Going Back To School. Meet Sam

|

|

|

- Beatrice George

- 5 years ago

- Views:

Transcription

1 Going Back To School Meet Sam Graduating Class of 12 Not a single callback for an interview Decision to go back to school Joined millions of students Why?

2 The Costs of Production Chapter 9

3 Explicit Costs Explicit Costs (Accounting Costs) Requires an outlay of money Labor services Materials Fuels Transportation services

4 Implicit Costs Implicit Costs (Opportunity Costs) Does not require an outlay of money Measured by the value (in dollars) of: Forgone entrepreneurial income Foregone rent Forgone interest Forgone wages

5 Let s Return to Sam Complete 2-year Education graduate program Teach the World Revenue $600,000 (lifetime) Loans $40,000 Interest $4,000 Spend 2 years working in original field of Advertising Work with the Mad Men Revenue beginning in 2 years $500,000 (lifetime) What is Sam s Profit? $56,000 is Sam s Accounting Profit

6 Accounting Profit =Revenues-Explicit Costs Sam earned a +$100,000 with the decision to go back to school Accounting Profit $100,000 (Revenue)- $44,000 Explicit Costs Accounting costs (explicit costs only)

7 Let s Return to Sam Complete 2-year Education graduate program Teach the World Spend 2 years working in original field of Advertising Work with the Mad Men Revenue $600,000 (lifetime) Loans $40,000 Interest $4,000 Revenue beginning in 2 years $500,000 (lifetime) The best economic decisions need to take Economic Profit into account. What other values must we consider?

8 Let s Return to Sam Complete 2-year Education graduate program Teach the World Revenue $600,000 (lifetime) Loans $40,000 Interest $4,000 Spend 2 years working in original field of Advertising Work with the Mad Men Revenue beginning in 2 years Salary during the 1 st two years $500,000 (lifetime) 57,000 (forgone) Economic Profit= $100,000 $44,000 (explicit) - $57,000 (implicit) = -$ !!!

9 Economic Profit Economic Profit Implicit costs (including a normal profit) Explicit Costs =Revenues-Explicit Costs- Implicit Costs Sam earned a +$100,000 with the decision to go back to school $100,000 (Revenue)- $44,000 Explicit Costs $57,000 Implicit Costs

10 Economic (opportunity) Costs Profits to an Profits to an Economist Accountant Economic Profit Implicit costs (including a normal profit) Explicit Costs T O T A L R E V E N U E Accounting Profit Accounting costs (explicit costs only)

11 Did You Know??? Then (1880) Now (2012) 50% of land 10% of land Acre of Land National Average New England $2,100 $15,300 USDA Sub $4,949 $15,366

12 Irrational Behavior Misperceptions of opportunity costs Being overconfident Unrealistic expectations about the future Counting dollars unequally Being loss-averse Having a bias toward the status quo

Variable Costs (VC) State why each of theses costs are")

13 Production Costs Make a list of all the costs associated with the given product. Identify them as being either: Fixed Costs (FC) Variable Costs (VC) State why each of theses costs are presumed FC or VC. And the product is

14 Some Encouragement

15 Short Run A period too brief to alter plant capacity Plant capacity if fixed in short run Can use more/less intensely in SR Long enough to permit change in the degree to which the fixed plant is used. Hourly labor Raw materials Fuel Power

16 Long Run Long enough to adjust the quantities of ALL resources, including plant capacity Firms can dissolve and leave industry or new firms can enter industry Adding new production facility Install more equipment

17 Short Run Production Costs Fixed Costs Costs that in total do not vary with changes in output Must be paid even if output is zero Rental payments, interest on debts, insurance premiums Variable Costs Costs that change with the level of output Materials, fuel, most labor Total Costs Sum of fixed & variable costs at each level of output

18 Costs (dollars) SHORT-RUN COSTS GRAPHICALLY Combining TVC With TFC to get Total Cost TC TVC Fixed Cost Total Cost Variable Cost TFC Quantity

19 Concepts Summarized Short-run Measurement Definition Mathematical Term Fixed Cost Cost that does not depend on the quantity of output produced Average Fixed Cost Fixed cost per unit of output AFC = FC/Q FC Variable Cost Cost that depends on the quantity of output produced Average Variable Cost Variable cost per unit of output AVC = VC/Q VC Short Run and Long Run Total Cost The sum of fixed costs and variable cost TC = FC + VC Average Total Cost Total cost per unit of output ATC = TC/Q Marginal Cost The change in total cost generated by producing one more unit of output MC = TC/ Q Long Run Long Run Average Total Costs Average total cost when fixed cost has been chosen to minimize average total cost for each level of output LRATC

20 Short Run Production Relationships Total Product (TP) Marginal Product (MP) Average Product (AP)

21 Total Product Total Quantity or Total Output of a particular good being produced.

22 Marginal Product Extra output per additional unit of variable resources (labor) MP = Change in TP Change in Labor

23 Average Product Labor productivity Output per unit of labor input AP = TP Units of Labor

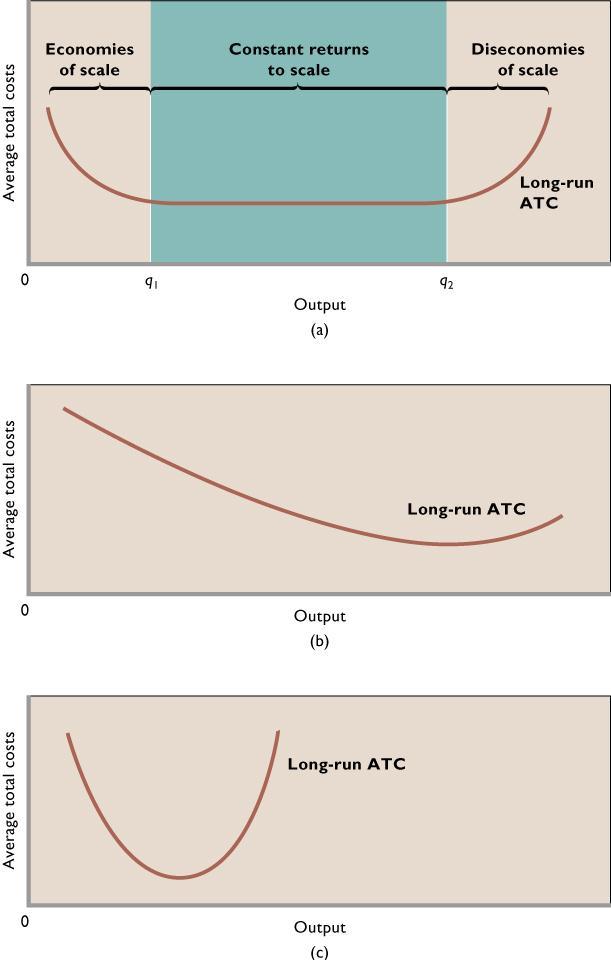

24 PRODUCTIVITY AND COST CURVES Average Product and Marginal Product Costs (dollars) AP MP Quantity of labor MC AVC Quantity of output

25 Average Product, AP, and Marginal Product, MP Total Product, TP SHORT-RUN PRODUCTION RELATIONSHIPS Law of Diminishing Returns Total Product Quantity of Labor Increasing Marginal Returns Quantity of Labor Average Product Marginal Product

26 Average Product, AP, and Marginal Product, MP Total Product, TP SHORT-RUN PRODUCTION RELATIONSHIPS Law of Diminishing Returns Total Product Quantity of Labor Diminishing Marginal Returns Quantity of Labor Average Product Marginal Product

27 Average Product, AP, and Marginal Product, MP Total Product, TP SHORT-RUN PRODUCTION RELATIONSHIPS Law of Diminishing Returns Total Product Quantity of Labor Negative Marginal Returns Quantity of Labor Average Product Marginal Product

28 Costs (dollars) SHORT-RUN COSTS GRAPHICALLY MC Plotting Average and Marginal Costs ATC AVC AFC Quantity

29 Marginal Cost Extra or additional cost of producing 1 more unit of output A firm can control MC directly and immediately Can be incurred or saved costs MC = Change in TC Change in Q

30 Marginal Costs MC intersects the ATC and AVC at their minimum points When MC is below ATC, ATC falls When MC is above ATC, ATC rises When MC is below AVC, AVC falls When MC is above AVC, AVC rises

31 Productivity Curves and Cost Curves MC curve and the AVC curve are mirror images of the MP and AP curves Assume labor is only variable input and price (wage rate) is constant When MP is rising, MC When MP is falling, MC When AP is rising, AVC When AP is falling,

32 Economies of Scale Economies of mass production Explain part of downward sloping longrun ATC Law of diminishing returns does not apply in the long-run Diminishing returns presume one resource is fixed in long run all resources are variable As plant size increases, a number of factors will for a time lead to lower average costs of production

33 Diseconomies of Scale Increases the average total cost of producing a product as the firm expands the size of its output in the long run Main cause is the difficulty to control operations as the firm becomes large scale producer

34

35 Normal Profit Cost of doing business Amount of money a firm must pay to obtain and retain an employee s entrepreneurial talent. Minimum income it would take to keep an employee