Consumer and Producer Surplus HOW MUCH DO CONSUMERS AND PRODUCERS BENEFIT FROM AN EXCHANGE?

|

|

|

- Francis Baldwin Campbell

- 5 years ago

- Views:

Transcription

1 Consumer and Producer Surplus HOW MUCH DO CONSUMERS AND PRODUCERS BENEFIT FROM AN EXCHANGE?

2 How much do consumers and producers benefit from an exchange? Consumer Surplus is the difference between what you are willing to pay and what you actually pay. CS = Buyer s Maximum Price Darren and Edwina are not willing If a person s maximum price is less than the market price, he or she will not buy and will gain no consumer surplus.

3 Consumer Surplus - the area below the demand curve and above the price. Price $10 Cons umer Surplus $5 What is paid D $ Quantity

4 Change in Consumer Surplus: Price Increase Price New Consumer Surplus Original Consumer Surplus P 1 P o Los s in Surplus: Consumers paying more Loss in Surplus: Consumers buying less D Q 1 Q o Quantity

5 Producer s Surplus is the difference between the price the seller received and the cost of producing the good. PS = Price Production Cost Donna and Engelbert s prod costs are too high

6 Producer Surplus - the area above the supply curve and below the price. Price S Producer Surplus P o What is paid Minimum Amount Needed to Supply Q o Q o Quantity

7 Efficiency - allocation that results in the maximization the total surplus (TS = CS + PS). Both consumers and producers can not increase their welfare without making each other worse off. Price P o Total Surplus = CS + PS Consumer Surplus Producer Surplus D S Free markets allocate the supply of goods to the buyers who value them most highly. the demand for goods to the sellers who can produce them at least cost. Q o Quantity A competitive free market maximizes total surplus!

8 Consumer and Producer Surplus P $10 S 8 6 $5 4 Calculate the area of: 1. Consumer Surplus 2. Producer Surplus 3. Total Surplus D Q

9 Consumer and Producer Surplus P $10 S 8 6 $5 4 CS PS 1. CS= $25 2. PS= $20 3. Total= $ D Q

10 GOVERNMENT INTERVENTION AND MARKET OUTCOMES

11 Government Intervention PRICE CONTROLS: CEILINGS AND FLOORS

to make housing more")

12 Should the government place a price ceiling (maximum price) to make housing more affordable?

13 The Market for Apartments Rental price of apts $3500 P S What price should the price ceiling be set at? $2800 $ D Q Quantity of apartments

14 How Price Ceilings Affect Market Outcomes A price ceiling above the equilibrium price is not binding it has no effect on the market outcome. $3500 $2800 P S Price ceiling 300 D Q

15 How Price Ceilings Affect Market Outcomes The price ceiling must below the market price to be effective. $2800 P S A PC of $2500 would actually make housing more affordable. $ D Price ceiling Q

16 How Price Ceilings Affect Market Outcomes What is the unintended consequence of this price ceiling? P S $2800 What happens to the quality of apartments that remain on the market? $2500 shortage D Price ceiling Q

17 Price Ceiling Government imposes a maximum price less than P e. Generally on essential items that have a very high market equilibrium price. ex. housing rent control This generates a shortage (Q d > Q s ). The market mechanism cannot clear the market. A permanent shortage exists. P P e Price ceiling Q s Q e S Shortage Q d D Q

18 Shortages and Rationing With a shortage, sellers must ration the goods among buyers. Some rationing mechanisms: (1) long lines (2) discrimination according to sellers biases These mechanisms are often unfair, and inefficient: the goods don t necessarily go to the buyers who value them most highly. In contrast, when prices are not controlled, the rationing mechanism is efficient (the goods go to the buyers that value them most highly) and impersonal (and thus fair).

19 How Price Ceilings Affect Market Outcomes How many apartments would have been rented if there was no price ceiling? 300 How many apartments are rented with this price ceiling? P $2800 $2500 S D Price ceiling Q 250 only 250 can be rented if only 250 are supplied

20 How Price Ceilings Affect Market Outcomes This price ceiling caused a loss of trades. $2800 P S $2500 Price ceiling MISSED OPPORTUNITIES!!! D Q

21 How Price Ceilings Affect Market Outcomes There is a loss of TS (CS & PS) P S deadweight loss value of transactions that could have been made, but are not made. $2800 $2500 DWL Price ceiling CS increases at the expense of PS D Q

22 Loss in Efficiency Too Low of Price (Price Ceiling) Price New Consumer Surplus Lost Consumer Surplus S Deadweight Loss P o Los t Producer Surplus New Producer Surplus P C D QC Q o Quantity

23 Price Floor Government imposes a minimum price greater than P e. Generally on essential items that have a very low market equilibrium price ex. agricultural price supports, minimum wage This generates a surplus (Q s > Q d ). Price floor P P e Surplus S The market mechanism cannot clear the market. D A permanent surplus exists. Q d Q e Q s Q

24 Minimum Wage Should the government raise the federal minimum wage to $10?

25 How Price Floors Affect Market Outcomes The floor is a binding constraint on the wage, and causes a surplus of labor (unemployment). W $5 $4 labor surplus S Price floor D L

26 The Minimum Wage Min wage laws do not affect highly skilled workers. They do affect teen workers. $5 $4 W unemployment S Min. wage WHY? Studies: A 10% increase in the min wage raises teen unemployment by 1-3% D L

27 How Price Floors Affect Market Outcomes Surplus of how many workers? # of loss trades? W $5 labor surplus S Price floor DWL? $4 PS? CS? D L

28 Loss in Efficiency Too High of Price (Price Floor) Price New Consumer Surplus Lost Consumer Surplus S Deadweight Loss P F P o Los t Producer Surplus New Producer Surplus D QF Q o Quantity

29 What are the effects of price controls? Persistent shortages/surpluses A loss of gains from trades (DWL) Reduction in quality or inefficiently high quality Misallocation of resources The person that needs the good may not end up getting it. Wasted time, effort and resources Emergence of black markets WHY? Price controls take away incentives that would otherwise regulate markets.

30 Prices efficiently allocate resources. Resources will only be used for only the most valuable purposes. Prices as Signals and Incentives Prices tell consumers and suppliers how to adjust. High prices are an incentive to suppliers to supply more. Low prices tell producers that a good is being over produced. Low prices to consumers signal to buy more of a good. A high price is a sign to stop and think carefully before buying.

31 Government Intervention TRADE TARIFFS Purpose: To protect domestic producers from a cheaper world price. To prevent domestic unemployment.

32

33

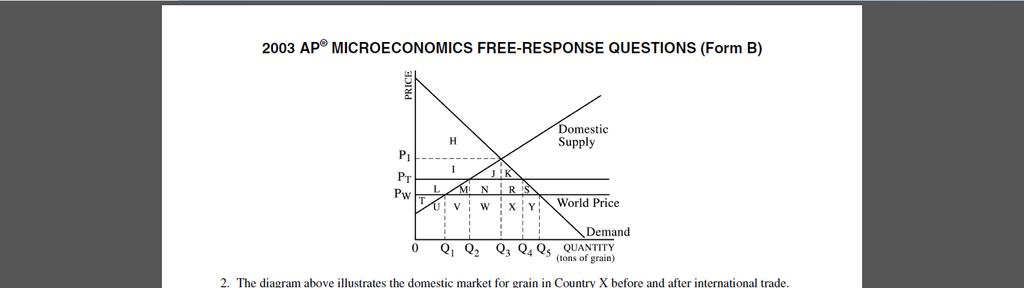

34 International Trade and Quotas Identify the following: 1. Equilibrium P & Q 2. CS with no trade 3. PS with no trade With Trade (World Price) 4. Quantity of imported grain? Q5 Q1 This graphs show the domestic supply and demand for grain. The letters represent area. With Tariff (PT) 5. Domestic production 6. Domestic consumption 7. CS Loss of LMNRS to tax 8. PS Gains L since the price increased Will produce at Q2. Change = Q2-Q1 Will consume at Q4. Change = Q4-Q5

35

36

37 = Q3 Q1. US production drops to Q1 but QD rises Q3

38 Government Intervention QUANTITY CONTROLS THE GOVERNMENT REGU LATES THE QU AN TITY OF A GOOD THAT C AN BE BOU GHT AN D SOL D RATHER THAN REGU L ATING THE PRI C E. Licenses Import quotas

39 International Trade and Quotas At the PW, what is CS and PS? If the government sets a quota on imports of Q 2, what happens to CS? (at Pw) This graphs show the domestic supply and demand for grain. The letters represent area. DEADWEIGHT LOSS Lost CS. INEFFICIENT!

ECONOMICS. Chapter 4 The Market Strikes Back

Lesson 1 ECONOMICS Chapter 4 The Market Strikes Back Review: Supply and Demand The previous lesson focused on demand and supply, we studied the demand curve and the supply curve P P S D Quantity Quantity

Lesson 1 ECONOMICS Chapter 4 The Market Strikes Back Review: Supply and Demand The previous lesson focused on demand and supply, we studied the demand curve and the supply curve P P S D Quantity Quantity

Unit 2 Supply and Demand

Unit 2 Supply and Demand Microeconomics - analyzes the Small Unit economic behavior of Individuals, Households and Firms to understand their decision-making process. -America s Free Enterprise- An economy

Unit 2 Supply and Demand Microeconomics - analyzes the Small Unit economic behavior of Individuals, Households and Firms to understand their decision-making process. -America s Free Enterprise- An economy

ECONOMICS. Chapter 4 The Market Strikes Back

Lesson 1 ECONOMICS Chapter 4 The Market Strikes Back Review: Supply and Demand The previous lesson focused on demand and supply, we studied the demand curve and the supply curve P P S D Quantity Quantity

Lesson 1 ECONOMICS Chapter 4 The Market Strikes Back Review: Supply and Demand The previous lesson focused on demand and supply, we studied the demand curve and the supply curve P P S D Quantity Quantity

Chapter 6: Combining Supply and Demand

SCHS SOCIAL STUDIES What you need to know UNIT TWO 1. Explain how supply and demand create balance in the marketplace 2. Explain how a market reacts to a fall in supply by moving to a new equilibrium 3.

SCHS SOCIAL STUDIES What you need to know UNIT TWO 1. Explain how supply and demand create balance in the marketplace 2. Explain how a market reacts to a fall in supply by moving to a new equilibrium 3.

MICROECONOMICS - CLUTCH CH. 5 - CONSUMER AND PRODUCER SURPLUS; PRICE CEILINGS AND FLOORS

!! www.clutchprep.com CONCEPT: CONSUMER SURPLUS AND WILLINGNESS TO PAY The represents the willingness to pay (reservation price) of consumers. A consumer surplus exists when someone is willing to pay than

!! www.clutchprep.com CONCEPT: CONSUMER SURPLUS AND WILLINGNESS TO PAY The represents the willingness to pay (reservation price) of consumers. A consumer surplus exists when someone is willing to pay than

Government Regulation

Government Regulation What do you think is the market price for renting an apartment in Plainfield? What happens to the quantity of demand and supply after the price change? List four outcomes that would

Government Regulation What do you think is the market price for renting an apartment in Plainfield? What happens to the quantity of demand and supply after the price change? List four outcomes that would

Supply, Demand, and Government Policies. Copyright 2004 South-Western

Supply, Demand, and Government Policies Copyright 2004 South-Western Supply, Demand, and Government Policies In a free, unregulated market system, market forces establish equilibrium prices and exchange

Supply, Demand, and Government Policies Copyright 2004 South-Western Supply, Demand, and Government Policies In a free, unregulated market system, market forces establish equilibrium prices and exchange

Economic efficiency. Who gains and who loses when prices change?

Economic efficiency Who gains and who loses when prices change? 1 The Efficiency of Competitive Markets Economic Surplus and Economic Efficiency Economic efficiency A market outcome in which the marginal

Economic efficiency Who gains and who loses when prices change? 1 The Efficiency of Competitive Markets Economic Surplus and Economic Efficiency Economic efficiency A market outcome in which the marginal

Supply and Demand Cont d

Supply and Demand Cont d D I A N N A D A S I LVA - G L A S G O W D E PA R T M E N T O F E C O N O M I C S U N I V E R S I T Y O F G U YA N A 5 O C T O B E R, 2 0 1 7 WK 4 Lecture I... SUPPLY AND DEMAND

Supply and Demand Cont d D I A N N A D A S I LVA - G L A S G O W D E PA R T M E N T O F E C O N O M I C S U N I V E R S I T Y O F G U YA N A 5 O C T O B E R, 2 0 1 7 WK 4 Lecture I... SUPPLY AND DEMAND

Econ 200: Lecture 6 October 14, 2014

Econ 200: Lecture 6 October 14, 2014 0. Learning Catalytics Session: 47811348 1. Economic Efficiency 2. Price Ceilings and Floors and Efficiency 3. Start Taxes (if time) Reminder: Article Response Writing

Econ 200: Lecture 6 October 14, 2014 0. Learning Catalytics Session: 47811348 1. Economic Efficiency 2. Price Ceilings and Floors and Efficiency 3. Start Taxes (if time) Reminder: Article Response Writing

Downloaded for free from 1

Micro Chapter 6 -price ceiling or price cap: government regulation that makes it illegal to charge a price higher then a specified level -effects of the price cap on the market depend on whether the ceiling

Micro Chapter 6 -price ceiling or price cap: government regulation that makes it illegal to charge a price higher then a specified level -effects of the price cap on the market depend on whether the ceiling

C. many buyers and many sellers C. Sue will likely purchase more than one bottle of shampoo. B. cause the demand for mangos to shift to the right

Multiple Choice 1. Competitive markets are characterized as having A. many buyers and a single seller B. many buyers and a few sellers. C. many buyers and many sellers D. a few buyers and many sellers

Multiple Choice 1. Competitive markets are characterized as having A. many buyers and a single seller B. many buyers and a few sellers. C. many buyers and many sellers D. a few buyers and many sellers

Bringing the curves together

Bringing the curves together 1. Create a combined demand and supply schedule (see at right). IMPORTANT: Make sure you create an equilibrium price by making one of the price levels have the exact same quantity

Bringing the curves together 1. Create a combined demand and supply schedule (see at right). IMPORTANT: Make sure you create an equilibrium price by making one of the price levels have the exact same quantity

EC133 Practice Midterm 1 JP Rabanal

EC133 Practice Midterm 1 JP Rabanal 1. Imagine that supply is given by P= 50*Q, while demand is P = 1000 200 Q a. The consumer surplus is. b. The producer surplus is c. If the government sets a price 5%

EC133 Practice Midterm 1 JP Rabanal 1. Imagine that supply is given by P= 50*Q, while demand is P = 1000 200 Q a. The consumer surplus is. b. The producer surplus is c. If the government sets a price 5%

Applications of supply and demand

Applications of supply and demand Comparative statics and government policy Comparative statics The simple supply and demand model we have developed can be used to analyze the effects of many events on

Applications of supply and demand Comparative statics and government policy Comparative statics The simple supply and demand model we have developed can be used to analyze the effects of many events on

LECTURE February Thursday, February 21, 13

LECTURE 10 21 February 2013 1 ANNOUNCEMENTS HW 4 due Friday at 11:45 PM Midterm 1 next Monday February 25th 7:30 PM - 8:30 PM in Anderson 270 (not this room) 2 old midterms are on Moodle; they are very

LECTURE 10 21 February 2013 1 ANNOUNCEMENTS HW 4 due Friday at 11:45 PM Midterm 1 next Monday February 25th 7:30 PM - 8:30 PM in Anderson 270 (not this room) 2 old midterms are on Moodle; they are very

6) Consumer surplus is the red area in the following graph. It is 0.5*5*5=12.5. The answer is C.

Consumer surplus is the red area in the following graph. It is 0.5*5*5=12.5. The answer is C.") These are solutions to Fall 2013 s Econ 1101 Midterm 1. No guarantees are made that this guide is error free, so please consult your TA or instructor if anything looks wrong. 1) If the price of sweeteners,

These are solutions to Fall 2013 s Econ 1101 Midterm 1. No guarantees are made that this guide is error free, so please consult your TA or instructor if anything looks wrong. 1) If the price of sweeteners,

Unit 2 Supply and Demand

Unit 2 Supply and Demand -Study Guide- Answer, Explain and define the following: 1) Demand 2) Consumer 3) Supply 4) Producer 5) Subsidy 6) Give examples of goods that would have inelastic demand 7) Give

Unit 2 Supply and Demand -Study Guide- Answer, Explain and define the following: 1) Demand 2) Consumer 3) Supply 4) Producer 5) Subsidy 6) Give examples of goods that would have inelastic demand 7) Give

Basics of Economics. Alvin Lin. Principles of Microeconomics: August December 2016

Basics of Economics Alvin Lin Principles of Microeconomics: August 2016 - December 2016 1 Markets and Efficiency How are goods allocated efficiently? How are goods allocated fairly? A normative statement

Basics of Economics Alvin Lin Principles of Microeconomics: August 2016 - December 2016 1 Markets and Efficiency How are goods allocated efficiently? How are goods allocated fairly? A normative statement

CHAPTER 2. 4) Taxes cause: a) Market distortions b) Reduce incentives to work c) Decrease wealth creating transactions d) All of the above ANS: D

Taxes cause: a) Market distortions b) Reduce incentives to work c) Decrease wealth creating transactions d) All of the above ANS: D") CHAPTER 2 1) When the market is in equilibrium, a) Total surplus is minimized b) Total surplus is maximized without government intervention c) Government maximizes total revenue 2) The difference between

CHAPTER 2 1) When the market is in equilibrium, a) Total surplus is minimized b) Total surplus is maximized without government intervention c) Government maximizes total revenue 2) The difference between

ECON 101 KONG Midterm 2 CMP Review Session. Presented by Benji Huang

ECON 101 KONG Midterm 2 CMP Review Session Presented by Benji Huang Chapter 5 Efficiency and Equity Benefit, Cost, Surplus Consumers (1) A consumer benefits from the consumption of a product this benefit

ECON 101 KONG Midterm 2 CMP Review Session Presented by Benji Huang Chapter 5 Efficiency and Equity Benefit, Cost, Surplus Consumers (1) A consumer benefits from the consumption of a product this benefit

2. Demand and Supply

2. Demand and Supply The following materials are taken from Chap. 3 to Chap. 7 of Economics, 2 nd ed., Krugman and Wells(2009), Worth Palgrave MaCmillan. 1 of 42 2. Demand and Supply, and Market Equilibrium

2. Demand and Supply The following materials are taken from Chap. 3 to Chap. 7 of Economics, 2 nd ed., Krugman and Wells(2009), Worth Palgrave MaCmillan. 1 of 42 2. Demand and Supply, and Market Equilibrium

Chapter 6: Prices Section 1

Chapter 6: Prices Section 1 Key Terms equilibrium: the point at which the demand for a product or service is equal to the supply of that product or service disequilibrium: any price or quantity not at

Chapter 6: Prices Section 1 Key Terms equilibrium: the point at which the demand for a product or service is equal to the supply of that product or service disequilibrium: any price or quantity not at

EC1000 MICROECONOMICS ' MOCK EXAM

EC1000 MICROECONOMICS ' MOCK EXAM Time Allowed Two Hours (2 Hours) Instructions to candidates This paper is in two sections. Students should attempt ALL the questions in both Sections The maximum mark

EC1000 MICROECONOMICS ' MOCK EXAM Time Allowed Two Hours (2 Hours) Instructions to candidates This paper is in two sections. Students should attempt ALL the questions in both Sections The maximum mark

Efficiency of Market Equilibrium 3.1 SAMPLE

Castle Got the answer? Be the first to stand with your group s flag. Market Equilibrium 3.1 Question 1: Define market equilibrium. Got it correct? MAKE or BREAK a castle, yours or any other group s. The

Castle Got the answer? Be the first to stand with your group s flag. Market Equilibrium 3.1 Question 1: Define market equilibrium. Got it correct? MAKE or BREAK a castle, yours or any other group s. The

Using Supply and Demand

CHAPTER 5 Using Supply and Demand It is by invisible hands that we are bent and tortured worst. Nietzsche McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved. Supply

CHAPTER 5 Using Supply and Demand It is by invisible hands that we are bent and tortured worst. Nietzsche McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved. Supply

1. Welfare economics is the study of a. the well-being of less fortunate people. b. welfare programs in the United States.

1. Welfare economics is the study of a. the well-being of less fortunate people. b. welfare programs in the United States. c. the effect of income redistribution on work effort. d. how the allocation of

1. Welfare economics is the study of a. the well-being of less fortunate people. b. welfare programs in the United States. c. the effect of income redistribution on work effort. d. how the allocation of

Mods 8 and 9 practice

Mods 8 and 9 practice Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The government imposes a price ceiling below the equilibrium price. The price ceiling

Mods 8 and 9 practice Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The government imposes a price ceiling below the equilibrium price. The price ceiling

This is the midterm 1 solution guide for Fall 2012 Form A. 1) The answer to this question is A, corresponding to Form A.

The answer to this question is A, corresponding to Form A.") This is the midterm 1 solution guide for Fall 2012 Form A. 1) The answer to this question is A, corresponding to Form A. 2) Since widgets are an inferior good (like ramen noodles) and income increases,

This is the midterm 1 solution guide for Fall 2012 Form A. 1) The answer to this question is A, corresponding to Form A. 2) Since widgets are an inferior good (like ramen noodles) and income increases,

Welfare economics part 2 (producer surplus) Application of welfare economics: The Costs of Taxation & International Trade

Application of welfare economics: The Costs of Taxation & International Trade") Welfare economics part 2 (producer surplus) Application of welfare economics: The Costs of Taxation & International Trade Dr. Anna Kowalska-Pyzalska Department of Operations Research Presentation is based

Welfare economics part 2 (producer surplus) Application of welfare economics: The Costs of Taxation & International Trade Dr. Anna Kowalska-Pyzalska Department of Operations Research Presentation is based

Prices and Decision Making (Clayton pages )

") 1 Prices and Decision Making (Clayton pages 126-149) Prices as Signals Prices act as signals to consumers and producers Prices answer the three basic questions: 1. What goods and services to produce? 2.

1 Prices and Decision Making (Clayton pages 126-149) Prices as Signals Prices act as signals to consumers and producers Prices answer the three basic questions: 1. What goods and services to produce? 2.

Price = The Interaction of Supply and Demand WEDNESDAY, FEBRUARY 17 THURSDAY, FEBRUARY 18

Price = The Interaction of Supply and Demand WEDNESDAY, FEBRUARY 17 THURSDAY, FEBRUARY 18 Chapter 4: Section 1 Understanding Demand What Is Demand? Markets are where people come together to buy and sell

Price = The Interaction of Supply and Demand WEDNESDAY, FEBRUARY 17 THURSDAY, FEBRUARY 18 Chapter 4: Section 1 Understanding Demand What Is Demand? Markets are where people come together to buy and sell

ANSWER KEY Multiple Choice. 3 marks each. Indicate your answers on the bubble sheet provided.

November 17, 2009 90 minutes No calculators, no aids allowed. Economics 103 Second Midterm Dr. J. Friesen ANSWER KEY Multiple Choice. 3 marks each. Indicate your answers on the bubble sheet provided. 1)

November 17, 2009 90 minutes No calculators, no aids allowed. Economics 103 Second Midterm Dr. J. Friesen ANSWER KEY Multiple Choice. 3 marks each. Indicate your answers on the bubble sheet provided. 1)

ECON 101 MIDTERM 1 REVIEW SESSION SOLUTIONS (WINTER 2015) BY BENJI HUANG

BY BENJI HUANG") ECON 101 MIDTERM 1 REVIEW SESSION SOLUTIONS (WINTER 2015) BY BENJI HUANG TABLE OF CONTENT I. CHAPTER 1: WHAT IS ECONOMICS II. CHAPTER 2: THE ECONOMIC PROBLEM III. CHAPTER 3: DEMAND AND SUPPLY IV. CHAPTER

ECON 101 MIDTERM 1 REVIEW SESSION SOLUTIONS (WINTER 2015) BY BENJI HUANG TABLE OF CONTENT I. CHAPTER 1: WHAT IS ECONOMICS II. CHAPTER 2: THE ECONOMIC PROBLEM III. CHAPTER 3: DEMAND AND SUPPLY IV. CHAPTER

9.1 Zero Profit for Competitive Firms in the Long Run

9.1 Zero Profit for Competitive Firms in the Long Run Chapter 9 Applications of the Competitive Model With Free Entry into the Market Along with identical costs and constant input prices, implies firms

9.1 Zero Profit for Competitive Firms in the Long Run Chapter 9 Applications of the Competitive Model With Free Entry into the Market Along with identical costs and constant input prices, implies firms

Markets in Perfect Competition (II)

") Markets in Perfect Competition (II) There is always an opportunity created by a new demand 1 of 41 Supply, Demand and Equilibrium (I) Finding the Equilibrium Price and Quantity (I) A competitive market

Markets in Perfect Competition (II) There is always an opportunity created by a new demand 1 of 41 Supply, Demand and Equilibrium (I) Finding the Equilibrium Price and Quantity (I) A competitive market

Policy Evaluation Tools. Willingness to Pay and Demand. Consumer Surplus (CS) Evaluating Gov t Policy - Econ of NA - RIT - Dr.

Evaluating Gov t Policy - Econ of NA - RIT - Dr.") Policy Evaluation Tools Evaluating Gov t Policy - Econ of NA - RIT - Dr. Jeffrey Burnette In economics we like to measure the impact government policies have on the economy and separate winners and losers.

Policy Evaluation Tools Evaluating Gov t Policy - Econ of NA - RIT - Dr. Jeffrey Burnette In economics we like to measure the impact government policies have on the economy and separate winners and losers.

Chapter 4. Demand, Supply and Markets. These slides supplement the textbook, but should not replace reading the textbook

Chapter 4 Demand, Supply and Markets These slides supplement the textbook, but should not replace reading the textbook 1 What is a market? A group of buyers and sellers with the potential to trade 2 What

Chapter 4 Demand, Supply and Markets These slides supplement the textbook, but should not replace reading the textbook 1 What is a market? A group of buyers and sellers with the potential to trade 2 What

Demand/Supply Unit Essential Questions

Demand/Supply Unit Essential Questions -What is the role of demand in free market capitalism? -How do changes in price influence quantity demanded? -What factors affect changes in demand that influence

Demand/Supply Unit Essential Questions -What is the role of demand in free market capitalism? -How do changes in price influence quantity demanded? -What factors affect changes in demand that influence

Government Policy, Efficiency, and Welfare

Government Policy, Efficiency, and Welfare Econ 102: Introduction to Microeconomics 1 1.1 Goals of today s class Goals of today s class Learn about consumer surplus and producer surplus, a convenient way

Government Policy, Efficiency, and Welfare Econ 102: Introduction to Microeconomics 1 1.1 Goals of today s class Goals of today s class Learn about consumer surplus and producer surplus, a convenient way

Government Intervention

Government Intervention Taxes - Aim of imposing indirect taxes: the government does such spending in order to raise tax revenues and to internalize externalities, to achieve the optimum level of output.

Government Intervention Taxes - Aim of imposing indirect taxes: the government does such spending in order to raise tax revenues and to internalize externalities, to achieve the optimum level of output.

Homework 4 Economics

Homework 4 Economics 501.01 Manisha Goel Due: Tuesday, March 1, 011 (beginning of class). Draw and label all graphs clearly. Show all work. Explain. Question 1. Governments often regulate the price of

Homework 4 Economics 501.01 Manisha Goel Due: Tuesday, March 1, 011 (beginning of class). Draw and label all graphs clearly. Show all work. Explain. Question 1. Governments often regulate the price of

SOLUTIONS TO TEXT PROBLEMS 6

SOLUTIONS TO TEXT PROBLEMS 6 Quick Quizzes 1. A price ceiling is a legal maximum on the price at which a good can be sold. Examples of price ceilings include rent control, price controls on gasoline in

SOLUTIONS TO TEXT PROBLEMS 6 Quick Quizzes 1. A price ceiling is a legal maximum on the price at which a good can be sold. Examples of price ceilings include rent control, price controls on gasoline in

GRAPHS WHAAAA???!!!???

Mumford and Sons Supply and Demand GRAPHS WHAAAA???!!!??? Demand Combination of desire, ability, and willingness to buy a product Question: Demand Schedule Price Quantity How many movie DVDs Demanded would

Mumford and Sons Supply and Demand GRAPHS WHAAAA???!!!??? Demand Combination of desire, ability, and willingness to buy a product Question: Demand Schedule Price Quantity How many movie DVDs Demanded would

Assessment Schedule 2017 Economics: Demonstrate understanding of the efficiency of market equilibrium (91399)

") NCEA Level 3 Economics (91399) 2017 page 1 of 8 Assessment Schedule 2017 Economics: Demonstrate understanding of the efficiency of market equilibrium (91399) Assessment Criteria Achievement Achievement

NCEA Level 3 Economics (91399) 2017 page 1 of 8 Assessment Schedule 2017 Economics: Demonstrate understanding of the efficiency of market equilibrium (91399) Assessment Criteria Achievement Achievement

Microeconomics. Lecture Outline. Claudia Vogel. Winter Term 2009/2010. Part II Producers, Consumers, and Competitive Markets

Microeconomics Claudia Vogel EUV Winter Term 2009/2010 Claudia Vogel (EUV) Microeconomics Winter Term 2009/2010 1 / 28 Lecture Outline Part II Producers, Consumers, and Competitive Markets 9 Evaluating

Microeconomics Claudia Vogel EUV Winter Term 2009/2010 Claudia Vogel (EUV) Microeconomics Winter Term 2009/2010 1 / 28 Lecture Outline Part II Producers, Consumers, and Competitive Markets 9 Evaluating

Microeconomics: Principles, Applications, and Tools NINTH EDITION. Chapter 6

Microeconomics: Principles, Applications, and Tools NINTH EDITION Chapter 6 Market Efficiency and Government Intervention The housing market in New York City is highly regulated. The city issues a relatively

Microeconomics: Principles, Applications, and Tools NINTH EDITION Chapter 6 Market Efficiency and Government Intervention The housing market in New York City is highly regulated. The city issues a relatively

Supply, demand and government policies. Dr. Anna Kowalska-Pyzalska

Supply, demand and government policies Dr. Anna Kowalska-Pyzalska Price ceiling Price floor Tax incidence In a free, unregulated market system, market forces establish equilibrium prices and exchange quantities.

Supply, demand and government policies Dr. Anna Kowalska-Pyzalska Price ceiling Price floor Tax incidence In a free, unregulated market system, market forces establish equilibrium prices and exchange quantities.

Choose the single best answer for each question. Do all of your scratch-work in the side and bottom margins of pages.

Econ 101, Sections 3 and 4, S11, Schroeter Exam #2, Special code = 0002 Choose the single best answer for each question. Do all of your scratch-work in the side and bottom margins of pages. 1. The cross-price

Econ 101, Sections 3 and 4, S11, Schroeter Exam #2, Special code = 0002 Choose the single best answer for each question. Do all of your scratch-work in the side and bottom margins of pages. 1. The cross-price

Price Ceilings and Price

Price Ceilings and Price Floors By: OpenStaxCollege Controversy sometimes surrounds the prices and quantities established by demand and supply, especially for products that are considered necessities.

Price Ceilings and Price Floors By: OpenStaxCollege Controversy sometimes surrounds the prices and quantities established by demand and supply, especially for products that are considered necessities.

within this range? c. Over what range of prices is the demand for motel rooms unit elastic? To

1. Identify the parts of the circular-flow diagram immediately involved in the following transactions. a. Mary buys a car from Jaguar for 40,000. b. Jaguar pays Joe 2,500/month for work on the assembly

1. Identify the parts of the circular-flow diagram immediately involved in the following transactions. a. Mary buys a car from Jaguar for 40,000. b. Jaguar pays Joe 2,500/month for work on the assembly

Homework 2 Answer Key

Econ 226 Principles of Microeconomics Fall, 24 Dr. Kathryn Wilson Due Date: Tuesday, September 28 th Homework 2 Answer Key 1. When the of movie admissions increases from $7 to $8, the demanded falls from

Econ 226 Principles of Microeconomics Fall, 24 Dr. Kathryn Wilson Due Date: Tuesday, September 28 th Homework 2 Answer Key 1. When the of movie admissions increases from $7 to $8, the demanded falls from

The Analysis of Competitive Markets

C H A P T E R 9 The Analysis of Competitive Markets Prepared by: Fernando & Yvonn Quijano CHAPTER 9 OUTLINE 9.1 Evaluating the Gains and Losses from Government Policies Consumer and Producer Surplus 9.2

C H A P T E R 9 The Analysis of Competitive Markets Prepared by: Fernando & Yvonn Quijano CHAPTER 9 OUTLINE 9.1 Evaluating the Gains and Losses from Government Policies Consumer and Producer Surplus 9.2

Model: Price Ceilings

Model: Price Ceilings Today, we will examine a model of price ceilings, one type of market distortion. This model reflects a pattern of policy used in response to unpopular fluctuations in the prices of

Model: Price Ceilings Today, we will examine a model of price ceilings, one type of market distortion. This model reflects a pattern of policy used in response to unpopular fluctuations in the prices of

Lecture 11: Government Intervention in Competitive Markets

Lecture 11: Government Intervention in Competitive Markets Read announcements on course website. Read announcement about final-exam conflicts Government Intervention p 1 If the price in this market were,

Lecture 11: Government Intervention in Competitive Markets Read announcements on course website. Read announcement about final-exam conflicts Government Intervention p 1 If the price in this market were,

Econ Test 2B Dr. Rupp Tuesday, March 3, 2009 Pledge: I have neither given or received aid on this exam Signature

Econ 2113 - Test 2B Dr. Rupp Tuesday, March 3, 2009 Name Pledge: I have neither given or received aid on this exam Signature Multiple Choice Identify the letter of the choice that best completes the statement

Econ 2113 - Test 2B Dr. Rupp Tuesday, March 3, 2009 Name Pledge: I have neither given or received aid on this exam Signature Multiple Choice Identify the letter of the choice that best completes the statement

Economics E201 (Professor Self) Sample Questions for Exam Two, Fall 2013

Sample Questions for Exam Two, Fall 2013") , Fall 2013 Your exam will have two parts covering the topics in chapters 4 (page 91 through end of chapter), 5 and 6 from the Parkin chapters and chapter 10 (up to page 317, up to but not including the

, Fall 2013 Your exam will have two parts covering the topics in chapters 4 (page 91 through end of chapter), 5 and 6 from the Parkin chapters and chapter 10 (up to page 317, up to but not including the

AP Microeconomics Review With Answers

AP Microeconomics Review With Answers 1. Firm in Perfect Competition (Long-Run Equilibrium) 2. Monopoly Industry with comparison of price & output of a Perfectly Competitive Industry (which means show

AP Microeconomics Review With Answers 1. Firm in Perfect Competition (Long-Run Equilibrium) 2. Monopoly Industry with comparison of price & output of a Perfectly Competitive Industry (which means show

Department of Economics University of California, Davis ECONOMICS 1A. Second Midterm Exam Version B

Department of Economics University of California, Davis ECONOMICS 1A Spring 2010 L. Jay Helms Second Midterm Exam Version B Last Name: First Name: Your Student ID Number: Please check your registered section

Department of Economics University of California, Davis ECONOMICS 1A Spring 2010 L. Jay Helms Second Midterm Exam Version B Last Name: First Name: Your Student ID Number: Please check your registered section

Eastern Mediterranean University Faculty of Business and Economics Department of Economics Fall Semester

Duration: 50 minutes Eastern Mediterranean University Faculty of Business and Economics Department of Economics 2016-17 Fall Semester ECON101 - Introduction to Economics I Quiz 2 Answer Key 16 December

Duration: 50 minutes Eastern Mediterranean University Faculty of Business and Economics Department of Economics 2016-17 Fall Semester ECON101 - Introduction to Economics I Quiz 2 Answer Key 16 December

Econ 1 Review Session 1. with Maggie aproberts-warren UCSC Fall 2012

Econ 1 Review Session 1 with Maggie aproberts-warren UCSC Fall 2012 Introduction What will be covered in the exam? Chs. 1-8 What will the exam look like? 20 multiple choice questions 4 short answer/graphing

Econ 1 Review Session 1 with Maggie aproberts-warren UCSC Fall 2012 Introduction What will be covered in the exam? Chs. 1-8 What will the exam look like? 20 multiple choice questions 4 short answer/graphing

Econ 101, sections 2 and 6, S06 Schroeter Exam #2, Red. Choose the single best answer for each question.

Econ 101, sections 2 and 6, S06 Schroeter Exam #2, Red Choose the single best answer for each question. 1. If the own-price elasticity of demand for a good is -2.0, this implies that consumers would a.

Econ 101, sections 2 and 6, S06 Schroeter Exam #2, Red Choose the single best answer for each question. 1. If the own-price elasticity of demand for a good is -2.0, this implies that consumers would a.

Top 10 Most Common Errors AP Economics 2011

Top 10 Most Common Errors AP Economics 2011 Overview of Trouble Spots 11. Finding the Socially Optimal Quantity 10. Deadweight Loss from a Positive Externality 9. Allocative Efficiency 7. Price Elasticity

Top 10 Most Common Errors AP Economics 2011 Overview of Trouble Spots 11. Finding the Socially Optimal Quantity 10. Deadweight Loss from a Positive Externality 9. Allocative Efficiency 7. Price Elasticity

Econ: CH 7 Test Review Demand & Supply

Econ: CH 7 Test Review Demand & Supply The Big Idea: 1. Scarcity is the basic economic problem that requires people to make choices about how to use limited resources 2. Buyers and sellers voluntarily

Econ: CH 7 Test Review Demand & Supply The Big Idea: 1. Scarcity is the basic economic problem that requires people to make choices about how to use limited resources 2. Buyers and sellers voluntarily

Competitive markets. Microéconomie, chapter 9. Solvay Business School Université Libre de Bruxelles

Competitive markets Microéconomie, chapter 9 Solvay Business School Université Libre de Bruxelles 1 List of subjects Evaluation of public policies Efficiency of competitive markets Minimum prices Support

Competitive markets Microéconomie, chapter 9 Solvay Business School Université Libre de Bruxelles 1 List of subjects Evaluation of public policies Efficiency of competitive markets Minimum prices Support

Exam 01 - ECON Friday, October 1st

Name: Exam 01 - ECON 2301-05 - Friday, October 1st Figure 1 1. Refer to Figure 1. This economy has the ability to produce at which point(s)? a. A, B, D b. A, B c. C, F, G d. A, B, C, F, G 2. Any point

Name: Exam 01 - ECON 2301-05 - Friday, October 1st Figure 1 1. Refer to Figure 1. This economy has the ability to produce at which point(s)? a. A, B, D b. A, B c. C, F, G d. A, B, C, F, G 2. Any point

1) Your answer to this question is what form of the exam you had. The answer is A if you have form A. The answer is B if you have form B etc.

Your answer to this question is what form of the exam you had. The answer is A if you have form A. The answer is B if you have form B etc.") This is the guide to Fall 2014, Midterm 1, Form A. If you have another form, the answers will be different, but the solution will be the same. Please consult your TA or instructor if you think there is

This is the guide to Fall 2014, Midterm 1, Form A. If you have another form, the answers will be different, but the solution will be the same. Please consult your TA or instructor if you think there is

Microeconomics. Use the graph below to answer question number 3

More Tutorial at Microeconomics 1. Opportunity costs are the values of the: a. minimal budgets of families on welfare b. hidden charges passed on to consumers c. monetary costs of goods and services *

More Tutorial at Microeconomics 1. Opportunity costs are the values of the: a. minimal budgets of families on welfare b. hidden charges passed on to consumers c. monetary costs of goods and services *

Microeconomics. Use the graph below to answer question number 3

More Tutorial at Microeconomics 1. Opportunity costs are the values of the: a. minimal budgets of families on welfare b. hidden charges passed on to consumers c. monetary costs of goods and services *

More Tutorial at Microeconomics 1. Opportunity costs are the values of the: a. minimal budgets of families on welfare b. hidden charges passed on to consumers c. monetary costs of goods and services *

LECTURE February Tuesday, February 19, 13

LECTURE 9 19 February 2013 1 ANNOUNCEMENTS HW 4 due Friday at 11:45 PM Midterm 1 next Monday February 25th 7:30 PM - 8:30 PM in Anderson 270 (not this room) 2 MIDTERM 1: STUDY TOOLS 2 old midterms are

LECTURE 9 19 February 2013 1 ANNOUNCEMENTS HW 4 due Friday at 11:45 PM Midterm 1 next Monday February 25th 7:30 PM - 8:30 PM in Anderson 270 (not this room) 2 MIDTERM 1: STUDY TOOLS 2 old midterms are

Recitation #3 Week from 01/26/09 to 02/01/09

EconS 101, Section 1 Professor Munoz Recitation #3 Week from 01/6/09 to 0/01/09 1. For each of the following situations in the table below, fill in the missing information: first, determine whether this

EconS 101, Section 1 Professor Munoz Recitation #3 Week from 01/6/09 to 0/01/09 1. For each of the following situations in the table below, fill in the missing information: first, determine whether this

Exam 01 - ECON Friday, October 1st

Name: ID: A Exam 01 - ECON 2301-05 - Friday, October 1st 1. Demand is said to be inelastic if the a. quantity demanded changes proportionately the same as price. b. quantity demanded changes proportionately

Name: ID: A Exam 01 - ECON 2301-05 - Friday, October 1st 1. Demand is said to be inelastic if the a. quantity demanded changes proportionately the same as price. b. quantity demanded changes proportionately

1. Suppose that policymakers have been convinced that the market price of cheese is too low.

ECNS 251 Homework 3 Supply & Demand II ANSWERS 1. Suppose that policymakers have been convinced that the market price of cheese is too low. a. Suppose the government imposes a binding price floor in the

ECNS 251 Homework 3 Supply & Demand II ANSWERS 1. Suppose that policymakers have been convinced that the market price of cheese is too low. a. Suppose the government imposes a binding price floor in the

Name Block Date. Three parts: 1) Additional Concept practice; 2) Concept Review Qs; 3) Graphing Review

Additional Concept practice; 2) Concept Review Qs; 3) Graphing Review") Name Block Date Choose-Your-Own S1 Study Adventure AP Microeconomics Three parts: 1) Additional Concept practice; 2) Concept Review Qs; 3) Graphing Review Part 1: Additional concept practice Perfect competition

Name Block Date Choose-Your-Own S1 Study Adventure AP Microeconomics Three parts: 1) Additional Concept practice; 2) Concept Review Qs; 3) Graphing Review Part 1: Additional concept practice Perfect competition

Test your understanding 4.5 (b) 1 2 (a) (c) (b) 4.5 Price controls (c) Introduction to price controls (d) (e) Price controls 3 (a) (b) (c) (d) 4

1 2 (a) (c) (b) 4.5 Price controls (c) Introduction to price controls (d) (e) Price controls 3 (a) (b) (c) (d) 4") Test your understanding 4.5 (b) The government grants a subsidy of 2 1 Why does a subsidy create a welfare (deadweight) loss? 2 (a) Using a diagram showing the cheese market, show equilibrium price and

Test your understanding 4.5 (b) The government grants a subsidy of 2 1 Why does a subsidy create a welfare (deadweight) loss? 2 (a) Using a diagram showing the cheese market, show equilibrium price and

Introduction to Economic Institutions

Introduction to Economic Institutions ECON 1500 Week 3 Lecture 2 13 September 1 / 35 Recap 2 / 35 LAW OF SUPPLY AND DEMAND the price of any good adjusts to bring the quantity supplied and quantity demanded

Introduction to Economic Institutions ECON 1500 Week 3 Lecture 2 13 September 1 / 35 Recap 2 / 35 LAW OF SUPPLY AND DEMAND the price of any good adjusts to bring the quantity supplied and quantity demanded

4. Which of the following statements about marginal revenue for a perfectly competitive firm is incorrect? A) TR

TR") Name: Date: 1. Which of the following will not be true of a perfectly competitive market? A) Buyers and sellers will have an imperceptible effect on the market. B) Firms can freely enter and exit the market.

Name: Date: 1. Which of the following will not be true of a perfectly competitive market? A) Buyers and sellers will have an imperceptible effect on the market. B) Firms can freely enter and exit the market.

1. /20 5. /10 2. /20 6. /10 3. /13 7. /5 4. /30 8. /5 TOTAL /113. Name: Team: Corrected By:

1. /20 5. /10 2. /20 6. /10 3. /13 7. /5 4. /30 8. /5 TOTAL /113 Name: Team: Corrected By: Unit II: Supply, Demand, and Consumer Choice Problem Set #2 1. EXPLAIN an experience or example that shows the

1. /20 5. /10 2. /20 6. /10 3. /13 7. /5 4. /30 8. /5 TOTAL /113 Name: Team: Corrected By: Unit II: Supply, Demand, and Consumer Choice Problem Set #2 1. EXPLAIN an experience or example that shows the

DEMAND AND SUPPLY. Chapter 3. Principles of Macroeconomics by OpenStax College is licensed under a Creative Commons Attribution 3.

DEMAND AND SUPPLY Chapter 3 Principles of Macroeconomics by OpenStax College is licensed under a Creative Commons Attribution 3.0 Unported License Demand for Goods and Services Demand refers to the amount

DEMAND AND SUPPLY Chapter 3 Principles of Macroeconomics by OpenStax College is licensed under a Creative Commons Attribution 3.0 Unported License Demand for Goods and Services Demand refers to the amount

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

HW 2 - Micro - Machiorlatti MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) What is measured by the price elasticity of supply? 1) A) The price

HW 2 - Micro - Machiorlatti MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) What is measured by the price elasticity of supply? 1) A) The price

Eco402 - Microeconomics Glossary By

Eco402 - Microeconomics Glossary By Break-even point : the point at which price equals the minimum of average total cost. Externalities : the spillover effects of production or consumption for which no

Eco402 - Microeconomics Glossary By Break-even point : the point at which price equals the minimum of average total cost. Externalities : the spillover effects of production or consumption for which no

9/24/2008. Visa-VersaVersa

Chapter 4/5 /Supply Def: ability, willingness and desire to purchase a product at all possible prices. Law: The quantity of products demanded will vary inversely with its price. Schedule Graph is abstract,

Chapter 4/5 /Supply Def: ability, willingness and desire to purchase a product at all possible prices. Law: The quantity of products demanded will vary inversely with its price. Schedule Graph is abstract,

Each person demands a washing machine at the price next to their name.

Market for Refurbished Washing Machines Each person demands a washing machine at the price next to their name. Jose $700 Richard $600 Amy $500 Anthony $400 Nathan $300 Darrell $200 Geoffrey $100 Each person

Market for Refurbished Washing Machines Each person demands a washing machine at the price next to their name. Jose $700 Richard $600 Amy $500 Anthony $400 Nathan $300 Darrell $200 Geoffrey $100 Each person

MICROECONOMICS SECTION I. Time - 70 minutes 60 Questions

MICROECONOMICS SECTION I Time - 70 minutes 60 Questions Directions: Each of the questions or incomplete statements below is followed by five suggested answers or completions. Select the one that is best

MICROECONOMICS SECTION I Time - 70 minutes 60 Questions Directions: Each of the questions or incomplete statements below is followed by five suggested answers or completions. Select the one that is best

Unit II: Supply, Demand, and Consumer Choice Problem Set #2

1. /20 4. /30 2. /20 5. /10 3. /10 6. /10 Total: /100 Name: Team: Unit II: Supply, Demand, and Consumer Choice Problem Set #2 1. EXPLAIN an experience or example that shows the real world application of

1. /20 4. /30 2. /20 5. /10 3. /10 6. /10 Total: /100 Name: Team: Unit II: Supply, Demand, and Consumer Choice Problem Set #2 1. EXPLAIN an experience or example that shows the real world application of

Chapter 2. Supply and Demand

Chapter 2 Supply and Demand Reading Assignment for the Week: Finish Chapter 2 Chapter 3 2-2 Copyright 2012 Pearson Addison-Wesley. All rights reserved. Topics 1. Demand. 2. Supply. 3. Market Equilibrium.

Chapter 2 Supply and Demand Reading Assignment for the Week: Finish Chapter 2 Chapter 3 2-2 Copyright 2012 Pearson Addison-Wesley. All rights reserved. Topics 1. Demand. 2. Supply. 3. Market Equilibrium.

P S1 S2 D2 Q D1 P S1 S2 D2 Q D1

This is the solution guide compiled by your instructors of Econ 1101. This is a guide for form A. If you had form B, you can still figure from this guide what the answers to your questions are. If you

This is the solution guide compiled by your instructors of Econ 1101. This is a guide for form A. If you had form B, you can still figure from this guide what the answers to your questions are. If you

Market Forces. Sherif Khalifa. Sherif Khalifa () Market Forces 1 / 62

Market Forces 1 / 62") Sherif Khalifa Sherif Khalifa () Market Forces 1 / 62 Sherif Khalifa () Market Forces 2 / 62 Sherif Khalifa () Market Forces 3 / 62 Sherif Khalifa () Market Forces 4 / 62 Sherif Khalifa () Market Forces

Sherif Khalifa Sherif Khalifa () Market Forces 1 / 62 Sherif Khalifa () Market Forces 2 / 62 Sherif Khalifa () Market Forces 3 / 62 Sherif Khalifa () Market Forces 4 / 62 Sherif Khalifa () Market Forces

MICROECONOMICS Midterm Test (sample)

") Student Name:.. MICROECONOMICS Midterm Test (sample) Time: 60 minutes Student Number:. Total Mark:... /50 Class:. Converted Mark:../10 Section A: QUIZ 20 marks Show your answers on the ANSWER SHEET at

Student Name:.. MICROECONOMICS Midterm Test (sample) Time: 60 minutes Student Number:. Total Mark:... /50 Class:. Converted Mark:../10 Section A: QUIZ 20 marks Show your answers on the ANSWER SHEET at

Chapter 9. Applying the Competitive Model

Chapter 9. Applying the Competitive Model We know that a change in supply curve or demand curve will change the price and quantity. But how does this affect consumers and producers? How much do they lose

Chapter 9. Applying the Competitive Model We know that a change in supply curve or demand curve will change the price and quantity. But how does this affect consumers and producers? How much do they lose

Econ 101, section 3, F06 Schroeter Exam #2, Red. Choose the single best answer for each question.

Econ 101, section 3, F06 Schroeter Exam #2, Red Choose the single best answer for each question. 1. Which of the following is consistent with elastic demand? a. A 10% increase in price results in a 5%

Econ 101, section 3, F06 Schroeter Exam #2, Red Choose the single best answer for each question. 1. Which of the following is consistent with elastic demand? a. A 10% increase in price results in a 5%

Microeconomics. More Tutorial at

Microeconomics Multiple Choice Identify the letter of the choice that best completes the statement or answers the question. 1. A legal maximum price at which a good can be sold is a price a. floor. b.

Microeconomics Multiple Choice Identify the letter of the choice that best completes the statement or answers the question. 1. A legal maximum price at which a good can be sold is a price a. floor. b.

Cosumnes River College Principles of Microeconomics Problem Set 4 Due March 3, 2015

pring 2015 Cosumnes River College rinciples of Microeconomics roblem et 4 ue March 3, 2015 Name: olutions rof. owell Instructions: Write the answers clearly and concisely on these sheets in the spaces

pring 2015 Cosumnes River College rinciples of Microeconomics roblem et 4 ue March 3, 2015 Name: olutions rof. owell Instructions: Write the answers clearly and concisely on these sheets in the spaces

Microeconomics Exam Notes

Microeconomics Exam Notes Opportunity Cost What you give up to get it Production Possibility Frontier Maximum attainable combination of two products (Concept of Opportunity Cost). Main Decision Makers:

Microeconomics Exam Notes Opportunity Cost What you give up to get it Production Possibility Frontier Maximum attainable combination of two products (Concept of Opportunity Cost). Main Decision Makers:

1. Fill in the missing blanks ( XXXXXXXXXXX means that there is nothing to fill in this spot):

:") 1. Fill in the missing blanks ( XXXXXXXXXXX means that there is nothing to fill in this spot): Quantity Total utility Marginal utility 0 0 XXXXXXXXXXX XXXXXXXXXXX XXXXXXXXXXX 200 0 = 200 1 200 XXXXXXXXXXX

1. Fill in the missing blanks ( XXXXXXXXXXX means that there is nothing to fill in this spot): Quantity Total utility Marginal utility 0 0 XXXXXXXXXXX XXXXXXXXXXX XXXXXXXXXXX 200 0 = 200 1 200 XXXXXXXXXXX

LECTURE NOTES ON MICROECONOMICS

LECTURE NOTES ON MICROECONOMICS ANALYZING MARKETS WITH BASIC CALCULUS William M. Boal Part 3: Firms and competition Chapter 12: Welfare analysis Problems (12.1) [Pareto improvement, economic efficiency]

LECTURE NOTES ON MICROECONOMICS ANALYZING MARKETS WITH BASIC CALCULUS William M. Boal Part 3: Firms and competition Chapter 12: Welfare analysis Problems (12.1) [Pareto improvement, economic efficiency]

Microeconomics: MIE1102

TEXT CHAPTERS TOPICS 1, 2 ECONOMICS, ECONOMIC SYSTEMS, MARKET ECONOMY 3 DEMAND AND SUPPLY. MARKET EQUILIBRIUM 4 ELASTICITY OF DEMAND AND SUPPLY 5 DEMAND & CONSUMER BEHAVIOR 6 PRODUCTION FUNCTION 7 COSTS

TEXT CHAPTERS TOPICS 1, 2 ECONOMICS, ECONOMIC SYSTEMS, MARKET ECONOMY 3 DEMAND AND SUPPLY. MARKET EQUILIBRIUM 4 ELASTICITY OF DEMAND AND SUPPLY 5 DEMAND & CONSUMER BEHAVIOR 6 PRODUCTION FUNCTION 7 COSTS

Efficiency and Fairness of Markets

Efficiency and Fairness of Markets Chapter 6 CHAPTER IN PERSPECTIVE In Chapter 6 we study the equilibrium quantities of goods, services, and factors of production to determine if markets are efficient.

Efficiency and Fairness of Markets Chapter 6 CHAPTER IN PERSPECTIVE In Chapter 6 we study the equilibrium quantities of goods, services, and factors of production to determine if markets are efficient.

Chapter 6: Prices Section 1

Chapter 6: Prices Section 1 Objectives 1. Explain how supply and demand create equilibrium in the marketplace. 2. Describe what happens to prices when equilibrium is disturbed. 3. Identify two ways that

Chapter 6: Prices Section 1 Objectives 1. Explain how supply and demand create equilibrium in the marketplace. 2. Describe what happens to prices when equilibrium is disturbed. 3. Identify two ways that