Marginal willingness to pay (WTP). The maximum amount a consumer will spend for an extra unit of the good.

|

|

|

- Duane Barber

- 6 years ago

- Views:

Transcription

1 McPeak Lecture 10 PAI 723 The competitive model. Marginal willingness to pay (WTP). The maximum amount a consumer will spend for an extra unit of the good. As we derived a demand curve for an individual s preferences, we can interpret the demand curve tracing out the consumer s marginal willingness to pay at different levels of consumption. Consumer surplus (CS) the monetary difference between what the consumer is willing to pay for a given quantity of good and what the good costs. [show graph] Relies on the fact that the demand curve is downward sloping and that the price for purchasing is the same for all units. The area under the demand curve and above the price line. The area below the price line is expenditure (p times q).

2 If price increases and demand is constant, consumer surplus falls. The decrease in consumer surplus for a given price increase will be larger: The greater the initial expenditure on the good The less elastic is the demand curve. Producer surplus. The difference between the minimum amount necessary for the seller to be willing to produce the good and the selling price. [show graph] Producer surplus is revenue minus variable cost. Since profit is revenue minus cost, the difference between profit and producer surplus is fixed cost in the short run, and there is no difference in the long run.

3 The maximum societal welfare comes from maximizing consumer surplus plus producer surplus. Why are there gains to trade? [show graph of when quantity is too low] [ show graph of when quantity is too high]

4 Monopoly. There is only one supplier of a good for which there is no close substitute. How can such a thing happen? 1) Technical reasons. a. Economies of scale. A natural monopoly exists when one firm can produce at a lower cost than several firms producing the same good and total output level (AC is downward sloping over the feasible range of output). 2) Legal reasons. a. Patents. b. Franchises c. Legal barriers. 3) Anti-competitive behavior Marginal revenue as you recall is the change in revenue divided by the change in q. In the competitive model, the price taking firm faced a marginal revenue of p, since price did not change with the output level of the firm. Now, the monopoly firm faces the entire demand curve. This is downward sloping, so by picking a level of q, there is also an associated p (the whole demand curve is defined by (p,q) pairs).

5 [show graph] Price Discrete MR Bisection MR Discrete MR Bisection MR Price TR

6 Note there is a difference between calculating the MR from one observation to the next compared to the MR at a given point. Bisection rule. Marginal revenue for a linear demand curve defined by: p=a-b*q is MR=a-2*b*q. For a linear demand curve, the marginal revenue curve bisects the demand curve. Why? Well demand is (24-q)=p in the example above, and we know p*q is revenue. So p*q is the same as (24-q)*q, or 24q-q 2. The marginal of this is the derivative with respect to q, or 24-2q. The competitive firms choose q given p. Here, the monopoly chooses p and q based on information about the entire demand curve. It is making its choices in the awareness that increasing q decreases price, and that marginal revenue is a function of the quantity they pick.

7 Profit maximization steps for the monopolist. 1) Identify q * that determines where MR(q * )= MC(q * ) 2) Calculate what is the implied p * for that q * from the demand curve. 3) Calculate profit which is defined by p * times q * minus cost at q * / look at p * compared to AC(q * ). 4) Shut down (produce q=0) if p * is less than average variable cost (SR) or average cost (LR). Simple example. Demand is defined by p=24-q, and total cost is defined by TC=q 2, so that MC = 2*q (you will be given this, not be expected to derive it). If we know that p=24-q, we can use the bisection rule to define MR=24-2*q, since R=p*q, =24q- q 2. Where is MR=MC? Where is 24-2*q=2*q, 24=4q, or q=6. At a quantity of six, I plug back into the demand curve and find that p=24-6, or 18. [note: a common mistake is to plug back into MR curve to solve for price]

8 Profit for me at this point is revenue minus cost, or 18*6-6*6, or 72. To make life easier on us, I will tend to give you a constant marginal cost, but the procedure is the same.

9 How does this differ from a perfectly competitive market in terms of outcome? If we use the given demand curve and recall that the MC curve traces out the supply curve in a perfectly competitive market, we find: 24-q=2q where supply and demand meet at a (p,q) pair, which solves for q * =8, implying that p * =16. [show on graph] There is a deadweight loss of monopoly. The market structure makes it so that transactions that would occur in a perfectly competitive market do no occur, thus reducing total societal welfare. Note efficiency / equity distinction.

10 Now we can modify the example. Change cost, so that TC=2*q, MC=AC=2. Keep demand at p=24-q. This is the horizontal supply curve discussed last class. For the monopolist, MR = MC, so 24-2q=2. This solves for q m =11, which is where p m =13. In perfect competition by contrast, 24-q=2 when q pc =22, so that p pc =2. CS with perfect competition is the area above the competition price line and below the demand curve, a triangle. When q=0, p=24 by the demand curve. So we have (p when q=0 - p competition )*(q competition )*(1/2)=(24-2)*22*(1/2)=242 CS with monopoly is the area above the monopoly price line and below the demand curve, a triangle. (p when q=0 - p monopoly )*(q monopoly )*(1/2)=(24-13)*11*(1/2)=60 ½. PS with perfect competition is the area below the price line and above the supply curve = 0. PS with monopoly is the area defined by: (p monopoly -mc)*(q monopoly ), or (13-2)*11 =121 Total welfare under competition is 0+242=242 Total welfare under monopoly is ½, or 181.5

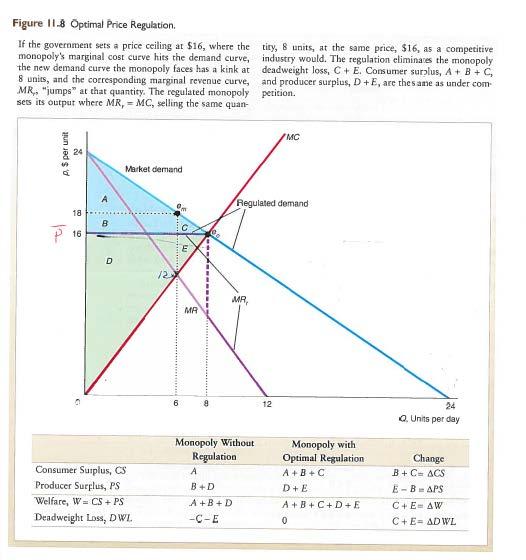

11 This illustrates a general result total welfare is reduced under monopoly market structure compared to a perfectly competitive market. So what can we do about a monopoly? 1) Optimal price regulation, which sets a price ceiling. What would the equilibrium market clearing price quantity pair be if the market was competitive? Set the price ceiling at this level, so that the demand curve facing the monopolist is modified to have a flat spot, then decrease after passing to the right of this p, q pair.

12

13 [show graph when the price ceiling is set too low]

14 This is very difficult to get right if you don t know the actual demand and cost curves. Also may have a natural monopoly that is defined by decreasing average costs over the total range of feasible output levels. This means MC is below AC over this range as well, since if AC is downward sloping, that means MC is below it. A policy that sets the price ceiling based on the marginal cost curve would make it better for the monopolist to shut down rather than produce (thus losing whatever consumer and producer surplus we are getting under the monopoly situation).

- Section one prohibits contracts, combinations, or conspiracies in restraint of trade.")

15 Anti-Trust Laws Beyond regulating prices, monopolies are prohibited by anti-trust laws and can be regulated through policy. There are anti-trust laws prohibiting actions that are likely to restrain competition. Sherman Act (1890) - Section one prohibits contracts, combinations, or conspiracies in restraint of trade. - Example: agreeing to restrict output or fix price. - Includes both explicit and implicit arrangements.

16 - For example, parallel conduct, in which firm B always follows firm A s pricing, is illegal, even if there is no formal agreement. We will match any competitors lowest price? - Section two makes it illegal to monopolize or attempt to monopolize a market. Clayton Act (1914) - The Sherman Act made it clear that monopolies were illegal, but was unclear about other practices. Thus in 1914, the Clayton Act was passed. - The Clayton Act helped to clarify the Sherman Act. - The Clayton Act prohibits actions that restrain competition. - For example, it prohibits mergers that substantially lessen competition Enforcement: - It also prohibits predatory pricing setting prices below cost to drive competitors out of business. 1. Federal Trade Commission - Created in 1914 to set standards dealing with anti-trust. 2. Department of Justice's Anti-Trust Division - Interpretation of laws may vary as political power changes, as it is part of the executive branch. 3. Private legal proceedings

Monopolistic Markets. Causes of Monopolies

Monopolistic Markets Causes of Monopolies The causes of monopolization Monoplositic resources Only one firm owns a resource which is crucial for production (e.g. diamond monopol of DeBeers). Monopols created

Monopolistic Markets Causes of Monopolies The causes of monopolization Monoplositic resources Only one firm owns a resource which is crucial for production (e.g. diamond monopol of DeBeers). Monopols created

Chapter 8 Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets

Managerial Economics & Business Strategy Chapter 8 Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All

Managerial Economics & Business Strategy Chapter 8 Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All

Lecture 12. Monopoly

Lecture 12 Monopoly By the end of this lecture, you should understand: why some markets have only one seller how a monopoly determines the quantity to produce and the price to charge how the monopoly s

Lecture 12 Monopoly By the end of this lecture, you should understand: why some markets have only one seller how a monopoly determines the quantity to produce and the price to charge how the monopoly s

ECN 3103 INDUSTRIAL ORGANISATION

ECN 3103 INDUSTRIAL ORGANISATION 3. Monopoly Mr. Sydney Armstrong Lecturer 1 The University of Guyana 1 Semester 1, 2016 OUR PLAN Monopoly Reference for reviewing these concepts: Carlton, Perloff, Modern

ECN 3103 INDUSTRIAL ORGANISATION 3. Monopoly Mr. Sydney Armstrong Lecturer 1 The University of Guyana 1 Semester 1, 2016 OUR PLAN Monopoly Reference for reviewing these concepts: Carlton, Perloff, Modern

CH 15: Monopoly. Lecture

CH 15: Monopoly Lecture Characteristics of Monopolies A monopoly is a market structure in which one firm makes up the entire market Firm=Industry Characteristics of Monopolies The monopolist is a price

CH 15: Monopoly Lecture Characteristics of Monopolies A monopoly is a market structure in which one firm makes up the entire market Firm=Industry Characteristics of Monopolies The monopolist is a price

Monopolistic Markets. Regulation

Monopolistic Markets Regulation Comparison of monopolistic and competitive equilibrium output The profits of a monopolist are maximized when MC(Q M ) = P(Q M ) + Q P (Q M ) negative In a competitive market:

Monopolistic Markets Regulation Comparison of monopolistic and competitive equilibrium output The profits of a monopolist are maximized when MC(Q M ) = P(Q M ) + Q P (Q M ) negative In a competitive market:

- pure monopoly: only one seller of a good/service with no close substitutes

Micro 101, Chapter 10 1 Chapter 10: Monopoly Main objectives: 1. Define what constitutes a monopoly - pure monopoly: only one seller of a good/service with no close substitutes 2. Describe types of barriers

Micro 101, Chapter 10 1 Chapter 10: Monopoly Main objectives: 1. Define what constitutes a monopoly - pure monopoly: only one seller of a good/service with no close substitutes 2. Describe types of barriers

Monopoly. Cost. Average total cost. Quantity of Output

While a competitive firm is a price taker, a monopoly firm is a price maker. A firm is considered a monopoly if... it is the sole seller of its product. its product does not have close substitutes. The

While a competitive firm is a price taker, a monopoly firm is a price maker. A firm is considered a monopoly if... it is the sole seller of its product. its product does not have close substitutes. The

Monopoly. While a competitive firm is a price taker, a monopoly firm is a price maker.

Monopoly Monopoly While a competitive firm is a price taker, a monopoly firm is a price maker. Monopoly A firm is considered a monopoly if... it is the sole seller of its product. its product does not

Monopoly Monopoly While a competitive firm is a price taker, a monopoly firm is a price maker. Monopoly A firm is considered a monopoly if... it is the sole seller of its product. its product does not

ECON 4100: Industrial Organization. Lecture 1- Introduction and a review of perfect competition versus monopoly

ECON 4100: Industrial Organization Lecture 1- Introduction and a review of perfect competition versus monopoly 1 Introductory Remarks Overview study of firms and markets strategic competition Different

ECON 4100: Industrial Organization Lecture 1- Introduction and a review of perfect competition versus monopoly 1 Introductory Remarks Overview study of firms and markets strategic competition Different

Monopoly. PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University

15 Monopoly PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University 1 Market power Why Monopolies Arise Alters the relationship between a firm s costs and the selling price Monopoly

15 Monopoly PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University 1 Market power Why Monopolies Arise Alters the relationship between a firm s costs and the selling price Monopoly

ECON 2100 (Summer 2016 Sections 10 & 11) Exam #3C

Exam #3C") ECON 21 (Summer 216 Sections 1 & 11) Exam #3C Multiple Choice Questions: (3 points each) 1. I am taking of the exam. C. Version C 2. is a market structure in which there is one single seller of a unique

ECON 21 (Summer 216 Sections 1 & 11) Exam #3C Multiple Choice Questions: (3 points each) 1. I am taking of the exam. C. Version C 2. is a market structure in which there is one single seller of a unique

ECON 2100 (Summer 2016 Sections 10 & 11) Exam #3D

Exam #3D") ECON 21 (Summer 216 Sections 1 & 11) Exam #3D Multiple Choice Questions: (3 points each) 1. I am taking of the exam. D. Version D 2. is a market structure in which there is one single seller of a unique

ECON 21 (Summer 216 Sections 1 & 11) Exam #3D Multiple Choice Questions: (3 points each) 1. I am taking of the exam. D. Version D 2. is a market structure in which there is one single seller of a unique

Monopoly. Chapter 15

Monopoly Chapter 15 Monopoly While a competitive firm is a price taker, a monopoly firm is a price maker. Monopoly u A firm is considered a monopoly if... it is the sole seller of its product. its product

Monopoly Chapter 15 Monopoly While a competitive firm is a price taker, a monopoly firm is a price maker. Monopoly u A firm is considered a monopoly if... it is the sole seller of its product. its product

ECON 2100 Principles of Microeconomics (Summer 2016) Monopoly

Monopoly") ECON 21 Principles of Microeconomics (Summer 216) Monopoly Relevant readings from the textbook: Mankiw, Ch. 15 Monopoly Suggested problems from the textbook: Chapter 15 Questions for Review (Page 323):

ECON 21 Principles of Microeconomics (Summer 216) Monopoly Relevant readings from the textbook: Mankiw, Ch. 15 Monopoly Suggested problems from the textbook: Chapter 15 Questions for Review (Page 323):

iv. The monopolist will receive economic profits as long as price is greater than the average total cost

Chapter 15: Monopoly (Lecture Outline) -------------------------------------------------------------------------------------------------------------------------- Monopolies have no close competitors and,

Chapter 15: Monopoly (Lecture Outline) -------------------------------------------------------------------------------------------------------------------------- Monopolies have no close competitors and,

Market structures. Why Monopolies Arise. Why Monopolies Arise. Market power. Monopoly. Monopoly resources

Market structures Why Monopolies Arise Market power Alters the relationship between a firm s costs and the selling price Charges a price that exceeds marginal cost A high price reduces the quantity purchased

Market structures Why Monopolies Arise Market power Alters the relationship between a firm s costs and the selling price Charges a price that exceeds marginal cost A high price reduces the quantity purchased

Market structure 1: Perfect Competition The perfectly competitive firm is a price taker: it cannot influence the price that is paid for its product.

Market structure 1: Perfect Competition The perfectly competitive firm is a price taker: it cannot influence the price that is paid for its product. This arises due to consumers indifference between the

Market structure 1: Perfect Competition The perfectly competitive firm is a price taker: it cannot influence the price that is paid for its product. This arises due to consumers indifference between the

Quiz #5 Week 04/12/2009 to 04/18/2009

Quiz #5 Week 04/12/2009 to 04/18/2009 You have 30 minutes to answer the following 17 multiple choice questions. Record your answers in the bubble sheet. Your grade in this quiz will count for 1% of your

Quiz #5 Week 04/12/2009 to 04/18/2009 You have 30 minutes to answer the following 17 multiple choice questions. Record your answers in the bubble sheet. Your grade in this quiz will count for 1% of your

Monopoly. 3 Microeconomics LESSON 5. Introduction and Description. Time Required. Materials

LESSON 5 Monopoly Introduction and Description Lesson 5 extends the theory of the firm to the model of a Students will see that the profit-maximization rules for the monopoly are the same as they were

LESSON 5 Monopoly Introduction and Description Lesson 5 extends the theory of the firm to the model of a Students will see that the profit-maximization rules for the monopoly are the same as they were

Question 1 A. In order to find optimal level of consumption and utility, we set MRS=MRT. These are found by:

Question 1 A. In order to find optimal level of consumption and utility, we set MRS=MRT. These are found by: With x isolated, we now insert to budget constraint: Therefore, optimal consumption is: x=100,

Question 1 A. In order to find optimal level of consumption and utility, we set MRS=MRT. These are found by: With x isolated, we now insert to budget constraint: Therefore, optimal consumption is: x=100,

Demand curve - using Game Results How much customers will buy at a given price Downward sloping - more demand at lower prices

31 October Bige Kahraman Class Notes First half of course (Michaelmas) is Microeconomics, second half (Hilary) is Macroeconomics Focusing on profit maximization & price formation Looking at industry level

31 October Bige Kahraman Class Notes First half of course (Michaelmas) is Microeconomics, second half (Hilary) is Macroeconomics Focusing on profit maximization & price formation Looking at industry level

Lecture 2: Market Structure I (Perfect Competition and Monopoly)

") Lecture 2: Market Structure I (Perfect Competition and Monopoly) EC 105. Industrial Organization Matt Shum HSS, California Institute of Technology October 1, 2012 EC 105. Industrial Organization ( Matt

Lecture 2: Market Structure I (Perfect Competition and Monopoly) EC 105. Industrial Organization Matt Shum HSS, California Institute of Technology October 1, 2012 EC 105. Industrial Organization ( Matt

Market Power at Work: Computer Market Revisited

Monopolies Part II Competition is always a good thing. It forces us to do our best. A monopoly renders people complacent and satisfied with mediocrity. Nancy Pearcey Market Power at Work: Computer Market

Monopolies Part II Competition is always a good thing. It forces us to do our best. A monopoly renders people complacent and satisfied with mediocrity. Nancy Pearcey Market Power at Work: Computer Market

Practice Exam 3: S201 Walker Fall with answers to MC

Practice Exam 3: S201 Walker Fall 2007 - with answers to MC Print Your Name: I. Multiple Choice (3 points each) 1. If marginal utility is falling then A. total utility must be falling. B. marginal utility

Practice Exam 3: S201 Walker Fall 2007 - with answers to MC Print Your Name: I. Multiple Choice (3 points each) 1. If marginal utility is falling then A. total utility must be falling. B. marginal utility

CHAPTER NINE MONOPOLY

CHAPTER NINE MONOPOLY This chapter examines how a market controlled by a single producer behaves. What price will a monopolist charge for his output? How much will he produce? The basic characteristics

CHAPTER NINE MONOPOLY This chapter examines how a market controlled by a single producer behaves. What price will a monopolist charge for his output? How much will he produce? The basic characteristics

Industrial Organisation ECON309

Industrial Organisation ECON309 Introduction Industrial Organisation is the study of how firms behave in markets. Industrial organisation takes a strategic view of how firms interact and it deals with

Industrial Organisation ECON309 Introduction Industrial Organisation is the study of how firms behave in markets. Industrial organisation takes a strategic view of how firms interact and it deals with

EconS Perfect Competition and Monopoly

EconS 425 - Perfect Competition and Monopoly Eric Dunaway Washington State University eric.dunaway@wsu.edu Industrial Organization Eric Dunaway (WSU) EconS 425 Industrial Organization 1 / 47 Introduction

EconS 425 - Perfect Competition and Monopoly Eric Dunaway Washington State University eric.dunaway@wsu.edu Industrial Organization Eric Dunaway (WSU) EconS 425 Industrial Organization 1 / 47 Introduction

Eastern Mediterranean University Faculty of Business and Economics Department of Economics Fall Semester

Eastern Mediterranean University Faculty of Business and Economics Department of Economics 2016-17 Fall Semester Duration: 110 minutes ECON101 - Introduction to Economics I Final Exam Type A 11 January

Eastern Mediterranean University Faculty of Business and Economics Department of Economics 2016-17 Fall Semester Duration: 110 minutes ECON101 - Introduction to Economics I Final Exam Type A 11 January

Monopoly. Basic Economics Chapter 15. Why Monopolies Arise. Monopoly

1 Why Monopolies Arise Basic Economics Chapter 15 Monopoly Monopoly - The monopolist is a firm that is the sole seller of a product (or service) without close substitutes - The monopolist is a price maker

1 Why Monopolies Arise Basic Economics Chapter 15 Monopoly Monopoly - The monopolist is a firm that is the sole seller of a product (or service) without close substitutes - The monopolist is a price maker

Practice Exam 3: S201 Walker Fall 2009

Practice Exam 3: S201 Walker Fall 2009 I. Multiple Choice (3 points each) 1. Which of the following statements about the short-run is false? A. The marginal product of labor may increase or decrease. B.

Practice Exam 3: S201 Walker Fall 2009 I. Multiple Choice (3 points each) 1. Which of the following statements about the short-run is false? A. The marginal product of labor may increase or decrease. B.

ECON 102 Brown Final Exam Practice Exam Solutions

www.liontutors.com ECON 102 Brown Final Exam Practice Exam Solutions 1. B 2. C 3. C All products are identical (homogenous) in perfect competition so there is no such thing as brand preference. 4. C Breakeven

www.liontutors.com ECON 102 Brown Final Exam Practice Exam Solutions 1. B 2. C 3. C All products are identical (homogenous) in perfect competition so there is no such thing as brand preference. 4. C Breakeven

Monopoly and How It Arises

Monopoly and How It Arises A monopoly is a market: That produces a good or service for which no close substitute exists In which there is one supplier that is protected from competition by a barrier preventing

Monopoly and How It Arises A monopoly is a market: That produces a good or service for which no close substitute exists In which there is one supplier that is protected from competition by a barrier preventing

Chapter 13 MODELS OF MONOPOLY. Copyright 2005 by South-Western, a division of Thomson Learning. All rights reserved.

Chapter 13 MODELS OF MONOPOLY Copyright 2005 by South-Western, a division of Thomson Learning. All rights reserved. 1 Monopoly A monopoly is a single supplier to a market This firm may choose to produce

Chapter 13 MODELS OF MONOPOLY Copyright 2005 by South-Western, a division of Thomson Learning. All rights reserved. 1 Monopoly A monopoly is a single supplier to a market This firm may choose to produce

Indicate whether the sentence or statement is True or False. Mark "A" if the statement is True or "B" if it is False.

2004 SLC Economics Page 1 Indicate whether the sentence or statement is True or False. Mark "A" if the statement is True or "B" if it is False. 1. The marginal social cost equals the marginal private cost

2004 SLC Economics Page 1 Indicate whether the sentence or statement is True or False. Mark "A" if the statement is True or "B" if it is False. 1. The marginal social cost equals the marginal private cost

Monopoly and How It Arises

13 MONOPOLY Monopoly and How It Arises A monopoly is a market: That produces a good or service for which no close substitute exists If a good has a close substitute, even if it is produced by only one

13 MONOPOLY Monopoly and How It Arises A monopoly is a market: That produces a good or service for which no close substitute exists If a good has a close substitute, even if it is produced by only one

The Four Main Market Structures

Competitive Firms and Markets The Four Main Market Structures Market structure: the number of firms in the market, the ease with which firms can enter and leave the market, and the ability of firms to

Competitive Firms and Markets The Four Main Market Structures Market structure: the number of firms in the market, the ease with which firms can enter and leave the market, and the ability of firms to

Eco 300 Intermediate Micro

Eco 300 Intermediate Micro Instructor: Amalia Jerison Office Hours: T 12:00-1:00, Th 12:00-1:00, and by appointment BA 127A, aj4575@albany.edu A. Jerison (BA 127A) Eco 300 Spring 2010 1 / 61 Monopoly Market

Eco 300 Intermediate Micro Instructor: Amalia Jerison Office Hours: T 12:00-1:00, Th 12:00-1:00, and by appointment BA 127A, aj4575@albany.edu A. Jerison (BA 127A) Eco 300 Spring 2010 1 / 61 Monopoly Market

Unit 6 Perfect Competition and Monopoly - Practice Problems

Unit 6 Perfect Competition and Monopoly - Practice Problems Multiple Choice Identify the choice that best completes the statement or answers the question. 1. One characteristic of a perfectly competitive

Unit 6 Perfect Competition and Monopoly - Practice Problems Multiple Choice Identify the choice that best completes the statement or answers the question. 1. One characteristic of a perfectly competitive

Chapter 13. Microeconomics. Monopolistic Competition: The Competitive Model in a More Realistic Setting

Microeconomics Modified by: Yun Wang Florida International University Spring, 2018 1 Chapter 13 Monopolistic Competition: The Competitive Model in a More Realistic Setting Chapter Outline 13.1 Demand and

Microeconomics Modified by: Yun Wang Florida International University Spring, 2018 1 Chapter 13 Monopolistic Competition: The Competitive Model in a More Realistic Setting Chapter Outline 13.1 Demand and

INTERPRETATION. SOURCES OF MONOPOLY (Related to P-R pp )

") ECO 300 Fall 2005 November 10 MONOPOLY PART 1 INTERPRETATION Literally, just one firm in an industry But interpretation depends on how you define industry General idea a group of commodities that are close

ECO 300 Fall 2005 November 10 MONOPOLY PART 1 INTERPRETATION Literally, just one firm in an industry But interpretation depends on how you define industry General idea a group of commodities that are close

Perfectly Competitive Markets

Characteristics: Fragmented: Many small firms, none of which have market power Undifferentiated Products: Products that consumers perceive as being identical. Perfect Pricing Information: Consumers have

Characteristics: Fragmented: Many small firms, none of which have market power Undifferentiated Products: Products that consumers perceive as being identical. Perfect Pricing Information: Consumers have

MICROECONOMICS - CLUTCH CH MONOPOLISTIC COMPETITION.

!! www.clutchprep.com CONCEPT: CHARACTERISTICS OF MONOPOLISTIC COMPETITION A market is in monopolistic competition when: Nature of Good: The goods for sale are, but not identical - Products are said to

!! www.clutchprep.com CONCEPT: CHARACTERISTICS OF MONOPOLISTIC COMPETITION A market is in monopolistic competition when: Nature of Good: The goods for sale are, but not identical - Products are said to

micro2 first module Social costs of monopoly Price regulation Price regulation Price regulation overshooting Natural monopoly Market power part III

Lecture 5 Market power part III Kosmas Marinakis, Ph.D. micro2 first module ocial costs of monopoly The social cost of monopoly is likely to exceed the deadweight loss Rent eeking: firms may use resources

Lecture 5 Market power part III Kosmas Marinakis, Ph.D. micro2 first module ocial costs of monopoly The social cost of monopoly is likely to exceed the deadweight loss Rent eeking: firms may use resources

Chapter 11 Perfect Competition

Chapter 11 Perfect Competition Introduction: To an economist, a competitive firm is a firm that does not determine its market price. This type of firm is free to sell as many units of its good as it wishes

Chapter 11 Perfect Competition Introduction: To an economist, a competitive firm is a firm that does not determine its market price. This type of firm is free to sell as many units of its good as it wishes

Principles of. Economics. Week 6. Firm in Competitive & Monopoly market. 7 th April 2014

Principles of Economics Week 6 Firm in Competitive & Monopoly market 7 th April 2014 In this week, look for the answers to these questions:!what is a perfectly competitive market?!what is marginal revenue?

Principles of Economics Week 6 Firm in Competitive & Monopoly market 7 th April 2014 In this week, look for the answers to these questions:!what is a perfectly competitive market?!what is marginal revenue?

EconS Monopoly - Part 1

EconS 305 - Monopoly - Part 1 Eric Dunaway Washington State University eric.dunaway@wsu.edu October 23, 2015 Eric Dunaway (WSU) EconS 305 - Lecture 23 October 23, 2015 1 / 50 Introduction For the rest

EconS 305 - Monopoly - Part 1 Eric Dunaway Washington State University eric.dunaway@wsu.edu October 23, 2015 Eric Dunaway (WSU) EconS 305 - Lecture 23 October 23, 2015 1 / 50 Introduction For the rest

BS2243 Lecture 9 Advertisement. Spring 2012 (Dr. Sumon Bhaumik)

") BS2243 Lecture 9 Advertisement Spring 2012 (Dr. Sumon Bhaumik) Why advertise? Building brands Creating markets for new products (scope economies) Price competition / Price protection Barrier to entry Product

BS2243 Lecture 9 Advertisement Spring 2012 (Dr. Sumon Bhaumik) Why advertise? Building brands Creating markets for new products (scope economies) Price competition / Price protection Barrier to entry Product

Industrial Organization

Industrial Organization Session 4: The Monopoly Jiangli Dou School of Economics Jiangli Dou (School of Economics) Industrial Organization 1 / 43 Introduction In this session, we study a theory of a single

Industrial Organization Session 4: The Monopoly Jiangli Dou School of Economics Jiangli Dou (School of Economics) Industrial Organization 1 / 43 Introduction In this session, we study a theory of a single

Lecture 10: Market Power and Monopoly

Lecture 10: Market Power and Monopoly November 8, 2016 Overview Course Administration Sources of Market Power Market Power and Marginal Revenue Profit Maximization and Market Power How a Firm With Market

Lecture 10: Market Power and Monopoly November 8, 2016 Overview Course Administration Sources of Market Power Market Power and Marginal Revenue Profit Maximization and Market Power How a Firm With Market

AP Microeconomics Review Session #3 Key Terms & Concepts

The Firm, Profit, and the Costs of Production 1. Explicit vs. implicit costs 2. Short-run vs. long-run decisions 3. Fixed inputs vs. variable inputs 4. Short-run production measures: be able to calculate/graph

The Firm, Profit, and the Costs of Production 1. Explicit vs. implicit costs 2. Short-run vs. long-run decisions 3. Fixed inputs vs. variable inputs 4. Short-run production measures: be able to calculate/graph

Unit 7. Firm behaviour and market structure: monopoly

Unit 7. Firm behaviour and market structure: monopoly Quiz 1. What of the following can be considered as the measure of a market power? A. ; B. ; C.. Answers A and B are both correct; E. All of the above

Unit 7. Firm behaviour and market structure: monopoly Quiz 1. What of the following can be considered as the measure of a market power? A. ; B. ; C.. Answers A and B are both correct; E. All of the above

Chapter 11. Monopoly. I think it s wrong that only one company makes the game Monopoly. Steven Wright

Chapter 11 Monopoly I think it s wrong that only one company makes the game Monopoly. Steven Wright Chapter 11 Outline 11.1 Monopoly Profit Maximization 11.2 Market Power 11.3 Welfare Effects of Monopoly

Chapter 11 Monopoly I think it s wrong that only one company makes the game Monopoly. Steven Wright Chapter 11 Outline 11.1 Monopoly Profit Maximization 11.2 Market Power 11.3 Welfare Effects of Monopoly

14.1 Comparison of Market Structures

14.1 Comparison of Structures Chapter 14 Oligopoly 14-2 14.2 Cartels Cartel in Korea Oligopolistic firms have an incentive to collude, coordinate setting their prices or quantities, so as to increase their

14.1 Comparison of Structures Chapter 14 Oligopoly 14-2 14.2 Cartels Cartel in Korea Oligopolistic firms have an incentive to collude, coordinate setting their prices or quantities, so as to increase their

Lecture 11: Market Power and Monopoly

Lecture 11: Market Power and Monopoly November 13, 2018 Overview Course Administration Sources of Market Power Market Power and Marginal Revenue Profit Maximization and Market Power How a Firm With Market

Lecture 11: Market Power and Monopoly November 13, 2018 Overview Course Administration Sources of Market Power Market Power and Marginal Revenue Profit Maximization and Market Power How a Firm With Market

PRINCIPLES OF MICROECONOMICS E L E V E N T H E D I T I O N CASE FAIR OSTER. PEARSON Prepared by: Fernando Quijano w/shelly Tefft

PRINCIPLES OF MICROECONOMICS E L E V E N T H E D I T I O N CASE FAIR OSTER PEARSON Prepared by: Fernando Quijano w/shelly Tefft 2 of 25 PART III MARKET IMPERFECTIONS AND THE ROLE OF GOVERNMENT Monopoly

PRINCIPLES OF MICROECONOMICS E L E V E N T H E D I T I O N CASE FAIR OSTER PEARSON Prepared by: Fernando Quijano w/shelly Tefft 2 of 25 PART III MARKET IMPERFECTIONS AND THE ROLE OF GOVERNMENT Monopoly

Lecture 2: Market Structure Part I (Perfect Competition and Monopoly)

") Lecture 2: Market Structure Part I (Perfect Competition and Monopoly) EC 105. Industrial Organization Matt Shum HSS, California Institute of Technology EC 105. Industrial Organization ( Matt ShumLecture

Lecture 2: Market Structure Part I (Perfect Competition and Monopoly) EC 105. Industrial Organization Matt Shum HSS, California Institute of Technology EC 105. Industrial Organization ( Matt ShumLecture

11.1 Monopoly Profit Maximization

11.1 Monopoly Profit Maximization CHAPTER 11 MONOPOLY A monopoly is the only supplier of a good for which there is no close substitute. Monopolies are not price takers like competitive firms Monopoly output

11.1 Monopoly Profit Maximization CHAPTER 11 MONOPOLY A monopoly is the only supplier of a good for which there is no close substitute. Monopolies are not price takers like competitive firms Monopoly output

Econ 2113: Principles of Microeconomics. Spring 2009 ECU

Econ 2113: Principles of Microeconomics Spring 2009 ECU Chapter 12 Monopoly Market Power Market power is the ability to influence the market, and in particular the market price, by influencing the total

Econ 2113: Principles of Microeconomics Spring 2009 ECU Chapter 12 Monopoly Market Power Market power is the ability to influence the market, and in particular the market price, by influencing the total

S11Microeconomics, Exam 3 Answer Key. Instruction:

S11Microeconomics, Exam 3 Answer Key Instruction: Exam 3 Student Name: Microeconomics, several versions Early May, 2011 Instructions: I) On your Scantron card you must print three things: 1) Full name

S11Microeconomics, Exam 3 Answer Key Instruction: Exam 3 Student Name: Microeconomics, several versions Early May, 2011 Instructions: I) On your Scantron card you must print three things: 1) Full name

Monopoly CHAPTER 15. Henry Demarest Lloyd. Monopoly is business at the end of its journey. Monopoly 15. McGraw-Hill/Irwin

CHAPTER 15 Monopoly Monopoly is business at the end of its journey. Henry Demarest Lloyd McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved. A Monopolistic Market A

CHAPTER 15 Monopoly Monopoly is business at the end of its journey. Henry Demarest Lloyd McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved. A Monopolistic Market A

Lecture 11: Market Power and Monopoly

Lecture 11: Market Power and Monopoly November 14, 2017 Overview Course Administration Sources of Market Power Market Power and Marginal Revenue Profit Maximization and Market Power How a Firm With Market

Lecture 11: Market Power and Monopoly November 14, 2017 Overview Course Administration Sources of Market Power Market Power and Marginal Revenue Profit Maximization and Market Power How a Firm With Market

MONOPOLY. Characteristics

OBJECTIVES Explain how managers should set price and output when they have market power With monopoly power, the firm s demand curve is the market demand curve. A monopolist is the only seller of a product

OBJECTIVES Explain how managers should set price and output when they have market power With monopoly power, the firm s demand curve is the market demand curve. A monopolist is the only seller of a product

Firms in competitive markets: Perfect Competition and Monopoly

Lesson 6 Firms in competitive markets: Perfect Competition and Monopoly Henan University of Technology Sino-British College Transfer Abroad Undergraduate Programme 0 In this lesson, look for the answers

Lesson 6 Firms in competitive markets: Perfect Competition and Monopoly Henan University of Technology Sino-British College Transfer Abroad Undergraduate Programme 0 In this lesson, look for the answers

Oligopoly and Monopolistic Competition

Oligopoly and Monopolistic Competition Introduction Managerial Problem Airbus and Boeing are the only two manufacturers of large commercial aircrafts. If only one receives a government subsidy, how can

Oligopoly and Monopolistic Competition Introduction Managerial Problem Airbus and Boeing are the only two manufacturers of large commercial aircrafts. If only one receives a government subsidy, how can

Average Cost 0 20 NA NA NA a) Is this a short run or long run information on cost? Why?

Is this a short run or long run information on cost? Why?") McPeak PPA 723 Exam 2 Name: All numbered questions are worth 2 points each, sub questions worth an equal share of these 2 points. 1) Complete the following table. Output Fixed Cost Total Cost Variable

McPeak PPA 723 Exam 2 Name: All numbered questions are worth 2 points each, sub questions worth an equal share of these 2 points. 1) Complete the following table. Output Fixed Cost Total Cost Variable

13 C H A P T E R O U T L I N E

PEARSON PRINCIPLES OF MICROECONOMICS E L E V E N T H E D I T I O N CASE FAIR OSTER Prepared by: Fernando Quijano w/shelly Tefft 2of 37 PART III MARKET IMPERFECTIONS AND THE ROLE OF GOVERNMENT Monopoly

PEARSON PRINCIPLES OF MICROECONOMICS E L E V E N T H E D I T I O N CASE FAIR OSTER Prepared by: Fernando Quijano w/shelly Tefft 2of 37 PART III MARKET IMPERFECTIONS AND THE ROLE OF GOVERNMENT Monopoly

4. Which of the following statements about marginal revenue for a perfectly competitive firm is incorrect? A) TR

TR") Name: Date: 1. Which of the following will not be true of a perfectly competitive market? A) Buyers and sellers will have an imperceptible effect on the market. B) Firms can freely enter and exit the market.

Name: Date: 1. Which of the following will not be true of a perfectly competitive market? A) Buyers and sellers will have an imperceptible effect on the market. B) Firms can freely enter and exit the market.

AGEC 105 Homework Consider a monopolist that faces the demand curve given in the following table.

AGEC 105 Homework 7 1. Consider a monopolist that faces the demand curve given in the following table. a. Fill in the table by calculating total revenue and marginal revenue at each price. Price Quantity

AGEC 105 Homework 7 1. Consider a monopolist that faces the demand curve given in the following table. a. Fill in the table by calculating total revenue and marginal revenue at each price. Price Quantity

Review. 1. Production function - Types of production functions - Marginal productivity - Returns to scale

Review 1. Production function - Types of production functions - Marginal productivity - Returns to scale 2. The cost minimization problem - Solution: MP L (K,L)/w = MP K (K,L)/r - What happens when price

Review 1. Production function - Types of production functions - Marginal productivity - Returns to scale 2. The cost minimization problem - Solution: MP L (K,L)/w = MP K (K,L)/r - What happens when price

Principles of Microeconomics ECONOMICS 103. Topic 8: Imperfect Competition. Single price monopoly. Monopolistic competition.

ECONOMICS 103 Topic 8: Imperfect Competition Single price monopoly. Monopolistic competition. 1 COMPETITIVE MARKETS V MONOPOLY Thus far, all firms have been price takers. - Markets are characterized by

ECONOMICS 103 Topic 8: Imperfect Competition Single price monopoly. Monopolistic competition. 1 COMPETITIVE MARKETS V MONOPOLY Thus far, all firms have been price takers. - Markets are characterized by

14.54 International Trade Lecture 17: Increasing Returns to Scale

14.54 International Trade Lecture 17: Increasing Returns to Scale 14.54 Week 11 Fall 2016 14.54 (Week 11) Increasing Returns Fall 2016 1 / 25 Today s Plan 1 2 Increasing Returns to Scale: General Discussion

14.54 International Trade Lecture 17: Increasing Returns to Scale 14.54 Week 11 Fall 2016 14.54 (Week 11) Increasing Returns Fall 2016 1 / 25 Today s Plan 1 2 Increasing Returns to Scale: General Discussion

I. Introduction to Monopolies

University of Pacific-Economics 53 Lecture Notes #13 I. Introduction to Monopolies As we saw in the last lecture, an industry in which individual firms have some control over setting the price of their

University of Pacific-Economics 53 Lecture Notes #13 I. Introduction to Monopolies As we saw in the last lecture, an industry in which individual firms have some control over setting the price of their

QUIZ 4 VERSION A "Introduction to Antitrust"

Drake University, Spring 2013 William M. Boal Signature: Printed name: QUIZ 4 VERSION A "Introduction to Antitrust" INSTRUCTIONS: This exam is closed-book, closed-notes. Simple calculators are permitted,

Drake University, Spring 2013 William M. Boal Signature: Printed name: QUIZ 4 VERSION A "Introduction to Antitrust" INSTRUCTIONS: This exam is closed-book, closed-notes. Simple calculators are permitted,

Chapter 8. Competitive Firms and Markets

Chapter 8 Competitive Firms and Markets Topics Perfect Competition. Profit Maximization. Competition in the Short Run. Competition in the Long Run. 8-2 Copyright 2012 Pearson Addison-Wesley. All rights

Chapter 8 Competitive Firms and Markets Topics Perfect Competition. Profit Maximization. Competition in the Short Run. Competition in the Long Run. 8-2 Copyright 2012 Pearson Addison-Wesley. All rights

Monopoly CHAPTER. Goals. Outcomes

CHAPTER 15 Monopoly Goals in this chapter you will Learn why some markets have only one seller Analyze how a monopoly determines the quantity to produce and the price to charge See how the monopoly s decisions

CHAPTER 15 Monopoly Goals in this chapter you will Learn why some markets have only one seller Analyze how a monopoly determines the quantity to produce and the price to charge See how the monopoly s decisions

EconS Monopoly - Part 2

EconS 305 - Monopoly - Part 2 Eric Dunaway Washington State University eric.dunaway@wsu.edu October 26, 2015 Eric Dunaway (WSU) EconS 305 - Lecture 24 October 26, 2015 1 / 47 Introduction Last time, we

EconS 305 - Monopoly - Part 2 Eric Dunaway Washington State University eric.dunaway@wsu.edu October 26, 2015 Eric Dunaway (WSU) EconS 305 - Lecture 24 October 26, 2015 1 / 47 Introduction Last time, we

Marginal Cost. Average Cost 0 20 NA NA NA a) Is this a short run or long run information on cost? Why?

Is this a short run or long run information on cost? Why?") McPeak PPA 723 Exam 2 Name: All numbered questions are worth 2 points each, sub questions worth an equal share of these 2 points. 1) Complete the following table. Output Fixed Cost Total Cost Variable

McPeak PPA 723 Exam 2 Name: All numbered questions are worth 2 points each, sub questions worth an equal share of these 2 points. 1) Complete the following table. Output Fixed Cost Total Cost Variable

ECON 2100 (Summer 2012 Sections 07 and 08) Exam #3C Answer Key

Exam #3C Answer Key") ECON 21 (Summer 212 Sections 7 and 8) Exam #3C Answer Key Multiple Choice Questions: (3 points each) 1. I am taking of the exam. C. Version C 2. is a market structure in which there is one single seller

ECON 21 (Summer 212 Sections 7 and 8) Exam #3C Answer Key Multiple Choice Questions: (3 points each) 1. I am taking of the exam. C. Version C 2. is a market structure in which there is one single seller

Economics. Monopoly. N. Gregory Mankiw. Premium PowerPoint Slides by Vance Ginn & Ron Cronovich C H A P T E R P R I N C I P L E S O F

C H A P T E R Monopoly Economics P R I N C I P L E S O F N. Gregory Mankiw Premium PowerPoint Slides by Vance Ginn & Ron Cronovich 2009 South-Western, a part of Cengage Learning, all rights reserved In

C H A P T E R Monopoly Economics P R I N C I P L E S O F N. Gregory Mankiw Premium PowerPoint Slides by Vance Ginn & Ron Cronovich 2009 South-Western, a part of Cengage Learning, all rights reserved In

These notes essentially correspond to chapter 11 of the text.

These notes essentially correspond to chapter 11 of the text. 1 Monopoly A monopolist is de ned as a single seller of a well-de ned product for which there are no close substitutes. In reality, there are

These notes essentially correspond to chapter 11 of the text. 1 Monopoly A monopolist is de ned as a single seller of a well-de ned product for which there are no close substitutes. In reality, there are

CH 14. Name: Class: Date: Multiple Choice Identify the choice that best completes the statement or answers the question.

Class: Date: CH 14 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. We define a monopoly as a market with a. one supplier and no barriers to entry. b. one

Class: Date: CH 14 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. We define a monopoly as a market with a. one supplier and no barriers to entry. b. one

Handout 1: Monopolistic Competition and International Trade

Handout 1: Monopolistic Competition and International Trade Introduction to monopolistic competition There are two differences between our previous models (Ricardian, SF and H-O) and models with monopolistic

Handout 1: Monopolistic Competition and International Trade Introduction to monopolistic competition There are two differences between our previous models (Ricardian, SF and H-O) and models with monopolistic

Review Chapters 1 & 2

Review Chapters 1 & 2 ECON 1 Midterm 1 Review Session Scarcity or No Free Lunch Principle. Cost-Benefit Principle. Reservation Price. Economic Surplus = Benefit Cost. Opportunity Cost (DO NOT FORGET!!).

Review Chapters 1 & 2 ECON 1 Midterm 1 Review Session Scarcity or No Free Lunch Principle. Cost-Benefit Principle. Reservation Price. Economic Surplus = Benefit Cost. Opportunity Cost (DO NOT FORGET!!).

Oligopoly and Monopolistic Competition

Oligopoly and Monopolistic Competition Introduction Managerial Problem Airbus and Boeing are the only two manufacturers of large commercial aircrafts. If only one receives a government subsidy, how can

Oligopoly and Monopolistic Competition Introduction Managerial Problem Airbus and Boeing are the only two manufacturers of large commercial aircrafts. If only one receives a government subsidy, how can

Name (Print in BLOCK letters) FIRST HOUR EXAM ECN 4350/6350

FIRST HOUR EXAM ECN 4350/6350") Professor Atkinson Fall, 2012 Name (Print in BLOCK letters) FIRST HOUR EXAM ECN 4350/6350 1) Market equilibria. a) I have drawn in and labelled the industry demand (D). Now draw an upward sloping supply

Professor Atkinson Fall, 2012 Name (Print in BLOCK letters) FIRST HOUR EXAM ECN 4350/6350 1) Market equilibria. a) I have drawn in and labelled the industry demand (D). Now draw an upward sloping supply

Monopoly, Oligopoly, and Monopolistic Competition Chapter 8 McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

Monopoly, Oligopoly, and Monopolistic Competition Chapter 8 McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Learning Objectives 1. Distinguish among three types

Monopoly, Oligopoly, and Monopolistic Competition Chapter 8 McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Learning Objectives 1. Distinguish among three types

Lesson 3-2 Profit Maximization

Lesson 3-2 Profit Maximization Standard 3b: Students will explain the 5 dimensions of market structure and identify how perfect competition, monopoly, monopolistic competition, and oligopoly are characterized

Lesson 3-2 Profit Maximization Standard 3b: Students will explain the 5 dimensions of market structure and identify how perfect competition, monopoly, monopolistic competition, and oligopoly are characterized

Networks, Telecommunications Economics and Strategic Issues in Digital Convergence. Prof. Nicholas Economides. Spring 2006

Networks, Telecommunications Economics and Strategic Issues in Digital Convergence Prof. Nicholas Economides Spring 2006 Basic Market Structure Slides The Structure-Conduct-Performance Model Basic conditions:

Networks, Telecommunications Economics and Strategic Issues in Digital Convergence Prof. Nicholas Economides Spring 2006 Basic Market Structure Slides The Structure-Conduct-Performance Model Basic conditions:

Unit 4: Imperfect Competition

Unit 4: Imperfect Competition 1 Monopoly 2 Characteristics of Monopolies 3 5 Characteristics of a Monopoly 1. Single Seller One Firm controls the vast majority of a market The Firm IS the Industry 2. Unique

Unit 4: Imperfect Competition 1 Monopoly 2 Characteristics of Monopolies 3 5 Characteristics of a Monopoly 1. Single Seller One Firm controls the vast majority of a market The Firm IS the Industry 2. Unique

Perfect Competition CHAPTER14

Perfect Competition CHAPTER14 MARKET TYPES The four market types are Perfect competition Monopoly Monopolistic competition Oligopoly MARKET TYPES Perfect Competition Perfect competition exists when Many

Perfect Competition CHAPTER14 MARKET TYPES The four market types are Perfect competition Monopoly Monopolistic competition Oligopoly MARKET TYPES Perfect Competition Perfect competition exists when Many

Econ 300: Intermediate Microeconomics, Spring 2014 Final Exam Study Guide 1

Econ 300: Intermediate Microeconomics, Spring 2014 Final Exam Study Guide 1 Chronological order of topics covered in class (to the best of my memory). Introduction to Microeconomics (Chapter 1) What is

Econ 300: Intermediate Microeconomics, Spring 2014 Final Exam Study Guide 1 Chronological order of topics covered in class (to the best of my memory). Introduction to Microeconomics (Chapter 1) What is

Economics 101 Spring 2001 Section 4 - Hallam Quiz 10. For questions 1-9, consider firms using a technology with cost and marginal cost functions:

Economics 101 Spring 2001 Section 4 - Hallam Quiz 10 For questions 1-9, consider firms using a technology with cost and marginal cost functions: Cost (q) = 256 + 16 q + q 2 MC(q) = 16 + 2q 1. What is the

Economics 101 Spring 2001 Section 4 - Hallam Quiz 10 For questions 1-9, consider firms using a technology with cost and marginal cost functions: Cost (q) = 256 + 16 q + q 2 MC(q) = 16 + 2q 1. What is the

Tutorial 3 - Sessions 6to8:

Simona Abis Tutorial 3 - Sessions 6to8: Session 7 - Pricing with market power: Essentials: Firms have market power, hence face downward sloping demand curves They can influence market price Charging a

Simona Abis Tutorial 3 - Sessions 6to8: Session 7 - Pricing with market power: Essentials: Firms have market power, hence face downward sloping demand curves They can influence market price Charging a

c) Will the monopolist described in (b) earn positive, negative, or zero economic profits? Explain your answer.

Will the monopolist described in (b) earn positive, negative, or zero economic profits? Explain your answer.") Economics 101 Summer 2015 Answers to Homework #4b Due Tuesday June 16, 2015 Directions: The homework will be collected in a box before the lecture. Please place your name, TA name and section number on

Economics 101 Summer 2015 Answers to Homework #4b Due Tuesday June 16, 2015 Directions: The homework will be collected in a box before the lecture. Please place your name, TA name and section number on

Course informa-on. Final exam. If you have a conflict, go to the Registrar s office for a form to bring to me

Course informa-on Final exam If you have a conflict, go to the Registrar s office for a form to bring to me To do today: Finish compe--on and start monopoly What it is and does: single price and price

Course informa-on Final exam If you have a conflict, go to the Registrar s office for a form to bring to me To do today: Finish compe--on and start monopoly What it is and does: single price and price

1.3. Levels and Rates of Change Levels: example, wages and income versus Rates: example, inflation and growth Example: Box 1.3

1 Chapter 1 1.1. Scarcity, Choice, Opportunity Cost Definition of Economics: Resources versus Wants Wants: more and better unlimited Versus Needs: essential limited Versus Demand: ability to pay + want

1 Chapter 1 1.1. Scarcity, Choice, Opportunity Cost Definition of Economics: Resources versus Wants Wants: more and better unlimited Versus Needs: essential limited Versus Demand: ability to pay + want

micro2 first module Basic assumptions of PC 2. Product homogeneity 1. Large number of firms Profit maximization in general 3. Free entry and exit

Lecture 2 Perfectly competitive markets Kosmas Marinakis, Ph.. Basic assumptions of PC A market is perfectly competitive when 1. Firms are many 2. Product is homogeneous 3. Entry and exit are free micro2

Lecture 2 Perfectly competitive markets Kosmas Marinakis, Ph.. Basic assumptions of PC A market is perfectly competitive when 1. Firms are many 2. Product is homogeneous 3. Entry and exit are free micro2

Perfect competition: occurs when none of the individual market participants (ie buyers or sellers) can influence the price of the product.

can influence the price of the product.") Perfect Competition In this section of work and the next one we derive the equilibrium positions of firms in order to determine whether or not it is profitable for a firm to produce and, if so, what quantities

Perfect Competition In this section of work and the next one we derive the equilibrium positions of firms in order to determine whether or not it is profitable for a firm to produce and, if so, what quantities

At P = $120, Q = 1,000, and marginal revenue is ,000 = $100

Microeconomics, monopoly, final exam practice problems (The attached PDF file has better formatting.) *Question 1.1: Marginal Revenue Assume the demand curve is linear.! At P = $100, total revenue is $200,000.!

Microeconomics, monopoly, final exam practice problems (The attached PDF file has better formatting.) *Question 1.1: Marginal Revenue Assume the demand curve is linear.! At P = $100, total revenue is $200,000.!