Quality Control Review of Air Force Audit Agency s Special Access Program Audits (Report No. D )

|

|

|

- Jason Wilkerson

- 5 years ago

- Views:

Transcription

1 August 26, 2005 Oversight Review Quality Control Review of Air Force Audit Agency s Special Access Program Audits (Report No. D ) Department of Defense Office of the Inspector General Quality Integrity Accountability

2 Report Documentation Page Form Approved OMB No Public reporting burden for the collection of information is estimated to average 1 hour per response, including the time for reviewing instructions, searching existing data sources, gathering and maintaining the data needed, and completing and reviewing the collection of information. Send comments regarding this burden estimate or any other aspect of this collection of information, including suggestions for reducing this burden, to Washington Headquarters Services, Directorate for Information Operations and Reports, 1215 Jefferson Davis Highway, Suite 1204, Arlington VA Respondents should be aware that notwithstanding any other provision of law, no person shall be subject to a penalty for failing to comply with a collection of information if it does not display a currently valid OMB control number. 1. REPORT DATE 26 AUG REPORT TYPE N/A 3. DATES COVERED - 4. TITLE AND SUBTITLE Oversight Review: Quality Control Review of Air Force Audit Agency s Special Access Program Audits 5a. CONTRACT NUMBER 5b. GRANT NUMBER 5c. PROGRAM ELEMENT NUMBER 6. AUTHOR(S) 5d. PROJECT NUMBER 5e. TASK NUMBER 5f. WORK UNIT NUMBER 7. PERFORMING ORGANIZATION NAME(S) AND ADDRESS(ES) Department of Defense Office of the Inspector General 400 Army Navy Drive Arlington, VA PERFORMING ORGANIZATION REPORT NUMBER 9. SPONSORING/MONITORING AGENCY NAME(S) AND ADDRESS(ES) 10. SPONSOR/MONITOR S ACRONYM(S) 12. DISTRIBUTION/AVAILABILITY STATEMENT Approved for public release, distribution unlimited 13. SUPPLEMENTARY NOTES 14. ABSTRACT 15. SUBJECT TERMS 11. SPONSOR/MONITOR S REPORT NUMBER(S) 16. SECURITY CLASSIFICATION OF: 17. LIMITATION OF ABSTRACT UU a. REPORT unclassified b. ABSTRACT unclassified c. THIS PAGE unclassified 18. NUMBER OF PAGES 17 19a. NAME OF RESPONSIBLE PERSON Standard Form 298 (Rev. 8-98) Prescribed by ANSI Std Z39-18

604-8760 or fax (703) 604-9808.")

3 Additional Copies To obtain additional copies of this report, visit the Web site of the Department of Defense Inspector General at or contact the Office of Audit Policy and Oversight at (703) or fax (703) Suggestions for Future Audits To suggest ideas for or to request future audits, contact the Office of Audit Policy and Oversight at (703) or fax (703) Ideas and requests can also be mailed to: OAIG-APO Department of Defense Inspector General 400 Army Navy Drive (Room 1015) Arlington, VA Acronyms AFAA AIC GAS NAS PCIE SAP Air Force Audit Agency Auditor-In-Charge Government Auditing Standards Naval Audit Service President s Council on Integrity and Efficiency Special Access Program

4

5

6 Appendix A. Scope and Methodology We limited our review to the adequacy of AFAA SAP auditors compliance with quality policies, procedures, and standards. We judgmentally selected 3 SAP audits from a universe of 27 formal reports issued by AFAA SAP auditors in FYs 2002, 2003, and 2004, and tested each audit for compliance with the AFAA system of quality control. The Naval Audit Service conducted a review of the AFAA internal quality control system for non-sap audits and/or attestation engagements and is issuing a separate report. The Assistant Inspector General for Audit Policy and Oversight will issue an overall opinion report on the AFAA internal quality control system that will include the combined results of the reviews of SAP and non-sap audits. In performing our review, we considered the requirements of quality control standards and other auditing standards contained in the 2003 Revision of the Government Auditing Standards (GAS) issued by the Comptroller General of the United States. GAS 3.52 states: The external peer review should determine whether, during the period under review, the reviewed audit organization s internal quality control system was adequate and whether quality control policies and procedures were being complied with to provide the audit organization with reasonable assurance of conforming to applicable professional standards. Audit organizations should take remedial, corrective actions based on the results of the peer review. We conducted this review in accordance with standards and guidelines established in the Draft 2004 President s Council on Integrity and Efficiency (PCIE) Guide for Conducting External Peer Reviews of the Audit Operations of Offices of Inspector General. We modified the Guide to ensure consistency with the Naval Audit Service review of non-sap audits, and to reflect the unique nature of auditing within a SAP environment. We interviewed AFAA auditors and their managers, reviewed AFAA internal audit-related policies and procedures. We performed this review in May 2005 at three AFAA field offices We used the following criteria to select the audits under review: Worked backward starting with FY 2004 audits in order to review the most current quality assurance procedures in place. Eliminated Base Realignment and Closure audits because they are not considered typical audits. Avoided audits with multiple SAPs associated with the audit for ease of access. Avoided audits that have the same or similar titles to ensure review of multiple types of projects. 3

7 The following table identifies the specific reports reviewed. Report Number Date Title F FA Jan 2004 Cash Controls F FA Jun 2004 Financial and Contracting Management F FA Jul 2004 Support Agreements Limitations of Review. Our review would not necessarily disclose all weaknesses in the system of quality control or all instances of noncompliance with it because we based our review on selective tests. There are inherent limitations in considering the potential effectiveness of any quality control system. In performing most control procedures, departures can result from misunderstanding of instructions, mistakes of judgment, carelessness, or other human factors. Projecting any evaluation of a quality control system into the future is subject to the risk that one or more procedures may become inadequate because conditions may change or the degree of compliance with procedures may deteriorate. 4

8 Appendix B. Comments, Observations, and Recommendations We are issuing an unqualified opinion because this is the first external peer review for AFAA SAP audits and the issues we identified were not cumulatively significant to the reports findings, conclusions, and recommendations. Overall, we found that AFAA could improve the quality control system and guidance for SAP audits related to the areas of Independence, Audit Planning, Supervision, Evidence and Audit Documentation, Reporting, and Quality Assurance. Implementing the recommendations identified below would improve the quality control system and help maintain an unqualified opinion. Independence. GAS 3.03 states that audit organizations and individual auditors should be free both in fact and appearance from personal, external, and organizational impairments to independence. AFAA Instruction (AFAAI) , Audit Management and Administration, requires auditors to sign an Independence Statement at the beginning of each audit to certify there are no relationships and beliefs that might cause the auditor or supervisor to limit the extent of the inquiry, limit disclosure, or slant audit findings in any way. We found no indications of impairment during our review. However, there were no Independence Statements for two of the three audits. The third audit had an Independence Statement that had been backdated by the auditor, who used a version of the AFAA Independence Statement that was not in effect until April 2004, after the date of his signature August The AFAA Chief, Special Programs Division stated that he had been unaware of the requirement for project-specific Independence Statements until the fall of He relied on annual Financial Disclosure Statements and the AFAA Annual Certification acknowledging the need to report any conflicts of interest to verify the auditors independence. However, AFAA had the project-specific Independence Standard in place since September 2002 and all three projects were initiated after this date. AFAA Policy, Oversight, and Systems Division personnel stated to us that new policy is placed on the AFAA intranet homepage, and disseminated in an to all AFAA personnel. 5

9 Audit Planning. GAS 7.02 states that work is to be adequately planned, and GAS 7.07 states that planning should be documented. GAS 7.41 requires auditors to document the planning, and states: [T]he form and content of the written audit plan will vary among audits, but should include an audit program or project plan, a memorandum, or other appropriate documentation of key decisions about the audit objectives, scope, and methodology and of the auditors basis for those decisions. It should be updated, as necessary, to reflect any significant changes to the plan made during the audit. AFAAI , Internal Audit Procedures, contains guidance on audit planning as well as a template audit planning program that all AFAA auditors are required to use during audits. AFAAI states that audit managers should: continuously monitor auditor progress during the planning phase, provide assistance as needed, and assure the auditor conducts the planning phase in accordance with AFAA policies and procedures; and ensure the auditor uses the Audit Planning Program and either completes each step or provides rationale for not completing the step. We found insufficient documentation related to audit planning in all three AFAA SAP audits we reviewed. For example, one of the audits did not have an audit program and another did not have supervisory approval for audit steps that were either not completed during the audit or were marked N/A. Supervision. GAS 7.45 requires staff to be properly supervised and GAS 7.47 states that supervisory reviews of audit work should be documented. AFAAI requires supervisors to use an Audit Review Record to document the supervision and supervisory reviews. According to AFAAI , the review record must include the supervisor s initials and date, and the working papers must contain clear evidence of supervisory review. We found that several working papers in each of the audits were either not reviewed in a timely manner or not reviewed at all by a supervisor. The AFAA Chief, Special Programs Division stated that since the office locations are widely scattered across the U.S., he visits each office only three to four times per year. In two audits, this prevented him from being able to review the working papers until five months after they were written. This is mitigated somewhat by the fact that all of the auditors at the AFAA SAP field offices are senior auditors. We recognize that the SAP audit environment presents challenges for complying with some of the AFAA quality processes. However, supervision is a key government auditing standard and a key element of an effective quality program. Supervisors must find ways to provide proper supervision even within such an environment. 6

10 Evidence and Audit Documentation. Working papers are used to organize, prepare, and collect relevant evidence and documentation during an audit. GAS 7.66 requires that auditors prepare and maintain audit documentation, and that the audit documentation should contain support for findings, conclusions, and recommendations before auditors issue their report. GAS 7.68 states that the audit documentation forms the principal support for the auditors report. AFAAI requires auditors to document the work performed to support significant conclusions and judgments, including descriptions of transactions and records examined that would enable an experienced auditor to examine the same transactions and records. AFAAI provides the following guidelines for working papers (excerpt): The working papers should be understandable without supplementary oral explanations. Anyone using or reviewing the working papers should be able to readily determine their purpose and source, the nature and scope of the work performed, and the auditor s conclusions. Although we found AFAA SAP audit working papers contained sufficient, competent, and relevant evidence to support judgments and conclusions in the reports, improvements could be made to audit documentation. We found that 6 of the 15 judgmentally selected facts and figures we reviewed in one report, 10 of 15 in another report, and 1 of 15 in the third report could have been better supported. Some of the deficiencies we noted during our review were: Source documents were missing information about the provider of the source documents, and in some cases it was impossible to determine whether a document was auditor-generated or a source document. Several figures in the report had no audit trail to source documents. We eventually identified the source documents and verified the data based on our review of source documents. A figure in the report referenced back to a note written by the auditor that did not include any source information. During our review, the auditor attributed the statement to management, but there was no attribution on the note or in the report. With such attribution a reviewer of the working papers or of the report can not know if the management that provided the information was a reliable source. Working papers, such as background information and briefing charts, were missing the AFAA-required elements of purpose, source, and conclusion. 7

11 Reporting. GAS 8.45 states that evidence included in audit reports should demonstrate the correctness and reasonableness of the matters reported GAS provides a best practice to help ensure this standard: One way to help ensure the audit report is accurate is to use a quality control process such as referencing in which an experienced auditor who is independent of the audit verifies that statements of fact, figures, and dates are correctly reported, that findings are adequately supported by the audit documentation, and that the conclusions and recommendations flow logically from the support. AFAAI requires auditors to obtain an independent reference review (IRR) before the draft report is issued to management. The guidance requires the independent referencers to trace information in the cross-referenced draft report through the summary working papers to the supporting working papers to determine that they are consistent with and supported by the working papers and to be alert to statements in the report which seem illogical or lack clarity, ensure the team chief has reviewed all supporting working papers and cleared any review notes, and refuse to sign the IRR record until the team chief has finished reviewing and signed off on the working papers. We found that the three AFAA SAP audit reports generally met the GAS reporting standards. However, none of the SAP reports we reviewed complied with the AFAA requirements for IRRs. None of the three reports received an IRR before the draft report was issued to management, and two of the three reports received no IRR. The AFAA Chief, Special Programs Division stated that he was unable to conduct IRRs before the draft reports were issued due to a lack of resources within the SAP environment, and that he relied on the experience of the auditors to ensure the quality of the audits. We found that the one completed IRR was not adequately documented; specifically, the referencer s signature on the IRR document was not dated so we were not able to ascertain whether the IRR was completed before the draft report was issued. Also, the referencer did not indicate any concerns during the IRR; however, we found discrepancies with the references, such as a figure cited in the report as representing fourth quarter data that was documented in the working papers as representing the first, second, and third quarters only. We found misleading or unsupported information in the final reports of the two audits that did not have IRRs. Although none of these inaccuracies affected the overall conclusions of the reports, they demonstrate instances that an IRR might have alerted the auditors to before the reports were issued to management. Specifically, we found: A figure cited in the report as a contract was established in April 2000 for $421.0 million ; however, $421.0 million was the amount of the contract after several contract modifications; the amount of the contract at the date of establishment was $402.0 million. 8

12 A figure cited in the report as $330,000 was documented in the working papers as $300,000. A figure cited in the report as 52 percent was documented in the working papers as 53 percent. Over time if errors continue to be found in reports, the report recipients may begin to question significant conclusions of the reports. AFAAI does not exclude the IRR from the SAP audits and does not define circumstances in which an IRR need not be done. Quality Assurance. GAS 3.50 requires than an audit organizations internal quality control system should include procedures for monitoring, on an ongoing basis, whether the policies and procedures related to the standards are suitably designed and are being effectively applied. This is often referred to as an internal quality assurance program. AFAAI , Internal Quality Control Review Program, provides guidance on the AFAA internal quality control program, and notes that it consists of four components: supervision, independent referencing, internal quality control reviews, and external quality control reviews. AFAA conducts three types of internal reviews: functional, management, and quality assurance. Quality assurance reviews evaluate whether AFAA activities adhere to applicable government auditing standards and internal policies and procedures for conducting audit projects. The AFAA internal quality control review program uses a team approach to accomplish this type review and a checklist based on GAS and AFAA policies and procedures. The AFAA Policy, Oversight, and Systems Division develops an annual review plan that describes the functional, management, and quality assurance reviews planned for the next year. The AFAA Policy, Oversight, and Systems Division also prepares a 3-year review plan for quality assurance reviews which ensures each AFAA audit division/region receives a quality assurance review at least once during the 3-year cycle. AFAAI does not exempt or waive SAP audits. However, AFAA personnel involved with the internal quality control review program stated that they do not conduct quality assurance reviews of SAP audits. AFAA has not conducted a quality assurance review of a SAP audit in at least 10 years, specifically due to the limitations on access because of security requirements. Conclusion. SAP audits seldom get the monitoring or oversight of non-sap audits because of the security requirements. AFAA guidance on the quality control system does not specifically address SAP audits. The AFAA Chief, Special Program Division has stated that he is unable to fully implement key elements of the AFAA quality control 9

13 system because of security-related limitations. We recognize the challenges that result from these limitations; however, AFAA needs to re-emphasize the importance of complying with the key elements of the quality control system. Although we did not find that any of the deficiencies we noted would individually or collectively justify an opinion other than unqualified, AFAA needs to ensure on an ongoing basis that their internal quality control system within the SAP environment taken as a whole still provides reasonable assurance that GAS is met. Recommendations. We recommend that the Air Force Auditor General: 1. Stress to SAP auditors the importance of complying with existing guidance and procedures related to independence, specifically in completing independence statements. Management Comments. The AFAA concurred in principle with the recommendation and stated that while they agree improvements were needed to document their independence on each project, the AFAA does not believe recommending a specific software package was inappropriate. The AFAA stated that the audit evaluated various processes used at several locations and recommended streamlining and improving the entire operation. At the Command-level, the newly developed software package allowed the auditor to easily reconcile total cash accountability. However, reconciliation was difficult and labor intensive at subordinate units because the tracking systems were not as effective. As a result, the AFAA report stated that the units used different procedures and recommended the Command direct use of the Command-level software package. While working paper documentation could have been better, the AFAA stated that they complied with GAS 3.14 and had sufficient evidence to justify recommending the Command-level system. The Special Programs Division Chief will issue a memorandum by September 30, 2005, to all SAP auditors stressing the importance of complying with guidance related to independence, including preparing independence statements and providing advice to management. Reviewer Response. Management comments meet the intent of the recommendation. We revised the report including this recommendation based on comments to the draft report related to circumstances in which the auditor provided advice to the command. No further comments are required. 10

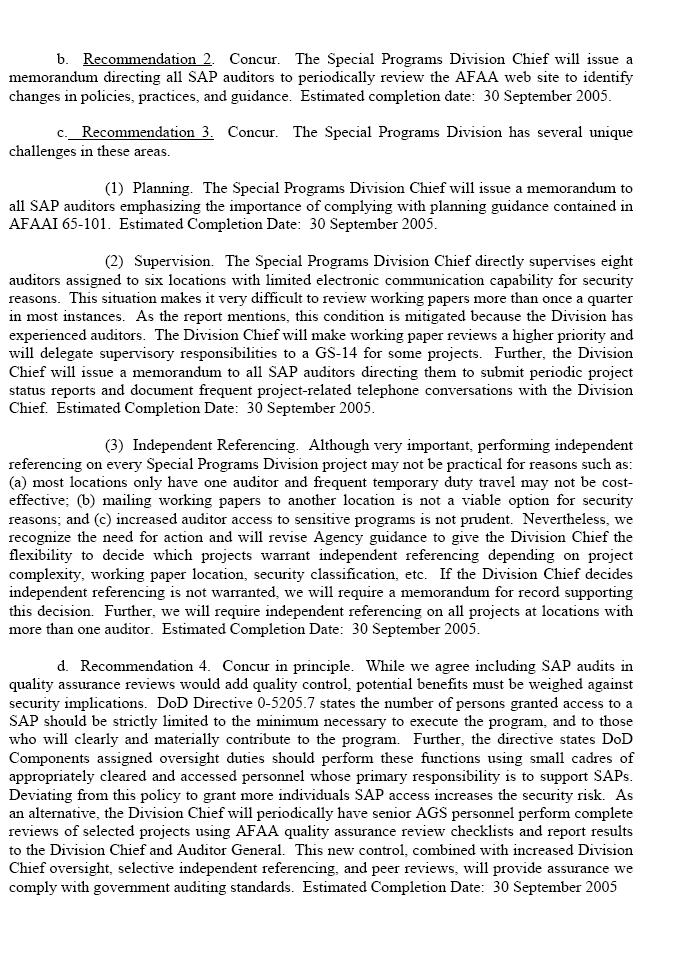

14 2. Ensure that the SAP auditors and supervisors are timely made aware of changes in policies, practices and guidance. Management Comments. The AFAA concurred with the recommendation and stated that the Special Programs Division Chief will issue a memorandum by September 30, 2005, directing all SAP auditors to periodically review the AFAA web site to identify changes in policies, practices, and guidance. Reviewer Response. Management comments are responsive. 3. Re-emphasize to SAP auditors and supervisors the importance of complying with the key elements of the AFAA quality control system, specifically related to audit planning, supervisory reviews, and independent reference reviews. Management Comments. The AFAA concurred with the recommendation and stated that for audit planning the Special Programs Division Chief will issue a memorandum by September 30, 2005, to all SAP auditors emphasizing the importance of complying with planning guidance contained in AFAAI Regarding supervision, the AFAA stated that the Special Programs Division Chief will make working paper reviews a higher priority and will delegate supervisory responsibilities to a GS-14 for some projects. In addition, the Division Chief will issue a memorandum by September 30, 2005, to all SAP auditors directing them to submit periodic project status reports and document project related telephone conversations with the Division Chief. For independent referencing, although very important, the AFAA stated that performing independent referencing on every Special Programs Division project may not be practical for reasons such as security considerations and most locations have only one auditor and temporary duty travel may not be cost-effective. However, the AFAA will revise guidance by September 30, 2005, to give the Division Chief the flexibility to decide which projects warrant independent referencing depending on project complexity, working paper location, and security classification. If the Division Chief decides independent referencing is not warranted, a memorandum for record supporting the decision will be required. Also, independent referencing on all projects at locations with more than one auditor will be required. Reviewer Response. Management comments meet the intent of recommendation. 11

15 4. Establish as part of its internal quality control review program, internal quality assurance reviews of selected SAP audits in order to comply with GAS Management Comments. The AFAA concurred in principle with the intent of the recommendation and stated while they agree including SAP audits in quality assurance reviews would add quality control, potential benefits must be weighed against security implications. As an alternative, the Division Chief will have senior personnel perform complete reviews of selected projects using AFAA quality assurance review checklists and report results to the Division Chief and Auditor General. Reviewer Response. Management comments meet the intent of recommendation. We recognize that the SAP audits could not necessarily be treated the same as non-sap audits in the internal quality assurance program. The AFAA alternative procedures meet the intent of GAS for on-going monitoring. 12

16 Appendix C. Management Comments 13

17 Final Report Reference Revised at pg. 11 Revised Report at pg. 6 14

18 15

Oversight Review January 27, Quality Control Review of Army Audit Agency's Special Access Program Audits. Report No.

Oversight Review January 27, 2012 Quality Control Review of Army Audit Agency's Special Access Program Audits Report No. DODIG-2012-045 Report Documentation Page Form Approved OMB No. 0704-0188 Public

Oversight Review January 27, 2012 Quality Control Review of Army Audit Agency's Special Access Program Audits Report No. DODIG-2012-045 Report Documentation Page Form Approved OMB No. 0704-0188 Public

Report No. DODIG September 10, Quality Control Review of the Defense Commissary Agency Internal Audit Function

Report No. DODIG-2012-126 September 10, 2012 Quality Control Review of the Defense Commissary Agency Internal Audit Function Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting burden

Report No. DODIG-2012-126 September 10, 2012 Quality Control Review of the Defense Commissary Agency Internal Audit Function Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting burden

Report Documentation Page

Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting burden for the collection of information is estimated to average 1 hour per response, including the time for reviewing instructions,

Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting burden for the collection of information is estimated to average 1 hour per response, including the time for reviewing instructions,

Report No. DODIG August 7, External Quality Control Review of the Defense Information Systems Agency Audit Organization

Report No. DODIG-2012-116 August 7, 2012 External Quality Control Review of the Defense Information Systems Agency Audit Organization Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting

Report No. DODIG-2012-116 August 7, 2012 External Quality Control Review of the Defense Information Systems Agency Audit Organization Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting

Report No. D August 1, Internal Controls Over U.S. Army Corps of Engineers, Civil Works, Disbursement Processes

Report No. D-2011-094 August 1, 2011 Internal Controls Over U.S. Army Corps of Engineers, Civil Works, Disbursement Processes Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting

Report No. D-2011-094 August 1, 2011 Internal Controls Over U.S. Army Corps of Engineers, Civil Works, Disbursement Processes Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting

Report No. D February 9, Controls Over Time and Attendance Reporting at the National Geospatial-Intelligence Agency

Report No. D-2009-051 February 9, 2009 Controls Over Time and Attendance Reporting at the National Geospatial-Intelligence Agency Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting

Report No. D-2009-051 February 9, 2009 Controls Over Time and Attendance Reporting at the National Geospatial-Intelligence Agency Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting

COMPLIANCE WITH THIS PUBICATION IS MANDATORY

BY ORDER OF THE COMMANDER AIR FORCE AUDIT AGENCY AIR FORCE AUDIT AGENCY INSTRUCTION 65-105 19 NOVEMBER 2010 Financial Management INTERNAL QUALITY CONTROL PROGRAM COMPLIANCE WITH THIS PUBICATION IS MANDATORY

BY ORDER OF THE COMMANDER AIR FORCE AUDIT AGENCY AIR FORCE AUDIT AGENCY INSTRUCTION 65-105 19 NOVEMBER 2010 Financial Management INTERNAL QUALITY CONTROL PROGRAM COMPLIANCE WITH THIS PUBICATION IS MANDATORY

Implementation of the Best in Class Project Management and Contract Management Initiative at the U.S. Department of Energy s Office of Environmental

Implementation of the Best in Class Project Management and Contract Management Initiative at the U.S. Department of Energy s Office of Environmental Management How It Can Work For You NDIA - E2S2 Conference

Implementation of the Best in Class Project Management and Contract Management Initiative at the U.S. Department of Energy s Office of Environmental Management How It Can Work For You NDIA - E2S2 Conference

Joint JAA/EUROCONTROL Task- Force on UAVs

Joint JAA/EUROCONTROL Task- Force on UAVs Presentation at UAV 2002 Paris 11 June 2002 Yves Morier JAA Regulation Director 1 Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting burden

Joint JAA/EUROCONTROL Task- Force on UAVs Presentation at UAV 2002 Paris 11 June 2002 Yves Morier JAA Regulation Director 1 Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting burden

Oversight Review March 16, External Quality Control Review of the Defense Logistics Agency Audit Organization. Report No.

Oversight Review March 16, 2011 External Quality Control Review of the Defense Logistics Agency Audit Organization Report No. D-2011-6-005 Report Documentation Page Form Approved OMB No. 0704-0188 Public

Oversight Review March 16, 2011 External Quality Control Review of the Defense Logistics Agency Audit Organization Report No. D-2011-6-005 Report Documentation Page Form Approved OMB No. 0704-0188 Public

Improvements to Hazardous Materials Audit Program Prove Effective

7 5 T H A I R B A S E W I N G Improvements to Hazardous Materials Audit Program Prove Effective 2009 Environment, Energy and Sustainability Symposium and Exhibition Report Documentation Page Form Approved

7 5 T H A I R B A S E W I N G Improvements to Hazardous Materials Audit Program Prove Effective 2009 Environment, Energy and Sustainability Symposium and Exhibition Report Documentation Page Form Approved

Tactical Equipment Maintenance Facilities (TEMF) Update To The Industry Workshop

Update To The Industry Workshop") 1 Tactical Equipment Maintenance Facilities (TEMF) Update To The Industry Workshop LTC Jaime Lugo HQDA, ODCS, G4 Log Staff Officer Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting

1 Tactical Equipment Maintenance Facilities (TEMF) Update To The Industry Workshop LTC Jaime Lugo HQDA, ODCS, G4 Log Staff Officer Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting

Trends in Acquisition Workforce. Mr. Jeffrey P. Parsons Executive Director Army Contracting Command

Trends in Acquisition Workforce Mr. Jeffrey P. Parsons Executive Director Army Contracting Command Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting burden for the collection of

Trends in Acquisition Workforce Mr. Jeffrey P. Parsons Executive Director Army Contracting Command Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting burden for the collection of

Fort Belvoir Compliance-Focused EMS. E2S2 Symposium Session June 16, 2010

Fort Belvoir Compliance-Focused EMS E2S2 Symposium Session 10082 June 16, 2010 Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting burden for the collection of information is estimated

Fort Belvoir Compliance-Focused EMS E2S2 Symposium Session 10082 June 16, 2010 Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting burden for the collection of information is estimated

Issues for Future Systems Costing

Issues for Future Systems Costing Panel 17 5 th Annual Acquisition Research Symposium Fred Hartman IDA/STD May 15, 2008 Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting burden

Issues for Future Systems Costing Panel 17 5 th Annual Acquisition Research Symposium Fred Hartman IDA/STD May 15, 2008 Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting burden

Earned Value Management on Firm Fixed Price Contracts: The DoD Perspective

Earned Value Management on Firm Fixed Price Contracts: The DoD Perspective Van Kinney Office of the Under Secretary of Defense (Acquisition & Technology) REPORT DOCUMENTATION PAGE Form Approved OMB No.

Earned Value Management on Firm Fixed Price Contracts: The DoD Perspective Van Kinney Office of the Under Secretary of Defense (Acquisition & Technology) REPORT DOCUMENTATION PAGE Form Approved OMB No.

Robustness of Communication Networks in Complex Environments - A simulations using agent-based modelling

Robustness of Communication Networks in Complex Environments - A simulations using agent-based modelling Dr Adam Forsyth Land Operations Division, DSTO MAJ Ash Fry Land Warfare Development Centre, Australian

Robustness of Communication Networks in Complex Environments - A simulations using agent-based modelling Dr Adam Forsyth Land Operations Division, DSTO MAJ Ash Fry Land Warfare Development Centre, Australian

75th MORSS CD Cover Page UNCLASSIFIED DISCLOSURE FORM CD Presentation

75th MORSS CD Cover Page UNCLASSIFIED DISCLOSURE FORM CD Presentation 712CD For office use only 41205 12-14 June 2007, at US Naval Academy, Annapolis, MD Please complete this form 712CD as your cover page

75th MORSS CD Cover Page UNCLASSIFIED DISCLOSURE FORM CD Presentation 712CD For office use only 41205 12-14 June 2007, at US Naval Academy, Annapolis, MD Please complete this form 712CD as your cover page

A Family of SCAMPI SM Appraisal Methods

Pittsburgh, PA 15213-3890 CMMI SM A Family of SCAMPI SM Appraisal Methods Will Hayes Gene Miluk Dave Kitson Sponsored by the U.S. Department of Defense 2003 by University SM CMMI, CMM Integration, and

Pittsburgh, PA 15213-3890 CMMI SM A Family of SCAMPI SM Appraisal Methods Will Hayes Gene Miluk Dave Kitson Sponsored by the U.S. Department of Defense 2003 by University SM CMMI, CMM Integration, and

Army Quality Assurance & Administration of Strategically Sourced Services

Army Quality Assurance & Administration of Strategically Sourced Services COL Tony Incorvati ITEC4, ACA 1 Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting burden for the collection

Army Quality Assurance & Administration of Strategically Sourced Services COL Tony Incorvati ITEC4, ACA 1 Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting burden for the collection

Sustainable Management of Available Resources and Technology (SMART) Cleanup

Cleanup") Sustainable Management of Available Resources and Technology (SMART) Cleanup Mr. Samuel Pierre (703) 601-1550 Headquarters, Department of the Army OACSIM, Installations Service Directorate Environmental

Sustainable Management of Available Resources and Technology (SMART) Cleanup Mr. Samuel Pierre (703) 601-1550 Headquarters, Department of the Army OACSIM, Installations Service Directorate Environmental

Systems Engineering Processes Applied To Ground Vehicle Integration at US Army Tank Automotive Research, Development, and Engineering Center (TARDEC)

") 2010 NDIA GROUND VEHICLE SYSTEMS ENGINEERING AND TECHNOLOGY SYMPOSIUM SYSTEMS ENGINEERING MINI-SYMPOSIUM AUGUST 17-19 DEARBORN, MICHIGAN Systems Engineering Processes Applied To Ground Vehicle Integration

2010 NDIA GROUND VEHICLE SYSTEMS ENGINEERING AND TECHNOLOGY SYMPOSIUM SYSTEMS ENGINEERING MINI-SYMPOSIUM AUGUST 17-19 DEARBORN, MICHIGAN Systems Engineering Processes Applied To Ground Vehicle Integration

ITEA LVC Special Session on W&A

ITEA LVC Special Session on W&A Sarah Aust and Pat Munson MDA M&S Verification, Validation, and Accreditation Program DISTRIBUTION STATEMENT A. Approved for public release; distribution is unlimited. Approved

ITEA LVC Special Session on W&A Sarah Aust and Pat Munson MDA M&S Verification, Validation, and Accreditation Program DISTRIBUTION STATEMENT A. Approved for public release; distribution is unlimited. Approved

11. KEYNOTE 2 : Rebuilding the Tower of Babel Better Communication with Standards

DSTO-GD-0734 11. KEYNOTE 2 : Rebuilding the Tower of Babel Better Communication with Standards Abstract Matthew Hause Co-chair of the UPDM group, OMG The book of Genesis tells the story of how the peoples

DSTO-GD-0734 11. KEYNOTE 2 : Rebuilding the Tower of Babel Better Communication with Standards Abstract Matthew Hause Co-chair of the UPDM group, OMG The book of Genesis tells the story of how the peoples

Augmenting Task-Centered Design With Operator State Assessment Technologies

Augmenting Task-Centered Design With Operator State Assessment Technologies Karl F. Van Orden Erik Viirre David A. Kobus Naval Health Research Center Technical Document No. 07-6F Book Chapter Augmented

Augmenting Task-Centered Design With Operator State Assessment Technologies Karl F. Van Orden Erik Viirre David A. Kobus Naval Health Research Center Technical Document No. 07-6F Book Chapter Augmented

versight eport DEFENSE CONTRACT AUDIT AGENCY S ROLE IN INTEGRATED PRODUCT TEAMS Report Number D March 23, 2001

versight eport DEFENSE CONTRACT AUDIT AGENCY S ROLE IN INTEGRATED PRODUCT TEAMS Report Number D-2001-6-003 March 23, 2001 Office of the Inspector General Department of Defense Form SF298 Citation Data

versight eport DEFENSE CONTRACT AUDIT AGENCY S ROLE IN INTEGRATED PRODUCT TEAMS Report Number D-2001-6-003 March 23, 2001 Office of the Inspector General Department of Defense Form SF298 Citation Data

Agenda. Current Acquisition Environment-Strategic Sourcing. Types of Contract Vehicles. Specific Contract Vehicles for Navy-wide Use DOD EMALL

Agenda Current Acquisition Environment-Strategic Sourcing Types of Contract Vehicles Specific Contract Vehicles for Navy-wide Use DOD EMALL Conclusion 1 Report Documentation Page Form Approved OMB No.

Agenda Current Acquisition Environment-Strategic Sourcing Types of Contract Vehicles Specific Contract Vehicles for Navy-wide Use DOD EMALL Conclusion 1 Report Documentation Page Form Approved OMB No.

Biased Cramer-Rao lower bound calculations for inequality-constrained estimators (Preprint)

") AFRL-DE-PS- JA-2007-1011 AFRL-DE-PS- JA-2007-1011 Biased Cramer-Rao lower bound calculations for inequality-constrained estimators (Preprint) Charles Matson Alim Haji 1 September 2006 Journal Article APPROVED

AFRL-DE-PS- JA-2007-1011 AFRL-DE-PS- JA-2007-1011 Biased Cramer-Rao lower bound calculations for inequality-constrained estimators (Preprint) Charles Matson Alim Haji 1 September 2006 Journal Article APPROVED

U.S. Trade Deficit and the Impact of Rising Oil Prices

Order Code RS22204 Updated December 13, 2006 U.S. Trade Deficit and the Impact of Rising Oil Prices James K. Jackson Specialist in International Trade and Finance Foreign Affairs, Defense, and Trade Division

Order Code RS22204 Updated December 13, 2006 U.S. Trade Deficit and the Impact of Rising Oil Prices James K. Jackson Specialist in International Trade and Finance Foreign Affairs, Defense, and Trade Division

How to Pass an ALGA Yellow Book Peer Review Training by the Association of Local Government Auditors (ALGA) Tampa, Florida September 20, 2013

Tampa, Florida September 20, 2013") How to Pass an ALGA Yellow Book Peer Review Training by the Association of Local Government Auditors (ALGA) Tampa, Florida September 20, 2013 7:30 8:00 Continental Breakfast & Registration 8:00 8:30 Section

How to Pass an ALGA Yellow Book Peer Review Training by the Association of Local Government Auditors (ALGA) Tampa, Florida September 20, 2013 7:30 8:00 Continental Breakfast & Registration 8:00 8:30 Section

Defense Business Board

TRANSITION TOPIC: Vision For DoD TASK: Develop a sample vision statement for DoD. In doing so assess the need, identify what a good vision statement should cause to happen, and assess the right focus for

TRANSITION TOPIC: Vision For DoD TASK: Develop a sample vision statement for DoD. In doing so assess the need, identify what a good vision statement should cause to happen, and assess the right focus for

Decision Framework for Incorporation of Sustainability into Army Environmental Remediation Projects

Decision Framework for Incorporation of Sustainability into Army Environmental Remediation Projects Carol Lee Dona, Ph.D., P.E. Michael M. Bailey, Ph.D., P.G. US Army Corps of Engineers Environmental and

Decision Framework for Incorporation of Sustainability into Army Environmental Remediation Projects Carol Lee Dona, Ph.D., P.E. Michael M. Bailey, Ph.D., P.G. US Army Corps of Engineers Environmental and

Enterprise Business System Was Not Configured to Implement the U.S. Government Standard General Ledger at the Transaction Level

Report No. DODIG-2013-057 March 20, 2013 Enterprise Business System Was Not Configured to Implement the U.S. Government Standard General Ledger at the Transaction Level Report Documentation Page Form Approved

Report No. DODIG-2013-057 March 20, 2013 Enterprise Business System Was Not Configured to Implement the U.S. Government Standard General Ledger at the Transaction Level Report Documentation Page Form Approved

Earned Value Management from a Behavioral Perspective ARMY

Earned Value Management from a Behavioral Perspective ARMY Henry C. Dubin May 24, 2000 dubinh@sarda.army.mil REPORT DOCUMENTATION PAGE Form Approved OMB No. 0704-0188 Public reporting burder for this collection

Earned Value Management from a Behavioral Perspective ARMY Henry C. Dubin May 24, 2000 dubinh@sarda.army.mil REPORT DOCUMENTATION PAGE Form Approved OMB No. 0704-0188 Public reporting burder for this collection

INVASIVE SPECIES IMPACT ON THE DEPARTMENT OF DEFENSE

INVASIVE SPECIES IMPACT ON THE DEPARTMENT OF DEFENSE By Alfred Cofrancesco 2004 Department of Defense Conservation Conference Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting

INVASIVE SPECIES IMPACT ON THE DEPARTMENT OF DEFENSE By Alfred Cofrancesco 2004 Department of Defense Conservation Conference Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting

Army Systems Engineering Career Development Model

Army Systems Engineering Career Development Model Final Technical Report SERC-2014-TR-042-2 March 28, 2014 Principal Investigators Dr. Val Gavito, Stevens Institute of Technology Dr. Michael Pennotti,

Army Systems Engineering Career Development Model Final Technical Report SERC-2014-TR-042-2 March 28, 2014 Principal Investigators Dr. Val Gavito, Stevens Institute of Technology Dr. Michael Pennotti,

Energy Security: A Global Challenge

A presentation from the 2009 Topical Symposium: Energy Security: A Global Challenge Hosted by: The Institute for National Strategic Studies of The National Defense University 29-30 September 2009 By DAVID

A presentation from the 2009 Topical Symposium: Energy Security: A Global Challenge Hosted by: The Institute for National Strategic Studies of The National Defense University 29-30 September 2009 By DAVID

NEC2 Effectiveness and Agility: Analysis Methodology, Metrics, and Experimental Results*

NEC2 Effectiveness and Agility: Analysis Methodology, Metrics, and Experimental Results* David S. Alberts dalberts@ida.org Mark E. Tillman mtillman@ida.org presented to MORS Workshop Joint Framework for

NEC2 Effectiveness and Agility: Analysis Methodology, Metrics, and Experimental Results* David S. Alberts dalberts@ida.org Mark E. Tillman mtillman@ida.org presented to MORS Workshop Joint Framework for

PL and Payment of CWA Stormwater Fees

Environment, Energy Security & Sustainability Symposium PL 111-378 and Payment of CWA Stormwater Fees Joe Cole Senior-Attorney Advisor USAF Environmental Law Field Support Center The opinions and conclusions

Environment, Energy Security & Sustainability Symposium PL 111-378 and Payment of CWA Stormwater Fees Joe Cole Senior-Attorney Advisor USAF Environmental Law Field Support Center The opinions and conclusions

Contractor Past Performance Information: An Analysis of Assessment Narratives and Objective Ratings. Rene G. Rendon Uday Apte Michael Dixon

Contractor Past Performance Information: An Analysis of Assessment Narratives and Objective Ratings Rene G. Rendon Uday Apte Michael Dixon Report Documentation Page Form Approved OMB No. 0704-0188 Public

Contractor Past Performance Information: An Analysis of Assessment Narratives and Objective Ratings Rene G. Rendon Uday Apte Michael Dixon Report Documentation Page Form Approved OMB No. 0704-0188 Public

U.S. Trade Deficit and the Impact of Rising Oil Prices

Order Code RS22204 Updated May 30, 2007 U.S. Trade Deficit and the Impact of Rising Oil Prices James K. Jackson Specialist in International Trade and Finance Foreign Affairs, Defense, and Trade Division

Order Code RS22204 Updated May 30, 2007 U.S. Trade Deficit and the Impact of Rising Oil Prices James K. Jackson Specialist in International Trade and Finance Foreign Affairs, Defense, and Trade Division

REFERENCE COPY TECHNICAL LIBRARY, E231 DAHLGREN DIVISION NAVAL SURFACE WARFARE CENTER DO NOT REMOUE. Science and. Engineerng

REFERENCE COPY TECHNICAL LIBRARY, E231 DAHLGREN DIVISION NAVAL SURFACE WARFARE CENTER DO NOT REMOUE I Science and Engineerng N r Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting

REFERENCE COPY TECHNICAL LIBRARY, E231 DAHLGREN DIVISION NAVAL SURFACE WARFARE CENTER DO NOT REMOUE I Science and Engineerng N r Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting

73rd MORSS CD Cover Page UNCLASSIFIED DISCLOSURE FORM CD Presentation

73rd MORSS CD Cover Page UNCLASSIFIED DISCLOSURE FORM CD Presentation 712CD For office use only 41205 21-23 June 2005, at US Military Academy, West Point, NY Please complete this form 712CD as your cover

73rd MORSS CD Cover Page UNCLASSIFIED DISCLOSURE FORM CD Presentation 712CD For office use only 41205 21-23 June 2005, at US Military Academy, West Point, NY Please complete this form 712CD as your cover

Panel 5 - Open Architecture, Open Business Models and Collaboration for Acquisition

Panel 5 - Open Architecture, Open Business Models and Collaboration for Acquisition Mr. Bill Johnson Deputy Major Program Manager Future Combat Systems Open Architecture (PEO-IWS 7DEP) Report Documentation

Panel 5 - Open Architecture, Open Business Models and Collaboration for Acquisition Mr. Bill Johnson Deputy Major Program Manager Future Combat Systems Open Architecture (PEO-IWS 7DEP) Report Documentation

Tailoring Earned Value Management

cost work schedule Tailoring Earned Value Management General Guidelines Eleanor Haupt ASC/FMCE Wright-Patterson AFB OH REPORT DOCUMENTATION PAGE Form Approved OMB No. 0704-0188 Public reporting burder

cost work schedule Tailoring Earned Value Management General Guidelines Eleanor Haupt ASC/FMCE Wright-Patterson AFB OH REPORT DOCUMENTATION PAGE Form Approved OMB No. 0704-0188 Public reporting burder

Kelly Black Neptune & Company, Inc.

New EPA QA Guidance for Quality Management and QA Project Plans Kelly Black Neptune & Company, Inc. Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting burden for the collection

New EPA QA Guidance for Quality Management and QA Project Plans Kelly Black Neptune & Company, Inc. Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting burden for the collection

EXPLOSIVE CAPACITY DETERMINATION SYSTEM. The following provides the Guidelines for Use of the QDARC Program for the PC.

EXPLOSIVE CAPACITY DETERMINATION SYSTEM Since the inception of explosive constrained storage structures, the determination of the individual structures' capacities has been one of much labor intensive

EXPLOSIVE CAPACITY DETERMINATION SYSTEM Since the inception of explosive constrained storage structures, the determination of the individual structures' capacities has been one of much labor intensive

Common Criteria Evaluation and Validation Scheme For. Information Technology Laboratory. Guidance to Validators of IT Security Evaluations

Common Criteria Evaluation and Validation Scheme For Information Technology Security Guidance to Validators of IT Security Evaluations Scheme Publication #3 Version 1.0 February 2002 National Institute

Common Criteria Evaluation and Validation Scheme For Information Technology Security Guidance to Validators of IT Security Evaluations Scheme Publication #3 Version 1.0 February 2002 National Institute

OUSD(A&T) Initiatives Update. Wayne Abba 8th Annual International Cost Schedule Performance Management Conference

Initiatives Update. Wayne Abba 8th Annual International Cost Schedule Performance Management Conference") OUSD(A&T) Initiatives Update Wayne Abba 8th Annual International Cost Schedule Performance Management Conference October 27, 1996 REPORT DOCUMENTATION PAGE Form Approved OMB No. 0704-0188 Public reporting

OUSD(A&T) Initiatives Update Wayne Abba 8th Annual International Cost Schedule Performance Management Conference October 27, 1996 REPORT DOCUMENTATION PAGE Form Approved OMB No. 0704-0188 Public reporting

US Naval Open Systems Architecture Strategy

US Naval Open Systems Architecture Strategy Nick Guertin Brian Womble United States Navy Adam Porter University of Maryland Douglas C. Schmidt Vanderbilt University SATURN 2012, St. Petersburg, FL, May

US Naval Open Systems Architecture Strategy Nick Guertin Brian Womble United States Navy Adam Porter University of Maryland Douglas C. Schmidt Vanderbilt University SATURN 2012, St. Petersburg, FL, May

Trusted Computing Exemplar: Configuration Management Plan

Calhoun: The NPS Institutional Archive DSpace Repository Reports and Technical Reports All Technical Reports Collection 2014-12-12 Trusted Computing Exemplar: Configuration Management Plan Clark, Paul

Calhoun: The NPS Institutional Archive DSpace Repository Reports and Technical Reports All Technical Reports Collection 2014-12-12 Trusted Computing Exemplar: Configuration Management Plan Clark, Paul

DoD Sustainability Strategy The Latest. Mr. Dave Asiello DUSD(I&E)/CMRM

/CMRM") DoD Sustainability Strategy The Latest Mr. Dave Asiello DUSD(I&E)/CMRM Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting burden for the collection of information is estimated to

DoD Sustainability Strategy The Latest Mr. Dave Asiello DUSD(I&E)/CMRM Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting burden for the collection of information is estimated to

Success with the DoD Mentor Protégé Program

Department of the Navy - Office of Small Business Programs 23rd Annual NAVY Gold Coast Small Business Symposium San Diego, CA Success with the DoD Mentor Protégé Program Vernon M. Reid, PE August 23, 2011

Department of the Navy - Office of Small Business Programs 23rd Annual NAVY Gold Coast Small Business Symposium San Diego, CA Success with the DoD Mentor Protégé Program Vernon M. Reid, PE August 23, 2011

UNITED STATES MARINE CORPS MARINE CORPS BASE 3250 CATLIN AVENUE QUANTICO VIRGINIA IN REPLY REFER TO: MCBO 5200.

UNITED STATES MARINE CORPS MARINE CORPS BASE 3250 CATLIN AVENUE QUANTICO VIRGINIA 22134 5001 IN REPLY REFER TO: MCBO 5200.3 B 64 MARINE CORPS BASE ORDER 5200.3 From: Commander To: Distribution List Subj:

UNITED STATES MARINE CORPS MARINE CORPS BASE 3250 CATLIN AVENUE QUANTICO VIRGINIA 22134 5001 IN REPLY REFER TO: MCBO 5200.3 B 64 MARINE CORPS BASE ORDER 5200.3 From: Commander To: Distribution List Subj:

Application of the HEC-5 Hydropower Routines

US Army Corps of Engineers Hydrologic Engineering Center Application of the HEC-5 Hydropower Routines March 1980 revised: July 1983 Approved for Public Release. Distribution Unlimited. TD-12 REPORT DOCUMENTATION

US Army Corps of Engineers Hydrologic Engineering Center Application of the HEC-5 Hydropower Routines March 1980 revised: July 1983 Approved for Public Release. Distribution Unlimited. TD-12 REPORT DOCUMENTATION

TITLE: Molecular Determinants Fundamental to Axon Regeneration after SCI

AWARD NUMBER: W81XWH-11-1-0645 TITLE: Molecular Determinants Fundamental to Axon Regeneration after SCI PRINCIPAL INVESTIGATOR: Jeffrey Alan Plunkett, Ph.D. CONTRACTING ORGANIZATION: St. Thomas University,

AWARD NUMBER: W81XWH-11-1-0645 TITLE: Molecular Determinants Fundamental to Axon Regeneration after SCI PRINCIPAL INVESTIGATOR: Jeffrey Alan Plunkett, Ph.D. CONTRACTING ORGANIZATION: St. Thomas University,

A udit R eport. Office of the Inspector General Department of Defense. Report No. D October 19, 2001

A udit R eport CONTROLS OVER THE COMPUTERIZED ACCOUNTS PAYABLE SYSTEM AT DEFENSE FINANCE AND ACCOUNTING SERVICE KANSAS CITY Report No. D-2002-008 October 19, 2001 Office of the Inspector General Department

A udit R eport CONTROLS OVER THE COMPUTERIZED ACCOUNTS PAYABLE SYSTEM AT DEFENSE FINANCE AND ACCOUNTING SERVICE KANSAS CITY Report No. D-2002-008 October 19, 2001 Office of the Inspector General Department

ESTABLISHMENT OF A QUALITY SYSTEM

GENERAL CIVIL AVIATION AUTHORITY OF BOTSWANA ADVISORY CIRCULAR CAAB Document GAC-009 ESTABLISHMENT OF A QUALITY SYSTEM GAC-009 Revision: Original 19 Mar 2013 Page 1 of 29 Intentionally left blank GAC-009

GENERAL CIVIL AVIATION AUTHORITY OF BOTSWANA ADVISORY CIRCULAR CAAB Document GAC-009 ESTABLISHMENT OF A QUALITY SYSTEM GAC-009 Revision: Original 19 Mar 2013 Page 1 of 29 Intentionally left blank GAC-009

GOODWILL INDUSTRIES OF COLORADO SPRINGS

GOODWILL INDUSTRIES OF COLORADO SPRINGS CORPORATE COMPLIANCE PROGRAM ADOPTED : By the Board of Directors Date: October 25, 2005 Attachment 2 Memorandum 10-41 TABLE OF CONTENTS Corporate Compliance Program

GOODWILL INDUSTRIES OF COLORADO SPRINGS CORPORATE COMPLIANCE PROGRAM ADOPTED : By the Board of Directors Date: October 25, 2005 Attachment 2 Memorandum 10-41 TABLE OF CONTENTS Corporate Compliance Program

SUBJECT: Microcomputer Hardware and Software Management Program

February 9, 2001 INSPECTOR GENERAL INSTRUCTION 7950.2 SUBJECT: Microcomputer Hardware and Software Management Program References: See Appendix A. A. Purpose. This Instruction updates the Office of the

February 9, 2001 INSPECTOR GENERAL INSTRUCTION 7950.2 SUBJECT: Microcomputer Hardware and Software Management Program References: See Appendix A. A. Purpose. This Instruction updates the Office of the

LeiningerCPA, Ltd. INTERNAL CONTROL PROCEDURE STATEMENT

LeiningerCPA, Ltd. INTERNAL CONTROL PROCEDURE STATEMENT Effective internal control is a foundation for safe and sound operations. Management and the Board of Directors are committed to providing sufficient

LeiningerCPA, Ltd. INTERNAL CONTROL PROCEDURE STATEMENT Effective internal control is a foundation for safe and sound operations. Management and the Board of Directors are committed to providing sufficient

RFID and Hazardous Waste Implementation Highlights

7 5 T H A I R B A S E W I N G RFID and Hazardous Waste Implementation Highlights Environment, Energy and Sustainability Symposium May 2009 Report Documentation Page Form Approved OMB No. 0704-0188 Public

7 5 T H A I R B A S E W I N G RFID and Hazardous Waste Implementation Highlights Environment, Energy and Sustainability Symposium May 2009 Report Documentation Page Form Approved OMB No. 0704-0188 Public

BIOSCRIP, INC. CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS

BIOSCRIP, INC. CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS Statement of Purpose 1. Oversight Responsibility. The purpose of the Audit Committee of the Board of Directors of BioScrip, Inc.,

BIOSCRIP, INC. CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS Statement of Purpose 1. Oversight Responsibility. The purpose of the Audit Committee of the Board of Directors of BioScrip, Inc.,

Alex G. Manganaris Director, Workforce Plans and Resources

U.S. Intelligence Community Workforce Retention Issues in the U.S. Intelligence Community y( (IC) Alex G. Manganaris Director, Workforce Plans and Resources UNCLASSIFIED 1 Report Documentation Page Form

U.S. Intelligence Community Workforce Retention Issues in the U.S. Intelligence Community y( (IC) Alex G. Manganaris Director, Workforce Plans and Resources UNCLASSIFIED 1 Report Documentation Page Form

Performance-Based Acquisitions (PBA) E2S2 Conference April 2011

E2S2 Conference April 2011") NAVFAC Environmental Restoration Program Performance-Based Contracting Policy, Perspective, and Implementation Performance-Based Acquisitions (PBA) E2S2 Conference April 2011 Brian P. Harrison, MPA, P.E.

NAVFAC Environmental Restoration Program Performance-Based Contracting Policy, Perspective, and Implementation Performance-Based Acquisitions (PBA) E2S2 Conference April 2011 Brian P. Harrison, MPA, P.E.

73rd MORSS CD Cover Page UNCLASSIFIED DISCLOSURE FORM CD Presentation

73rd MORSS CD Cover Page UNCLASSIFIED DISCLOSURE FORM CD Presentation 712CD For office use only 41205 21-23 June 2005, at US Military Academy, West Point, NY Please complete this form 712CD as your cover

73rd MORSS CD Cover Page UNCLASSIFIED DISCLOSURE FORM CD Presentation 712CD For office use only 41205 21-23 June 2005, at US Military Academy, West Point, NY Please complete this form 712CD as your cover

STANDARDIZATION DOCUMENTS

STANDARDIZATION DOCUMENTS Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting burden for the collection of information is estimated to average 1 hour per response, including the

STANDARDIZATION DOCUMENTS Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting burden for the collection of information is estimated to average 1 hour per response, including the

SE Tools Overview & Advanced Systems Engineering Lab (ASEL)

") SE Tools Overview & Advanced Systems Engineering Lab (ASEL) Pradeep Mendonza TARDEC Systems Engineering Group pradeep.mendonza@us.army.mil June 2, 2011 Unclassified/FOUO Report Documentation Page Form

SE Tools Overview & Advanced Systems Engineering Lab (ASEL) Pradeep Mendonza TARDEC Systems Engineering Group pradeep.mendonza@us.army.mil June 2, 2011 Unclassified/FOUO Report Documentation Page Form

ADMINISTRATIVE INTERNAL AUDIT Board of Trustees Approval: 03/10/2004 CHAPTER 1 Date of Last Cabinet Review: 04/07/2017 POLICY 3.

INTERNAL AUDIT Board of Trustees Approval: 03/10/2004 POLICY 3.01 Page 1 of 14 I. POLICY The Internal Audit Department assists Salt Lake Community College in accomplishing its objectives by providing an

INTERNAL AUDIT Board of Trustees Approval: 03/10/2004 POLICY 3.01 Page 1 of 14 I. POLICY The Internal Audit Department assists Salt Lake Community College in accomplishing its objectives by providing an

International Standards for the Professional Practice of Internal Auditing (Standards)

") INTERNATIONAL STANDARDS FOR THE PROFESSIONAL PRACTICE OF INTERNAL AUDITING (STANDARDS) Attribute Standards 1000 Purpose, Authority, and Responsibility The purpose, authority, and responsibility of the

INTERNATIONAL STANDARDS FOR THE PROFESSIONAL PRACTICE OF INTERNAL AUDITING (STANDARDS) Attribute Standards 1000 Purpose, Authority, and Responsibility The purpose, authority, and responsibility of the

Diminishing Returns and Policy Options in a Rentier State: Economic Reform and Regime Legitimacy in Saudi Arabia

polhlcal Crossrlads 1997 James Nicholas Publishers Vol. 5 Nos. 1 & 2 pp.31-50 Diminishing Returns and Policy Options in a Rentier State: Economic Reform and Regime Legitimacy in Saudi Arabia Robert E.

polhlcal Crossrlads 1997 James Nicholas Publishers Vol. 5 Nos. 1 & 2 pp.31-50 Diminishing Returns and Policy Options in a Rentier State: Economic Reform and Regime Legitimacy in Saudi Arabia Robert E.

THE NATIONAL SHIPBUILDING RESEARCH PROGRAM

SHIP PRODUCTION COMMITTEE FACILITIES AND ENVIRONMENTAL EFFECTS SURFACE PREPARATION AND COATINGS DESIGN/PRODUCTION INTEGRATION HUMAN RESOURCE INNOVATION MARINE INDUSTRY STANDARDS WELDING INDUSTRIAL ENGINEERING

SHIP PRODUCTION COMMITTEE FACILITIES AND ENVIRONMENTAL EFFECTS SURFACE PREPARATION AND COATINGS DESIGN/PRODUCTION INTEGRATION HUMAN RESOURCE INNOVATION MARINE INDUSTRY STANDARDS WELDING INDUSTRIAL ENGINEERING

TITLE: Identification of Protein Kinases Required for NF2 Signaling

AD Award Number: W81XWH-06-1-0175 TITLE: Identification of Protein Kinases Required for NF2 Signaling PRINCIPAL INVESTIGATOR: Jonathan Chernoff, M.D., Ph.D. CONTRACTING ORGANIZATION: Fox Chase Cancer Center

AD Award Number: W81XWH-06-1-0175 TITLE: Identification of Protein Kinases Required for NF2 Signaling PRINCIPAL INVESTIGATOR: Jonathan Chernoff, M.D., Ph.D. CONTRACTING ORGANIZATION: Fox Chase Cancer Center

DOD Methodology for the Valuation of Excess, Obsolete, and Unserviceable Inventory and Operating Materials and Supplies

Report No. D-2010-048 March 25, 2010 DOD Methodology for the Valuation of Excess, Obsolete, and Unserviceable Inventory and Operating Materials and Supplies Report Documentation Page Form Approved OMB

Report No. D-2010-048 March 25, 2010 DOD Methodology for the Valuation of Excess, Obsolete, and Unserviceable Inventory and Operating Materials and Supplies Report Documentation Page Form Approved OMB

Bio-Response Operational Testing & Evaluation (BOTE) Project

Project") Bio-Response Operational Testing & Evaluation (BOTE) Project November 16, 2011 Chris Russell Program Manager Chemical & Biological Defense Division Science & Technology Directorate Report Documentation

Bio-Response Operational Testing & Evaluation (BOTE) Project November 16, 2011 Chris Russell Program Manager Chemical & Biological Defense Division Science & Technology Directorate Report Documentation

Issues in Using a Process as a Game Changer

Issues in Using a Process as a Game Changer by Dr. Stephen Sherman Data Analysts Observations Based on 10 Years as a Process Engineer- Contractor in the Systems Engineering Process Group of the 554 Electronic

Issues in Using a Process as a Game Changer by Dr. Stephen Sherman Data Analysts Observations Based on 10 Years as a Process Engineer- Contractor in the Systems Engineering Process Group of the 554 Electronic

Ranked Set Sampling: a combination of statistics & expert judgment

Ranked Set Sampling: a combination of statistics & expert judgment 1 Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting burden for the collection of information is estimated to

Ranked Set Sampling: a combination of statistics & expert judgment 1 Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting burden for the collection of information is estimated to

OFFICE OF THE SPECIAL INSPECTOR GENERAL

OFFICE OF THE SPECIAL INSPECTOR GENERAL FOR AFGHANISTAN RECONSTRUCTION INSPECTION OF ABDUL MANAN SECONDARY SCHOOL CONSTRUCTION PROJECT IN KAPISA PROVINCE: INSUFFICIENT PLANNING, SAFETY PROBLEMS, AND POOR

OFFICE OF THE SPECIAL INSPECTOR GENERAL FOR AFGHANISTAN RECONSTRUCTION INSPECTION OF ABDUL MANAN SECONDARY SCHOOL CONSTRUCTION PROJECT IN KAPISA PROVINCE: INSUFFICIENT PLANNING, SAFETY PROBLEMS, AND POOR

DISTRIBUTION A: APPROVED FOR PUBLIC RELEASE; DISTRIBUTION IS UNLIMITED

SPECIAL REPORT OPTICAL SYSTEMS GROUP LEASE VERSUS PURCHASE OF EQUIPMENT WHITE SANDS MISSILE RANGE KWAJALEIN MISSILE RANGE YUMA PROVING GROUND DUGWAY PROVING GROUND ABERDEEN TEST CENTER NATIONAL TRAINING

SPECIAL REPORT OPTICAL SYSTEMS GROUP LEASE VERSUS PURCHASE OF EQUIPMENT WHITE SANDS MISSILE RANGE KWAJALEIN MISSILE RANGE YUMA PROVING GROUND DUGWAY PROVING GROUND ABERDEEN TEST CENTER NATIONAL TRAINING

Kentucky State University Office of Internal Audit

Draft for Discussion Only P&P Manual Section - Policy# I. Function and Responsibilities MISSION Mission Statement Definition of Internal Auditing PURPOSE, AUTHORITY, RESPONSIBILITY Audit Charter STANDARDS

Draft for Discussion Only P&P Manual Section - Policy# I. Function and Responsibilities MISSION Mission Statement Definition of Internal Auditing PURPOSE, AUTHORITY, RESPONSIBILITY Audit Charter STANDARDS

Internal Audit Appendix: IIA Standards

Accountability Modules Internal Audit Appendix: IIA Standards Return to Table of ontents The following section provides additional detailed steps to examine when evaluating an internal audit function.

Accountability Modules Internal Audit Appendix: IIA Standards Return to Table of ontents The following section provides additional detailed steps to examine when evaluating an internal audit function.

A Primer on. Software Licensing. Charlene Gross Software Engineering Institute. Do You Own It or Not? Charlene Gross, April 19-23, 2010

- A Primer on Noncommercial Software Licensing Charlene Gross Software Engineering Institute Carnegie Mellon University Charlene Gross, April 19-23, 2010 Report Documentation Page Form Approved OMB No.

- A Primer on Noncommercial Software Licensing Charlene Gross Software Engineering Institute Carnegie Mellon University Charlene Gross, April 19-23, 2010 Report Documentation Page Form Approved OMB No.

ROCK STRIKE TESTING OF TRANSPARENT ARMOR NLE-01

Distribution A. Approved for public release ROCK STRIKE TESTING OF TRANSPARENT ARMOR NLE-01 David N. Hansen, Ph.D. Ashley Wagner Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting

Distribution A. Approved for public release ROCK STRIKE TESTING OF TRANSPARENT ARMOR NLE-01 David N. Hansen, Ph.D. Ashley Wagner Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting

NOGAPS/NAVGEM Platform Support

DISTRIBUTION STATEMENT A. Approved for public release; distribution is unlimited. NOGAPS/NAVGEM Platform Support Dr. Young-Joon Kim Naval Research Laboratory 7 Grace Hopper Ave, MS2 Monterey, CA 93943

DISTRIBUTION STATEMENT A. Approved for public release; distribution is unlimited. NOGAPS/NAVGEM Platform Support Dr. Young-Joon Kim Naval Research Laboratory 7 Grace Hopper Ave, MS2 Monterey, CA 93943

CORROSION CONTROL Anniston Army Depot

CORROSION CONTROL Anniston Army Depot February 9, 2010 Presented by Chris Coss- ANAD Production Engineer Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting burden for the collection

CORROSION CONTROL Anniston Army Depot February 9, 2010 Presented by Chris Coss- ANAD Production Engineer Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting burden for the collection

DESCRIPTIONS OF HYDROGEN-OXYGEN CHEMICAL KINETICS FOR CHEMICAL PROPULSION

DESCRIPTIONS OF HYDROGEN-OXYGEN CHEMICAL KINETICS FOR CHEMICAL PROPULSION By Forman A. Williams Center for Energy Research Department of Mechanical and Aerospace Engineering University of California, San

DESCRIPTIONS OF HYDROGEN-OXYGEN CHEMICAL KINETICS FOR CHEMICAL PROPULSION By Forman A. Williams Center for Energy Research Department of Mechanical and Aerospace Engineering University of California, San

Report on Inspection of Deloitte LLP (Headquartered in Toronto, Canada) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2014 (Headquartered in Toronto, Canada) Issued by the Public Company Accounting Oversight

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2014 (Headquartered in Toronto, Canada) Issued by the Public Company Accounting Oversight

DoD Solid Waste Diversion

DoD Solid Waste Diversion Environment, Energy Security & Sustainability Symposium & Exhibition Edmund D. Miller Office of Deputy Under Secretary of Defense (Installations & Environment) May 10, 2011 1

DoD Solid Waste Diversion Environment, Energy Security & Sustainability Symposium & Exhibition Edmund D. Miller Office of Deputy Under Secretary of Defense (Installations & Environment) May 10, 2011 1

SIGAR. USAID s Support for the American University of Afghanistan: Audit of Costs Incurred by the American University of Afghanistan M A R C H

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 16-27 Financial Audit USAID s Support for the American University of Afghanistan: Audit of Costs Incurred by the American University

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 16-27 Financial Audit USAID s Support for the American University of Afghanistan: Audit of Costs Incurred by the American University

ADVISORY CIRCULAR AC

GHANA CIVIL AVIATION AUTHORITY ADVISORY CIRCULAR AC-00-002 DEVELOPMENT OF AN ACCEPTABLE QUALITY ASSURANCE SYSTEM SECTION 1 GENERAL 1.1 PURPOSE This Advisory Circular (AC) provides guidance to organizations

GHANA CIVIL AVIATION AUTHORITY ADVISORY CIRCULAR AC-00-002 DEVELOPMENT OF AN ACCEPTABLE QUALITY ASSURANCE SYSTEM SECTION 1 GENERAL 1.1 PURPOSE This Advisory Circular (AC) provides guidance to organizations

Master Document Audit Program. Version 9.6, dated November 2017 B-1 Planning Considerations. Purpose and Scope

Activity Code 13010 B-1 Planning Considerations Accounting and Control of Labor Cost Purpose and Scope The major objectives of this audit are to: Evaluate the adequacy of and the contractor s compliance

Activity Code 13010 B-1 Planning Considerations Accounting and Control of Labor Cost Purpose and Scope The major objectives of this audit are to: Evaluate the adequacy of and the contractor s compliance

Memo. Date: October 2018 INTRODUCTION

Memo To: All Public Accounting Firms From: Kathy Zaplitny, CPA, CA Senior Director, Stakeholder Services & Engagement Re: FOCUS ON PRACTICE INSPECTION REPORTABLE DEFICIENCIES 2017-18 Date: October 2018

Memo To: All Public Accounting Firms From: Kathy Zaplitny, CPA, CA Senior Director, Stakeholder Services & Engagement Re: FOCUS ON PRACTICE INSPECTION REPORTABLE DEFICIENCIES 2017-18 Date: October 2018

Developing an Army Water Security Strategy

Developing an Army Water Security Strategy Presented by Marc Kodack, Army Environmental Policy Institute Juli MacDonald-Wimbush, Marstel-Day, LLC May 2011 Environmental and Energy Security and Sustainability

Developing an Army Water Security Strategy Presented by Marc Kodack, Army Environmental Policy Institute Juli MacDonald-Wimbush, Marstel-Day, LLC May 2011 Environmental and Energy Security and Sustainability

Inferring Patterns in Network Traffic: Time Scales and Variation

Inferring Patterns in Network Traffic: Time Scales and Variation Soumyo Moitra smoitra@sei.cmu.edu INFORMS 2014 San Francisco 2014 Carnegie Mellon University Report Documentation Page Form Approved OMB

Inferring Patterns in Network Traffic: Time Scales and Variation Soumyo Moitra smoitra@sei.cmu.edu INFORMS 2014 San Francisco 2014 Carnegie Mellon University Report Documentation Page Form Approved OMB

Earned Value Management

Earned Value Management 8th Annual International Cost/Schedule Performance Conference 27-31 October 1996 M0435K6001 REPORT DOCUMENTATION PAGE Form Approved OMB No. 0704-0188 Public reporting burder for

Earned Value Management 8th Annual International Cost/Schedule Performance Conference 27-31 October 1996 M0435K6001 REPORT DOCUMENTATION PAGE Form Approved OMB No. 0704-0188 Public reporting burder for

Policy Changes Needed at Defense Contract Management Agency to Ensure Forward Pricing Rates Result in Fair and Reasonable Contract Pricing

Inspector General U.S. Department of Defense Report No. DODIG-2015-006 OCTOBER 9, 2014 Policy Changes Needed at Defense Contract Management Agency to Ensure Forward Pricing Rates Result in Fair and Reasonable

Inspector General U.S. Department of Defense Report No. DODIG-2015-006 OCTOBER 9, 2014 Policy Changes Needed at Defense Contract Management Agency to Ensure Forward Pricing Rates Result in Fair and Reasonable

SEDD Our Vision. Anand Mudambi. Joseph Solsky USACE USEPA 3/31/2011 1

SEDD Our Vision Anand Mudambi USEPA Joseph Solsky USACE 3/31/2011 1 Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting burden for the collection of information is estimated to average

SEDD Our Vision Anand Mudambi USEPA Joseph Solsky USACE 3/31/2011 1 Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting burden for the collection of information is estimated to average

Supply Chain Modeling: Downstream Risk Assessment Methodology (DRAM)

") These Slides are Unclassified and Not Proprietary DMSMS Conference 2013 Supply Chain Modeling: Downstream Risk Assessment Methodology (DRAM) Dr. Sean Barnett December 5, 2013 Institute for Defense Analyses

These Slides are Unclassified and Not Proprietary DMSMS Conference 2013 Supply Chain Modeling: Downstream Risk Assessment Methodology (DRAM) Dr. Sean Barnett December 5, 2013 Institute for Defense Analyses

Addressing Species at Risk Before Listing - MCB Camp Lejeune and Coastal Goldenrod

Addressing Species at Risk Before Listing - MCB Camp Lejeune and Coastal Goldenrod Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting burden for the collection of information is

Addressing Species at Risk Before Listing - MCB Camp Lejeune and Coastal Goldenrod Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting burden for the collection of information is