Robert Ackerman Office Hours: 2:00-3:00PM T/Th Office: PA202 (Phillips Hall Annex) Economics 101

|

|

|

- Beverly Tate

- 6 years ago

- Views:

Transcription

1 Robert Ackerman Office Hours: 2:00-3:00PM T/Th Office: PA202 (Phillips Hall Annex) Economics 101

2 Economics 101

3 Today Questions/issues? Frequently missed Aplia Q s Week 2 topics Week 3 topics Economics 101

4 Aplia Questions Overall people are doing really well, especially with the recent material Two commonly missed problems from Week 1, Class 2 HW

5 Week 1, Class 2 #11 Economics 101

6 Electric Cars Production Possibilities Frontier U.S. PPF Smart phones

7 Production Possibilities Frontier: A graph that indicates the maximum amount of one good that can be produced for every possible level of production of the other good Does a shift in the unemployment rate, change the possible combinations of goods we could make if we employed all of our available resources?

8 Week 1, Class 2 #15 What is the decision we are being asked to analyze?

9 Opportunity cost Definition: the value of the next best alternative that the decision forces the decision-maker to forgo. Economics 101

10 Week 1, Class 2 #15 Start a Business Get a Job Pay workers -$100 Income 8x$10 Buy machines -$100 Profits +$240 Total +$40 Total +$80 Opportunity cost: Total costs: Profits-costs:

11 Week 1, Class 2 #15 Start a Business Get a Job Pay workers -$100 Income 8x$10 Buy machines -$100 Profits +$240 Total +$40 Total +$80 Opportunity cost: -$80 Total cost: -$280 Profits-costs: $240-$100-$100-$80=-$40

12 Week 1, Class 2 #15 Go to college Get a Job Pay tuition -$100 Income 8x$10 Buy books -$100 Total -$200 Total +$80 Opportunity cost: Total cost:

13 Week 1, Class 2 #15 Go to college Get a Job Pay tuition -$100 Income 8x$10 Buy books -$100 Total -$200 Total +$80 Opportunity cost: -$80 Total cost: -$280 What is missing? Why go to college?

14 Week 1, Class 2 #15 Go to college Get a Job Pay tuition -$100 Income 8x$10 Buy books -$100 Get a better job +$300 Total $100 Total +$80 Benefit-cost: $300-$100-$100-$80=$20

15 Week 2 topics Principle of Increasing Cost Division of Labor Specialization Demand/Supply Curves Equilibrium Anything particularly troubling?

16 Week 2 topics Demand/Supply Curves Equilibrium Economics 101

17 Pizza example Price Demand Supply

18 George s Demand Curve Price Quantity

19 Price George s Demand Curve Quantity

20 George and Maria s Demand Curves Price Quantity

21 Aggregate Market Supply & Demand Price Supply p* Demand q* Quantity

=1/2(5*5)=12.")

22 Price p Consumer Surplus ½(B*H)=1/2(5*5)=12.5 Demand Quantity

=10 0 1 2 3 4 5 6 7 8 9 10 Quantity")

23 Consumer Surplus Price ( )= Quantity

24 Week 3 topics Price floors/ceilings Consumer Choice Law of Demand Utility Budget Set Optimal Purchase rule Marginal Utility Indifference Curves Consumer surplus Economics 101

25 Consumer choice example from class George has $50 He can only spend his money on two things pizza ($5) and coffee ($2) He can afford many different combinations but they give him different utility

26 George pizza/coffee table Economics 101 Pizza Total utility MU MU per $ Coffee Total utility MU MU per $

27 Budget Set: all of the possible combinations that a consumer can afford Economics 101

28 George pizza/coffee example Economics 101 P C

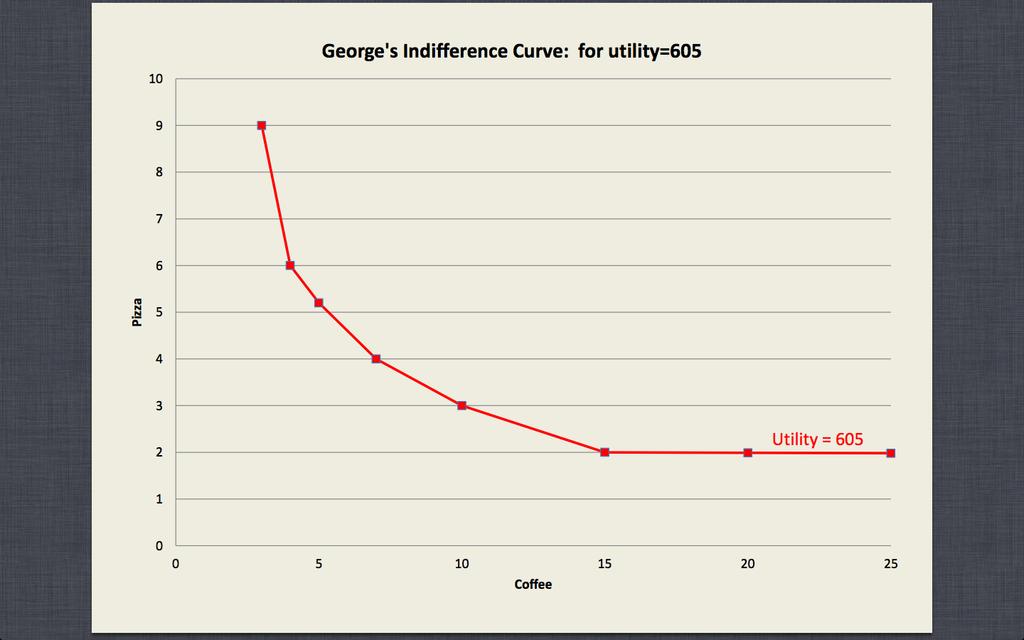

29 George pizza/coffee example Economics 101 P C

30 George s Budget Set Pizza Coffee

31 George s Budget Set Pizza Coffee

32 Utility: A measure of satisfaction associated with consuming a good or service. Economics 101

33 Marginal utility: Marginal utility is the additional utility associated with consuming an additional unit of a good or service Economics 101

34 Marginal utility per dollar spent Marginal utility price per unit Economics 101

35 Book vs. class on marginal utility Book: monetary utility Class: utility Book: marginal monetary utility Class: marginal utility per dollar spent Book: Forcing a one to one ratio between a unit of utility and price Class: A more general form of this specific assumption the book makes

36 Calculating total combined utility Pizza Coffee Total combined utility

37 Pizza Coffee Total combined utility Economics 101 Calculating total combined utility

38 George s Budget Set Pizza (445) (695) 7 6 (775) 5 4 (730) (605) (460) Coffee

39 Indifference curves it connects all combinations of the commodities that are equally desirable to the consumer. Another name: isoutility = same utility Why indifferent? Because you get the same utility.

40

41 Indifference curve for 605 Utility Pizza Utility Coffee Utility Total < > < < < > < < Economics 101

42 Optimal Purchase Rule The consumer chooses the one combination of goods and services that gives the maximum utility from among the set of all affordable combinations Economics 101

43

44 Optimal Purchase Rule One good: Book: Marginal Monetary Utility(MMU)=price Two goods: Class: Marginal Utility 1 /$spent=marginal Uitility 2 /$spent

45 Optimal Purchase Rule As long as the ratio (marginal utility per dollar spent) for good A is larger than for good B, you should expand consumption of good A and reduce consumption of good B. Start with 4 Pizza and 15 Coffee. What are the marginal-utility ratios? What do we do? Where do we stop?

46 Optimal Purchase Rule (for X.5 values of coffee just split the difference) Pizza MU/$ Coffee MU/$

47 Optimal Purchase Rule Pizza MU/$ Coffee MU/$

48 Optimal purchase rule & the Demand Curve Price Pizzas

49 Optimal purchase rule & the Demand Curve What if the price of pizza changes? George again solves his optimal purchase rule, and we get a new point on the demand curve. Demand curves come from optimal choices!

50 For next week Continue to send me any examples you find in the news Complete Aplia assignment for week Do the Preparing the Equilibrium Price and Quantity Experiment on Aplia.

1. T F The resources that are available to meet society s needs are scarce.

1. T F The resources that are available to meet society s needs are scarce. 2. T F The marginal rate of substitution is the rate of exchange of pairs of consumption goods or services to increase utility

1. T F The resources that are available to meet society s needs are scarce. 2. T F The marginal rate of substitution is the rate of exchange of pairs of consumption goods or services to increase utility

Robert Ackerman Office Hours: 2:00-3:00PM T/Th Office: PA202 (Phillips Hall Annex) Economics 101

Economics 101") Robert Ackerman rkackerm@live.unc.edu Office Hours: 2:00-3:00PM T/Th Office: PA202 (Phillips Hall Annex) Economics 101 Today Questions/concerns Administrative Wrap up Consumer Choice Begin The Producer

Robert Ackerman rkackerm@live.unc.edu Office Hours: 2:00-3:00PM T/Th Office: PA202 (Phillips Hall Annex) Economics 101 Today Questions/concerns Administrative Wrap up Consumer Choice Begin The Producer

Problem Set 1 Suggested Answers

Problem Set 1 Suggested Answers Problem 1. Think what is the cost of one can of Coca-cola. First try to figure out what is the accounting cost, i.e. the monetary cost. Next think what would be a total

Problem Set 1 Suggested Answers Problem 1. Think what is the cost of one can of Coca-cola. First try to figure out what is the accounting cost, i.e. the monetary cost. Next think what would be a total

Introduction to Agricultural Economics Agricultural Economics 105 Spring 2017 First Hour Exam Version 1

1 Name Introduction to Agricultural Economics Agricultural Economics 105 Spring 2017 First Hour Exam Version 1 There is only ONE best, correct answer per question. Place your answer on the attached sheet.

1 Name Introduction to Agricultural Economics Agricultural Economics 105 Spring 2017 First Hour Exam Version 1 There is only ONE best, correct answer per question. Place your answer on the attached sheet.

The Foundations of Microeconomics

The Foundations of Microeconomics D I A N N A D A S I L V A - G L A S G O W D E P A R T M E N T O F E C O N O M I C S U N I V E R S I T Y O F G U Y A N A 1 4 S E P T E M B E R, 2 0 1 7 Wk 3 Lectures I

The Foundations of Microeconomics D I A N N A D A S I L V A - G L A S G O W D E P A R T M E N T O F E C O N O M I C S U N I V E R S I T Y O F G U Y A N A 1 4 S E P T E M B E R, 2 0 1 7 Wk 3 Lectures I

TEN PRINCIPLES OF ECONOMICS. The word Economy... An individual economic agent faces many decisions: Intro Macroeconomic Theory Professor Minseong Kim

TEN PRINCIPLES OF ECONOMICS Chapter 1 The word Economy... Comes from a Greek word for one who manages a household. An individual economic agent faces many decisions: Should I go to college or should I

TEN PRINCIPLES OF ECONOMICS Chapter 1 The word Economy... Comes from a Greek word for one who manages a household. An individual economic agent faces many decisions: Should I go to college or should I

ECON Midterm #2 Practice Problems

ECON 1101 - Midterm #2 Practice Problems Question #1 Suppose that there is a small country known as Econland. Now lets open up Econland to the world economy. Suppose the world price of widgets is $2. Since

ECON 1101 - Midterm #2 Practice Problems Question #1 Suppose that there is a small country known as Econland. Now lets open up Econland to the world economy. Suppose the world price of widgets is $2. Since

Exercise questions. ECON 102. Answer all questions. Multiple Choice Questions. Choose the best answer.

Exercise questions. ECON 102 Answer all questions. Multiple Choice Questions. Choose the best answer. 1.On Saturday morning, you rank your choices for activities in the following order: go to the library,

Exercise questions. ECON 102 Answer all questions. Multiple Choice Questions. Choose the best answer. 1.On Saturday morning, you rank your choices for activities in the following order: go to the library,

Econ Alive Study Guide

Econ Alive Study Guide Directions: After you put your Final Portfolio in order, go through it and using this Study Guide as a map, answer these questions to the best of your ability. If you find that you

Econ Alive Study Guide Directions: After you put your Final Portfolio in order, go through it and using this Study Guide as a map, answer these questions to the best of your ability. If you find that you

Chapter 1: The Ten Lessons in Economics

Textbook Notes Page 1 Chapter 1: The Ten Lessons in Economics Saturday, 25 May 2013 1:09 PM Economics: The study of how society manages its scarce resources Individual Decision-Making Lesson 1: People

Textbook Notes Page 1 Chapter 1: The Ten Lessons in Economics Saturday, 25 May 2013 1:09 PM Economics: The study of how society manages its scarce resources Individual Decision-Making Lesson 1: People

Unit One, Day One (pages 6-20, 28) ECONOMICS: The study of how limited productive resources are efficiently allocated in a world of unlimited wants.

ECONOMICS: The study of how limited productive resources are efficiently allocated in a world of unlimited wants.") Unit One, Day One (pages 6-20, 28) ECONOMICS: The study of how limited productive resources are efficiently allocated in a world of unlimited wants. SCARCITY: WANTS EXCEED RESOURCES We want more than we

Unit One, Day One (pages 6-20, 28) ECONOMICS: The study of how limited productive resources are efficiently allocated in a world of unlimited wants. SCARCITY: WANTS EXCEED RESOURCES We want more than we

OCR Economics A-level

OCR Economics A-level Microeconomics Topic 1: Scarcity and Choice 1.4 Opportunity cost Notes The scarcity of resources gives rise to opportunity cost. The opportunity cost of a choice is the value of the

OCR Economics A-level Microeconomics Topic 1: Scarcity and Choice 1.4 Opportunity cost Notes The scarcity of resources gives rise to opportunity cost. The opportunity cost of a choice is the value of the

07. Engel s Law of family expenditure and significance. - Consumer's surplus estimation and applications.

07. Engel s Law of family expenditure and significance. - Consumer's surplus estimation and applications. Engel s Law on Family Expenditure Every family has to spend money on necessaries of life, education,

07. Engel s Law of family expenditure and significance. - Consumer's surplus estimation and applications. Engel s Law on Family Expenditure Every family has to spend money on necessaries of life, education,

Opportunity Cost. First quiz on Monday. Your First Job Ten Principles Scarcity Opportunity Cost. Fundamental Economic Concepts and Reasoning

Opportunity Cost First quiz on Monday. Your First Job Ten Principles Scarcity Opportunity Cost Fundamental Economic Concepts and Reasoning But first, a review of scarcity https://www.youtube.com/watch?v=np-dzsdzymk&li

Opportunity Cost First quiz on Monday. Your First Job Ten Principles Scarcity Opportunity Cost Fundamental Economic Concepts and Reasoning But first, a review of scarcity https://www.youtube.com/watch?v=np-dzsdzymk&li

Principles of Macroeconomics, 11e - TB1 (Case/Fair/Oster) Chapter 2 The Economic Problem: Scarcity and Choice

Chapter 2 The Economic Problem: Scarcity and Choice") Principles of Macroeconomics, 11e - TB1 (Case/Fair/Oster) Chapter 2 The Economic Problem: Scarcity and Choice 2.1 Scarcity, Choice, and Opportunity Cost 1) The process by which resources are transformed

Principles of Macroeconomics, 11e - TB1 (Case/Fair/Oster) Chapter 2 The Economic Problem: Scarcity and Choice 2.1 Scarcity, Choice, and Opportunity Cost 1) The process by which resources are transformed

Chapter. The Economic Problem CHAPTER IN PERSPECTIVE

The Economic Problem Chapter CHAPTER IN PERSPECTIVE Chapter studies the production possibilities frontier, PPF. The PPF shows how the opportunity cost of a good or service increases as more of the good

The Economic Problem Chapter CHAPTER IN PERSPECTIVE Chapter studies the production possibilities frontier, PPF. The PPF shows how the opportunity cost of a good or service increases as more of the good

ECON MACROECONOMIC PRINCIPLES Instructor: Dr. Juergen Jung Towson University. J.Jung Chapter Introduction Towson University 1 / 69

ECON 202 - MACROECONOMIC PRINCIPLES Instructor: Dr. Juergen Jung Towson University J.Jung Chapter 2-4 - Introduction Towson University 1 / 69 Disclaimer These lecture notes are customized for the Macroeconomics

ECON 202 - MACROECONOMIC PRINCIPLES Instructor: Dr. Juergen Jung Towson University J.Jung Chapter 2-4 - Introduction Towson University 1 / 69 Disclaimer These lecture notes are customized for the Macroeconomics

Short-Run Versus Long-Run Elasticity (pp )

") Short-Run Versus Long-Run Elasticity (pp. 38-46) Price elasticity varies with the amount of time consumers have to respond to a price Short-run demand and supply curves often look very different from their

Short-Run Versus Long-Run Elasticity (pp. 38-46) Price elasticity varies with the amount of time consumers have to respond to a price Short-run demand and supply curves often look very different from their

AP Macroeconomics. You can use whichever format you want. Web view is recommended -- the responsive design works seamlessly on any device.

AP Macroeconomics Instructor Mrs. Crisler Room 428 Office Hours 2:42-3:15 M,T,W,TH 2:00-3:15 F E-mail jcrisler@satsumaschools.com Phone 380-8190 Twitter Joy Crisler @ shsgovteach Economics : Macroeconomics

AP Macroeconomics Instructor Mrs. Crisler Room 428 Office Hours 2:42-3:15 M,T,W,TH 2:00-3:15 F E-mail jcrisler@satsumaschools.com Phone 380-8190 Twitter Joy Crisler @ shsgovteach Economics : Macroeconomics

1. Demand: willingness to buy a good or service and the ability to pay for it; how much of an item an individual is willing to purchase at each price

1. Demand: willingness to buy a good or service and the ability to pay for it; how much of an item an individual is willing to purchase at each price 2. The two things needed for demand to exist are: willingness

1. Demand: willingness to buy a good or service and the ability to pay for it; how much of an item an individual is willing to purchase at each price 2. The two things needed for demand to exist are: willingness

Unit 4: Consumer choice

Unit 4: Consumer choice In accordance with the APT programme the objective of the lecture is to help You to: gain an understanding of the basic postulates underlying consumer choice: utility, the law of

Unit 4: Consumer choice In accordance with the APT programme the objective of the lecture is to help You to: gain an understanding of the basic postulates underlying consumer choice: utility, the law of

Ecn Intermediate Microeconomic Theory University of California - Davis December 10, 2009 Instructor: John Parman. Final Exam

Ecn 100 - Intermediate Microeconomic Theory University of California - Davis December 10, 2009 Instructor: John Parman Final Exam You have until 12:30pm to complete this exam. Be certain to put your name,

Ecn 100 - Intermediate Microeconomic Theory University of California - Davis December 10, 2009 Instructor: John Parman Final Exam You have until 12:30pm to complete this exam. Be certain to put your name,

Recitation #3 Week from 01/26/09 to 02/01/09

EconS 101, Section 1 Professor Munoz Recitation #3 Week from 01/6/09 to 0/01/09 1. For each of the following situations in the table below, fill in the missing information: first, determine whether this

EconS 101, Section 1 Professor Munoz Recitation #3 Week from 01/6/09 to 0/01/09 1. For each of the following situations in the table below, fill in the missing information: first, determine whether this

ECON 1010 Principles of Macroeconomics. Midterm Exam #1. Professor: David Aadland. Spring Semester February 14, 2017.

ECON 1010 Principles of Macroeconomics Midterm Exam #1 Professor: David Aadland Spring Semester 2017 February 14, 2017 Your Name Section 1: Multiple Choice and T/F (60 pts). Circle the correct answer;

ECON 1010 Principles of Macroeconomics Midterm Exam #1 Professor: David Aadland Spring Semester 2017 February 14, 2017 Your Name Section 1: Multiple Choice and T/F (60 pts). Circle the correct answer;

AP Microeconomics Chapter 7 Outline

I. Learning Objectives In this chapter students should learn: A. How to define and explain the relationship between total utility, marginal utility, and the law of diminishing marginal utility. B. How

I. Learning Objectives In this chapter students should learn: A. How to define and explain the relationship between total utility, marginal utility, and the law of diminishing marginal utility. B. How

Exam 1. Pizzas. (per day) Figure 1

Figure 1") ECONOMICS 10-008 Dr. John Stewart Sept. 30, 2003 Exam 1 Instructions: Mark the letter for your chosen answer for each question on the computer readable answer sheet using a No.2 pencil. Note a)=1, b)=2

ECONOMICS 10-008 Dr. John Stewart Sept. 30, 2003 Exam 1 Instructions: Mark the letter for your chosen answer for each question on the computer readable answer sheet using a No.2 pencil. Note a)=1, b)=2

The Economic Problem: Scarcity and Choice

Chapter 2 The Economic Problem: Prepared by: Fernando & Yvonn Quijano 2007 Prentice Hall Business Publishing Principles of Economics 8e by Case and Fair The Economic Problem: 2 Chapter Outline Scarcity,

Chapter 2 The Economic Problem: Prepared by: Fernando & Yvonn Quijano 2007 Prentice Hall Business Publishing Principles of Economics 8e by Case and Fair The Economic Problem: 2 Chapter Outline Scarcity,

APEC 1101, Fall 2015 Tade Okediji

APEC 1101, Fall 2015 Tade Okediji Yanghao Wang December 9, 2015 Contents I Lecture Note 1 1 September 14 th 1 1.1 What is Economics?................................ 1 1.2 Guide to Economic Reasoning............................

APEC 1101, Fall 2015 Tade Okediji Yanghao Wang December 9, 2015 Contents I Lecture Note 1 1 September 14 th 1 1.1 What is Economics?................................ 1 1.2 Guide to Economic Reasoning............................

ECO232 Chapter 25 Homework. Name: Date: Use the following to answer question 1: Figure: Coffee and Comic Books

ECO232 Chapter 25 Homework Name: Date: Use the following to answer question 1: Figure: Coffee and Comic Books 1. (Figure: Coffee and Comic Books) Refer to the figure. A consumer has $5 to spend on comic

ECO232 Chapter 25 Homework Name: Date: Use the following to answer question 1: Figure: Coffee and Comic Books 1. (Figure: Coffee and Comic Books) Refer to the figure. A consumer has $5 to spend on comic

Unit 5: The Resource Market. (The Factor Market or Input Market)

") Unit 5: The Resource Market (The Factor Market or Input Market) 1 2 The Circular Flow Model The Product Market- The place where goods and services produced by businesses are sold to households. The Resource

Unit 5: The Resource Market (The Factor Market or Input Market) 1 2 The Circular Flow Model The Product Market- The place where goods and services produced by businesses are sold to households. The Resource

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

HW 2 - Micro - Machiorlatti MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) What is measured by the price elasticity of supply? 1) A) The price

HW 2 - Micro - Machiorlatti MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) What is measured by the price elasticity of supply? 1) A) The price

People who are actively seeking work and can start work immediately, but can t find a job at the current wage rate.

1 QUESTION ONE: THE AGGREGATE SUPPLY AND DEMAND MODEL (a) Define the term involuntary unemployment. People who are actively seeking work and can start work immediately, but can t find a job at the current

1 QUESTION ONE: THE AGGREGATE SUPPLY AND DEMAND MODEL (a) Define the term involuntary unemployment. People who are actively seeking work and can start work immediately, but can t find a job at the current

New House UNDERSTANDING ECONOMICS. For NCEA Level THREE INTERNAL MICRO-ECONOMIC CONCEPTS. Skills and Activities for the Key Competencies.

New House UNDERSTANDING ECONOMICS For NCEA Level THREE INTERNAL MICRO-ECONOMIC CONCEPTS Skills and Activities for the Key Competencies Dan Rennie Understanding Economics for NCEA Level Three: Micro-economic

New House UNDERSTANDING ECONOMICS For NCEA Level THREE INTERNAL MICRO-ECONOMIC CONCEPTS Skills and Activities for the Key Competencies Dan Rennie Understanding Economics for NCEA Level Three: Micro-economic

Introduction. Consumer Choice 20/09/2017

Consumer Choice Introduction Managerial Problem Paying employees to relocate: when Google wants to transfer an employee from its Seattle office to its London branch, it has to decide how much compensation

Consumer Choice Introduction Managerial Problem Paying employees to relocate: when Google wants to transfer an employee from its Seattle office to its London branch, it has to decide how much compensation

L2 Efficiency, Opportunity Cost, PPF

L2 Efficiency, Opportunity Cost, PPF Pareto Efficiency: A state in which it is impossible to make at least one individual better off without hurting the others. The action that makes at least one individual

L2 Efficiency, Opportunity Cost, PPF Pareto Efficiency: A state in which it is impossible to make at least one individual better off without hurting the others. The action that makes at least one individual

Making choices in a world of scarcity means we must pass up some goods and services. Every decision we make is a trade-off:

Lecture Notes Chapter 1 - The Art and Science of Economic Analysis Introduction Economics is about choices. Definition: Scarcity: A resource is scarce when it is not freely available - when its price exceeds

Lecture Notes Chapter 1 - The Art and Science of Economic Analysis Introduction Economics is about choices. Definition: Scarcity: A resource is scarce when it is not freely available - when its price exceeds

Chapter 2 Production Possibilities, Opportunity Cost,

Chapter 2 Production Possibilities, Opportunity Cost, and Economic Growth CHAPTER IN A NUTSHELL In this chapter, you continue your quest to learn the economic way of thinking. The chapter begins with the

Chapter 2 Production Possibilities, Opportunity Cost, and Economic Growth CHAPTER IN A NUTSHELL In this chapter, you continue your quest to learn the economic way of thinking. The chapter begins with the

Macroeconomics, 4e (Hubbard/O'Brien) Chapter 2 Trade-offs, Comparative Advantage, and the Market System

Chapter 2 Trade-offs, Comparative Advantage, and the Market System") Macroeconomics, 4e (Hubbard/O'Brien) Chapter 2 Trade-offs, Comparative Advantage, and the Market System 2.1 Production Possibilities Frontiers and Opportunity Costs 1) Scarcity A) stems from the incompatibility

Macroeconomics, 4e (Hubbard/O'Brien) Chapter 2 Trade-offs, Comparative Advantage, and the Market System 2.1 Production Possibilities Frontiers and Opportunity Costs 1) Scarcity A) stems from the incompatibility

SMT Quick-Tips: selecting a custom or used machine. Robert Voigt, DDM Novastar

SMT Quick-Tips: selecting a custom or used machine Robert Voigt, DDM Novastar When to Consider a Custom or Used Machine Let s say you have an unusual product configuration, a unique space requirement,

SMT Quick-Tips: selecting a custom or used machine Robert Voigt, DDM Novastar When to Consider a Custom or Used Machine Let s say you have an unusual product configuration, a unique space requirement,

UNIT 4 PRACTICE EXAM

UNIT 4 PRACTICE EXAM 1. The prices paid for resources affect A. the money incomes of households in the economy B. the allocation of resources among different firms and industries in the economy C. the

UNIT 4 PRACTICE EXAM 1. The prices paid for resources affect A. the money incomes of households in the economy B. the allocation of resources among different firms and industries in the economy C. the

ECON 251. Exam 1 Pink. Fall 2013

ECON 251 1. By definition, opportunity cost is a. The value of the best alternative b. The sum of the value of all available alternatives c. The amount of money it takes to buy an item d. Always greater

ECON 251 1. By definition, opportunity cost is a. The value of the best alternative b. The sum of the value of all available alternatives c. The amount of money it takes to buy an item d. Always greater

Exam 1. Number of Pretzels (per 8 hour day) Figure 1

Figure 1") ECONOMICS 10-008 Dr. John Stewart Feb. 11, 1999 Exam 1 Instructions: Mark the letter for your chosen answer for each question on the computer readable answer sheet. On the answer sheet make sure that you

ECONOMICS 10-008 Dr. John Stewart Feb. 11, 1999 Exam 1 Instructions: Mark the letter for your chosen answer for each question on the computer readable answer sheet. On the answer sheet make sure that you

Production Possibilities and Opportunity Cost

Production Possibilities and Opportunity Cost 0 The production possibilities frontier (PPF) is the boundary between those combinations of goods and services that can be produced and those that cannot.

Production Possibilities and Opportunity Cost 0 The production possibilities frontier (PPF) is the boundary between those combinations of goods and services that can be produced and those that cannot.

7.1 The concept of consumer s surplus

Microeconomics I. Antonio Zabalza. University of Valencia 1 Lesson 7: Consumer s surplus 7.1 The concept of consumer s surplus The demand curve can also be interpreted as giving information on the maimum

Microeconomics I. Antonio Zabalza. University of Valencia 1 Lesson 7: Consumer s surplus 7.1 The concept of consumer s surplus The demand curve can also be interpreted as giving information on the maimum

After studying this chapter you will be able to

3 Demand and Supply After studying this chapter you will be able to Describe a competitive market and think about a price as an opportunity cost Explain the influences on demand Explain the influences

3 Demand and Supply After studying this chapter you will be able to Describe a competitive market and think about a price as an opportunity cost Explain the influences on demand Explain the influences

Part II: Economic Growth. Part I: LRAS

LRAS & LONG-RUN EQUILIBRIUM - 1 - Part I: LRAS 1) The quantity of real GDP supplied at full employment is called A) hypothetical GDP. B) short-run equilibrium GDP. C) potential GDP. D) all of the above.

LRAS & LONG-RUN EQUILIBRIUM - 1 - Part I: LRAS 1) The quantity of real GDP supplied at full employment is called A) hypothetical GDP. B) short-run equilibrium GDP. C) potential GDP. D) all of the above.

Practice Exam 3: S201 Walker Fall with answers to MC

Practice Exam 3: S201 Walker Fall 2007 - with answers to MC Print Your Name: I. Multiple Choice (3 points each) 1. If marginal utility is falling then A. total utility must be falling. B. marginal utility

Practice Exam 3: S201 Walker Fall 2007 - with answers to MC Print Your Name: I. Multiple Choice (3 points each) 1. If marginal utility is falling then A. total utility must be falling. B. marginal utility

, Z.~ ( 2) 11= ~1ft ;f: -m; :t Jjo':JJ!

11= ~1ft ;f: -m; :t Jjo':JJ!") ~PJT~JJU : ~~iej\~iijfjefijtetl, Z.~ ~~f4 : ~!~~ ilfilii:bm: 0224 ~*: 2 ~.t. ;t : ( 1) 1!-ft{:JJ! ~J(;JiiJUf 11o ~ ( 2) 11= ~1ft ;f: -m; :t Jjo':JJ! (20 11--)I. M~.rJ. r ~ tiij (!)Law of comparative advantage

~PJT~JJU : ~~iej\~iijfjefijtetl, Z.~ ~~f4 : ~!~~ ilfilii:bm: 0224 ~*: 2 ~.t. ;t : ( 1) 1!-ft{:JJ! ~J(;JiiJUf 11o ~ ( 2) 11= ~1ft ;f: -m; :t Jjo':JJ! (20 11--)I. M~.rJ. r ~ tiij (!)Law of comparative advantage

Chapter 21. Consumer Choice

Consumer Choice Utility is most closely defined as a) extra. b) marginal. c) usefulness. d) satisfaction. e) opportunity cost. Copyright Houghton Mifflin Company. All rights reserved. 21 2 Utility is most

Consumer Choice Utility is most closely defined as a) extra. b) marginal. c) usefulness. d) satisfaction. e) opportunity cost. Copyright Houghton Mifflin Company. All rights reserved. 21 2 Utility is most

Benefits, Costs, and Maximization

11 Benefits, Costs, and Maximization CHAPTER OBJECTIVES To explain the basic process of balancing costs and benefits in economic decision making. To introduce marginal analysis, and to define marginal

11 Benefits, Costs, and Maximization CHAPTER OBJECTIVES To explain the basic process of balancing costs and benefits in economic decision making. To introduce marginal analysis, and to define marginal

Got stuff? I. The Economic Problem. Chapter 1: The Economic Way of Thinking

Chapter 1: The Economic Way of Thinking The Economic Problem Production Possibilities Economic Analysis Got stuff? Who made it? How was it made? How did you get it? I. The Economic Problem the basic economic

Chapter 1: The Economic Way of Thinking The Economic Problem Production Possibilities Economic Analysis Got stuff? Who made it? How was it made? How did you get it? I. The Economic Problem the basic economic

PCP (2017): Environmental Economic Theory, No. 1 Benefits and Costs, Supply and Demand

: Environmental Economic Theory, No. 1 Benefits and Costs, Supply and Demand") PCP (2017): Environmental Economic Theory, No. 1 Benefits and Costs, Supply and Demand Instructor: Eiji HOSODA Textbook: Barry.C. Field & Martha K. Fields (2009) Environmental Economics - an introduction,

PCP (2017): Environmental Economic Theory, No. 1 Benefits and Costs, Supply and Demand Instructor: Eiji HOSODA Textbook: Barry.C. Field & Martha K. Fields (2009) Environmental Economics - an introduction,

Chapter 5: A Closed-Economy One-Period Macroeconomic Model

Chapter 5: A Closed-Economy One-Period Macroeconomic Model Introduce the government. Construct closed-economy one-period macroeconomic model, which has: (i) representative consumer; (ii) representative

Chapter 5: A Closed-Economy One-Period Macroeconomic Model Introduce the government. Construct closed-economy one-period macroeconomic model, which has: (i) representative consumer; (ii) representative

Chapter 1: What is Economics?

SCHS SOCIAL STUDIES What you need to know UNIT ONE 1. Explain why scarcity and choice are basic problems of economics 2. Explain the role of entrepreneurs 3. Explain why economists say all resources are

SCHS SOCIAL STUDIES What you need to know UNIT ONE 1. Explain why scarcity and choice are basic problems of economics 2. Explain the role of entrepreneurs 3. Explain why economists say all resources are

2 THE ECONOMIC PROBLEM

2 THE ECONOMIC PROBLEM Why does food cost much more today than it did a few years ago? One reason is that we now use part of our corn crop to produce ethanol, a clean biofuel substitute for gasoline.

2 THE ECONOMIC PROBLEM Why does food cost much more today than it did a few years ago? One reason is that we now use part of our corn crop to produce ethanol, a clean biofuel substitute for gasoline.

Name: Eddie Jackson. Course & Section: BU Mid-term

Name: Eddie Jackson Course & Section: BU204 02 Mid-term Date: July 1st, 2012 Questions: 1. Atlantis is a small, isolated island in the South Atlantic. The inhabitants grow potatoes and catch fresh fish.

Name: Eddie Jackson Course & Section: BU204 02 Mid-term Date: July 1st, 2012 Questions: 1. Atlantis is a small, isolated island in the South Atlantic. The inhabitants grow potatoes and catch fresh fish.

Consumer Choice and Behavioral Economics. Can Jay-Z Get You to Drink Cherry Coke? Learning Objectives. Chapter 9. Utility and Consumer Decision Making

Chapter 9 Consumer Choice and Behavioral Economics Prepared by: Fernando & Yvonn Quijano 008 Prentice Hall Business Publishing Economics R. Glenn Hubbard, Anthony Patrick O Brien, e. Can Jay-Z Get You

Chapter 9 Consumer Choice and Behavioral Economics Prepared by: Fernando & Yvonn Quijano 008 Prentice Hall Business Publishing Economics R. Glenn Hubbard, Anthony Patrick O Brien, e. Can Jay-Z Get You

Chapter 1: What is Economics? Section 3

Chapter 1: What is Economics? Section 3 Objectives 1. Interpret a production possibilities curve. 2. Explain how production possibilities curves show efficiency, growth, and cost. 3. Explain why a country

Chapter 1: What is Economics? Section 3 Objectives 1. Interpret a production possibilities curve. 2. Explain how production possibilities curves show efficiency, growth, and cost. 3. Explain why a country

Problem Set 3. I. Problem 1. Explain each of the following statements using supply-and-demand diagrams.

Problem Set 3 I. Problem 1. Explain each of the following statements using supply-and-demand diagrams. a) When the weather turns warm in New England every summer, the price of hotel rooms in Caribbean

Problem Set 3 I. Problem 1. Explain each of the following statements using supply-and-demand diagrams. a) When the weather turns warm in New England every summer, the price of hotel rooms in Caribbean

Thinking Like an Economist. Thinking Like an Economist THE ECONOMIST AS A SCIENTIST. Chapter 2. Thinking Like an Economist

Chapter 2 Thinking Like an Economist Thinking Like an Economist Every field of study has its own terminology Mathematics integrals axioms vector spaces Psychology ego id cognitive dissonance Law promissory

Chapter 2 Thinking Like an Economist Thinking Like an Economist Every field of study has its own terminology Mathematics integrals axioms vector spaces Psychology ego id cognitive dissonance Law promissory

Demand - the desire, ability, and willingness to buy a product.

Demand - the desire, ability, and willingness to buy a product. 1. You must have the desire for the product 2. You must be able to make a purchase 3. You must be willing to make a purchase 4. Purchases

Demand - the desire, ability, and willingness to buy a product. 1. You must have the desire for the product 2. You must be able to make a purchase 3. You must be willing to make a purchase 4. Purchases

Chapter 11. Microeconomics. Technology, Production, and Costs. Modified by: Yun Wang Florida International University Spring 2018

Microeconomics Modified by: Yun Wang Florida International University Spring 2018 1 Chapter 11 Technology, Production, and Costs Chapter Outline 11.1 Technology: An Economic Definition 11.2 The Short Run

Microeconomics Modified by: Yun Wang Florida International University Spring 2018 1 Chapter 11 Technology, Production, and Costs Chapter Outline 11.1 Technology: An Economic Definition 11.2 The Short Run

SOLUTION MANUAL FOR ECON MACROECONOMICS 4 4TH EDITION MCEACHERN

SOLUTION MANUAL FOR ECON MACROECONOMICS 4 4TH EDITION MCEACHERN Link download full: http://testbankcollection.com/download/econ-macroeconomics-4-4thedition-mceachern-solutions COMPLETE DOWNLOADABLE FILE

SOLUTION MANUAL FOR ECON MACROECONOMICS 4 4TH EDITION MCEACHERN Link download full: http://testbankcollection.com/download/econ-macroeconomics-4-4thedition-mceachern-solutions COMPLETE DOWNLOADABLE FILE

D. People would continue to consume the same amount of the good.

17. Because prices serve as incentives in a market economy, which of the following would be a likely result of a large increase in the price of a good? A. People would increase their consumption of the

17. Because prices serve as incentives in a market economy, which of the following would be a likely result of a large increase in the price of a good? A. People would increase their consumption of the

Microconomics. Chapter 2 Trade-offs, Comparative Advantage, and the Market System. 6 th edition

1 Microconomics 6 th edition Chapter 2 Trade-offs, Comparative Advantage, and the Market System Modified by Yulin Hou For Principles of Microeconomics Florida International University Fall 2017 Production

1 Microconomics 6 th edition Chapter 2 Trade-offs, Comparative Advantage, and the Market System Modified by Yulin Hou For Principles of Microeconomics Florida International University Fall 2017 Production

Wallingford Public Schools - HIGH SCHOOL COURSE OUTLINE

Wallingford Public Schools - HIGH SCHOOL COURSE OUTLINE Course Title: Advanced Placement Economics Course Number: 3552 Department: Social Studies Grade(s): 11-12 Level(s): Advanced Placement Credit: 1

Wallingford Public Schools - HIGH SCHOOL COURSE OUTLINE Course Title: Advanced Placement Economics Course Number: 3552 Department: Social Studies Grade(s): 11-12 Level(s): Advanced Placement Credit: 1

AGEC 105 Fall 2010 Test #1 Capps (70 questions)

") (70 questions) Please put the following pieces of information on your scantron: (a) Name (b) UIN # (c) Section #: 504 505 506 (d) Sign the ggie pledge on the back of your scantron. On my honor, as an ggie,

(70 questions) Please put the following pieces of information on your scantron: (a) Name (b) UIN # (c) Section #: 504 505 506 (d) Sign the ggie pledge on the back of your scantron. On my honor, as an ggie,

ECON 251 Practice Exam 2 Questions from Fall 2013 Exams

ECON 251 Practice Exam 2 Questions from Exams Gordon spends all his income on spatulas and mixing bowls. Spatulas cost $4 and mixing bowls cost $12. Gordon has $60 of income and considers both spatulas

ECON 251 Practice Exam 2 Questions from Exams Gordon spends all his income on spatulas and mixing bowls. Spatulas cost $4 and mixing bowls cost $12. Gordon has $60 of income and considers both spatulas

Price = The Interaction of Supply and Demand WEDNESDAY, FEBRUARY 17 THURSDAY, FEBRUARY 18

Price = The Interaction of Supply and Demand WEDNESDAY, FEBRUARY 17 THURSDAY, FEBRUARY 18 Chapter 4: Section 1 Understanding Demand What Is Demand? Markets are where people come together to buy and sell

Price = The Interaction of Supply and Demand WEDNESDAY, FEBRUARY 17 THURSDAY, FEBRUARY 18 Chapter 4: Section 1 Understanding Demand What Is Demand? Markets are where people come together to buy and sell

Microeconomics. More Tutorial at

Microeconomics 1. Suppose a firm in a perfectly competitive market produces and sells 8 units of output and has a marginal revenue of $8.00. What would be the firm s total revenue if it instead produced

Microeconomics 1. Suppose a firm in a perfectly competitive market produces and sells 8 units of output and has a marginal revenue of $8.00. What would be the firm s total revenue if it instead produced

Framingham State College Department of Economics and Business Principles of Microeconomics 1 st Midterm Practice Exam Fall 2006

Name Framingham State College Department of Economics and Business Principles of Microeconomics 1 st Midterm Practice Exam Fall 2006 This exam provides questions that are representative of those contained

Name Framingham State College Department of Economics and Business Principles of Microeconomics 1 st Midterm Practice Exam Fall 2006 This exam provides questions that are representative of those contained

ECON 1010 Principles of Macroeconomics Exam #1. Section A: Multiple Choice Questions. (30 points; 2 pts each)

") ECON 1010 Principles of Macroeconomics Exam #1 Section A: Multiple Choice Questions. (30 points; 2 pts each) #1. The figure Sam and DiMitri s Production Possibilities depicts production frontiers for Sam

ECON 1010 Principles of Macroeconomics Exam #1 Section A: Multiple Choice Questions. (30 points; 2 pts each) #1. The figure Sam and DiMitri s Production Possibilities depicts production frontiers for Sam

Production Possibilities, Opportunity Cost, and Economic Growth

Chapter 2 Production Possibilities, Opportunity Cost, and Economic Growth CHAPTER SUMMARY The What, How and For Whom are introduced as the fundamental economic questions that must be addressed by all societies.

Chapter 2 Production Possibilities, Opportunity Cost, and Economic Growth CHAPTER SUMMARY The What, How and For Whom are introduced as the fundamental economic questions that must be addressed by all societies.

Fundamentals of Markets

Fundamentals of Markets Daniel Kirschen University of Manchester 2006 Daniel Kirschen 1 Let us go to the market... Opportunity for buyers and sellers to: compare prices estimate demand estimate supply

Fundamentals of Markets Daniel Kirschen University of Manchester 2006 Daniel Kirschen 1 Let us go to the market... Opportunity for buyers and sellers to: compare prices estimate demand estimate supply

Perfectly Competitive Supply. Chapter 6. Learning Objectives

Perfectly Competitive Supply Chapter 6 McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Learning Objectives 1.Explain how opportunity cost is related to the supply

Perfectly Competitive Supply Chapter 6 McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Learning Objectives 1.Explain how opportunity cost is related to the supply

Walter Nicholson, Amherst College Christopher Snyder, Dartmouth College PowerPoint Slide Presentation Philip Heap, James Madison University

Intermediate Microeconomics and Its Application 11th edition by Walter Nicholson, Amherst College Christopher Snyder, Dartmouth College PowerPoint Slide Presentation Philip Heap, James Madison University

Intermediate Microeconomics and Its Application 11th edition by Walter Nicholson, Amherst College Christopher Snyder, Dartmouth College PowerPoint Slide Presentation Philip Heap, James Madison University

Scarcity and the Factors of Production. What is economics? How do economists define scarcity? What are the three factors of production?

Scarcity and the Factors of Production What is economics? How do economists define scarcity? What are the three factors of production? What Is Economics? Economics is the study of how people make choices

Scarcity and the Factors of Production What is economics? How do economists define scarcity? What are the three factors of production? What Is Economics? Economics is the study of how people make choices

ECON 251 Exam 2 Pink. Fall 2012

ECON 251 Exam 2 Pink Use the table below to answer the following four questions The table below shows Harry s total utility from consuming beer and wine. The price of beer is $2 per bottle. The price of

ECON 251 Exam 2 Pink Use the table below to answer the following four questions The table below shows Harry s total utility from consuming beer and wine. The price of beer is $2 per bottle. The price of

CLEP Microeconomics Practice Test

Practice Test Time 90 Minutes 80 Questions For each of the questions below, choose the best answer from the choices given. 1. In economics, the opportunity cost of an item or entity is (A) the out-of-pocket

Practice Test Time 90 Minutes 80 Questions For each of the questions below, choose the best answer from the choices given. 1. In economics, the opportunity cost of an item or entity is (A) the out-of-pocket

Interpreting Price Elasticity of Demand

INTRO Go to page: Go to chapter Bookmarks Printed Page 466 Interpreting Price 9 Behind the 48.2 The Price of Supply 48.3 An Menagerie Producer 49.1 Consumer and the 49.2 Producer and the 50.1 Consumer,

INTRO Go to page: Go to chapter Bookmarks Printed Page 466 Interpreting Price 9 Behind the 48.2 The Price of Supply 48.3 An Menagerie Producer 49.1 Consumer and the 49.2 Producer and the 50.1 Consumer,

Production Possibilities, Opportunity Cost, and Economic Growth

Chapter 2 Production Possibilities, Opportunity Cost, and Economic Growth CHAPTER SUMMARY The What, How and For Whom questions are introduced as the fundamental economic questions that must be addressed

Chapter 2 Production Possibilities, Opportunity Cost, and Economic Growth CHAPTER SUMMARY The What, How and For Whom questions are introduced as the fundamental economic questions that must be addressed

PRINCIPLES OF ECONOMICS. J. Mao

PRINCIPLES OF ECONOMICS J. Mao Principle #1: People Face Tradeoffs All decisions involve trade offs. To get one thing we like, we usually have to give up another thing we like. Xbox or Iphone 6 Playing

PRINCIPLES OF ECONOMICS J. Mao Principle #1: People Face Tradeoffs All decisions involve trade offs. To get one thing we like, we usually have to give up another thing we like. Xbox or Iphone 6 Playing

Marginal Analysis. Thinking on the Margin. This is what you do when you make a decision. You weigh your options, and make a choice.

1 Marginal Analysis 6 Thinking on the Margin This is what you do when you make a decision. You weigh your options, and make a choice. If I do this, then I can t do that is it worth it? 7 Marginal Analysis

1 Marginal Analysis 6 Thinking on the Margin This is what you do when you make a decision. You weigh your options, and make a choice. If I do this, then I can t do that is it worth it? 7 Marginal Analysis

JANUARY EXAMINATIONS 2005

No. of Pages: (A) 7 No. of Questions: 26 EC1000A ' JANUARY EXAMINATIONS 2005 Subject Title of Paper ECONOMICS EC1000 MICROECONOMICS Time Allowed Two Hours (2 Hours) Instructions to candidates This paper

No. of Pages: (A) 7 No. of Questions: 26 EC1000A ' JANUARY EXAMINATIONS 2005 Subject Title of Paper ECONOMICS EC1000 MICROECONOMICS Time Allowed Two Hours (2 Hours) Instructions to candidates This paper

PRINCIPLES OF ECONOMICS IN CONTEXT CONTENTS

PRINCIPLES OF ECONOMICS IN CONTEXT By Neva Goodwin, Jonathan M. Harris, Julie A. Nelson, Brian Roach, and Mariano Torras CONTENTS PART ONE The Context for Economic Analysis Chapter 0: Economics and Well-Being

PRINCIPLES OF ECONOMICS IN CONTEXT By Neva Goodwin, Jonathan M. Harris, Julie A. Nelson, Brian Roach, and Mariano Torras CONTENTS PART ONE The Context for Economic Analysis Chapter 0: Economics and Well-Being

Bremen School District 228 Social Studies Common Assessment 2: Midterm

Bremen School District 228 Social Studies Common Assessment 2: Midterm AP Microeconomics 55 Minutes 60 Questions Directions: Each of the questions or incomplete statements in this exam is followed by five

Bremen School District 228 Social Studies Common Assessment 2: Midterm AP Microeconomics 55 Minutes 60 Questions Directions: Each of the questions or incomplete statements in this exam is followed by five

MICRO-ECONOMIC THEORY I STUDY NOTES CHAPTER ONE

MICRO-ECONOMIC THEORY I STUDY NOTES CHAPTER ONE UNIT 1 BASIC CONCEPT OF CONSUMER BEHAVIOUR CHAPTER ONE CONTENTS Introduction Objectives Main Content Theory of Consumer Behaviour Consumer Preferences Decisiveness

MICRO-ECONOMIC THEORY I STUDY NOTES CHAPTER ONE UNIT 1 BASIC CONCEPT OF CONSUMER BEHAVIOUR CHAPTER ONE CONTENTS Introduction Objectives Main Content Theory of Consumer Behaviour Consumer Preferences Decisiveness

Chapter 2: Scarcity, Choice and Economic Systems

Chapter 2: Scarcity, Choice and Economic Systems Opportunity Cost How do we decide about the cost of a good/service? Money? Economist: Money is a part of its cost Opportunity Cost: most accurate and complete

Chapter 2: Scarcity, Choice and Economic Systems Opportunity Cost How do we decide about the cost of a good/service? Money? Economist: Money is a part of its cost Opportunity Cost: most accurate and complete

Key Stage 3: End of Term Test 3. Name: Teacher:

GCSE Mathematics 1MA0 Formulae: Foundation Tier You must not write on this formulae page. Anything you write on this formulae page will gain NO credit. Key Stage 3: End of Term Test 3 a Area of trapezium

GCSE Mathematics 1MA0 Formulae: Foundation Tier You must not write on this formulae page. Anything you write on this formulae page will gain NO credit. Key Stage 3: End of Term Test 3 a Area of trapezium

Unit 5: The Resource Market. (aka: The Factor Market or Input Market)

") Unit 5: The Resource Market (aka: The Factor Market or Input Market) 1 Perfect Competition Resource Markets Monopsony Perfectly Competitive Labor Market Characteristics: Many small firms are hiring workers

Unit 5: The Resource Market (aka: The Factor Market or Input Market) 1 Perfect Competition Resource Markets Monopsony Perfectly Competitive Labor Market Characteristics: Many small firms are hiring workers

Q.1 Distinguish between increase in demand and increase in quantity demanded of a commodity.

Q.1 Distinguish between increase in demand and increase in quantity demanded of a commodity. Q. 2 Given price of a good, how does a consumer decide as to how much of that good to buy? Q. 3 A consumer consumers

Q.1 Distinguish between increase in demand and increase in quantity demanded of a commodity. Q. 2 Given price of a good, how does a consumer decide as to how much of that good to buy? Q. 3 A consumer consumers

Chapter 2 Production possibilities and opportunity cost

Chapter 2 Production possibilities and opportunity cost MULTIPLE CHOICE The three fundamental economic questions 1. Why must every nation answer the three fundamental economic questions? A. Because of

Chapter 2 Production possibilities and opportunity cost MULTIPLE CHOICE The three fundamental economic questions 1. Why must every nation answer the three fundamental economic questions? A. Because of

Scarcity and the Factors of Production

Scarcity and the Factors of Production What is economics? How do economists define scarcity? What are the three factors of production? What Is Economics? Economics is the study of how people make choices

Scarcity and the Factors of Production What is economics? How do economists define scarcity? What are the three factors of production? What Is Economics? Economics is the study of how people make choices

Economics 110 Midterm #2 Practice Multiple Choice Qs Spring 2014

Midterm #2 Practice Multiple Choice Questions: Elasticity is a. a measure of how much buyers and sellers respond to changes in market conditions. b. the study of how the allocation of resources affects

Midterm #2 Practice Multiple Choice Questions: Elasticity is a. a measure of how much buyers and sellers respond to changes in market conditions. b. the study of how the allocation of resources affects

Thinking Like an Economist

The Economist as a Scientist Thinking Like an Economist Chapter 2 The economic way of thinking... Involves thinking analytically and objectively. Makes use of the scientific method. Copyright 2001 by Harcourt,

The Economist as a Scientist Thinking Like an Economist Chapter 2 The economic way of thinking... Involves thinking analytically and objectively. Makes use of the scientific method. Copyright 2001 by Harcourt,

PICK ONLY ONE BEST ANSWER FOR EACH BINARY CHOICE OR MULTIPLE CHOICE QUESTION.

Econ 101 Summer 2015 Answers to Second Mid-term Date: June 15, 2015 Student Name Version 1 READ THESE INSTRUCTIONS CAREFULLY. DO NOT BEGIN WORKING UNTIL THE PROCTOR TELLS YOU TO DO SO You have 75 minutes

Econ 101 Summer 2015 Answers to Second Mid-term Date: June 15, 2015 Student Name Version 1 READ THESE INSTRUCTIONS CAREFULLY. DO NOT BEGIN WORKING UNTIL THE PROCTOR TELLS YOU TO DO SO You have 75 minutes

Chapter 1 The Science of Macroeconomics

Chapter 1 The Science of Macroeconomics Modified by Yun Wang Eco 3203 Intermediate Macroeconomics Florida International University Summer 2017 2016 Worth Publishers, all rights reserved Learning Objectives

Chapter 1 The Science of Macroeconomics Modified by Yun Wang Eco 3203 Intermediate Macroeconomics Florida International University Summer 2017 2016 Worth Publishers, all rights reserved Learning Objectives

LECTURE 2: MODELS IN ECONOMICS. Today s Topics

LECTURE 2: MODELS IN ECONOMICS Today s Topics > LECTURE 2: MODELS IN ECONOMICS Today s Topics 1. Economists apply the scientific method. > LECTURE 2: MODELS IN ECONOMICS Today s Topics 1. Economists apply

LECTURE 2: MODELS IN ECONOMICS Today s Topics > LECTURE 2: MODELS IN ECONOMICS Today s Topics 1. Economists apply the scientific method. > LECTURE 2: MODELS IN ECONOMICS Today s Topics 1. Economists apply

Figure 4 1 Price Quantity Quantity Per Pair Demanded Supplied $ $ $ $ $10 2 8

Econ 101 Summer 2005 In class Assignment 2 Please select the correct answer from the ones given Figure 4 1 Price Quantity Quantity Per Pair Demanded Supplied $ 2 18 3 $ 4 14 4 $ 6 10 5 $ 8 6 6 $10 2 8

Econ 101 Summer 2005 In class Assignment 2 Please select the correct answer from the ones given Figure 4 1 Price Quantity Quantity Per Pair Demanded Supplied $ 2 18 3 $ 4 14 4 $ 6 10 5 $ 8 6 6 $10 2 8