Week 3: Fraud, Procure to Pay Process Controls

|

|

|

- Miles Dean

- 6 years ago

- Views:

Transcription

1 Edward Beaver ff MIS 5121: Business Processes, ERP Systems & Controls Week 3: Fraud, Procure to Pay Process Controls

2 Video: Record the Class

3 Discussion v Something really new, different you learned in this course in last week v Questions you have about this week s content (readings, videos, links, )? v Question still in your mind, something not adequately answered in prior readings or classes? 3

4 Definition Risk Probability or threat of damage, injury, liability, loss, or any other negative occurrence that is caused by external or internal vulnerabilities, and that may be avoided through preemptive actions (controls?) Business Dictionary Anything that could go wrong Class Definition 4

")

5 Fraud Definition deception (misrepresentation or omission) deliberately practiced in order to secure unfair or unlawful gain 5

Ø Poor internal controls Ø Lack of")

Ø Meet")

6 Environment Favorable to Fraud Framework for spotting high- risk situations Perceived opportunity (I can do it / conceal it and not get caught) Ø Poor internal controls Ø Lack of oversight Incentive or Pressure (Financial or emotional force pushing to commit fraud) Ø Meet expectations Ø Avoid criticism Ø Cover a mistake Ø Personal failures, needs Rationalization (Personal justification for dishonest actions) Ø Low compensation Ø Company is profitable Fraud Rationalization Fraud Triangle

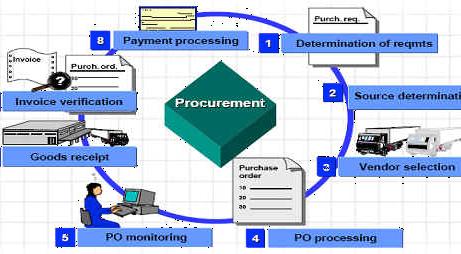

7 Business Process Controls Procure to Pay 7

8 Procurement Process

9 Procurement at GBI C u s t o m e r s Customer Service Goods Receipt Warehouse Distribution Billing Accounts Receivable Marketing / Sales Supply Chain Reqmts Conversion Finance / HR Payment Purchase Order Procurement Vendor / Sourcing Invoice Verify Accounts Payable S u p p l i e r s

10 The Many Flavors of Procurement What Does Global Bike, Inc. Procure?

Logistics Information Technology No PO Inter- company vs.")

11 The Many Flavors of Procurement Materials / Raw Materials Labor Services Other Services Leases / Rentals Supplies (Office, Maintenance, Production, ) Logistics Information Technology No PO Inter- company vs. 3 rd Party Acquisitions

12 Procure to Pay: Common Risks Vendor / Purchase Order Creation of fictitious vendors, purchase orders and service/good receipt Purchases not correctly Authorized Delivery address modification Inadequate price negotiation Price increase in purchase orders (to establish a kickback program) Records lost / destroyed Goods / Service Receipt Import / export control violations Quality of goods / services received Inventory manipulation Records lost / destroyed Over / under charged workload / hours / costs

13 Procure to Pay: Common Risks Invoice Processing / Payment Modification of vendors payment information Manipulation of client names and addresses on vouchers / refund Price increase in purchase orders (to establish a kickback program) Over / under charged workload / hours / costs Wrong payments / duplicate payments Approval of fictitious travel expenses Records lost / destroyed

14 Controls: 3- way Match SAP: Example of Configurable Control

15 Controls: GR/IR Reconciliation Account GR / IR: Goods Receipt / Invoice Receipt Standard accounting method for P2P In/Process type of account For given transaction (PO) once complete the account value should be zero Easy focus on incomplete, erroneous transactions

16 Procure to Pay: Common Controls Segregation of Duties Purchasing policies (Written, taught, monitored) Contract / PO approvals PO revisions monitored / controlled Vendor / source / price Decisions Monitored Supplier / Procurement independence Avoid Advance payments Invoices sent to A/P Monitor GR / IR Account Return Procedures (written, taught, monitored) No PO payments avoided / controlled 3- way Match used where possible

17 Reference Checklist: Standards of Internal Control for Purchasing and Ordering (Institute of Finance & Management) Checklist: Standards of Internal Control for Supplier Selection (Institute of Finance & Management)

18 Purchase- to- Pay Exercise Primary Learning objectives Experience the steps in a typical purchasing transaction See how an ERP system handles typical purchasing transactions Work through the procedures involved in a test of transactions Investigate related application controls in an ERP system Secondary learning objectives: See the integration between materials management (MM) and financial accounting (FI) modules of SAP View some basic FI module settings than enable proper system functions

19 Exercise 1: Purchase to Pay Agenda Last Class (September 12): Logging On; Steps 1-6 This Class (September 19): Steps 7-14 Due Thursday September 22 11:59 PM: Assignment Submission

20 Exercise 1: Purchase to Pay Task 7 Create a Purchase Order to Buy the Trading Good Menu: Logistics Materials Management Purchasing Purchase Order Create Vendor/Supplying Plant Known Transaction: ME21N Task 8 - Check Status of Various Accounts Check Inventory: MM Inventory Quantity Transaction: MMBE (Stock Overview) Check GL Inventory, GL Cash, GL A/P, GR/IR (Goods Received / Invoice Received): Transaction: S_ALR_ (Line Item Journal) Recommend: Use /MIS5121 Layout Variant Check A/P Vendor sub- ledger: Transaction: FBL1N (Vendor line item display)

21 Exercise 1: Purchase to Pay Task 9 Receive the Product from the Vendor Menu: Logistics Materials Management Inventory Management Goods Movement Goods Receipt For Purchase Order PO Number Known Transaction: MIGO Task 10 - Check Status of Various Accounts See details of Task 8 Task 11 Receive the Invoice from the Vendor Menu: Logistics Materials Management Purchasing Purchase Order Follow- on Functions Logistics Invoice Verification Transaction: MIRO

22 Exercise 1: Purchase to Pay Task 12 - Check Status of Various Accounts See details of Task 8 Task 13 Make the Payment to the Vendor Menu: Accounting Financial Accounting Accounts Payable Document Entry Outgoing Payment Post Transaction: F- 53 Task 14 - Check Status of Various Accounts See details of Task 8 Task 15 Write down the system- generated journal entries Non- SAP task

23 Extra Slides

24 Most Common Fraud Techniques Understatement of expenses/liabilities (31%) Other techniques such as acquisitions, JVs, netting of amounts (20%) Disguised through use of related parties (18%) Misappropriated assets (14%) Source: Fraudulent Financial Reporting and Analysis of US Public Companies by COSO 24

25 Asset Misappropriation Fraud Schemes Category Description Examples % cases Billing Non- Cash Revenue Reimburse Skimming Check tampering Cash on Hand Cash Larceny Payroll Cash Register Causes employer to issue payment by submitting invoices for fictitious goods or services, inflated invoices or invoices for personal purchases Employee steals or misuses non- cash assets of the organization Employee makes a claim for reimbursement of fictitious or inflated business expenses Cash is stolen from an organization before it is recorded on the organization's books and records Person steals his employer's funds by intercepting, forging, or altering a check drawn on one of the organization's bank accounts Perpetrator misappropriates cash kept on hand at the victim organization's premises Cash is stolen from an organization after it is recorded on the organization's books / records. Employee causes his employer to issue a payment by making false claims for compensation Person makes false entries on a cash register to conceal fraudulent removal of cash Employee creates a shell company and bills employer 26.0 % for services not actually rendered Employee steals or misuses non- cash assets of the Organization steals or misuses confidential customer financial information 16.3 % Employee files fraudulent expense report, claiming 15.1 % personal travel, etc. Employee accepts payment a customer, but does not 14.5 % record the sale, and instead pockets the money Employee steals blank company checks and makes 13.4 % them out to himself or an accomplice Employee steals cash from a company vault 12.6 % Employee steals cash and checks from daily receipts 9.8 % before they can be deposited in the bank Employee claims overtime for hours not worked or 8.5 % adds ghost employees to the payroll Employee voids a sale on the cash register and steals 3.0 % the cash Source: Association of Certified Fraud Examiners 2010 Report to the Nations on Occupational Fraud and Abuse Global Fraud Study 25

26

27 Exercise 1: Purchase to Pay Task 6 - Check Status of Various Accounts Check Inventory: MM Inventory Quantity Transaction: MMBE (Stock Overview) Check GL Inventory, GL Cash, GL A/P, GR/IR (Goods Received / Invoice Received): Transaction: S_ALR_ (Line Item Journal) Recommend: Use /MIS5121 Layout Variant Check A/P Vendor sub- ledger: Transaction: FBL1N (Vendor line item display)

Fraud in the Insurance Industry How it Can Impact Your Agency

A MarshBerry Publication Volume XXIX, Issue 4 APRIL 2013 Authored by Molly McCarthy, Senior Consultant 440.392.6584 email: Molly.McCarthy@MarshBerry.com Fraud in the Insurance Industry How it Can Impact

A MarshBerry Publication Volume XXIX, Issue 4 APRIL 2013 Authored by Molly McCarthy, Senior Consultant 440.392.6584 email: Molly.McCarthy@MarshBerry.com Fraud in the Insurance Industry How it Can Impact

SEGREGATION OF DUTIES for SAP

SEGREGATION OF DUTIES for SAP SEGREGATION-OF-DUTIES In todays modern, technology driven world, segregation-of-duties (SoD) is enforced through business applications and ERP s, but highlighting breakdowns

SEGREGATION OF DUTIES for SAP SEGREGATION-OF-DUTIES In todays modern, technology driven world, segregation-of-duties (SoD) is enforced through business applications and ERP s, but highlighting breakdowns

OUTSMART FRAUD. Strategic Internal Controls to Prevent Business Fraud

OUTSMART FRAUD Strategic Internal Controls to Prevent Business Fraud GrowthForce LLC 800 Rockmead Drive Suite 200 Phone 281.358.2007 Fax 281.358.4120 OUTSMART BUSINESS FRAUD Using statistical data from

OUTSMART FRAUD Strategic Internal Controls to Prevent Business Fraud GrowthForce LLC 800 Rockmead Drive Suite 200 Phone 281.358.2007 Fax 281.358.4120 OUTSMART BUSINESS FRAUD Using statistical data from

Eric Kinsherf, CPA MMAAA Conference June 12, 2018

Eric Kinsherf, CPA MMAAA Conference June 12, 2018 Agenda Overview What is Fraud? How does Fraud happen? How to Detect and Prevent Fraud Summarize Objectives Gain better Understanding of Fraud Risk Illustrate

Eric Kinsherf, CPA MMAAA Conference June 12, 2018 Agenda Overview What is Fraud? How does Fraud happen? How to Detect and Prevent Fraud Summarize Objectives Gain better Understanding of Fraud Risk Illustrate

Fraud Prevention Training

Fraud Prevention Training The Massachusetts Collectors and Treasurers Association Sixty-Sixth Annual Education Conference June 15, 2015 Presented By: Eric Demas, CFE Melanson Heath edemas@melansonheath.com

Fraud Prevention Training The Massachusetts Collectors and Treasurers Association Sixty-Sixth Annual Education Conference June 15, 2015 Presented By: Eric Demas, CFE Melanson Heath edemas@melansonheath.com

STUDY UNIT TEN INTERNAL AUDIT RESPONSIBILITIES FOR FRAUD

STUDY UNIT TEN INTERNAL AUDIT RESPONSIBILITIES FOR FRAUD 1 10.1 Fraud -- Nature, Prevention, and Detection..................................... 1 10.2 Fraud -- Indicators........................................................

STUDY UNIT TEN INTERNAL AUDIT RESPONSIBILITIES FOR FRAUD 1 10.1 Fraud -- Nature, Prevention, and Detection..................................... 1 10.2 Fraud -- Indicators........................................................

MIS 5208 Week 2 Fraud Detection & Prevention

MIS 5208 Week 2 Fraud Detection & Prevention Introductions, Course Outline, and Other Administration Issues Ed Ferrara, MSIA, CISSP eferrara@temple.edu Fraud Awareness & Internal Controls Awareness Internal

MIS 5208 Week 2 Fraud Detection & Prevention Introductions, Course Outline, and Other Administration Issues Ed Ferrara, MSIA, CISSP eferrara@temple.edu Fraud Awareness & Internal Controls Awareness Internal

ACL ESSENTIALS. Get insight into your ERP process health, compliance & financial exposure SEGEREGATION OF DUTIES

ACL ESSENTIALS Get insight into your ERP process health, compliance & financial exposure SEGEREGATION OF DUTIES Page Analytic Name User creates a vendor and an invoice for this vendor SD Analytic 01 User

ACL ESSENTIALS Get insight into your ERP process health, compliance & financial exposure SEGEREGATION OF DUTIES Page Analytic Name User creates a vendor and an invoice for this vendor SD Analytic 01 User

Effective Internal Control Strategies

Effective Internal Control Strategies 1. The unique nonprofit environment A. Reliance on contributed services of volunteers B. Many volunteers have a limited nonprofit financial background C. Revenue often

Effective Internal Control Strategies 1. The unique nonprofit environment A. Reliance on contributed services of volunteers B. Many volunteers have a limited nonprofit financial background C. Revenue often

Can You Spot Fraudsters?

Can You Spot Fraudsters? CACUBO Workshop March 22, 2018 Eric Conforti, CPA, CFE 1 Who Are We? A One-Firm Firm: Over 2,200 industry experts to partner with when specific industry knowledge is needed during

Can You Spot Fraudsters? CACUBO Workshop March 22, 2018 Eric Conforti, CPA, CFE 1 Who Are We? A One-Firm Firm: Over 2,200 industry experts to partner with when specific industry knowledge is needed during

MIS 5121:Business Processes, ERP Systems & Controls Week 13: SAP Futures, Special System Access. Edward Beaver

MIS 5121:Business Processes, ERP Systems & Controls Week 13: SAP Futures, Special System Access Edward Beaver Edward.Beaver@temple.edu ff MIS 5121: Upcoming Events Guest Moderator: SAP Futures - December

MIS 5121:Business Processes, ERP Systems & Controls Week 13: SAP Futures, Special System Access Edward Beaver Edward.Beaver@temple.edu ff MIS 5121: Upcoming Events Guest Moderator: SAP Futures - December

2/20/15. Trevor Stewart, CPA Director of Business Services Source documentation includes CCIA and FCMAT

2/20/15 Trevor Stewart, CPA Director of Business Services Source documentation includes CCIA and FCMAT The Fraud Triangle factors that influence the commission of fraud The Fraud Tree occupational fraud

2/20/15 Trevor Stewart, CPA Director of Business Services Source documentation includes CCIA and FCMAT The Fraud Triangle factors that influence the commission of fraud The Fraud Tree occupational fraud

Alyssa G. Martin, CPA Brandon Tanous, CIA, Using the COSO CFE, CGAP, CRMA Framework to Develop a Strong and Preventive Control Environment

Speakers Using the COSO Framework to Develop a Strong and Preventive Control Environment Weaver Public Sector CPE Event Alyssa G. Martin, CPA Dallas Executive Partner, Advisory Services 25+ years of public

Speakers Using the COSO Framework to Develop a Strong and Preventive Control Environment Weaver Public Sector CPE Event Alyssa G. Martin, CPA Dallas Executive Partner, Advisory Services 25+ years of public

Christopher Dawkins, CPA, CIA Director of County Audit Phil Diamond, CPA Orange County Comptroller s Office

Christopher Dawkins, CPA, CIA Director of County Audit Phil Diamond, CPA Orange County Comptroller s Office What Will I Talk About? Why we have auditors and the difference between external auditors and

Christopher Dawkins, CPA, CIA Director of County Audit Phil Diamond, CPA Orange County Comptroller s Office What Will I Talk About? Why we have auditors and the difference between external auditors and

Fraud: Welcome to Your Worst Nightmare

Fraud: Welcome to Your Worst Nightmare Fraud: It can happen to you A Not-For-Profit Fraud Survey conducted by BDO in 2014 highlighted the following facts concerning fraud in Australia & New Zealand among

Fraud: Welcome to Your Worst Nightmare Fraud: It can happen to you A Not-For-Profit Fraud Survey conducted by BDO in 2014 highlighted the following facts concerning fraud in Australia & New Zealand among

FRD510. Principles of Fraud Examination - 20 hours. Objectives

FRD510 Principles of Fraud Examination - 20 hours Objectives Call them the CSI experts of the financial world. Accountants play a central role in the detection and deterrence of fraud in all its notorious

FRD510 Principles of Fraud Examination - 20 hours Objectives Call them the CSI experts of the financial world. Accountants play a central role in the detection and deterrence of fraud in all its notorious

MIS 5121:Business Processes, ERP Systems & Controls Week 12: Table Security, Systems Development 2, Control Framework

MIS 5121:Business Processes, ERP Systems & Controls Week 12: Table Security, Systems Development 2, Control Framework Edward Beaver Edward.Beaver@temple.edu ff Video: Record the Class Discussion v Something

MIS 5121:Business Processes, ERP Systems & Controls Week 12: Table Security, Systems Development 2, Control Framework Edward Beaver Edward.Beaver@temple.edu ff Video: Record the Class Discussion v Something

Fraud Prevention, Detection and Control. Elizabeth Coles, CPA Aldrich CPAs + Advisors LLP

Fraud Prevention, Detection and Control Elizabeth Coles, CPA Aldrich CPAs + Advisors LLP 1 Agenda Who and Why? Fraud Schemes and Risks Fraud Prevention what can you do? 3 Who Commits Fraud? Long time,

Fraud Prevention, Detection and Control Elizabeth Coles, CPA Aldrich CPAs + Advisors LLP 1 Agenda Who and Why? Fraud Schemes and Risks Fraud Prevention what can you do? 3 Who Commits Fraud? Long time,

FRAUD SCHEMES. South Carolina HFMA Finance & Reimbursement Forum. November 13, 2012 WITH RELATED INTERNAL CONTROLS

FRAUD SCHEMES WITH RELATED INTERNAL CONTROLS South Carolina HFMA Finance & Reimbursement Forum November 13, 2012 2 Fraud Facts: Estimated loss of 5% of annual revenues to occupational fraud Financial statement

FRAUD SCHEMES WITH RELATED INTERNAL CONTROLS South Carolina HFMA Finance & Reimbursement Forum November 13, 2012 2 Fraud Facts: Estimated loss of 5% of annual revenues to occupational fraud Financial statement

Presented by Ed Williamson and Erica Bailey

Presented by Ed Williamson and Erica Bailey Internal Controls & Fraud Detection Objectives Background on internal controls Review of organizational and functional level controls Fraud prevention and risk

Presented by Ed Williamson and Erica Bailey Internal Controls & Fraud Detection Objectives Background on internal controls Review of organizational and functional level controls Fraud prevention and risk

SMALL BUSINESS FRAUD ASSESSMENT INTERNAL CONTROL QUESTIONNAIRE Download your risk assessment form at

SMALL BUSINESS FRAUD ASSESSMENT INTERNAL CONTROL QUESTIONNAIRE Download your risk assessment form at www.businessfraudprevention.org/forms.html Owner: Date: Discussed with: Question Yes No N/A Comments

SMALL BUSINESS FRAUD ASSESSMENT INTERNAL CONTROL QUESTIONNAIRE Download your risk assessment form at www.businessfraudprevention.org/forms.html Owner: Date: Discussed with: Question Yes No N/A Comments

Accounts Payable. Accounting FI02. May-09 1

Accounts Payable Accounting FI02 May-09 1 Course Outline Course Outline Finance Organizational structures & Accounts Payable Master Data Accounting Transaction In Accounts Payable Period End closing in

Accounts Payable Accounting FI02 May-09 1 Course Outline Course Outline Finance Organizational structures & Accounts Payable Master Data Accounting Transaction In Accounts Payable Period End closing in

Fraud Prevention, Detection, and Internal Controls

Fraud Prevention, Detection, and Internal Controls Budget, Accounting and Reporting Council May 28, 2015 Sherrie Ard, CPA, CFE Financial Management Specialist Local Government Performance Center Local

Fraud Prevention, Detection, and Internal Controls Budget, Accounting and Reporting Council May 28, 2015 Sherrie Ard, CPA, CFE Financial Management Specialist Local Government Performance Center Local

SAP FICO Syllabus SAP TRAINING DIVISION. SAP ECC 6.0 FICO Contents. SAP Overview

SAP TRAINING DIVISION SAP FICO Syllabus SAP ECC 6.0 FICO Contents SAP Overview Ø Introduction to ERP And SAP Ø History of SAP Ø Organization Ø Technology Ø Implementation Tools (Asap and Solution Manager)

SAP TRAINING DIVISION SAP FICO Syllabus SAP ECC 6.0 FICO Contents SAP Overview Ø Introduction to ERP And SAP Ø History of SAP Ø Organization Ø Technology Ø Implementation Tools (Asap and Solution Manager)

716 West Ave Austin, TX USA

Fundamentals of Computer and Internet Fraud GLOBAL Headquarters the gregor building 716 West Ave Austin, TX 78701-2727 USA II. THE USE OF COMPUTERS IN OCCUPATIONAL FRAUD Occupational fraud refers to the

Fundamentals of Computer and Internet Fraud GLOBAL Headquarters the gregor building 716 West Ave Austin, TX 78701-2727 USA II. THE USE OF COMPUTERS IN OCCUPATIONAL FRAUD Occupational fraud refers to the

Financial Controls Checklist

Financial Controls Checklist Board of Health: Board of Health for the Leeds, Grenville & Lanark District Health Unit Period ended: Dec. 31/17 Objective: The objective of the Financial Controls Checklist

Financial Controls Checklist Board of Health: Board of Health for the Leeds, Grenville & Lanark District Health Unit Period ended: Dec. 31/17 Objective: The objective of the Financial Controls Checklist

All the Inventory transactions will look for the valuation class and the corresponding G.L. Accounts and post the values in the G.L accounts.

Inventory Accounting Entries All the Inventory transactions will look for the valuation class and the corresponding G.L. Accounts and post the values in the G.L accounts. For Example: during Goods Receipt

Inventory Accounting Entries All the Inventory transactions will look for the valuation class and the corresponding G.L. Accounts and post the values in the G.L accounts. For Example: during Goods Receipt

Karen L. Mosteller, CPA, CHBC

Karen L. Mosteller, CPA, CHBC Recognize the Red Flags of Fraud and areas of vulnerability Examine checks and balances that should be implemented Establish processes and procedures needed for fraud protection

Karen L. Mosteller, CPA, CHBC Recognize the Red Flags of Fraud and areas of vulnerability Examine checks and balances that should be implemented Establish processes and procedures needed for fraud protection

Fraud Risk Management

Fraud Risk Management Using Automated Continuous Monitoring Tools 2017 Association of Certified Fraud Examiners, Inc. Discussion Questions 1. Does your organization use continuous and/or automated monitoring

Fraud Risk Management Using Automated Continuous Monitoring Tools 2017 Association of Certified Fraud Examiners, Inc. Discussion Questions 1. Does your organization use continuous and/or automated monitoring

Laurie Beets. PDG 27 th National College & University Bursars & SFS Conference

Foiling Fraudsters Laurie Beets Oklahoma State University Acknowledgements 2006 Fraud Examiners Manual, Association of Certified Fraud Examiners (ACFE) 2012 Report to the Nation on Occupational Fraud &

Foiling Fraudsters Laurie Beets Oklahoma State University Acknowledgements 2006 Fraud Examiners Manual, Association of Certified Fraud Examiners (ACFE) 2012 Report to the Nation on Occupational Fraud &

Detecting & Preventing Procurement Fraud Using Data Analysis to Detect Improper Disbursements

Detecting & Preventing Procurement Fraud Using Data Analysis to Detect Improper Disbursements April 29, 2014 2:00 3:00pm ET Andrew Simpson, MBA Chief Operating Officer, CaseWare Analytics Paul Soos, CFE,

Detecting & Preventing Procurement Fraud Using Data Analysis to Detect Improper Disbursements April 29, 2014 2:00 3:00pm ET Andrew Simpson, MBA Chief Operating Officer, CaseWare Analytics Paul Soos, CFE,

SAP MM - PROCUREMENT CYCLE

SAP MM - PROCUREMENT CYCLE http://www.tutorialspoint.com/sap_mm/sap_mm_procurement_cycle.htm Copyright tutorialspoint.com Every organization acquires material or services to complete its business needs.

SAP MM - PROCUREMENT CYCLE http://www.tutorialspoint.com/sap_mm/sap_mm_procurement_cycle.htm Copyright tutorialspoint.com Every organization acquires material or services to complete its business needs.

Chapter 12: The Revenue Cycle

Chapter 12: The Revenue Cycle Syaiful Ali, SE., MIS., Ak. Introduction Revenue Cycles tend to be similar for all types of firms. Two subsystems perform the processing steps within the revenue cycle: The

Chapter 12: The Revenue Cycle Syaiful Ali, SE., MIS., Ak. Introduction Revenue Cycles tend to be similar for all types of firms. Two subsystems perform the processing steps within the revenue cycle: The

Internal Controls Integrating COSO

Community Action Partnership 2016 Annual Convention August 30 September 2, 2016 Austin, TX J.W. Marriott Austin Internal Controls Integrating COSO Thursday, September 1, 2016 9:15 am 10:45 am Presented

Community Action Partnership 2016 Annual Convention August 30 September 2, 2016 Austin, TX J.W. Marriott Austin Internal Controls Integrating COSO Thursday, September 1, 2016 9:15 am 10:45 am Presented

FRAUD DETERRENCE AND DETECTION

FRAUD DETERRENCE AND DETECTION Segregation of Duties Corruption Scheme Red Flags Unchecked authority to approve No formal documented procedures Circumventing normal policies and procedures Employees receiving

FRAUD DETERRENCE AND DETECTION Segregation of Duties Corruption Scheme Red Flags Unchecked authority to approve No formal documented procedures Circumventing normal policies and procedures Employees receiving

ACCTG 533: Module 14: Asset Misappropriation Fraud. [Slide Content]: Asset Misappropriation Fraud. [Jeanne H. Yamamura]: Asset Misappropriation Fraud

![ACCTG 533: Module 14: Asset Misappropriation Fraud. [Slide Content]: Asset Misappropriation Fraud. [Jeanne H. Yamamura]: Asset Misappropriation Fraud](/thumbs/81/83190759.jpg "ACCTG 533: Module 14: Asset Misappropriation Fraud. [Slide Content]: Asset Misappropriation Fraud. [Jeanne H. Yamamura]: Asset Misappropriation Fraud") ACCTG 533: Module 14: Asset Misappropriation Fraud Asset Misappropriation Fraud Asset Misappropriation Fraud Asset Misappropriation Fraud Theft or misuse of company assets Most common type of fraud Every

ACCTG 533: Module 14: Asset Misappropriation Fraud Asset Misappropriation Fraud Asset Misappropriation Fraud Asset Misappropriation Fraud Theft or misuse of company assets Most common type of fraud Every

Division of Student Affairs Internal Control Questionnaire FY 2011

Control Environment Yes No N/A Notations Are the roles and responsibilities of financial and administrative staff (including the establishment of the unit Director as the appropriate signature authority)

Control Environment Yes No N/A Notations Are the roles and responsibilities of financial and administrative staff (including the establishment of the unit Director as the appropriate signature authority)

Virginia Association of School Business Officers Getting Reacquainted with Internal Controls Presented by John S. Aldridge, CPA

Virginia Association of School Business Officers Getting Reacquainted with Internal Controls Presented by John S. Aldridge, CPA Introduction What are internal controls? Simple Definition Internal control

Virginia Association of School Business Officers Getting Reacquainted with Internal Controls Presented by John S. Aldridge, CPA Introduction What are internal controls? Simple Definition Internal control

BFSv9 Internal Controls Guidance

presented by: Hans Gude, MBA, CIA Barbara VanCleave Smith, PhD, CPA Office of Ethics, Compliance, and Risk Management Presented May 10 and 17, 2010 LMS Course Number BECTR306 1 Today s Topics 1. Overview

presented by: Hans Gude, MBA, CIA Barbara VanCleave Smith, PhD, CPA Office of Ethics, Compliance, and Risk Management Presented May 10 and 17, 2010 LMS Course Number BECTR306 1 Today s Topics 1. Overview

Fraud Risk Management

Fraud Risk Management Specific Anti-Fraud Controls (Process or Transaction Level) 2017 Association of Certified Fraud Examiners, Inc. Discussion Questions 1. Does your organization have adequate staffing

Fraud Risk Management Specific Anti-Fraud Controls (Process or Transaction Level) 2017 Association of Certified Fraud Examiners, Inc. Discussion Questions 1. Does your organization have adequate staffing

Purchase-to-Pay Assignment Using SAP ERP

Purchase-to-Pay Assignment Using SAP ERP The objective of this assignment is for you to become familiar with the steps and the documents involved in a typical purchasing transaction and also investigate

Purchase-to-Pay Assignment Using SAP ERP The objective of this assignment is for you to become familiar with the steps and the documents involved in a typical purchasing transaction and also investigate

Fraud Awareness February 27, 2015

Fraud Awareness February 27, 2015 Clara Ewing Megan Dix Fraud Defined The term fraud is defined in Black's Law Dictionary (Sixth Edition, 1990) as: An intentional perversion of truth for the purpose of

Fraud Awareness February 27, 2015 Clara Ewing Megan Dix Fraud Defined The term fraud is defined in Black's Law Dictionary (Sixth Edition, 1990) as: An intentional perversion of truth for the purpose of

Cash Receipting: Fraud Prevention and Internal Controls

Office of the Washington State Auditor Pat McCarthy Cash Receipting: Fraud Prevention and Internal Controls WACO Annual Conference October 3, 2018 Table of Contents Fraud Statistics and Overview... 2 Importance

Office of the Washington State Auditor Pat McCarthy Cash Receipting: Fraud Prevention and Internal Controls WACO Annual Conference October 3, 2018 Table of Contents Fraud Statistics and Overview... 2 Importance

INTERNAL CONTROLS. Revision A

INTERNAL CONTROLS Internal Controls Approved. CHANGE HISTORY Sections Affected/Description of Change Section All: Consolidate original document and all changes approved Through ; standardize formatting

INTERNAL CONTROLS Internal Controls Approved. CHANGE HISTORY Sections Affected/Description of Change Section All: Consolidate original document and all changes approved Through ; standardize formatting

Contract and Procurement Fraud. Fraud in Procurement without Competition

Contract and Procurement Fraud Fraud in Procurement without Competition Sole-Source Awards Noncompetitive procurement process through the solicitation of only one source Procurement through sole-source

Contract and Procurement Fraud Fraud in Procurement without Competition Sole-Source Awards Noncompetitive procurement process through the solicitation of only one source Procurement through sole-source

Creating a Fraud Risk Assessment and Implementing a Continuous Monitoring Program. Christopher DiLorenzo, CFE, CPA, CIA, CRMA

Creating a Fraud Risk Assessment and Implementing a Continuous Monitoring Program Christopher DiLorenzo, CFE, CPA, CIA, CRMA 2015 Association of Certified Fraud Examiners, Inc. Creating a Robust Fraud

Creating a Fraud Risk Assessment and Implementing a Continuous Monitoring Program Christopher DiLorenzo, CFE, CPA, CIA, CRMA 2015 Association of Certified Fraud Examiners, Inc. Creating a Robust Fraud

OVERVIEW 4/19/10. Internal Controls and the Audit Process May 4, 2010 OVERVIEW. Definition and historical perspective of internal auditing

and the Audit Process May 4, 2010 Presented by: Deborah A. Stevens CPA Wichita County Auditor 1 OVERVIEW Definition and historical perspective of internal auditing Role and responsibilities of the internal

and the Audit Process May 4, 2010 Presented by: Deborah A. Stevens CPA Wichita County Auditor 1 OVERVIEW Definition and historical perspective of internal auditing Role and responsibilities of the internal

This Questionnaire/Guide is intended to assist you in decision making, as well as in day-to-day operations. Best Regards,

In an effort to disseminate information and assure that we are in compliance with guidelines caused by the Sarbanes Oxley Act that proper internal controls are being adhered to, we have developed some

In an effort to disseminate information and assure that we are in compliance with guidelines caused by the Sarbanes Oxley Act that proper internal controls are being adhered to, we have developed some

INTERNAL CONTROLS REVIEW PROGRESS REPORT Yellow highlighted items have been completed/validated since last report in August 2016

INTERNAL S REVIEW PROGRESS REPORT Yellow highlighted items have been completed/validated since last report in August 2016 RECOMMENDATIONS ADDRESSED THROUGH INTERNAL AUDIT WORK PLANS Monthly Reconciliation

INTERNAL S REVIEW PROGRESS REPORT Yellow highlighted items have been completed/validated since last report in August 2016 RECOMMENDATIONS ADDRESSED THROUGH INTERNAL AUDIT WORK PLANS Monthly Reconciliation

ACL ESSENTIALS. Get insight into your ERP process health, compliance & financial exposure PURCHASE ORDER MANAGEMENT

ACL ESSENTIALS Get insight into your ERP process health, compliance & financial exposure PURCHASE ORDER MANAGEMENT Page Analytic Name Split purchase orders PO Analytic 01 Duplicate purchase orders PO Analytic

ACL ESSENTIALS Get insight into your ERP process health, compliance & financial exposure PURCHASE ORDER MANAGEMENT Page Analytic Name Split purchase orders PO Analytic 01 Duplicate purchase orders PO Analytic

Information and and training provid v ed by Smith Elliott Elliott Kearns & Compan

Nuts and Bolts of Avoiding Fraud in Your Organization Information and training provided by Smith Elliott Kearns & Company, LLC as part of this Fraud Avoidance presentation is intended for reference only.

Nuts and Bolts of Avoiding Fraud in Your Organization Information and training provided by Smith Elliott Kearns & Company, LLC as part of this Fraud Avoidance presentation is intended for reference only.

INTERNAL CONTROLS REVIEW PROGRESS REPORT Highlighted items have been completed since last report in January 2016

INTERNAL S REVIEW PROGRESS REPORT Highlighted items have been completed since last report in January 2016 RECOMMENDATIONS ADDRESSED THROUGH INTERNAL AUDIT WORK PLANS Internal Audit: prepare documentation

INTERNAL S REVIEW PROGRESS REPORT Highlighted items have been completed since last report in January 2016 RECOMMENDATIONS ADDRESSED THROUGH INTERNAL AUDIT WORK PLANS Internal Audit: prepare documentation

GFMIS. MIS MIS - BW SEM Operating System SAP R/3 (GFMIS) FI CO. e-payroll, e-pension AFMIS. ก ก (e-catalog,e-shopping list

FI CO. e-payroll, e-pension AFMIS. ก ก (e-catalog,e-shopping list") ก GFMIS: ก. 1 GFMIS MIS ( ) MIS - BW SEM Operating System SAP R/3 (GFMIS) FM PO HR ก FI ก ก RP AP ก CM FA GL ก CO BIS. DPIS ก. e-procurement ก ก (e-catalog,e-shopping list e-auction) e-payroll, e-pension

ก GFMIS: ก. 1 GFMIS MIS ( ) MIS - BW SEM Operating System SAP R/3 (GFMIS) FM PO HR ก FI ก ก RP AP ก CM FA GL ก CO BIS. DPIS ก. e-procurement ก ก (e-catalog,e-shopping list e-auction) e-payroll, e-pension

INTERNAL CONTROLS REVIEW PROGRESS REPORT Yellow highlighted items have been updated since last report in October 2017

INTERNAL S REVIEW PROGRESS REPORT Yellow highlighted items have been updated since last report in October 2017 RECOMMENDATIONS ADDRESSED THROUGH INTERNAL AUDIT WORK PLANS Internal Audit: prepare documentation

INTERNAL S REVIEW PROGRESS REPORT Yellow highlighted items have been updated since last report in October 2017 RECOMMENDATIONS ADDRESSED THROUGH INTERNAL AUDIT WORK PLANS Internal Audit: prepare documentation

A Practical Guide To Internal Controls

A Practical Guide To Internal Controls 1 Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations, was issued pursuant to the Single Audit Act of 1984, P.L. 98-502, and the Single

A Practical Guide To Internal Controls 1 Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations, was issued pursuant to the Single Audit Act of 1984, P.L. 98-502, and the Single

Contract and Procurement Fraud

Contract and Procurement Fraud Performance Schemes 2018 Association of Certified Fraud Examiners, Inc. Invoicing Schemes Vendor submits fraudulent invoices to generate false payments. False invoices Inflated

Contract and Procurement Fraud Performance Schemes 2018 Association of Certified Fraud Examiners, Inc. Invoicing Schemes Vendor submits fraudulent invoices to generate false payments. False invoices Inflated

Fraud and Business Analytics

Study Unit 6 Fraud and Business Analytics ANL 309 Business Analytics Applications Introduction Fraud Different types of fraud Two common types of customer fraud: mortgage fraud and credit card fraud Why

Study Unit 6 Fraud and Business Analytics ANL 309 Business Analytics Applications Introduction Fraud Different types of fraud Two common types of customer fraud: mortgage fraud and credit card fraud Why

Cash Receipting: Fraud Prevention and Internal Controls

Cash Receipting: Fraud Prevention and Internal Controls Your government works hard to serve its residents with the resources available. This can mean that the internal processes you rely on to do your

Cash Receipting: Fraud Prevention and Internal Controls Your government works hard to serve its residents with the resources available. This can mean that the internal processes you rely on to do your

APPENDIX 2 COMMUNITY DEVELOPMENT COMMISSION FINANCIAL CHECKLIST REQUIRED FOR ALL APPLICANTS (A SITE VISIT MAY BE CONDUCTED LATER)

") REQUIRED FOR ALL APPLICANTS (A SITE VISIT MAY BE CONDUCTED LATER) AGENCY NAME: AGENCY ADDRESS AGENCY PHONE: DATE PREPARED: PREPARED BY: TITLE: EMAIL: AGENCY GENERAL INFORMATION EXECUTIVE DIRECTOR /CITY

REQUIRED FOR ALL APPLICANTS (A SITE VISIT MAY BE CONDUCTED LATER) AGENCY NAME: AGENCY ADDRESS AGENCY PHONE: DATE PREPARED: PREPARED BY: TITLE: EMAIL: AGENCY GENERAL INFORMATION EXECUTIVE DIRECTOR /CITY

Financial Transactions and Fraud Schemes

Financial Transactions and Fraud Schemes Asset Misappropriation: Cash Receipts 2016 Association of Certified Fraud Examiners, Inc. Fraud Tree 2016 Association of Certified Fraud Examiners, Inc. 2 of 27

Financial Transactions and Fraud Schemes Asset Misappropriation: Cash Receipts 2016 Association of Certified Fraud Examiners, Inc. Fraud Tree 2016 Association of Certified Fraud Examiners, Inc. 2 of 27

2/20/2014. Agenda. Allen Still & Ryan Merryman March 31, CLAconnect.com CliftonLarsonAllen LLP Continuous Auditing Programs

Continuous Auditing Programs Allen Still & Ryan Merryman March 31, 2014 CLAconnect.com Agenda Presentation Objectives Defining Continuous Auditing Programs The Benefits of Continuous Auditing Demonstration

Continuous Auditing Programs Allen Still & Ryan Merryman March 31, 2014 CLAconnect.com Agenda Presentation Objectives Defining Continuous Auditing Programs The Benefits of Continuous Auditing Demonstration

INTERNAL CONTROLS REVIEW PROGRESS REPORT Yellow highlighted items have been updated since last report in October 2016

INTERNAL S REVIEW PROGRESS REPORT Yellow highlighted items have been updated since last report in October 2016 RECOMMENDATIONS ADDRESSED THROUGH INTERNAL AUDIT WORK PLANS Internal Audit: prepare documentation

INTERNAL S REVIEW PROGRESS REPORT Yellow highlighted items have been updated since last report in October 2016 RECOMMENDATIONS ADDRESSED THROUGH INTERNAL AUDIT WORK PLANS Internal Audit: prepare documentation

With Jodi Kippe, CPA & Partner Retail Dealer Practice at Crowe Horwath LLP. Moderated by Mike Bowers, Executive Editor at DealersEdge

How to Identify and Stop Internal Theft in the Dealership! Failing to be alert for employee schemes to embezzle or otherwise steal from the dealership can be not only costly - It's embarrassing! With Jodi

How to Identify and Stop Internal Theft in the Dealership! Failing to be alert for employee schemes to embezzle or otherwise steal from the dealership can be not only costly - It's embarrassing! With Jodi

Contract and Procurement Fraud

Contract and Procurement Fraud Fraud in Procurement Without Competition 2018 Association of Certified Fraud Examiners, Inc. Sole-Source Awards The procurement process is noncompetitive through the solicitation

Contract and Procurement Fraud Fraud in Procurement Without Competition 2018 Association of Certified Fraud Examiners, Inc. Sole-Source Awards The procurement process is noncompetitive through the solicitation

Chapter 5 Purchase Order to Payment

Chapter 5 Purchase Order to Payment Purchase order process of creating order to making vendor payment. Product SAP ERP G.B.I. Release 6.04 Level Undergraduate Beginner Focus MM Purchase Order Authors Simha

Chapter 5 Purchase Order to Payment Purchase order process of creating order to making vendor payment. Product SAP ERP G.B.I. Release 6.04 Level Undergraduate Beginner Focus MM Purchase Order Authors Simha

Chapter 2 (new version)

") Chapter 2 (new version) MULTIPLE CHOICE 1. An agreement between two entities to exchange goods or services or any other event that can be measured in economic terms by an organization is a) give-get exchange

Chapter 2 (new version) MULTIPLE CHOICE 1. An agreement between two entities to exchange goods or services or any other event that can be measured in economic terms by an organization is a) give-get exchange

FRAUD AWARENESS UPDATE

Tammy Michaud, CPA, Principal Sarah Belliveau, CPA, Senior Manager FRAUD AWARENESS UPDATE berrydunn.com CATEGORIES OF FRAUD Asset misappropriations (stealing) Theft or misuse of assets Corruption Inappropriate

Tammy Michaud, CPA, Principal Sarah Belliveau, CPA, Senior Manager FRAUD AWARENESS UPDATE berrydunn.com CATEGORIES OF FRAUD Asset misappropriations (stealing) Theft or misuse of assets Corruption Inappropriate

Journal of Business & Economics Research January 2006 Volume 4, Number 1

Family Owned Business Fraud: The Silent Thief M. Tony Bledsoe, (E-mail: bledsoem@meredith.edu), Meredith College Susan B. Wessels, (E-mail: wesselss@meredith.edu), Meredith College Abstract The ACFE 2002

Family Owned Business Fraud: The Silent Thief M. Tony Bledsoe, (E-mail: bledsoem@meredith.edu), Meredith College Susan B. Wessels, (E-mail: wesselss@meredith.edu), Meredith College Abstract The ACFE 2002

Internal Controls. They Are Everyone s Business. Valdosta State University Office of Internal Audits June 2016

Internal Controls They Are Everyone s Business Valdosta State University Office of Internal Audits June 2016 1 Presentation Overview Understand Internal Controls Identify Control Weaknesses Fraud Best

Internal Controls They Are Everyone s Business Valdosta State University Office of Internal Audits June 2016 1 Presentation Overview Understand Internal Controls Identify Control Weaknesses Fraud Best

MIS 5121:Business Processes, ERP Systems & Controls Week 10: Data Migration & Interfaces, Segregation of Duties (SOD) 2

2") MIS 5121:Business Processes, ERP Systems & Controls Week 10: Data Migration & Interfaces, Segregation of Duties (SOD) 2 Edward Beaver Edward.Beaver@temple.edu ff Video: Record the Class Discussion v Something

MIS 5121:Business Processes, ERP Systems & Controls Week 10: Data Migration & Interfaces, Segregation of Duties (SOD) 2 Edward Beaver Edward.Beaver@temple.edu ff Video: Record the Class Discussion v Something

Sage MAS 90 and 200 Product Update 2 Delivers Added Value!

Sage MAS 90 and 200 Product Update 2 Delivers Added Value! The second Sage MAS 90 and 200 4.4 Product Update 4.40.0.2 is available via a compact download from Sage Online. Delivering additional features

Sage MAS 90 and 200 Product Update 2 Delivers Added Value! The second Sage MAS 90 and 200 4.4 Product Update 4.40.0.2 is available via a compact download from Sage Online. Delivering additional features

MSD Internal Control Policy 01/16/08. Metropolitan Sewerage District of Buncombe County Internal Control Policy

Metropolitan Sewerage District of Buncombe County Internal Control Policy Purpose: To document how the management of the Metropolitan Sewerage District of Buncombe County ( District ) has fulfilled their

Metropolitan Sewerage District of Buncombe County Internal Control Policy Purpose: To document how the management of the Metropolitan Sewerage District of Buncombe County ( District ) has fulfilled their

Alfa Laval (India) Limited Whistle Blower Policy

Limited Whistle Blower Policy") Alfa Laval India Limited expects employees and Business Associates* to report breaches, or suspected breaches of the law, Alfa Laval Business Principles, policies and/or any violation of Alfa Laval Code

Alfa Laval India Limited expects employees and Business Associates* to report breaches, or suspected breaches of the law, Alfa Laval Business Principles, policies and/or any violation of Alfa Laval Code

With Jodi Kippe, CPA & Partner Retail Dealer Practice at Crowe Horwath LLP. Moderated by Mike Bowers, Executive Editor at DealersEdge

How to Identify and Stop Internal Theft in the Dealership! Failing to be alert for employee schemes to embezzle or otherwise steal from the dealership can be not only costly - It's embarrassing! With Jodi

How to Identify and Stop Internal Theft in the Dealership! Failing to be alert for employee schemes to embezzle or otherwise steal from the dealership can be not only costly - It's embarrassing! With Jodi

Advanced Finance for Governing Board Members. Charter Schools: Advancing the Promise!! 2015 Annual Conference

Advanced Finance for Governing Board Members Charter Schools: Advancing the Promise!! 2015 Annual Conference Governing Body Responsibilities with regard to finance Fiduciary responsibilities outlined in

Advanced Finance for Governing Board Members Charter Schools: Advancing the Promise!! 2015 Annual Conference Governing Body Responsibilities with regard to finance Fiduciary responsibilities outlined in

AUDIT STATUS. Continuous Auditing Ideas and Priority Ranking Draft: 8/7/2012

Compliance Identify single day stays and subsequent re-admissions Identify inappropriate unbundling of lab tests Identify frequent use of high risk organizations Match OIG-excluded providers list with

Compliance Identify single day stays and subsequent re-admissions Identify inappropriate unbundling of lab tests Identify frequent use of high risk organizations Match OIG-excluded providers list with

Contents. 1. Introduction Services Application Standards Real Estate Management ERP Solution Production Management 47

ERP Application Contents 1. Introduction 3 7. Services 42 2. Application Standards 5 8. Real Estate 44 3. ERP Solution 10 9. Production 47 4. Accounts 11 5. Inventory 30 10. Car Rentals 49 11. HRMS & Payroll

ERP Application Contents 1. Introduction 3 7. Services 42 2. Application Standards 5 8. Real Estate 44 3. ERP Solution 10 9. Production 47 4. Accounts 11 5. Inventory 30 10. Car Rentals 49 11. HRMS & Payroll

Chapter 7 Internal Controls

Chapter 7 Internal Controls Establishment of and adherence to internal controls is a major part of managing an organization. Internal controls serve as the first line of defense in safeguarding assets

Chapter 7 Internal Controls Establishment of and adherence to internal controls is a major part of managing an organization. Internal controls serve as the first line of defense in safeguarding assets

Materials Management

Materials Management 1. In which of the following cases can you define scales for the condition type a. Purchase order b. Contract c. Info record d. Vendor e. Quotation f. Scheduling agreement 2. What

Materials Management 1. In which of the following cases can you define scales for the condition type a. Purchase order b. Contract c. Info record d. Vendor e. Quotation f. Scheduling agreement 2. What

Chapter 13: The Expenditure Cycle

Accounting Information Systems: Essential Concepts and Applications Fourth Edition by Wilkinson, Cerullo, Raval, and Wong-On-Wing Chapter 13: The Expenditure Cycle Slides Authored by Somnath Bhattacharya,

Accounting Information Systems: Essential Concepts and Applications Fourth Edition by Wilkinson, Cerullo, Raval, and Wong-On-Wing Chapter 13: The Expenditure Cycle Slides Authored by Somnath Bhattacharya,

MIS 5121:Enterprise Resource Planning Systems Week 6: General Computer vs. SAP System Controls, Order to Cash Process,

MIS 5121:Enterprise Resource Planning Systems Week 6: General Computer vs. SAP System Controls, Order to Cash Process, Edward Beaver Edward.Beaver@temple.edu ff Control Failure: Wipro Background: v 2014:

MIS 5121:Enterprise Resource Planning Systems Week 6: General Computer vs. SAP System Controls, Order to Cash Process, Edward Beaver Edward.Beaver@temple.edu ff Control Failure: Wipro Background: v 2014:

Using Data Analytics as a Management Tool to Identify Organizational Risks

2013 CliftonLarsonAllen LLP Using Data Analytics as a Management Tool to Identify Organizational Risks Government Finance Officers Association of South Carolina October 13, 2014 cliftonlarsonallen.com

2013 CliftonLarsonAllen LLP Using Data Analytics as a Management Tool to Identify Organizational Risks Government Finance Officers Association of South Carolina October 13, 2014 cliftonlarsonallen.com

SAP FICO Course Content

Introduction to SAP R/3 Introduction to ERP, Advantages of SAP over other ERP Packages Introduction to SAP R/3 FICO Financial Accounting Basic Settings: Definition of company Definition of company code

Introduction to SAP R/3 Introduction to ERP, Advantages of SAP over other ERP Packages Introduction to SAP R/3 FICO Financial Accounting Basic Settings: Definition of company Definition of company code

Maxim Chuprunov. Auditing and. GRC Automation. in SAP. ^ Springer

Maxim Chuprunov Auditing and GRC Automation in SAP ^ Springer Contents List ofabbreviations xxix I From Legislation to Concept: ICS and Compliance in the ERP Environment 1 Legal Requirements in ICS Compliance

Maxim Chuprunov Auditing and GRC Automation in SAP ^ Springer Contents List ofabbreviations xxix I From Legislation to Concept: ICS and Compliance in the ERP Environment 1 Legal Requirements in ICS Compliance

- Excessive gambling or investment habits - Strong challenge to beat the system - Undue family pressure such as divorce - Overwhelming desire for pers

RED FLAGS OF INTERNAL FRAUD PROFILE OF THE PERPETRATOR: - Most frequently it is the person you trust the most - Has the technical skills to pull off the theft secretly - The activity is clandestine - The

RED FLAGS OF INTERNAL FRAUD PROFILE OF THE PERPETRATOR: - Most frequently it is the person you trust the most - Has the technical skills to pull off the theft secretly - The activity is clandestine - The

OCCUPATIONAL FRAUD IN GOVERNMENT AND STEPS TO PREVENT AND DETECT IT

OCCUPATIONAL FRAUD IN GOVERNMENT AND STEPS TO PREVENT AND DETECT IT This session will explore government fraud risks as well as common areas of abuse and corresponding red flags. It will also provide ideas

OCCUPATIONAL FRAUD IN GOVERNMENT AND STEPS TO PREVENT AND DETECT IT This session will explore government fraud risks as well as common areas of abuse and corresponding red flags. It will also provide ideas

Committee for Senior Business Administrators. Segregation of Duties

Committee for Senior Business Administrators Segregation of Duties Presented by: Tammy R. Hoskens and Margaret (Peggy) B. Zapalac University Risk and Compliance May 21, 2009 Segregation of Duties Segregation

Committee for Senior Business Administrators Segregation of Duties Presented by: Tammy R. Hoskens and Margaret (Peggy) B. Zapalac University Risk and Compliance May 21, 2009 Segregation of Duties Segregation

INTERNAL CONTROL HANDBOOK

INTERNAL CONTROL HANDBOOK INTERNAL CONTROL HANDBOOK ILLINOIS STATE BOARD OF EDUCATION SCHOOL BUSINESS SERVICES DIVISION Revised July, 2017 Most Content remains the same as published in 1993 Prepared by

INTERNAL CONTROL HANDBOOK INTERNAL CONTROL HANDBOOK ILLINOIS STATE BOARD OF EDUCATION SCHOOL BUSINESS SERVICES DIVISION Revised July, 2017 Most Content remains the same as published in 1993 Prepared by

Internal Controls Dealerships Should Have but May Not Have Thought About

October 2017 Internal Controls Dealerships Should Have but May Not Have Thought About An article by Edmund J. Reinhard, CPA Audit / Tax / Advisory / Risk / Performance Smart decisions. Lasting value. Internal

October 2017 Internal Controls Dealerships Should Have but May Not Have Thought About An article by Edmund J. Reinhard, CPA Audit / Tax / Advisory / Risk / Performance Smart decisions. Lasting value. Internal

FI113 Umoja Accounts Payable Overview. Umoja Accounts Payable Overview Version 10 1

FI113 Umoja Accounts Payable Overview Umoja Accounts Payable Overview Version 10 Copyright Last Modified: United 01-Aug-13 Nations 1 Agenda Course Introduction Module 1: Financial Accounting in Umoja Module

FI113 Umoja Accounts Payable Overview Umoja Accounts Payable Overview Version 10 Copyright Last Modified: United 01-Aug-13 Nations 1 Agenda Course Introduction Module 1: Financial Accounting in Umoja Module

SAP FICO TRAINING DOCUMENT

Financial Accounting Basic Settings Define Company Company code Business Area Fiscal year variant Posting Period Variant Field Status Variant Document Types and Number Ranges. General Ledger (GL) Chart

Financial Accounting Basic Settings Define Company Company code Business Area Fiscal year variant Posting Period Variant Field Status Variant Document Types and Number Ranges. General Ledger (GL) Chart

9/12/2013. CAPITALIZE ON YOUR PURCHASING CARD PROGRAM September 20, Agenda. With a card payment you can:

CAPITALIZE ON YOUR PURCHASING CARD PROGRAM September 20, 2013 Agenda Why Use a Commercial Card? Review the benefits of a card solution Travel Cards Automate expense reporting and gain visibility into spend

CAPITALIZE ON YOUR PURCHASING CARD PROGRAM September 20, 2013 Agenda Why Use a Commercial Card? Review the benefits of a card solution Travel Cards Automate expense reporting and gain visibility into spend

Microsoft Dynamics SL

Microsoft Dynamics SL 2015 Year-End Close Procedures The information contained herein is the property of MIG & Co. and may not be copied, used or disclosed in whole or In part to any third party except

Microsoft Dynamics SL 2015 Year-End Close Procedures The information contained herein is the property of MIG & Co. and may not be copied, used or disclosed in whole or In part to any third party except

Finance Committee, Board of Health Elizabeth Bowden, Interim Director of Administrative Services FINANCIAL CONTROLS CHECKLIST

March 20, 2016 Report To: Submitted by: Subject: Finance Committee, Board of Health Elizabeth Bowden, Interim Director of Administrative Services FINANCIAL CONTROLS CHECKLIST RECOMMENDATION(S): (a) That

March 20, 2016 Report To: Submitted by: Subject: Finance Committee, Board of Health Elizabeth Bowden, Interim Director of Administrative Services FINANCIAL CONTROLS CHECKLIST RECOMMENDATION(S): (a) That

Employee Dishonesty: Prevention and Detection

Employee Dishonesty: Prevention and Detection Frontline Risk Management Series Welcome to this session on Employee Dishonesty, a risk management module presented by CUMIS General Insurance s Risk Solutions

Employee Dishonesty: Prevention and Detection Frontline Risk Management Series Welcome to this session on Employee Dishonesty, a risk management module presented by CUMIS General Insurance s Risk Solutions

Internal Control Awareness: Tips for Improving Business Practices

Internal Control Awareness: Tips for Improving Business Practices S U S A N H A C K E R I N T E R N A L A U D I T O R Agenda Understand the value of internal controls. Learn some basic principles and best

Internal Control Awareness: Tips for Improving Business Practices S U S A N H A C K E R I N T E R N A L A U D I T O R Agenda Understand the value of internal controls. Learn some basic principles and best

Welcome to the topic on purchasing items.

Welcome to the topic on purchasing items. 1 In this topic, we will perform the basic steps for purchasing items. As we go through the process, we will explain the consequences of each process step on inventory

Welcome to the topic on purchasing items. 1 In this topic, we will perform the basic steps for purchasing items. As we go through the process, we will explain the consequences of each process step on inventory

Division of Student Affairs General Fund Units Internal Control Questionnaire FY 2012

FY 0 Control Environment Yes No N/A Notations Are the roles and responsibilities of financial and administrative staff, including the establishment of the appropriate signature authority, in your unit

FY 0 Control Environment Yes No N/A Notations Are the roles and responsibilities of financial and administrative staff, including the establishment of the appropriate signature authority, in your unit

INTERNAL CONTROLS REVIEW PROGRESS REPORT

INTERNAL S REVIEW PROGRESS REPORT RECOMMENDATIONS ADDRESSED THROUGH INTERNAL AUDIT WORK PLANS Monthly Reconciliation 1 High High Accounts Receivable Training 2, 8, 9 High Moderate 1 12, 13 High High 3

INTERNAL S REVIEW PROGRESS REPORT RECOMMENDATIONS ADDRESSED THROUGH INTERNAL AUDIT WORK PLANS Monthly Reconciliation 1 High High Accounts Receivable Training 2, 8, 9 High Moderate 1 12, 13 High High 3

2/27/2017. Segregation of Duties/ Internal Controls. Objectives. Agenda

Segregation of Duties/ Internal Controls 2017 WASBO Accounting Conference David Maccoux, Shareholder Objectives Discuss failures of internal controls to detect or prevent fraud and learn how to implement

Segregation of Duties/ Internal Controls 2017 WASBO Accounting Conference David Maccoux, Shareholder Objectives Discuss failures of internal controls to detect or prevent fraud and learn how to implement