Copyright 2005 by South-Western, a division of Thomson Learning. All

Contemporary Economics: An Applications Approach By Robert J. Carbaugh 4th Edition Chapter 4: Production and the Costs of Production Copyright 2005 by South-Western, a division of Thomson Learning. All

Introduction. Learning Objectives. Learning Objectives. Chapter 23. The Firm: Cost and Output Determination

Chapter 23 The Firm: Cost and Output Determination Introduction Freight dispatchers use real-time information transmitted by computers to monitor the positions of locomotives and rolling stock along the

Chapter 23 The Firm: Cost and Output Determination Introduction Freight dispatchers use real-time information transmitted by computers to monitor the positions of locomotives and rolling stock along the

Preview from Notesale.co.uk Page 6 of 89

Guns Butter 200 0 175 75 130 125 70 150 0 160 What it shows: the maximum combinations of two goods an economy can produce with its existing resources and technology; an economy can produce at points on

Guns Butter 200 0 175 75 130 125 70 150 0 160 What it shows: the maximum combinations of two goods an economy can produce with its existing resources and technology; an economy can produce at points on

CONTENT TOPIC 3: SUPPLY, PRODUCTION AND COST. The Supply Process. The Role of the Firm 10/10/2016

CONTENT TOPIC 3: SUPPLY, PRODUCTION AND COST - The factors of production - Combining factors of production: The law of returns - Costs of production: Short & Long Run - Deciding whether to produce in the

CONTENT TOPIC 3: SUPPLY, PRODUCTION AND COST - The factors of production - Combining factors of production: The law of returns - Costs of production: Short & Long Run - Deciding whether to produce in the

Short Run Costs. The Costs of Production. Fixed Costs, Variable Costs, and Total Costs. Fixed Costs, Variable Costs, and Total Costs

The Costs of Production Short Run Costs Part 2 There are many different types of costs. Invariably, firms believe costs are too high and try to lower them. Fixed Costs, Variable Costs, and Total Costs

The Costs of Production Short Run Costs Part 2 There are many different types of costs. Invariably, firms believe costs are too high and try to lower them. Fixed Costs, Variable Costs, and Total Costs

Practice Exam 3: S201 Walker Fall 2009

Practice Exam 3: S201 Walker Fall 2009 I. Multiple Choice (3 points each) 1. Which of the following statements about the short-run is false? A. The marginal product of labor may increase or decrease. B.

Practice Exam 3: S201 Walker Fall 2009 I. Multiple Choice (3 points each) 1. Which of the following statements about the short-run is false? A. The marginal product of labor may increase or decrease. B.

Module 55 Firm Costs. What you will learn in this Module:

What you will learn in this Module: The various types of cost a firm faces, including fixed cost, variable cost, and total cost How a firm s costs generate marginal cost curves and average cost curves

What you will learn in this Module: The various types of cost a firm faces, including fixed cost, variable cost, and total cost How a firm s costs generate marginal cost curves and average cost curves

Unit 5. Producer theory: revenues and costs

Unit 5. Producer theory: revenues and costs Learning objectives to understand the concept of the short-run production function, describing the relationship between the quantity of inputs and the quantity

Unit 5. Producer theory: revenues and costs Learning objectives to understand the concept of the short-run production function, describing the relationship between the quantity of inputs and the quantity

AP Microeconomics Review Session #3 Key Terms & Concepts

The Firm, Profit, and the Costs of Production 1. Explicit vs. implicit costs 2. Short-run vs. long-run decisions 3. Fixed inputs vs. variable inputs 4. Short-run production measures: be able to calculate/graph

The Firm, Profit, and the Costs of Production 1. Explicit vs. implicit costs 2. Short-run vs. long-run decisions 3. Fixed inputs vs. variable inputs 4. Short-run production measures: be able to calculate/graph

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Sample Test 3 Ch 10-13 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A cost incurred in the production of a good or service and for which

Sample Test 3 Ch 10-13 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A cost incurred in the production of a good or service and for which

ECONOMICS ASSIGNMENT CLASS XII MICRO ECONOMICS UNIT I INTRODUCTION. 4. Is free medicine given to patients in Govt. Hospital a scarce commodity?

ECONOMICS ASSIGNMENT CLASS XII MICRO ECONOMICS UNIT I INTRODUCTION 1. What is the Slope of PPC? What does it show? 2. When can PPC be a straight line? 3. Do all attainable combination of two goods that

ECONOMICS ASSIGNMENT CLASS XII MICRO ECONOMICS UNIT I INTRODUCTION 1. What is the Slope of PPC? What does it show? 2. When can PPC be a straight line? 3. Do all attainable combination of two goods that

Production and Costs. Bibliography: Mankiw and Taylor, Ch. 6.

Production and Costs Bibliography: Mankiw and Taylor, Ch. 6. The Importance of Cost in Managerial Decisions Containing costs is a key issue in managerial decisionmaking Firms seek to reduce the number

Production and Costs Bibliography: Mankiw and Taylor, Ch. 6. The Importance of Cost in Managerial Decisions Containing costs is a key issue in managerial decisionmaking Firms seek to reduce the number

8 CHAPTER OUTLINE Costs in the Short Run Fixed Costs

e PART II I The Market System: Choices Made by Households and Firms e CASE FAIR OSTER PEARSON 2012 Pearson Education, Inc. Publishing as Prentice Hall PRINCIPLES OF MICROECONOMICS E L E V E N T H E D I

e PART II I The Market System: Choices Made by Households and Firms e CASE FAIR OSTER PEARSON 2012 Pearson Education, Inc. Publishing as Prentice Hall PRINCIPLES OF MICROECONOMICS E L E V E N T H E D I

START UP: STREET CLEANING AROUND THE WORLD

CHAPTER 8 Production and Cost START UP: STREET CLEANING AROUND THE WORLD It is dawn in Shanghai, China. Already thousands of Chinese are out cleaning the city s streets. They are using brooms. On the other

CHAPTER 8 Production and Cost START UP: STREET CLEANING AROUND THE WORLD It is dawn in Shanghai, China. Already thousands of Chinese are out cleaning the city s streets. They are using brooms. On the other

Chief Reader Report on Student Responses:

Chief Reader Report on Student Responses: 2018 AP Microeconomics Free-Response Questions Number of Students Scored 90,032 Number of Readers 91 Score Distribution Exam Score N %At 5 18,827 20.9 4 25,070

Chief Reader Report on Student Responses: 2018 AP Microeconomics Free-Response Questions Number of Students Scored 90,032 Number of Readers 91 Score Distribution Exam Score N %At 5 18,827 20.9 4 25,070

Demand & Supply of Resources

Resource Markets 1 Demand & Supply of Resources Resource demand Firms demand resources As long as marginal revenue exceeds marginal cost To maximize profit Resource supply People supply resources To the

Resource Markets 1 Demand & Supply of Resources Resource demand Firms demand resources As long as marginal revenue exceeds marginal cost To maximize profit Resource supply People supply resources To the

Practice Exam 3: S201 Walker Fall with answers to MC

Practice Exam 3: S201 Walker Fall 2007 - with answers to MC Print Your Name: I. Multiple Choice (3 points each) 1. If marginal utility is falling then A. total utility must be falling. B. marginal utility

Practice Exam 3: S201 Walker Fall 2007 - with answers to MC Print Your Name: I. Multiple Choice (3 points each) 1. If marginal utility is falling then A. total utility must be falling. B. marginal utility

If the industry s short-run supply curve equals the horizontal sum of individual firms short-run supply curves, which of the following may we infer?

Microeconomics, Module 8: Competition: Long Run (Chapter 7) Illustrative Test Questions (The attached PDF file has better formatting.) Question 8.1: Long Run Equilibrium When is a competitive profit-maximizing

Microeconomics, Module 8: Competition: Long Run (Chapter 7) Illustrative Test Questions (The attached PDF file has better formatting.) Question 8.1: Long Run Equilibrium When is a competitive profit-maximizing

Chapter Summary and Learning Objectives

CHAPTER 11 Firms in Perfectly Competitive Markets Chapter Summary and Learning Objectives 11.1 Perfectly Competitive Markets (pages 369 371) Explain what a perfectly competitive market is and why a perfect

CHAPTER 11 Firms in Perfectly Competitive Markets Chapter Summary and Learning Objectives 11.1 Perfectly Competitive Markets (pages 369 371) Explain what a perfectly competitive market is and why a perfect

Pledge (sign) I did not copy another student s answers

I did not copy another student s answers") Economics 4020 Dr. Rupp Test #1 Fri. Sept 23 rd, 2011 20 Multiple Choice questions (2.5 points each) Pledge (sign) I did not copy another student s answers 1. The profit maximization rule for a firm is

Economics 4020 Dr. Rupp Test #1 Fri. Sept 23 rd, 2011 20 Multiple Choice questions (2.5 points each) Pledge (sign) I did not copy another student s answers 1. The profit maximization rule for a firm is

MICRO EXAM REVIEW SHEET

MICRO EXAM REVIEW SHEET 1. Firm in Perfect Competition (Long-Run Equilibrium) 2. Monopoly Industry with comparison of price & output of a Perfectly Competitive Industry 3. Natural Monopoly with Fair-Return

MICRO EXAM REVIEW SHEET 1. Firm in Perfect Competition (Long-Run Equilibrium) 2. Monopoly Industry with comparison of price & output of a Perfectly Competitive Industry 3. Natural Monopoly with Fair-Return

COST THEORY. I What costs matter? A Opportunity Costs

COST THEORY Cost theory is related to production theory, they are often used together. However, here the question is how much to produce, as opposed to which inputs to use. That is, assume that we use

COST THEORY Cost theory is related to production theory, they are often used together. However, here the question is how much to produce, as opposed to which inputs to use. That is, assume that we use

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

AUBG, Fall 2015, Principles Micro with P. Stankov, Sample MT2 NOTE: The actual no. of questions on the actual MT will be 30, each for 0.67 grade points. MULTIPLE CHOICE. Choose the one alternative that

AUBG, Fall 2015, Principles Micro with P. Stankov, Sample MT2 NOTE: The actual no. of questions on the actual MT will be 30, each for 0.67 grade points. MULTIPLE CHOICE. Choose the one alternative that

OVERVIEW. 5. The marginal cost is hook shaped. The shape is due to the law of diminishing returns.

10 COST OVERVIEW 1. Total fixed cost is the cost which does not vary with output. Total variable cost changes as output changes. Total cost is the sum of total fixed cost and total variable cost. 2. Explicit

10 COST OVERVIEW 1. Total fixed cost is the cost which does not vary with output. Total variable cost changes as output changes. Total cost is the sum of total fixed cost and total variable cost. 2. Explicit

AP Microeconomics Review With Answers

AP Microeconomics Review With Answers 1. Firm in Perfect Competition (Long-Run Equilibrium) 2. Monopoly Industry with comparison of price & output of a Perfectly Competitive Industry (which means show

AP Microeconomics Review With Answers 1. Firm in Perfect Competition (Long-Run Equilibrium) 2. Monopoly Industry with comparison of price & output of a Perfectly Competitive Industry (which means show

Understanding Markets

Understanding Markets EC8005 Lecture 7 2014 Michael King 1 Revision: Consumer Theory 1. Qd = f(p,ps, Pc, Y, T, O) 2. Sd = f(p, T, I, G, Tx, Sy, O) 3. Types of goods 4. Shift along v s shift in demand/supply

Understanding Markets EC8005 Lecture 7 2014 Michael King 1 Revision: Consumer Theory 1. Qd = f(p,ps, Pc, Y, T, O) 2. Sd = f(p, T, I, G, Tx, Sy, O) 3. Types of goods 4. Shift along v s shift in demand/supply

Chapter Chapter 6. Sellers and Incentives. Outline. Sellers in a Perfectly Competitive Market. The Seller s Problem

Long- Part II: Foundation of Microeconomics 5. Consumers and 6. 7. Perfect Competition and the Invisible Hand 8. Trade 9. Externalities and Public Goods 10. The Government in the Economy: Taxation and

Long- Part II: Foundation of Microeconomics 5. Consumers and 6. 7. Perfect Competition and the Invisible Hand 8. Trade 9. Externalities and Public Goods 10. The Government in the Economy: Taxation and

SCHOOL OF ACCOUNTING AND BUSINESS BSc. (APPLIED ACCOUNTING) GENERAL / SPECIAL DEGREE PROGRAMME END SEMESTER EXAMINATION JULY 2016

GENERAL / SPECIAL DEGREE PROGRAMME END SEMESTER EXAMINATION JULY 2016") All Rights Reserved No. of Pages - 08 No of Questions - 08 SCHOOL OF ACCOUNTING AND BUSINESS BSc. (APPLIED ACCOUNTING) GENERAL / SPECIAL DEGREE PROGRAMME END SEMESTER EAMINATION JULY 2016 BEC 30325 Managerial

All Rights Reserved No. of Pages - 08 No of Questions - 08 SCHOOL OF ACCOUNTING AND BUSINESS BSc. (APPLIED ACCOUNTING) GENERAL / SPECIAL DEGREE PROGRAMME END SEMESTER EAMINATION JULY 2016 BEC 30325 Managerial

Benefits, Costs, and Maximization

11 Benefits, Costs, and Maximization CHAPTER OBJECTIVES To explain the basic process of balancing costs and benefits in economic decision making. To introduce marginal analysis, and to define marginal

11 Benefits, Costs, and Maximization CHAPTER OBJECTIVES To explain the basic process of balancing costs and benefits in economic decision making. To introduce marginal analysis, and to define marginal

Edexcel (A) Economics A-level

Economics A-level") Edexcel (A) Economics A-level Theme 3: Business Behaviour & the Labour Market 3.3 Revenue Costs and Profits 3.3.2 Costs Notes Formulae to calculate types of costs Total cost: This is how much it costs

Edexcel (A) Economics A-level Theme 3: Business Behaviour & the Labour Market 3.3 Revenue Costs and Profits 3.3.2 Costs Notes Formulae to calculate types of costs Total cost: This is how much it costs

INTI COLLEGE MALAYSIA BUSINESS FOUNDATION PROGRAMME ECO 181: INTRODUCTORY ECONOMICS FINAL EXAMINATION: AUGUST 2003 SESSION

ECO 181 (F) / Page 1 of 15 INTI COLLEGE MALAYSIA BUSINESS FOUNDATION PROGRAMME ECO 181: INTRODUCTORY ECONOMICS FINAL EXAMINATION: AUGUST 2003 SESSION SECTION A There are SIXTY questions on this paper.

ECO 181 (F) / Page 1 of 15 INTI COLLEGE MALAYSIA BUSINESS FOUNDATION PROGRAMME ECO 181: INTRODUCTORY ECONOMICS FINAL EXAMINATION: AUGUST 2003 SESSION SECTION A There are SIXTY questions on this paper.

Chapter 9 Making Decisions

Goldwasser AP Microeconomics Chapter 9 Making Decisions BEFORE YOU READ THE CHAPTER Summary Chapter 9 explores two questions either-or and how much and then provides a framework for making decisions arising

Goldwasser AP Microeconomics Chapter 9 Making Decisions BEFORE YOU READ THE CHAPTER Summary Chapter 9 explores two questions either-or and how much and then provides a framework for making decisions arising

Chapter 11 Technology, Production, and Costs

Economics 6 th edition 1 Chapter 11 Technology, Production, and Costs Modified by Yulin Hou For Principles of Microeconomics Florida International University Fall 2017 Technology: An Economic Definition

Economics 6 th edition 1 Chapter 11 Technology, Production, and Costs Modified by Yulin Hou For Principles of Microeconomics Florida International University Fall 2017 Technology: An Economic Definition

Ch. 8 Costs and the Supply of Goods. 1. they purchase productive resources from households and other firms

Ch. 8 Costs and the Supply of Goods Organization of the business firm What do firms do? 1. they purchase productive resources from households and other firms 2. then they transform those resources into

Ch. 8 Costs and the Supply of Goods Organization of the business firm What do firms do? 1. they purchase productive resources from households and other firms 2. then they transform those resources into

Microeconomics (Cost, Ch 7)

") Microeconomics (Cost, Ch 7) Lectures 10-11-12 Feb 09/13/16, 2017 7.1 MEASURING COST: WHICH COSTS MATTER? Economic Cost versus Accounting Cost Opportunity Cost accounting cost Actual expenses plus depreciation

Microeconomics (Cost, Ch 7) Lectures 10-11-12 Feb 09/13/16, 2017 7.1 MEASURING COST: WHICH COSTS MATTER? Economic Cost versus Accounting Cost Opportunity Cost accounting cost Actual expenses plus depreciation

ECON 260 (2,3) Practice Exam #4 Spring 2007 Dan Mallela

Practice Exam #4 Spring 2007 Dan Mallela") ECON 260 (2,3) Practice Exam #4 Spring 2007 Dan Mallela Multiple Choice Identify the letter of the choice that best completes the statement or answers the question. 1. Profit is defined as a. net revenue

ECON 260 (2,3) Practice Exam #4 Spring 2007 Dan Mallela Multiple Choice Identify the letter of the choice that best completes the statement or answers the question. 1. Profit is defined as a. net revenue