Length: 2 Weeks Chapters: 1 and 2 Assignments: Unit 1 Workbook Problem Sets Vocab NC

|

|

|

- Wesley Boone

- 5 years ago

- Views:

Transcription

1 Length: 2 Weeks Chapters: 1 and 2 Assignments: Unit 1 Workbook Problem Sets Vocab NC

2 What is Economics in General? Economics is the science of scarcity. Scarcity is the condition in which our wants are greater than our limited (scarce) resources. Since we are unable to have everything we desire, we must make choices on how we will use our resources. In economics we will study the choices of individuals, firms, and governments. Economics is the study of. choices

3 Examples: You must choose between buying jeans or buying shoes. Businesses must choose how many people to hire Governments must choose how much to spend on welfare. Economics Defined Economics-Social science concerned with the efficient use of limited resources to achieve maximum satisfaction of economic wants. (Study of how individuals and societies deal with scarcity)

4 "It is not from the benevolence of the butcher, the brewer, or the baker, that we can expect our dinner, but from their regard to their own interest -Adam Smith

Unit 2 MACROeconomics- Study of the large economy as a whole or in its basic")

5 Micro vs. Macro MICROeconomics- Study of small economic units such as individuals, firms, and industries (competitive markets, labor markets, personal decision making, etc.) Unit 2 MACROeconomics- Study of the large economy as a whole or in its basic subdivisions (National Economic Growth, Government Spending, Inflation, Unemployment, etc.) Unit 3-6

6 How is Economics used? Economists use the scientific method to make generalizations and abstractions to develop theories. This is called theoretical economics. These theories are then applied to fix problems or meet economic goals. This is called policy economics. Positive vs. Normative Positive Statements- Based on facts. Avoids value judgments (what is). A fall in incomes will lead to a rise in demand for own-label supermarket foods Normative Statements- Includes value judgments (what ought to be). Pollution is the most serious economic problem

7 What Does Short-Run Mean? EVERYTHING in this class is always in the short-run this time period varies, just always think of it as short like me. The only time this will change for you on a FRQ is if the FRQ specifically states longrun. Same is true for a MCQ You will see the short-run when we cover issues such as aggregates, the short-run prevents our models from reaching market equilibrium.

8 Thinking at the Margin # Times Watching Movie Benefit Cost 1st $30 $10 2nd $15 $10 3rd $5 $10 Total $50 $30 Would you see the movie three times? Notice that the total benefit is more than the total cost but you would NOT watch the movie the 3 rd time.

9 Marginal Analysis In economics the term marginal = additional Thinking on/at the margin, or MARGINAL ANALYSIS involves making decisions based on the additional benefit vs. the additional cost. For Example: You have been shopping at the mall for a half hour, the additional benefit of shopping for an additional half-hour might outweigh the additional cost (the opportunity cost). After three hours, the additional benefit from staying an additional half-hour would likely be less than the additional cost.

10 Marginal Analysis Notice that the decision making process wasn t should I go to the mall for 3 hours or should I stay home In reality the decision making process started with should I go to the mall at all. Once you are there you thought should I stay for an additional half hour or should I go. The MARGINAL ANALYSIS approach to decision making is more comely used than the all or nothing approach.

11 Marginal Analysis Notice that the decision making process wasn t should I go to the mall for 3 hours or should I stay home You will continue to do something until the In reality the decision making process was should I go to the marginal mall at all. cost outweighs the marginal Once you are there you benefit. thought should I stay for an additional half hour or should I go. The MARGINAL ANALYSIS approach to decision making is more comely used than the all or nothing approach.

12 5 Key Economic Assumptions 1. Society s wants are unlimited, but ALL resources are limited (scarcity). 2. Due to scarcity, choices must be made. Every choice has a cost (a trade-off). 3. Everyone s goal is to make choices that maximize their satisfaction. Everyone acts in their own selfinterest. 4. Everyone acts rationally by comparing the marginal costs and marginal benefits of every choice 5. Real-life situations can be explained and analyzed through simplified models and graphs.

13 Analyzing Choices

14 Given the following assumptions, make a rational choice in your own self-interest (hold everything else constant) 1. You want to visit your friend for a week 2. You work every weekday earning $100 per day 3. You have three flights to choose from: Thursday Night Flight = $275 Friday Early Morning Flight = $300 Friday Night Flight = $325 Which flight should you choose? Why?

The most desirable alternative given up as a result of a decision is known as opportunity cost. What are trade-offs of deciding to go to college?")

15 Trade-offs and Opportunity Cost ALL decisions involve trade-offs. Trade-offs are all the alternatives that we give up whenever we choose one course of action over others. (Examples: going to the movies) The most desirable alternative given up as a result of a decision is known as opportunity cost. What are trade-offs of deciding to go to college? What is the opportunity cost of going to college? GEICO assumes you understand opportunity cost. Why?

16 Comparative and Absolute Advantage

17 Opportunity Cost and the Relation to Absolute/Comparative Advantage Opportunity Cost is when what you are giving up to perform a task. How does this relate to Absolute/Comparative Advantage? As a class we will read Introduction to Comparative/Absolute Advantage 17

18 Introduction to Comparative/Absolute Advantage Work with your partner to complete the Problem Set. What you do not get done is homework. We will review this tomorrow. Problem Set

19 Concept review with your partner 1. Define scarcity 2. Define Economics 3. Identify the relationship between scarcity and choices 4. Explain how Macroeconomics is different than Micro 5. Explain the difference between positive and normative economics 6. Identify the 5 main assumptions of Economics 7. Give an example of marginal analysis 8. Name 10 Disney movies

20 Economic Terminology Utility = Satisfaction! Marginal = Additional! Allocate = Distribute! 20

21 Scarcity versus Shortage Scarcity is forever, shortage is just a temporary condition Example: There is a shortage of Ferrari 488 s at the moment BUT a NART Spyder is scarce due to the fact it is no longer being built. Which one is worth more? Why? Lets find out! 21

22 1967 NART Spider 22

pays Cost= Amount seller pays to")

23 Price vs. Cost What s the price? vs. How much does that cost? Price= Amount buyer (or consumer) pays Cost= Amount seller pays to produce a good Investment Investment= the money spent by BUSINESSES to improve their production Ex: $1,000 new computer, $1 Million new factory 23

24 Goods vs. Services Give examples Goods= physical objects that satisfy needs and wants Consumer Goods- created for direct consumption (example: pizza) Capital Goods- created for indirect consumption (oven, blenders, knives, etc.) Goods used to make consumer goods Services= actions or activities that one person performs for another (teaching, cleaning, cooking) 24

25 The 4 Factors of Production 25

26 The Factors of Productions and PPF s

27 The Four Factors of Production Producing goods and services requires the use of resources- DUH!. ALL resources can be classified as one of the following four factors of production: Land Labor Capital Entrepreneurship 27

Labor = Any effort a")

28 The Four Factors of Production Land = All natural resources that are used to produce goods and services. Anything that comes from mother nature. (Water, Sun, Plants, Oil, Trees, Stone, Animals, etc.) Labor = Any effort a person devotes to a task for which that person is paid. (manual laborers, lawyers, doctors, teachers, waiters, etc.) 28

2.")

29 The Four Factors of Production Two Types of Capital: 1. Physical Capital- Any human-made resource that is used to create other goods and services (tools, tractors, machinery, buildings, factories, etc.) 2. Human Capital- Any skills or knowledge gained by a worker through education and experience (college degrees, vocational training, etc.) 29

30 The Four Factors of Production Entrepreneurship= ambitious leaders that combine the other factors of production to create goods and services. Examples-Henry Ford, Bill Gates, Inventors, Store Owners, etc. Entrepreneurs: 1. Take The Initiative 2. Innovate 3. Act as the Risk Bearers So they can obtain. PROFIT Profit = Revenue - Costs 30

31 The Four Factors of Production Classify the Four Factors of Production in the following scenario: You decide to order a pizza to satisfy your wants. First, you picked up the telephone and gave your order to the owner that entered it into her computer. This information came up on the chief baker s monitor in the kitchen and he assigned it to one of his cooks. The cook was busy mixing dough out of salt, flour, eggs, and milk. The cook finished mixing dough, washed his hands in the sink, and prepared your pizza using tomato sauce, cheese, and sausage. He then placed the pizza in the oven. Within 10 minutes the pizza was cooked and placed in a cardboard box. The delivery person then grabbed your pizza, jumped in the company car, and delivered it to your door.

32 The Four Factors of Production Classify the Factors of Production in the following scenario: You decide to order a pizza to satisfy your wants. First, you picked up the telephone and gave your order to the owner that entered it into her computer. This information came up on the chief baker s monitor in the kitchen and he assigned it to one of his cooks. The cook was busy mixing dough out of salt, flour, eggs, and milk. The cook finished mixing dough, washed his hands in the sink, and prepared your pizza using tomato sauce, cheese, and sausage. He then placed the pizza in the oven. Within 10 minutes the pizza was cooked and placed in a cardboard box. The delivery person then grabbed your pizza, jumped in the company car, and delivered it to your door.

33 Accountants vs. Economists Accountants look at only EXPLICIT COSTS. Explicit costs are the traditional out-of pocket costs of decision making. Ex: Going to Disneyland Economists look at the EXPLICIT COSTS and the IMPLICIT COSTS. Implicit costs are the opportunity costs such as forgone time and forgone income. Ex: Payton Manning leaves the NFL to open a taco shop. 33

34 Concept review with partner Explain relationship between scarcity and choices 2. Differentiate between positive & normative 3. Differentiate between price and cost 4. Explain the Invisible Hand of Capitalism 5. Differentiate between consumer and capital goods 6. Give examples of each of the 4 Factors of Production 7. Define tradeoffs 8. Define opportunity cost 9. Differentiate between accounting costs and economic costs 10.Name 10 different teachers at THS. 34

35 Introduction to Production Possibility Curves Problem Set Work with your partner to complete the Problem Set. What you do not get done is homework. We will review this tomorrow.

36 WE HAVE A PROBLEM!! The Economizing Problem Scarcity Society has unlimited wants but limited resources 36

37 The Production Possibilities Curve (PPC) Using Economic Models Step 1: Explain concept in words Step 2: Use numbers as examples Step 3: Generate graphs from numbers Step 4: Make generalizations using graph 37

38 What is the Production Possibilities Curve? A production possibilities graph (PPG) is a model that shows alternative ways that an economy can use its scarce resources This model graphically demonstrates scarcity, trade-offs, opportunity costs, and efficiency. 4 Key Assumptions Only two goods can be produced Full employment of resources Fixed Resources (Ceteris Paribus) Fixed Technology 38

39 Production Possibilities Table A B C D E Bikes (Y) Computers (X) Each point represents a specific combination of goods that can be produced given full employment of resources. NOW GRAPH IT: Put bikes on y-axis and computers on x-axis 39

40 Bikes Production Possibilities How does the PPG graphically demonstrates scarcity, trade-offs, opportunity costs, and efficiency? A B Impossible/Unattainable (given current resources) C G Inefficient/ Unemployment D E Computers Efficient 40

41 Opportunity Cost Example: 1. The opportunity cost of moving from a to b is 2 Bikes 2.The opportunity cost of moving from b to d is 7 Bikes 3.The opportunity cost of moving from d to b is 4 Computer 4.The opportunity cost of moving from f to c is 0 Computers 5.What can you say about point G? Unattainable 41

42 The Production Possibilities Curve (or Frontier) 42

43 Production Possibilities A B C D E CALZONES PIZZA List the Opportunity Cost of moving from a-b, b-c, c-d, and d-e. Constant Opportunity Cost- Resources are easily adaptable for producing either good. Result is a straight line PPC (not common) 43

will increase. Why?")

44 Production Possibilities A B C D E PIZZA ROBOTS List the Opportunity Cost of moving from a-b, b-c, c-d, and d-e. Law of Increasing Opportunity Cost- As you produce more of any good, the opportunity cost (forgone production of another good) will increase. Why? Resources are NOT easily adaptable to producing both goods. Result is a bowed out (Concave) PPC

45 Corn Constant vs. Increasing Opportunity Cost Identify which product would have a straight line PPC and which would be bowed out? Cactus Wheat Pineapples

46 PER UNIT Opportunity Cost How much each marginal unit costs = Opportunity Cost Units Gained Example: 1. The PER UNIT opportunity cost of moving from a to b is 1 Bike 2.The PER UNIT opportunity cost of moving from b to c is 1.5 (3/2) Bikes 3.The PER UNIT opportunity cost of moving from c to d is 2 Bikes 4.The PER UNIT opportunity cost of moving from d to e is 2.5 (5/2) Bikes NOTICE: Increasing Opportunity Costs 46

47 The Production Possibilities Curve and Efficiency 47

48 Two Types of Efficiency Productive Efficiency- Products are being produced in the least costly way. This is any point ON the Production Possibilities Curve Allocative Efficiency- The products being produced are the ones most desired by society. This optimal point on the PPC depends on the desires of society. 48

49 Bikes Productive and Allocative Efficiency Which points are productively efficient? Which are allocatively efficient? A B E G C D F Productively Efficient combinations are A through D Computers Allocative Efficient combinations depend on the wants of society (What if this represents a country with no electricity?) 49

50 Why two types of efficiency? Is combination A efficient? Yes and No. It is productively efficient but it is not the combination society wants Size 20 running shoes A Size 10 running shoes

51 Shifting the Production Possibilities Curve 51

52 Production Possibilities 4 Key Assumptions Revisited Only two goods can be produced Full employment of resources Fixed Resources (4 Factors: LLCE) Fixed Technology What if there is a change? 3 Shifters of the PPC 1. Change in resource quantity or quality 2. Change in Technology 3. Change in Trade 52

53 Robots Production Possibilities What happens if there is an increase in population? Pizzas 53

54 Robots Production Possibilities What happens if there is an increase in population? Pizzas 54

55 Robots Production Possibilities What if there is a technology improvement in pizza ovens Pizzas 55

56 Robots Production Possibilities What if there is a technology improvement in pizza ovens Pizzas 56

57 Capital Goods Capital Goods Capital Goods and Future Growth Countries that produce more capital goods will have more growth in the future. Panama Favors Consumer Goods Mexico Favors Capital Goods Current PPC Future PPC Future PPC Current PPC Consumer goods Consumer goods Panama Mexico 57

58 PPC Practice Draw a PPC showing changes for each of the following: Pizza and Robots (3) 1. New robot making technology 2. Decrease in the demand for pizza 3. Mad cow disease kills 85% of cows Consumer goods and Capital Goods (4) 4. BP Oil Spill in the Gulf 5. Faster computer hardware 6. Many workers unemployed 7. Significant increases in education 58

59 Robots Question #1 New robot making technology Q A shift only for Robots Pizzas Q 59

60 Robots Decrease in the demand for pizza Q Question #2 The curve doesn t shift! A change in demand doesn t shift the curve Pizzas Q 60

61 Robots Question #3 Mad cow disease kills 85% of cows Q A shift inward only for Pizza Pizzas Q 61

62 Capital Goods (Guns) Question #4 Q BP Oil Spill in the Gulf Decrease in resources decrease production possibilities for both Consumer Goods (Butter) Q 62

63 Capital Goods (Guns) Q Question #5 Faster computer hardware Quality of a resource improves shifting the curve outward Consumer Goods (Butter) Q 63

64 Capital Goods (Guns) Q Question #6 Many workers unemployed The curve doesn t shift! Unemployment is just a point inside the curve Consumer Goods (Butter) Q 64

65 Capital Goods (Guns) Significant increases in education Q Question #7 The quality of labor is improved. Curve shifts outward. Consumer Goods (Butter) Q 65

66 Partner Review: Scarcity Bus Ride Scenario: A group of 40 college students get on a bus to go to a dance 30 miles away. Shortly after leaving, the bus finds that it is too heavy to go over a large hill 10 students need to get off the bus You and your partner need to find 5 different ways to decide who should get off the bus. 1. Are any of the solutions fair? 2. How are resources allocated in communism? 3. How are resources allocated in capitalism? 4. What role do prices play in capitalism? 66

")

67 Scarcity Means There Is Not Enough For Everyone Government must step in to help allocate (distribute) resources 67

68 The Four Basic Economic Systems Traditional Based on tradition, custom/culture limited to no growth Command Economy (Centrally Planned) All factors of production are controlled by the Government limited to no growth Free Market Economy (Capitalism) Factors of Production are owned by individuals who make economic choices, NO GOVERNMENT INVOLVEMENT possible high growth, but dangerous Mixed Economy (Free Enterprise) Combo of command/free market growth w/reduced risk 68

69 Every society must answer three questions: The Three Economic Questions 1. What goods and services should be produced? 2. How should these goods and services be produced? 3. Who consumes these goods and services? The way these questions are answered determines the economic system An economic system is the method used by a society to produce and distribute goods and services. 69

70 Centrally-Planned Economies (aka Communism) 70

71 Centrally Planned Economies In a centrally planned economy (communism) the government 1. owns all the resources. 2. decides what to produce, how much to produce, and who will receive it. Examples: Cuba, North Korea, former Soviet Union, and China? Why do centrally planned economies face problems of poor-quality goods, shortages, and unhappy citizens? NO PROFIT MEANS NO INCENTIVE TO W!! 71

72 Irrational Soviet Production Soviet companies were not guided by prices or profit. Gov t officials determined output quotas based on quantitative measurements. Businesses were paid based on meeting these quotas. 1. Why did a business make desk lamps that were filled with lead that were almost too heavy to carry? Production quota based on weight 2. Why did light bulb producers only make tiny night light size bulbs? Production quota based number of bulbs produced 3. Why did oil companies drill many shallow holes when they knew that oil deposits are usually found in deep holes that require slower drilling? Production quota based number of feet drilled 4. Why did a construction superintendent order his workers to remove bathtubs from the first floor and install them in the third floor while he slowly lead inspectors through apartment building. Quota on # of apartments complete at inspection 5. Why did black market vendors sell burned out light bulbs? Business got resources before the public so workers would steal good 72 light bulbs from work and replace them with burnt out bulbs

73 Advantages and Disadvantages What is GOOD about Communism? 1. Low unemploymenteveryone has a job 2. Great Job Securitythe government doesn t go out of business 3. Equal incomes means no extremely poor people 4. Free Health Care What is BAD about Communism? 1. No incentive to work harder 2. No incentive to innovate or come up with good ideas 3. No Competition keeps quality of goods poor. 4. Corrupt leaders 5. Few individual freedoms 73

74 Free Market System (aka Capitalism) 74

75 Characteristics of Free Market 1. Little government involvement in the economy. (Laissez Faire = Let it be) 2. Individuals OWN resources and answer the three economic questions. 3. The opportunity to make PROFIT gives people INCENTIVE to produce quality items efficiently. 4. Wide variety of goods available to consumers. 5. Competition and Self-Interest work together to regulate the economy (keep prices down and quality up). 75

76 Example of Free Market Example of how the free market regulates itself: If consumers want computers and only one company is making them Other businesses have the INCENTIVE to start making computers to earn PROFIT. This leads to more COMPETITION. Which means lower prices, better quality, and more product variety. We produce the goods and services that society wants because resources follow profits. The End Result: Most efficient production of the goods that consumers want, produced at the lowest prices and the highest quality. 76

77 Example of Communism Example of why communism failed: If consumers want computers and only one company is making them Other businesses CANNOT start making computers. There is NO COMPETITION. Which means higher prices, lower quality, and less product variety. More computers will not be made until the government decides to create a new factory. The End Result: There is a shortage of goods that consumers want, produced at the highest prices and the lowest quality. 77

78 The Invisible Hand The concept that society s goals will be met as individuals seek their own self-interest. Example: Society wants fuel efficient cars Profit seeking producers will make more. Competition between firms results in low prices, high quality, and greater efficiency. The government doesn t need to get involved since the needs of society are automatically met. Competition and self-interest act as an invisible hand that regulates the free market. 78

79 The Invisible Hand!!! 79

80 Attacks Against Capitalism 1. Companies are greedy and do anything to screw over consumers! Companies have an incentive to satisfy the needs of consumers. If they don t they will go out of business. 2. Capitalism causes companies to outsource US jobs overseas. America suffers because companies want more profit! How many of you lost your job to outsourcing? How many of you benefit in the form of lower prices? 3. Capitalism only helps the rich. US companies enslave and exploit third-world workers in sweatshops! Sweatshop workers are not forced labor. They make the decision to work there voluntarily. Why? Although the working conditions are far below US standards, working in a sweatshop is better that the alternative Sweatshop wages in Vietnam, Honduras, and Nicaragua are more than double the country s average wage. 80

81 Sweatshops Then Sweatshops Now Sweatshops "My concern is not that there are too many sweatshops, but that there are too few." -Jeffrey Sachs, Harvard University Question: Who is to blame for these people being so poor? Answer: Low productivity. If a country doesn t produce very much, it can afford to pay it s workers very much. Why do these countries have such low productivity? Corrupt governments, inadequate physical capital and infrastructure, and underdeveloped human capital. What does foreign investment bring to poor countries? 81

82 Capital Goods Capital Goods Connection to the PPC Communism in the Long Run Free Markets in the Long Run CURRENT CURVE FUTURE CURVE FUTURE CURVE CURRENT CURVE Consumer goods Cuba Consumer goods Puerto Rico 82

83 The Difference Between Capitalism and Communism North Korea and South Korea at Night North Korea's GDP is $40 Billion South Korea's GDP is $1.3 Trillion (32 times greater).

84 The Circular Flow Model The Product Market- The place where goods and services produced by businesses are sold to households. The Resource (Factor) Market- The place where resources (land, labor, capital, and rent.) are sold to businesses. 84

85 DEMAND Resource Market SUPPLY Businesses Individuals SUPPLY Product Market 85 DEMAND

86 Introduction to Circular-Flow Work with your partner to complete the Problem Set. Model Problem Set What you do not get done is homework. We will review this tomorrow.

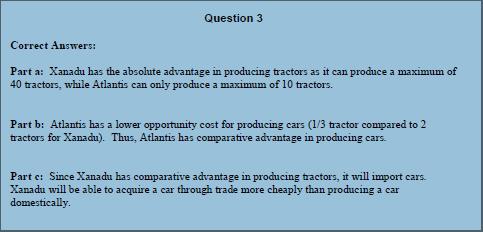

87 AP Microeconomics Exam 2003, #3 Complete the FRQ in your notes 87

88 Use the OOO Method! Tractors Cars Atlantis 10 (1T = 30/10C) 30 (1C =10/30T) Xanadu 40 (1T = 20/40C) 20 (1C = 40/20T) A.Xanadu B.Atlantis C.Xanadu 88

89 89

Unit I: Basic Economic Concepts

Unit I: Basic Economic Concepts What is Economics in General? Economics is the science of scarcity. Scarcity is the condition in which our wants are greater than our limited resources. Since we are unable

Unit I: Basic Economic Concepts What is Economics in General? Economics is the science of scarcity. Scarcity is the condition in which our wants are greater than our limited resources. Since we are unable

Unit I: Basic Economic Concepts

Unit I: Basic Economic Concepts What is Economics in General? Economics is the science of scarcity. Scarcity is the condition in which our wants are greater than our limited resources. Since we are unable

Unit I: Basic Economic Concepts What is Economics in General? Economics is the science of scarcity. Scarcity is the condition in which our wants are greater than our limited resources. Since we are unable

Marginal Analysis. Thinking on the Margin. This is what you do when you make a decision. You weigh your options, and make a choice.

1 Marginal Analysis 6 Thinking on the Margin This is what you do when you make a decision. You weigh your options, and make a choice. If I do this, then I can t do that is it worth it? 7 Marginal Analysis

1 Marginal Analysis 6 Thinking on the Margin This is what you do when you make a decision. You weigh your options, and make a choice. If I do this, then I can t do that is it worth it? 7 Marginal Analysis

Economics. Econ, Econ. Econ

Economics Econ, Econ Econ Introduction to Economics I WON THE LOTTERY! I ll give you anything you want other than money. What do you want? Would your list ever end? Why not? Scarcity!!! What is Economics?

Economics Econ, Econ Econ Introduction to Economics I WON THE LOTTERY! I ll give you anything you want other than money. What do you want? Would your list ever end? Why not? Scarcity!!! What is Economics?

SCARCITY: THREE BASIC QUESTIONS

ECONOMIC SYSTEMS SCARCITY: THREE BASIC QUESTIONS All societies experience scarcity which requires them to make choices, so they must answer three fundamental questions: 1. WHAT to produce? E.g., food,

ECONOMIC SYSTEMS SCARCITY: THREE BASIC QUESTIONS All societies experience scarcity which requires them to make choices, so they must answer three fundamental questions: 1. WHAT to produce? E.g., food,

Unit 1: Basic Economic Concepts

Unit 1: Basic Economic Concepts 1 REVIEW 1. Explain relationship between scarcity and choices 2. Differentiate between positive & normative 3. Differentiate between price and cost \ 4. Differentiate between

Unit 1: Basic Economic Concepts 1 REVIEW 1. Explain relationship between scarcity and choices 2. Differentiate between positive & normative 3. Differentiate between price and cost \ 4. Differentiate between

How do we construct and interpret Production Possibility Curves?

How do we construct and interpret Production Possibility Curves? Do Now: Describe any costs associated with taking AP classes as opposed to Regents level classes. 1 I. The Economizing Problem Scarcity

How do we construct and interpret Production Possibility Curves? Do Now: Describe any costs associated with taking AP classes as opposed to Regents level classes. 1 I. The Economizing Problem Scarcity

Unit I: Basic Economic Concepts

Unit I: Basic Economic Concepts What is Economics in General? Economics is the science of scarcity. Scarcity is the condition in which our wants are greater than our limited resources. Since we are unable

Unit I: Basic Economic Concepts What is Economics in General? Economics is the science of scarcity. Scarcity is the condition in which our wants are greater than our limited resources. Since we are unable

Economic Systems. Economies and Circular Flow

Economies and Circular Flow Every society must answer three questions: The Three Economic Questions 1. What goods and services should be produced? 2. How should these goods and services be produced? 3.

Economies and Circular Flow Every society must answer three questions: The Three Economic Questions 1. What goods and services should be produced? 2. How should these goods and services be produced? 3.

CH 1: Economics and Economic Reasoning

CH 1: Economics and Economic Reasoning What is Economics? Economics is the study of how human beings coordinate their wants and desires, given the decision-making mechanism, social customs, and political

CH 1: Economics and Economic Reasoning What is Economics? Economics is the study of how human beings coordinate their wants and desires, given the decision-making mechanism, social customs, and political

Micro Unit 1, Lesson 1 (one day)

") Micro Unit 1, Lesson 1 (one day) ECONOMICS: Concerned with the efficient use and management of limited productive resources to achieve maximum satisfaction of human material wants. ECONOMICS: The study

Micro Unit 1, Lesson 1 (one day) ECONOMICS: Concerned with the efficient use and management of limited productive resources to achieve maximum satisfaction of human material wants. ECONOMICS: The study

Exam#1 Review Economics:

Exam#1 Review Economics: Social Science; Study of choices Resources Renewable Nonrenewable Wants Scarcity Because of scarcity socities and economies have to answer the 3 major economic questions Limited

Exam#1 Review Economics: Social Science; Study of choices Resources Renewable Nonrenewable Wants Scarcity Because of scarcity socities and economies have to answer the 3 major economic questions Limited

Economics is the social science concerned with how individuals, institutions, and society make optimal (best) choices under conditions of scarcity.

choices under conditions of scarcity.") Chapter 1: Limits, Alternatives, and Choices Learning objectives: List the ten key concepts to retain for a lifetime. Define economics and the features of the economic way of thinking. Describe the role

Chapter 1: Limits, Alternatives, and Choices Learning objectives: List the ten key concepts to retain for a lifetime. Define economics and the features of the economic way of thinking. Describe the role

Unit One, Day One (pages 6-20, 28) ECONOMICS: The study of how limited productive resources are efficiently allocated in a world of unlimited wants.

ECONOMICS: The study of how limited productive resources are efficiently allocated in a world of unlimited wants.") Unit One, Day One (pages 6-20, 28) ECONOMICS: The study of how limited productive resources are efficiently allocated in a world of unlimited wants. SCARCITY: WANTS EXCEED RESOURCES We want more than we

Unit One, Day One (pages 6-20, 28) ECONOMICS: The study of how limited productive resources are efficiently allocated in a world of unlimited wants. SCARCITY: WANTS EXCEED RESOURCES We want more than we

Got stuff? I. The Economic Problem. Chapter 1: The Economic Way of Thinking

Chapter 1: The Economic Way of Thinking The Economic Problem Production Possibilities Economic Analysis Got stuff? Who made it? How was it made? How did you get it? I. The Economic Problem the basic economic

Chapter 1: The Economic Way of Thinking The Economic Problem Production Possibilities Economic Analysis Got stuff? Who made it? How was it made? How did you get it? I. The Economic Problem the basic economic

A.P. Microeconomics. In Class Review #1 Economic Principles & Systems

A.P. Microeconomics In Class Review #1 Economic Principles & Systems Micro vs. Macro Economics: study decisions and use of resources Micro: study decisions of small units (households & firms) Macro: study

A.P. Microeconomics In Class Review #1 Economic Principles & Systems Micro vs. Macro Economics: study decisions and use of resources Micro: study decisions of small units (households & firms) Macro: study

The Foundations of Economics. Chapter 1

The Foundations of Economics Chapter 1 A Social Science Study of people in society and how they interact with each other Earth= Finite have limited resources use resources to produce goods and services

The Foundations of Economics Chapter 1 A Social Science Study of people in society and how they interact with each other Earth= Finite have limited resources use resources to produce goods and services

Economics is the study of how society manages and allocates its scarce resources. Scarcity refers to society s limited number of resources

Economics Notes 10 Lessons From Economics Chapter 1 What is Economics? Economics is the study of how society manages and allocates its scarce resources. Scarcity refers to society s limited number of resources

Economics Notes 10 Lessons From Economics Chapter 1 What is Economics? Economics is the study of how society manages and allocates its scarce resources. Scarcity refers to society s limited number of resources

+ What is Economics? societies use scarce resources to produce valuable commodities and distribute them among different people

ECONOMICS The word economy comes from a Greek word oikonomia for one who manages a household. is the study of how society manages its scarce resources. Traditionally land, labor, and capital resources

ECONOMICS The word economy comes from a Greek word oikonomia for one who manages a household. is the study of how society manages its scarce resources. Traditionally land, labor, and capital resources

Full file at

CHAPTER 2 Economic Activities: Producing and Trading Chapter 2 introduces the basics of the PPF, comparative advantage, and trade. This is not exactly a tools of economics chapter; instead it explores

CHAPTER 2 Economic Activities: Producing and Trading Chapter 2 introduces the basics of the PPF, comparative advantage, and trade. This is not exactly a tools of economics chapter; instead it explores

FOR YOUR REVIEW ANSWER KEY

FOR YOUR REVIEW ANSWER KEY CHAPTER 2 SCARCITY, TRADE-OFFS, AND PRODUCTION POSSIBILITIES SECTION 2.1 THE PRODUCTION POSSIBILITIES CURVE 1. a. b. 1 side of beef; 6 kegs of beer; 9 kegs of beer c. 35 kegs

FOR YOUR REVIEW ANSWER KEY CHAPTER 2 SCARCITY, TRADE-OFFS, AND PRODUCTION POSSIBILITIES SECTION 2.1 THE PRODUCTION POSSIBILITIES CURVE 1. a. b. 1 side of beef; 6 kegs of beer; 9 kegs of beer c. 35 kegs

Mr Sydney Armstrong ECN 1100 Introduction to Microeconomic Lecture Note (2)

") Mr Sydney Armstrong ECN 1100 Introduction to Microeconomic Lecture Note (2) Economics Systems The market System The private ownership of resources and the use of markets and prices to coordinate and direct

Mr Sydney Armstrong ECN 1100 Introduction to Microeconomic Lecture Note (2) Economics Systems The market System The private ownership of resources and the use of markets and prices to coordinate and direct

Economics for Business Decision Making

Week 1: Explain that: People are rational Consumers and firms use as much of the available information as they can to achieve their goals rational individuals weigh the benefits and costs of each action,

Week 1: Explain that: People are rational Consumers and firms use as much of the available information as they can to achieve their goals rational individuals weigh the benefits and costs of each action,

Ch. 1 LECTURE NOTES Learning objectives II. Definition of Economics III. The Economic Perspective CONSIDER THIS Free for All?

Ch. 1 LECTURE NOTES I. Learning objectives In this chapter students will learn: A. The definitions of economics and the features of the economic perspective. B. The role of economic theory in economics.

Ch. 1 LECTURE NOTES I. Learning objectives In this chapter students will learn: A. The definitions of economics and the features of the economic perspective. B. The role of economic theory in economics.

Reading Essentials and Study Guide

Lesson 3 Using Economic Models ESSENTIAL QUESTION In what ways do people cope with the problem of scarcity? Reading HELPDESK Academic Vocabulary mechanism process or means by which something can be accomplished

Lesson 3 Using Economic Models ESSENTIAL QUESTION In what ways do people cope with the problem of scarcity? Reading HELPDESK Academic Vocabulary mechanism process or means by which something can be accomplished

Economics Unit 1 Exam Scarcity and Economic Reasoning

Economics Unit 1 Exam Scarcity and Economic Reasoning Multiple Choice (2 points each) Identify the choice that best completes the statement or answers the question. Directions: Use the chart below to answer

Economics Unit 1 Exam Scarcity and Economic Reasoning Multiple Choice (2 points each) Identify the choice that best completes the statement or answers the question. Directions: Use the chart below to answer

- Scarcity leads to tradeoffs - Normative statements=opinion - Positive statement=fact with evidence - An economic model is tested by comparing its

Macroeconomics Final Notes: CHAPTER 1: What is economics? We want more than we can get. Our inability to satisfy all of our wants is called scarcity. All resources are finite even if they are abundant.

Macroeconomics Final Notes: CHAPTER 1: What is economics? We want more than we can get. Our inability to satisfy all of our wants is called scarcity. All resources are finite even if they are abundant.

Test Yourself: Basic Terminology. If all economists were laid end to end, they would still not reach a conclusion. GB Shaw

Test Yourself: Basic Terminology If all economists were laid end to end, they would still not reach a conclusion. GB Shaw What is economics? What is macroeconomics? What is microeconomics? Economics is

Test Yourself: Basic Terminology If all economists were laid end to end, they would still not reach a conclusion. GB Shaw What is economics? What is macroeconomics? What is microeconomics? Economics is

Name Economics: Unit One Study Guide Unit One Standards

Name Economics: Unit One Study Guide Unit One Standards Fundamental Economic Concepts SSEF1: The student will explain why limited productive resources and unlimited wants result in scarcity, opportunity

Name Economics: Unit One Study Guide Unit One Standards Fundamental Economic Concepts SSEF1: The student will explain why limited productive resources and unlimited wants result in scarcity, opportunity

WHAT IS ECONOMICS? Understanding Economics Chapter 1

WHAT IS ECONOMICS? Understanding Economics Chapter 1 Chapter 1, Lesson 1 Scarcity and the Science of Economics Needs vs. Wants! Need a basic requirement for survival, such as food, clothing and shelter.!

WHAT IS ECONOMICS? Understanding Economics Chapter 1 Chapter 1, Lesson 1 Scarcity and the Science of Economics Needs vs. Wants! Need a basic requirement for survival, such as food, clothing and shelter.!

Reading Essentials and Study Guide

Lesson 3 Using Economic Models ESSENTIAL QUESTION In what ways do people cope with the problem of scarcity? Reading HELPDESK Academic Vocabulary mechanism process or means by which something can be accomplished

Lesson 3 Using Economic Models ESSENTIAL QUESTION In what ways do people cope with the problem of scarcity? Reading HELPDESK Academic Vocabulary mechanism process or means by which something can be accomplished

ECON MACROECONOMIC PRINCIPLES Instructor: Dr. Juergen Jung Towson University. J.Jung Chapter Introduction Towson University 1 / 69

ECON 202 - MACROECONOMIC PRINCIPLES Instructor: Dr. Juergen Jung Towson University J.Jung Chapter 2-4 - Introduction Towson University 1 / 69 Disclaimer These lecture notes are customized for the Macroeconomics

ECON 202 - MACROECONOMIC PRINCIPLES Instructor: Dr. Juergen Jung Towson University J.Jung Chapter 2-4 - Introduction Towson University 1 / 69 Disclaimer These lecture notes are customized for the Macroeconomics

REVIEW FOR TEST I (Chapters 1-4 of Case, Fair, Oster text) HCCS Spring Branch Campus Instructor: J.H. Ewing. What Economics is About

HCCS Spring Branch Campus Instructor: J.H. Ewing. What Economics is About") REVIEW FOR TEST I (Chapters 1-4 of Case, Fair, Oster text) HCCS Spring Branch Campus Instructor: J.H. Ewing What Economics is About Economics deals with the human condition that arises when Wants > Limited

REVIEW FOR TEST I (Chapters 1-4 of Case, Fair, Oster text) HCCS Spring Branch Campus Instructor: J.H. Ewing What Economics is About Economics deals with the human condition that arises when Wants > Limited

Section 1 Guided Reading and Practice: Basic Economic Concepts

Name AP ECONOMICS Section 1 Guided Reading and Practice: Basic Economic Concepts Module 1: The Study of Economics (pages 2-9) - Define 1. Terms: a. economics b. individual choice c. economy d. market economy

Name AP ECONOMICS Section 1 Guided Reading and Practice: Basic Economic Concepts Module 1: The Study of Economics (pages 2-9) - Define 1. Terms: a. economics b. individual choice c. economy d. market economy

Unit 1. Economic Fundamentals. Module 1. Krugman, pp What is Economics? The Fundamental Economic Problem

Unit 1 Economic Fundamentals Module 1 Krugman, pp. 2-21 What is Economics? The Fundamental Economic Problem 1 Unlimited Wants Scarce Resources What do economists study? How people make choices. 2 How do

Unit 1 Economic Fundamentals Module 1 Krugman, pp. 2-21 What is Economics? The Fundamental Economic Problem 1 Unlimited Wants Scarce Resources What do economists study? How people make choices. 2 How do

Opportunity Cost. First quiz on Monday. Your First Job Ten Principles Scarcity Opportunity Cost. Fundamental Economic Concepts and Reasoning

Opportunity Cost First quiz on Monday. Your First Job Ten Principles Scarcity Opportunity Cost Fundamental Economic Concepts and Reasoning But first, a review of scarcity https://www.youtube.com/watch?v=np-dzsdzymk&li

Opportunity Cost First quiz on Monday. Your First Job Ten Principles Scarcity Opportunity Cost Fundamental Economic Concepts and Reasoning But first, a review of scarcity https://www.youtube.com/watch?v=np-dzsdzymk&li

Chapter 1: What is Economics? A. Economic questions arise because we face scarcity we all want more than we can get.

Chapter 1: What is Economics? I. Definition of Economics A. Economic questions arise because we face scarcity we all want more than we can get. 1. Because we are unable to satisfy all of our wants, we

Chapter 1: What is Economics? I. Definition of Economics A. Economic questions arise because we face scarcity we all want more than we can get. 1. Because we are unable to satisfy all of our wants, we

Understanding Economics

Understanding Economics 4 th edition by Mark Lovewell, Khoa Nguyen and Brennan Thompson Chapter 1 The Economic Problem Learning Objectives In this chapter, you will: 1. consider the economic problem that

Understanding Economics 4 th edition by Mark Lovewell, Khoa Nguyen and Brennan Thompson Chapter 1 The Economic Problem Learning Objectives In this chapter, you will: 1. consider the economic problem that

Economics. Turn in your Career Packet. All assignments in Google Classroom should be submitted by this time.

Economics Turn in your Career Packet. All assignments in Google Classroom should be submitted by this time. We are going to start this morning with our Interview Challenge after the QOD. Your first assessment

Economics Turn in your Career Packet. All assignments in Google Classroom should be submitted by this time. We are going to start this morning with our Interview Challenge after the QOD. Your first assessment

The Foundations of Microeconomics

The Foundations of Microeconomics D I A N N A D A S I L V A - G L A S G O W D E P A R T M E N T O F E C O N O M I C S U N I V E R S I T Y O F G U Y A N A 1 4 S E P T E M B E R, 2 0 1 7 Wk 3 Lectures I

The Foundations of Microeconomics D I A N N A D A S I L V A - G L A S G O W D E P A R T M E N T O F E C O N O M I C S U N I V E R S I T Y O F G U Y A N A 1 4 S E P T E M B E R, 2 0 1 7 Wk 3 Lectures I

WEEK 4: Economics: Foundations and Models

WEEK 4: Economics: Foundations and Models Economics: study of the choices people and societies make to attain their unlimited wants, given their scarce resources Market: group of buyers and seels of good

WEEK 4: Economics: Foundations and Models Economics: study of the choices people and societies make to attain their unlimited wants, given their scarce resources Market: group of buyers and seels of good

CURRICULUM COURSE OUTLINE

CURRICULUM COURSE OUTLINE Course Name(s): Grade(s): 11-12 Department: Course Length: Pre-requisite: Microeconomics Social Studies 1 Semester Teacher Approved Textbook/Key Resource: McConnell and Brue Microeconomics

CURRICULUM COURSE OUTLINE Course Name(s): Grade(s): 11-12 Department: Course Length: Pre-requisite: Microeconomics Social Studies 1 Semester Teacher Approved Textbook/Key Resource: McConnell and Brue Microeconomics

Bremen School District 228 Social Studies Common Assessment 2: Midterm

Bremen School District 228 Social Studies Common Assessment 2: Midterm AP Microeconomics 55 Minutes 60 Questions Directions: Each of the questions or incomplete statements in this exam is followed by five

Bremen School District 228 Social Studies Common Assessment 2: Midterm AP Microeconomics 55 Minutes 60 Questions Directions: Each of the questions or incomplete statements in this exam is followed by five

Unit 5: The Resource Market. (The Factor Market or Input Market)

") Unit 5: The Resource Market (The Factor Market or Input Market) 1 2 The Circular Flow Model The Product Market- The place where goods and services produced by businesses are sold to households. The Resource

Unit 5: The Resource Market (The Factor Market or Input Market) 1 2 The Circular Flow Model The Product Market- The place where goods and services produced by businesses are sold to households. The Resource

Full file at https://fratstock.eu

CHAPTER 2 THE PRODUCTION POSSIBILITIES FRONTIER FRAMEWORK OF ANALYSIS Chapter 2 introduces the basics of the PPF, comparative advantage, and trade. This is not exactly a tools of economics chapter; instead

CHAPTER 2 THE PRODUCTION POSSIBILITIES FRONTIER FRAMEWORK OF ANALYSIS Chapter 2 introduces the basics of the PPF, comparative advantage, and trade. This is not exactly a tools of economics chapter; instead

INTRODUCTION TO ECONOMICS

INTRODUCTION TO ECONOMICS Instructor: Ghislain Nono Gueye AUBURN UNIVERSITY 1 The basic economic problem - Scarcity All human beings have various needs (e.g. hunger, thirst, education, etc) All their needs

INTRODUCTION TO ECONOMICS Instructor: Ghislain Nono Gueye AUBURN UNIVERSITY 1 The basic economic problem - Scarcity All human beings have various needs (e.g. hunger, thirst, education, etc) All their needs

PRINCIPLES OF MACROECONOMICS. Chapter 1 Welcome to Economics!

PRINCIPLES OF MACROECONOMICS Chapter 1 Welcome to Economics! 2 Chapter Outline 1.1 Three Key Economic Ideas 1.2 The Economic Problem That Every Society Must Solve 1.3 Economic Models 1.4 Microeconomics

PRINCIPLES OF MACROECONOMICS Chapter 1 Welcome to Economics! 2 Chapter Outline 1.1 Three Key Economic Ideas 1.2 The Economic Problem That Every Society Must Solve 1.3 Economic Models 1.4 Microeconomics

Choice, Opportunity Costs, and Specialization

CHAPTER 2 (MACRO CHAPTER 2; MICRO CHAPTER 2) Choice, Opportunity Costs, and Specialization FUNDAMENTAL QUESTIONS 1. What are opportunity costs? Are they part of the economic way of thinking? 2. What is

CHAPTER 2 (MACRO CHAPTER 2; MICRO CHAPTER 2) Choice, Opportunity Costs, and Specialization FUNDAMENTAL QUESTIONS 1. What are opportunity costs? Are they part of the economic way of thinking? 2. What is

Principles of BABY THOMAS 2016

Principles of 1 UNIT I INTRODUCTION TO MACROECONOMICS Learning Objectives 1. Introduction to economics, meaning and definition of economics, Principles of economics 2. Economic models, the circular flow

Principles of 1 UNIT I INTRODUCTION TO MACROECONOMICS Learning Objectives 1. Introduction to economics, meaning and definition of economics, Principles of economics 2. Economic models, the circular flow

Chapter 1 Scarcity, Choice, and Opportunity Costs

Chapter 1 Scarcity, Choice, and Opportunity Costs After reading Chapter 1, SCARCITY, CHOICE, AND OPPORTUNITY COSTS, you should be able to: Define Economics. Identify and explain the major themes in studying

Chapter 1 Scarcity, Choice, and Opportunity Costs After reading Chapter 1, SCARCITY, CHOICE, AND OPPORTUNITY COSTS, you should be able to: Define Economics. Identify and explain the major themes in studying

Principles of Microeconomics, 11e -TB1 (Case/Fair/Oster) Chapter 2 The Economic Problem: Scarcity and Choice

Chapter 2 The Economic Problem: Scarcity and Choice") Principles of Microeconomics, 11e -TB1 (Case/Fair/Oster) Chapter 2 The Economic Problem: Scarcity and Choice 2.1 Scarcity, Choice, and Opportunity Cost 1) The process by which resources are transformed

Principles of Microeconomics, 11e -TB1 (Case/Fair/Oster) Chapter 2 The Economic Problem: Scarcity and Choice 2.1 Scarcity, Choice, and Opportunity Cost 1) The process by which resources are transformed

Scarcity and the Factors of Production. What is economics? How do economists define scarcity? What are the three factors of production?

Scarcity and the Factors of Production What is economics? How do economists define scarcity? What are the three factors of production? What Is Economics? Economics is the study of how people make choices

Scarcity and the Factors of Production What is economics? How do economists define scarcity? What are the three factors of production? What Is Economics? Economics is the study of how people make choices

CHAPTER 2 Production Possibilities Frontier Framework

CHAPTER 2 Production Possibilities Frontier Framework Chapter 2 introduces the basics of the PPF, comparative advantage, and trade. This is not exactly a tools of economics chapter; instead it explores

CHAPTER 2 Production Possibilities Frontier Framework Chapter 2 introduces the basics of the PPF, comparative advantage, and trade. This is not exactly a tools of economics chapter; instead it explores

Click to return to In this Lesson

In This Lesson I Chapter 1 What Economics is About Paul Schneiderman, Ph.D., Professor of Finance & Economics, Southern New Hampshire University 2011 South Western/Cengage Learning Goods and Bads and Resources

In This Lesson I Chapter 1 What Economics is About Paul Schneiderman, Ph.D., Professor of Finance & Economics, Southern New Hampshire University 2011 South Western/Cengage Learning Goods and Bads and Resources

Principles of Microeconomics , 10e (Case/Fair/Oster) TB2 Chapter 2 The Economic Problem: Scarcity and Choice

TB2 Chapter 2 The Economic Problem: Scarcity and Choice") Principles of Microeconomics, 10e (Case/Fair/Oster) TB2 Chapter 2 The Economic Problem: Scarcity and Choice 2.1 Scarcity, Choice, and Opportunity Cost 1) Production is the process by which A) products

Principles of Microeconomics, 10e (Case/Fair/Oster) TB2 Chapter 2 The Economic Problem: Scarcity and Choice 2.1 Scarcity, Choice, and Opportunity Cost 1) Production is the process by which A) products

INTI COLLEGE MALAYSIA FOUNDATION IN BUSINESS INFORMATION TECHNOLOGY (CFP) ECO105: ECONOMICS 1 FINAL EXAMINATION: JANUARY 2006 SESSION

ECO105: ECONOMICS 1 FINAL EXAMINATION: JANUARY 2006 SESSION") ECO105 (F) / Page 1 of 12 Section A INTI COLLEGE MALAYSIA FOUNDATION IN BUSINESS INFORMATION TECHNOLOGY (CFP) ECO105: ECONOMICS 1 FINAL EXAMINATION: JANUARY 2006 SESSION Instructions: This section consists

ECO105 (F) / Page 1 of 12 Section A INTI COLLEGE MALAYSIA FOUNDATION IN BUSINESS INFORMATION TECHNOLOGY (CFP) ECO105: ECONOMICS 1 FINAL EXAMINATION: JANUARY 2006 SESSION Instructions: This section consists

ECON 101 MIDTERM 1 REVIEW SESSION SOLUTIONS (WINTER 2015) BY BENJI HUANG

BY BENJI HUANG") ECON 101 MIDTERM 1 REVIEW SESSION SOLUTIONS (WINTER 2015) BY BENJI HUANG TABLE OF CONTENT I. CHAPTER 1: WHAT IS ECONOMICS II. CHAPTER 2: THE ECONOMIC PROBLEM III. CHAPTER 3: DEMAND AND SUPPLY IV. CHAPTER

ECON 101 MIDTERM 1 REVIEW SESSION SOLUTIONS (WINTER 2015) BY BENJI HUANG TABLE OF CONTENT I. CHAPTER 1: WHAT IS ECONOMICS II. CHAPTER 2: THE ECONOMIC PROBLEM III. CHAPTER 3: DEMAND AND SUPPLY IV. CHAPTER

Scarcity and the Factors of Production

Scarcity and the Factors of Production What is economics? How do economists define scarcity? What are the three factors of production? What Is Economics? Economics is the study of how people make choices

Scarcity and the Factors of Production What is economics? How do economists define scarcity? What are the three factors of production? What Is Economics? Economics is the study of how people make choices

Principles of Macroeconomics, 11e - TB1 (Case/Fair/Oster) Chapter 2 The Economic Problem: Scarcity and Choice

Chapter 2 The Economic Problem: Scarcity and Choice") Principles of Macroeconomics, 11e - TB1 (Case/Fair/Oster) Chapter 2 The Economic Problem: Scarcity and Choice 2.1 Scarcity, Choice, and Opportunity Cost 1) The process by which resources are transformed

Principles of Macroeconomics, 11e - TB1 (Case/Fair/Oster) Chapter 2 The Economic Problem: Scarcity and Choice 2.1 Scarcity, Choice, and Opportunity Cost 1) The process by which resources are transformed

Unit 1: Fundamentals of Economics Notes

Economics: Problem of Scarcity Economics study of how people & societies choose to use limited resources to satisfy their needs & unlimited wants #1 ongoing problem that all economists face is SCARCITY!!!!!!!!!!!!

Economics: Problem of Scarcity Economics study of how people & societies choose to use limited resources to satisfy their needs & unlimited wants #1 ongoing problem that all economists face is SCARCITY!!!!!!!!!!!!

In this chapter, look for the answers to these questions

In this chapter, look for the answers to these questions What are economists two roles? How do they differ? What are models? How do economists use them? What are the elements of the Circular-Flow Diagram?

In this chapter, look for the answers to these questions What are economists two roles? How do they differ? What are models? How do economists use them? What are the elements of the Circular-Flow Diagram?

Production Possibilities, Opportunity Cost, and Economic Growth

Chapter 2 Production Possibilities, Opportunity Cost, and Economic Growth CHAPTER SUMMARY The What, How and For Whom questions are introduced as the fundamental economic questions that must be addressed

Chapter 2 Production Possibilities, Opportunity Cost, and Economic Growth CHAPTER SUMMARY The What, How and For Whom questions are introduced as the fundamental economic questions that must be addressed

Basic Economic Concepts. Section 1 Module 1 The Study of Economics

Basic Economic Concepts Section 1 Module 1 The Study of Economics THERE IS NO SUCH THING AS A FREE LUNCH Basically, this means that there is a cost to everything. Even though someone might get something

Basic Economic Concepts Section 1 Module 1 The Study of Economics THERE IS NO SUCH THING AS A FREE LUNCH Basically, this means that there is a cost to everything. Even though someone might get something

EC 201 Lecture Notes 1 Page 1 of 1

EC 201 Lecture Notes 1 Page 1 of 1 ECON 201 - Macroeconomics Lecture Notes 1 Metropolitan State University Allen Bellas The textbooks for this course are Macroeconomics: Principles and Policy by William

EC 201 Lecture Notes 1 Page 1 of 1 ECON 201 - Macroeconomics Lecture Notes 1 Metropolitan State University Allen Bellas The textbooks for this course are Macroeconomics: Principles and Policy by William

Josh = 7 bananas an hour x 8 hours = 56 bananas Sarah = 4 bananas an hour x 8 hours = 32 bananas

www.liontutors.com ECON 102 Brown Exam 1 Practice Exam Solutions 1. C The study of how people make choices. 2. D Prioritizing what is best for you as an individual. 3. C The thought process of consumers.

www.liontutors.com ECON 102 Brown Exam 1 Practice Exam Solutions 1. C The study of how people make choices. 2. D Prioritizing what is best for you as an individual. 3. C The thought process of consumers.

L2 Efficiency, Opportunity Cost, PPF

L2 Efficiency, Opportunity Cost, PPF Pareto Efficiency: A state in which it is impossible to make at least one individual better off without hurting the others. The action that makes at least one individual

L2 Efficiency, Opportunity Cost, PPF Pareto Efficiency: A state in which it is impossible to make at least one individual better off without hurting the others. The action that makes at least one individual

SHORT QUESTIONS AND ANSWERS FOR ECO402

SHORT QUESTIONS AND ANSWERS FOR ECO402 Question: How does opportunity cost relate to problem of scarcity? Answer: The problem of scarcity exists because of limited production. Thus, each society must make

SHORT QUESTIONS AND ANSWERS FOR ECO402 Question: How does opportunity cost relate to problem of scarcity? Answer: The problem of scarcity exists because of limited production. Thus, each society must make

Microeconomics. Ten Principles of Economics. Principles of. N. Gregory Mankiw. Sixth Edition. Premium PowerPoint Slides by Ron Cronovich

N. Gregory Mankiw Microeconomics Principles of Sixth Edition 1 Ten Principles of Economics Premium PowerPoint Slides by Ron Cronovich In this chapter, look for the answers to these questions: What kinds

N. Gregory Mankiw Microeconomics Principles of Sixth Edition 1 Ten Principles of Economics Premium PowerPoint Slides by Ron Cronovich In this chapter, look for the answers to these questions: What kinds

ECONOMICS. Mr. Hughes Student Information Syllabus & Class Rules What is Economics? Term of the Day

ECONOMICS Mr. Hughes Student Information Syllabus & Class Rules What is Economics? Term of the Day Unit One Fundamental Economic Concepts Standard SSEF1: The student will explain why limited productive

ECONOMICS Mr. Hughes Student Information Syllabus & Class Rules What is Economics? Term of the Day Unit One Fundamental Economic Concepts Standard SSEF1: The student will explain why limited productive

EC202- Macroeconomics. Aaron Jenkins Business Management Linn-Benton Community College Winter 2018

EC202- Macroeconomics Aaron Jenkins Business Management Linn-Benton Community College Winter 2018 If not here, where would you be? What s your opportunity cost? Opportunity cost = highest valued alternative

EC202- Macroeconomics Aaron Jenkins Business Management Linn-Benton Community College Winter 2018 If not here, where would you be? What s your opportunity cost? Opportunity cost = highest valued alternative

Unit 2 Supply and Demand

Unit 2 Supply and Demand Microeconomics - analyzes the Small Unit economic behavior of Individuals, Households and Firms to understand their decision-making process. -America s Free Enterprise- An economy

Unit 2 Supply and Demand Microeconomics - analyzes the Small Unit economic behavior of Individuals, Households and Firms to understand their decision-making process. -America s Free Enterprise- An economy

The principles of HOW PEOPLE MAKE DECISIONS

1 Ten Principles of Economics P R I N C I P L E S O F MICROECONOMICS FOURTH EDITION N. GREGORY MANKIW Premium PowerPoint Slides by Ron Cronovich 2007 update 2008 Thomson South-Western, all rights reserved

1 Ten Principles of Economics P R I N C I P L E S O F MICROECONOMICS FOURTH EDITION N. GREGORY MANKIW Premium PowerPoint Slides by Ron Cronovich 2007 update 2008 Thomson South-Western, all rights reserved

Production Possibilities, Opportunity Cost, and Economic Growth

Chapter 2 Production Possibilities, Opportunity Cost, and Economic Growth CHAPTER SUMMARY The What, How and For Whom questions are introduced as the fundamental economic questions that must be addressed

Chapter 2 Production Possibilities, Opportunity Cost, and Economic Growth CHAPTER SUMMARY The What, How and For Whom questions are introduced as the fundamental economic questions that must be addressed

2 THE ECONOMIC PROBLEM

2 THE ECONOMIC PROBLEM Why does food cost much more today than it did a few years ago? One reason is that we now use part of our corn crop to produce ethanol, a clean biofuel substitute for gasoline.

2 THE ECONOMIC PROBLEM Why does food cost much more today than it did a few years ago? One reason is that we now use part of our corn crop to produce ethanol, a clean biofuel substitute for gasoline.

Ten Principles of Economics

Seventh Edition Principles of Economics N. Gregory Mankiw CHAPTER 1 Ten Principles of Economics In this chapter, look for the answers to these questions What kinds of questions does economics address?

Seventh Edition Principles of Economics N. Gregory Mankiw CHAPTER 1 Ten Principles of Economics In this chapter, look for the answers to these questions What kinds of questions does economics address?

Ten Principles of Economics. Chapter 1

Ten Principles of Economics Chapter 1 Economy...... The word economy comes from a Greek word for one who manages a household. A household and an economy face many decisions: Who will work? What goods and

Ten Principles of Economics Chapter 1 Economy...... The word economy comes from a Greek word for one who manages a household. A household and an economy face many decisions: Who will work? What goods and

Production Possibilities, Opportunity Cost, Economic Growth

Chapter 2 Production Possibilities, Opportunity Cost, Economic Growth CHAPTER SUMMARY The "What," "How" and "For Whom" are introduced as the fundamental economic questions that must be addressed by all

Chapter 2 Production Possibilities, Opportunity Cost, Economic Growth CHAPTER SUMMARY The "What," "How" and "For Whom" are introduced as the fundamental economic questions that must be addressed by all

LECTURE NOTES. HCS 112 Fundamentals of economics INTRODUCTION. After completing this part, students should be able to:

INTRODUCTION After completing this part, students should be able to: 1. Define economics. 2. Describe the economic perspective (or economic way of thinking ), including definitions of scarcity, opportunity

INTRODUCTION After completing this part, students should be able to: 1. Define economics. 2. Describe the economic perspective (or economic way of thinking ), including definitions of scarcity, opportunity

AP Econ Unit 1. Name: Date: ID: A. Essay

Name: Date: _ ID: A AP Econ Unit 1 Essay 1. (Module 4) The table below shows the production possibilities for the Theodorean and Dodgelandian economies. Both economies are based solely on the production

Name: Date: _ ID: A AP Econ Unit 1 Essay 1. (Module 4) The table below shows the production possibilities for the Theodorean and Dodgelandian economies. Both economies are based solely on the production

FIRST INTRODUCTION TO. Dr. Mohammed A. Alwosabi. ECON140: Microeconomics Ch.1 Dr. Mohammed Alwosabi. Chapter 1

Chapter 1 FIRST INTRODUCTION TO ECONOMICS Dr. Mohammed A. Alwosabi 1 The Fundamental Problem of Economics: Scarcity and Choice It is a fact of life that we cannot get everything we want. We all want more

Chapter 1 FIRST INTRODUCTION TO ECONOMICS Dr. Mohammed A. Alwosabi 1 The Fundamental Problem of Economics: Scarcity and Choice It is a fact of life that we cannot get everything we want. We all want more

1 Macroeconomics SAMPLE QUESTIONS

Sample Multiple-Choice Questions Circle the letter of each correct answer. 1. The crucial problem of economics is (A) establishing a fair tax system. (B) providing social goods and services. (C) developing

Sample Multiple-Choice Questions Circle the letter of each correct answer. 1. The crucial problem of economics is (A) establishing a fair tax system. (B) providing social goods and services. (C) developing

Ten Principles of Economics

C H A P T E R 1 Ten Principles of Economics Economics P R I N C I P L E S O F N. Gregory Mankiw Premium PowerPoint Slides by Ron Cronovich 2009 South-Western, a part of Cengage Learning, all rights reserved

C H A P T E R 1 Ten Principles of Economics Economics P R I N C I P L E S O F N. Gregory Mankiw Premium PowerPoint Slides by Ron Cronovich 2009 South-Western, a part of Cengage Learning, all rights reserved

ECON 120 SAMPLE QUESTIONS

ECON 120 SAMPLE QUESTIONS 1) The price of cotton clothing falls. As a result, 1) A) the demand for cotton clothing decreases. B) the quantity demanded of cotton clothing increases. C) the demand for cotton

ECON 120 SAMPLE QUESTIONS 1) The price of cotton clothing falls. As a result, 1) A) the demand for cotton clothing decreases. B) the quantity demanded of cotton clothing increases. C) the demand for cotton

Lecture 1: Introduction

Lecture 1: Introduction Yulei Luo SEF of HKU January 19, 2013 Luo, Y. (SEF of HKU) ECON1002C/D January 19, 2013 1 / 16 Economics, Microeconomics and Macroeconomics Economics: The study of the choices people

Lecture 1: Introduction Yulei Luo SEF of HKU January 19, 2013 Luo, Y. (SEF of HKU) ECON1002C/D January 19, 2013 1 / 16 Economics, Microeconomics and Macroeconomics Economics: The study of the choices people

Chapter 3 The Economic Problem

Chapter 3 The Economic Problem 3.1 Production Possibilities 1) The United States produced approximately worth of goods and services in 2004. A) $12 trillion B) $12 billion C) $120 trillion D) $120 billion

Chapter 3 The Economic Problem 3.1 Production Possibilities 1) The United States produced approximately worth of goods and services in 2004. A) $12 trillion B) $12 billion C) $120 trillion D) $120 billion

Chapter 2: The Economic Problem. McTaggart, Findlay, Parkin: Microeconomics 2007 Pearson Education Australia

Chapter 2: The Economic Problem Objectives After studying this chapter, you will be able to: Define the production possibilities frontier and calculate opportunity cost Distinguish between production possibilities

Chapter 2: The Economic Problem Objectives After studying this chapter, you will be able to: Define the production possibilities frontier and calculate opportunity cost Distinguish between production possibilities

Economics: Foundations and Models

R. GLENN HUBBARD ANTHONY PATRICK O BRIEN Macroeconomics FOURTH EDITION CHAPTER 1 Economics: Foundations and Models Chapter Outline and Learning Objectives 1.1 Three Key Economic Ideas 1.2 The Economic

R. GLENN HUBBARD ANTHONY PATRICK O BRIEN Macroeconomics FOURTH EDITION CHAPTER 1 Economics: Foundations and Models Chapter Outline and Learning Objectives 1.1 Three Key Economic Ideas 1.2 The Economic

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Chapters 1-3: Additional Questions MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A recurring theme in economics is that people: A) Can increase

Chapters 1-3: Additional Questions MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A recurring theme in economics is that people: A) Can increase

Production Possibilities, Opportunity Cost, and Economic Growth

Chapter 2 Production Possibilities, Opportunity Cost, and Economic Growth CHAPTER SUMMARY The What, How and For Whom questions are introduced as the fundamental economic questions that must be addressed

Chapter 2 Production Possibilities, Opportunity Cost, and Economic Growth CHAPTER SUMMARY The What, How and For Whom questions are introduced as the fundamental economic questions that must be addressed

Full file at Production Possibilities, Opportunity Cost, and Economic Growth

Chapter 2 Production Possibilities, Opportunity Cost, and Economic Growth CHAPTER SUMMARY The What, How and For Whom questions are introduced as the fundamental economic questions that must be addressed

Chapter 2 Production Possibilities, Opportunity Cost, and Economic Growth CHAPTER SUMMARY The What, How and For Whom questions are introduced as the fundamental economic questions that must be addressed

1 Ten Principles of Economics CHAPTER 1 TEN PRINCIPLES OF ECONOMICS 0

1 Ten Principles of Economics CHAPTER 1 TEN PRINCIPLES OF ECONOMICS 0 In this chapter, look for the answers to these questions: What kinds of questions does economics address? What are the principles of

1 Ten Principles of Economics CHAPTER 1 TEN PRINCIPLES OF ECONOMICS 0 In this chapter, look for the answers to these questions: What kinds of questions does economics address? What are the principles of

Chapter 1: Economics: The Core Issues Solutions Manual

Learning Objectives for Chapter 1 Chapter 1: Economics: The Core Issues Solutions Manual After reading this chapter, you should know LO 01-01. How scarcity creates opportunity costs. LO 01-02. What the

Learning Objectives for Chapter 1 Chapter 1: Economics: The Core Issues Solutions Manual After reading this chapter, you should know LO 01-01. How scarcity creates opportunity costs. LO 01-02. What the

CH 1-2. Name: Class: Date: Multiple Choice Identify the choice that best completes the statement or answers the question.

Class: Date: CH 1-2 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The inability of society to provide senior citizens with all of the prescription drugs

Class: Date: CH 1-2 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The inability of society to provide senior citizens with all of the prescription drugs

Ten Principles of Economics

Wojciech Gerson (1831-1901) Seventh Edition Principles of Macroeconomics N. Gregory Mankiw The principles of HOW PEOPLE MAKE DECISIONS CHAPTER 1 Ten Principles of Economics lithian/shutterstock.com In

Wojciech Gerson (1831-1901) Seventh Edition Principles of Macroeconomics N. Gregory Mankiw The principles of HOW PEOPLE MAKE DECISIONS CHAPTER 1 Ten Principles of Economics lithian/shutterstock.com In

Production Possibilities, Opportunity Cost, and Economic Growth

Chapter 2 Production Possibilities, Opportunity Cost, and Economic Growth CHAPTER SUMMARY The What, How and For Whom are introduced as the fundamental economic questions that must be addressed by all societies.

Chapter 2 Production Possibilities, Opportunity Cost, and Economic Growth CHAPTER SUMMARY The What, How and For Whom are introduced as the fundamental economic questions that must be addressed by all societies.

TEN PRINCIPLES OF ECONOMICS. The word Economy... An individual economic agent faces many decisions: Intro Macroeconomic Theory Professor Minseong Kim

TEN PRINCIPLES OF ECONOMICS Chapter 1 The word Economy... Comes from a Greek word for one who manages a household. An individual economic agent faces many decisions: Should I go to college or should I

TEN PRINCIPLES OF ECONOMICS Chapter 1 The word Economy... Comes from a Greek word for one who manages a household. An individual economic agent faces many decisions: Should I go to college or should I