MAC2601 EXAM PACK PAST QUESTIONS AND TUTORIALS GR SOLUTIONS

|

|

|

- Evan Baldwin

- 6 years ago

- Views:

Transcription

1 MAC2601 EXAM PACK PAST QUESTIONS AND GR TUTORIALS SOLUTIONS Tel:

2 MAC REVISION STUDY PACK TOPIC 1: NATURE AND BEHAVIOUR OF COSTS (1) Manufacturing cost/ Production cost Manufacturing costs - costs incurred in the manufacturing process of a product. Direct + Indirect cost = Manufacturing cost Direct cost = Direct Material + Direct Labour Total Direct cost = Prime cost Conversion cost = Direct Labour + Manufacturing overheads Indirect cost = Indirect material + Indirect Labour Total Indirect cost = Overheads Direct cost costs directly linked to the product. Indirect cost costs indirectly linked to the product Manufacturing Total cost = variable cost + fixed cost Variable cost costs that vary with production e.g. material costs Fixed cost costs that are constant throughout the manufacturing period e.g. Rent. Semi variable cost cost that have both elements variable element and fixed element e.g. Telephone bill Non Manufacturing cost / Period costs Non Manufacturing cost costs incurred after the manufacturing process a. Marketing cost costs related to the sale and distribution of the final product. b. Administrative costs costs incurred in directing and controlling the organization. Splitting fixed from variable cost GR TUTORIALS Methods used High low method Linear equation Scatter diagram Simple regression analysis / least squares methods We will concentrate on the high low method e.g. Observations No. of Units Total overhead cost

3 1 step - identify the two points highest level and the lowest level and calculated the differences. High Low Calculate the variable rate = = R100/m Variable cost after producing 900 units and 900 x 100 = R Calculating fixed cost Total cost = fixed cost + variable cost = fixed cost (900x100) = f x d cost = f x d COH = FX d cost GR TUTORIALS 2

4 3

5 Cost Volume profit analysis It investigates the change in profit that from changes in activity levels Selling price per unit Variable cost per unit Total fixed costs NB: Assumptions of the cost CVP analysis Selling price per unit in consultant unless stated. All cost is linear and can be accurately dividend into variable and fixed elements. Variable costs are constant per unit, where as fixed cost, we content in total over the relevant range. Inventory levels do not change CVP. Analysis applies to the relevant range only. Relevant range activity levels within which the organization normally operates and for which cost and remains behavior are known and can be predicted. Formulas Contribution = sales - total variable costs Contribution ratio = x 100 % Breakeven Point Point where income is equal to expenses i.e. profit is zero Contribution = total fixed cost Can be expressed in units or value (Rand value) BEP in units = Contribution per units = selling price/unit variable cost per unit BEP in value = NOTE: BEV = BE units x selling price per unit BE units = GR TUTORIALS Margin of safety (MOS) Amount, or number of units or percentage by which sales revenue may decline before incurring a loss. Margin of safety In value = total sales breakdown sales In units = total sales (units) break even sales units Margin of safety Ratio C 4

6 Mos ratio (units) = x 100 % Mos ratio value = x 100 % Targeted Profit Analysis Used to determine the sales value that will produce a certain net profit. NB. If you understand bep it should be easier to remember the following formulas and also calculating. Target sales In value = In units = Key important things to note in the effect of price and changes on breakeven point. When sales increase it would be due to increase in selling price/unit or increase in units sold. Increase in selling price limit no effect on production cost. Increase in sales volume - variable cost are affected, they have to be increased in the same proportion (remember the nature of variable cost and cvp assumption) BEP Graph R GR TUTORIALS TOTAL SALES Profit 20x BEP VARIABLE COST BEV loss BEQ Quantity/units produced 5

7 Topic 3 Material, Labour, Overhead Material Physical materials converted in products during the manufacturing process (direct material, indirect materials, and other consumables used by the organization). Reasons for holiday inventory Transaction motive holding inventory for day to day use in production process or for sales, where the supplier might not be able to supply at short notice. Precautionary motive holding extra inventory when future demand is uncertain. Speculative motive holding more or less inventory than usual because a change in the supplier s price is anticipated. Carrying and ordering cost Carrying / holding cost relevant costs of keeping inventory on the organization s premises until used and includes handling costs and storage cost. Average inventory = 1 2 x order size Average wage per day = GR TUTORIALS Ordering costs Relevant cost of ordering Inventory and may include delivery and transport costs, administrative cost of preparing and processing the order. N3 Quantity to order a t a given time should therefore be determined by balancing the following factors. Inventory carrying costs Ordering cost The order Quantity at which annual carrying and ordering costs are minimized is the EOQ. NB. EOQ has nothing to do with economies of scale. 6

8 Determining EOQ (1) Tabular Method Annual demand for is 2400 units Variable cost of placing an order is R25 Variable cost of carrying one unit f or one year is R3. Order Qnty Number of Orders Demand/Order Qnty Average Inventory / Order Qnty/ Relevant annual cost R R R R R R R Ordering cost No. of orders x R Carrying cost Total Therefore: EOQ = 200 Average Inventory = 100 units Number of orders = 12 Fomular Method EOQ = ( ) GR TUTORIALS 2 = a constant C = variable cost of placing an order. U = annual usage / demand H = variable holding cost (excl interest) per annum per unit I = interest rate or required return (use only w hen given) P = Purchase price per unit use only when provided Question A company has collected the following data for a given year EOQ in units EOQ in units 5000 Total variable cost to place purchase orders for the year R Variable cost to place one order R50 Variable cost to carry one unit for 1 year R4 7

9 Required What is the annual usage in units? Calculate the total annual variable carrying costs based on the EOQ. Assuming are ordered in lots of units. (batches) What would be the implication be for variable costs? Solution Annual usage Total number of orders = = = 200 Annual demand number of order x EOQ 200 X 5000 = units Total annual variable carrying cost x 4 = R TUTORIALS ( c) If orderly in lots of units Orderly costs would be x GR Carry cost 2 x Increase of R Total cost Total cost R Less orderly Carrying cost Difference

10 Labour Types of remunerations Remunerations Is the amount an employer pays to an employee or on behalf of an employee for services rendered in terms of the employment contract. Fixed monthly salary employee receives a fixed salary regardless of the quantity of work done or spent on it. The time wage system employee is paid in accordance with the number of how is that he /she works not based on performance (hours worked x hourly rate (basic)). Piece wage system employee paid for the work he/she has done and not according to the time spent on it payment is based on output. (Units produced x basic rate/unit) Payroll terms Gross remuneration amount earned by the employee for the hours worked, includes overtime wages, allowances, bonus. Overtime premium an additional amount paid over and above the normal rate / time Taxable income gross remuneration remaining after deducting any contribution by the employee to any pension fund. GR TUTORIALS Cost to company total amount expended by the employer to and on behalf of the employee. NB Note Activity is 1 and Activity 5.2 in the study guide Labour Recovery rate Budgeted Labour recovery rate expected labour cost per hour. = Clock hours - the hours the employee clock in to b on the premises. Idle time the time when the employee is clocked in but not working owing to smoke breaks, tea, lunch etc. 9

11 Productive work hours the hours that the employee is expected to be physically working in the production process or on jobs. These correspond to job card hours. Question Ezakheni Ltd is a small business that manufactures computer stands. It is situated in KZN. The business wishes to determine the available productive time to be used in the calculation of the hourly recovery rate for the forth coming year. Nakiwe Mkhwanazi the business s wages clerk prepared the following wage summary for Mike Mvelase, who works at the assembly department. Normal wage rate R15 / hour Holiday bonus R4 800 Ezakheni Ltd makes the following contributions. 16% of normal wage (including vocation pay) to the pension fund. 14% of normal wage (including vocation pay) to the medical aid fund. Additional Information The company operates on a 45 hour week (Mon Friday) for 52 weeks a year. Vocation leave is 20 work days for employee annually. There are 10 paid public holidays per year. Idle time makes up 5% of available clock time. Required Calculate the following: a) Annual productive work hours b) The normal annual wage cost. c) The total annual labour cost. d) The productive work hour labour recovery rate. GR TUTORIALS (b) Annual Productive Hours Number of clock hours in a year 45 x Less Public holidays 10 days x 9 hours 90 Less vacation hours 20 days x Total clock hours available for production Less Idle the 2070 x 5% Annual productive hours Normal annual wage cost Number of weeks in a year Less vacation Actual working weeks Normal wage 48 weeks x 45 hrs x R15 = R wks 4wks 48wks 10

12 ( C) Total annual Labour cost Annual normal wage 2700 Vocation pay 15 x 180 hrs Pension fund x 16% 5616 Medical aid R X 14% 4914 Total annual labour costs (d) Labour Recovery Rate = R25, 64 per productive operating hour Overheads Total Indirect cost Applied manufacturing overhead Total annual labour cost annual productive hours R GR TUTORIALS Actual overheads, these are the actual overheads costs incurred during a period. Budgeted overheads, estimated overhead cost before or at the beginning of a financial year. Applied overheads, These are the total overheads allocated to the cost of the products based on the predetermined, or recovery rate. For each actual produced a budgeted rate will be assigned, thus accounting for the total applied overheads. Overhead recovery rate - Under or over applied overheads Applied overheads < actual overheads under application Applied overheads > actual overheads over application 11

13 12

14 NB check Activity 6.7 study guide for possible predetermined overhead recovery. 13

15 Methods of stock valuation Process of assigning cost to inventory FIFO According to FIFO, the accounting assumption is that materials received or purchased first are issued first are issued first, units are issued in the order they were received. Weighted average No assumptive about the flow of materials. The issuing of materials at a weighted average cost assumes that each batch taken from the storeroom is made up of the same quantities from each consignment in inventory a t the date of issue, no attempt is made to identify when the units were purchased. N3 you only average stock price after a purchases. Effects of movement of stock on the balance in the warehouse for both methods. Supplier warehouse production Returns to supplier returns stock in the warehouse and it s treated as a negative receipts. Returns to warehouse Increases stock in the warehouse and it treated as a negative issue. (add back to what is in the warehouse). GR TUTORIALS 14

16 15

17 16

18 17

19 Topic 4 Direct casting method vs the absorption costing method The difference between the two methods lies on the treatment of cost/how to calculate manufacturing cost. Direct costing method only accounts for variable manufacturing cost ass the total manufacturing cost. Absorption costing method absorbs all manufacturing cost that is fixed and manufacturing cost as the total manufacturing. Areas to be carefully with, when answering question Method used direct/absorption method tell you how to calculate manufacturing cost. Method of stock valuation. FIFO/WAVE tell you how to calculate value of Calculating units of closing/opening inventory stocks. The layout/structure is the same they do not change Direct Method structure /layout Direct Method Sales Less variable cost of sales Opening Inventory Variable manufacturing cost Cost of goods available for sale Less closing Inventory Variable manufacturing cost of sales Add other variable cost Contribution/marginal income Less Fixed cost Net Profit before tax Absorption Sales Less Manufacturing cost. VC Fixed cost Cost of goods available for sale Less closing stock Gross Profit Less: Selling and admin cost Not profit before tax GR TUTORIALS xxx xxx xxx (xxx) xxx xxx xxx xxx xxx xxx xxx xxx xxx xxx xxx xxx xxx xxx xxx 18

20 Calculation of closing units Opening Inventory Production Units available for sale Less sales Closing inventory units Units xxx xxx xxx xxx xxx Calculation of value of stock Weighted Average method Absortion Methods x units of opening inventory Closing stock Direct x vc/unit Closing stock x units of closing inventory x units of closing inventory FIFO x units of opening inventory GR TUTORIALS Closing x units of closing stock 19

21 Direct x VC/unit Closing Inventory Units of closing inventory x VC /unit GR TUTORIALS 20

22 21

23 22

24 23

25 Topic 5 ABC and Traditional Traditional costly Fixed production overhead cost is allocated to products by linking it to only one volume driven allocation base e.g. machine hours. [Very crude way in which to allocate support overheads]. ABC assumes that activities cause or drive the cost and that products are created by activities. Allocation of costs is therefore based on the utilization of activities. Purpose to allocate cost based on the cause of the cost. Two stage allocation process. Traditional Method vs ABC 1. Allocates overheads to production and 1. Pools overheads to each major activity service departments then reallocates rather than departments. service department costs to the production departments (secondary allocation) 2. Allocation of overheads to products based on a small number of second stage allocation bases (units/hours) resulting in overhead allocation rate. Steps to follow answering ABC question Identify activities Identify cost drivers Create cost pool for each activity Calculate activity cost rate Allocate cost to cost object 2. Cost driven rate is used rather than allocation rate, a widen base for more accurate results. Activity - is a task, action or unit of work that is carried out in the organization. GR TUTORIALS Transaction driver count the number of times that an activity is performed. Duration driver- represents the length of time required to perform an activity. 24

26 25

27 26

28 Topic 6 Job costing system Method of calculating the cost per unit is used were goods are manufactured according to a clients specifications that is, where heterogeneous products are manufactured using the same production facilities. When calculating the cost per unit, 1 job is looked at independently from the other jobs. An independent ledger account for a specific job is opened that will be debited with all specific job is opened that will be debited with all that was used for the job i.e. materials, labour and overheads. If the job was completed the account is closed off against the finished goods account. If not finished it will be closed of against the work in progress account. NB The basis for allocating overheads. GR TUTORIALS 27

29 28

30 29

31 30

32 Required GR TUTORIALS Draft a cost and income statement for May 19.9 showing the situation regarding each job and stock levels of each at the end of the month. 31

33 32

34 Topic 7 Process costing system A process costing system is a costing system used to obtain record, and report cost data in industries where large quantities of similar products pass through a single process or a consecutive process in the course of production. Unit cost in system with a single process Process 1 Unit cost in a system with two or consecutive process labour material overheads Labour &overhead Material Labour Overhead Manufacturing cost P1 P2 P3 Labour &overhead GR TUTORIALS Prev Process Finished goods Material Labour Overhead Total units Cost/unit R5 R86 R13 Process cost Reports Quantity statement Production cost statement Allocation statement 33

35 Quantity Statement Accounts for all the units produced in the process NB Only Quantities involved Key things to note Input = output Method of stock valuation used Calculation of units that reached/passed the wastage point during the current period (Losses). Wastage points Stage of completion of opening and closing stock Equivalent completed units Frame works Quantity statement for the period ended (weighted average method) Inputs Details Output Raw Materials conservation % % Input xxx xxx Opening WIP Put into production Out put Completed and transferred xxx xxx xxx xxx xxx Normal loss xxx xxx xxx xxx xxx Abnormal loss xxx xxx xxx xxx xxx Closing WIP xxx xxx xxx xxx xxx xxx xxx xxx xxx FIFO Method GR TUTORIALS Inputs Details Output Raw Materials conservation % % Input xxx Opening WIP xxx Put into production Out put Completed and transferred xxx - xxx xxx xxx Opening wip Current production xxx xxx xxx xxx xxx normal loss xxx xxx xxx xxx xxx Abnormal loss xxx xxx xxx xxx xxx Closing WIP xxx xxx xxx xxx xxx xxx xxx xxx xxx 34

36 Equivalent Completed units Ecus are used to compare partially completed units. (WIP) by coveting them into a comparable number of fully completed units called equivalent units. e.g. If unit cost R100 /unit to manufacture and there are 2 00 WIP units which are 40% complete (material 100%) it means, ECU = 200 X 40 % = 80 units we use stage of completion to calculate the ECU. NB. When calculating ECU for materials and conversion. Using the same above mention scenario and assuming that this was opening stock. Remember Opening stock these are units which were started to be produced in the previous period to be finished in the current period so what written took place in the previous period. We are to account for the current period. For material 100 % - 100% = 0 Conversation N 100% - 4 0% = 60 % i.e. 60% of conversation would be done this current period. Losses Abnormal avoidable Balancing figure in the Quantity statement Normal unavoidable - calculated Normal Loss We have to calculate the unit that would have passed to wastage point during the current period. Losses are accounted for in the period are incurred. Look at opening stock and closing stock whether they readed the wastage point in the current period or not. For opening stock ascertain if the loss was accounted for in the previous period or not. As for closing stock ascertain whether the loss on closing units has been incurred or will be incurred in the following period. GR TUTORIALS Oct / Nov 2008 Question (20 marks) Ping cc manufactures a single product in one process. The following information for August 2008 is available Work in process 1 August units Material-100% complete R Conversion costs 50 % complete R Material issued for units R Conversation cost R Units completed units Work in process 31 August units Material 100% 35

37 Conversation 75% Additional Information 1. Material is added at the beginning of the process conversation costs are incurred evenly throughout the process. 2. Normal spoilage is 5% of input that reaches the point of spoilage. 3. Losses occur when the process is 90% complete. 4. Stock is valued according to the first in first method Required Prepare the following statement for August 2008 Quantity Statement Production cost statement Allocation statement SOLUTION Key things to note: method of stock valuation Wastage point Normal loss percentages Input Details Output Material conversion Opening WIP Put Into Production Completed & transferred from WIP Current production Spoilage :Normal %( ) Abnormal Closing wip GR TUTORIALS LOSS Opening WIP Opening WIP WP Prev Period 50%Current period 90%

38 Opening units reached/passed wastage point in the current period therefore loss on opening stock to be accounted for in the current period. CLOSING WIP Closing WIP WP 0 Current period Closing WIP units has passed the wastage point; they will pass in the following period therefore no loss has to be accounted for during the current period. Production cost statement It deals with cost incurred during the process. NOTE: the method of stock valuation used it affects the cost statement. Using the Oct/Nov Question First in First Out 75% 90% 100% GR TUTORIALS Total Material Conversation Opening WIP Current costs :Equivalent units EC/unit Assuming that weighted average was used Total Material Conversation Opening WIP Current cost =

39 Weighted price Allocation Statement Allocation statements links the Quantity Statements to cost incurred during the period (production cost statement). Note Normal losses are accounted as product cost. Abnormal losses are period cost. OCTOMBER NOVEMEBR 2008 Normal loss to be allocated (87000x16.97)+(7830x19.06) = Aportioned to units completed x Abnormal units Allocation Statement Opening WIP Material Conversation ( x Current cost Material (81600x16.97) Conversion (115800x19.06) Normal loss Completed and transferred Abnormal spoilage Material x Conversion x Normal loss Closing WIP Material x Conversation x Difference due to rounding GR TUTORIALS

40 Topic 8 Joint and by production costing system Joint production Production arising from the joint process which have significant value. Joint process is internationally completed to obtain these products. Joint process Two or more different products which are not separately identifiable until this process is completed, emerge from the joint process. Split of point Point in the production process where the separate joint products can be identified for the first time. Joint cost Common cost incurred prior to the split off point are known as joint costs Further processing costs Extra cost incurred to further convert the separated joint products into final products. By product Products that is insignificant in value to the joint products. Methods used to allocate joint cost 1. Physical standard method Physical quantities of products will be used to proportion the joint cost (in proportion to the physical quantity of each joint product produced). Suitable where the output is similar in nature and value. 2. Market value at slit off point method Joint calls are allocated to each product in proportion to their potential market value of the product at split off point in the production process. Assumes that higher selling prices are accompanied by higher costs. 3. Net realizable value at split off point method Market value of the final product is taken and reduced by any costs incurred for processing of the product beyond the split off pout and by selling and distribution costs incurred to sell the final product. GR TUTORIALS NRV values are used to establish the ratio in which the joint cost costs are to be apportioned. 4. Reversal costing method When using this method, the question is not what portion of the costs should be allocated to the products but what amount should be absorbed by each product to arrive at a constant gross profit percentage for all or specific products. 39

41 Refer to Activity 19.2 study guide May / June 2008 Gee Gee Ltd manufactures three products in a single process. The following are actual result for March A V M Selling split off point(per litre) Selling price after further processing (per litre) Cost after split off point Output 35000L 25000L 20000L The following cost are incurred in a joint process Direct material R Direct Labour R Manufacturing overheads R It is the policy of the company to allocate joint costs according t o the relative market value of the final product method. There was no stock on hand at the end of March Required a. Calculate the actual Profit/loss on sale of each product for March 2008 if all three products are further processed. b. Calculate how profits could be maximized if one or more products are sold at split off point. Joint cost GR TUTORIALS 35000L A L V L M Split off point Further processing cost 40

42 (a) Product Rel Market Value J. C Allocation A ( X 14) = X V M (25000 X 12) = X ( X 21) = X A V M Sales 35000x x x21 Less cost Joint cost ( ) ( ) ( ) Additional cost (188500) ( ) ( ) Net Profit (b) A V M Sales x x x Less joint cost GR TUTORIALS Therefore: Product A should be processed further Product V should of split off point Product M should be further processed Max Profit

43 Accounting for by products Revenue from by-products are accounted for in the ways. Reduction of joint cost. This method, reduce the joint cost by subtracting revenue from byproducts from the total. Joint cost before being allocated. Separate income It can also be seen as additional income and after calculating net profit the revenue from by-products will be added as a separate income. Reduction of cost sales Reduce the cost of sale with the revenue from by products. GR TUTORIALS 42

44 Topic 9 Standard costing Standards predetermined targets, they are targets inputs that should be achieve under efficient operating conditions. Note: A budget represents the costs of an entire activity or operation where as standards represents the same information per unit. Calculating variances Basically we are comparing the actual results to the standards in all the variances calculated. When Actual < standards = favourable variances Actual > Standards = unfavourable variances Income Actual < standards = unfavorable variance Actual > standards = favourable Fomula Materials TMO = MPV + MQV MPV = (AP SP) AQ MQV = (AQ SQ) SP Labour TLV = LRV + LEFFV LRV = (AR SR) Act hour LEffV = (Act hrs Shrs) SR GR TUTORIALS Variable manufacturing variance (Vm olho) Varying with Labour hours TVmo/hv = VM0/h Rate variance + VM 0/h efficiency variance. Vm 0/h rate v = (AR SR ) Actual hrs V m 0/heefv = (Act hours 5 hours) SR Vary with Production TVM 0/hv = VM 0/h rate variance VM 0/h rate v = (Ar Sr) Actual output V M 0/h rate V = 0 (always) efficiency is measured with hours not units only. October / November

45 GoGoGo cc manufactures and sells a single product the following information was obtained f or June 2008 Budgeted sales R (Budgeted selling price per unit R16.50 Actual sales R units were manufactured and sold during the June The standard cost per unit is calculated as follows. R Material R5 120 per kg 7.80 Labour R8 per hour 4.00 Variable overheads Vary with production 1.20 Fixed overheads R3.60 per machine hour Actual labour hours for June 2008 were hours Actual material costs were R Variable overheads of R95200 were paid Fixed overheads amounting R were paid in June 2008 Budgeted and actual net profit is R and R respectively. The following variances were calculated. Material purchase price variance Material quantity variance Labour rate variance Fixed overhead variance Required a. Calculate the following for the 2008 i. Sales price variance ii. Actual quantity purchased iii. Actual rate paid per labour hour. iv. Labour efficiently variance v. Variable overhead variance. b. Reconcile the budgeted profit with actual profit for June R Unfavourable 1300 favourable 6330 unfavourable favourable GR TUTORIALS Solution i. Sales price variance = Act sale standard sales 44

46 = (splu Ssplu) Units sold ( ) u ii. Actual quantity purchased = MQV = (AQ-SQ) sp (f) = (x (84500x1.5)) ( ). 250(f) = x = ( ).. Note : variance is 250(f) which means the Actual Quantity must be less than the standard Quantity of 250(f) = x Change the favourable variance to a negative to get the correct answer. (Always to the opposite) -250 = x X = AQ = Actual rate paid LRV = (Ar SR) Actual hours ( ) 0.15 A = x -8 = ( ) Remember how we treated the previous question = x GR TUTORIALS 45

47 X = 8.15 Actual rate = R8.15/hour vi Labour efficiency variance = (Actual hrs 5hrs) SR = (42200 (0.5x84500)) 8 =( )8 =400(8) v.variable overhead variance = Rate variance = (AR SR)Production = ( ) ( ) (f) Reconciliation Budgeted profit Actual profit Selling price v (42200) Total mat v (11200) Total labour (5930) Variable overhead v 6200 Fixed overhead v GR TUTORIALS 46

48 Topic 10 Relevant Info for short term Decision Relevant Information Relevant Information This is the information that should be taken into account in order to choose an appropriate course of action from a set of possible options. Criteria for Relevance To be relevant to a specific decision a cost should meet the following: It relates to the future (not a sunk cost) Payable/ receivable in cash. It is directly determined by the alternative selected. It arises as a result of the decision. Sunk costs Cost incurred in the past and cannot be changed. Committed costs/increase (unavoidable) Future cash flows that arise as a result of a decision or action taken in the past. They are unaffected by the decision that need to be taken now and cannot be presented by selecting anyone of the available alternatives. Incremental cost Additional cost that will be incurred if a specific alternative is selected and that will lead to future cash outflow for the organization Incremental Income Additional income generated if a specific alternative is selected and that will lead to a future cash inflow for the organization. Avoidable costs Cost that an organisation prevents from being incurred by choosing a specific option. Avoidable costs are relevant cost. Opportunity costs Forfeited cost GR TUTORIALS 47

49 48

50 49

51 50

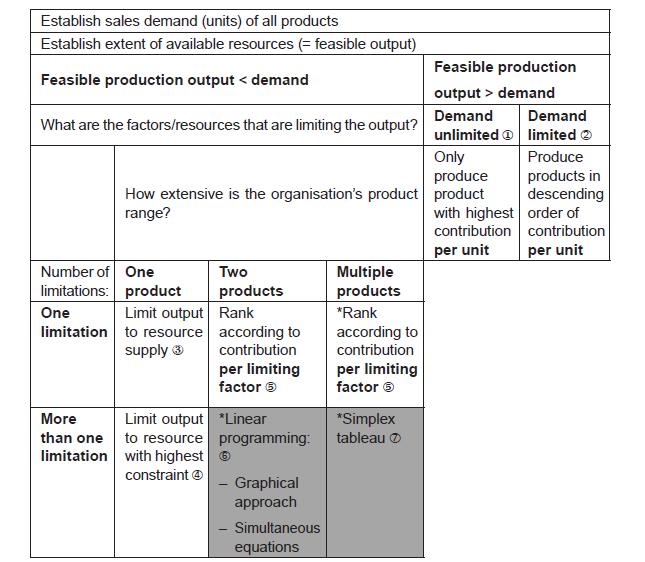

52 Limiting factors and allocation of resources GR TUTORIALS 51

53 52

54 53

55 54

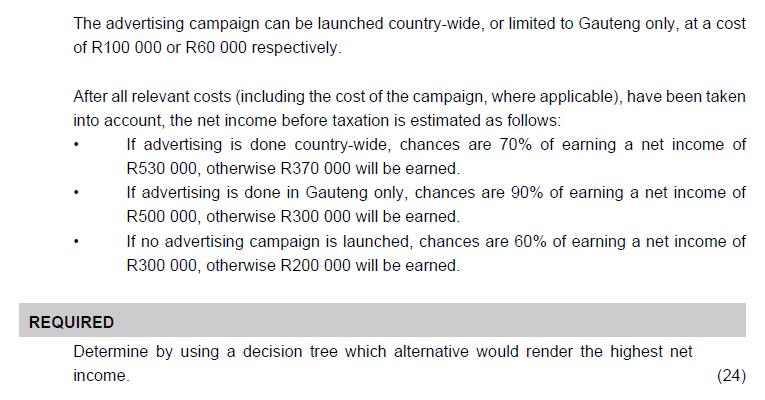

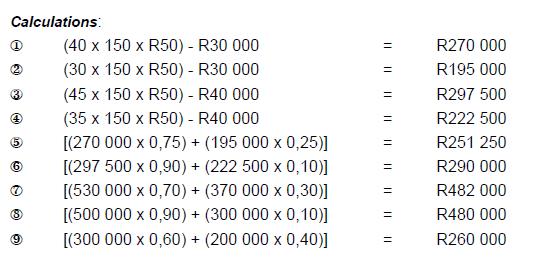

56 Probabilities and decision tree GR TUTORIALS 55

57 56

58 57

59 58

60 59

61 Question papers and answers GR TUTORIALS 60

62 61

63 62

64 63

65 64

66 65

67 66

68 67

69 68

70 69

71 70

72 71

73 72

74 73

75 74

76 75

77 76

78 77

79 78

80 79

81 80

82 81

83 82

84 83

85 84

86 85

87 86

88 87

89 88

90 89

91 90

92 91

93 92

94 93

95 94

96 95

97 96

98 97

99 98

100 99

101 100

102 101

103 102

104 103

105 104

106 105

107 106

108 107

109 108

110 109

111 110

112 111

113 112

114 113

115 114

116 115

117 116

118 117

119 118

120 119

121 Extra questions 120

122 121

123 122

124 123

125 124

126 125

127 126

128 127

129 128

1). Fixed cost per unit decreases when:

. Fixed cost per unit decreases when:") 1). Fixed cost per unit decreases when: a. Production volume increases. b. Production volume decreases. c. Variable cost per unit decreases. d. Variable cost per unit increases. 2). Prime cost + Factory

1). Fixed cost per unit decreases when: a. Production volume increases. b. Production volume decreases. c. Variable cost per unit decreases. d. Variable cost per unit increases. 2). Prime cost + Factory

Process Costing Joint and By Product CA Past Years Exam Question

CA R. K. Mehta Process Costing Joint and By Product CA Past Years Exam Question Question : 1 May, 2012 A product passes through two processes A and B. During the year, the input to Process A of Basic raw

CA R. K. Mehta Process Costing Joint and By Product CA Past Years Exam Question Question : 1 May, 2012 A product passes through two processes A and B. During the year, the input to Process A of Basic raw

MARGINAL COSTING CATEGORY A CHAPTER HIGH MARKS COVERAGE IN EXAM

1 MARGINAL COSTING CATEGORY A CHAPTER HIGH MARKS COVERAGE IN EXAM Question 1 Arnav Ltd. manufacture and sales its product R-9. The following figures have been collected from cost records of last year for

1 MARGINAL COSTING CATEGORY A CHAPTER HIGH MARKS COVERAGE IN EXAM Question 1 Arnav Ltd. manufacture and sales its product R-9. The following figures have been collected from cost records of last year for

Financial Accounting and Auditing Paper-III Financial Accounting

Revised Syllabus of the Courses of B.Com. Programme at T.Y.B.Com. with Effect from the Academic Year 2015-2016 for IDOL Students Financial Accounting and Auditing Paper-III Financial Accounting SECTION

Revised Syllabus of the Courses of B.Com. Programme at T.Y.B.Com. with Effect from the Academic Year 2015-2016 for IDOL Students Financial Accounting and Auditing Paper-III Financial Accounting SECTION

COST C O S T COST. Cost is not a simple concept. It is important to distinguish between four different types - fixed,, variable, average and marginal.

Ir. Haery Sihombing/IP Pensyarah Fakulti Kejuruteraan Pembuatan Universiti Teknologi Malaysia Melaka Chapter 3 DIRECT COST Chapter 4 INDIRECT COSTS C O S T COST Cost is not a simple concept. It is important

Ir. Haery Sihombing/IP Pensyarah Fakulti Kejuruteraan Pembuatan Universiti Teknologi Malaysia Melaka Chapter 3 DIRECT COST Chapter 4 INDIRECT COSTS C O S T COST Cost is not a simple concept. It is important

COST ACCOUNTING b.com part II Regular & Private (SUPPLEMENTARY) Solved Paper. Compiled & Solved by: Sameer Hussain

Solved Paper. Compiled & Solved by: Sameer Hussain") COST ACCOUNTING b.com part II 2014 Regular & Private (SUPPLEMENTARY) Solved Paper Compiled & Solved by: Sameer Hussain Instructions: (1) Attempt any FIVE questions. (2) All questions carry equal marks.

COST ACCOUNTING b.com part II 2014 Regular & Private (SUPPLEMENTARY) Solved Paper Compiled & Solved by: Sameer Hussain Instructions: (1) Attempt any FIVE questions. (2) All questions carry equal marks.

2. Standard costs imply a) Predetermined cost for a period b) Incurred cost c) Conversion cost d) Incremental cost

Predetermined cost for a period b) Incurred cost c) Conversion cost d) Incremental cost") QUESTION BANK PAPER: COST ACCOUNTING COURSE: B.Com (Semester IV) MCQs 1. The basic objective of cost accounting is a) Recording of cost b) Reporting of cost c) Cost control d) EarningProfit 2. Standard

QUESTION BANK PAPER: COST ACCOUNTING COURSE: B.Com (Semester IV) MCQs 1. The basic objective of cost accounting is a) Recording of cost b) Reporting of cost c) Cost control d) EarningProfit 2. Standard

Selling Price 60 Direct material 28 Direct Rs. 3 p. hr. 12 Variable overheads 6 Fixed cost (Total) 1,05,500

1,05,500") Question 1 (a) PAPER 5 : ADVANCED MANAGEMENT ACCOUNTING Answer all questions. Working notes should form part of the answer. E Ltd. is engaged in the manufacturing of three products in its factory. The

Question 1 (a) PAPER 5 : ADVANCED MANAGEMENT ACCOUNTING Answer all questions. Working notes should form part of the answer. E Ltd. is engaged in the manufacturing of three products in its factory. The

Inventory Cost Accounting Tips and Tricks. Nick Bergamo, Senior Manager Linda Pei, Senior Manager

1 Inventory Cost Accounting Tips and Tricks Nick Bergamo, Senior Manager Linda Pei, Senior Manager 2 Disclaimer The material appearing in this presentation is for informational purposes only and is not

1 Inventory Cost Accounting Tips and Tricks Nick Bergamo, Senior Manager Linda Pei, Senior Manager 2 Disclaimer The material appearing in this presentation is for informational purposes only and is not

Standard Costing and Variance Analysis

5 Standard Costing and Variance Analysis Standard Costing and Variance Analysis 5 LEARNING OUTCOMES After completing this chapter, you should be able to: explain the difference between ascertaining costs

5 Standard Costing and Variance Analysis Standard Costing and Variance Analysis 5 LEARNING OUTCOMES After completing this chapter, you should be able to: explain the difference between ascertaining costs

Chapter 3. Accounting for Labor

Chapter 3 Accounting for Labor Learning Objectives LO1 Distinguish between features of hourly rate and piece-rate plans. LO2 Specify procedures for controlling labor costs. LO3 Account for labor costs

Chapter 3 Accounting for Labor Learning Objectives LO1 Distinguish between features of hourly rate and piece-rate plans. LO2 Specify procedures for controlling labor costs. LO3 Account for labor costs

CA IPC ASSIGNMENT MATERIAL, MARGINAL COSTING & BUDGETARY CONTROL

CA IPC ASSIGNMENT MATERIAL, MARGINAL COSTING & BUDGETARY CONTROL MM: 87 Marks Question 1: Arnav Udyog, a small scale manufacturer, produces a product X by using two raw materials A and B in the ratio of

CA IPC ASSIGNMENT MATERIAL, MARGINAL COSTING & BUDGETARY CONTROL MM: 87 Marks Question 1: Arnav Udyog, a small scale manufacturer, produces a product X by using two raw materials A and B in the ratio of

Management Accounting

Management Accounting Suggested Solutions to Practice Questions Professional, Practical, Proven www.accountingtechniciansireland.ie Table of Contents Part 1:... 2 Part 2:... 8 Part 3:... 14 Part 4:...

Management Accounting Suggested Solutions to Practice Questions Professional, Practical, Proven www.accountingtechniciansireland.ie Table of Contents Part 1:... 2 Part 2:... 8 Part 3:... 14 Part 4:...

Paper T4. Accounting for Costs. Thursday 10 December Certified Accounting Technician Examination Intermediate Level

Certified Accounting Technician Examination Intermediate Level Accounting for Costs Thursday 10 December 2009 Time allowed: 2 hours This paper is divided into two sections: Section A ALL 20 questions are

Certified Accounting Technician Examination Intermediate Level Accounting for Costs Thursday 10 December 2009 Time allowed: 2 hours This paper is divided into two sections: Section A ALL 20 questions are

Accounting for Overheads - Marginal Costing

Accounting for Overheads - Marginal Costing Marginal cost is the variable cost of one unit of product or service. Marginal costing is an alternative method of costing to absorption costing. In marginal

Accounting for Overheads - Marginal Costing Marginal cost is the variable cost of one unit of product or service. Marginal costing is an alternative method of costing to absorption costing. In marginal

Cost & Management Accounting Bachelors of Business (Specialized in Finance) Study Notes & Tutorial Questions Chapter 3: Labor Costing

Study Notes & Tutorial Questions Chapter 3: Labor Costing") Cost & Management Accounting Bachelors of Business (Specialized in Finance) Study Notes & Tutorial Questions Chapter 3: Labor Costing 1 INTRODUCTION Labour is the second element of cost after materials.

Cost & Management Accounting Bachelors of Business (Specialized in Finance) Study Notes & Tutorial Questions Chapter 3: Labor Costing 1 INTRODUCTION Labour is the second element of cost after materials.

10 Joint Products & By Products

10 Joint Products & By Products BASIC CONCEPTS AND FORMULAE Basic Concepts 1. Joint Products and By-Products (i) Joint Products - Two or more products of equal importance, produced, simultaneously from

10 Joint Products & By Products BASIC CONCEPTS AND FORMULAE Basic Concepts 1. Joint Products and By-Products (i) Joint Products - Two or more products of equal importance, produced, simultaneously from

Basic Costing Guidance

Basic Costing Guidance The Association of Accounting Technicians April 2010 Basic costing (BCCG) Introduction Please read this document in conjunction with the standards for all relevant units. Basic Principles

Basic Costing Guidance The Association of Accounting Technicians April 2010 Basic costing (BCCG) Introduction Please read this document in conjunction with the standards for all relevant units. Basic Principles

Part 1 Study Unit 5. Cost Accumulations Systems Jim Clemons, CMA Ronald Schmidt, CMA, CFM

Part 1 Study Unit 5 Cost Accumulations Systems Jim Clemons, CMA Ronald Schmidt, CMA, CFM 1 Overview Cost accounting systems record manufacturing activities using a perpetual inventory system, which continuously

Part 1 Study Unit 5 Cost Accumulations Systems Jim Clemons, CMA Ronald Schmidt, CMA, CFM 1 Overview Cost accounting systems record manufacturing activities using a perpetual inventory system, which continuously

Welcome to: FNSACC507A Provide Management Accounting Information

Welcome to: FNSACC507A Provide Management Accounting Information Week 1 Chapter 1 COST CONCEPTS FNSACC507A Provide Management Accounting Information By the end of this lesson, you will be able to 1. Explain

Welcome to: FNSACC507A Provide Management Accounting Information Week 1 Chapter 1 COST CONCEPTS FNSACC507A Provide Management Accounting Information By the end of this lesson, you will be able to 1. Explain

FFQA 1. Complied by: Mohammad Faizan Farooq Qadri Attari ACCA (Finalist) Contact:

Contact:") FFQA 1 Objective of IAS 2 The objective of IAS 2 is to prescribe the accounting treatment for inventories. It provides guidance for determining the cost of inventories and for subsequently recognising

FFQA 1 Objective of IAS 2 The objective of IAS 2 is to prescribe the accounting treatment for inventories. It provides guidance for determining the cost of inventories and for subsequently recognising

Part 3 : 11/11/10 07:42:55. MultiFrame Company has the following revenue and cost budgets for the two products it sells.

Question 1 - CMA 1290 4-4 - Decision Making MultiFrame Company has the following revenue and cost budgets for the two products it sells. Plastic Frames Glass Frames Budgeted unit sales 100,000 300,000

Question 1 - CMA 1290 4-4 - Decision Making MultiFrame Company has the following revenue and cost budgets for the two products it sells. Plastic Frames Glass Frames Budgeted unit sales 100,000 300,000

PAPER 5 : COST MANAGEMENT QUESTIONS

Decision Making - Profit Maximization PAPER 5 : COST MANAGEMENT QUESTIONS 1. ABC Co Ltd which produces household electronic gadget HIFY had 90% capacity utilization (4.5 lakh units) current year of Department

Decision Making - Profit Maximization PAPER 5 : COST MANAGEMENT QUESTIONS 1. ABC Co Ltd which produces household electronic gadget HIFY had 90% capacity utilization (4.5 lakh units) current year of Department

CHAPTER 6 PROCESS COST ACCOUNTING ADDITIONAL PROCEDURES

CHAPTER 6 PROCESS COST ACCOUNTING ADDITIONAL PROCEDURES Review Summary 1. In many industries where a process cost system is used, the materials may be put into production in irregular quantities and at

CHAPTER 6 PROCESS COST ACCOUNTING ADDITIONAL PROCEDURES Review Summary 1. In many industries where a process cost system is used, the materials may be put into production in irregular quantities and at

1) Operating costs, such as fuel and labour. 2) Maintenance costs, such as overhaul of engines and spraying.

Operating costs, such as fuel and labour. 2) Maintenance costs, such as overhaul of engines and spraying.") NUMBER ONE QUESTIONS Boni Wahome, a financial analyst at Green City Bus Company Ltd. is examining the behavior of the company s monthly transportation costs for budgeting purposes. The transportation costs

NUMBER ONE QUESTIONS Boni Wahome, a financial analyst at Green City Bus Company Ltd. is examining the behavior of the company s monthly transportation costs for budgeting purposes. The transportation costs

1. The cost of an item is the sacrifice of resources made to acquire it. 2. An expense is a cost charged against revenue in an accounting period.

Chapter 02 Cost Concepts and Behavior True / False Questions 1. The cost of an item is the sacrifice of resources made to acquire it. True False 2. An expense is a cost charged against revenue in an accounting

Chapter 02 Cost Concepts and Behavior True / False Questions 1. The cost of an item is the sacrifice of resources made to acquire it. True False 2. An expense is a cost charged against revenue in an accounting

1. Cost accounting involves the measuring, recording, and reporting of: A. product costs. B. future costs. C. manufacturing processes.

1. Cost accounting involves the measuring, recording, and reporting of: A. product costs. B. future costs. C. manufacturing processes. D. managerial accounting decisions. 2. In accumulating raw materials

1. Cost accounting involves the measuring, recording, and reporting of: A. product costs. B. future costs. C. manufacturing processes. D. managerial accounting decisions. 2. In accumulating raw materials

Section A: Summary Content Notes

COST ACCOUNTING 30 JULY 2015 Section A: Summary Content Notes MANUFACTURING ACCOUNTS: NEW LEDGER ACCOUNTS New Ledger Accounts pertaining to manufacturing concerns are divided into the following categories:

COST ACCOUNTING 30 JULY 2015 Section A: Summary Content Notes MANUFACTURING ACCOUNTS: NEW LEDGER ACCOUNTS New Ledger Accounts pertaining to manufacturing concerns are divided into the following categories:

This is the second in our series of blog posts looking at recording and evaluating costs and revenues (ECR) Unit 6.

Unit 6.") This is the second in our series of blog posts looking at recording and evaluating costs and revenues (ECR) Unit 6. In the last post took a detailed looked at stock in both the simulation and the exam.

This is the second in our series of blog posts looking at recording and evaluating costs and revenues (ECR) Unit 6. In the last post took a detailed looked at stock in both the simulation and the exam.

Paper P2 Management Accounting Decision Management. Examiner s Brief Guide to the Paper 16

May 2005 Examinations Managerial Level Paper P2 Management Accounting Decision Management Question Paper 2 Examiner s Brief Guide to the Paper 16 Examiner s Answers 17 The answers published here have been

May 2005 Examinations Managerial Level Paper P2 Management Accounting Decision Management Question Paper 2 Examiner s Brief Guide to the Paper 16 Examiner s Answers 17 The answers published here have been

P2 Performance Management September 2013 examination

Management Level Paper P2 Performance Management September 2013 examination Examiner s Answers Note: Some of the answers that follow are fuller and more comprehensive than would be expected from a well-prepared

Management Level Paper P2 Performance Management September 2013 examination Examiner s Answers Note: Some of the answers that follow are fuller and more comprehensive than would be expected from a well-prepared

SUPPLY. definition: Supply means the quantity offered for sale by sellers at particular prices, during a certain period of time.

SUPPLY definition: Supply means the quantity offered for sale by sellers at particular prices, during a certain period of time. First factor affecting price is demand. Second factor affecting price is

SUPPLY definition: Supply means the quantity offered for sale by sellers at particular prices, during a certain period of time. First factor affecting price is demand. Second factor affecting price is

CAS -7 COST ACCOUNTING STANDARD ON EMPLOYEE COST

Cost Accounting Standards Board CAS -7 COST ACCOUNTING STANDARD ON EMPLOYEE COST The following is the COST ACCOUNTING STANDARD 7 (CAS - 7) issued by the Council of The Institute of Cost Accountants of

Cost Accounting Standards Board CAS -7 COST ACCOUNTING STANDARD ON EMPLOYEE COST The following is the COST ACCOUNTING STANDARD 7 (CAS - 7) issued by the Council of The Institute of Cost Accountants of

Arrow Ltd manufactures Product Lto which the following information relates. (b) Calculate the margin ofsafety as a % of budgeted sales.

Calculate the margin ofsafety as a % of budgeted sales.") Marginal and absorption costing Illustration 6 - Margin of safety and target profits Arrow Ltd manufactures Product Lto which the following information relates. Selling price per unit Variable cost per

Marginal and absorption costing Illustration 6 - Margin of safety and target profits Arrow Ltd manufactures Product Lto which the following information relates. Selling price per unit Variable cost per

Akuntansi Biaya. Modul ke: 09FEB. Direct Material Cost. Fakultas. Diah Iskandar SE., M.Si dan Nurul Hidayah,SE,Ak,MSi. Program Studi Akuntansi

Modul ke: Akuntansi Biaya Direct Material Cost Fakultas 09FEB Diah Iskandar SE., M.Si dan Nurul Hidayah,SE,Ak,MSi Program Studi Akuntansi Effective Cost Control Specific assignment of duties and responsibilities.

Modul ke: Akuntansi Biaya Direct Material Cost Fakultas 09FEB Diah Iskandar SE., M.Si dan Nurul Hidayah,SE,Ak,MSi Program Studi Akuntansi Effective Cost Control Specific assignment of duties and responsibilities.

Variable Costing: A Tool for Management. M. En C. Eduardo Bustos Farías

Variable Costing: A Tool for Management M. En C. Eduardo Bustos Farías 1 Absorption Costing A system of accounting for costs in which both fixed and variable production costs are considered product costs.

Variable Costing: A Tool for Management M. En C. Eduardo Bustos Farías 1 Absorption Costing A system of accounting for costs in which both fixed and variable production costs are considered product costs.

CHAPTER 4 ACCOUNTING FOR MERCHANDISING OPERATIONS

CHAPTER 4 ACCOUNTING FOR MERCHANDISING OPERATIONS Key Terms and Concepts to Know Income Statements: Single-step income statement Multiple-step income statement Gross Margin = Gross Profit = Net Sales Cost

CHAPTER 4 ACCOUNTING FOR MERCHANDISING OPERATIONS Key Terms and Concepts to Know Income Statements: Single-step income statement Multiple-step income statement Gross Margin = Gross Profit = Net Sales Cost

Cost Behavior. Material Cost: Direct material: 1. seen in the final product 2. economic/visible to trace Indirect Material:

1 Chapter 2 Introduction to Cost Terms and Purposes Cost A cost is the value of economic resources (e.g., money) sacrificed or used up to achieve a particular objective (e.g., produce a product or perform

1 Chapter 2 Introduction to Cost Terms and Purposes Cost A cost is the value of economic resources (e.g., money) sacrificed or used up to achieve a particular objective (e.g., produce a product or perform

rate is used to apply overhead costs to products. Our purpose in this section is to provide a detailed example of cost flows in an ABC system.

Appendix 6A Cost Flows in an -Based Costing System 6A-1 Cost Flows in an -Based Costing System In Chapter 4, we discussed the flow of costs in a job-order costing system. The flow of costs through raw

Appendix 6A Cost Flows in an -Based Costing System 6A-1 Cost Flows in an -Based Costing System In Chapter 4, we discussed the flow of costs in a job-order costing system. The flow of costs through raw

Cost concepts, Cost Classification and Estimation

Cost concepts, Cost Classification and Estimation BY G H A N E N DR A F A G O Cost Concepts Cost refers the amount of expenses spent to generate product or services. Cost refers expenditure that may be

Cost concepts, Cost Classification and Estimation BY G H A N E N DR A F A G O Cost Concepts Cost refers the amount of expenses spent to generate product or services. Cost refers expenditure that may be

Kianoff & Associates Crystal Clear Reports for Sage 100

Kianoff & Associates Crystal Clear Reports for Sage 100 We have developed Crystal Reports for all current versions of Sage 100 and are available for most all modules. Accounts Payable BP801- Vendor File

Kianoff & Associates Crystal Clear Reports for Sage 100 We have developed Crystal Reports for all current versions of Sage 100 and are available for most all modules. Accounts Payable BP801- Vendor File

Part 1 Study Unit 4. Cost Management Concepts Patricia Burnett, CMA Ronald Schmidt, CMA, CFM

Part 1 Study Unit 4 Cost Management Concepts Patricia Burnett, CMA Ronald Schmidt, CMA, CFM 1 Remember most common reasons for missing questions! 1. Misreading the requirement (stem) Read the question

Part 1 Study Unit 4 Cost Management Concepts Patricia Burnett, CMA Ronald Schmidt, CMA, CFM 1 Remember most common reasons for missing questions! 1. Misreading the requirement (stem) Read the question

Introduction to Cost & Management Accounting ACCT 1003(MS 15B)

") UNIVERSITY OF WEST INDIES OPEN CAMPUS Introduction to Cost & Management Accounting ACCT 1003(MS 15B) INVENTORY VALUATION INVENTORY VALUATION & CONTROL At the end of an accounting period, inventory/stock

UNIVERSITY OF WEST INDIES OPEN CAMPUS Introduction to Cost & Management Accounting ACCT 1003(MS 15B) INVENTORY VALUATION INVENTORY VALUATION & CONTROL At the end of an accounting period, inventory/stock

Financial Transfer Guide DBA Software Inc.

Contents 3 Table of Contents 1 Introduction 4 2 Why You Need the Financial Transfer 6 3 Total Control Workflow 10 4 Financial Transfer Overview 12 5 Multiple Operating Entities Setup 15 6 General Ledger

Contents 3 Table of Contents 1 Introduction 4 2 Why You Need the Financial Transfer 6 3 Total Control Workflow 10 4 Financial Transfer Overview 12 5 Multiple Operating Entities Setup 15 6 General Ledger

MANAGERIAL ACCOUNTING. 2 nd topic COST CLASSIFICATION

MANAGERIAL ACCOUNTING 2 nd topic COST CLASSIFICATION Structureofthelecture2 2.1 Definition of cost and related terms 2.2 Types of cost classification 2.3 Identification of cost classification 2.4 Reporting

MANAGERIAL ACCOUNTING 2 nd topic COST CLASSIFICATION Structureofthelecture2 2.1 Definition of cost and related terms 2.2 Types of cost classification 2.3 Identification of cost classification 2.4 Reporting

Govt. Contracting, Dynamics 365 Operations Implementing Dynamics 365 Operations for Govt. Contractors PVBS

Implementing Dynamics 365 Operations for Govt. Contractors PVBS Contents Background... 4 Setups... 4 Project Management and Accounting... 4 Ledger Posting Setup... 4 Category Groups... 4 Category Group

Implementing Dynamics 365 Operations for Govt. Contractors PVBS Contents Background... 4 Setups... 4 Project Management and Accounting... 4 Ledger Posting Setup... 4 Category Groups... 4 Category Group

Activant Prophet 21. Perfecting Your Month and Year End Closing Routines

Activant Prophet 21 Perfecting Your Month and Year End Closing Routines This class is designed for System Administrators Operation Managers Accounting Managers Objectives Suggested month end and year end

Activant Prophet 21 Perfecting Your Month and Year End Closing Routines This class is designed for System Administrators Operation Managers Accounting Managers Objectives Suggested month end and year end

UNIT 2 : FINAL ACCOUNTS OF MANUFACTURING ENTITIES

7.63 UNIT 2 : FINAL ACCOUNTS OF MANUFACTURING ENTITIES LEARNING OUTCOMES After studying this unit, you will be able to: Understand the purpose of preparing Manufacturing Account. Learn the items to be

7.63 UNIT 2 : FINAL ACCOUNTS OF MANUFACTURING ENTITIES LEARNING OUTCOMES After studying this unit, you will be able to: Understand the purpose of preparing Manufacturing Account. Learn the items to be

JOINT UNIVERSITIES PRELIMINARY EXAMINATIONS BOARD 2015 EXAMINATIONS BUSSINESS STUDIES - MSS J132 MULTIPLE CHOICE QUESTIONS

JOINT UNIVERSITIES PRELIMINARY EXAMINATIONS BOARD 2015 EXAMINATIONS BUSSINESS STUDIES - MSS J132 MULTIPLE CHOICE QUESTIONS 1. What do the letters EOQ stand for? A. Estimated Order Quantity B. Economic

JOINT UNIVERSITIES PRELIMINARY EXAMINATIONS BOARD 2015 EXAMINATIONS BUSSINESS STUDIES - MSS J132 MULTIPLE CHOICE QUESTIONS 1. What do the letters EOQ stand for? A. Estimated Order Quantity B. Economic

Sri Lanka Accounting Standard-LKAS 2. Inventories

Sri Lanka Accounting Standard-LKAS 2 Inventories CONTENTS paragraphs SRI LANKA ACCOUNTING STANDARD-LKAS 2 INVENTORIES OBJECTIVE 1 SCOPE 2 5 DEFINITIONS 6 8 MEASUREMENT OF INVENTORIES 9 33 Cost of inventories

Sri Lanka Accounting Standard-LKAS 2 Inventories CONTENTS paragraphs SRI LANKA ACCOUNTING STANDARD-LKAS 2 INVENTORIES OBJECTIVE 1 SCOPE 2 5 DEFINITIONS 6 8 MEASUREMENT OF INVENTORIES 9 33 Cost of inventories

PART ONE OF A TWO PART PAPER QUESTION BOOKLET

PART ONE OF A TWO PART PAPER QUESTION BOOKLET 22 November 2010 FNSACCT613A/B Prepare and Analyse Management Accounting Information Aids to be supplied by college: None. Instructions to students: Time allowed

PART ONE OF A TWO PART PAPER QUESTION BOOKLET 22 November 2010 FNSACCT613A/B Prepare and Analyse Management Accounting Information Aids to be supplied by college: None. Instructions to students: Time allowed

Chapter 2. Job Order Costing and Analysis QUESTIONS

Chapter 2 Job Order Costing and Analysis QUESTIONS 1. Factory overhead is not identified with specific units (jobs) or batches (job lots). Therefore, to assign costs, estimates of the relation between

Chapter 2 Job Order Costing and Analysis QUESTIONS 1. Factory overhead is not identified with specific units (jobs) or batches (job lots). Therefore, to assign costs, estimates of the relation between

NORTH MAHARASHTRA UNIVERSITY, JALGAON (NAAC Re-accredited B Grade {CGPA 2.88})

") NORTH MAHARASHTRA UNIVERSITY, JALGAON (NAAC Re-accredited B Grade {CGPA 2.88}) FACULTY OF COMMERCE & MANAGEMENT New Syllabus: M.Com (w.e.f. June 2014) SEMESTER : I Specialization Paper : I 104 (B) Advanced

NORTH MAHARASHTRA UNIVERSITY, JALGAON (NAAC Re-accredited B Grade {CGPA 2.88}) FACULTY OF COMMERCE & MANAGEMENT New Syllabus: M.Com (w.e.f. June 2014) SEMESTER : I Specialization Paper : I 104 (B) Advanced

Activity-Based Costing Systems

4 Activity-Based Costing Systems 4-2 Learning Objective 1 4-3 Traditional Costing Systems Traditional cost systems were created when manufacturing processes were labor intensive. A single company-wide

4 Activity-Based Costing Systems 4-2 Learning Objective 1 4-3 Traditional Costing Systems Traditional cost systems were created when manufacturing processes were labor intensive. A single company-wide

Chapter 6 Process Costing

Chapter 6: Process Costing 239 Chapter 6 Process Costing LEARNING OBJECTIVES Chapter 6 addresses the following questions: LO1 LO2 LO3 LO4 LO5 Assign costs to mass-produced products using equivalent units

Chapter 6: Process Costing 239 Chapter 6 Process Costing LEARNING OBJECTIVES Chapter 6 addresses the following questions: LO1 LO2 LO3 LO4 LO5 Assign costs to mass-produced products using equivalent units

Chapter 2--Measuring Product Costs

Chapter 2--Measuring Product Costs Student: 1. Which of the following is notone of the three major manufacturing cost categories? A. Direct materials costs that can be easily traced to a product B. Direct

Chapter 2--Measuring Product Costs Student: 1. Which of the following is notone of the three major manufacturing cost categories? A. Direct materials costs that can be easily traced to a product B. Direct

Chapter 17 Job Order Costing Study Guide Solutions Fill-in-the-Blank Equations. Exercises. 1. Estimated activity base. 2. Underapplied. 3.

Chapter 17 Job Order Costing Study Guide Solutions Fill-in-the-Blank Equations 1. Estimated activity base 2. Underapplied 3. Overapplied Exercises 1. An automobile manufacturer produces various lines of

Chapter 17 Job Order Costing Study Guide Solutions Fill-in-the-Blank Equations 1. Estimated activity base 2. Underapplied 3. Overapplied Exercises 1. An automobile manufacturer produces various lines of

Test 1 Multiple Choice Questions. F5 - Performance Management

Test 1 Multiple Choice Questions F5 - Performance Management Mr. Ghan Shyam Dubey Name - Student ID - E-mail ID - Please write answers in the below given column. Question No. 1. 2. 3. 4. 5. 6. 7. 8. 9.

Test 1 Multiple Choice Questions F5 - Performance Management Mr. Ghan Shyam Dubey Name - Student ID - E-mail ID - Please write answers in the below given column. Question No. 1. 2. 3. 4. 5. 6. 7. 8. 9.

Level II Foundation Certificate in Accounting

Level II Foundation Certificate in Accounting Who should choose to study this qualification? The AAT Foundation Certificate in Accounting is an ideal starting point for anyone looking to pursue a career

Level II Foundation Certificate in Accounting Who should choose to study this qualification? The AAT Foundation Certificate in Accounting is an ideal starting point for anyone looking to pursue a career

15.4 Income Statement under Marginal Costing and Absorption Costing

UNIT 15 Structure MARGINAL COSTING 15.0 Objectives 15.1 Introduction 15.2 Segregation of Mixed Costs 15.3 Concept of Marginal Cost and Marginal Costing 15.4 Income Statement under Marginal Costing and

UNIT 15 Structure MARGINAL COSTING 15.0 Objectives 15.1 Introduction 15.2 Segregation of Mixed Costs 15.3 Concept of Marginal Cost and Marginal Costing 15.4 Income Statement under Marginal Costing and

Sri Lanka Accounting Standard LKAS 2. Inventories

Sri Lanka Accounting Standard LKAS 2 Inventories CONTENTS paragraphs SRI LANKA ACCOUNTING STANDARD LKAS 2 INVENTORIES OBJECTIVE 1 SCOPE 2 5 DEFINITIONS 6 8 MEASUREMENT OF INVENTORIES 9 33 Cost of inventories

Sri Lanka Accounting Standard LKAS 2 Inventories CONTENTS paragraphs SRI LANKA ACCOUNTING STANDARD LKAS 2 INVENTORIES OBJECTIVE 1 SCOPE 2 5 DEFINITIONS 6 8 MEASUREMENT OF INVENTORIES 9 33 Cost of inventories

Overview. This Accounting Standard is aimed to streamline the accounting methods for inventories.

IAS 2 INVENTORIES Overview This Accounting Standard is aimed to streamline the accounting methods for inventories. The foremost concern in Inventory accounting is that the cost would be considered as asset

IAS 2 INVENTORIES Overview This Accounting Standard is aimed to streamline the accounting methods for inventories. The foremost concern in Inventory accounting is that the cost would be considered as asset

P2 Performance Management September 2012 examination

Management Level Paper P2 Performance Management September 2012 examination Examiner s Answers Note: Some of the answers that follow are fuller and more comprehensive than would be expected from a well-prepared

Management Level Paper P2 Performance Management September 2012 examination Examiner s Answers Note: Some of the answers that follow are fuller and more comprehensive than would be expected from a well-prepared

Pricing Decisions & Profitability Analysis

Pricing Decisions & Profitability Analysis Economic theory The optimum selling price is the price at which marginal revenue equals marginal cost. 1 Problems with applying economic theory 1. Difficult and

Pricing Decisions & Profitability Analysis Economic theory The optimum selling price is the price at which marginal revenue equals marginal cost. 1 Problems with applying economic theory 1. Difficult and

Chapter 3--Product Costing: Manufacturing Processes, Cost Terminology, and Cost Flows

Chapter 3--Product Costing: Manufacturing Processes, Cost Terminology, and Cost Flows Student: 1. Which of the following types of organizations is most likely to have a raw materials inventory account?

Chapter 3--Product Costing: Manufacturing Processes, Cost Terminology, and Cost Flows Student: 1. Which of the following types of organizations is most likely to have a raw materials inventory account?

Business Strategy. AIS Applications

PART III Figure 1 A Framework for Studying AIS TRANSACTION CYCLES AND ACCOUNTING APPLICATIONS In Part I of the text we developed a conceptual foundation for understanding AIS in terms of business processes.

PART III Figure 1 A Framework for Studying AIS TRANSACTION CYCLES AND ACCOUNTING APPLICATIONS In Part I of the text we developed a conceptual foundation for understanding AIS in terms of business processes.

Understanding the meaning of Learning Curve. Understanding the meaning of Learning Curve Effect. Feature and Limitations of Learning Curve Theory.

C H A P T E R 15 Learning Curve Learning Objectives: Understanding the meaning of Learning Curve. Understanding the meaning of Learning Curve Effect. Feature and Limitations of Learning Curve Theory. Past

C H A P T E R 15 Learning Curve Learning Objectives: Understanding the meaning of Learning Curve. Understanding the meaning of Learning Curve Effect. Feature and Limitations of Learning Curve Theory. Past

CHAPTER 6. Inventory Costing. Brief Questions Exercises Exercises 4, 5, 6, 7 3, 4, *14 3, 4, 5, 6, *12, *13 7, 8, 9, 10, 11, 12, 13

CHAPTER 6 Inventory Costing ASSIGNMENT CLASSIFICATION TABLE Study Objectives Brief Questions Exercises Exercises Problems Set A Problems Set B 1. Describe the steps in determining inventory quantities.

CHAPTER 6 Inventory Costing ASSIGNMENT CLASSIFICATION TABLE Study Objectives Brief Questions Exercises Exercises Problems Set A Problems Set B 1. Describe the steps in determining inventory quantities.

Total incremental costs of making in-house 313,100. Cost of buying (80,000 x $4 10/$4 30) 328,000 Total saving from making 14,900

328,000 Total saving from making 14,900") Answers Fundamentals Level Skills Module, Paper F5 Performance Management June 2012 Answers 1 (a) Keypads Display screens Variable costs $ $ Materials ($160k x 6/12) + ($160k x 1 05 x 6/12) 164,000 ($116k

Answers Fundamentals Level Skills Module, Paper F5 Performance Management June 2012 Answers 1 (a) Keypads Display screens Variable costs $ $ Materials ($160k x 6/12) + ($160k x 1 05 x 6/12) 164,000 ($116k

FEEDBACK TUTORIAL LETTER

FEEDBACK TUTORIAL LETTER 1 st SEMESTER 2017 ASSIGNMENT 2 COST AND MANAGEMENT ACCOUNTING 3A CMA311S 1 ASSIGNMENT 02 SOLUTIONS QUESTION 1 a) Order Cost 56,250 = 50 orders 1,125 = 50 x $10 = $500 (25 Marks)

FEEDBACK TUTORIAL LETTER 1 st SEMESTER 2017 ASSIGNMENT 2 COST AND MANAGEMENT ACCOUNTING 3A CMA311S 1 ASSIGNMENT 02 SOLUTIONS QUESTION 1 a) Order Cost 56,250 = 50 orders 1,125 = 50 x $10 = $500 (25 Marks)

6. Refer to the Michael's Manufacturing, Inc. information above. Raw materials used for July is:

Review II NUMBER 1. Which of the following is a characteristic of managerial accounting? a. It is used primarily by external users. b. It often lacks flexibility. c. It is often future-oriented. d. The

Review II NUMBER 1. Which of the following is a characteristic of managerial accounting? a. It is used primarily by external users. b. It often lacks flexibility. c. It is often future-oriented. d. The

Product Costing: Analyze the Financial Entries in Make-to-Stock. Birgit Starmanns SAP Marketing

Product Costing: Analyze the Financial Entries in Make-to-Stock Birgit Starmanns SAP Marketing Agenda Financial Excellence with SAP Solutions The End-to-End Process Plan to Manufacture: The Process Introduction

Product Costing: Analyze the Financial Entries in Make-to-Stock Birgit Starmanns SAP Marketing Agenda Financial Excellence with SAP Solutions The End-to-End Process Plan to Manufacture: The Process Introduction

Copyright ownership: United Business Services (Aust) Pty Ltd.

Pty Ltd.") Assessment Tasks Candidate Guide BSBSMB402A Plan small business finances Copyright ownership: United Business Services (Aust) Pty Ltd. This book is copyright protected under the Berne Convention. All rights

Assessment Tasks Candidate Guide BSBSMB402A Plan small business finances Copyright ownership: United Business Services (Aust) Pty Ltd. This book is copyright protected under the Berne Convention. All rights

Chapter 5 Job Costing

Chapter 5: Job Costing 203 Chapter 5 Job Costing LEARNING OBJECTIVES Chapter 5 addresses the following questions: LO1 LO2 LO3 LO4 LO5 LO6 Explain product costs and cost flows through the manufacturing

Chapter 5: Job Costing 203 Chapter 5 Job Costing LEARNING OBJECTIVES Chapter 5 addresses the following questions: LO1 LO2 LO3 LO4 LO5 LO6 Explain product costs and cost flows through the manufacturing

SELF ASSESSMENT PROBLEMS

CHAPTER2 MATERIALS COST SELF ASSESSMENT PROBLEMS LEVELS OF INVENTORY Q67: Two components, A and B are used as follows: Normal Usage 50 units per week each Minimum Usage 25 units per week each Maximum Usage

CHAPTER2 MATERIALS COST SELF ASSESSMENT PROBLEMS LEVELS OF INVENTORY Q67: Two components, A and B are used as follows: Normal Usage 50 units per week each Minimum Usage 25 units per week each Maximum Usage

End of Month Processing

End of Month Processing Ver 040510 Overview: Each of the MAS accounting modules, excluding Bill of Lading, Packaging, Custom Office, Library Master and Report Master require a closing process at or near

End of Month Processing Ver 040510 Overview: Each of the MAS accounting modules, excluding Bill of Lading, Packaging, Custom Office, Library Master and Report Master require a closing process at or near

ACCOUNTING FOR MERCHANDISING ACTIVITIES

Chapter 6 ACCOUNTING FOR MERCHANDISING ACTIVITIES Presented by: Endra M. Sagoro Economic Faculty YSU endra_ms@uny.ac.id Operating Cycle of a Merchandising Company Cash Accounts Receivable 2. Sale of merchandise

Chapter 6 ACCOUNTING FOR MERCHANDISING ACTIVITIES Presented by: Endra M. Sagoro Economic Faculty YSU endra_ms@uny.ac.id Operating Cycle of a Merchandising Company Cash Accounts Receivable 2. Sale of merchandise

Pre-typeset final version

Pearson LCCI Level 3 Certificate in Cost and Management Accounting Examination Paper Sample assessment material for first teaching January 2015 Time: 3 hours You do not need any other materials. Total

Pearson LCCI Level 3 Certificate in Cost and Management Accounting Examination Paper Sample assessment material for first teaching January 2015 Time: 3 hours You do not need any other materials. Total

Pass4Sure.C_TERP10_65 (85Q) C_TERP10_65. SAP Certified - Associate Business Foundation & Integration with SAP ERP 6.0 EHP5

C_TERP10_65. SAP Certified - Associate Business Foundation & Integration with SAP ERP 6.0 EHP5") Pass4Sure.C_TERP10_65 (85Q) Number: C_TERP10_65 Passing Score: 800 Time Limit: 120 min File Version: 4.4 C_TERP10_65 SAP Certified - Associate Business Foundation & Integration with SAP ERP 6.0 EHP5 A)

Pass4Sure.C_TERP10_65 (85Q) Number: C_TERP10_65 Passing Score: 800 Time Limit: 120 min File Version: 4.4 C_TERP10_65 SAP Certified - Associate Business Foundation & Integration with SAP ERP 6.0 EHP5 A)

JOB ORDER COSTING. LO 1: Cost Systems. Determine whether job order costing or process costing would be more appropriate for each industry.

JOB ORDER COSTING Terms Cost Accounting Process Cost System Job Order Cost System LO 1: Cost Systems Job-Order Costing Used for custom or unique items Each job is accounted for separately Measures cost

JOB ORDER COSTING Terms Cost Accounting Process Cost System Job Order Cost System LO 1: Cost Systems Job-Order Costing Used for custom or unique items Each job is accounted for separately Measures cost

Association of Accounting Technicians

Association of Accounting Technicians Basic Costing Level 2 Published by: Home Learning College 1 Hammersmith Broadway London W6 9DL Home Learning College Ltd 2013 Version 2.0 aat2_bcst_v2_170315 All

Association of Accounting Technicians Basic Costing Level 2 Published by: Home Learning College 1 Hammersmith Broadway London W6 9DL Home Learning College Ltd 2013 Version 2.0 aat2_bcst_v2_170315 All

PURCHASING AND JOB COSTING FOR CONTRACTORS. Leslie Shiner Owner, Principal of The ShinerGroup

PURCHASING AND JOB COSTING FOR CONTRACTORS Leslie Shiner Owner, Principal of The ShinerGroup Leslie Shiner The ShinerGroup - Owner and Principal Financial & Management Consultant for Contractors MBA in

PURCHASING AND JOB COSTING FOR CONTRACTORS Leslie Shiner Owner, Principal of The ShinerGroup Leslie Shiner The ShinerGroup - Owner and Principal Financial & Management Consultant for Contractors MBA in

Indian Accounting Standard (Ind AS) 2 Inventories

2 Inventories") Indian Accounting Standard (Ind AS) 2 Inventories Indian Accounting Standard (Ind AS) 2, Inventories, prescribes the accounting treatment for inventories, such as, determination of cost and its subsequent

Indian Accounting Standard (Ind AS) 2 Inventories Indian Accounting Standard (Ind AS) 2, Inventories, prescribes the accounting treatment for inventories, such as, determination of cost and its subsequent

Answer to MTP_Intermediate_Syllabus 2012_Jun2017_Set 1 Paper 10- Cost & Management Accountancy

Paper 10- Cost & Management Accountancy Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 10- Cost & Management Accountancy Full

Paper 10- Cost & Management Accountancy Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 10- Cost & Management Accountancy Full

The Best CA IPC COST SUMMARY THEORY BOOK FOR NOV hshshhhh. "Winners don t do different things, they do things differently"

The Best CA IPC COST SUMMARY THEORY BOOK FOR NOV. 2017 In the World of Darkness, I Let There Be Light! hshshhhh "Winners don t do different things, they do things differently" CA Purushottam Aggarwal SIR

The Best CA IPC COST SUMMARY THEORY BOOK FOR NOV. 2017 In the World of Darkness, I Let There Be Light! hshshhhh "Winners don t do different things, they do things differently" CA Purushottam Aggarwal SIR

Oracle Hospitality Reporting and Analytics Advanced

Oracle Hospitality Reporting and Analytics Advanced User Guide Release 8.5.0 E65823-01 September 2015 Oracle Hospitality Reporting and Analytics Advanced User Guide, Release 8.5.0 E65823-01 Copyright 2000,

Oracle Hospitality Reporting and Analytics Advanced User Guide Release 8.5.0 E65823-01 September 2015 Oracle Hospitality Reporting and Analytics Advanced User Guide, Release 8.5.0 E65823-01 Copyright 2000,

COST OF GOODS MANUFACTURES B.COM. PART II

COST OF GOODS MANUFACTURES B.COM. PART II Q#1 Following are the balances appear on the Trial Balance of SAMREEN & Co. for the year ended April 30, 1980. Inventory of Goods in Process April, 01 Rs.109,000

COST OF GOODS MANUFACTURES B.COM. PART II Q#1 Following are the balances appear on the Trial Balance of SAMREEN & Co. for the year ended April 30, 1980. Inventory of Goods in Process April, 01 Rs.109,000

COST COST OBJECT. Cost centre. Profit centre. Investment centre

COST The amount of money or property paid for a good or service. Cost is an expense for both personal and business assets. If a cost is for a business expense, it may be tax deductible. A cost may be paid

COST The amount of money or property paid for a good or service. Cost is an expense for both personal and business assets. If a cost is for a business expense, it may be tax deductible. A cost may be paid

: ACCA Paper F8. Audit and Assurance. Your Contact Number :

Mock Examination : ACCA Paper F8 Audit and Assurance Session : June 2014 Set by : Mr Neil Han Your Contact Number : I wish to have my script marked by the lecturer and collect the marked script at the

Mock Examination : ACCA Paper F8 Audit and Assurance Session : June 2014 Set by : Mr Neil Han Your Contact Number : I wish to have my script marked by the lecturer and collect the marked script at the

PAYROLL ACCOUNTING (125) Secondary

Secondary") Page 1 of 7 Contestant Number: Time: Rank: PAYROLL ACCOUNTING (125) Secondary REGIONAL 2017 Multiple Choice & Short Answer Section: Multiple Choice (15 @ 2 points each) Short Answers (10 @ 2 points each)

Page 1 of 7 Contestant Number: Time: Rank: PAYROLL ACCOUNTING (125) Secondary REGIONAL 2017 Multiple Choice & Short Answer Section: Multiple Choice (15 @ 2 points each) Short Answers (10 @ 2 points each)

JOB COSTING AND OVERHEAD

JOB COSTING AND OVERHEAD Key Topics to Know Differences and similarities between job order and process costing Key document is the Job Cost Sheet Flow of product costs through inventory accounts to cost

JOB COSTING AND OVERHEAD Key Topics to Know Differences and similarities between job order and process costing Key document is the Job Cost Sheet Flow of product costs through inventory accounts to cost

INTRODUCTION. Professional Accounting Supplementary School (PASS) Page 1

Page 1") INTRODUCTION Under the new CPA certification program, management accounting has become very important on the CFE and it will therefore be critical for students to have a strong grounding in this area.

INTRODUCTION Under the new CPA certification program, management accounting has become very important on the CFE and it will therefore be critical for students to have a strong grounding in this area.

Similarities Between Job-Order and Process Costing

Similarities Between Job-Order and Process Costing 4-1 Both systems assign material, labor, and overhead costs to products and they provide a mechanism for computing unit product costs. Both systems use

Similarities Between Job-Order and Process Costing 4-1 Both systems assign material, labor, and overhead costs to products and they provide a mechanism for computing unit product costs. Both systems use

Chapter 2 Cost Terms, Concepts, and Classifications

Multiple Choice Questions 16. Indirect labor is a part of: A) Prime cost. B) Conversion cost. C) Period cost. D) Nonmanufacturing cost. Answer: B Level: Medium LO: 1,2 Source: CPA, adapted 17. The cost

Multiple Choice Questions 16. Indirect labor is a part of: A) Prime cost. B) Conversion cost. C) Period cost. D) Nonmanufacturing cost. Answer: B Level: Medium LO: 1,2 Source: CPA, adapted 17. The cost

Visual Cash Focus - User Tip 32

Visual Cash Focus - User Tip 32 How do I model Work in Progress and Finished Goods? How to model WIP in service based organisations How to model WIP and Finished Goods for manufacturers and producers The

Visual Cash Focus - User Tip 32 How do I model Work in Progress and Finished Goods? How to model WIP in service based organisations How to model WIP and Finished Goods for manufacturers and producers The

MOJAKOE AKUNTASI BIAYA

Presented by : Accounting Study Division MoJaKoe Akuntansi Biaya MOJAKOE AKUNTASI BIAYA UAS AB 2012/2013 ACCOUNTING STUDY DIVISION DILARANG memperbanyak MOJAKOE ini tanpa seijin SPA FEUI. Download MOJAKOE

Presented by : Accounting Study Division MoJaKoe Akuntansi Biaya MOJAKOE AKUNTASI BIAYA UAS AB 2012/2013 ACCOUNTING STUDY DIVISION DILARANG memperbanyak MOJAKOE ini tanpa seijin SPA FEUI. Download MOJAKOE

CMS Notes Lecture 1 Management vs. financial accounting Management accounting internal Financial accounting external