NUMERICALS FROM UNIT-1 TO UNIT -8

|

|

|

- Hannah Lyons

- 6 years ago

- Views:

Transcription

1 UNIT-1 INTRODUCTION NUMERICALS FROM UNIT-1 TO UNIT A country produces two goods Its production possibilities are shows in the following table. Calculate MOC and draw PPC. Give reason. (AISSCE-2015) Possibilities Good-X(UNITS) Good-Y(UNITS) A B 95 1 C 85 2 D A chartered accountant is earning Re 1 lac per month from his own practice. He could earn Rs p.m. from a job in Reliance industries or Rs p. m. from a consultancy. What will be his opportunity cost? (Rs 75000) 3. Calculate MOC in the following example. Plot the PPC by taking cloth consumption on the X- axis.comment on t6he shape the curve. (22,25,28,30) (AISSCE-2001) Food Consumption Cloth Consumption UNIT-2 CONSUMER S BEHAVIOUR AND DEMAND 1. A commodity has Rs 5 as price per unit. His TU Schedule is given below. Determine equilibrium point. (Rs.5) Units of good TU A consumer consumes only two goods X and Y whose prices are Rs.5 and Rs. 4 respectively. If the consumer chooses a combination of the two goods with MU of X equal to 4 and that of Y equal to 5, is the consumer in equilibrium? Why or why not? What will a rational consumer do in this equal? Use utility analysis. (AISSCE-2015) 3. A consumer wants to consume two goods I and II. Price of two goods are Rs.8 and Rs 10. Consumer s income is Rs. 80. Write down the equation of budget line and determine units of

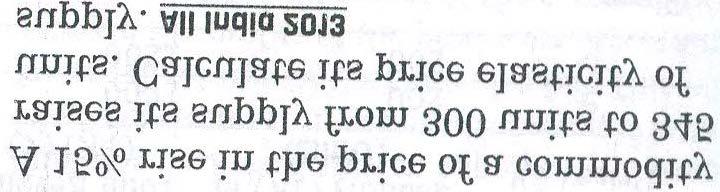

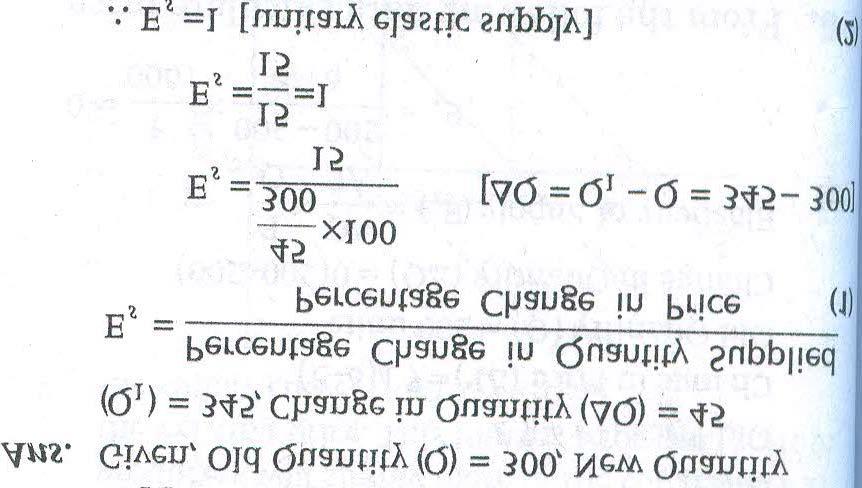

2 good I and II bought by him and the slope of the budget line. (X=10 Units, Y=8Units and slope=4/5) 4. Suppose a consumer wants to consume two goods, which are available only in integer units. The two goods are equally priced at Rs. 10 and consumer s income is Rs.40. (i)make all the possible bundles that are available to the consumer. (ii) Among the bundles that are available to the consumer, identify those which cost him exactly Rs Suppose there are three buyers A,B And C in a market for commodity X Demand functions for these buyers are as under: Dxa=30-0.5Px Dxb=20-o.4Px Dxc=10-0.2Px If prices of x commodity in rupees are 10,20,30, Draw the market demand function and estimate the market demand. (49, 38 and 27) 6. A consumer buys 27 units of a good at a price of Rs. 10 per unit. When the price falls to Rs. 9 per unit, the demand rises to 30 units. What can you say about price elasticity of demand of good through the expenditure approach? (ed=1) (AISSCE-2014) 7. A consumer spends Rs on a good priced at Rs. 8 per unit. When price rises by 25% consumer continues to spend Rs,1000 on the good. Calculate price elasticity of demand by percentage method. (ed=0.8) (AISSCE-2015) 8. What will be the effect of 10% rise in price of a good on its demand if price elasticity of demand is (a) 0 (b) -1 (c) -2 (AISSCE-2016) 9. Given Px=Rs2 and Py=Re 1, income=rs 12 Find how a consumer spends her income in order to maximize TU AND CAL CULATE tu RECEIVED BY THE CONSUMER. Show that equilibrium conditions for the consumer are satisfied (TU=93) Q MUx MUy A consumer spends Rs 40 on a good at a price of Re 1 per unit and Rs 60 at a price of Rs 2 per unit. What is the price elasticity of demand? What kind of good it is? What shape its demand curve will take? (Ed=0.25) (inelastic demand like food demand curve will be steeper) 11. Price elasticity of demand of a good is (-) 3. If the price rises from Rs 10 per unit to Rs 12 per unit. What is the % change in demand? (Ed=1) (AISSCE-2008) UNIT: 3 PRODUCER S BEHAVIOUR AND SUPPLY 1. The price elasticity of good X is half the price elasticity of supply of good Y. A 10% rise in the price of good Y results in a rise in its supply from 400 units to 520 units. Calculate the percentage change in quantity supplied of good X when its price falls from RS.10 to Rs.8 per unit. (30%) (AISSCE-2010) 2. Complete the following: Output AR(Rs) MR(Rs) TR(Rs)

3 Given below is the cost schedule of a firm. Its TFC is Rs Calculate the MC and AVC at each level of output. Output(units) ATC Following information is available regarding the production of a firm Labour TP Determine various stages of production. 5. The ratio of elasticity of supply of commodities A and B is 1: % fall in price of A results 40% gall in supply. Calculate the percentage increase in supply of B, If its price rises from Rs.10 per unit to Rs. 11 per unit. (30%) (AISSCE-2010) 6. The price elasticity of supply of a commodity is 2.0 A firm supplies 200 units of it at a price of Rs. 8 per unit. At what price will it supply 250 units. (Rs.9) (AISSCE-2013) 7. When the price of a commodity is Rs. 10 per unit, its quantity supplied is 100 units.when its price rises by 10 %, its quantity supplied rises by 9 units. Calculate its elasticity of supply. Is its supply elastic? Give reasons. (0.9, NO) (AISSCE-2014) 8. Find out (a) Explicit Cost (b) Implicit Cost SL.No. Items Rs in thousands i Investment in fixed assets 2000 ii Borrowings at 12% interest per annum 1500 iii Wages paid during year 120 iv Annual rental value of the owner s factory building 180 v Annual depreciation 100 vi Estimated annual value of the management services of the owner Using following data find out producer s equilibrium using MR-MC Approach Output(units) TR(Rs) TC(Rs) TFC is Rs 90 complete the table (AISSCE-2002) Output (units) AVC (Rs) TC (Rs) MC(Rs) Calculate TR, MR AND AR (AISSCE- 2006) OUTPUT PRICE (Rs) 50 1

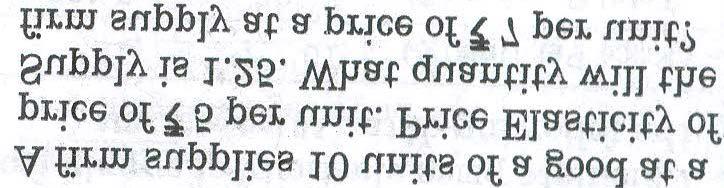

4 A seller of potatoes sells 80 quintals a day when the price of potatoes is Rs 4 per Kg. The elasticity of supply of potatoes is known to be 2. How much quantity will this seller supply when the price rises to Rs 5 per Kg? UNIT: 4 FORMS OF THE MARKET AND PRICE DETERMINATION 1. When demand function is given as Qd= 100-p and supply function is Qs=60+p Determine equilibrium price and equilibrium quantity. Draw demand and supply curves. (p=rs.20 and quantity=80 units) 2. Market demand and supply schedule of apples (per day) are given Price (per Kg) Q(in Kg) Q(in Kg) Determine (a) Equilibrium price and equilibrium quantity (b) Excess demand at Re 1 per Kg (c) Excess supply at Rs 5 per Kg UNIT 5 NATIONAL INCOME (NUMERICALS) 1) Calculate NNPfc by product method Items (Rs. Crore) a) Intermediate consumption of i) Primary sector 500 ii) Secondary sector 400 iii) Tertiary sector 300 b) Value of Output of i) Primary sector 1000 ii) Secondary sector 900 iii) Tertiary sector 700 c) Net factor income from abroad -20 d) Consumption of fixed capital 40 e) Net indirect taxes 10 Ans. NNPfc = (b-a)+c+d+e

5 = ) Calculate GDPmp by Income method a) Rent 10 b) Emoluments of employees 400 c) Mixed income 650 d) Operating surplus 300 e) Consumption of fixed capital 40 f) Interest 5 g) Net indirect taxes 10 Ans. GDPmp = b+d+c+e+g = ) Calculate NNPmp by Expenditure method a) Personal consumption expenditure 4000 b) Gross domestic capital formation 1000 c) Government consumption expenditure 2000 d) Net export 100 e) Depreciation 200 f) Net factor income from abroad -100 Ans. NNPmp = a+b+c+d-e+f = ) Calculate national income a) Net Export 15 b) Net factor income to abroad -10 c) Net domestic fixed capital formation 180 d) Consumption of fixed capital 100 e) Net indirect taxes 50 f) Private final consumption expenditure 900 g) government final consumption expenditure 400 h) change in stock 0

6 Ans. NNPfc = a+c+f+g+h+d-d+b+e = ) Find National income a) Subsidy 5 b) Change in stock 7 c) Net domestic capital formation 50 d) Indirect taxes 30 e) Government final consumption expenditure 100 f) Net factor income from abroad 10 g) Private final consumption expenditure 400 h) Net export -20 Ans. NI = g+e+c+h-f-d+a = 495 6) Calculate GDPfc a) Consumption of fixed capital 120 b) Mixed income of self employed 7000 c) Interest 250 d) Rent 300 e) Profit 800 f) Compensation of employees 2000 Ans. GDPfc = b+c+d+e+f+a = ) Calculate NNPfc a) Profit 1000 b) Mixed income c) Dividend 200 d) Interest 400 e) Compensation of employee 7000 f) Net factor income to abroad 100 g) Depreciation 400 h) Rent 500 Ans. NNPfc = e+a+b+d+h-f

7 = ) Calculate NNPmp a) Gross domestic fixed capital formation 400 b) Private final consumption expenditure 8000 c) Government final consumption expenditure 3000 d) Change in stock 50 e) Consumption of fixed capital 40 f) Net indirect taxes 100 g) Net export -60 h) Net factor income to abroad -80 i) Dividend 100 Ans. NNPmp = a+b+c+d+g-e-h = ) Calculate national income by income method a) Mixed income 2500 b) Net factor income from abroad -50 c) Rent 500 d) Corporate tax 700 e) Profit 300 f) Compensation of employees 1600 g) Interest 500 h) Dividend 60 Ans. NI = f+a+c+e+g+b = ) Calculate National income a) Rent 200 b) Wages and salaries 700 c) Undistributed profit 20 d) Corporation tax 30 e) Interest 150 f) Social security contributions 100 g) Dividend 50 h) Net factor income to abroad 10

8 Ans. NI = a+b+c+d+e+f+g-h = 1240 UNIT-7 DETERMINATION OF INCOME AND EXPENDITURE Q.1. Ans: Q.2. Ans: Find consumption expenditure from the following: National Income= Rs 5000/- Autonomous consumption= Rs 1000/- Marginal propensity to consume=0.80 C=c +b.y =Rs (0.8)x5000 =Rs Rs Rs 5000/-.(Ans) Find National Income from the following: Autonomous Consumption=Rs 100/- Marginal propensity to consume=0.60 Investment=Rs 200/- At equilibrium Y=C+I Y=c +b.y+i =100+(0.6)Y+200 =300+(0.6)Y (0.4)Y=300 Y=Rs 750 (Ans) Q.3 Find Investment from the following: National Income= Rs 600 Autonomous consumption= Rs 150 Marginal propensity to consume=0.70 Ans: I=Y-C =600-[150+(0.7)x600] =600-[ ] = =30 (Ans) Q.4 An economy is in equilibrium. Calculate the Investment Expenditure from the following: National Income=Rs 800 Marginal propensity to sale=0.3 Autonomous consumption=rs 100 Ans: At Equilibrium Y=C+I I=Y-C Or at Equilibrium I=S

9 S=(-)s+(1-b)Y =(-)100+(1-0.3)x800 =460 (Ans) Q.5 An economy is in Equilibrium. Calculate the MPS from the following: National Income=1000 Autonomous Consumption=100 Investment=120 Ans: C=Y-I = =880 C=c +b.y 880=100+b.1000 b=780/1000=0.78 (Ans) Q.6 An Economy is in Equilibrium. Calculate the National Income from the following: Autonomous Consumption=120 Marginal propensity to save=0.2 Investment expenditure=150 Ans: MPC=1-MPS=1-0.2=0.8 At Equilibrium Y=C+I C=c +b.y =120+(0.8)Y Y=120+(0.8)Y Y=270 Y=1350 (Ans) Q.7 From the data given below for an Economy, Calculate a)investment Expenditure ; b) Consumption Expenditure Equilibrium level of Income=5000 Autonomous Consumption=500 Marginal propensity to consume=0.4 Ans: C=c +b.y C=500+(0.4)x5000 =2500 I=Y-C = =2500 (Ans) Q.8 In an Economy, C= Y is the consumption function where C is consumption Expenditure and Y is National Income. Investment expenditure is Calculate equilibrium level of Income and Consumption Expenditure. Ans: At Equilibrium y=c+i Y= Y Y=4200 Y=16800 and C=200+(0.75)x16800 =12800 (Ans) Q.9 From the following data about an Economy, Calculate

10 Ans: a) Equilibrium level of National Income b) Total consumption expenditure at equilibrium level of National Income (i) C= Y is the Consumption function where C is the consumption expenditure and Y is the National Income (ii) Investment Expenditure is 1500 At equilibrium Y=C+I Y= Y Y=1700 Y=3400 (Ans) Q.10 Calculate marginal propensity to consume from the following data about an economy which is in equilibrium National Income=2000 Autonomous consumption expenditure=200 Investment Expenditure=100 Ans: At Equilibrium Y=C+I Y=c +b.y+i 2000=200+b.(2000)+100 b=1700/2000=0.85 (Ans) Q.11 Calculate Investment Expenditure from the following data about an economy which is in Equilibrium: National Income=1000 Marginal propensity to save=0.20 Autonomous consumption expenditure=100 Ans: MPC=1-MPS =1-0.2=0.8 At Equilibrium Y=C+I Y=c +b.y+i 1000=100+(0.8).1000+I I= =100 (Ans) Q.12 Calculate autonomous consumption expenditure from the following data about an economy which is in equilibrium: National Income=500 Marginal propensity to save=0.3 Investment expenditure=100 Ans: C=Y-I C= =400 We know C=c +b.y 400=c+(1-0.3)x =c+(0.7)x500 c= =50 (Ans) Q.13. In an economy C= Y and I=1000 (where C=Consumption, Y=Income, I=Investment Calculate the following: a) Equilibrium level of income

11 Ans: b) Consumption expenditure at equilibrium level of income At Equilibrium Y=C+I Y= Y Y=1500 Y=15000 (Ans) Q.14. In an economy the ratio of APC and APS is 5:3. The level of Income is Rs How much are Savings, Calculate. Ans: APC:APS=5:3 Consumption=(5/8)x6000=3750 And Savings= =2250 Alternatively; (3/8)x6000=2250 (Ans) Q.15 Complete the following table: Income Consumption Expenditure Ans: Y=C+S S=Y-C MPS=(ΔS)/(ΔY) APC=C/Y MPS APC Income Consumption Saving MPS APC Expenditure Q.16. In an economy, the equilibrium level of income is Rs The ratio of MPC to MPS is equal to3:1. Calculate the additional investment required to reach a new equilibrium level of income of Rs Ans: MPC=3/4=0.75 MPS=1/4=0.25 K=1/MPS=1/0.25=4 K=(ΔY)/(ΔI) ΔI=8000/4 [As ΔY= =8000] =2000 (Ans)

12 Q.17. An increase of Rs 250 in investment in an economy resulted in total increase in income of Rs Calculate the following: a) MPC(Marginal propensity to consume) b) ΔS(Change in Saving) Ans: K=(ΔY)/(ΔI)=1000/250=4 We know K=1/(1-MPC)=4 K=1/MPS=4 MPS=0.25 MPS=(ΔS)/(ΔY)=0.25 ΔS=(0.25)(ΔY)=(0.25)(1000)=250 (Ans) UNIT-8 GOVT. BUDGET AND ECONOMY Q.1 From the following data about a govt. budget, find a)revenue deficit, b)fiscal deficit, c)primary deficit i) Tax Revenue ii) Capital Receipts iii) Non tax revenue iv) Borrowings v) Revenue Expenditure vi)interest payments Ans: a) Revenue Deficit=Revenue Expenditure-Tax Revenue-Non-tax revenue = =23 b Fiscal Deficit=Borrowings=32 c) Primary Deficit=Fiscal Deficit-Interest payments =32-20=12 Q.2. Ans: From the following data about a govt. budget, find a)revenue deficit, b)fiscal deficit, c)primary deficit i)plan Capital Expenditure ii)revenue Expenditure iii)non-plan expenditure iv)revenue Receipt v)capital receipts net of borrowing vi)interest pyment a) Revenue Deficit=100-70=30 b)fiscal deficit= =90 c)primary deficit=fiscal deficit-interest payment=90-30=60

13

14 Scanned by CamScanner

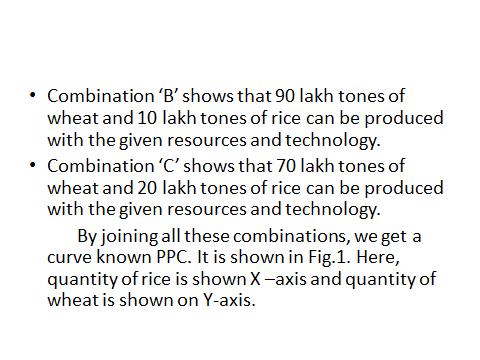

15 CLASS- XII ECONOMICS PART: A Introductory Micro Economics Capsules UNIT: I TOPIC: INTRODUCTION A: Basic concepts 1. Definition of Economics 2. Central problems of an economy 3. Production possibility curve 4. Opportunity Cost 5. Micro Economics and Macro Economics Definition of Economics: Economics is a Social Science. It seeks to answer questions relating to the economic behavior of the people of the society and the economy. Central Problems of an economy: I) Problem of allocation of recourses a) What to produce & How much to produce? b) How to produce? c) For whom to produce? II) Fuller utilization of resources III) Growth of resources of economic development. 1. The what problem refers to which goods and services will be produced in an economy and in what quantities. 2. The how problem refers to the choice of methods of production of goods and services. 3. The for whom problem concerns with the distribution of income and wealth. Marks : 4 Production possibility curve. A production possibility curve depicts those different combinations of two commodities that an economy can produce with the help of available resources. 4. Normally, the production possibility curve is concave to the origin. It is because of increasing marginal opportunity cost. 5. A production possibility curve shifts out due to technological progress or increases in the supply of resources available to an economy or both. Opportunity Cost. It refers to the cost of a factor in the next best use/ activity. Micro and Macro Economics: ECONOMICS Q1-XII-3

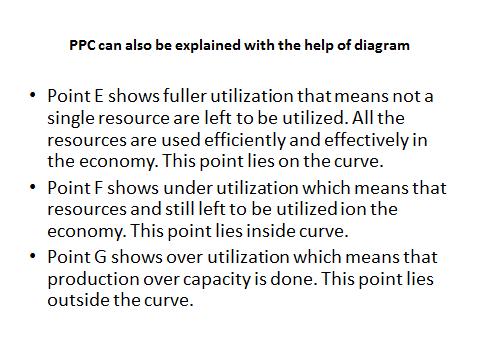

16 Micro economics studies the economic activities of individual units in the economy like a consumer, a producer, a market. Macro economics studies aggregates at the level of the economy like aggregate demand, aggregate supply, total saving, total investment, population etc..positive Economics and Normative Economics Positive Economics deals with what is and Normative Economics deals with what ought to be. B: Question Answer: Very short answer type questions with answers ( 1 mark each) 1) What is meant by economic problem? Ans. By economic problem we mean the problem of choice. 2) Why does economic problem arise? Ans. The economic problem arises due to scarcity of resources. 3) What is the shape of production possibility curve? Ans. PPC is concave to the origin and slopes downwards. 4) Who is known as the Father of economics? Ans. Adam Smith. 5) What is meant by scarcity definition? Ans. Economics is a science that studies human behavior as a relationship between ends and scarce means which have alternative uses. 6) What are the main features of human wants? Ans. i.wants are unlimited. ii. They arise again and again (wants are recurrent). 7) Who gave the welfare definition of economics? Ans. Dr. Marshall 8) What do you mean by allocation of resources? Ans. It means the distribution of resources for the production of consumer goods and services. 9) What is meant by economising resources? Ans. Making the best utilization of scarce resources. 10) Why do all economies have similar economic problems? Ans. Scarcity of resources gives birth to economic problems in all economies. 11) Use production possibility curve technique to show growth of resources in an economy. Ans: ECONOMICS Q1-XII-4

1. Draw a production possibility curves and show the following situations in the diagram.")

17 12) Define marginal opportunity cost along the PPC? Ans: Marginal Opportunity cost refers to the loss of output of good-y when resources are shifted from Y to produce an additional unit of good-x. Short answer type questions with answers (3 or 4 marks each) 1. Draw a production possibility curves and show the following situations in the diagram. a) Full employment of resources b) Under utilization of resources c) Growth of resources Ans. 2. What are the central problems of the economy? Ans. They are as follows: a) The problem of allocation of resources i. What to produce and how much to produce ii. How to produce? iii. For whom to produce? b) How to achieve fuller utilization of resources c) How to achieve growth of resources. 3. What are the economic activities of economy? Explain them. Ans. 1) Production: The production is the process of creation of utility like wood into furniture as Table, chair etc. 2) Consumption: The process of using up the commodity for the satisfaction of wants. 3) Investment: Addition made to the stock of capital. 4.What are the characteristics of PPC? Ans. i) The production possibility curve slopes downwards to the right indicating that the economy has to sacrifice,more and more amount of the other good per unit increase in the production of the good in question. ECONOMICS Q1-XII-5

18 ii) It is concave to the point of origin: it shows the operation of the law of increasing marginal opportunity cost. 5. An economy always produces on, but not inside, a PPC. Define or refute? Ans. In the economy with the given resources being fully employed and technology given, the combination of two goods will be any where on PPC. The society decides any combination like A,B on PPC. If there is inefficient use of resources or unemployment in any form in the economy, the economy will operate strictly within the PPC, for example, at point G. 6. Distinguish between Micro and Macro economics. Micro 1.It deals with the behaviour of individual economic units. 2. Demand and supply are the main tools of analysis. 3.It explains how resources are allocated among various goods and services and how N.I. is distributed in the economy 4.It is concerned with the determination of equilibrium level of prices of goods and services of a firm. Macro 1.It deals with the study of the economy as whole 2.Aggregate demand and aggregate supply are the main tools of analysis. 3.It explains how productive capacity and N.I. of the country increase over time. 4.It is concerned with the determination of equilibrium level of output, employment and income etc. of the economy. 7. Explain the central problems facing an economy. Scarcity of resources is a common feature of all types of economics.every economy has to face problems relating to choice which are known as central problems. 1. Problem of allocation of resources. Every economy has to allocate its available resources in the production of goods and services. While allocating resources the economy has to decide what, how and for whom to produce. 2. Problem of Efficient utilization of resources. The problem refers how to use available resources in the best possible manner and to get maximum production. 3. Problem of Growth of Recourses. It has become most essential for under developed countries not only to make the full use of their resources but to increase their production capacities also through the growth of resources. ECONOMICS Q1-XII-6

19 UNIT-II Consumer s Equilibrium and demand CHAPTER II Consumer Choice and demand curve A. Basic Concepts: 1. Consumers are the persons who make demand for final goods and services. 2. Producers are those who supply final goods and services. 3. Final goods are the things consumed by household. 4. Intermediate goods are consumed by producers. 5. Utility refers to the want satisfying power of a commodity. 6. Total utility refers to the total psychological satisfaction obtained by a consumer from consuming a given amount of particular good. 7. Marginal utility is the extra or additional utility obtained from the last unit consumed. 8. Law of diminishing marginal utility states that as a consumer consumes more and more of a commodity, the M.U. derived from each additional unit goes on diminishing. 9. The consumer is in equilibrium when he maximizes his satisfaction at a given income and price of commodity and it is attained when = Its price M.U. of a Product M.U. of a Rupee Marks : 13 Or, M.U. of a Product = M.U. of a rupee Consumers equilibrium through IC approach; Consumer equilibrium refers to a situation, in which a consumer derives maximum satisfaction, with no intention to change it and subject to given prices and his given income. The point of maximum satisfaction is achieved by studying indifference map and budget line together. On an indifference map, higher indifference curve represents a higher level of satisfaction than any lower indifference curve. So, a consumer always tries to remain at the highest possible indifference curve, subject to his budget constraint. The consumer s equilibrium under the indifference curve theory must meet the following two conditions: (i) MRSXY = Ratio of prices or PX/PY Let the two goods be X and Y. (iii) The first condition for consumer s equilibrium is that MRSXY = PX/PY a. If MRSXY > PX/PY, it means that the consumer is willing to pay more for X than the price prevailing in the market. As a result, the consumer buys more of X. As a result, MRS falls till it becomes equal to the ratio of prices and the equilibrium is established. b. If MRSXY < PX/PY, it means that the consumer is willing to pay less for X than the price prevailing in the market. It induces the consumer to buys less of X and more of Y. As a result, MRS rises till it becomes equal to the ratio of prices and the equilibrium is established. (ii) MRS continuously falls: The second condition for consumer s equilibrium is that MRS must be diminishing at the point of equilibrium, i.e. the indifference curve must be convex to the origin at the point of equilibrium. Unless MRS continuously falls, the equilibrium cannot be established. Thus, both the conditions ECONOMICS Q1-XII-7

20 need to be fulfilled for a consumer to be in equilibrium. Let us now understand this with the help of a diagram:, IC1, IC2 and IC3 are the three indifference curves and AB is the budget line. With the constraint of budget line, the highest indifference curve, which a consumer can reach, is IC2. The budget line is tangent to indifference curve IC2 at point E. This is the point of consumer equilibrium, where the consumer purchases OM quantity of commodity X and ON quantity of commodity Y. All other points on the budget line to the left or right of point E will lie on lower indifference curves and thus indicate a lower level of satisfaction. As budget line can be tangent to one and only one indifference curve, consumer maximizes his satisfaction at point E, when both the conditions of consumer s equilibrium are satisfied: (i) MRS = Ratio of prices or PX/PY: At tangency point E, the absolute value of the slope of the indifference curve (MRS between X and Y) and that of the budget line (price ratio) are same. Equilibrium cannot be established at any other point as MRSXY > PX/PY at all points to the left of point E and MRSXY < PX/PY at all points to the right of point E. So, equilibrium is established at point E, when MRSXY = PX/PY. (ii) MRS continuously falls: The second condition is also satisfied at point E as MRS is diminishing at point E, i.e. IC2 is convex to the origin. Demand and its determinants 1.Demand is the quantity of a good that that the consumer is willing to buy at a price at a time. 2.Price of related goods, income and tastes of the consumer are the determinants of demand. 3.Law of demand states that other things remaining same, as the price of commodity increases, the quantity demanded by a consumer falls and vice-versa. 4.Demand curve slopes downwards because of operation of diminishing marginal utility, income effect and substitution effect. 5.Exceptions to the law of demand conspicuous consumption, Giffen goods, Necessary goods, Expectations of future change in price. 6.Change in quantity demanded or Movement along the demand curve- whenever there is a change in the price of commodity, the quantity demanded of the commodity changes, other things remaining constant.. 7. Increase and decrease of demand: when demand changes not due to price but due to other factors like income, tastes & preferences then it is termed as change in demand. Elasticity of demand 1. The degree of responsiveness of demand to a change in the price of a commodity. 2. Price elasticity - the percentage change in quantity demanded divided. by the percentage change in the price of the commodity. Ep = %Change in Quantity Demanded % Change in price Measurement of Elasticity of demand.1. Proportionate or percentage method. ECONOMICS Q1-XII-8

21 (i) e p = (Q 1 -Q 0 )/Q 0 (P 1 -P 0 )/P 0 OR (ii) e p = Q/ P x P 0 / Q 0 Types of Elasticity of demand 1. Perfectly inelastic demand. 2. Inelastic demand. 3. Unitary elastic demand. 4. Elastic demand. 5. Perfectly Elastic demand. Determinants of Elasticity of demand or Factors affecting elasticity of demand. 1. Availability of close substitutes 2. Habits. 3. Change in income 4. Proportion of income spent on a particular good. 5. Postponement of demand. B. Question-Answer [1 mark each] 1. What is equilibrium?, Ans. The position or state of rest. 2. What are final goods? Ans. All those goods which are used for consumption or for capital formation. Example - Bread, vegetables, machines.etc. 3. What are intermediate goods? Ans. They are the raw materials consumed in producing other goods. 4. What is total utility? Ans. The total psychological satisfaction obtained by a consumer from consuming a particular commodity., 5. What is marginal utility? Ans. The utility derived from the last unit consumed. 6. State the law of diminishing marginal utility. Ans. The law states that after consuming a certain amount of a good or service the Marginal utility from it diminishes as more and more is consumed. 7. State the condition of consumer's equilibrium. Ans.The condition is - Marginal utility of a product =its price. Marginal utility of a Rupee 8.What are inferior goods? Ans.Inferior goods are those for which demand falls as income increase. ECONOMICS Q1-XII-9

22 Short type questions - answers [3/4 marks each] 1. What is meant by income effect? Ans. Income effect is the part of the price effect. When the price of a commodity falls, real income of the individual increases. As a result, more of the goods will be bought and his demand increases. This part of the increase in demand due to increase in real income is income effect of a fall in the price of a good on its demand. 2. What is substitution effect? Ans. When the price of a commodity falls, the commodity becomes relatively cheaper than its substitutes. So the people consuming.the substitute also start demanding this commodity and its demand increases. This is substitution effect. 3. Can the demand curve slope upwards? Ans. In some cases the demand curve slopes upwards. i) Giffen goods. Inferior goods have large negative income effect. ii) Demand increases when prestige is attached to the possession of a good, 4. What is meant by Elasticity of demand? Ans. Elasticity of demand shows the degree of responsiveness of demand to change in the price of a commodity. 5. Price of a commodity rises from Rs. 5 to Rs. 6. As a result its demand falls from 100 units to 80 units. Find out price elasticity of demand by percentage method. Ans: E P = Q/ P X P/Q = 20/1 X 5/100 =1 6. On the basis of information given below compare the price elasticities of good A and B. a) Good A (b) Good B Price Total expenditure (Rs) Price Total expenditure(rs) Ans: (a) Price T.E QD (b) price T.E QD E P = Q/ P X P/ Q E P = Q/ P X P/Q = 1/1 x 4/5=0.8 = 1/ 1 x 3/5 = 0.6 Demand for good A is more elastic than that of good B.. 7. Differentiate between change in demand and change in quantity demanded. Ans. Change in demand or Shift of the demand curve: i) This happens when at the same price more or less is demanded. ii) Other factors affecting demand change causing a right or leftward shift of the demand curve. iii) It is of two types - increase in demand (rightward shift) and decrease in demand (leftward shift). Change in Quantity demanded ECONOMICS Q1-XII-10

It is of two types expansion(downward movement along a demand curve and contraction of demand (upward movement along a demand curve). Long questions [ 6 Marks each] 1.")

income of the consumer - The effect of change in Income on the demand depends on the Nature of commodity.... Normal Goods: - If Income Increases the demand for normal goods Increases.")

23 Change in quantity demanded or movement along the demand curve: i) This happens, when at a lower(higher) price, more(less) is demanded. ii) Other factors affecting demand remain constant. iii) It is of two types expansion(downward movement along a demand curve and contraction of demand (upward movement along a demand curve). Long questions [ 6 Marks each] 1. What are the determinants of demand? Explain. Ans. Following are the determinant of demand. / (i)income of the consumer - The effect of change in Income on the demand depends on the Nature of commodity.... Normal Goods: - If Income Increases the demand for normal goods Increases. Inferior goods :- Their demand falls with an increase in the income. ii) Prices of related goods: Substitute goods:- There is a direct (positive) relationship between the price of a good and demand of its substitute goods. If the price of coffee increases, its demand will fall and people will start consuming its substitute-tea. Complementary goods :- There is a negative or inverse relationship between the price and demand of complementary goods. If the price of sugar increases, demand for tea will decrease. iii) Tastes - If there is a favorable change in taste, demand will increase and the demand curve shifts rightwards and vice-versa. iv) Expectations: If the expectation is for the prices to rise in future, then there is increase in demand and ECONOMICS Q1-XII-11

24 if the expectation is for the prices to fall in future then there is fall in demand.. 2. Explain the factors affecting price elasticity of demand. Ans. Elasticity of demand is the responsiveness of demand to changes in the price of a commodity. i) Availability of close substitutes - If close substitutes of a product are available, elasticity is high because a small increase in price will make the consumers switch over to other products in a big way. As a result, there is a proportionately large fall in demand for the product. In the absence of close substitutes the elasticity is likely to be small. ii) Nature of the commodity. Demands for essential products are likely to be in elastic whereas demand for luxury items is relatively elastic. iii) Proportion of total expenditure spent on the product. If the amount spent on a product forms a small proportion of the, total expenditure on all goods and services we consume, then the price elasticity is likely to be small.. iv) Habits - If a person gets into the habit of consuming a commodity, it becomes difficult for him to reduce the consumption of that commodity even at a higher price and hence for such commodities demand is relatively inelastic. Production and Costs A: Basic Concepts UNIT- III Producer Behaviour and Supply Chapter - 3 Production - is the transformation of inputs into output. Production function It is a relationship between inputs used and output produced by the firm. Various combinations of inputs. Factors inputs are classified as (i) Fixed factors and (ii) variable factors. [Marks 13] i) Fixed Factors are those factors which do not vary to change the level output. Their costs remain fixed even with the change in output e.g. land, machinery, top management etc. ii) Variable Factors are those factors which vary to change the level of output. The costs of such factors vary with level of output. E.g. labour, raw material etc. ECONOMICS Q1-XII-12

25 The Short run and The Long run: Short run refers to that period when all the factors can not be changed by a firm to change the level of output. Some factors of production are fixed and some are variable. Long run refers to the period when all the factors can be changed by a firm to change the level of output. All factors are variable and no factor is fixed. Law of variable proportions and Law of Diminishing Returns : Law of variable proportions : It says that the marginal product of a factor input initially rises with its employment level. But after reaching a certain level of employment, it starts falling. Law of Diminishing marginal product or law of diminishing returns : It says that if we keep increasing the employment of an input, with other inputs fixed, eventually a point will be reached after which the marginal product of that input will start falling. The reasons behind the law of diminishing returns or the law of variable proportions. (i) Initially, the factor proportions become more and more suitable for the production, as a result marginal product increases. (ii) After a certain level, the production process becomes too crowded with the variable input and the factor proportions become less and less suitable for production. As a result marginal product of the variable input starts falling. Returns To A Variable Factor Units of Labour Total product AP MP (Quintals) (Quintals) (Quintals) Stage I Stage of increasing returns to a factor Stage II Stage of Diminishing returns to a factor Stage III Stage of negative returns to a factor ECONOMICS Q1-XII-13

26 According to this law as more and more units of a variable factor are applied with fixed factors, in the short run, initially the TP increases at an increasing rate ; after a certain level of employment the TP increases at diminishing rate and finally, total product starts declining with every increase in the variable input. First Stage : i) TPP increases at an increasing rate ii) MPP increases and reaches its maximum point. Second Stage : i) TPP increases at a diminishing rate ii) MPP decreases but remains positive & finally becomes zero. Third Stage : i) TPP begins to fall. ii) MPP becomes negative.. COSTS A: Basic Concept: COSTS : The expenses incurred by the producer on hiring & Purchasing the factors of production are known as the cost of production. Total cost is the amount of money incurred on the production of a given level of output. Short Run: There are two types of costs 1. Fixed Costs are those costs which do not vary with the level of output. These costs include depreciation allowance, interest on fixed capital, rent of building, wages and salaries of permanent employees, insurance premium etc. These are called overhead costs. ECONOMICS Q1-XII-14

27 2. Variable costs are those costs that change with the level of output. For e.g. labour costs and costs of raw materials. TC = Total Fixed Cost (TFC) + Total variable cost (TVC) (a) Total fixed cost curve is horizontal because fixed costs do not change with the change in output. (b) TVC and TC increase with the output. These curves are upward sloping. (c) Total cost curve is the vertical summation of the total fixed cost and total variable cost curves. (a) At the zero level of output, TC = TFC because TVC is zero, when output is zero. COST T C T V C T F C OUT PUT Output TFC TVC TC Average cost is the cost per unit of output : AC = TC/Q TC = Total cost, Q = Quantity of output. Average cost is the sum of average fixed cost and average variable cost. AC = AFC + AVC Reasons for U - shape of the SAC Curve. (i)operation of the law of variable proportions. ECONOMICS Q1-XII-15

28 (ii)the shapes of AFC and AVC curves. Average fixed cost is the per unit fixed cost of producing a commodity. AFC = TFC/Q TFC = Total Fixed Cost, Q = Quantity of output. AFC can be calculated by dividing total fixed cost by quantity of output produced. The shape of AFC curve is rectangular hyperbola. Average variable cost is the per unit variable cost of producing a commodity. AVC =TVC/Q TVC = Total variable cost, Q = Quantity of output. AVC is obtained by dividing total variable cost by the quantity of output. Note : i) The AFC curve continuously decreases as output increases because the numerator of the ratio TFC / Q is constant while the denominator increases. ii) The AVC and ATC curves slope downwards initially and then rise upwards i.e. they are U-shaped. Marginal cost is defined as the change in total cost when one extra unit of output is produced. Inotherwords, it is the additional cost of producing an extra unit of output. Total costs and total variable costs differ only by a constant amount i.e. TFC. MC is the increase in TVC when one extra unit is produced. TVC = the sum of MCs. = The area under the marginal cost curve. Output : MC(Rs) : Here, the TVC of producing 5 units of output is Rs ( ) = Rs. 27. Similarly, the TVC of producing 9 units will be Rs( ) = Rs. 100 The MC is initially decreasing in output and then it is increasing i.e. it is U ` shaped. The reason behind the U shape of the MC curve is the law of diminishing returns. i.e. other inputs remaining the same, when a firm raises a variable input in the short run, initially the MP rises which leads to a fall in MC ; after a certain point the employment of Input leads to a decrease in its marginal product and then MC rises. As more and more output is produced, initially the rate of increase in the requirement of the variable input will be less and less ; and after a certain point, it will be more and more. Initially, the rate of increase in the variable cost which is same as the MC will be less as output increase and then, it will be more and more when output increases further. so the MC curve is U- shaped. ECONOMICS Q1-XII-16

The AVC curve is decreasing in the range of output from O to q 0. At any output level in this range MC<AVC (b) At any output greater than q 0, AVC is increasing in output, hence MC>AVC.")

29 Relationship between AVC, ATC and MC. 1. AVC, ATC and MC curves are U shaped. 2. MC curve cuts the AVC and ATC curves at their minimum points. 3. MC is the addition to both the TVC and the TC. (a) The AVC curve is decreasing in the range of output from O to q 0. At any output level in this range MC<AVC (b) At any output greater than q 0, AVC is increasing in output, hence MC>AVC. (c) (a) and (b) together imply that the MC curve must cut the AVC curve at the AVC s minimum point. Relationship between TC and MC. 1. When the TC rises at a diminishing rate, the MC declines. 2. When the rate of increase in TC stops, the MC is at its minimum. 3. When the rate of increase in TC starts rising, the MC is increasing. Chapter - 4 The Theory of the Firm under Perfect Competition A: Basic Concepts: Revenue : The money receipts from the sale of the product. Total Revenue : refers to the total amount of money received by the firm from the sale of its products. TR = Price x output. Average Revenue is the revenue per unit of the output AR = TR / Q = P X Q / Q = P AR is always equal to price. Marginal Revenue is defined as the change in total revenue when one extra unit is sold. i.e. it is the revenue obtained from one extra or last unit sold.suppose the firm s output has increased from q0 to (q0+1). Given market price is P, notice that MR= ( TR from output(q0+1) ) (TR from output q0) = (P * (q0+1) ) (pq0) = P In other words, for a price taking firm, marginal revenue equals the market price. ECONOMICS Q1-XII-17

30 A Competitive firm is a price taker. If it sells one extra unit, the extra revenue generated will be equal to whatever the price is MR = P for a competitive firm. Profit : the difference between TR and TC. Producer s equilibrium : an equilibrium notion in the sense that if the firm selects the level of output at which profit is maximized, it would like to stay or rest at that level of output ; there is no incentive for it to increase or decrease output from that level. Producer s equilibrium : The Basis of the supply curve 1. TVC = the areas under the marginal cost curve. 2. TR is equal to the area under the price line The Profit maximizing condition : A competitive firm faces the market price Po i.e. PoA is the price line and its marginal cost curve is denoted by MC. A competitive firm s profit is maximized at the point where the price line intersects the MC curve i.e. P = MC (i.e. at point q 0 ) with P denoting the market price. This is the profit maximizing condition or the condition for producer s equilibrium. Why is profit maximized where the price line intersects the MC curve? Gross profit = TR TVC = profit + TFC. Since TFC is constant, profit is maximized where gross profit is maximized and vice-versa. At the market price Po, the gross profit is maximized at the output q 0, where the price line Po inter sects the MC curve. TR = the area under the price line = OPoAq 0. TVC = the area under the MC curve = ODAq 0 Gross profit = OPoAq 0 ODAq 0 = DPoA At any output less than q 0 say q, the gross profit = DPoA B. This is less than DPoA. ECONOMICS Q1-XII-18

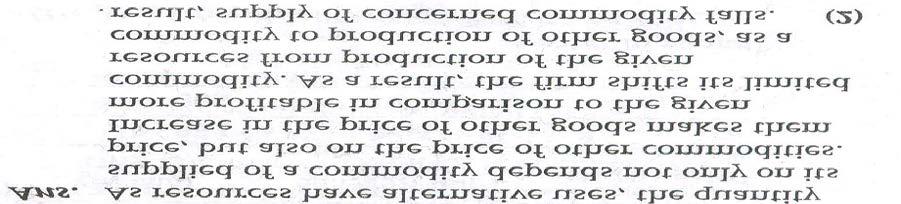

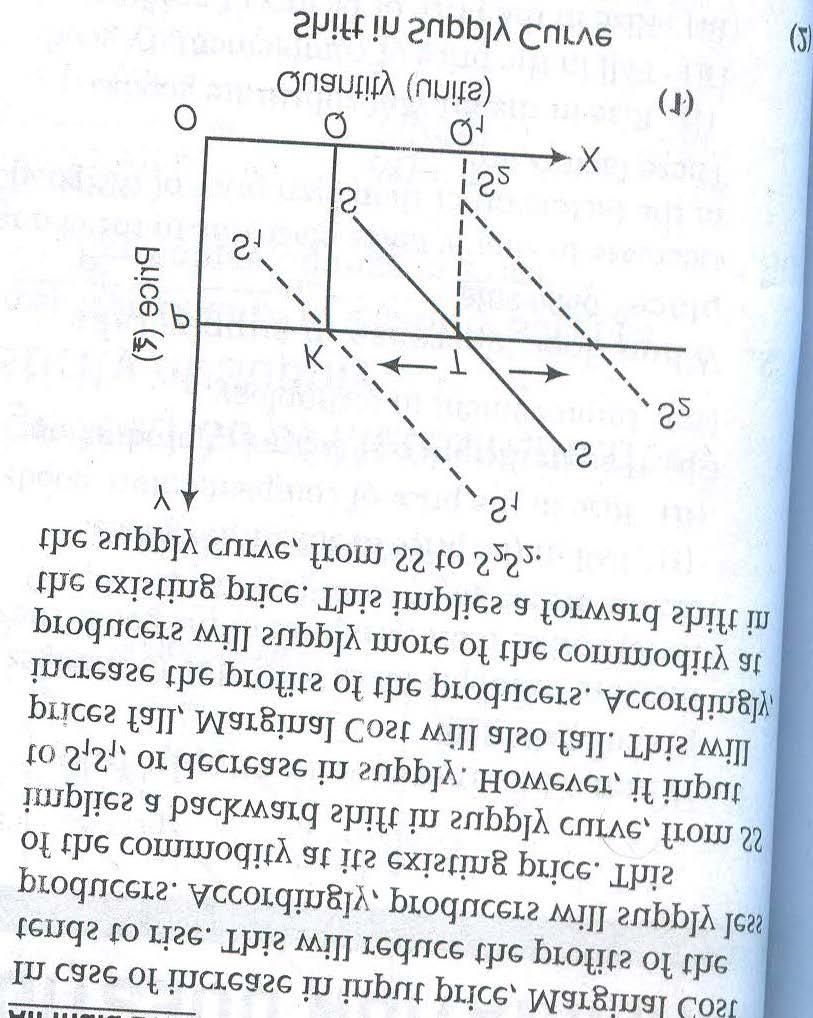

31 At the level of output greater than q 0 i.e. q, the total revenue = OPoA q and the total variable cost = ODCq. Gross profit = OPoAOq ODPCq = DPoA ACA This is also less than DPoA. Hence, at any level of output either less or greater than q 0, the gross profit is less. Hence, profits are maximum at q 0 where P=MC. Rational behind the condition P = MC. Producer s equilibrium condition P = MC be increasing with output. Starting from the level of output at which P = MC, the firm decides to produce one unit more. Given that MC is increasing in output, P will be less than MC. But P and MC are respectively equal to extra revenues earned & extra costs incurred. Hence, extra revenues will be less than the extra costs, implying that the profits will be less. Suppose the firm decides to produce one unit less than where P = MC. In this case the revenues sacrificed (equal to P) are greater than savings in costs. (equal to MC) Hence profits will also be less. Increasing or decreasing output from where P = MC results in less profits. Profit is maximized where P = MC as long as MC is increasing in output. A competitive firm chooses an output only on the rising portion of the MC curve. General profit maximizing condition : For a competitive firm, P = MR, MR = MC Law of supply and the supply curve : Supply : Quantity of a commodity which a firm or an industry is willing to produce at a particular price, during a given time period. Law of supply : Other things remaining unchanged, an increase in the price of a product leads to an increase in the quantity supplied of it and vice-versa. Supply schedule : The table which shows the quantities of a commodity supplied at various prices during a given time period. Supply curve : The graphical representation of a supply schedule. The rising part of the MC curve is the supply curve itself. All price output combinations are simply the points of the rising part of the MC curve. Change in quantity supplied : a movement along a given supply curve because of a price change. Change in supply : a shift of the supply curve due to a change in other factors. Determinants of supply or the supply curve : the factors that change the supply are the determinants of supply ECONOMICS Q1-XII-19

32 1. Technological Change : Science and research laboratories and business firms look for new technology or methods that reduce costs of production. Such a technological advance lowers marginal costs at any given level of output. Since the MC curve is essentially the supply curve, a technological progress shifts the supply curve to the right. 2. Input Prices : changes in raw material prices, wages to workers etc. can also affect the MC curve and the supply curve. An increase (a decrease) in an input price shifts the supply curve to the left (right). 3. Unit Tax : A tax that the government imposes per unit sale of output. Hence they add to the TVC, and a change in the rate of this tax affects the overall MC. An increase (a decrease) in the unit tax shifts the supply curve to the left (right) 4. The prices of related products An increase (a decrease) in the price of a substitute good in production shifts the supply curve of a good to the left (right). Market supply curve is derived by the horizontal summation of the individual supply curves. Factors affecting the market supply curve: i) Technological change ii) Change in input prices iii) No, of firms: An increase (a decrease) in the number of firms shifts the market supply curve to the right (left). iv) More (less) competition shifts the market supply curve to the right (left). v) Time Horizon: In a short period within which firms cannot adjust their output to any change in price, the supply curve of a firm or the whole industry is vertical. In a longer run the supply curve will be upward sloping because inputs can be changed. Movement along a supply curve : When other factors influencing supply do not change, and the own price of the commodity changes, the change in supply takes place along the curve only. This is called movement along a supply curve. A movement from one point to another on the same supply curve is also referred to as a change in quantity supplied. Shifts of the supply curve : When supply changes due to changes in factors other than the own price of the commodity, it results in a shift of the supply curve. This is also referred to as a change in supply. ECONOMICS Q1-XII-20

33 Extension and Contraction of Supply: Other things remaining the same, the rise in supply of a commodity due to rise in its price is called extension of supply. Extension of supply leads to an upward movement along the supply curve. price P1 S P S O Q Q1 Q.S. Other things remaining the same, the fall in supply of a commodity due to fall in its price is called contraction of supply.contraction of supply leads to a downward movement along the supply curve. price P E S P1 E1 O Q1 Q Q.S. Increase and Decrease in Supply: The price of the commodity remaining the same, rise in supply of the commodity due to other factors like improvement in technology, low input price etc. is known as increase in supply. Increase in supply leads to a rightward shift of the supply curve. Price S S1 P E E1 O Q Q1 Q.S. ECONOMICS Q1-XII-21

34 The price of the commodity remaining the same, fall in the supply of a commodity due to other factors like rise in input prices, rise in unit tax etc.is known as decrease in supply.decrease in supply leads to a leftward shift of the supply curve. S1 Price S P O Q1 Q Q.S. PRICE ELASTICITY OF SUPPLY: Quantifies the responsiveness of quantity supplied to a change in price of a commodity. e s = P / S x s / p denotes the change If the supply curve is vertical, then the price elasticity of supply is obviously zero. Supply curve is positively sloped. The price elasticity is positive. B: Question-Answer Very short answer questions : (1 mark each) 1) What is production function? Production function is the technological relationship between factors of production and physical quantities of output. 2) What is meant by total physical product (TPP)? TPP refers to the total volume of goods and services produced during a specified period at a particular level of employment of an input when the employment of other inputs is unchanged. TPP = Σ MPP or TPP = APP x L (L = variable factor) 3) What is meant by average physical product? APP is production per unit of the variable factor. APP = TPP/L 4) What is marginal physical product? MPP = TPP n TPP n 1 5) How is the TPP derived from MPP schedule? By adding up marginal physical product of various units of a variable factor. TPP = Σ MPP. 6) What is meant by returns to a factor? ECONOMICS Q1-XII-22

35 Returns to a factor explain the behaviour of the output while the employment of one input varies, keeping other inputs constant. 7) State the law of variable proportions. If one factor is increased keeping other factors constant, MPP initially increases with an increase in the employment of the input, then it diminishes and finally becomes negative. 8) State the law of diminishing returns. The employment of other inputs remaining the same as more of a particular input is used in production, after a certain level, the MPP decreases with further employment of it. 9) What is meant by fixed factors? Those factors of production whose supply cannot be increased in the short run. 10) What are variable factors? Those factors whose supply can be changed at any time according to requirement for more production. 11) What is meant by fixed cost? Those short run costs which do not vary with the level of output are known as fixed costs. For e.g. depreciation of machines, interest on fixed capital. 12) What is meant by variable cost? Those costs which vary with the level of output ; e.g. Cost of raw material. 13) What is total cost? It is the total of all costs equal to the sum of total fixed costs and total variable costs. 14) What is total variable costs? It is the total of all costs that vary with the level of output. 15) What is average cost? It is the total cost divided by the output AC = TC/ Q 16) What is average fixed cost? It is the total fixed costs divided by the output. AFC = TFC / Q 17) What is average variable cost? It is the total variable cost divided by the output. AVC = TVC / Q 18) What is meant by marginal cost? MC is the increase in total cost or total variable cost incurred when an extra unit of output is produced. 19) What is the general shape of AFC? AFC is a rectangular hyperbola. 21) What do you mean by volume discount? It is the discount on price when a large quantity of input is purchased by a firm. ECONOMICS Q1-XII-23

36 22) What does producer s equilibrium mean? It is a situation when a producer maximizes his profits, minimizes losses (if any) in the production of goods and services. 23) What is the condition of producer s equilibrium? P = MC in perfect market. MR = MC in imperfect market. 24) What is price-line? It is the horizontal line that represents the market price facing a competitive firm. 25) What is profit? Profit is the difference between total revenue and total cost. 26) What is market structure? It refers to the no. of firms, the nature of competition between them and the nature of the product. 27) What is market period? It is that short a period within which firms cannot adjust their output to any change in price and thus a firm s output is given. 28) What is overhead cost? It is the total of all costs that are independent of the level of output. 29) What does supply mean? Supply refers to the quantity of a commodity that a seller offers for sale at a given price, at a point of time in specific market. 30) What does stock imply? Stock of a commodity refers to the total quantity of a commodity which at any point of time a seller can make available for sale in the market. 31) State the law of supply. Other things remaining the same, higher the price, greater the quantity supplied and lower the price, smaller the quantity supplied. 32) What is supply schedule? A supply schedule is a tabular statement that gives a full account of supply of a particular commodity at different prices at a point of time in a specific market. 33) What is supply curve? It is the graphic presentation of quantity supplied of a product showing that higher the price, the greater is the quantity supplied and vice-versa. 34) What is market supply curve? Market supply curve is the graphic presentation of market supply schedule which shows total quantities offered for sale at various prices by different firms producing a particular commodity. 35) What is meant by change in supply? If the price of the commodity remains constant and the supply is changed by the changes in other factors, it is known as change in supply. 36) What is extension in supply? ECONOMICS Q1-XII-24

37 Other things being equal, when quantity supplied of a commodity increases due to rise in price alone, it is known as extension in supply. 37) What is contraction in supply? When there is a fall in supply due to a fall in price, it is known as contraction in supply. 38) What is increase in supply? When supply of a product increases due to other factors like improvement in technique of production, changes in goals of firms etc. it is known as increase in supply. 39) What does decrease in supply mean? When supply of a product falls due to other factors like expected fall in prices in future, rise in factor prices etc. it is known as decrease in supply. 40) What is price elasticity of supply? Elasticity of supply is the responsiveness of supply of a commodity to a change in its price. 41) Write the formula for elasticity of supply. e s = P / S x s / p 42) What does supply function mean? It is a functional relation between supply of a commodity and its various determinants. 43) What effect does a cost saving technical progress have on the supply curve? Supply curve shifts rightward. 44) What effect does an increase in input price have on supply curve? Supply curve shifts leftward. 45) What effect does an increase in excise tax rate have on the supply curve of the product? Leftward shift of the supply curve. Short Answer Question [ 3 or 4 marks each ] 1. Explain the determinants of supply i) Price of the commodity Higher the price, greater would be the supply. ii) Prices of factors of production with he rise in prices of factors of production, cost of product will rise. So the supply will fall. iii) Goals of the firms If the firm has the goal of profit maximisation, supply will rise. 2. Distinguish between short run and long run Short Run Long Run i) The period when all the factors cannot i) All the factors of production be changed become variable ii) Some factors are fixed and some are ii) All are variable variable 3. Returns to a factor Returns to scale i) Short run concept i) Long run concept ii) Only one or some inputs can be changed ii) All factors are variable keeping other inputs fixed. iii) Factor ratio changes iii) No change in factor ratio iv) There is no change in scale of production iv) change in scale of production v) Refers to change in output when one input v) Refers to change in output when all ECONOMICS Q1-XII-25

AP falls even when MP is zero. 5. What is the relationship between TP & MP?")

38 input is variable. 4. What is the relationship between AP and MP? i) When MP increases, AP also increases ii) iii) iv) MP increases at a greater rate as compared to AP. At one stage AP becomes equal to marginal product. AP falls when MP falls at a greater rate. v) AP falls even when MP is zero. 5. What is the relationship between TP & MP? i) When MP increases TP increases at an increasing rate. ii) iii) iv) When MP falls, TP increases at a diminishing rate. When TP is maximum, MP is zero and AP falls. When MP is negative, TP diminishes. 6. Differentiate between fixed cost and variable cost Fixed cost inputs are variable. Variable cost i) amount spent on fixed factor i) amount spent on variable factors ii) does not vary with the change in output ii) varies with the change in output iii) remains the same even when output is zero iii) It s zero when output is nil iv) Example - rent, insurance premium iv)example cost of raw materials, salaries of permanent workers. 7. Explain the relationship between MC and AC i) When MC<AC, AC falls. ii) iii) iv) When MC = AC, AC is at its minimum. When MC>AC, AC increases. When MC starts rising, AC continue of fall. v) Minimum point of MC comes before the minimum points of AC. 8. What is the relationship between MC and TC. i) When TC rises at a decreasing rate MC falls ii) When the rate of increase in TC starts diminishing, MC becomes minimum iii) When TC increases at an increasing rate MC increases 9. Why are the MR and AR of a perfectly competitive firm equal? Because price of the good remains same at all levels of output due to the existence of a large number of firms and the firms produce and sell homogeneous product. Output Price TR AR ECONOMICS Q1-XII-26

39 Why is the AC curve U shaped? i) Because of law of variable proportion :- In the beginning, with increase in output, AC falls because of the operation of the law of increasing returns. After reaching the minimum point, when we increase the output, AC starts increasing due to the operation of diminishing returns. ii) Indivisibilities of the factor In the short run when a firm increases the output, due to indivisibilities of some fixed factors of production, AC curve falls in the beginning. After the optimum point, AC increases. Thus AC curve gets U-shape. 11. What is producer s equilibrium? Write the condition of producer s equilibrium? A producer is in equilibrium when it maximizes profits and has no tendency to move away from this situation till circumstances remain unchanged. Conditions: i) ii) MR = MC MC curve cuts MR from below. 12. Calculate TFC, TVC, AFC, AVC, MC when Output : TC : Ans: Output TC TFC TVC AFC AVC MC Differentiate between increase in supply and decrease in supply Increase in supply More quantity at the same price Same quantity at a lower price Decrease in supply Less quantity at the same price Same quantity at a higher price ECONOMICS Q1-XII-27

No.")

40 ii) Causes Causes Improvement in technique of production Obsolete technology Change in goals of firm Changes in goals of firm Fall in factor prices Rise in factor prices Increase in number of firms Decrease in number of firms Tax concessions and subsidies Increase in tax rates Increase in prices of related goods Fall in prices of related goods. 14. Distinguish between extension in supply and contraction in supply Extension in supply Contraction in supply i) A rise in supply of a commodity due to i) There is a fall in supply due to fall in rise in its price, other things remaining price, other factors remaining unchanged. Constant. Note : Draw the diagram below the explanation. 15. Mention the factors affecting market supply curve. i) No. of firms. ii) Possibility of expected change in price iii) Taxes and subsidies. iv) Change in technology v) Input price changes vi) Agreement among producers. 16. Mention the factors determining elasticity of supply. i) Nature of commodity ECONOMICS Q1-XII-28

41 Perishable and agricultural goods-inelastic Durable goods elastic ii) Cost of production If the production is subject to diminishing costs supply will be more elastic. In case of increasing costs, supply will be less elastic. iii) Time period During short period, supply will be less elastic In long period, supply is more elastic iv) Technique of production Goods using simple technique of production elastic supply In case of complex goods, less elastic v) Risk bearing capacity The goods will have elastic supply if risk bearing capacity of the firms is large. If producers are unable to bear risk, they will produce less elastic goods. 17. When the price of wheat was Rs. 500 per quintal, a producer supplies 10 quintals but when price rises to Rs. 550 per quintal, he supplies 12 quintals of wheat. Determine price elasticity of supply. e s = P / S x s / p = 500 / 10 x 2 / 50 Thus, e s = A seller sells 80 Kgs of potatoes a day when the price of potatoes is Rs. 4 per kilogram. The price elasticity of supply of potatoes is known to be 2, how much quantity of potatoes will the seller supply when the price rises to Rs. 5 per Kgs. e s = P / S x s / p 2 = 4 / 80 x s /1 2 = 4 s / 80 4 s = 80 x 2 4 s = 160 s = 160 / 4 = 40 Total supply by the seller at price of Rs. 5 = S + S = = 120 Kgs 19. The co-efficient of elasticity of supply is 1 5. What percentage change in supply will happen if its price rises by 40%. e s = % change in quantity supply / % change in price 1 5 = x% / 40% x% =1.5 x 40 = 60 Long Answer Questions (6 marks each) 1. Explain the law of variable proportion with the help of a suitable diagram. ECONOMICS Q1-XII-29

There is one variable input and the other inputs are fixed.")

42 The law of variable proportions states that if the input of one resource is increased by equal amount per unit of time while the inputs of other resources are held constant, total output will increase, but beyond some point the resulting output increases will become smaller and smaller. Assumptions of the law : i) There is one variable input and the other inputs are fixed. ii) Units of variable input are increased by an equal amount each time. iii) All the units of variable input are homogeneous. iv) The state of technology is given. v) Different factors can be employed in varying proportions. Units of labour Total product Marginal Product Average Product Stage I : Stage II : Stage III : Stages Total Product Marginal Product Average Product 1st TP increases at an increasing At initial stage MP increases AP also increases Stage rate and reaches maximum level 2nd TP increases at a diminishing Decreases and becomes Zero AP falls, becomes equal Stage rate and becomes the highest. to MP. Starts decreasing further but never becomes zero. 3rd Starts declining Becomes negative Further decreases but ECONOMICS Q1-XII-30

43 Stage never becomes zero or negative. UNIT IV Forms of Market and Price determination CHAPTER 5 Price determination under perfect competition with simple applications A. Basic concepts 1) Excess demand pushes up the market price by causing competition among buyers. Excess supply pushes down the market price by causing competition among the sellers. 2) At the market equilibrium, there is no excess demand or excess supply and demand and supply curves intersect. 3) Equilibrium price is the price at which the quantity demanded is equal to quantity supplied. 4) A non-viable industry is one in which demand and supply curves do not intersect. The supply curve lies above the demand curve and thus nothing is produced. 5) A rightward (left ward) shift of the demand curve leads to an increase (a decrease in) price and quantity transacted. If the demand curve shifts to the right and the supply curve to the left, the price rises. 6) A rightward (leftward) shift of the supply curve leads to a decrease (an increase) in price and an increase (a decrease) in quantity transacted. 7) An increase in the price of a substitute (complementary) good in consumption leads to an increase (a decrease) in price and quantity transacted of a good in question. 8) An increase in income results in higher (a lower) price and quantity transacted if the good is normal (inferior). 9) A favourable (unfavourable) taste shift leads to a higher (lower) price and quantity transacted. 10)A cost reducing technological progress leads to a lower price and more quantity being sold. 11)An increase in an input price leads to a higher price, and less quantity being sold. 12)An increase in rate of exise duty leads to a higher price and less quantity being exchanged. 13)A price control system includes a rationing scheme. Marks : 10 14)A price support system leads to a surplus of output, which is purchased by the government. B: Question Answer ECONOMICS Q1-XII-31

44 Very short type questions : (1 mark each) 1. Give the meaning of excess demand for a product? Ans: When quantity supplied is less than quantity demanded of a product. 2. What do you mean by excess supply of a product? Ans: When quantity demanded is less than quantity supplied of a product. 3. Define market equilibrium. Ans: It refers to a market situation in which demand equals supply. 4. What is meant by equilibrium price. Ans: The price at which quantity demanded is equal to quantity supplied. 5. What is the relationship between the control price and the equilibrium price? Ans: The control price is less than equilibrium price. 6. What is the relationship between the support price and the equilibrium price? Ans: The support price is higher than the equilibrium price. 7. What is equilibrium quantity? Ans: The quantity sold at the equilibrium price. 8. What is control price? Ans: The price fixed by the government in case of essential commodities. 9. When will an increase in demand imply an increase in price but no change in quantity supplied? Ans: When the supply is perfectly inelastic during very short period. 10. What is black marketing? Ans: It refers to a situation in which a particular commodity is sold at a price higher than the price fixed by the government (control price). Short type questions [3 or 4 marks] 1. How does an increase in input price affect the equilibrium quantity exchanged in the product market? Ans: An increase in an input price leads to a higher price and less quantity being exchanged. Use diagram showing supply curve shifting to the left. 2. How does an increase in the income affect the equilibrium price of a product? Ans: An increase in income results in a higher (a lower) price and quantity exchanged according as the good is normal (inferior). [Hints: Use diagram showing demand curve shifting to the right in case of normal goods, as income increases. 3. What will be impact on market price and quantity exchanged when there is a rightward shift in the demand curve? Ans: Supply remaining the same, a rightward shift in the demand curve means higher price and higher quantity sold. Use diagram. 4. What will be impact on market price and quantity exchanged when the demand curve is perfectly elastic and the supply curve shifts out? Ans: No change in the market price, equilibrium quantity will increase. 5. What will be impact on market price and quantity exchanged when both the demand and supply curve decrease in same proportion? Ans: Price remains the same, equilibrium quantity decreases. Use diagram. Long answer type questions [ 6 Marks] ECONOMICS Q1-XII-32

45 1. Equilibrium price may or may not change with shifts in both demand and supply curves Comment. Ans: i) If both demand and supply curves increase in same proportion, there will be no change in equilibrium price but equilibrium quantity will increase. ii) When both the demand and supply curve decrease in same proportion, price remains the same but the equilibrium quantity will decrease. iii) If the supply curve increases in a greater proportion than the demand curve, price of the product will decrease. Note: Use diagram in each case. A: BASIC CONCEPTS: CHAPTER - 6 FORM OF MARKET STRUCTURE Imperfectly competitive markets are of three types: monopoly, monopolistic competition and oligopoly. In perfect competition there are a large number of sellers selling a homogeneous product. In monopoly there is a single seller selling a product which has no close substitute. Monopolistic competition is a market having a large number of sellers selling differentiated products. It consists of competitive and monopolistic elements. In other words, the monopolistic compete with each other in this market structure. A monopoly market structure emerges from licensing, granting of a patent or forming a cartel. A monopoly is a price maker. A perfectly competitive firm is a price taker. In perfect competition price remains low and hence consumers are gainers. In monopoly a higher price is charged and less is sold. Patents encourage discovery and invention. Oligopoly market has few sellers.a perfect oligopoly market produces only homogeneous products whereas an imperfect oligopoly market produces differentiated products. In collusive oligopoly market,firms cooperate with each other in taking price and output decisions whereas in non-collusive oligopoly, firms compete with each other in taking price and output decisions, B: QUESTION-ANSWER: Very short type questions: [1 Mark each] 1. What is perfect competion? Ans. It is a market situation in which there are large number of buyers and sellers selling a homogeneous product at a uniform price. ECONOMICS Q1-XII-33

46 2. What is abnormal profit? Ans. It is equal to the producer s excess earning over the opportunity cost. 3. What is normal profit? Ans. It is the profit which a firm must earn in the long run to remain in business. 4. What is monopoly? Ans. It is a market situation in which there is a single seller selling a commodity which has no close substitute. 5. What is monopolistic competition? Ans. It is a market situation where there are large number of sellers selling differentiated products. 6. What is the shape of the demand curve under Monopoly? Ans. It is downward sloping and price-inelastic. 7. What is the shape of demand curve under Monopolistic competition? Ans. It is down ward sloping & price - elastic. 8. Why is the demand curve under monopoly downward sloping? Ans. It is so because a monopolist can sell more only by reducing price. 9. Why is the demand curve under monopolistic competition flatter? Ans. The demand curve is flatter because a large number of substitutes(differentiated product) are sold in this market. 10. What is the shape of demand curve under perfect competition? Ans. A perfectly competitive firm faces a perfectly elastic demand curve. Short answer questions (3 or 4 marks) 11. What are the main features of prefect competition? Ans. Perfect competition has the following features: (a) There are a large number of buyers and sellers in the market. (b) Product is homogeneous (c) There is free entry and exit of firms. 12. What are the conditions for monopoly market? Ans. (a) There must be a single seller of the commodity. (b) No close substitute of the product of the firm is available. (c) There are barriers to entry. The barriers can be economic, institutional or artificial in nature. These barriers are so strong that they prevent entry of any firm except the one firm which is already in the field. 13. What are the main features of monopolistic competition? Ans. It is a market situation which has both the competitive elements and monopolistic elements. It has the following features : (a) There are a large number of sellers and buyers. (b) There is free entry and exit in the long run. ECONOMICS Q1-XII-34

47 (c) There is product differentiation i.e. each firm produces a brand that is unique and different from what other firm produces. 14. How is a firm under perfect competition a price-taker but the industry is a price-maker? On the other hand, the number of firms in the industry is so large that any individual firm, through its action, can not influence the market price. They have to take the price determined at the industry level as given. So, the firms are considered to be price takers. Under perfect competition, the price is determined by intersection of demand and supply curve of the industry as a whole. So, the industry is called the price maker. 15. Why is the shape of the demand curve under monopoly less elastic? Explain : Ans. (a) The demand curve facing a monopolist is downward sloping as he can expect to sell more by reducing the price. This is shown in the diagram. The monopolist sells OM quantity at OP price. If he wants to increase his sales by MM 1 he can do this by reducing price by PP 1, as a fall in price will cause an increase in quantity demanded. (b) The demand curve under monopoly is also very steep, that is, the demand curve DD in the diagram is in-elastic due to the absence of close substitutes. 16. Why is the shape of the demand curve under monopolistic competition more elastic? Explain : Ans. (a) The demand curve facing a producer under monopolistic competition is downward sloping as shown by the demand curve DD in the diagram. A producer in such a market can increase his sales by reducing his price. Quantity demanded i.e. sale can be increased by MM 1 if price is reduced by PP 1. (b) (c) The demand curve is more elastic as the differentiated products are close substitutes of each other. Number of firms is large. 17. Long answer questions (6 marks each) Ans. Differentiate between Perfect competition and monopolistic competition. ECONOMICS Q1-XII-35

48 Perfect Competition Monopolistic competition a) Infinitely large number of firms a) A large numbers of firms b) Homogeneous products b) Differentiated products c) Firms have no control over price. c) Firms have some control over price. d) Demand is infinitely elastic d) Demand is more elastic e) Demand curve (AR) is a straight line e) Demand curve is a flatter downward parallel to horizontal axis shown below showing greater elasticity f) P = MC at equilibrium point. f) P>MC at equilibrium point. g) No selling costs incurred g) Selling costs are important features in this competition. h) Price is lower than the price in h) Price is higher than competitive price due monopolistic competition. to the monopoly element. i) AR = MR i) AR>MR or MR<AR 18. Differentiate between monopoly and monopolistic competition. Monopolistic competition Monopoly a) There are a large number of sellers. a) There is a single seller. b) There is product differentiation, products b) Unique products with no close are close substitutes for each other. substitutes. c) Price elasticity of demand is more c) Price elasticity of demand is less. d) Firms have some control over price. d) Monopolist has considerable control over price. e) Presence of selling cost is an important e) No selling cost as there is no feature. competition. f) Free entry and exit of the firm f) Barriers to entry of a new firm g) Price discrimination can not be followed. g) Price discrimination may be followed under certain conditions. 19. Explain the relationship between TR and MR under monopoly with the help of a schedule and diagram : Ans. TR increases as long as MR is positive. TR is maximum when MR = O TR decreases as MR is negative. Table Output Price TR MR (in units) (in Rs.) (in Rs.) (in Rs.) ECONOMICS Q1-XII-36

49 If we plot the above schedule on the graph paper we obtain the TR and MR curves. The TR curve is inverse U-shaped because the monopolist can sell more by reducing the price. So, the TR first increases with output and then it decreases. Thus, the shape of the TR curve is different under monopoly, than the one under a competitive firm SIMPLE APPLICATION TOOLS Price Ceiling:- means maximum price of a commodity fixed by the government that the sellers can charge from the buyers. It is imposed on necessary commodities like wheat, rice, kerosene, oil, sugar etc. Price ceiling results in excess demand and less supply in the market. It is below the equilibrium price.the shortage of commodity in the market results in following implications a) Emergence of black market b) Rationing Price Floor (minimum support Price) :- it is fixed by the government necessarily above the equilibrium price. Sometimes when government feels that the price for a particular good or service should not fall below certain level and sets a floor or a minimum price for these goods and services Example: - Imposition of support price on agricultural commodities in case of requirement the government fixes the support price above the equilibrium price. Price floor results in excess supply and less demand Part - B I ntroductory M acro Economics Capsules UNIT V National I ncome and Related aggregates A: Basic concepts: 1. National Income(NNP FC ) : N.I. is the sum of domestic factor income (NDP FC ) and net factor income from abroad (NFIA). MARKS 10 ECONOMICS Q1-XII-37

50 2. Closed Economy : An Economy which does not have economic relations with other countries. 3. Open Economy : An Economy which has economic relations with other countries. 4. Final Goods : All goods which are meant either for consumption or for investment. 5. Net Domestic product : It is the gross domestic product less consumption of fixed capital. 6. Accounting period : An accounting year or a financial year often does not coincide with a calendar year. It covers the period from 1 st April of the present year up to 31 st March of the next year 7. Nominal GNP : GNP measured in terms of current market prices. 8. Real GNP : GNP computed as per constant prices. 9. Real Flow : The flow of income in terms of goods and services. 10. Money Flow : The flow of income in terms of money. B: Question- Answers Very short answer-questions (1 mark) 1. Define National income at current prices? Ans. N.I. at current prices is the money value of final goods and services estimated at current prices produced by normal residents during an accounting year. 2. Define factor income? Ans. Income earned by a factor of production i.e. in form of Rent, wages, interest and profit, in the process of production. 3. What is the name of income earned from property and entrepreneurship? Ans. Operating surplus. 4. What are the components of profit. Ans. (i) Undistributed profit, (ii) corporation tax, (iii) dividends. 5. Define personal Income? Ans. It is defined as current income of persons or household from all sources. 6. Define personal disposable income. Ans. It is that part of the personal income which is available to the households for expenditure 7. What is meant by double counting? Ans. Double counting means counting the value of the commodity more than once. 8. What is meant by Net indirect taxes? Ans. Net indirect taxes is the difference between indirect taxes and economic subsidies. 9. What are the main components of operating surplus? Ans. (i) Rent (ii) Interest (iii) Profit 10. Who prepares the National Income estimates of the country? Ans. Central Statistical Organization (C. S. O.) 11. What is added to domestic factor income to obtain national income? Ans. Net factor income from abroad is added to domestic factor income to obtain national income. 12. What is final consumption expenditure? Ans. Expenditure incurred on final goods and services is called final expenditure. ECONOMICS Q1-XII-38