Business Math Boot Camp. Revenue, Cost, and Profit

|

|

|

- Christina Shaw

- 5 years ago

- Views:

Transcription

1 Zoologic Learning Solutions Business Math Boot Camp Revenue, Cost, and Profit Copyright SS&C Technologies, Inc. All rights reserved.

2 Course: Business Math Boot Camp Lesson 10: Revenue, Cost, and Profit

3 Every individual company is significantly impacted by the interplay of supply and demand. Just as important to every company are the concepts of profit, revenue, and total cost. The general equations for these concepts are depicted above. How do cost functions relate to management strategy? The notion that cost structure plays a role in strategy and the exploitation of advantages is again a fundamental notion in competitive strategy. Let's look at the case of AOL. The fact that AOL, or that a software business, has high fixed costs and low marginal costs has very important implications about the role of installed base, and it has very important implications about how many firms can survive in the marketplace. I oftentimes in my competitive strategy class use the term "winner-take-all markets". These are markets in which only one firm will survive the competitive battle at the end of the day. What are the characteristics of winner-take-all markets? Well, one important characteristic is that they are markets with lots of operating leverage, low marginal costs, and high fixed costs. In any business with significant amounts of operating leverage, installed base is the name of the game. The key success factor is to build installed base and to build it quickly. And the firm that can win the race

4 for installed base, whether it's a software firm or some sort of internet firm (like an AOL for example), is going to be the one that is left standing at the end of the day. Fixed costs are those costs that are borne by a company regardless of the level of production. A company knows that it will incur these costs, and it knows with fairly high accuracy what the amount of the cost will be. Rent is a good example of a fixed cost. At the end of each month, a company knows it will have to pay rent for its office space and it knows exactly how much rent it will pay. Further, the company will pay the same amount of rent regardless of whether the company produces one unit of product or one thousand units of product for the month. Fixed Costs Costs that will remain unchanged whether sales increase or decrease over a fairly broad range of unit sales and production levels.

5 Variable costs are costs that vary with the level of production. A classic example of a variable cost is the cost of labor. The more products a company produces, the more workers it needs or the more hours it needs the current employees to work, and that increases the level of labor costs. Likewise, raw material costs are typically variable costs. As more products are produced, more units of raw material are needed. Variable Costs Costs that will change directly as sales and production levels change.

6 Fixed and variable costs represent the extremes of the cost "spectrum." However, between fixed and variable costs, there is a category of costs that are neither entirely fixed, nor entirely variable. These costs move in the same direction as production, but not in a directly proportional manner. A good example of a semi-fixed cost is equipment in a factory. The installed equipment represents a fixed cost. However, as production increases, there comes a time when the existing equipment does not have sufficient capacity. At that point, additional equipment must be purchased and equipment costs will jump higher. You can see the nature of this cost rise reflected in the step-like nature of the above graph.

7

8 An important variable for every firm is the total cost of production per unit of product produced and sold. A firm won't stay in business for long if the per unit revenue is less than the per unit total cost to produce the product. There are some key factors to determining total product cost. The first is defining what units the total cost is measured in and ensuring that all costs are measured in like units. For example, labor costs paid per hour and raw material costs paid by the pound must be converted to costs per unit produced. The second factor concerns the fixed and semi-fixed costs. Fixed and semi-fixed costs are associated with the production of the sum total of units. A mathematical methodology must be developed to allocate these expenses to individual units produced over the relevant time horizon.

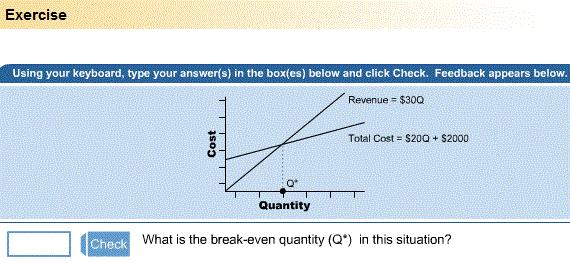

9 An important consideration for any company is the number of units of product that must be sold to cover costs. This quantity is called the break-even quantity. Therefore, if a company sells the break-even quantity exactly, its profit will be zero. Consider the above specific example of a company selling its product for $50 per unit. The costs associated with producing this product are summarized in the table above. The total revenue generated from selling Q units is Revenue = $50Q. Notice that this is a linear equation. Likewise, the total cost (variable costs + fixed costs) of building Q units is given by the linear equation $45Q + $4,000.

10 Recall that the break-even quantity is the quantity of units sold that results in Profit = 0. In other words, it is the quantity such that Revenue = Total Cost. Depicted above are two methods of determining the break-even quantity. As you can see, the breakeven quantity in this situation is 800. Therefore, when selling less than 800 units, the company has negative profit; when selling more than 800 units, the company has positive profit. revenues An accounting term referring to the inflows of assets as a result of a firm's ongoing operations.

11

12 A firm's break-even point and its ability to earn profits beyond the break-even point are impacted by its operating leverage. Operating leverage describes the sensitivity of profits to changes in revenue. Firms with high operating leverage tend to have higher fixed costs and lower variable costs, while firms with lower operating leverage have lower fixed costs and higher variable costs. A firm with high operating leverage has to generate more revenue to cover its fixed expenses than a company with low leverage. However, once break-even is achieved, each incremental dollar of revenue will contribute significantly to profits. For such a firm, a significant increase in demand leads to a large rise in profits. However, if demand falls unexpectedly, the impact to profits can be catastrophic. For the firm with lower operating leverage, the opposite is true. Due to lower fixed costs, breakeven is achieved more quickly. But beyond break-even, each dollar of revenue must cover a higher variable cost leaving less for profits. In and of itself, higher operating leverage is neither good nor bad. It is a reflection of the business model of the firm, and the nature of the industry the firm is a part of. However, it is important to understand a firm's operating leverage and the consequences of higher or lower leverage as market demand and revenues change. Fixed Costs Costs that will remain unchanged whether sales increase or decrease over a fairly broad range of unit sales and production levels. Variable Costs Costs that will change directly as sales and production levels change.