2013 HIMSS Leadership Survey Senior IT Executive Results

|

|

|

- Dinah Quinn

- 5 years ago

- Views:

Transcription

1 2013 HIMSS Leadership Survey Senior IT Executive Results March 4, 2013 Sponsored by: transforming healthcare through IT

2 24 th Annual HIMSS Leadership Survey Final Report: Healthcare Senior IT Executive Sponsored by Infor The 24 th Annual HIMSS Leadership Survey reflects the opinions of information technology (IT) professionals in U.S. healthcare provider organizations regarding the use of IT in their organizations. This study covers a wide array of topics crucial to healthcare IT leaders including IT priorities, issues driving and challenging technology adoption, IT security, as well as IT staffing & budgeting plans. Contents 1. Executive Summary 2. Methodology 3. Profile of Survey Respondents 4. IT Priorities 5. IT Barriers 6. IT and Patient Care 7. IT Security 8. Health Information Exchange (HIE) Participation 9. IT Governance 10. Federal Initiatives 11. IT Budget and Staff 12. About HIMSS 13. About Infor Healthcare 14. About Infor 15. How to Cite This Study 16. For More Information 2

3 Figures Figure 1. Participant Profile Title Figure 2. Participant Profile Facility Type Figure 3. Participant Profile Type of Hospital Figure 4. Participant Profile Revenue Figure 5. Participant Profile Region Figure 6. Top IT Priority Next Two Years Figure 7. Primary Clinical IT Focus Figure 8. Primary Financial IT Focus Figure 9. Primary IT Infrastructure Focus Figure 10. Key Business Objective Figure 11. Business Issue with Most Impact on Healthcare Figure 12. Most Significant Barriers to Implementing IT Figure 13. Area that IT Can Most Impact Patient Care Figure 14. Role of Clinicians Figure 15. Access to On-line Patient Information from Remote Location Figure 16. Security Breach Figure 17. Top Concerns Security of Computerized Medical Information Figure 18. Health Information Exchange (HIE) Adoption Figure 19. Alignment of Organizational & IT Strategic Plan Figure 20. Member of Organization s Executive Committee Figure 21. Senior IT Executive Responsibilities Figure 22. Organization s Approach to IT Spending Based on Meaningful Use Figure 23. Percent of Organizations that Expect to Qualify for Stage One Meaningful Use Figure 24. Level of Investments Made by Healthcare Organizations in Meaningful Use Stage 1 Figure 25. Percent of Organizations that Expect to Qualify for Stage 2 Meaningful Use Figure 26. Level of Investment Made by Healthcare Organizations in Meaningful Use Stage 2 Figure 27. Anticipated ROI for Meeting Meaningful Use Stage 1 Requirements Figure 28. Anticipated ROI for Meeting Meaningful Use Stage 2 Requirements Figure 29. Preparedness to Meet ICD-10 Conversion Figure 30. Level of Investment Made in ICD-10 Conversion Figure 31. Expected Change in IT Staff in Next 12 Months Figure 32. Number of IT FTEs Budgeted to be Added Figure IT Staffing Needs (Top Ten) Figure 34. Additional Functions Managed by Senior IT Executives Figure 35. Projected Change in IT Operating Budget Figure 36. Reason for Increase in Budget Figure 37. Reason for Decrease in Budget 3

4 1. Executive Summary The findings from this year s Annual HIMSS Leadership Survey, sponsored by Infor, strongly suggest that the federal government s efforts to impact provider investments in information technologies to qualify for Meaningful Use (MU) and ICD-10 conversions, are paying off. To illustrate, two-thirds of survey respondents have already qualified for Stage 1 Meaningful Use while three-quarters indicated they expect to qualify for Stage 2 in Additionally, 87 percent of respondents indicated they expect to complete their conversion to ICD-10 by October Now that a majority of IT executives report having achieved Meaningful Use Stage 1, many leaders have turned their attention to MU Stage 2. In fact, findings reveal that more than one-quarter (28 percent) of organizations have identified the implementation of the systems needed to achieve Meaningful Use as their key IT priority. One-quarter (25 percent) of respondents also reported that they will invest a minimum of $1 million to achieve Stage 2. Respondents also continue to express concerns about IT staffing shortages. While half of the respondents (51 percent) indicated they plan to increase their IT staff in the next year, 21 percent are concerned that they won t be able to secure the IT staff needed to successfully achieve their IT objectives. The leading areas in which respondents need staff are in the areas of clinical application support, network/architecture support and clinical informatics professionals. Other key survey results include: Health Information Exchanges (HIEs): Approximately half of respondents (51 percent) reported their organization participates in at least one HIE in their area, a finding that is slightly increased from last year s participation level. ICD-10: Approximately half (47 percent) of respondents to this study indicated that implementing CPT-10/ICD-10 continues to be the top focus for financial IT systems. Impact of IT on Patient Care: Respondents were most likely to indicate that IT can impact patient care by improving clinical/quality outcomes, reducing medical errors or helping to standardize care by allowing for the use of evidence-based medicine. Role of Clinicians: Clinicians are active participants in many aspects of IT use at their organizations, including selecting IT systems for use in their department and acting as project champions. 4

5 Security Concerns: Nineteen (19) percent of respondents indicated that their organization has experienced a security breach in the past year. Respondents were most likely to indicate that securing information on mobile devices was the top security concern at their organization. Organizational Infrastructure: Almost one-quarter of respondents (22 percent) indicated that a focus on security systems was their current key infrastructure priority. IT Governance: There continues to be a strong level of integration between an organization s overall strategic plan and their IT strategic plan as half of respondents reported that their IT plan is part of their overall organizational strategic plan. Senior IT Executive Responsibilities: Executives were most likely to report that they play a role in contributing to overall business strategy and driving value from IT investments. External Areas of Responsibilities: Nearly all senior IT executives reported that they were responsible for at least one IT area outside of the traditional IT department, primarily telecommunications. Consumer Attitudes on Health IT: On a scale of one to seven, where one is of no importance and seven is a high degree of importance, IT executives recorded an average score of 4.94 with regard to the importance that patient/consumer attitudes have on adoption of new technology. 5

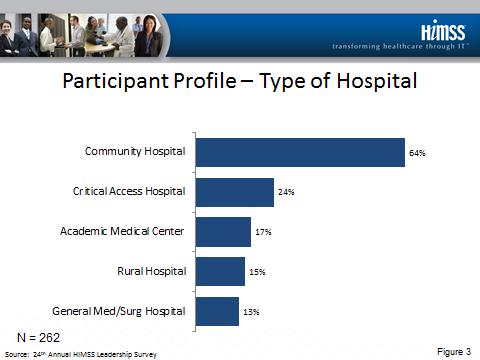

6 2. Methodology A total of 298 valid responses were received for this year s Web-based survey. Data was collected between December 2012 and February Survey respondents represent nearly 600 hospitals throughout the United States. The average bed size of the hospitals represented in this survey is 468 (median = 200 beds). 3. Profile of Survey Respondents More than half of respondents (55 percent) identified themselves as a Chief Information Officer (CIO), at either the corporate-level (36 percent) or the facility level (19 percent). Another third (31 percent) of respondents indicated they were a Director of Information Systems/Information Technology (IS/IT) and six percent of the respondents were Chief Medical Information Officers (CMIOs). The remaining respondents include Chief Nursing Information Officer (CNIO) and Manager of ITs. Nearly 90 percent of survey respondents reported working for an acute care hospitalbased environment, either at a stand-alone hospital (48 percent), a healthcare system (27 percent) or hospital as a part of a multi-hospital system (14 percent). Another six percent of respondents work at an outpatient setting. The remaining respondents reported working for other types of healthcare facilities including mental/behavioral health facilities, long-term care facilities and home care agencies. Respondents working for an acute care, hospital-based environment were asked to identify the types of hospitals that were part of their organization. Approximately twothirds of respondents (64 percent) noted that at least one facility in their organization was a community hospital. One-quarter of respondents indicated that their organization contained at least one critical access hospital and 17 percent reported working for an academic medical center. Thirteen (13) percent reported that they work for a general medical/surgical hospital. Annual gross operating revenues for the provider organizations represented in this year s survey were: $50 million or less 25 percent; $51 million to $200 million 23 percent; $201 million to $350 million 11 percent; $351 million to $500 million 7 percent; $501 million to $1 billion 10 percent; More than $1 billion 15 percent; and Don t Know/Not Applicable 10 percent. 6

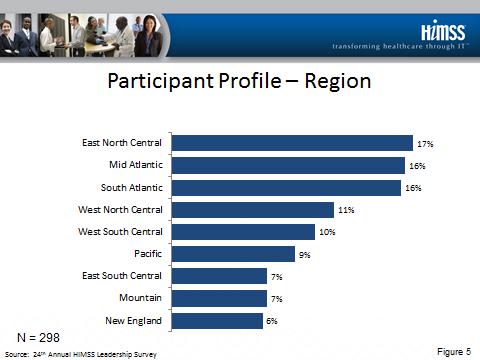

7 Respondents were most likely to work in the East North Central 1 region of the United States (17 percent), followed by the Mid Atlantic 2 and South Atlantic 3 regions (16 percent each). New England 4 had the fewest number of respondents (six percent). Figures: Figure 1. Participant Profile Title Figure 2. Participant Profile Facility Type Figure 3. Participant Profile Type of Hospital Figure 4. Participant Profile Revenue Figure 5. Participant Profile Region 4. IT Priorities Healthcare reform 5 was identified as the key issue that would most impact healthcare delivery in the next two years. In this context, IT executives reported their organizations were focused on achieving Meaningful Use, optimizing currently installed systems and leveraging information housed in existing systems to improve healthcare. IT Priorities When asked to identify the top IT priority to be addressed at their organization in the next two years, respondents were most likely to identify implementing the systems needed to achieve Meaningful Use (28 percent). However, the number of respondents identifying this area as a top IT priority continues to drop from a peak of half of respondents (50 percent) in 2011 and 38 percent in Another twenty percent of respondents indicated their top IT priority was to optimize the effective use of their currently installed systems. A focus on leveraging information housed in data warehouses and business intelligence systems rounds out the top three for the second consecutive year. This was identified by 17 percent of respondents. Less than one percent of respondents indicated that securing patient information was a top IT priority at their organization at this time. None of the respondents identified a focus on revenue cycle management (RCM) or supply chain systems as a top IT priority in the next two years. 1 Illinois, Indiana, Michigan, Ohio, Wisconsin 2 New Jersey, New York, Pennsylvania 3 Delaware, Florida, Georgia, Maryland, North Carolina, South Carolina, Virginia, Washington, DC, West Virginia, 4 Connecticut, Maine, Massachusetts, New Hampshire, Rhode Island, Vermont 5 Referred to in this study as ACOs, new care models or payment structures 7

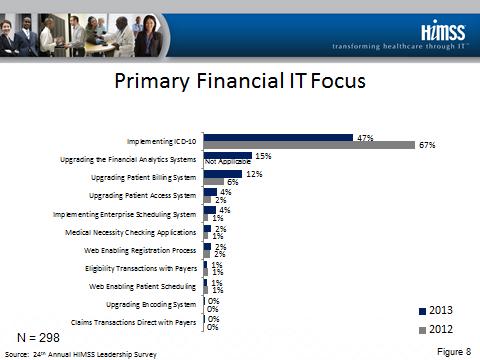

8 To more fully understand the areas on which IT executives were focusing their attention, respondents were also asked to identify the primary focus their organization has with regard to clinical IT, financial IT and infrastructure at their organizations. Primary Clinical IT Focus In 2013, respondents indicated that ensuring their organization has a fully functional EHR is their primary clinical IT focus (19 percent). However, the number of respondents indicating this to be the case declined from the 25 percent reported in A focus on physician systems, such as physician documentation or clinical decision support tools, was identified by 16 percent of respondents as a priority; another 16 percent of respondents indicated a focus on linking clinical systems with quality measures and outcomes. Less than one percent of respondents indicated that creating clinical documentation flow sheets was a primary clinical focus. None of the respondents indicated that installing a PACS system was a top clinical focus at this time. Primary Financial IT Focus Implementing CPT-10/ICD-10 continues to be the top focus for financial IT systems among the respondents to this study. Approximately half of respondents (47 percent) indicated this to be their top financial IT focus; this is a decrease from the two-thirds of respondents who reported this to be the case in Another 15 percent of respondents indicated their organization s key financial IT focus was to upgrade financial analytics systems to support Accountable Care Organizations (ACOs) and a bundled payment system. Rounding out the top three is upgrading the patient billing system, identified by 12 percent of respondents. One percent of respondents or fewer indicated that the following items were a top IT priority with regard to financial systems at their organizations. Implementing claims transactions directly with payers (no clearinghouse); Web-enabling the patient scheduling process to improve patient self-service; Implementing direct eligibility transactions with payers; and Upgrading the encoding system. None of the respondents indicated their organization had a present focus on webenabling the bill payment process to improve patient self-service functions. 8

9 Primary Infrastructure Focus With regard to their top infrastructure priority, nearly one-quarter of respondents identified a focus on security systems (22 percent), up from 16 percent in This is followed by last year s top response, servers/virtual servers, which was identified by 18 percent of respondents. Rounding out the top three is a focus on mobile devices, which was identified by 16 percent of respondents. Respondents were least likely to identify that either deploying a vendor neutral archive system or telemedicine were key infrastructure priorities at their organizations. Each of these was identified by less than three percent of respondents. Key Business Objective When asked to identify the single key business objective their organization was trying to achieve in the next 12 months, nearly one quarter of respondents (21 percent) indicated sustaining financial viability. This represents an increase from the 15 percent of respondents that selected this response in the 2012 study. Rounding out the top three key business objectives are improving patient care/quality of care and improved outcomes and improved operational efficiencies. These were selected by 19 and 17 percent of respondents, respectively. Last year s top response, achieving Meaningful Use dropped to fourth place, identified by only 15 percent of respondents. For the past several years, very few respondents have indicated that attracting qualified staff or improving supply chain dynamics are key business objectives for their organizations. This continues to be the case in 2013, when these items were selected by a combined total of one percent of respondents. Business Issue Driving Healthcare This year s survey respondents continue to identify healthcare reform as the top business issues that would have the most impact on healthcare in the next two years. This option, which includes items such as ACOs, new care models and payment structures was selected by 37 percent of respondents. Rounding out the top three responses are financial considerations such as the demand for capital (16 percent) or creating new revenue sources and policy mandates such as ICD-10 and Meaningful Use (14 percent). These items also rounded out the top three responses in No other option was selected by more than 10 percent of respondents. 9

10 Respondents were least likely to indicate hospital non-it infrastructure needs, such as facility upgrades and mergers or acquisitions (one percent), would be a business issue impacting healthcare. None of the respondents indicated that external threats or hospital infrastructure needs were drivers that will have a significant impact on healthcare in the next two years. Figures: Figure 6. Top IT Priority Next Two Years Figure 7. Primary Clinical IT Focus Figure 8. Primary Financial IT Focus Figure 9. Primary IT Infrastructure Focus Figure 10. Key Business Objective Figure 11. Business Issue with Most Impact on Healthcare 5. IT Barriers For the second consecutive year, respondents indicated that the ability to hire the necessary staffing resources was the key barrier to being able to implement IT at their organizations today. Having the appropriate financial resources also continues to be a key barrier to IT implementation. Respondents indicated that being able to hire adequate staffing resources was the top barrier to successfully implementing IT at their organizations for the second year in a row. This was selected by 21 percent of respondents. Rounding out the top three responses are lack of financial support (15 percent) and vendors inability to effectively deliver products or services to respondents satisfaction (13 percent). These responses also rounded out the top three in the 2012 survey. No other response was identified by more than 10 percent of respondents. One percent of respondents indicated that laws and regulations prohibiting technology sharing with referring providers was a barrier to IT implementation at their organizations. The same number of respondents indicated that the ability to secure data was a barrier to IT implementation. Only one respondent noted that his/her organization had no barriers to IT implementation. Figures: Figure 12. Most Significant Barriers to Implementing IT 10

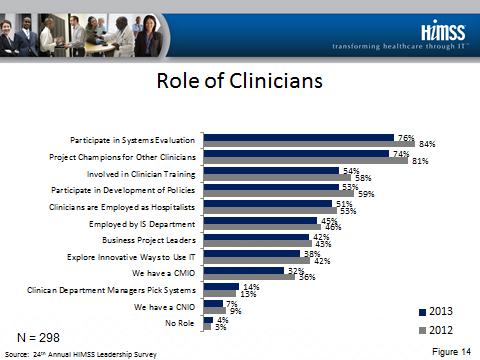

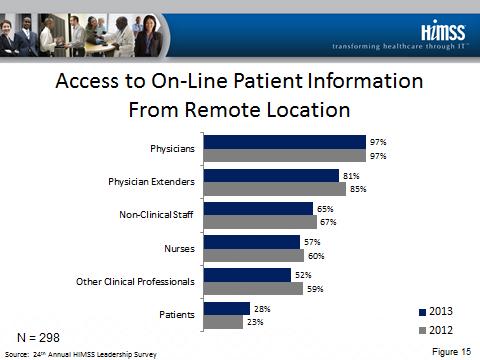

11 6. IT and Patient Care IT leaders continued to indicate that IT positively impacts patient care through improved clinical/quality outcomes, reduced medical errors or standardized care by allowing for the use of evidence-based medicine. IT professionals also reported that clinicians continue to be widely engaged in the IT process, including participation in the evaluation and selection of IT systems. Respondents continue to indicate that IT can most impact patient care by improving clinical and quality outcomes. This was selected by 31 percent of respondents and was also the most frequently identified response for the past two years. One-quarter of respondents (25 percent) indicated that IT can impact patient care by reducing medical errors/improving patient safety, while 12 percent indicated that standardization of clinical care using evidence-based medicine would be a benefit. These items also rounded out the top three responses last year. Less than two percent of respondents indicated the greatest impact that IT could have on patient care would be to ensure that patient data is private and secure. This was also the least frequently identified option in the 2012 study. Nearly all of survey respondents noted that clinicians play some role in the IT process as four percent of the respondents indicated that clinicians have no role in the IT process. This is consistent with the data collected in Respondents were most likely to report that clinicians participate in IT systems evaluation and selection (76 percent). Nearly three-quarters of respondents (74 percent) also reported that clinicians act as project champions to educate and lead other clinicians. These were also the top two responses identified in the 2012 study. Approximately one-third of respondents (32 percent) indicated that their organization employs a Chief Medical Information Officer (CMIO). This is a slight decrease in the number of respondents who reported this to be the case in 2012 (36 percent). The number of respondents reporting that their organizations employ a Chief Nursing Information Officer (CNIO) has also decreased slightly in the past year (seven percent compared to nine percent). When asked which individuals have remote access to secure, on-line clinical patient information, physician mentions are almost universal; 97 percent of respondents reported this to be the case. This is consistent with what was reported in The percent of respondents indicating that different groups of individuals have access to this type of information is noted below. 11

12 Physicians 97 percent; Physician extenders 81 percent; Non-clinical staff (i.e. transcriptionists) 65 percent; Nurses 57 percent; Other clinical professionals (i.e. occupational therapists) 52 percent; and Patients 28 percent. While the availability to access data remotely has remained relatively constant for most of the groups identified above, there has been a steady increase in the number of organizations that are making this type of information available to patients. The percent of respondents indicating this to be the case has increased from 19 percent in 2011 to the current 28 percent. Finally, on a scale of one to seven, where one is of no importance and seven is a high degree of importance, IT executives recorded an average score of 4.94 with regard to the importance that patient/consumer attitudes have on adoption of new technology. This question was not asked in Figures: Figure 13. Area that IT Can Most Impact Patient Care Figure 14. Role of Clinicians Figure 15. Access to On-line Patient Information from Remote Location 7. IT Security IT Security breaches continue to plague organizations but the reduction in actual violations reported this year suggests efforts to secure patient information may be working. Respondents were most likely to indicate that securing information on mobile devices was the top security concern at their organization. Nineteen (19) percent of respondents noted their organization had experienced some type of security breach in the past 12 months. In 2012, 22 percent of respondents reported this to be the case. Respondents were also asked to identify no more than two concerns that they had regarding the security of electronic medical information at their organizations. Only three percent of respondents indicated that they did not have any concerns at this time. More than one-third of respondents (36 percent) indicated that securing information on mobile devices was the top security concern at their organization; this is a substantial increase from the six percent of respondents who indicated this to be a top security concern in Compliance with HIPAA security regulations and CMS security audits was identified as a top concern by 28 percent of respondents. Rounding out the top 12

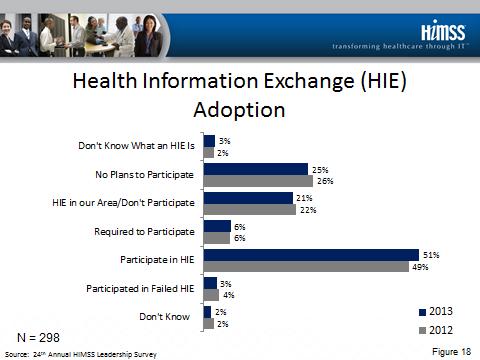

13 three responses was an internal breach of security, identified by 27 percent of respondents. The percent of respondents indicating that funding/financial support for the security process is a barrier continues to decline. This was identified by eight percent of respondents in 2013, compared to 13 percent in 2012 and 17 percent in Respondents were least likely to indicate concerns about the ability of their business associates to comply with existing business associate agreements; this was selected by three percent of respondents. Figures: Figure 16. Security Breach Figure 17. Top Concerns Security of Computerized Medical Information 8. Health Information Exchange (HIE) Participation Approximately half of respondents reported their organization participates in at least one HIE in their area, a finding that is slightly increased from last year s participation level. Respondents were asked to identify their current involvement in an HIE, defined as an organization which brings together healthcare stakeholders to oversee and govern the exchange of health-related information according to nationally recognized standards (which could include a state-designated health information exchange). As would be expected, the vast majority of respondents (ninety-seven percent) had some degree of familiarity with the concept of an HIE. More than half of respondents (51 percent) reported their organization participates in at least one HIE in their area, a finding that is slightly increased from last year s participation level. Only six percent claimed their participation was mandated by some level of government. Similar to previous surveys, approximately 21 percent of respondents indicated there was an HIE in their area, but have chosen not to participate in it at this time. Three percent of respondents reported that they participated in an HIE in the past, but that HIE has failed. One-quarter (25 percent) of respondents noted their organization had yet to start planning to participate in an HIE. This is consistent to what was reported in Figures: Figure 18. Health Information Exchange (HIE) Adoption 13

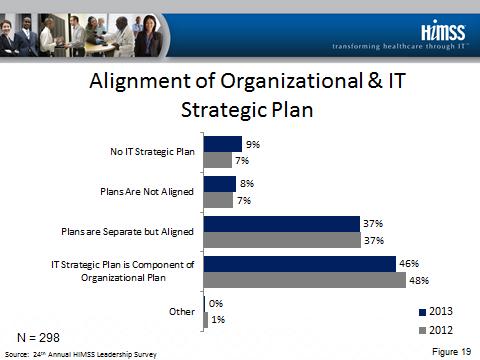

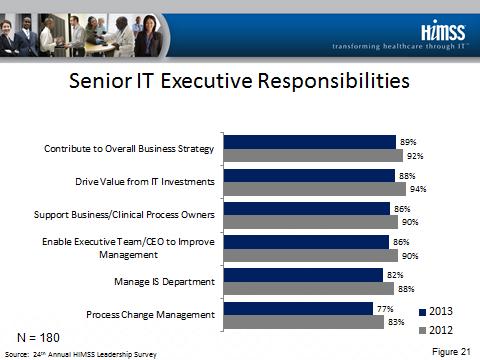

14 9. IT Governance There continues to be a strong level of integration between the IT strategic plan at respondents organizations and their organizations overall strategic plans. Senior IT executives also play a key role in contributing to overall business strategy at their organizations. Respondents were asked to characterize the level of integration between their IT plans and their organization s strategic operating, clinical and capital plans. The vast majority of respondents claimed their IT strategies were aligned with the organization s overall strategy with almost half of respondents (46 percent) indicating that the IT plan at their organization is a specific component of the organization s overall strategic plan; and another 37 percent reporting that their organizations IT strategic plans are integrated with overall strategic plan, even though the two plans are separate. These findings are consistent with feedback from previous HIMSS Leadership surveys. Nine percent of respondents indicated that their organization does not have an IT strategic plan. Another eight percent of respondents indicated that while their organization has a strategic plan, the IT strategic plan is not integrated with the organizations overall strategic plan. Sixty (60) percent of respondents claimed they are a member of their organization s executive committee, defined in this study as the leadership team that drives overall organization strategy and direction. This is slightly higher than the 57 percent of respondents that reported this to be the case in Individuals identifying themselves a senior IT executive were asked to identify which responsibilities they assume on a regular basis as part of their job. Contributing to overall business strategy was most frequently identified (89 percent). Last year s most frequently identified response, driving value from IT investments, was identified by 88 percent of respondents. The percent of respondents identifying each option is listed below. Contribute to overall business strategy 89 percent; Drive value from IT investments 88 percent; Enable the CEO/executive team to improve management through IT 86 percent; Support Business and clinical process owners 86 percent; Manage IS department operations 82 percent; and Responsible for process change management to be supported by IT 77 percent. 14

15 Figures: Figure 19. Alignment of Organizational & IT Strategic Plan Figure 20. Member of Organization s Executive Committee Figure 21. Senior IT Executive Responsibilities 10. Federal Initiatives Investments in technologies to help position organizations to qualify for meaningful use and the conversion to ICD-10 are paying off. Sixty percent of respondents reported that they have already qualified for Stage 1 and threequarters indicated that they expect to qualify for Stage 2 in Nearly all respondents, 87 percent, indicated they expect to complete their conversion to ICD-10 October Respondents were asked to identify their approach to the investments that will be made to achieve Meaningful Use. The majority of respondents (60 percent) indicated that because they have already achieved Stage 1, they are focusing their investments on achieving Stage 2. Less than one-third of respondents (30 percent) indicated that they are making additional investments to qualify for Meaningful Use incentives, while four percent are identifying the gaps in their environment, but waiting to invest at this time. Only one percent of the respondents indicated that they are not making any investments to qualify for Meaningful Use at this time. Meaningful Use Stage 1 Two-thirds (66 percent) of respondents indicated their organization has already attested to Stage 1 of Meaningful Use. Another four percent of respondents reported they expected to attest by the end of 2012 (and presumably have since the time they completed this survey). Another quarter (24 percent) of respondents reported that they expect to attest by the close of Less than two percent will not attest at any time. Regarding the amount of money spent (or will spend) to achieve Stage 1, approximately five percent of respondents indicated their organization made no additional investment. One-third (33 percent) reported they will ultimately invest less than $1 million, while 28 percent reported that their organization will invest between $1 million and $4 million to achieve Stage 1 requirements. Eighteen (18) percent will invest $5 million or more on achieving Stage 1 Meaningful Use. The remaining respondents either did not know the answer to this question or chose not to disclose this information. Respondents working for an organization that includes at least one hospital were asked to identify how much money their organization would receive for meeting Stage 1 Meaningful Use requirements. Less than one percent of respondents reported that they 15

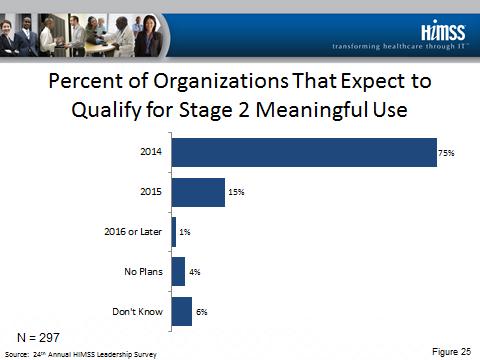

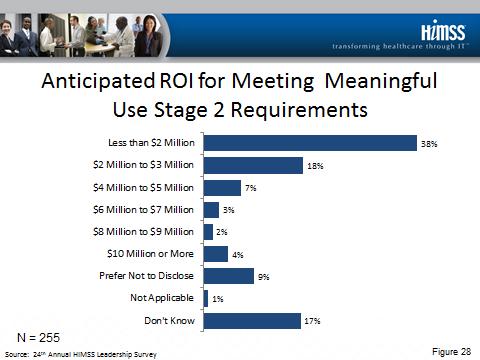

16 would not receive incentives in Stage 1. The below list identifies the money that organizations anticipate that they will receive for their investment. Less than $2 million 30 percent; $2 million to $3 million 23 percent; $4 million to $5 million 16 percent; $6 million to $7 million 6 percent; $8 million to $9 million 3 percent; and $10 million or more 7 percent. The remaining respondents either preferred not to disclose the level of money they expected to receive or did not know the amount. Meaningful Use Stage 2 Respondents were also asked to identify when they expected that their organization would qualify for the Stage 2 Meaningful Use requirements. Three-quarters (75 percent) of respondents indicated that they anticipated that their organization would qualify for the incentives available through Stage 2 in Another 15 percent noted that they would qualify for these incentives in One percent indicated that their organization would qualify for Stage 2 in 2016 or later and four percent indicated they had no plans to qualify for Stage 2. Six percent were unsure of their plans at this time. As to how much money spent (or will spend) to achieve Stage 2, 11 percent of respondents indicated that their organization will make no additional investment in IT at this time. More than one third (38 percent) indicated that their organization will invest less than $1 million to achieve Stage 2, while 18 percent will make an investment of $1 to $4 million. Seven percent expect their organization to make an investment of at least $5 million to achieve Stage 2. A large percent of respondents (17 percent) also indicated that they were unsure of the level of investment that would be needed at their organization at this time. When asked to project the amount of money they anticipated their organization will receive as a result of Stage 2, two percent of respondents working for a hospital-based organization did not believe they would receive any incentive. The below list identifies the money that organizations anticipate that they will receive for their investment. Less than $2 million 38 percent; $2 million to $3 million 18 percent; $4 million to $5 million 7 percent; $6 million to $7 million 3 percent; $8 million to $9 million 2 percent; and $10 million or more 4 percent. 16

17 The remaining respondents either preferred not to disclose the level of money they expected to receive or did not know the amount. ICD-10 In the past year, the date by which healthcare organizations needed to convert from ICD-9 to ICD-10 was deferred one year, to October 1, Respondents were very optimistic they would be able to achieve this objective, as 87 percent of respondents indicated that they expect to complete their conversion by this deadline. Respondents were also asked to identify the level of investment they were making in their ICD-10 conversion efforts. More than one-third (39 percent) of respondents indicated they were investing less than $1 million in this conversion. Another 13 percent indicated they were spending between $1million and $4 million, and three percent spent $5 million or more. While these numbers represent, in general, a lower level of investment than was reported last year, a very large percent of respondents (33 percent) were unsure of the level of investment they made in their ICD-10 conversion. Figures: Figure 22. Organization s Approach to IT Spending based on Meaningful Use Figure 23. Percent of Organizations that Expect to Qualify for Stage 1 Meaningful Use Figure 24. Level of Investments Made by Healthcare Organizations in Meaningful Use Stage 1 Figure 25. Percent of Organizations that Expect to Qualify for Stage 2 Meaningful Use Figure 26. Level of Investments Made by Healthcare Organizations in Meaningful Use Stage 2 Figure 27. Anticipated ROI for Meeting Meaningful Use Stage 1 Requirements Figure 28. Anticipated ROI for Meeting Meaningful Use Stage 2 Requirements Figure 29. Preparedness to Meet ICD-10 Conversion Figure 30. Level of Investment Made in ICD-10 Conversion 11. IT Budget and Staff Driven by an overall increase in the number of systems they need to manage, IT leaders expect both their operating budgets and the number of individuals employed in the IT department to increase in the next year. Staffing needs are greatest in the area of clinical application support. IT Staffing According to the 2012 HIMSS Analytics Database, U.S. hospital IT departments employed an average of 35 IT FTEs (median six IT FTEs). Half of respondents (51 percent) in this year s survey indicated they anticipated to increase the number of IT staff at their organization in the next 12 months. This represents a reduction from the 61 percent who reported this to be the case in

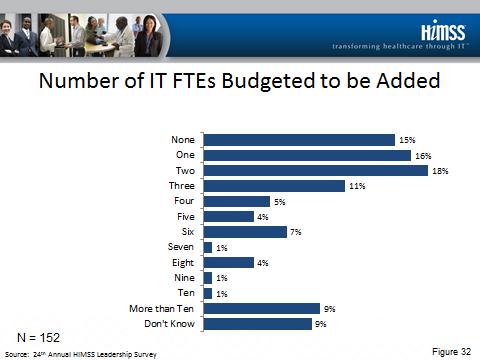

18 More specifically, seven percent of respondents indicated their staff would increase by more than 20 percent this coming year, 17 percent are targeting a 10 to 20 percent increase while 28 percent believe the increase will be less than 10 percent. More than one-third (38 percent) of respondents indicated that staffing levels would remain the same over the next 12 months, while seven percent of respondents indicated they expected a staffing decrease in the next 12 months. Of those respondents expecting staffing increases in 2012, approximately nine percent reported plans to add more than ten IT FTEs, 13 percent planned to add six to ten IT FTEs, 20 percent have budgeted to add three to five IT FTEs, and over one-third (34 percent) indicated their organization had budgeted to add one to two IT FTEs. Fifteen (15) percent reported that the IT FTEs they plan to add to their organization were not budgeted. All respondents were asked to identify the areas in which they have the most critical IT staffing needs. Six percent of respondents reported that their organization did not have any IT staffing needs at this time. Clinical application support continues to be the area in which respondents were most likely to indicate a staffing need, identified by 34 percent of respondents. This is followed by network/architecture support professionals (21 percent) and clinical informatics professionals (18 percent). These areas have been the top three areas of need for the past three years. Five percent or fewer respondents reported having critical staffing needs in the below areas: IT management (five percent); and IT planning (four percent). Among senior IT executives, 92 percent indicated they were responsible for at least one area outside of the IT department. Senior IT executives were most likely to report that they were also responsible for the telecommunications functions at their organizations (75 percent). Respondents had responsibilities in other areas such as medical/clinical informatics (51 percent), health information management (26 percent), and biomedical/clinical engineering (18 percent). IT Budgets According to the HIMSS Analytics Database, the average IS operating expense as a total expense for U.S. hospitals in 2012, was 2.73 percent. Slightly more than threequarters of survey respondents (76 percent) noted their organizations operating budgets for 2013 would increase over 2012 levels. These findings are consistent with what was 18

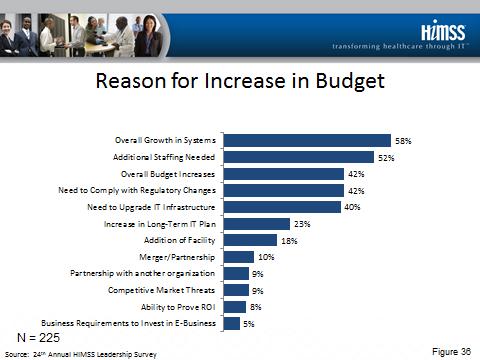

19 reported in the 2012 study. Approximately half (47 percent) of the respondents noted their budget would definitely increase in the next year while 29 percent identified a probable increase. Fifteen (15) percent of respondents reported their IT budget would remain unchanged and eight percent of respondents indicated their budget would decrease in the next year. These findings are similar to what was reported in Respondents continue to report an increase in their organization s IT operating budget is due to the overall growth in the number of systems and technologies in their organization (58 percent of respondents). Half of respondents (52 percent) indicated the increase would be due to additional staffing or consulting services needed to comply with governmental regulations. These were also the top items reported in the 2012 survey. Overall budget increases and a need to comply with regulatory changes were each identified by 42 percent of respondents respectively as a reason for driving an increased IT operating budget. Respondents were least likely to identify business requirements needed to invest in e- business as an item to create an increase in IT operating budget; only five percent of respondents indicated this to be the case. This area was also least likely to drive an expected increase in Among the handful of respondents noting their budget would decrease, approximately half (46 percent) indicated that the decrease was tied to a reduction in the organization s revenues. More than one-third (36 percent) indicated that an IT budget decrease was a result of a reduction in hospital revenues. None of the respondents indicated that a decrease in revenue was the result of outsourcing IT services to a low cost provider. Figures: Figure 31. Expected Change in IT Staff in Next 12 Months Figure 32. Number of IT FTEs Budgeted To Be Added Figure IT Staffing Needs (Top Ten) Figure 34. Additional Functions Managed by Senior IT Executives Figure 35. Projected Change in IT Operating Budget Figure 36. Reason for Increase in Budget Figure 37. Reason for Decrease in Budget 19

20 12. About HIMSS HIMSS is a cause-based, not-for-profit organization exclusively focused on providing global leadership for the optimal use of information technology (IT) and management systems for the betterment of healthcare. Founded 51 years ago, HIMSS and its related organizations are headquartered in Chicago with additional offices in the United States, Europe and Asia. HIMSS represents more than 44,000 individual members, of which more than two thirds work in healthcare provider, governmental and not-for-profit organizations. HIMSS also includes over 570 corporate members and more than 170 not-for-profit organizations that share our mission of transforming healthcare through the effective use of information technology and management systems. HIMSS frames and leads healthcare practices and public policy through its content expertise, professional development, research initiatives, and media vehicles designed to promote information and management systems contributions to improving the quality, safety, access, and cost-effectiveness of patient care. To learn more about HIMSS and to find out how to join us and our members in advancing our cause, please visit our website at About Infor Healthcare Infor is an industry-leading provider of healthcare IT solutions that help to standardize, centralize, and automate business processes across an entire organization. Infor s solutions for healthcare business applications and healthcare integration platforms are recognized as market leaders by the most recent HIMSS Analytics Vendor Market Share report. To learn more about Infor Healthcare, please visit About Infor Infor is the third-largest provider of enterprise applications and services, helping 70,000 customers in 194 countries improve operations, drive growth, and quickly adapt to changes in business demands. Infor offers deep industry-specific applications and suites, engineered for speed, using ground-breaking technology that delivers a rich user experience, and flexible deployment options that give customers a choice to run their businesses in the cloud, on-premises, or both. To learn more about Infor, please visit How to Cite This Study Individuals are encouraged to cite this report and any accompanying graphics in printed matter, publications, or any other medium, as long as the information is attributed to the 24 th Annual HIMSS Leadership Survey, sponsored by Infor. 20

21 16. For More Information, Contact: Joyce Lofstrom Director, Corporate Communications HIMSS 312/

22 Appendix 22

23 23

24 24

25 25

26 26

27 27

28 28

29 29

30 30

31 31

32 32

33 33

34 34

35 35

36 36

37 37

38 38

39 39

40 40

Wide Variation in Staffing Levels

Appendix I Wide Variation in Staffing Levels FTE Distribution Across Selected IT Functionalities Functionalities Size Min Max Median Std. Dev. Our surveys demonstrate a high degree of variation in IT staffing

Appendix I Wide Variation in Staffing Levels FTE Distribution Across Selected IT Functionalities Functionalities Size Min Max Median Std. Dev. Our surveys demonstrate a high degree of variation in IT staffing

2014 National Survey on ICD-10 Readiness. sponsored by Edifecs

2014 National Survey on ICD-10 Readiness sponsored by Edifecs 2014 National Survey on ICD-10 Readiness ehealth Initiative and AHIMA, hosted an industry wide survey on ICD-10 readiness in June 2014. The

2014 National Survey on ICD-10 Readiness sponsored by Edifecs 2014 National Survey on ICD-10 Readiness ehealth Initiative and AHIMA, hosted an industry wide survey on ICD-10 readiness in June 2014. The

Health Solutions. Commercial Health Solutions Overview EXPANDING INSIGHT. ENSURING VALUE. IMPROVING OUTCOMES.

Health Solutions Commercial Health Solutions Overview EXPANDING INSIGHT. ENSURING VALUE. IMPROVING OUTCOMES. Expanding Insight. Ensuring Value. Improving Outcomes. Organizations look to experienced solutions

Health Solutions Commercial Health Solutions Overview EXPANDING INSIGHT. ENSURING VALUE. IMPROVING OUTCOMES. Expanding Insight. Ensuring Value. Improving Outcomes. Organizations look to experienced solutions

THE FUTURE OF THE REVENUE CYCLE. A survey of provider executives about the next generation of revenue cycle management

THE FUTURE OF THE REVENUE CYCLE A survey of provider executives about the next generation of revenue cycle management OVERVIEW 1 Survey At-a-Glance 2 RCM Technology Trends/EHRs 3 4 Revenue Integrity Trends

THE FUTURE OF THE REVENUE CYCLE A survey of provider executives about the next generation of revenue cycle management OVERVIEW 1 Survey At-a-Glance 2 RCM Technology Trends/EHRs 3 4 Revenue Integrity Trends

Legacy Health Data Management, an Overview of Data Archiving & System Decommissioning with Rick Adams

Legacy Health Data Management, an Overview of Data Archiving & System Decommissioning with Rick Adams Rick Adams is the co-founder and Managing Partner of Harmony Healthcare IT. He has 22 years of healthcare

Legacy Health Data Management, an Overview of Data Archiving & System Decommissioning with Rick Adams Rick Adams is the co-founder and Managing Partner of Harmony Healthcare IT. He has 22 years of healthcare

Leveraging Integration Engines for Strategic Data Sharing under Value-Based Care. Produced in partnership with. Featuring industry research by

Leveraging Integration Engines for Strategic Data Sharing under Value-Based Care Produced in partnership with Featuring industry research by The need to share information is becoming a top capability for

Leveraging Integration Engines for Strategic Data Sharing under Value-Based Care Produced in partnership with Featuring industry research by The need to share information is becoming a top capability for

HIMSS RCM Survey. Understanding Health Systems Revenue Cycle Management and Challenges

HIMSS RCM Survey Understanding Health Systems Revenue Cycle Management and Challenges As healthcare delivery continues to evolve, hospitals are struggling to make the most of their revenues. The shift

HIMSS RCM Survey Understanding Health Systems Revenue Cycle Management and Challenges As healthcare delivery continues to evolve, hospitals are struggling to make the most of their revenues. The shift

2017 Healthcare Compliance Benchmark Study

2017 Healthcare Compliance Benchmark Study Executive Summary and Results EXECUTIVE SUMMARY This report represents SAI Global s eighth annual survey gathering insights from compliance professionals in the

2017 Healthcare Compliance Benchmark Study Executive Summary and Results EXECUTIVE SUMMARY This report represents SAI Global s eighth annual survey gathering insights from compliance professionals in the

Physician Practice ICD-10 Readiness Survey: Seven Key Survey Findings and Action Items June XX, 2013

Physician Practice ICD-10 Readiness Survey: Seven Key Survey Findings and Action Items June XX, 2013 Survey Background In the fourth quarter of 2013, Navicure commissioned Porter Research to conduct a

Physician Practice ICD-10 Readiness Survey: Seven Key Survey Findings and Action Items June XX, 2013 Survey Background In the fourth quarter of 2013, Navicure commissioned Porter Research to conduct a

CHKD Nets $22M in CFO-Validated Savings with a Blend of CBA s 100-Day Workouts and High Impact Margin Improvements

CHKD Nets $22M in CFO-Validated Savings with a Blend of CBA s 100-Day Workouts and High Impact Margin Improvements CHALLENGE With reimbursement rates the lowest in history, and a higher cost structure

CHKD Nets $22M in CFO-Validated Savings with a Blend of CBA s 100-Day Workouts and High Impact Margin Improvements CHALLENGE With reimbursement rates the lowest in history, and a higher cost structure

Driving Improvement to your Bottom Line:

White Paper Title Driving Improvement to your Bottom Line: Untapped Opportunities to Begin Tackling Now Given the current and anticipated reimbursement and cost pressures facing healthcare providers today,

White Paper Title Driving Improvement to your Bottom Line: Untapped Opportunities to Begin Tackling Now Given the current and anticipated reimbursement and cost pressures facing healthcare providers today,

Rethinking the Role of IT

White Paper Title Rethinking the Role of IT The Second Curve of Health IT Value Authors: Shawna Schueller, Carol Chouinard and Bob Schwyn Fueled by the Meaningful Use (MU) program, healthcare organizations

White Paper Title Rethinking the Role of IT The Second Curve of Health IT Value Authors: Shawna Schueller, Carol Chouinard and Bob Schwyn Fueled by the Meaningful Use (MU) program, healthcare organizations

Configuring Electronic Health Records: Migration to an Electronic Health Record System

Configuring Electronic Health Records: Migration to an Electronic Health Record System Lecture 2 Audio Transcript Slide 1 Welcome to Configuring Electronic Health Records: Migration to an Electronic Health

Configuring Electronic Health Records: Migration to an Electronic Health Record System Lecture 2 Audio Transcript Slide 1 Welcome to Configuring Electronic Health Records: Migration to an Electronic Health

TABLE OF CONTENTS ONLY

TABLE OF CONTENTS ONLY Business Continuity Compensation Report - United States of America Compensation Review May 2017 Benchmarking. Plan Ahead. Be Ahead. Data collected between January March 2017 with

TABLE OF CONTENTS ONLY Business Continuity Compensation Report - United States of America Compensation Review May 2017 Benchmarking. Plan Ahead. Be Ahead. Data collected between January March 2017 with

Beyond Meaningful Use: Harnessing Data s Potential in the Post- Reform Era Executive Perspectives

Jan 14 Beyond Meaningful Use: Harnessing Data s Potential in the Post- Reform Era Executive Perspectives By Ezra Mehlman 565 Fifth Avenue, 26th Floor, New York, New York 10017 Table of Contents Background...

Jan 14 Beyond Meaningful Use: Harnessing Data s Potential in the Post- Reform Era Executive Perspectives By Ezra Mehlman 565 Fifth Avenue, 26th Floor, New York, New York 10017 Table of Contents Background...

Healthcare Information and Management Systems Society. U.S. Healthcare Industry HIPAA Compliance Survey Results: Summer 2004

Healthcare Information and Management Systems Society U.S. Healthcare Industry HIPAA Compliance Survey Results: Summer 2004 HIMSS / Phoenix Health Systems U.S. Healthcare Industry HIPAA Survey Results:

Healthcare Information and Management Systems Society U.S. Healthcare Industry HIPAA Compliance Survey Results: Summer 2004 HIMSS / Phoenix Health Systems U.S. Healthcare Industry HIPAA Survey Results:

Strategic Issues for DPH IT DPH IT Governance Structure Healthcare Reform Key Aspects Healthcare Reform Project Status Meaningful Use Project

March 20, 2012 Strategic Issues for DPH IT DPH IT Governance Structure Healthcare Reform Key Aspects Healthcare Reform Project Status Meaningful Use Project Schedule and Budget CCSF IT Consolidation Status

March 20, 2012 Strategic Issues for DPH IT DPH IT Governance Structure Healthcare Reform Key Aspects Healthcare Reform Project Status Meaningful Use Project Schedule and Budget CCSF IT Consolidation Status

Eight User Secrets for Community Health Centers EIGHT E EIGHTEIG EIGHT. Why more community health centers choose NextGen solutions

Eight User Secrets for Community Health Centers EIGHTEIG EIGHT EIGHT E Why more community health centers choose NextGen solutions Pick ONE partner with an easy-touse solution and comprehensive 1services

Eight User Secrets for Community Health Centers EIGHTEIG EIGHT EIGHT E Why more community health centers choose NextGen solutions Pick ONE partner with an easy-touse solution and comprehensive 1services

Simplify processess Increase revenue Reach your MU goals

NextGen Professional Consulting Services Simplify processess Increase revenue Reach your MU goals Running a medical practice isn t easy. With daily responsibilities of patient care, managing staff, and

NextGen Professional Consulting Services Simplify processess Increase revenue Reach your MU goals Running a medical practice isn t easy. With daily responsibilities of patient care, managing staff, and

Is Your Local Government Plugged In? Highlights of the 2000 Electronic Government Survey

Is Your Local Government Plugged In? Highlights of the 2000 Electronic Government Survey Prepared for ICMA and PTI by Donald F. Norris, Patricia D. Fletcher, and Stephen H. Holden University of Maryland,

Is Your Local Government Plugged In? Highlights of the 2000 Electronic Government Survey Prepared for ICMA and PTI by Donald F. Norris, Patricia D. Fletcher, and Stephen H. Holden University of Maryland,

WHITE PAPER. Annual IIoT Maturity Survey. Adoption of IIoT in Manufacturing, Oil and Gas, and Transportation

WHITE PAPER 2017 Adoption of IIoT in Manufacturing, Oil and Gas, and Transportation 1 Executive Summary A survey of senior-level, experienced Industrial Internet of Things (IIoT) decision-makers and influencers

WHITE PAPER 2017 Adoption of IIoT in Manufacturing, Oil and Gas, and Transportation 1 Executive Summary A survey of senior-level, experienced Industrial Internet of Things (IIoT) decision-makers and influencers

SI Benchmarking Data Elements

Introductory data Participant Agreement Are you willing to be identified to peer organizations for more in-depth, one-on-one discussions? Organization ID number (entered by SI) What fiscal year does this

Introductory data Participant Agreement Are you willing to be identified to peer organizations for more in-depth, one-on-one discussions? Organization ID number (entered by SI) What fiscal year does this

HEALTHCARE CONSULTING GROUP

MAZARS USA LLP HEALTHCARE CONSULTING GROUP As one of the nation s leading professional service firms, Mazars USA provides the resources, experience and global expertise to help you adapt in a dynamically

MAZARS USA LLP HEALTHCARE CONSULTING GROUP As one of the nation s leading professional service firms, Mazars USA provides the resources, experience and global expertise to help you adapt in a dynamically

ICD-10 Readiness and Implementation SCHFMA. Presented by: Christine Kalish, MBA, CMPE Executive Consultant Date: June 1, 2011

ICD-10 Readiness and Implementation SCHFMA Presented by: Christine Kalish, MBA, CMPE Executive Consultant Date: June 1, 2011 2 Agenda ICD 10 - Background and timeline 5010 -Technical aspects of change

ICD-10 Readiness and Implementation SCHFMA Presented by: Christine Kalish, MBA, CMPE Executive Consultant Date: June 1, 2011 2 Agenda ICD 10 - Background and timeline 5010 -Technical aspects of change

About Us Advantages Contact us. Benchmark Billing Solutions

Benchmark Billing Solutions About Us Advantages Contact us Our Vision Our Clients Our Services About Us Benchmark Billing Solutions is a Delaware based LLC with rich relationships in the US. Organizational

Benchmark Billing Solutions About Us Advantages Contact us Our Vision Our Clients Our Services About Us Benchmark Billing Solutions is a Delaware based LLC with rich relationships in the US. Organizational

EHR AND ERP INTEGRATION. January 25, 2018

EHR AND ERP INTEGRATION January 25, 2018 Your Instructor Agenda Introduction to EHR and ERP EHR and ERP integration opportunities Evaluating the potential impact of EHR and ERP integration to your organization

EHR AND ERP INTEGRATION January 25, 2018 Your Instructor Agenda Introduction to EHR and ERP EHR and ERP integration opportunities Evaluating the potential impact of EHR and ERP integration to your organization

Venn Health Partners. Venn Health Partners, 906 Oak Tree Ave, Suite R, South Plainfield New Jersey, 07080,

Venn Health Partners Venn Health Partners, 906 Oak Tree Ave, Suite R, South Plainfield New Jersey, 07080, 732-992-8366 visit vennhp.com About Us We connect the dots Provide Best in Class project/program

Venn Health Partners Venn Health Partners, 906 Oak Tree Ave, Suite R, South Plainfield New Jersey, 07080, 732-992-8366 visit vennhp.com About Us We connect the dots Provide Best in Class project/program

ABOUT THE PRACTICE PROFITABILITY INDEX (PPI)

") ABOUT THE PRACTICE PROFITABILITY INDEX (PPI) The PPI provides an annual window into the issues affecting the financial and operational health of physician practices across the United States. It serves

ABOUT THE PRACTICE PROFITABILITY INDEX (PPI) The PPI provides an annual window into the issues affecting the financial and operational health of physician practices across the United States. It serves

Successful healthcare analytics begin with the right data blueprint

IBM Software Information Management Healthcare Successful healthcare analytics begin with the right data blueprint 2 Successful healthcare analytics begin with the right data blueprint Executive summary

IBM Software Information Management Healthcare Successful healthcare analytics begin with the right data blueprint 2 Successful healthcare analytics begin with the right data blueprint Executive summary

FINANCIAL SOLUTIONS PRIORITIZATION AND COST CONTAINMENT IN THE IT WORLD

FINANCIAL SOLUTIONS PRIORITIZATION AND COST CONTAINMENT IN THE IT WORLD Jackie Lucas, FACHE CIO Consultant Associate Faculty University of Phoenix Online Financial Solutions - Prioritization and Cost Containment

FINANCIAL SOLUTIONS PRIORITIZATION AND COST CONTAINMENT IN THE IT WORLD Jackie Lucas, FACHE CIO Consultant Associate Faculty University of Phoenix Online Financial Solutions - Prioritization and Cost Containment

Common Sense Strategies for Uncommon Times. Presented by: Tim Tindle, Executive Vice President & Chief Information Officer

Common Sense Strategies for Uncommon Times Presented by: Tim Tindle, Executive Vice President & Chief Information Officer What Will We Cover Today? Overview of Harris Health Our Transformational Journey

Common Sense Strategies for Uncommon Times Presented by: Tim Tindle, Executive Vice President & Chief Information Officer What Will We Cover Today? Overview of Harris Health Our Transformational Journey

EMC Information Infrastructure Solutions for Healthcare Providers. Delivering information to the point of care

EMC Information Infrastructure Solutions for Healthcare Providers Delivering information to the point of care Healthcare information growth is unrelenting More tests. More procedures. New technologies.

EMC Information Infrastructure Solutions for Healthcare Providers Delivering information to the point of care Healthcare information growth is unrelenting More tests. More procedures. New technologies.

Labor Market Outlook. Labor Market Outlook Survey Q (October December) Published by the Society for Human Resource Management

Published by the Society for Human Resource Management") October December 2010 Labor Market Outlook Published by the Society for Human Resource Management Labor Market Outlook Survey Q4 2010 (October December) LABOR MARKET OUTLOOK SURVEY Q4 2010 (October December)

October December 2010 Labor Market Outlook Published by the Society for Human Resource Management Labor Market Outlook Survey Q4 2010 (October December) LABOR MARKET OUTLOOK SURVEY Q4 2010 (October December)

3M All Rights Reserved. Your guide to ICD-10 success

Your guide to ICD-10 success How to use this guide This ICD-10 eguide provides a basic overview of steps hospitals can take now to ready their organizations for the transition from ICD-9 to ICD-10, including

Your guide to ICD-10 success How to use this guide This ICD-10 eguide provides a basic overview of steps hospitals can take now to ready their organizations for the transition from ICD-9 to ICD-10, including

HEALTHCARE CONSULTING GROUP

MAZARS USA LLP HEALTHCARE CONSULTING GROUP As one of the nation s leading professional service firms, Mazars USA provides the resources, experience and global expertise to help you adapt in a dynamically

MAZARS USA LLP HEALTHCARE CONSULTING GROUP As one of the nation s leading professional service firms, Mazars USA provides the resources, experience and global expertise to help you adapt in a dynamically

A Best Practices Approach to Best of Breed

A Best Practices Approach to Best of Breed A Complimentary Webinar From healthsystemcio.com Sponsored by Sunquest Information Systems Your Line Will Be Silent Until Our Event Begins Thank You! Housekeeping

A Best Practices Approach to Best of Breed A Complimentary Webinar From healthsystemcio.com Sponsored by Sunquest Information Systems Your Line Will Be Silent Until Our Event Begins Thank You! Housekeeping

The 2018 Law Firm Digital Marketing Survey

The 2018 Law Firm Digital Marketing Survey Table of Contents 1. INTRODUCTION 2. METHODOLOGY AND DEMOGRAPHICS 3. OPPORTUNITIES 4. CHALLENGES 5. SOCIAL MEDIA PLATFORMS 6. STAFF AND TRAINING 7. DIGITAL MARKETING

The 2018 Law Firm Digital Marketing Survey Table of Contents 1. INTRODUCTION 2. METHODOLOGY AND DEMOGRAPHICS 3. OPPORTUNITIES 4. CHALLENGES 5. SOCIAL MEDIA PLATFORMS 6. STAFF AND TRAINING 7. DIGITAL MARKETING

How to Put Your Meaningful Use Program Into AutoPilot. AMGA April 3, 2014

How to Put Your Meaningful Use Program Into AutoPilot AMGA April 3, 2014 Presenters Teresa Hall Director of Outcomes Improvement and Reporting Intermountain Medical Group Beth Houck Vice President, Client

How to Put Your Meaningful Use Program Into AutoPilot AMGA April 3, 2014 Presenters Teresa Hall Director of Outcomes Improvement and Reporting Intermountain Medical Group Beth Houck Vice President, Client

AWEA State RPS Market Assessment Released September 26, 2017

AWEA State RPS Market Assessment 2017 Released September 26, 2017 AWEA sincerely thanks its member companies and other organizations for their contribution to this report. Review of the analysis and methodology

AWEA State RPS Market Assessment 2017 Released September 26, 2017 AWEA sincerely thanks its member companies and other organizations for their contribution to this report. Review of the analysis and methodology

Taking the Lead in Revenue Cycle Transformation

Taking the Lead in Revenue Cycle Transformation Kamron Lachney Vice President of RCM Operations, McKesson Change Healthcare August 29, 2017 Today s Speaker Kamron Lachney, MBA Vice President, Hospital

Taking the Lead in Revenue Cycle Transformation Kamron Lachney Vice President of RCM Operations, McKesson Change Healthcare August 29, 2017 Today s Speaker Kamron Lachney, MBA Vice President, Hospital

Labor Market Outlook. Labor Market Outlook Survey Q (October December) Published by the Society for Human Resource Management

Published by the Society for Human Resource Management") October December 2009 Labor Market Outlook Published by the Society for Human Resource Management Labor Market Outlook Survey Q4 2009 (October December) LABOR MARKET OUTLOOK SURVEY Q4 2009 (October December)

October December 2009 Labor Market Outlook Published by the Society for Human Resource Management Labor Market Outlook Survey Q4 2009 (October December) LABOR MARKET OUTLOOK SURVEY Q4 2009 (October December)

TABLE OF CONTENTS ONLY

TABLE OF CONTENTS ONLY Business Continuity Compensation Report - United States of America Compensation Review July 2015 Benchmarking. Plan Ahead. Be Ahead. Data collected between February May 2015 with

TABLE OF CONTENTS ONLY Business Continuity Compensation Report - United States of America Compensation Review July 2015 Benchmarking. Plan Ahead. Be Ahead. Data collected between February May 2015 with

Clearinghouse Roadmap to Testing ICD-10. Mary Rita Hyland CPO & VP Regulatory Affairs The SSI Group, Inc.

Clearinghouse Roadmap to Testing ICD-10 Mary Rita Hyland CPO & VP Regulatory Affairs The SSI Group, Inc. About The SSI Group, Inc. Founded in 1986, SSI s EHNAC certified healthcare claims clearinghouse

Clearinghouse Roadmap to Testing ICD-10 Mary Rita Hyland CPO & VP Regulatory Affairs The SSI Group, Inc. About The SSI Group, Inc. Founded in 1986, SSI s EHNAC certified healthcare claims clearinghouse

How to Put Your Meaningful Use Program Into AutoPilot. AMGA April 3, 2014

How to Put Your Meaningful Use Program Into AutoPilot AMGA April 3, 2014 Presenters Teresa Hall Director of Outcomes Improvement and Reporting Intermountain Medical Group Beth Houck Vice President, Client

How to Put Your Meaningful Use Program Into AutoPilot AMGA April 3, 2014 Presenters Teresa Hall Director of Outcomes Improvement and Reporting Intermountain Medical Group Beth Houck Vice President, Client

HIMSS Analytics Survey. Sponsored by Dimensional Insight. How Successful Is Analytics in Supporting Executive Level Strategic Decision-Making?

HIMSS Analytics Survey Sponsored by Dimensional Insight How Successful Is Analytics in Supporting Executive Level Strategic Decision-Making? EXECUTIVE SUMMARY We ve all heard that data is king and that

HIMSS Analytics Survey Sponsored by Dimensional Insight How Successful Is Analytics in Supporting Executive Level Strategic Decision-Making? EXECUTIVE SUMMARY We ve all heard that data is king and that

Hackensack University Medical Center

CUSTOMER INNOVATION STUDY Hackensack University Medical Center gets one step closer to precision medicine with cloud-based Infor Cloverleaf Integration Suite We are trying to understand human beings. So

CUSTOMER INNOVATION STUDY Hackensack University Medical Center gets one step closer to precision medicine with cloud-based Infor Cloverleaf Integration Suite We are trying to understand human beings. So

Survey findings. Annual IT Forecast

2013 Survey findings IT Executive outlook Annual IT Forecast To drive successful business outcomes, it is critical to evaluate IT initiatives within the context of the broader market environment. TEKsystems

2013 Survey findings IT Executive outlook Annual IT Forecast To drive successful business outcomes, it is critical to evaluate IT initiatives within the context of the broader market environment. TEKsystems

White Paper Searchable Data:

White Paper Searchable Data: Analyzing What It Means To Your Practice 2 Searchable Data: Analyzing What It Means To Your Practice What is Searchable Data and Why is it Important? Searchable data means

White Paper Searchable Data: Analyzing What It Means To Your Practice 2 Searchable Data: Analyzing What It Means To Your Practice What is Searchable Data and Why is it Important? Searchable data means

From Interaction to Integration to Transformation: Healthcare s Journey & Information s Role

From Interaction to Integration to Transformation: Healthcare s Journey & Information s Role HealthBridge is one of the nation s largest and most successful health information exchange organizations. Mike

From Interaction to Integration to Transformation: Healthcare s Journey & Information s Role HealthBridge is one of the nation s largest and most successful health information exchange organizations. Mike

US state auditor deploys machine learning to tackle healthcare fraud at scale

US state auditor deploys machine learning to tackle healthcare fraud at scale This e-book focuses on how a US state auditor leveraged machine learning to detect and prevent fraud in healthcare. The biggest

US state auditor deploys machine learning to tackle healthcare fraud at scale This e-book focuses on how a US state auditor leveraged machine learning to detect and prevent fraud in healthcare. The biggest

Revenue Mitigation Strategies Offsetting The Financial Impact Of ICD-10

Revenue Mitigation Strategies Offsetting The Financial Impact Of ICD-10 January 23, 2014 What the industry is saying about the Transition to ICD-10 Staff alignment between business and IT is critical to

Revenue Mitigation Strategies Offsetting The Financial Impact Of ICD-10 January 23, 2014 What the industry is saying about the Transition to ICD-10 Staff alignment between business and IT is critical to

Components of a Comprehensive Legacy Data Management Strategy: Challenges and Strategic Considerations

Components of a Comprehensive Legacy Data Management Strategy: Challenges and Strategic Considerations A White Paper May 2016 Impact Advisors LLC 400 E. Diehl Road Suite 190 Naperville IL 60563 1-800-

Components of a Comprehensive Legacy Data Management Strategy: Challenges and Strategic Considerations A White Paper May 2016 Impact Advisors LLC 400 E. Diehl Road Suite 190 Naperville IL 60563 1-800-

Epic Integrated Consulting Services Seamless integration for system implementation, transition, optimization, legacy support and training

Epic Integrated Consulting Services Seamless integration for system implementation, transition, optimization, legacy support and training With nearly a third of all electronic health record (EHR) inpatient

Epic Integrated Consulting Services Seamless integration for system implementation, transition, optimization, legacy support and training With nearly a third of all electronic health record (EHR) inpatient

White Paper RAISING THE BAR: Four coding staffing models to consider when preparing for ICD-10

White Paper RAISING THE BAR: Four coding staffing models to consider when preparing for ICD-10 TABLE OF CONTENTS Introduction The Staffing Model Tune-Up Trends in Coding Staffing Dynamics Key Change Drivers

White Paper RAISING THE BAR: Four coding staffing models to consider when preparing for ICD-10 TABLE OF CONTENTS Introduction The Staffing Model Tune-Up Trends in Coding Staffing Dynamics Key Change Drivers

Business Intelligence Decision Support Through Better Data Management

Of all the transformations reshaping American Healthcare, none is more profound than the shift towards payment for value - HFMA s Value Project Phase 2 Business Intelligence Decision Support Through Better

Of all the transformations reshaping American Healthcare, none is more profound than the shift towards payment for value - HFMA s Value Project Phase 2 Business Intelligence Decision Support Through Better

A Mini-Handbook for. Successful ICD-10 Conversion

A Mini-Handbook for Successful ICD-10 Conversion This ebook has been designed to simplify your understanding of ICD-10. Our aim is to help you successfully implement the change at your practice with valuable

A Mini-Handbook for Successful ICD-10 Conversion This ebook has been designed to simplify your understanding of ICD-10. Our aim is to help you successfully implement the change at your practice with valuable

Industry Report: The State of QPP Preparedness

White paper Industry Report: The State of QPP Preparedness New research reveals that health systems relying on ehr and phm systems for quality performance management are at risk of falling short of their

White paper Industry Report: The State of QPP Preparedness New research reveals that health systems relying on ehr and phm systems for quality performance management are at risk of falling short of their

REVENUE CYCLE TECHNOLOGY TRENDS

REVENUE CYCLE TECHNOLOGY TRENDS A survey of provider executives about revenue cycle IT budgets, EHRs, and consumer self-pay November 2018 Lead. Solve. Grow. HFMA/Navigant Survey At-a-Glance According to

REVENUE CYCLE TECHNOLOGY TRENDS A survey of provider executives about revenue cycle IT budgets, EHRs, and consumer self-pay November 2018 Lead. Solve. Grow. HFMA/Navigant Survey At-a-Glance According to

Q October-December. Jobs Outlook Survey Report. Published by the Society for Human Resource Management

Q4 2013 October-December Jobs Outlook Survey Report Published by the Society for Human Resource Management JOBS OUTLOOK SURVEY REPORT Q4 2013 (October-December) OPTIMISM ABOUT JOB GROWTH IN Q4 2013 (OCTOBER-DECEMBER)

Q4 2013 October-December Jobs Outlook Survey Report Published by the Society for Human Resource Management JOBS OUTLOOK SURVEY REPORT Q4 2013 (October-December) OPTIMISM ABOUT JOB GROWTH IN Q4 2013 (OCTOBER-DECEMBER)

Optimization: The Next Frontier

Optimization: The Next Frontier A White Paper Impact Advisors LLC January 2015 400 E. Diehl Road Suite 190 Naperville IL 60563 1 800 680 7570 Impact Advisors.com Table of Contents Introduction... 3 Optimization

Optimization: The Next Frontier A White Paper Impact Advisors LLC January 2015 400 E. Diehl Road Suite 190 Naperville IL 60563 1 800 680 7570 Impact Advisors.com Table of Contents Introduction... 3 Optimization

Choosing The Right EHR For You: Best Practices In Vendor Selection & Contracting

Choosing The Right EHR For You: Best Practices In Vendor Selection & Contracting Presented By: Joseph Naughton-Travers, Ed.M., Senior Associate, OPEN MINDS Presented On: July 26, 2013 An OPEN MINDS Executive

Choosing The Right EHR For You: Best Practices In Vendor Selection & Contracting Presented By: Joseph Naughton-Travers, Ed.M., Senior Associate, OPEN MINDS Presented On: July 26, 2013 An OPEN MINDS Executive

EHR Data Conversion Guide & Workbook

EHR Data Conversion Guide & Workbook EHR Data Conversion Guide Healthcare today is faced with an aging population, a shortage of providers and a growing demand for chronic disease management. In addition

EHR Data Conversion Guide & Workbook EHR Data Conversion Guide Healthcare today is faced with an aging population, a shortage of providers and a growing demand for chronic disease management. In addition

M*Modal CDI Solutions. Elevating Clinical Documentation Improvement with Artificial Intelligence

M*Modal CDI Solutions Elevating Clinical Documentation Improvement with Artificial Intelligence At a time when the long-term viability of healthcare organizations is directly dependent on meeting the twin

M*Modal CDI Solutions Elevating Clinical Documentation Improvement with Artificial Intelligence At a time when the long-term viability of healthcare organizations is directly dependent on meeting the twin

MACRA Year 2 Moving out of the Transition Period and Into Reality February 16, 2018

MACRA ear 2 Moving out of the Transition Period and Into Reality February 16, 2018 February 16, 2018: Where are we in MACRA implementation? The 2018 performance year is underway. Cost will take effect

MACRA ear 2 Moving out of the Transition Period and Into Reality February 16, 2018 February 16, 2018: Where are we in MACRA implementation? The 2018 performance year is underway. Cost will take effect

M*Modal CDI Solutions

M*Modal CDI Solutions #1 CDI Software, 2019 KLAS Category Leader Elevating Clinical Documentation Improvement with Artificial Intelligence At a time when the long-term viability of healthcare organizations

M*Modal CDI Solutions #1 CDI Software, 2019 KLAS Category Leader Elevating Clinical Documentation Improvement with Artificial Intelligence At a time when the long-term viability of healthcare organizations

TEST AUTOMATION: A PREPARATORY GUIDE FOR HEALTHCARE ORGANIZATIONS

TEST AUTOMATION: A PREPARATORY GUIDE FOR HEALTHCARE ORGANIZATIONS 2 TEST AUTOMATION: A PREPARATORY GUIDE FOR HEALTHCARE ORGANIZATIONS The time has finally come for healthcare test automation. In fact,

TEST AUTOMATION: A PREPARATORY GUIDE FOR HEALTHCARE ORGANIZATIONS 2 TEST AUTOMATION: A PREPARATORY GUIDE FOR HEALTHCARE ORGANIZATIONS The time has finally come for healthcare test automation. In fact,

UC Health: Better Together Information Technology & Leveraging Scale for Value (LSfV) A Presentation to HIMSS So Cal December 1, 2015

A Presentation to HIMSS So Cal December 1, 2015") UC Health: Better Together Information Technology & Leveraging Scale for Value (LSfV) A Presentation to HIMSS So Cal December 1, 2015 UC Health By The Numbers 6 Medical schools $1.8B NIH funding 4 th Largest

UC Health: Better Together Information Technology & Leveraging Scale for Value (LSfV) A Presentation to HIMSS So Cal December 1, 2015 UC Health By The Numbers 6 Medical schools $1.8B NIH funding 4 th Largest

Best Practices in EHR Implementations

WHITE PAPERS FOR REAL PEOPLE Best Practices in EHR Implementations by TIM LIDDELL VICE PRESIDENT, PROVIDER DEPLOYMENT BETSY CROSS DIRECTOR, PROVIDER DEPLOYMENT CONTENTS The SaaS Delivery Model... 1 January

WHITE PAPERS FOR REAL PEOPLE Best Practices in EHR Implementations by TIM LIDDELL VICE PRESIDENT, PROVIDER DEPLOYMENT BETSY CROSS DIRECTOR, PROVIDER DEPLOYMENT CONTENTS The SaaS Delivery Model... 1 January

An Overview of the HIMSS Mergers & Acquisitions Technology Framework. A Resource Update for Senior Executives

An Overview of the HIMSS Mergers & Acquisitions Technology Framework A Resource Update for Senior Executives Speakers Barry Blumenfeld, MD, MS Principal BHB Clinical Informatics Greg Wolverton CIO ARcare

An Overview of the HIMSS Mergers & Acquisitions Technology Framework A Resource Update for Senior Executives Speakers Barry Blumenfeld, MD, MS Principal BHB Clinical Informatics Greg Wolverton CIO ARcare

QUICK FACTS. Supporting a Healthcare Provider s Transformation to ICD-10 TEKSYSTEMS GLOBAL SERVICES CUSTOMER SUCCESS STORIES.

[Healthcare Services, Managed IT Services] TEKSYSTEMS GLOBAL SERVICES CUSTOMER SUCCESS STORIES Client Profile Industry: Healthcare Services Revenue: Nearly $2 billion Employees: More than 20,000 Geographic

[Healthcare Services, Managed IT Services] TEKSYSTEMS GLOBAL SERVICES CUSTOMER SUCCESS STORIES Client Profile Industry: Healthcare Services Revenue: Nearly $2 billion Employees: More than 20,000 Geographic

CAQH CORE Phase I Measures of Success. May 2009

CAQH CORE Phase I Measures of Success Executive Summary and Industry-wide Savings Projection May 2009 Table of Contents Study background Findings common across stakeholder groups Findings by stakeholder

CAQH CORE Phase I Measures of Success Executive Summary and Industry-wide Savings Projection May 2009 Table of Contents Study background Findings common across stakeholder groups Findings by stakeholder

Navigating Meaningful Use Rapids Physician Onboarding

Navigating Meaningful Use Rapids Physician Onboarding April 14, 2015 Karen Wilding / Director of Operations / University Of Maryland Medical System Anantachai (Tony) Panjamapirom / Senior Consultant /

Navigating Meaningful Use Rapids Physician Onboarding April 14, 2015 Karen Wilding / Director of Operations / University Of Maryland Medical System Anantachai (Tony) Panjamapirom / Senior Consultant /

MELISSA STAHL RESEARCH MANAGER THE HEALTH MANAGEMENT ACADEMY

TECHNOLOGY INTEGRATION AT LEADING HEALTH SYSTEMS VENDOR NEUTRAL ARCHIVES AT INDIANA UNIVERSITY HEALTH MELISSA STAHL RESEARCH MANAGER THE HEALTH MANAGEMENT ACADEMY The Academy The Health Management Academy

TECHNOLOGY INTEGRATION AT LEADING HEALTH SYSTEMS VENDOR NEUTRAL ARCHIVES AT INDIANA UNIVERSITY HEALTH MELISSA STAHL RESEARCH MANAGER THE HEALTH MANAGEMENT ACADEMY The Academy The Health Management Academy

2018 Resources for HealthIT Vendors

AMA HEALTH SOLUTIONS 2018 Resources for HealthIT Vendors HealthIT Toolkit for Counting Users & FAQs September 2017 User Proxy Model Calculator for data file licensing (CPT, ICD-10 and HCPCS) Hospital Setting:

AMA HEALTH SOLUTIONS 2018 Resources for HealthIT Vendors HealthIT Toolkit for Counting Users & FAQs September 2017 User Proxy Model Calculator for data file licensing (CPT, ICD-10 and HCPCS) Hospital Setting:

Revitalizing an RTLS Initiative

Revitalizing an RTLS Initiative According to our estimates nearly 100% of hospitals in the U.S., with over 400 licensed beds, have implemented some type of Real-Time Location Solution (RTLS). Beyond the

Revitalizing an RTLS Initiative According to our estimates nearly 100% of hospitals in the U.S., with over 400 licensed beds, have implemented some type of Real-Time Location Solution (RTLS). Beyond the

Cost Reduction is Top Priority for Leading Health Systems

THE ACADEMY H2C STRATEGIC SURVEY Q2 2017 Cost Reduction Melissa Stahl Research Manager The Health Management Academy Key Findings Most (90%) responding executives rank cost reduction as a high or very