Chapter 5: Supply Section 3

|

|

|

- Sabrina Reeves

- 6 years ago

- Views:

Transcription

1 Chapter 5: Supply Section 3

2 Objectives 1. Explain how factors such as input costs create changes in supply. 2. Identify three ways that the government can influence the supply of goods. 3. Analyze other factors that affect supply. 4. Explain how firms choose a location to produce goods. Slide 2

3 Key Terms subsidy: a government payment that supports a business or market excise tax: a tax on the production or sale of a good regulations: government intervention in a market that affects the production of a good Slide 3

4 Introduction Why does the supply curve shift? Several factors cause the supply curve to shift. These include: Shifts in prices Rising costs Technology Changes in the global economy Future expectations of prices Number of suppliers Slide 4

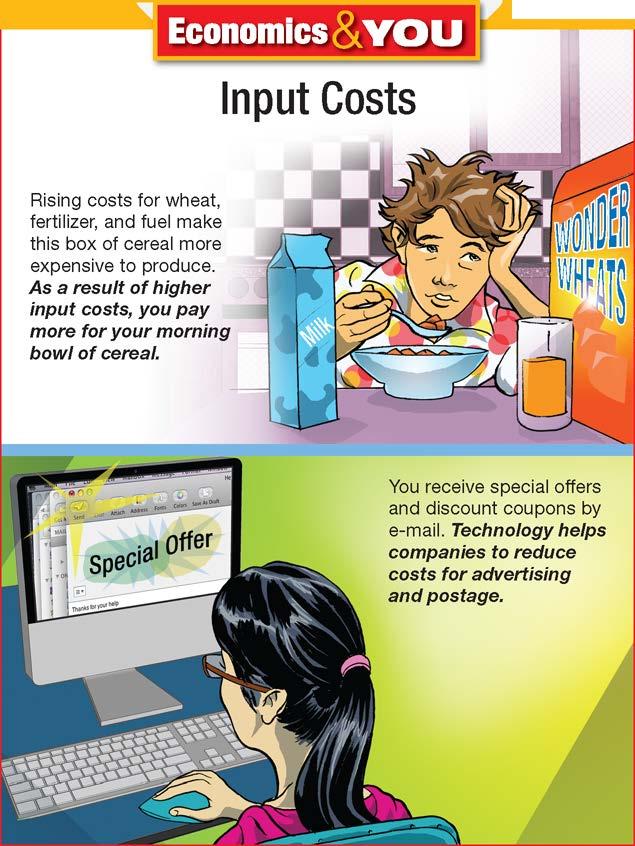

5 Input Costs Any changes in the cost of an input used to make a good will affect supply. A rise in the cost of raw materials, for example, will result in a decrease in supply because the good has become more expensive to produce. The high input costs that dairy farmers pay for feed, labor, and fuel result in higher prices for milk and other dairy products. Slide 5

6 Rising Costs and Technology If costs continue to rise, a firm will have to cut production and lower its marginal cost. It is possible for input costs to drop. In many industries, advances in technology can lower production costs. Examples of technology advances include: Automation Computers Slide 6

7

8 Government s Influence In addition to input costs, the federal government also has the power to affect the supplies of many types of good. Subsidies The government often gives subsidies to the producers of a good. Subsidies generally lower cost, which allows a firm to produce more goods. Reasons for subsidizing products include: To provide for people during food shortages To protect young industries from foreign competition. Slide 8

9 Government Influences, cont. Taxes Excise taxes increase production costs by adding an extra cost for each unit sold. They are sometimes used to discourage the sale of a good the government deems harmful, such as cigarettes and alcohol. Slide 9

10 Government Influences, cont. Regulation Indirectly, government regulation often has the effect of raising costs. When the government regulated the auto industry to cut down on pollution, these regulations led to an increase in the cost of manufacturing cars. Slide 10

11 Non-Price Influences Changes in the global economy Since many goods and services are imported, changes in other countries can affect the supply of those goods. An increase in wages in one country or the increased supply of a good in another will cause the overall supply curve to shift. Restrictions on imports also affect supply. Slide 11

12 Shifts in the Supply Curve Factors that reduce supply shift the supply curve to the left, while factors that increase supply move the supply curve to the right. Which graph best represents the effects of higher costs? Which graph best represents advances in technology? Slide 12

13 Future Expectations of Prices Checkpoint: What happens to supply if the price of a good is expected to rise in the future? If a seller expects the price of a good to rise in the future, the seller will store the goods now in order to sell more in the future. If the prices of good is expected to drop in the near future, sellers will earn more by placing goods on the market immediately, before the price falls. Slide 13

14 Number of Suppliers If more suppliers enter a market, the market supply will rise and the supply curve will shift to the right. If suppliers stop producing a good and leave the market, market supply will decline, causing the supply curve to shift to the left. Slide 14

15 Where do Firms Produce? Checkpoint: When is a firm likely to locate close to its consumers? A key factor in where a firm will locate is transportation. When inputs such as raw materials are expensive to transport, a firm will locate close to the inputs. When outputs (the final product) are more costly to transport, firms will locate close to the consumer. Slide 15

16 Review Now that you have learned why the supply curve shifts, go back and answer the Chapter Essential Question How do suppliers decide what goods and services to offer? Slide 16

Chapter 5: Supply Section 1

Chapter 5: Supply Section 1 Key Terms supply: the amount of goods available law of supply: producers offer more of a good as its price increases and less as its price falls quantity supplied: the amount

Chapter 5: Supply Section 1 Key Terms supply: the amount of goods available law of supply: producers offer more of a good as its price increases and less as its price falls quantity supplied: the amount

Supply. Understanding Economics, Chapter 5

Supply Understanding Economics, Chapter 5 What is Supply? Chapter 5, Lesson 1 What is Supply?! Supply the amount of a product a producer or seller would be willing to offer for sale at all possible prices

Supply Understanding Economics, Chapter 5 What is Supply? Chapter 5, Lesson 1 What is Supply?! Supply the amount of a product a producer or seller would be willing to offer for sale at all possible prices

1. Demand: willingness to buy a good or service and the ability to pay for it; how much of an item an individual is willing to purchase at each price

1. Demand: willingness to buy a good or service and the ability to pay for it; how much of an item an individual is willing to purchase at each price 2. Quantity demanded vs demand: quantity demanded is

1. Demand: willingness to buy a good or service and the ability to pay for it; how much of an item an individual is willing to purchase at each price 2. Quantity demanded vs demand: quantity demanded is

1. Demand: willingness to buy a good or service and the ability to pay for it; how much of an item an individual is willing to purchase at each price

1. Demand: willingness to buy a good or service and the ability to pay for it; how much of an item an individual is willing to purchase at each price 2. The two things needed for demand to exist are: willingness

1. Demand: willingness to buy a good or service and the ability to pay for it; how much of an item an individual is willing to purchase at each price 2. The two things needed for demand to exist are: willingness

Understanding Supply. Chapter 5 Section Main Menu

Understanding Supply What is the law of supply? What are supply schedules and supply curves? What is elasticity of supply? What factors affect elasticity of supply? The Law of Supply According to the law

Understanding Supply What is the law of supply? What are supply schedules and supply curves? What is elasticity of supply? What factors affect elasticity of supply? The Law of Supply According to the law

Objective: What is the law of supply? What are supply schedules and supply curves? What is elasticity of supply?

Understanding Supply Objective: What is the law of supply? What are supply schedules and supply curves? What is elasticity of supply? *Be sure to leave a couple blank lines under each question and answer

Understanding Supply Objective: What is the law of supply? What are supply schedules and supply curves? What is elasticity of supply? *Be sure to leave a couple blank lines under each question and answer

ORGANIZING YOUR THOUGHTSII Use the diagram to help you take notes. Supply and prices are related. Indicate how they are related in the diagram.

Chapter 21, Section 1 For use with textbook pages 462 465 What Is Supply? KEY TERMS supply the various quantities of a good or service that producers are willing to sell at all possible market prices (page

Chapter 21, Section 1 For use with textbook pages 462 465 What Is Supply? KEY TERMS supply the various quantities of a good or service that producers are willing to sell at all possible market prices (page

Chapter 6: Prices Section 1

Chapter 6: Prices Section 1 Objectives 1. Explain how supply and demand create equilibrium in the marketplace. 2. Describe what happens to prices when equilibrium is disturbed. 3. Identify two ways that

Chapter 6: Prices Section 1 Objectives 1. Explain how supply and demand create equilibrium in the marketplace. 2. Describe what happens to prices when equilibrium is disturbed. 3. Identify two ways that

Section 1 Understanding Supply

Chapter 5 - Supply Section 1 Understanding Supply Supply the amount of goods available Law of Supply Tendency for suppliers to offer more of a good at a higher price. Law of Supply Price As price increases

Chapter 5 - Supply Section 1 Understanding Supply Supply the amount of goods available Law of Supply Tendency for suppliers to offer more of a good at a higher price. Law of Supply Price As price increases

Chapter 4. Demand, Supply and Markets. These slides supplement the textbook, but should not replace reading the textbook

Chapter 4 Demand, Supply and Markets These slides supplement the textbook, but should not replace reading the textbook 1 What is a market? A group of buyers and sellers with the potential to trade 2 What

Chapter 4 Demand, Supply and Markets These slides supplement the textbook, but should not replace reading the textbook 1 What is a market? A group of buyers and sellers with the potential to trade 2 What

SOLUTIONS TO TEXT PROBLEMS 6

SOLUTIONS TO TEXT PROBLEMS 6 Quick Quizzes 1. A price ceiling is a legal maximum on the price at which a good can be sold. Examples of price ceilings include rent control, price controls on gasoline in

SOLUTIONS TO TEXT PROBLEMS 6 Quick Quizzes 1. A price ceiling is a legal maximum on the price at which a good can be sold. Examples of price ceilings include rent control, price controls on gasoline in

CH 4: Supply and Demand

CH 4: Supply and Demand Demand The law of demand states that the quantity of a good demanded is inversely related to the good s price In other words: Quantity demanded rises as price falls Quantity demanded

CH 4: Supply and Demand Demand The law of demand states that the quantity of a good demanded is inversely related to the good s price In other words: Quantity demanded rises as price falls Quantity demanded

Producing Goods & Services

Producing Goods & Services Supply is the quantities of a product or service that a firm is willing and able to make available for sale at all possible prices. The Law of Supply states that the quantity

Producing Goods & Services Supply is the quantities of a product or service that a firm is willing and able to make available for sale at all possible prices. The Law of Supply states that the quantity

ECONOMICS. Chapter 4 The Market Strikes Back

Lesson 1 ECONOMICS Chapter 4 The Market Strikes Back Review: Supply and Demand The previous lesson focused on demand and supply, we studied the demand curve and the supply curve P P S D Quantity Quantity

Lesson 1 ECONOMICS Chapter 4 The Market Strikes Back Review: Supply and Demand The previous lesson focused on demand and supply, we studied the demand curve and the supply curve P P S D Quantity Quantity

Lesson 4. Adam Smith and the Free Market 1/27/2013. Markets and Competition. Supply. Unit 2. Krugman, Module 6 pp

Unit 2 Adam Smith and the Free Market Lesson 4 Krugman, Module pp. 59-9 0 Markets and Competition A market is a group of buyers and sellers of a particular product. A competitive market is one with many

Unit 2 Adam Smith and the Free Market Lesson 4 Krugman, Module pp. 59-9 0 Markets and Competition A market is a group of buyers and sellers of a particular product. A competitive market is one with many

Supply and Demand Cont d

Supply and Demand Cont d D I A N N A D A S I LVA - G L A S G O W D E PA R T M E N T O F E C O N O M I C S U N I V E R S I T Y O F G U YA N A 5 O C T O B E R, 2 0 1 7 WK 4 Lecture I... SUPPLY AND DEMAND

Supply and Demand Cont d D I A N N A D A S I LVA - G L A S G O W D E PA R T M E N T O F E C O N O M I C S U N I V E R S I T Y O F G U YA N A 5 O C T O B E R, 2 0 1 7 WK 4 Lecture I... SUPPLY AND DEMAND

Chapter 6: Combining Supply and Demand

SCHS SOCIAL STUDIES What you need to know UNIT TWO 1. Explain how supply and demand create balance in the marketplace 2. Explain how a market reacts to a fall in supply by moving to a new equilibrium 3.

SCHS SOCIAL STUDIES What you need to know UNIT TWO 1. Explain how supply and demand create balance in the marketplace 2. Explain how a market reacts to a fall in supply by moving to a new equilibrium 3.

Demand/Supply Unit Essential Questions

Demand/Supply Unit Essential Questions -What is the role of demand in free market capitalism? -How do changes in price influence quantity demanded? -What factors affect changes in demand that influence

Demand/Supply Unit Essential Questions -What is the role of demand in free market capitalism? -How do changes in price influence quantity demanded? -What factors affect changes in demand that influence

Producing Goods & Services

Producing Goods & Services Supply is the quantities of a product or service that a firm is willing and able to make available for sale at all possible prices. The Law of Supply states that the quantity

Producing Goods & Services Supply is the quantities of a product or service that a firm is willing and able to make available for sale at all possible prices. The Law of Supply states that the quantity

Chapter 5: Understanding Supply

SCHS SOCIAL STUDIES What you need to know UNIT TWO 1. Explain the law of supply 2. Explain how firms decide how much labor to hire to produce a certain level of output 3. Identify three was government

SCHS SOCIAL STUDIES What you need to know UNIT TWO 1. Explain the law of supply 2. Explain how firms decide how much labor to hire to produce a certain level of output 3. Identify three was government

DEMAND AND SUPPLY. Chapter 3. Principles of Macroeconomics by OpenStax College is licensed under a Creative Commons Attribution 3.

DEMAND AND SUPPLY Chapter 3 Principles of Macroeconomics by OpenStax College is licensed under a Creative Commons Attribution 3.0 Unported License Demand for Goods and Services Demand refers to the amount

DEMAND AND SUPPLY Chapter 3 Principles of Macroeconomics by OpenStax College is licensed under a Creative Commons Attribution 3.0 Unported License Demand for Goods and Services Demand refers to the amount

Chapter 7: Market Structures Section 1

Chapter 7: Market Structures Section 1 Objectives 1. Describe the four conditions that are in place in a perfectly competitive market. 2. List two common barriers that prevent firms from entering a market.

Chapter 7: Market Structures Section 1 Objectives 1. Describe the four conditions that are in place in a perfectly competitive market. 2. List two common barriers that prevent firms from entering a market.

Chapter 9. The Instruments of Trade Policy

Chapter 9 The Instruments of Trade Policy Preview Partial equilibrium analysis of tariffs in a single industry: supply, demand, and trade Costs and benefits of tariffs Export subsidies Import quotas Voluntary

Chapter 9 The Instruments of Trade Policy Preview Partial equilibrium analysis of tariffs in a single industry: supply, demand, and trade Costs and benefits of tariffs Export subsidies Import quotas Voluntary

Reading Essentials and Study Guide

Lesson 1 What Is Supply? ESSENTIAL QUESTION What are the basic differences between supply and demand? Reading HELPDESK Academic Vocabulary various different Content Vocabulary supply amount of a product

Lesson 1 What Is Supply? ESSENTIAL QUESTION What are the basic differences between supply and demand? Reading HELPDESK Academic Vocabulary various different Content Vocabulary supply amount of a product

Basic Economics Chapter 4

1 Basic Economics Chapter 4 The Market Forces of Supply and Markets and Competition Market = a group of buyers and sellers of a particular good or service Buyers = determine the demand for the product

1 Basic Economics Chapter 4 The Market Forces of Supply and Markets and Competition Market = a group of buyers and sellers of a particular good or service Buyers = determine the demand for the product

GRAPHS WHAAAA???!!!???

Mumford and Sons Supply and Demand GRAPHS WHAAAA???!!!??? Demand Combination of desire, ability, and willingness to buy a product Question: Demand Schedule Price Quantity How many movie DVDs Demanded would

Mumford and Sons Supply and Demand GRAPHS WHAAAA???!!!??? Demand Combination of desire, ability, and willingness to buy a product Question: Demand Schedule Price Quantity How many movie DVDs Demanded would

Problem Set 3 Eco 112, Spring 2011 Chapters covered: Ch. 6 and Ch. 7 Due date: March 3, 2011

Problem Set 3 Eco 112, Spring 2011 Chapters covered: Ch. 6 and Ch. 7 Due date: March 3, 2011 There are 30 multiple choice questions in this problem set. Answer these questions by the beginning of the class

Problem Set 3 Eco 112, Spring 2011 Chapters covered: Ch. 6 and Ch. 7 Due date: March 3, 2011 There are 30 multiple choice questions in this problem set. Answer these questions by the beginning of the class

Lesson 1: What is Supply? Lesson 2: The Theory of Production Lesson 3: Cost, Revenue, and Profit Maximization

Lesson 1: What is Supply? Lesson 2: The Theory of Production Lesson 3: Cost, Revenue, and Profit Maximization 1 5 Supply BIG IDEAS = Responsibility, Choices, Changes, and Relationships Essential Questions:

Lesson 1: What is Supply? Lesson 2: The Theory of Production Lesson 3: Cost, Revenue, and Profit Maximization 1 5 Supply BIG IDEAS = Responsibility, Choices, Changes, and Relationships Essential Questions:

DEMAND. Economics Unit 2 Just the Facts Handout

DEMAND Economics Unit 2 Just the Facts Handout What is Demand? A market is a place where people buy and sell things. A market has two sides. There is a buying side and a selling side. The buying side of

DEMAND Economics Unit 2 Just the Facts Handout What is Demand? A market is a place where people buy and sell things. A market has two sides. There is a buying side and a selling side. The buying side of

Exam #1 Time: 1h 15m Date: 4 or 5 September Instructor: Brian B. Young. Multiple Choice. 2 points each

Economics 211 Macroeconomic Principles Exam #1 Time: 1h 15m Date: 4 or 5 September 2013 Name The value of this exam is 100 points. Instructor: Brian B. Young Please show your work where appropriate! Multiple

Economics 211 Macroeconomic Principles Exam #1 Time: 1h 15m Date: 4 or 5 September 2013 Name The value of this exam is 100 points. Instructor: Brian B. Young Please show your work where appropriate! Multiple

2. Which of the following is a distinguishing feature of a market system? A. public ownership of all capital.

Practice Test Chapter 2 1. Which of the following is a distinguishing feature of a command system? A. private ownership of all capital. B. central planning. C. heavy reliance on markets. D. wide-spread

Practice Test Chapter 2 1. Which of the following is a distinguishing feature of a command system? A. private ownership of all capital. B. central planning. C. heavy reliance on markets. D. wide-spread

Chapter 2. Supply and Demand

Chapter 2 Supply and Demand Reading Assignment for the Week: Finish Chapter 2 Chapter 3 2-2 Copyright 2012 Pearson Addison-Wesley. All rights reserved. Topics 1. Demand. 2. Supply. 3. Market Equilibrium.

Chapter 2 Supply and Demand Reading Assignment for the Week: Finish Chapter 2 Chapter 3 2-2 Copyright 2012 Pearson Addison-Wesley. All rights reserved. Topics 1. Demand. 2. Supply. 3. Market Equilibrium.

ECON (ENT) COURSE LESSON THREE. Supply and Demand. CHAPTER 7 Supply and Demand. Lesson Three Supply and Demand 93

COURSE LESSON THREE. Supply and Demand. CHAPTER 7 Supply and Demand. Lesson Three Supply and Demand 93") ECON (ENT) COURSE LESSON THREE Supply and Demand CHAPTER 7 Supply and Demand Lesson Three Supply and Demand 93 EXERCISES Matching (28 points) From the list below, select the term that matches each of the

ECON (ENT) COURSE LESSON THREE Supply and Demand CHAPTER 7 Supply and Demand Lesson Three Supply and Demand 93 EXERCISES Matching (28 points) From the list below, select the term that matches each of the

2015 Pearson. Why does tuition keep rising?

Why does tuition keep rising? Demand and Supply 4 When you have completed your study of this chapter, you will be able to CHAPTER CHECKLIST 1 Distinguish between quantity demanded and demand, and explain

Why does tuition keep rising? Demand and Supply 4 When you have completed your study of this chapter, you will be able to CHAPTER CHECKLIST 1 Distinguish between quantity demanded and demand, and explain

WHAT IS DEMAND? CHAPTER 4.1

Economics Unit 2 TEACHER WHAT IS DEMAND? CHAPTER 4.1 What is demand? THE DESIRE, ABILITY, AND WILLINGNESS TO BUY A PRODUCT. What is microeconomics? THE AREA OF ECONOMICS THAT DEALS WITH BEHAVIOR AND DECISION

Economics Unit 2 TEACHER WHAT IS DEMAND? CHAPTER 4.1 What is demand? THE DESIRE, ABILITY, AND WILLINGNESS TO BUY A PRODUCT. What is microeconomics? THE AREA OF ECONOMICS THAT DEALS WITH BEHAVIOR AND DECISION

7.1 Prices are economic stop lights. They direct buying and selling. When prices become sticky: The market is less efficient in allocating resources.

7.1 Prices are economic stop lights. They direct buying and selling. When prices become sticky: The market is less efficient in allocating resources. When demand increases faster than supply increases:

7.1 Prices are economic stop lights. They direct buying and selling. When prices become sticky: The market is less efficient in allocating resources. When demand increases faster than supply increases:

PowerPoint to accompany

PowerPoint to accompany Chapter 2 Markets, Demand and Supply Learning Objectives 2.1 Economic systems How do countries differ in the way their economies are organised? 2.2 Demand How much will people buy

PowerPoint to accompany Chapter 2 Markets, Demand and Supply Learning Objectives 2.1 Economic systems How do countries differ in the way their economies are organised? 2.2 Demand How much will people buy

1. Suppose that policymakers have been convinced that the market price of cheese is too low.

ECNS 251 Homework 3 Supply & Demand II ANSWERS 1. Suppose that policymakers have been convinced that the market price of cheese is too low. a. Suppose the government imposes a binding price floor in the

ECNS 251 Homework 3 Supply & Demand II ANSWERS 1. Suppose that policymakers have been convinced that the market price of cheese is too low. a. Suppose the government imposes a binding price floor in the

Markets. Markets. The Market Forces of Supply and Demand. The Market Forces of Supply and Demand. Competition: Perfect and Otherwise

The Market Forces of and Demand Chapter 4 All rights reserved. Copyright 21 by Harcourt, Inc. Requests for permission to make copies of any part of the work should be mailed to: Permissions Department,

The Market Forces of and Demand Chapter 4 All rights reserved. Copyright 21 by Harcourt, Inc. Requests for permission to make copies of any part of the work should be mailed to: Permissions Department,

Downloaded for free from 1

Micro Chapter 6 -price ceiling or price cap: government regulation that makes it illegal to charge a price higher then a specified level -effects of the price cap on the market depend on whether the ceiling

Micro Chapter 6 -price ceiling or price cap: government regulation that makes it illegal to charge a price higher then a specified level -effects of the price cap on the market depend on whether the ceiling

Markets, Equilibrium, and Prices

Markets, Equilibrium, and Prices Think of a product you recently purchased. Product: Price Paid: What are some reasons you were willing to buy the product at this price? What are some reasons the seller

Markets, Equilibrium, and Prices Think of a product you recently purchased. Product: Price Paid: What are some reasons you were willing to buy the product at this price? What are some reasons the seller

Individual & Market Demand and Supply

Mr Sydney Armstrong ECN 1100 Introduction to Microeconomic Lecture Note (3) Individual & Market Demand and Supply The tools of demand and supply can take us a far way in understanding both specific economic

Mr Sydney Armstrong ECN 1100 Introduction to Microeconomic Lecture Note (3) Individual & Market Demand and Supply The tools of demand and supply can take us a far way in understanding both specific economic

ECONOMICS. Chapter 4 The Market Strikes Back

Lesson 1 ECONOMICS Chapter 4 The Market Strikes Back Review: Supply and Demand The previous lesson focused on demand and supply, we studied the demand curve and the supply curve P P S D Quantity Quantity

Lesson 1 ECONOMICS Chapter 4 The Market Strikes Back Review: Supply and Demand The previous lesson focused on demand and supply, we studied the demand curve and the supply curve P P S D Quantity Quantity

- Scarcity leads to tradeoffs - Normative statements=opinion - Positive statement=fact with evidence - An economic model is tested by comparing its

Macroeconomics Final Notes: CHAPTER 1: What is economics? We want more than we can get. Our inability to satisfy all of our wants is called scarcity. All resources are finite even if they are abundant.

Macroeconomics Final Notes: CHAPTER 1: What is economics? We want more than we can get. Our inability to satisfy all of our wants is called scarcity. All resources are finite even if they are abundant.

Unit 2 Supply and Demand

Unit 2 Supply and Demand -Study Guide- Answer, Explain and define the following: 1) Demand 2) Consumer 3) Supply 4) Producer 5) Subsidy 6) Give examples of goods that would have inelastic demand 7) Give

Unit 2 Supply and Demand -Study Guide- Answer, Explain and define the following: 1) Demand 2) Consumer 3) Supply 4) Producer 5) Subsidy 6) Give examples of goods that would have inelastic demand 7) Give

I can explain the law of supply and analyze changes in supply in response to price and determinants.

I can explain the law of supply and analyze changes in supply in response to price and determinants. Success Criteria: Identify determinants of supply and accurately graph changes in supply. Basics of

I can explain the law of supply and analyze changes in supply in response to price and determinants. Success Criteria: Identify determinants of supply and accurately graph changes in supply. Basics of

Chapter 6: Prices Section 1

Chapter 6: Prices Section 1 Key Terms equilibrium: the point at which the demand for a product or service is equal to the supply of that product or service disequilibrium: any price or quantity not at

Chapter 6: Prices Section 1 Key Terms equilibrium: the point at which the demand for a product or service is equal to the supply of that product or service disequilibrium: any price or quantity not at

Supply and Demand Study Guide

Supply and Demand Study Guide Fill in the blank Demand 1. If price increases, quantity demanded. 2. If the number of buyers decreases, demand. 3. Increasing demand causes the demand curve to shift to the.

Supply and Demand Study Guide Fill in the blank Demand 1. If price increases, quantity demanded. 2. If the number of buyers decreases, demand. 3. Increasing demand causes the demand curve to shift to the.

Econ103_Midterm (Fall 2016)

") Econ103_Midterm (Fall 2016) Total 50 Points. Multiple Choice Identify the choice that best completes the statement or answers the question. 1 point for each question. Total 15 pts. c 1. Which of the following

Econ103_Midterm (Fall 2016) Total 50 Points. Multiple Choice Identify the choice that best completes the statement or answers the question. 1 point for each question. Total 15 pts. c 1. Which of the following

Supply and Demand Michael Powell, All Rights Reserved

Supply and Demand We have learnt that demand is the amount of a good or service consumers are willing to buy. The opposite of demand is supply. Supply is how much of a good or service a producer (a business)

Supply and Demand We have learnt that demand is the amount of a good or service consumers are willing to buy. The opposite of demand is supply. Supply is how much of a good or service a producer (a business)

This is what we call a demand schedule. It is a table that shows how much consumers are willing and able to purchase at various prices.

Demand Market: an institution or mechanism, which brings together buyers ("demanders") and sellers ("suppliers") of particular goods and services. The remainder of this unit assumes a perfectly competitive

Demand Market: an institution or mechanism, which brings together buyers ("demanders") and sellers ("suppliers") of particular goods and services. The remainder of this unit assumes a perfectly competitive

What is a market? demand goods and services to satisfy their needs and wants. supply goods and services to earn profits

What is a market? The market for a good or service consists of all those producers willing and able to supply it and all those consumers willing and able to demand it. A market exists where there are buyers

What is a market? The market for a good or service consists of all those producers willing and able to supply it and all those consumers willing and able to demand it. A market exists where there are buyers

Assignment 2: Supply and Demand

Assignment 2: Supply and Demand (Reference: Mankiw and Taylor, Chapters 4, 5, 6) Multiple Choice 1. Suppose that a large dairy farmer is able to raise the market price of milk by restricting milk supply

Assignment 2: Supply and Demand (Reference: Mankiw and Taylor, Chapters 4, 5, 6) Multiple Choice 1. Suppose that a large dairy farmer is able to raise the market price of milk by restricting milk supply

Chapter 7: Market Structures Section 2

Chapter 7: Market Structures Section 2 Objectives 1. Describe characteristics and give examples of a monopoly. 2. Describe how monopolies, including government monopolies, are formed. 3. Explain how a

Chapter 7: Market Structures Section 2 Objectives 1. Describe characteristics and give examples of a monopoly. 2. Describe how monopolies, including government monopolies, are formed. 3. Explain how a

Chapter 7: Market Structures Section 2

Chapter 7: Market Structures Section 2 Objectives 1. Describe characteristics and give examples of a monopoly. 2. Describe how monopolies, including government monopolies, are formed. 3. Explain how a

Chapter 7: Market Structures Section 2 Objectives 1. Describe characteristics and give examples of a monopoly. 2. Describe how monopolies, including government monopolies, are formed. 3. Explain how a

Economics N. Gregory Mankiw. The Markets for the Factors of Production. In this chapter, look for the answers to these questions CHAPTER

Seventh Edition Principles of Economics N. Gregory Mankiw CHAPTER 18 The Markets for the Factors of Production In this chapter, look for the answers to these questions hat determines a competitive firm

Seventh Edition Principles of Economics N. Gregory Mankiw CHAPTER 18 The Markets for the Factors of Production In this chapter, look for the answers to these questions hat determines a competitive firm

AP Microeconomics Chapter 3 Outline

I. Learning Objectives In this chapter students should learn: II. Markets III. Demand A. What demand is and how it can change. B. What supply is and how it can change. C. How supply and demand interact

I. Learning Objectives In this chapter students should learn: II. Markets III. Demand A. What demand is and how it can change. B. What supply is and how it can change. C. How supply and demand interact

Outlining the Chapter

Outlining the Look over the chapter for an overview of the material. Pay attention to the main topics in the book. As you look over each section of the book, fill in the missing words in the outline below.

Outlining the Look over the chapter for an overview of the material. Pay attention to the main topics in the book. As you look over each section of the book, fill in the missing words in the outline below.

Government Price Setting, and Taxes

CHAPTER 4 Economic Efficiency, Government Price Setting, and Taxes Chapter Summary and Learning Objectives 4.1 Consumer Surplus and Producer Surplus (pages 98 102) Distinguish between the concepts of consumer

CHAPTER 4 Economic Efficiency, Government Price Setting, and Taxes Chapter Summary and Learning Objectives 4.1 Consumer Surplus and Producer Surplus (pages 98 102) Distinguish between the concepts of consumer

AP Microeconomics [last name, first name] Pre-Test

![AP Microeconomics [last name, first name] Pre-Test](/thumbs/95/123047287.jpg "AP Microeconomics [last name, first name] Pre-Test") AP Microeconomics [last name, first name] Pre-Test Directions: Use pencil only to answer the following questions. Return your completed pre-test on the first day of class. READING GRAPHS 1: Refer to the

AP Microeconomics [last name, first name] Pre-Test Directions: Use pencil only to answer the following questions. Return your completed pre-test on the first day of class. READING GRAPHS 1: Refer to the

Case: An Increase in the Demand for the Product

1 Appendix to Chapter 22 Connecting Product Markets and Labor Markets It should be obvious that what happens in the product market affects what happens in the labor market. The connection is that the seller

1 Appendix to Chapter 22 Connecting Product Markets and Labor Markets It should be obvious that what happens in the product market affects what happens in the labor market. The connection is that the seller

2-1 Copyright 2012 Pearson Education. All rights reserved.

2-1 Copyright 2012 Pearson Education. All rights reserved. Chapter 2 Read this chapter together with unit 1 and 2 in the study guide Supply and Demand Topics 1. Demand. 2. Supply. 3. Market Equilibrium.

2-1 Copyright 2012 Pearson Education. All rights reserved. Chapter 2 Read this chapter together with unit 1 and 2 in the study guide Supply and Demand Topics 1. Demand. 2. Supply. 3. Market Equilibrium.

Government Regulation

Government Regulation What do you think is the market price for renting an apartment in Plainfield? What happens to the quantity of demand and supply after the price change? List four outcomes that would

Government Regulation What do you think is the market price for renting an apartment in Plainfield? What happens to the quantity of demand and supply after the price change? List four outcomes that would

EXTERNALITIES. Problems and Applications

10 EXTERNALITIES Problems and Applications 1. The Club conveys a negative externality on other car owners because car thieves will not attempt to steal a car with The Club visibly in place. This means

10 EXTERNALITIES Problems and Applications 1. The Club conveys a negative externality on other car owners because car thieves will not attempt to steal a car with The Club visibly in place. This means

Entrepreneurship. Unit 1.1: Understanding basic economic concepts related to business ownership

Entrepreneurship Unit 1.1: Understanding basic economic concepts related to business ownership Students will understand basic economic concepts related to business ownership Students will be able to: Define

Entrepreneurship Unit 1.1: Understanding basic economic concepts related to business ownership Students will understand basic economic concepts related to business ownership Students will be able to: Define

Unit 2 Supply and Demand

Unit 2 Supply and Demand Microeconomics - analyzes the Small Unit economic behavior of Individuals, Households and Firms to understand their decision-making process. -America s Free Enterprise- An economy

Unit 2 Supply and Demand Microeconomics - analyzes the Small Unit economic behavior of Individuals, Households and Firms to understand their decision-making process. -America s Free Enterprise- An economy

Unit II: Supply, Demand, and Consumer Choice Problem Set #2

1. /20 4. /30 2. /20 5. /10 3. /10 6. /10 Total: /100 Name: Team: Unit II: Supply, Demand, and Consumer Choice Problem Set #2 1. EXPLAIN an experience or example that shows the real world application of

1. /20 4. /30 2. /20 5. /10 3. /10 6. /10 Total: /100 Name: Team: Unit II: Supply, Demand, and Consumer Choice Problem Set #2 1. EXPLAIN an experience or example that shows the real world application of

Getting ready for the AP Macroeconomics Exam Lesson 2

Getting ready for the AP Macroeconomics Exam Lesson 2 Quantity S / D vs. Supply and Demand, Law of Supply and Demand, Reasons for Change of Supply and Demand How does a demand schedule differ from a market

Getting ready for the AP Macroeconomics Exam Lesson 2 Quantity S / D vs. Supply and Demand, Law of Supply and Demand, Reasons for Change of Supply and Demand How does a demand schedule differ from a market

Edexcel Economics AS-level

Edexcel Economics AS-level Unit 1: Markets in Action Topic 7: Government Intervention in Markets 7.1 Methods of government intervention Notes The existence of market failure, in its various forms, provides

Edexcel Economics AS-level Unit 1: Markets in Action Topic 7: Government Intervention in Markets 7.1 Methods of government intervention Notes The existence of market failure, in its various forms, provides

Edexcel (A) Economics A-level

Economics A-level") Edexcel (A) Economics A-level Theme 1: Introduction to Markets and Market Failure 1.4 Government Intervention 1.4.1 Government intervention in markets Notes Government intervention to target market failure:

Edexcel (A) Economics A-level Theme 1: Introduction to Markets and Market Failure 1.4 Government Intervention 1.4.1 Government intervention in markets Notes Government intervention to target market failure:

Chapter 1: What is Economics? Section 3

Chapter 1: What is Economics? Section 3 Objectives 1. Interpret a production possibilities curve. 2. Explain how production possibilities curves show efficiency, growth, and cost. 3. Explain why a country

Chapter 1: What is Economics? Section 3 Objectives 1. Interpret a production possibilities curve. 2. Explain how production possibilities curves show efficiency, growth, and cost. 3. Explain why a country

Homework 2 Answer Key

Econ 226 Principles of Microeconomics Fall, 24 Dr. Kathryn Wilson Due Date: Tuesday, September 28 th Homework 2 Answer Key 1. When the of movie admissions increases from $7 to $8, the demanded falls from

Econ 226 Principles of Microeconomics Fall, 24 Dr. Kathryn Wilson Due Date: Tuesday, September 28 th Homework 2 Answer Key 1. When the of movie admissions increases from $7 to $8, the demanded falls from

Professor Christina Romer SUGGESTED ANSWERS TO PROBLEM SET 3

Economics 2 Spring 2018 rofessor Christina Romer rofessor David Romer SUGGESTED ANSWERS TO ROBLEM SET 3 1.a. A monopolist is the only seller of a good. As a result, it faces the downward-sloping market

Economics 2 Spring 2018 rofessor Christina Romer rofessor David Romer SUGGESTED ANSWERS TO ROBLEM SET 3 1.a. A monopolist is the only seller of a good. As a result, it faces the downward-sloping market

EXAM 2: Professor Walker - S201 - Fall 2008

EXAM 2: Professor Walker - S201 - Fall 2008 I. (3 Points Each) Multiple Choice 1. Leisure Hours Grades 10 80 15 40 20 20 The tradeoff shown in the PPF table above depicts A. decreasing per unit O.C. of

EXAM 2: Professor Walker - S201 - Fall 2008 I. (3 Points Each) Multiple Choice 1. Leisure Hours Grades 10 80 15 40 20 20 The tradeoff shown in the PPF table above depicts A. decreasing per unit O.C. of

Policy Evaluation Tools. Willingness to Pay and Demand. Consumer Surplus (CS) Evaluating Gov t Policy - Econ of NA - RIT - Dr.

Evaluating Gov t Policy - Econ of NA - RIT - Dr.") Policy Evaluation Tools Evaluating Gov t Policy - Econ of NA - RIT - Dr. Jeffrey Burnette In economics we like to measure the impact government policies have on the economy and separate winners and losers.

Policy Evaluation Tools Evaluating Gov t Policy - Econ of NA - RIT - Dr. Jeffrey Burnette In economics we like to measure the impact government policies have on the economy and separate winners and losers.

2013 Pearson. Why did the price of coffee soar in 2010 and 2011?

Why did the price of coffee soar in 2010 and 2011? How do markets work? We have seen the circular flows diagram, which shows that households and firms interact in factor markets and goods markets. In this

Why did the price of coffee soar in 2010 and 2011? How do markets work? We have seen the circular flows diagram, which shows that households and firms interact in factor markets and goods markets. In this

AQA Economics A-level

AQA Economics A-level Microeconomics Topic 8: Market Mechanism, Market Failure and Government Intervention in Markets 8.9 Government intervention in markets Notes The existence of market failure, in its

AQA Economics A-level Microeconomics Topic 8: Market Mechanism, Market Failure and Government Intervention in Markets 8.9 Government intervention in markets Notes The existence of market failure, in its

Price = The Interaction of Supply and Demand WEDNESDAY, FEBRUARY 17 THURSDAY, FEBRUARY 18

Price = The Interaction of Supply and Demand WEDNESDAY, FEBRUARY 17 THURSDAY, FEBRUARY 18 Chapter 4: Section 1 Understanding Demand What Is Demand? Markets are where people come together to buy and sell

Price = The Interaction of Supply and Demand WEDNESDAY, FEBRUARY 17 THURSDAY, FEBRUARY 18 Chapter 4: Section 1 Understanding Demand What Is Demand? Markets are where people come together to buy and sell

Admission Examination in Economics. Version A

MA in Economic Analysis Admission Examination in Economics Version A NAME: Instructions: 1. Do not turn this page until told to do so. 2. The exam consists of 20 questions that are all equally weighted.

MA in Economic Analysis Admission Examination in Economics Version A NAME: Instructions: 1. Do not turn this page until told to do so. 2. The exam consists of 20 questions that are all equally weighted.

Edexcel Economics AS-level

Edexcel Economics AS-level Unit 1: Markets in Action Topic 6: Market Failure 6.1 Market failure Notes Types of market failure Market failure occurs when the free market fails to allocate resources to the

Edexcel Economics AS-level Unit 1: Markets in Action Topic 6: Market Failure 6.1 Market failure Notes Types of market failure Market failure occurs when the free market fails to allocate resources to the

Embedded Economies. No Net Flow of Goods. Embedded Economies - Econ. of NA - RIT - Dr. Jeffrey Burnette

Embedded Economies Embedded Economies - Econ. of NA - RIT - Dr. Jeffrey Burnette Embedded Economy - a sovereign economy contained within a larger economy. An embedded economy is different from that surrounding

Embedded Economies Embedded Economies - Econ. of NA - RIT - Dr. Jeffrey Burnette Embedded Economy - a sovereign economy contained within a larger economy. An embedded economy is different from that surrounding

Supply and Demand. Chapter 3. McGraw-Hill/Irwin. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

Supply and Demand Chapter 3 McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Learning Objectives 1. Describe how the demand and supply curves summarize the behavior

Supply and Demand Chapter 3 McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Learning Objectives 1. Describe how the demand and supply curves summarize the behavior

7-1 L ECTURE LAUNCHER PAGES PAGES

7-1 L ECTURE LAUNCHER Proctor & Gamble s introduced disposable diapers to the marketplace in 1961. At first parents only used Pampers for special occasions. Today, 95% of American parents use disposable

7-1 L ECTURE LAUNCHER Proctor & Gamble s introduced disposable diapers to the marketplace in 1961. At first parents only used Pampers for special occasions. Today, 95% of American parents use disposable

Chapter 3 Demand and Supply John Petroff (2002)

") Chapter 3 Demand and Supply John Petroff (2002) INTRODUCTION The purpose of this lesson is to reach an understanding of how markets operate, how prices are set and transactions occur. The two market forces

Chapter 3 Demand and Supply John Petroff (2002) INTRODUCTION The purpose of this lesson is to reach an understanding of how markets operate, how prices are set and transactions occur. The two market forces

Market Equilibrium, the Price Mechanism and Market Efficiency. Chapter 3

Market Equilibrium, the Price Mechanism and Market Efficiency Chapter 3 Equilibrium Equilibrium is defined as a state of rest, self-perpetuating in the absence of any outside disturbance. Example: a book

Market Equilibrium, the Price Mechanism and Market Efficiency Chapter 3 Equilibrium Equilibrium is defined as a state of rest, self-perpetuating in the absence of any outside disturbance. Example: a book

Perfectly Competitive Supply. Chapter 6. Learning Objectives

Perfectly Competitive Supply Chapter 6 McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Learning Objectives 1.Explain how opportunity cost is related to the supply

Perfectly Competitive Supply Chapter 6 McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Learning Objectives 1.Explain how opportunity cost is related to the supply

Economic efficiency. Who gains and who loses when prices change?

Economic efficiency Who gains and who loses when prices change? 1 The Efficiency of Competitive Markets Economic Surplus and Economic Efficiency Economic efficiency A market outcome in which the marginal

Economic efficiency Who gains and who loses when prices change? 1 The Efficiency of Competitive Markets Economic Surplus and Economic Efficiency Economic efficiency A market outcome in which the marginal

Managerial Economics ECO404 SUPPLY ANALYSIS

SUPPLY ANALYSIS Lesson 5 BASIS FOR SUPPLY The term Supply refers to the quantity of a good or service that producers are willing and able to sell during a certain period under a given set of conditions.

SUPPLY ANALYSIS Lesson 5 BASIS FOR SUPPLY The term Supply refers to the quantity of a good or service that producers are willing and able to sell during a certain period under a given set of conditions.

Introduction. Learning Objectives. Chapter 24. Perfect Competition

Chapter 24 Perfect Competition Introduction Estimates indicate that since 2003, the total amount of stored digital data on planet Earth has increased from 5 exabytes to more than 200 exabytes. Accompanying

Chapter 24 Perfect Competition Introduction Estimates indicate that since 2003, the total amount of stored digital data on planet Earth has increased from 5 exabytes to more than 200 exabytes. Accompanying

Microeconomics. The Market Forces of Supply and Demand. Markets and Competition. In this chapter, look for the answers to these questions:

C H A T E R 4 The Market Forces of Supply and Demand R I N C I L E S O F Microeconomics N. Gregory Mankiw remium oweroint Slides by Ron Cronovich 2010 South-Western, a part of Cengage Learning, all rights

C H A T E R 4 The Market Forces of Supply and Demand R I N C I L E S O F Microeconomics N. Gregory Mankiw remium oweroint Slides by Ron Cronovich 2010 South-Western, a part of Cengage Learning, all rights

LECTURE February Thursday, February 21, 13

LECTURE 10 21 February 2013 1 ANNOUNCEMENTS HW 4 due Friday at 11:45 PM Midterm 1 next Monday February 25th 7:30 PM - 8:30 PM in Anderson 270 (not this room) 2 old midterms are on Moodle; they are very

LECTURE 10 21 February 2013 1 ANNOUNCEMENTS HW 4 due Friday at 11:45 PM Midterm 1 next Monday February 25th 7:30 PM - 8:30 PM in Anderson 270 (not this room) 2 old midterms are on Moodle; they are very

Micro Semester Review Name:

Micro Semester Review Name: The following review is set up to emphasize certain concepts, graphs and terms. It is the responsibility of the individual teachers to emphasize and review the analysis aspects

Micro Semester Review Name: The following review is set up to emphasize certain concepts, graphs and terms. It is the responsibility of the individual teachers to emphasize and review the analysis aspects

Chapter 3: American Free Enterprise Section 3

Chapter 3: American Free Enterprise Section 3 Objectives 1. Identify examples of public goods. 2. Analyze market failures. 3. Evaluate how the government allocates some resources by managing externalities.

Chapter 3: American Free Enterprise Section 3 Objectives 1. Identify examples of public goods. 2. Analyze market failures. 3. Evaluate how the government allocates some resources by managing externalities.

Economics for Managers, 3e (Farnham) Chapter 2 Demand, Supply, and Equilibrium Prices

Chapter 2 Demand, Supply, and Equilibrium Prices") Economics for Managers, 3e (Farnham) Chapter 2 Demand, Supply, and Equilibrium Prices 1) According to the case for analysis (Demand and Supply in the Copper Industry) in the text, all of the following

Economics for Managers, 3e (Farnham) Chapter 2 Demand, Supply, and Equilibrium Prices 1) According to the case for analysis (Demand and Supply in the Copper Industry) in the text, all of the following

Mechanism through which buyers (demanders) and sellers (suppliers) communicate to trade goods and services.

and sellers (suppliers) communicate to trade goods and services.") By the end of this learning plan, you will be able to: Use marginal (Cost-Benefit) analysis in decision-making Apply supply and demand analysis to price determination Assess the role price plays in a market

By the end of this learning plan, you will be able to: Use marginal (Cost-Benefit) analysis in decision-making Apply supply and demand analysis to price determination Assess the role price plays in a market

Economic Systems. Economies and Circular Flow

Economies and Circular Flow Every society must answer three questions: The Three Economic Questions 1. What goods and services should be produced? 2. How should these goods and services be produced? 3.

Economies and Circular Flow Every society must answer three questions: The Three Economic Questions 1. What goods and services should be produced? 2. How should these goods and services be produced? 3.

Demand, Supply, and Market Equilibrium

Demand, Supply, and Market Equilibrium Markets Interaction between buyers and sellers Markets may be: Local National International rice is discovered in the interactions of buyers and sellers LO - Demand

Demand, Supply, and Market Equilibrium Markets Interaction between buyers and sellers Markets may be: Local National International rice is discovered in the interactions of buyers and sellers LO - Demand

Edexcel (B) Economics A-level

Economics A-level") Edexcel (B) Economics A-level Theme 1: Markets, Consumers and Firms 1.5 Market Failure and Government Intervention 1.5.2 Government intervention and failure Notes Purposes of intervention with reference

Edexcel (B) Economics A-level Theme 1: Markets, Consumers and Firms 1.5 Market Failure and Government Intervention 1.5.2 Government intervention and failure Notes Purposes of intervention with reference

Chapter. Externalities CHAPTER CHECKLIST

Externalities Chapter CHAPTER CHECKLIST An externality in an unregulated market leads to inefficiency and creates a deadweight loss. Chapter 9 explains the role of the government in markets where an externality

Externalities Chapter CHAPTER CHECKLIST An externality in an unregulated market leads to inefficiency and creates a deadweight loss. Chapter 9 explains the role of the government in markets where an externality

Coffee is produced at a constant marginal cost of $1.00 a pound. Due to a shortage of cocoa beans, the marginal cost rises to $2.00 a pound.

Microeconomics, Module 11: Monopoly (Chapter 10) Illustrative Test Questions (The attached PDF file has better formatting.) Updated: June 27, 2005 Question 11.1: Monopoly All but which of the following

Microeconomics, Module 11: Monopoly (Chapter 10) Illustrative Test Questions (The attached PDF file has better formatting.) Updated: June 27, 2005 Question 11.1: Monopoly All but which of the following