ORGANIZING PRODUCTION

|

|

|

- Phoebe Turner

- 5 years ago

- Views:

Transcription

1 ORGANIZING PRODUCTION M. En C. Eduardo Bustos Farías 1

2 Objectives After studying this lecture, you will able to Explain what a firm is and describe the economic problems that all firms face Distinguish between technological efficiency and economic efficiency Define and explain the principal-agent problem and describe how different types of business organizations cope with this problem M. En C. Eduardo Bustos Farías 2

3 Objectives After studying this lecture, you will able to Describe and distinguish between different types of markets in which firms operate Explain why markets coordinate some economic activities and firms coordinate others M. En C. Eduardo Bustos Farías 3

4 Spinning a Web Tim Berners-Lee s idea, the World Wide Web, has provided a platform for the creation of thousands of profitable businesses from tiny owner-operated firms to giant multinationals. This lecture explains the role of firms and the problems that all firms face. M. En C. Eduardo Bustos Farías 4

5 The Firm and Its Economic Problem A firm is an institution that hires factors of production and organizes them to produce and sell goods and services. The Firm s Goal A firm s goal is to maximize profit. If the firm fails to maximize profits it is either eliminated or bought out by other firms seeking to maximize profit. M. En C. Eduardo Bustos Farías 5

6 The Firm Measuring a Firm s Profit Accountants measure a firm s profit using rules laid down by the Internal Revenue Service and the Financial Accounting Standards Board. Their goal is to report profit so that the firm pays the correct amount of tax and is open and honest about its financial situation with its bank and other lenders. M. En C. Eduardo Bustos Farías 6

7 The Firm and Its Economic Problem Economists measure profit based on an opportunity cost measure of cost. M. En C. Eduardo Bustos Farías 7

8 The Firm and Its Economic Problem Opportunity Cost A firm s decisions respond to opportunity cost and economic profit. A firm s opportunity cost of producing a good is the best, forgone alternative use of its factors of production, usually measured in dollars. M. En C. Eduardo Bustos Farías 8

9 Opportunity Cost Opportunity cost includes both: Explicit costs Implicit costs M. En C. Eduardo Bustos Farías 9

10 The Firm and Its Economic Problem Explicit costs are costs paid directly in money. Implicit costs are costs incurred when a firm uses its own capital or its owners time for which it does not make a direct money payment. The firm can rent capital and pay an explicit rental cost reflecting the opportunity cost of using the capital. The firm can also buy capital and incur an implicit opportunity cost of using its own capital, called the implicit rental rate of capital. M. En C. Eduardo Bustos Farías 10

11 The Firm and Its Economic Problem The implicit rental rate of capital is made up of: Economic depreciation Interest forgone Economic depreciation is the change in the market value of capital over a given period. Interest forgone is the return on the funds used to acquire the capital. M. En C. Eduardo Bustos Farías 11

12 The Firm and Its Economic Problem The cost of the owner s resources is his or her entrepreneurial ability and labor expended in running the business. The opportunity cost of the owner s entrepreneurial ability is the average return from this contribution that can be expected from running another firm. This return is called a normal profit. The opportunity cost of the owner s labor spent running the business is the wage income forgone by not working in the next best alternative job. M. En C. Eduardo Bustos Farías 12

13 The Firm and Its Economic Problem Economic Profit Economic profit equals a firm s total revenue minus its opportunity cost of production. A firm s opportunity cost of production is the sum of the explicit costs and implicit costs. Normal profit is part of the firm s opportunity costs, so economic profit is profit over and above normal profit. M. En C. Eduardo Bustos Farías 13

14 Table summarizes the economic accounting concepts M. En C. Eduardo Bustos Farías 14

15 The Firm and Its Economic Problem Economic Accounting: A Summary To maximize profit, a firm must make five basic decisions: What goods and services to produce and in what quantities How to produce the production technology to use How to organize and compensate its managers and workers How to market and price its products What to produce itself and what to buy from other firms M. En C. Eduardo Bustos Farías 15

16 The Firm and Its Economic Problem The Firm s Constraints The five basic decisions of a firm are limited by the constraints it faces. There are three constraints a firm faces: Technology Information Market M. En C. Eduardo Bustos Farías 16

17 The Firm and Its Economic Problem Technology Constraints Technology is any method of producing a good or service. Technology advances over time. Using the available technology, the firm can produce more only if it hires more resources, which will increase its costs and limit the profit of additional output. M. En C. Eduardo Bustos Farías 17

18 The Firm and Its Economic Problem Information Constraints A firm never possesses complete information about either the present or the future. It is constrained by limited information about the quality and effort of its work force, current and future buying plans of its customers, and the plans of its competitors. The cost of coping with limited information limits profit. M. En C. Eduardo Bustos Farías 18

19 The Firm and Its Economic Problem Market Constraints What a firm can sell and the price it can obtain are constrained by its customers willingness to pay and by the prices and marketing efforts of other firms. The resources that a firm can buy and the prices it must pay for them are limited by the willingness of people to work for and invest in the firm. The expenditures a firm incurs to overcome these market constraints will limit the profit the firm can make. M. En C. Eduardo Bustos Farías 19

20 Technology and Economic Efficiency Technological Efficiency Technological efficiency occurs when a firm produces a given level of output by using the least amount inputs. Table shows four ways of making a TV set, one of which is technologically inefficient. There may be different combinations of inputs to use for producing a given level of output. If it is impossible to maintain output by decreasing any one input, holding all other inputs constant, then production is technologically efficient. M. En C. Eduardo Bustos Farías 20

21 M. En C. Eduardo Bustos Farías 21

22 Technology and Economic Efficiency Economic Efficiency Economic efficiency occurs when the firm produces a given level of output at the least cost. Next table shows how the economically efficient method depends on the relative costs of capital and labor. The difference between technological and economic efficiency is that technological efficiency concerns the quantity of inputs used in production for a given level of output, whereas economic efficiency concerns the cost of the inputs used. M. En C. Eduardo Bustos Farías 22

23 The costs of different ways of making 10 tv set a day M. En C. Eduardo Bustos Farías 23

24 The costs of different ways of making 10 tv set a day M. En C. Eduardo Bustos Farías 24

25 The costs of different ways of making 10 tv set a day M. En C. Eduardo Bustos Farías 25

26 Technology and Economic Efficiency An economically efficient production process also is technologically efficient.\ A technologically efficient process may not be economically efficient. Changes in the input prices influence the value of the inputs, but not the technological process for using them in production. M. En C. Eduardo Bustos Farías 26

27 Information and Organization A firm organizes production by combining and coordinating productive resources using a mixture of two systems: Command systems Incentive systems M. En C. Eduardo Bustos Farías 27

28 Information and Organization Command Systems A command system uses a managerial hierarchy. Commands pass downward through the hierarchy and information (feedback) passes upward. These systems are relatively rigid and can have many layers of specialized management. M. En C. Eduardo Bustos Farías 28

29 Information and Organization Incentive Systems An incentive system, uses market-like mechanisms to induce workers to perform in ways that maximize the firm s profit. M. En C. Eduardo Bustos Farías 29

30 Information and Organization Mixing the Systems Most firms use a mix of command and incentive systems to maximize profit. They use commands when it is easy to monitor performance or when a small deviation from the ideal performance is very costly. They use incentives whenever monitoring performance is impossible or too costly to be worth doing. M. En C. Eduardo Bustos Farías 30

31 Information and Organization The Principal-Agent Problem The principal-agent problem is the problem of devising compensation rules that induce an agent to act in the best interests of a principal. For example, the stockholders of a firm are the principals and the managers of the firm are their agents. M. En C. Eduardo Bustos Farías 31

32 Information and Organization Coping with the Principal-Agent Problem Three ways of coping with the principal-agent problem are: Ownership Incentive pay Long-term contracts M. En C. Eduardo Bustos Farías 32

33 Information and Organization Ownership, often offered to managers, gives the managers an incentive to maximize the firm s profits, which is the goal of the owners, the principals. M. En C. Eduardo Bustos Farías 33

34 Incentive pay links managers or workers pay to the firm s performance and helps align the managers and workers interests with those of the owners, the principal. M. En C. Eduardo Bustos Farías 34

35 Long-term contracts can tie managers or workers longterm rewards to the long-term performance of the firm. This arrangement encourages the agents work in the best long-term interests of the firm owners, the principals. M. En C. Eduardo Bustos Farías 35

36 Information and Organization Types of Business Organization There are three types of business organization: Proprietorship Partnership Corporation M. En C. Eduardo Bustos Farías 36

37 Information and Organization Proprietorship A proprietorship is a firm with a single owner who has unlimited liability, or legal responsibility for all debts incurred by the firm up to an amount equal to the entire wealth of the owner. The proprietor also makes management decisions and receives the firm s profit. Profits are taxed the same as the owner s other income. M. En C. Eduardo Bustos Farías 37

38 Information and Organization Partnership A partnership is a firm with two or more owners who have unlimited liability. Partners must agree on a management structure and how to divide up the profits. Profits from partnerships are taxed as the personal income of the owners. M. En C. Eduardo Bustos Farías 38

39 Information and Organization Corporation A corporation is owned by one or more stockholders with limited liability, which means the owners who have legal liability only for the initial value of their investment. The personal wealth of the stockholders is not at risk if the firm goes bankrupt. The profit of corporations is taxed twice once as a corporate tax on firm profits, and then again as income taxes paid by stockholders receiving their after-tax profits distributed as dividends. M. En C. Eduardo Bustos Farías 39

40 Information and Organization Pros and Cons of Different Types of Firms Each type of business organization has advantages and disadvantages. Table lists the pros and cons of different types of ownership. M. En C. Eduardo Bustos Farías 40

41 M. En C. Eduardo Bustos Farías 41

42 Information and Organization Proprietorships are easy to set up Managerial decision making is simple Profits are taxed only once But bad decisions made by the manager are not subject to review The owner s entire wealth is at stake The firm dies with the owner The cost of capital and labor can be high M. En C. Eduardo Bustos Farías 42

43 Information and Organization Partnerships are easy to set up Employ diversified decision-making processes Can survive the death or withdrawal of a partner Profits are taxed only once But partnerships make attaining a consensus about managerial decisions difficult Place the owners entire wealth at risk The cost of capital can be high, and the withdrawal of a partner might create a capital shortage M. En C. Eduardo Bustos Farías 43

44 Information and Organization A corporation offers perpetual life Limited liability for its owners Large-scale and low-cost capital that is readily available Professional management Lower costs from long-term labor contracts But a corporation s management structure may lead to slower and expensive decision-making Profit is taxed twice as corporate profit and shareholder income. M. En C. Eduardo Bustos Farías 44

45 Information and Organization The Relative Importance of Different Types and Firms There are a greater number of proprietorships than other form of business, but corporations account for the majority of revenue received by businesses. M. En C. Eduardo Bustos Farías 45

46 Information and Organization Figure shows the frequency of each type of business organization. 46

47 Information and Organization Figure shows the dominant type of business organization for various industries. 47

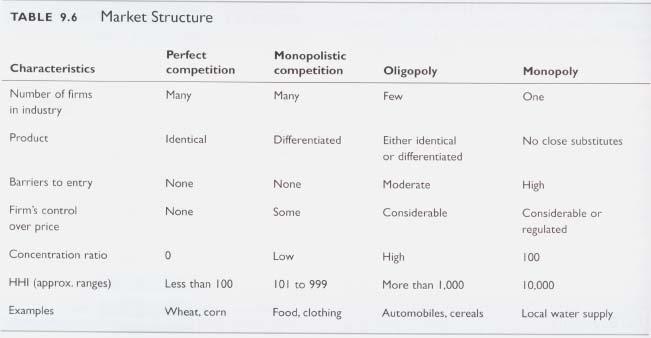

48 Markets and the Competitive Environment Economists identify four market types: Perfect competition Monopolistic competition Oligopoly Monopoly 48

49 Markets and the Competitive Environment Perfect competition is a market structure with: Many firms Each sells an identical product Many buyers No restrictions on entry of new firms to the industry Both firms and buyers are all well informed of the prices and products of all firms in the industry. 49

50 Markets and the Competitive Environment Monopolistic competition is a market structure with: Many firms Each firm produces similar but slightly different products called product differentiation Each firm possesses an element of market power No restrictions on entry of new firms to the industry 50

51 Markets and the Competitive Environment Oligopoly is a market structure in which: A small number of firms compete The firms might produce almost identical products or differentiated products Barriers to entry limit entry into the market. 51

52 Markets and the Competitive Environment Monopoly is a market structure in which One firm produces the entire output of the industry There are no close substitutes for the product There are barriers to entry that protect the firm from competition by entering firms 52

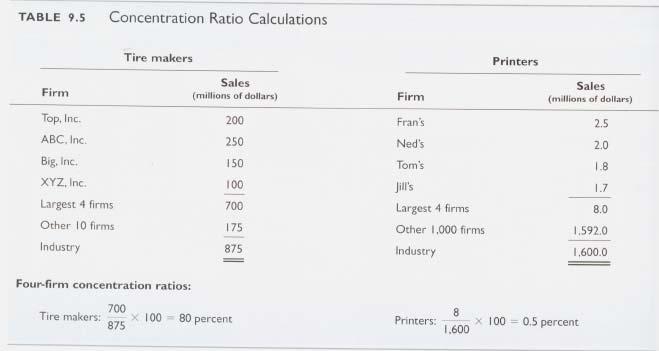

53 Markets and the Competitive Environment Measures of Concentration Two measures of market concentration in common use are: The four-firm concentration ratio The Herfindahl Hirschman index (HHI) 53

54 The four-firm concentration ratio Is the percentage of the total industry sales accounted for by the four largest firms in the industry. 54

55 55

56 The Herfindahl Hirschman index (HHI) Is the sum of the squared market shares of the 50 largest firms in the industry. The larger the measure of market concentration, the less competition that exists in the industry. 56

57 57

58 Markets and the Competitive Environment Concentration Measures for the U.S. Economy The U.S. Justice Department uses the HHI to classify markets. A market with an HHI of less than 1,000 is regarded as highly competitive A market with an HHI between 1,000 and 1,800 is regarded as moderately competitive A market with an HHI greater than 1,800 is uncompetitive 58

59 Markets and the Competitive Environment Figure shows the four-firm concentration ratio for various industries in the United States. The figure also shows the HHI for these industries. 59

60 Markets and the Competitive Environment Limitations of Concentration Measures Concentration measures alone are not sufficient to identify the market structure of a given industry. Concentration ratios are based on the national market. For some goods, the relevant market is local (e.g., newspapers) For some goods, the relevant market is the world (e.g., automobiles). 60

61 Markets and the Competitive Environment Concentration ratios convey no information about the extent of barriers to entry. For some industries, few firms may be currently operating in the market but competition might be fierce, with firms regularly entering and exiting the industry. Even potential entry might be enough to maintain competition. 61

62 Markets and the Competitive Environment Table 9.6 on page 203 summarizes the range of other information used with the concentration ratio to determine market structure. 62

63 Markets and the Competitive Environment Market Structures in the U.S. Economy Figure shows the distribution of market structures in the U.S. economy. The economy is mainly competitive. 63

64 Markets and Firms Market Coordination Markets both coordinate production. Demand and supply coordinate the plans of buyers and sellers. Outsourcing buying parts or products from other firms is an example of market coordination of production. But firms coordinate more production than do markets. Why? M. En C. Eduardo Bustos Farías 64

65 Markets and Firms Why Firms? Firms coordinate production when they can do so more efficiently than a market. Four key reasons might make firms more efficient. Firms can achieve: Lower transactions costs Economies of scale Economies of scope Economies of team production M. En C. Eduardo Bustos Farías 65

66 Markets and Firms Transactions costs are the costs arising from finding someone with whom to do business, reaching agreement on the price and other aspects of the exchange, and ensuring that the terms of the agreement are fulfilled. M. En C. Eduardo Bustos Farías 66

67 Economies of scale occur when the cost of producing a unit of a good falls as its output rate increases. M. En C. Eduardo Bustos Farías 67

68 Economies of scope arise when a firm can use specialized inputs to produce a range of different goods at a lower cost than otherwise. Firms can engage in team production, in which the individuals specialize in mutually supporting tasks. M. En C. Eduardo Bustos Farías 68

69 s Password: password M. En C. Eduardo Bustos Farías 69

9 ORGANIZING PRODUCTION. Chapter. Key Concepts. to buy its products and by the prices and marketing efforts of other firms.

Chapter 9 ORGANIZING PRODUCTION Key Concepts The Firm and Its Economic Problem A firm is an institution that hires factors of production and uses these factors to produce and sell output. The firm s goal

Chapter 9 ORGANIZING PRODUCTION Key Concepts The Firm and Its Economic Problem A firm is an institution that hires factors of production and uses these factors to produce and sell output. The firm s goal

ECO201: PRINCIPLES OF MICROECONOMICS FIRST MIDTERM EXAMINATION

YOUR NAME Row Number ECO201: PRINCIPLES OF MICROECONOMICS FIRST MIDTERM EXAMINATION Prof. Bill Even Novermber 12, 2014 FORM 1 Directions 1. Fill in your scantron with your unique-id and the form number

YOUR NAME Row Number ECO201: PRINCIPLES OF MICROECONOMICS FIRST MIDTERM EXAMINATION Prof. Bill Even Novermber 12, 2014 FORM 1 Directions 1. Fill in your scantron with your unique-id and the form number

ECO201: PRINCIPLES OF MICROECONOMICS FIRST MIDTERM EXAMINATION

YOUR NAME Row Number ECO201: PRINCIPLES OF MICROECONOMICS FIRST MIDTERM EXAMINATION Prof. Bill Even Novermber 12, 2014 FORM 3 Directions 1. Fill in your scantron with your unique-id and the form number

YOUR NAME Row Number ECO201: PRINCIPLES OF MICROECONOMICS FIRST MIDTERM EXAMINATION Prof. Bill Even Novermber 12, 2014 FORM 3 Directions 1. Fill in your scantron with your unique-id and the form number

Monopolistic Competition

Monopolistic Competition CHAPTER16 C H A P T E R C H E C K L I S T When you have completed your study of this chapter, you will be able to 1 Describe and identify monopolistic competition. 2 Explain how

Monopolistic Competition CHAPTER16 C H A P T E R C H E C K L I S T When you have completed your study of this chapter, you will be able to 1 Describe and identify monopolistic competition. 2 Explain how

ECO 2023 Principles of Microeconomics Fall 2013 Practice Test #2. 1. Which of the following are factors of production?

ECO 2023 Principles of Microeconomics Fall 2013 Practice Test #2 1. Which of the following are factors of production? A. Output in a production function. B. Productivity. C. Land, labor, capital, and entrepreneurship.

ECO 2023 Principles of Microeconomics Fall 2013 Practice Test #2 1. Which of the following are factors of production? A. Output in a production function. B. Productivity. C. Land, labor, capital, and entrepreneurship.

ECO201: PRINCIPLES OF MICROECONOMICS SECOND MIDTERM EXAMINATION

Name Seat Assignment ECO201: PRINCIPLES OF MICROECONOMICS SECOND MIDTERM EXAMINATION November 17, 2009 FORM 3. Directions 1. FILL IN YOUR SCANTRON WITH YOUR UNIQUE ID AND THE FORM NUMBER LISTED ON THIS

Name Seat Assignment ECO201: PRINCIPLES OF MICROECONOMICS SECOND MIDTERM EXAMINATION November 17, 2009 FORM 3. Directions 1. FILL IN YOUR SCANTRON WITH YOUR UNIQUE ID AND THE FORM NUMBER LISTED ON THIS

ECO201: PRINCIPLES OF MICROECONOMICS SECOND MIDTERM EXAMINATION

Name Seat Assignment ECO201: PRINCIPLES OF MICROECONOMICS SECOND MIDTERM EXAMINATION November 17, 2009 FORM 4. Directions 1. FILL IN YOUR SCANTRON WITH YOUR UNIQUE ID AND THE FORM NUMBER LISTED ON THIS

Name Seat Assignment ECO201: PRINCIPLES OF MICROECONOMICS SECOND MIDTERM EXAMINATION November 17, 2009 FORM 4. Directions 1. FILL IN YOUR SCANTRON WITH YOUR UNIQUE ID AND THE FORM NUMBER LISTED ON THIS

ECO201: PRINCIPLES OF MICROECONOMICS SECOND MIDTERM EXAMINATION

Name Seat Assignment ECO201: PRINCIPLES OF MICROECONOMICS SECOND MIDTERM EXAMINATION November 17, 2009 FORM 1. Directions 1. FILL IN YOUR SCANTRON WITH YOUR UNIQUE ID AND THE FORM NUMBER LISTED ON THIS

Name Seat Assignment ECO201: PRINCIPLES OF MICROECONOMICS SECOND MIDTERM EXAMINATION November 17, 2009 FORM 1. Directions 1. FILL IN YOUR SCANTRON WITH YOUR UNIQUE ID AND THE FORM NUMBER LISTED ON THIS

INTRODUCTION ECONOMIC PROFITS

INTRODUCTION This chapter addresses the following key questions: What are profits? What are the unique characteristics of competitive firms? How much output will a competitive firm produce? Chapter 7 THE

INTRODUCTION This chapter addresses the following key questions: What are profits? What are the unique characteristics of competitive firms? How much output will a competitive firm produce? Chapter 7 THE

Eco402 - Microeconomics Glossary By

Eco402 - Microeconomics Glossary By Break-even point : the point at which price equals the minimum of average total cost. Externalities : the spillover effects of production or consumption for which no

Eco402 - Microeconomics Glossary By Break-even point : the point at which price equals the minimum of average total cost. Externalities : the spillover effects of production or consumption for which no

Microeconomics: MIE1102

TEXT CHAPTERS TOPICS 1, 2 ECONOMICS, ECONOMIC SYSTEMS, MARKET ECONOMY 3 DEMAND AND SUPPLY. MARKET EQUILIBRIUM 4 ELASTICITY OF DEMAND AND SUPPLY 5 DEMAND & CONSUMER BEHAVIOR 6 PRODUCTION FUNCTION 7 COSTS

TEXT CHAPTERS TOPICS 1, 2 ECONOMICS, ECONOMIC SYSTEMS, MARKET ECONOMY 3 DEMAND AND SUPPLY. MARKET EQUILIBRIUM 4 ELASTICITY OF DEMAND AND SUPPLY 5 DEMAND & CONSUMER BEHAVIOR 6 PRODUCTION FUNCTION 7 COSTS

Section I (20 questions; 1 mark each)

") Foundation Course in Managerial Economics- Solution Set- 1 Final Examination Marks- 100 Section I (20 questions; 1 mark each) 1. Which of the following statements is not true? a. Societies face an important

Foundation Course in Managerial Economics- Solution Set- 1 Final Examination Marks- 100 Section I (20 questions; 1 mark each) 1. Which of the following statements is not true? a. Societies face an important

ECON 101 KONG Midterm 2 CMP Review Session. Presented by Benji Huang

ECON 101 KONG Midterm 2 CMP Review Session Presented by Benji Huang Chapter 5 Efficiency and Equity Benefit, Cost, Surplus Consumers (1) A consumer benefits from the consumption of a product this benefit

ECON 101 KONG Midterm 2 CMP Review Session Presented by Benji Huang Chapter 5 Efficiency and Equity Benefit, Cost, Surplus Consumers (1) A consumer benefits from the consumption of a product this benefit

Microeconomics Exam Notes

Microeconomics Exam Notes Opportunity Cost What you give up to get it Production Possibility Frontier Maximum attainable combination of two products (Concept of Opportunity Cost). Main Decision Makers:

Microeconomics Exam Notes Opportunity Cost What you give up to get it Production Possibility Frontier Maximum attainable combination of two products (Concept of Opportunity Cost). Main Decision Makers:

Domain 3 MICROECONOMICS

Domain 3 MICROECONOMICS Georgia Standards of Excellence MICRO CONCEPT CLUSTER SSEMI1 Describe how households and businesses are interdependent and interact through flows of goods, services, resources,

Domain 3 MICROECONOMICS Georgia Standards of Excellence MICRO CONCEPT CLUSTER SSEMI1 Describe how households and businesses are interdependent and interact through flows of goods, services, resources,

GACE Economics Assessment Test I (038) Curriculum Crosswalk

Curriculum Crosswalk") Subarea I. Fundamental Economic Concepts (20%) Objective 1: Demonstrates an understanding of the fundamental concepts of economics A. Understands the concepts of scarcity, choice, and opportunity cost

Subarea I. Fundamental Economic Concepts (20%) Objective 1: Demonstrates an understanding of the fundamental concepts of economics A. Understands the concepts of scarcity, choice, and opportunity cost

Chapter 1: MANAGERS, PROFITS, AND MARKETS

Chapter 1: MANAGERS, PROFITS, AND MARKETS Essential Concepts 1. Managerial economics applies microeconomic theory the study of the behavior of individual economic agents to business problems in order to

Chapter 1: MANAGERS, PROFITS, AND MARKETS Essential Concepts 1. Managerial economics applies microeconomic theory the study of the behavior of individual economic agents to business problems in order to

Economics. East Poinsett County School District

Economics East Poinsett County School District Economics: Third Quarter Strand: Economic Fundamentals Content Standard 1: Students shall examine scarcity and choice. EF.1.E.1 Explain the role scarcity

Economics East Poinsett County School District Economics: Third Quarter Strand: Economic Fundamentals Content Standard 1: Students shall examine scarcity and choice. EF.1.E.1 Explain the role scarcity

1. Identify the 5 characteristics of perfect competition. 1. Numerous buyers and sellers 2. Standardized/identical product 3. Freedom to enter and

1. Identify the 5 characteristics of perfect competition. 1. Numerous buyers and sellers 2. Standardized/identical product 3. Freedom to enter and exit the market 4. Producers have no control over prices

1. Identify the 5 characteristics of perfect competition. 1. Numerous buyers and sellers 2. Standardized/identical product 3. Freedom to enter and exit the market 4. Producers have no control over prices

Types of Business Organizations (SSEMI3a)

") Types of Business Organizations (SSEMI3a) Sole proprietorship: A sole proprietorship has a single owner. Partnership: A partnership divides up the risk and reward among a group of people. Corporations:

Types of Business Organizations (SSEMI3a) Sole proprietorship: A sole proprietorship has a single owner. Partnership: A partnership divides up the risk and reward among a group of people. Corporations:

4. A mixed economy combines two different economic types. Which two economic types are combined?

1. Identify the type of economy featured in the United States. A. Command Economy B. Market Economy C. Mixed Economy D. Traditional Economy 2. Which is the strongest motivating force within a market economy

1. Identify the type of economy featured in the United States. A. Command Economy B. Market Economy C. Mixed Economy D. Traditional Economy 2. Which is the strongest motivating force within a market economy

Choose the single best answer for each question. Do all of your scratch work in the margins or in the blank space at the bottom of the last page.

Econ 0, Section 2, S0, Schroeter Exam #4, Special code = Choose the single best answer for each question. Do all of your scratch work in the margins or in the blank space at the bottom of the last page..

Econ 0, Section 2, S0, Schroeter Exam #4, Special code = Choose the single best answer for each question. Do all of your scratch work in the margins or in the blank space at the bottom of the last page..

Choose the single best answer for each question. Do all of your scratch work in the margins or in the blank space at the bottom of the last page.

Econ 0, Section 2, S0, Schroeter Exam #4, Special code = 2 Choose the single best answer for each question. Do all of your scratch work in the margins or in the blank space at the bottom of the last page..

Econ 0, Section 2, S0, Schroeter Exam #4, Special code = 2 Choose the single best answer for each question. Do all of your scratch work in the margins or in the blank space at the bottom of the last page..

INTI COLLEGE MALAYSIA BUSINESS FOUNDATION PROGRAMME ECO 181: INTRODUCTORY ECONOMICS FINAL EXAMINATION: AUGUST 2003 SESSION

ECO 181 (F) / Page 1 of 15 INTI COLLEGE MALAYSIA BUSINESS FOUNDATION PROGRAMME ECO 181: INTRODUCTORY ECONOMICS FINAL EXAMINATION: AUGUST 2003 SESSION SECTION A There are SIXTY questions on this paper.

ECO 181 (F) / Page 1 of 15 INTI COLLEGE MALAYSIA BUSINESS FOUNDATION PROGRAMME ECO 181: INTRODUCTORY ECONOMICS FINAL EXAMINATION: AUGUST 2003 SESSION SECTION A There are SIXTY questions on this paper.

Intermediate Macroeconomic Theory, 01/07/2003. A Glossary of Macroeconomics Terms

A Glossary of Macroeconomics Terms The Digital Economist -A- Absolute Advantage A comparison of input requirements between two regions or countries where one country can produce a given level of output

A Glossary of Macroeconomics Terms The Digital Economist -A- Absolute Advantage A comparison of input requirements between two regions or countries where one country can produce a given level of output

Econ Microeconomics Notes

Econ 120 - Microeconomics Notes Daniel Bramucci December 1, 2016 1 Section 1 - Thinking like an economist 1.1 Definitions Cost-Benefit Principle An action should be taken only when its benefit exceeds

Econ 120 - Microeconomics Notes Daniel Bramucci December 1, 2016 1 Section 1 - Thinking like an economist 1.1 Definitions Cost-Benefit Principle An action should be taken only when its benefit exceeds

Week One What is economics? Chapter 1

Week One What is economics? Chapter 1 Economics: is the social science that studies the choices that individuals, businesses, governments, and entire societies make as they cope with scarcity and the incentives

Week One What is economics? Chapter 1 Economics: is the social science that studies the choices that individuals, businesses, governments, and entire societies make as they cope with scarcity and the incentives

ECON 102 Brown Final Exam (New Material) Practice Exam Solutions

Practice Exam Solutions") www.liontutors.com ECON 102 Brown Final Exam (New Material) Practice Exam Solutions 1. B A very large percent of their earnings comes from economic rent 2. B Any funds left, after everyone who has a claim

www.liontutors.com ECON 102 Brown Final Exam (New Material) Practice Exam Solutions 1. B A very large percent of their earnings comes from economic rent 2. B Any funds left, after everyone who has a claim

A Glossary of Macroeconomics Terms

A Glossary of Macroeconomics Terms -A- Absolute Advantage A comparison of input requirements between two regions or countries where one country can produce a given level of output with less input relative

A Glossary of Macroeconomics Terms -A- Absolute Advantage A comparison of input requirements between two regions or countries where one country can produce a given level of output with less input relative

American Free Market System

Unit 7a Economics American Free Market System Introduction The U.S. economy Challenges in a free market Factors of Production Supply and Demand Business organizations Economic systems The Circular flow

Unit 7a Economics American Free Market System Introduction The U.S. economy Challenges in a free market Factors of Production Supply and Demand Business organizations Economic systems The Circular flow

Microeconomics. Use the Following Graph to Answer Question 3

More Tutorial at www.dumblittledoctor.com Microeconomics 1. To an economist, a good is scarce when: *a. the amount of the good available is less than the amount that people want when the good's price equals

More Tutorial at www.dumblittledoctor.com Microeconomics 1. To an economist, a good is scarce when: *a. the amount of the good available is less than the amount that people want when the good's price equals

ECO201: PRINCIPLES OF MICROECONOMICS FIRST MIDTERM EXAMINATION

YOUR NAME Row Number ECO201: PRINCIPLES OF MICROECONOMICS FIRST MIDTERM EXAMINATION Prof. Bill Even November 14, 2011 FORM 2 Directions 1. Fill in your scantron with your unique-id and the form number

YOUR NAME Row Number ECO201: PRINCIPLES OF MICROECONOMICS FIRST MIDTERM EXAMINATION Prof. Bill Even November 14, 2011 FORM 2 Directions 1. Fill in your scantron with your unique-id and the form number

ECO201: PRINCIPLES OF MICROECONOMICS FIRST MIDTERM EXAMINATION

YOUR NAME Row Number ECO201: PRINCIPLES OF MICROECONOMICS FIRST MIDTERM EXAMINATION Prof. Bill Even November 14, 2011 FORM 4 Directions 1. Fill in your scantron with your unique-id and the form number

YOUR NAME Row Number ECO201: PRINCIPLES OF MICROECONOMICS FIRST MIDTERM EXAMINATION Prof. Bill Even November 14, 2011 FORM 4 Directions 1. Fill in your scantron with your unique-id and the form number

ECO201: PRINCIPLES OF MICROECONOMICS SECOND MIDTERM EXAMINATION

YOUR NAME Row Number ECO201: PRINCIPLES OF MICROECONOMICS SECOND MIDTERM EXAMINATION Prof. Bill Even April 20, 2016 FORM 1 Directions 1. Fill in your scantron with your unique-id and the form number listed

YOUR NAME Row Number ECO201: PRINCIPLES OF MICROECONOMICS SECOND MIDTERM EXAMINATION Prof. Bill Even April 20, 2016 FORM 1 Directions 1. Fill in your scantron with your unique-id and the form number listed

1.3. Levels and Rates of Change Levels: example, wages and income versus Rates: example, inflation and growth Example: Box 1.3

1 Chapter 1 1.1. Scarcity, Choice, Opportunity Cost Definition of Economics: Resources versus Wants Wants: more and better unlimited Versus Needs: essential limited Versus Demand: ability to pay + want

1 Chapter 1 1.1. Scarcity, Choice, Opportunity Cost Definition of Economics: Resources versus Wants Wants: more and better unlimited Versus Needs: essential limited Versus Demand: ability to pay + want

Economics. E.1.4 Describe how people respond predictably to positive and negative incentives.

Standard 1: Scarcity and Economic Reasoning Students will understand that productive resources are limited; therefore, people cannot have all the goods and services they want. As a result, they must choose

Standard 1: Scarcity and Economic Reasoning Students will understand that productive resources are limited; therefore, people cannot have all the goods and services they want. As a result, they must choose

FINALTERM EXAMINATION FALL 2006

FINALTERM EXAMINATION FALL 2006 QUESTION NO: 1 (MARKS: 1) - PLEASE CHOOSE ONE Compared to the equilibrium price and quantity sold in a competitive market, a monopolist Will charge a price and sell a quantity.

FINALTERM EXAMINATION FALL 2006 QUESTION NO: 1 (MARKS: 1) - PLEASE CHOOSE ONE Compared to the equilibrium price and quantity sold in a competitive market, a monopolist Will charge a price and sell a quantity.

A Correlation of. To the Mississippi College- and Career- Readiness Standards Social Studies

A Correlation of To the 2018 Mississippi College- and Career- Readiness Standards Social Studies Table of Contents E.1... 3 E.2... 6 E.3... 7 E.4... 11 E.5... 15 E.6... 19 E.7... 24 E.8... 26 E.9... 28

A Correlation of To the 2018 Mississippi College- and Career- Readiness Standards Social Studies Table of Contents E.1... 3 E.2... 6 E.3... 7 E.4... 11 E.5... 15 E.6... 19 E.7... 24 E.8... 26 E.9... 28

1. Economic systems differ according to what two main characteristics? A. Ownership of resources and methods of coordinating economic activity.

Essentials of Economics 3rd Edition Brue Test Bank Full Download: http://testbanklive.com/download/essentials-of-economics-3rd-edition-brue-test-bank/ Chapter 02 The Market System and the Circular Flow

Essentials of Economics 3rd Edition Brue Test Bank Full Download: http://testbanklive.com/download/essentials-of-economics-3rd-edition-brue-test-bank/ Chapter 02 The Market System and the Circular Flow

Goal 8 The United States Economic System

Practice Test of Goal 8 The United States Economic System Note to teachers: These unofficial sample questions were created to help students review state Goal 8 content, as well as practice for the Civics

Practice Test of Goal 8 The United States Economic System Note to teachers: These unofficial sample questions were created to help students review state Goal 8 content, as well as practice for the Civics

Unit 2 Supply and Demand

Unit 2 Supply and Demand Microeconomics - analyzes the Small Unit economic behavior of Individuals, Households and Firms to understand their decision-making process. -America s Free Enterprise- An economy

Unit 2 Supply and Demand Microeconomics - analyzes the Small Unit economic behavior of Individuals, Households and Firms to understand their decision-making process. -America s Free Enterprise- An economy

Chapter 1: Managers and Economics

Economics for Managers by Paul Farnham Chapter 1: Managers and Economics 1.1 The best time for a managerial angle on life 1.2 What happened on the global markets in the last year? Governments designing

Economics for Managers by Paul Farnham Chapter 1: Managers and Economics 1.1 The best time for a managerial angle on life 1.2 What happened on the global markets in the last year? Governments designing

ECO201: PRINCIPLES OF MICROECONOMICS FIRST MIDTERM EXAMINATION

YOUR NAME Row Number ECO201: PRINCIPLES OF MICROECONOMICS FIRST MIDTERM EXAMINATION Prof. Bill Even Novermber 12, 2015 FORM 3 Directions 1. Fill in your scantron with your unique-id and the form number

YOUR NAME Row Number ECO201: PRINCIPLES OF MICROECONOMICS FIRST MIDTERM EXAMINATION Prof. Bill Even Novermber 12, 2015 FORM 3 Directions 1. Fill in your scantron with your unique-id and the form number

ECO201: PRINCIPLES OF MICROECONOMICS FIRST MIDTERM EXAMINATION

YOUR NAME Row Number ECO201: PRINCIPLES OF MICROECONOMICS FIRST MIDTERM EXAMINATION Prof. Bill Even Novermber 12, 2015 FORM 1 Directions 1. Fill in your scantron with your unique-id and the form number

YOUR NAME Row Number ECO201: PRINCIPLES OF MICROECONOMICS FIRST MIDTERM EXAMINATION Prof. Bill Even Novermber 12, 2015 FORM 1 Directions 1. Fill in your scantron with your unique-id and the form number

BA5101 ECONOMIC ANALYSIS FOR BUSINESS MBA/IYear/ I Semester 2 Marks Questions & Answers

BA5101 ECONOMIC ANALYSIS FOR BUSINESS MBA/IYear/ I Semester 2 Marks Questions & Answers 1. Define consumer behavior Consumer behavior is the study of when, why, how, and where people do or do not buy a

BA5101 ECONOMIC ANALYSIS FOR BUSINESS MBA/IYear/ I Semester 2 Marks Questions & Answers 1. Define consumer behavior Consumer behavior is the study of when, why, how, and where people do or do not buy a

Ch. 8 Costs and the Supply of Goods. 1. they purchase productive resources from households and other firms

Ch. 8 Costs and the Supply of Goods Organization of the business firm What do firms do? 1. they purchase productive resources from households and other firms 2. then they transform those resources into

Ch. 8 Costs and the Supply of Goods Organization of the business firm What do firms do? 1. they purchase productive resources from households and other firms 2. then they transform those resources into

HOMEWORK ECON SFU

HOMEWORK 1998-2 ECON 103 - SFU the law of diminishing returns have on short-run costs? Be specific. (e) âwhen... And when marginal product is diminishing, marginal cost is rising.â Illustrate and... ECON

HOMEWORK 1998-2 ECON 103 - SFU the law of diminishing returns have on short-run costs? Be specific. (e) âwhen... And when marginal product is diminishing, marginal cost is rising.â Illustrate and... ECON

Economic Profit. Accounting. Profit. Explicit. Costs. Implicit costs (including a normal profit) Accounting. costs (explicit costs only) T O T A L

Accounting. costs (explicit costs only) T O T A L") Profits Least expensive source of money for expanding business operations ost firms attempt to maximize profit Ultimately must break-even cover their costs of production Profits act as an incentive and

Profits Least expensive source of money for expanding business operations ost firms attempt to maximize profit Ultimately must break-even cover their costs of production Profits act as an incentive and

CLEP Microeconomics Practice Test

Practice Test Time 90 Minutes 80 Questions For each of the questions below, choose the best answer from the choices given. 1. In economics, the opportunity cost of an item or entity is (A) the out-of-pocket

Practice Test Time 90 Minutes 80 Questions For each of the questions below, choose the best answer from the choices given. 1. In economics, the opportunity cost of an item or entity is (A) the out-of-pocket

Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing)

") Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Forms of Business Organization Sole Trader Partnership Limited Company Sole Trader What is your understanding

Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Forms of Business Organization Sole Trader Partnership Limited Company Sole Trader What is your understanding

ECO201: PRINCIPLES OF MICROECONOMICS. Second MIDTERM EXAMINATION

YOUR NAME Assigned Seat IF YOU ARE NOT SEATED IN YOUR ASSIGNED SEAT OR TAKE AN EXAM WITHOUT YOUR INITIALS LISTED ON THE EXAM, YOU WILL RECEIVE A GRADE OF ZERO ON THE EXAM. ECO201: PRINCIPLES OF MICROECONOMICS

YOUR NAME Assigned Seat IF YOU ARE NOT SEATED IN YOUR ASSIGNED SEAT OR TAKE AN EXAM WITHOUT YOUR INITIALS LISTED ON THE EXAM, YOU WILL RECEIVE A GRADE OF ZERO ON THE EXAM. ECO201: PRINCIPLES OF MICROECONOMICS

EOCT Test Semester 2 final

EOCT Test Semester 2 final 1. The best definition of Economics is a. The study of how individuals spend their money b. The study of resources and government c. The study of the allocation of scarce resources

EOCT Test Semester 2 final 1. The best definition of Economics is a. The study of how individuals spend their money b. The study of resources and government c. The study of the allocation of scarce resources

Managerial Economics Prof. Trupti Mishra S.J.M School of Management Indian Institute of Technology, Bombay. Lecture -29 Monopoly (Contd )

") Managerial Economics Prof. Trupti Mishra S.J.M School of Management Indian Institute of Technology, Bombay Lecture -29 Monopoly (Contd ) In today s session, we will continue our discussion on monopoly.

Managerial Economics Prof. Trupti Mishra S.J.M School of Management Indian Institute of Technology, Bombay Lecture -29 Monopoly (Contd ) In today s session, we will continue our discussion on monopoly.

CHAPTER 8: SECTION 1 A Perfectly Competitive Market

CHAPTER 8: SECTION 1 A Perfectly Competitive Market Four Types of Markets A market structure is the setting in which a seller finds itself. Market structures are defined by their characteristics. Those

CHAPTER 8: SECTION 1 A Perfectly Competitive Market Four Types of Markets A market structure is the setting in which a seller finds itself. Market structures are defined by their characteristics. Those

MICROECONOMICS SECTION I. Time - 70 minutes 60 Questions

MICROECONOMICS SECTION I Time - 70 minutes 60 Questions Directions: Each of the questions or incomplete statements below is followed by five suggested answers or completions. Select the one that is best

MICROECONOMICS SECTION I Time - 70 minutes 60 Questions Directions: Each of the questions or incomplete statements below is followed by five suggested answers or completions. Select the one that is best

GACE Economics Assessment Test at a Glance

GACE Economics Assessment Test at a Glance Updated June 2017 See the GACE Economics Assessment Study Companion for practice questions and preparation resources. Assessment Name Economics Grade Level 6

GACE Economics Assessment Test at a Glance Updated June 2017 See the GACE Economics Assessment Study Companion for practice questions and preparation resources. Assessment Name Economics Grade Level 6

CONTENTS. Introduction to the Series. 1 Introduction to Economics 5 2 Competitive Markets, Demand and Supply Elasticities 37

CONTENTS Introduction to the Series iv 1 Introduction to Economics 5 2 Competitive Markets, Demand and Supply 17 3 Elasticities 37 4 Government Intervention in Markets 44 5 Market Failure 53 6 Costs of

CONTENTS Introduction to the Series iv 1 Introduction to Economics 5 2 Competitive Markets, Demand and Supply 17 3 Elasticities 37 4 Government Intervention in Markets 44 5 Market Failure 53 6 Costs of

Economics 101. Chris Gan July Economics 101 1

Economics 101 Chris Gan July 2010 Economics 101 1 What is Economics A study of charts, tables, statistics and numbers? Study of rational human behavior in pursuit to fulfill needs and wants Problem we

Economics 101 Chris Gan July 2010 Economics 101 1 What is Economics A study of charts, tables, statistics and numbers? Study of rational human behavior in pursuit to fulfill needs and wants Problem we

Curriculum Standard One: The students will understand common economic terms and concepts and economic reasoning.

Curriculum Standard One: The students will understand common economic terms and concepts and economic reasoning. *1. The students will examine the causal relationship between scarcity and the need for

Curriculum Standard One: The students will understand common economic terms and concepts and economic reasoning. *1. The students will examine the causal relationship between scarcity and the need for

Economics Unit 2. The United States Economic System

Economics Unit 2 The United States Economic System Demand Objective 2.01: Illustrate how supply and demand affects prices. What is Demand? Demand: The desire, willingness, and ability to buy a good or

Economics Unit 2 The United States Economic System Demand Objective 2.01: Illustrate how supply and demand affects prices. What is Demand? Demand: The desire, willingness, and ability to buy a good or

Monopolistic Competition. Chapter 17

Monopolistic Competition Chapter 17 The Four Types of Market Structure Number of Firms? Many firms One firm Few firms Differentiated products Type of Products? Identical products Monopoly Oligopoly Monopolistic

Monopolistic Competition Chapter 17 The Four Types of Market Structure Number of Firms? Many firms One firm Few firms Differentiated products Type of Products? Identical products Monopoly Oligopoly Monopolistic

Business. Management 113. Complete

Business Management 113 Complete 1 CHAPTER 1:Business Environment BUSINESS: A DEFINITION BUSINESS: The organised effort of individuals to produce and sell, for a profit, the goods and services that satisfy

Business Management 113 Complete 1 CHAPTER 1:Business Environment BUSINESS: A DEFINITION BUSINESS: The organised effort of individuals to produce and sell, for a profit, the goods and services that satisfy

2013 sample MC CH 15. Name: Class: Date: Multiple Choice Identify the choice that best completes the statement or answers the question.

Class: Date: 2013 sample MC CH 15 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. Monopolistic competition is identified by a. many firms producing a slightly

Class: Date: 2013 sample MC CH 15 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. Monopolistic competition is identified by a. many firms producing a slightly

ECON 2100 (Summer 2016 Sections 10 & 11) Exam #3C

Exam #3C") ECON 21 (Summer 216 Sections 1 & 11) Exam #3C Multiple Choice Questions: (3 points each) 1. I am taking of the exam. C. Version C 2. is a market structure in which there is one single seller of a unique

ECON 21 (Summer 216 Sections 1 & 11) Exam #3C Multiple Choice Questions: (3 points each) 1. I am taking of the exam. C. Version C 2. is a market structure in which there is one single seller of a unique

ECON 2100 (Summer 2016 Sections 10 & 11) Exam #3D

Exam #3D") ECON 21 (Summer 216 Sections 1 & 11) Exam #3D Multiple Choice Questions: (3 points each) 1. I am taking of the exam. D. Version D 2. is a market structure in which there is one single seller of a unique

ECON 21 (Summer 216 Sections 1 & 11) Exam #3D Multiple Choice Questions: (3 points each) 1. I am taking of the exam. D. Version D 2. is a market structure in which there is one single seller of a unique

The following key should help you understand the different types of activities students engage in during the course:

AP Microeconomics Course Overview Name Description AP Microeconomics AP Microeconomics studies the behavior of individuals and businesses as they exchange goods and services in the marketplace. Students

AP Microeconomics Course Overview Name Description AP Microeconomics AP Microeconomics studies the behavior of individuals and businesses as they exchange goods and services in the marketplace. Students

ECO201: PRINCIPLES OF MICROECONOMICS SECOND MIDTERM EXAMINATION

YOUR NAME Row Number ECO201: PRINCIPLES OF MICROECONOMICS SECOND MIDTERM EXAMINATION Prof. Bill Even November 11, 2013 FORM 3 Directions 1. Fill in your scantron with your unique-id and the form number

YOUR NAME Row Number ECO201: PRINCIPLES OF MICROECONOMICS SECOND MIDTERM EXAMINATION Prof. Bill Even November 11, 2013 FORM 3 Directions 1. Fill in your scantron with your unique-id and the form number

ECO201: PRINCIPLES OF MICROECONOMICS SECOND MIDTERM EXAMINATION

YOUR NAME Row Number ECO201: PRINCIPLES OF MICROECONOMICS SECOND MIDTERM EXAMINATION Prof. Bill Even November 11, 2013 FORM 4 Directions 1. Fill in your scantron with your unique-id and the form number

YOUR NAME Row Number ECO201: PRINCIPLES OF MICROECONOMICS SECOND MIDTERM EXAMINATION Prof. Bill Even November 11, 2013 FORM 4 Directions 1. Fill in your scantron with your unique-id and the form number

chapter: Solution Monopolistic Competition and Product Differentiation

Monopolistic Competition and Product Differentiation chapter: 15 1. Use the three conditions for monopolistic competition discussed in the chapter to decide which of the following firms are likely to be

Monopolistic Competition and Product Differentiation chapter: 15 1. Use the three conditions for monopolistic competition discussed in the chapter to decide which of the following firms are likely to be

Market structures Perfect competition

Market structures Perfect competition Market Structures Market structure refers to the number and size of buyers and sellers in the market for a good or service. A market can be defined as a group of firms

Market structures Perfect competition Market Structures Market structure refers to the number and size of buyers and sellers in the market for a good or service. A market can be defined as a group of firms

Economics 101 Section 5

Economics 101 Section 5 Lecture #17 March 23, 2004 Chapter 7 -The Firms long-run decisions -The Principal-Agent problem Chapter 8 -Perfect Competition - Competition in the Short-Run Lecture Outline Recap

Economics 101 Section 5 Lecture #17 March 23, 2004 Chapter 7 -The Firms long-run decisions -The Principal-Agent problem Chapter 8 -Perfect Competition - Competition in the Short-Run Lecture Outline Recap

The economics of competitive markets Rolands Irklis

The economics of competitive markets Rolands Irklis www. erranet.org Presentation outline 1. Introduction and motivation 2. Consumer s demand 3. Producer costs and supply decisions 4. Market equilibrium

The economics of competitive markets Rolands Irklis www. erranet.org Presentation outline 1. Introduction and motivation 2. Consumer s demand 3. Producer costs and supply decisions 4. Market equilibrium

MARKETS. Part Review. Reading Between the Lines SONY CORP. HAS CUT THE U.S. PRICE OF ITS PLAYSTATION 2

Part Review 4 FIRMS AND MARKETS Reading Between the Lines SONY CORP. HAS CUT THE U.S. PRICE OF ITS PLAYSTATION 2 On May 14, 2002 Sony announced it was cutting the cost of its PlayStation 2 by 33 percent,

Part Review 4 FIRMS AND MARKETS Reading Between the Lines SONY CORP. HAS CUT THE U.S. PRICE OF ITS PLAYSTATION 2 On May 14, 2002 Sony announced it was cutting the cost of its PlayStation 2 by 33 percent,

ECONOMICS 12. [Market Structures] Introduction & Background

![ECONOMICS 12. [Market Structures] Introduction & Background](/thumbs/95/122839379.jpg "ECONOMICS 12. [Market Structures] Introduction & Background") ECONOMICS 12 [Market Structures] Introduction & Background TERM 2 Progress reports Questions about test- come see me. Keeping tests until everyone has written the test. Unit: Market Structures Intro to

ECONOMICS 12 [Market Structures] Introduction & Background TERM 2 Progress reports Questions about test- come see me. Keeping tests until everyone has written the test. Unit: Market Structures Intro to

COST CONCEPTS Introduction: Cost: Types of cost: Direct cost or explicit cost:

COST CONCEPTS Introduction: A firm carries out business to earn maximum profits. Profits are the revenues collected by a business firm after production and sale of their goods and services. But to gain

COST CONCEPTS Introduction: A firm carries out business to earn maximum profits. Profits are the revenues collected by a business firm after production and sale of their goods and services. But to gain

Microeconomics. More Tutorial at

Microeconomics 1. Suppose a firm in a perfectly competitive market produces and sells 8 units of output and has a marginal revenue of $8.00. What would be the firm s total revenue if it instead produced

Microeconomics 1. Suppose a firm in a perfectly competitive market produces and sells 8 units of output and has a marginal revenue of $8.00. What would be the firm s total revenue if it instead produced

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Which of the following statements is correct? A) Consumers have the ability to buy everything

Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Which of the following statements is correct? A) Consumers have the ability to buy everything

Introduction to Business and Marketing Semester 1 Exam Review

Name: Class: Date: Introduction to Business and Marketing Semester 1 Exam Review Completion Complete each statement. 1. wants are wants that are widely shared by many people. 2. Most companies that sell

Name: Class: Date: Introduction to Business and Marketing Semester 1 Exam Review Completion Complete each statement. 1. wants are wants that are widely shared by many people. 2. Most companies that sell

Strategic Management and Competitive Advantage, 5e (Barney) Chapter 2 Evaluating a Firm's External Environment

Chapter 2 Evaluating a Firm's External Environment") Strategic Management and Competitive Advantage, 5e (Barney) Chapter 2 Evaluating a Firm's External Environment 1) A firm's general environment consists of broad trends in the context within which the firm

Strategic Management and Competitive Advantage, 5e (Barney) Chapter 2 Evaluating a Firm's External Environment 1) A firm's general environment consists of broad trends in the context within which the firm

Market Structure & Imperfect Competition

In the Name of God Sharif University of Technology Graduate School of Management and Economics Microeconomics (for MBA students) 44111 (1393-94 1 st term) - Group 2 Dr. S. Farshad Fatemi Market Structure

In the Name of God Sharif University of Technology Graduate School of Management and Economics Microeconomics (for MBA students) 44111 (1393-94 1 st term) - Group 2 Dr. S. Farshad Fatemi Market Structure

Which store has the lower costs: Wal-Mart or 7-Eleven? 2013 Pearson

Which store has the lower costs: Wal-Mart or 7-Eleven? Production and Cost 14 When you have completed your study of this chapter, you will be able to 1 Explain and distinguish between the economic and

Which store has the lower costs: Wal-Mart or 7-Eleven? Production and Cost 14 When you have completed your study of this chapter, you will be able to 1 Explain and distinguish between the economic and

Preview from Notesale.co.uk Page 6 of 89

Guns Butter 200 0 175 75 130 125 70 150 0 160 What it shows: the maximum combinations of two goods an economy can produce with its existing resources and technology; an economy can produce at points on

Guns Butter 200 0 175 75 130 125 70 150 0 160 What it shows: the maximum combinations of two goods an economy can produce with its existing resources and technology; an economy can produce at points on

ECON 2100 (Summer 2015 Sections 07 & 08) Exam #3A

Exam #3A") ECON 2100 (Summer 2015 Sections 07 & 08) Exam #3A Multiple Choice Questions: (3 points each) 1. I am taking of the exam. A. Version A 2. For a firm with market power Marginal Revenue, while for a firm

ECON 2100 (Summer 2015 Sections 07 & 08) Exam #3A Multiple Choice Questions: (3 points each) 1. I am taking of the exam. A. Version A 2. For a firm with market power Marginal Revenue, while for a firm

ECON 260 (2,3) Practice Exam #4 Spring 2007 Dan Mallela

Practice Exam #4 Spring 2007 Dan Mallela") ECON 260 (2,3) Practice Exam #4 Spring 2007 Dan Mallela Multiple Choice Identify the letter of the choice that best completes the statement or answers the question. 1. Profit is defined as a. net revenue

ECON 260 (2,3) Practice Exam #4 Spring 2007 Dan Mallela Multiple Choice Identify the letter of the choice that best completes the statement or answers the question. 1. Profit is defined as a. net revenue

Managerial Economics Prof. Trupti Mishra S. J. M. School of Management Indian Institute of Technology, Bombay

Managerial Economics Prof. Trupti Mishra S. J. M. School of Management Indian Institute of Technology, Bombay Lecture - 2 Introduction to Managerial Economics (Contd ) So, welcome to the second session

Managerial Economics Prof. Trupti Mishra S. J. M. School of Management Indian Institute of Technology, Bombay Lecture - 2 Introduction to Managerial Economics (Contd ) So, welcome to the second session

ECO201: PRINCIPLES OF MICROECONOMICS FIRST MIDTERM EXAMINATION

YOUR NAME Row Number ECO201: PRINCIPLES OF MICROECONOMICS FIRST MIDTERM EXAMINATION Prof. Bill Even November 17, 2010 FORM 4 Directions 1. Fill in your scantron with your unique-id and the form number

YOUR NAME Row Number ECO201: PRINCIPLES OF MICROECONOMICS FIRST MIDTERM EXAMINATION Prof. Bill Even November 17, 2010 FORM 4 Directions 1. Fill in your scantron with your unique-id and the form number

Exam #2 Time: 1h 15m Date: 10 July Instructor: Brian B. Young. Multiple Choice. 2 points each

Economics 212 Microeconomic Principles Exam #2 Time: 1h 15m Date: 10 July 2013 Name The value of this exam is 100 points. Instructor: Brian B. Young Please show your work where appropriate! Multiple Choice

Economics 212 Microeconomic Principles Exam #2 Time: 1h 15m Date: 10 July 2013 Name The value of this exam is 100 points. Instructor: Brian B. Young Please show your work where appropriate! Multiple Choice

ECONOMICS. Chapter 4 The Market Strikes Back

Lesson 1 ECONOMICS Chapter 4 The Market Strikes Back Review: Supply and Demand The previous lesson focused on demand and supply, we studied the demand curve and the supply curve P P S D Quantity Quantity

Lesson 1 ECONOMICS Chapter 4 The Market Strikes Back Review: Supply and Demand The previous lesson focused on demand and supply, we studied the demand curve and the supply curve P P S D Quantity Quantity

6) The mailing must be postmarked by June 15. 7) If you have any questions please me at

The mailing must be postmarked by June 15. 7) If you have any questions please me at") Examination Instructions: 1) Answer the examination only after you have read the honesty pledge below. 2) The multiple choice section will be taken in WebCT and a tutorial for using WebCT is to be found

Examination Instructions: 1) Answer the examination only after you have read the honesty pledge below. 2) The multiple choice section will be taken in WebCT and a tutorial for using WebCT is to be found

Handout. Ekonomi Manajerial [EMKU4402] Drs. Wihandaru SP, M.Si. Fak. Ekonomi / Manajemen

![Handout. Ekonomi Manajerial [EMKU4402] Drs. Wihandaru SP, M.Si. Fak. Ekonomi / Manajemen](/thumbs/75/72741083.jpg "Handout. Ekonomi Manajerial [EMKU4402] Drs. Wihandaru SP, M.Si. Fak. Ekonomi / Manajemen") Handout Ekonomi Manajerial [EMKU4402] Drs. Wihandaru SP, M.Si Fak. Ekonomi / Manajemen Chapter 1 Managers, Profits, and Markets 1-1 Managerial Economics & Theory Managerial economics applies microeconomic

Handout Ekonomi Manajerial [EMKU4402] Drs. Wihandaru SP, M.Si Fak. Ekonomi / Manajemen Chapter 1 Managers, Profits, and Markets 1-1 Managerial Economics & Theory Managerial economics applies microeconomic

CHAPTER 2. 4) Taxes cause: a) Market distortions b) Reduce incentives to work c) Decrease wealth creating transactions d) All of the above ANS: D

Taxes cause: a) Market distortions b) Reduce incentives to work c) Decrease wealth creating transactions d) All of the above ANS: D") CHAPTER 2 1) When the market is in equilibrium, a) Total surplus is minimized b) Total surplus is maximized without government intervention c) Government maximizes total revenue 2) The difference between

CHAPTER 2 1) When the market is in equilibrium, a) Total surplus is minimized b) Total surplus is maximized without government intervention c) Government maximizes total revenue 2) The difference between

Eco 202 Exam 2 Spring 2014

Eco 202 Exam 2 Spring 2014 PLEASE ANSWER 50 OF THE FOLLOWING QUESTIONS. 1. Jon Brooks quit his job in a bicycle shop, where he earned $15,000 per year, to become a graduate student in economics. At the

Eco 202 Exam 2 Spring 2014 PLEASE ANSWER 50 OF THE FOLLOWING QUESTIONS. 1. Jon Brooks quit his job in a bicycle shop, where he earned $15,000 per year, to become a graduate student in economics. At the

Unit 1 Notes Fundamental Econ Concepts PART 1.1 THE BASICS OF ECONOMICS

Economics Unit 1 Notes Fundamental Econ Concepts Name Date Per. PART 1.1 THE BASICS OF ECONOMICS What is economics? The study of how people try to satisfy seemingly unlimited and competing needs and wants

Economics Unit 1 Notes Fundamental Econ Concepts Name Date Per. PART 1.1 THE BASICS OF ECONOMICS What is economics? The study of how people try to satisfy seemingly unlimited and competing needs and wants

ECONOMIC ANALYSIS PART-A

ECONOMIC ANALYSIS TWO MARK QUESTIONS: PART-A 1. State Alfred Marshall s definition of economics? Alfred Marshall defines economics as, A study of mankind in the ordinary business of life. An altered form

ECONOMIC ANALYSIS TWO MARK QUESTIONS: PART-A 1. State Alfred Marshall s definition of economics? Alfred Marshall defines economics as, A study of mankind in the ordinary business of life. An altered form

CH short answer study questions Answer Section

CH 15-16 short answer study questions Answer Section ESSAY 1. ANS: There are a large number firms; each produces a slightly different product; firms compete on price, quality and marketing; and firms are

CH 15-16 short answer study questions Answer Section ESSAY 1. ANS: There are a large number firms; each produces a slightly different product; firms compete on price, quality and marketing; and firms are

Postgraduate Diploma in Marketing December 2017 Examination Economic and Legal Impact (Econ)

") Postgraduate Diploma in Marketing December 2017 Examination Economic and Legal Impact (Econ) Date: 20 December 2017 Time: 0830 Hrs 1130 Hrs Duration: Three (03) Hrs ) Total marks for this paper is 100

Postgraduate Diploma in Marketing December 2017 Examination Economic and Legal Impact (Econ) Date: 20 December 2017 Time: 0830 Hrs 1130 Hrs Duration: Three (03) Hrs ) Total marks for this paper is 100

Unit 1 What is an Entrepreneur?

Name Period Day Unit 1 What is an Entrepreneur? Objectives: Define what it means to be an entrepreneur Compare the pros and cons of being an entrepreneur Identify successful entrepreneurs and their achievements

Name Period Day Unit 1 What is an Entrepreneur? Objectives: Define what it means to be an entrepreneur Compare the pros and cons of being an entrepreneur Identify successful entrepreneurs and their achievements

DEFINITIONS A 42. Benjamin Disraeli. I hate definitions.

DEFINITIONS I hate definitions. Benjamin Disraeli adverse selection: opportunism characterized by an informed person s benefiting from trading or otherwise contracting with a less informed person who does

DEFINITIONS I hate definitions. Benjamin Disraeli adverse selection: opportunism characterized by an informed person s benefiting from trading or otherwise contracting with a less informed person who does

Lecture 11 Imperfect Competition

Lecture 11 Imperfect Competition Business 5017 Managerial Economics Kam Yu Fall 2013 Outline 1 Introduction 2 Monopolistic Competition 3 Oligopoly Modelling Reality The Stackelberg Leadership Model Collusion

Lecture 11 Imperfect Competition Business 5017 Managerial Economics Kam Yu Fall 2013 Outline 1 Introduction 2 Monopolistic Competition 3 Oligopoly Modelling Reality The Stackelberg Leadership Model Collusion