THIRD-PARTY RISK MANAGEMENT

|

|

|

- Virginia Clarke

- 6 years ago

- Views:

Transcription

1 THIRD-PARTY RISK MANAGEMENT Beyond a Regulatory Requirement April 28, 2017 Ken Glascock, CPA, CAMS, CIA, CFSA, CRCM Director kglascock@bkd.com

2 AGENDA Let s Break It Down What Is Third-Party Risk Management? It s Just for Big Institutions, Right? Why You Need a Third-Party Risk Management Program Regulatory Requirements Are the Right People Involved? It s Not Just an IT Responsibility Common Pitfalls in Third-Party Risk Management Programs Best Practices

3 What Is Third-Party Risk Management? Let s Break It Down

4 LET S BREAK IT DOWN What Is a Third Party? More than just IT services More than just critical vendors Formal Definition How to Identify All Third Parties

5 LET S BREAK IT DOWN What Is Risk Management? Process of Assessing Measuring Monitoring Controlling

6 Why You Need a Third-Party Risk Management Program It s Just for Big Institutions, Right?

7 IT S JUST FOR BIG INSTITUTIONS, RIGHT? No size threshold For all institutions using third parties Applicable to all third-party arrangements

8 WHY YOU NEED A THIRD-PARTY RISK MANAGEMENT PROGRAM

Regulatory requirement Evaluate whether")

9 WHY YOU NEED A THIRD-PARTY RISK MANAGEMENT PROGRAM Lack of control of process (increased risk) Regulatory requirement Evaluate whether capital is sufficient to support risk exposures think AIG in the great recession Evaluate whether third party is doing its job properly

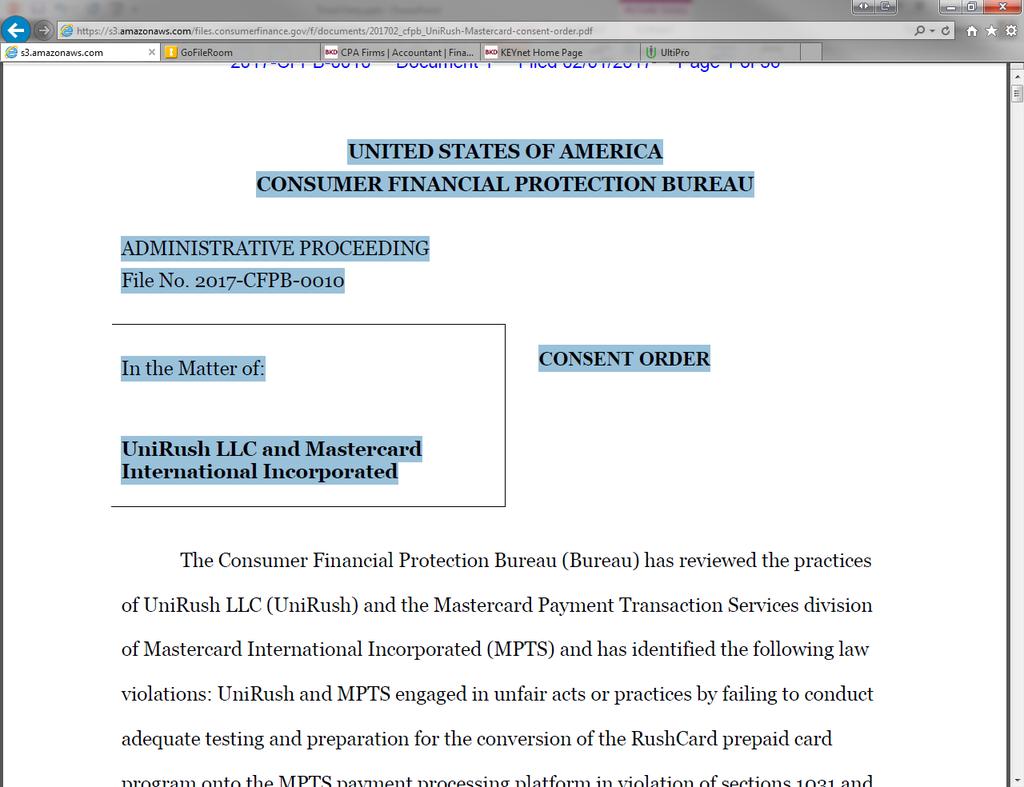

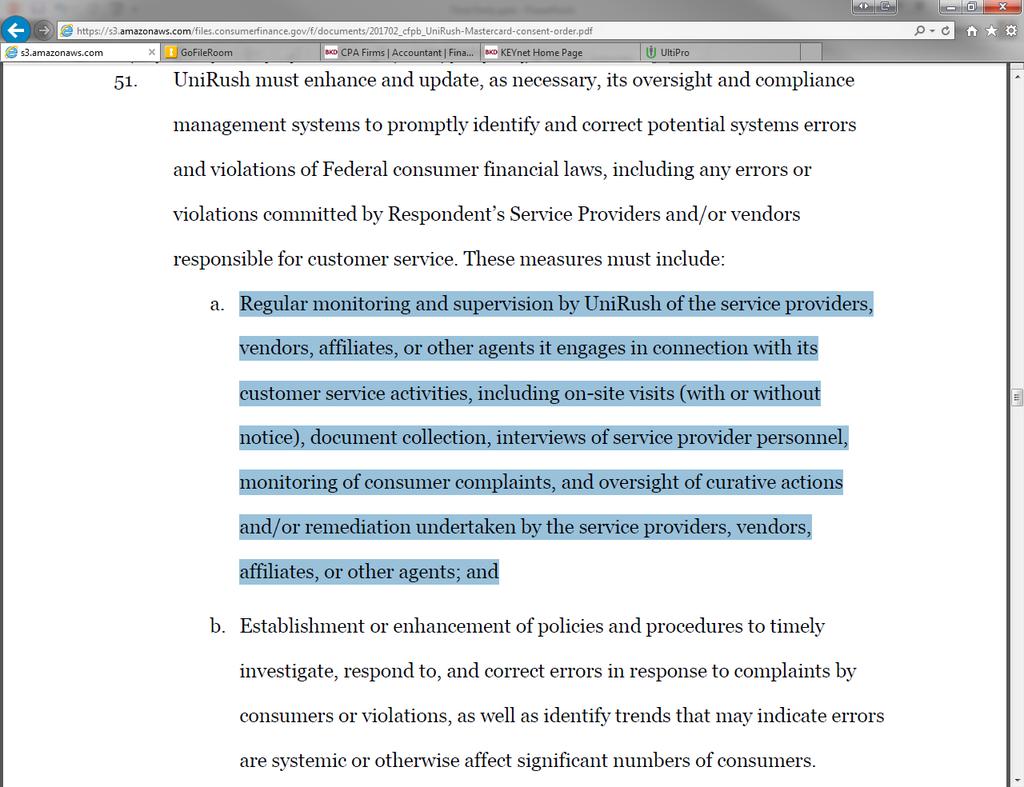

10 OUTSOURCING CASE STUDY Unirush, LLC and MasterCard International

11 CFPB ORDERS MASTERCARD AND UNIRUSH, LLC TO PAY $13 MILLION RushCard breakdowns cut off consumers access to funds Preventable failures left tens of thousands of economically vulnerable consumers unable to pay for necessitates Many customers could not use their RushCard to get their paychecks and other direct deposits, take out cash, make purchases, pay bills or get accurate balance information

12

13

14

15 Regulatory Requirements

16 POTENTIAL REGULATORS NCUA OCC FDIC Federal Reserve FFIEC CFPB

17 NCUA SUPERVISORY LETTER NO.: 07-01, 10/2007 Evaluating Third Party Relationships Ultimately, credit unions are responsible for safeguarding member assets and ensuring sound operations irrespective of whether or not a third party is involved. Risks may be mitigated, transferred, avoided, or accepted; however, they are rarely eliminated.

18 NCUA SUPERVISORY LETTER (CONT.) Exposure to full range of risks: Credit Interest rate Liquidity Transaction Compliance Strategic Reputation

19 NCUA SUPERVISORY LETTER (CONT.) Credit unions must complete the due diligence necessary to ensure the risks undertaken in a third party relationship are acceptable in relation to their risk profile and safety and soundness requirements.

Risk Assessment Credit unions should complete a risk assessment prior to engaging in a third party relationship to")

20 NCUA SUPERVISORY LETTER (CONT.) Risk Assessment Credit unions should complete a risk assessment prior to engaging in a third party relationship to assess what internal changes, if any, will be required to safely and soundly participate.

21 NCUA SUPERVISORY LETTER (CONT.) Risk Assessment consider all seven risk areas and specifically: Expectations for Outsourced Functions Staff Expertise Criticality Risk-Reward or Cost-Benefit Relationship Insurance Impact on Membership Exit Strategy

22 NCUA SUPERVISORY LETTER (CONT.) Due Diligence Background Check Business Model Cash Flows Financial and Operational Control Review Contract Issues and Legal Review Accounting Considerations

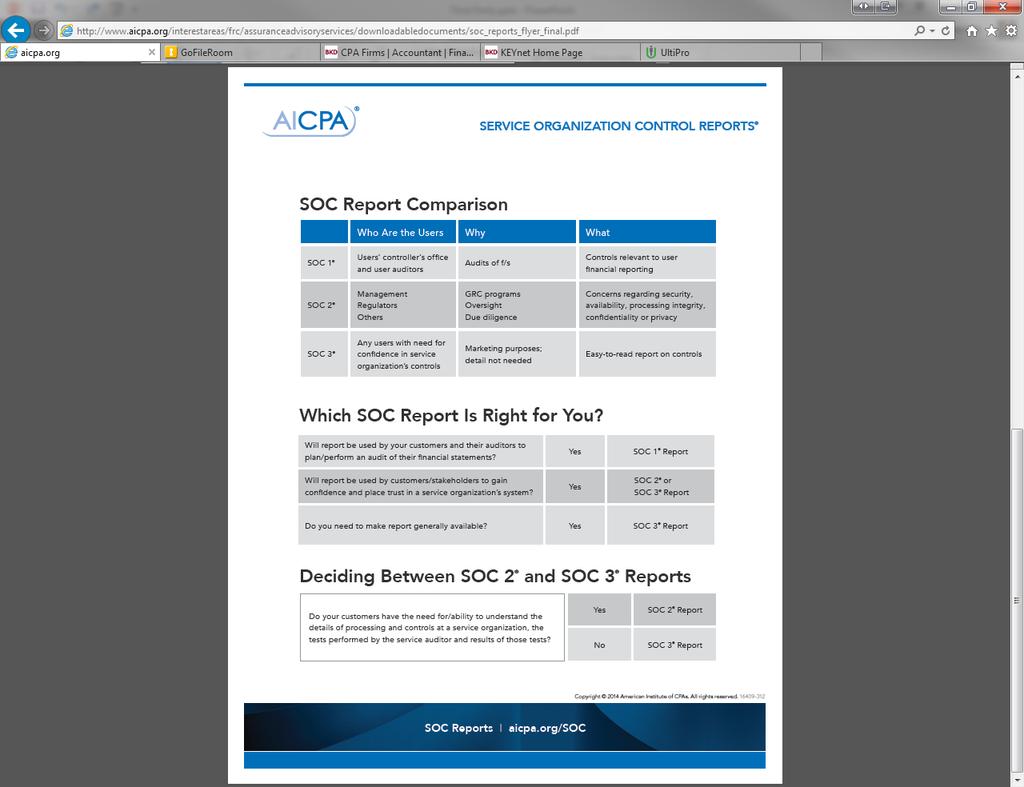

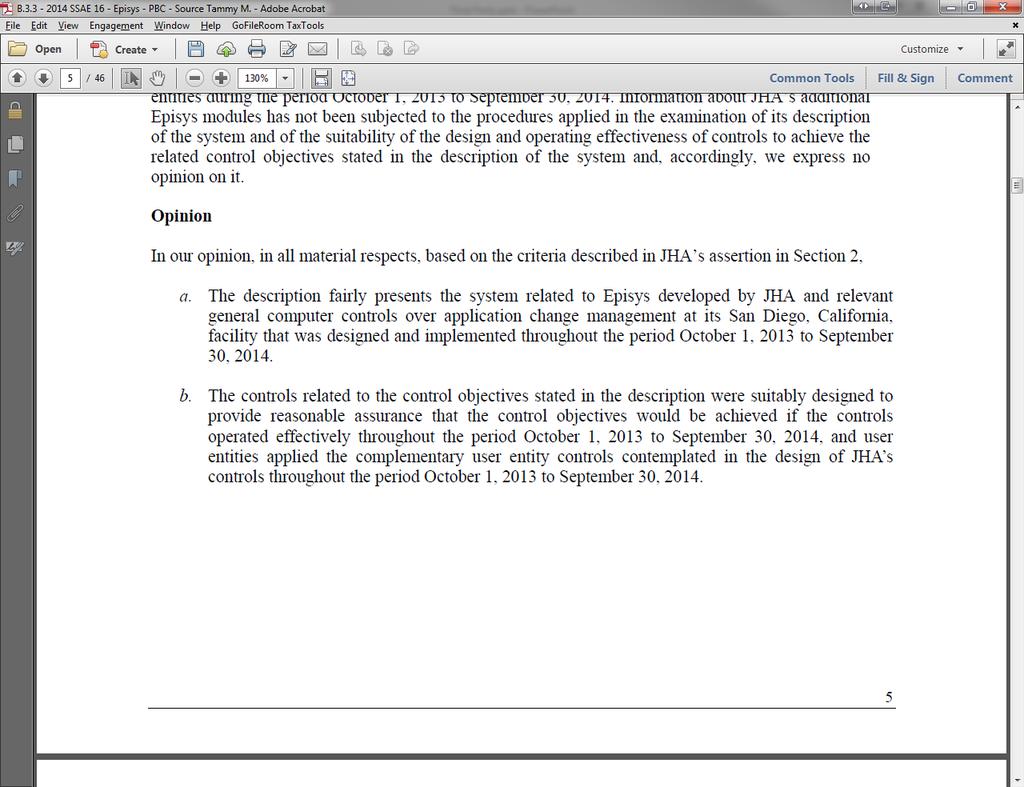

23 AUDIT REPORTS SAS70 SSAE16 SSAE18 SOC I-III Type I-II

24

25 AUDIT REPORTS (CONT.) Effective May 1, 2017: SOC Reports will now be issued under SSAE 18 (AT-C Section 320) SSAE 18 replaces SSAE 10-14, 16 & 17 SSAE 18 covers all attestation engagements Refer to reports by their individual names (i.e., SOC1, SOC2 and SOC3), and not SSAE 18

26 SSAE 18 - IMPACT TO SERVICE ORGANIZATIONS AND USER ENTITIES Monitoring the effectiveness of internal controls at subservice organizations Service organizations must implement sufficient controls to monitor the relevant controls at their subservice organizations Assess the risk of material misstatement and perform procedures in response to those risks, i.e., perform a risk assessment Under SSAE 18, service auditors are instructed to better identify potential areas of risk specifically in regards to material misstatement

27 SSAE 18 - IMPACT TO SERVICE ORGANIZATIONS AND USER ENTITIES (CONT.) Complimentary subservice organization controls and modifications to management s assertion SSAE 18 introduces an additional requirement to include complementary subservice organization controls in SOC reports Evaluating the reliability of evidence produced by the service organization SSAE 18 clarifies the requirements to ensure that evidence provided by service organizations is complete, accurate and sufficiently detailed. The management assertion must be signed by management of the company.

28

29

30 NCUA SUP. LETTER (CONT.) CONTRACT ISSUES Scope of arrangement, services offered and activities authorized Responsibilities of all parties Service level agreements Performance reports Penalties for lack of performance Ownership, control, maintenance and access Ownership of servicing rights Audit rights and requirements Data security and member confidentiality Business resumption or contingency planning Insurance Member complaints and member service Compliance with regulatory requirements Dispute resolution Default, termination and escape clauses

31 NCUA SUPERVISORY LETTER (CONT.) Since credit unions may ultimately be responsible for consumer compliance violations committed by their agents, credit unions should be familiar with the third party s internal controls for ensuring regulatory compliance and adherence to agreed upon practices.

32 NCUA SUPERVISORY LETTER (CONT.) Risk Measurement, Monitoring and Control of Third Party Relationships Policies and Procedures Risk Measurement and Monitoring Control Systems and Reporting

33 The CFPB expects supervised banks and nonbanks to have an effective process for managing the risks of service provider relationships CFPB Bulletin

34 To limit the potential for statutory or regulatory violations and related consumer harm, supervised banks and nonbanks should take steps to ensure that their business arrangements with service providers do not present unwarranted risks to consumers CFPB Bulletin

35 CFPB & CREDIT UNIONS CFPB Orders Navy Federal Credit Union to Pay $28.5 Million for Improper Debt Collection Actions Credit Union Used False Threats to Collect Debts and Placed Unfair Restrictions on Account Access - OCT 11, 2016

36 FFIEC Outsourcing Technology Services Supervision of Technology Service Providers

37

38

39 OCC Comptroller s Handbooks Asset Management Other Real Estate Owned Internal and External Audits Merchant Processing Retail Nondeposit Investment Sales Etc.

40 A bank should adopt risk management processes commensurate with the level of risk and complexity of its third-party relationships OCC Bulletin , Third-Party Relationships

41 the OCC expects more comprehensive and rigorous oversight and management of third-party relationships that involve critical activities significant bank functions (e.g., payments, clearing, settlements, custody) or significant shared services (e.g., information technology) OCC Bulletin , Third-Party Relationships

42 Appropriately managed third-party relationships can enhance competitiveness, provide diversification, and ultimately strengthen the safety and soundness of insured institutions. Third-party arrangements can also help institutions attain key strategic objectives FDIC s Summer 2011 Supervisory Insights

43 A third-party relationship should be considered significant if the institution s relationship with the third party is a new relationship or involves implementing new bank activities FDIC Financial Institution Letter , Guidance for Managing Third-Party Risk

44 A community banking organization may have critical activities being outsourced, but the number may be few and to highly reputable service providers. Therefore, the risk management program may be simpler and use less elements and considerations Federal Reserve SR 13-19, Guidance on Managing Outsourcing Risk

45 As the service provider represents the institution by selling products or services on its behalf, the institution should consider whether the incentives provided might encourage the service provider to take imprudent risks Federal Reserve SR 13-19, Guidance on Managing Outsourcing Risk

46 It s Not Just an IT Responsibility Are the Right People Involved?

47 ARE THE RIGHT PEOPLE INVOLVED? Must know aspects of proper third-party risk management program to know who should be involved

48 ARE THE RIGHT PEOPLE INVOLVED? Five Phase Approach 1. Planning & risk assessment 2. Due diligence & third-party selection 3. Contracts 4. Ongoing monitoring 5. Termination

49 ARE THE RIGHT PEOPLE INVOLVED? Phase I - Planning & Risk Assessment (board of directors, management, line personnel) Is it a need or a want? Will it help accomplish strategy? Opportunity cost?

50 ARE THE RIGHT PEOPLE INVOLVED? Phase II - Due Diligence & Third-Party Selection Persons involved should be those who can properly evaluate Whether vendor will perform task(s) assigned (direct users) Cost/benefit (CFO, executive management, board)

51 ARE THE RIGHT PEOPLE INVOLVED? Phase III Contracts Legal CEO CFO

Financial stability (CFO,")

52 ARE THE RIGHT PEOPLE INVOLVED? Phase IV - Ongoing Monitoring Performance (direct users & IT) Financial stability (CFO, credit analysts) Business continuity (IT) Cybersecurity (IT)

53 BANKS FAIL TO ENFORCE CYBERSECURITY STANDARDS ON THIRD-PARTY PROVIDERS: FDIC WATCHDOG WASHINGTON Banks are woefully unprepared to face potential cybersecurity threats stemming from third-party technology providers, according to a report issued Wednesday by the Federal Deposit Insurance Corp. s independent watchdog. The FDIC's Office of Inspector General found that financial institutions failed to include important cybersecurity provisions in their contracts with the thirdparty firms. Typically, financial institution contracts with technology service providers did not clearly address TSP responsibilities and lacked specific contract provisions to protect FI interests or preserve FI rights, the report said.

54 ARE THE RIGHT PEOPLE INVOLVED? Phase V - Termination Legal IT Project management Business owner AP

55 Common Pitfalls in Third-Party Risk Management Programs

56 COMMON PITFALLS 1. Assuming IT can/should take on the responsibility alone 2. Performing only to appease examiners (checking the box) 3. Not including [*****] third parties 4. Board of directors not taking responsibility for oversight What do they see and when do they see it? 5. Obtaining documentation but doing nothing more 6. Not anticipating exit/transition costs in contract negotiations 7. Not having the VM Program reviewed/audited on a recurring basis

57 COMMON PITFALLS (CONT.) 8. Insufficient reference checks &/or not calling references 9. No risk ratings and/or outdated ratings 10. Not reviewing third party promotional (advertising) materials, as it represents your institution and/or contractually limiting use of your name / logo 11. Inadequate staff training & organizational communication 12. Out of synch with regulatory issuances and expectations 13. Not understanding business case for having a VM program

58 COMMON PITFALLS (CONT.) 14. Decentralization of contracts where are they? 15. Accepting automatically renewable clauses in contracts 16. Allowing contracts to renew automatically and unintentionally 17. Decentralized purchase / acquisition process 18. Relying on the wrong SOC report

59 BEST PRACTICES New Vendor Form AP will not set-up a new vendor until: Business Owner signs off Business Owner s superior signs off Vendor Management team signs off

60 BEST PRACTICES (CONT.) Vendor Monitoring / Performance Review Form Annual Process Dated? Business Owner Signoff? Meeting Service Level Agreements? Site Visit? Customer Complaints Reviewed?

61 BEST PRACTICES (CONT.) ANNUAL SUMMARY SHEET Vendor Manager Signoff Risk Rating Affirmed / Changed Financial Analysis Complete? Risk Trend Noted Annual monitoring sufficient? Implementation / Testing of User Considerations Complete IT Security Involved?

62 BEST PRACTICES SOFTWARE Software / Vendors Can We Outsource Vendor Management? Can the vendor manager-manager monitor itself? Software Vendor / Functionality Repository of documents Risk Assessment / Risk Rating Functionality Tickler Alerts / Contract Renewals Financial Analysis Security / Audited

63 BEST PRACTICES (CONT.) Vendor Manager Qualifications / Experience People person + detail oriented Audit / exam administration Project management Contract administration Compliance Risk assessment Appreciates the value of documentation IT background Financial statement analysis

64 VENDOR CRITICALITY Risk Considerations Possession of or access to member data (physical or logical) Direct contact with members IT infrastructure / provides critical application(s) Loan underwriting Compliance services

65 VENDOR CRITICALITY (CONT.) Other Issues What s a manageable number? Critical Total vendors tracked How many risk ratings? Can I safely ignore non-critical vendors?

66 WHAT S IN YOUR AUDIT PROGRAM? Vendor Management Program Review Policies & Procedures Risk Assessment / Risk Ranking Methodology Sample High Risk (Critical Vendors) Assess due diligence performed Review contracts Assess annual monitoring Financial statement analysis SOC report / Client Considerations implemented Sample Terminated Critical Vendors Top 30 payees? Are they tracked in the VM Program? Board / Supervisory Reporting Adequacy and Frequency

67 PULLING IT ALL TOGETHER INTERNAL STAKEHOLDERS Board & Supervisory Committee CFO Insurance Procurement Credit Analysis Accounts Payable Legal Compliance Internal Audit Contract Administration ERM + Vendor Manager + Software BCP IT Security Project Management Business Owners

68

69 Ken Glascock

70

Vendor Management Challenges and Expectations An Open Discussion April 13, 2017

1 Practical solutions driving tangible results Vendor Management Challenges and Expectations An Open Discussion April 13, 2017 Agenda Common Themes Discussion Expectations Overcoming Obstacles Common Comments

1 Practical solutions driving tangible results Vendor Management Challenges and Expectations An Open Discussion April 13, 2017 Agenda Common Themes Discussion Expectations Overcoming Obstacles Common Comments

Effective Vendor Risk Management. April 21, Mario A. Mosse. This Training is Brought to you by ComplianceOnline. Presenter:

This Training is Brought to you by ComplianceOnline. Effective Vendor Risk Management Presenter: Mario A. Mosse April 21, 2017 This training session is sponsored by 2014 ComplianceOnline www.complianceonlie.com

This Training is Brought to you by ComplianceOnline. Effective Vendor Risk Management Presenter: Mario A. Mosse April 21, 2017 This training session is sponsored by 2014 ComplianceOnline www.complianceonlie.com

VENDOR MANAGEMENT 101

VENDOR MANAGEMENT 101 Enterprise Risk Management Vendor Management Business Continuity IT GRC Internal Audit Regulatory Compliance Manager Introduction to Vendor Management About Your Presenter Andrea

VENDOR MANAGEMENT 101 Enterprise Risk Management Vendor Management Business Continuity IT GRC Internal Audit Regulatory Compliance Manager Introduction to Vendor Management About Your Presenter Andrea

Hot Topics in Third Party Management. April 5, 2018 MEMBER OF ALLINIAL GLOBAL, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS

Hot Topics in Third Party Management April 5, 2018 MEMBER OF ALLINIAL GLOBAL, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS 2018 Wolf & Company, P.C. Before we get started Today s presentation slides can

Hot Topics in Third Party Management April 5, 2018 MEMBER OF ALLINIAL GLOBAL, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS 2018 Wolf & Company, P.C. Before we get started Today s presentation slides can

Strengthening Vendor Risk Management Program

Strengthening Vendor Risk Management Program ACUIA Region 5 Fall Meeting Portsmouth, N.H. October 2017 PKF O Connor Davies Risk Advisory Services Governance & Regulations Cyber-Security Risk Management

Strengthening Vendor Risk Management Program ACUIA Region 5 Fall Meeting Portsmouth, N.H. October 2017 PKF O Connor Davies Risk Advisory Services Governance & Regulations Cyber-Security Risk Management

VENDOR RISK MANAGEMENT FCC SERVICES

VENDOR RISK MANAGEMENT FCC SERVICES Introductions Chris Tait, CISA, CFSA, CCSK, CCSFP Principal, Financial Services Baker Tilly Russ Sommers, CPA, CISA Senior Manager, Financial Services Baker Tilly Agenda

VENDOR RISK MANAGEMENT FCC SERVICES Introductions Chris Tait, CISA, CFSA, CCSK, CCSFP Principal, Financial Services Baker Tilly Russ Sommers, CPA, CISA Senior Manager, Financial Services Baker Tilly Agenda

Vendor Management 101

Vendor Management 101 January 18, 2018 Presented by Branan Cooper Chief Risk Officer at Venminder branan.cooper@venminder.com (502) 909-0325 Session Agenda Vendor risk management why it s required today

Vendor Management 101 January 18, 2018 Presented by Branan Cooper Chief Risk Officer at Venminder branan.cooper@venminder.com (502) 909-0325 Session Agenda Vendor risk management why it s required today

Self Assessment Workbook

Self Assessment Workbook Corporate Governance Audit Committee January 2018 Ce document est aussi disponible en français. Applicability The Self Assessment Workbook: Corporate Governance Audit Committee

Self Assessment Workbook Corporate Governance Audit Committee January 2018 Ce document est aussi disponible en français. Applicability The Self Assessment Workbook: Corporate Governance Audit Committee

DIVIDE BY JEFFREY NAIMON & MOORARI SHAH

DIVIDE & Conquer CFPB Intensifies Focus on Third-Party Vendors, Launches Direct Supervision Program Focused on Mortgage Industry BY JEFFREY NAIMON & MOORARI SHAH Jeffrey Naimon Moorari Shah The Consumer

DIVIDE & Conquer CFPB Intensifies Focus on Third-Party Vendors, Launches Direct Supervision Program Focused on Mortgage Industry BY JEFFREY NAIMON & MOORARI SHAH Jeffrey Naimon Moorari Shah The Consumer

IT Service Delivery And Support Week Seven: SLA. IT Auditing and Cyber Security Fall 2016 Instructor: Liang Yao

IT Service Delivery And Support Week Seven: SLA IT Auditing and Cyber Security Fall 2016 Instructor: Liang Yao 1 Outsourcing Drivers Outsourced IT Works Outsourced IT Activity Samples Top Three Outsourcing

IT Service Delivery And Support Week Seven: SLA IT Auditing and Cyber Security Fall 2016 Instructor: Liang Yao 1 Outsourcing Drivers Outsourced IT Works Outsourced IT Activity Samples Top Three Outsourcing

Best Practices for Establishing a Cost-Effective Internal Audit Function. Article by Heidi Wier June 2016

Best Practices for Establishing a Cost-Effective Internal Audit Function Article by Heidi Wier June 2016 Best Practices for Establishing a COST-EFFECTIVE INTERNAL AUDIT FUNCTION BY HEIDI WIER The heightened

Best Practices for Establishing a Cost-Effective Internal Audit Function Article by Heidi Wier June 2016 Best Practices for Establishing a COST-EFFECTIVE INTERNAL AUDIT FUNCTION BY HEIDI WIER The heightened

The Role of the VMO in Regulatory Compliance Planning, Due Diligence and Contract Negotiation

: The Role of the VMO in Regulatory Compliance Planning, Due Diligence and Contract Negotiation David England, Director, ISG ISG WHITE PAPER 2017 Information Services Group, Inc. All Rights Reserved EXECUTIVE

: The Role of the VMO in Regulatory Compliance Planning, Due Diligence and Contract Negotiation David England, Director, ISG ISG WHITE PAPER 2017 Information Services Group, Inc. All Rights Reserved EXECUTIVE

Navigating the Intersection of Vendor Management and Business Continuity

Navigating the Intersection of Vendor Management and Business Continuity MICHAEL BERMAN, J.D. Table of Contents Why are we here? Business Continuity and Vendor Management Primary Intersection BCP Each

Navigating the Intersection of Vendor Management and Business Continuity MICHAEL BERMAN, J.D. Table of Contents Why are we here? Business Continuity and Vendor Management Primary Intersection BCP Each

Guidance Note: Corporate Governance - Board of Directors. January Ce document est aussi disponible en français.

Guidance Note: Corporate Governance - Board of Directors January 2018 Ce document est aussi disponible en français. Applicability The Guidance Note: Corporate Governance - Board of Directors (the Guidance

Guidance Note: Corporate Governance - Board of Directors January 2018 Ce document est aussi disponible en français. Applicability The Guidance Note: Corporate Governance - Board of Directors (the Guidance

Financial Institutions Consulting. Quality service. Personal attention.

Financial Institutions Consulting Quality service. Personal attention. Why Weaver? With more than 65 years of experience and a commitment to our financial institution clients, Weaver is established as

Financial Institutions Consulting Quality service. Personal attention. Why Weaver? With more than 65 years of experience and a commitment to our financial institution clients, Weaver is established as

Guidance Note: Corporate Governance - Audit Committee. March Ce document est aussi disponible en français.

Guidance Note: Corporate Governance - Audit Committee March 2015 Ce document est aussi disponible en français. Applicability The Guidance Note: Corporate Governance Audit Committee (the Guidance Note )

Guidance Note: Corporate Governance - Audit Committee March 2015 Ce document est aussi disponible en français. Applicability The Guidance Note: Corporate Governance Audit Committee (the Guidance Note )

Guidance Note: Corporate Governance - Audit Committee. January Ce document est aussi disponible en français.

Guidance Note: Corporate Governance - Audit Committee January 2018 Ce document est aussi disponible en français. Applicability The Guidance Note: Corporate Governance Audit Committee (the Guidance Note

Guidance Note: Corporate Governance - Audit Committee January 2018 Ce document est aussi disponible en français. Applicability The Guidance Note: Corporate Governance Audit Committee (the Guidance Note

Risk Assessment - Balancing Risk While Enhancing Controls

Risk Assessment - Balancing Risk While Enhancing Controls cliftonlarsonallen.com Session Objectives Define risk and risk assessment. Execution of assessment and approach Impact on controls and future state

Risk Assessment - Balancing Risk While Enhancing Controls cliftonlarsonallen.com Session Objectives Define risk and risk assessment. Execution of assessment and approach Impact on controls and future state

Self Assessment Workbook

Self Assessment Workbook Corporate Governance - Board of Directors March 2015 Ce document est aussi disponible en français. Deposit Insurance Corporation of Ontario Applicability The Self Assessment Workbook:

Self Assessment Workbook Corporate Governance - Board of Directors March 2015 Ce document est aussi disponible en français. Deposit Insurance Corporation of Ontario Applicability The Self Assessment Workbook:

Vendor Management from an Auditor s Perspective

Vendor Management from an Auditor s Perspective Mike Morris Partner mmorris@pkm.com (404) 420-5669 Mary Beth Marchione Systems Manager mmarchione@pkm.com (404) 548-2825 April 25, 2017 Session Agenda Understand

Vendor Management from an Auditor s Perspective Mike Morris Partner mmorris@pkm.com (404) 420-5669 Mary Beth Marchione Systems Manager mmarchione@pkm.com (404) 548-2825 April 25, 2017 Session Agenda Understand

REGULATORY HOT TOPIC Third Party IT Vendor Management

REGULATORY HOT TOPIC Third Party IT Vendor Management 1 Todays Outsourced Technology Services Core Processing Internet Banking Mobile Banking Managed Security Services Managed Data Center Services And

REGULATORY HOT TOPIC Third Party IT Vendor Management 1 Todays Outsourced Technology Services Core Processing Internet Banking Mobile Banking Managed Security Services Managed Data Center Services And

CFPB Compliance Management Review

General Principles and Introduction Supervised entities within the scope of CFPB s supervision and enforcement authority include both depository institutions and non-depository consumer financial services

General Principles and Introduction Supervised entities within the scope of CFPB s supervision and enforcement authority include both depository institutions and non-depository consumer financial services

Corporate Governance Management tool. Executing On Corporate Governance

Corporate Governance Management tool Executing On Corporate Governance Corporate Governance continues to be rated HIGH on the Regulatory priority for safety and soundness 2 Corporate Governance Guidance...

Corporate Governance Management tool Executing On Corporate Governance Corporate Governance continues to be rated HIGH on the Regulatory priority for safety and soundness 2 Corporate Governance Guidance...

2016 Focus Groups CFO Strategies Roundtable

2016 Focus Groups CFO Strategies Roundtable Wednesday, March 23, 2016 9:00am 12:00pm Today s Agenda Audits and Examinations 45 minutes Let s hear from each other and talk about what s new from CU*Answers

2016 Focus Groups CFO Strategies Roundtable Wednesday, March 23, 2016 9:00am 12:00pm Today s Agenda Audits and Examinations 45 minutes Let s hear from each other and talk about what s new from CU*Answers

Final May Corporate Governance Guideline

Final May 2006 Corporate Governance Guideline Table of Contents 1. INTRODUCTION 1 2. PURPOSES OF GUIDELINE 1 3. APPLICATION AND SCOPE 2 4. DEFINITIONS OF KEY TERMS 2 5. FRAMEWORK USED BY CENTRAL BANK TO

Final May 2006 Corporate Governance Guideline Table of Contents 1. INTRODUCTION 1 2. PURPOSES OF GUIDELINE 1 3. APPLICATION AND SCOPE 2 4. DEFINITIONS OF KEY TERMS 2 5. FRAMEWORK USED BY CENTRAL BANK TO

Vendor Management Table of Contents. Table of Contents. Equity Loans

Table of Contents Table of Contents Table of Contents... 1 Chapter 1 Introduction... 5 1.1 Goals & Objectives... 5 1.2 Required Review... 5 1.3 Applicability... 5 Chapter 2 Monitoring and Quality Control...

Table of Contents Table of Contents Table of Contents... 1 Chapter 1 Introduction... 5 1.1 Goals & Objectives... 5 1.2 Required Review... 5 1.3 Applicability... 5 Chapter 2 Monitoring and Quality Control...

STRATEGIES FOR EFFECTIVELY WORKING WITH THIRD-PARTIES. September 2017

STRATEGIES FOR EFFECTIVELY WORKING WITH THIRD-PARTIES September 2017 Your presenters Nancy Aubrey Partner Boston, MA Nancy.aubrey@rsmus.com Rick Shriner Principal McLean, VA Rick.shriner@rsmus.com 2 Agenda

STRATEGIES FOR EFFECTIVELY WORKING WITH THIRD-PARTIES September 2017 Your presenters Nancy Aubrey Partner Boston, MA Nancy.aubrey@rsmus.com Rick Shriner Principal McLean, VA Rick.shriner@rsmus.com 2 Agenda

IT Risk Management: IT Audit

IT Risk Management: IT Audit Agenda Purpose of Presentation Define Purpose of IT Audit Coverage Identify Scope of IT Audit/Risk Based Audit Describe Roles and Responsibilities Identify Supervisory Expectations

IT Risk Management: IT Audit Agenda Purpose of Presentation Define Purpose of IT Audit Coverage Identify Scope of IT Audit/Risk Based Audit Describe Roles and Responsibilities Identify Supervisory Expectations

Internal Control Questionnaire and Assessment

Bureau of Financial Monitoring and Accountability Florida Department of Economic Opportunity September 15, 2016 107 East Madison Street Caldwell Building Tallahassee, Florida 32399 www.floridajobs.org

Bureau of Financial Monitoring and Accountability Florida Department of Economic Opportunity September 15, 2016 107 East Madison Street Caldwell Building Tallahassee, Florida 32399 www.floridajobs.org

Social Media Policy Manual Table of Contents [Sample Client] Table of Contents. Sample

![Social Media Policy Manual Table of Contents [Sample Client] Table of Contents. Sample](/thumbs/95/124893583.jpg "Social Media Policy Manual Table of Contents [Sample Client] Table of Contents. Sample") Table of Contents Table of Contents TABLE OF CONTENTS... 1 CHAPTER 1 INTRODUCTION... 3 1.1 GOALS AND OBJECTIVES... 3 1.2 REQUIRED REVIEW... 3 1.3 APPLICABILITY... 3 1.4 ROLES AND RESPONSIBILITIES... 4

Table of Contents Table of Contents TABLE OF CONTENTS... 1 CHAPTER 1 INTRODUCTION... 3 1.1 GOALS AND OBJECTIVES... 3 1.2 REQUIRED REVIEW... 3 1.3 APPLICABILITY... 3 1.4 ROLES AND RESPONSIBILITIES... 4

Risk Assessment. Consumer Risk Assessment. Using the Risk Assessment Template

Consumer CFPB s process is designed to evaluate on a consistent basis the extent of risk to consumers arising from the activities of a particular supervised entity and to identify the sources of that risk.

Consumer CFPB s process is designed to evaluate on a consistent basis the extent of risk to consumers arising from the activities of a particular supervised entity and to identify the sources of that risk.

VENDORINSIGHTU P D A T E

VENDORINSIGHTU P D A T E November 12, 2013 COMPLIANCE VendorInsight is the industry-leading solution for financial institutions offering the most features and capabilities for vendor risk monitoring. Ask

VENDORINSIGHTU P D A T E November 12, 2013 COMPLIANCE VendorInsight is the industry-leading solution for financial institutions offering the most features and capabilities for vendor risk monitoring. Ask

Transparency in the Workforce System Establishing Firewalls & Internal Controls

Transparency in the Workforce System Establishing Firewalls & Internal Controls Presented by the Today s Objectives Define internal controls Identify components of an internal control structure Discuss

Transparency in the Workforce System Establishing Firewalls & Internal Controls Presented by the Today s Objectives Define internal controls Identify components of an internal control structure Discuss

International Standard on Auditing (Ireland) 402 Audit Considerations Relating to an Entity using a Service Organisation

402 Audit Considerations Relating to an Entity using a Service Organisation") International Standard on Auditing (Ireland) 402 Audit Considerations Relating to an Entity using a Service Organisation MISSION To contribute to Ireland having a strong regulatory environment in which

International Standard on Auditing (Ireland) 402 Audit Considerations Relating to an Entity using a Service Organisation MISSION To contribute to Ireland having a strong regulatory environment in which

MALIN CORPORATION PLC CORPORATE GOVERNANCE GUIDELINES. Adopted on 3 March 2015 and Amended on 26 May 2015

MALIN CORPORATION PLC CORPORATE GOVERNANCE GUIDELINES Adopted on 3 March 2015 and Amended on 26 May 2015 The following Corporate Governance Guidelines (the "Guidelines") and Schedule of Matters reserved

MALIN CORPORATION PLC CORPORATE GOVERNANCE GUIDELINES Adopted on 3 March 2015 and Amended on 26 May 2015 The following Corporate Governance Guidelines (the "Guidelines") and Schedule of Matters reserved

SA 402(REVISED) AUDIT CONSIDERATIONS RELATING TO AN ENTITY USING

AUDIT CONSIDERATIONS RELATING TO AN ENTITY USING") Part I : Engagement and Quality Control Standards I.271 SA 402(REVISED) AUDIT CONSIDERATIONS RELATING TO AN ENTITY USING A SERVICE ORGANISATION (EFFECTIVE FOR ALL AUDITS RELATING TO ACCOUNTING PERIODS

Part I : Engagement and Quality Control Standards I.271 SA 402(REVISED) AUDIT CONSIDERATIONS RELATING TO AN ENTITY USING A SERVICE ORGANISATION (EFFECTIVE FOR ALL AUDITS RELATING TO ACCOUNTING PERIODS

Internal Control Questionnaire and Assessment

Bureau of Financial Monitoring and Accountability Florida Department of Economic Opportunity September 30, 2017 107 East Madison Street Caldwell Building Tallahassee, Florida 32399 www.floridajobs.org

Bureau of Financial Monitoring and Accountability Florida Department of Economic Opportunity September 30, 2017 107 East Madison Street Caldwell Building Tallahassee, Florida 32399 www.floridajobs.org

Effects of Changes in Attest Standards on SOC 1 Examinations

Executive Summary Subservice organizations, management s assertion responsibilities and other items are addressed in Statement on Standards for Attestation Engagements (SSAE) No. 18, Attestation Standards:

Executive Summary Subservice organizations, management s assertion responsibilities and other items are addressed in Statement on Standards for Attestation Engagements (SSAE) No. 18, Attestation Standards:

CFPB Examination Procedures

Compliance Management Review General Principles and Introduction Institutions within the scope of the CFPB s supervision and enforcement authority include both depository institutions and non-depository

Compliance Management Review General Principles and Introduction Institutions within the scope of the CFPB s supervision and enforcement authority include both depository institutions and non-depository

An Examination of an Entity s Internal Control Over Financial Reporting That Is Integrated With an Audit of Its Financial Statements

ASB Meeting July 30 August 1, 2013 Agenda Item 3B AT Section 501 An Examination of an Entity s Internal Control Over Financial Reporting That Is Integrated With an Audit of Its Financial Statements Source:

ASB Meeting July 30 August 1, 2013 Agenda Item 3B AT Section 501 An Examination of an Entity s Internal Control Over Financial Reporting That Is Integrated With an Audit of Its Financial Statements Source:

Crowe Consumer Compliance Consulting Services

Crowe Consumer Compliance Consulting Services How Well Is Your Organization Managing Regulatory Risk in Consumer Banking and Financial Services? Audit / Tax / Advisory / Risk / Performance Smart decisions.

Crowe Consumer Compliance Consulting Services How Well Is Your Organization Managing Regulatory Risk in Consumer Banking and Financial Services? Audit / Tax / Advisory / Risk / Performance Smart decisions.

Ensuring Organizational & Enterprise Resiliency with Third Parties

Ensuring Organizational & Enterprise Resiliency with Third Parties Geno Pandolfi Tuesday, May 17, 2016 Room 7&8 (1:30-2:15 PM) Session Review Objectives Approaches to Third Party Risk Management Core Concepts

Ensuring Organizational & Enterprise Resiliency with Third Parties Geno Pandolfi Tuesday, May 17, 2016 Room 7&8 (1:30-2:15 PM) Session Review Objectives Approaches to Third Party Risk Management Core Concepts

OFFICE OF FINANCIAL INSTITUTIONS

OFFICE OF FINANCIAL INSTITUTIONS OFI BULLETIN BL-01-2005 (B,SB,SL) February 1, 2005 TO: FROM: SUBJECT: THE CHAIRMAN OF THE AUDIT COMMITTEE AND CHIEF EXECUTIVE OFFICER/MANAGER OF ALL BANKS AND THRIFTS SIDNEY

OFFICE OF FINANCIAL INSTITUTIONS OFI BULLETIN BL-01-2005 (B,SB,SL) February 1, 2005 TO: FROM: SUBJECT: THE CHAIRMAN OF THE AUDIT COMMITTEE AND CHIEF EXECUTIVE OFFICER/MANAGER OF ALL BANKS AND THRIFTS SIDNEY

Internal Audit s Role in Third Party Risk Management (TPRM)

") www.pwc.com Internal Audit s Role in Third (TPRM) Jon Pastore, Nick Fullmer Third (TPRM) Framework What is Third? Third Party risk management is focused on understanding and managing risks associated with

www.pwc.com Internal Audit s Role in Third (TPRM) Jon Pastore, Nick Fullmer Third (TPRM) Framework What is Third? Third Party risk management is focused on understanding and managing risks associated with

WHAT DO WE LEASE? CONDUCTING AN ENTERPRISE-WIDE CENSUS. THE TEN PLACES TO LOOK TO FIND ALL OF YOUR LEASES

WHAT DO WE LEASE? CONDUCTING AN ENTERPRISE-WIDE CENSUS THE TEN PLACES TO LOOK TO FIND ALL OF YOUR LEASES How to Conduct an Enterprise-Wide Lease Census 2 WHAT DO WE LEASE? Since the publication of the

WHAT DO WE LEASE? CONDUCTING AN ENTERPRISE-WIDE CENSUS THE TEN PLACES TO LOOK TO FIND ALL OF YOUR LEASES How to Conduct an Enterprise-Wide Lease Census 2 WHAT DO WE LEASE? Since the publication of the

Risk-Focused Examinations

Risk-Focused Examinations Session 704 IASA 86 TH ANNUAL EDUCATIONAL CONFERENCE & BUSINESS SHOW Understanding the Examination Process In order to be able to maximize examination efficiency and have examiners

Risk-Focused Examinations Session 704 IASA 86 TH ANNUAL EDUCATIONAL CONFERENCE & BUSINESS SHOW Understanding the Examination Process In order to be able to maximize examination efficiency and have examiners

STEPS FOR EFFECTIVE MANAGEMENT OF VENDOR AND SUPPLIER CYBERSECURITY RISKS. April 25, 2018 In-House Counsel Conference

STEPS FOR EFFECTIVE MANAGEMENT OF VENDOR AND SUPPLIER CYBERSECURITY RISKS April 25, 2018 In-House Counsel Conference Presenters: Daniela Ivancikova, Assistant General Counsel, University of Delaware Evan

STEPS FOR EFFECTIVE MANAGEMENT OF VENDOR AND SUPPLIER CYBERSECURITY RISKS April 25, 2018 In-House Counsel Conference Presenters: Daniela Ivancikova, Assistant General Counsel, University of Delaware Evan

Guidelines of Corporate Governance

Guidelines of Corporate Governance December 2017 The Board of Directors (the Board ) of Radian Group Inc. ( Radian or the Company ) has established guidelines for corporate governance based on an assessment

Guidelines of Corporate Governance December 2017 The Board of Directors (the Board ) of Radian Group Inc. ( Radian or the Company ) has established guidelines for corporate governance based on an assessment

International Standards for the Professional Practice of Internal Auditing (Standards)

") INTERNATIONAL STANDARDS FOR THE PROFESSIONAL PRACTICE OF INTERNAL AUDITING (STANDARDS) Attribute Standards 1000 Purpose, Authority, and Responsibility The purpose, authority, and responsibility of the

INTERNATIONAL STANDARDS FOR THE PROFESSIONAL PRACTICE OF INTERNAL AUDITING (STANDARDS) Attribute Standards 1000 Purpose, Authority, and Responsibility The purpose, authority, and responsibility of the

The CFPB Examination Process

The CFPB Examination Process Eric J. Mogilnicki Valerie M. Song Wilmer Cutler Pickering Hale and Dorr LLP Copyright 2013 All rights reserved. Prepared on February 5, 2013 I. Overview A. B. C. D. CFPB Examination

The CFPB Examination Process Eric J. Mogilnicki Valerie M. Song Wilmer Cutler Pickering Hale and Dorr LLP Copyright 2013 All rights reserved. Prepared on February 5, 2013 I. Overview A. B. C. D. CFPB Examination

AUDIT COMMITTEE HANDBOOK

AUDIT COMMITTEE HANDBOOK 2016 Ce document est également disponible en français Deposit Insurance Corporation of Ontario Page 1 Contents INTRODUCTION... 3 ORGANIZATION OF THE AUDIT COMMITTEE... 5 AUDIT

AUDIT COMMITTEE HANDBOOK 2016 Ce document est également disponible en français Deposit Insurance Corporation of Ontario Page 1 Contents INTRODUCTION... 3 ORGANIZATION OF THE AUDIT COMMITTEE... 5 AUDIT

IT EXAMS TOP 5 CITATIONS. Top 5 citations LOUISIANA BANKERS ASSOCIATION TECHNOLOGY CONFERENCE Policy and Risk Assessment 2.

IT EXAMS LOUISIANA BANKERS ASSOCIATION TECHNOLOGY CONFERENCE 2015 @TrainaCPA TOP 5 CITATIONS Top 5 citations 1. Policy and Risk Assessment 2. ACH/CATO 3. Disaster planning 4. Audit 5. Oversight 1. POLICY

IT EXAMS LOUISIANA BANKERS ASSOCIATION TECHNOLOGY CONFERENCE 2015 @TrainaCPA TOP 5 CITATIONS Top 5 citations 1. Policy and Risk Assessment 2. ACH/CATO 3. Disaster planning 4. Audit 5. Oversight 1. POLICY

BSA Risk Assessments and Transaction Monitoring Systems: Partners in Crime Prevention and Detection

BSA Risk Assessments and Transaction Monitoring Systems: Partners in Crime Prevention and Detection Presented by Lynn English Lafayette Federal Credit Union Key Takeaways After this webinar, participants

BSA Risk Assessments and Transaction Monitoring Systems: Partners in Crime Prevention and Detection Presented by Lynn English Lafayette Federal Credit Union Key Takeaways After this webinar, participants

Government Auditing Standards

United States Government Accountability Office GAO By the Comptroller General of the United States August 2011 Government Auditing Standards 2011 Internet Version CONTENTS CHAPTER 1... 1 GOVERNMENT AUDITING:

United States Government Accountability Office GAO By the Comptroller General of the United States August 2011 Government Auditing Standards 2011 Internet Version CONTENTS CHAPTER 1... 1 GOVERNMENT AUDITING:

FDICIA Reporting for Financial Institutions. Reporting Changes Under Part 363 and SAS 130

FDICIA Reporting for Financial Institutions Reporting Changes Under Part 363 and SAS 130 CONTENTS 02 INTRODUCTION REQUIREMENTS BY TIER 03 03 Management Assessment 04 05 03 Independent Auditors FILING DEADLINES

FDICIA Reporting for Financial Institutions Reporting Changes Under Part 363 and SAS 130 CONTENTS 02 INTRODUCTION REQUIREMENTS BY TIER 03 03 Management Assessment 04 05 03 Independent Auditors FILING DEADLINES

International Standards for the Professional Practice of Internal Auditing (Standards)

") Attribute Standards 1000 Purpose, Authority, and Responsibility The purpose, authority, and responsibility of the internal audit activity must be formally defined in an internal audit charter, consistent

Attribute Standards 1000 Purpose, Authority, and Responsibility The purpose, authority, and responsibility of the internal audit activity must be formally defined in an internal audit charter, consistent

Work Plan Updated March 3, 2014

Work Plan Updated March 3, 2014 Office of Inspector General Work Plan Updated March 3, 2014 Board of Governors of the Federal Reserve System Consumer Financial Protection Bureau Overview The Work Plan

Work Plan Updated March 3, 2014 Office of Inspector General Work Plan Updated March 3, 2014 Board of Governors of the Federal Reserve System Consumer Financial Protection Bureau Overview The Work Plan

Table of Contents. Chapter 1...1

Table of Contents Chapter 1...1 The Compliance Officer...1 Overview...2 The Compliance Officer...2 What is Compliance Risk?...3 NCUA s Defined Risk Categories... 3 Skills of a Compliance Officer...6 Identifying

Table of Contents Chapter 1...1 The Compliance Officer...1 Overview...2 The Compliance Officer...2 What is Compliance Risk?...3 NCUA s Defined Risk Categories... 3 Skills of a Compliance Officer...6 Identifying

THE IMPORTANCE OF DEVELOPING A SOCIAL MEDIA COMPLIANCE POLICY

THE IMPORTANCE OF DEVELOPING A POLICY Why Your Financial Institution Needs to Have a Proactive Policy in Place BY OPTIMAL BLUE e-series of 7 WHITE PAPER THE IMPORTANCE OF DEVELOPING A POLICY Why Your Financial

THE IMPORTANCE OF DEVELOPING A POLICY Why Your Financial Institution Needs to Have a Proactive Policy in Place BY OPTIMAL BLUE e-series of 7 WHITE PAPER THE IMPORTANCE OF DEVELOPING A POLICY Why Your Financial

Community Bankers Conference

3rd Annual Regional and Community Bankers Conference The Federal Reserve Bank of Boston Disclaimer NEVER WRONG DON T COMPLETELY RELY UPON Recent Developments in Audit Practice SOX, FDICIA 112, Other Robert

3rd Annual Regional and Community Bankers Conference The Federal Reserve Bank of Boston Disclaimer NEVER WRONG DON T COMPLETELY RELY UPON Recent Developments in Audit Practice SOX, FDICIA 112, Other Robert

SOC Reports: What are they and what should you do with them? berrydunn.com GAIN CONTROL

SOC Reports: What are they and what should you do with them? berrydunn.com GAIN CONTROL AGENDA SOC REPORTS OVERVIEW RELEVANT SECTIONS TO REVIEW SOC REVIEW CHECKLIST 2 SOC REPORTS OVERVIEW 3 SOC REPORTS

SOC Reports: What are they and what should you do with them? berrydunn.com GAIN CONTROL AGENDA SOC REPORTS OVERVIEW RELEVANT SECTIONS TO REVIEW SOC REVIEW CHECKLIST 2 SOC REPORTS OVERVIEW 3 SOC REPORTS

Internal and External Audits Table of Contents

Internal and External Audits Table of Contents Appendixes...108 A: Statutory and Regulatory Requirements...108 B: Part 363 Annual Report Worksheet...119 C: Part 363 Periodic Report Worksheet...122 D: OCC

Internal and External Audits Table of Contents Appendixes...108 A: Statutory and Regulatory Requirements...108 B: Part 363 Annual Report Worksheet...119 C: Part 363 Periodic Report Worksheet...122 D: OCC

Format and organization of GAGAS Auditor preparation of financials is a significant threat to independence 3 party arrangements in government State

The Yellow Book = GAGAS GAGAS = Generally Accepted Government Auditing Standards Overlay of Generally Accepted Auditing Standards (GAAS) issued by the Auditing Standards Board GAGAS contains the framework

The Yellow Book = GAGAS GAGAS = Generally Accepted Government Auditing Standards Overlay of Generally Accepted Auditing Standards (GAAS) issued by the Auditing Standards Board GAGAS contains the framework

IAASB Main Agenda (September 2004) Page Agenda Item PROPOSED REVISED INTERNATIONAL STANDARD ON AUDITING 540

Page Agenda Item PROPOSED REVISED INTERNATIONAL STANDARD ON AUDITING 540") IAASB Main Agenda (September 2004) Page 2004 1651 Agenda Item 4-A PROPOSED REVISED INTERNATIONAL STANDARD ON AUDITING 540 AUDITING ACCOUNTING ESTIMATES AND RELATED DISCLOSURES (EXCLUDING THOSE INVOLVING

IAASB Main Agenda (September 2004) Page 2004 1651 Agenda Item 4-A PROPOSED REVISED INTERNATIONAL STANDARD ON AUDITING 540 AUDITING ACCOUNTING ESTIMATES AND RELATED DISCLOSURES (EXCLUDING THOSE INVOLVING

GUIDANCE NOTE FOR DEPOSIT TAKERS (Class 1(1) and Class 1(2))

and Class 1(2))") GUIDANCE NOTE FOR DEPOSIT TAKERS (Class 1(1) and Class 1(2)) Operational Risk Management MARCH 2017 STATUS OF GUIDANCE The Isle of Man Financial Services Authority ( the Authority ) issues guidance for

GUIDANCE NOTE FOR DEPOSIT TAKERS (Class 1(1) and Class 1(2)) Operational Risk Management MARCH 2017 STATUS OF GUIDANCE The Isle of Man Financial Services Authority ( the Authority ) issues guidance for

AUDIT COMMITTEE CHARTER AS AMENDED AS OF MAY 6, 2015

AUDIT COMMITTEE CHARTER AS AMENDED AS OF MAY 6, 2015 This Audit Committee Charter ("Charter") was originally adopted by the Board of Directors (the "Board") of Kate Spade & Company (the "Company") at its

AUDIT COMMITTEE CHARTER AS AMENDED AS OF MAY 6, 2015 This Audit Committee Charter ("Charter") was originally adopted by the Board of Directors (the "Board") of Kate Spade & Company (the "Company") at its

Is Your Credit Union at Risk? Five Key Due Diligence Questions to Ask Your Vendors

Is Your Credit Union at Risk? Five Key Due Diligence Questions to Ask Your Vendors About Vanessa Stanfield Vanessa Stanfield Client Program Director, Vendor Management vstanfield@affiniongroup.com Vanessa

Is Your Credit Union at Risk? Five Key Due Diligence Questions to Ask Your Vendors About Vanessa Stanfield Vanessa Stanfield Client Program Director, Vendor Management vstanfield@affiniongroup.com Vanessa

Statement on February 2014 Auditing Standards 128. Using the Work of Internal Auditors

Statement on February 2014 Auditing Standards 128 Issued by the Auditing Standards Board Using the Work of Internal Auditors (Supersedes Statement on Auditing Standards [SAS] No. 65, The Auditor's Consideration

Statement on February 2014 Auditing Standards 128 Issued by the Auditing Standards Board Using the Work of Internal Auditors (Supersedes Statement on Auditing Standards [SAS] No. 65, The Auditor's Consideration

Australian Financial Markets Association. Principles relating to product approval - retail structured financial products

Australian Financial Markets Association Principles relating to product approval - retail structured financial products October 2012 Copyright in this publication is owned by the Australian Financial Markets

Australian Financial Markets Association Principles relating to product approval - retail structured financial products October 2012 Copyright in this publication is owned by the Australian Financial Markets

Consumer Financial Protection Bureau Independent Audit of Selected Operations and Budget

Consumer Financial Protection Bureau Independent Audit of Selected Operations and Budget March 26, 2018 KPMG LLP Suite 12000 1801 K Street, NW Washington, DC 20006 Table of Contents EXECUTIVE SUMMARY...

Consumer Financial Protection Bureau Independent Audit of Selected Operations and Budget March 26, 2018 KPMG LLP Suite 12000 1801 K Street, NW Washington, DC 20006 Table of Contents EXECUTIVE SUMMARY...

In Control: Getting Familiar with the New COSO Guidelines. CSMFO Monterey, California February 18, 2015

In Control: Getting Familiar with the New COSO Guidelines CSMFO Monterey, California February 18, 2015 1 Background on COSO Part 1 2 Development of a comprehensive framework of internal control Internal

In Control: Getting Familiar with the New COSO Guidelines CSMFO Monterey, California February 18, 2015 1 Background on COSO Part 1 2 Development of a comprehensive framework of internal control Internal

The Who, What, and Why of Service Organization Control (SOC) Engagements. Presentation to: 2nd Annual 'I Heart Audit' Conference

Engagements. Presentation to: 2nd Annual 'I Heart Audit' Conference") The Who, What, and Why of Service Organization Control (SOC) Engagements Presentation to: 2nd Annual 'I Heart Audit' Conference February 24, 2016 Agenda What is SOC? Who needs SOC? Types of SOC Engagements

The Who, What, and Why of Service Organization Control (SOC) Engagements Presentation to: 2nd Annual 'I Heart Audit' Conference February 24, 2016 Agenda What is SOC? Who needs SOC? Types of SOC Engagements

MARIANNE E. ROCHE ATTORNEY AT LAW

CORPORATE GOVERNANCE FOR FINANCIAL INSTITUTION DIRECTORS Prepared and presented by: MARIANNE E. ROCHE ATTORNEY AT LAW SILVER, FREEDMAN & TAFF, L.L.P. DIRECT DIAL NUMBER 3299 K STREET, N.W., SUITE 100 (202)

CORPORATE GOVERNANCE FOR FINANCIAL INSTITUTION DIRECTORS Prepared and presented by: MARIANNE E. ROCHE ATTORNEY AT LAW SILVER, FREEDMAN & TAFF, L.L.P. DIRECT DIAL NUMBER 3299 K STREET, N.W., SUITE 100 (202)

FINANCIAL INSTITUTIONS AUDIT COMMITTEE GUIDE FOR FINANCIAL INSTITUTIONS

FINANCIAL INSTITUTIONS AUDIT COMMITTEE GUIDE FOR FINANCIAL INSTITUTIONS Dear clients and friends of the firm, Corporate governance is a significant area of focus for stakeholders of financial institutions.

FINANCIAL INSTITUTIONS AUDIT COMMITTEE GUIDE FOR FINANCIAL INSTITUTIONS Dear clients and friends of the firm, Corporate governance is a significant area of focus for stakeholders of financial institutions.

Catching Fraud During a Recession Through Superior Internal Controls. FICPA s 25 th Annual Accounting Show. J. Stephen Nouss September 29, 2010

Catching Fraud During a Recession Through Superior Internal Controls FICPA s 25 th Annual Accounting Show J. Stephen Nouss September 29, 2010 1 Session Objectives Fraud Facts (2008 Association of Certified

Catching Fraud During a Recession Through Superior Internal Controls FICPA s 25 th Annual Accounting Show J. Stephen Nouss September 29, 2010 1 Session Objectives Fraud Facts (2008 Association of Certified

Application: All licensed institutions and supervisory personnel

Title: SR-1 Strategic Risk Management Date: FINAL Purpose: To set out the approach which the NBRM will adopt in the supervision of licensed institutions strategic risk, and to provide guidance to licensed

Title: SR-1 Strategic Risk Management Date: FINAL Purpose: To set out the approach which the NBRM will adopt in the supervision of licensed institutions strategic risk, and to provide guidance to licensed

1.3.1 The responsibilities of the Parent Board include, but are not limited to, the following 1 :

POLICY: CORPORATE GOVERNANCE APPROVED BY: Board of Directors APPROVAL DATE: 13 February, 2018 EFFECTIVE DATE: 13 February, 2018 PREVIOUS UPDATES: 27 February, 2017, 25 July, 2016, 19 February, 2016, 27

POLICY: CORPORATE GOVERNANCE APPROVED BY: Board of Directors APPROVAL DATE: 13 February, 2018 EFFECTIVE DATE: 13 February, 2018 PREVIOUS UPDATES: 27 February, 2017, 25 July, 2016, 19 February, 2016, 27

NTGA Compliance & Operational Manager Due Diligence Process

NORTHERN TRUST 2010 PROGRAM SOLUTIONS CONFERENCE Investment Solutions in an Uncertain World: WHAT S NEXT? NTGA Compliance & Operational Manager Due Diligence Process Allison K. Fraser VP & Sr. Compliance

NORTHERN TRUST 2010 PROGRAM SOLUTIONS CONFERENCE Investment Solutions in an Uncertain World: WHAT S NEXT? NTGA Compliance & Operational Manager Due Diligence Process Allison K. Fraser VP & Sr. Compliance

Types of Systems Audit & Relevance. Presented By: Prasad Pendse, CISA

Types of Systems Audit & Relevance Presented By: Prasad Pendse, CISA Agenda Systems Audit Categories & Types of Systems Audit, Relevance IT & Application Audits Security Audits Process Audits Advantages

Types of Systems Audit & Relevance Presented By: Prasad Pendse, CISA Agenda Systems Audit Categories & Types of Systems Audit, Relevance IT & Application Audits Security Audits Process Audits Advantages

Auditing for Effective Training

Maleka Ali M. Ali 2013 Director of Consulting & Education Page 0 Banker s Toolbox Auditing for Effective Training I. INTRODUCTION Banking organizations must develop, implement, and maintain effective AML

Maleka Ali M. Ali 2013 Director of Consulting & Education Page 0 Banker s Toolbox Auditing for Effective Training I. INTRODUCTION Banking organizations must develop, implement, and maintain effective AML

AUDIT UNDP COUNTRY OFFICE KUWAIT. Report No Issue Date: 20 May 2014

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN KUWAIT Report No. 1265 Issue Date: 20 May 2014 Table of Contents Executive Summary i I. About the Office 1 II. Audit results 1 A. Governance

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN KUWAIT Report No. 1265 Issue Date: 20 May 2014 Table of Contents Executive Summary i I. About the Office 1 II. Audit results 1 A. Governance

The Basics of Internal Controls & Segregation of Duties

The Basics of Internal Controls & Segregation of Duties Presented by: Kevin L. Pegish, CPA Senior Audit Manager Northwest Region klpegish@ohioauditor.gov Internal Controls, we will discuss the following:

The Basics of Internal Controls & Segregation of Duties Presented by: Kevin L. Pegish, CPA Senior Audit Manager Northwest Region klpegish@ohioauditor.gov Internal Controls, we will discuss the following:

(Effective for audits of financial statements for periods ending on or after December 15, 2013) CONTENTS

CONTENTS") INTERNATIONAL STANDARD ON AUDITING 315 (REVISED) IDENTIFYING AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT THROUGH UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT Introduction (Effective for audits of

INTERNATIONAL STANDARD ON AUDITING 315 (REVISED) IDENTIFYING AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT THROUGH UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT Introduction (Effective for audits of

Ministry of Finance Comptroller General Victoria, BC

Ministry of Finance Comptroller General Victoria, BC Provide your strong leadership, financial aptitude, and communication skills to this integral role in the executive team The Ministry of Finance plays

Ministry of Finance Comptroller General Victoria, BC Provide your strong leadership, financial aptitude, and communication skills to this integral role in the executive team The Ministry of Finance plays

Oversight of external auditors by the audit committee

Oversight of external auditors by the audit committee MCCG Intended Outcome 8.0 There is an effective and independent Audit Committee. The board is able to objectively review the Audit Committee s findings

Oversight of external auditors by the audit committee MCCG Intended Outcome 8.0 There is an effective and independent Audit Committee. The board is able to objectively review the Audit Committee s findings

Job Family Matrix. Core Duties Core Duties Core Duties

Job Family Matrix Job Function: Finance Job Family: Banking - Professional Job Family Summary: Perform or manage a wide range of banking activities while ensuring compliance in various functions which

Job Family Matrix Job Function: Finance Job Family: Banking - Professional Job Family Summary: Perform or manage a wide range of banking activities while ensuring compliance in various functions which

Audit and Risk Committee Charter

Audit and Risk Committee Charter Purpose The Audit and Risk Committee ( Committee ) has been established as a committee of the board of directors ( Board ) of Trustpower Limited (the Company ) to assist

Audit and Risk Committee Charter Purpose The Audit and Risk Committee ( Committee ) has been established as a committee of the board of directors ( Board ) of Trustpower Limited (the Company ) to assist

FRIENDSHIP HOUSE JOB DESCRIPTION. Full Time: Monday - Friday 9AM-6PM, Weekends and evenings as needed

FRIENDSHIP HOUSE JOB DESCRIPTION Position: Supervisor: Working Schedule: Employment Status: Chief Financial Officer Executive Director Full Time: Monday - Friday 9AM-6PM, Weekends and evenings as needed

FRIENDSHIP HOUSE JOB DESCRIPTION Position: Supervisor: Working Schedule: Employment Status: Chief Financial Officer Executive Director Full Time: Monday - Friday 9AM-6PM, Weekends and evenings as needed

ACING YOUR REMOTE DEPOSIT CAPTURE AUDIT:

ACING YOUR REMOTE DEPOSIT CAPTURE AUDIT: LESSONS FROM BANKERS WHO HAVE BEEN THERE AND DONE THAT! COMPLIANCE STARTS AT THE TOP Many banks are becoming savvy about how to ace their audits after experiencing

ACING YOUR REMOTE DEPOSIT CAPTURE AUDIT: LESSONS FROM BANKERS WHO HAVE BEEN THERE AND DONE THAT! COMPLIANCE STARTS AT THE TOP Many banks are becoming savvy about how to ace their audits after experiencing

Microsoft Cloud Agreement Financial Services Amendment

Microsoft Cloud Agreement Financial Services Amendment This Financial Services Amendment ( Amendment ) is entered into between Customer and the Microsoft Affiliate who are parties to the Microsoft Cloud

Microsoft Cloud Agreement Financial Services Amendment This Financial Services Amendment ( Amendment ) is entered into between Customer and the Microsoft Affiliate who are parties to the Microsoft Cloud

In 1992, the Committee of Sponsoring Organizations of the Treadway Commission (COSO) issued a

issued a") Checkpoint Contents Accounting, Audit & Corporate Finance Library Editorial Materials Audit and Attest Internal Control Communications Chapter 1 INTRODUCTION AND OVERVIEW 100 Background 100 Background

Checkpoint Contents Accounting, Audit & Corporate Finance Library Editorial Materials Audit and Attest Internal Control Communications Chapter 1 INTRODUCTION AND OVERVIEW 100 Background 100 Background

Family Office and Concierge Services

Family Office and Concierge Services our service promise... listening, communicating and responding Table of Contents Why Outsource? Finance Management and Accounting Services About Us Additional Grassi

Family Office and Concierge Services our service promise... listening, communicating and responding Table of Contents Why Outsource? Finance Management and Accounting Services About Us Additional Grassi

CODE OF ETHICS/CONDUCT

CODE OF ETHICS/CONDUCT This Code of Ethics/Conduct ( Code ) covers a wide range of business practices and procedures. It does not cover every possible issue that may arise, but rather provides information

CODE OF ETHICS/CONDUCT This Code of Ethics/Conduct ( Code ) covers a wide range of business practices and procedures. It does not cover every possible issue that may arise, but rather provides information

OPERATIONAL RISK MANAGEMENT MODULE

OPERATIONAL RISK MANAGEMENT MODULE MODULE OM Operational Risk Management Table of Contents OM-A OM-B OM-1 OM-2 OM-3 OM-4 Date Last Changed Introduction OM-A.1 Purpose 01/2012 OM-A.2 [This Chapter was deleted

OPERATIONAL RISK MANAGEMENT MODULE MODULE OM Operational Risk Management Table of Contents OM-A OM-B OM-1 OM-2 OM-3 OM-4 Date Last Changed Introduction OM-A.1 Purpose 01/2012 OM-A.2 [This Chapter was deleted

Extended Enterprise Risk Management

Extended Enterprise Risk Management Driving performance through the extended enterprise October 2015 A network within a network The Extended Enterprise is the concept that an organization does not operate

Extended Enterprise Risk Management Driving performance through the extended enterprise October 2015 A network within a network The Extended Enterprise is the concept that an organization does not operate

Chiyoda Corporation Corporate Governance Policy (Revised on June 23, 2016)

") [Translation] Chiyoda Corporation Corporate Governance Policy (Revised on June 23, 2016) This policy sets forth the basic views and basic guideline of Chiyoda Corporation (hereinafter the Company ) with

[Translation] Chiyoda Corporation Corporate Governance Policy (Revised on June 23, 2016) This policy sets forth the basic views and basic guideline of Chiyoda Corporation (hereinafter the Company ) with

Corporate Governance Statement

- 2017 OVERVIEW The Board is responsible for the overall corporate governance of the Company, including establishing and monitoring key performance goals. It is committed to attaining standards of corporate

- 2017 OVERVIEW The Board is responsible for the overall corporate governance of the Company, including establishing and monitoring key performance goals. It is committed to attaining standards of corporate

Corporate Governance Statement John Bridgeman Limited

Corporate Governance Statement John Bridgeman Limited 1 Definition In this document: ASX Board Chair CFO Company Secretary Corporations Act Director means ASX Limited ACN 008 624 691 or the securities

Corporate Governance Statement John Bridgeman Limited 1 Definition In this document: ASX Board Chair CFO Company Secretary Corporations Act Director means ASX Limited ACN 008 624 691 or the securities

Firm Profile TURNING RISKS INTO OPPORTUNITIES

Firm Profile TURNING RISKS INTO OPPORTUNITIES You can measure opportunity with the same yardstick that measures the risk involved. They go together. Earl Nightingale TRUSTED ADVISORS RiSK Opportunities

Firm Profile TURNING RISKS INTO OPPORTUNITIES You can measure opportunity with the same yardstick that measures the risk involved. They go together. Earl Nightingale TRUSTED ADVISORS RiSK Opportunities

SRI LANKA AUDITING STANDARD 315 (REVISED)

") SRI LANKA AUDITING STANDARD 315 (REVISED) IDENTIFYING AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT THROUGH UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT (Effective for audits of financial statements

SRI LANKA AUDITING STANDARD 315 (REVISED) IDENTIFYING AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT THROUGH UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT (Effective for audits of financial statements