CA SHEEL BHANUSHALI.

|

|

|

- Berniece Shepherd

- 5 years ago

- Views:

Transcription

1 ARTICLES ORIENTATION PROGRAM THE CHAMBER OF TAX CONSULTANTS 7TH JUNE, 2018

2 THANK YOU ELECTRONIC 9 7WAY BILL 344 bhanushalisheel@yahoo.com bhanushalisheel@gmail.com 2

3 IMPLEMENTATION OF NATIONWIDE E-WAY BILL SYSTEM INTER STATE ALL STATES W.E.F. 1ST APRIL, 2018 INTRA STATE AT DISCRETION OF RESPECTIVE STATES, LATEST BY 1ST JUNE, 2018

4 NEED FOR E-WAYBILL SUPPLIER TRANSPORTER OF GOODS RECIPIENT Section 68 of the CGST Act, 2017 authorise the Government to prescribe that the person in charge of a conveyance carrying any consignment of goods of value exceeding prescribed amount to carry with him such documents and such devices as may be prescribed. Rule 138 of CGST Rules, 2017 mandates to carry e-way bill for transportation of goods of consignment of value more than Rs.50,000/-. 4

5 E-WAY BILL RULES R. 138 Information to be Furnished Generation of E-Way Bill Documents R. 138 A Devices Prior to Commencement of Movement of Goods To be Carried by a person-in-charge of a conveyance Documents R. 138 B Verification Conveyances Inspection R. 138 C Of Goods Verification R. 138 D Facility for Uploading Information Regarding Detention of Vehicles 5

6 R.138 Information to be Furnished Prior to Commencement of Movement of Goods and Generation of E-Way Bill Before Commencement of Such Movement, (1) Every RP who causes Movement of Goods Having (i) in relation to a supply, (ii) for reasons other than supply, - Sent for Job Work - Sent for Testing - Sent on Approval - Intra State Branch Transfer - Sent as Samples / Trial - Warranty Removal Such RP shall himself Consignment Furnish Information r.t. said goods Value electronically, on the common portal > Rs in Part A of FORM GST EWB-01 (iii) due to inward supply from URP A Unique Number will be generated on the said portal Number is Valid for 15 Days for Updation of Part B Of FORM GST EWB 01 Such RP Can Authorise - A Transporter - A Courier Agency - An E-Commerce Operator To Furnish Information 6

7 FAQ - How the consignor is supposed to give authorization to transporter or e-commerce operator and courier agency for generating PART-A of e-way bill? It is their mutual agreement and way out to do the same. If a transporter or courier agency or the e-commerce operator fills PART-A, it will be assumed by the department that they have got authorization from consignor for filling PART-A. WHAT IS CONSIGNMENT 7

8 MEANING Consignment a batch of goods consigned Consign deli er to someone's custody. se d (goods) by a public carrier. put someone or something in (a place) in order to be rid of them 8

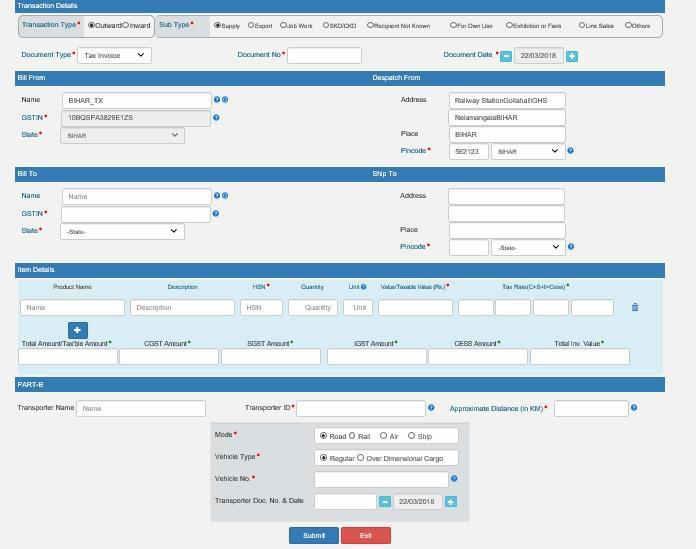

9 FORM GST EWB-01 E-Way Bill No. : E-Way Bill date : Generator : Valid from : Valid until : PART A A.1 GSTIN OF SUPPLIER IF UNREGISTERED MENTION URP PIN CODE - MUST A.2 PLACE OF DISPATCH A.3 GSTIN OF RECIPIENT IF UNREGISTERED MENTION URP A.4 PLACE OF DELIVERY A.5 DOCUMENT NUMBER PIN CODE - MUST A.6 DOCUMENT DATE TAX INVOICE, BILL OF SUPPLY, DELIVERY CHALLAN, BILL OF ENTRY A.7 VALUE OF GOODS AS PER SEC. 15 CGST ACT 2 DIGITS IF T.O. IN Pr.FY 5 CR A.8 HSN CODE 4 DIGITS IF T.O. IN Pr.FY > 5 CR 1. SUPPLY 2. EXPORT OR IMPORT 3. JOB WORK 4. SKD OR CKD 5. RECIPIENT NOT KNOWN A.9 REASON FOR TRANSPORTATION 6. LINE SALES 7. SALES RETURN 8. EXHIBITION OR FAIRS 9. FOR OWN USE 10. OTHERS 9

10 PART B B.1 VEHICLE NUMBER FOR ROAD TRANSPORT DOCUMENT B.2 NUMBER GOODS RECEIPT NO. RAILWAY RECEIPT NO. AIRWAY BILL NO. BILL OF LADING NO. DEFENCE VEHICLE NO. TEMPORARY VEHICLE REGN NO. NEPAL or BHUTAN VEHICLE REGN NO. Goods Transported by Railways, Air, Vessel - Ewaybill to be Generated by RP - Supplier RP - Recipient FAQ - When does the validity of the e-way bill start? It starts when first entry is made in Part-B i.e. vehicle entry is made first time in case of road transportation or first transport document number entry in case of rail/air/ship transportation, whichever is the first entry. It may be noted that validity is not re-calculated for subsequent entries in Part-B. 10

11 11

12 BILL TO SHIP TO TRANSACTION SUPPLIER INVOICE IGST S ORDERS DELIVERS T THIRD PERSON INSTRUCTING PERSON R INVOICE IGST RECIPIENT

SHIP TO ADDRESS R (KOLKATTA) PLACE 700001 PINCODE * 00 AAAAA 0000 A 0 AA / URP MAHARASHTRA VALUE/ TAXABLE VALUE (Rs) * STATE 60 000 DELHI E WAYBILL S BILL TO Rs.")

13 BILL TO SHIP TO TRANSACTION NAME GSTIN * STATE * NAME GSTIN * STATE * BILL FROM T (MAHARASHTRA) DESPATCH FROM ADDRESS S (DELHI) PLACE PINCODE * STATE AAAAA 0000 A 0 AA / URP MAHARASHTRA BILL TO T (MAHARASHTRA) SHIP TO ADDRESS R (KOLKATTA) PLACE PINCODE * 00 AAAAA 0000 A 0 AA / URP MAHARASHTRA VALUE/ TAXABLE VALUE (Rs) * STATE DELHI E WAYBILL S BILL TO Rs SHIP TO T MAHARASHTRA DISCLOSURE OF PRICE R Rs KOLKATTA

14 BILL TO SHIP TO TRANSACTION NAME GSTIN * STATE * NAME GSTIN * STATE * BILL FROM T (MAHARASHTRA) DESPATCH FROM ADDRESS S (DELHI) PLACE PINCODE * STATE AAAAA 0000 A 0 AA / URP MAHARASHTRA BILL TO R (KOLKATTA) SHIP TO ADDRESS R (KOLKATTA) PLACE PINCODE * 00 AAAAA 0000 A 0 AA / URP KOLKATTA VALUE/ TAXABLE VALUE (Rs) * DELHI REGD. PERSON CAUSING THE MOVEMENT S BILL TO Rs E WAYBILL STATE SHIP TO T MAHARASHTRA NO DISCLOSURE OF PRICE R Rs KOLKATTA

15 Where Goods are Sent Irrespective of Consignment Value - by a Principal located in One State - to a Job Worker located in Any Other State The Principal or The Job Worker [if Registered] shall Generate the E-Way Bill Where Handicraft Goods [u/n. 32/2017 CT dt ] are Transported from One State to Another State by a person who has been exempted from obtaining registration u/s 24(i) Person making Inter State Supply, u/s 24(ii) Casual Taxable Person making Taxable Supply The Said Person Irrespective of Consignment Value shall Generate the E-Way Bill 15

16 i) Value of Goods Declared in Invoice Consignment Value of Goods Determined as per Sec. 15 CGST Act Issued i.r.o. Such consignment Bill of Supply Delivery challan ii) Value includes CGST, SGST, UTGST, IGST, CESS Charged if any ii) Value Excludes Value of Exempt Supply of Goods Where Invoice is issued for Exempt & Taxable Supply of Goods Details Case I Case II Case III Invoice Value Add: 18% IGST Total No No Yes Ewaybill Yes/No 16

17 the Consignor, Consignee (2) Where Goods are Transported (i) by RP as a Consignor (ii) by RP as the Recipient of supply as Consignee - in their Own Conveyance - in a Hired Conveyance - by Public Conveyance Having May Generate the E-Way Bill in FORM GST EWB-01 Electronically Consignment on the common portal Value after furnishing information > Rs in Part B of FORM GST EWB-01 Main Menu Select In Own Conveyance - Update In Public Conveyance - As Transporter/Tax Payer Generate OTP OPT to be Filed in Part B If TRANS ID Available To be Filed in Part B If TRANS ID Not Available OTP as Above In Hired Conveyance FAQ - In case of Public transport, how to carry e-way bill? E-way bill shall be generated by the person who is causing the movement of the goods, in case of any verification, he can show e-way bill number to the proper officer. 17

18 (2A) Where the Goods are Transported by Railways, Air, Vessel Where the Goods are Transported by Railways Supplier - RP Recipient - RP Either Before or After The Commencement of Movement By furnishing information in Part B of FORM GST EWB-01 E Waybill to be Generated by Rail Authorities Shall not Deliver The goods Unless the Required E WayBill Is Produced at the Time of Delivery FAQ - In case of transportation of goods via rail/air/ship mode, when is user required to enter transport document details, as it is available only after submitting of goods to the concerned authority? The Part B of the e-way bill can be updated either before or after the commencement of movement. But, where the goods are transported by railways, the railways shall not deliver the goods, unless the e-way bill as required under these rules is produced to them, at the time of delivery. 18

19 The RP shall Furnish the Information (3) The Goods are Handed Over to a Transporter in Part A of FORM GST EWB-01 for Transportation by Road Not Transported (i) by RP as a Consigner (ii) by RP as the Recipient of supply as Consignee Assign a Transporter The RP shall Furnish the Information Relating to Transporter in Part B of FORM GST EWB-01 on the common Portal Where Movement of Goods is Caused by an URP - in their Own Conveyance - in a Hired Conveyance - through a Transporter The Transporter shall Generate EWB in Part B of FORM GST EWB-01 The Transporter shall Generate EWB Based on the information furnished by RP The URP or Transporter at their Option May Generate the E-Way Bill in FORM GST EWB-01 on the common portal 19

20 Where Goods are Transported Within State/UT When the Distance For Further Transportation between the POBs From the POB of the Consignor is 5 Kilometers To the POB of the Transporter the Supplier or the Recipient or the Transporter May Not Furnish the Details of Conveyance in Part B of FORM GST EWB-01 Where Goods are Transported When the Distance The Details of Conveyance Within State/UT between the POBs May Not be Updated From the POB of Transporter Finally To the POB of Consignee is 50 Kilometers in the E-Way Bill Dista ce 5 Kilometers Dista ce 5 Kilometers PART B Optional POB Consignor PART B Updating is Optional POB Transporter Where Goods are Supplied IF Such Recipient RP By Supplier - URP Is Known at the Time of commencement of Movement of Goods To Recipient - RP POB Consignee The Movement is deemed to have been caused by the Recipient RP 20

21 (4) Upon Generation of the E-Way Bill on the common portal a Unique E-Way Bill Number (EBN) (5) Any Transporter Transferring Goods Before Such Transfer and Further Movement of Goods From One Conveyance To Another Conveyance in the course of transit Transhipment shall be made available on the common portal - to the supplier, - to the recipient and - to the transporter Consignor, Consignee, OR Such Transporter the Details of Conveyance in the EWB In Part B Of FORM GST EWB-01 Shall Update 21

22 (6) Where Multiple Consignments The Transporter Prior to The Transporter are Intended to be Transported Movement of Goods in One Conveyance may Generate May Indicate a Consolidated E-Way Bill the Serial Number For Each Such Consignments in FORM GST EWB-02 their E-Way Bill of All the EWB electronically on have been already Generated Generated the common portal The Transporter on the basis of invoice, bill of supply, delivery challan Shall Generate FORM GST EWB-01 (7) Where FORM GST EWB-01 as per (1) is Not Generated by - the Consignor, - the Consignee Plus Consignment Carried in Conveyance is Having Value > Rs The Transporter Prior to Movement of Goods May Also generate a Consolidated e-way bill in FORM GST EWB-02 Rule 7 - Not Applicable to Rail, Air, Vessel C OR INVOICE I Rs. 20,000 C EE VEHICLE C OR 2 INVOICE 2 Rs. 30,000 C EE C OR 3 INVOICE 3 Rs. 45,000 C EE 23

23 FAQ - If the value of the goods carried in a single conveyance is more than 50,000/though value of all or some of the individual consignments is below Rs. 50,000/does transporter need to generate e-way bill for all such smaller consignments? As rule 138(7) will be notified from a future date, hence till the notification for that effect comes, transporter need not generate e-way bill for consignments having value less than Rs 50,000/-, even if the value of the goods carried in single conveyance is more than Rs 50,000/till the said sub-rule is notified. 24

24 When goods to be transported are supplied through an E-Commerce Operator a Courier Agency Such E-Commerce Operator, Courier Agency May furnish Information in Part A of FORM GST EWB-01 (8) The information furnished shall be made available Use it for furnishing in Part A to the Registered Supplier FORM GSTR-1 of FORM GST EWB-01 on the common portal When information is furnished the Unregistered Person is by an Unregistered Supplier shall be informed electronically in FORM GST EWB-01 If the mobile number or the is available. (9) Where an e-way bill has been generated under this rule but goods are either the e-way bill may be cancelled within 24 hours of generation electronically on the common portal - not transported or - are not transported as per the details furnished in the e-way bill either directly or through a Facilitation Centre notified by the Commissioner An e-way bill cannot be cancelled if it has been verified in transit in accordance with these rules 25

25 shall be Valid (10) An e-way bill or A Consolidated e-way bill generated under this rule i) for the Validity Period Counted from Time of Generation Of EWB ii) from the Relevant Date Date of Generation Of EWB iii) for the Distance to be Transported Sr.No. Distance 1. Upto 100 Km 2. For every 100 km or part thereof thereafter Upto 20 Km For every 20 km or part thereof thereafter Validity Period One Day One Additional Day One Day One Additional Day For Other than Over Dimensional Cargo For Over Dimensional Cargo Over Dimensional Cargo - mean a cargo carried as a single indivisible unit Exceeding the dimensional limits prescribed in rule 93 of the Central Motor Vehicle Rules, 1989, made u/motor Vehicles Act, 1988 (59 of 1988) One Day = the Period Expiring at - Midnight of the Day Immediately following the Date of generation of E-Way Bill Tomorrow Night 26

26 the Commissioner may, by notification, Extend the validity period of e-way bill for certain categories of specified goods The Transporter may u/circumstances of an Exceptional Nature Generate Another e-way bill If the goods cannot be transported after updating the details within the validity period of the EWB in Part B of FORM GSTEWB-01 FAQ - What has to be done, if the validity of the e-way bill expires? If validity of the e-way bill expires, the goods are not supposed to be moved. However, under circumstance of e ceptio al ature a d tra s-ship e t, the transporter may extend the validity period after updating reason for the extension and the details in PART-B of FORM GST EWB-01 FAQ - Can I extend the validity of the e-way bill? Yes, one can extend the validity of the e-way bill, if the consignment has not reached the destination within the validity period due to exceptional circumstance like atural calamity, la and order issues, tra s-shipment delay, accide t of conveyance, etc. The transporter needs to explain this reason in details while extending the validity period. 27

27 FAQ - How to extend the validity period of e-way bill? There is an option under e-way bill to extend the validity period. This option is available for extension of e-way bill before 4 hours and after 4 hours of expiry of the validity. Here, transporter will enter the e-way bill number and enter the reason for the requesting the extension, from place (current place), approximate distance to travel and Part-B details. It may be noted that he cannot change the details of Part-A. He will get the extended validity based on the remaining distance to travel. FAQ - Who can extend the validity of the e-way bill? The transporter - can extend the validity period who is carrying the consignment as per the e-way bill system at the time of expiry of validity period 28

28 (11) The details of e-way bill generated under (1) shall be made available on the common portal (12) The Recipient has to Communicate His Acceptance, Rejection At the Earlier of who shall communicate to the Registered His Acceptance of the Consignment Recipient covered by EWB His Rejection within 72 hours If not Communicated of the details available in time on the common portal it shall be deemed or To have been Accepted At the Time of Delivery of Goods (13) The e-way bill generated - u/this rule or - u/rule 138 of the GST Rules of any State shall be Valid in every State & UT 29

29 (14) No E-Way Bill is required to be generated (a) where the goods being transported are specified in Annexure ANNEXURE [(See rule 138(14)] Sr. NO Description of Goods 1. Liquefied petroleum gas for supply to household and non domestic exempted category (NDEC) customers 2. Kerosene oil sold under PDS 3. Postal baggage transported by Department of Posts 4. Natural or cultured pearls and precious or semi-precious stones precious metals and metals clad with precious metal (Chpt 71) 5. Jewellery, golds iths a d sil ers iths (Chpt 71) 6. Currency 7. Used personal and household effects 8. Coral, unworked (0508) and worked coral (9601) ares a d other articles 30

30 (b) where the goods are being transported by a Non-motorised Conveyance (14) No E-Way Bill is required to be generated (c) where the goods are being transported from the - Customs port, - airport, - air cargo complex, - land customs station (d) i.r.o movement of goods within such areas The facility of Generation & Cancellation of EWB may also be made available through SMS To - an ICD - a CFS for clearance by Customs as are notified u/gst Rules of Concerned State (e) Exempted Goods as per schedule in Ntfn. 02/ th June 2017 as amended Except De-Oiled Cake (f) Alcoholic liquor for Human Consumption, Petroleum Crude, HS Diesel, Motor Spirit (Petrol), Natural Gas, Aviation Turbine Fuel (g) Goods Transported - are treated as No Supply under Schedule III of the Act. 31

31 (h) where the goods are being transported (14) No E-Way Bill is required to be generated U/Custo s Bo d from ICD/CFS Fro O e - Customs Station - Customs Port To - a Customs Port - an Airport - Air Cargo Complex - Land Customs Station To Another - Customs Station - Customs Port U/Custo s Super isio U/Custo s Seal (i) where the goods are being transported (j) where the goods are being transported Are Exempt from Tax Are Transit Cargo - From or To Nepal or Bhutan - CSD Canteens to Unit Run Canteens [un. 7/2017 CT (R) dt ] - Heavy Water, Nuclear Fuels by Atomic Energy Dept. to Nuclear Power COI [un. 26/2017 CT (R) dt ] 32

32 (k) any Movement of Goods Caused by Defence Formation (14) No E-Way Bill is required to be generated (l) any Movement of Goods for Transport by Rail As Consignor or As Consignee By Central Government By State Government By Local authority (m) where Empty Cargo Containers are being transported (n) where the goods are being transported Accompanied with A Delivery Challan From POB of Consignor To a Weighbridge From Weighbridge To POB of Consignor Upto Distance of 20KM 33

33 R.138 A Documents and Devices to be carried by a Person-in-Charge of a Conveyance (a) the Invoice, the Bill of Supply, the Deli er Challa (1) The person in charge (b) a Copy of the E-Way Bill or of a conveyance shall carry the E-Way Bill Number - in Electronic Form the E-Way Bill Number - Mapped MANDATORY to a Radio Frequency Identification Device (RFID) Embedded on to the conveyance as Notified Clause (b) Not Applicable to Rail, Air, Vessel (2) A RP may obtain an Invoice Reference Number from the common portal Valid for 30 Days from date of uploading) by Uploading, on the said portal, a Tax Invoice issued by him in FORM GST INV-1 Produce IRN for verification in lieu of the Tax Invoice by the proper officer 34

34 (3) Where RP has Obtained the IRN on the basis of the information furnished in FORM GST INV-1. the information in Part A of FORM GST EWB-01 shall be Auto-Populated by the common portal (4) A Class of Transporter may be required to get Embedded on to the Conveyance A Unique Radio Frequency Identification Device (URFID) Prior to the movement of goods the E-Way Bill will be Mapped to URFID (5) Where Circumstances So Warrant The Person in charge of the Conveyance will have to carry Instead of E-Way Bill u/notification from Commissioner u/notification from Commissioner (a) Tax Invoice, Bill of Supply, Bill of Entry (b) a Delivery Challan, Where the Goods are Transported for Reasons other than by way of supply. 35

35 R.138 B Verification of Documents and Conveyances (1) The Commissioner, or an Empowered officer may authorise a proper officer to Verify to Intercept Any Conveyance - the E-Way Bill in Physical Form - the E-Way Bill Form (Number ) for All Inter- State, Intra-State Movement of goods (2) The Commissioner shall get RFID Readers Installed at Places where Verification of Movement of Goods is to be carried out Where the E-Way Bill has been mapped with the said device Verification of Movement of Vehicles shall be done through such Device Readers A Proper Officer (3) The Physical verification of Conveyances shall be carried out by [in the Normal Course] Any Officer [on receipt of Specific Information on Evasion of Tax] Authorised by by the Commissioner, or an Empowered officer On Approval by by the Commissioner, or an Empowered officer 36

36 R.138C Inspection and Verification of Goods (1) The Proper Officer Shall Record Online A Summary Report within 24 Hours of Inspection of Every Inspection in Part A of Goods In Transit of FORM GST EWB-03 within 3 days of such inspection in Part B of FORM GST EWB-03 A Final Report (2) Where the Physical Verification of Goods being transported on any conveyance has been done during transit at one place within the State or i any other State R.138D Further Physical Verification shall be carried out again in State Only when specific information relating to evasion of tax is made available subsequently Facility for Uploading Information regarding Detention of Vehicle Where a Vehicle has been Intercepted & Detained No Further Physical Verification of the said conveyance shall be carried out again in the State, for a Period >30 Minutes the Transporter may upload the said information in FORM GST EWB-04 on the common portal 37

37 FAILURE TO COMPLY S. 122 (xiv) (CGST ACT) Penalty For Certain Offences Where Taxable Person who transports any taxable goods without cover of documents, He will be Liable to Pay Penalty of: Higher of Rs. A ou t Equivalent to Tax Evaded

38 FAILURE TO COMPLY Detention, seizure and release of goods and Conveyances in S. 129(CGST ACT) transit. where any person transports any goods in contravention of the provisions of this Act or the rules Then Such goods, Vehicle & Documents related to such goods and vehicle Liable for Detention or seizure These will be released after payment of - Tax & Penalty as under upon furnishing a security equivalent to the amount payable In (a) or (b) as prescribed Type of Goods (a) Owner Comes forward For Payment (b) Owner Does Not Come Forward for Payment Taxable Goods Tax + Penalty 100% 50% of Value of Goods Less: Tax paid thereon Exempted Goods Least of 2% of Value of Goods Least of 5% of Value of Goods Rs Rs

39 AUDIT UNDER GST AUDIT BY CA/CMA AUDIT BY DEPARTMENT SPECIAL AUDIT DURING SCRUTINY, INCESTIGATION - IF COMPLEX CASE, HIGH STAKES VAUE DECLARED INCORRECTLY, - IF ITC WRONGLY CLAIMED SPECIAL AUDIT BY CA/CMA ON NOMINATION REGISTERED PERSON TURNOVER IN FY EXCEEDS Rs. 2 CRORE COMMISSIONER AUTHORISES OFFICER OF CGST,SGST,UTGST AUDIT PERIOD A FINANCIAL YEAR AUDIT PERIOD A FINANCIAL YEAR OR MULTIPLES FORM GST ADT 03 DIRECTION TO AUDIT DONE BY COMMISSIONER NOMINATED CA/CMA AUDIT REPORT + RECONCILIATION STATEMENT FORM GST ADT 01 NOTICE ISSUED 15 DAYS PRIOR BY PO CA/CMA TO SUBMIT REPORT 90 DAYS ANNUAL RETURN + ANNUAL AUDITED ACCOUNTS AUDIT TO BE COMLEPETED 3 MONTHS FROM COMMENCEMENT FURTHER EXTENTION 90 DAYS TIME LIMIT EARLIER OF 30 SEPT OF NEXT FY 31 DEC OF NEXT FY [DD OF ANNUAL RETURN] FURTHER EXTENTION 6 MONTHS BY COMMISSIONER FORM GST ADT 02 AUDIT FIDINGS FORM GST ADT 04 AUDIT FIDINGS

40 CGST ACT CHPT VIII - ACCOUNTS & RECORDS Every Registered Person whose Turnover s. 2(6) Aggregate Turnover during a Financial Year Limit Exceeds the Prescribed Limit r. 80(3) Aggregate Turnover Exceeding Rs. 2 Crores s. 35(5) AUDIT ENABLING PROVISION shall get his Accounts Audited 1) FORMAT OF AUDIT REPORT 2) ANNEXURES THERETO - by a Chartered Accountant or - by a Cost Accountant NOT YET PRESCRIBED BY GOVERNMENT and shall Submit a Copy - of the Audited Annual Accounts, - of the Reconciliation Statement u/s. 44(2) r. 80(3) Certified in GSTR 9C For a Financial year Reconciliation between - Value of supplies - declared in the Return furnished - Value of supplies - declared in the Audited Annual Financial Statements - Such other documents in such form & manner as prescribed

41 INDEPENDENT AUDIT EXAMINATION RELIABLE REGISTERED PREPARERS PERSON ASSERTIONS FINANCIAL GST LAW STATEMENTS COMPLIANCE APPREHENSION GST USERS AUTHORITIES S.2(13) AUDIT MEANS OF RECORDS EXAMINATION OF RETURNS OF OTHER DOCUMENTS TO VERIFY CORRECTNESS OF - TURNOVER DECLARED - TAXES PAID - REFUND CLAIMED - ITC AVAILED TO ASSESS COMPLIANCE WITH - GST PROVISIONS - GST RULES MAINTAINED BY RP FURNISHED BY RP - U/GST LAW - U/OTHER LAWS CORRECTNESS FACTUAL AUDIT v/s CERTIFICATE REPORT

42 Aggregate Turnover Supply Made By Taxable Person Will INCLUDE the Aggregate Value of 1) All Taxable Supplies 2) Exempt Supplies ALL INDIA BASIS Supply of G/S Leviable to Tax a) Attracting Nil rate of Tax b) Wholly Exempt from Tax (u/s. 11) c) Non Taxable Supply - Not Leviable to Tax - Alcoholic Liquor for Human Consumption - Petroleum Crude - Motor Spirit (Petrol) - High speed Diesel (HSD) - Natural Gas & Aviation Turbine Fuel (ATF) of Goods Taking goods out of India To a place outside India 3) Exports of Services a) Supplier located in India & Recipient Outside India b) Place of Supply is Outside India c) Supplier receives Payment in Convertible Forex d) Supplier & Receiver are not merely Branches 4) Inter State Supplies of Persons Having Same PAN - Branch Transfers Aggregate Turnover will EXCLUDE the Value of 1) Inward Supplies on which tax payable u/rcm 2) CGST, IGST, SGST, UTT

43 THANK YOU THANK YOU

E-WAY BILL. {Section 68 of CGST Act Read Along With Rule 138 of CGST Rules}

E-WAY BILL {Section 68 of CGST Act Read Along With Rule 138 of CGST Rules} MEANING OF WAYBILL Waybill is a receipt or a document issued by a carrier giving details and instructions relating to the shipment

E-WAY BILL {Section 68 of CGST Act Read Along With Rule 138 of CGST Rules} MEANING OF WAYBILL Waybill is a receipt or a document issued by a carrier giving details and instructions relating to the shipment

E-way Bill. Chapter XXII. FAQ s. Q1. Under what all cases a registered person has to generate e-way bill?

FAQ s Q1. Under what all cases a registered person has to generate e-way bill? Chapter XXII E-way Bill Ans. Every registered person who causes movement of goods of consignment value exceeding ` 50,000/-

FAQ s Q1. Under what all cases a registered person has to generate e-way bill? Chapter XXII E-way Bill Ans. Every registered person who causes movement of goods of consignment value exceeding ` 50,000/-

The. Extraordinary Published by Authority GOVERNMENT OF WEST BENGAL FINANCE DEPARTMENT REVENUE NOTIFICATION. No. 12/2018-State Tax

Registered No. WB/SC-247 PART I] THE KOLKATA GAZETTE, EXTRAORDINARY, MARCH 7, No. 2018 WB(Part-I)/2018/SAR-123 1 The Kolkata Gazette Extraordinary Published by Authority PHALGUNA 16] WEDNESDAY, MARCH 7,

Registered No. WB/SC-247 PART I] THE KOLKATA GAZETTE, EXTRAORDINARY, MARCH 7, No. 2018 WB(Part-I)/2018/SAR-123 1 The Kolkata Gazette Extraordinary Published by Authority PHALGUNA 16] WEDNESDAY, MARCH 7,

E-way bill is an electronic document generated on the GST portal evidencing movement of goods.

GST E-Way Bills What is e-way bill? E-way bill is an electronic document generated on the GST portal evidencing movement of goods. The bill shall be generated from the GSTN portal and every registered

GST E-Way Bills What is e-way bill? E-way bill is an electronic document generated on the GST portal evidencing movement of goods. The bill shall be generated from the GSTN portal and every registered

Presentation on E Way Bill

Presentation on E Way Bill 1 Background In the 24 th Meeting of GST Council held through video conference under the chairmanship of the Union Minister of Finance and Corporate Affairs, Shri Arun Jaitley,

Presentation on E Way Bill 1 Background In the 24 th Meeting of GST Council held through video conference under the chairmanship of the Union Minister of Finance and Corporate Affairs, Shri Arun Jaitley,

Frequently Asked Questions (FAQs) on Electronic Way Bill (E-Way Bill)

on Electronic Way Bill (E-Way Bill)") Frequently Asked Questions (FAQs) on Electronic Way Bill (E-Way Bill) 1 Preface The Government of India, for an inclusive growth of the Nation, has enacted and implemented various reforms confirming economic

Frequently Asked Questions (FAQs) on Electronic Way Bill (E-Way Bill) 1 Preface The Government of India, for an inclusive growth of the Nation, has enacted and implemented various reforms confirming economic

[To be published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i)] Government of India. Ministry of Finance

![[To be published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i)] Government of India. Ministry of Finance](/thumbs/80/80474415.jpg "[To be published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i)] Government of India. Ministry of Finance") [To be published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i)] Government of India Ministry of Finance Department of Revenue [Central Board of Excise and Customs] Notification

[To be published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i)] Government of India Ministry of Finance Department of Revenue [Central Board of Excise and Customs] Notification

Revised E- Way Bill. It means, the consignor or consignee, as a registered person or a transporter of the goods can generate the e-way bill

Revised E- Way Bill IMPORTANT POINTS CA Chandrasekhar Kutty 1. Who can generate E- Way bill? Every registered person who causes movement of goods of consignment value exceeding Rs. 50,000/- In relation

Revised E- Way Bill IMPORTANT POINTS CA Chandrasekhar Kutty 1. Who can generate E- Way bill? Every registered person who causes movement of goods of consignment value exceeding Rs. 50,000/- In relation

Nationwide roll-out of e- way bill system for inter-state movement of goods 1 st February 2018

Nationwide roll out of e- way bill system on a trial basis 16 th January 2018 Nationwide roll-out of e- way bill system for inter-state movement of goods 1 st February 2018 State-wise roll-out of e- way

Nationwide roll out of e- way bill system on a trial basis 16 th January 2018 Nationwide roll-out of e- way bill system for inter-state movement of goods 1 st February 2018 State-wise roll-out of e- way

E-WAY BILL Prepared by : CA Mahendra Kotadiya CA Jagdish Vaishnav

E-WAY BILL Prepared by : CA Mahendra Kotadiya CA Jagdish Vaishnav Why Centralise E-Way Bill required? Unique Selling Proposition (USP) of Goods and Services Tax is Nation- One Tax One Market. One Introducing

E-WAY BILL Prepared by : CA Mahendra Kotadiya CA Jagdish Vaishnav Why Centralise E-Way Bill required? Unique Selling Proposition (USP) of Goods and Services Tax is Nation- One Tax One Market. One Introducing

E-Way Bill under GST. CA Yashwant J. Kasar B.Com, FCA, DISA, CISA, PMP, FAIA

E-Way Bill under GST CA Yashwant J. Kasar B.Com, FCA, DISA, CISA, PMP, FAIA The Central Government made 6th amendment in Central Goods and Services Tax Rules, 2017 (CGST Rules, 2017) to incorporate the

E-Way Bill under GST CA Yashwant J. Kasar B.Com, FCA, DISA, CISA, PMP, FAIA The Central Government made 6th amendment in Central Goods and Services Tax Rules, 2017 (CGST Rules, 2017) to incorporate the

«±ÉõÀ gádå ÀwæPÉ. FINANCE SECRETARIAT NOTIFICATION (4-N/2017) No. FD 47 CSL 2017, Bengaluru, Dated:

No. FD 47 CSL 2017, Bengaluru, Dated:") RNI No. KARBIL/2001/47147 PÀ ÁðlPÀ gádå ÀvÀæ sáuà IVA Part IVA C üpàèvàªáv ÀæPÀn À ÁzÀÄzÀÄ «±ÉõÀ gádå ÀwæPÉ ÉAUÀ¼ÀÆgÀÄ, UÀÄgÀĪÁgÀ, ªÀiÁZïð 15, 2018 ( sá ÄÎt 24, ±ÀPÀ ªÀµÀð 1939) Bengaluru, Thursday,

RNI No. KARBIL/2001/47147 PÀ ÁðlPÀ gádå ÀvÀæ sáuà IVA Part IVA C üpàèvàªáv ÀæPÀn À ÁzÀÄzÀÄ «±ÉõÀ gádå ÀwæPÉ ÉAUÀ¼ÀÆgÀÄ, UÀÄgÀĪÁgÀ, ªÀiÁZïð 15, 2018 ( sá ÄÎt 24, ±ÀPÀ ªÀµÀð 1939) Bengaluru, Thursday,

ALL YOU WANT TO KNOW ABOUT E-WAY BILL

ALL YOU WANT TO KNOW ABOUT E-WAY BILL Below article explains the concept of E-way bill, which is going to be introduced soon. To understand the different practical situations which may arise during the

ALL YOU WANT TO KNOW ABOUT E-WAY BILL Below article explains the concept of E-way bill, which is going to be introduced soon. To understand the different practical situations which may arise during the

Schedule of E-Way SNo Particulars Scheduled 1 Voluntary E Way Bills opted by Traders/ Transporters 2 Mandatory E Way Bills for Inter

Schedule of E-Way SNo Particulars Scheduled 1 Voluntary E Way Bills opted by Traders/ Transporters 2 Mandatory E Way Bills for Inter State Movement 3 E Way Bill introduction by States (Discretionary) 4

Schedule of E-Way SNo Particulars Scheduled 1 Voluntary E Way Bills opted by Traders/ Transporters 2 Mandatory E Way Bills for Inter State Movement 3 E Way Bill introduction by States (Discretionary) 4

E- WAY BILL S.No Question Answer

E- WAY BILL I. Basics on E-Way Bill (FAQ type) S.No Question Answer 1 What is an E-Way Bill (EWB) A document to be carried by the person in charge of conveyance, generated electronically from the common

E- WAY BILL I. Basics on E-Way Bill (FAQ type) S.No Question Answer 1 What is an E-Way Bill (EWB) A document to be carried by the person in charge of conveyance, generated electronically from the common

1. Meaning of E-way bill-

From Karvy Data Management Services Ltd. Date September 13, 2017 Subject E-Way Bill Notification Category Notification No 27 /2017 - Central Tax dated 30 th August, 2017 The Government vide Central Tax

From Karvy Data Management Services Ltd. Date September 13, 2017 Subject E-Way Bill Notification Category Notification No 27 /2017 - Central Tax dated 30 th August, 2017 The Government vide Central Tax

Schedule of E-Way SNo Particulars Scheduled 1 Voluntary E Way Bills opted by Traders/ Transporters 2 Mandatory E Way Bills for Inter

Schedule of E-Way SNo Particulars Scheduled 1 Voluntary E Way Bills opted by Traders/ Transporters 2 Mandatory E Way Bills for Inter State Movement 3 E Way Bill introduction by States (Discretionary) 4

Schedule of E-Way SNo Particulars Scheduled 1 Voluntary E Way Bills opted by Traders/ Transporters 2 Mandatory E Way Bills for Inter State Movement 3 E Way Bill introduction by States (Discretionary) 4

PRESENTED BY: K.VIJAYA KUMAR ASST.COMMISSIONER, BELGAUM

PRESENTED BY: K.VIJAYA KUMAR ASST.COMMISSIONER, BELGAUM Foreword Under GST law, every registered person who causes movement of goods of consignment value exceeding rupees fifty thousand, before commencement

PRESENTED BY: K.VIJAYA KUMAR ASST.COMMISSIONER, BELGAUM Foreword Under GST law, every registered person who causes movement of goods of consignment value exceeding rupees fifty thousand, before commencement

E-WAY BILL UNDER GST AN OVERVIEW, PROCEDURE & ANALYSIS

E-WAY BILL UNDER GST AN OVERVIEW, PROCEDURE & ANALYSIS CMA Susanta Kumar Saha GST Consultant Nation-wide E-Way Bill system under GST was set to be implemented with effect from 1st February 2018. Implementation

E-WAY BILL UNDER GST AN OVERVIEW, PROCEDURE & ANALYSIS CMA Susanta Kumar Saha GST Consultant Nation-wide E-Way Bill system under GST was set to be implemented with effect from 1st February 2018. Implementation

Schedule of E-Way SNo Particulars Scheduled 1 Voluntary E Way Bills opted by Traders/ Transporters 2 Mandatory E Way Bills for Inter

Schedule of E-Way SNo Particulars Scheduled 1 Voluntary E Way Bills opted by Traders/ Transporters 2 Mandatory E Way Bills for Inter State Movement 3 E Way Bill introduction by States (Discretionary) 4

Schedule of E-Way SNo Particulars Scheduled 1 Voluntary E Way Bills opted by Traders/ Transporters 2 Mandatory E Way Bills for Inter State Movement 3 E Way Bill introduction by States (Discretionary) 4

Schedule of E-Way S. No Particulars Scheduled 1 E Way Bills for Inter State Movement 2 E Way Bill for Intra State Movement

Schedule of E-Way S. No Particulars Scheduled 1 E Way Bills for Inter State Movement 2 E Way Bill for Intra State Movement Note 1 st Feb, 2018 1 st April, 2018 15 th April, 2018 Onwards (note) Staggered

Schedule of E-Way S. No Particulars Scheduled 1 E Way Bills for Inter State Movement 2 E Way Bill for Intra State Movement Note 1 st Feb, 2018 1 st April, 2018 15 th April, 2018 Onwards (note) Staggered

Content: 1. Analysis of E WAY BILL Provisions & Procedures Bill to-ship to, Bill from-ship from Model under E Way Bill Import - Expor

Edition 2 nd - BY Analysis FAQ Rules Forms Issues All Right Reserved 1 Content: 1. Analysis of E WAY BILL Provisions & Procedures... 4 1. Bill to-ship to, Bill from-ship from Model under E Way Bill...

Edition 2 nd - BY Analysis FAQ Rules Forms Issues All Right Reserved 1 Content: 1. Analysis of E WAY BILL Provisions & Procedures... 4 1. Bill to-ship to, Bill from-ship from Model under E Way Bill...

GST FCBM

The Central Government vide Notification no.74/2017 dated 29th December, 2017 has notified 1st day of February, 2018, as the date from which the provisions of E- Way bill system as notified in Notification

The Central Government vide Notification no.74/2017 dated 29th December, 2017 has notified 1st day of February, 2018, as the date from which the provisions of E- Way bill system as notified in Notification

GST FCBM

The Central Government vide Notification no.74/2017 dated 29th December, 2017 has notified 1st day of February, 2018, as the date from which the provisions of E- Way bill system as notified in Notification

The Central Government vide Notification no.74/2017 dated 29th December, 2017 has notified 1st day of February, 2018, as the date from which the provisions of E- Way bill system as notified in Notification

Dear Sir/Madam, Q. What is an e-way bill?

Dear Sir/Madam, This if for you kind info, if any query you has regarding E-Way Bill, may go through below FAQ. And further you may call 0120-4888999 if there is any doubt and not clarified by below FAQ.

Dear Sir/Madam, This if for you kind info, if any query you has regarding E-Way Bill, may go through below FAQ. And further you may call 0120-4888999 if there is any doubt and not clarified by below FAQ.

Electronic Way Bill. Information to be furnished prior to commencement of movement of goods and generation of e-way bill

DISCLAIMER: Electronic Way Bill The views expressed in this article are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed by the author(s).

DISCLAIMER: Electronic Way Bill The views expressed in this article are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed by the author(s).

E-WAY BILL SYSTEM ONE NATION ONE TAX ONE MARKET NOW, ONE E-WAY

E-WAY BILL SYSTEM ONE NATION ONE TAX ONE MARKET NOW, ONE E-WAY BILL e-waybill System - A paradigm Shift From Departmental Policing Model - a post movement capture model (Move and make him to account) Towards

E-WAY BILL SYSTEM ONE NATION ONE TAX ONE MARKET NOW, ONE E-WAY BILL e-waybill System - A paradigm Shift From Departmental Policing Model - a post movement capture model (Move and make him to account) Towards

E-WAY BILL UNDER GST ACT

E-WAY BILL UNDER GST ACT SURESH AGGARWAL ADVOCATE MOBILE NO. 9810032846 EMAIL ID: SURESHAGG@GMAIL.COM WEBSITE: WWW.SURESHTAXATION.COM E-WAY BILL RULES 2017 Till such time as an E-Way bill system is developed

E-WAY BILL UNDER GST ACT SURESH AGGARWAL ADVOCATE MOBILE NO. 9810032846 EMAIL ID: SURESHAGG@GMAIL.COM WEBSITE: WWW.SURESHTAXATION.COM E-WAY BILL RULES 2017 Till such time as an E-Way bill system is developed

Frequently Asked Questions (FAQs) on e-way bill

on e-way bill") Frequently Asked Questions (FAQs) on e-way bill 1. What is an e-way bill? e-way bill is a document required to be carried by a person in charge of the conveyance carrying any consignment of goods of value

Frequently Asked Questions (FAQs) on e-way bill 1. What is an e-way bill? e-way bill is a document required to be carried by a person in charge of the conveyance carrying any consignment of goods of value

Rule# Rule Title Form# Provision Bizsol Analysis

GST Invoice Rules: Rule# Rule Title Form# Provision Bizsol Analysis 1 Tax Invoice - 1. Subject to rule 7, a tax invoice referred to in section 31 shall be issued by the registered person containing the

GST Invoice Rules: Rule# Rule Title Form# Provision Bizsol Analysis 1 Tax Invoice - 1. Subject to rule 7, a tax invoice referred to in section 31 shall be issued by the registered person containing the

1. Outward and inward supply of goods. {e.g. Sale and purchase of goods}.

GST Circular 05/2018 To All Addl. SEs/Sr. Xens/REs/AOs/SrAOs(DDOs) Under PSPCL (Through Website Only) Memo No: 5030/5204 Dated: 28/05/2018 Sub: Implementation of E-Way Bill Rules for Intra-state movement

GST Circular 05/2018 To All Addl. SEs/Sr. Xens/REs/AOs/SrAOs(DDOs) Under PSPCL (Through Website Only) Memo No: 5030/5204 Dated: 28/05/2018 Sub: Implementation of E-Way Bill Rules for Intra-state movement

1.1 Clarity on interpretation of consignment in order to determine the value of INR 50,000

Annexure 1 Recommendations on E-waybills 1. IMMEDIATE CLARIFICATIONS 1.1 Clarity on interpretation of consignment in order to determine the value of INR 50,000 As per Rule 138(1) of the CGST Rules, an

Annexure 1 Recommendations on E-waybills 1. IMMEDIATE CLARIFICATIONS 1.1 Clarity on interpretation of consignment in order to determine the value of INR 50,000 As per Rule 138(1) of the CGST Rules, an

The Telangana Goods and Services Tax Rules, 2017 Amendment to certain Rules Notification-Orders - Issued.

GOVERNMENT OF TELANGANA ABSTRACT The Telangana Goods and Services Tax Rules, 2017 Amendment to certain Rules Notification-Orders - Issued. REVENUE (COMMERCIAL TAXES-II) DEPARTMENT G.O.Ms.No. 39 Dated:

GOVERNMENT OF TELANGANA ABSTRACT The Telangana Goods and Services Tax Rules, 2017 Amendment to certain Rules Notification-Orders - Issued. REVENUE (COMMERCIAL TAXES-II) DEPARTMENT G.O.Ms.No. 39 Dated:

E-way bill - basic provisions

from India Tax & Regulatory Services E-way bill - basic provisions January 31, 2018 In detail The provisions pertaining to the E-way bill for inter-state movement of goods will be effective from 01 February,

from India Tax & Regulatory Services E-way bill - basic provisions January 31, 2018 In detail The provisions pertaining to the E-way bill for inter-state movement of goods will be effective from 01 February,

EWAY BILL FAQ 1. What is an e-way bill? 2. Why is the e-way bill required? 3. Who all can generate the e-way bill?

EWAY BILL FAQ 1. What is an e-way bill? E-way bill is a document required to be carried by a person in charge of the conveyance carrying any consignment of goods of value exceeding fifty thousand rupees

EWAY BILL FAQ 1. What is an e-way bill? E-way bill is a document required to be carried by a person in charge of the conveyance carrying any consignment of goods of value exceeding fifty thousand rupees

Frequently Asked Questions (FAQ)

") Frequently Asked Questions (FAQ) 1. What is an E-Way Bill? a. E-Way Bill is an electronic way bill for movement of goods which can be generated on the e-way Bill Portal. Transport of goods of more than

Frequently Asked Questions (FAQ) 1. What is an E-Way Bill? a. E-Way Bill is an electronic way bill for movement of goods which can be generated on the e-way Bill Portal. Transport of goods of more than

Relevant Provisions Issues Recommendations

Rule 1(1) of the Electronic Way Bill Rules 1. Information to be furnished prior to commencement of movement of goods and generation of e-way bill (1) Every registered person who causes movement of goods

Rule 1(1) of the Electronic Way Bill Rules 1. Information to be furnished prior to commencement of movement of goods and generation of e-way bill (1) Every registered person who causes movement of goods

GST IN INDIA INVOICE & PAYMENTS

GST IN INDIA INVOICE & PAYMENTS 1 INVOICE The most important aspect in GST is tax invoice. No statutory format prescribed. Tax payers are free to design their own invoice format. Certain mandatory details

GST IN INDIA INVOICE & PAYMENTS 1 INVOICE The most important aspect in GST is tax invoice. No statutory format prescribed. Tax payers are free to design their own invoice format. Certain mandatory details

E-Way Bill under GST

E-Way Bill under GST (Updated with changes as per Notification No. 3/2018 Central Tax dated 23 rd January, 2018) CA Yashwant J. Kasar B.Com, FCA, DISA, CISA, PMP, FAIA Section 68 of CGST Act, 2017 Inspection

E-Way Bill under GST (Updated with changes as per Notification No. 3/2018 Central Tax dated 23 rd January, 2018) CA Yashwant J. Kasar B.Com, FCA, DISA, CISA, PMP, FAIA Section 68 of CGST Act, 2017 Inspection

E-Way Bill and Process

E-Way Bill and Process Deepak Mata, Assistant Director, National Academy of Customs, Indirect Taxes and Narcotics (NACIN), Mumbai E way Bill- Posers What is it? Why? Benefits? When is to be generated?

E-Way Bill and Process Deepak Mata, Assistant Director, National Academy of Customs, Indirect Taxes and Narcotics (NACIN), Mumbai E way Bill- Posers What is it? Why? Benefits? When is to be generated?

Frequently Asked Questions (FAQs) on e-way bill

on e-way bill") Frequently Asked Questions (FAQs) on e-way bill 1. What is an e-way bill? e-way bill is a document required to be carried by a person in charge of the conveyance carrying any consignment of goods of value

Frequently Asked Questions (FAQs) on e-way bill 1. What is an e-way bill? e-way bill is a document required to be carried by a person in charge of the conveyance carrying any consignment of goods of value

The common portal for generation of e-way bill is

1. FAQs- General Portal What is the common portal for generation of e-way bill? The common portal for generation of e-way bill is https://ewaybillgst.gov.in I am not getting OTP on my mobile, what should

1. FAQs- General Portal What is the common portal for generation of e-way bill? The common portal for generation of e-way bill is https://ewaybillgst.gov.in I am not getting OTP on my mobile, what should

Tax Invoice, Credit & Debit Notes

Tax Invoice, Credit & Debit Notes C HAPTER V II OF THE CGST A C T -By Prakhar Jain SECTION 31 TAX INVOICE GSTINATION.COM Normal Invoice: RTP supplying taxable goods shall issue a Tax Invoice If Supply

Tax Invoice, Credit & Debit Notes C HAPTER V II OF THE CGST A C T -By Prakhar Jain SECTION 31 TAX INVOICE GSTINATION.COM Normal Invoice: RTP supplying taxable goods shall issue a Tax Invoice If Supply

E-Way Bill System User Manual

2017 E-Way Bill System User Manual National Informatics Centre New Delhi No part of this document shall be reproduced without prior permission of National Informatics Centre, New Delhi. User Manual Release

2017 E-Way Bill System User Manual National Informatics Centre New Delhi No part of this document shall be reproduced without prior permission of National Informatics Centre, New Delhi. User Manual Release

E-Way Bills under GST

Legislative History Notification 10/2017 Central Tax dated 28-06-2017. Notification 27/2017 Central Tax dated 30-08-2017. Notification no. FD CSL 2017, Bengaluru dated 06-09-2017. Notification 34/2017

Legislative History Notification 10/2017 Central Tax dated 28-06-2017. Notification 27/2017 Central Tax dated 30-08-2017. Notification no. FD CSL 2017, Bengaluru dated 06-09-2017. Notification 34/2017

Chapter- TAX INVOICE, CREDIT AND DEBIT NOTES

Chapter- TAX INVOICE, CREDIT AND DEBIT NOTES 1. Tax invoice Subject to rule 7, a tax invoice referred to in section 31 shall be issued by the registered person containing the following particulars:- a

Chapter- TAX INVOICE, CREDIT AND DEBIT NOTES 1. Tax invoice Subject to rule 7, a tax invoice referred to in section 31 shall be issued by the registered person containing the following particulars:- a

GEARED UP FOR BILLING UNDER GST

GEARED UP FOR BILLING UNDER GST CA. Nayan Jain (Associate member of Team GST Cornor) Invoicing is a crucial aspect of tax compliance for every business. Input tax credit can be availed on the basis of

GEARED UP FOR BILLING UNDER GST CA. Nayan Jain (Associate member of Team GST Cornor) Invoicing is a crucial aspect of tax compliance for every business. Input tax credit can be availed on the basis of

Particulars of E way bill. Who When Part Form In case of MPPKVVCL. Before movement of goods. Fill Part A. Fill Part B. Before movement of goods

Annexure - I Brief description about E way bill E-way bill is an electronic document to be generated from on the GST portal evidencing movement of goods. It has two Components-Part A comprising of details

Annexure - I Brief description about E way bill E-way bill is an electronic document to be generated from on the GST portal evidencing movement of goods. It has two Components-Part A comprising of details

E-publication on E-way Bill under GST

E-publication on E-way Bill under GST The Institute of Chartered Accountants of India (Set up by an Act of Parliament) New Delhi The Institute of Chartered Accountants of India All rights reserved. No

E-publication on E-way Bill under GST The Institute of Chartered Accountants of India (Set up by an Act of Parliament) New Delhi The Institute of Chartered Accountants of India All rights reserved. No

Tax Invoice (Format 1)

") Tax Invoice (Format 1) 1. 2. 3. 4. Serial No. of Invoice 5. Date of Invoice Details of Recipient (Buyer) Place of supply (Inter-) Details of Consignee Date: No. Description of Goods / Services HS N / SAC

Tax Invoice (Format 1) 1. 2. 3. 4. Serial No. of Invoice 5. Date of Invoice Details of Recipient (Buyer) Place of supply (Inter-) Details of Consignee Date: No. Description of Goods / Services HS N / SAC

Standard operating procedure on e-way bill implementation

Optitax s R Standard operating procedure on e-way bill implementation 30 January 2018 1 Abbreviations Abbreviations Full form API Application Program Interface CGST Central Goods and Service Tax CKD Completely

Optitax s R Standard operating procedure on e-way bill implementation 30 January 2018 1 Abbreviations Abbreviations Full form API Application Program Interface CGST Central Goods and Service Tax CKD Completely

Please check whether your system has proper version of the browser as suggested by the e-way bill portal and the security settings of the browser.

1 1. FAQs - General Portal What is the common portal for generation of e-way bill? The common portal for generation of e-way bill is http://ewaybillgst.nic.in I am not getting the OTP to my mobile, what

1 1. FAQs - General Portal What is the common portal for generation of e-way bill? The common portal for generation of e-way bill is http://ewaybillgst.nic.in I am not getting the OTP to my mobile, what

1. GSTIN/Temporary ID: 2. Legal Name: 3. Trade Name, if any: 4. Address: 5. Tax Period: From <DD/MM/YY> To <DD/MM/YY>

FORM-GST-RFD-01 [See rule------] Application for Refund Select: Registered / Casual/ Unregistered/Non-resident taxable person 1. GSTIN/Temporary ID: 2. Legal Name: 3. Trade Name, if any: 4. Address: 5.

FORM-GST-RFD-01 [See rule------] Application for Refund Select: Registered / Casual/ Unregistered/Non-resident taxable person 1. GSTIN/Temporary ID: 2. Legal Name: 3. Trade Name, if any: 4. Address: 5.

1. GSTIN/Temporary ID: 2. Legal Name: 3. Trade Name, if any: 4. Address: 5. Tax Period: From <DD/MM/YY> To <DD/MM/YY>

FORM-GST-RFD-01 [See rule------] Application for Refund Select: Registered / Casual/ Unregistered/Non-resident taxable person 1. GSTIN/Temporary ID: 2. Legal Name: 3. Trade Name, if any: 4. Address: 5.

FORM-GST-RFD-01 [See rule------] Application for Refund Select: Registered / Casual/ Unregistered/Non-resident taxable person 1. GSTIN/Temporary ID: 2. Legal Name: 3. Trade Name, if any: 4. Address: 5.

Invoice under GST. Abhay M Sharma & Co. 302/1 Ujjaval Complex, Nr. Akota Stadium, Akota, Vadodara

Invoice under GST Abhay M Sharma & Co. 302/1 Ujjaval Complex, Nr. Akota Stadium, Akota, Vadodara For More information contact 0265-2352829, 7600881610 The views contained in the above presentation does

Invoice under GST Abhay M Sharma & Co. 302/1 Ujjaval Complex, Nr. Akota Stadium, Akota, Vadodara For More information contact 0265-2352829, 7600881610 The views contained in the above presentation does

Form GSTR-1. Details of outward supplies of goods or services

Form GSTR-1 [See rule (59(1)] Details of outward supplies of goods or services Year Month 1. GSTIN 2. (a) Legal name of the registered person 3. (b) Trade name, if any (a) Aggregate Turnover in the preceding

Form GSTR-1 [See rule (59(1)] Details of outward supplies of goods or services Year Month 1. GSTIN 2. (a) Legal name of the registered person 3. (b) Trade name, if any (a) Aggregate Turnover in the preceding

GST Training Programme Hosted by WIRC of ICAI. CA Pathik Shah

GST Training Programme Hosted by WIRC of ICAI CA Pathik Shah Topics to be covered S.No. Topics Covered in 1 Time of Supply Sec 12 & 13 2 Tax Invoice Sec 31 & 34 & Rules 3 E-way bill Rules 4 Value of Taxable

GST Training Programme Hosted by WIRC of ICAI CA Pathik Shah Topics to be covered S.No. Topics Covered in 1 Time of Supply Sec 12 & 13 2 Tax Invoice Sec 31 & 34 & Rules 3 E-way bill Rules 4 Value of Taxable

E-Way bill. Microsoft Dynamics AX This document will help you learn how to extend tax configurations to meet the E-Way bill requirement.

Microsoft Dynamics AX 2012 E-Way bill This document will help you learn how to extend tax configurations to meet the E-Way bill requirement. Demo script Prabhat Bhargava June 2018 Send feedback. www.microsoft.com/dynamics/ax

Microsoft Dynamics AX 2012 E-Way bill This document will help you learn how to extend tax configurations to meet the E-Way bill requirement. Demo script Prabhat Bhargava June 2018 Send feedback. www.microsoft.com/dynamics/ax

E-Way Bill under GST

E-Way Bill under GST Introduction of Goods and Services Tax (GST) across India with effect from 1st of July 2017 is a very significant step in the field of indirect tax reforms in India. For quick and

E-Way Bill under GST Introduction of Goods and Services Tax (GST) across India with effect from 1st of July 2017 is a very significant step in the field of indirect tax reforms in India. For quick and

ॐ सह न ववत सह न भ नक त सह व र य करव वह त जस व न वध तमस त म ववव ष वह ॐ श स वत श स वत श स वत

ॐ सह न ववत सह न भ नक त सह व र य करव वह त जस व न वध तमस त म ववव ष वह ॐ श स वत श स वत श स वत Om, May God Protect us Both (the Teacher and the Members), May God Nourish us Both, May we Work Together with

ॐ सह न ववत सह न भ नक त सह व र य करव वह त जस व न वध तमस त म ववव ष वह ॐ श स वत श स वत श स वत Om, May God Protect us Both (the Teacher and the Members), May God Nourish us Both, May we Work Together with

Goods & Service Tax: Clarification required on various issues under Business Processes on GST. Date:

Goods & Service Tax: Clarification required on various issues under Business Processes on GST Date: 31-10-2015 Multiple Line item-wise HS Code updation is mandatory for Sales Register & Purchase Register

Goods & Service Tax: Clarification required on various issues under Business Processes on GST Date: 31-10-2015 Multiple Line item-wise HS Code updation is mandatory for Sales Register & Purchase Register

GOODS & SERVICES TAX / IDT UPDATE 41

GOODS & SERVICES TAX / IDT UPDATE 41 Clarifications regarding GST in respect of certain services The Central Government vide Circular No.34/08/2018-GST dated 1 st March, 2018 has clarified certain issues

GOODS & SERVICES TAX / IDT UPDATE 41 Clarifications regarding GST in respect of certain services The Central Government vide Circular No.34/08/2018-GST dated 1 st March, 2018 has clarified certain issues

E Way Bill http://ewaybill.nic.in 1 Agenda Registration e-way Bill Generation Modification Cancellation Rejection Acceptance Utilities SMS API Json 2 Who can Register and use e-way bill Portal Who can

E Way Bill http://ewaybill.nic.in 1 Agenda Registration e-way Bill Generation Modification Cancellation Rejection Acceptance Utilities SMS API Json 2 Who can Register and use e-way bill Portal Who can

GST FCBM

Capital goods and its Credit under GST : GST is a tax on the supply of goods or services or both. The registered person who is engaged in taxable supply or export of goods or services or both can avail

Capital goods and its Credit under GST : GST is a tax on the supply of goods or services or both. The registered person who is engaged in taxable supply or export of goods or services or both can avail

E-publication On E-way Bill under GST

E-publication On E-way Bill under GST The Institute of Chartered Accountants of India (Set up by an Act of Parliament) New Delhi The Institute of Chartered Accountants of India All rights reserved. No

E-publication On E-way Bill under GST The Institute of Chartered Accountants of India (Set up by an Act of Parliament) New Delhi The Institute of Chartered Accountants of India All rights reserved. No

E-Waybill. Comprehensive Guide on. (Updated up to 2 nd April, 2018)

") Comprehensive Guide on E-Waybill (Updated up to 2 nd April, 2018) Conceptof E-waybill E-waybill refers to Electronic Waybill. It is an electronically document generated on GST portal permitting movement

Comprehensive Guide on E-Waybill (Updated up to 2 nd April, 2018) Conceptof E-waybill E-waybill refers to Electronic Waybill. It is an electronically document generated on GST portal permitting movement

Hosted By GHANDHIDHAM Branch of ICAI

Two Day s Conference Hosted By GHANDHIDHAM Branch of ICAI PRESENTED BY RAJIV LUTHIA AN INVESTMENT IN KNOWLEDGE PAYS THE BEST RETURN 5th November, 2017 CA Rajiv Luthia 1 COVERAGE ISSUES IN GOODS TRANSPORT

Two Day s Conference Hosted By GHANDHIDHAM Branch of ICAI PRESENTED BY RAJIV LUTHIA AN INVESTMENT IN KNOWLEDGE PAYS THE BEST RETURN 5th November, 2017 CA Rajiv Luthia 1 COVERAGE ISSUES IN GOODS TRANSPORT

Tax Period: Integrated Tax. Central Tax. Amt. Rate Amt. Rate Amt. Rate. Tax/ UT Cess (G/S)

") ment 1: (Note: - All statements are auto populated from the corresponding returns taxpayer have to select the invoices accordingly and fields like egm/ebrc to be filled if the same was not filled in the

ment 1: (Note: - All statements are auto populated from the corresponding returns taxpayer have to select the invoices accordingly and fields like egm/ebrc to be filled if the same was not filled in the

Procedures & Transition Provisions under GST

Procedures & Transition Provisions under GST On 23-06-2017 at Hotel JP Celestial, Bangalore -BY CA Chandrashekar B D M/s. Shekar & Yathish Bangalore M/S. SHEKAR & YATHISH 1 . Flow of the Session Time of

Procedures & Transition Provisions under GST On 23-06-2017 at Hotel JP Celestial, Bangalore -BY CA Chandrashekar B D M/s. Shekar & Yathish Bangalore M/S. SHEKAR & YATHISH 1 . Flow of the Session Time of

GOODS & SERVICES TAX / IDT UPDATE 52

GOODS & SERVICES TAX / IDT UPDATE 52 Central Goods and Services tax (Sixth Amendment ) Rules, 2018 The Central Government vide Notification No. 28/2018 GST dated 19 th June, 2018 has notified following

GOODS & SERVICES TAX / IDT UPDATE 52 Central Goods and Services tax (Sixth Amendment ) Rules, 2018 The Central Government vide Notification No. 28/2018 GST dated 19 th June, 2018 has notified following

GST in Microsoft Dynamics NAV 2016

GST in Microsoft Dynamics NAV 2016 Aug 2018 Goods and Services Tax Contents Goods and Services Tax... 1 1. Key Areas of GST Impact on Product Design... 2 2. GST Setups... 13 3. GST Fields in Masters..

GST in Microsoft Dynamics NAV 2016 Aug 2018 Goods and Services Tax Contents Goods and Services Tax... 1 1. Key Areas of GST Impact on Product Design... 2 2. GST Setups... 13 3. GST Fields in Masters..

GST in Microsoft Dynamics NAV 2016

GST in Microsoft Dynamics NAV 2016 Dec 2018 Goods and Services Tax Contents Goods and Services Tax... 1 Revision History... 2 1. Key Areas of GST Impact on Product Design... 3 2. GST Setups... 14 3. GST

GST in Microsoft Dynamics NAV 2016 Dec 2018 Goods and Services Tax Contents Goods and Services Tax... 1 Revision History... 2 1. Key Areas of GST Impact on Product Design... 3 2. GST Setups... 14 3. GST

Ease of Doing Business Duty Free Warehousing

Finance Act, 2016 introduced the provision of Special Warehouse u/s 58A of Customs Act 1962, which states (1) The Principal Commissioner of Customs or Commissioner of Customs may, subject to such conditions

Finance Act, 2016 introduced the provision of Special Warehouse u/s 58A of Customs Act 1962, which states (1) The Principal Commissioner of Customs or Commissioner of Customs may, subject to such conditions

E-Way bill. Microsoft Dynamics AX This document will help you learn how to extend tax configurations to meet the E-Way bill requirement.

Microsoft Dynamics AX 2009 E-Way bill This document will help you learn how to extend tax configurations to meet the E-Way bill requirement. Demo script Prabhat Bhargava June 2018 Send feedback. www.microsoft.com/dynamics/ax

Microsoft Dynamics AX 2009 E-Way bill This document will help you learn how to extend tax configurations to meet the E-Way bill requirement. Demo script Prabhat Bhargava June 2018 Send feedback. www.microsoft.com/dynamics/ax

GUIDE ON IGST REFUNDS IN ICES DIRECTORATE GENERAL OF SYSTEMS CBEC

GUIDE ON IGST REFUNDS IN ICES DIRECTORATE GENERAL OF SYSTEMS CBEC Check IGST Claimed Status Report in NewMIS (export based reports) for IGST Payment & Scroll Details IGST REFUND MODULE-STEP BY STEP FLOWCHART

GUIDE ON IGST REFUNDS IN ICES DIRECTORATE GENERAL OF SYSTEMS CBEC Check IGST Claimed Status Report in NewMIS (export based reports) for IGST Payment & Scroll Details IGST REFUND MODULE-STEP BY STEP FLOWCHART

Subject: Refund of IGST on Export Invoice mis-match Cases Alternative Mechanism with Officer Interface - reg.

Circular No. 05/2018-Customs To F.No.450/119/2017-Cus.IV Government of India Ministry of Finance Department of Revenue (Central Board of Excise & Customs) **** Room No. 227B, North Block, New Delhi. Dated

Circular No. 05/2018-Customs To F.No.450/119/2017-Cus.IV Government of India Ministry of Finance Department of Revenue (Central Board of Excise & Customs) **** Room No. 227B, North Block, New Delhi. Dated

Circular No. 05/2018-Customs To F.No.450/119/2017-Cus.IV Government of India Ministry of Finance Department of Revenue (Central Board of Excise & Customs) **** Room No. 227B, North Block, New Delhi. Dated

Circular No. 05/2018-Customs To F.No.450/119/2017-Cus.IV Government of India Ministry of Finance Department of Revenue (Central Board of Excise & Customs) **** Room No. 227B, North Block, New Delhi. Dated

INVOICE UNDER GST CA. PAYAL VASANI

INVOICE UNDER GST CA. PAYAL VASANI INVOICE (Sec. 31) & Invoice Rules What are we Going to learn today Kinds of Invoices When it is to be used Invoice Rules Manner of Issue of Invoice Contents of Invoice

INVOICE UNDER GST CA. PAYAL VASANI INVOICE (Sec. 31) & Invoice Rules What are we Going to learn today Kinds of Invoices When it is to be used Invoice Rules Manner of Issue of Invoice Contents of Invoice

Date & Day : Wednesday, 04th April, Venue : Jaihind College, A. V. Room, 4th Floor, Presented by : CA Mitesh Katira & CA Parag Mehta

E-Way Bill Subject : E-Way Bill - Issues Date & Day : Wednesday, 04th April, 2018 Venue : Jaihind College, A. V. Room, 4th Floor, A Road, Churchgate, Mumbai 400 020. Presented by : CA Mitesh Katira & CA

E-Way Bill Subject : E-Way Bill - Issues Date & Day : Wednesday, 04th April, 2018 Venue : Jaihind College, A. V. Room, 4th Floor, A Road, Churchgate, Mumbai 400 020. Presented by : CA Mitesh Katira & CA

Generic Standard Operating procedures for transiting and importing goods/supplies

1. Introduction This annex provides a general description of the usual process for importing and transporting goods into countries. It also describes the documents required for obtaining these authorisations.

1. Introduction This annex provides a general description of the usual process for importing and transporting goods into countries. It also describes the documents required for obtaining these authorisations.

CUSTOMS AND EXCISE ACT, 1964 AMENDMENT OF RULES

SOUTH AFRICAN REVENUE SERVICE No. R. 2017 CUSTOMS AND EXCISE ACT, 1964 AMENDMENT OF RULES Under sections 8 and 120 of the Customs and Excise Act, 1964 (Act 91 0f 1964), the rules published in Government

SOUTH AFRICAN REVENUE SERVICE No. R. 2017 CUSTOMS AND EXCISE ACT, 1964 AMENDMENT OF RULES Under sections 8 and 120 of the Customs and Excise Act, 1964 (Act 91 0f 1964), the rules published in Government

ubooks User Guide Table of Contents Login

Table of Contents Login ----------------------------------------------------------------------------------------- 4-4 1 Org. Management 1.1 Org. Profile ----------------------------------------------------------------------

Table of Contents Login ----------------------------------------------------------------------------------------- 4-4 1 Org. Management 1.1 Org. Profile ----------------------------------------------------------------------

Tax Invoice Invoice No. Invoice date. State code

In case of goods In case of services. Original for Recipient Original for Recipient Duplicate for Transporter Duplicate for Supplier Triplicate for Supplier N/A Tax Invoice Invoice No. Invoice date Billed

In case of goods In case of services. Original for Recipient Original for Recipient Duplicate for Transporter Duplicate for Supplier Triplicate for Supplier N/A Tax Invoice Invoice No. Invoice date Billed

ASSOCIATION OF MULTIMODAL TRANSPORT OPERATORS OF INDIA

ASSOCIATION OF MULTIMODAL TRANSPORT OPERATORS OF INDIA For Private Circulation only Disclaimer ** AMTOI / the author does not guarantee the accuracy of opinions and views expressed, and take no responsibility

ASSOCIATION OF MULTIMODAL TRANSPORT OPERATORS OF INDIA For Private Circulation only Disclaimer ** AMTOI / the author does not guarantee the accuracy of opinions and views expressed, and take no responsibility

ISSUES RELATED TO GST IN LOGISTICS INDUSTRY

ISSUES RELATED TO GST IN LOGISTICS INDUSTRY SEMINAR ORGANIZED BY WIRC OF ICAI PRESENTED BY RAJIV LUTHIA 10th August, 2018 AN INVESTMENT IN KNOWLEDGE PAYS THE BEST RETURN CA Rajiv Luthia 1 TRANSPORT OF

ISSUES RELATED TO GST IN LOGISTICS INDUSTRY SEMINAR ORGANIZED BY WIRC OF ICAI PRESENTED BY RAJIV LUTHIA 10th August, 2018 AN INVESTMENT IN KNOWLEDGE PAYS THE BEST RETURN CA Rajiv Luthia 1 TRANSPORT OF

GST PLACE AND TIME OF SUPPLY. K. VAITHEESWARAN ADVOCATE CHENNAI

GST PLACE AND TIME OF SUPPLY K. VAITHEESWARAN ADVOCATE CHENNAI vaithilegal@gmail.com Goods Services Inter-State Supply Intra-State Supply Place of supply for goods Place of supply for services Section

GST PLACE AND TIME OF SUPPLY K. VAITHEESWARAN ADVOCATE CHENNAI vaithilegal@gmail.com Goods Services Inter-State Supply Intra-State Supply Place of supply for goods Place of supply for services Section

Central Board of Excise and Customs

Central Board of Excise and Customs FREQUENTLY ASKED QUESTIONS on IGST Refunds on Goods Exported out of India Zero Rated Supply What is under GST? Under GST, exports and supplies to SEZ are zero rated

Central Board of Excise and Customs FREQUENTLY ASKED QUESTIONS on IGST Refunds on Goods Exported out of India Zero Rated Supply What is under GST? Under GST, exports and supplies to SEZ are zero rated

Official Journal of the European Union L 98/3

17.4.2009 Official Journal of the European Union L 98/3 COMMISSION REGULATION (EC) No 312/2009 of 16 April 2009 amending Regulation (EEC) No 2454/93 laying down provisions for the implementation of Council

17.4.2009 Official Journal of the European Union L 98/3 COMMISSION REGULATION (EC) No 312/2009 of 16 April 2009 amending Regulation (EEC) No 2454/93 laying down provisions for the implementation of Council

GOODS AND SERVICES TAX PLACE & TIME OF SUPPLY PROVISIONS M. VINOD KUMAR I.R.S

GOODS AND SERVICES TAX PLACE & TIME OF SUPPLY PROVISIONS M. VINOD KUMAR I.R.S Time of supply for : Criticality of Place & Time of Supply for determination of liability under GST - goods - services Relevance

GOODS AND SERVICES TAX PLACE & TIME OF SUPPLY PROVISIONS M. VINOD KUMAR I.R.S Time of supply for : Criticality of Place & Time of Supply for determination of liability under GST - goods - services Relevance

Q1. How can I update Sale / Purchase Type master for GST?... 2 Q2. Is there a single Tax Category for both VAT and GST transactions?

FAQ for GST Q1. How can I update Sale / Purchase Type master for GST?... 2 Q2. Is there a single Tax Category for both VAT and GST transactions? If yes then how it will work?... 2 Q3. How can I create

FAQ for GST Q1. How can I update Sale / Purchase Type master for GST?... 2 Q2. Is there a single Tax Category for both VAT and GST transactions? If yes then how it will work?... 2 Q3. How can I create

GST AUDIT An Approach Note. Indirect Taxation Process & Technology Advisory Compliance I Outsourcing

GST AUDIT An Approach Note Indirect Taxation Process & Technology Advisory Compliance I Outsourcing GST Audit An Overview What is GST Audit? On whom it applies to? Types of Audit & Who will do? Examination

GST AUDIT An Approach Note Indirect Taxation Process & Technology Advisory Compliance I Outsourcing GST Audit An Overview What is GST Audit? On whom it applies to? Types of Audit & Who will do? Examination

For HINDUSTAN ZINC LIMITED,

HINDUSTAN ZINC LIMITED CHANDERIYA LEAD ZINC SMELTER P.O. PUTHOLI, DISTT. CHITTAURGARH, (RAJ.) 01472 254115, 254117 NOTICE OF INVITATION OF TENDER FOR TRANSPORTATION OF CALCINE BY BULKERS Tender No.HZL/CLZS/CONT/CALCINE/16-18/04

HINDUSTAN ZINC LIMITED CHANDERIYA LEAD ZINC SMELTER P.O. PUTHOLI, DISTT. CHITTAURGARH, (RAJ.) 01472 254115, 254117 NOTICE OF INVITATION OF TENDER FOR TRANSPORTATION OF CALCINE BY BULKERS Tender No.HZL/CLZS/CONT/CALCINE/16-18/04

Free Zone Process - Sea

High Level Process Pre-clearance Process 1 2 3 4 Ministries Departments and Agencies (MDA) Process Free Zone eexemption Process Shipping Agent Process Pre-clearance Movement Process Scans Bill of Lading

High Level Process Pre-clearance Process 1 2 3 4 Ministries Departments and Agencies (MDA) Process Free Zone eexemption Process Shipping Agent Process Pre-clearance Movement Process Scans Bill of Lading

Single Tender Enquiry

NATIONAL INSTITUTE OF TECHNOLOGY RAIPUR 492 010, CHHATTISGARH Single Tender Enquiry Department: Electrical Engineering Enquiry No: NITRR/S & P/Prop/EE/2019/19 Date: 18/01/2019 To, M/s Hind Electronika

NATIONAL INSTITUTE OF TECHNOLOGY RAIPUR 492 010, CHHATTISGARH Single Tender Enquiry Department: Electrical Engineering Enquiry No: NITRR/S & P/Prop/EE/2019/19 Date: 18/01/2019 To, M/s Hind Electronika

THE MINISTRY OF FINANCE

THE MINISTRY OF FINANCE Circular No. 139/2013/TT-BTC of October 9, 2013, on customs procedures for petrol and oil exported, imported, temporarily imported for re-export and transferred from/to border gate;

THE MINISTRY OF FINANCE Circular No. 139/2013/TT-BTC of October 9, 2013, on customs procedures for petrol and oil exported, imported, temporarily imported for re-export and transferred from/to border gate;

6. In case BOE not submitted at the time of Direct Import Payment, BOE to be submitted within 15 days from the date of transaction.

Direct Import Payment Sr. No. 1. 2. 3. 4. 5. Particular of Documents Request Letter Commercial Invoice Copy of Transport Documents (BL/LR/TR/AWB etc.) Original exchange control copy of Bill of Entry (BOE).

Direct Import Payment Sr. No. 1. 2. 3. 4. 5. Particular of Documents Request Letter Commercial Invoice Copy of Transport Documents (BL/LR/TR/AWB etc.) Original exchange control copy of Bill of Entry (BOE).

NOTICE INVITING QUOTATIONS. File No. NITT/F.No. 020/PROJ/ /DAC Date:

NATIONAL INSTITUTE OF TECHNOLOGY, TIRUCHIRAPPALLI - 620 015 DEPARTMENT OF ACADEMIC OFFICE NOTICE INVITING QUOTATIONS File No. NITT/F.No. 020/PROJ/2018-19/DAC Date: 10.10.2018 To Sealed quotations are invited

NATIONAL INSTITUTE OF TECHNOLOGY, TIRUCHIRAPPALLI - 620 015 DEPARTMENT OF ACADEMIC OFFICE NOTICE INVITING QUOTATIONS File No. NITT/F.No. 020/PROJ/2018-19/DAC Date: 10.10.2018 To Sealed quotations are invited