Chapter 6: Prices Section 1

|

|

|

- Sheila Sims

- 6 years ago

- Views:

Transcription

1 Chapter 6: Prices Section 1

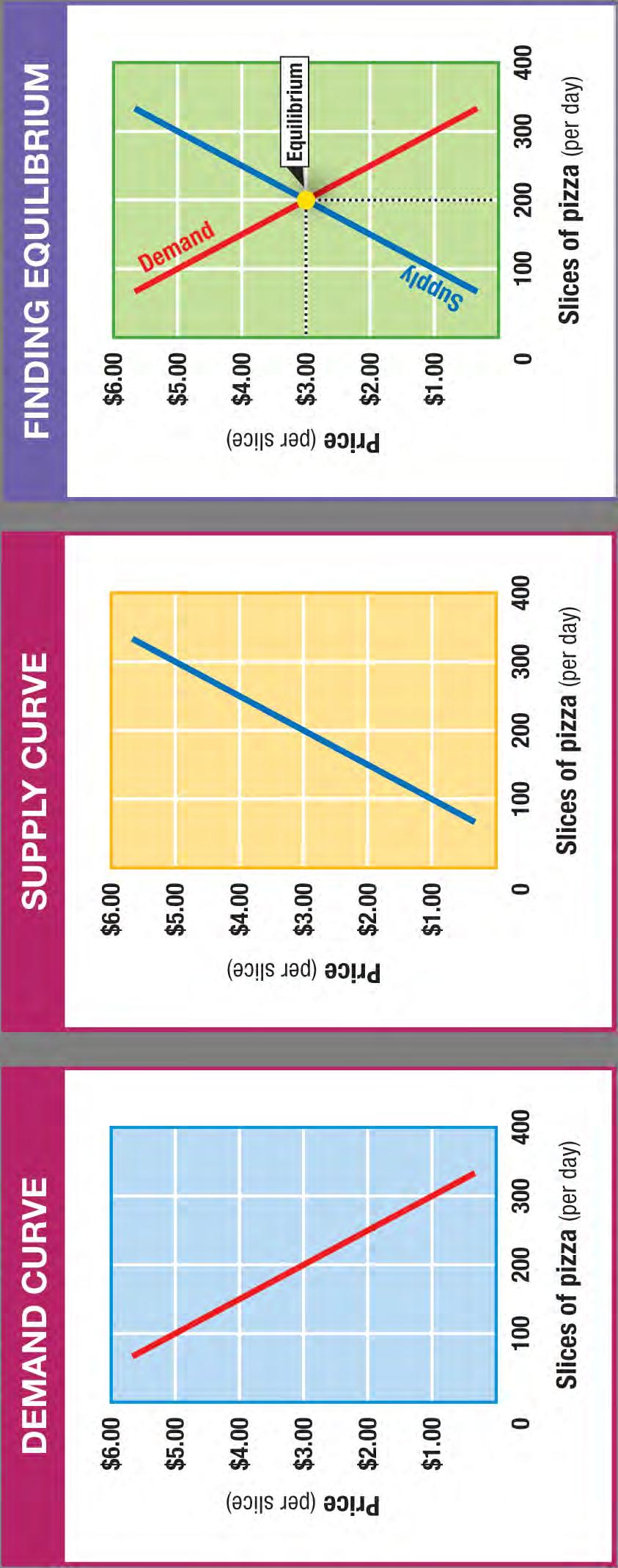

2 Key Terms equilibrium: the point at which the demand for a product or service is equal to the supply of that product or service disequilibrium: any price or quantity not at equilibrium shortage: when quantity demanded is more than quantity supplied surplus: when quantity supplied is more than quantity demanded

3 Key Terms, cont. price ceiling: a maximum price that can legally be charged for a good or service rent control: a price ceiling placed on apartment rent price floor: a minimum price for a good or service minimum wage: a minimum price that an employer can pay a worker for one hour of labor

4 Introduction What factors affect price? Prices are affected by the laws of supply and demand. They are also affected by actions of the government. Often times the government will intervene to set a minimum or maximum price for a good or service.

5 What is Equilibrium?

6 Equilibrium In order to find the equilibrium price and quantity, you can use supply and demand schedules. When a market is at equilibrium, both buyers and sellers benefit. How many slices are sold at equilibrium?

7 Disequilibrium Checkpoint: What market condition might cause a pizzeria owner to throw out many slices of pizza at the end of the day? If the market price or quantity supplied is anywhere but at equilibrium, the market is said to be at disequilibrium. Disequilibrium can produce two possible outcomes: Shortage A shortage causes prices to rise as the demand for a good is greater than the supply of that good. Surplus A surplus causes a drop in prices as the supply for a good is greater than the demand for that good.

8 Shortage and Surplus Shortage and surplus both lead to a market with fewer sales than at equilibrium. How much is the shortage when pizza is sold at $2.00 per slice?

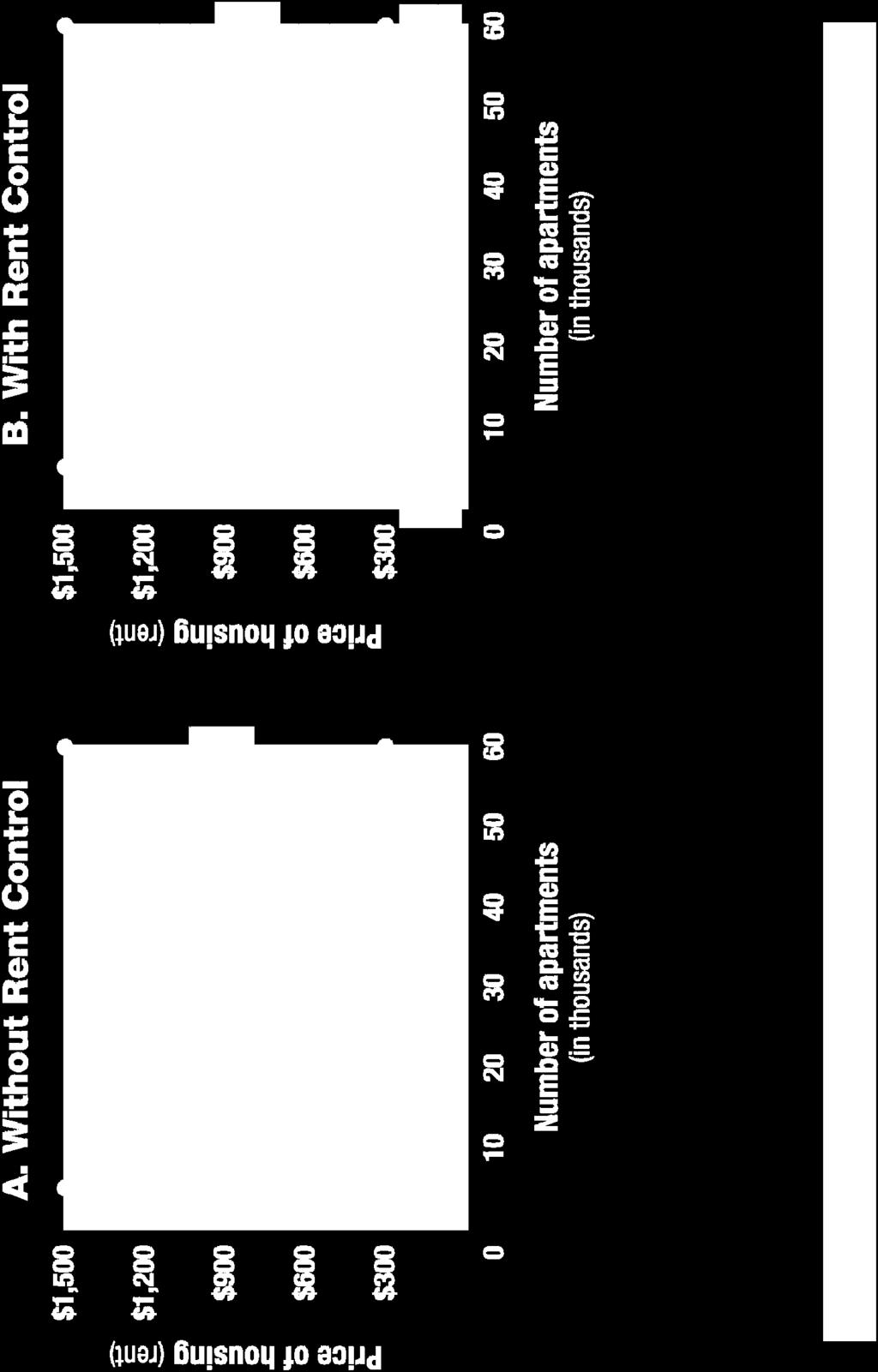

9 Price Ceiling While markets tend toward equilibrium on their own, sometimes the government intervenes and sets market prices. Price ceilings are one way the government controls prices. Rent Control Sets a price ceiling on apartment rent Prevents inflation during housing crises Helps the poor cut their housing costs Can lead to poorly managed buildings because landlords cannot afford the upkeep.

10 The Effects of Rent Control

11 Price Floors A price floor is a minimum price set by the government. The minimum wage is an example of a price floor. Minimum wage affects the demand and the supply of workers. At what wage is the labor market at equilibrium?

12 Price Supports in Agriculture Price supports in agriculture are another example of a price floor. They began during the Great Depression to create demand for crops. Opponents of price supports argue that the regulations dictate to farmers what they should produce. Supporters say that without government intervention, farmers would overproduce.

13 Chapter 6: Prices Section 2

14 Key Terms inventory: the quantity of goods that a firm has on hand fad: a product that is popular for a short period of time search costs: the financial and opportunity costs that consumers pay when searching for a good or service

15 Equilibrium When a market is in disequilibrium, it experiences either shortages or surpluses, both of which will eventually lead the market back toward equilibrium. Shortages cause a firm to raise its prices. Higher prices cause the quantity supplied to rise and the quantity demanded to fall until the two values are equal again. The same holds true for a surplus, only in reverse: Surpluses cause a firm to drop its prices. Lower prices cause the quantity supplied to fall and the quantity demanded to rise until equilibrium is restored.

16 Increase in Supply A shift in the supply curve will change the equilibrium price and quantity. As supply increases, it will cause the market to move toward a new equilibrium price. An example of a product that saw a radical market change in recent years is the digital camera.

17 Falling Prices and the Supply Curve

18 Changes in Supply Checkpoint: What happens to the equilibrium price when the supply curve shifts to the right? An increase in supply shifts the supply curve to the right. This shift throws the market into disequilibrium. Something will have to change in order to bring the market back to equilibrium.

19 A Moving Target Equilibrium for most products is in constant motion. Think of equilibrium as a moving target that changes as market conditions change. As supply or demand increases or decreases, a new equilibrium is created for that product.

20 Decrease in Supply Some factors lead to a decrease in supply, which shifts the supply curve to the left and results in a higher market price and a decrease in quantity sold. These factors include: An increase in the costs of resources to produce a good An increase in labor costs An increase in government regulations

21 A Change in Demand: Fads Fads often lead to an increase in demand for a particular good. The sudden increase in market demand cause the demand curve to shift to the right. What impact did the change in demand shown in the graph have on the equilibrium price?

22 Fads and Shortages As a result of fads, shortages appear to customers in different forms: Empty shelves at the stores Long lines to buy a product in short supply Search costs, such as driving to multiple stores to find a product.

23 Reaching a New Equilibrium Checkpoint: How is equilibrium reached after a shortage? Eventually, the increase in demand for a particular good will push the product to a new equilibrium price and quantity. Once a fad reaches its peak, though, prices will drop as quickly as they rose: A shortage becomes a surplus, causing the demand curve to shift to the left and restoring the original price and quantity supplied. New technology can also lead to a decrease in consumer demand for one product as a more high-tech substitute becomes available.

24 Chapter 6: Prices Section 3

25 Key Terms supply shock: a sudden shortage of a good rationing: a system of allocating scarce goods and services using criteria other than price black market: a market in which goods are sold illegally, without regard for government controls on price quantity

26 Introduction What roles do prices play in a free market economy? In a free market economy, prices are used to distribute goods and resources throughout the economy. Prices play other roles, including: Serving as a language for buyers and sellers Serving as an incentive for producers Serving as a signal of economic conditions

27 Price as an Incentive Prices provide a standard of measure of value throughout the world. Prices act as a signal that tells producers and consumers how to adjust. Prices tell buyers and sellers whether goods are in short supply or readily available. The price system is flexible and free, and it allows for a wide diversity of goods and services.

28 Prices as a Signal Prices can act as a signal to both producers and consumers: A high price tells producers that a product is in demand and they should make more. A low price indicates to producers that a good is being overproduced. A high price tells consumers to think about their purchases more carefully. A low price indicates to consumers to buy more of the product.

29 Flexibility of Prices Prices are flexible, which means they can be increased to solve problems of shortage and decreased to solve problems of surplus. Raising prices is one of the quickest ways to solve a shortage. It reduces quantity demanded and only people who have enough money will be able to pay the higher prices. This will cause the market to settle at a new equilibrium.

30 Free Market v. Command Free market systems based on prices cost nothing to administer. Central planning, on the other hand, requires a number of people to decide how resources are distributed, such as in the former Soviet Union. Unlike central planning, free market pricing is based on decisions made by consumers and suppliers.

31 Consumer Choices In a free market economy, prices help consumers choose among similar products and allow producers to target their customers with the products the customers want most. In a command economy, production is restricted to a few varieties of each product. As a result, there are fewer consumer choices.

32 Rationing & the Black Market In a command economy, or in a free market economy during wartime, shortages are common. One response to shortages is rationing. Since the government cannot track all of the goods passing through the economy, people sometimes conduct business on the illegal black market in order to bypass rationing.

33 Rationing During WWII During World War II, the federal government used rationing to control shortages. Each family was given tickets for such items as butter, sugar, or shoes. If you used up your allotment, you could not legally buy these items again until new tickets were issued.

34 Efficient Resource Allocation The free market system allows for efficient resource allocation, which means that the factors of production will be used for their most valuable purposes. Efficient resource allocation works with the profit incentive. Producers will use the resources available to them to ensure the greatest amount of profit.

35 The Profit Incentive In The Wealth of Nations, Adam Smith wrote that businesses do best when they provide what people need. Financial rewards motivate people. How have you provided or benefited from the profit incentive?

36 Market Problems Checkpoint: Under what circumstances may the free market system fail to allocate resources efficiently? Imperfect Competition Can affect prices, which in turn affect consumer decisions Negative Externalities Side effects of production, which include unintended costs Imperfect Information Prevents a market from operating smoothly

Chapter 6:3: The Role of Prices

Chapter 6:3: The Role of Prices In this section, we will see how prices affect consumer behavior and how producers respond. 1Co_6:20 For ye are bought with a price: therefore glorify God in your body,

Chapter 6:3: The Role of Prices In this section, we will see how prices affect consumer behavior and how producers respond. 1Co_6:20 For ye are bought with a price: therefore glorify God in your body,

Chapter 6: Combining Supply and Demand

SCHS SOCIAL STUDIES What you need to know UNIT TWO 1. Explain how supply and demand create balance in the marketplace 2. Explain how a market reacts to a fall in supply by moving to a new equilibrium 3.

SCHS SOCIAL STUDIES What you need to know UNIT TWO 1. Explain how supply and demand create balance in the marketplace 2. Explain how a market reacts to a fall in supply by moving to a new equilibrium 3.

Price = The Interaction of Supply and Demand WEDNESDAY, FEBRUARY 17 THURSDAY, FEBRUARY 18

Price = The Interaction of Supply and Demand WEDNESDAY, FEBRUARY 17 THURSDAY, FEBRUARY 18 Chapter 4: Section 1 Understanding Demand What Is Demand? Markets are where people come together to buy and sell

Price = The Interaction of Supply and Demand WEDNESDAY, FEBRUARY 17 THURSDAY, FEBRUARY 18 Chapter 4: Section 1 Understanding Demand What Is Demand? Markets are where people come together to buy and sell

Chapter 5: Supply Section 1

Chapter 5: Supply Section 1 Key Terms supply: the amount of goods available law of supply: producers offer more of a good as its price increases and less as its price falls quantity supplied: the amount

Chapter 5: Supply Section 1 Key Terms supply: the amount of goods available law of supply: producers offer more of a good as its price increases and less as its price falls quantity supplied: the amount

Multiple Choice Identify the letter of the choice that best completes the statement or answers the question.

Final day 2 Multiple Choice Identify the letter of the choice that best completes the statement or answers the question. 1. What determines how a change in prices will affect total revenue for a company?

Final day 2 Multiple Choice Identify the letter of the choice that best completes the statement or answers the question. 1. What determines how a change in prices will affect total revenue for a company?

Name & Block: Word Definition Provide an Example (Must be a sentence) Demand (79)

Demand (79)") Name & Block: Economics: Unit Two Study Guide Standards: SSEMI2 Explain how the law of demand, the law of supply, and prices work to determine production and distribution in a market economy. a. Define

Name & Block: Economics: Unit Two Study Guide Standards: SSEMI2 Explain how the law of demand, the law of supply, and prices work to determine production and distribution in a market economy. a. Define

Eastern Mediterranean University Faculty of Business and Economics Department of Economics Spring Semester

Eastern Mediterranean University Faculty of Business and Economics Department of Economics 2015 16 Spring Semester ECON101 Introduction to Economics I First Midterm Exam Duration: 90 minutes Answer Key

Eastern Mediterranean University Faculty of Business and Economics Department of Economics 2015 16 Spring Semester ECON101 Introduction to Economics I First Midterm Exam Duration: 90 minutes Answer Key

Edexcel (B) Economics A-level

Economics A-level") Edexcel (B) Economics A-level Theme 1: Markets, Consumers and Firms 1.3 Introducing the Market 1.3.3 Price determination Notes Equilibrium price and quantity and how they are determined This is when supply

Edexcel (B) Economics A-level Theme 1: Markets, Consumers and Firms 1.3 Introducing the Market 1.3.3 Price determination Notes Equilibrium price and quantity and how they are determined This is when supply

Curriculum Standard One: The students will understand common economic terms and concepts and economic reasoning.

Curriculum Standard One: The students will understand common economic terms and concepts and economic reasoning. *1. The students will examine the causal relationship between scarcity and the need for

Curriculum Standard One: The students will understand common economic terms and concepts and economic reasoning. *1. The students will examine the causal relationship between scarcity and the need for

In Section 1, you read how supply and

Preview Objectives After studying this section you will be able to: 1. Analyze the role of prices in a free market. 2. List the advantages of a price-based system. 3. Explain how a price-based system leads

Preview Objectives After studying this section you will be able to: 1. Analyze the role of prices in a free market. 2. List the advantages of a price-based system. 3. Explain how a price-based system leads

Market Equilibrium, the Price Mechanism and Market Efficiency. Chapter 3

Market Equilibrium, the Price Mechanism and Market Efficiency Chapter 3 Equilibrium Equilibrium is defined as a state of rest, self-perpetuating in the absence of any outside disturbance. Example: a book

Market Equilibrium, the Price Mechanism and Market Efficiency Chapter 3 Equilibrium Equilibrium is defined as a state of rest, self-perpetuating in the absence of any outside disturbance. Example: a book

1. Demand: willingness to buy a good or service and the ability to pay for it; how much of an item an individual is willing to purchase at each price

1. Demand: willingness to buy a good or service and the ability to pay for it; how much of an item an individual is willing to purchase at each price 2. The two things needed for demand to exist are: willingness

1. Demand: willingness to buy a good or service and the ability to pay for it; how much of an item an individual is willing to purchase at each price 2. The two things needed for demand to exist are: willingness

IB Economics Competitive Markets: Demand and Supply 1.4: Price Signals and Market Efficiency

IB Economics: www.ibdeconomics.com 1.4 PRICE SIGNALS AND MARKET EFFICIENCY: STUDENT LEARNING ACTIVITY Answer the questions that follow. 1. DEFINITIONS Define the following terms: [10 marks] Allocative

IB Economics: www.ibdeconomics.com 1.4 PRICE SIGNALS AND MARKET EFFICIENCY: STUDENT LEARNING ACTIVITY Answer the questions that follow. 1. DEFINITIONS Define the following terms: [10 marks] Allocative

Unit I The Principles of Economics

Economics Chapters 1-2 & 4-6 Duke Chapter 1 Unit I The Principles of Economics Explain the difference between a need and a want. Explain the difference between goods and services. Scarcity - Find three

Economics Chapters 1-2 & 4-6 Duke Chapter 1 Unit I The Principles of Economics Explain the difference between a need and a want. Explain the difference between goods and services. Scarcity - Find three

- Scarcity leads to tradeoffs - Normative statements=opinion - Positive statement=fact with evidence - An economic model is tested by comparing its

Macroeconomics Final Notes: CHAPTER 1: What is economics? We want more than we can get. Our inability to satisfy all of our wants is called scarcity. All resources are finite even if they are abundant.

Macroeconomics Final Notes: CHAPTER 1: What is economics? We want more than we can get. Our inability to satisfy all of our wants is called scarcity. All resources are finite even if they are abundant.

Market Equilibrium: Part II

Market Equilibrium: Part II Announcements PS #4 is posted on web page. It is big and not all questions are very easy. It is time to start studying. PS#5 will be even bigger. (also more challenging) A sample

Market Equilibrium: Part II Announcements PS #4 is posted on web page. It is big and not all questions are very easy. It is time to start studying. PS#5 will be even bigger. (also more challenging) A sample

Chapter 1: The Ten Lessons in Economics

Textbook Notes Page 1 Chapter 1: The Ten Lessons in Economics Saturday, 25 May 2013 1:09 PM Economics: The study of how society manages its scarce resources Individual Decision-Making Lesson 1: People

Textbook Notes Page 1 Chapter 1: The Ten Lessons in Economics Saturday, 25 May 2013 1:09 PM Economics: The study of how society manages its scarce resources Individual Decision-Making Lesson 1: People

Chapter 2: Economic Systems Section 2

Chapter 2: Economic Systems Section 2 Objectives 1. Explain why markets exist. E3, 5, 9 2. Analyze a circular flow model of a free market economy. E6, 3. Describe the self-regulating nature of the marketplace.

Chapter 2: Economic Systems Section 2 Objectives 1. Explain why markets exist. E3, 5, 9 2. Analyze a circular flow model of a free market economy. E6, 3. Describe the self-regulating nature of the marketplace.

Supply, Demand, and Government Policies. Copyright 2004 South-Western

Supply, Demand, and Government Policies Copyright 2004 South-Western Supply, Demand, and Government Policies In a free, unregulated market system, market forces establish equilibrium prices and exchange

Supply, Demand, and Government Policies Copyright 2004 South-Western Supply, Demand, and Government Policies In a free, unregulated market system, market forces establish equilibrium prices and exchange

Efficiency and Fairness of Markets

Efficiency and Fairness of Markets Chapter 6 CHAPTER IN PERSPECTIVE In Chapter 6 we study the equilibrium quantities of goods, services, and factors of production to determine if markets are efficient.

Efficiency and Fairness of Markets Chapter 6 CHAPTER IN PERSPECTIVE In Chapter 6 we study the equilibrium quantities of goods, services, and factors of production to determine if markets are efficient.

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

HW 2 - Micro - Machiorlatti MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) What is measured by the price elasticity of supply? 1) A) The price

HW 2 - Micro - Machiorlatti MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) What is measured by the price elasticity of supply? 1) A) The price

8/31/09. Understanding economic resources and economic systems is essential to lessening economic problems.

Chapter 2 Economic Resources and Systems pp. 18-33 Back to Table of Contents Introduction to Business, Economic Resources and Systems Slide 2 of 64 Understanding economic resources and economic systems

Chapter 2 Economic Resources and Systems pp. 18-33 Back to Table of Contents Introduction to Business, Economic Resources and Systems Slide 2 of 64 Understanding economic resources and economic systems

1 Ten Principles of Economics CHAPTER 1 TEN PRINCIPLES OF ECONOMICS 0

1 Ten Principles of Economics CHAPTER 1 TEN PRINCIPLES OF ECONOMICS 0 In this chapter, look for the answers to these questions: What kinds of questions does economics address? What are the principles of

1 Ten Principles of Economics CHAPTER 1 TEN PRINCIPLES OF ECONOMICS 0 In this chapter, look for the answers to these questions: What kinds of questions does economics address? What are the principles of

PowerPoint to accompany

PowerPoint to accompany Chapter 2 Markets, Demand and Supply Learning Objectives 2.1 Economic systems How do countries differ in the way their economies are organised? 2.2 Demand How much will people buy

PowerPoint to accompany Chapter 2 Markets, Demand and Supply Learning Objectives 2.1 Economic systems How do countries differ in the way their economies are organised? 2.2 Demand How much will people buy

CHAPTER THREE DEMAND AND SUPPLY

CHAPTER THREE DEMAND AND SUPPLY This chapter presents a brief review of demand and supply analysis. The materials covered in this chapter provide the essential background for most of the managerial economic

CHAPTER THREE DEMAND AND SUPPLY This chapter presents a brief review of demand and supply analysis. The materials covered in this chapter provide the essential background for most of the managerial economic

Supply, demand and government policies. Dr. Anna Kowalska-Pyzalska

Supply, demand and government policies Dr. Anna Kowalska-Pyzalska Price ceiling Price floor Tax incidence In a free, unregulated market system, market forces establish equilibrium prices and exchange quantities.

Supply, demand and government policies Dr. Anna Kowalska-Pyzalska Price ceiling Price floor Tax incidence In a free, unregulated market system, market forces establish equilibrium prices and exchange quantities.

CCC (ECO 231) Exam pts. (+ 5 built-in bonus) J. Payne PLEASE DO NOT MARK ON THIS EXAM FORM.

Exam pts. (+ 5 built-in bonus) J. Payne PLEASE DO NOT MARK ON THIS EXAM FORM.") CCC (ECO 231) Exam 1 100 pts. (+ 5 built-in bonus) J. Payne PLEASE DO NOT MARK ON THIS EXAM FORM. BEFORE YOU BEGIN: Using a PENCIL, IN THE BLUE BOX on the Accuscan 100AS answer form, please write: your

CCC (ECO 231) Exam 1 100 pts. (+ 5 built-in bonus) J. Payne PLEASE DO NOT MARK ON THIS EXAM FORM. BEFORE YOU BEGIN: Using a PENCIL, IN THE BLUE BOX on the Accuscan 100AS answer form, please write: your

OCR Economics A-level

OCR Economics A-level Microeconomics Topic 2: How Competitive Markets Work 2.3 Supply and demand, and the interaction of markets Notes A market is created when buyers and sellers interact. A sub-market

OCR Economics A-level Microeconomics Topic 2: How Competitive Markets Work 2.3 Supply and demand, and the interaction of markets Notes A market is created when buyers and sellers interact. A sub-market

2. Which of the following is a distinguishing feature of a market system? A. public ownership of all capital.

Practice Test Chapter 2 1. Which of the following is a distinguishing feature of a command system? A. private ownership of all capital. B. central planning. C. heavy reliance on markets. D. wide-spread

Practice Test Chapter 2 1. Which of the following is a distinguishing feature of a command system? A. private ownership of all capital. B. central planning. C. heavy reliance on markets. D. wide-spread

Ten Principles of Economics. Chapter 1

Ten Principles of Economics Chapter 1 Economy...... The word economy comes from a Greek word for one who manages a household. A household and an economy face many decisions: Who will work? What goods and

Ten Principles of Economics Chapter 1 Economy...... The word economy comes from a Greek word for one who manages a household. A household and an economy face many decisions: Who will work? What goods and

Chapter 5: Supply Section 3

Chapter 5: Supply Section 3 Objectives 1. Explain how factors such as input costs create changes in supply. 2. Identify three ways that the government can influence the supply of goods. 3. Analyze other

Chapter 5: Supply Section 3 Objectives 1. Explain how factors such as input costs create changes in supply. 2. Identify three ways that the government can influence the supply of goods. 3. Analyze other

Supply and Demand. Price and Quantity. Demand. The Law of Demand. Coach Burnett AP Macroeconomics

upply and emand Coach Burnett A Macroeconomics 1 rice and uantity rice - the amount of money paid for an economic good/service. Ex. A gallon of gas is roughly $3.00 a gallon (national average) OUCH!!!

upply and emand Coach Burnett A Macroeconomics 1 rice and uantity rice - the amount of money paid for an economic good/service. Ex. A gallon of gas is roughly $3.00 a gallon (national average) OUCH!!!

Econ 101, sections 2 and 6, S06 Schroeter Exam #2, Red. Choose the single best answer for each question.

Econ 101, sections 2 and 6, S06 Schroeter Exam #2, Red Choose the single best answer for each question. 1. If the own-price elasticity of demand for a good is -2.0, this implies that consumers would a.

Econ 101, sections 2 and 6, S06 Schroeter Exam #2, Red Choose the single best answer for each question. 1. If the own-price elasticity of demand for a good is -2.0, this implies that consumers would a.

C. many buyers and many sellers C. Sue will likely purchase more than one bottle of shampoo. B. cause the demand for mangos to shift to the right

Multiple Choice 1. Competitive markets are characterized as having A. many buyers and a single seller B. many buyers and a few sellers. C. many buyers and many sellers D. a few buyers and many sellers

Multiple Choice 1. Competitive markets are characterized as having A. many buyers and a single seller B. many buyers and a few sellers. C. many buyers and many sellers D. a few buyers and many sellers

After studying this chapter you will be able to

3 Demand and Supply After studying this chapter you will be able to Describe a competitive market and think about a price as an opportunity cost Explain the influences on demand Explain the influences

3 Demand and Supply After studying this chapter you will be able to Describe a competitive market and think about a price as an opportunity cost Explain the influences on demand Explain the influences

Supply and Demand. Objective 8.04

Supply and Demand Objective 8.04 Supply and Demand Pages 258-259 259 copy bold terms and give a definition or description of each. Page 261 Copy the questions Worksheet A-2A 1. Surplus When the amount

Supply and Demand Objective 8.04 Supply and Demand Pages 258-259 259 copy bold terms and give a definition or description of each. Page 261 Copy the questions Worksheet A-2A 1. Surplus When the amount

Chapter 1: Ten Principles of Economics Principles of Economics, 8 th Edition N. Gregory Mankiw Page 1

Page 1 I. Introduction A. Use the margins in your book for note keeping. B. My comments in these chapter summaries are in italics. C. For testing purposes, you are responsible for material covered in the

Page 1 I. Introduction A. Use the margins in your book for note keeping. B. My comments in these chapter summaries are in italics. C. For testing purposes, you are responsible for material covered in the

TEN PRINCIPLES OF ECONOMICS. The word Economy... An individual economic agent faces many decisions: Intro Macroeconomic Theory Professor Minseong Kim

TEN PRINCIPLES OF ECONOMICS Chapter 1 The word Economy... Comes from a Greek word for one who manages a household. An individual economic agent faces many decisions: Should I go to college or should I

TEN PRINCIPLES OF ECONOMICS Chapter 1 The word Economy... Comes from a Greek word for one who manages a household. An individual economic agent faces many decisions: Should I go to college or should I

CHAPTER 2 ECONOMIC SYSTEMS, RESOURCE ALLOCATION, AND SOCIAL WELL-BEING: LESSONS FROM CHINA'S TRANSITION

CHAPTER 2 ECONOMIC SYSTEMS, RESOURCE ALLOCATION, AND SOCIAL WELL-BEING: LESSONS FROM CHINA'S TRANSITION LESSONS FROM CHINA S TRANSITION The transition of China s economy from centralized planning to a

CHAPTER 2 ECONOMIC SYSTEMS, RESOURCE ALLOCATION, AND SOCIAL WELL-BEING: LESSONS FROM CHINA'S TRANSITION LESSONS FROM CHINA S TRANSITION The transition of China s economy from centralized planning to a

Applications of supply and demand

Applications of supply and demand Comparative statics and government policy Comparative statics The simple supply and demand model we have developed can be used to analyze the effects of many events on

Applications of supply and demand Comparative statics and government policy Comparative statics The simple supply and demand model we have developed can be used to analyze the effects of many events on

Ten Principles of Economics

C H A P T E R 1 Ten Principles of Economics Economics P R I N C I P L E S O F N. Gregory Mankiw Premium PowerPoint Slides by Ron Cronovich 2009 South-Western, a part of Cengage Learning, all rights reserved

C H A P T E R 1 Ten Principles of Economics Economics P R I N C I P L E S O F N. Gregory Mankiw Premium PowerPoint Slides by Ron Cronovich 2009 South-Western, a part of Cengage Learning, all rights reserved

Competitive Markets: Applications

7784d_c10_409-461 5/23/01 6:48 AM Page 409 10 C H A P T E R Competitive Markets: Applications 10.1 THE INVISIBLE HAND 10.2 IMPACT OF AN EXCISE TAX Incidence of a Tax EXAMPLE 10.1 Gasoline Taxes 10.3 SUBSIDIES

7784d_c10_409-461 5/23/01 6:48 AM Page 409 10 C H A P T E R Competitive Markets: Applications 10.1 THE INVISIBLE HAND 10.2 IMPACT OF AN EXCISE TAX Incidence of a Tax EXAMPLE 10.1 Gasoline Taxes 10.3 SUBSIDIES

MICRO TEST 1: Economics. Economizing Problem. Resources (Inputs) Capitalism. Market. Law of Demand. Law of Supply. Equilibrium.

Capitalism. Market. Law of Demand. Law of Supply. Equilibrium.") MICRO TEST 1: Economics Economizing Problem Resources (Inputs) Capitalism Market Law of Demand Law of Equilibrium Price Mechanism Surplus Shortage Change in Quantity Demanded Change in Demand Change in

MICRO TEST 1: Economics Economizing Problem Resources (Inputs) Capitalism Market Law of Demand Law of Equilibrium Price Mechanism Surplus Shortage Change in Quantity Demanded Change in Demand Change in

MACRO TEST 1: Economics. Economizing Problem. Resources (Inputs) Production Possibilities Curve (Transformation Curve) Full Production

Production Possibilities Curve (Transformation Curve) Full Production") MACRO TEST 1: Economics Economizing Problem Resources (Inputs) Production Possibilities Curve (Transformation Curve) Full Production Law of Increasing Costs Division of Labor (Specialization) Capital Intensive

MACRO TEST 1: Economics Economizing Problem Resources (Inputs) Production Possibilities Curve (Transformation Curve) Full Production Law of Increasing Costs Division of Labor (Specialization) Capital Intensive

EC 201 Lecture Notes 1 Page 1 of 1

EC 201 Lecture Notes 1 Page 1 of 1 ECON 201 - Macroeconomics Lecture Notes 1 Metropolitan State University Allen Bellas The textbooks for this course are Macroeconomics: Principles and Policy by William

EC 201 Lecture Notes 1 Page 1 of 1 ECON 201 - Macroeconomics Lecture Notes 1 Metropolitan State University Allen Bellas The textbooks for this course are Macroeconomics: Principles and Policy by William

Chapter 4 DEMAND. Essential Question: How do we decide what to buy?

Chapter 4: Demand Section 1 Chapter 4 DEMAND Essential Question: How do we decide what to buy? Key Terms demand: the desire to own something and the ability to pay for it law of demand: consumers will

Chapter 4: Demand Section 1 Chapter 4 DEMAND Essential Question: How do we decide what to buy? Key Terms demand: the desire to own something and the ability to pay for it law of demand: consumers will

Ten Principles of Economics

Wojciech Gerson (1831-1901) Seventh Edition Principles of Economics N. Gregory Mankiw CHAPTER 1 Ten Principles of Economics In this chapter, look for the answers to these questions What kinds of questions

Wojciech Gerson (1831-1901) Seventh Edition Principles of Economics N. Gregory Mankiw CHAPTER 1 Ten Principles of Economics In this chapter, look for the answers to these questions What kinds of questions

CHAPTER 3 SUPPLY AND DEMAND: AN INITIAL LOOK

CHAPTER 3 SUPPLY AND DEMAND: AN INITIAL LOOK 1. This question is intended to help students develop an intuitive sense of the origins of the demand curve. If you deal with this question in class or discussion

CHAPTER 3 SUPPLY AND DEMAND: AN INITIAL LOOK 1. This question is intended to help students develop an intuitive sense of the origins of the demand curve. If you deal with this question in class or discussion

PLEASE PLACE YOUR ANSWER ON THE FRONT OF THE ATTACHED SCANNER SHEET

PART 1: MULTIPLE CHOICE -- 90 POINTS Choose the single best answer for the following 30 questions. PLEASE PLACE YOUR ANSWER ON THE FRONT OF THE ATTACHED SCANNER SHEET STARTING WITH NUMBER 1. Circle your

PART 1: MULTIPLE CHOICE -- 90 POINTS Choose the single best answer for the following 30 questions. PLEASE PLACE YOUR ANSWER ON THE FRONT OF THE ATTACHED SCANNER SHEET STARTING WITH NUMBER 1. Circle your

EOCT Test Semester 2 final

EOCT Test Semester 2 final 1. The best definition of Economics is a. The study of how individuals spend their money b. The study of resources and government c. The study of the allocation of scarce resources

EOCT Test Semester 2 final 1. The best definition of Economics is a. The study of how individuals spend their money b. The study of resources and government c. The study of the allocation of scarce resources

Demand, Supply, and Price

Demand, Supply, and Price The amount of a good or service that we demand, the amount of a good or service that suppliers supply, and the price of a good or service all affect one another. Let's examine

Demand, Supply, and Price The amount of a good or service that we demand, the amount of a good or service that suppliers supply, and the price of a good or service all affect one another. Let's examine

CHAPTER 2. Demand and Supply

CHAPTER 2 Demand and Supply The Supply_and_demand model A model for understanding the determination of the price of quantity of a good sold on the market Two groups: buyers and sellers Types of Competition

CHAPTER 2 Demand and Supply The Supply_and_demand model A model for understanding the determination of the price of quantity of a good sold on the market Two groups: buyers and sellers Types of Competition

AP Microeconomics Review With Answers

AP Microeconomics Review With Answers 1. Firm in Perfect Competition (Long-Run Equilibrium) 2. Monopoly Industry with comparison of price & output of a Perfectly Competitive Industry (which means show

AP Microeconomics Review With Answers 1. Firm in Perfect Competition (Long-Run Equilibrium) 2. Monopoly Industry with comparison of price & output of a Perfectly Competitive Industry (which means show

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. FIGURE 1-2

Questions of this SAMPLE exam were randomly chosen and may NOT be representative of the difficulty or focus of the actual examination. The professor did NOT review these questions. MULTIPLE CHOICE. Choose

Questions of this SAMPLE exam were randomly chosen and may NOT be representative of the difficulty or focus of the actual examination. The professor did NOT review these questions. MULTIPLE CHOICE. Choose

JANUARY EXAMINATIONS 2008

No. of Pages: (A) 9 No. of Questions: 38 EC1000A micro 2008 JANUARY EXAMINATIONS 2008 Subject Title of Paper ECONOMICS EC1000 MICROECONOMICS Time Allowed Two Hours (2 Hours) Instructions to candidates

No. of Pages: (A) 9 No. of Questions: 38 EC1000A micro 2008 JANUARY EXAMINATIONS 2008 Subject Title of Paper ECONOMICS EC1000 MICROECONOMICS Time Allowed Two Hours (2 Hours) Instructions to candidates

Exploring the World of Business and Economics

Chapter 1 Exploring the World of Business and Economics 1 Discuss what you must do to be successful in the world of business. 2 Define business and identify potential risks and rewards. 3 Define economics

Chapter 1 Exploring the World of Business and Economics 1 Discuss what you must do to be successful in the world of business. 2 Define business and identify potential risks and rewards. 3 Define economics

Supply and Demand. Chapter 3. McGraw-Hill/Irwin. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

Supply and Demand Chapter 3 McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Learning Objectives 1. Describe how the demand and supply curves summarize the behavior

Supply and Demand Chapter 3 McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Learning Objectives 1. Describe how the demand and supply curves summarize the behavior

Econ 101, section 3, F06 Schroeter Exam #2, Red. Choose the single best answer for each question.

Econ 101, section 3, F06 Schroeter Exam #2, Red Choose the single best answer for each question. 1. Which of the following is consistent with elastic demand? a. A 10% increase in price results in a 5%

Econ 101, section 3, F06 Schroeter Exam #2, Red Choose the single best answer for each question. 1. Which of the following is consistent with elastic demand? a. A 10% increase in price results in a 5%

Lecture 1: Introduction

Lecture 1: Introduction Yulei Luo SEF of HKU January 19, 2013 Luo, Y. (SEF of HKU) ECON1002C/D January 19, 2013 1 / 16 Economics, Microeconomics and Macroeconomics Economics: The study of the choices people

Lecture 1: Introduction Yulei Luo SEF of HKU January 19, 2013 Luo, Y. (SEF of HKU) ECON1002C/D January 19, 2013 1 / 16 Economics, Microeconomics and Macroeconomics Economics: The study of the choices people

Chapter 4: Demand Section 3

Chapter 4: Demand Section 3 Objectives 1. Explain how to calculate elasticity of demand. 2. Identify factors that effect elasticity. 3. Explain how firms use elasticity and revenue to make decisions. Copyright

Chapter 4: Demand Section 3 Objectives 1. Explain how to calculate elasticity of demand. 2. Identify factors that effect elasticity. 3. Explain how firms use elasticity and revenue to make decisions. Copyright

Econ Alive Study Guide

Econ Alive Study Guide Directions: After you put your Final Portfolio in order, go through it and using this Study Guide as a map, answer these questions to the best of your ability. If you find that you

Econ Alive Study Guide Directions: After you put your Final Portfolio in order, go through it and using this Study Guide as a map, answer these questions to the best of your ability. If you find that you

Boğaziçi University, Department of Economics Spring 2016 EC 102 PRINCIPLES of MACROECONOMICS MIDTERM I , Tuesday 11:00 Section 06 TYPE A

NAME: NO: SECTION: Boğaziçi University, Department of Economics Spring 2016 EC 102 PRINCIPLES of MACROECONOMICS MIDTERM I 15.03.2016, Tuesday 11:00 Section 06 TYPE A Do not forget to write your full name,

NAME: NO: SECTION: Boğaziçi University, Department of Economics Spring 2016 EC 102 PRINCIPLES of MACROECONOMICS MIDTERM I 15.03.2016, Tuesday 11:00 Section 06 TYPE A Do not forget to write your full name,

Section 1.2 Introduction to Economics

Section 1.2 Introduction to Economics Economics Economics is a science that examines how goods and services are produced, sold, and used All economic resources are limited; needs and wants are unlimited

Section 1.2 Introduction to Economics Economics Economics is a science that examines how goods and services are produced, sold, and used All economic resources are limited; needs and wants are unlimited

Section I (20 questions; 1 mark each)

") Foundation Course in Managerial Economics- Solution Set- 1 Final Examination Marks- 100 Section I (20 questions; 1 mark each) 1. Which of the following statements is not true? a. Societies face an important

Foundation Course in Managerial Economics- Solution Set- 1 Final Examination Marks- 100 Section I (20 questions; 1 mark each) 1. Which of the following statements is not true? a. Societies face an important

Downloaded for free from 1

Micro Chapter 6 -price ceiling or price cap: government regulation that makes it illegal to charge a price higher then a specified level -effects of the price cap on the market depend on whether the ceiling

Micro Chapter 6 -price ceiling or price cap: government regulation that makes it illegal to charge a price higher then a specified level -effects of the price cap on the market depend on whether the ceiling

Chapter 1: What is Economics? Section 3

Chapter 1: What is Economics? Section 3 Objectives 1. Interpret a production possibilities curve. 2. Explain how production possibilities curves show efficiency, growth, and cost. 3. Explain why a country

Chapter 1: What is Economics? Section 3 Objectives 1. Interpret a production possibilities curve. 2. Explain how production possibilities curves show efficiency, growth, and cost. 3. Explain why a country

ECON 200 Homework 3 Answer Key

ECON 200 Homework 3 Answer Key Due Monday 4/26/10 1. Because of the baby boom, there are more people in the U.S. between the age of 40 and 66 than any other age group. There is concern about what is going

ECON 200 Homework 3 Answer Key Due Monday 4/26/10 1. Because of the baby boom, there are more people in the U.S. between the age of 40 and 66 than any other age group. There is concern about what is going

Economics: Core Concepts Part II

Economics: Core Concepts Part II When everybody else is better off, they can buy more, they strengthen demand, strengthen the market, strengthen the country. -Carlos Slim Helu The production possibilities

Economics: Core Concepts Part II When everybody else is better off, they can buy more, they strengthen demand, strengthen the market, strengthen the country. -Carlos Slim Helu The production possibilities

Managerial Economics Prof. Trupti Mishra S.J.M School of Management Indian Institute of Technology, Bombay. Lecture -29 Monopoly (Contd )

") Managerial Economics Prof. Trupti Mishra S.J.M School of Management Indian Institute of Technology, Bombay Lecture -29 Monopoly (Contd ) In today s session, we will continue our discussion on monopoly.

Managerial Economics Prof. Trupti Mishra S.J.M School of Management Indian Institute of Technology, Bombay Lecture -29 Monopoly (Contd ) In today s session, we will continue our discussion on monopoly.

Market System. and purchase goods & services to satisfy material wants

2 primary decision makers in market system: Market System Households (consumers) economic unit of one or more persons that provide resources and purchase goods & services to satisfy material wants Firms

2 primary decision makers in market system: Market System Households (consumers) economic unit of one or more persons that provide resources and purchase goods & services to satisfy material wants Firms

Principles of Economics, Fourth Edition N. Gregory Mankiw

PowerPoint Lecture Presentation to accompany Principles of Economics, Fourth Edition N. Gregory Mankiw Prepared by Kathryn Nantz and Laurence Miners, Fairfield University. Economy...... The word economy

PowerPoint Lecture Presentation to accompany Principles of Economics, Fourth Edition N. Gregory Mankiw Prepared by Kathryn Nantz and Laurence Miners, Fairfield University. Economy...... The word economy

Econ 200 Lecture 4 April 12, 2016

Econ 200 Lecture 4 April 12, 2016 0. Learning Catalytics Session 62335486 1. Change in Demand 2. Supply and the Law of Supply 3. Changes in Supply 4. Equilibrium Putting Supply and Demand Together 5. Impact

Econ 200 Lecture 4 April 12, 2016 0. Learning Catalytics Session 62335486 1. Change in Demand 2. Supply and the Law of Supply 3. Changes in Supply 4. Equilibrium Putting Supply and Demand Together 5. Impact

Chapter 1: Ten Principles of Economics Principles of Economics, 4 th Edition N. Gregory Mankiw Page 1

Page 1 1. Introduction a. My comments in these chapter summaries are in italics. b. For testing purposes, you are responsible for material covered in the text, but not for my comments. c. The margins in

Page 1 1. Introduction a. My comments in these chapter summaries are in italics. b. For testing purposes, you are responsible for material covered in the text, but not for my comments. c. The margins in

MIDTERM I. GROUP A Instructions: November 3, 2010

EC101 Sections 04 Fall 2010 NAME: ID #: SECTION: MIDTERM I November 3, 2010 GROUP A Instructions: You have 60 minutes to complete the exam. There will be no extensions. Students are not allowed to go out

EC101 Sections 04 Fall 2010 NAME: ID #: SECTION: MIDTERM I November 3, 2010 GROUP A Instructions: You have 60 minutes to complete the exam. There will be no extensions. Students are not allowed to go out

Chapter 3 Where Prices Come From: The Interaction of Demand and Supply

Economics 6 th edition 1 Chapter 3 Where Prices Come From: The Interaction of Demand and Supply Modified by Yulin Hou For Principles of Microeconomics Florida International University Fall 2017 What determines

Economics 6 th edition 1 Chapter 3 Where Prices Come From: The Interaction of Demand and Supply Modified by Yulin Hou For Principles of Microeconomics Florida International University Fall 2017 What determines

Subtleties of the Supply and Demand Model: Price Floors, Price Ceilings, and Elasticity

CHAPTER 4 Subtleties of the Supply and Demand Model: Price Floors, Price Ceilings, and Elasticity CHAPTER OVERVIEW Price elasticity is one of the most useful concepts in economics. It measures the responsiveness

CHAPTER 4 Subtleties of the Supply and Demand Model: Price Floors, Price Ceilings, and Elasticity CHAPTER OVERVIEW Price elasticity is one of the most useful concepts in economics. It measures the responsiveness

Ten Principles of Economics

C H A P T E R 1 Ten Principles of Economics Economics P R I N C I P L E S O F N. Gregory Mankiw Premium PowerPoint Slides by Ron Cronovich 2009 South-Western, a part of Cengage Learning, all rights reserved

C H A P T E R 1 Ten Principles of Economics Economics P R I N C I P L E S O F N. Gregory Mankiw Premium PowerPoint Slides by Ron Cronovich 2009 South-Western, a part of Cengage Learning, all rights reserved

T ( P ( ) * FA F D A S

* FA F D A S") Supply and Demand Basics Law of Supply Law of Demand Equilibrium Key Topics Demand Supply Equilibrium (shortage/surplus) Floor/Ceiling Elasticity Indifference Curves Utility Physical Product (Supply Side)

Supply and Demand Basics Law of Supply Law of Demand Equilibrium Key Topics Demand Supply Equilibrium (shortage/surplus) Floor/Ceiling Elasticity Indifference Curves Utility Physical Product (Supply Side)

Econ Midterm One Practice Questions

Econ 101-008 Midterm One Practice Questions The following questions will help students prepare for the first midterm examination in Econ 101-008. Each question has one correct answer. However, Professor

Econ 101-008 Midterm One Practice Questions The following questions will help students prepare for the first midterm examination in Econ 101-008. Each question has one correct answer. However, Professor

Econ 1 Review Session 1. with Maggie aproberts-warren UCSC Fall 2012

Econ 1 Review Session 1 with Maggie aproberts-warren UCSC Fall 2012 Introduction What will be covered in the exam? Chs. 1-8 What will the exam look like? 20 multiple choice questions 4 short answer/graphing

Econ 1 Review Session 1 with Maggie aproberts-warren UCSC Fall 2012 Introduction What will be covered in the exam? Chs. 1-8 What will the exam look like? 20 multiple choice questions 4 short answer/graphing

Bremen School District 228 Social Studies Common Assessment 2: Midterm

Bremen School District 228 Social Studies Common Assessment 2: Midterm AP Microeconomics 55 Minutes 60 Questions Directions: Each of the questions or incomplete statements in this exam is followed by five

Bremen School District 228 Social Studies Common Assessment 2: Midterm AP Microeconomics 55 Minutes 60 Questions Directions: Each of the questions or incomplete statements in this exam is followed by five

CONTENTS. Introduction to the Series. 1 Introduction to Economics 5 2 Competitive Markets, Demand and Supply Elasticities 37

CONTENTS Introduction to the Series iv 1 Introduction to Economics 5 2 Competitive Markets, Demand and Supply 17 3 Elasticities 37 4 Government Intervention in Markets 44 5 Market Failure 53 6 Costs of

CONTENTS Introduction to the Series iv 1 Introduction to Economics 5 2 Competitive Markets, Demand and Supply 17 3 Elasticities 37 4 Government Intervention in Markets 44 5 Market Failure 53 6 Costs of

Total Test Questions: 80 Levels: Grades Units of Credit:.50

DESCRIPTION This course focuses on the study of economic problems and the methods by which societies solve them. Characteristics of the market economy of the United States and its function in the world

DESCRIPTION This course focuses on the study of economic problems and the methods by which societies solve them. Characteristics of the market economy of the United States and its function in the world

SUPPLY AND DEMAND Principles of Economics in Context (Goodwin et al.)

") CHAPTER 4 UPPLY AND DEMAND Principles of Economics in Context (Goodwin et al.) Chapter Overview In this chapter, you ll find the basics of supply and demand analysis. The chapter explains how the curves

CHAPTER 4 UPPLY AND DEMAND Principles of Economics in Context (Goodwin et al.) Chapter Overview In this chapter, you ll find the basics of supply and demand analysis. The chapter explains how the curves

Making choices in a world of scarcity means we must pass up some goods and services. Every decision we make is a trade-off:

Lecture Notes Chapter 1 - The Art and Science of Economic Analysis Introduction Economics is about choices. Definition: Scarcity: A resource is scarce when it is not freely available - when its price exceeds

Lecture Notes Chapter 1 - The Art and Science of Economic Analysis Introduction Economics is about choices. Definition: Scarcity: A resource is scarce when it is not freely available - when its price exceeds

1. T F The resources that are available to meet society s needs are scarce.

1. T F The resources that are available to meet society s needs are scarce. 2. T F The marginal rate of substitution is the rate of exchange of pairs of consumption goods or services to increase utility

1. T F The resources that are available to meet society s needs are scarce. 2. T F The marginal rate of substitution is the rate of exchange of pairs of consumption goods or services to increase utility

D. People would continue to consume the same amount of the good.

17. Because prices serve as incentives in a market economy, which of the following would be a likely result of a large increase in the price of a good? A. People would increase their consumption of the

17. Because prices serve as incentives in a market economy, which of the following would be a likely result of a large increase in the price of a good? A. People would increase their consumption of the

Mods 8 and 9 practice

Mods 8 and 9 practice Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The government imposes a price ceiling below the equilibrium price. The price ceiling

Mods 8 and 9 practice Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The government imposes a price ceiling below the equilibrium price. The price ceiling

Lecture 11: Government Intervention in Competitive Markets

Lecture 11: Government Intervention in Competitive Markets Read announcements on course website. Read announcement about final-exam conflicts Government Intervention p 1 If the price in this market were,

Lecture 11: Government Intervention in Competitive Markets Read announcements on course website. Read announcement about final-exam conflicts Government Intervention p 1 If the price in this market were,

MICROECONOMICS SECTION I. Time - 70 minutes 60 Questions

MICROECONOMICS SECTION I Time - 70 minutes 60 Questions Directions: Each of the questions or incomplete statements below is followed by five suggested answers or completions. Select the one that is best

MICROECONOMICS SECTION I Time - 70 minutes 60 Questions Directions: Each of the questions or incomplete statements below is followed by five suggested answers or completions. Select the one that is best

1.3. Levels and Rates of Change Levels: example, wages and income versus Rates: example, inflation and growth Example: Box 1.3

1 Chapter 1 1.1. Scarcity, Choice, Opportunity Cost Definition of Economics: Resources versus Wants Wants: more and better unlimited Versus Needs: essential limited Versus Demand: ability to pay + want

1 Chapter 1 1.1. Scarcity, Choice, Opportunity Cost Definition of Economics: Resources versus Wants Wants: more and better unlimited Versus Needs: essential limited Versus Demand: ability to pay + want

Ten Principles of Economics. Principles of Economics. Economy... Scarcity... N. Gregory Mankiw. A household and an economy face many decisions:

A Lecture Presentation in PowerPoint to Accompany Principles of Economics Second Edition by N. Gregory Mankiw Ten Principles of Economics by Greg Mankiw Chapter 1 Copyright by Harcourt, Inc. Prepared by

A Lecture Presentation in PowerPoint to Accompany Principles of Economics Second Edition by N. Gregory Mankiw Ten Principles of Economics by Greg Mankiw Chapter 1 Copyright by Harcourt, Inc. Prepared by

ECON MACROECONOMIC PRINCIPLES Instructor: Dr. Juergen Jung Towson University. J.Jung Chapter Introduction Towson University 1 / 69

ECON 202 - MACROECONOMIC PRINCIPLES Instructor: Dr. Juergen Jung Towson University J.Jung Chapter 2-4 - Introduction Towson University 1 / 69 Disclaimer These lecture notes are customized for the Macroeconomics

ECON 202 - MACROECONOMIC PRINCIPLES Instructor: Dr. Juergen Jung Towson University J.Jung Chapter 2-4 - Introduction Towson University 1 / 69 Disclaimer These lecture notes are customized for the Macroeconomics

ECON 251 Exam #1 Spring 2013

ECON 251 Exam #1 Spring 2013 1. A is an example of a labor resource, while is an example of a capital resource. a. Schoolteacher; a computer programmer b. Football player; tree c. Business owner; checking

ECON 251 Exam #1 Spring 2013 1. A is an example of a labor resource, while is an example of a capital resource. a. Schoolteacher; a computer programmer b. Football player; tree c. Business owner; checking

ECON 1010 Principles of Macroeconomics Exam #1. Section A: Multiple Choice Questions. (30 points; 2 pts each)

") ECON 1010 Principles of Macroeconomics Exam #1 Section A: Multiple Choice Questions. (30 points; 2 pts each) #1. The figure Sam and DiMitri s Production Possibilities depicts production frontiers for Sam

ECON 1010 Principles of Macroeconomics Exam #1 Section A: Multiple Choice Questions. (30 points; 2 pts each) #1. The figure Sam and DiMitri s Production Possibilities depicts production frontiers for Sam

Using Supply and Demand

CHAPTER 5 Using Supply and Demand It is by invisible hands that we are bent and tortured worst. Nietzsche McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved. Supply

CHAPTER 5 Using Supply and Demand It is by invisible hands that we are bent and tortured worst. Nietzsche McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved. Supply

PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University

PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University 1 1 Ten Principles of Economics PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University 2 Ten Principles

PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University 1 1 Ten Principles of Economics PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University 2 Ten Principles

Problem Set 3. I. Problem 1. Explain each of the following statements using supply-and-demand diagrams.

Problem Set 3 I. Problem 1. Explain each of the following statements using supply-and-demand diagrams. a) When the weather turns warm in New England every summer, the price of hotel rooms in Caribbean

Problem Set 3 I. Problem 1. Explain each of the following statements using supply-and-demand diagrams. a) When the weather turns warm in New England every summer, the price of hotel rooms in Caribbean

Supply and Demand: Where do Prices come from?

Supply and Demand: Where do Prices come from? 3.1 Overview 58 3.2 The Middletown housing market, a parable 58 3.3 The Econoland corn market 64 3.3.1 Crop failure 67 3.3.2 Consumer surplus 68 3.3.3 Price

Supply and Demand: Where do Prices come from? 3.1 Overview 58 3.2 The Middletown housing market, a parable 58 3.3 The Econoland corn market 64 3.3.1 Crop failure 67 3.3.2 Consumer surplus 68 3.3.3 Price